💰 EQT - The Nordic Private Equity Baron

Overlooked #25

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m talking about EQT which is a Nordic private equity house with €40bn of asset under management and investment activities into numerous assets classes (buyouts, private debt, infrastructure, real estate, venture capital etc.).

Last week, EQT opened its office in Paris. The fund has strong ambitions for the French market having recruited or promoted French professionals to senior roles in several business units (buy-out, infrastructure, venture and real estate). EQT is replicating in France its strategy to have a local presence in the markets the fund invests into.

10 investment professionals will be working in Paris.

EQT has already invested into 7 French companies including Saur with its infrastructure fund as well as CallDesk and Tinyclues with its venture fund.

EQT Ventures has also announced the arrival of Rania Belkahia (former Afrimarket founder) as partner to lead the French coverage.

I thought it was good excuse to dig into EQT and explain you why EQT is my favorite multi-products European Private Equity (PE) house. In this paper, (i) I set the stage of the current PE market, (ii) I discuss the rise of EQT as a top tier private equity house, and (iii) I talk about EQT Ventures great debuts since its creation in 2016.

In this section, I’m referring to Bain 2020 Private Equity Report. It’s a must read if you are interested into private markets. I’m just summarizing the key elements to understand the current PE environment in which EQT is evolving.

1/ The PE market was in a bull phase before the crisis

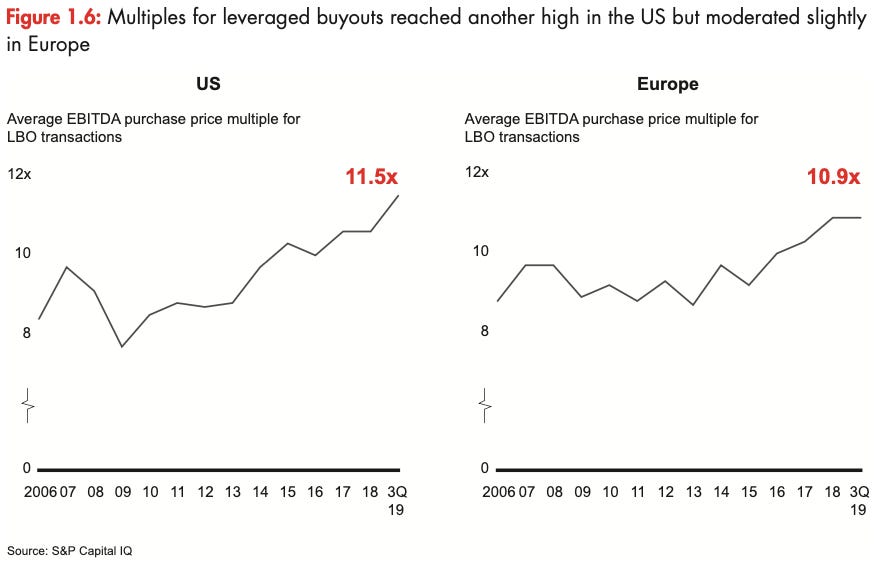

Asset prices were at an all time high in the US and close to an all time high in Europe. The average EV/EBITDA multiple for a leveraged buyout reached 11.5x in the US and 10.9x in Europe.

Buyout deals were heavily leveraged with more than 75% of deals levered at more than 6x Net Debt / EBITDA (vs. less the 25% during the global financial crisis).

Average holding periods were decreasing dramatically to avoid the risk of selling during a downturn. The median holding period across all exits fall to 4.3y in 2019 vs. 6.0y in 2014.

2/ There is more dry powder than ever in PE

There is $2.5tn of uncalled capital in private markets i.e. funds that have been raised by GPs but have not been invested yet. It means that GPs have funds that they will need to deploy in the coming 3-5 years - despite a potential long lasting downturn.

3/ There are two main winning strategies in PE: single product or multiproducts

Being extremely successful in deploying a focused investment strategy (one asset class, one sector, one geography). You raise funds easily because you have a differentiated brand delivering strong returns to LPs on a specific investment strategy. For instance, Benchmark is extremely successful while being exclusively focused on venture capital early stage investment. Pantera has outstanding returns because of its specialization into crypto. Same for Triton with distressed assets or PAI with large cap European buyouts.

Becoming a multi-product private equity house able to fulfill all LPs investment needs in the PE market. You raise funds easily because you are able to deploy large LPs investment tickets in your different investment strategies. Some LPs have billions to deploy. They don't want to lose time finding GPs on all the investment strategies they are interested into to build a diversified portfolio. In the end, PE could also be considered as a customer driven business. You can be successful by tailoring your offer to your LPs needs. KKR, Blackstone, Blackrock are in this category. EQT too. The top 20 fund managers have increased their stake in the total capital raised in private market from 26% in 2016 to 36% in 2018 - meaning that their is a strong premium to be a large multi-products fund.

