📖 Venture Chronicles - June 2024

Overlooked #179

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of June.

Saturday, Jun. 1st: AI-based search engine Perplexity is rumored to raise a $250m round led by Bessemer at a $3bn valuation. Perplexity’s ARR went from $3m in October to $20m today, providing further evidence that certain AI companies are beginning to achieve strong commercial traction. - The Information, Techcrunch

In Jan. 24, Perplexity raised $74m at a $540m valuation. In Mar. 24, it raised another $63m round at a $1bn valuation.

“Unlike other enterprise tools for knowledge work like Microsoft Copilot, Perplexity Enterprise Pro is also the only enterprise AI offering that offers all the cutting-edge foundation models in the market in one single product: OpenAI GPT-4, Anthropic Claude Opus, Mistral, and more to come.”

Sunday, Jun. 2nd: Discord’s CEO, Jason Citron, shared an update on Discord announcing that the company was refocusing on its gaming roots. - Jason Citron

“Today, gaming has become the largest form of entertainment in the world, bigger than movies and music combined, and it’s the fastest growing as well. It’s a major way people use their personal devices, including PCs, smartphones, tablets, or consoles.”

“Discord is used by 200m people every month for many different reasons, but there’s one thing that nearly everyone does on our platform: play video games.”

“We’ve recognised the need to narrow our focus from broadly being a community-centric chat app to being a place that helps people deepen their friendships around games and shared interests.”

“We also announced a new Embedded App SDK as a way for platform devs to bring new kinds of games and apps to market directly within Discord, letting players instantly enjoy with their friends.”

Monday, Jun. 3rd: Ed Sim commented the stock market performance of multiple SaaS companies after disappointing Q1-24’s earnings (e.g. Salesforce, UiPath). - Ed Sim

“It has been one of the most brutal weeks for enterprise software stocks, with several iconic companies forecasting slower growth ahead, despite emphasizing the potential of AI. Earnings calls frequently mentioned macroeconomic headwinds and contract delays, but the crucial issue remains: Is the deceleration in software growth due to macroeconomic factors, or is it a consequence of AI advancements?”

“Salesforce Inc. shares dropped the most in almost two decades after projecting the slowest quarterly sales growth in its history, renewing concerns that the company will be left behind in the artificial intelligence boom. Revenue will rise as much as 8% to $9.25 billion in the period ending in July, the San Francisco-based company said Wednesday in a statement. That would be the first quarter of single-digit sales growth for Salesforce in its almost two decades as a publicly traded company."

“The future is not evenly distributed as foundational infrastructure cos like Nvidia for chips, Dell for servers, and Microsoft for cloud continue to accelerate growth while SaaS application cos like Salesforce and Workday are actually slowing down despite promises of GenAI in the future.”

“~50% of AI spend is expected to come from outside of traditional IT budgets, today and in the next three years, a positive for expansion of overall IT budgets as labor savings opportunities from AI are explored. The remaining ~50% is coming from a combination of existing budgets, a headwind we are perhaps seeing today in our CIO survey where spend indications have not yet reaccelerated. Microsoft, unsurprisingly, continues to be the biggest beneficiary of AI spend today, but that is expected to broaden out slightly.” “50% of these dollars for new AI spend will come from outside of IT focusing on jobs to be done while the other 50% seems to be a reallocation which can be a headwind for some SaaS application companies.”

“UiPath has an innovator’s dilemma as I frankly believe many of these larger automation deals can be delivered for much cheaper with GenAI and agentic workflows. There is zero incentive for UiPath to cannibalize itself at the moment until it has to. There will be lots of opportunities for startups who can move fast, price appropriately, and deliver value.”

“Salesforce’s share price dropped more than 20% after releasing its Q2 2024 earnings, despite earnings falling just 0.3% below Wall Street analysts' expectations. What's going on? Two factors appear to be responsible for this decline. First, a slowing economy poses a risk to revenues as customers more carefully evaluate the return on investment of Salesforce’s products before committing to a purchase. Second, analysts are concerned that generative AI could help competitors deliver similar functionalities to Salesforce at much lower costs, which could erode the company’s margins over time.”

Tuesday, Jun. 4th: Mercedes Bent who is a partner at Lighstpeed wrote about the multiple reasons behind the low distribution in the 2019-2022 venture vintage compared to previous vintages. - Mercedes Bent

“The 2019-2022 DPI curve is so flat because: (i) higher entry prices, (ii) bear market crash closed M&A and IPO windows, higher IPO thresholds, (iii) number of acquisitions in 2022 lower than all prior 10 years, (iv) higher funding levels enabling companies to live longer and (v) less ability/focus for managers in vintage to sell early.”

“The real question is whether the most recent cohort can reaccelerate with the next bull market? Or will the initial S-curve trajectory weigh them down?”

Wednesday, Jun. 5th: I listened to Jason Lemkin’s SaaStr talk on the most common go-to-market mistakes. - SaaStr

You should not hire a VP of sales who doesn’t want to sell or learn your product. You should not hire salespeople (from SDRs to CROs) who are not great at demoing your product, and demoing your product should be part of the recruiting process. Moreover, there are many VPs of sales who are burned out. They no longer want to sell. They just want to manage, look at dashboards, and stay at home.

You should not hire a VP of marketing who can’t do demand generation. In the early days (i.e. before $10m in ARR), you don’t need a product marketer creating landing pages per product and customer persona. You should not hire a strategist who tells you that he needs a team and does not want to get his hands dirty. You should hire marketing people who are proud to deliver outcomes to sales (e.g. X number of leads per month).

Founders should not step out of sales for a long time in the company’s journey. When the founder steps out of sales, the hardest deals don’t get closed because others don’t know all the nuances from day one (e.g., product details, competition, etc.). Sales teams will be better openers and closers, but involving the CEO in a deal increases the odds of closing because customers love to talk to the CEO, who is the best middler.

If you cut your marketing budget too deeply, it’s going to be impossible to sustain a good growth rate in the mid-term. When you cut sales, you cut your present. When you cut marketing, you cut your future.

You should jump on the AI bandwagon. Even if integrating AI does not seem magical in your B2B application, you should add it because most software budgets have become AI budgets, and your competition will certainly move in that direction. You will lose deals if you don’t have AI feature parity.

You should not put profitability above growth. Growth is worth much more than profitability in venture because you want to build a $100-200m ARR in 5-10 years. You go nowhere in venture by being profitable with no growth.

Thursday, Jun. 6th: I listened to Jason Lemkin’s introduction talk at SaaStr on the tech market. - SaaStr

Founders cannot control everything (e.g. public multiples) but they can keep increasing their competitive position (e.g. building a better product, being more customer centric).

Tech companies are not performing equally. There are three categories:

Tech companies selling to the real world (e.g. prosumer, vertical SaaS, security) are doing well:

Canva growing at 40% YoY at $2.3bn in ARR and being profitable for years

Toast growing 32% YoY at $1.3bn in ARR

Samsara growing 39% YoY at $1.1bn in ARR

Klaviyo growing 42% YoY at $750m in ARR

Monday (Asana for non tech companies) growing 34% at $900m in ARR

Zscaler growing 32% at $2.2bn in ARR and other cybersecurity companies like Wiz, Crowdstrike

Tech companies selling to other tech companies are not doing well because companies are still cutting drastically their software expenses:

MongoDB down 23% after earning reports because lower growth forecasts

UiPath down 30% after earning reports because no net new customers

Salesforce was down 20% after its earnings report because it disclosed that it was going to grow only in single digits, meaning that it is no longer a growth stock. Deals are contracting. Deals are smaller and take longer to close. Salesforce disclosed today that they need 3x pipeline coverage to make their numbers compared to 2x 18-24 months ago.

ZoomInfo’s tech NRR is down from triple digits to 85%.

AI companies that are living in their own tech bubble.

B2B lags B2C about 2 years. B2C started to bounce back in 2023 which implies that B2B could bounce back in 2025.

In May 2024, Gartner raised its estimate for software spent growth to 20% for 2024 to reach $674bn mainly driven by AI (captured mostly by cloud providers and Nvidia). AI budget is not a net new budget but it’s a budget coming from other software budgets (e.g. Veeva’s pharmaceutical customers cutting their budgets for Veeva to do AI drug discovery).

VCs are deploying a lot of capital into AI companies (e.g., $1bn raised by Scale AI, $6bn raised by xAI) because they believe that several AI companies will have a commercial trajectory similar to OpenAI.

VCs are deploying capital into three segments in the market: (i) seed rounds, (ii) AI companies and (iii) winners in their portfolio.

Most US funds are focused on finding $10bn+ outcomes. When these funds look at the public market, there aren’t many companies worth more than $10bn (e.g., Rubrik and Klaviyo are valued below $10bn), and these funds concluded that AI might be the only category that can produce these types of outcomes.

SaaS companies should not fight the AI wave. You need to implement AI in your product no matter what because you’re going to lose deals to competitors that are promoting it. Customers believe that AI is the future and that its impact will improve over time.

Many SaaS companies are taken private by PE funds because the public market does not work for many SaaS companies (e.g. Squarespace acquired for $6.9bn by Permira).

Vista wrote off its Pluralsight’s $3.5bn acquisition because the company was no longer able to service its debt due to slower revenue growth and higher debt costs. PE funds don’t typically handle multiple write-offs. If we see many more write-offs, we could see PE funds retreating from investing in startups, removing a key exit option for the tech market.

Friday, Jun. 7th: Creandum raised €500m for its seventh fund to invest in 35-40 European companies at seed and series A stages. - Creandum, Sifted

The fund was raised in 12 weeks from 30 global GPs and with 50% of the capital coming from US investors. “5 out of the 8 largest US university endowments are now invested in Creandum funds.”

Creandum has offices in Stockholm, Berlin, London and San Francisco. Creandum was successful in expanding beyond its initial Nordics market (esp. in the UK and Germany) and in betting earlier than other funds in emerging tech ecosystems in Europe (e.g. Spain and Eastern Europe).

Creandum has a strong track record, with 1/6 of its 200 investments reaching unicorn status. Previous funds have achieved valuations between 6x and 13x. The firm has backed companies like Spotify, Klarna, Bolt and Kahoot!

“Europe has all the ingredients to produce the category-defining companies of the future and we can’t wait to support a new generation of founders on their paths to get there.”

Saturday, Jun. 8th: SAP announced its intention to acquire WalkMe, a leading digital adoption platform (DAP) provider, for $1.5bn in an all-cash deal. - SAP, Techcrunch

A DAP is a software tool designed to facilitate the seamless adoption and proficient use of other software applications by providing real-time, in-context guidance and support (e.g. walkthroughs, smart tips, self-help menus, notification bubbles, and in-app training content). DAPs also provide analytics to track user engagement and identify areas where users struggle, enabling continuous improvement of the user experience.

