📖 Venture Chronicles - Apr. 2024

Overlooked #175

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of April.

Monday, Apr. 1st: I listened to a podcast on stock-based compensation with Bob Mylod who used to be CFO at Booking. - BG2

Equity participation has always been part of the VC model, creating alignment between employees, founders, and investors.

In the late 90s, we experienced the dot-com boom and bust. Before that, the main vehicle used to incentivize employees was stock options, priced at the current market value of the company. When most companies crashed in the public market, people began to argue that options created too much risk, with repricing and backdating occurring to ensure that employees remained incentivized. At the same time, concerns arose (especially at Microsoft) about the dilution caused by stock options. This created an opportunity to switch from stock options to Restricted Stock Units (RSUs), which incentivized employees with a model that could reduce dilution by a factor of three (from approximately 3% annually to about 1% annually).

The issue with stock options was that they were hard to communicate to employees as having value (based on the Black-Scholes model). For an employee, an option is worth something only if the stock goes up. RSUs work differently because employees see them as having a cash value that is accessible when the shares are vested, and as something that is never worthless.

With RSUs, you can create misalignment between investors and management. For instance, if management leads a company to a 20% decline over 1-2 years, they will still be able to receive 80% of their equity award, while investors will see their shares decrease by 20%.

“You shifted from stock options which as a shareholder I like because nobody makes money unless I make money to RSUs where people made money even if I lost.” RSUs used to be accounted as a cash expense in the P&L but companies started to adjust their P&L removing RSUs from the EBITDA calculation.

“When you proforma something out, when you stop treating it like cash, it leads to a misallocation of resources because you're effectively saying this doesn't exist. When you know what what happens when the cost of something disappears you get a lot more of it.”

“At Booking, we adopted the practice of not performing out the cost of stock-based compensation because it's a very real cost.”

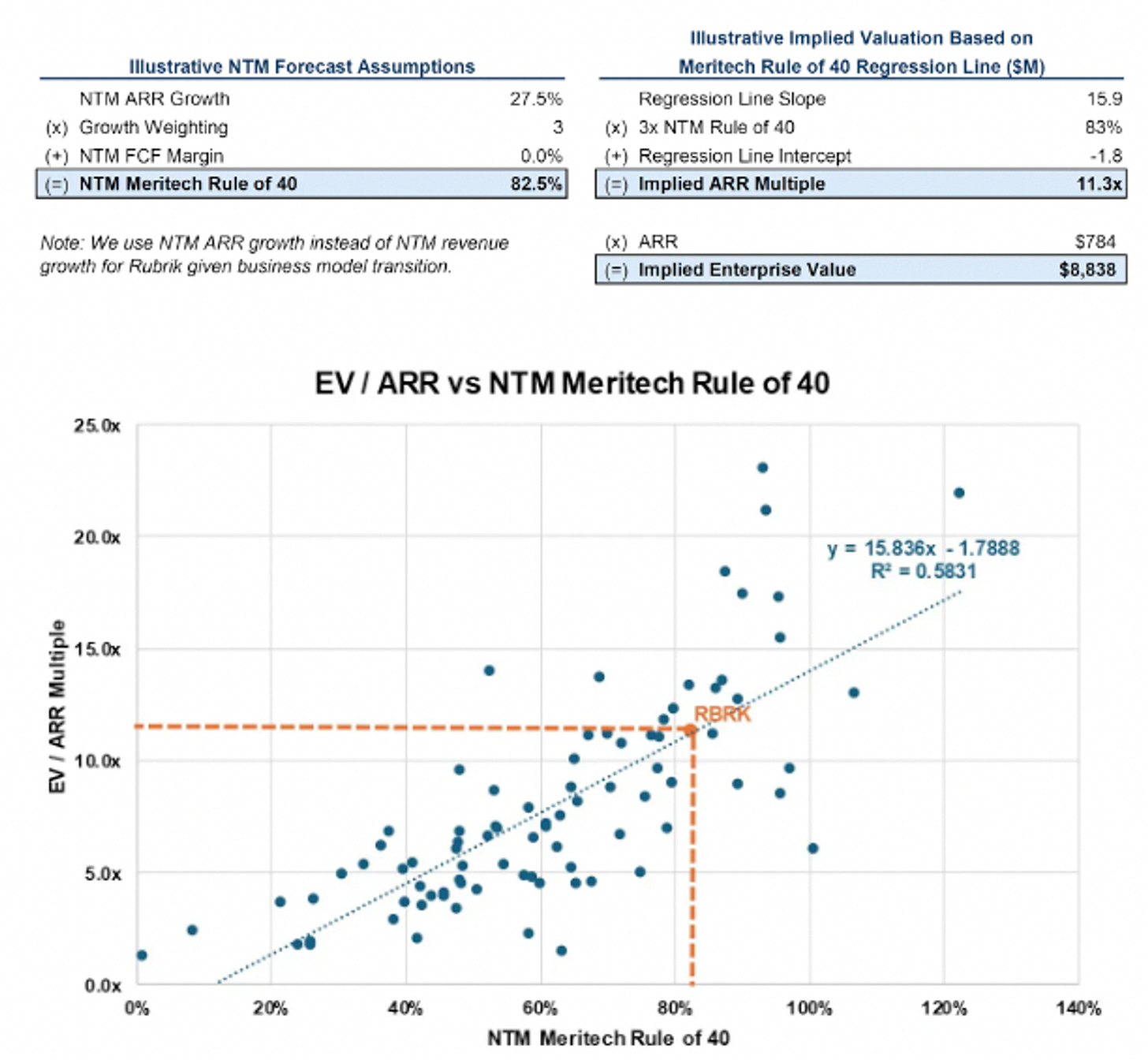

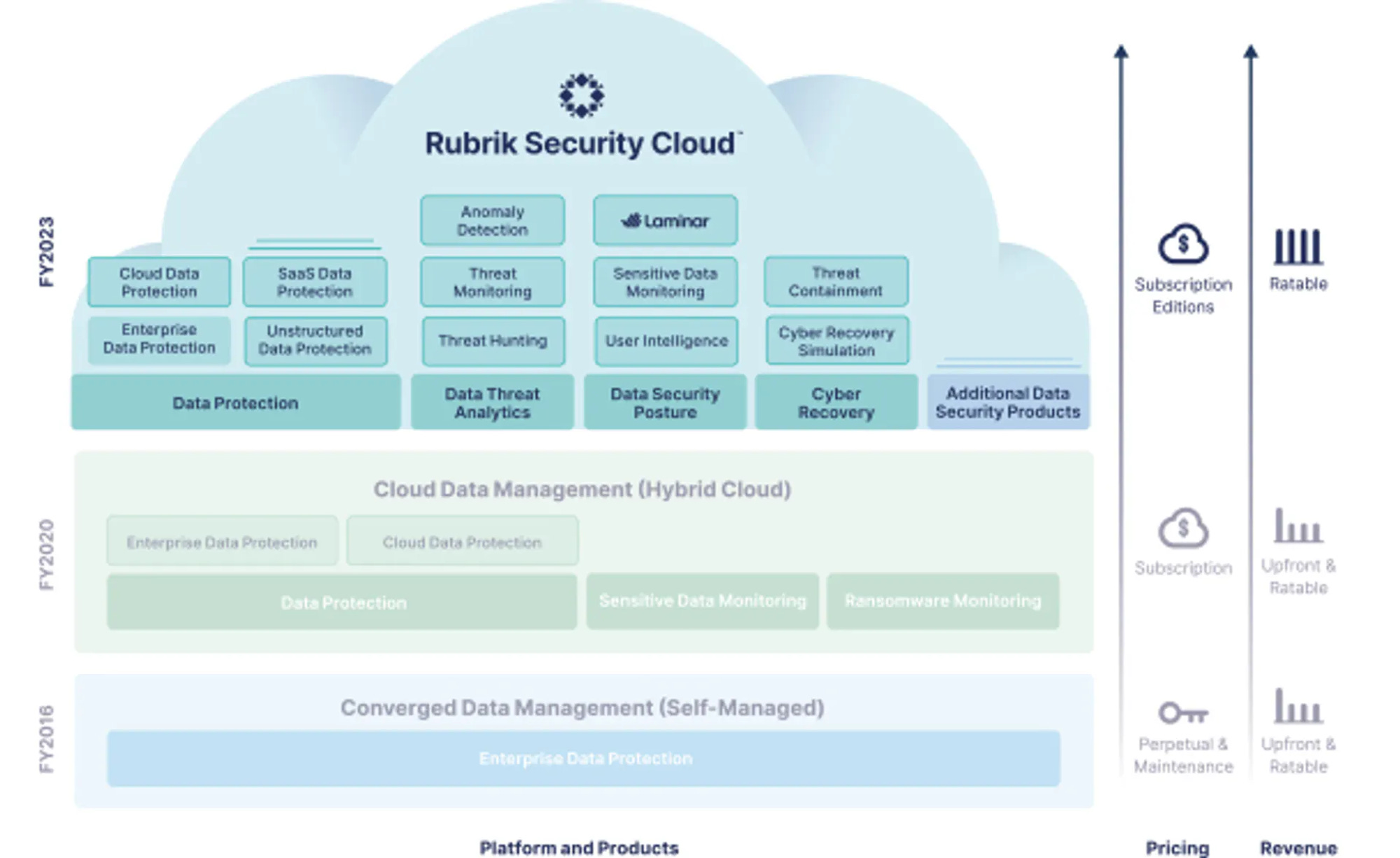

Tuesday, Apr. 2nd: Rubrik published its S1. It’s a leader in data management and security software founded in 2013. - Meritech, S1, Tom Tunguz

“The company was founded in December of 2013 (firstly under the name ScaleData which was changed to Rubrik in 2014) and began selling in 2016. It only offered its RSC, or Rubrik Security Cloud, as a cloud-native platform in FY 2023 (the year ending January 31st, 2023).”