When you are in the middle of these two strategies, it's hard to thrive. You will be struggling to raise funds from LPs, to win deals, to recruit talents etc.

4/ With the current crisis, it's time to shine for private equity asset classes

Private markets are sought by investors because they produce uncorrelated returns from public markets.

Some asset classes like buyouts are also supposed to produce higher returns than public markets. This key thesis has been challenged over the past few years. For instance, returns of private and public equity have started to converge in the US and the 10y net IRR of the S&P 500 PME is even superior to buyout funds.

During economic crises, the gap between private and public returns has historically increased legitimating the investors appeal into private markets. Let's see if it will be the case again with the current crisis.

1/ EQT is the 2nd largest European PE Fund after CVC

We mentioned that fundraising is becoming more concentrated in the hands of the top PE firms and that EQT is one of them. Every year, PEI is ranking the world largest PE firms based on the capital raised in the past 5 years. EQT is the 7th largest global fund and the 2nd European one.

2/ EQT is an outstanding success story in the European PE market

EQT started as a small leverage buyout fund in Northern Europe but has been successful in expanding in other geographies (Europe and US) and in launching and scaling other investment strategies like Real Estate, Venture Capital or Credit.

EQT has now €40bn asset under management and has raised more than €62bn since its inception.

EQT has delivered strong and consistent financial returns with a 19% net IRR (post carried interest, management fees and costs) and 2.4x gross MOIC (pre carried, management fees and costs). A special mention for their real asset investment strategy which has delivered a 18% net IRR which is quite remarkable for this asset class and has allowed EQT to raise €9.1bn for EQT Infrastructure IV in only six months.

3/ EQT today in terms of business lines and geographical footprint

3 business segments: (i) Private Capital (Private Equity, Mid Market Asia, Public Value, Venture), (ii) Real Assets (Infrastructure, Real Estate) and (iii) Credit. Private Equity and Infrastructure are EQT’s flagship investment strategies.

19 offices worldwide in Europe, Asia and in the US

4/ What are EQT key differentiators?

EQT is a well-oiled machine to raise funds from LPs.

In the past few years, EQT has put a strong emphasis in increasing the fund size of its different investment strategies (+100% for its last infra fund, +151% for its direct lending fund and +71% for its PE fund).

EQT knows how to up-sell and cross-sell investment products to its LPs: 17 of the largest investors into EQT funds have invested into 2-3 investment strategies and the average AUM per investor has increased from €40m in 2009 to €80m in 2019.

EQT has also a great retention rate on its LPs base with 85% investors in EQT Infra Fund III coming back to invest in EQT Infra Fund IV.

LPs are coming from everywhere in the world and EQT has been able to attract pension funds - two rare characteristics in the European PE market. EQT has 470 LPs (vs 250 in 2009): 73% of funds raised are coming from outside the Nordic region (vs. 51% in 2009), 35% funds raised are from pension funds (30% from financial institutions, 13% from sovereign wealth funds, 11% from fund of funds and 10% from foundations & family offices)

In the end, EQT has two revenue streams that are complementary and exciting from a shareholder perspective. On the one hand, you have recurring and predictable revenues from management fees. On the other hand, you have an uncapped upside from the carried interest which is dependent from the performance of the different investment strategies.

EQT is geographically present in the local markets it invests adopting a "local with locals" approach. EQT believes that you need to spend time on the ground to source the best opportunities, to win the best deals, to avoid competitive auctions, to build a local network and to support your portfolio companies.

EQT's transformation playbook is centered around digitalization and sustainability which are two century trends that are reshaping mature economies.

EQT has a strong employee culture. For instance, before joining EQT, every new hire has to spend 12 months in an onboarding program to learn the ropes and the culture of the firm.

EQT is implementing a world-class governance model in the company it invests into. This "Troika" core governance model in which the management will be heavily supported by the Chairperson who will be an EQT advisor with a relevant industry background, the portfolio company CEO and the EQT private equity partner.

EQT has an operating platform with in-house experts (100 people in specialist teams and 60 in a digital team) paid to bring expertise to support portfolio companies.

5/ EQT did a successful IPO in Sep. 2019.

At the first sight, it's always bizarre to have a private equity house trading publicly. What does it mean? In the case of EQT, you are owning shares of the general partnership. You are shareholder in a company earning management fees and carried interest (same structure as Blackstone, KRR, Carlyle, Silver Lake).

But for other private equity houses trading publicly, you could be shareholder in the PE holding which owns stakes in all the underlying portfolio companies or shareholder in a Limited Partner holding.

6/ What was the rationale behind the IPO?

