🗞 Venture Chronicles - June 2020

Overlooked #27

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful news of June.

For 2020, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for June!

Please note that the date picked for each event is not always the exact date of the event but the date I decided to write about the event.

Monday, June 1st: a16z has started to release the recording of its Crypto Startup School classes. If you want to get into crypto, it’s a great introduction far from the boring SEO-optimized articles teaching you what is Bitcoin and why all the industries will be disrupted by the blockchain technology. For instance, Ali Yahya did an amazing session on the defensibility of business models in the crypto-industry. He is explaining that cryptonetworks are multisided platforms that are building defensibility thanks to same-side and cross-side network effects with the interactions between all the stakeholders in the network (e.g. infra graph for layer 1 network effects). (a16z)

Tuesday, June 2nd: Zynga acquired Istanbul-based mobile gaming startup Peak for $1.8bn. This is an outstanding exit in the middle of the covid crisis for the European gaming industry and for Earlybird which owned an unusually high 30% stake into the company ($520m exit value for the fund). Peak was initially developing games for the Arab world before releasing two international successes with Toy Blast and Toon Blast. It generated $600m in sales in 2019. Tencent was also in line to acquire the company. To win big money in venture, not only do you have to be right but you have to be right against the consensus. Betting on casual mobile gaming is contrarian. Owning 30% of a company as a venture investor is contrarian. Congrats to Earlybird! (Hendelsblatt, Hummingbird)

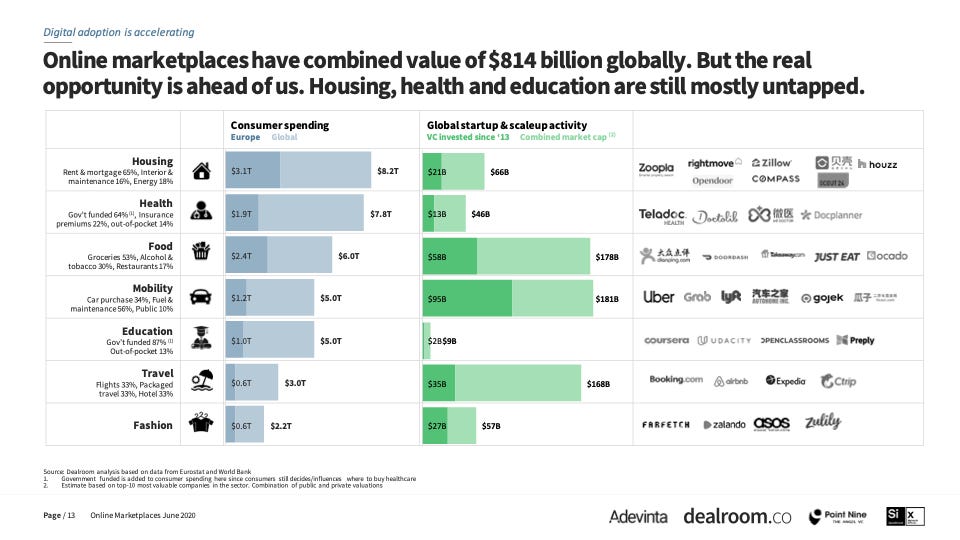

Wednesday, Jun. 3rd: Dealroom released an exciting report on marketplaces in partnership with Speedinvest, Point Nine and Adevinta. Marketplaces are playing an increasing role in our consumer lives and covid has accelerated their adoption. The report is giving good indications on what's next for marketplaces.

Some of the biggest consumer spending areas remain untapped by venture capital like housing, healthcare and education.

Three key categories have to be disrupted by marketplaces: regulated services, sustainability and future of work.

Thursday, Jun. 4th: Zoom reported its Q1 with $328m in sales (169% growth compared to last year) proving that it had been able to convert a good stake of its user growth into paying customers. Ben Thomson is right. It's just unbelievable that Zoom has been able to ramp up its capacities to support such growth in usage. I have been using Zoom on a daily basis for the last 6 months and I have never had a lagging issue (except for Zoom recordings). The rise of cloud providers like AWS, Google Cloud and Microsoft Azure is a true revolution in the software world and it's still clearly overlooked. (Stratecherry)

Friday, Jun. 5th: Following a sharp decline in revenues due to the covid crisis, The Family downsized its operations by (i) laying off part of its team (reduced from 24 to 12 people) and (ii) going full remote closing its offices in London, Berlin and Paris. It must have been hard months for the team but I'm sure that they will get out of this crisis stronger than ever. Going remote implies that they can now hunt startups from all around the world and focus on what they are the best at: provide education to companies in The Family. (🇫🇷 Maddyness, Tech.eu)

Saturday, June 6th: Christoph Janz (Point Nine) looked at Crunchbase figures to measure the covid impact on venture capital funding in April and May 2020. Figures must be taken cautiously because Crunchbase data is not always super clean and there is a lagging effect. (Christoph Janz)

Compared to last year, early stages rounds (pre-seed, seed, series A and series B) are down both in terms of volume and quantity but median deal size are increasing

SaaS seems to be less affected than other business models. Pre-seed and seed SaaS financing has even doubled in May 2020 compared with May 2019.

