📖 Venture Chronicles - July 2023

Overlooked #152

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of July.

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

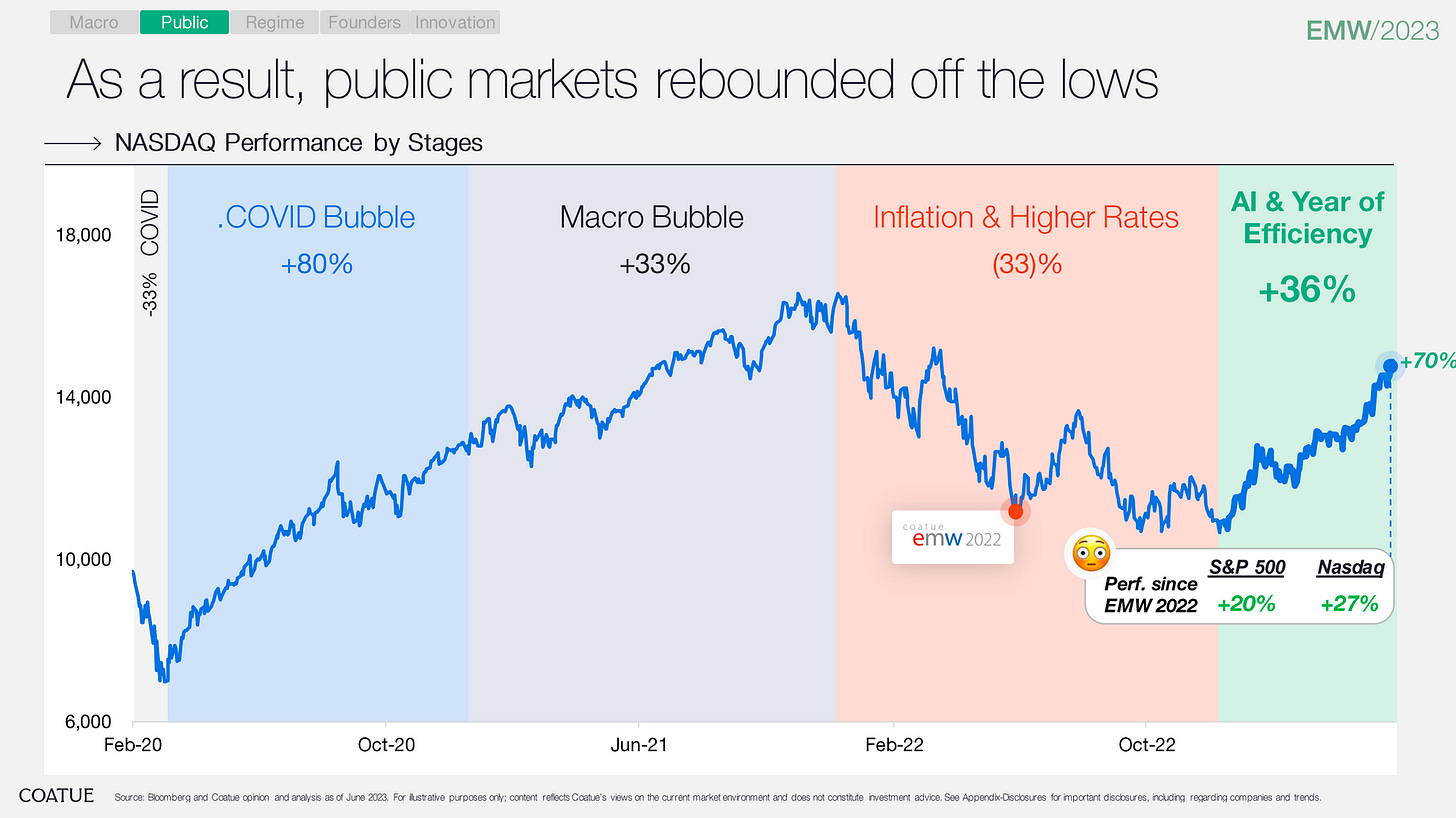

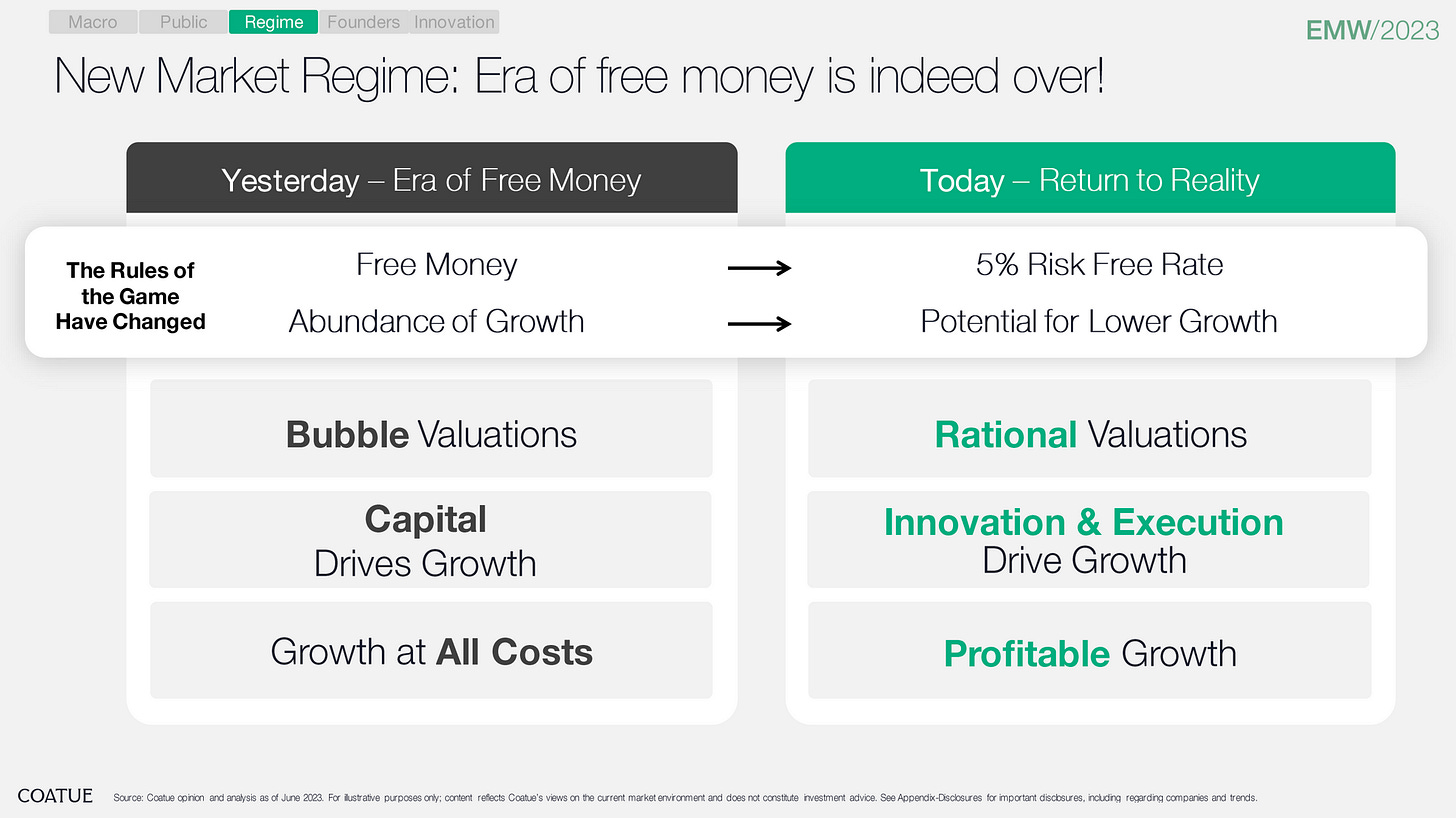

