👩🍳 Toast - A Lesson on Expanding Your Total Addressable Market

Overlooked #176

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m writing another post on Toast focusing on the company’s playbook to expand its total addressable market.

Toast has experienced a rocky start as a publicly listed company since its IPO in Sep. 2021 at a $20bn market capitalisation in the middle of the tech bubble. Its market cap. peaked at $32.8bn in Nov. 2021 before being massively slashed by investors, reaching a low in May 2022 at $6.5bn market. capitalisation. As of June 2024, Toast trades at a $12.3bn market capitalisation representing a 89% premium from its lowest point but still a 39% discount from its IPO and a 63% discount from its peak.

In the meantime, Toast significantly expanded its business, growing from 57k locations, $10.0k in ARPU and $568m in ARR in 2021 to 106k locations, $11.5k in ARPU and $1.2bn in ARR in 2023. Toast’s strong growth since its IPO and its future growth rely on multiple levers that the company is activating to expand its initial addressable market. On May 29th, Toast held its first Investor Day and provided more insights into these levers. It was a perfect occasion to write a post about them.

(By the way, happy to share my notes on the Investor Day. Feel free to send me an email at alexandre.dewez@gmail.com).

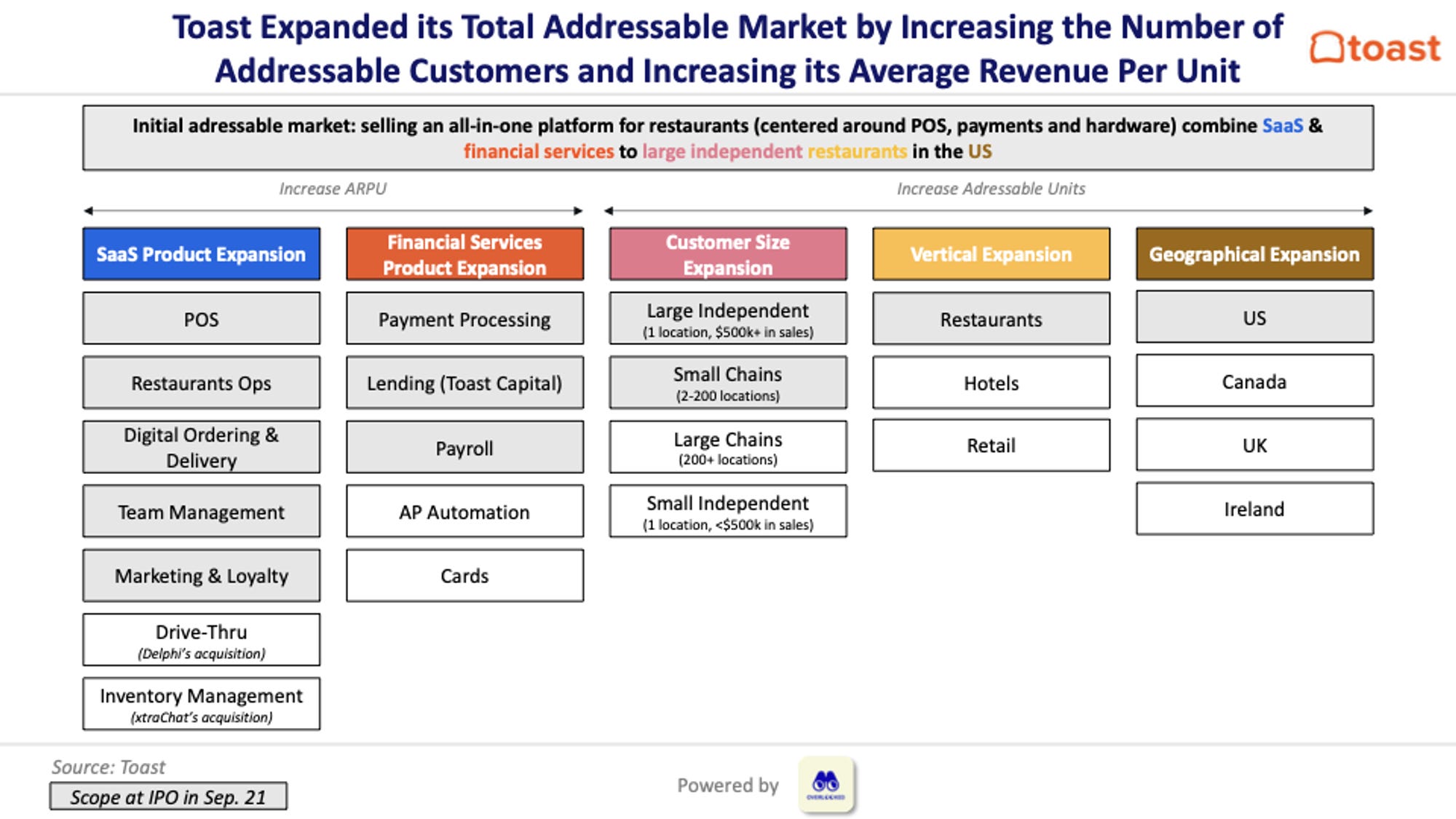

In this post, we’re going to delve into the 5 different levers activated by Toast to expand its total addressable market since its IPO: (i) adding new SaaS modules to its platform, (ii) embedding new financial services into its platform, (iii) moving downmarket and upmarket in the restaurants vertical, (iv) expanding beyond the restaurants vertical, and (v) expanding beyond the US.

Lever n°1 - Launching New SaaS Modules Either Organically or via M&A (5x Potential SaaS ARPU)

Toast’s all-in-one value proposition for restaurants is based on 6 key pillars: (i) restaurant operations, (ii) fintech solutions, (iii) marketing, (iv) digital storefront, (v) team management, and (vi) suppliers and accounting.

The historical and most common entry point for restaurants in Toast’s ecosystem is purchasing the point of sales system bundled with payment processing and hardware. After this, Toast upsells its other modules. In Q4-2023, 43% of Toast’s restaurants were using 6+ products beyond its initial entry point, compared to 32% in Q4-2021.