WalkMe was founded in 2011 in Israël. It went public in Jun. 2021 at a $2.6bn valuation. Its stock has been massively impacted in the public market reaching a $600m market capitalisation bottom. WalkMe had 1.6k global customers (35% of F500 companies, 42 customers doing $1m+ in ARR), a 101% net dollar retention in Q1-24 (vs. $121% at its peak as a public company in Q4-21) and a 6% operating margin in Q1-24. SAP’s acquisition is done at a 4.5x EV/ARR multiple (vs. 5.9x EV/ARR median multiple for SaaS companies using Meritech’s simplified definition for ARR multiplying the last quarter SaaS revenues by 4).

WalkMe recently introduced WalkMeX which is an AI-powered copilot suggesting the best next step for any workflow, anywhere using its existing contextual awareness. It will be integrated into SAP’s AI copilot called Joule.

It is SAP’s third $1bn+ acquisition in the past 4 years after Signavio’s acquisition (business process automation) in Jan. 2021 for $1.2bn and LeanIX’s acquisition (software architecture mapping) in Sep. 2023.

Sunday, Jun. 9th: Sam Blond shared GTM advice to founders at SaaStr. - SaaStr

Do not outsource sales recruiting because you end up loosing more time compare to doing it in-house and because sales candidates working with recruitment agencies are not the best salespeople.

Focus on demand until you have too much. The biggest opportunity in sales should not be on optimising conversion rates within your sales pipeline but on creating much more pipeline than you can process. In a sales demand poor environment, the right answer is to work on generating more demand and not to hire more salespeople.

How to generate demand?

You should do things that stand out (e.g. Salesforce’s no software campaign outside a Siebel conference to challenge the market incumbent) instead of relying only on basic demand generation channels (e.g. paid advertising on Meta & Linkedin, sponsoring events, cold-calling). The most successful campaigns to generate demand are things that are completely out of the box. You should do 2-3 creative campaigns to generate demand that nobody else is doing.

You should leverage happy customers to generate new ones. If you’re delighting customers, customers will generate referrals, will talk on social media about their experience or will talk at a conference you organise. You can go above and beyond to leverage your happy customers by thanking them with a unique and personalised gesture (vs. just thanking them over email).

Content distribution is as important as the announcement. You should work on finding the supporters to help you amplify your distribution. For its fundraising announcement, Brex created a spreadsheet with all the famous people employees knew and ask them to talk about the fundraising the day it was announced.

You should be prescriptive on how to buy your product. As you’re introducing a customer to your product, you should give him the details on the purchasing process (e.g. pricing, steps in the sales process, etc.). Customers want to be educated on how to buy your product. Customers will give you feedback along the way but it’s better to proactive than reactive.

You should meet prospective customers in person. It changed during covid with many people working from home but the reality is that the conversion rate is higher when you meet customers in person compared to over zoom (e.g. 3x more conversion rate at Brex).

Monday, Jun. 10th: I watched a SaaStr’s video on bringing efficiency to your go-to-market strategy with Kyle Norton who is CRO at Owner which is selling a marketing platform for independent restaurants. - SaaStr

Kyle joined Owner as CRO when the company was generating $3m in ARR. The company went from $3m in 2021 to $6m in 2022 before scaling to $16m in 2023. Today, the company is generating $21m in ARR. Owner managed to achieve this growth while improving efficiency, with the burn multiple going from 1.2 to 0.9 as the company grew from $6m in ARR to $16m.

At the beginning, Kyle inherited a team with 1 manager, 4 sales reps and a massive 30% churn rate after 90 days. In 2022, Kyle rebooted the sales organisation firing 2 sales reps, addressed the churn rate, re-platformed Salesforce and reviewed the sales tech stack.

Initially, Owner was closing many poor fit customers because of bad targeting on prospects and sketchy handoff post signing. Owner had to learn to say no to many customers (40% of prospects Owners used to close). You should focus on customers quality before focusing on bringing as much quantity as possible.

“We had a growth plan. I basically paused on it. I said until we get churn in a better place, I don't want to add a bunch of reps and I don't want to spend a bunch of money in marketing. Let's just dial in the economics and get to a sustainable place to feel like the machine was working before we add gas to it.”

“To focus on high quality customers that would turn into high quality customers, we built an expected GMV scoring thanks to machine learning trained on online restaurants data (reviews, volumes from 3P delivery apps) and on data in our customer base. The higher the potential GMV, the higher the retention rate. It’s hard because you’re taking away a lot of your ICP and TAM but it’s the right way to scale.”

Companies should invest earlier in prospect data. You should position your BDR team so they don’t have to do any research on their leads. If you don’t, BDRs will spend a lot of time calling restaurants without good data or will spend a lot of time doing data research.

You should not scale too early. You should make the math work before scaling. Most companies have a pipeline problem, not a rep capacity problem. If you do the calendar test with reps, you will see that most of them don’t have 3-4 calls per day with new customers. In this case, you should focus on generating more leads for them, including increasing the number of SDRs. You should have 2 SDRs per AE to serve SMB models if you’re great at outbound.

Your sales leaders should also be responsible for post-sales. Otherwise, they are not sufficiently concerned about deal quality and the link handover between the sales team and the onboarding/customer success team.

How to operate a sales team at scale with rigour? Kyle talks about 3 main instruments: monthly business reviews, performance management and documentation.

The monthly business review is something that the sales team does every month at the beginning of the month to reflect on the past month. Every leader in the sales organisation has to complete a section and the sales ops team will add the sales data. You set up a framework with questions that sales leader will answer. Everyone reviews the docs and pull up the discussion topics.

In the monthly business review, you will also review the performance of sales reps with a constant comparison with previous months. You should only keep the best performing sales people.

You should be best in class in documentation (e.g. training pages) to onboard sales people faster and to remove the need to answer basic questions.

Tuesday, Jun. 11th: PowerSchool is taken private by Bain in a $5.6bn deal paying a 37% premium on the company’s shares price and valuing the company at a 7.8x EV/ARR multiple. Existing investors Vista and Onex will remain shareholders in the company. I previously covered PowerSchool in this newsletter. It’s an all-in-one platform for K-12 schools in North America to manage their operations. It’s used by 17k schools and 55m students. It generates $720m in ARR and 33% EBITDA margin. Bain’s value creation playbook seems to be centered around international expansion beyond North America as well as adding AI capabilities to the platform. It’s yet another example of private equity funds being active buyers of publicly listed tech firms. - Techcrunch, BusinessWire

Wednesday, Jun. 12th: Carta is orchestrating a secondary sale that would value the company at $2bn compared to the $8.5bn previous valuation when it did its previous secondary in late 2022. Carta started as cap. table management software for startups before expanding into the broader private equity asset class and into VC funds administration. It tried but failed to launch a stock secondary marketplace. - Techcrunch, Sheel Mohnot, Henry Ward

Carta tried to sell its secondary shares with Jefferies at a $4bn valuation but it did not work. In total, Carta raised $1.2bn from investors including USV, Spark, Tribe and a16z.

Carta is doing $370m in revenues per year with cap. table management doing $200m in revenues, fund admin $100m and private equity $20m. It also lost $65m in 2023.

“I’ve been working on the startup liquidity problem for almost a decade and spent $150M trying to solve it. After a lost decade (and an unbelievable amount of money) I have concluded that building a secondary private marketplace is an intractable problem that can’t be solved.”

“One of the features of being a Private Company CEO is that we don’t have to enter a transaction without knowing the price beforehand. We don’t want to discover the price. We want to set the price and we want to keep the price we set.”

“Startups are volatile. The way we protect employees (and shareholders) from that volatility is to create (artificial) stability in the stock by preventing price discovery outside of funding rounds”

Thursday, Jun. 13th: Frank Rotman who is a GP at QED talked about the current venture market. - Frank Rotman 1, Frank Rotman 2

“Early in the correction cycle there was a lot of denial by Founders, VCs and LPs, but this denial has for the most part gone away. For many startups it’s clear that it will be challenging if not impossible to earn their way into their last valuation. For many investors it’s clear that they’re playing to recoup their money (i.e. – playing for pref) rather than playing for “fund returning outcomes”. And for many LPs, they realize that this is an industry wide phenomenon because every active fund manager played the game that was on the field.”

“VC know that they have one or two funds that are going to underperform but are excited about their front book opportunities. So the “new deal” they’re making with LPs is that they’ll try to quickly recoup what they can and make the most of the back book in return for being more disciplined going forward.”

“The “new deal” they’re making with VCs is that they’ll forgive a bad vintage if the VCs will be honest with them about what the back book is “worth”, be more disciplined going forward and they’ll do everything they can to return some cash “soon”.”

“The net result of this “Grand Reset” is that there’s no longer incentive for anyone to maintain the illusion they can shepherd mediocre companies towards billion-dollar IPOs that aren’t going to happen. Instead, the focus has shifted towards "landing the plane" for the 90% of companies that aren’t ever going to achieve escape velocity. This generally means navigating an acquihire for struggling companies and helping “good but not great” portfolio companies find exits through acquisitions or mergers even if it means selling for a fraction of their inflated peak valuations.”

“VCs are re-evaluating their investment theses, focusing on strong unit economics and caring about capital efficiency.”

“LPs are seeking to re-up with Funds that have great pre-2018 track records and have a true competitive edge in today’s new normal environment.”

“The unfortunate truth is that once it’s clear that a Startup is going to struggle to achieve escape velocity, they need to work with their Investors to “Land The Plane.””

“Most successful M&A transactions occur between known parties. […] Many times the buyer is a company that already interacts with the Startup in some form or fashion or has already expressed interest in the past.”

“Companies have to cut the burn and get down to being default-alive. Acquisitions then become more attractive for the buyer and the seller. A company becomes an asset when it starts making money. It can be seen as a liability in many cases as long as it's burning cash.”

Friday, Jun. 14th: Matt Turck who is a GP at Firstmark wrote about the impact of AI on the software market. - Matt Turck

“What seems to be happening: (i) tough macro, cost cutting, (ii) AI sucking the air out of the room, (iii) SaaS vendors perceived as “last generation” despite best efforts to add AI quickly, (iv) enterprise budgets for AI are not net new, they’re taken from somewhere (SaaS budgets cut), (v) bulk of budgets going to OpenAI/Azure etc because low hanging fruit to “do AI” (knowledge bot, coding), (vi) for the more specialized enterprise apps, customers feel like they can/should “build” internally rather than “buy”.

“What happens next: (i) customers realize that “build” is a headache, not always good, (ii) OpenAI / Azure etc can’t / doesn’t want to build hundreds of problem specific/ vertical specific apps, (iii) takes time, but legacy and new SaaS companies truly become AI-first (not just marketing), abstract away complexity of deploying LLMs, (iv) macro environment eventually rebounds, (v) AIaaS becomes the new SaaS - what is old is new.”

“Given the speed at which you can build SaaS products and services, will current SaaS companies keep expanding and dominate because they already have distribution or there is space for new SaaS companies starting from zero? I think there is room for a new generation of “intelligence first” SaaS startups leveraging AI to do things that can only be done with AI (combing through massive amounts of documents or data to generate something). But not every problem needs AI.”

Saturday, Jun. 15th: I watched Apple’s 2024 WWDC. - Apple

On visionOS which is Apple’s OS for its Apple Vision Pro released in Feb. 2024:

“Apple Vision Pro and visionOS unlock completely new possibilities for entertainment, productivity, collaboration, and so much more.”