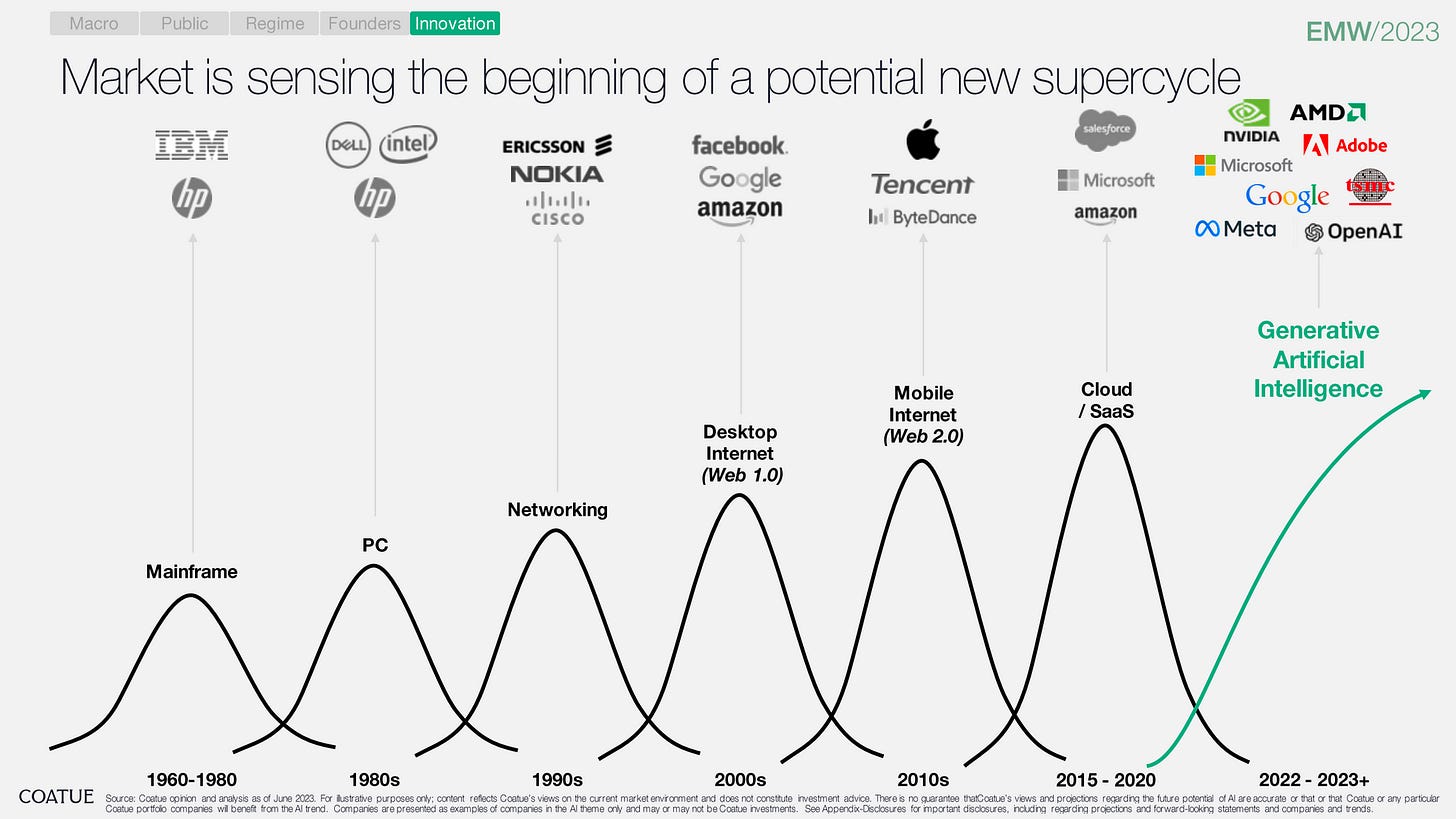

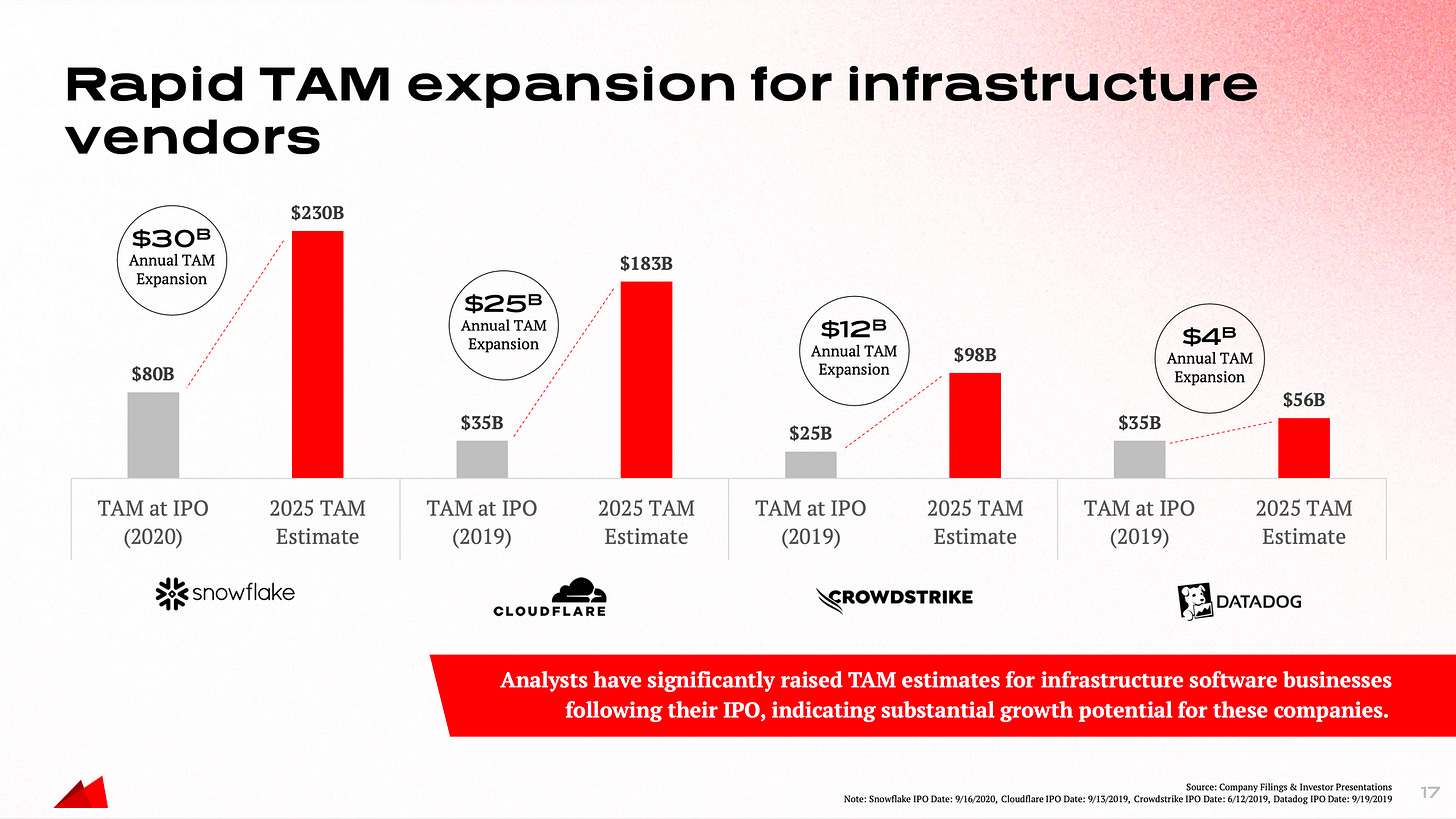

Saturday, Jul. 1st: Coatue published a presentation called “Coatue View on the State of the Markets” showcased during its annual conference called East Meets West. - Coatue

