🥙 Olo - Unlocking Digital Hospitality for Restaurants

Overlooked #123

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m digging into Olo which is a vertical-SaaS targeting multi-location restaurant brands with a digital ordering and marketing platform.

In this newsletter, I previously covered Toast which is an all-in-one solution for restaurants. It started with a Point-of-Sales (PoS) sold to the long-tail of restaurants before evolving into an all-in-one solution with products like workforce management, digital ordering, marketing, loans, etc.

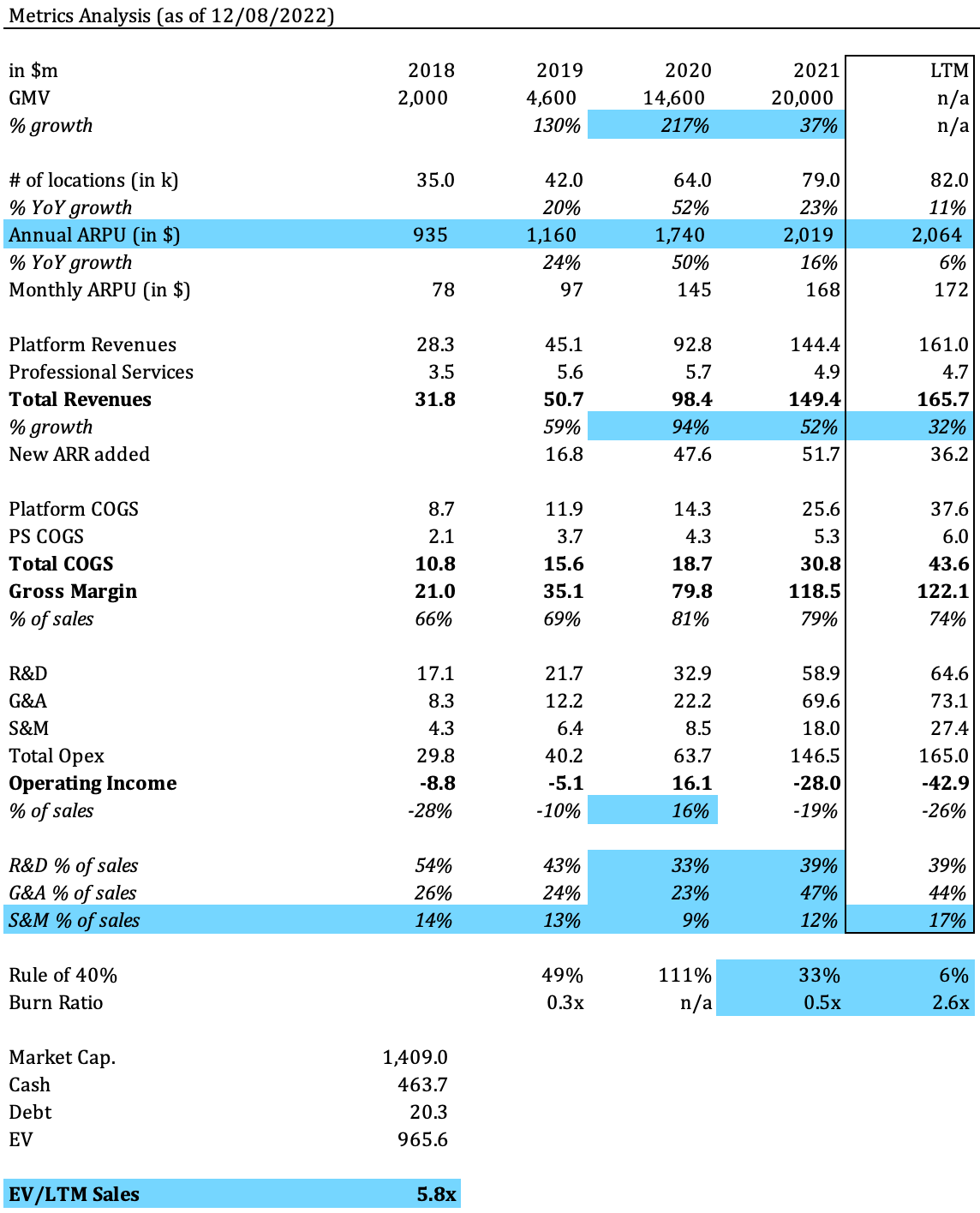

Olo is the other publicly-listed vertical SaaS specifically targeting restaurants. It had a different starting point (i) targeting enterprise customers in the restaurant industry (targeting multi-location restaurant brands like Shake Shack, Five Guys or Subway) and (ii) selling a digital ordering platform (managing offsite orders like pickup and deliveries). It went public in March 2021. Today, Olo has a $1.4bn market capitalization and it generated $166m in revenues over the last twelve months.

With Olo, I’m adding a new company deep-dive into my collection of vertical solutions (SaaS, marketplaces and fintech) for In Real Life entrepreneurs along with Procore and Toast. If you’re building in this space, I’d love to chat. You can write me at adewez@eurazeo.com.

What is Olo?