There are already 2k apps specifically created for the Apple Vision Pro.

“visionOS 2 propels spatial computing forward with new ways to connect with your most important memories, great enhancements to productivity, and powerful new developer APIs for immersive shared experiences.”

Apple is releasing new APIs for developers to build new apps on VisionOS including: (i) Advanced Volumetric API to allow even the most complex 3D apps to run side by side for the ultimate multitasking experience, (ii) TableTopKit to quickly create apps that anchor to flat surfaces like manufacturing workstations or board games, and (iii) enterprise specific APIs to power use cases like surgical training in healthcare and equipment maintenance in manufacturing.

On iOS 18:

You can now lock a specific app with Face ID or Touch ID to avoid people accessing certain apps when they use your phone. You can also hide some apps.

“You can use the satellite capabilities on iPhone 14 to connect to satellites hundreds of miles above the Earth to text your friends and family when you're off the grid all right from the Messages app.”

“We're introducing Tap to Cash, a quick and private way to exchange Apple Cash without sharing phone numbers or email addresses. With Tap to Cash, you can pay someone back for dinner just by holding your phones together.”

On WatchOS 11:

“We're introducing Training Load, an insightful way to measure how the intensity and duration of your workouts are impacting your body over time.”

“The personalization even extends to your Activity rings where you can now adjust your goals by the day of the week. Or if you have an injury that's making it harder to close your rings, or maybe you just need a day off, you can pause them, for a rest day, week, or more and keep your award streak going!”

On AI:

“Recent developments in generative intelligence and large language models offer powerful capabilities that provide the opportunity to take the experience of using Apple products to new heights.”

Apple aims to build AI products that are powerful easy to use, context aware and respectful of privacy.

“Apple Intelligence is the personal intelligence system that puts powerful generative models right at the core of your iPhone, iPad, and Mac.”

“It draws on your personal context to give you intelligence that's most helpful and relevant for you.”

“Apple Intelligence will enable your iPhone, iPad, and Mac to understand and create language, as well as images, and take action for you to simplify interactions across your apps.”

“For example, your iPhone can prioritize your notifications to minimize unnecessary distractions, while ensuring you don't miss something important. Apple Intelligence also powers brand-new Writing Tools that you can access systemwide to feel more confident in your writing. Writing Tools can rewrite, proofread, and summarize text for you, whether you are working on an article or blog post, condensing ideas to share with your classmates, or looking over a review before you post it online.”

“Apple Intelligence is grounded in your personal information and context with the ability to retrieve and analyze the most relevant data from across your apps, as well as to reference the content on your screen, like an email or calendar event you are looking at.”

“Today, Siri helps you get everyday tasks done quickly and easily. In fact, Siri users make 1.5 billion voice requests every single day. Thirteen years ago, we introduced Siri. The original intelligent assistant. And we had an ambitious vision for it. We've been steadily building towards that vision. And now, thanks to the incredible power of Apple Intelligence, we have the foundational capabilities to take a major step forward. So we can make Siri more natural, more contextually relevant, and of course, more personal to you.” “You can switch between text and voice, communicating in whatever way feels right for the moment.”

“There are other AI tools available that can be useful for tasks that draw on broad world knowledge, or offer specialized domain expertise. We want you to be able to use these external models without having to jump between different tools. So we're integrating them right into your experiences. And we're starting out with the best of these, the pioneer and market leader ChatGPT from Open AI, powered by GPT-4o.”

Sunday, Jun. 16th: I watched a SaaStr’s video with Jason Lemkin about under-discussed SaaS metrics that matter in 2024. - SaaStr

In the long term, net new customers count has a bigger impact on your business than revenue growth. “If your new customers didn't grow at least half of your revenue growth, your future is not secure because you’re shrinking in relevance and market share. In the last 18-24 months, it got worse because companies tried to squeeze every dollar from the customer base with price increases, higher deal sizes, aggressive renewal policies, etc. It’s financial engineering that might work for a couple of years but not in the long term. Of course, revenue growth at the end of the day is what matters for a while in SaaS but your future is secured only by growing your customer count.”

Growth is worth 2-3 times more than efficiency. It’s not the era of profitability. Profitability is not the key to success. You need to be efficient, but you need growth to be valuable. In the public market, if you grow less than 10% YoY, you’re no longer considered a growth company, and your market valuation is drastically impacted. Being profitable is necessary but not sufficient for a VC-backed company because being only profitable will not give you a high valuation.

The bar to go public has never been as high as it is today. Since the crash in December 2021, only two companies have gone public: Klaviyo and Rubrik. Both were generating $500m in ARR, growing 50% YoY, and being profitable. They’re trading at less than 10x EV/ARR.

