🩺 Weave - Streamlining Doctor-to-Patient Communication

Overlooked #199

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a company deep-dive a publicly listed vertical software in the healthcare industry named Weave.

Today, I’m sharing a deep-dive on Weave, a publicly listed vertical SaaS company in the healthcare industry. It’s an all-in-one communication platform between healthcare professionals and their patients covering phone systems, texting, team chat, scheduling, automated reminders, payments, and online review management. Like Olo and Lightspeed which I’ve previously covered in the newsletter, Weave is not a success story on the stock market.

The company went public in Nov. 2021, at the peak of the tech bubble. The stock briefly traded at 8x EV/NTM Sales in Q4-21 and Q1-22, but has never surpassed a 6x multiple since. Today, it trades at a $737m Enterprise Value, with a 3.0x EV/NTM Sales multiple - significantly below the software peer median of 6.1x.

Weave is an interesting story to unpack for two main reasons:

First, Weave is a poster child for the wave of startups that became unicorns in 2020-2021 by raising at inflated valuations and are now struggling. Unlike most of those still-private companies, Weave is publicly traded. It tells the harsh reality story of businesses that failed to evolve from a single-product offering to a true platform, lack meaningful scale, grow slowly, and are barely profitable.

Second, Weave offers vertical SaaS founders meaningful insights into both best practices and common pitfalls.

I divided this post into the following sections: (i) key learnings for vertical SaaS founders, (ii) company history, (iii) product breakdown, (iv) financials.

Part I - Key Learnings for Vertical SaaS Founders

#1 - Finding the right balance between breadth and depth when expanding into adjacent verticals.

Weave began in 2008 focusing on the dental sub-segment of the healthcare industry, before expanding into adjacent verticals like optometry (2015) and veterinary clinics (2018). Around the time of its IPO in 2021, Weave attempted to move beyond healthcare into new markets such as home services promoting a so-called “Vertical Domino Expansion” playbook for scaling across industries. Spoiler alert: it didn’t work. In the years since, Weave has refocused on its core healthcare vertical. Deep industry focus creates defensibility through tailored integrations and support for segment-specific workflows. Companies like Mindbody, ServiceTitan, and Toast have shown that expanding across sub-segments within a single industry can work well. But when a company strays too far from its core vertical, it often loses the retention strength and capital efficiency that make vertical SaaS models so compelling.

#2 - Failing to evolve from a single product offering to a true platform.

Weave boasts gross dollar retention (above 90%), which is impressive for an SMB-focused business and reflects customer loyalty to its core communication product. Over the past few years, the company has introduced several new modules—most notably in payments and AI—but these additions have failed to meaningfully lift key metrics like Net Dollar Retention (still below 100%) and ARPU (which has grown at just a 6.5% CAGR over the past four years). This suggests that Weave is struggling to drive high attach rates for its add-on modules. At the time of its IPO, the company disclosed a payments attach rate of just 12%. When you’re not the system of record for your customers, driving adoption of ancillary products becomes significantly harder.

#3 -Starting with a SaaS business model before layering on financial services and now “AI replacing work”. Weave began as a traditional SaaS platform and later expanded into financial services by offering payment processing with POS and pay-by-link options. More recently, the company now expanding aggressively into AI with a potential to replace work (e.g. AI to automate inbound and outbound calls).

#4 - The “unified phone number” strategy: selling a cloud based phone system acting as a as a central nervous system for handling every interaction between healthcare professionals and patients.

Staff can use a single, shared phone number—accessible via desktop or mobile app—to call or text patients. All communications are visible and collaborative, allowing both front-office and clinical staff to coordinate seamlessly. Recognising the power of this wedge, Weave has aggressively subsidised hardware costs to eliminate onboarding friction and accelerate adoption.

#5 - Missing the defensibility from being a system of records or from having network effects.