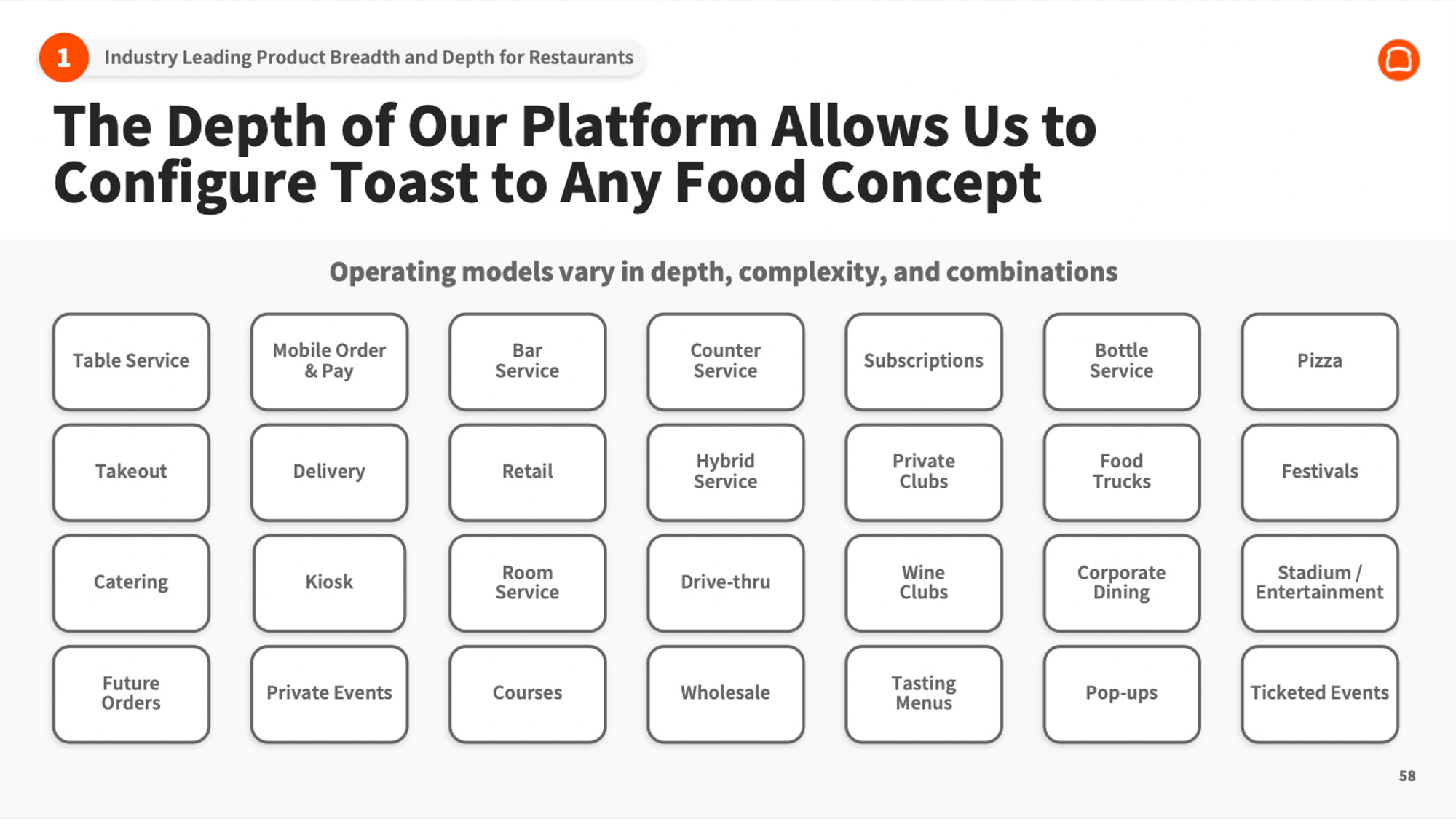

Since its IPO, Toast has maintained strong product execution by adding both new SaaS and fintech modules to its platform. On the SaaS side, Toast is pursuing two directions in parallel: (i) verticalising the platform to better serve various food concepts (e.g. drive-thru, catering, hotels) and (ii) launching new products to strengthen its 6 key pillars.

Toast’s product expansion results from acquisitions and in-house product development. In the past 5 years, Toast acquired 4 companies:

StratEx (Jul. 2019): HR and payroll software for restaurants that Toast integrated into its Toast Payroll and Team Management product.

xtraCHEF (Jun. 2021): suite of back-office tools for restaurants including AP automation and inventory management that was the genesis of Toast’s product expansion into suppliers and accounting.

Sling (Jul. 2022): employee scheduling, communication and management solution that Toast also integrated into Toast Payroll and Team Management product.

Delphi (Feb. 2023): digital display solutions and drive thru technology for Quick Service Restaurants (QSRs) which enabled Toast to better serve the QSR segment.

When it comes to organic product development, Toast launched the following features:

Toast Invoicing (Oct. 2022): catering and wholesale orders management.

Toast Tables (Apr. 2023): reservation, waitlist and tables management integrated with Toast’s guest engagement product in order to get reservations from Google and to have detailed information guests.

