🍒 Mapping Grocery Startups in Europe

Overlooked #87

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, with Eléonore, we’re sharing a mapping of European grocery startups.

I’m thrilled to co-write this article with Eléonore. She has become my go to person to talk about grocery trends and startups. It was natural to work together on a mapping like this one. Eléonore is working at Five Seasons which is a pan-European venture fund specalized in foodtech. With two portfolio companies in e-grocery, La Fourche and Cortilia, Five Seasons Ventures has been an early believer in the digitization of grocery shopping and has the conviction that it's only the beginning!

During Covid, grocery made a come back under the spotlight, as the pandemic forced us to adopt new habits and many households had no other choice but to order their groceries online.

Normally, it's extremely hard to change individuals habits. You have to come with a alternative 10x better or to pitch a different worldview for people to switch to your product or your service. Or... you need an earthquake like covid to push people to test your product or service a couple of times to understand that there definitely are advantages to your option compared to traditional alternatives. This is what happened for online grocery in the past 18m. People tested online grocery and have definitely adopted it - at least for a significant part of their grocery basket. Online grocery gained several years of customer adoption and a period of consumer experimentation is underway creating unique opportunities for entrepreneurs.

In this paper, we'll try to give you an exhaustive view of the online grocery startup ecosystem in Europe. Many papers have been written on the different existing models but we believe that it's interesting to take a step back and capture the broad picture. We will dig into the following topics:

Mental models to compare categories

Mapping 19 different categories and 70+ European startups

Interesting trends to watch-out for

Mental models to compare categories

To compare grocery categories, we believe that you can use several criteria including:

Price positioning: discounts, prices on par with super/hypermarkets, prices on par with convenience stores, premium prices.

Targeted geographical scope: focusing on city centers only, to serve consumers beyond cities, in the suburbs and even in rural areas.

Type of food: generalist players or targeting a specific segment of food (bio products, dry products, vegetables, drinks)

Degree of integration. For each piece in the value chain, you can decide whether you want to internalize it: suppliers, "inside logistics" to warehouses, warehouses, "outside logistics" to consumers.

Consumer personas targeted: single individuals, small families (2 adults + 0-2 kids), large families (2 adults + 2+ kids).

Usages targeted: convenience, weekly shopping, monthly stock up and specialized shopping (fruits & vegetables, organic, drinks, etc.).

In our mapping, we will use some of these criteria to compare the different categories and we believe that they are a good starting point to evaluate a new grocery model.

Mapping 19 different categories and 70+ European startups

Disclaimers: (i) this mapping is not exhaustive, (ii) some players are blurring the lines between categories, (iii) if we missed a company or a category, please send me an email at adewez@eurazeo.com.