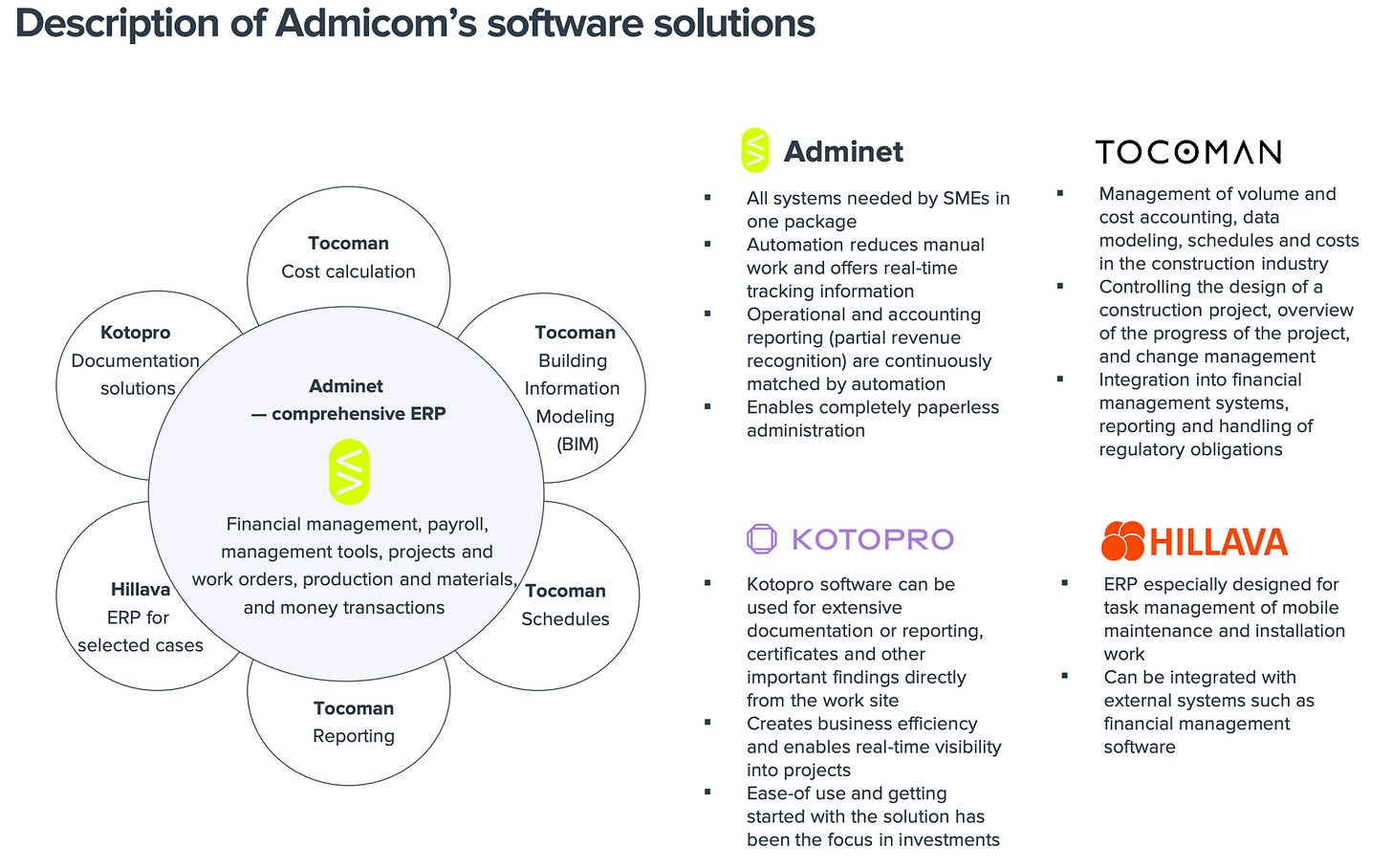

Sunday, Jul. 2nd: I read a broker note report from Inderes on Admicom which is a publicly listed vSol in the construction industry operating in Finland. - Admicom

In 2022, it generated €31.6m in sales with an EBIT margin close to 45%. It was founded in 2004 and wen public in 2018. It has 240 FTEs and 90% of revenues are recurring revenues. It took the company 6y of R&D to build a modern ERP (cloud-based) for technical building services before moving into construction in 2013 and industrial solutions in 2017.

“The cloud-based ERP system Adminet is Admicom's core product. The basic idea of Adminet is based on 1) SaaS software that enables scalability, up-todateness and location independence, 2) advanced automation of routine work, 3) a modular turnkey solution, and 4) real-time business data and reporting.”

It made several acquisitions in recent years: (i) Tocoman (2020) doing cost accounting, data modelling & scheduling, (ii) PlanMan (2022) doing schedule management, (iii) Hilava (2021) doing task management for mobile maintenance & installation work and (iv) Kotopro doing documentation and information management.

Monday, Jul. 3rd: Business Insider wrote about Fractal which is a startup studio building vSaaS businesses. - Business Insider

Since December 2020, Fractal has created 130+ vSaaS. c.10 startups managed to raise a seed round (e.g. Whoosh backed by Craft doing SaaS for golf operations, Aktos backed by 8VC doing debt collection, Barti backed Vertical Venture doing software for optometrists) with 50% of them backed by Bienville Capital which is Fractal’s venture arm and only 1 managed to raise a series A round (GreenSpark making software for scrap recyclers backed by Tiger).

Fractal has a major issue with its model. It does not give enough equity to founders making it impossible for portfolio companies to raise from traditional venture funds. Fractal’s ownership in certain startups can reach up to 47.5%. “Founders have criticized Fractal for taking so much equity off the table, arguing that it makes them radioactive in this market.”

In Jun. 2023, Fractal decided to stop building new companies and to refocus its efforts on supporting its portfolio.

“Fractal's mission was to create software for forgotten American businesses, from country clubs to scrapyards to funeral homes. The studio gave recruits $1m and an opportunity to start the next Procore or Toast. The biggest draw for some Fractal founders was its plug-and-play approach. The studio had a stockpile of vetted business ideas and would match people with a cofounder. It had dialed in processes to get a company started legally. And Fractal's own employees supported sales, product, and recruiting.”

Tuesday, Jul. 4th: Forbes wrote on Vanta which is a SaaS automating security compliance. - Forbes

It was founded by Christina Cacioppo. She is 36. She studied at Stanford. She worked in venture at USV. She built a first startup called Nebula Labs which failed. She moved to Dropbox and worked in product management on a new Dropbox product to compete with Google Docs called Dropbox Paper. She discovered the insight to create Vanta during her time at Dropbox when Dropbox customers could not start using Dropbox Paper before upgrading their security compliance standards.

Vanta has 5k customers. It raised over $200m including a $160m series B in June 2022 at a $1.6bn valuation. “Vanta has at least doubled its annual recurring revenue every year since its founding to an estimated $80 million.”

“Prior to Vanta, the way security and compliance was done was entirely with spreadsheets and screenshots of information that were collected in folders and shown to certified public accountants. What we built was a way to do almost all of that work, and do it automated.”

To maintain its lead over competition, Vanta has launched several initiatives: (i) build deep product/distribution/financial partnerships with software it works with, (ii) expand the number of supported standards, and (iii) expand to Europe.

Wednesday, Jul. 5th: GlossGenius raised a $28m series C at a $510m valuation led by L. Catterton with the participation of Bessemer and Imaginary Ventures. It’s a vSol for the beauty and wellness industry. It’s an all-in-one platform handling everything from booking to payments, client management, inventory, marketing and analytics. It charges a monthly SaaS fee between $24 and $48 per month and a 2.6% processing fee on payments. More than 50% of its revenues comes from payments. It has 50k customers and processes more than $2bn annually. - Techcrunch

Thursday, Jul. 6th: The Financial Times recently highlighted the noteworthy trend of companies which went public in recent years and which are now taken private by private equity funds. In Europe, take-privates accounted for c.80% of private equity transactions in 2023. It can happen in several circumstances: (i) companies failing massively in the public market after having been overvalued and after missing financial targets and (ii) companies reaching their business targets but which are not well valued by the public market. Several factors contribute to phenomenon: (i) public investors struggle to value companies which went public recently, (ii) public companies don’t have the right shareholder base, (iii) IPOs are priced too expensively don’t leaving enough money on the table for public investors. - FT