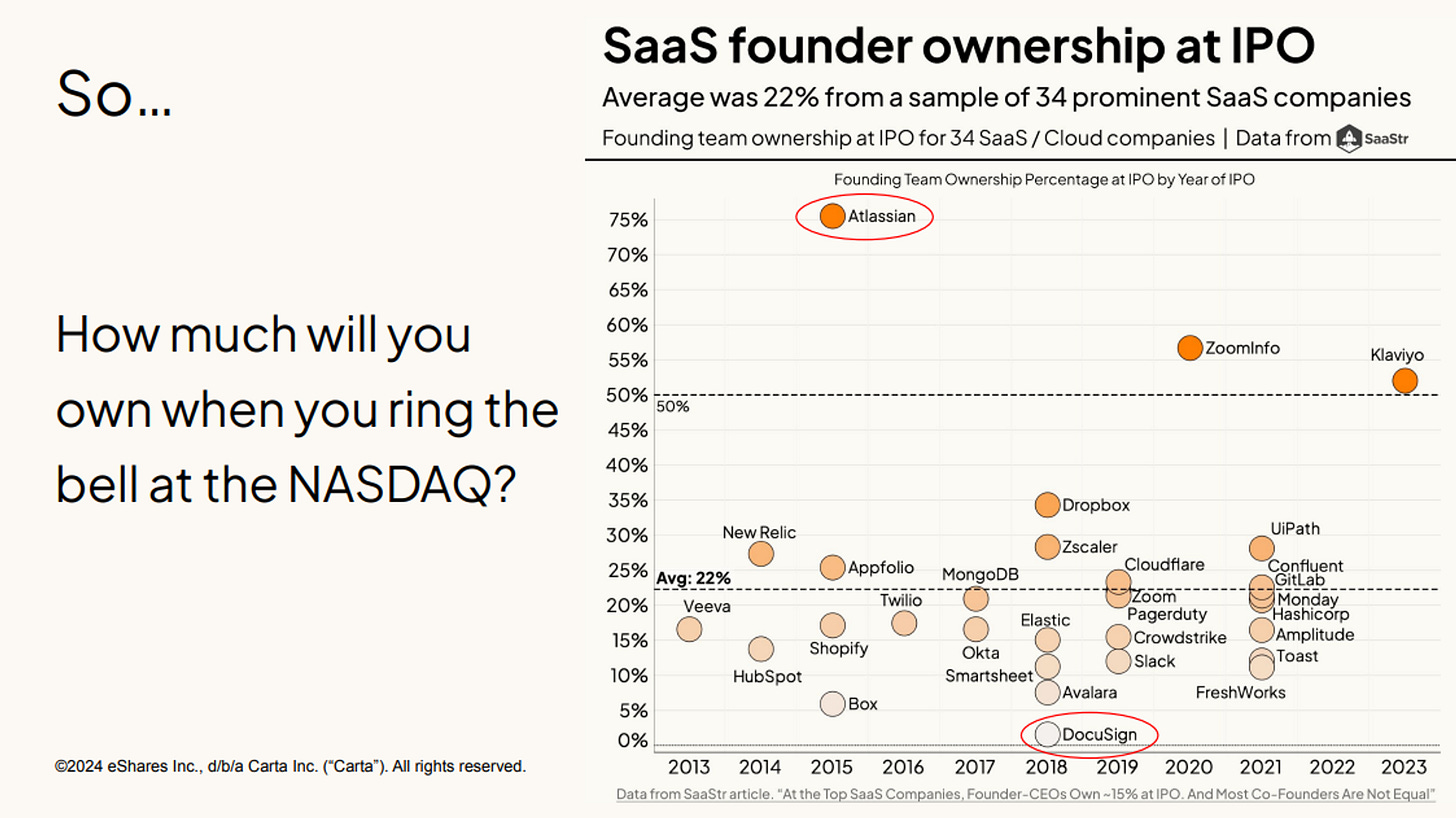

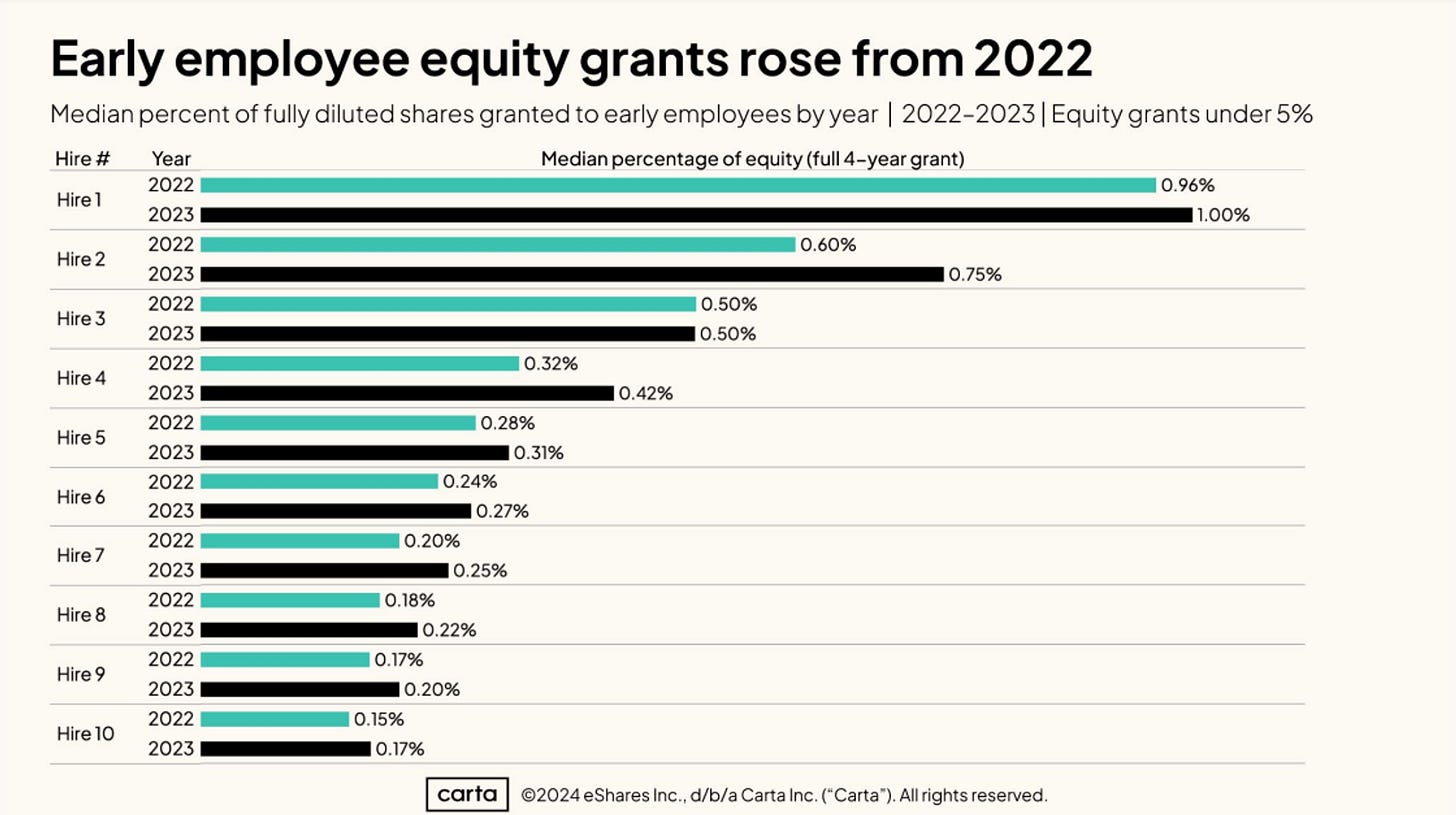

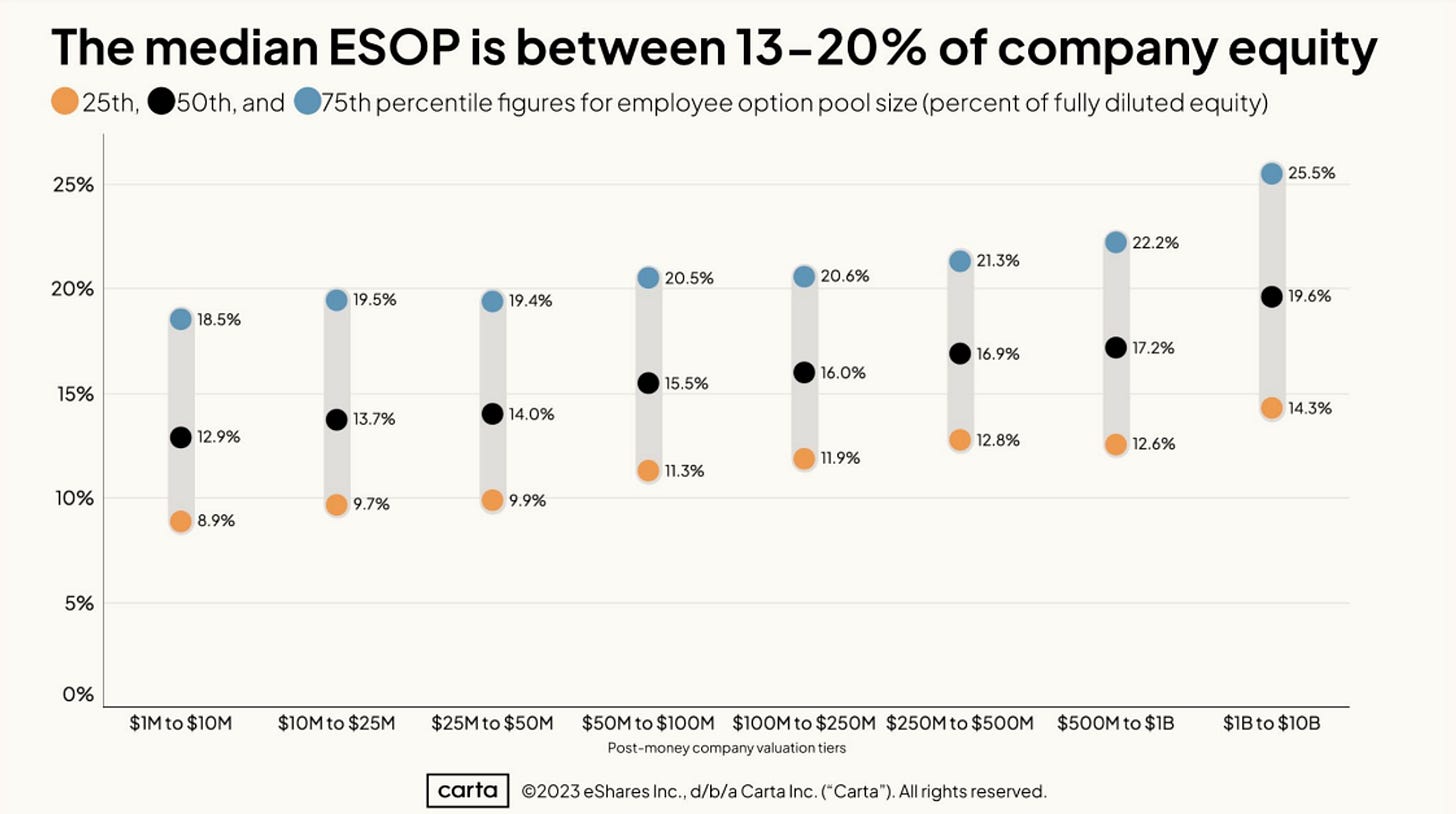

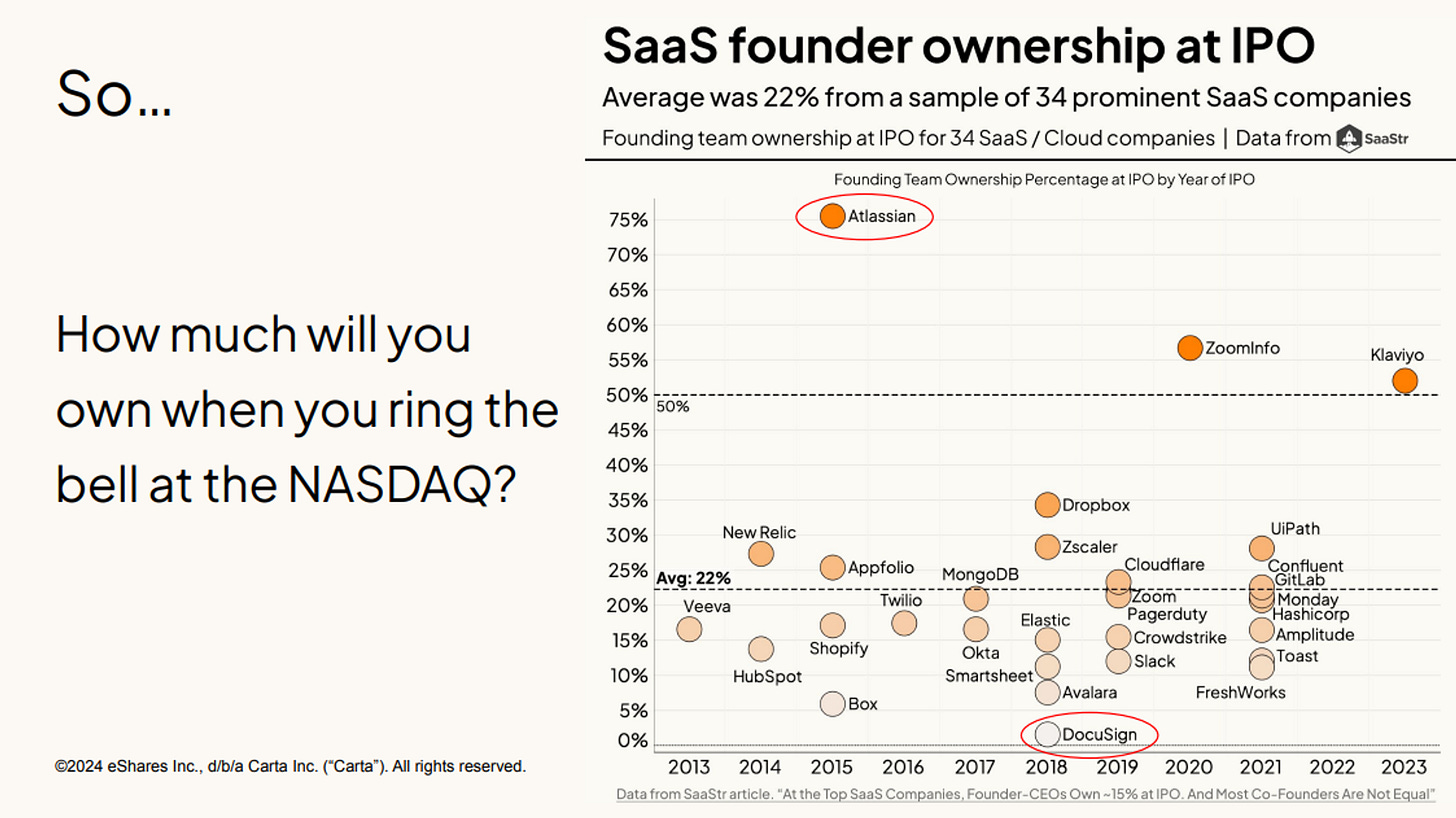

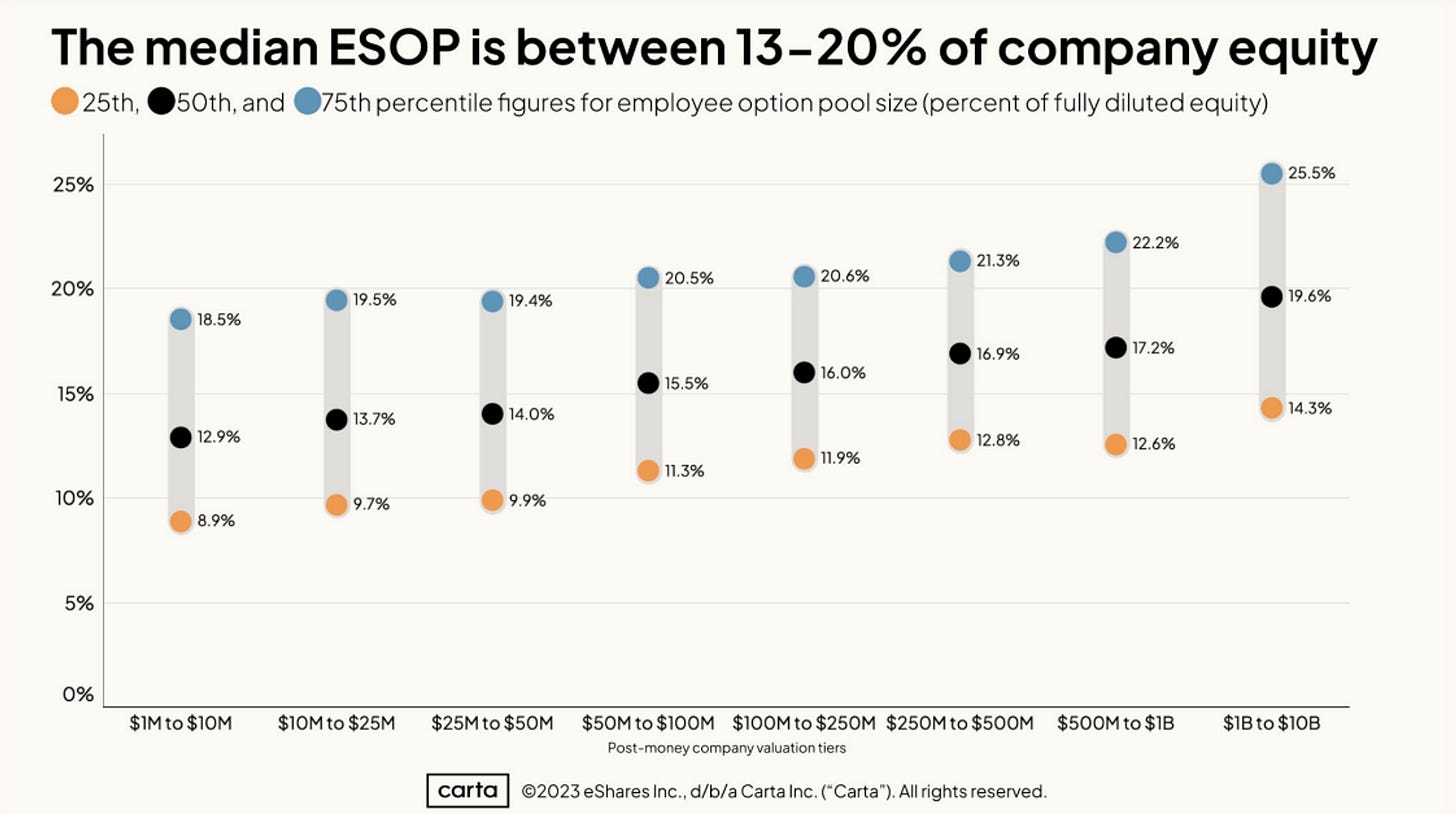

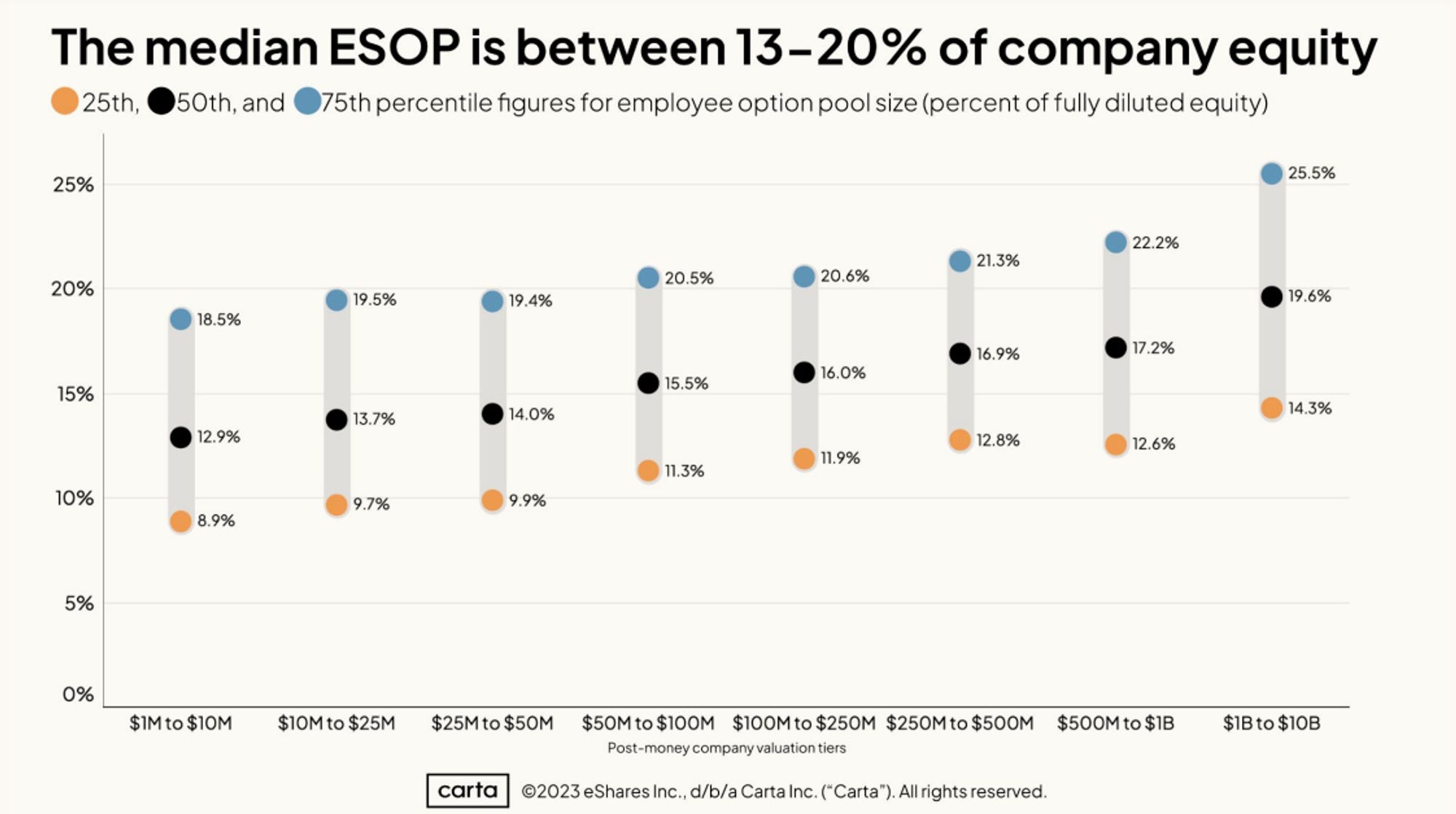

Wednesday, Jun. 19th: Carta shared a great deck on equity dilution in startups benchmarking equity split between founders, equity granted to employees, median dilution per priced round and median dilution per bridge round. - Carta

Monday, Jun. 17th: Mark Leonard at Constellation Software shared an insightful comment on vertical SaaS using Veeva as an example during its latest shareholder call. Mark Leonard argues that vertical SaaS should start by capturing market share with a low cost product before creating moats by adding product depth to better lock customers. - Mark Leonard

“The Silicon Valley crowd got very excited about vertical market software 7 or 8 years ago, and billions went into creating a venture- backed disruptors in the vertical market software space. A lot of those billions have been frittered away. But some of them have gotten traction, and those that have gotten traction are the ones that we tend to study.

Now where do we tend to get traction? It appears that if you can use a penetration pricing approach to entering the market, you can do pretty well with these businesses. And so what you need to compete on price is inherently low cost ideally. And a client base that is price sensitive, that cares about what they pay for IT systems that is willing to move based on price. And that generally means that they face fairly low switching costs.

Now one of the challenges, of course, is if you build up a high market share and a low switching cost business, that someone else is going to come along at some stage after you start to increase your prices to make some money and just steal the clients back from you. And so the challenge is to create a moat as you capture those clients.

And I talked -- I think it was a couple of years ago about Veeva, and they are a wonderful example of this, creating a moat after penetrating a market. They did a great job of capturing pharma, in particular, big pharma with a CRM system that was built on top of Salesforce, so relatively low cost to create. And then they have subsequently reduced their COGS on that by building out their own platform underneath the CRM system and adding to it a whole series of applications that sell into the same client base, building up the moat inside of their business. So that's a sort of prototypical approach to building a great disruptive vertical market software business. We see very few of these. But when we do, we revel in the learnings that we can garner from them.”

Tuesday, Jun. 18th: Voodoo acquired social app BeReal for €500m with 1/3 of the proceeds paid upfront in cash and shares while 2/3 of the proceeds are based on an earn out paid only if BeReal reaches certain business targets. - Eric Seufret, The Verge, Les Echos, FT, Techcrunch

BeReal was launched in 2020 by French entrepreneurs Alexis Barreyat and Kévin Perreau. It’s a social media app based on authenticity. BeReal reached over 40m active users, with significant popularity in the US, Japan, and France. It raised c.$115m from investors like DST, Accel, a16z and Newwave including a $85m series B at a $600m valuation.

