🏗 Vertical Solutions in the Construction Space in Europe

Overlooked #162

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing a personal investment thesis on vSol as industry operating systems (OS).

This is the fourth article in my series dedicated to the construction industry. In my previous pieces, I covered Procore and ServiceTitan which are both category leaders in the construction industry. I also shared a personal thesis on arguing that the best vertical Solutions (vSol) have the potential to evolve into industry operating system (OS) building and monetising products for multiple stakeholders in the industry they target. This post is about European startup trends in the construction industry. If you build or invest in the construction industry, I’d love to meet you! You can reach out at adewez@eurazeo.com.

Why Construction is Exciting?

It’s a massive market. In Europe, in 2022, the sector contributed to c.10% of the GDP ($1.5tn) and employed 11.1m workers (6.4% of total employment).

It’s extremely fragmented. There are 3.2m construction companies in Europe including 340k in the UK, 440k in Germany and 424k in France. 94.1% of companies have less than 10 employees and 5.3% companies have between 10 and 50 employees.

It suffers from low productivity growth compared to other sectors. Labor productivity grew by 1.0% per year in the past 2 decades compared to 2.7% for the total economy and 2.7% for the manufacturing sector.

It’s a low margin business. Large construction companies achieve an EBITDA margin between 8 and 12%, while smaller construction companies typically have an EBITDA margin below 5% (on average 4% for companies between 10 and 50 employees and 1% for companies with less than 10 employees).

It’s underdigitized. According to the McKinsey Industry Digitalization Index, only the agriculture sector is less digitized than construction. The typical IT spend for construction companies is 1-2% of the revenue, compared with the 3-5% average across industries. Moreover, there are many barriers to digital technology adoption including skill management issues, reluctance to change, lack of budget and time allocated.

It’s a greenfield market. Most SMBs are being digitally unequipped. Over 50% are still managing their business using pen, paper, and Microsoft Office. 60% of construction companies don’t use a cloud based construction management software.

There is currently a massive labor shortage. In the US, an estimated 41% of the current US construction workforce is projected to retire by 2031 and there are 440k vacancies in the sector in 2023 (vs. 300k in 2019). Furthermore, the number of individuals entering the construction workforce is declining annually in developed countries.