Toast Catering & Events (Aug. 2023): manage large catering orders and event planning.

An upgrade to Toast Digital Storefront & Marketing Suite (May 2024): adding a websites builders, AI features for content marketing and more marketing automations.

AI features for Toast Now which is Toast’s mobile app including benchmarking to offer restaurants aggregated data on how they perform against their peers as well as an AI copilot called “Sous Chef” (to be launched in 2024) to provide restaurants with tailor made recommendations.

Lever n°2 - Launching New Financial Services (2x Potential Fintech ARPU)

Embedding payment processing into its POS was a key success factor in Toast’s history. In recent years, the company has decided to double down on financial services by launching products beyond payments including:

Toast Capital (Nov. 2019): $5-300k short-term loans for restaurants via a merchant cash advance solution, in which the loan is repaid based on a fixed percentage of the restaurant’s daily sales. Toast Capital Loans are issued by WebBank, an industrial bank that also works with startups like Shopify, Klarna, and PayPal. Toast earns revenue from underwriting, marketing, and servicing loans, with additional fees based on the performance of the loan portfolio. It has exposure to loan defaults up to 15% of the principal amount. In Q4 2022, Toast disclosed that it made $24m in gross profit from this product, accounting for 17.5% of its total financial technology solutions gross profit. In May 2024, it announced that it had passed the $1bn threshold in loans originated.

