Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m exploring the idea of building a modern version of Constellation Software.

In a previous edition of this newsletter, I covered the most successful vertical market software conglomerate called Constellation Software (CSU). In this edition, I want to explore the idea of building a modern version of CSU.

I don’t think it’s worth trying to build a pure copycat for 3 main reasons:

The world has changed since CSU’s inception in 1995.

A newcomer will never be able to compete directly with CSU’s acquisition flywheel based on decentralisation, a low-cost of capital and on expertise in vertical software markets.

When CSU started, it was operating in a greenfield market, which had no competitors when it tried to acquire companies. Since then, it acquired 800+ companies and has built privileged relationships with 50k+ companies in its CRM. It means that (i) the inventory of great targets in North America and Europe has decreased and that (ii) any other company would start with a disadvantage as many targets already have a close relationship with CSU.

Nonetheless, it’s interesting to look at some parameters that have changed since 1995 and how a new player could counter-position CSU.

The World has Changed

On the one hand, many tech paradigm shifts have happened in the past two decades.

The shift to the cloud: most companies acquired by CSU are on-premise products monetised with an upfront fee and a recurring maintenance licence when most software are now cloud based and monetised via a SaaS subscription. Moreover, the transition to the cloud makes software products more interoperable with open ecosystems and APIs.

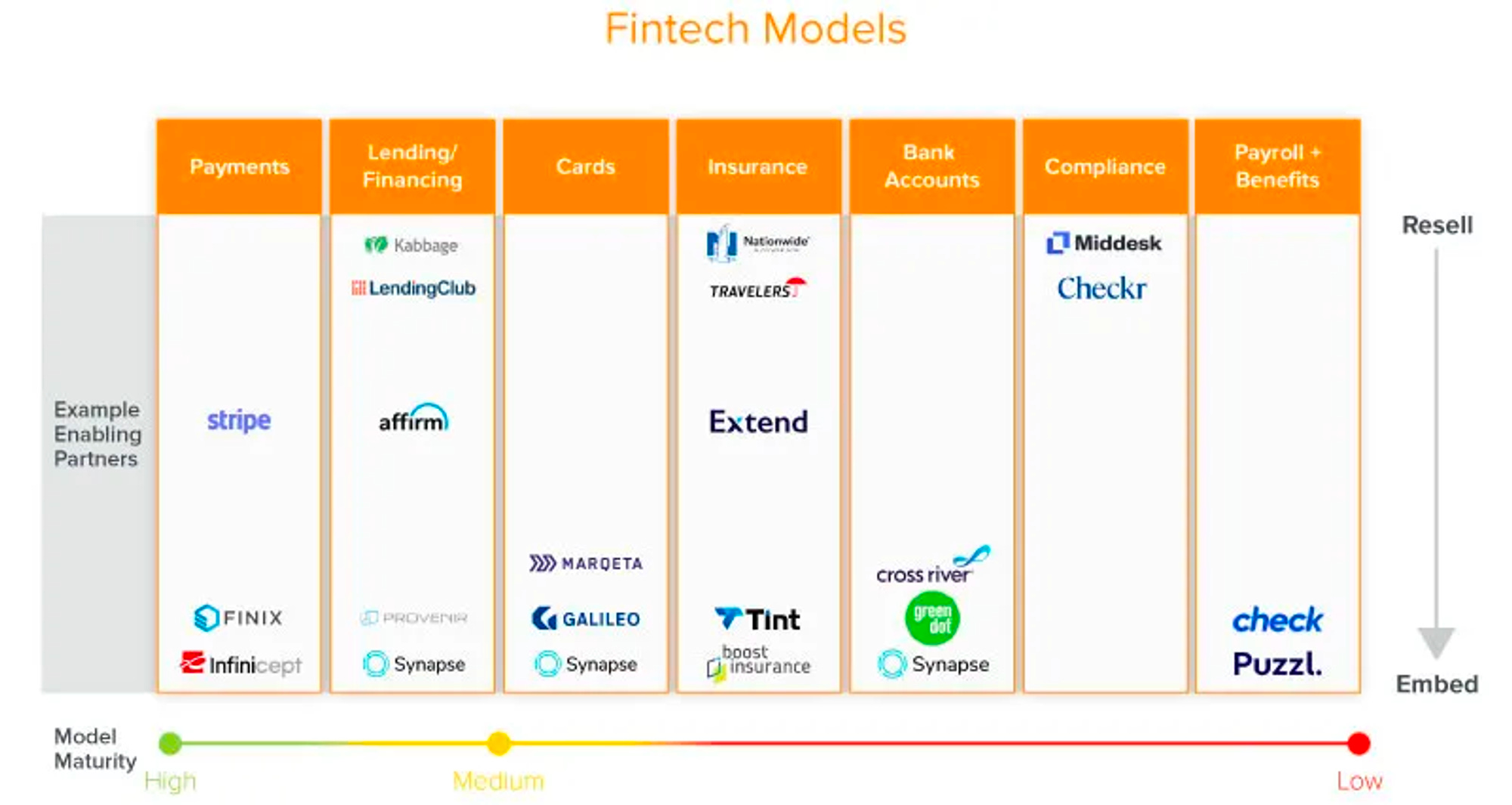

The emergence of embedded finance: it’s now possible to embed financial services into vertical market software: payments can be a first step before expanding into other services like lending, insurance or payroll.

The generative AI revolution: there is a strong potential to integrate AI into vertical market software in order to launch complementary products to generate upsell or to drastically cut costs by automating key processes (e.g. in sales and customer success).

On the other hand, there is a new generation of business owners and operators which have come on the labour market. I’m part of this generation and I can tell you that working or selling a company to CSU is not attractive - at all.

For young operators: on paper, CSU has appealing roles like working in an acquisition teams or contributing to the operation of a vertical software with high autonomy. In reality, CSU is too old school to be attractive. With a model like CSU, there is room to create the best place to start a career for people who tend to go into consulting, banking or to join a startup - a mix of McKinsey, Goldman Sachs and Rocket Internet.

For young business owners: the shift to the cloud has decreased the barrier to entry to start a company, empowering a new generation of entrepreneurs to start great internet bootstrapped businesses with lean teams, SaaS business models, low-sales efforts and a focus on growth. CSU is too price sensitive to acquire these businesses and as a consequence to attract these talents.

For individuals working on their own as freelancers or as indie businessman: if traditional corporations are not appealing for younger generations, my belief is that many individuals will also be fed up with working on their own and will be willing to work with like-minded folks in structures like collectives giving them a good balance between freedom, security and human bonding. This is a value proposition that a modern CSU can serve.

