📖 Venture Chronicles - September 2023

Overlooked #157

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of September.

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Friday, Sep. 1st: Hugo Amsellem published a great deep-dive on the loneliness economy. - Hugo Amsellem

Despite being constantly connected to each other thanks to the internet, we have never been as lonely as we are today. Hugo’s thesis is that technology can help us belong by mimicking institutions (religion, family, neighborhood, friend group, couple, and company) which have historically played a significant role in fostering a sense of belonging.

60% of Americans are lonely. “The younger you are, the more likely you are now to feel lonely.” “Loneliness is now one of the most important problems our generation has to solve, alongside climate change and obesity.”

If we’re becoming less religious, we are gradually substituting religion with other forms of cults like astrology, wellness clubs, or group therapies (e.g., Alcoholics Anonymous for X).

“Only 25% of people living in urban areas actually socialize with strangers at least once a week.”

“I believe the pandemic has brought us to a tipping point with loneliness. First, most of us experienced social isolation during lockdowns and realized it made us unhappy. Second, many have grown accustomed to solitude and haven't yet returned to their previous levels of social activity. Third, we've lost numerous connections with friends, co-workers, and acquaintances as people moved or started working from home.”

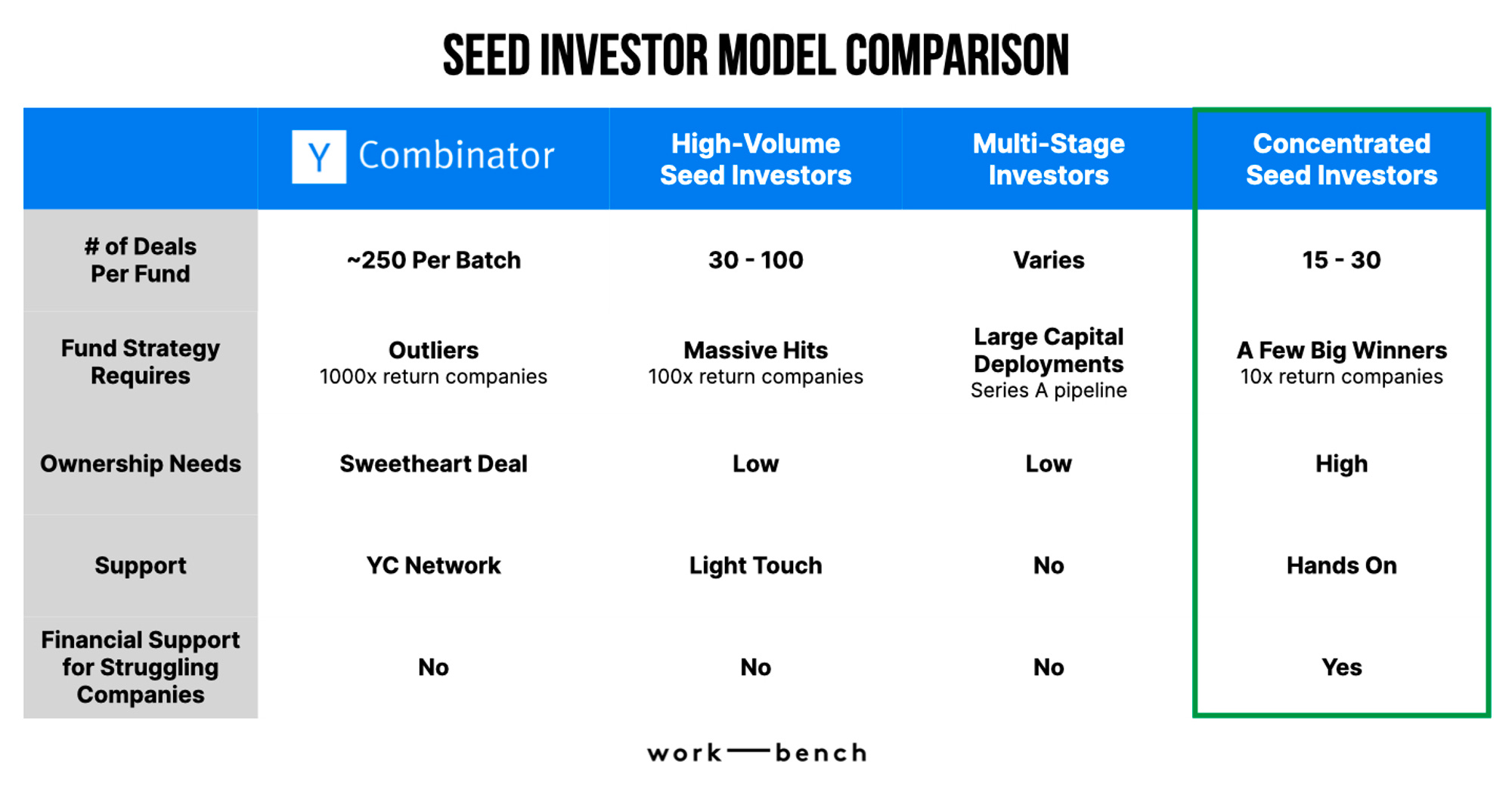

Saturday, Sep. 2nd: Jonathan Lehr (GP at Work Bench) wrote an interesting paper comparing the incentives of the different players you can raise money from at seed stage. - Techcrunch

“What’s important to understand is that YC’s goal is around finding and investing in extreme outliers.” “Raising a $2 million SAFE at a $20 million cap limits the type of investor you can pitch (whether the company realises it or not) and raises the bar for the milestones needed to raise a Series A.”

“The nature of partnering with a high-volume seed firm is that their strategy provides limited hands-on resources for portfolio company support. Given their exposure to so many startups, these firms often focus on community and content initiatives.”

“While multistage firms often tout seed-stage investments as being important and getting full support of their firm, in reality they get limited time with their partner and limited access to broader firm resources.”

“I’d strongly recommend not raising a $2 million SAFE on a $20 million cap. Pricing too high at such an early stage is rife with issues that can plague the company’s growth if it doesn’t operate to perfection.”

Sunday, Sep. 3rd: Gil Dibner (GP at Angular) wrote about what will happen in the next 18 months in the tech ecosystem. - Gil Dibner

“The bridge rounds and the burn rate cuts of 2022 set many companies up with enough runway to get through the year — and so the crucial question has become in what condition will we exit the year? Will growth be impressive enough to attract investment? Will runway be long enough to reach breakeven in 2024 or will a round be necessary?”

