🇨🇳 Look East, Not West - Pinduoduo's New Grocery Business

Overlooked #73

Hi, it’s Alexandre from Eurazeo (ex. Idinvest). I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m introducing a new series of articles around interesting consumer innovations in Asia starting with Pinduoduo’s new grocery business and the broader community group buying trend in China.

I have the feeling that Europe and the United States are lagging behind when it comes to consumer innovations compared to Asia. I’ve decided to dedicate a significant part of my summer to learn as much as I can on consumer tech giants in Asia to validate or refute my intuition. I’ll share my learnings with you along the way. I will dig into companies like Grab, Tencent, Pinduoduo or Meituan. I will also dig into trends like community group buying, consumer to manufacturer, super-apps, live-streaming, social commerce, etc.

I want to talk to anyone who has spent some time in this same rabbit hole. You can reach out at adewez@eurazeo.com.

I will start with a Chinese trend in the grocery category. I will look at Pinduoduo’s new grocery model and the broader community group buying trend in China. In August 2020, in the middle of the covid crisis, Pinduoduo launched a new grocery business called Duo Duo Grocery that is now available in more than 300 Chinese cities. It's a super interesting model. I won't be surprised if entrepreneurs in the West start launching startups inspired by Duo Duo Grocery and the broader Chinese community group buying space.

In this article, I’ll cover the following topics:

Detailing the Duo Duo Grocery's model

Explaining how this model is integrated into the broader Pinduoduo's ecosystem and is an example of the broader community group buying in China

What does it take to replicate the model in the West?

Part I - Detailing the Duo Duo Grocery's Model

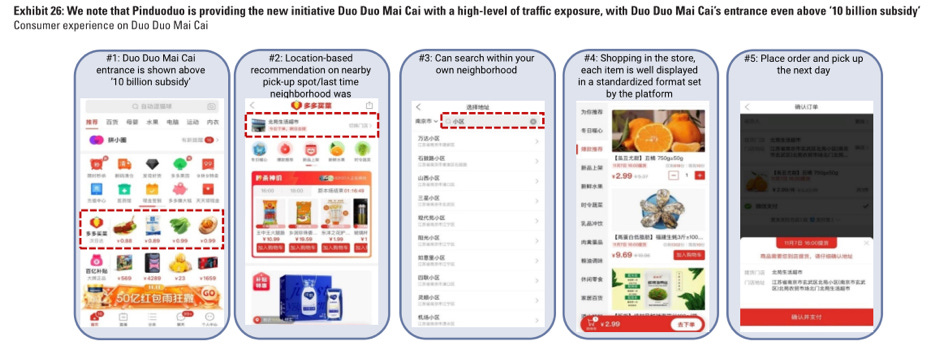

Duo Duo Grocery is a local next day grocery pick up services. Local farmers will list their fruits and vegetables for direct sales to local consumers. Consumers place their orders before 11PM on the Pinduoduo's app and can pick up their purchase after 4PM the next day in a pick up location.

On the Pinduoduo's app, you can access Duo Duo Grocery in the 1st navigation page of the app. You select a pick-up point close to your home or your workplace. You select the items that you want to purchase and you pre-pay them before 11PM. If the pick up point has reached a critical mass of orders, a group order is sent to local farmers. Products are delivered the next day to the pick up point and consumers can collect their orders after 4PM.

This model solves many issues associated with traditional online grocery delivery.

You are cutting intermediaries between farmers and consumers. Online grocery retail is massively intermediated with retailers and wholesalers. In this model, farmers are listing their products directly on Pinduoduo and consumers can order them on the Pinduoduo app. You have no middlemen. As a result, at the same time, consumers get cheaper prices and farmers higher margins.

Last mile delivery is "crowdsourced". Last mile logistics represent up to 30% of the total logistic cost for an order. In this model, products are delivered to a pick up point and consumers are doing the last mile by picking up their orders.

Strong social dynamics reduce customer acquisition costs, increase conversion rate and purchasing frequency. Pinduoduo's core strength has always been to aggregate demand on its platform and to leverage it thanks to social dynamics. With Duo Duo Grocery, orders are accepted only if a pick-up point reach a certain critical mass in terms of order size. It pushes community members to bring their friends to the platform and to incentivize them to make orders.