Sunday, Jun. 7th: Fabrice Grinda wrote a paper on FJ Labs genesis. FJ Labs is an hybrid structure composed of both a venture fund and a startup studio. With Thibault Elzière and Xavier Niel, Fabrice is probably one of the most active and successful French business angels. Fabrice started to invest a long time ago as an angel while he was running OLX. He started FJ Labs in Jan. 2016 with a $225m fund raised from external investors (inc. $50m from Telenor) on top of his personal capital. As of Apr. 2020, FJ Labs invested $284m into 571 companies. It had 193 exits at a 62% IRR - which is… outstanding. (Fabrice Grinda)

Monday, Jun 8th: Lemonade filled to go public. Lemonade was founded in 2015 and raised €430m+ with investors like Sequoia, General Catalyst, Aleph, Allianz X and Softbank pre-IPO. (S1, Rob Moffat)

Tuesday, Jun. 9th: a16z invested into a second European entertainment startup in less than 6 months. After Mainframe (cloud based multiplayer game), the SV-based fund added Whatifi to its portfolio leading a $10m series A. It's a video-based mobile app in which you are playing interactive stories (similar to BlackMirror's Bandersnatch episode) with your friends. (Engadget, Andrew Chen)

Wednesday, Jun. 10th: EQT opened an office in Paris. The fund has strong ambitions for the French market having recruited or promoted French professionals to senior roles in several business units (buy-out, infrastructure, venture and real estate). 10 investment professionals will be working in Paris. EQT is looking to have a local presence in all the market the fund invests into, and has replicated this strategy in both Europe and Asia. EQT had already done 7 investments in France including Saur with its infrastructure fund as well as CallDesk and Tinyclues with its venture fund. EQT Ventures has also announced the arrival of Rania Belkahia (former Afrimarket founder) as partner to lead the French coverage. I wrote an extensive deep dive on EQT that you can find here. (EQT Ventures)

Thursday, Jun. 11th: Kahoot! raised $28m at a $1.4bn valuation with Northzone and Kahoot!’s CEO. A $62m secondary sale was also announced at the same time. The company was founded in 2013 and is a user generated educational gaming platform. 50% K-12 students are using Kahoot! in 200 countries and it will generate between $32m and $38m in revenues for 2020. The company will IPO in 2021. (Techcrunch)

Friday, Jun. 12th: Robinhood retail investors are investing into bankrupted company Hertz as if they were playing with a slot machine in a casino. Short-term car rental company Hertz filed for bankruptcy at the end of May - implying a restructuration procedure that will probably wipe out most of the equity of the company. The first trading day following the announcement, the stock price closed to $0.56 reflecting the high-risk of equity wipe out. Then something unexpected happened. In the next two weeks, the stock price rose up to $5.53 following high but irrational demand from retail investors. Hertz even tried to raise capital to strengthen its position during its bankruptcy process waving on this spike in demand. Investing is not supposed to be gambling and I'm afraid of the rise in trading apps like Robinhood that does not put sufficient UX and education efforts into their product to make sure that investors are aware of the risks of trading extremely risky assets even if trading democratisation is a huge consumer finance innovation. (Alex Danco, Matt Levine, CNN)

Saturday, Jun. 13th: Lenny Rachitsky published a presentation sharing his learnings on launching a paying weekly newsletter on product and growth topics. (Lenny)

Metrics: 15k free subscribers, 500 paid subscribers, free version launched 12m ago, paid version launched 2m ago, $65k revenues p.y. before fees.

Valuable pieces of advice: (i) mix regular posts with epic posts, (ii) write guest posts where your audience is, (iii) leverage influencers, (iv) if you switch to a paid plan, you must get the launch right

Sunday, Jun. 14th: I watched Snap Partner Summit. So many French companies are working within the Snap ecosystem (including Voodoo, HomaGames, Yuka, Yubo, Yolo, etc.). (Snapchat, 🇫🇷 Le Panier). Here are my three favorite announcements:

Local Lenses which "enable a persistent, shared AR world built right on top of your neighborhood"(e.g. paint together with your friends the building in front of you).