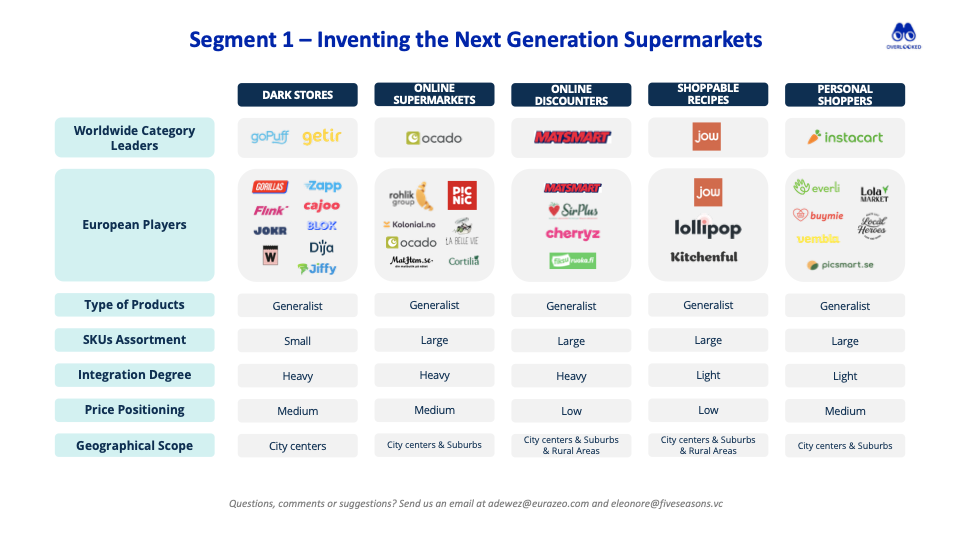

Segment 1: Inventing the Next Generation Supermarkets

Dark stores: pioneered by GoPuff in the US and by Getir in Turkey, these players offer 15-min grocery delivery in city centers by operating a network of small dark stores (1,500m2, 1.5-3.0k SKUs). It's a vertically integrated model in which you have to operate an app, a fleet of drivers as well as a warehouse with pickers & packers. Players are going after the convenience use case (e.g. missing an ingredient for your dinner tonight, buying alcohol for your Friday night party, etc.). There are several challenges in this category, the first one being the harsh competition leading to CAC rise and the second one being to move from the convenience use case to the weekly shopping use case to improve unit economics.

Online supermarkets: it brings online the wide product catalogue of traditional grocery stores with a better purchasing experience and logistics tricks to make the model sustainable (e.g. Picnic's milkman delivery model to optimize last mile delivery costs). It is one of the most difficult model as it is vertically integrated and unlike dark stores the product assortment is much wider (+5k SKUs).

Online discounters: in exchange of an annual subscription, you can access to discounted entry level products. Traditional discounters are one of the fastest growing players in Europe with a forecasted market share of 26% in 2023 (vs. 23% in 2018). It’s therefore natural that new entrants see it as an opportunity to bring discounted products online. However, one must not forget that this model is a very though one, as customers are not loyal at all and margins are extremely thin.

Shoppable recipes: it's an asset-light model in which consumers will pick the recipes they want to cook during the week and transform them into a grocery cart at their favorite retailer. It's just a front on top of the infrastructure of retailers. The challenges are technical (integration with retailers) and from a business model perspective as you need to team up with both retailers and CPG brands to generate revenues.

Personal shoppers: pioneered by Instacart in the US, it's a marketplace between gig workers and individuals who want to have someone to replace them to purchase and deliver their grocery basket. The challenge of this model is to generate revenue from three different sources: retailers (revenue share), customers and CPG brands (in the longer term).

Segment 2: Specialists in a Given Product Category

Farm to table: it cuts intermediaries between farmers and end consumers to provide better economics to farmers and better prices to consumers. A first wave of startups emerged at the beginning of the 2010s (Goodeggs and La Ruche were both created in 2011), got financed by tier-1 investors like Sequoia, Index or USV and experienced a couple of years of exponential growth. Nonetheless, these companies ended up plateauing due to operational complexities inherent to their models (logistics, relationship with producers) and an incapacity to address mainstream customers (high prices, low convenience). With covid, a second wave of startups emerged (Crisp, Crowdfarming, Membo) with a stronger market momentum. Best practices have emerged around how to manage online grocery operations. Moreover, buying organic products and products directly sourced from farmers are becoming key purchasing criteria.

Meal kits: in exchange of a subscription, boxes of grocery products are delivered to your home every week with ingredients and recipes to be cooked. Products are pre-portioned and sometimes are even pre-cooked. Just like fresh vegetable boxes, meal kits saw their popularity shoot up during covid but their price point remains a barrier to massive adoption.

Organic discounted: in exchange of an annual subscription, you can get access to a wide catalogue of organic products that can be purchased at attractive prices compared to what you can find in supermarkets. Consumers use these services for their monthly stock-up of organic products and companies are adding product categories (like meat, fish, fruits & vegetables) to also be able to target the weekly grocery purchase of their user-base. What is particularly interesting in this model is that low-margin discounted products are balanced by the yearly subscriptions which are pure profit.

Ethnic Food: it builds a specialised product offering targeting a single type of cuisine instead of being generalist. You can attract both casual eaters of your cuisine type as well as population segments in a given demographic. This model is pretty interesting because it allows to have a community-oriented marketing strategy and as a result to decrease CAC considerably, which in a post-covid world it a huge strength.

Segment 3: Avoid Waste

Avoid waste upstream: it partners with food producers (farmers but also CPG brands) to help them reduce waste on items that have small imperfections that make them unsellable in traditional grocery channels. Most of the time, these players are bundling products into a recurring weekly basket. This category, which historically was lagging behind due to its lack of convenience, resurrected during Covid (leading to Oddbox bagging in £16m in new investment in August). The question is for how long.