Weave is a weak vertical software company because it has no built-in defensibility. The best vertical software companies have defensibility either because they have network effects (e.g. Procore, Doctolib, CCC) or because they have strong lock-in effects as system of records (e.g. Toast, Epic, Mews).

#6 - A gentle reminder that scaling SMBs sales is extremely hard.

Weave’s GTM equation doesn’t work / barely works with a low $5.9k ACV, a Net Dollar Retention below 100%, a CAC payback well above 2 years and increasing at scale. As Weave is not a core system, it has a lower gross/net dollar retention and struggles to significantly increase ARPU. As Weave has no network effects, it does not see CAC decreasing as it scales.

#7 - At scale, vertical software companies serving SMBs are always leveraging the same growth levers:

SaaS product expansion to move from a single product to a multi-product platform (i.e. from phone communications to texts, team chat & appointment reminders),

business model expansion into financial services (i.e. POS & pay by link) and “AI replacing work” (i.e. AI powered receptionist),

going upmarket (i.e. going after DSOs),

geographical expansion beyond the core market (i.e. Canada).

“At the start of 2024, we identified several key focus areas to open up and expand new vectors of growth, including expanding into specialty medical verticals, strengthening integration partnerships, enhancing solutions for multi-location practices, elevating payments as a core component of our product and delivering AI-powered innovations.” - Brett White (Q4-2024 Earnings Call)

#8 - Incumbent vertical software companies are well positioned to rip the benefits of the AI revolution.

As the trusted software provider, incumbents are well placed to embed AI into industry-specific workflows and leverage proprietary data to build superior AI products. Weave is going all-in on AI, with features like review response assistants, personalized email drafting, SMS tagging, and call intelligence for transcription, summarization, and analysis.

#9 - If you are not the operating system of your industry, you’re always at risk of counter-positioning.

Weave is built on top of existing healthcare operating systems—such as patient management systems for dentists or EHRs for hospitals. The advantage of this approach is clear: it allows Weave to integrate seamlessly without replacing entrenched systems, which shortens the sales cycle and lowers CAC. However, if you’re too successful, the operating system provider may attempt to replicate your product, bundle it into their core offering, and undercut you on price. This is exactly what has happened in dentistry, where communication platforms like Lighthouse 360 and Demandforce—both owned by Henry Schein, which also owns Dentrix, the leading dental PMS—compete directly with Weave.

Part II - History

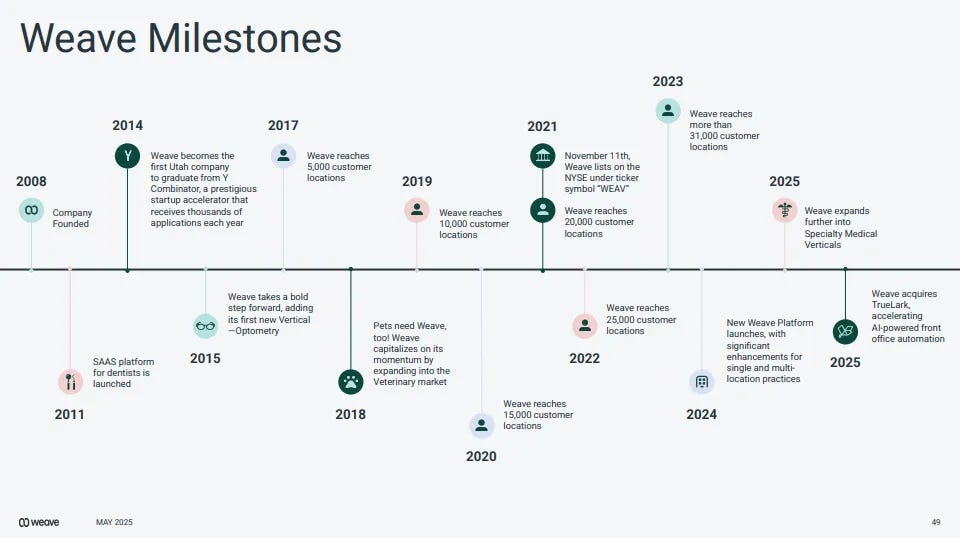

Founded in 2008 in Utah by Brandon Rodman (CEO), his brother Jared Rodman (CCO), and Clint Berry (CTO), the company was originally called Recall Solutions. It initially offered a call-center service to help dentists reconnect with patients for routine appointments. In 2010, the team pivoted away from a manual calling service to a cloud-based communication platform integrating phone and text messages synchronising with patients data. It rebranded as Weave.

