📣 Vertical SaaS Earnings - Q2-2024

Overlooked #181

Hi, it’s Alexandre. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing insights from quarterly earnings results from top vertical SaaS companies including Toast, Lightspeed and Olo.

Today, I’m launching a new quarterly series that shares insights on the earnings of publicly listed vertical SaaS companies. I’ve selected three initial vertical SaaS focused on the restaurant industry - Toast, Olo and Lightspeed - as a starting point, but I intend to add a few more in the coming quarters. As a reminder:

Toast is an all-in-one platform for independent restaurants, primarily in the US, centered around point-of-sale (POS) and payment processing. I previously covered Toast in the newsletter here and here.

Lightspeed is a point-of-sale system serving both the restaurant and retail sectors. Like Toast, it primarily targets independent businesses. However, Lightspeed’s business is more geographically diversified between Europe and the US. The company is currently undergoing restructuring to enforce the bundling of payment processing and POS services for its customer base. I’ll publish a more detailed post on Lightspeed soon but if you want to learn more you can find a draft here.

Olo is a guest-facing platform for restaurant chains in the US. It offers three modules: digital ordering, guest engagement, and payments. Olo’s current major business initiative is integrating payment processing within its customer base through Olo Pay. I previously covered Olo in this newsletter here.

I’ve divided this post into two sections: (i) general vertical SaaS insights and (ii) company specific insights. If you have any feedback on improving the format or suggestions for the next publicly listed vertical SaaS companies to cover, feel free to reach out at alexandre.dewez@gmail.com.

General Vertical SaaS Insights

Vertical SaaS companies are rapidly incorporating AI features into their platform offerings.

Toast has introduced 3 AI-powered features: (i) AI-driven customer support for restaurants, (ii) a benchmarking tool that allows restaurants to compare their performance with peers, and (iii) a marketing assistant to create text and images for marketing purposes.

“In June, Toast launched an AI innovation hub, highlighting some of Toast’s AI-powered innovations released to date such as Benchmarking, Instant Toast Support, and an AI-Powered Marketing Assistant. A recent survey from Toast showed that 57% of restaurants surveyed reported already using or wanting to use AI-powered experiences.” - Toast’s Q2-24 Earnings

Lightspeed has launched an AI feature designed to enhance product photos for its retailers who sell online.

Olo has unveiled an AI Creative Assistant that uses generative AI to produce marketing content integrated into Engage, Olo’s guest engagement product.

Vertical SaaS companies are doubling down on their expansion into financial services.

While Toast has always bundled payment processing with its POS, it is now expanding into lending through Toast Capital. In Q2-2024, Toast Capital generated $34 million in gross profit, accounting for 10.5% of the company’s total gross margin.

Lightspeed is transitioning its customer base to offerings that combine payment processing with POS, while also expanding into lending through Lightspeed Capital. In Q1-2025, Lightspeed Capital generated $7.8m in revenues with a gross margin exceeding 95% compared to $1.6m in the same quarter last year accounting for 6.8% of the company’s total gross margin.

Olo’s major product initiative is integrating payment processing into its platform with Olo Pay, which initially aims to capture payments for online orders, with a long-term vision to also process in-store payments through partnerships with incumbent POS providers or via its Kiosk offering.