“They sell subscriptions on 4 different types of data: private cloud or enterprise, enterprise NAS or network-attached storage, cloud, and SaaS applications.”

“Unlike traditional backup and recovery solutions, Rubrik’s focus on security (with a Zero Trust architecture) gives them an advantage in the market. An impressive feat is that Rubrik started as an on premise backup and recovery company and, in only a few years, transitioned its business model to a cloud-based data security platform. Rarely do we see businesses that go through successful business model transitions in such a short period of time.“

“Rubrik has large scale at $784M of Subscription ARR (annual recurring revenue), growing 47% year-over-year in FY 2024. The company has 6,100+ customers and 130%+ average subscription dollar-based net revenue retention.” It has 99 customers with $1m+ ARR and 1.7k customers with $100k ARR.

Rubrik latest funding round was a $374m series A led by MS&AD Ventures in Apr. 2021 at a $4bn post money valuation.

“The model is land-and-expand, much like many companies that sell to larger enterprises, and the land happens in 4 ways by securing: 1) enterprise or private cloud environments 2) enterprise NAS or unstructured data 3) cloud environments 4) and SaaS applications. The expansion motion happens across 3 vectors and includes: 1) growth of data in applications 2) new applications secured, and 3) additional data security products.”

“Rubrik has $279M in cash and has raised $715.1M of equity (according to liquidation preference disclosure in S-1) and $287M of debt, implying they have burned through a little over $700M to get to almost $800M of implied ARR, a ratio of ~1.1x, which is impressive for their product, enterprise segment and business model transition.”

“Rubrik is a top 10 growth software company with higher-than-average gross margins, lower-than-average profitability, on-par cash-flow-from-ops margins, & negative contribution margins. Contribution margin is the unit profit generated from a marginal license sold : it’s -12%. This means the more software sold, the more money the company loses. The contribution margin has improved from -117% in 2022, to -38% in 2023, to -12% in 2024. For most software companies, contribution margin is typically very high, around 80-90%. This is a burn-the-boats strategy which requires a lot of courage, a phenomenal commitment to the long term, & a big balance sheet to sustain the short-term losses & invest in a new product & new sales & marketing strategy to transform a massive caterpillar into an even bigger butterfly.”

“Multiples are most highly correlated to what we call the “Meritech Rule of 40”, defined as 3x NTM revenue growth + NTM free cash flow margin. Said another way, in today’s environment, growth has roughly three times the impact on the valuation of a public SaaS company vs. profitability (defined as free cash flow margin), and this metric appropriately captures that weighting.”

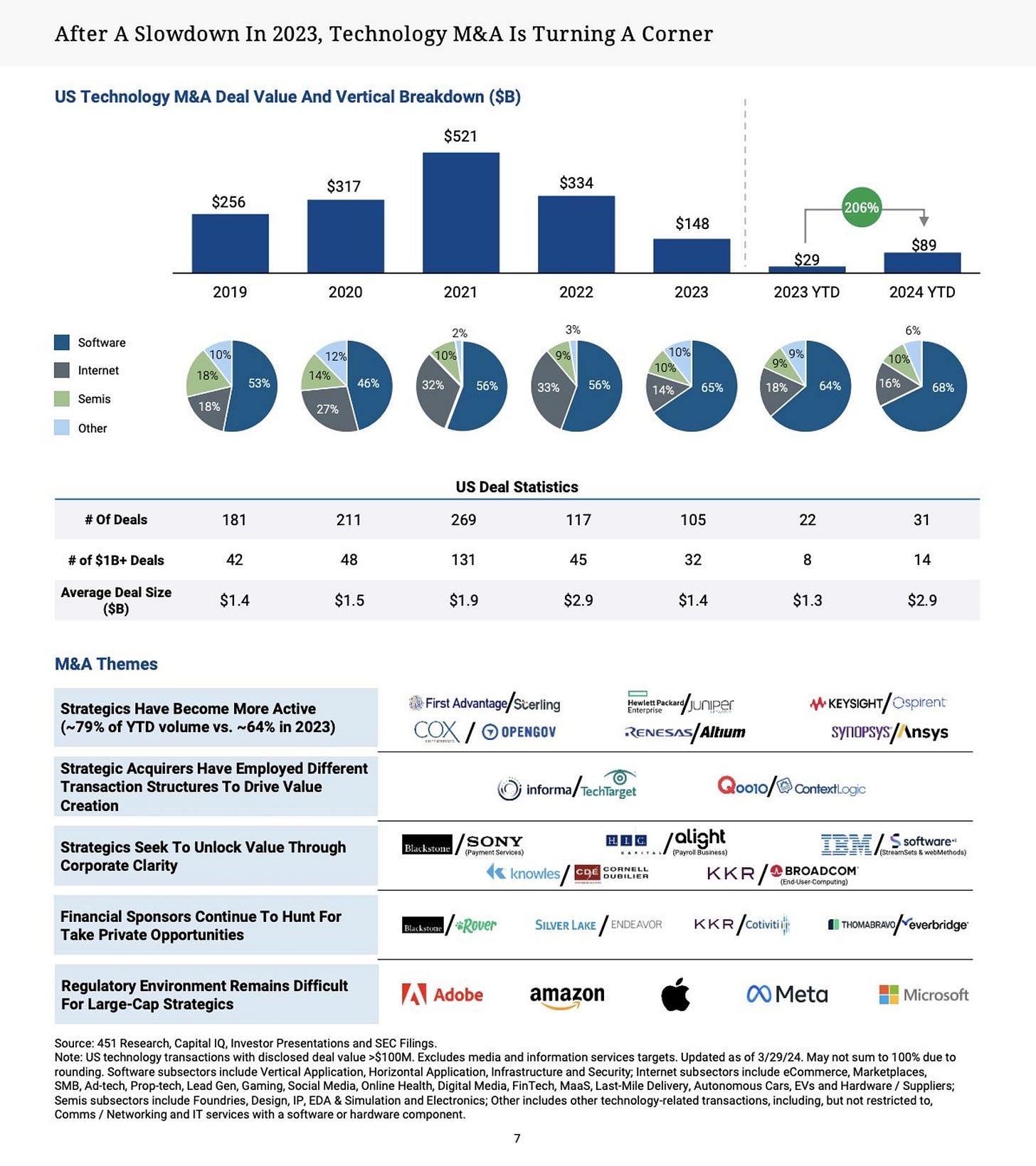

Wednesday, Apr. 3rd: ServiceTitan acquired Convex to expand its platform in the commercial services segment. - ServiceTitan

“ServiceTitan has entered into a definitive agreement to acquire Convex, a leading sales and marketing platform built specifically for the commercial services industry. This new partnership will help deliver an industry-leading end-to-end solution that enables commercial service businesses to grow profitably, from initial outreach to new prospects, through work order execution, invoicing, job costing, and everything in between.”

Convex was founded in 2017. It sells to commercial services businesses (HVAC, security, fire & life safety, facilities & janitorial, elevators). It’s mostly a sales and marketing platform to identify leads (with a rich properties database), to contact them and to turn them into customers.

Thursday, Apr. 4th: Iconiq shared the key characteristics that they’re looking for to lead a series B: (i) ARR growth above 100%, (ii) NDR above 100%, (iii) gross margins above 70%, an (iv) efficiency in the GTM. - Iconiq

“Even in this market, however, ARR growth rate and new logo velocity are the most reliable indicators of product market fit, and it is therefore difficult for sub $10 million dollar run rate companies to raise venture capital that are not doubling year over year.”

“According to our published data the median YoY growth rate for companies in our study at sub $25m ARR is 125% while the top quartile is 240%, and for companies between $5m and $10m, the median YoY growth is 165%. Investors won’t need to see a full 24 months for a year-on-year comparison, however, 3 months of 7% monthly growth isn’t really going to be enough, whereas 8 months of 15% monthly growth becomes very interesting.”

“The median NRR for sub $25m ARR companies according to our publications above is 105% while the top quartile retains at a rate of 125%. This metric has the tendency to remain relatively similar over various stages of a company’s life, so it will receive real scrutiny at this stage.”

“Accordingly, it will be vital for companies raising a Series B to present plans for effective growth. One way for CEOs to think about this is the company’s net magic number which is the current quarter’s net new ARR divided by the prior quarter’s sales and marketing opex. This metric is designed to measure the net revenue generation against sales and marketing operating costs, while accounting for the lag of a typical sales cycle. For sub $25m ARR companies, the median net magic number is 0.8 while the top quartile is 1.7.”

Friday, Apr. 5th: Bloomberg wrote about Hertz’s failed bet on aggressively transitioning its fleet towards EVs. - Bloomberg

“Earlier that day, Hertz, the rental-car giant that careened into bankruptcy during the first two months of Covid-19 burdened with a bad balance sheet and generations of even worse management, had raised $1.3 billion in an initial public offering. Somehow, in slightly more than five months, Wagner and O’Hara had pulled off one of the greatest turnarounds in corporate history.”

“By the time Wagner’s hedge fund, Knighthead Capital Management, and O’Hara’s private equity firm, Certares Management, bought Hertz in a June 2021 bankruptcy auction, the company had slashed its debt and cut 15,000 jobs. Neither Wagner nor O’Hara had any experience in the industry, but to the self-styled disrupters in an archaic business, that was a virtue.”