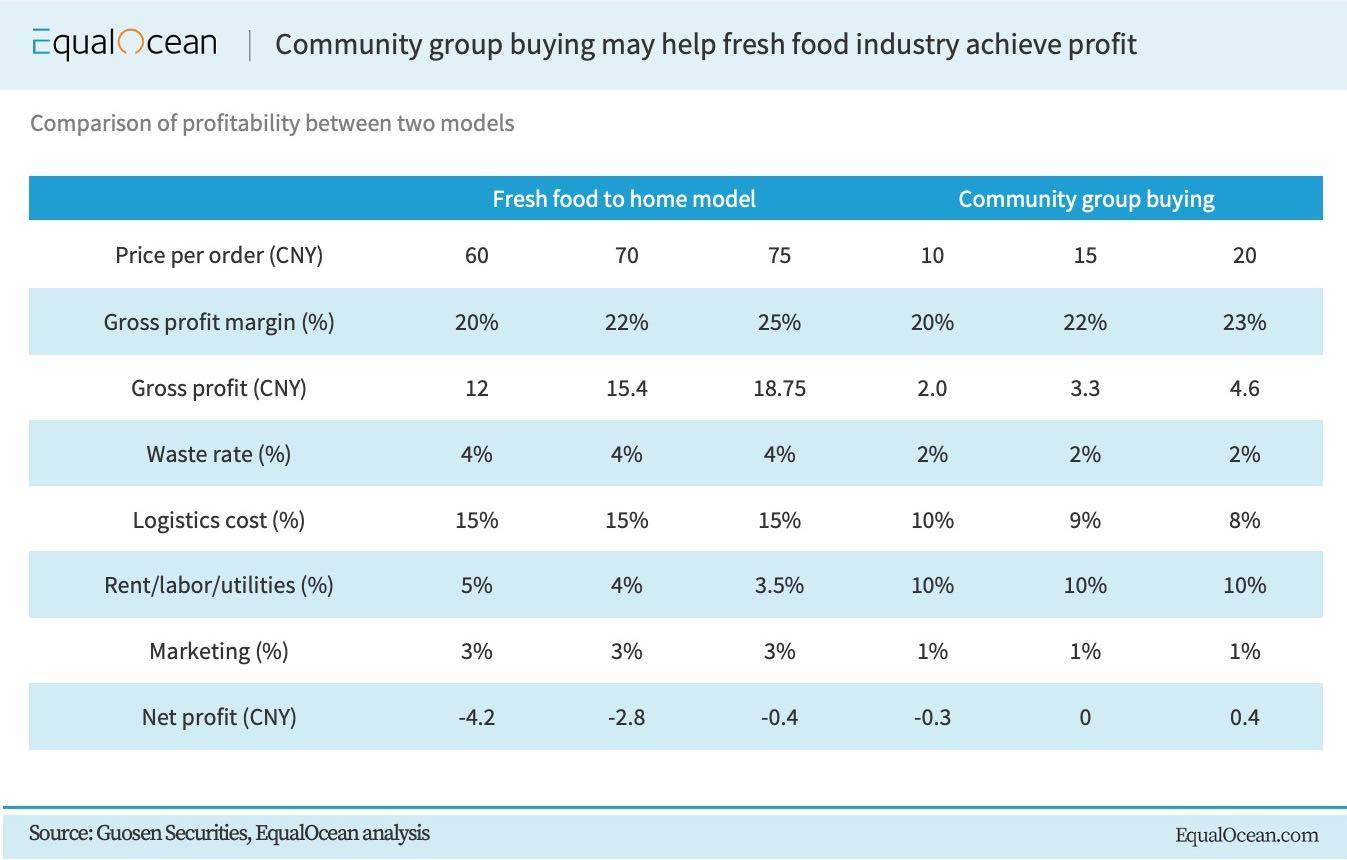

When you do the maths, it's a model that can be sustainable for online grocery. Equal Ocean compared the unit economics between online grocery delivery and this Duo Duo Grocery model. As you can see, it's extremely hard to make the unit economics work because profit margins are low, logistics costs are high and marketing costs can rise quite quickly.

Part II - Duo Duo Grocery as a Subset of the Pinduoduo’s Ecosystem and of the Broader Community Group Buying’s Space

The Duo Duo Grocery model is not an innovation that is coming out of nowhere. On the one hand, it's rooted in Pinduoduo's history which started its social ecommerce operations with the agriculture vertical. On the other hand, it's part of a broader trend around the community group buying in which Chinese tech giants and local venture capitalists have poured hundreds of millions.

The Pinduoduo’s Ecosystem

In 2015, Pinduoduo started by bringing farmers products directly to the consumer through group purchase (if you team with 1, 10 or 20 other people, you get a discount on the product you buy). Since then, the company expanded its ecommerce offering into multiple categories but has preserved a strong tie with its agriculture roots working with 12m Chinese farmers and generating $42bn GMV in agriculture related products (vs. $21bn in 2019).

Duo Duo Grocery is a natural extension of PinDuoDuo's traditional offering for food products. It provides customers with local products and reduces the delivery time from 3-4 days to less than 24h.

