✨ Constellation Software - Rolling Up Vertical Market Software

Overlooked #140

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing what I think are the 3 key ingredients behind the success of Constellation Software.

Constellation Software (CSU) is a great success story. It’s a Canadian-based roll-up of Vertical Market Software (VMS). It started in 1995. It went public in 2006. It has a $40bn enterprise value. It made c.800 acquisitions in 100+ verticals. In 2021, it generated $5.1bn in revenues (29% YoY growth) and $1.1bn in EBITDA (22% margin).

CSU’s success is based on 3 ingredients:

A decentralised, meritocratic, data-driven and long-term oriented culture,

A scalable and disciplined M&A machine,

Acquiring VMS which are businesses with strong fundamentals.

A Decentralised, Meritocratic, Data-Driven and Long-Term Oriented Culture

Decentralised: CSU is structured in Operating Groups (OGs) which are holdings operating in multiple geographies/verticals and composed of dozens of Business Units (BUs). Every acquisition becomes a BU. Each BU is run autonomously by a manager who has latitude on the strategy and ownership on his P&L. There is no integration with other BUs. Moreover, BUs and OGs have autonomy to make new acquisitions as long as they hit CSU’s hurdle rate and are below a certain size (above which you need an approval from the HQ). Each BU can have its own sub-culture as long as it fits with CSU’s general culture principles described in this section. For its BUs, CSU provides mentorship, access to best practices to operate a VMS and access to VMS data benchmarks.

“When we buy a good company, we identify and address the reasons they have not yet become an Exceptional company. To this end, we offer coaching and resources in a number of areas including establishing values and capital allocation processes, profit-sharing programs, benchmarking against our other businesses, the chance to share best practices with other CSI companies, formal management training and ongoing mentoring.” - CSU’s website

Meritocratic: CSU pays its employees well and incentivises them in the long term with stock options plans. It removes as much bureaucracy as possible (useless processes & middle management). It offers great career-tracks for both “craftsmen” (who want to master the craft of operating a unique vertical solution) and “compounders” (who want to learn about other verticals and who want to participate more actively in M&A).

“My motivation is to help create a company where worthy people succeed. Whether they join us with an acquisition or are hired from the outside, I want to support and encourage employees who work hard, treat others well, continuously learn, and share best practices. I try to make sure that sycophants, spin-doctors, and mercenaries don’t survive in Constellation’s senior ranks. Harder, but not impossible, is helping identify and remove hidebound managers who rely upon habit and folklore to run their businesses rather than rational enquiry and experimentation. Constellation is as close to a meritocracy as I have experienced.” - Mark Leonard (2017 Letter to Shareholders)

Data-driven: CSU operates 800+ VMS and has a database of 40k VMS targets. As a result, it has a unique data advantage which can be leveraged to make more successful acquisitions and to operate VMS more efficiently compared to other players.

“We use a disciplined set of key operating ratios and metrics to monitor and manage the performance of each of our VMS businesses. These ratios and metrics are compared to a series of benchmarks which we have developed. This allows us to assess how each VMS business is performing in order to pursue optimal financial returns and capital allocation.” - IPO Prospectus

Long-term oriented: CSU owns VMS in perpetuity. It’s not a PE firm acquiring a business to resell it 3-5 years later. It optimises to win in the long-term.

“We encourage our managers to launch initiatives, which in our industry, often require 5 to 10 years to generate payback. We are comfortable providing them with capital to purchase businesses that won't be immediately accretive, but that have the potential to be long-term franchises for CSI.“ - Mark Leonard (2011 Letter to Shareholders)