“Hertz’s new owners were making a fully charged bet to swap Hertz’s gas-powered rental-car fleet for EVs.”

“The November IPO valued Hertz at $15.3 billion, more than two-and-a-half times the $5.9 billion Wagner and O’Hara had paid to buy it out of bankruptcy.”

“By early 2024 it was clear the massive bet on electrification was a catastrophe. Musk had slashed Tesla prices by as much as 30%, sending the value of Hertz’s EVs plummeting. Wagner and O’Hara’s plan was filled with countless other miscalculations that only deepened the wound. All that talk of a radical makeover for a tired industry has gone silent, and the company is now doubling down on gas guzzlers.”

“Together they raised a $1.5 billion fund to snap up travel and leisure companies like Hertz that had been crushed by the pandemic and might eventually soar once the economy reopened.”

“Over the years, Hertz invested in plenty of software and cloud services, but it ended up with a jumbled mess of technology for different parts of the business and chronically failed to get those programs working in tandem.”

“In the field, everything started looking different from what was on the spreadsheets.”

Saturday, Apr. 6th: Bowery wrote about the benefits for vertical SaaS to target midmarket and enterprise customers instead of SMBs. - Bowery

There are 4 main benefits to sell to mid-market and enterprise customers: (i) higher ACVs making it easier to acquire customers efficiently, (ii) stickier customers (less bankruptcy, higher gross retention, higher potential for upsell), (iii) existing willingness to pay, (iv) less competition.

“SMB-focused vSaaS businesses tend to benefit initially from quick sales cycles, but then struggle with high churn and difficult retention metrics inherent to these buyers.”

“Many of the less ‘technical’ SMB opportunities have become quite crowded with four or five venture-backed players competing over a relatively small pie.”

“The enterprise grade vertical software approach has minted a number of public scale success stories including nCino (selling into commercial banks), Duck Creek (selling into P&C insurance carriers), and Veeva (selling into large life sciences businesses). I estimate the ACVs of nCino at $275K, Veeva at $1.5MM and Duck Creek at $1.7MM based on some back of the envelope math on their 10-K’s comparing customer count and topline revenue.”

Sunday, Apr. 7th: I read several blog posts from Josh Tarasoff who is the founder of a US based hedge fund called Greenlea Lane. - Greenlea Lane 1, Greenlea Lane 2, Greenlea Lane 3

“Only genuine and well-placed implicit conviction, a qualitative knowing that the company will do what it needs to and ought to do, is equipped to ably traverse this kind of terrain. Unlike analysis-based explicit conviction, implicit conviction comes from something deeper than the cause and effect we perceive in the unfolding of events—it is both analytical and, crucially, intuitive.”

“My best investments have erred on the side of management and cultural excellence (implicit) when faced with disappointing fundamental performance or a seemingly stretched valuation (explicit).”

““Some companies have a soul,” I found myself saying to a friend over lunch, “others are just going through the motions.””

“The following is a selection of (neither necessary nor sufficient) indicators that I have found to be suggestive of Quality in companies: (i) “Wow” customer experiences, (ii) mission to solve an important problem, (iii) domain mastery (the best at what they do), (iv) first-principles-based thinking and invention, (v) unlimited ambition combined with no-nonsense realism, (vi) overcapitalized balance sheet, (vi) founder mentality (life’s work).”

“The necessity to be continuously on the verge of some great new [investing] idea sows an endemic hurriedness that can be seen on people’s faces and heard in their voices. This struck me as unhealthy for decision making.”

“Instead of having a finite time frame for my investments, I decided to have an infinite time frame. I approach each investment with a permanent attitude, hoping and expecting the company to shoulder the work of compounding itself, ideally allowing Greenlea Lane to own it forever.”

“Sustainable long-term growth requires positive feedback loops. A positive feedback loop is when an increase in the quantity of something causes a further increase in the quantity of that thing. Perhaps the best-known positive feedback loop is a network effect: because the utility of the network increases directly as a function of the number of users, growth in the number of users causes further user growth. Another commonly cited positive feedback loop is scale economies shared: because the customer value proposition improves as sales volumes increase, growth in sales volumes causes further sales volume growth.”

“My investment theses are underpinned by what I call an endgame: a long-term state of affairs in which I have high conviction. The basis for this conviction is what I think of as overwhelming logic: forces that make too much sense not to prevail in the fullness of time.”

“Another reason I like endgames is that they tend to be undervalued. They are so far into the future—typically 10 years or more—that most market participants simply do not care. Even if they intellectually grasp the overwhelming logic, it simply might not matter to them.”

“In reality, though, the path is rarely predictable with any degree of precision—not even by companies themselves, let alone by outside observers. Near-term events are subject to any number of influences. By contrast, endgames can be predictable because they are so far into the future that feedback loops, quality, and overwhelming logic will have had plenty of time to play out.”

Monday, Apr. 8th: The Economist explored an unexpected consequence of climate change which is the vulnerability of residential properties worldwide. - The Economist

c.10% of the world's residential property, regardless of proximity to the coast, is at risk from climate change-induced severe weather events.

Climate change and mitigation efforts could potentially cause a loss of 9% of global housing value by 2050, amounting to $25tn, with homeowners likely bearing the costs.

Home insurance costs are rising due to increased natural disasters, potentially leading to a "climate-insurance bubble," and governments may need to intervene to cover losses or underwrite risks.

Challenges include investing in property protection and infrastructure, funding domestic modifications for emissions reduction, and balancing incentives for homeowners with collective action on climate resilience without subsidizing risky behavior.

“House prices show little sign of adjusting to climate risk. In Miami, the subject of much worrying about rising sea levels, they have increased by four-fifths this decade, much more than the American average.” “The evidence shows that house prices react to these risks only after disaster has struck, when it is too late for preventive investments.”

Tuesday, Apr. 9th: Jason Lemkin shared his concerns about the current SaaS landscape characterised by slowed growth, multiples below historical average, buyers consolidating their tech stack & asking for price rebates as well as VC funding drying up. Jason believes that companies should implement 4 strategies to go through this period: (i) generating efficiency gains for customers, (ii) be at least on par with other players on AI features, (iii) bring new customers, (iv) grow usage more than revenues. - Jason Lemkin

Drive genuine efficiency gains: Rather than relying on superficial ROI calculations, prioritize delivering tangible efficiency improvements to customers, even if it means significant restructuring or process optimization.

Attain AI parity with alternatives: While AI might not revolutionize every aspect of SaaS, ensuring competitive parity in AI capabilities is crucial, as customers increasingly demand enhanced efficiency from AI-driven solutions.

Prioritize customer acquisition and satisfaction: Shift focus from short-term tactics like price hikes to a long-term strategy centered on closing every prospect who can be satisfied, potentially even by offering cheaper or more flexible options.

Emphasize usage growth: While revenue growth remains essential, surpassing it with even faster growth in core usage metrics like MAUs or API calls ensures a brighter future and stronger customer engagement.

Wednesday, Apr. 10th: Jehoshaphat Research wrote a short-selling reporting on Doximity. It’s a publicly listed vertical SaaS in the US building a social network for medical professionals which is monetised via advertising and productivity tooling. - Jehoshaphat Research

“We believe Doximity’s underlying sales, contrary to the Street’s expectations for double-digit growth, are declining at a negative -3-6% rate, but that this decline has been masked through accelerated revenue recognition.”

“Our research suggests that Doximity’s customer ROI is declining, and if so there appear to be two potential reasons for this: declining user engagement overall, and ad inventory in excess of what the “real estate” available on the platform can support. Doximity, unlike say Instagram or Facebook, is not an app that users sit on and scroll for hours a day. The amount of ads that can be served on a platform like this is naturally limited.”

“Another fundamental problem is the emergence of LinkedIn as a viable threat: “Doximity used to be called LinkedIn for physicians, but in lieu of that, now we’re just using LinkedIn!” says one marketer. Another explains why their pharma customers’ digital budgets for Doximity have been slashed: “Oh, I can just use LinkedIn for that.” This change appears to have started within the past two years, as pharma companies have increasingly aimed their marketing budgets at other influencers in the drug value chain – influencers not in Doximity’s sweet spot.”

“Engagement with the Doximity platform appears to be falling, consistent with being a product that was novel in the 2010s but has become stale in the 2020s. There are a multitude of markers suggesting that declining user engagement within the Doximity app is at the root of the problem.”

Thursday, Apr. 11th: Pigment raised a $145m series D led by Iconiq with the participation of Sandberg Bernthal Venture Partners, IVP Meritech and Greenoaks. The company seems to have reached the $1bn valuation threshold. - Pigment, Techcrunch, Sifted

Together with Pennylane, Pigment is demonstrating the resilience and the maturity of the French tech ecosystem. Both companies have many similarities: (i) they became unicorns in a short timeframe despite the market correction, (ii) they were founded by repeat entrepreneurs, (iii) they built complex and deep platforms which took time before scaling commercially, (iv) they have an amazing growth endurance (i.e. continuing to grow exponentially at a large scale beyond $10m in ARR).

“89% of finance leaders are making decisions every month based on inaccurate or incomplete data.”

“90% of our customers are now using the platform across multiple departments.” “It’s a modern SaaS platform, meaning that you can integrate it with all your company’s data (ERP, HRIS, data lakes, etc.) and use it as a collaboration tool. In addition to finance teams, sales teams can use Pigment to create quotas and see how everyone is performing against quarterly quotas. HR teams can see how they should scale the workforce up and down based on strategic changes and financial objectives.”

In 2023, Pigment tripled its ARR and doubled its number of customers. It generates more than 50% of its revenues in the US. It implemented many partnerships with companies like Deloitte, Slalom and BearingPoint.