By 2013, the startup was nearly out of money and struggling to raise funds in Utah. As a last resort, the founders applied and were accepted to YC in its Winter 2014 batch. It enables them to raise a $5m series A with A Capital to keep building the product and grow the team.

After this, Weave raised multiple funding rounds from investors including Crosslink ($15.5m series B in 2015), Lead Edge ($37.5m series C in 2018) and Tiger ($70m series D at a $900m premoney valuation in 2019).

In Dec. 2020, Roy Banks – a veteran tech CEO with a background in payments – was brought in to replace founder Brandon Rodman as CEO to prepare the company to go public. In 2020-2021, Weave started to aggressively expand its product surface adding payments in Apr. 2020, analytics in May 2020, multi-location in Feb. 2021, and both forms and web assistant in May 2021. It also tried to go beyond the healthcare industry launching in home services.

Weave went public on Nov. 2021 raising $120m at a $1.5bn valuation during the peak of the tech bubble. By mid-2022, Weave’s market cap had fallen below $300m (valued <2× ARR), reflecting the general investor skepticism.

In Oct. 2022, CEO Roy Banks resigned due to health and family reasons, and Brett White (ex. COO/CFO of Mindbody) stepped in as interim and then permanent CEO. Brett shifted the business toward operational efficiency improving margins, refocusing on the healthcare sector and launching new product bets on financial services and AI. In May 2025, Weave acquired TrueLark, an AI-driven virtual front-desk assistant, to advance its automation capabilities.

Part III - Product

Weave is an entire suite of communication tools into a single simple platform available both via desktop and mobile including phone system, texting, team chat, scheduling, automated reminders, payments, and online review management.

Phone system: internet based phone service replacing your existing phone provider with unlimited local & long distance calls, unlimited texting & unlimited rollover lines all through the existing office’s phone number. It’s integrated with the leading PMS and EHR systems to showcase patient information (name, date of the next appointment, overdue payment notes, notes from past interactions) based on the number calling. Weave recently added Call Intelligence which is doing AI generated analysis of calls including sentiment analysis, categorization, transcription, and revenue opportunity identification.

Mobile app: everyone in the office can take calls from anywhere on their mobile devices.

Messaging: the staff can text back and forth with patients from the same dedicated number that you use for phone calls. Weave enables practices to immediately send an automatic text message whenever they miss a call to tell their patients that they will follow-up as soon as they are available. Messaging includes templates, tags and forms to automate conversations management.

Team Chat: it allows practices to keep all team communications in one place - either messages between individual staff members or internal groups messages. It’s HIPAA compliant by design.

Auto Appointment Reminders: the staff can set up auto appointment reminders via text or emails. Reminders can be customised by time, date and type of appointment to make them more personal.

Payments: Weave offers multiple payment options following appointments like text to pay, in person terminal payments or manual entry. Practicians can ability monitor and track payments and payment history on a patient-to-patient basis. In Jul. 2022, it added buy now, pay later.

