🗞 Venture Chronicles - July 2020

Overlooked #31

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m sharing the most insightful news of July.

For 2020, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for July!

Please note that the date picked for each event is not always the exact date of the event but the date I decided to write about the event.

Wednesday, Jul. 1st: Société Générale acquired Shine for a reported €100m valuation. Shine was started in February 2018 to build the best financial and administrative assistant for freelancers. I added numerous sources if you want to build a more knowledgable opinion on this acquisition. (🇫🇷 Maddyness, 🇫🇷 Pierre Entremont, Techcrunch, Société Générale, 🇫🇷 Grégoire Gambatto)

As investor, I'm happy that the Société Générale is buying another French startup after Treezor. To have an healthy venture ecosystem over the long run, we should have many more local corporates willing to sign cheques to acquire startups. Now Shine has a responsibility to make the integration within Société Générale as smooth as possible in the upcoming years to send a positive signal to other corporates.

One could say that we should target billion-dollar exits for our startups and that Shine has failed to enter this category and has sold too early on in their startup journey. I disagree. It's already a great success. Building and exiting a business is extremely hard. All outcomes (failures, small and large exits) should be celebrated - as they are all bringing back talent, playbooks and capital to the ecosystem.

Thursday, Jul. 2nd: India banned 59 Chinese applications from its mobile stores including TikTok which had 200m MAUs users and which was the most downloaded app in the country. As a result, alternatives to TikTok like Moj, Josh and Trell all mentioning Made in India in their names have experienced a strong growth in the past few weeks. Geopolitic considerations are increasingly impacting the tech industry and can no longer be ignored when you think about expanding internationally. (Techcrunch)

Friday, Jul. 3rd: Los Angeles-based Nacelle raised a $4.8m seed round with Index and Accomplice to build a headless e-commerce platform. The idea of building headless platforms is to decouple the front end infrastructure of a website from its backend. Decoupling the backend has several benefits: increasing the website performance and scalability, offering developers a better experience and reducing hosting costs. Headless CMS like Contentful and Strapi have experienced a phenomenal growth and we are now seeing the emergence of headless e-commerce platforms. Benchmark funded an Italian company called Commerce Layer which is doing something similar. Increasing the performance of an ecommerce website is obviously detrimental to optimize conversion and enhance the customer experience. Nacelle is integrating within your Shopify store and has built integrations with the most used tools in the Shopify ecosystem (e.g. Gorgias, Contentful, Klaviyo, Algolia, Klarna, Zendesk etc.). (Techcrunch)

Saturday, Jul. 4th: Lululemon bought Mirror for $500m which is a startup selling a wall mirror to follow fitness classes at home. (The New York Times)

Lululemon invested $1m in 2019 into the company. I believe that letting potential acquirers invest a small ticket is a good way to help them build conviction over your business and to give them access to the backdoors on how you run your business.

Fitness at home is definitely something. I'm amazed by the successes of Mirror, Zwift and Peloton. I would have not bet that those startups would have been able to sell an expensive hardware to consumers and on top of this push them to buy a subscription fee to access sporting classes.

Community is more important than ever. Retail brands are understanding that they need to go beyond a one to one relationship with their customers and they should build and animate community of fans. Lululemon was pretty good at it with fitness classes organized within its retail network. Adding an online layer seems to make a lot of sense.

Sunday, Jul. 5th: Dealroom published a report on the Polish and more broadly the Central and Eastern Europe tech ecosystem. The region has an incredible pool of technical talents that are accessible at a much lower cost than in the US or even in Western Europe. Numerous foreign investors have taken a bet in the past few years on the Polish market including Khosla Ventures (Nomagic), Hoxton (Nomagic), Whitestar (Packhelp), Piton Capital (Docplanner and Booksy) and obviously P9 (Docplanner, Brainly, Infakt, Ofertero). (Dealroom)

Monday, Jul. 6th: Github stars metrics are the new proxies used by investors to invest in open source projects. Konstantin from Runa Capital has collected data on 24k repositories with more than 1k Github stars. France is pretty well positioned with 4 projects that are amongst the top 20 fastest growing projects: Strapi, Meilisearch, Huggingface and Genymobile. (Runa Capital)

Tuesday, Jul. 7th: London-based Wagestream raised an additional £20m round led by Northzone. I'm in love with the concept of earning your income in real time. There is no longer any technical barrier justifying the fact that employees should be paid only once or twice per month. Realtime payment is bringing financial freedom to people who could be struggling to make ends meet every month. For instance, real time salary payment can save you from making an overdraft to pay your telco or utility bill before being paid at the end of the month. (Tech.eu)