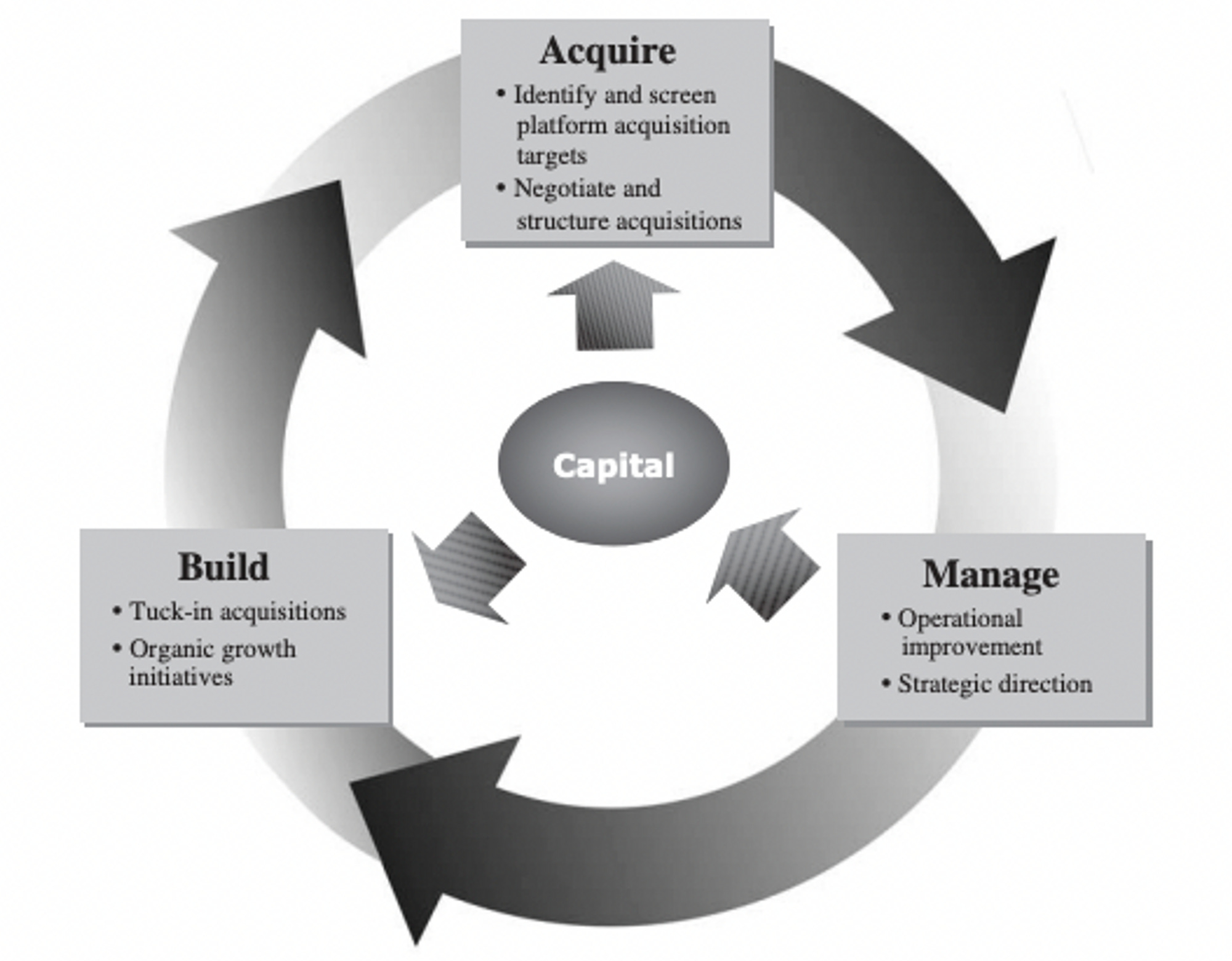

A Scalable and Disciplined M&A Machine

“Constellation is an acquirer of vertical market software companies that provide mission critical solutions to the customers that utilize our software. We manage, build and grow these businesses and never sell. Our goal is to generate a rate of return on each of these investments at or above our hurdle rates.” - Jamal Baksh (Constellation Software’s CFO)

CSU acquires and operates VMS in perpetuity. It uses the cash generated by its portfolio of VMS to fund new acquisitions.

CSU looks for acquisitions that can generate a return above its internal hurdle rate (above 20% for small acquisitions). Ideally, CSU wants to acquire founders led businesses because these have a better fit with CSU’s culture favouring long term orientation and autonomy. Besides, CSU looks for businesses with the following characteristics: (i) revenues above $5m and EBIT above $1m, (ii) rule of 40 (EBITDA margin + annual growth > 40%) above 20%, (iii) category leadership (n°1 or n°2 market share holder), (iv) low competition, (v) fragmented customer base.

“Our favourite and most frequent acquisitions are the businesses that we buy from founders. When a founder invests the better part of a lifetime building a business, a long term orientation tends to permeate all aspects of the enterprise: employee selection and development, establishing and building symbiotic customer relationships, and evolving sophisticated product suites.”

As we saw in the previous section, M&A is (i) decentralised with BUs and OGs in charge of finding targets and acquiring them and (ii) data-driven based on proprietary benchmarks to avoid making emotion M&A decisions.

CSU has successfully scaled its M&A machine. Its core model is to make many small acquisitions (below $5m) at a cheap price (below 1x EV/Sales). Since 2005, CSU made over 780 acquisitions deploying $6.6bn in capital. CSU managed to scale annual acquisition pace from 12 deals to deploy $29m in 2005 to 134 deals to deploy $1.7bn. In recent years, CSU struggled to reinvest its operating cash flows into new acquisitions. It started to explore and execute on adjacent strategies: (i) acquiring larger assets at a lower hurdle rate, (ii) spinning-off OGs into individual companies with more leeway to scale, (iii) launching a venture fund to find additional levers to boost organic growth, (iv) exploring other opportunities beyond vertical market software in which they could execute a roll-up play.

VMS are Businesses with Strong Fundamentals

“Our objective is to be a great perpetual owner of VMS businesses. We like VMS businesses because they are asset-light, have robust moats, and attract the sort of managers and employees with whom we enjoy working.” - Mark Leonard (2017 Letter to Shareholders)

VMS are great businesses because they combine several fundamentals:

Mission-critical: CSU acquires VMS which are industry systems of records. Customers depends on CSU’s BUs to run their business on a daily basis. As a result, CSU has a high usage rate and a high retention rate (95% annual retention rate which is stellar for a customer base mainly composed of SMBs).

Low competition: CSU’s VMS operate in non-competitive markets (competing with horizontal solutions not suited for the vertical, with pen & paper and with in-house cumbersome tooling) in which they have market leadership.

Capital efficient: industry focus gives VMS unfair unit economics (e.g. lower CAC and lower churn rate) which enable them to have a great growth/profitability balance early on in their journey.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