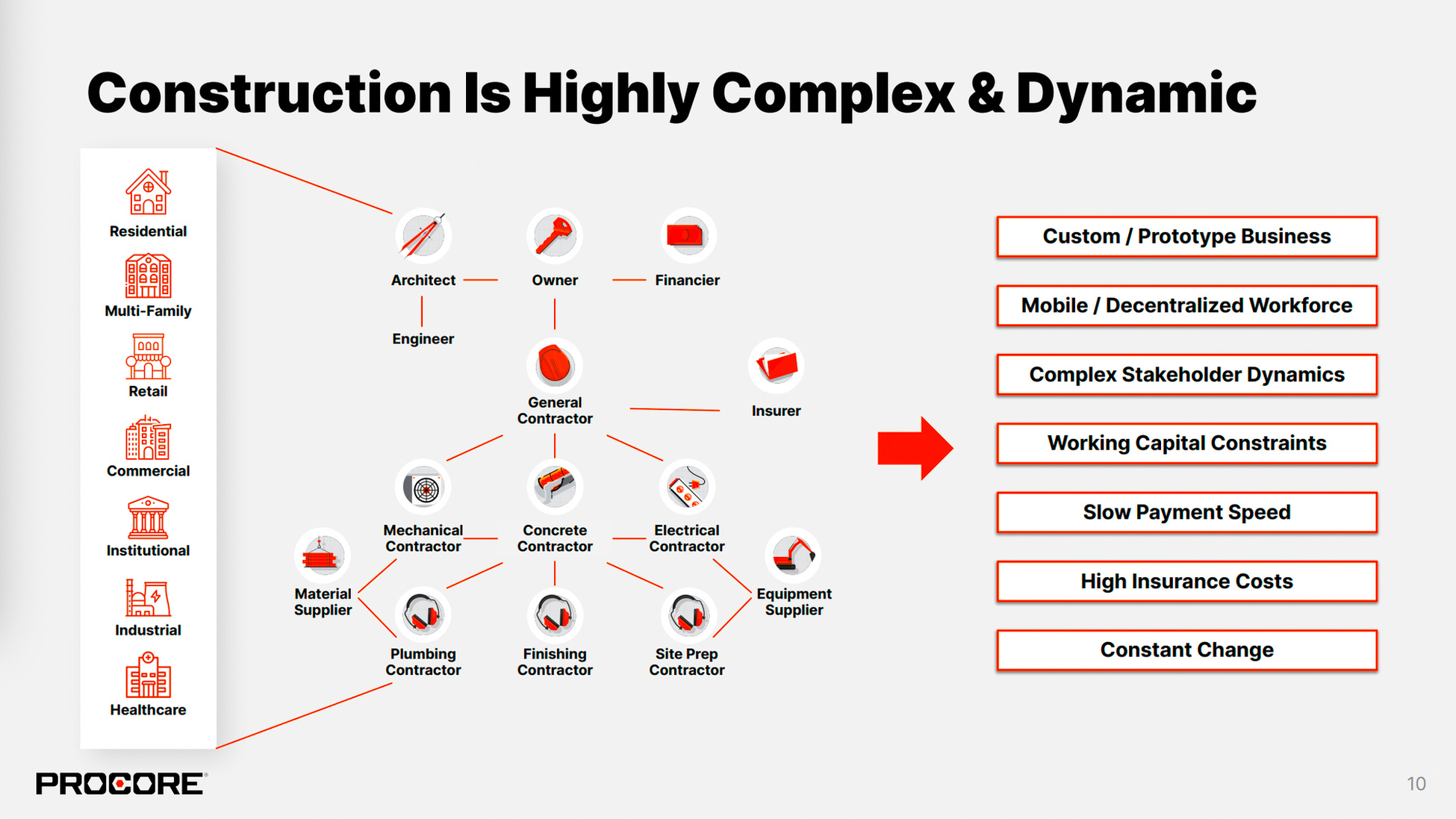

In a given construction project, there are often many stakeholders involved, especially in large projects:

Owners: They initiate construction projects, working with architects and engineers to design the project. They also hire a general contractor to operationally build the project.

General Contractors: They work for owners and are responsible for leading construction projects. They hire and coordinate specialty contractors.

Specialty Contractors: Specialty contractors are hired for their specific skills, such as electrical, plumbing, roofing.

Architects and Engineers: They collaborate with owners and general contractors in the project's design.

Financiers: They fund the project through equity or debt, which is released progressively when milestones are hit.

Insurers: Insurers protect the project against unforeseen events, such as injuries, defects, or natural disasters.

Materials and Equipment Suppliers: These suppliers provide the necessary materials and equipment to complete the project.

Trend n°1 - Financial Services for the Construction Industry

Payment delays are longer in construction than in any other industry. More precisely, it takes on average 83 days for a contractor to be paid. Only 12% of construction companies report being consistently paid on time. 83% of companies in the US have already filed liens due to slow payment. In the US, a mechanics lien is a legal instrument that suppliers, subcontractors, and contractors can leverage to recoup their labor and materials costs from the owner of a construction project for delayed payments to stakeholders.

There is a complex payment chain in the construction industry wherein the money has to flow from the top (the owner/the lender) to all the stakeholders involved in the construction project, starting with the General Contractor (GC) and going down to the different tiers of subcontractors and suppliers. Subcontractors often purchase materials upfront with a 30-day delay to pay them and typically pay their workers on a weekly basis. Subcontractors are generally paid weekly or monthly, based on the completed work's percentage. They send an invoice to the GC, who collects these invoices and ensures that the work has been done and that the subcontractor is fully compliant. The GC does the same for all subcontractors and consolidates a single invoice for the owner. The owner then conducts its own due diligence on the project before paying the GC, and then the money flows down the payment chain. GC’s payment can be done directly or done after a draw request to the funding bank. This complex payment chain in the construction industry opens up opportunities to streamline payments for startups.