Wednesday, Jul. 8th: US-based tech fund Silverlake acquired French bootstrapped payroll management company Silae for €600m at a 12x EV/EBITDA multiple. Silae was founded in 2010, is based in Lyon and Aix-en-Provence, has 150 employees and 550k customers. Payfit has been building a product in this category since 2015, has chosen the venture path raising c.€90m up to date from investors like Kima, Accel, Eurazeo and Bpifrance. It will be interesting to compare the outcomes. (🇫🇷 Les Echos, 🇫🇷 Christophe Raynaud, Silverlake)

Tuesday, Jul. 9th: SBI invested $30m into UK-based B2C2 which is a crypto market maker and liquidity provider. With this round, B2C2 will complement its offering by building a full crypto prime broker and will be at the perfect sweet spot to serve institutional investors entering the crypto market. (Max Boonen)

Friday, Jul. 10th: Sifted published a paper on UK-based "discrete if not secret" venture fund Hedosophia founded by Ian Osborne in 2012. The fund has built a remarkable European portfolio in the finance sector by investing €10-30m tickets into series B and has also made investments in the US (Oscar) and in China (Ant Financial, Lufax). (Sifted)

Saturday, Jul. 11th: US carbon-offsetting startup Wren published its first financial report. The company went to YC last year and received funding from USV. Having public access to the metrics of an early stage company is super rare and it's also a good report to take the pulse of the carbon offsetting market. (Wren)

Sunday, Jul. 12th: I listened to a podcast with Dataiku’s CEO Florian Douetteau. He gives great insights for any European entrepreneur willing to expand in the US: Dataiku entered the US market just after raising a seed round. Generating 25%+ revenues in the US was detrimental to raise their series A with an US investor. Opening your business in the US is like re-starting the company from scratch as you lose all the goodwill you have built in your home country to recruit talents, sign customers etc. (🇫🇷 Funding Crush)

Monday, Jul. 13th: UIPath is the first European cloud startup to exceed the $10bn valuation threshold with a new $225m funding round. The company has reached a $400m ARR run-rate and demonstrated a strong resilience during the covid crisis. UiPath is proving that 1/ Europe is able to be at a forefront of certain tech trends, 2/ outstanding companies can emerge from anywhere in Europe and especially outside the main European tech hubs (London, Berlin, Stockholm, Paris). Accel should make a nice return on this investment after having led both the series A and the series B. (Philippe Botteri, Techcrunch)

Tuesday, Jul. 14th: Julia Morrongiello from P9 published the 2020 version of her B2B marketplaces mapping. I love this category because it's a relatively young model for which successful playbooks are currently being written by entrepreneurs all over the world. Idinvest (💙) is an investor in a couple of B2B marketplaces listed in this mapping like Meero, ManoMano (both B2C and B2B), Ontruck, Malt, Andjaro, Agriconomie, Kactus, Shipfix or Storefront.

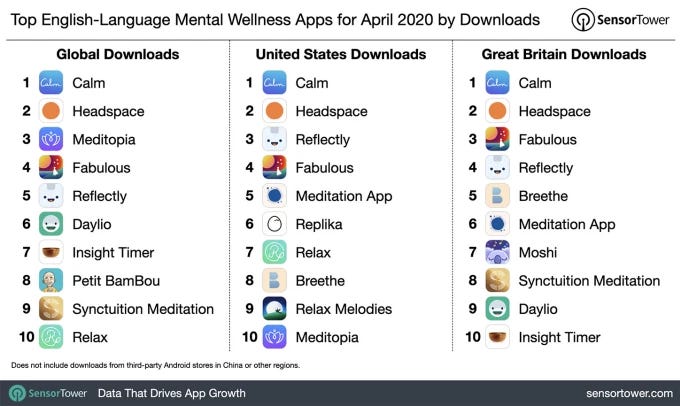

Wednesday, Jul. 15th: Meditopia raised a $15m series A co-led by Creandum and Highland Capital. Meditopia is a meditation app competing directly with Calm and Headspace. I love their positioning as the reference meditation app for non-English countries as I'm convinced that this kind of content is much more relevant when it's localized. Meditopia has 14m users in 75 countries, has been super capital efficient and has built a tier-one team split between Istanbul and Berlin. (Techcrunch)

Thursday, Jul. 16th: Thibaud Elziere published some data on its angel investing activity. Thibaud is investing on the side in startups all over the world. His main job is running startup studio eFounders (which has kickstarted startups like Front, Aircall, Spendesk and more recently Bonjour, Cycle, Folk) and being the CEO of Folk (contact management software). (Thibaud Elziere)

125 investments since 2009 in 95 different companies (3/4 investments done in the past 5y) with a $4.5m entry price for seed rounds.