Toast Restaurant Card (Nov. 2021): a business debit card for restaurants that provides quicker access to sales and a useful cash-back rewards program for restaurants (e.g. to order kitchen equipments or food from suppliers). Toast earns revenues from interchange fees on these cards.

Toast Pay Card (Nov. 2021): cards for employees to access a portion of their salaries and tips more quickly. Toast earns also revenues from interchange fees on these cards.

Accounts Payable (AP) Automation via xtraCHEF: automates payments to food suppliers with automatic accounting reconciliation. Toast can monetise payments from AP automation by processing payouts through methods like ACH, RTP or virtual cards.

Toast Capital is already generating significant revenues, while other financial products are still in their early stages.

Lever n°3 - Moving Downmarket & Upmarket within the Restaurant Vertical (2x the Number of Addressable Locations in the US)

Historically, Toast focused on large independent restaurants with a sufficient turnover ($500k+ in sales). It did not want to serve large chains because they are slow to transition to the cloud, are hard to monetise through payments, and tend to prefer a best-of-breed approach instead of buying an all-in-one platform.

Toast also avoided small independent hospitality businesses (e.g. small restaurants, bakeries or coffee) because they are much more price sensitive and have a high failure rate compared to Toast’s high single digit annual customer churn.

More recently, Toast started to adapt its platform to serve these two segments:

On the lower end of the market, Toast launched in Sep. 2023 a dedicated offering for cafes and bakeries with more agressive pricing (e.g. a starter kit with a free SaaS and no upfront hardware cost monetising only with a 3.09% + $0.15 per transaction payment processing fee) to compete more efficiently with Lightspeed and Square.