BeReal users are notified once daily to take a snapshot using both the front and back cameras of their phone. They can unlock additional “posts” by uploading their images within an allotted two-minute time window immediately after the notification.

“Voodoo’s own social media app, Wizz, is growing faster than BeReal in the US: it sits at Top Downloaded rank #17 in the Social Networking category vs. 27 for BeReal. The CEO of Wizz, Voodoo’s social media app, will become the CEO of BeReal. My sense is that Voodoo may integrate the functionality of BeReal into Wizz at some point to accommodate BeReal’s core demographic and serve a larger TAM.”

“BeReal was something of a gimmick, and it may work better as a feature than a standalone app. If Voodoo can use BeReal’s core mechanic to grow Wizz into a scaled social media property, with strong retention and long-term engagement, it can pair its existing advertising infrastructure with Wizz to service ads not just in its social media footprint but against an audience network across its published titles.”

“It’s a big project for Voodoo. It’s the biggest acquisition we’ve ever made. We really believe we can create the next iconic social network focused on authenticity.” - Alexandre Yazdi (CEO at Voodoo)

“BeReal waited too long to focus on a business model and completely resisted advertising.”

“Since the deal was made public, I’ve heard speculation that Voodoo bought BeReal primarily to promote its other revenue-generating apps. Yazdi says that isn’t the case, however, and that he intends to run BeReal independently and focus on “product-led” growth. “We won’t use BeReal for generating traffic for games. Our only goal is to grow BeReal.” Voodoo plans to put ads in BeReal, which I’ve heard the cofounders were adamantly opposed to. There could be a subscription or in-app purchases added down the road.” Voodoo is on track to generate €700m in revenues in 2024 while being profitable.

BeReal's CEO and co-founder, Alexis Barreyat, will oversee the transition to new management before stepping down. He will be replaced by Aymeric Roffé who is the CEO of Wizz, one of Voodoo’s social media apps.

Wednesday, Jun. 19th: Carta shared a great deck on equity dilution in startups benchmarking equity split between founders, equity granted to employees, median dilution per priced round and median dilution per bridge round. - Carta

Thursday, Jun. 20th: US should increase its defense spending to counter growing threats from China and maintain its military superiority and ability to deter conflicts. - The Dispatch

“American military readiness is declining due to stagnant budgets, mismanagement, and escalating costs.”

“As a share of the economy, defense spending has been halved since the 1980s, falling from 6% to 3% of GDP.”

“The size of America’s Navy fleet has fallen from 600 to 285 ships over the past three decades while China’s shipbuilding surge is set to reach 440 naval ships within six years. China became the world’s leading shipbuilder by investing and building more efficiently than the U.S.”

“In the absence of significant new funding and with a need to build its industrial base, it is imperative that the Defense Department streamline procurement policies, become much more cost-efficient, pass an audit, limit the spiraling growth of compensation costs, and shed all non-essential, politically driven congressional mandates.”