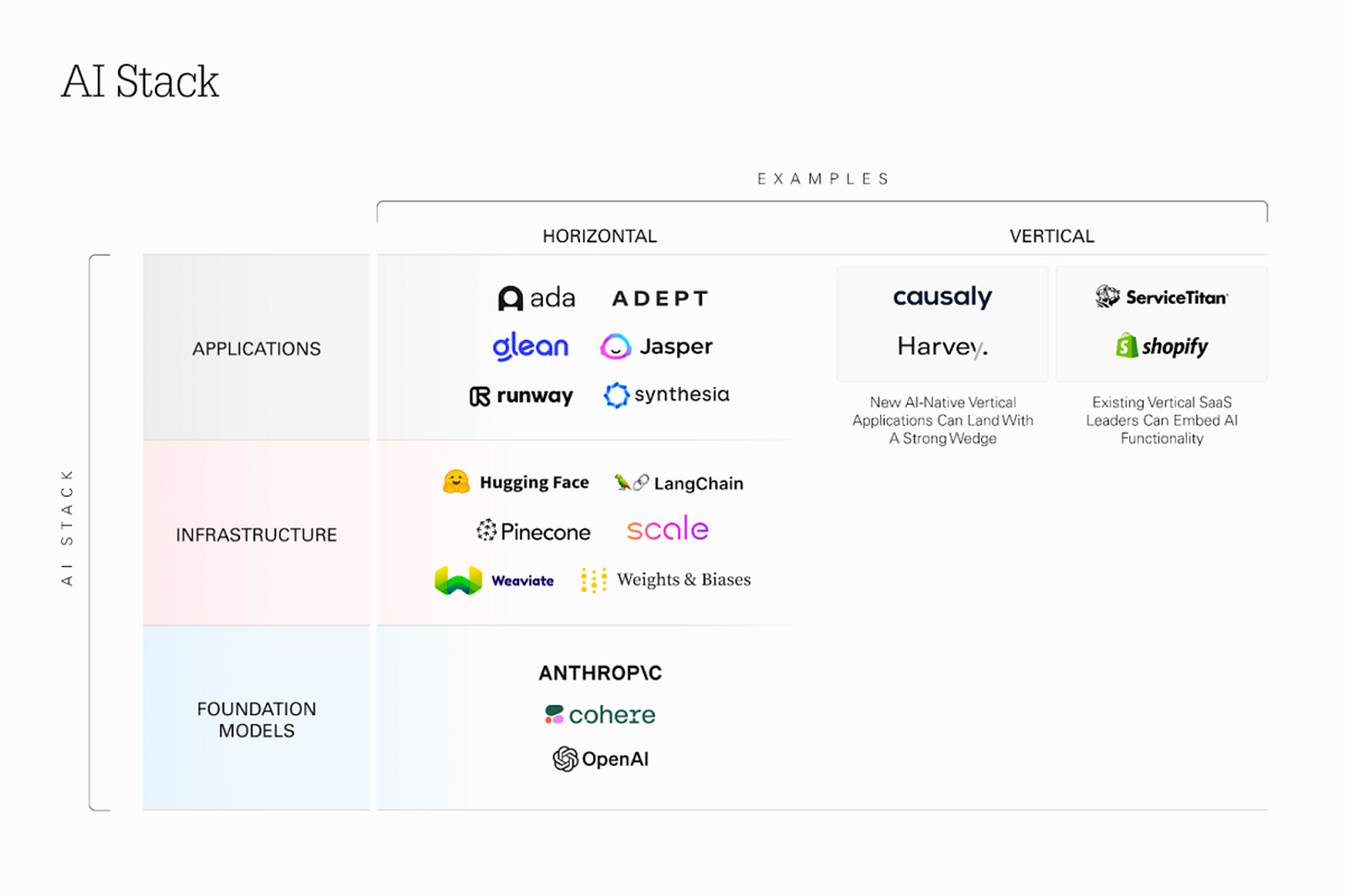

Friday, Jul. 7th: Paris Heymann at Index wrote about the impact of AI on vertical SaaS making the distinction between vertical AI-native companies (e.g. Causaly, Harvey) and existing vertical SaaS embedding AI features into their platform (e.g. Shopify, Service Titan). - Techcrunch

“Vertical AI winners will ultimately be those who can access proprietary industry data, effectively train large language models against those datasets, package those models via applications and ultimately deliver tremendous utility with fast time-to-value for customers.”

“AI can serve as a powerful wedge into a vertical market because it’s a new technology that buyers and users are receptive to and AI-powered features can deliver automation, which delivers value quickly. If you’re trying to sell a customer their tenth piece of software, there’s less urgency in the buying process. But with everybody clamoring to use AI, technology buyers are receptive to new pitches and experimentation right now.”

“Proprietary data and distribution will be a winning combination in the race to build both horizontal and vertical AI applications.”

Saturday, Jul. 8th: Frst is raising a third €100m fund. It announced a first closing at €72m. It raised from LPs including EIF, BPI, Axa Venture Partners and Isomer. It backs French companies at pre-seed and seed stages with tickets between €1m and €30m. Frst previously backed companies such as Pigment, Electra, Doctrine, PayFit, Shippeo and Owkin. - Techcrunch, Pierre Entremont

Sunday, Jul. 9th: Paul Graham wrote on what does it take to do great work. - Paul Graham

“The work you choose needs to have three qualities: it has to be something you have a natural aptitude for, that you have a deep interest in, and that offers scope to do great work.”

“It's good to know about multiple things; some of the biggest discoveries come from noticing connections between different fields.”

“What are you excessively curious about — curious to a degree that would bore most other people? That's what you're looking for.”

“Once you've found something you're excessively interested in, the next step is to learn enough about it to get you to one of the frontiers of knowledge. Knowledge expands fractally, and from a distance its edges look smooth, but once you learn enough to get close to one, they turn out to be full of gaps.”

“Four steps: choose a field, learn enough to get to the frontier, notice gaps, explore promising ones. This is how practically everyone who's done great work has done it, from painters to physicists.”

“A field should become increasingly interesting as you learn more about it. If it doesn't, it's probably not for you.”

“I think for most people who want to do great work, the right strategy is not to plan too much. At each stage do whatever seems most interesting and gives you the best options for the future. I call this approach "staying upwind.””

“That's the key: consistency. People who do great things don't get a lot done every day. They get something done, rather than nothing.”

Monday, Jul. 10th: I listened to a podcast interview on vSaaS with Dave Yuan who is the founder of Tidemark Capital and who invested in multiple vSaaS including Toast, Karbon and CCC. - Colossus

vSaaS are solutions specifically designed for a specific end-industry. They are control points which have (i) data gravity (system of records), (ii) workflow gravity (what you do every day to operate your business) and (iii) account gravity (system you turn off last if you were to go out of business).

A perfect industry for a vSaaS has (i) a large addressable market, (ii) a low competitive intensity and (iii) a high growth dynamic.

In a mature vertical, it’s harder to acquire market share (i) because it’s more a replacement play than an equipment play and (ii) vertical buyers are not natural software buyers tending to stick for a long time with a given solution. In a mature market, your role is to identify the 5% of vertical buyers who are reassessing their software solutions annually and secure a 75% success rate in winning these deals.

vSaaS should aim at capturing several pieces in the industry value chain. For instance, if you sell to the auto insurance, you should also sell to auto repair shops which have 70%+ of their revenues coming from insurance companies paying for insured consumers.

In horizontal SaaS, as your penetration deepens, it becomes harder to acquire the next customer because you have to step outside your ICP. In vertical SaaS, local network effects come into play, facilitating the acquisition of the next customer once a specific level of market penetration has been achieved.

vSaaS can either attempt to disrupt the established industry system of records, or they can integrate with legacy software while provide transformative surrounding features (e.g. in the hotel industry, building a PMS like Mews or building a channel manager like SiteMinder which integrates with the PMS and distribute the hotel inventory to all OTAs).

The most successful founders vSaaS founders possess industry expertise (personal tie with the industry, experience working in the industry, having credibility in the industry) and think multi-product from the outset (you need to start by building a control point but to build a massive business overtime, you need to become multi-product).

If you're a vSaaS disruptor in a very large and competitive TAM, you should be very aggressive and accept poor acquisition unit economics until you become the new category leader.

Tuesday, Jul. 11th: Andrew Rea wrote a paper arguing that founders should focus on solving unsexy problems in unsexy industries because everything easy to digitalise has been digitalised. - Andrew Rea

"Rather than pursuing high-status, cool ideas, more founders should start companies that solve unsexy problems and compete in unsexy industries.”

“LLMs bring new anxieties for builders. Many fear a world in which software becomes easier and faster to replicate than ever before, driving down the returns of software companies.”