Pinduoduo has a broader strategic initiative called "Internet + Agriculture" - of which Duo Duo Grocery is only one pillar. Pinduoduo wants to bring farmers to the digital age: (i) it trains farmers so that they can learn how to have a digital presence and to sell their products online, (ii) it cuts the intermediaries between farmers and consumers through its demand aggregation platform and (iii) it contributes to modernizing farms operations and distribution.

"Under its “Internet + Agriculture” strategy, Pinduoduo coached farmers on setting up stores online, provided them with access to end demand, and helped them to increase their household income. By training young men and women from rural areas to become e-commerce savvy “New Farmers”, many of them became champions for digital inclusion, often catalyzing a multiplier effect and wealth creation for their local communities."

The Community Group Buying Space

Community group buying is one of the hottest spaces in Chinese tech at the moment. Both tech giants and venture funds are crazy about it. They believe that grocery is a massive category that is yet to be digitized and that community group buying has sounder unit economics compared to other online grocery models. Forecasts predict that it's a $22bn market in 2020 that will grow at a 71% CAGR in the coming years to reach $191bn by 2025. Moreover, Chinese tech giants are fighting to build super-apps driving proprietary trafic that they can leverage to cross-sell multiple services. Community group buying for groceries is a perfect Trojan horse to build a super app because it can generate both high app usage and high gross volume.

Most community group buying models differ slightly to the Duo Duo Grocery offering. The picking point is replaced by a community leader who will animate actively a small community of customers.

For a 10% commission on each order, the community leader will create a WeChat group, will onboard customers in his neighbourhood and will send every day a list or products that people can order. Then, the next day, the community leader receives the bulk order and prepare the individual orders. People in the community can either pick up their order or have it delivered by the community leader.

Compared to Duo Duo Grocery, this common community group buying model is doubling down on its social dynamics. The group leader has a strong incentive to make the group successful as he takes a 10% commission on orders and he has to reach a certain volume of monthly orders to remain on a community group buying platform ($4.7k sales per month to be reached in 3m to stay on the platform knowing that the average group reaches $6.3k per month). As a result, daily conversion rates can be up to 10% in a group compared to 2-3% conversion rates on most ecommerce websites. A group leader will have a true entrepreneurship mindset to build a community, to animate it to generate repeat and more expensive orders.

Part III - What Does it Take to Replicate the Model in the West?

I believe that the model is working in China for the following reasons:

WeChat: most community group buying platforms were started as WeChat Mini Programs and group purchases are organized in a WeChat's group managed by a group leader.

Mobile payment infrastructure: thanks to WeChat Pay and Alipay, there is no friction to make micro-purchases on mobile. Chinese consumers all have access to an Apple-Pay like experience on their mobile.

Logistics infrastructure: China has built a strong ecommerce logistics infrastructure and is doubling down on cold chain delivery to be able to bring quickly grocery goods to the consumers.

High urban density: it's required to make this pick-up point model sustainable.

Social dynamics: Chinese consumers are used to make group purchases and are fine with bringing their friends & family to join them in a group buying.

When it comes to replicability, in Europe, I have the feeling that there is a willingness from consumers to buy more local products and from suppliers to sell their products directly to the consumers.

Moreover, we have adjacent models that are already existing including La Ruche qui dit Oui (small consumer communities aggregating products from local suppliers and led by somebody who takes a 20% cut on orders) in France and Lifvs in Sweden (1 person managing several unstaffed stores and communities of local buyers).

We don't have a WeChat equivalent that would help to populate the explosive social growth of these models. Moreover, our mobile payment and logistics infrastructures are weaker compared to China. I also have doubts on the replicability of the social dynamics in a much more individualist culture in the West.

If you are experimenting around this concept of community group buying, I would love to get in touch. You can reach out at adewez@eurazeo.com.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Curious about the CGB TAM and projected CAGR quoted in the article: $22B and 70%. What is the source for these figures?

Hi Alexandre and thank you for this interesting summary.

One point that I am trying to figure out is how does Duo Duo Grocery aggregate orders and team buying. I understand that Pin Duo Duo app has two prices - one for individual and the other for group buy. Would you happen to know if it is similar on DDG?

Regarding your comments on replicability I would agree that WeChat and gamification enabled an unprecedented PDD user growth however I would argue that their model is actually centered around D2M model which enables price competitiveness. All the other fancy features are basically employed in order to grow and engage user base which means that different tools could be used to adjust for the cultural differences. Therefore a model replica is surely something to watch for in the West in the coming years however it seems that all the focus currently is on q-commerce which in my view will prove to be only temporary.