While defense spending is already high, it remains a relatively small portion of the federal budget and economy compared to past major conflicts, and that sacrificing military readiness could have catastrophic consequences for U.S. national security.

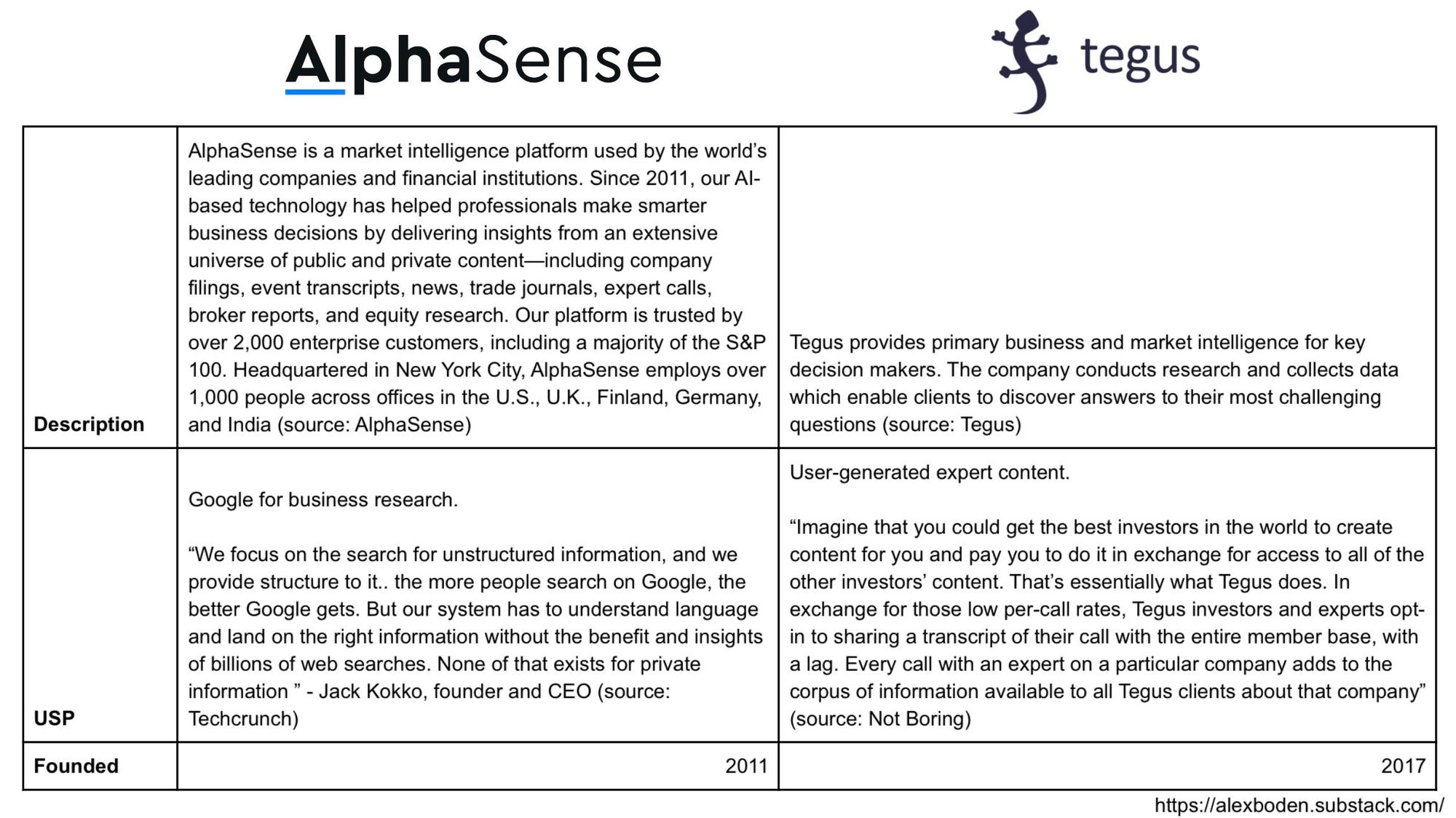

Friday, Jun. 21st: AlphaSense acquired Tegus for $930m strengthening its positioning as key leader in the private market intelligence sector. Tegus was valued at $3bn in its last fundraising round in Nov. 2021 an had raised $112m in total since its inception in 2016. Alphasense also raised $650m at a $4bn valuation. - Asymetric Advantage, Reuters

Saturday, Jun. 22nd: I listened to an Invest Like the Best’s podcast episode with Pat Grady who is a growth investor at Sequoia who invested in companies like Snowflake, Zoom, ServiceNow, Qualtrics, Okta, HubSpot, Notion, and OpenAI. - Invest Like the Best

“I have my personal long-term plans and then my personal annual OKRs, which cascade down into my quarterly OKRs, which cascade down into what I'm doing this week, this day, this minute. I suppose I put the pressure on myself by creating that structure.”

“I joined in 2007, when I was 24 years old. I was the youngest person we had ever hired, so I was going to experiment. I felt so lucky to be here. I put an enormous amount of pressure on myself to live up to the expectations that I had for what it meant to be part of Sequoia.”

“At Sequoia, the two things we care about most is performance and teamwork. Then each team operates in a slightly different context and the growth team has its own values which are: (i) aggressive but humble, (ii) demanding and supportive, (iii) I give a shit, zero bull and (iv) strong under scrutiny.”

“We think that being demanding of one another is being supportive. The best thing we can do for each other is to demand excellence, first of ourselves and then of each other.”

“The simpler you can keep things, the more straightforward you can be, the more transparent you can be, the more people are going to trust you and the more people trust you, the easier life becomes.”

“The way that I like to do that is to go for a long walk with founders and try to understand who they are in all the ways that don't show up on LinkedIn. What was their childhood like, what experience in their childhood most contributed to who they are today? What characteristic did they take from their mom? What characteristic did they take from their dad? Do they have brothers and sisters? How do they view themselves in relation to their brothers and sisters? What was the happiest moment from their childhood? What was the biggest mistake that they made in their childhood? All those questions that in and of themselves may not tell you much, but when you go deeper and deeper and deeper, you really start to understand who they are and what they value, and if you can understand that, you start to understand what drives them. Then you can start to map that on to the business they're trying to build and figure out if they're actually likely to build something for the long term or if this is more of a passing fancy and they want to play the game of entrepreneur versus actually building something that matters.”

“One of our core beliefs is that anybody can beat us on any given day. We believe that in part because our competitors are no joke. They are very smart people who know what they're doing, who work really hard, who have killer instincts, who have a nice way with founders at lots of other firms and any given one of them could beat us on any given day. When we're in a competitive situation, we can't just waltz in and hope that the Sequoia business card is going to give us the advantage. It is hand-to-hand combat, and we have to be on our absolute best if we have any hopes of making that investment.”

“I think the biggest mistake people make is selling by telling founders how awesome you are. Founders don't care how awesome you are. They want to know how awesome they have a chance to become. The thing we really want to do is understand who are you, what do you want to become and what is it you want to build. If we can understand those things and we can feed that back to you to show you that we understand those things and to show you that we are interested in those things, and we want to be a part of those things, then maybe some of the resources that we have here could help you in achieving those things but the main thing is not our resources [i.e. value added that we can provide with the Sequoia’s platform].”

“If you look at some of the all-time greats in our business, Doug Leone, Michael Moritz, Jim Goetz, one of their superpowers was really understanding human being. The common thing here is they basically have two superpowers. Number one, understanding human beings. Number two, having a sense for where the world is going.”

“The most powerful thing you can do, is to make a founder feel like they're seen, you understand them and try to validate their ambition through the way that you describe their business.”

“We are in a product-led growth business. Our product is the service that we provide to our founders. When our founders tell other founders what they think of us, that's ultimately the thing that gets them over the line. Our objective function is to maximize net multiple money returns for our limited partners, not to maximize founder NPS, but if we can have our cake and eat it too, that's the best of both worlds, and so founder NPS and net multiple money returns are the two metrics that we probably care most about.”

“Whoever ends up #1 in the market doesn't just have their proportional share of the market cap. They have a disproportionate share of the market cap. So investing in #2 or #3 in a market, maybe you can make a little bit of money, but you're not going to produce outsized returns for your limited partners. So it's really important for us to invest in the companies that we think are going to be #1 in the market.”

Sunday, Jun. 23rd: Mistral raised a €600m series B at a €5.8bn valuation in a round co-led by General Catalyst and DST. Other investors include Lighspeed, a16z, Eurazeo, Korelya, Hanwha, BPI, BNP, Nvidia, Salesforce, Samsung, ServiceNow and IBM. Mistral is competing directly with OpenAI building large general purpose models. Mistral has only 60 employees with 45 in France, 10 in the US and 5 in the UK with 3/4 of the team working in R&D. Mistral’s core differentiation to OpenAI is to have open-source multiple models which is key to get adoption from large enterprises which want to preserve their data privacy and companies which want to go deep into twisting models for their business. Mistral raised €1bn+ in funding but founders remain majority shareholders. - FT, Techcrunch, Sifted

Mistral also has released proprietary models including Mistral Large (its most advanced model consumable via API) or Codestral (a gen. AI model for code generation). The company also offers Le Chat which is a free to use chat assistant similar to ChatGPT.

Monday, Jun. 24th: Platform SaaS are exciting investment opportunity at the moment due to strong business fundamentals and potential AI integration, despite stagnant stock performance. Most software sectors are saturated post-COVID, leading to intense competition across all segments. Innovation has slowed to evolutionary improvements, with excessive duplication of products and inflated stock compensation. Strategic platforms integrating multiple products show promise with reasonable valuations. - X

“Platform SaaS is very interesting here - great businesses, great earnings potential, likely AI beneficiaries, attractive valuations, stocks that have moved sideways for years despite improved fundamentals. The other 80-90% of software names strike me as uninteresting / too difficult.”

“Most end-markets in software are now competitive and have multiple viable vendors. This includes all aspects of software for employees: marketing, sales, customer support, productivity / collaboration, communication, HR / payroll, etc. It also includes all aspects of software for engineers / operations: coding platforms / repositories, security (endpoint / servers / network), databases, monitoring, etc. It was most certainly not this way 10 years ago, nor even 5 years ago. But today, nearly everyone has competition in nearly all of their product lines.”

“Most new products from existing and new players are evolutionary, not revolutionary.”

“There is a lot of clean-up potential over the next 10 years. Growth is not over but it is mature and investment needs to slow down. There is no urgency to expand rapidly into a neighboring TAM which has a strong incumbent. Rather, rightsize the existing employee base and pursue consolidation where appropriate.”

“I think the protected and interesting businesses are the platforms which sell multiple, strategic products that hook customers and serve as distribution channels for incremental products. These platforms can be horizontal (Salesforce, Hubspot, Workday, Snowflake) or vertical (Autodesk, Adobe, Veeva, Procore).”