If you’re starting a tech company today you want to be at one of two extremes: (i) building unsexy software, (ii) building frontier tech.” “On one end of the spectrum, you have software’s march into unsexy problems and industries. Examples would include vertical SaaS, logistics, financial services, healthcare, etc. On the other, you have the frontier of technology. Think areas like AI, quantum computing, biotech, etc.”

Wednesday, Jul. 12th: John Luttig at Founders Fund wrote an article challenging many pre-conceived ideas that we hear in tech about AI . - Pirate Wires

“Since the 1950s, AI has been a story of the boy who cried wolf — prophecies were over-promised and under-delivered.”

Pre-conceived idea n°1: foundation models have already plateaued. “Between new model capabilities and software products built around current LLM technology, we won’t look back on 2023 as a plateau.”

Pre-conceived idea n°2: open source models will dominate. “Open source will not be the dominant modality for frontier, productionized models.” “The current open source AI discussion has echoes of the early iPhone vs Android debate. Modular, open source approaches undoubtedly democratize technologies. But integrated products almost always capture the value.”

Pre-conceived idea n°3: only incumbents will win in AI. “There will be entirely new product form factors that won’t have the formula of incumbent software workflow + AI.” “To say that only incumbents will win is lazy thinking: it justifies a mopey attitude of doing nothing since the game is over.”

Pre-conceived idea n°4: there are many VC-investable AI opportunities. “If there aren’t many VC-investable opportunities, then VCs will have no economics in the most important platform shift of the last several decades.”

Thursday, Jul. 13th: The Washington Post wrote about Goodreads. - The Washington Post

Goodreads has been poorly managed since its acquisition by Amazon in 2013 for $150m. It’s built on an outdated tech infrastructure. Its UX and UI have not been updated for years. Additionally, there is not enough content moderation with review bombing campaigns being super common to trash an author or a book.

On Goodreads, you don’t need to have read a book to review it. Many authors release in advance book copies to readers and professional critics to generate pre-publication buzz. They expect to have good reviews on websites like Amazon and Goodreads. But what’s happening on Goodreads is that they can end up with multiple fake reviews from people who have never read the book.

Amazon acquired Goodreads for several reasons: (i) create a social reading experience in which Kindle’s readers could share their book highlights and comments within their community and (ii) provide reading data to book publishers.

Friday, Jul. 14th: Mo Golshan gathered all the publicly shared lessons from Keith Rabois who is a partner at Founders Fund. - Mo Golshan

“Identify an incredibly fragmented industry that is generally disliked by consumers, and disrupt it by vertically integrating, simplifying the process, and taking on the burden of achieving a high NPS score.”

“List 2-3 main risks or challenges of your startup, find a directly responsible individual (DRI) for solving and delivering each challenge.“

“The team you build is the company you build.” “Ultimately, you can get a lot of credit for the success of your company, but it really comes down to the people. If you have the right people, it is amazingly easy to succeed. If you have the wrong people, it's almost impossible.”

“To succeed, you need to assemble a critical density of talent and sustain it for a long period.”

“At Square, “Jack [Dorsey] and I realized pretty early that when we were getting to declines and offers, it was people who were going to found their own company. We put together a mentoring program where we said, "If you spend two years with us, we will teach you a whole bunch of stuff that will actually be useful when you start your own company."“

“Vertical integration is a better strategy because it allows creating the best user experience by controlling the whole experience and creating and capturing more value.”

“The earlier you invest, you need to be right only about the founder and everything will take care of itself.“

“Pick smart talented founders as they navigate you to successful interesting opportunities. You can embrace the idea later.”

Saturday, Jul. 15th: AngelSquare and Challenges published a ranking of the 30 most active angels in France in the past 18 months. - AngelSquare

It includes many top angels who have professionalised their activity via a fund or a family office like Pierre-Edouard Stérin (via Otium/Resonance), Xavier Niel (via Kima), Michaël Benabou (via Financière Saint James), Guillaume Houzé (via Motier), Bruno Rousset (via Evolem).

I also discovered top profiles I did not know they invested as angels like Andréa Bensaid (CEO at Eskimoz), Gary Anssens (CEO Alltricks) and Alexandre Fretti (CEO at Malt).

Sunday, Jul. 16th: I read an interesting thread on Hacker News discussing the lack of startups in the construction sector. - Hacker News

“The construction industry's fundamental constraint is that it manufactures products that are too big to fit in highway lanes. That means they can't be shipped from a centrally-located factory to their final destinations. So they need to be built at the site, which means they need to be built with more labor-intensive methods (since it's too expensive to build a capital-intensive factory for just one unit of output).”

“Construction projects always take far longer and cost far more than expected because of what's happening in the field, not because of what's happening in the office, so software simply isn't a bottleneck in this industry.”

“The problem is that nobody can align the incentives of the tradespeople and the office folks when it comes to integrating into an information system together. You have to cross multiple organizational boundaries between owner, builder, contractor, and subcontractor of which very few people have a bottom up understanding.”

Monday, Jul. 17th: Notion Capital raised its fifth fund. It’s a €300m fund (almost 2x the size of the fourth fund) to invest €3-10m tickets into 20 B2B SaaS series A all over Europe. Notion has also (i) a pre-seed program called Pioneers to invest €50k tickets into pre-seed/seed startups and (ii) an opportunity fund to double down into portfolio winners and invest into other growth stage startups. It raised from LPs including Cortes Capital, KfW Capital, TNO, British Patient Capital, Novo Holdings, Shelby County Tennessee Retirement System, the Medical University of South Carolina Foundation and RSJ. Notion invested into companies including CurrencyCloud, GoCardless, YuLife, Upvest, Mews, Cobee, Unbabel or TestGorillas. - Techcrunch, Sifted, Notion

“Our typical entry point remains Series A but we are flexible across the early-stage lifecycle as we recognise you can’t always perfectly time entry into the very best companies. The best deals are competitive, and you need to work hard to be in them. As such we like to engage as early as possible and nurture relationships over time.”

Tuesday, Jul. 18th: Skift compared Tripadvisor (via its Viator tours and activities brand) to GetYourGuide which are competing in the travel experience market. - Skift

GetYourGuide has 75k activities from 16k operators. 80m activities have been booked on the platform since its inception in 2009.

Tripadvisor has 300k activities on its platform (mix of 1st party and 3rd party activities). Viator generates $460m in annualised revenues. Tripadvisor acquired Viator in 2014. It promotes Viator’s activities on its platform bringing a massive and qualified audience to Viator. Tripadvisor is stronger in the US when GetYourGuide is stronger in Europe.

The tours and activities market ($235bn in 2023) is mostly an offline market with online players having a combined market share below 10%.

Wednesday, Jul. 19th: Dave Kellog and Michael Lavner who work at Balderton published a presentation showcasing the metrics that matter in 2023 for B2B SaaS companies. - Dave Kellog

Thursday, Jul. 20th: Julian Lehr wrote on the role of calendars in the productivity stack. - Julian Lehr

“Calendars, on the other hand, cover the entire spectrum of time. Past, present and future. They are the closest thing we have to a time machine. Calendars allow us to travel forward in time and see the future. More importantly, they allow us to change the future. Changing the future means dedicating time to things that matter. It means allocating our most precious resource to activities with the highest expected return on investment.”

“Treating todos as calendar events is helpful because calendars introduce constraints. A calendar forces you to estimate how long each task will take and then find empty space for it on a 24 hours × 7 days grid, which is already cluttered with other things.”

“I agree that tasks should live in your calendar, but that doesn’t mean every calendar event should be a task. The way I see it, tasks are just one of many different types of calendar events.”

“We tend to think of calendars as 2D grids with mutually exclusive blocks of time, but as this example shows, not all events automatically cancel each other out. Depending on their characteristics, they can be layered on top of each other.”

“Calendars should natively differentiate between different types of calendar events. Tasks, meetings, blocked time, and other activities should look and behave differently depending on their respective attributes. This would open the door for a virtually infinite amount of other use cases that could be integrated into the calendar experience in the form of unique calendar layers.”