With the IPO, EQT raised $500m in primary shares and allowed existing investors to cash out part of their shares for a total of 20% of the shareholding structure. There were several reasons justifying the IPO:

First, managing a succession issue by allowing the Wallenberg family and the old generation of managing partners to sell part of their shares. EQT had historically a weird set up in which the Wallenberg family was partly owner of the general partnership. With the IPO, the family is reducing its stake and will no longer be entitled to carried interest fees.

Second, it's a way to build a powerful balance sheet to initiate new investment strategies (e.g. EQT is working on several strategies: a growth fund, a real estate fund, a niche credit fund and a fund focused on Asia with €50-250m for each strategy): you can invest into 3-4 companies directly from the fund's balance sheet to test the viability of the strategy before raising funds with external LPs. It allows the fund to gain time (no need to have an inception fund) and start with a large fund size. To build this balance sheet, PE funds have either gone public or sold a stake in the GPs to private investors (e.g. SilverLake and CVC).

Third, being public allows EQT to strengthen its brand awareness to facilitate their activities: raising funds, investing into company, recruiting talents

1/ In November 2019, EQT announced the closing of their EQT Venture II for €660m. It is the largest venture fund raised in Europe in 2019.

It’s remarkable knowing that (i) EQT raised its first €566m venture fund only in 2016, (ii) almost all the big venture players in Europe expect Index announced a new fund this year: Accel ($575m), Northzone ($500m), Balderton ($400m) and Creandum ($265m).

EQT fundraising was facilitated by an early successful exit with SmallGiants sold to Zynga for $700m in Dec. 2018 but it demonstrates how good EQT has become in fundraising funds for their different investment strategies.

2/ Why EQT Ventures matters for EQT?

EQT venture arm is relatively small compared to the other asset classes but I believe that it's going to play a key role in EQT's future.

Venture capital is ahead of the curve to identify potential disruptive trends and companies. This knowledge is valuable for EQT other asset classes (e.g. to perform a due diligence on a new investments or to define a strategic plan for a portfolio company).

Venture capital is the basis to kickstart adjacent investment strategies (e.g. the growth fund EQT is working on).

I'm convinced that certain venture backed companies have a good investment profile for private equity funds. Last EQT buyout fund investment in Freepik (a Spanish marketplace of vector graphic and stock photos) is a good example. Dragos Novac dug into this €250m acquisition here and here, but the overall idea is that Freepik was a business that could attract both PE and VC investors. Freepik management team decided to go for a PE investor because they considered that PE guys were "better business mentors" and would not put as much pressure to grow the company. My view is that VC has a lot to learn from PE (especially in Europe where the industry in less mature than in the US) and that the porosity between VC and PE is much more present that what people may think.

3/ EQT Ventures is a mix of what EQT does best and what entrepreneurs could expect from a newly-created ambitious VC.

EQT replicates its troika governance model in Venture by involving industrial experts together with investment professionals to work with the entrepreneurs. It claims to have a network of 250 independent tech advisors.

EQT Ventures also uses a same local with locals approach by opening offices in the countries they are investing. It already has offices and a local presence in Stockholm, London, San Francisco, Amsterdam, Berlin and now Paris.

At the same time, the venture structure was built to take into account the main trends in the VC industry.

First, EQT Ventures investment professionals pitch themselves as "half VC, half startup" with numerous team members from previous successful European tech companies (King, Spotify, Booking, Huddle etc.). EQT bets on the fact that entrepreneurs turned VCs will be better than investors with other backgrounds at picking opportunities and helping their portfolio companies.

Second, EQT Ventures has a platform approach by bringing more than just capital with a full service team (design, marketing, data science, talent, sales etc.).

Third, the fund heavily invested in tech to source and analyze investment opportunities. The tech tool is called "Motherbrain". It is a software to source investment leads in a data driven approach. It is an internal startup within EQT. Motherbrain is tracking 8m companies and 40k VCs. They claim that the software was already able to source deals like Peakon, AnyDesk, Handshake, Warducks and Standard Cognition.

5/ EQT is expecting to invest in early stage European startups (series A and series B). But it has another interesting investment strategy: bridging the gap between Europe and the US.

On the one hand, it is helping its European companies to enter the US market. On the other hand, it is backing US entrepreneurs at Series B and C to help them penetrate the European market.

🔎Global Private Equity Report (Bain, 2020)

🔎 IPO Prospectus (EQT, Sep. 2019)

💌 Why PE beats VC and the new new media consolidation (Dragos Novac, Jun. 2020)

📊 Top 300 PE firms worldwide (PEI, 2019)

🗞Can private-equity firms turn a crisis into an opportunity? (The Economist, May 2020)

🗞Will covid-19 halt the rise of private equity in Europe? (The Economist, May 2020)

Thanks to Julia for the feedbacks! 🦒

Thanks for reading! See you next week for another issue! 👋