Moreover, it highlights that subcontractors face cash flow constraints, bearing significant working capital needs on their balance sheets to fund workers and materials before being paid by GCs. It creates an opportunity to provide subcontractors with working capital financing to avoid being cash trapped and use their balance sheet to grow their business instead of funding working capital.

In financial services, there is also an opportunity in insurance. Construction companies are underserved by traditional insurers that use generic models to price risk in the construction sector and often charge high premiums due to perceiving the industry as extremely risky. Moreover, there are business workflows associated with insurance in a construction project like the collection of certificates of insurance for all the stakeholders. This creates an opportunity for startups to digitize insurance-related workflows and to develop a superior, tailor-made risk assessment model for the construction industry.

In 2022, Procore began expanding into financial services, focusing on the three opportunities we have just described: streamlining payments, offering working capital financing, and improving insurance in construction. In the US, Procore is competing with startups on these three opportunities. The delayed expansion of these products by Procore to Europe presents an even more interesting opportunity there.

Trend n°3 - Solving the HR Talent Shortage

A global shortage exists of skilled blue-collar workers in the construction sector, encompassing areas such as buildings, solar panels, wind turbines, and oil & gas plants. Construction companies win projects but often struggle to deliver due to recruitment challenges. At the same time, blue-collar workers lack access to a specialized job platform, transparency regarding job opportunities and salaries, and have limited options to transition between sub-sectors.

Workrise in the US and PowerUs in Europe have emerged to offer platforms that address pain points for both construction companies and highly skilled blue-collar workers. They help construction companies find talented workers for project-based or long-term employment. Simultaneously, they have created a platform similar to Linkedin for blue-collar workers, where they can easily find their next job or project, update their skills, and acquire new ones.

Another approach is building a company around temporary staffing. Large construction companies frequently work with subcontractors and temporary workers on their projects. There's an opportunity to aim to grab market share from Adecco, Randstand, and Manpower with a specialized temporary staffing agency for the construction sector. There's a demand for both low-skilled and high-skilled blue-collar workers. In France, Asap.work is pursuing this value proposition.

Trend n°4 - Riding Climate Change’s Impact on Construction

Europe’s ambitious climate change mitigation efforts include evolving the energy mix towards renewable energies and renovating buildings for greater energy efficiency. This opens opportunities for startups to develop solutions supporting construction companies, consumers, and businesses in this transition.

1Komma5 is creating a vertically integrated home-services company focused on energy renovation, such as solar installation and energy storage, augmented by technology like its in-house energy management system called Heartbeat.

Lun is developing a vertical SaaS for heat pump installers streamlining processes including lead management, quoting, installation and invoicing.

Effy operates in the residential home renovation market with a model that includes a network of contractors focused solely on execution, while Effy manages the rest, including quoting, material sourcing, and financing.

Trend n°5 - Plaid for the construction industry

In finance, Plaid has developed APIs to act as a connective tissue between financial institutions, financial applications, consumers, and businesses. Originally facilitating read/write access to bank account information, it has evolved into a broader financial platform capable of initiating payments, verifying identities, and assessing creditworthiness. This access to bank account information catalyzed the explosion of consumer fintechs in the US, such as Robinhood, Venmo, and CashApp.

In many vertical markets, tooling fragmentation and closed ecosystems are common issues. Multiple solutions are needed to run a business, and these solutions often lack interoperability. Moreover, different stakeholders use various solutions that could generate significant value if interconnected. This is why a verticalized version of Plaid can be impactful, particularly in construction.