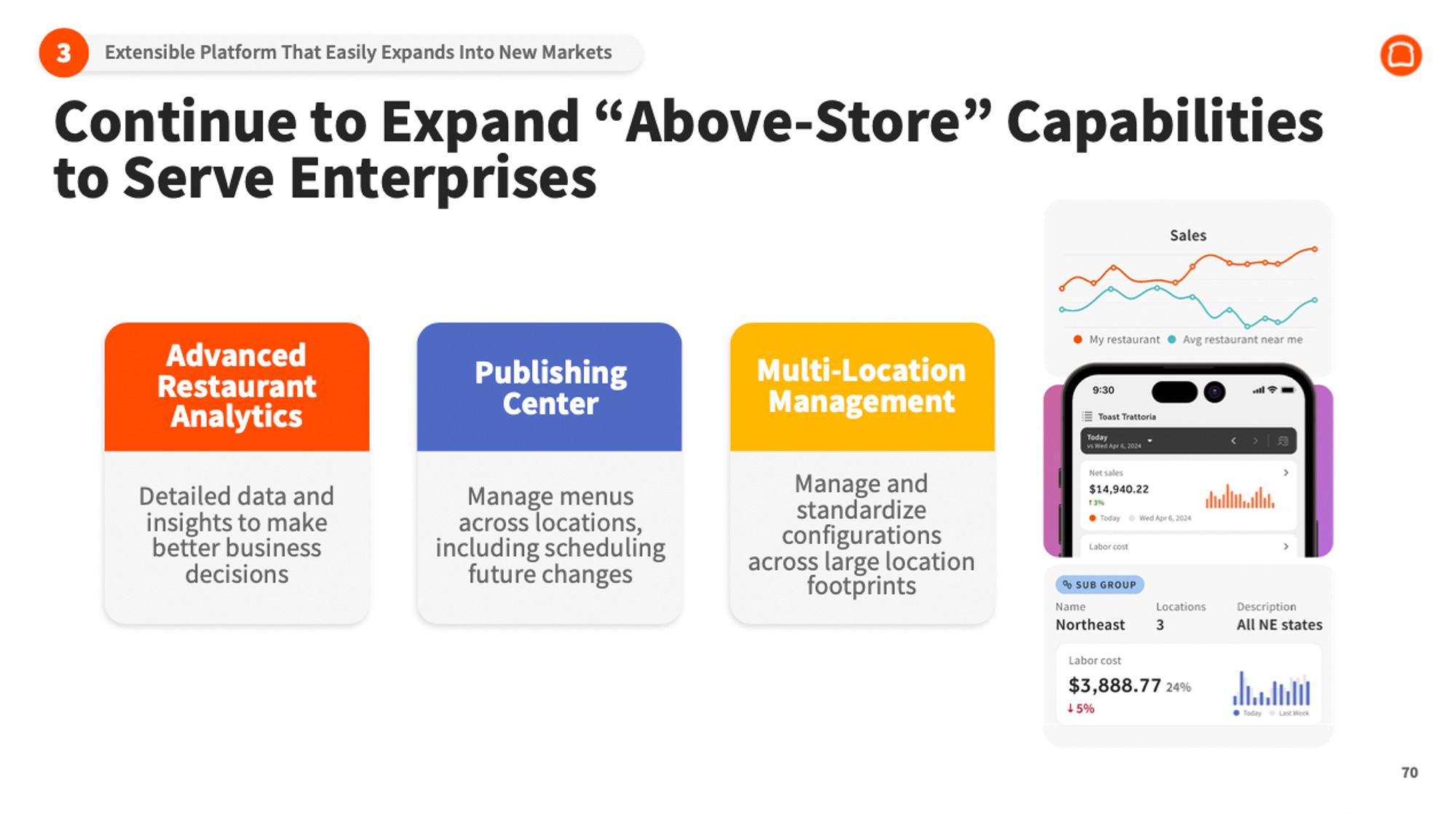

On the higher end of the market, Toast started to build “above-store” capabilities (e.g. analytics, publishing center, multi-location management, benchmarking between restaurants in a group and with the rest of the industry) to serve the multi-location needs of larger chains via its Restaurant Management Suite launched in Apr. 2024.

Lever n°4 - Expanding Beyond the Restaurants Vertical (Adding 220k Locations)

In May 2022, Toast launched a dedicated product to serve hotels food & beverage operations with a strong focus on integrating with leading hotel property management systems (e.g. Stayntouch, BarefootPMS, Mews, Infor) and hotel-specific features (e.g. easily charge a room, handle in-room dining).

In May 2024, Toast announced during its Investor Day that it was expanding into a new vertical beyond restaurants which is the food and beverage retail. The genesis of this expansion comes from restaurants in its customer base evolving to add retail concepts in order to add new revenue streams. Toast began building these retail specific features before expanding into selling to more traditional retail businesses.

Toast’s platform offers numerous horizontal capabilities, including payment processing, lending, scheduling, and payroll, which can be leveraged across multiple verticals. Additionally, Toast has developed a playbook for building vertical-specific features, as demonstrated with its restaurant platform. The company aims to replicate this approach for retail, with innovations such as a mobile app-based smart scan capability that allows businesses to manage their inventory directly on the store floor.

Toast started selling its platform to the retail vertical in 2023 and has since attracted 1k locations. There are 220k addressable locations in the US generating $660bn in GPV ($3m in GPV per location).

