🍻 Toast - The Ultimate Vertical SaaS For Restaurants

Overlooked #83

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m digging into Toast’s IPO Prospectus to understand why this all-in-one platform to help restaurants manage their business has become of the largest vertical SaaS in history.

Over the past couple of months, with colleagues from Eurazeo, we have been digging into vertical SaaS for local businesses. For our research, we looked at role models to understand their key success factors. Toast was obviously high on our list and we were thrilled to dig into their S1 when the company announced its intention to become public. Last week, the company eventually went public raising $870m at a $20bn valuation.

In this post, I’ll cover Toast’s IPO Prospectus looking at the following topics: (i) what is Toast, (ii) Toast’s history and (iii) learnings for other vertical SaaS.

Part I - What is Toast?

Toast is a verticalised end-to-end platform for restaurants to manage their business. It started as a Point of Sales (PoS) system to process transactions. A PoS is the system used to process transactions from customers. It records all the items purchased, it computes the taxes on all transactions and it centralize all the payment means (cards, cash, checks, mobile payments etc.). Then, Toast expanded overtime in other key areas such as online ordering, inventory, workforce management, payroll, capital, customer review management and marketing.

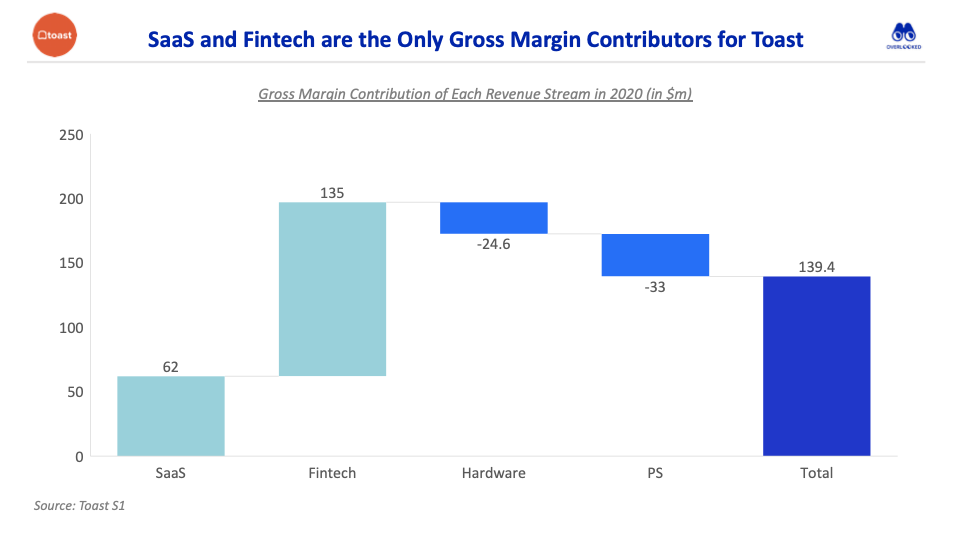

Toast has 4 revenue streams: SaaS, financial services (payment processing and loans), hardware and professional services.

SaaS: restaurants pay to access SaaS products developed by Toast (e.g. POS, kitchen display system, invoice management, digital ordering and delivery, marketing and loyalty, and team management) with a 12-36m engagement.

Financial services: restaurants pay fees to get access to Toast’s services which facilitate payment transactions or to get working capital loans.

Hardware: sale of terminals, tablets, handhelds to restaurants, etc.

Professional services: installation and configuration services for new locations.

SaaS and financial services are Toast's bread and butter. Hardware and professional services are used to reduce the friction to acquire and onboard new customers. However, Toast is generating a negative gross profit on these 2 revenues streams which are only used to reduce the Customers Acquisition Costs (CAC).

Toast is generating $494m in ARR (it includes both SaaS & fintech fees) with 48k restaurants/29k customers, a 118% annual growth rate (super impressive knowing that they were selling to restaurants in the middle of covid) and a 110% annual retention rate.

In the US, there are 11m people working in 860k restaurants. With 48k locations, Toast has only a 6% market share in the country. Restaurants generated $700bn in sales in 2020 (3% of GDP, $810k sales per year per restaurant) and this figures is expected to reach $1.1tn by 2024. Restaurants spend less than 3% of their total revenues on technology ($25bn in 2019, $2.4k per restaurant). It's an industry which underspends on technology as the average for all industries is more around 5% of total sales. If the restaurant industry catches up in the coming year, Toast's total addressable market in the US will be $55bn by 2024 ($4k per restaurant).