“Our current investors told us ‘if you’re going to raise money in 18 months to scale with others, we might as well offer you great terms right now for an internal round.’ And everything happened very quickly … In one week, it was a done deal.” - Eléonore Crespo (co-CEO and cofounder at Pigment)

Friday, Apr. 12th: Gokul Rajaram wrote about what it takes for a venture backed company to go public in terms of scale. - Gokul Rajaram

“Companies with less than $700m annualized revenue underperform after going public. Actually, not just underperform - they have negative absolute returns. This makes it hard to retain employees, sustain analyst interest or build a book of permanent buy-and-hold shareholders.”

“A few months ago, I had posited that one needs $500m in revenue to go public. If a startup goes public with $250m in revenues, unless they are growing really fast (>50% YoY if not faster), they should expect the next few years to be a daily struggle. Sadly, an acquisition by a larger company or by PE might be an inevitability, as we’re seeing almost daily today.”

“Public markets want growth and efficiency. Unfortunately, many of the smaller companies don't have efficiency (yet). Many are smaller, not profitable, and have the same revenue growth rates at ~20% as the largest, but have a 0 Rule of 40 vs. 41 Rule of 40 for the $3B+ revenue businesses. So as an investor you can buy the same growth rate with significantly more margin with the largest businesses. The Rule of 40 line for these companies goes up with scale. Also note that many of the smaller companies IPO'ed in 2021 and would not likely make it out in today's market with their current unit economics.”

“Klaviyo is the poster child here. Absolutely monster business in terms of growth, efficiency, etc, and I'm always shocked that it doesn't get a premium of any kind.”

Saturday, Apr. 13th: Andy Jassy published Amazon’s 2023 letter to shareholders. - Amazon

“Amazon’s advertising progress remains strong, growing 24% YoY from $38B in 2022 to $47B in 2023, primarily driven by our sponsored ads.”

“Shifting to AWS, we started 2023 seeing substantial cost optimization, with most companies trying to save money in an uncertain economy. […] This work diminished short-term revenue, but was best for customers, much appreciated, and should bode well for customers and AWS longer-term.”

“Kuiper is our low Earth orbit satellite initiative that aims to provide broadband connectivity to the 400-500 million households who don’t have it today (as well as governments and enterprises seeking better connectivity and performance in more remote areas), and is a very large revenue opportunity for Amazon. We’re on track to launch our first production satellites in 2024.”

“We spend enormous energy thinking about how to empower builders, inside and outside of our company. We characterize builders as people who like to invent. They like to dissect a customer experience, assess what’s wrong with it, and reinvent it. Builders tend not to be satisfied until the customer experience is perfect. This doesn’t hinder them from delivering improvements along the way, but it drives them to keep tinkering and iterating continually. While unafraid to invent from scratch, they have no hesitation about using high-quality, scalable, cost-effective components from others. What matters to builders is having the right tools to keep rapidly improving customer experiences.”

How does Amazon break down the Gen. AI stack?

“The bottom layer is for developers and companies wanting to build foundation models (“FMs”). The primary primitives are the compute required to train models and generate inferences (or predictions), and the software that makes it easier to build these models”

“The middle layer is for customers seeking to leverage an existing FM, customize it with their own data, and leverage a leading cloud provider’s security and features to build a GenAI application—all as a managed service.”

“The top layer of this stack is the application layer. We’re building a substantial number of GenAI applications across every Amazon consumer business. These range from Rufus (our new, AI-powered shopping assistant), to an even more intelligent and capable Alexa, to advertising capabilities (making it simple with natural language prompts to generate, customize, and edit high-quality images, advertising copy, and videos), to customer and seller service productivity apps, to dozens of others. We’re also building several apps in AWS, including arguably the most compelling early GenAI use case—a coding companion.”

“How does Amazon remain resilient? While simple in its wording, it’s profound because it gets to the heart of our success to date as well as for the future. The answer lies in our discipline around deeply held principles: 1/ hiring builders who are motivated to continually improve and expand what’s possible; 2/ solving real customer challenges, rather than what we think may be interesting technology; 3/ building in primitives so that we can innovate and experiment at the highest rate; 4/ not wasting time trying to fight gravity (spoiler alert: you always lose)—when we discover technology that enables better customer experiences, we embrace it; 5/ accepting and learning from failed experiments—actually becoming more energized to try again, with new knowledge to employ.”

Sunday, Apr. 14th: Emergence Capital wrote a great post arguing that many services heavy businesses had the potential to be disrupted with AI. - Emergence

“We even have a beacon out there showing the way: Palantir. What started as a services business is now amongst the most highly-valued (on a multiples basis) venture-backed company in the industry.”

“Service businesses that leverage both AI and humans to deliver holistic solutions to clients are poised to outgun and outpace the services behemoths that’ve dominated for the last 50 years.”

More specifically, AI has a strong potential to disrupt services firms doing “a job that the client doesn’t have the bandwidth or expertise to do” (e.g. IT implementations, financial audits, outsourced customer support).

Monday, Apr. 15th: Compound published its 2023 annual letter sharing how the deep-tech fund thinks about its core verticals including AI, robotics, TechBio and crypto. - Compound

“Our core competency at Compound is not necessarily an ability to pick the best company in a crowded, overfunded area, but instead to notice “n-of-1” approaches or company types that are underappreciated or could be special for a variety of reasons.”

“This orthogonal approach may mean we will have a high failure rate as markets mature and become more consensus, but it also should mean we will be able to back founders who are uniquely creatively-minded and unafraid to look stupid, something we believe creates asymmetric outcomes.”

“Across many technology category cycles, people routinely underestimate the value of distribution. Our view on robotics, which could age horribly if we are underestimating deployment time, cost curve, and functionality of humanoid robots, is that while a subset of high value tasks will be enabled with costly but highly performant humanoid platforms, many others will see very large businesses built in the next 3-5 years by companies that build models, create data flywheels, and can operate with 90%+ autonomy in order to get distribution with a subset of customers on their way to 99.999% autonomy over time.”

Tuesday, Apr. 16th: The Economist wrote on the Gen Z going after the general consensus that they constitute a despondent generation destined for lesser financial prosperity than their predecessors, and characterized by excessive smartphone and internet dependency. - The Economist 1, The Economist 2

Generation Z is experiencing strong economic conditions with a youth unemployment rate at its lowest in decades across the rich world.

More Gen Z individuals are pursuing degrees in science, engineering, and medical fields, moving away from humanities.

Gen Z's strong wage growth has improved their financial stability, allowing them to save more and, in some cases, enter the housing market earlier than previous generations.

Gen Z tends to be more serious and less indulgent in risky behaviors compared to previous generations. They show greater concern for social issues like climate change and mental health, which influences their voting and consumption behaviors.

“For each generation there is a simple narrative. For Gen Z the popular view is that smartphones have made them miserable and they will live grimmer lives than their elders.”

“In some ways, Gen Z-ers are unusual. Young people today are less likely to form relationships than those of yesteryear. They are more likely to be depressed or say they were assigned the wrong sex at birth. They are less likely to drink, have sex, be in a relationship—indeed to do anything exciting. Americans aged between 15 and 24 spend just 38 minutes a day socialising in person on average, down from almost an hour in the 2000s, according to official data.”

“Gen Z-ers are less likely to be entrepreneurs. We estimate that just 1.1% of 20-somethings in the eu run a business that employs someone else.”