“For founders, if 2022 was a year of realisation, 2023 is a year of execution in a new and very challenging reality.”

“In 2024, I expect we are going to start to see the clouds lift a bit. Customer budgets may start to recover which may make it easier to grow revenues. Some optimism will inevitably return to the hearts of investors. IPOs, slightly lower interest rates, and perhaps an end to the war in Ukraine may contribute to a more optimistic vibe.”

“Next year may see the dawn break. It will not be roses and unicorns, but we are likely to return to a much more functional market in which customers are willing to buy and investors are willing to price risk.”

Monday, Sep. 4th: Ryan Hoover (GP at WeekFund & founder at Product Hunt) shared learnings from decks used by VCs to raise money from LPs. - Ryan Hoover

“The purpose of your pitch deck is to convince LPs in your ability to make outlier investments. Making exceptional investments relies on access, sound decision-making, and an ability to win deals. Your pitch deck should breakdown how you do this effectively.”

“Let others speak to your strengths and establish social credibility. As with GPs investing in startups, many LPs value social proof, consciously or subconsciously. Highlight positive quotes from founders you’ve backed, testimonials from strong references, and LPs already committed to investing in your fund.”

Tuesday, Sep. 5th: Hexa (ex. eFounders) launched a new initiative called “second life” to give a second chance to VC-backed seed/series A startups which are about to go bankrupt because they can’t exit the business or reach breakeven. - Hexa

“Especially in today’s macroeconomic context, many VC backed companies, flush with recently raised capital, are likely about to meet a hard reckoning.”

“At Hexa, we want to give founders another path. If you don’t want to go the breakeven and M&A routes because of the potential hurdles described above - then we want to give founders the opportunity to turn it around.”

“The type of companies which would benefit from this second life alternative and our help would be early-stage companies that have already raised early-stage funding (Seed, Series A), who are generating recurring revenue with low burn in sight and have reached the first signs of product market fit but who are no longer “VC” fundable because of slow market traction or lower than expected growth, or other similar reasons. We will focus our efforts on B2B SaaS companies in France and Belgium, as those are our areas of expertise and geographical locations.”

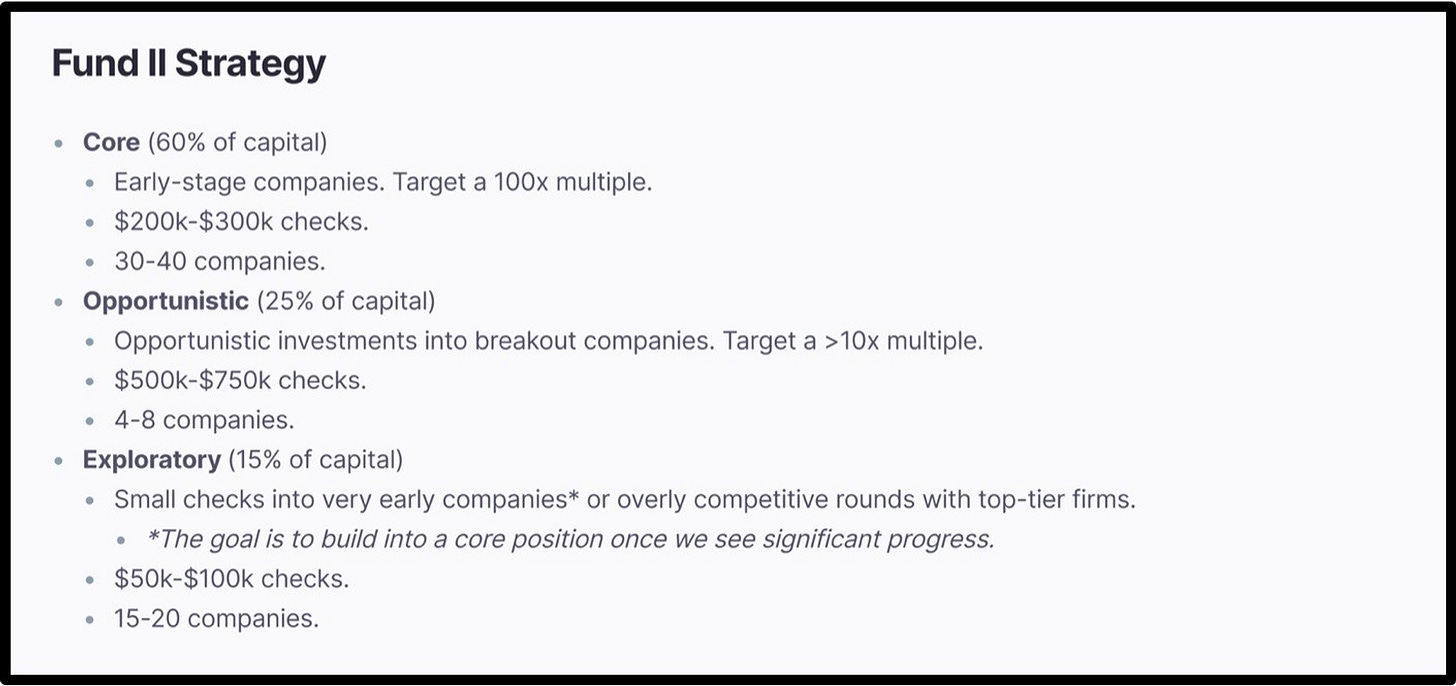

Wednesday, Sep. 6th: I listened to a 20VC’s podcast episode with Finn Murphy. - 20VC, Finn Murphy, Sifted

Finn created a solo-GP fund called Nebular leading pre-seed and seed rounds in software companies in Europe and in the US. Finn is raising a $25m fund ($500-1.5m tickets, 5-6 tickets per year). He has closed $15m and has already invested into 5 companies including Co:Helm, Teton and Trace.Space. He will keep 20-30% of its fund for follow-ons and he targets a 10% average ownership.

He previously worked at Frontline for 4.5y where he was involved in 20 investments and 8 angel investments on the side.

“In the last couple of years in venture, everyone has been trying to derisk an asset class that is inherently averse to derisking. That’s not the point of venture. The point of venture is to take big risk and to have a chance at outlier upside. You don’t make money in venture by hedging your bets.”

Finn does not chase founders who are high signal (repeat entrepreneurs, experienced operators) because most of these deals are too competitive. He looks for individuals who have deviated from the traditional career path (not following the typical trajectory of attending top schools, working in consulting, or joining high-growth startups before becoming founders). The initiative to do the thing that is not in the standard path is a great signal to find founders who can be successful without supporting systems around them.

