🔨 ServiceTitan's S-1 Breakdown

Overlooked #187

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m breaking down ServiceTitan’s S-1.

Last week, ServiceTitan publicly filed its S-1 to prepare for its IPO. This is exciting news for the vertical SaaS enthusiasts, as ServiceTitan is one of the most prominent private vertical SaaS companies. The S-1 filling offers valuable insights into the business.

ServiceTitan is an all-in-one platform designed for mid-market and enterprise trades (e.g. HVAC, plumbing, electrical, garage door repair, chimney sweeping, landscaping). The company has raised $1.5bn from investors such as Sequoia, Iconiq, Battery, Index, and Bessemer. Its private market valuation peaked in Jun. 2021, when it raised a $200m series G at a $9.5bn valuation led by Thoma Bravo. ServiceTitan generates $740m in ARR growing 25% YoY from 8k customers.

In a previous article, I discussed ServiceTitan’s key learnings for vertical SaaS founders and Michael Tan provided an great introduction to the business for Contrary. This post is divided into 3 sections: (i) a summary of the business, (ii) a metrics overview and (iii) additional learnings for vertical SaaS founders based on the S-1 filing.

Part 1 - Summary of the Business

In North America, there are over 30+ distinct construction trades, including HVAC technicians, electricians, plumbers, carpenters, landscapers, painters and roofers. Each trade specialises either in construction and/or maintenance works and typically operates within the residential and/or the commercial segments of the market.

ServiceTitan was founded in 2007 to provide plumbers specialised in residential maintenance with a comprehensive sales, marketing and operations platform. Over time, the company expanded in 3 key directions simultaneously: (i) adding new trades, (ii) adding products to become an all-in-one platform and (iii) entering the construction and commercial segments.

An all-in-one platform means that a trade can manage its entire business on ServiceTitan including generating leads, converting them into customers, serving customers, invoicing and handling back-office operations.

In the S-1, ServiceTitan explains that it has rebuilt and tailored specifically for the trades all the main system of records typically found in a company. These include Customer Relationship Management (CRM), Field Service Management (FSM), Entreprise Resource Planning (ERP) and Human Capital Management (HCM).

Following the traditional vertical SaaS playbook, ServiceTitan has also expanded into financial services by bundling payment processing and consumer financing into its platform. Payment processing enables technicians to accept multiple payment methods, either on-site or via a customer portal, while consumer financing connects end customers with third-party financing options to cover the cost of services.

Part 2 - Metrics Overview

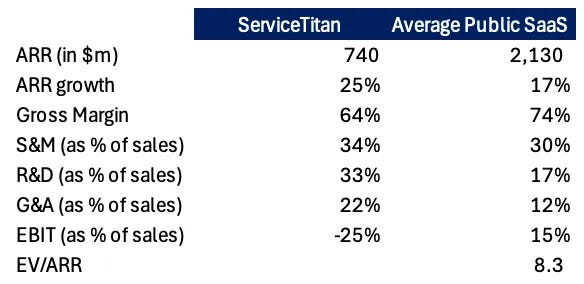

Service Titan is a vertical software platform targeting the mid-market & large companies in the trades industry, in contrast to most of its competitors, such as Jobber or Housecall Pro which focus on serving smaller and long-tail businesses It generates $740m in ARR (growing 25% YoY) from 8k customers ($77k ACV) including 1k customers which are bringing $100k+ in ACV ($308k average) accounting for 50% of revenues.

As a result, ServiceTitan’s customers exhibit strong retention behaviour, with an exceptionally high Gross Dollar Retention (GDR) rate above 95% and a Net Dollar Retention (NDR) rate above 110%. Currently, c.40% of ServiceTitan’s new ARR is generated by its Fintech & Pro modules. ServiceTitan has also a $183k CAC implying a 20.2-month payback on gross margin consistent with expectations for a mid-market and enterprise-focused company.

ServiceTitan holds a 9.5% market share of addressable trade spending in the US and Canada ($62bn of a $650bn market) and captures 1.1% of its customers’ total sales, with a mid-term goal of reaching 2%.

The main weakness of ServiceTitan’s P&L is its poor profitability, leading to an imbalanced growth-to-profitability ratio, achieving only 8.4% on the Rule of 40 (calculated as the sum of ARR growth and EBIT margin). It has made significant efforts to improve profitability, reducing its EBIT margin loss from -61% in Q1-22 to -17% in Q2-24. This underperformance stems from two main factors:

A 64% LTM gross margin, compared to the 74% average for public SaaS companies. This is largely driven by professional services, which are heavily subsidized, resulting in a -112% gross margin on professional services over the past twelve months.

A 22% G&A expense-to-sales ratio, significantly higher than the 12% average for public SaaS companies. This is mainly due to integration costs from ServiceTitan’s recent acquisitions.