Camera Kit added to the Snap Kit to let 3P applications use Snap's AR camera (e.g. Snap lenses x Squad or Triller or… Yubo 🤫)

Snap Minis which are micro-apps developed by third parties and integrated into Snap chat (e.g. mini-relaxation with friends on Headspace, compare your class schedules on Saturn). Snap is getting one step closer to Asian super apps.

Monday, Jun. 15th: FirstMark disclosed two new investment funds: a $380m early-stage fund (FirstMark IV) focused on seed and series A and a $270m opportunity fund (FirstMark Opportunity III) to double down in portfolio companies and to make growth investments. FirstMark is one of the most active US investor in France with investments in companies like Dashlane, Ledger, Dataiku, Sketchfab. (Techcrunch)

Tuesday, Jun. 16th: The European Commission opened an antitrust investigation against Apple practices within the AppStore which takes a generous 30% cut on every mobile application transactions. It's problematic because Apple does it on services (music, movies and e-books) for which it has its own offer. Spotify and Rakuten are leading the war against Apple. It would not be irrelevant to have Apple forced to lower its cut rate down to 1-2% -something similar to other payment systems like Stripe or Adyen. (The Verge)

Wednesday, Jun. 17th: Berlin-based headless CMS startup Contenful raised a $80m series E at a valuation close to $1bn led by Sapphire Ventures with the participation of General Catalyst and Salesforce Ventures. Contentful has 2.2k paying customers including 22% of the Fortune 500. It's an impressive European SaaS success story founded and seeded by Balderton and Point Nine in 2013 followed by a series B with US investor Benchmark in 2016. (Techcrunch)

Thursday, Jun. 18th: Bellman raised $4.5m for its property management system in a seed extension led by Lakestar with the participation of existing investors Connect Ventures and Financière Saint James. Bellman is working with 100 buildings representing 2.5k customers. Watch out for this space in France. Matera also raised a series A with Index. Bellman and Matera have both outstanding teams and there are huge pain points to be solved in property management. (Techcrunch, Pietro Bezza, Clément Parramon)

Friday, Jun. 19th: Kaia Health is raising a $26m series B led by Optum, Idinvest (💙) and Capital300. Kaia is a digital therapeutics startup with 400k users which is using computer vision in a mobile application to help people suffering back pains to do physiotherapy exercices on their own. (Techcrunch)

Saturday, Jun. 20th: I listened an insightful 30-min interview on France Culture with Malcom Gladwell. He discussed his last book (Talking to Strangers) but also the future of media. For instance, he explained that the media industry is starting to get decentralized at a fast pace (with both professional journalists like him leaving media corporations to build their own media as well as citizens starting their own media) and that we are far away from measuring all the consequences of this shift. My girlfriend is Malcolm Gladwell’s biggest fan and we cannot recommend enough his podcast Revisionist History, which inspired this newsletter’s name. (🇫🇷 France Culture)

Sunday, Jun. 21th: Sarah Tavel has published three posts to detail the three levels to build a successful marketplace. The overall thesis is to say that you should start slow be creating the perfect experience for both sellers and buyers before growing fast until the market tips in your direction. Once you have a good market positioning, don't rest and go for a total market domination. (Part I, Part II, Part III)

Level 1: kickstart the marketplace by creating experience for both side of the marketplace that is significantly better than on any other substitute. You should now start by focusing on growing your GMV.

Level 2: tip the marketplace in your direction by identifying and maximising growth and happiness tipping loops. The market will tip when network effects start to kick in and it gets easier to grow the marketplace.

Level 3: dominate your market by becoming the indisputable market leader across all categories and all geographies.

Monday, Jun. 22th: Swile raised a €70m series led by Index (doubling down after leading the series B) with the participation of Bpifrance Large Venture and Idinvest (💙). 210k people in France are using Swile in 8k companies. Swile started as a booking mobile app for teams to book takeout lunches with discounts. Then it evolved to take down the French meal voucher cartel (Sodexo, Edenred, Up and Natixis Intertitres). Swile is now going after all employee benefits (gift card, transportation subscription etc.) and is expanding outside France (Brazil this year, other European countries next year). (Techcrunch, Funding Crush 🇫🇷 )

Tuesday, Jun. 23th: Memo Bank (ex. Margo Bank) raised a $22.5m series led by Blackfin with the participation of existing investors Daphni and Bpifrance. Founded by Jean-Daniel Guyot, Memo Bank is a bank with a proper credit institution agreement targeting SMBs (10+ FTEs and €2m+ sales). Memo Bank spent 2 years building a full core banking system and obtaining the right banking agreement. (Techcrunch)