“I don't buy that "AI makes coding easy" will result in everyone building their own software and obviating the need for packaged SaaS. That doesn't pass the smell test. The whole point of buying versus building is it is better, faster and cheaper; and I think that value proposition persists. Especially because it is very tough to get AI to actually work. Will tech-forward companies like Klarna build their own? Sure, but I think that will be how the minority of companies approach it. Furthermore, companies should focus internal development on company-specific AI (e.g. Pfizer should work on AI for drug discovery / testing but just use Veeva or Salesforce for their sales people).”

“At least for now, it seems to me we are only seeing AI be a feature, not a product. So, for now, the incumbents are best positioned to layer in AI features and race to get to product stage over time.”

“Everyone is [crazy] over AI right now. Like I said, we still only have features (writing assistant, summarization, translation, etc.) from all the effort. If the investment in semis slow down and/or we go through a digestion period, the fundamental story for SaaS platforms will strengthen and the stocks ought to benefit.”

Tuesday, Jun. 25th: Benchmark is raising a $425m eleventh fund dedicated to investing in AI technologies. It will make c.30 early stage investments. Benchmark is maintaining the same fund size to preserve its investment discipline. - Forbes

“The new fund will be styled as ‘Benchmark 1’ as part of a reset for the generative AI era, the letter added. All of the firm’s partners are expected to look at AI companies within their typical areas of concentration such as consumer tech, cloud computing or crypto.”

“Its symbolic $425m size doesn’t include the considerable amount of capital the firm’s own partners pour into its funds, the person said. Factoring in those general partner commitments, Benchmark will have effectively more than $500m to deploy.”

“They were meant to be joined by investor Miles Grimshaw, who joined from Josh Kushner’s Thrive Capital in 2020. But in March, Grimshaw returned to Thrive, in large part because he wanted to invest more flexibly across stages and check sizes than was possible within Benchmark’s rigid portfolio structure.”

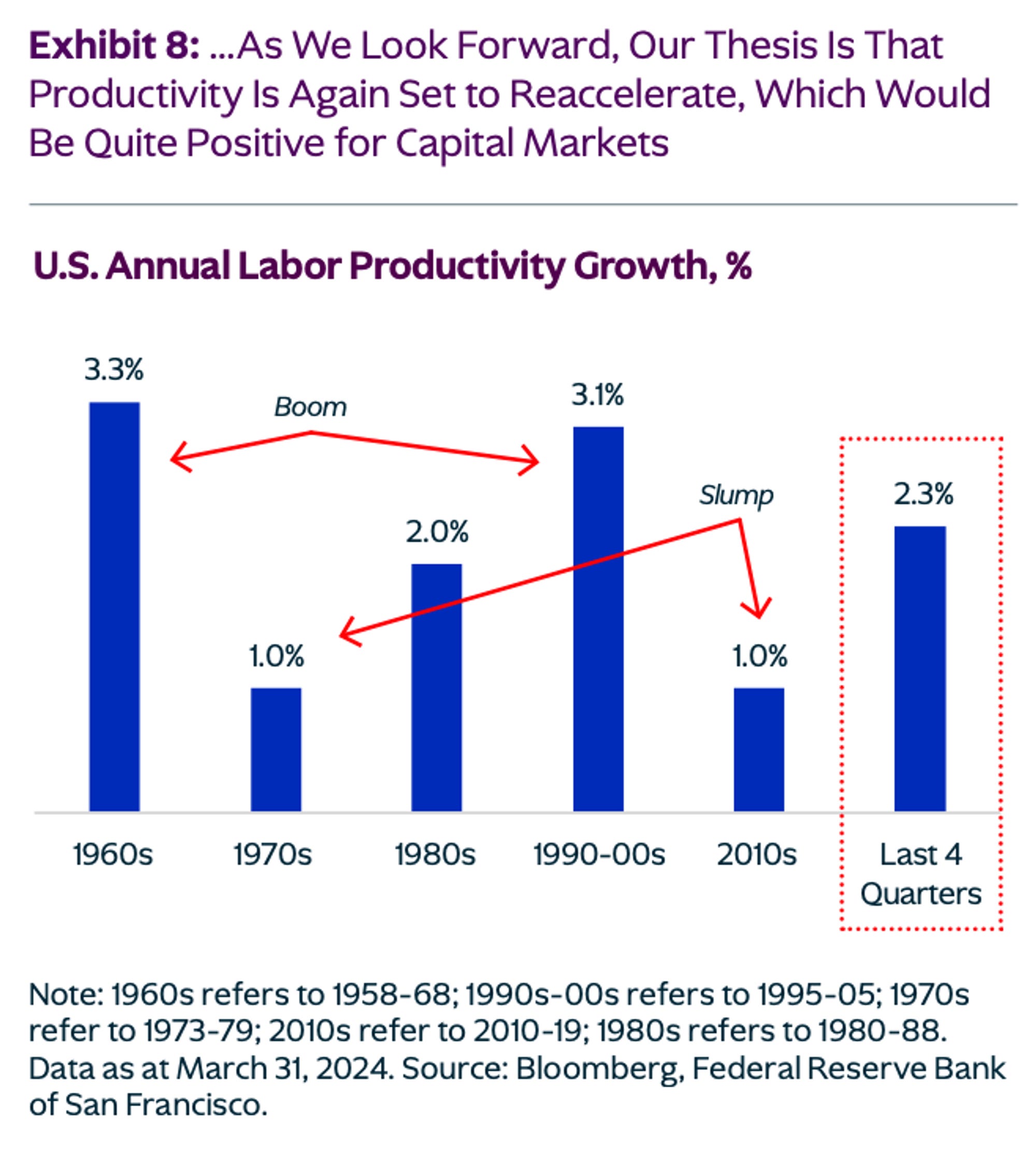

Wednesday, Jun. 26th: I read KKR’s mid year outlook written by Henry McVey who is CIO at KKR’s Balance Sheet. - KKR

“In terms of areas to lean in, we think that the current vintage will be a strong one for Private Equity, especially opportunities linked to value creation by operational improvement and/or corporate carve-outs.”

“Our view is that, similar to the Internet boom in the 1990s (and the corresponding period of solid economic growth leading up to 2000), the AI boom will drive a sustained period of higher capex before it is actually reflected in corporate profitability results. Implicit in what we are saying, though, is that the recent ongoing surge in productivity has actually occurred before AI benefits have been realized at scale, further underscoring our view that the corporate sector could enjoy a longer-tailed profitability renaissance. Importantly, though, unlike the dot-com bubble 20+ years ago, the companies financing this spending this cycle have bullet proof balance sheets, lower costs of capital, and a more consolidated market.”

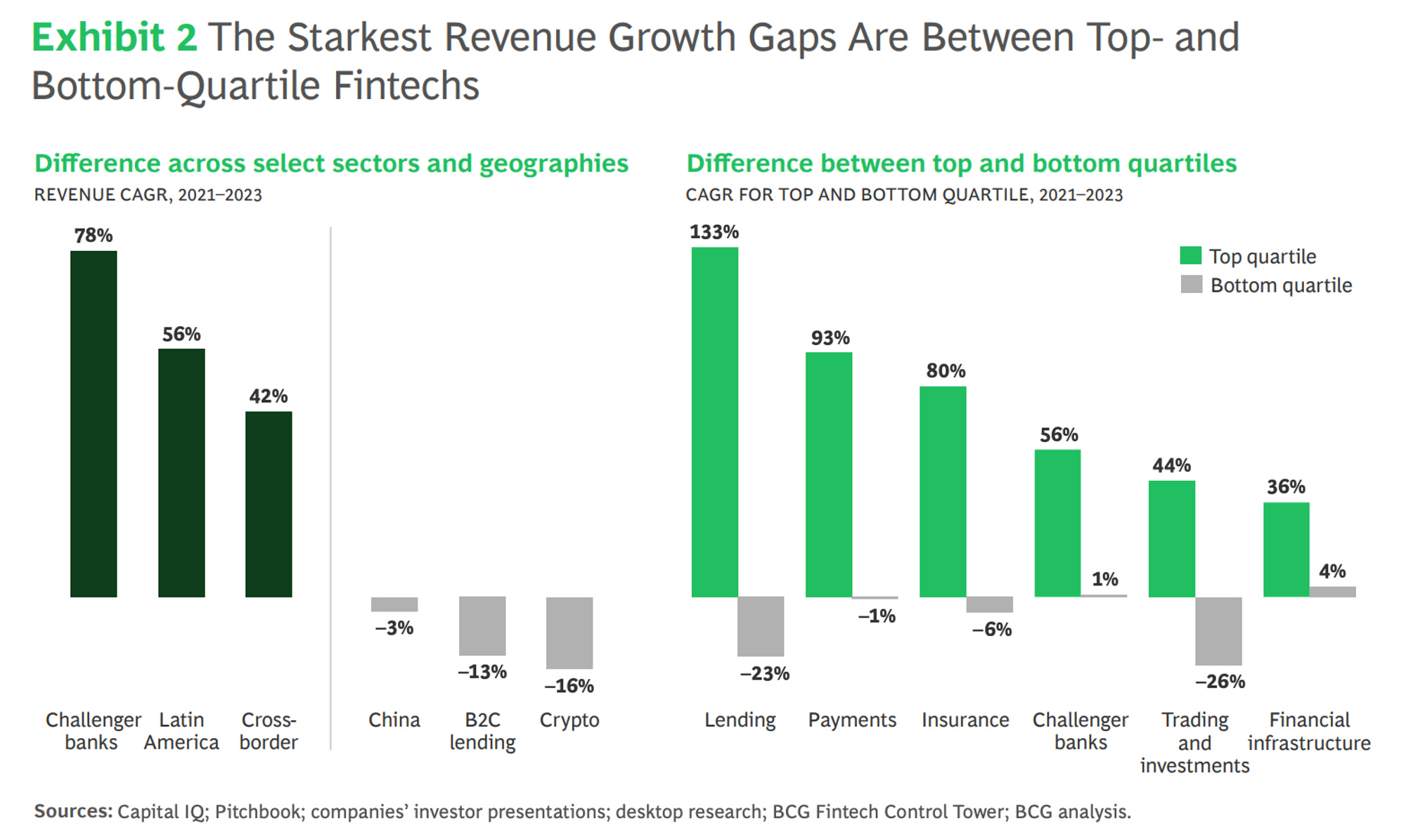

Thursday, Jun. 27th: QED and BCG co-published a report on financial technologies. - QED

“Globally, we are entering a prolonged period of higher interest rates that will continue to increase funding costs for fintechs, while private capital continues to push for profitable growth that will ultimately yield investment returns. The days of “growth at all costs,” funded by cheap capital, are well and truly over.”

“On the regulatory front, the past year has seen a narrowing of the regulatory advantage that fintechs have enjoyed since the birth of the sector. Regulatory actions have included consent orders against several fintech sponsor banks, increased scrutiny of banking as a service (BaaS) overall, moves against crypto firms, and the proposal from the US Consumer Financial Protection Bureau (CFPB) on the supervision of big tech companies and other providers of digital wallets and payment apps.”