Avoid waste downstream: it partners with retailers and restaurants to help them reduce their waste. Consumers can access end of life prepared food and grocery products at a discounted price. These models are leveraging national regulations which are preventing players in the food industry to destroy close to end of life food waste. The limit of this model is the lack of convenience for customers who don't choose what they buy and when they buy it. For consumers who are motivated by prices rather than the environment (which is still the case in majority), discounters are much more appropriate.

Reusable containers: it orchestrates a modern deposit system for recurring household products like beverages or bulk products. We believe that reusable containers is a great marketing hack to generate recurrence because consumers have the branded containers under their eyes everyday and want to recover their financial deposit when they return the containers. This model requires a special logistic to source the containers, to strike partnerships with producers, to distribute containers, to wash them and re-employ them which makes it very difficult to have decent unit economics.

Segment 4: Traditional Food Delivery Players Going into Grocery

Dark kitchens: players either operating delivery only restaurants or offering the real estate infrastructure to restaurants to expand their delivery only kitchen capacity. Some players like Taster and Curb are building a portfolio of food brands distributed only on delivery platforms. Others are opening pick-up locations or retail locations that could be leveraged in the future to also offer grocery products. We can give the example of CloudKitchens which launched CloudRetail, a service to CPG brands looking for last-mile cold and dry storage to sell products via on-demand marketplaces.

Restaurant food delivery: players like Deliveroo and Justeat in Europe or like UberEats and DoorDash in the U.S. have built three-sided marketplaces between restaurants, riders and consumers. It enables restaurants to start offering delivery without having to manage an internal fleet of riders. With covid, food delivery platforms started to expand in the grocery space by partnering with national retailers to make part of their catalogue accessible through delivery and/or by operating dark stores to offer fast grocery delivery. In the US, DoorDash has even released a product feature called DoubleDash to combine in a single order both food from a restaurant and grocery products from its network of dark-stores/grocery partners.

Multi-category delivery: players in emerging countries like Rappi in Latin America and Meituan in China are leveraging their last mile network of riders to deliver several categories of products. With covid, these players reacted quickly to add grocery into their offering combining several models such as community group buying, grocery dark stores or partnership with leading grocery chains.

Food to offices: it distributes prepared meals and grocery products through small stores located in offices. If you are providing a great offering at the right price, this positioning is powerful because you have a natural monopoly in the offices in which you are located. The complexity is both in the product (hardware + perishable goods) and the distribution strategy (first sale to the corporate and then target the customers with in-app notifications, etc.).

Segment 5: Future Grocery Models from Other Geographies

Community group buying: it's a next-day grocery pick up service that has become mainstream in China's city centers. I covered it in a previous edition of the newsletter. It connects local farmers and small urban communities. Communities are animated by group leaders who are in charge of recruiting members, gathering orders in a given day, receptionning the grouped order to be dispatched into individual orders. It's an interesting model because (i) it's a farm to table model cutting intermediaries between farmers and end consumers and (ii) last-mile delivery which can represent up to 30% of the total logistic cost for an order is crowdsourced.

Augmented stores: Amazon (AmazonGo) and Alibaba (Freshippo) are both experimenting massively to create the next-generation of retail stores augmented by technology. AmazonGo is an unmanned store and Freshippo is testing 10+ different retail formats in China - the most common one being a retail store combining a restaurant, a traditional grocery store and a warehouse into a single location. Needless to say that the challenge here is first and foremost technological but building a brand that customers trust come right after (that is what Storelift is trying to do with their Boxy supermarkets).

Full stack farm to table: in the US, Grubmarket has built a unique farm to table model. It's acquiring wholesalers and farmers at a strong pace to aggregate them into a marketplace powered by technology to serve both B2B and B2C players who are looking to buy their products directly from farmers.

Interesting trends to watch-out

Question-mark on the grocery-store form-factor: in city-centres, I don't believe in a purely online model. Independent traders and grocery physical stores won't disappear. First, certain products categories will never completely shift towards online like fruits, vegetables, meat and fish. Moreover, consumers are eager for restaurant-like food experiences opening the door for new grocery store formats. I believe that stores similar to Freshippo in China will emerge in Europe combining in a single location a restaurant, a grocery store and a fullfilment center (by the way, if you are planning to build this in Europe, please do send me an email at adewez@eurazeo.com). These stores will reinvent the grocery shopping experience making it completely omnichannel and modular. You will be able to order online or shop onsite. You will be able to have your products cooked on site, delivered to your place or you will be able to pick them while coming back to home after work.