Olo is a vertical SaaS targeting multi-location restaurant brands (e.g. Shake Shack, The Cheesecake Factory, Wing Stop, Denny’s, Five Guys, Nando’s etc.) with a platform unlocking digital hospitality.

Noah Glass defines digital hospitality as “utilizing first-party data to provide guests with a memorable and personalized experience and to make every guest at the restaurant feel like a regular”. It empowers restaurant brands to build direct, digital and personalised relationships with their consumers.

Olo is a platform around 6 core products:

Ordering: a white-label digital ordering solution supporting multiple channels (mobile, web, voice, social, kiosk, etc.).

Delivery with Dispatch (to enable branded delivery from your website and mobile app with delivery service partners) and Rails (to integrate and control third party marketplaces).

Host: an on-premise guest management product with feature like a table management, waitlist and platform.

Marketing: a CRM to push email and SMS marketing campaigns.

Customer Data Platform: data analytics tool to personalise client experience with your restaurant brand.

Pay: a payment solution built on top of Stripe for digital sales with workflows specific to the restaurant verticals (e.g. reducing fraud rate thanks to Stripe Radar, managing chargebacks or Olo Pay to login once to pay in all the restaurant brands served by Olo).

Olo was founded in 2005 under the name Mobo by Noah Glass and Andrew Murray after raising a $500k angel round from David Frankel (partner at Founder Collective). In 2010, it signed Five Guys and the business was rebranded as Olo: the company had finally found its product market fit by (i) focusing on enterprise customers (i.e. restaurant brands with 50+ locations) and by (ii) selling its digital ordering product. In 2016, it raised a $40m round from the Raine Group. Before its IPO, Olo raised additional capital from investors like Tiger, Wellington and Battery Ventures. Olo added a delivery module by releasing Dispatch in 2015 and Rails in 2017. Olo accelerated its evolution to become a platform more recently after its IPO in Mar. 2021 (raising $475m). It acquired Wisely in Oct. 2021 which added 3 products to its suite (marketing, CDP and host) and released Olo Pay in Feb. 2022.

Olo is a $161m ARR business growing at 32% YoY. At IPO, it was an extremely capital efficient business (111% rule of 40%, 16% operating income margin). In the past 18 months, unit economics have deteriorated for a couple of reasons: (i) slowing growth and ARPU expansion driven by a covid hangover and a looming economic recession, (ii) R&D increase to push forward Olo’s vision to build a platform for digital hospitality, (iii) S&M increase to expand beyond Olo’s core market (top 500 restaurant brands in the US). As a result, the business is now trading at 5.8x EV/LTM Sales compared to 42.3x EV/LTM Sales at IPO.

Going forward, Olo is highlighting the following growth levers:

Upselling its platform to its existing enterprise customer base (esp. newly released products like Marketing, CDP, Host and Pay).

Expanding into other geographies by piggy backing its restaurant brands that are present beyond the US.

Going downmarket by targeting emerging multi-location restaurant groups with fast growth (5-50 locations) which have the potential to become enterprise customers (50+ locations).

Expanding into other verticals like groceries in which Olo signed its first customer with Kwik Trip.

Why is Olo a Noteworthy Business?

Compared to horizontal solutions, vertical solutions can reach extremely high market penetration by becoming a standard in their industry. With 82k restaurants as customers, Olo has a 27% market share in its core market (i.e. US enterprise restaurant brands with 50+ locations). In the mid-term, all enterprise restaurant brands will either have Olo or a complex DIY solution to manage digital ordering and its broader digitisation.

When most vertical solutions in the restaurant industry target the long tail of independent restaurants, Olo is laser focused on the mid-market and enterprise segments with multi-location restaurant brands. It’s harder to build an enterprise grade product. Sales cycles are also longer and more complex. But it seems to be a winning go to market strategy in an industry with a 3-5% operating margin and a 30% failure rate which make it extremely hard to acquire and retain the long-tail. At IPO, Olo had almost no-churn with a 95% retention on locations and a 99% retention on brands in the prior 5 years. It also displayed a strong 120% net dollar retention.

Like Shopify, Olo has the potential to become a fintech-enabled business. I’m extremely bullish on adding financial services to expand the TAM of vertical SaaS. With Olo Pay, Olo estimates that it can generate 4x more revenue per order. Olo Pay is a fully integrated payment solution verticalised for the restaurant industry handling industry-specific workflows like chargeback or fraud management. Consumers interact with Olo Pay when they order digitally on-site (e.g. from a kiosk or from a QR-code based app) or off-site (e.g. from the web or from mobile). Moreover, like Shop Pay, Olo Pay is storing account and payment information making it seamless to order from any restaurant brands in Olo’s ecosystem. When you see how much revenues Toast is generating from payments (82% of total revenues in 2021) and how the split between SaaS and payments has evolved for Shopify (71% of total revenues in 2021), there are reasons to believe that payment is a massive mid-term opportunity for Olo.