Friday, Jul. 21st: BlaBlaCar doubled its revenues in 2022 to reach €197m in sales (vs. €100m in 2021, €80m in 2020 and €130m in 2019). It plans to grow its revenues by 30% in 2023. The company’s growth is driven by (i) international expansion (80% of BlaBlaCar’s riders are outside France), (ii) expansion into bus trips beyond carpooling, (iii) French government subsidies to push people to start carpooling, and (iv) expansion into short distance carpooling (home <> work). VNV is buying company’s shares into the secondary market to increase its ownership from 10.5% to 14.1%. - Les Echos, Sifted

“Its playbook calls for building a base of carpooling which creates an identity, community and trust. From there, the company can mix in bus bookings to expand that relationship. But the real goal is to cover every step of the journey, door to door, between cities. While rail lines serve major cities, getting to a family home in rural Brittany from Paris is more complicated if you don’t want to use your own car. BlaBlaCar wants to be the place where you can book the entire trip which may include a train, a bus and a carpool to that final destination.”

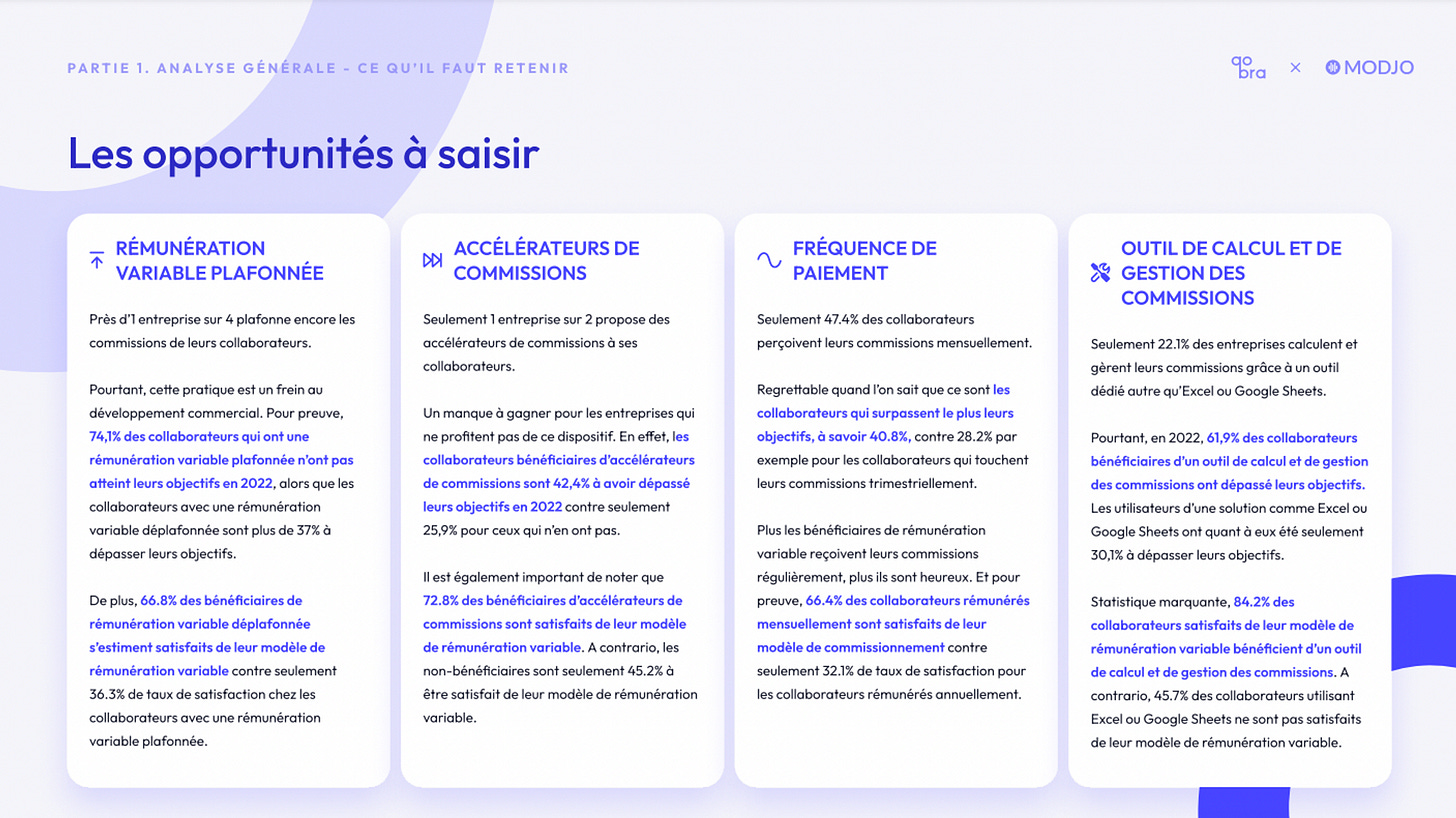

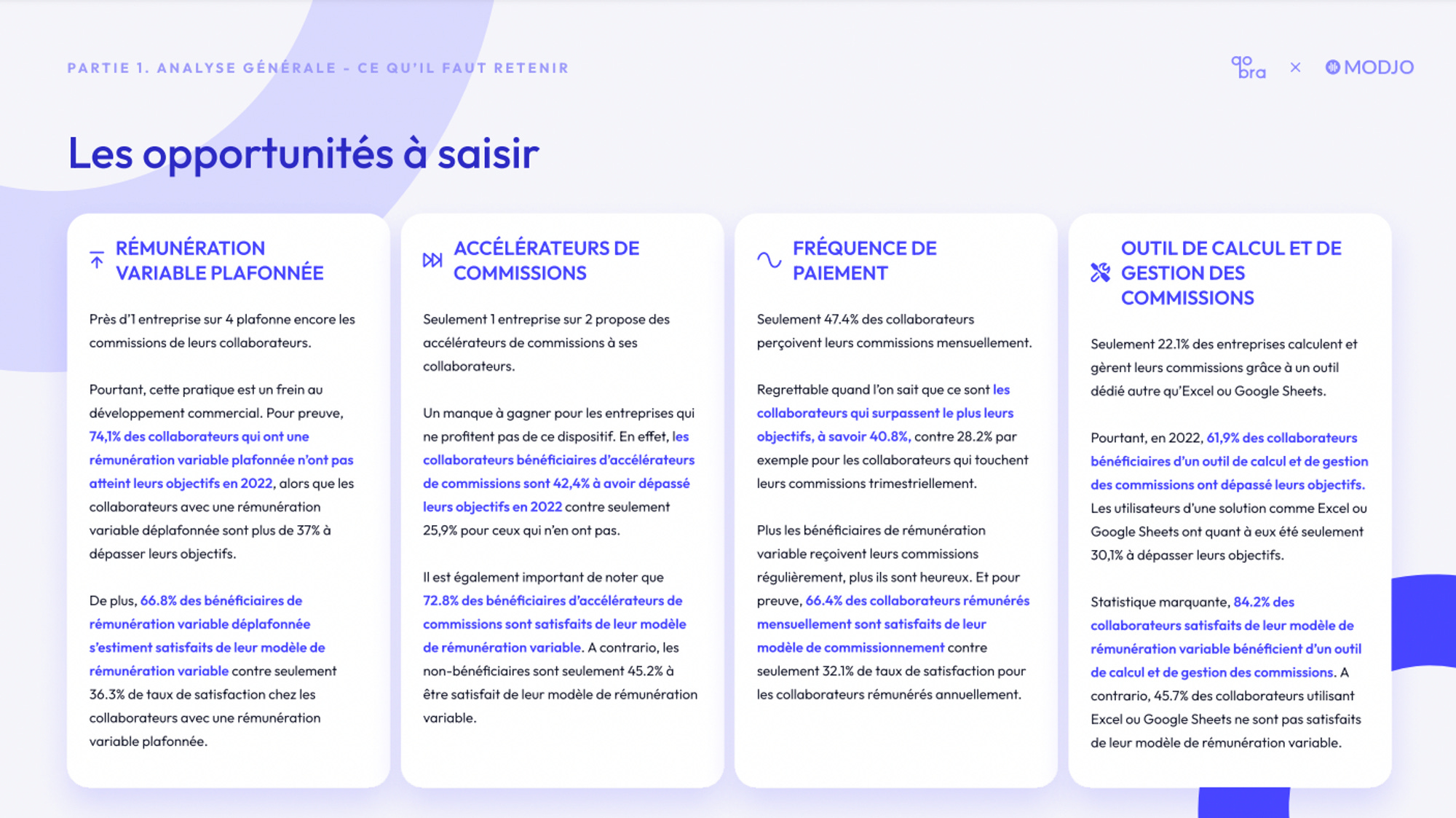

Saturday, Jul. 22nd: Qobra and Modjo published a study on variable sales compensation in France with benchmarks on salaries and advice to build a compensation plan for SDRs, AEs and CSMs. - Qobra (🇫🇷)

66% of sales reps did not reach their goals in 2022. 41% of salespeople are not satisfied by their current sales compensation plan. 47% of sales reps have their variable compensation paid every month and 37% every quarter. Only 22% of companies are using a dedicated software for sales compensation.