Serving the tech underserved: most investors and players in the online grocery have built/founded that mirror their persona (white affluent individuals living in city centres which are not price sensitive). Most startups are building solutions providing products that are way too expensive for the majority of the population - which is wild in a market whose primary consumer driver is price. Moreover, there are definitely opportunities to serve the tech underserved with solutions targeting suburbs/rural areas or solutions targeting certain demographics (families, a certain ethnicity, etc.). For instance, we love Storelift because they are making convenience stores sustainable in rural areas thanks to their unmanned store format.

Looking at traditional retailers to see the future of online grocery startups: using a franchise-model to scale (Taster, Getir), launching a white-label brand (Flaschenpost, Kazidomi, La Fourche), launching an advertising program for FMCG brands (Jow, Gopuff), subscription as fidelity programs (La Fourche, GoPuff) are not innovations but only old recipes reinvented and digitalised.

Becoming multi use cases (convenience, weekly basket, monthly stock-up, specialised food): in the future, we should expect category leaders to expand their market by going into other categories and by addressing other use cases. There are 21 meals occasions per week and you cannot believe you’re done until you are positioned to capture all of them. You can also be positioned to capture every consumer behavior - be it an instant need or a stock-up. It's not a surprise that DoorDash is opening dark stores, launching dark kitchens and is becoming a personal shopper by partnering with traditional retailers. Traditional grocery players are already multi-use cases combining several store formats (convenience, supermarkets, hypermarkets) and shopping option (in store, pick-up, delivery).

Putting sustainability at the core: 40% of all products is wasted, 25% of which happens at the farm level and the remaining 15% occurs downstream at retail. Taking this into account, it's impossible to operate in the grocery space without taking into account social and environmental matters. On the social front, we don't know what is the right employment model for blue-collar workers (pickers, packers and drivers). European regulations are challenging the gig-economy model and some players have decided to hire their workers with more stable contracts (dark stores players, JustEat). On the environmental front, it has become a key purchasing factor for consumers and European countries are constraining players to build more sustainable supply chain. As a player, you can work on the whole value chain from product sourcing to logistics, packaging and waste management. We added in our mapping 3 categories of startups putting sustainability at the core of their offering but we believe that sustainability is core in any grocery model.

Becoming data-driven to offer a tailor-made experience: on average, customers spend 2 hours per week doing their groceries. Browsing through Carrefour's website trying to figure out what you want takes time... But what if your favorite retailer knew better? What if he knew better because you've been shopping with him for such a long time that he could help you make your shopping list and elaborate your weekly meal plan? Well, grocery players are clearly looking in this direction, from traditional retailers (with Albert Heijn acquiring the personalized recommendation app Foodfirst) to new entrants like Jow with its grocery mobile app making recipes shoppable.

Offering a seamless experience: whether it be traditional retailers or new online entrants, grocery players have understood the importance to offer a seamless experience in a world where convenience has become the buzz word. It's obviously easier for new entrants as they can design their product with this in mind. Hopefully, traditional retailers are helped by a bunch of actors focused on making the shopping experience as personalized as possible (like Jow or Lollipop), on digitalizing in-store purchase (like Sensei), on making delivery as fast as possible (with personal shoppers like Lola Market or with bespoke fufillment centers like Takeoff Technologies in the US).

Conclusion

Being trendy is one thing. Building a sustainable business is another. It's tough to be successful in the grocery space. Traditional retailers are operating at low digit margins. Many startups in this space like Webvan or TakeEatEasy failed because of poor unit economics. There is no doubt that tech and consumer innovations can enhance or reshuffle the unit economics of the industry. Many startups have successfully used old tricks to improve both topline and profitability, like launching their own brand, advertising services for FMCG, loyalty programs for consumers, etc. Yet, it remains to be seen which categories and players will be sustainable over the long run. Of course, when billions are poured into a sector, it takes more time to figure out who will win. Or lose.

Thanks to Paul and Julia (🦒) for the feedback! Thanks for reading! See you next week for another issue! 👋

Lose not loose.

To start, look to fully understand 7-11 stores & procedures in Japan and you will learn a ton

@ value add for Western supermarket chains! Especially for those in dense urban areas