“The way to make real venture returns is through having differentiated opinions.”

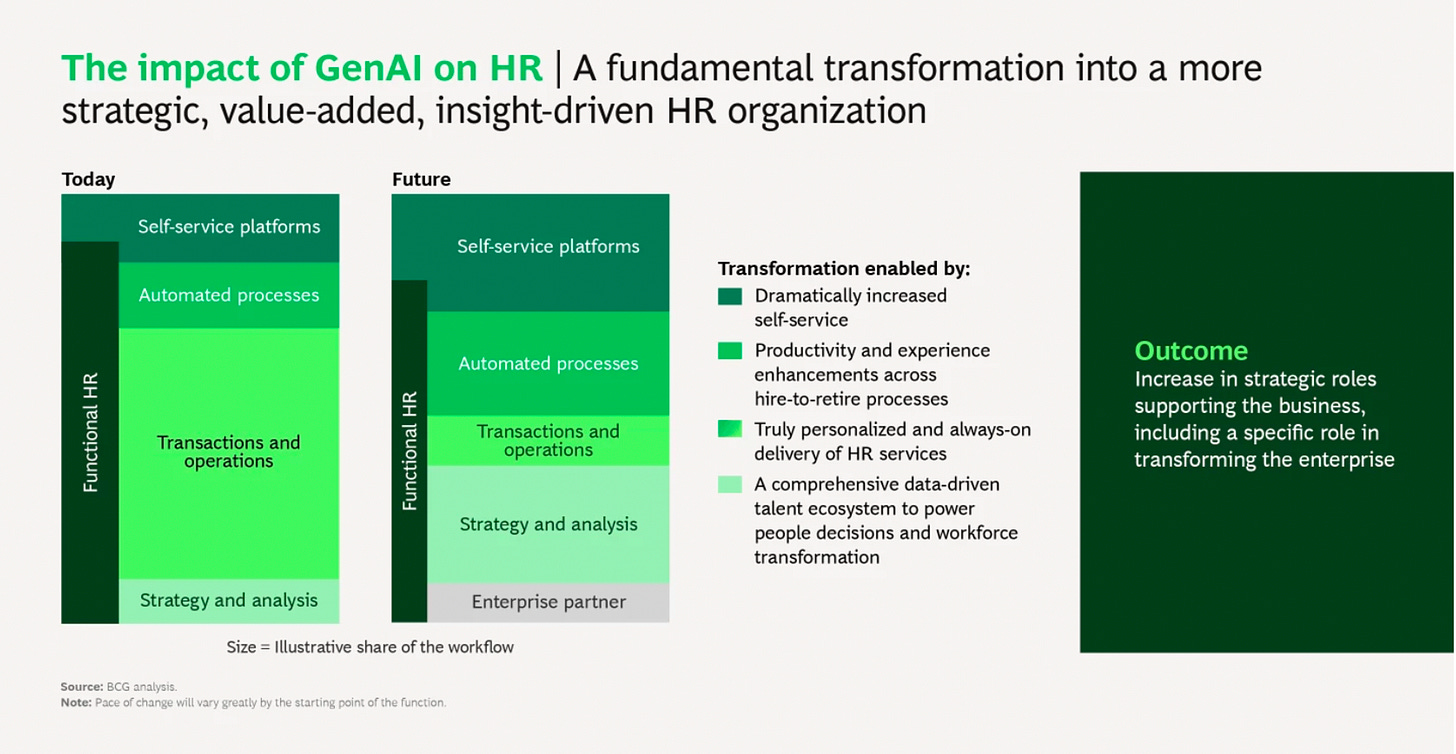

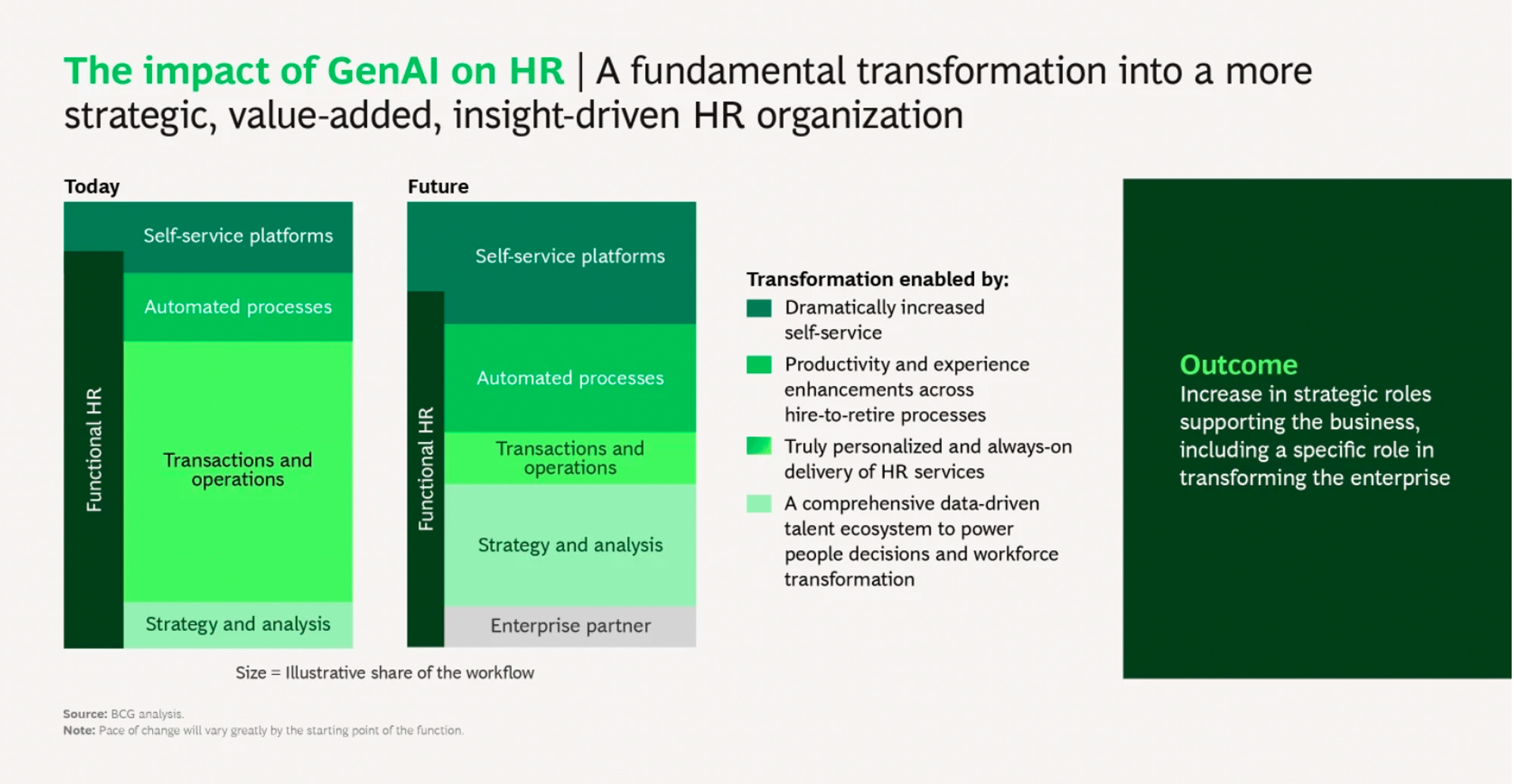

Thursday, Sep. 7th: BCG published a report on how Gen. AI will transform HR. - BCG

“With stronger automation and data insights, current GenAI use cases show 3x faster content creation and visualization, automation of greater than 50% of tasks in an onboarding journey, and recruiting engagement rates that are twice as high as when personalized messages were written with GenAI.”

Gen. AI will increase HR self-service thanks to more conversational workflows and tailored information which was previously missing to have high adoption rates.

Friday, Sep. 8th: Roblox held its 2023 Roblox Developer Conference. - Roblox