Olo is transitioning from a white label digital ordering and delivery product to a full platform to unlock digital hospitality. It’s a transition that many vertical solutions will follow and that I’ve previously noticed while digging into Procore (construction space) and Toast (restaurant space). Olo did it by combining M&A (acquiring Wisely and Omnivore) and internal product development. It’s a recent move for Olo and it will be interesting to see in the following quarters if the company is successful at upselling this platform vision to its customer base.

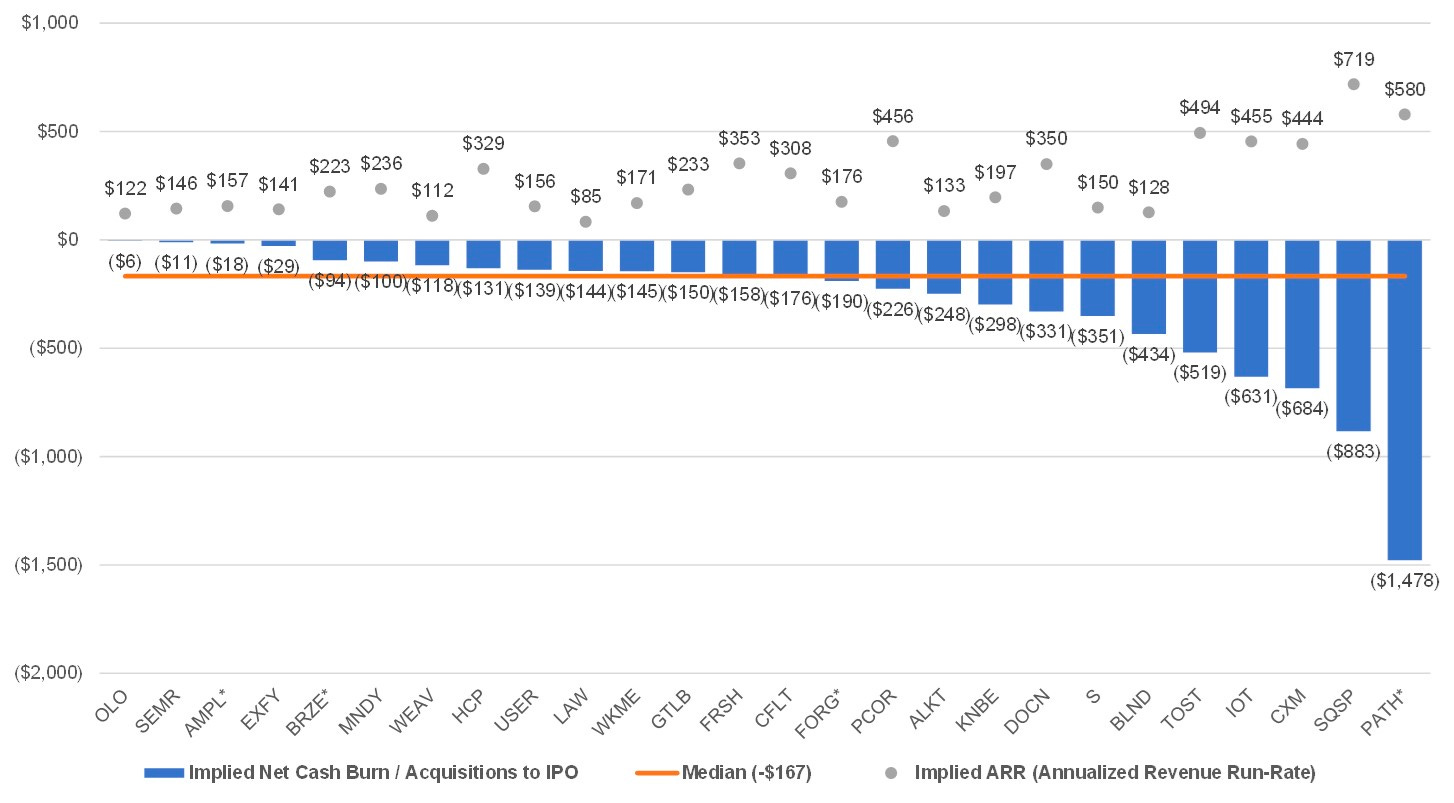

Olo is a super capital efficient business. The company burnt only $6m to reach $122m in ARR when it went public in Mar. 21 compared to a $167m median burn for all the flagship SaaS companies which went public in 2021.

Restaurants are omni-channel businesses. Like Dave Harris (CIO at Shake Shack) says: “It’s not an on premise business and an off premise business anymore. It’s one business.” Olo is successful because it supports restaurants in becoming omni-channel and in offering an unified and personalised experience across consumption modes (delivery, pick-up, on-site) and restaurant locations to their customers.

Olo is a remedy for restaurant chains to their dependency towards food marketplaces and aggregators like DoorDash, UberEats or Grubhub. Restaurants operate in a low single-digit operating margin industry. Marketplaces and aggregators help them generate incremental sales but (i) they disintermediate the relationship between restaurants and their consumers and (ii) they damage their profitability. With its white label ordering and delivery solution, Olo helps them solve these two issues.

Thanks Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