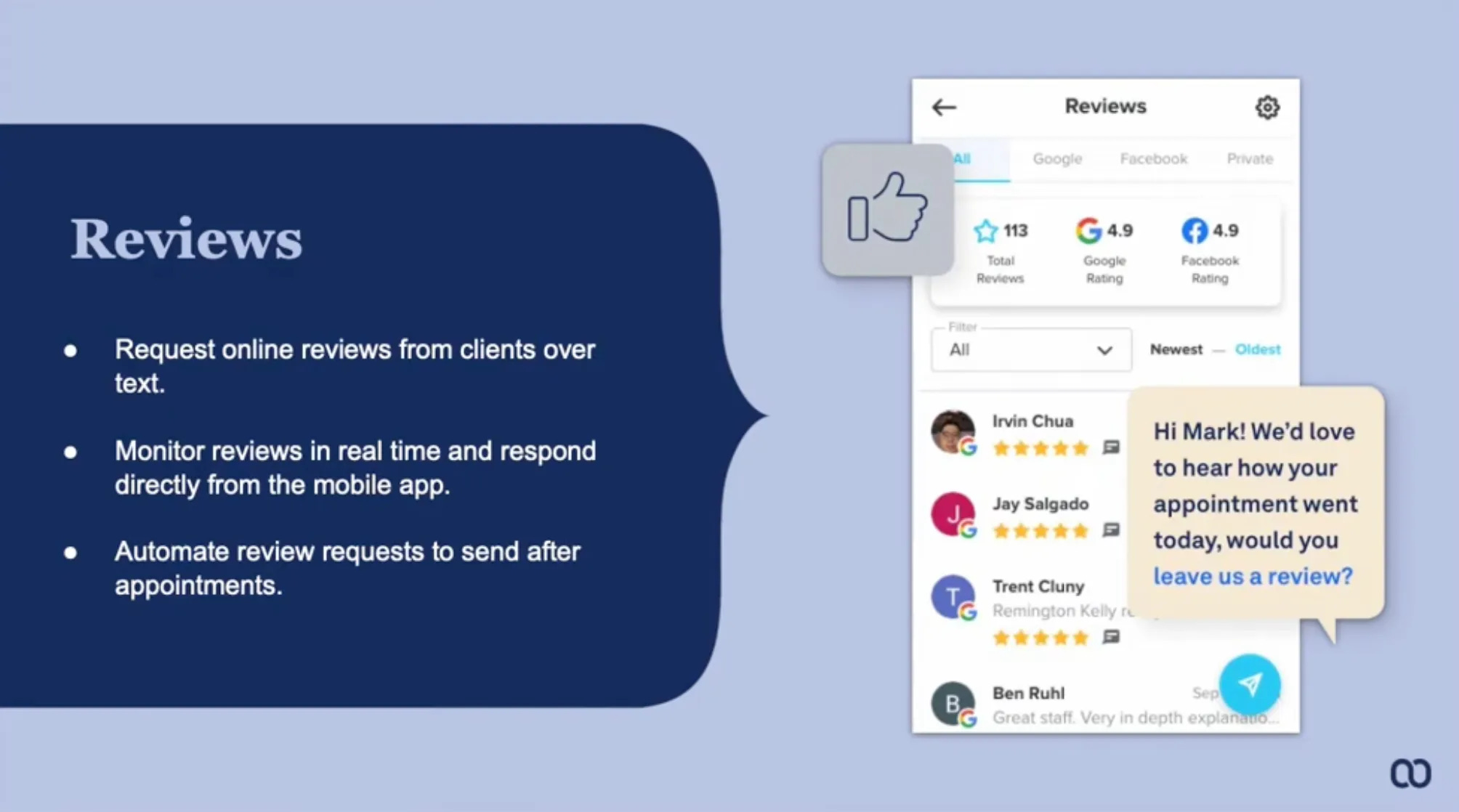

Reviews Management: monitor and manage reviews in real time. Practicians can request reviews from the best patients over text. They can also answer reviews directly from the app. Weave included an AI Response Assistant.

Online scheduling: widget enabling customers to book appointments directly from the website.

Email marketing: enable practicians to craft and send marketing campaigns to patients with pre-built templates and specific call to actions. It integrates AI to pre-draft certain emails.