It launched Roblox Connext. “Connect will enable people to call a friend from their Roblox friends list using their real name and facial expressions and be transported to a shared immersive space on Roblox for their conversation, sitting together by a campfire or standing beside a waterfall.”

It launched Assistant. It’s a conversational AI to make creation on Roblox more accessible. It’s “a conversational AI that makes creation on Roblox more accessible and empowers advanced creators to build richer, more engaging experiences faster.”

Roblox is also waiving its Creator Marketplace fee to enable creators to keep 100% of the proceeds from items they created.

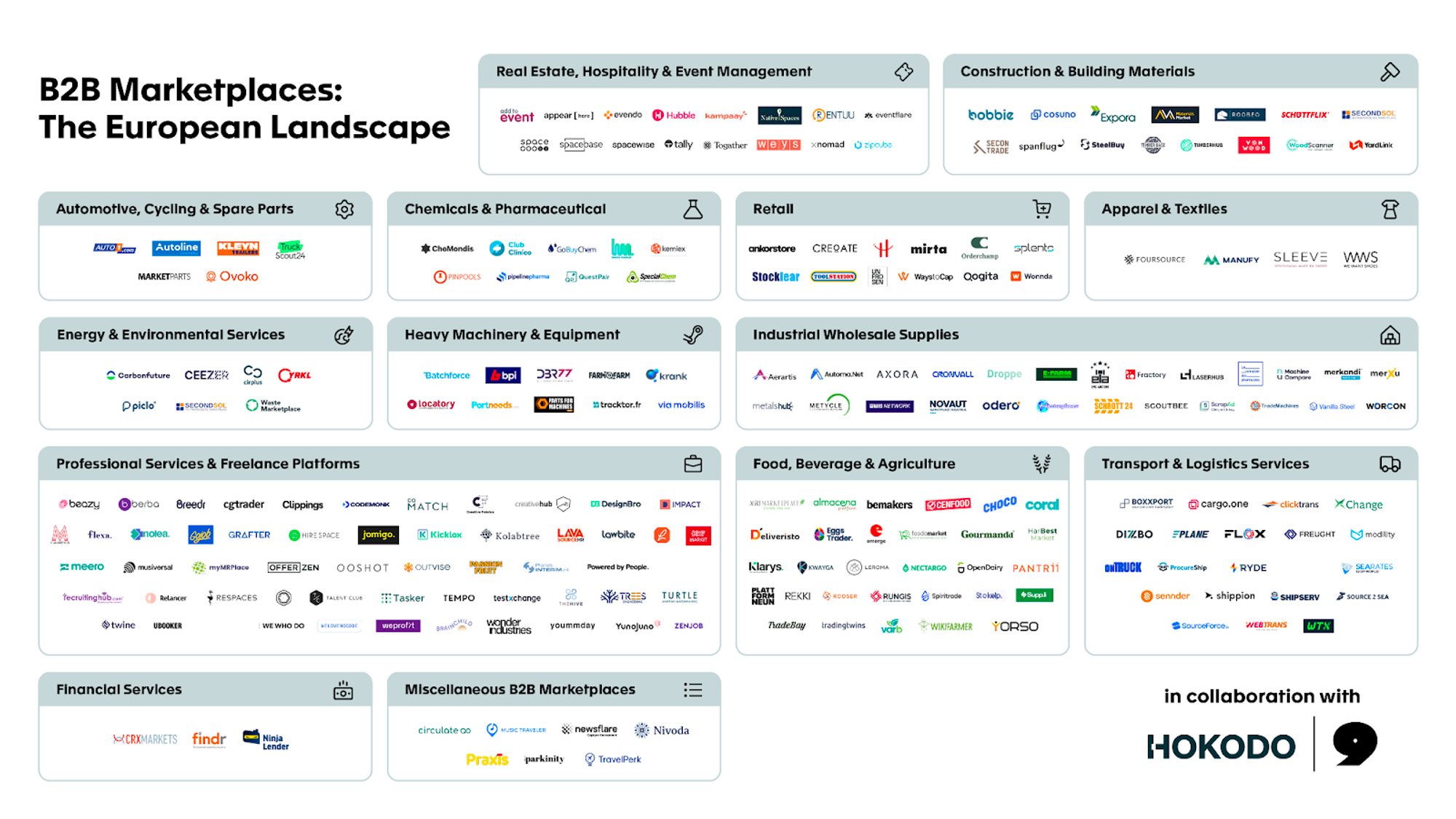

Saturday, Sep. 9th: Louis Coppey at P9 published an updated version of P9’s B2B European marketplaces map and shared some learnings on building & scaling B2B marketplaces. - P9

“There are approximately 15 to 20 new B2B marketplace businesses created every year in Europe.”