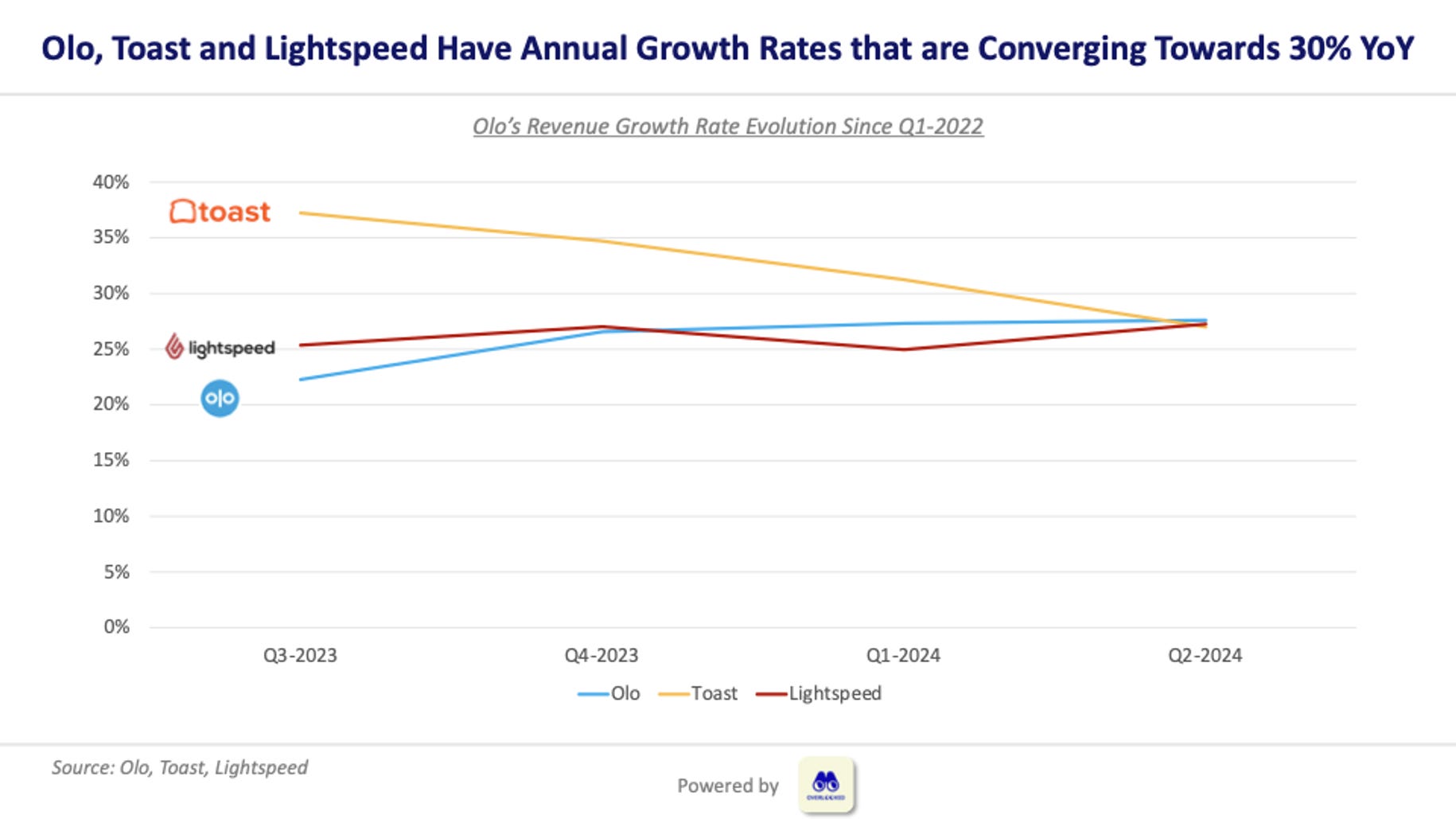

Vertical SaaS companies are racing towards achieving operating income profitability while striving to sustain high top-line growth (c.30% YoY).

Toast has managed to maintain robust growth endurance, while Olo and Lightspeed have successfully re-accelerated their growth trajectories. Last quarter, both Toast and Olo achieved operating income profitability while recording an annual growth rates close to 30%, despite recently implementing restructuring plans. For Lightspeed, returning to operating income profitability will require more time, but the business is progressing in that direction.

There is a valuation premium for vertical SaaS companies like Toast that can drive growth by both adding more locations and increasing ARPU.

As shown in the graph below, there is a significant valuation disparity between Toast, on the one hand, and Olo and Lightspeed, on the other. Toast trades at an 8.7x EV/ARR multiple, compared to 1.7x for Olo and 2.5x for Lightspeed. Another way to look at this is that each Toast location is valued at $106k in EV, while each Olo location is valued at $6k and each Lightspeed location at $8k. Olo and Lightspeed trade at a substantial discount compared to Toast because they have been unable to grow their location counts at a strong pace, despite being reasonably successful at expanding their ARPU over time. Olo added only 1.2k locations per quarter over the last five quarters, while Lightspeed lost 3k locations during its last fiscal year as it shifted its focus toward higher GMV merchants.

