🇫🇷 H1-2020 French Funding Rounds & Covid Impact

Overlooked #29

Hi, it’s Alexandre from Idinvest. Overlooked is a weekly newsletter about underrated trends in the European tech industry. Today, I’m looking at the state of the French fundraising market in during the first semester of 2020.

In the previous edition, with Thibault, we investigated the funding rounds that happened in 2019 in France. In this issue, we are continuing our deep dive in the French fundraising market by looking at what happened during the first semester of 2020 and by trying to measure the potential covid impact on fundraising rounds.

If you want to look more closely at the data used for both articles, I’m sharing the Airtable I used with the data on all French funding rounds that have happened since 2017.

In this paper, we will cover the following topics:

Top 15 funding rounds during H1-2020

Evaluating the covid impact on French fundraising rounds

France compared with the rest of Europe during H1-2020

What should we expect in the coming quarters

Foreign investors update

Hot industries and trends

Early stage companies to follow in the next 18 months

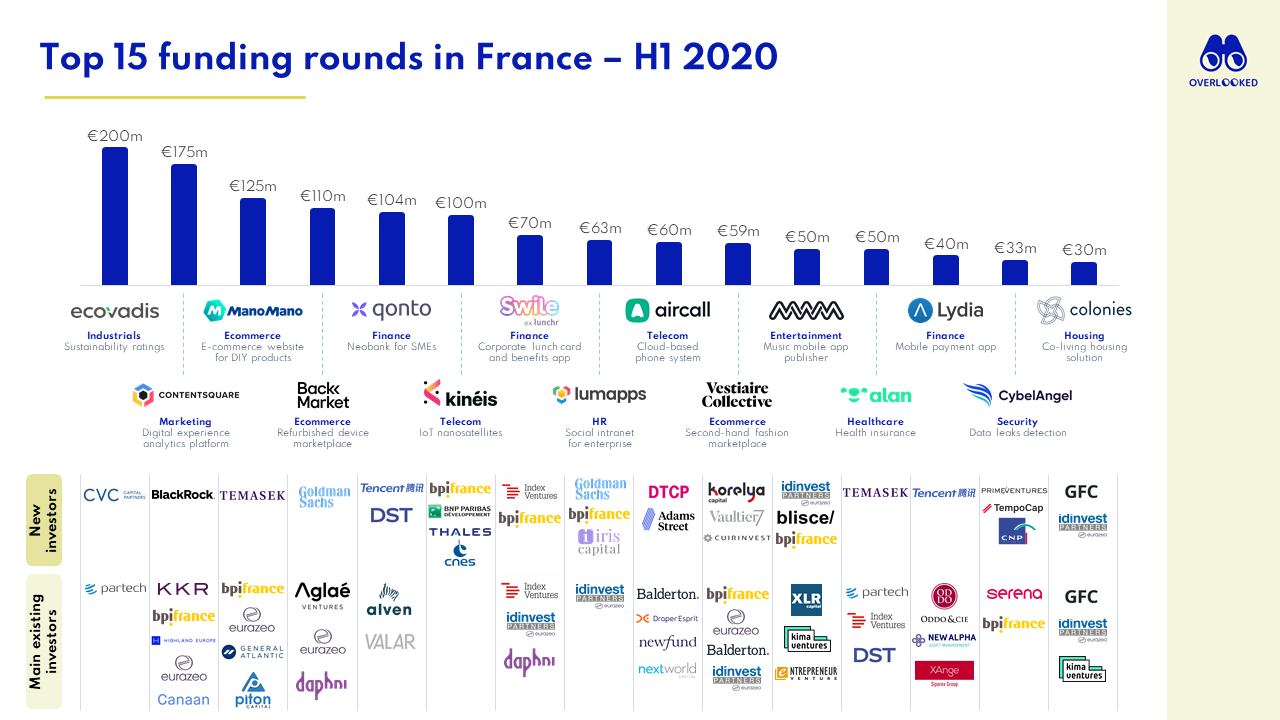

Top 15 Funding Rounds in H1-2020

The Asian growth funds made a remarkable entrance. Singapore-based fund Temasek (ManoMano, Alan) or Chinese giant Tencent (Qonto, Lydia) led 4 of the 15 biggest rounds in France. 2020 marks the beginning of an ever increasing impact of these two funds in France: prior to that, Temasek had never invested in France and Tencent made only 2 investments (Team8, Axereal).