“The best founding teams [in B2B Marketplaces] often come from the epicenter(s) of the industries they’re trying to digitize rather than from startup hubs. For example, Container xChange in the container logistics industry is based in Hamburg, one of the largest ports in Europe, while cargo.one started in Germany and partnered with Lufthansa, the largest European cargo airline.”

“The previous funding environment favored (GMV) growth (at all costs), and we now see a pretty significant shift back (overreaction) to focusing on net revenue, gross margin, and profitability. Just like in SaaS where public markets have realized that revenue multiples should be adjusted on a gross margin basis, we see more and more investors valuing marketplaces on net revenue and/or gross margin multiples instead of their historical use of ~1x GMV.” With this in mind and as founders think about future financing rounds, one of the strictest (and probably overly strict) ways to run a B2B marketplace these days is to operate it like a SaaS business, setting targets on a net revenue and/or a gross margin basis assuming they are the equivalent of ARR and/or gross margin in SaaS.”

“B2B marketplaces tend to develop business models that are more sophisticated than their B2C counterparts, often mixing (low) take rates with SaaS fees and charging a margin on top of value-added services like logistics or financing.”

Sunday, Sep. 10th: Voss Value published their investment thesis into a publicly listed vSaaS company called i3 Verticals selling software and financial services to the public (e.g. municipalities for utility payments, states for auto registration billing) and healthcare sectors. - Voss

“i3 Verticals was originally known as more of a pure-play payment processor, but over the last few years, the company has employed a software acquisition strategy whereby they acquire the software assets and then layer their payments engine onto the acquired businesses to fuel organic growth. Through the implementation of this strategy, i3 Verticals has been rapidly shifting to a higher mix of recurring SaaS revenue and transitioning from majority “payments” revenue to a majority “software” company.”

“It is our thesis that the market will soon take notice of this positive mix shift and value the company more as a software firm than a pure payments company. Profitable, growing payments companies tend to trade closer to what i3 Verticals’ trades at (9-12x EBITDA), while software companies with similar profiles will tend to trade closer to 15-20x, or higher, especially those with noncyclical end customers like i3 Verticals’s.”

“The company claims that with their more complete offering of software solutions to state agencies, they are now being invited to and winning more RFPs at a larger scale. Their management team has reiterated over the last few quarters that they have made substantial progress in integrating their 48 acquisitions since 2018 into more complete sub-vertical solutions that can win statewide mandates.”

“i3 Verticals management team has exhibited a disciplined approach to M&A. In an era when many executives and buyout firms were paying >10x revenue for young and growing software firms, i3 Verticals has not paid >10x EBITDA for small software tuck-ins.”

Monday, Sep. 11th: Ben Robinson wrote about fintechs. - Ben Robinson

“Fintech is still a massively viable and flourishing sector for innovation: it’s the world’s most profitable vertical market with the most legacy infrastructure and digital services, still riddled with inefficiency and ripe for disruption.”

For fintech startups, it’s hard to replicate the distribution edge that large financial firms (based on the fact that they’re incumbents and that they are trusted institutions) and social networks (based on their product virality and network effects) have.

Successful consumer fintechs have all started with a “killer first product” with sufficient virality to attract a meaningful user base before expanding into an all-in-one finance platform bundling multiple products (e.g. Revolut starting with FX) to grow their customers lifetime value.

“There is a big role for vertical SaaS in distributing financial services to SMEs.” “Products will be increasingly embedded at the point of need. Product insurance will be sold when and through the same channel as the product is purchased, product financing will be sold when and through the same channel the product is purchased, payment will be made when and through the same channel as the product is purchased, etc.” “Vertical SaaS platforms become the ideal medium for distributing financial services to SMEs. This is because they have both high engagement, and the data to be able to offer and price financial services correctly.”