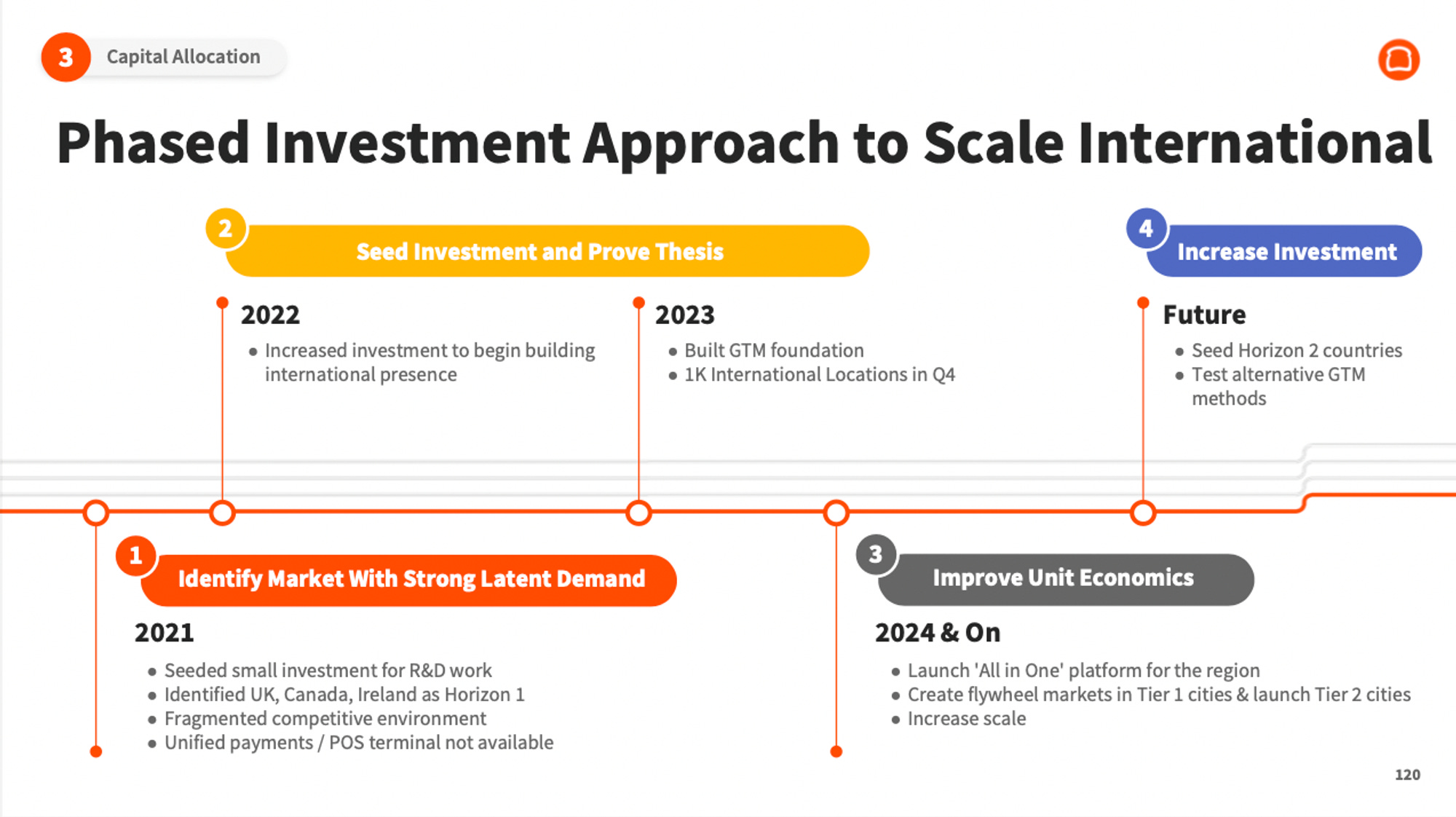

Lever n°5 - Expanding Beyond the US (Adding 280k Locations)

In 2021, Toast began investing c.$10-20m per year to expand beyond the US. It selected Canada, Ireland and the UK (280k locations in these 3 countries vs. 875k locations in the US) as initial targets, arguing that these English-speaking countries had market dynamics similar to Toast’s early days, with a fragmented competitive environment and the absence of a strong local players bundling POS and payments.

To expand abroad, Toast added 4 localisation capabilities (currency, fiscalisation, translation, and local payment methods). When entering a new geography, Toast starts with a limited set of products (POS, payments, KDS and scheduling) before releasing its entire platform.

In Q4-2023, Toast had 1k locations abroad. In May 2024, Toast reached 2k locations adding 1k locations in just 5 months. Going forward, Toast plans to accelerate its acquisition of new restaurants in the UK, Ireland and Canada by replicating successful US GTM playbooks while identifying the next wave of countries to launch.

Conclusion

Since its IPO, Toast has used two main strategies to drastically expand its total addressable market: (i) tripling its number of addressable locations from 438k locations initially to 1.4m today through international expansion, retail expansion and moving upmarket/downmarket within the US restaurant vertical, (ii) increasing its ARPU potential from both SaaS ($5.9k SaaS ARPU in 2023 vs. $30k ARPU potential with its current SaaS suite) and fintech revenues ($5.6k fintech ARPU in 2023 which could potentially double with other financial services like lending, AP automation, cards for employees and for food expenses).

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Merci pour cette analyse pointue et les actions structurées qu'elle sous-tend, profitables à d'autres, même dans d'autres domaines !