Weave is an interesting product for multiple reasons:

It streamlines multiple point solutions (email, messaging, reviews, payments, forms, scheduling, etc.) used by practicians to interact with their customers into a single platform saving cost and time.

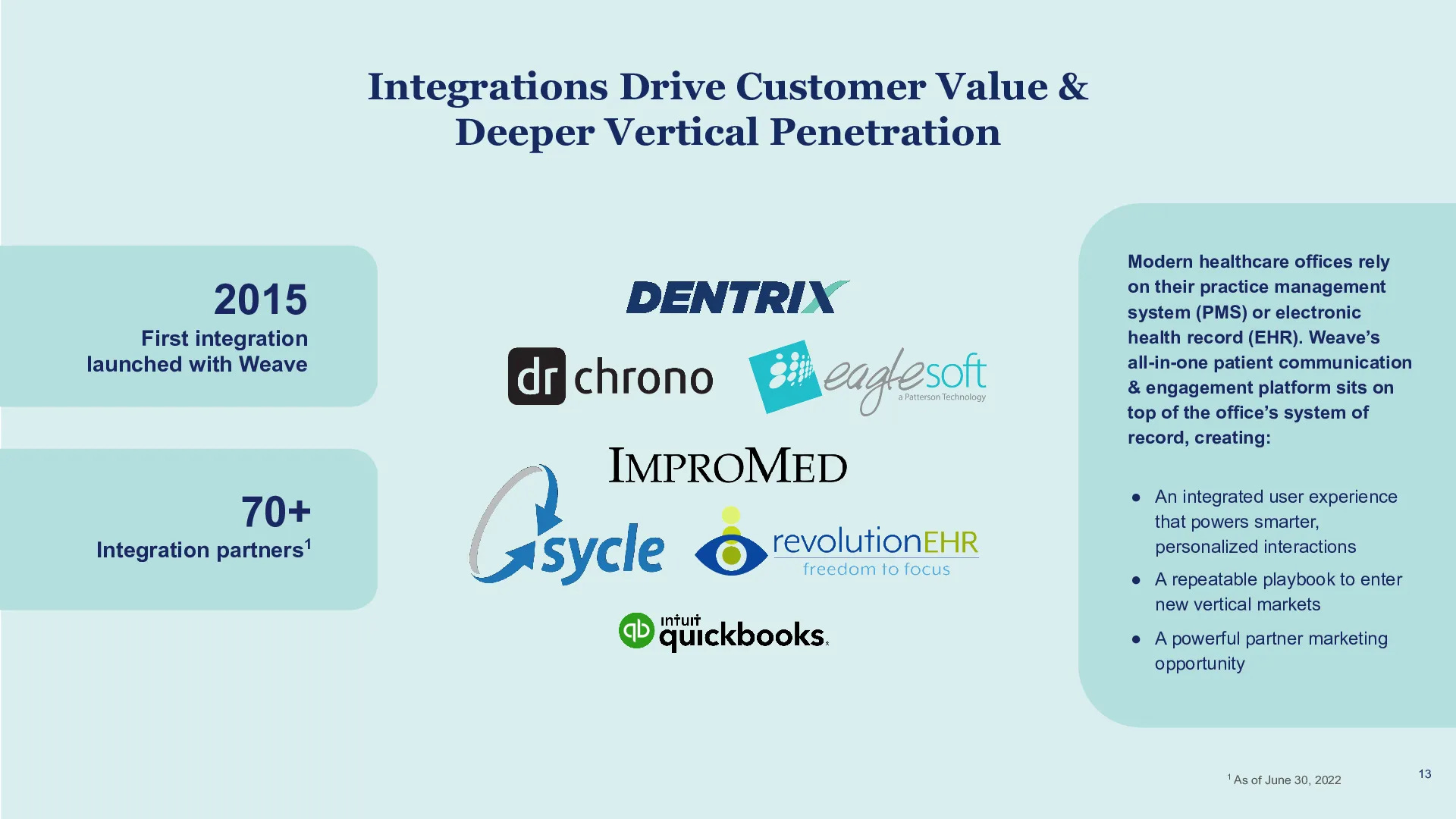

It’s not an industry system of records (e.g. an Electronic Health Records) which makes it easier to sell because you don’t have to rip & replace the core system of your customers and easier to internationalise because you don’t have to adapt to local regulations. Weave has been aggressively integrating with vertical system of records to push/pull data from these systems and to collaborate on co-marketing campaigns.