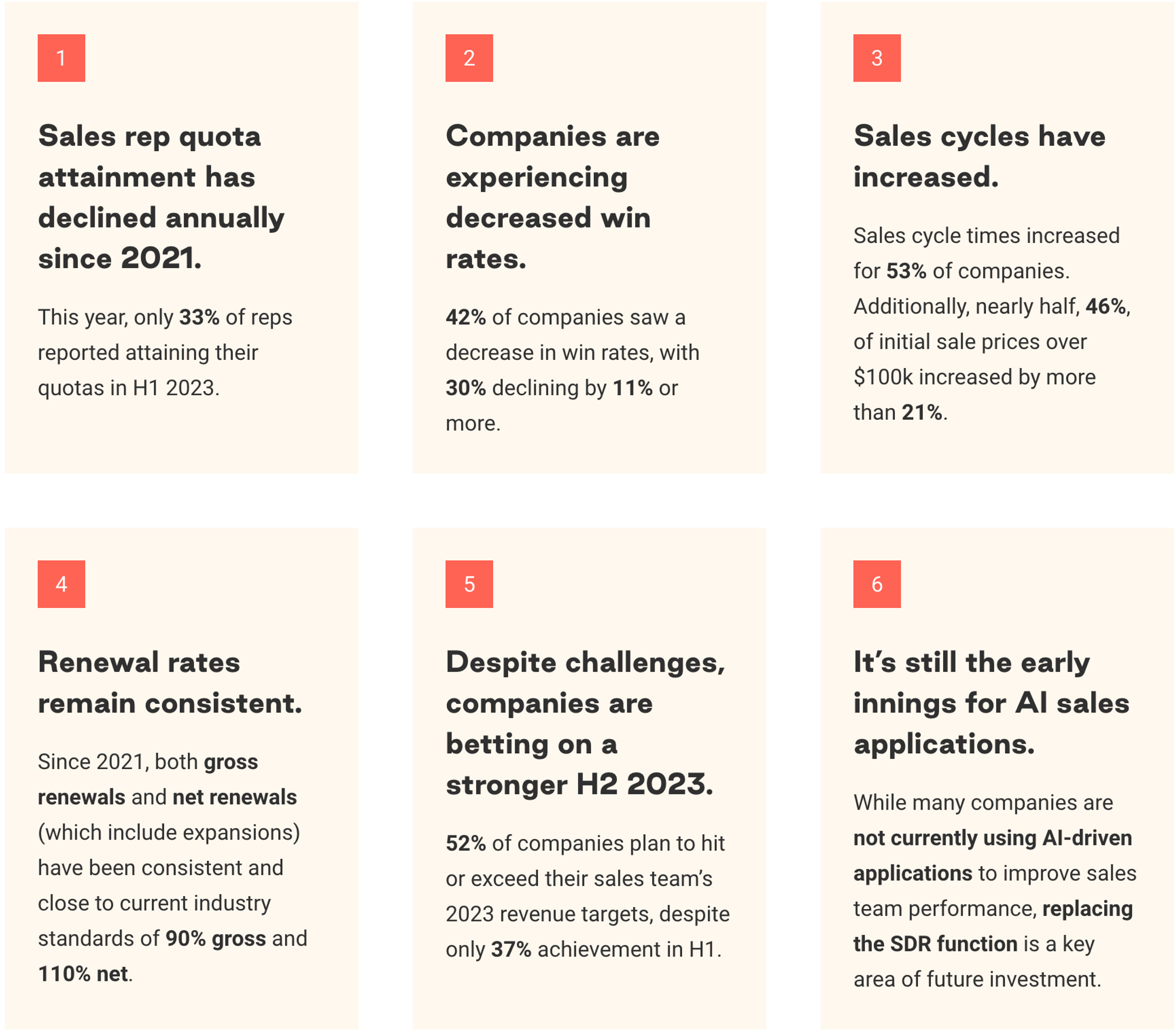

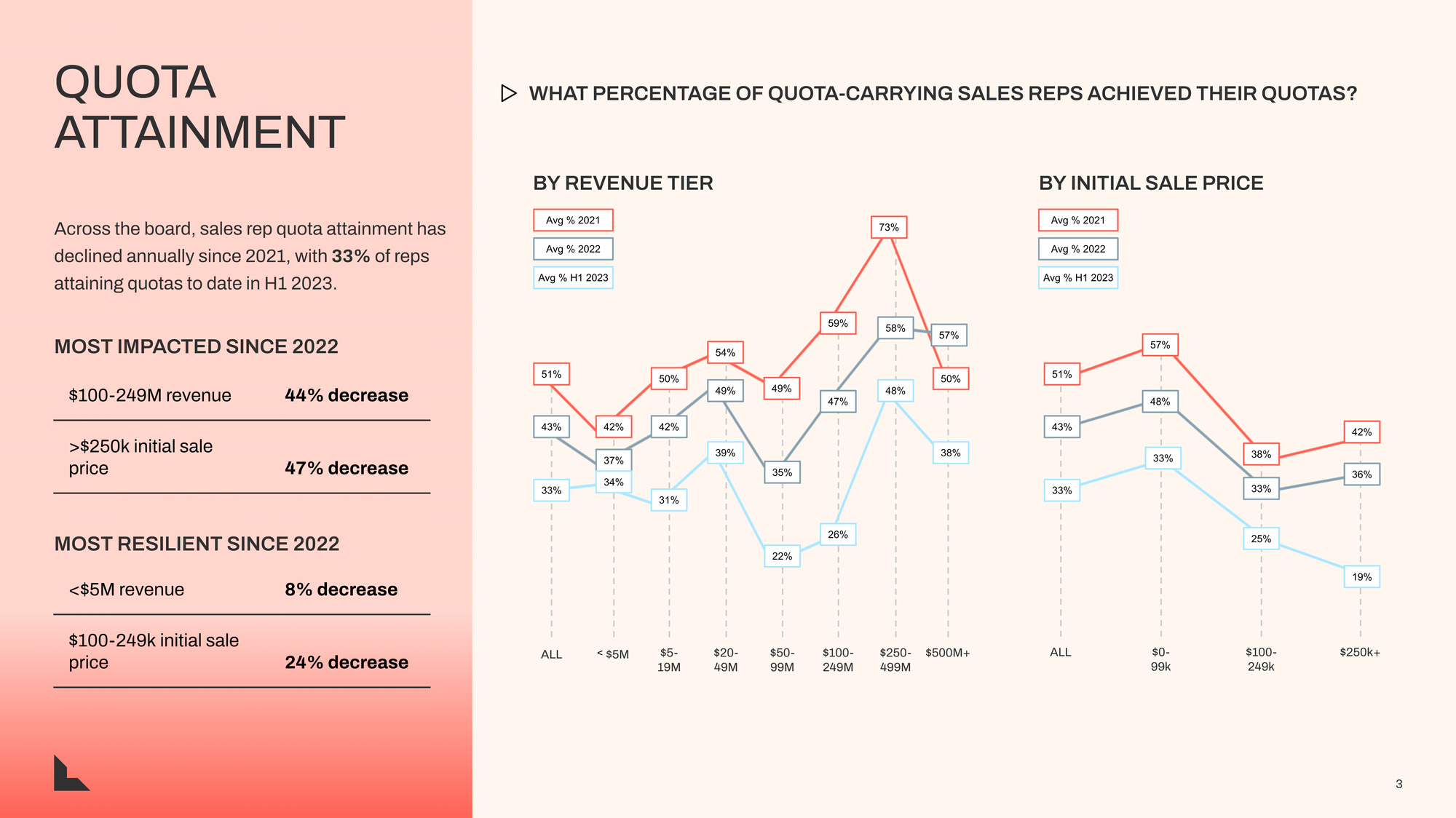

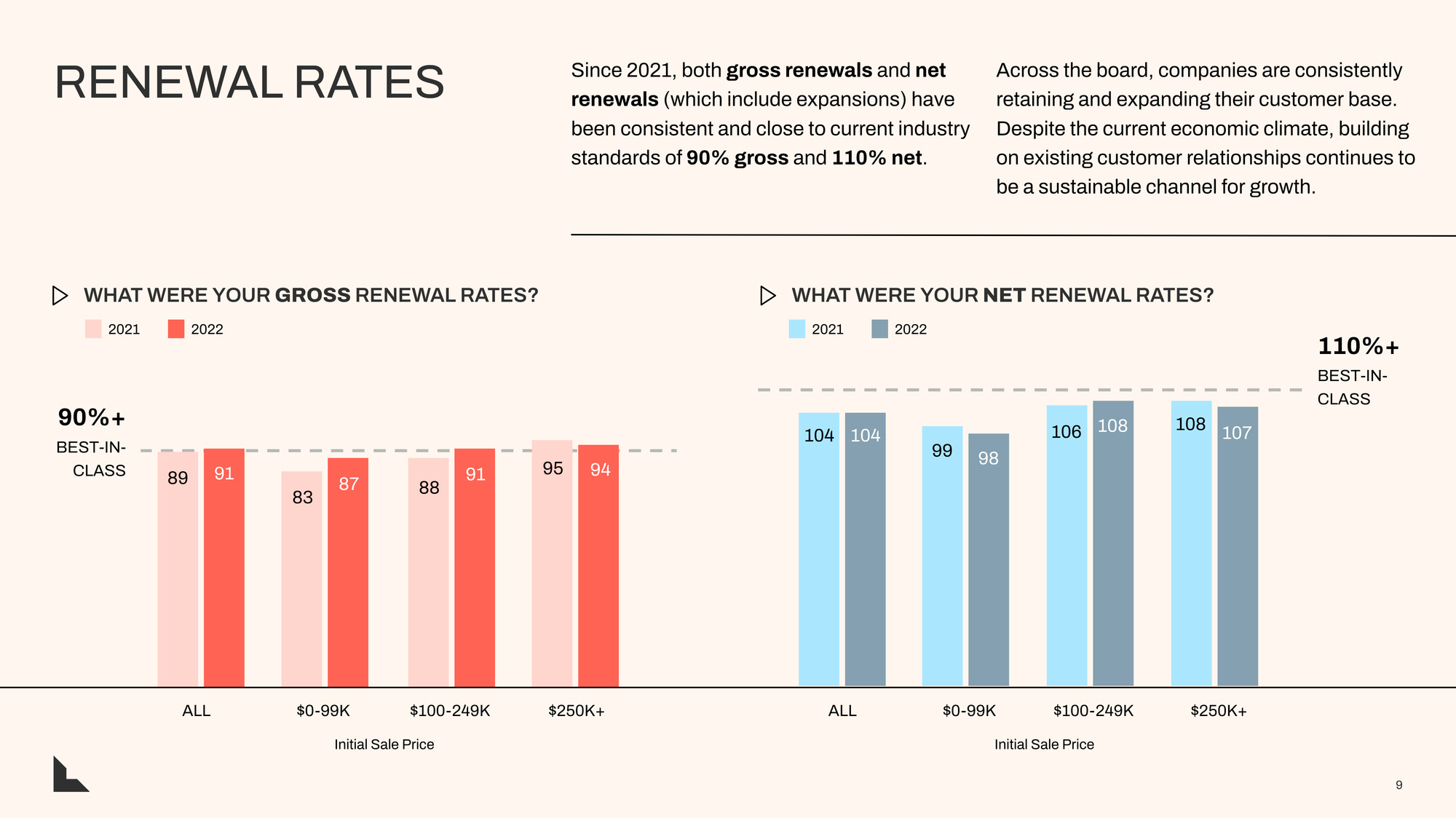

Tuesday, Sep. 12th: Lightspeed published a report on B2B sales. - Lightspeed

Wednesday, Sep. 13th: Haystack raised $75m for Haystack VII core seed fund and a $25m companion fund. - Semil Shah, The Peel, Turner Novak

“Since 2013, Haystack has made approximately 290 pre-seed or seed-stage investments, of which (after proactively marking down our portfolios in 2022), we have over 60 companies valued at $100m+, 16 companies valued at $1bn+, and 36 accretive exits to date. Over the past few years, our median initial check size has stabilised around $700k on a median entry post-money valuation of $15m.”

Semil Shah started Haystack in 2013 and invested in the seed rounds of DoorDash, Instacart, Hashicorp, and Envoy within the first 6m of starting Haystack.

He failed 3 times to get into venture before raising his own fund because he did not have the right background. Even when he started Haystack, his game-plan was to make a couple of investments before joining a venture firm.

He participated into Hashicorp’s $570k seed round at $3.75m post money valuation which was led by True Ventures and which was an extremely hard round to raise.

He started with a first $1m fund deployed in 1.5y on which he did not take management fees. He was working on the side as a venture partner to pay his bills. His second fund was a $3.2m fund invested in 1y. His third fund was a $8.2m fund (vs. a $20m target).

“The product of a VC fund is an investment decision process and those investment decisions are bundled into one blind pool product which is the fund vintage. You need to have the geometry of that right.”

On a $0-20m fund, ownership does not matter. On a $20-40m fund, you should target a 5-10% ownership. On a $40-100m fund, you should target 15-20% ownership. On a $100m+ fund, you should target a 20-25% ownership.

Thursday, Sep. 14th: Apple held its annual iPhone launch event announcing the iPhone 15. - Stratecherry

Apple is replacing its lightning port with USB-C in order to comply with UE regulations and to enable data transfer at high speed.

“Boring is fine when you are a product as successful as the iPhone with the built-in obsolescence inherent to a battery-powered portable device that you carry with you every moment of every day.”

“For years Apple talked about being a services company, but it was hard to take them seriously when their pricing strategy seemed focus on maximizing revenue instead of maximizing their user base. However, that strategy has meaningfully changed over the last few years, thanks to inflation.”