Bpifrance (almost) everywhere. The French public fund dedicated to investing into strategical sectors invested in 8 of these 15 companies. Bpifrance Large Venture fund has played a strategic role in late-stage investment in a country in which growth capital is still a scarce resource.

It remains uncommon to raise large rounds with French funds. According to this sample, most of the late stage investors are Asian (Temasek, Tencent, DST Global), American (BlackRock, Goldman Sachs) or European (CVC, Index, GFC, Prime Ventures, Tempo Cap). On the other hand, Eurazeo (4 portfolio companies), Korelya, Iris Capital and Blisce (one deal) are the few France-based investors which stand out.

Corporate funds were able to seize the opportunities. The best example is probably DTCP (the German Telecom company) which took a stake in cloud-based phone system Aircall. We can also highlight the French giant of the aerospace industry Thales which invested into Kinéis, a subsidiary of the CNES (French National Center of Space Research) which builds a nanosatellites constellation for the IoT sector.

Evaluating the Covid Impact on French Fundraising Rounds

This should not be taken as a definitive analysis of the covid impact on French startup funding rounds. It's a work in progress analysis for several reasons: (i) we are still in the middle of the crisis, (ii) there is a lagging effect between the effectivity of the funding round and its public announcement, (iii) struggling French startups are on a drip of State-backed aids and we are still waiting for a wave of layoffs and bankruptcies in the ecosystem.

French startups raised €2.3bn through 237 deals in H1-2020 - implying a 12% decrease in amount raised compared to H1-2019 (€2.7bn raised) but a 11% increase in number of deals (214 deals).

I broke down the first half of the year into months and quarters to have a more granular analysis of the situation. The year 2020 got off to a great start with January being the best month ever for French fundraising rounds with €763m raised through 51 transactions.

The hard lockdown period in France was between mid March and mid May. March and April were the two months which saw both a decline in terms of amount raised and number of deals compared to last year because less transactions happened but also because it was not a good period to announce a fundraising.

I believe that numerous fundraising announcements were delayed until May explaining the strong recovery with 45 transactions announced for a total amount raised of €554m. But the negative impact seems real when looking at June data with a 52% decline in amount raised vs. June 2019 (even if we take out the €205m funding round of Meero in June 2019, this is a 32% decline in amount raised).

The number of deals has suffered less that the amount raised during the crisis. As a result, the average deal size has declined from €12.4m to €9.9m between H1-2019 and H1-2020 (21% decline).

When you break down the deals by amount, you see that the decline is coming mainly from the growth stage with rounds > €20m. The early stage (< €20m corresponding to seed and series A) is still growing compared to last year (26% YoY growth for rounds below €5m and 13% growth for deals between €5m and €20m).

France Compared with the Rest of Europe

French public arm Bpifrance has taken massive actions to support local startups - at a much more important scale than any other European countries. €5.2bn are being deployed through different measures including €160m to finance equity bridges together with existing investors, €2bn in loans with low interest rates backed by the State (PGE), €1.5bn in tax savings, €250m in subsidies to fund innovation, €1.2bn to "protect" French tech companies from foreign investments etc. French startups have also benefited from partial unemployment measures and it was not uncommon to see startups with 50%+ of their workforce under partial unemployment.

Looking at Dealroom data on European funding rounds in H1-2020, France seems to be one of the most resilient countries with the UK and the Netherlands (less than 15.0% decline in amount raised vs. 18.5% decline for all European funding rounds). Having in mind the outstanding figures for January and the new slowdown in June, I will not over-emphasise this resilience.

What Should we Expect in the Coming Quarters?

So far, the French economy has been relatively preserved by public measures implemented by the State (State-backed loans and partial unemployment being the most impactful measures).

BPI has done a great job at deploying these measures and others in the tech sectors. As a result, we did not experience massive bankruptcies and layoffs as it happened in the US. But it does not mean that we will not have them.

The State will take a step back from supporting its economy and we will have to wait until then to measure the real impact of covid on French startups. Some signals are worrying (e.g. decline of the amount raised in June, number of employees stagnating or even declining in the most funded French startups).

Nevertheless, I'm 100% convinced that startups will be much more resilient during this crisis: (i) we are going forward and not backward in terms of digitization of our economy (e.g. remote working, tele-health, ecommerce, etc.), (ii) startups are not levered and most of them are used to losing cash every month, (iii) entrepreneurs have been amazing during these months and have proven that they are much more agile to adapt to new circumstances than more traditional companies.