In the US, Agave is building a “Plaid for the construction industry”, connecting 30 different systems via APIs. Agave provides software vendors in the construction industry with the ability to offer integrations with all relevant vendors. It also enables contractors to synchronise data between different software and build analytics pulling data from multiple tools.

Trend n°6 - Unbundling ServiceTitan by building vSol focused on specific trades

ServiceTitan is currently the most valuable private vertical solution (vSol). Its last funding round valued it at $9.5 billion, and it aimed for a $20 billion valuation for its public debut before the public market downturn. Initially a highly specialized SaaS, it has now evolved into a more horizontal platform, opening the door for new players to unbundle ServiceTitan.

ServiceTitan began as a vSol dedicated to plumbing, but it quickly expanded to include other trades such as HVAC and electrical. Currently, it serves 21 different trades, such as HVAC, plumbing, electrical, garage door, chimney, and many others.

There is potential to unbundle ServiceTitan by developing a vSol specifically tailored to the business workflows of a particular trade. For example, in the U.S., Broadlume is focused solely on flooring, Rooparis on commercial kitchen repairs, and Rundoo on painting. In Europe, the opportunity to build a vSol for a specific trade not only exists but is likely the most strategic first step in replicating ServiceTitan’s success on the continent.

Trend n°7 - Streamlining the Contractual Work around Construction Projects

Construction is a heavily regulated industry. In North America, the number of regulations related to construction (e.g. related to workers' safety or the environment) increased from 463 in 1970 to 5.2k in 2017.

Furthermore, construction is a complex industry where multiple stakeholders are involved in the same construction project, from project owners to general contractors, subcontractors, suppliers, and workers.

As a result, the industry needs solutions that streamline contractual work in construction projects at all stages, from pre-construction (tendering & bidding) to procurement (subcontractor and supplier agreements, purchase orders), and from construction (construction contracts, change orders) to post-construction (dispute resolution agreements, warranty & maintenance, closeout).

For example, startups like Pulley ($4.4m seed in Jun. 2022 led by Susa) and PermitFlow ($5.5m seed in May 2023 led by Initialized) are streamlining contractual work related to the permitting process. They develop software that handles all municipal requirements for construction projects (19k different jurisdictions in the US), aiming to reduce the cost and time associated with the permitting process. Additionally, they've assembled networks of local experts to assist with regional specificities.

It’s an interesting entry point into the construction software stack because construction permitting is upstream in the construction process. All documents and construction project information collected could be leveraged to build products for downstream steps in the construction process, such as in pre-construction for budgeting and in bid management.

Trend n°8 - Mobile First Products for Workers in the Field

In many vertical markets, there is an opportunity to build mobile-first products, especially for field workers, such as blue-collar workers in construction or nurses in healthcare. Solving tech adoption in the field is key to disrupting incumbent platforms using a bottom-up approach and a differentiated business model.

I believe that adoption from the field is powerful because often, these workers are the least digitized. They often have to perform redundant tasks, entering information into poorly designed systems (e.g., a nurse going back to a computer after seeing several patients to re-enter patient information into the system, or a construction site manager returning to the office at day's end to document field activities). They are also the ones facing massive labor shortages.

Regarding the business model, these mobile-first products tend to be freemium to encourage adoption from the field before charging for more complex modules, which are adopted and paid for by the office, for instance, safety & quality reports in construction.

Trend n°9 - Leveraging Computer Vision to Increase Construction Productivity

Computer vision offers significant opportunities across various verticals. In construction, it can be used for tasks like site monitoring, quality control, progress tracking, safety monitoring, risk mitigation, and worker productivity.

For example, in the US, Openspace (which raised $200m from investors such as Lux, Menlo, and Alpaca) utilizes cameras mounted on helmets or drones to capture an experience similar to Google Street View of the job site. This can be juxtaposed with the initial construction plans and leveraged for multiple use cases, including change orders and punch lists.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