Toast

Key Metrics

$1.5bn in ARR (29% YoY growth)

120k locations (29% YoY growth)

$12.3k ARPU (0% YoY growth)

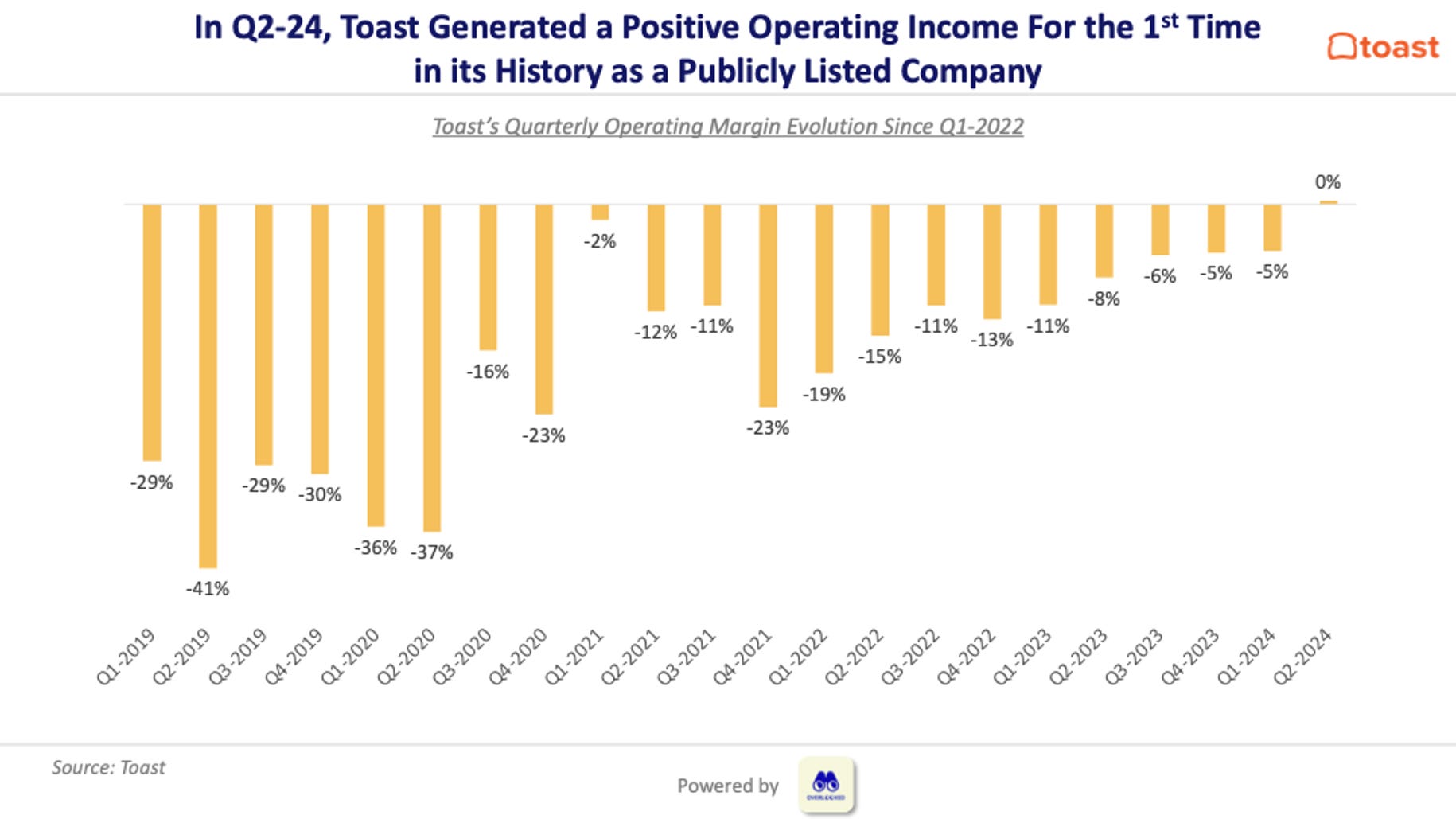

0% operating income margin (vs. -8% operating margin 1 year ago)

Qualitative Assessment

Toast’s restructuring plan enabled the company to achieve a positive operating income margin for the first time in its history as a publicly listed company.