96.7% non realized IRR and a 52.7% realized IRR (on investments existed) with 10 exits and 7 losses - to be compared (taking a pinch of salt and knowing that they all have stellar performances compared with VC standards) with 1/ Kima's 29.2% non realized IRR and 59.4% realized IRR on their investments since 2015 and 2/ FJ Labs 62% realized IRR on its 193 exits.

2-3 companies in his dealflow per day and 1-2 meetings with entrepreneur per week.

Friday, Jul. 17th: Harry Stebbings launched a $8.3m micro-VC backed by investors, startup executives and entrepreneurs. The fund will invest in the US alongside with tier one investors with cheques around $250k. With his podcast, Harry has built the right network to launch initiatives like this one and it's another great example of what you can built on top of a media. (Techcrunch)

Saturday, Jul. 18th: I listened to a podcast with Denis Ladegaillerie who is the founder and CEO of Believe Digital - a distribution and marketing company for the music industry. It's an overlooked success in the French ecosystem. TCV, Xange and Ventech are investors in this company founded in 2005, which generated €700m in revenues in 2019 and which is breakeven since 2010. (🇫🇷 GDIY) Here are some learnings / figures on Believe and the music industry:

You already know that I'm skeptical on the future prospects of music labels. The cost to produce music has shrunk massively in the past two decades and there is no fundamental reasons for labels to hold artist music rights because they are no longer needed to manage recordings.

Believe is building the music intermediary needed in a world where artists are keeping their rights to their recording and where music is now mainly distributed online. Believe is combining music and tech expertises to find artists and help them develop their activity by distributing their work and helping them on marketing operations. For instance, in France, Believe is working with PNL and Jul.

Jul is the best illustration of what Believe is doing. Jul is a rapper producing everything on his own and is the most listened French artist. Believe signed him early on to manage his distribution for his 1st album which sold 1.5k copies. After the second album sold 10-15k copies, Believe offered to finance in advance video clips for his third album to better promote it. It sold 100k copies. Then, they worked with him on a €500k marketing deal with Apple Music to promote his fourth album which sold 150k copies etc. For each album, Believe works together with Jul to build the best distribution and marketing plan. Jul is free to pick what he wants and still owns his musical rights.

Artists earn €400k for every 100m streams. Jul was listened to a 850m times on streaming platforms last year, earning €3.4m from streaming - which is not that much for the most famous artist in France.

Top artists (100 people in France) are earning 1/3 of streaming revenues. Middle class artists (4-5k in France) another 1/3. And emerging artists (30-40k) the last part of the pie.

Sunday, Jul. 19th: A good place for Sunday reading sessions with a curation of articles from Brett Bivens on the rise of famous companies including Softbank, Discord, Figma, Supercell, Pinduoduo, Visa, Spotify, TikTok etc. (Brett Bivens)

Monday, Jul. 20th: Dance raised a seed round led by BlueYard. The company was created by SoundCloud founders and is a subscription-based ebike service. For €59 per month, you have a state of the art e-bike that you can change whenever you need to replace or repair it. The idea is to remove the pain points associated with both ownership and free-floating. (Techcrunch, BlueYard)

Tuesday, Jul. 21st: Silverlake made another tech acquisition in France buying Meilleurtaux.com from Goldman Sachs which is a comparator and broker for financial products. The company has been working with private equity funds since 2013 with a strong external growth strategy to reach €10bn of real estate loans volume intermediated. A French startup called Pretto is operating in the same space with the ambition to bring a fresher approach to this real estate loan brokerage market. It has raised a €8m series A in February 2019 with Alven and Blackfin. (AFP, 🇫🇷 Le Panier)

Wednesday, Jul. 22nd: AB Tasty raised a $40m series C led by Crédit Mutuel Innovation. It helps merchants to customize their website depending on the customers they are interacting with. AB Tasty started as a digital marketing web agency that built an AB-testing product and then evolved into a more complex suite of products to customize web pages and make feature testing. It has 900 customers, generates 60% sales outside France and has a strong revenue growth in the US (480% over the past 2y). (Techcrunch, AB Tasty, Sifted)

Thursday, Jul. 23rd: Paul Murphy (general partner at Northzone) did a great interview with Protocol. (Protocol)

"The idea of being a specialist is kind of bullshit." Most of the time, an industry is reshuffled by people who will have a contrarian view on how things should work in it. As an investor, if you pretend to be a specialist in an industry by developing specific investment theses on the future of this industry, you will be struggle to be open to this contrarian view.

Investment themes: look at "how people spend their discretionary time," micromobility, messaging.