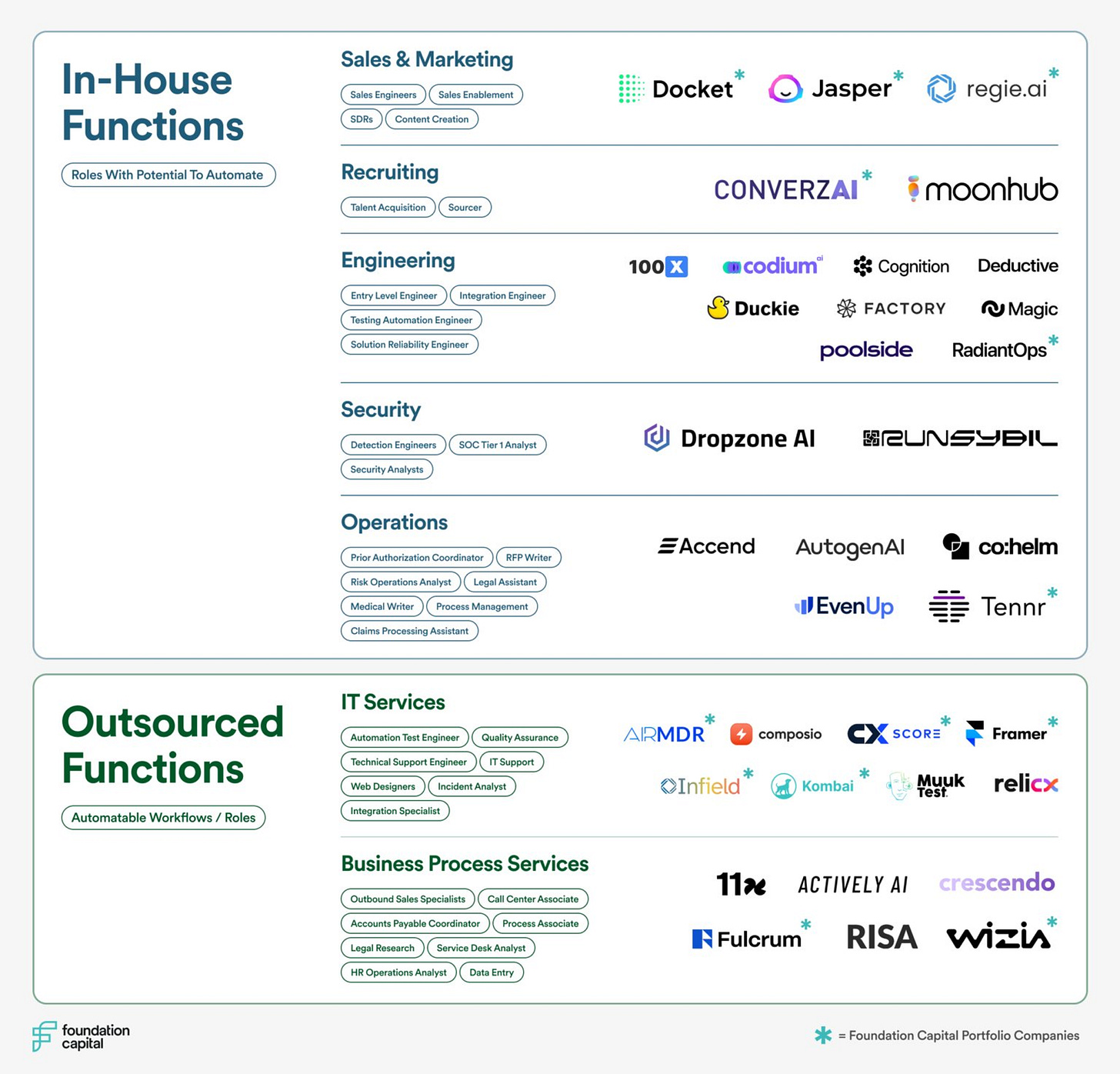

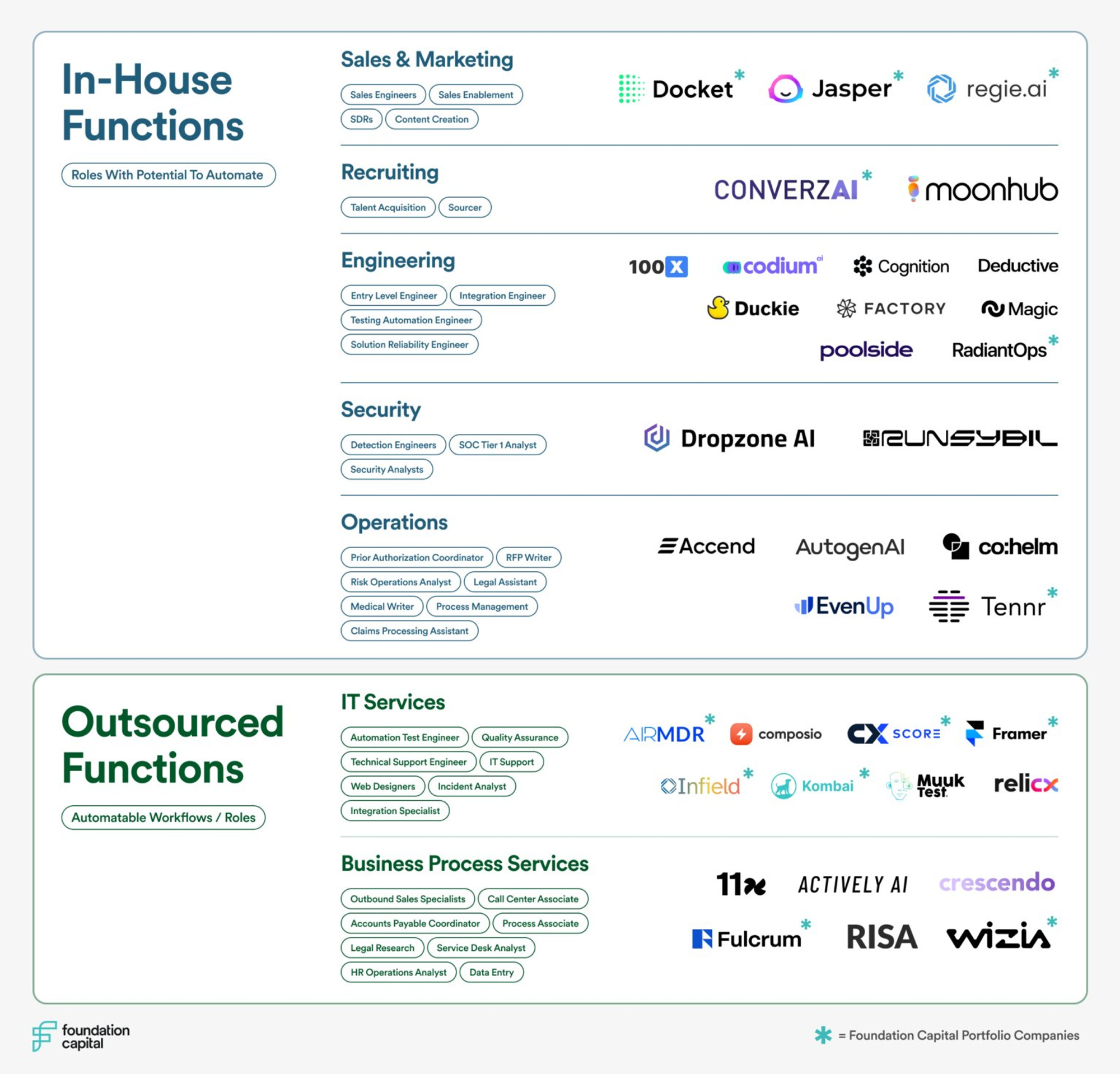

Wednesday, Apr. 17th: Foundation Capital shared an interesting market map on AI startups that are trying to fully automate services. - Foundation Capital

“AI companies are leading a transition from Software-as-a-Service to Service-as-Software, turning the table on the very essence of SaaS.“

“In the software business, a company may sell access to its platform or tool, but customers are still responsible for using that tool to achieve the desired outcome. In the services business, responsibility for achieving the desired outcome sits with the company selling the service.”

“In the coming decade, we believe software will continue to boost productivity and also will take a bite out of the services market.”

Thursday, Apr. 18th: I listened to a podcast with Bill Gurley and Brad Gerstner on the IPO market. - BG2

“It's quite clear that risk seems to be on the rise with the US elections coming and the different conflicts around the world.”

The number of US public companies has gone down from 6.5k to c.4k over the last 20 years. It’s paradoxical because historically the number of public companies had always been increasing. Moreover, in recent years, more startups than ever are being funded and should have increased the public companies pool.

“In the past, you could go public with a $500m market cap. … [and] $50m in revenue. Today, we think that you can’t go public without $1bn in revenue, $10bn in market cap.” - Philippe Laffont (Chief Investment Officer at Coatue)

“Median LTM revenue at IPO for software companies is ~$185m. With median quarterly YoY growth rate >50%. Lots of super successful companies went public with <$150m of revenue (Shopify, HubSpot, Coupa, Zendesk, Coupa, Mongo, etc). But you have to be growing fast.” - Jamin Ball (Investor at Altimeter)

“Personally, I believe that being public is great for companies. It raises the bar in terms of their performance to achieve more than what they would have done otherwise. It gives mom and pop investors exposure to the tech ecosystem if tech companies are going public sooner rather than later.”

“I feel the bar for size is somewhere between $200m and $300m of revenues, premium growth rates to peers, and attractive unit economics. I think you need to net out at greater than $2bn, that generates an IPO of at least $200m to $250M, which has enough float to make it reasonable position for investors. To me, the IPO market is slow in volume terms for lack of supply, not lack of demand.”

“It’s not a demand problem but a supply problem that companies don’t want to go on the public market at that size.”

What are the causes behind the decline in the number of public companies?

First, there is immense capital availability in the private capital market. Companies that don’t want to be public don’t have to be because they can get access to private capital and that private capital will let them do secondaries that was an historical reason to become a public company.

Second, investment bankers have built their businesses to cater to large companies and so they prefer to work on bigger IPOs.

Third, the cost of being public has massively increased ($2-3m per year) because of the regulation (e.g. insurance, SEC reporting).

Many venture backed companies which are in the pipeline to go public are afraid to do so because their last private valuation was set up in 2020-2021 and was done at multiples that are way above what we currently see in the public market.

“If you're public with $100m in revenue and 10% growth rate, your valuation not going to be all that great but guess what if you're private at $100m with a 10% growth rate it's not like you're better off. You’re just fooling yourself.”

“As a tech community, we need to be more serious about the public exit option because large tech companies have been pushed away from M&A by regulatory reducing the number of potentiel buyers for tech companies.”

“The public market is wide open for strong businesses with great unit economics, that can grow above market rates for a long period of time and that can expand margins overtime.”