Toast has a successful value proposition for restaurant because:

It's an all-in-one platform which is compelling in an under-digitized industry with mostly non-tech savvy workers. Moreover, Toast offers restaurants an unified view of their business instead of having 4-5 different software with siloed data.

It brings operational efficiency in a 4-5% operating margin industry. With Toast, restaurants reduce costs by digitizing and automating processes that were manual and paper based.

It only targets the restaurant industry. It's not an horizontal product. Toast's product is tailor-made for restaurants.

In the coming years, Toast will center its growth strategy on (i) acquiring new customers & upselling existing customer base in North America, (ii) expanding its platform by releasing new product features and adding new partners to its open ecosystem, (iii) expansing geographically beyond North America, (iv) acquiring companies mainly to expand Toast's platform.

Part II - A Quick History of Toast

In 2011, Steve Fredette, Aman Narang and Jonathan Grimm co-founded Toast. They were working together at Endeca (selling software in the ecommerce space) and decided to leave when the company was sold to Oracle. Toast was started as a layer on top of existing POS systems to help restaurants implement consumer-facing innovations such as mobile payments, customer loyalty and social medias. It did not work because it was too hard to integrate with outdated and closed POS.

"Our first attempt at solving this problem failed miserably. It was too difficult to integrate with legacy systems, and we didn’t understand the immense challenges of running a restaurant. So we went door-to-door, listening to restaurant operators"

In 2013, Toast pivoted and decided to create its own POS from scratch. It was a cloud based POS running on Android.

In 2013, Toast raised a round with angels - including former Endeca executives.

In 2014, Toast added online ordering, gift cards, loyalty and kitchen display systems to its platform.

In 2015, Toast brought Chris Comparato as CEO. Chris previously worked as VP of Customer Success at Endeca (together with Toast's cofounder) and at Acquia (digital experience platform for Drupal).

In Jan. 2016, Toast raised a $30m series B led by Bessemer (Kent Bennett) and GV.

In Jul. 2018, Toast reached a unicorn valuation through a $115m series D led by T. Rowe with the participation of Tiger and existing investors at a $1.4bn valuation.

In 2019, Toast raised $250m series E at a $2.7bn valuation in a round co-led by TCV and Tiger.

In 2019, Toast acquired Stratex. It was a US-based company specialised in HR and payroll management. Stratex's product was quickly integrated into Toast platform.

In Feb. 2020, Toast raised a $400m series F at a $4.9bn valuation led by Bessemer, TPG, GreenOaks and Tiger.

In Apr. 2020, Toast laid-off 50% of its workforce as a reaction to the covid crisis. At the time, Toast had staffed its team to expand the business in a normal environment while restaurants sales were down by 80%.

In Nov. 2020, Toast allowed current and former employees to sell part of their shares in a $60m secondary transaction valuing the company at $8bn.

In Jun. 2021, Toast acquired xtraChef. The startup offers tools to streamline back-office operations for restaurants (e.g. account payable automation or inventory management).

In Aug. 2021, Toast filed for IPO. MS and JP lead the offering.

In Sep. 2021, Toast went public raising $870m at a $20bn valuation. During the 1st day of trading, the stock popped by 60%+ increasing the valuation to $33bn.

Part III - What You Can Learn from Toast as a Vertical SaaS?

SaaS TAM = 5% of vertical sales. On average, companies spend 5% of their sales on technologies. It means that a vertical SaaS with an-in-one platform can charge up to 5% of the revenues generated by its customers.

Being the record system. For restaurants, Toast's platform is at the core of their business. Toast started with the POS which put the solution at the center of their customer operations as all transactions passed through the POS. It was a great position to become the tech backbone of their customers.

Expand your TAM by processing payments. Toast is a perfect fintech-enabled business. It has a SaaS product but generates 78% of its revenues and 97% of its gross profit from financial services (both payment fees and interests on working capital loans).

Vertical SaaS can support longer payback period than generalist SaaS. Historically, Toast had a 18-month payback period which is extremely long for a company selling to small businesses (I would have expected something between 6 to 12 months). It works because Toast has a verticalised and all-in-one platform. As a result, it becomes the last software that you will un-plug before closing the restaurant and you have a strong room to land and expand in your customer base by selling them more features every year (illustrated by Toast's 114% net retention rate).

You need to be a vertical expert to succeed. 2/3 of Toast employees previously worked in a restaurant which makes it easier to build and sell the right product for restaurants.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