Sunday, Jul. 23rd: French unicorn Swile which is disrupting the meal voucher market in France and in Brazil published its annual results. After acquiring an old school meal voucher incumbent called Bimpli in 2022, Swile generated €138m in sales (inc. €37m from Swile implying a 236% YoY growth) and €72m in negative net results. It aims to be profitable in Q3-2023 and to generate €30m in EBITDA in 2024. Swile has 5.5m users (inc. 500k in Brazil) and 85k customers (vs. 60m users for Edenred and 7.6m users for Up). Swile also started to expand beyond the corporate benefits segment (meal vouchers, transportation benefits and gift cards) by launching Swile Travel which is a B2B travel booking solution and which is the result of the acquisition of a startup called Okarito. - Les Echos

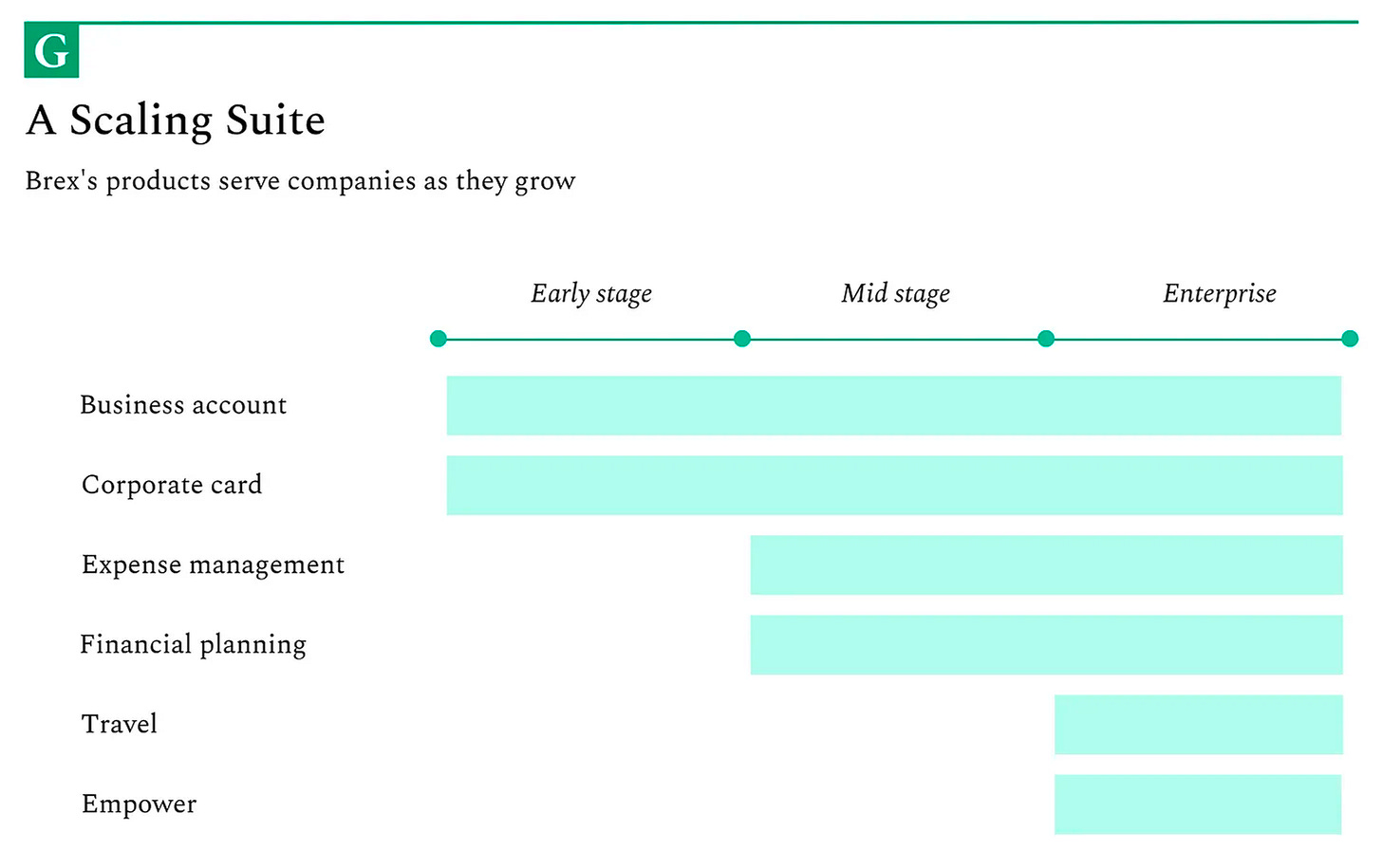

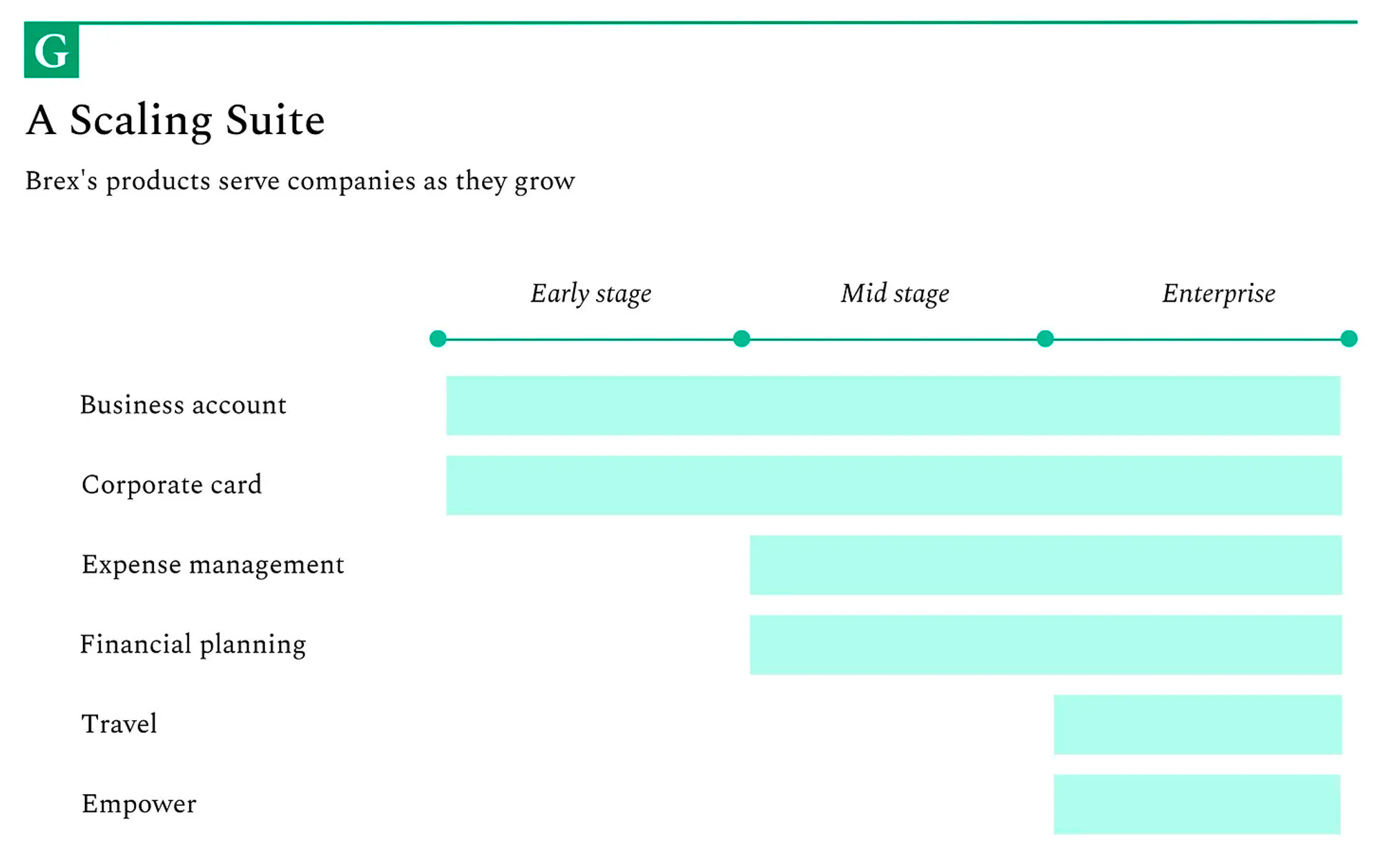

Monday, Jul. 24th: The Generalist wrote on Brex which is a US-based all-in-one financial platform competing head to head with Ramp. - The Generalist

In 2022, it grew its revenues by 200% and it will reach $500m in ARR in the next 12 months. 25% of US startups are Brex’s customers.