It’s a platform that can be radically improved by AI because you’re dealing with communications between practicians and patients. Today, calls are automatically transcribed, summarised and analysed. Tomorrow, AI voice agents will automatically process inbound calls. Text messaging, reviews and email marketing have also been augmented by AI.

Part IV - Financials & Metrics

Unfortunately, Weave is a poster child of all the companies which became unicorns during 2020-2021 tech bubble on a first product growing at a good pace and which are now struggling to move to their second act. When most of these companies are still private, Weave went public in Q4-2021 with $118m in ARR growing 40% YoY and with a -3.7% rule of 40 being largely unprofitable. Since then, sales growth has decelerated below 20% YoY while the business is slowly moving towards profitability. In Q1-2025, Weave reached $210m in ARR growing 18.8% while recording a -16.7% EBIT margin (+1.1% on the rule of 40).

Weave is struggling to grow its annual net new locations count. Weave has 35k locations (+22% CAGR over the last 5 years). In 2020, it added 5.5k net new locations. Since then, it has failed to surpass this number - partly because Weave refocused on healthcare customers to improve the quality of its business (higher retention & upsell potential) restraining the pool of addressable customers.

Weave has a net dollar retention below 100% which is hard to sustain to compound high growth at scale. It means that every year, the company is loosing revenues from its existing customer base not being able to compensate customer churn and downgrade by upsell. Businesses targeting SMBs tend to have a net dollar retention around 100% but the best ones are able to reach 110%. Weave’s core issue is less on the retention side as it has a good 91% gross dollar retention for a SMB business but more on the upselling side. It has a $5.9k ARPU which has only grown at a 6.5% CAGR over the past 4 years. It does not have a strong second product that can be upsold for a meaningful amount on top of its communications platform. It has only small modules and payments adoption is too limited to be impactful. Moreover, the fact that Weave is not the operating system of its customers makes it less legitimate to upsell new products on top of the operating system.

Weave’s go-to-market motion is inefficient. Weave has a $23k CAC (including S&M, hardware & onboarding costs) implying a 2 years and 8 months payback period which is extremely long for SMBs (6-12 months would be more standard). Another way to look at it is to compare the number of new locations added to the percentage of sales spent in Sales & Marketing. As discussed, Weave is struggling to grow its annual net new location counts but Sales & Marketing as a percentage of total sales has remained around 41.5% over the past two years.