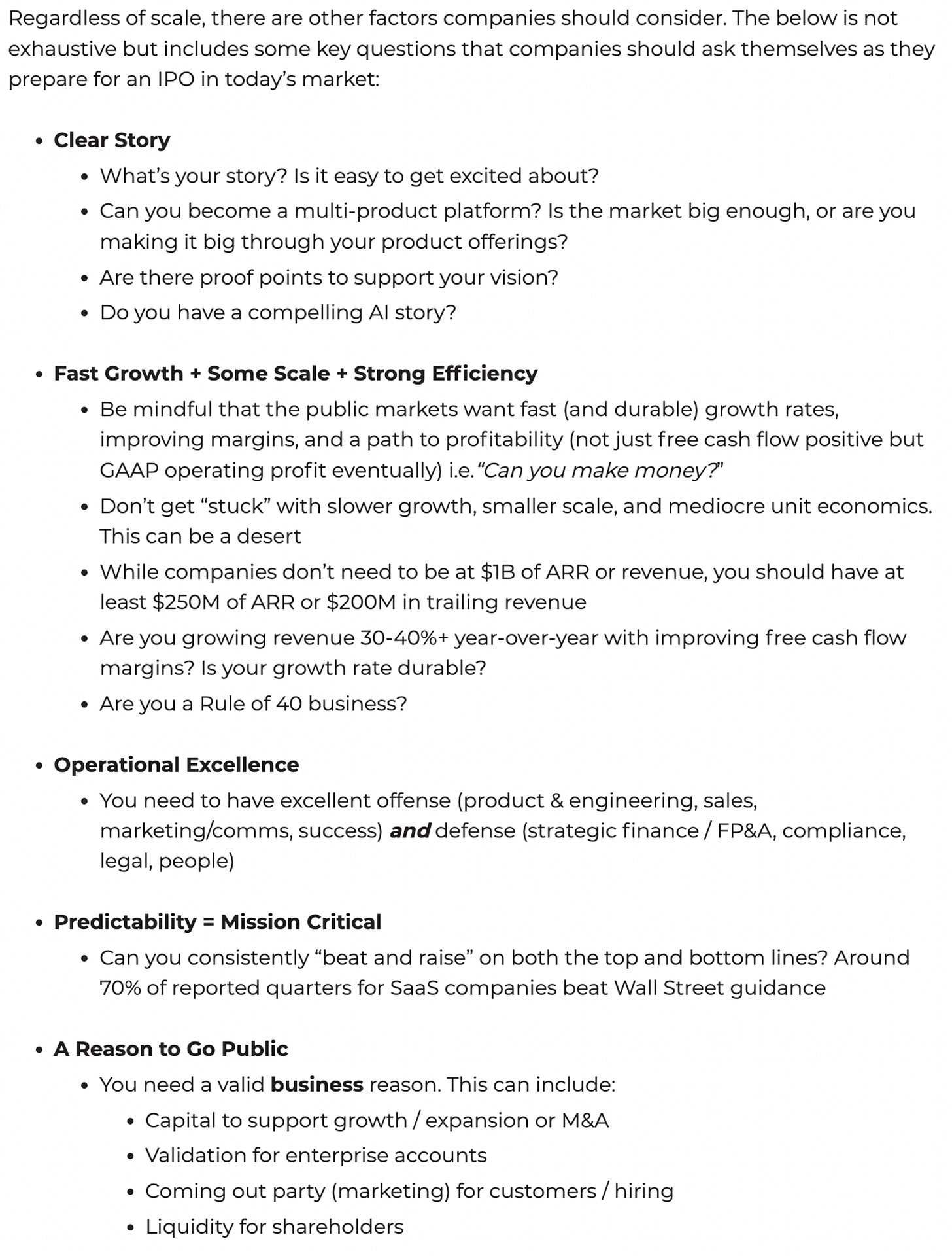

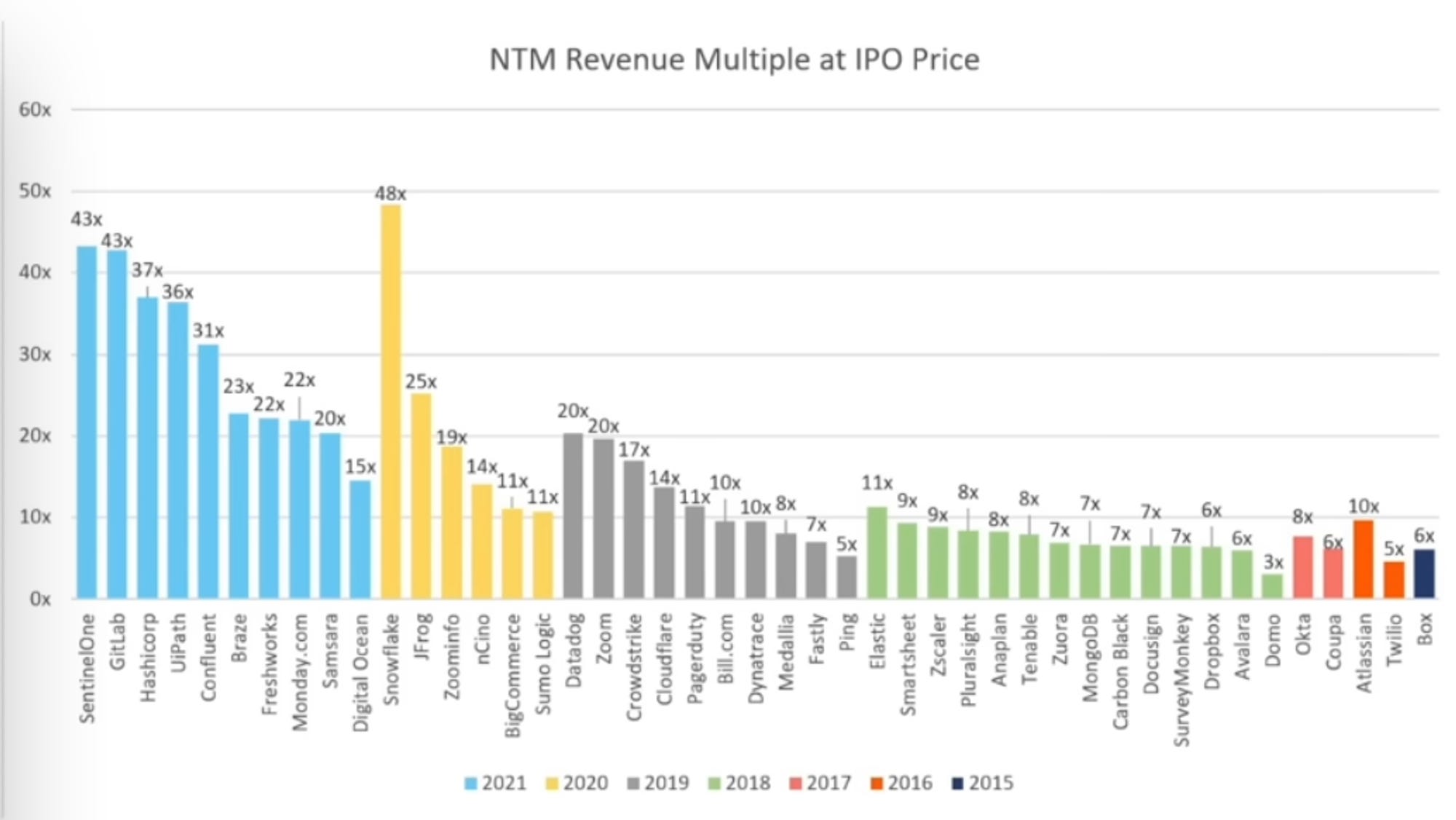

Friday, Apr. 19th: Meritech published an article on IPOs. - Meritech

“While the goalposts have shifted over time toward larger companies, other factors such as revenue growth rate and durability of growth, business predictability, operating leverage and margins (i.e. Rule of 40), and a strong platform story are more important than absolute revenue scale.”

“For a SaaS company to go public today, there is a narrative that you must be large, i.e. $1B in ARR or close to it. While there may have been a time when that was true over the past 2 years, we do not believe that is the case today. Moreover, there are many examples of companies going public at a smaller scale and going on to create massive, enduring platform companies (like CrowdStrike, Datadog, HubSpot, Shopify, Snowflake, and others) and, in doing so, have rewarded shareholders very handsomely.”

“We believe the best businesses, even at $250M+ of ARR, can be hugely successful in IPOs if they have the attributes of best-in-class businesses with great teams, large markets, fast and predictable growth, strong unit economics, and potential for platform businesses (and with an AI story too, of course!).”

Saturday, Apr. 20th: Spruce Point published a short-selling report on PowerSchool, a publicly listed vertical SaaS company building an all-in-one platform for K-12 education that I previously covered in this newsletter. - Spruce Point

“We have concerns over the Company’s aggressive accounting practices, unsustainable growth expectations, and sales of a product that may potentially be violating several states’ child privacy laws.”

“In response to the COVID-19 emergency, federal, state, and local legislatures passed a series of spending bills aimed at supporting K-12 districts through the pandemic.” “As the last of the federal COVID funding is required to be spent by September 2024, we believe this will create a fiscal cliff that will pressure growth across the ed-tech industry.”

“Our analysis of the budgets of 50 of the largest school districts in the U.S. shows that tech spending by school districts is decelerating, and in many cases is declining.”

“The Company has aggressively increased its reported TAM by 4x since its IPO. We question the rationale given by management for the increase and believe this is an attempt to attach itself to the recent hype around artificial intelligence/machine learning and to artificially increase the Company’s perceived growth prospects and valuation.”

“Curiously, PowerSchool obscures its 1997 founding date in its SEC filings. We could only find the date on a chart within its IPO prospectus that cannot be word searched. We believe this a potential attempt by management to gloss over the fact that its core products appear to have been pieced together via acquisitions over 25 years.”

“PowerSchool appears to be losing momentum in its core SIS product. Recent data confirms PowerSchool has been losing share to competitors such as FACTS SIS, Gradelink SIS, and others.”

“PowerSchool’s largest smartphone app, PowerSchool Mobile, has almost 34K reviews and has been downloaded over 5 million times on the Google Play store, carrying a mediocre 2.3-star average rating.”