I believe that the impact of this crisis will remain limited at early stage. Capital is here to be deployed at seed stage and series A. Investors will be willing to make the early bets. It will get more complicated at later stages for which we will have a polarization between tier one startups that will become overfunded and other startups that will struggle to raise growth rounds. Tomasz Tunguz described in 2017 the series B as the "hardest round to raise". I agree with him and I think that this statement will be more relevant than ever in France in the upcoming quarters.

Foreign Investors Update

Despite the covid crisis, the percentage of rounds with a foreign investors is still increasing in 2020 with 17.3% rounds involving a non-French investor (vs. 16.5% in 2019, 10.4% in 2018 and 9.9% in 2017). There is also no substantial decline between Q1 and Q2 2020 (18.4% vs. 16.3%).

I looked at all the foreign funds with more than 4 investments in France since 2017. As I said in my previous post, Index, Balderton and Accel have been the most consistant foreign investors in France. Seed funds like LocalGlobe, Samaipata, Point Nine and Speedinvest are also increasingly investing in France. These seven funds all have French people in charge of covering the French market.

In 2020, new foreign funds have also signed their first cheque to invest in French startup: Blossom Capital into Api.video, Lakestar into Bellman, Boldstart into Cycle, Tencent into Qonto and Lydia, Temasek into ManoMano and Alan.

Industry Breakdown and Trending Investment Themes

Industry Breakdown

Let's now take a closer look at the total invested by industry. Despite the difficulty of having consistent set of data, we can draw a few conclusions on the most attractive sectors for VCs.

Finance (18% of total amount invested in H1 2020), Retail/Ecommerce (17%) and Marketing (12%) occupy pole positions. Finance is not a big surprise since it already was the most attractive space for VCs last year, contrary to retail/ecommerce whose share jumped from 2% of the total invested in 2019 to 17% in 2020, mainly due to the big funding rounds of ManoMano, BackMarket and Vestiaire Collective. Marketing has always been a hot topic and the past 6 months were no exception to the rule with the €175m Series D of the new unicorn Contentsquare, as well as other impressive rounds like the large Series A of PlayPlay led by Balderton.

HealthTech is one of the most vibrant industries in France but only accounted for 3% of the money invested since January 2020. Fortunately, the investments in healthcare were more qualitative than quantitative, with promising startups funded like Inato (€12m with Obvious Ventures and Serena) in the patient recruitment space.

HR was a hot sector in the past 6 months, as 8 HR-related startups raised €5m or more (second highest total behind Finance). The most significant funding rounds in this sector include Lumapps (€63m with Goldman Sachs and Bpifrance), InsideBoard (€25m with ISAI, Orange Ventures and AXA), Hivebrite (€18m with Insight Partners) or Powell (€16m with CapHorn and Level Equity).

Hot Trends

D2C brands. No less than 17 French D2C startups raised funds in the last 6 months. This emerging trend is still at its early stages, proof of this can be seen in the average amount of funding (around €1m). BonneGueule raised €6m (with Generis Capital and Bpifrance) for its online clothing blog for men turned fashion brand, Spring raised €2m (with Ventech, Eutopia and Aglaé) to launch its laundry products and Jho got €2m (from XAnge, Founders Future and Bamboo Capital) to grow its sanitary towels brand, to mention just a few.

Sustainability. It goes hand in hand with the rise of D2C brands: BonneGueule highlights responsible products, Spring is developing "clean" laundry products, Jho's tampons are made of organic cotton... The top 15 of funding rounds also gives prominence to sustainability with EcoVadis (CSR ratings for companies to evaluate their suppliers), Back Market (refurbished IT products) or Vestiaire Collective (second-hand fashion goods).

Amazon verticalization. In addition to ManoMano's Series E, we observed several companies raising funds to develop verticalized marketplaces competing with Amazon: Snowleader (€10m with Sofimac and BNP Paribas), an online store for mountain equipment, or Colizey (€2m with Kima and Aglaé), an ecommerce website for sports goods. In an area somewhat further away from Amazon's offer (for now, but who knows what will come next!), Singulart (€10m with Ventech) launched a platform to buy pieces of art.