“As real-time payments and GenAI become increasingly integral parts of consumer financial services, the risk of fraud ramps up. In the US, for example, incidence of data compromise increased by 78% in 2023, up to a record of 3,205 incidents broadly, according to the Identity Theft Resource Center.”

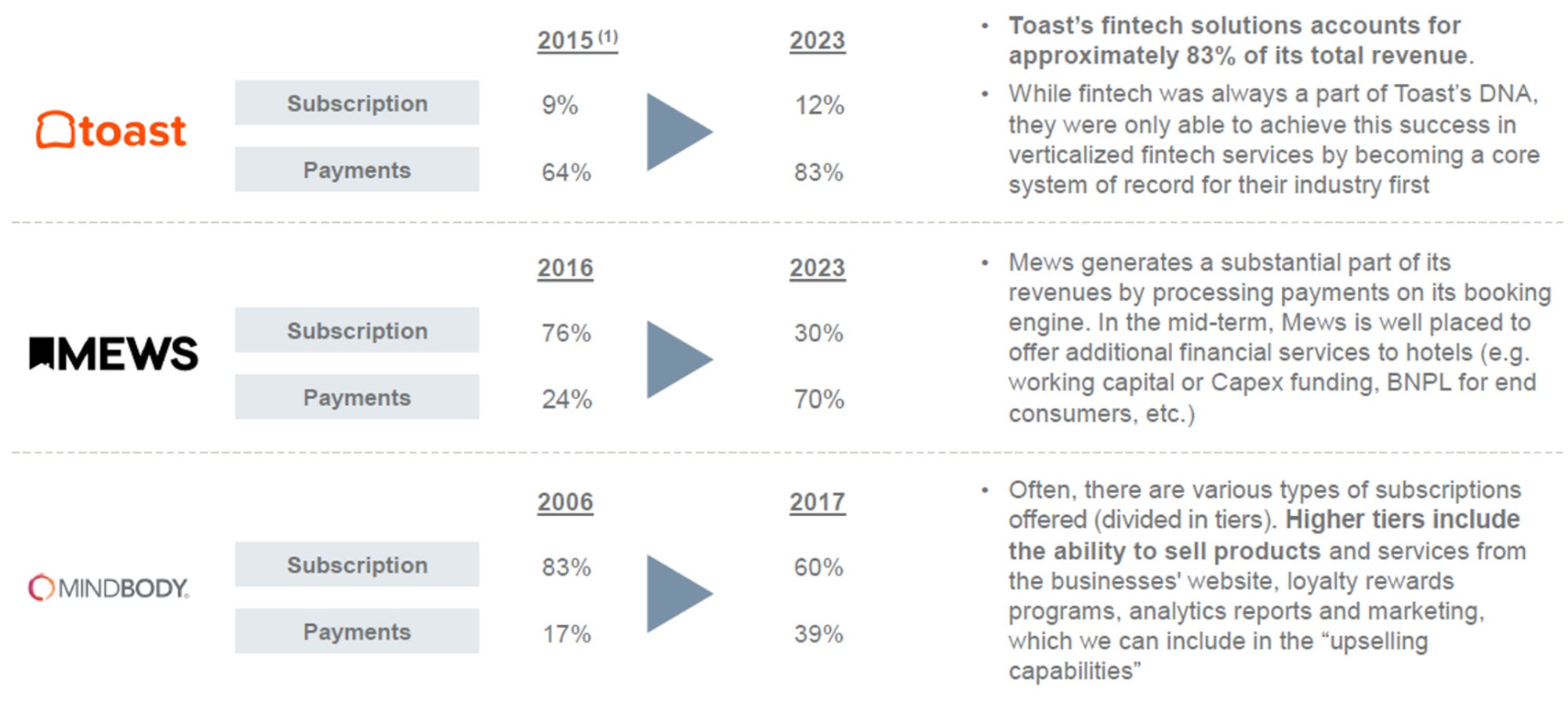

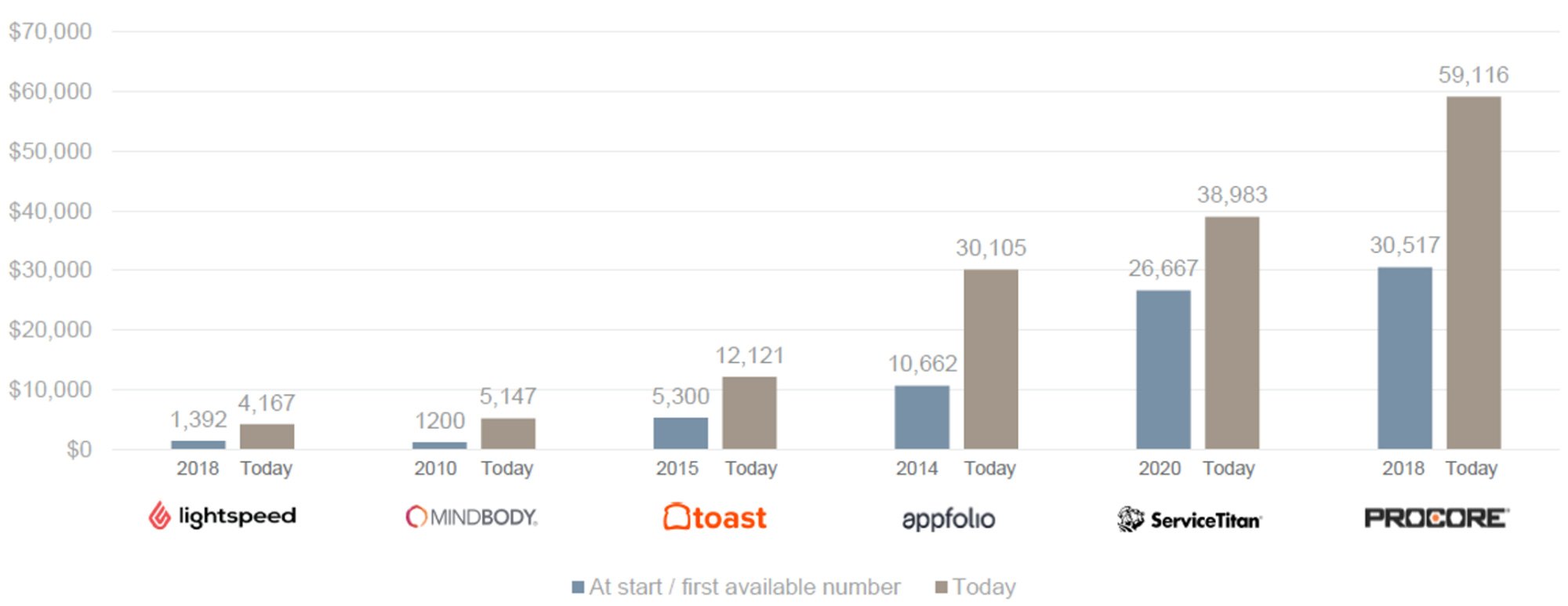

Friday, Jun. 28th: Virginia Bassano and Lucile Cornet from Eight Roads published a paper on vertical SaaS companies targeting small and medium businesses. - Eight Roads

There are 4 main drivers for the emergence of vertical SaaS: (i) generational change, (ii) the emergence of embedded finance, (iii) increasing market sophistication and post-Covid digitalisation shift and (iv) the AI revolution.

“For instance, Mindbody expanded its client base from 42k to 68k (+62%) in 6 years (2014-2022), with ACV doubling from $2.4k to $5.2k (+116%) through product diversification (initially started just as a scheduling tool, then added payments, marketing tools, lead management and others).”

“Most success stories in the SME vertical SaaS sector have managed to double or triple their ACV over the past 5-10 years. For example, Mindbody's ACV was $1.2k when the company started, and it has since increased by 320% to $5.1k. Top-performing companies also regularly reassess pricing, incorporating annual increases during renewals. For instance, Doctolib Patient started at €1.2k per year and now stands at €1.7k per year (3.5% CAGR).”

“Private Equity (PE) firms often find vertical SaaS companies particularly attractive because they can be platform plays for future roll-up strategies. Also, they tend to have a sticky product, high margins, and tend to achieve positive FCF faster than horizontal companies. PE firms will typically want to see at least $20M in ARR and profitability.”

Saturday, Jun. 29th: I read a post from Travis Cocke who is CIO at Voss Capital on being a value investor in software. - MOI Global

“I have a screen that immediately gets me interested in a software name: (i) FCF positive/neutral, (ii) annual Customer retention >90% and (iii) EV/SaaS Revenues < 3.0x (2.0x for companies with a market cap. lower than $1bn).”

“The incremental EBIT margin of high quality maintenance revenue is higher than 65%, generally (sometimes 85-90%) and thus attractive to an acquirer who could cut costs and fold the revenue into their existing support structure. It is very rare for a software company to get bought out for under 2x maintenance or SaaS revenues unless it’s hemorrhaging cash or has some other major problem (e.g. accounting or major customer concentration issues).”

“It is important for me to understand the long term historical churn of customers, the primary reasons for churn, and the steps/costs needed to maintain current churn. A company that does not explicitly report its retention numbers (both customer and dollar retention) or at least verbally give updates on a retention framework is generally crossed off my list. If the retention was great, they would probably report it.”

“Gross profit is a nice way to normalize companies that have a mix of software, hardware, and service revenues. Scanning the entire United States Technology landscape, the median EV/Gross Profit is about 6x, so when I look at this metric I look for any company below 3x as “interesting”.”

“The dream of any value oriented software investor is that ultimately fundamentals improve enough that growth and more neutral investors begin to pile in. This is a rare occurrence, but when it does happen it can result in incredible returns. The largest outsized returns occur when both revenue growth accelerates (sometimes from negative to positive) along with rising margins.”

Sunday, Jun. 30th: The Economist wrote about AI's transformative impact on the defense industry. - The Economist

“Today’s rapid change has several causes.

One is the crucible of war itself, most notably in Ukraine. Small, inexpensive chips routinely guide Russian and Ukrainian drones to their targets, scaling up a technology once confined to a superpower’s missiles.

A second is the recent exponential advance of AI, enabling astonishing feats of object recognition and higher-order problem solving.

A third is the rivalry between America and China, in which both see AI as the key to military superiority.”

“What is most visible about military AI is not what is most important. As our briefing explains, the technology is also revolutionising the command and control that military officers use to orchestrate wars.”

“AI systems, coupled with autonomous robots on land, sea and air, are likely to find and destroy targets at an unprecedented speed and on a vast scale.”

“AI-enabled tools and weapons are not just being deployed in exercises. They are also in use on a growing scale in places like Gaza and Ukraine.”

“A recent study by the rand Corporation, a think-tank, found that AI, by predicting when maintenance would be needed on a-10c warplanes, could save America’s air force $25m a month by avoiding breakdowns and overstocking of parts.”

“Both Russia and Ukraine have been rushing to develop software to make drones capable of navigating to and homing in on a target autonomously, even if jamming disrupts the link between pilot and drone. Both sides typically use small chips for this purpose, which can cost as little as $100.”

“It is a blurring of the line between intelligence, surveillance and reconnaissance (ISR) and command and control (C2)—between making sense of data and acting on it.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