“We believe PowerSchool's recent acquisition of SchoolMessenger represents an extension of the Company’s portfolio of lowquality technology. On the Company’s Q4’23 earnings call, management disclosed that SchoolMessenger provided roughly $40 million in ARR; based on its reported 28 million student base, this implies an average per student pricing of $1.48, near the low end of ed-tech module pricing. Management disclosed that SchoolMessenger EBITDA margin is similar to PowerSchool’s, which reported a ~33% margin in FY23; this implies $13M-$14M of EBITDA from SchoolMessenger. At the $300 million purchase price, this implies a 7.5x sales and ~22x EBITDA multiple. We believe this represents a significant premium to pay for low-grade technology with limited pricing power.”

Sunday, Apr. 21st: Ben Evans wrote about current and future AI use cases. - Ben Evans

“The one really big use-case that took off in 2023 was writing code, but I don’t write code. People use it for brainstorming, and making lists and sorting ideas, but again, I don’t do that. I don’t have homework anymore. I see people using it to get a generic first draft, and designers making concept roughs with MidJourney, but, again, these are not my use-cases. I have not, yet, found anything that matches with a use-case that I have.”

“As these models get better and become multi-modal, the really transformative thesis is that one model can do ‘any’ use-case without anyone having to write the software for that task in particular.”

“These are probabilistic rather than deterministic systems, so they’re much better for some kinds of task than others. They’re now very good at making things that look right, and for some use-cases this is what you want, but for others, ‘looks right’ is different to ‘right’.”

“No matter how good the tech is, you have to think of the use-case. You have to see it. You have to notice something you spend a lot of time doing and realise that it could be automated with a tool like this.”

“The change would be that these new use-cases would be things that are still automated one-at-a-time, but that could not have been automated before, or that would have needed far more software (and capital) to automate.”

Monday, Apr. 22nd: Ramp and Rippling are demonstrating that the US tech growth scene is bouncing back. Investors seems to be willing to invest in up-rounds at rich revenue multiples and with secondaries. - Techcrunch for Ramp, Techcrunch for Rippling

Ramp raised a $150m series D extension at a $7.65bn valuation co-led by Founders Fund and Khosla (vs. $8.1bn valuation in Mar. 2022 and $5.8bn valuation in Aug. 2024).

Rippling is raising a $870m series F (inc. $670m in secondaries) at a $13.4bn valuation (vs. $11.3bn valuation in Mar. 2023). Founders Fund is rumoured to invest in the company alongside Coatue and Greenoaks.

Tuesday, Apr. 23rd: Elaia and Lazard disclosed more information about their partnership. They are creating a new entity (25% ownership for Elaia, 75% ownership for Lazard) to raise a new growth fund to be launched in 2025, which could potentially reach €1bn and to invest €30-40m tickets. Lazard will raise capital from its large customer base in its investment banking and private wealth businesses. Moreover, Lazard took a minority ownership stake in Elaia with the possibility of acquiring 100% of the company overtime. - Sifted, Tech.eu

Wednesday, Apr. 24th: Euclid Ventures shared its investment thesis on vertical SaaS. Euclid is a pre-seed fund in the US investing exclusively in vertical SaaS and writing $0.5-1.5m tickets as lead investor. - Euclid

“As a category, Vertical SaaS is uniquely well suited to thrive in volatile market conditions and produce fund-returning outcomes.”

“The best founding teams for an industry-specific SaaS solution understand stakeholder workflows first-hand–not only their day-to-day but also what it takes to drive lasting behavior change. This experience can come from working at a vertical software startup or from direct industry operating experience.”

“The best vertical SaaS salespeople often have a background in the industry. For example, many of Toast’s best account executives are former chefs or food distribution reps.”

“Today, roughly half of the sub-sectors composing GDP are without category-specific software.”

“What is an underserved market? Ideally, one lacking in existing software options. But spaces with dominant, legacy market-share leaders can also be interesting if there is a compelling reason to believe unseating them is possible. Aging incumbents, high levels of PE consolidation, and rock-bottom NPS are positive indicators. We are most compelled by technology-driven advantages that would be hard for legacy leaders to replicate. Scope is also critical here: you can rarely rip-and-replace full-stack solutions. The selection of a beachhead where we can get early adopters quickly and set the stage for product expansion beyond that initial wedge is paramount.”

“The strongest points of control revolve around increasing revenue by opening up new markets, speeding up sales cycles, or improving end-customer experience.”

“On average, vertical SaaS startups are more capital-efficient than their horizontal peers. First, vSaaS players tend to spend less on sales & marketing per dollar of ARR, both public companies and in earlier stages. Second, we see consistent examples of vertical startups achieving venture-scale outcomes with less-than-average private capital paid in.”

Thursday, Apr. 25th: Rippling raised a $200m series F at a $13.5bn valuation led by Coatue with the participation from Founders Fund, Greenoaks and Dragoneer. The round also includes a $590m secondary from employees and early investors. - Rippling 1, Rippling 2

“Rippling’s one underlying insight is that most business systems are full of information about employees. Everyone knows that’s true for HR systems. But we know this is true beyond the HR department as well.”

“One unexpected side benefit of the memo has been recruiting. I always give candidates a copy of this memo before meeting with them, and our recruiting team uses it broadly, as well. It’s a great way for prospective employees to build an understanding of the company.”

“The administrative burden that Rippling solves is significant. The proof is that when businesses use Rippling, they need half the headcount in HR, IT, and Finance roles compared to what’s required if they use one of our competitors.”

“The corollary opportunity for Rippling, then, is to rebuild business software across each software vertical, but to embed an understanding of your company’s employees in the foundations and tissue of each of these products.”

“Compound products have five specific advantages over focused, point-SaaS competitors: (i) more integrated with other products in Rippling, (ii) more deeply integrated with employee data, (iii) built on a set of middleware or platform components, (iv) composed of common UX patterns, (v) bundled pricing & contracting.”

“Because point-SaaS companies can amortize sales and marketing and R&D costs over only a single SKU, they will increasingly be at a pricing disadvantage to compound companies like Rippling.”

“As the cloud software ecosystem matures and the underlying delivery mechanisms like “cloud” and “mobile” grow firmer roots, the overwhelming advantages of deep systems integration and bundled contracting and pricing will begin to re-dominate.”

“Rippling has an important “second-mover advantage” in SaaS markets. The more mature the market, the more there is an existing spec for the capabilities we need to have to compete head-to-head with point-SaaS incumbents. We’re going to win on the capabilities we have that are common to all Rippling products.”

“While Rippling’s R&D investment is unusually high as a percent of revenue and will need to come down as a percentage of revenue over time, we believe our HCM competitors have been underinvesting in R&D for years. We are going to make them regret this misstep.”