Toast recorded strong ARR growth (29% YoY) reaching $1.5bn in ARR, primarily driven by impressive location growth (26% YoY). However, GPV per location has been flat since the beginning of the year showing that customers are cutting back expenses on restaurant spending, which is impacting ARPU growth.

The company continues to expand beyond the US with operations now in Ireland, Canada and the UK. Toast has now 2k locations abroad. It also introduced additional modules in these international markets including Online Ordering, Mobile Order & Pay, Gift Cards, and Kiosk.

Toast shared initial results from its product suite segmentation into multiple pricing tiers aimed at increasing net dollar retention. The inclusion of its new website builder for restaurants in the highest tier of the Digital Storefront Suite led to 30% of locations using the Digital Storefront Suite upgrading to this top tier.

Lightspeed

Key Metrics

$8.4bn in GTV (65% YoY growth, 36% GMV penetration rate)

$518m in ARR (17% YoY growth)

$6k ARPU (31% YoY growth)

-17% operating income margin (vs. -28% operating margin 1 year ago)

Qualitative Assessment

Lightspeed recorded a 27% YoY revenue growth, primarily driven by a 31% increase in ARPU. Financial services revenue is growing 44% YoY compared to just 6% YoY growth in subscription revenue. This growth is a direct result of Lightspeed’s strategy to mandate the integration of payment processing into its POS system for its customer base.

Gross margin on payment processing continues to decline as Lightspeed transitions to in-house payment processing, with margins dropping to 26% compared to 46% in Q1 2021 when it relied on revenue sharing with third-party payment processors. Despite the overall decline in gross margin, this transition is intended to increase platform stickiness and enhance the net dollars in gross margin per restaurant, even if it comes at the expense of the gross margin as a percentage of sales. As shown in the graph below, Lightspeed’s gross and net take rates on financial transactions are converging toward those of Toast.

“So from a gross margin perspective, the quarter came in at close to 41% which is relatively in line with our gross margin a year ago, 42%. That slight delta that you see there is really coming from the fact that are residuals, which is the payments revenue that we would get from integrated partners that's declining and those come in at 100% margin. Those are declining as we take those cohorts of customers and bring them over to Lightspeed payments. So the net dollars that we get are higher. The net take is also higher but from a gross margin perspective, that would come in at 100% gross margin, whereas Lightspeed payments is 20% to 25% gross margin. And in Europe, actually over 30% gross margin. Where Capital is concerned, you're right. Capital did very well in the quarter, and that does help our gross margins in Lightspeed Capital comes in at over 95% gross margins.”

Lightspeed’s operating income has shown improvement, with the operating margin rising from a low of -78% in Q4 2022 (excluding goodwill impairment in Q3 2023) to -17% for the most recent quarter.

Olo

Key Metrics

$278m in ARR (28% YoY growth)

82k locations (6% YoY growth)

$3.4k ARPU (19% YoY growth)

120% NDR (vs. 115% NDR 1 year ago)

1% operating income margin (vs. -38% operating margin 1 year ago)

Qualitative Assessment

Olo’s efforts to re-accelerate growth and streamline costs is starting to pay off delivering its first quarter of positive operating income.

Olo’s growth is primarily driven by upselling within its existing customer base, with a net Net Dollar Retention rate exceeding 120%, rather than by acquiring new locations, as evidenced by the addition of only 1.2k locations per quarter on average over the last five quarters.

Olo’s gross margin has declined, dropping to 57% in Q2-2024 from 69% in Q1-2022, as the company has begun to more aggressively monetize its gross merchandise volume, increasing its payment penetration rate through Olo Pay from 1% in 2022 to 4% in 2023. In 2023, Olo generated $30 million in revenue from Olo Pay, with a target of reaching $60 million in 2024.

Olo now has a much more attractive financial profile than it did a few quarters ago, achieving a 29% rule of 40, driven by 28% year-over-year growth and a return to profitability.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