It moved from an expense management solution based on credit cards to an all-in-one financial platform including other modules such as bill payment, travel and business accounts.

“In watching their [YC] batchmates’ operational challenges, Franceschi and Dubugras found their opportunity. Despite receiving investment from YC, startups struggled to secure a corporate credit card.” It was hard to get a business credit cards for startups founders and when you have the chance to have one, you had an extremely low credit limit. “By underwriting companies based on their capital, Brex could safely increase credit limits 10-20x beyond those proffered by a traditional bank. Critically, the newcomer didn’t put founders on the hook from a liability perspective. It was, in short, a credit product built for startups like them.”

“In 2022, Brex released “Empower,” a software platform designed to help larger companies better manage their finances.” “From a business perspective, Empower essentially removes graduation risk; high-growth players like Retool don’t need to switch to SAP Concur or Coupa – they simply grow with Brex.”

“In just the week of SVB’s crash alone, Brex brought 4,000 new businesses and $2 billion in deposits aboard.”

Tuesday, Jul. 25th: I read several interesting papers on e-bikes startups VanMoof and Cowboy which both raised venture funding with high profile VCs. - Techcrunch on VanMoof, L’Echo on Cowboy, The Verge on VanMoof

VanMoof is bankrupt. It struggled to have good unit economics on its e-bike due to its full-stack production model as well as the management of repairs/returns. The Dutch court is exploring an asset sale to a third party to keep the company running.

Cowboy generated €41m in sales (2.7x YoY growth) in 2022 with 20k bikes sold during the year and lost €32m in net result. It increased its gross margin from 16% in 2022 to more than 40% in 2023. It raised €12.8m in 2023 (€6.4m in equity from VCs, €1.4m in equity from crowdfunding and €5m in debt from Triple Point). It laid off 20% of its workers in 2022. It aims to reach EBITDA profitability by Q3-2023. Cowboy is also facing a lawsuit with a tech supplier for patent infringement.

Wednesday, Jul. 26th: Colossus published a podcast episode on a US-based vSol for restaurants called Toast that I previously covered in the newsletter. - Colossus

Toast is a cloud-based and open Point of Sales (POS) system (vs. on-premise incumbents like Aloha or NCR) targeting independent and small chain restaurants across the US (vs. enterprise segment).

Toast developed custom software on the Android ecosystem (vs. just building on iOS and expecting customers to buy an iPad). It empowered Toast to have several POS offerings and an enhanced software versatility.

It was founded by three engineers named Steve Fredette, Aman Narang and Jonathan Grimm. They had previously collaborated at a successful company called Endeca which specialised in databases for retailers and was eventually acquired by Oracle for $1bn. Originally, their intention was to develop a mobile ordering app for restaurants. Despite considering building a POS, they dismissed the idea due to its perceived complexity. When they introduced their mobile app to the market, they encountered challenges in gaining commercial traction. This was due to the product's early introduction (at a time when mobile-app based solutions for restaurants were premature) and its lack of integration with established POS systems.

Upon revisiting the POS concept, they quickly found product market fit. Initially, they were turned down by investors (e.g. restaurants are low margin businesses, restaurants are too solicited by software vendors, restaurants are not tech savvy). Ultimately, Steve Papa, who was the CEO and cofounder of Endeca, decided to personally fund the business for a couple of years.

At inception, Toast's primary value proposition to restaurants was centered on delivering an intuitive and user-friendly POS. It contrasted with the challenging usability of on-premise incumbents' solutions. Today, the value proposition revolves more around the comprehensive all-in-one platform tailored to meet the specific needs of restaurants.

The POS is the core system used used by all stakeholders in a restaurant: (i) the waiters when they take orders, (ii) the chefs when they prepare the food, (iii) the restaurant manager when he oversees the operations, (iv) the end customers when they pay the bill.

On average, a restaurant using Toast generates $100k per month. It contrasts with 60% of Square’s merchants which process less than $125k per year. Toast charges a SaaS fee ranging from free to $170 per month and per location. Additionally, restaurants need to purchase a hardware terminal for transaction processing, which is a one-time cost ranging between $100 and $1k and Toast has a 2.6% take rate on transactions (with a 0.5% net margin for Toast, $2.6k monthly cost per restaurant).

“One thing that really helped Toast grow in the beginning was a commitment to customer success and onboarding.” “For a very low price, Toast would do a deep installation and migration work for their customers.”

When establishing a marketplace featuring third-party apps (e.g. Shopify, Toast, Procore), there is a tension between internal development of features to expand the product’s scope and creating ample room for partners to thrive with their own successful apps (without scaring them with the copy-risk).

Toast faces several challenges going forward: (i) expanding internationally (with the challenge that you’ll have lower payment fees in Europe), (ii) going upmarket (Toast has 85k customers out of 860k restaurants in the US but there are only 160k independent restaurants - remaining restaurants belong to chains which are harder to address for Toast) and (iii) upselling new products to its existing customer base.

Thursday, Jul. 27th: Robin Dechant wrote on how AI will help the field services industry to face its current skill shortage. - Robin Dechant

“To combat the climate crisis in Europe, we are in the process of completely rebuilding our infrastructure. This means, we are installing solar panels, heat pumps, energy storage systems, EV charging stations, sustainable housing units, carbon removal solutions and much more.”

“Due to the lack of skilled field workers in the renewable energy industry, we see a market shift towards a more specialized value chain. The specialization of roles does not solve the labor shortage but it allows greater efficiency, hence a greater number of installations.”

“To get to maximum efficiency in field services, knowledge needs to be embedded in the processes and software as this leaves no room for mistakes even for inexperienced field workers.”

“The basis to enable automation and AI application is the underlying data. Even today, field service companies often work in different siloed systems (think CRM, ERP, field service software, custom built solutions). A scattered data landscape makes it impossible to automate processes or enable AI applications.”

Friday, Jul. 28th: Redpoint published a report on the cloud infrastructure (dev. tools, cyber, data, AI). - Redpoint

Saturday, Jul. 29th: Tractable raised a $65m series E led by Softbank with the participation of Insight and Georgian. It’s a vertical SaaS in the insurance industry. It uses computer vision to automate the insurance claims and damage assessment process, particularly for home and car insurance. Tractable manages $7bn in claims on an annual basis and works with insurance companies like Aviva, Geico and Admiral. - Techcrunch, PR Newswire

Sunday, Jul. 30th: Terminal secured $17m in seed funding from 8VC and Prologis. It’s a vertical SaaS for yards. It builds a Yard Management System (YMS). In the US, there exists 140k manufacturing plants or distribution warehouse yards. 92% of them are not powered by technology. Terminal will start by using computer vision to index and analyse information in the yard in order to address various business needs (process improvement, capacity visibility, detention, etc.). - 8VC, BusinessWire

Monday, Jul. 31st: Shopify is further expanding into financial services by launching a business credit card for its merchants on top of Stripe and Celtic Bank. Shopify offers a cash-back ranging between 1 and 3%. Moreover, it does not charge any fee (e.g. FX fees or late fees). Shopify is already leveraging Stripe for its payment solution and for Balance which is a money management account. Shopify has also a fintech service called Capital which grants merchants access to working capital. - Techcrunch

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