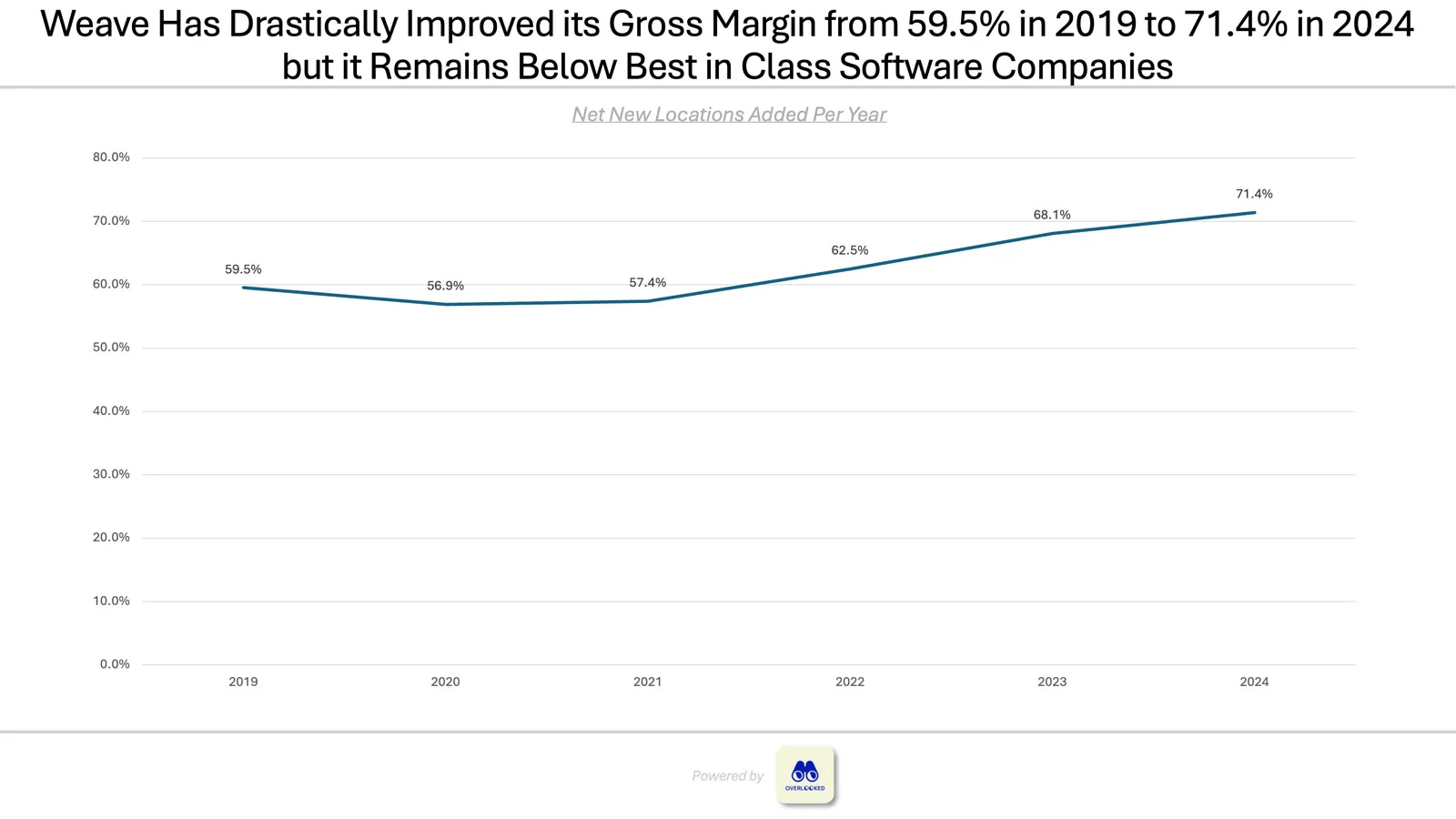

Despite massive improvements, Weave has a gross margin below best in class software companies which is hampering its profitability. In 2019, Weave had a gross margin below 60% for three main reasons: (i) it was optimising growth over profitability, (ii) it was massively subsidising hardware & onboarding to remove any friction to attract new customers and (iii) it’s a communication platform relying on third party providers like Twilio to process phone calls & messages. In 2024, Weave lifted this gross margin to 71.4% but still has room to be best in class.

Weave is underperforming compared to public software companies on almost all key indicators. Compared to the median of Meritech’s tech index, Weave is operating at a smaller scale (4.8x smaller revenues, 7.4x smaller enterprise value). It has a better annual growth rate which is logical because it’s a smaller business but it has a lower rule of 40% due to worse unit economics (barely operating income profitable and smaller gross margin). The median software company is serving mid-market customers with a $77k ACV and a 110% Net Dollar Retention when Weave has a SMBs business with $6k ACV and a Net Dollar Retention below 100%.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