Audio vs. video. Both of them have seen notable funding rounds in the past 6 months in France. On the audio side, music mobile app studio MWM closed a €50m round with Idinvest, Blisce and Bpifrance. The French podcast industry has been quite active too: podcast management solution Ausha (€1m) and podcast studio Louie Media (€500k) are two interesting cases. On the other hand, video-related startups attracted Tier-1 investors: PlayPlay raised €10m with Balderton and Api.video got a €5m funding from Blossom Capital.

Data management. Data is definitely too often seen in the hot topics section. However, it cannot be denied that the past 6 months have seen great startups raising funds: DataOps platform Saagie (€25m with Crédit Mutuel, NewAlpha and Seventure), BI software dedicated to local authorities Manty (€2m with Axeleo and Kima) or privacy-first data analytics platform Sarus (€2m with XAnge and Serena).

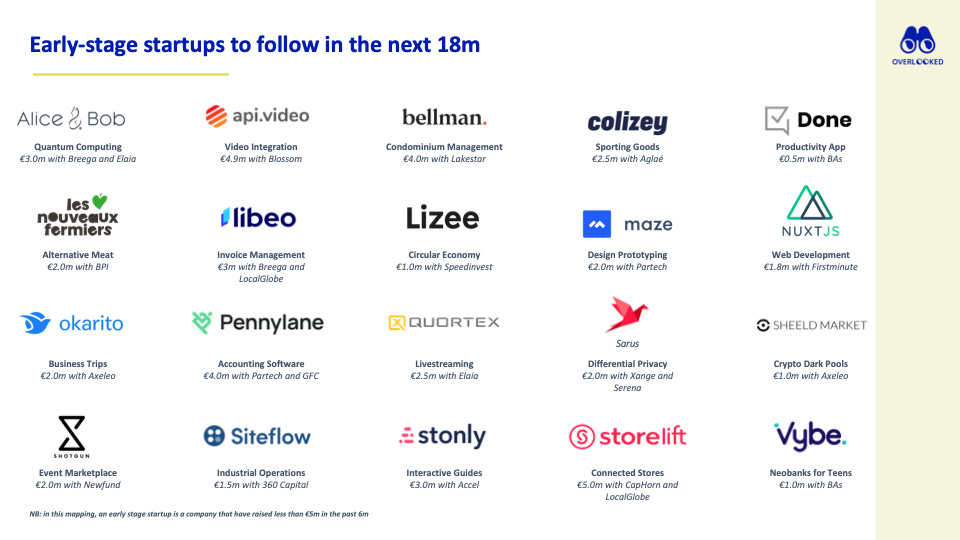

Early Stage Companies to Follow in the Next 18 Months

Most of the times, in these funding round reviews, we discussed only the companies which raised the biggest rounds. I believe that younger companies also deserve to be in the spotlight. Therefore, I made an arbitrary selection of companies that raised in the past 6m less than €5m and that you should follow in the coming years.

The selection is based either on (i) investors (e.g. Blossom investing into api.video), (ii) trendy topics (e.g. Alternative Meat with Les Nouveaux Fermiers, Quantum Computing with Alice & Bob, Privacy with Sarus), (iii) exceptional founders (e.g. Gilles Raymond at Done, Arthur Waller at Pennylane).

🚨 Data Accuracy Warning 🚨

It's impossible to have a 100% coverage of the funding rounds announced publicly. I did my best to build a database over the past four years. I'm conscious that certain funding rounds will be missing and that other will contain wrong or incorrect information.

Having said this,

1/ I still believe that this exercise of interpreting the funding round data is useful to have an overview of our ecosystem and to detect the trends discussed in this paper,

2/ the database is open to anyone and if you want to correct / add a funding round, drop me an email (ade@idinvest.com) and I will modify the base. Most of the charts in this paper will be automatically updated in the Block section of Airtable.

Resources

🗞 Are VCs Still Investing? (Christoph Janz, Jun. 2020)

🗞 Q2 2020 Global Venture Report: Funding Through The Pandemic (Crunchbase, Jul. 2020)

🔎 Europe Stepping Up to Global Tech Leadership (Dealroom, Jul. 2020)

🗞 VCs are Cutting Checks Remotely, but deal volume could be slowing (Tehcrunch, Jul. 2020)

🗞 Hyperactive (Fred Wilson, Jul. 2020)

🗞 Not so Hyperactive (Fred Wilson, Jul. 2020)

🔎 Venture Monitor (Pitchbook, Jul. 2020)

🗞 Q2 shows risk appetite in European tech is back. But not everywhere (Dealroom, Jul. 2020)

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