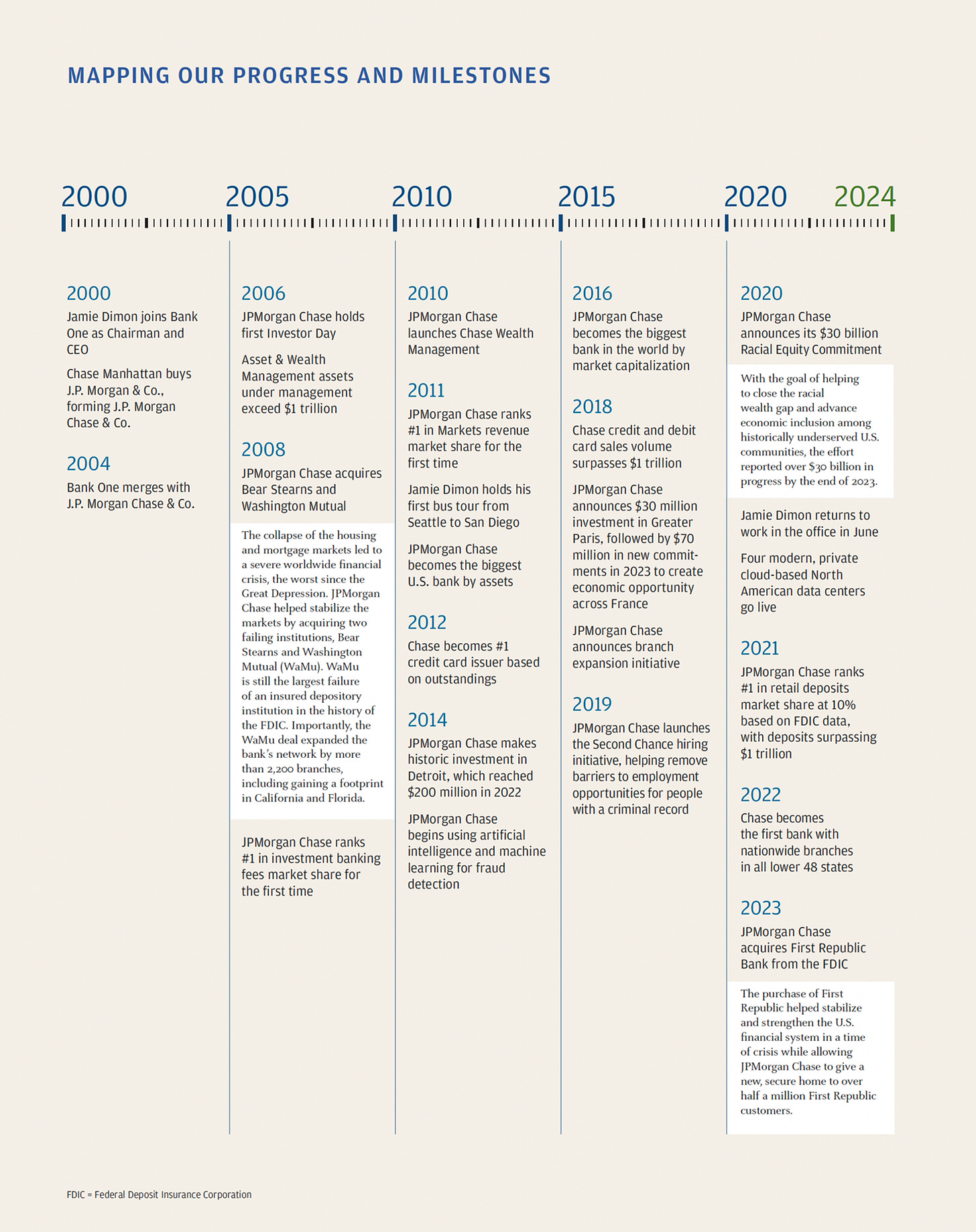

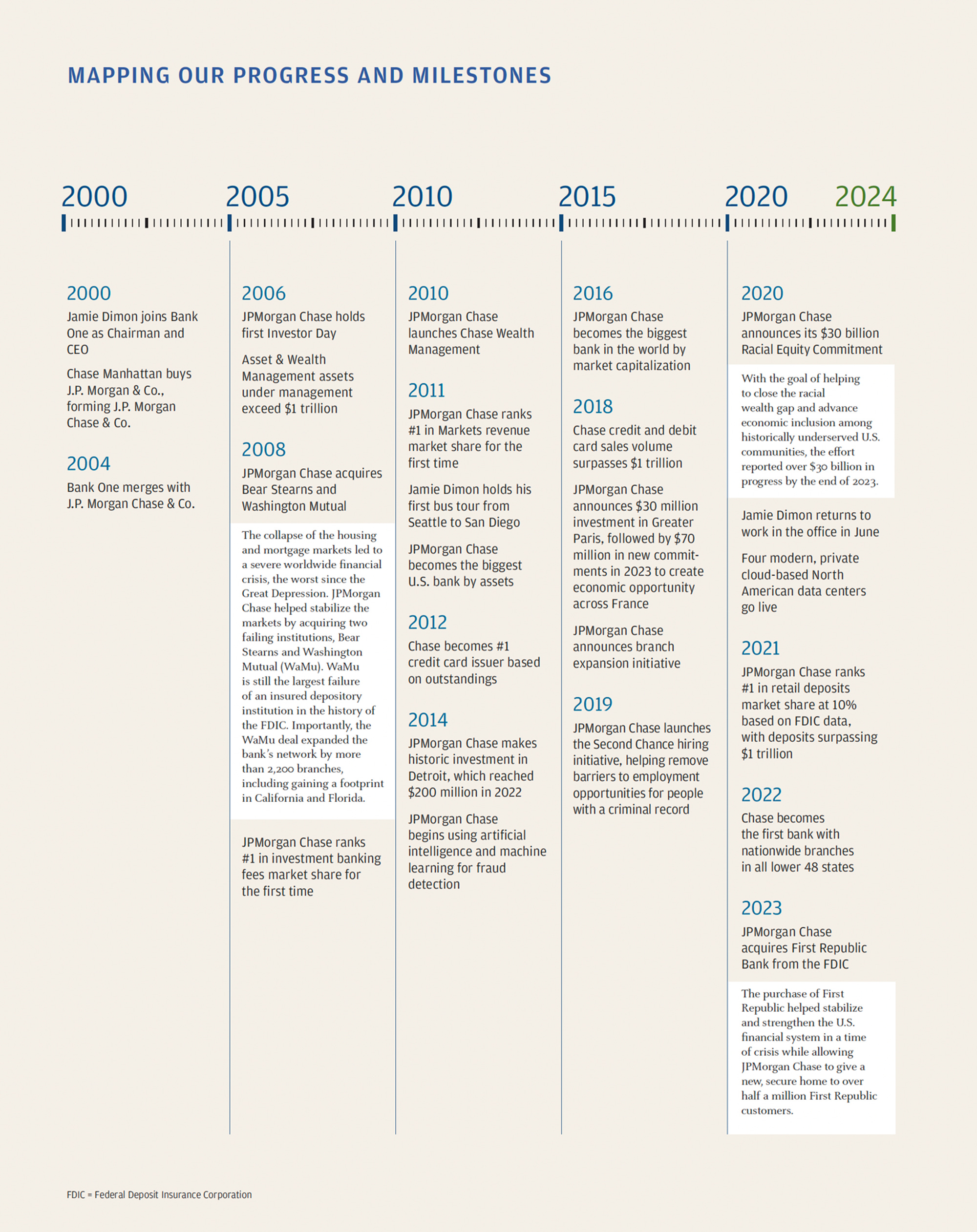

Friday, Apr. 26th: I read Jamie Dimon’s 2023 annual letter to shareholders. - JP Morgan

“Shareholder value can be built only if you maintain a healthy and vibrant company, which means doing a good job of taking care of your customers, employees and communities.”

“In previous letters, I have described the diminishing role of public companies in the American financial system. From their peak in 1996 at 7,300, U.S. public companies now total 4,300 — the total should have grown dramatically, not shrunk. Meanwhile, the number of private U.S. companies backed by private equity firms — which does not include the rising number of companies owned by sovereign wealth funds and family offices — has grown from 1,900 to 11,200 over the last two decades. This trend is serious and may very well increase with more regulation and litigation coming.”

“I fear we may be driving companies from the public markets. The reasons are complex and may include factors such as intensified reporting requirements (including investors’ growing needs for environmental, social and governance information), higher litigation expenses, costly regulations, cookie-cutter board governance, shareholder activism, less compensation flexibility, less capital flexibility, heightened public scrutiny and the relentless pressure of quarterly earnings.”

“The military, which often operates in extreme intensity of life and death and in the fog and uncertainty of war, uses the term “OODA loop” (Observe, Orient, Decide, Act — repeat), a strategic process of constant review, analysis, decision making and action.”

Saturday, Apr. 27th: Samir Desai wrote about Square’s closed loop ecosystem when consumers are paying Square’s merchants via CashApp - Samir Desai

“If Cash App can incentivize more payments volume to go through Cash App Pay, there is an opportunity for massive gross profit uplift, because Cash App Pay’s take rate is substantially higher than Cash Card’s take rate on purchase volume.”

“In the case of Cash App Pay, there’s potentially a few magic tricks at work. The first is that in this case, Block is both the acquiring processor + bank and the issuing bank, because it’s facilitating the Square merchant’s acquiring POS and it’s issuing the Cash App user’s debit card, thereby cutting the intermediaries down in the typical payments flow and seemingly increasing Cash App take rates by 35-50% (instead of just interchange, you’re now getting interchange and the markup).”

“If you’re both the acquirer and the issuer, you don’t even need the payment network at all. You can simply move money by book transfer between your merchant’s bank account and your user’s bank account in a perfectly closed loop payment network.”

“Owning the payment network delivers all sorts of value from pricing power to instant settlement, risk mitigation, full lifecycle transaction analytics and of course, the bragging rights of being one of the few fintechs not beholden to the whims of the card networks.”

Sunday, Apr. 28th: Dripos raised a $11m series A led by Base10 to build the all-in-one platform for coffee shops, unbundling Toast on a specific sub-vertical. The company brands itself as “the only software you’ll ever need”, replacing multiple point solutions with a single application that combines POS, mobile ordering, marketing, team management, and payroll. - Techcrunch,

“Many were using a simple point-of-sale system, like Square. It wasn’t bad, necessarily, but not “meant exactly for their workflow,” Pawlik said. Many shops then employed 5 to 10 other pieces of software to fill in the gaps. Pawlik and Durrant decided to pivot and build a tool that would replace Square, Toast and those eight other pieces of software with one comprehensive tool.”

“Dripos brings together point-of-sale; mobile payments; employee management and payroll; loyalty and marketing automation; and administrative functions like accounting and banking.”

“Last year was the company’s first full year with the new tool; it now has a presence in coffee shops across 46 states. The number of locations relying on Dripos increased 400%, and the company processes hundreds of millions in annual payments.”

Monday, Apr. 29th: Gamesindustry wrote a post on the tough fundraising environment for mobile gaming companies. - Gamesindustry

“The mobile gaming market has become more challenging for new entrants due to its maturity and the dominance of established games, making it harder for new projects to achieve success.”

“During the pandemic, the margins in the mobile games market continued to grow, surpassing expectations. Even after the initial surge, the market remained attractive despite a slight decline in growth, enabling high margins or significant returns when selling a share.”

“Without resorting to the usual doomsaying about the hypercasual market, it still represents a massive portion of global installs, accounting for 26% of all mobile games in 2023. A few years ago, almost every project had the potential to soar. But currently, out of a thousand new games, there might not be a single hit.”

“It's nearly impossible for a small, young team to launch a successful project.”

“In hyper-casual gaming, the average development cost for a project that demonstrates promising metrics, accounting for all iterations, can easily surpass $20,000.” “Three to five years ago, hypercasual games were at their zenith, often developed by just one or two individuals. Fast forward to 2023/ 2024, and the typical team composition for hypercasual game development looks something like this: 1-2 developers, 1 game designer, 1 art manager, 1 FX specialist.”

In casual and midcore, “statistically, one out of every ten projects hits the mark, ensuring a return on investment for the other nine within a two to three year span.” “Investment costs for developing a single casual project start at around $500,000 initially and can balloon to $2 million to $3 million if the project makes it to launch.”

“In mobile game development, project profitability has declined on average, with successful launches becoming increasingly rare.”

Tuesday, Apr. 30th: Jefferies published its annual state of the internet report. - Jefferies

Tech companies are moving from a growth at all costs model to a profitable growth model in which the balance between EBITDA margin and revenue growth in the rule of 40 is much more skewed towards profitability.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