Friday, Jul. 24th: Revolut added $80m from TSG Consumer Partners to its series D for a total amount of $580m valuing the company at $5.5bn. It's interesting to look at the new challenges ahead for Revolut and its 12m users: (i) expanding into the US, (ii) rolling-out banking products in Europe thanks to its brand new banking license (inc. lending) and (iii) releasing new features to move toward the best financial hub to manage everything related to your money (inc. a subscription management tool, insurances, trading etc.). (Techcrunch)

Saturday, Jul. 25th: The New York Times acquired the podcasting house behind Serial for $25m. The newspaper is already producing podcasts including The Daily and has acquired another company called Audm which is transforming long form articles into audio content. Audio journalism is growing and The New York Times wants to rise with the trend. (Techcrunch, The Verge)

Sunday, Jul. 26th: I listened to an Invest Like the Best podcast episode in which Benchmark GP Eric Vishria describes the three successive generations of SaaS. (Invest Like the Best)

Generation 1 (Salesforce, Workday, ServiceNow): the first wave of SaaS brought a new delivery model (vendor-hosted vs. buyer-hosted) and a new revenue model (recurring fee vs. one time fee + small maintenance fee) but shared numerous similarities with the old paradigm of Application Service Providers (single instance, enterprise sales, heavy implementation, poor usability).

Generation 2 (New Relic, Zendesk, Docusign, Asana): the second wave of SaaS added a better adoption model (top down adoption by individuals vs. bottom up adoption with an enterprise decision) and focused on building easy to consume products (nice UX, trying before paying, no expensive implementation). It also expanded the reach of potential customers from F500 to the mid market.

Generation 3 (Twilio, Stripe): shift from people using a software to get a job done through a graphical user interface (e.g. a sales person using SF to manage its pipeline) to software communicating with other software through APIs (e.g. payment block provided by Stripe, communication block provided by Twilio).

Monday, Jul. 27th: Cargo.one raised a $18.6m series A led by Index. Cargo.one is a B2B marketplace helping freight forwarders to search and book instantly air freight capacities with airlines. (Index)

With the covid crisis and the temporary shutdown of people travel, air freight has become a key revenue source for airlines. For instance, Finnair disclosed that cargo bookings represented 70% of their revenues during the second quarter.

Cargo.one is working with 12 airlines and 1,500 freight forwarders. With this new funding round, the company will expand in East Asia and in North America and will build new tools to enhance the booking experience (demand prediction, dynamic pricing, route optimization etc.)

Tuesday, Jul. 28th: Idinvest (💙) is leading a $60m investment into Withings which sells healthcare devices like smartwatches, weighing scales, tensiometers etc. along with BPI and Gilde Healthcare. Withings was founded in 2008. We backed the company a first time and we sold it to Nokia in 2016 for €170m. Eric Carreel bought back the company at a relatively low price in 2018, was able to restructure Withings and build a newer and fresher vision for the company. We are thrilled to be on the road again with him for this new journey in a company that move from selling IoT gadgets to impressive healthcare hardware. (Sifted)

Wednesday, Jul. 29th: Peter Levine published another paper on how to sell a B2B software to enterprise customers. (a16z)

He is pushing startups to start growing through a bottom-up product adoption approach that will be later complemented with a more traditional top-down enterprise sales machine - referring on success stories like Github, Atlassian, Zoom or Slack.

I also love this idea that in the first bottom-up period, product-led B2B companies should track and optimize usage and engagement with the same metrics used by B2C companies: DAU, WAU, MAU, time spent and number of sessions per day/week/month, number of days active in a given week, usage retention etc.

Thursday, Jul. 30th: I already made a deep dive on EQT in this newsletter and told you that its venture arm was using AI to source companies with a software called Motherbrain. Below are some learnings on this initiative. (Venture Beat)

Sourced 7 deals out of the 50 deals done through outbound reach before any previous contact (Peakon, Handshake, Anydesk, Warducks, Standard Cognition, Netlify and Anyfin),

Used as a tool to prioritize the dealflow and eliminating less promising companies,

API connections and scrapping from 40 data sources,

Re-engineering of the processes and tools to have all the dealflow management connected to the software.

Friday, Jul. 31st: Substack has passed the threshold of 100k paid subscribers, usage has double in the first three months of the pandemic and revenues grew by 60% over the same period. (Business Insider)

Whe the media industry is suffering from a sharp advertising revenue decline, Substack subscription based model is thriving and more traditional journalists are onboarded on the platform to write content and find an alternative revenue source.

Azeem Azhar started his newsletter Exponential View in 2015, switched to Substack at 35k free subscribers after talking to the founders and has now 53k free subscribers and several thousands who are paying $120 per year.

Substack is adding additional services to attract writers on its platform like a grant program to support nascent writers or legal support.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