Overall, I don’t believe ServiceTitan will command a premium valuation over the public SaaS market. While it has a superior ARR growth rate compared to the market, its unit economics underperform. Assuming ServiceTitan trades at the average public SaaS EV/ARR multiple of 8.3x, its implied valuation would be $6.1bn —significantly below its $9.5bn peak in 2021.

Part 3 - Additional Learnings for Vertical SaaS Founders

As I mentioned, I previously shared in this newsletter 9 initial learnings on the business (i.e. go upmarket, expand your total addressable market as you grow, don’t rush into financial services, build the serial acquirer muscle, build for several stakeholders in your value chain, leverage industry expertise, private equity roll-ups as software adoption drivers, be the premium software in your market and onboard customers with the same cadence and specialisation as when acquiring them). In this section, I’ll cover additional learnings from reading the S1:

Finding the right balance between expanding your total addressable market by entering adjacent categories and going deep within each category. ServiceTitan began in the residential plumbing market but has since significantly expanded, entering multiple trades (such as HVAC, electrical, landscaping and janitorial services) as well as diversifying into various customer segments (residential, commercial, construction). I found fascinating that they’ve done so while keep building specific workflows for each of the trades they are serving.

“The industry consists of a wide array of trades that service different needs of households and businesses. Though each trade has similar operational challenges and business goals, there are often many unique workflows and specifications that require configurations based on the nuances of a particular trade and/or end customer.” - S1

Over-investing in professional services to shorten its sales cycle, ensure high customer retention and position itself well for upselling. ServiceTitan heavily subsidises professional services, spending $2.12 for every dollar charged. Its hands-on onboarding process includes data migration, account set-up and employee training. It significantly impacts its unit economics reducing its gross margin by 4.6 percentage points compared to charging professional services at cost. Despite this, the strategy is a critical success factor for ServiceTitan’s growth, enabling a sales cycle of less than 60 days, a GDR rate above 95% and a NDR rate exceeding 110%.

Hiring industry insiders to enhance sales credibility and inform product development. Similar to Toast, ServiceTitan employs numerous industry experts to bolster its sales efforts and contribute to product improvement.

“We employ industry experts (former employees of customers, industry partners and others) and partner with trade industry organizations to ensure we understand trades businesses and address their needs from product innovation to end-customer success.” - S1

Adding a verticalised marketing product to its all-in-one platform. ServiceTitan has developed a comprehensive marketing suite that includes email marketing, reputation management (prompting end-customers to leave reviews), ads measurement and optimisation, and a audience builder (automatically sending marketing messages to key customer segments). I believe that all vertical SaaS should include a marketing product when they build an all-in-one platform as marketing features have a direct impact on revenues and can be tied to multiple other products to create sticky workflows (e.g. using the marketing product as lead generation engine for a sales platform or using the ops product to prompt end customers to generate reviews in the marketing product).

Obsessing on boosting customers’ top line to to shorten sales cycles and strengthen retention. The median trade using ServiceTitan grows its revenue by 18% YoY and ServiceTitan’s initial product scope was almost entirely focused on generating more sales for trades with a CRM and marketing management tools.

Being uniquely positioned as a vertical SaaS to integrate AI into its platform. ServiceTitan is integrating AI into its platform by embedding AI features into its existing products (e.g. read documents, summarising jobs, demand forecasting) or by creating new AI-native products (Dispatch Pro which is an AI driven dispatching and routing solution optimised for the customer based on its historical data). As an all-in-one platform, ServiceTitan has access both to proprietary data and customers which are key success factors to win in the new AI paradigm.

“We believe ServiceTitan has the three necessary ingredients to truly harness the power of AI to drive value for our customers: (i) massive and growing proprietary data assets, (ii) similar customer profiles with common workflows, (iii) an end to end platform allowing us to put insights into action.” - S1

Leveraging partnerships with trade associations to generate leads and build credibility within a vertical. ServiceTitan collaborated with trade associations to develop playbooks and share best practices with their members. This approach positioned ServiceTitan as a trusted partner within the industry and created a lead generation channel that now accounts for 15-25% of the company’s total leads.

Thanks to Julia (🦒) and Paul for the feedback! Thanks for reading! See you next week for another issue! 👋

A question on the CAC payback period: How does 183k CAC imply a 20.2 CAC payback? If I understand correctly then the calculation is CAC / (ACV - COGS). Hence, 183k / (77k * 0,64) which would yield 3.7 years or 44 months CAC payback. Where am I missing something?

Great recap!

ACV struck me as crazy high for this vertical - the wonders of vSaaS!

For early stage founders/investors it would be super interesting to learn how ACV has grown over time. Unit economics are not their greatest strength at scale - I bet they required real faith in the plan along the way. Crazy that they pulled it off!