It’s Possible to Build a Vertical Software Market Conglomerate on Other Premises than the Ones Used by Constellation Software

If I had to start a modern CSU tomorrow, I would build a conglomerate with several industry-specific platforms in which products are interoperable per industry and in which you can embed financial services. This conglomerate would retain certain key ingredients in CSU’s model and would counterposition others.

On one hand, I would keep (i) the single focus on vertical market software, (ii) the structure with operating groups specialised in certain verticals, (iii) the acquisition and integration expertise, (iv) cultural specificities like being data-driven, giving strong ownership to employees and having great financial incentives for everyone working in the organisation.

On the other hand, I would counterposition three ingredients in CSU’s model. I would:

Focus on growth over profitability. I would only buy modern softwares (cloud based, SaaS as business model, open to third party applications) which have a better balance between growth and profitability when CSU is too price sensitive to buy businesses with an annual growth rate above 10%.

Focus on quality over quantity. I would not buy as many companies as possible as long as they meet my hurdle rate but I would only buy prime assets that make sense to build an all-in-one solution in certain verticals.

Focus on building synergies over decentralisation. I would try to create vertical all-in-one solutions. I would have an internal product team focused on (i) making acquired solutions in one vertical interoperable, (ii) building complementary products to the acquired products and (iii) embedding financial services into these all-in-one solutions. CSU is compounding because it has a decentralised acquisition and operation model. A modern CSU would compound because you’re able to have a strong Net Dollar Retention rate (NDR) thanks to the assembly of vertical all in-one solutions.

I believe that a stronger focus on growth and modern software make the model much more appealing for younger generations both when you’re looking at sellers and at operators. I believe that building synergies allow the model to have uncapped upside and a growth trajectory that is more exponential than linear.

If you have been thinking about how to build a modern CSU, I’d love to have your feedback. It’s a first iteration. It’s obvious that I have blind spots and that there are things that I can improve on. I’d love to sharpen my conception of what a modern version of CSU could look like with your ideas.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Hi Alexandre! Sharp and interesting piece as always.

2 areas of debate for me:

- "the inventory of great targets in North America and Europe has decreased": why in your opinion? I'd say that the share of tech in the GDP is growing, and there is a creative destruction process at play in the industry, hence in the end great targets are minted regularly (even for models that are not part of the VC model)

- "growth over profitability" + "quality over quantity" + "synergies over decentralization" = isn't the answer a growth PE fund with a build-up strategy in vertical SaaS? Not sure you need to keep your companies forever to benefit from a data feedback loop.