Wednesday, Jun. 24th: Jumbo raised a series $8m led by Balderton. It's a B2C mobile app to manage your privacy and data on the internet launched by Sunrise Calendar (sold to Microsoft) founder Pierre Valade who is well known for being a top product-oriented founder. Monetizing consumer privacy services will be hard but I'm convinced that we are moving into this direction. My personal opinion is that privacy is a human right that should be enforced by every democracy and States should even subsidize solutions like Jumbo. (Bernard Liautaud, NextView, Tech.eu)

I'm super excited about these three companies (Swile, Memo Bank and Jumbo). It's the best proof of the growing maturity of the French ecosystem. Loic Soubeyrand (Teads sold to Altice for $307m in Mar. 2017), Jean-Daniel Guyot (Captain Train CEO sold to Trainline for $189m in Mar. 2016) and Pierre Valade (Sunrise Calendar sold to Microsoft for $100m in Feb. 2015) are three successful repeat entrepreneurs. They did not need to start a new business to get rich or become well known in France. Yet, the three of them decided that they wanted to build a new bigger project tackling super complex topics (meal vouchers, banking, privacy) and applying the learnings from their previous experience (e.g. taking all the time needed to build a top notch product before scaling).

Thursday, Jun. 25th: Checkout raised a $150m series B at a $5.5bn valuation led by Coatue. Insight, DST and GIC are also investing. Checkout was created in 2012 and has been profitable since year 1. It's an API-based platform to help merchants to build checkout solutions (multiple forms of payments accepted, 150 currencies, fraud protection, analytics) competing directly with players like Adyen, Square and Stripe. It reported a 250% increase in the number of transactions in the past 12 months. (Techcrunch)

Friday, Jun. 26th: Hopin raised an unusual $40m series A led by US growth fund IVP together with new entrants Salesforce and Slack venture arms as well as existing investors Accel, Northzone and Seedcamp. Hopin is a platform you can use to organize virtual events. The company was founded in 2019. It was already super hyped before covid announcing a seed round in early 2020 and must have experienced a skyrocketed growth since then. 175k people attended an Hopin event in May vs. 16k in March. Run the Wolrd (a16z and Founders Fund backed) is building a similar product in the US and is experiencing a similar growth trajectory. (Techcrunch, Ben Evans)

Saturday, Jun. 27th: I watched Apple 2020 WWDC. (Apple) Here are my personal highlights:

Mac hardware and software integration is pushed one step further with Apple replacing Intel with its proprietary chip (Apple already used to do this in the past).

A brand positioning at the crossroad of (i) privacy (on the edge ML, Apple sign in, Safari privacy features), (ii) healthcare (Apple Watch) and (iii) sustainability (Iphone with recycling components).

Apple is releasing AppClips on iOS which are flash applications (e.g. booking a Uber without downloading the app). Like Snap minis, these are the future of mobile applications and are the Western tentatives of Asian super apps. Easier discoverability, no friction, integrated into a larger platform, no account creation, embedded payment, activation through camera. It will become the norm for most of our use cases in which the app does not provide sufficient value (food delivery, ride-hailing, electric scooter, e-commerce, restaurant booking etc.)

Sunday, Jun. 28th: George Henry (Localglobe) is putting the right words to describe an emerging pattern in startups targeting SMBs (e.g. Rekki). 1/ Startups starts to develop a productivity tool dedicated to employees (restaurant chefs booking food orders). 2/ The productivity tool user base is growing thanks to its virality within and outside the organization (employees, other restaurants). 3/ Startups monetize this user base using the network effects generated (building a marketplace between restaurants and suppliers). (George Henry)

Monday, Jun. 29th: UK-based seed fund Connect Venutres raised a $80m third fund to invest in “product-led” founders all over Europe. Connect started in 2012 and was one of the first European seed funds doing high conviction seed rounds with relatively large tickets in a limited number of companies per year. Past investments include: Citymapper, Typeform, Truelayer, Lifebit, Side, Forest, Bellman, Emma. There is an ongoing love story between Connect and The Family as the four last deals I have just mentioned worked with the Paris-based structure.

Tuesday, Jun. 30th: France Invest published its annual report on French private equity performances. In France, venture capital has awful financial performances with a 3.1% IRR and a 1.21x multiple (all time and all the performances are not realized because it includes participations that are not exited). (🇫🇷 France Invest 🇫🇷 Christophe Raynaud)

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