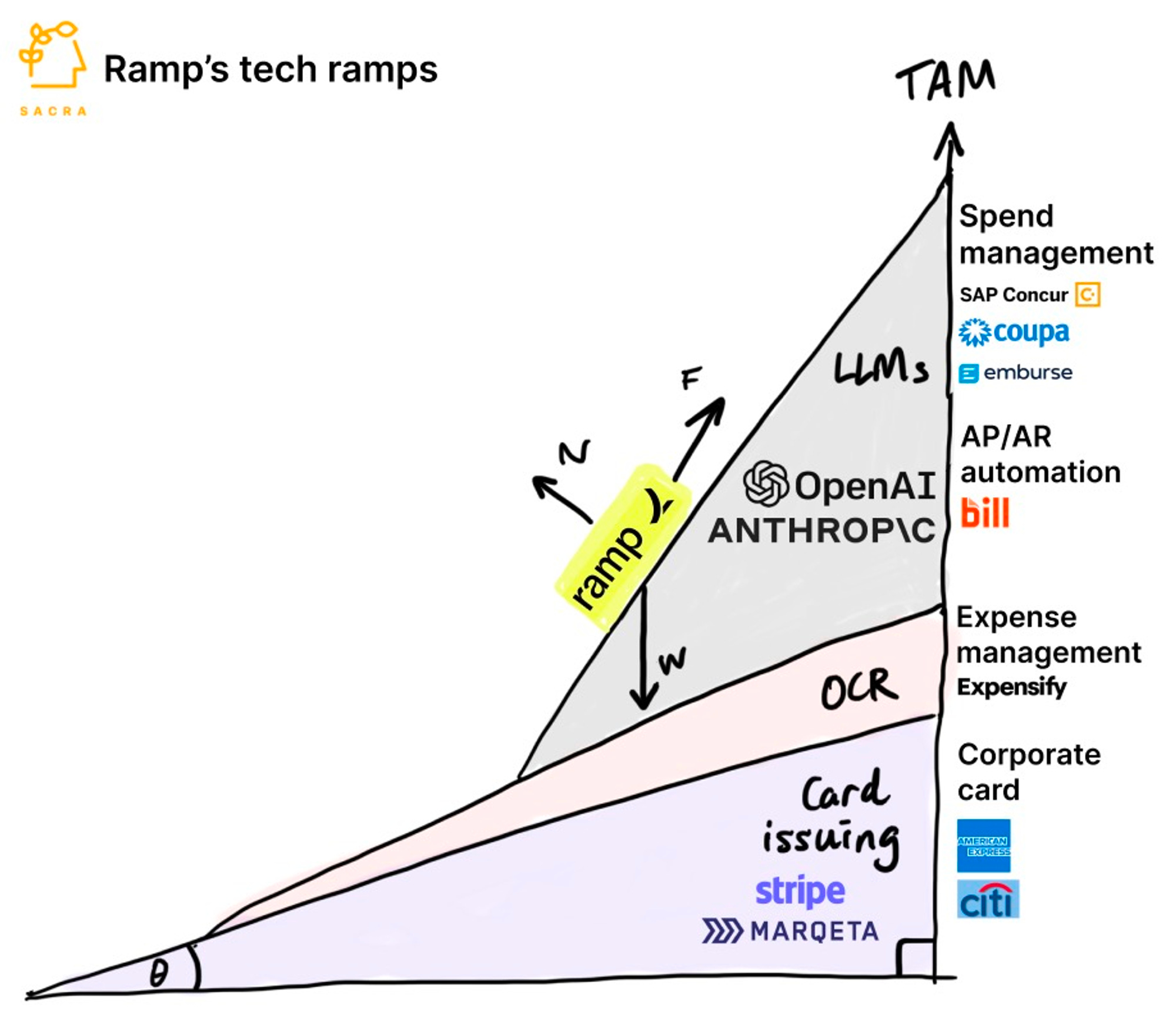

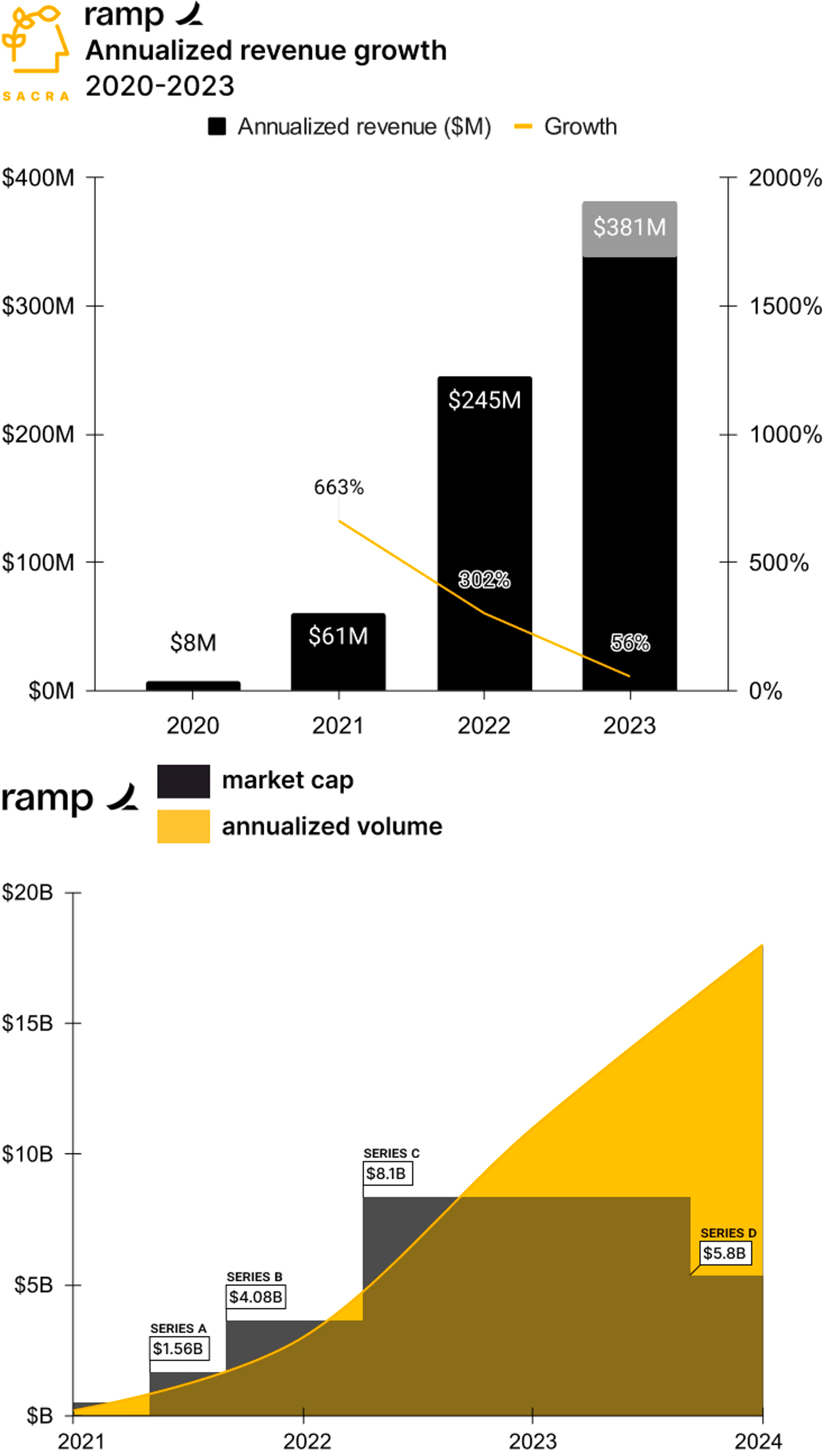

Friday, Sep. 15th: Sacra wrote about Ramp’s AI strategy. - Sacra

Ramp is building a B2B finance platform including corporate cards (competing with Amex), expense management (competing with SAP Concur and Expensify), AP/AR automation (competing with Bill.com) and spend management/procurement (competing with Coupa).

“By limiting their hiring and instead emphasizing the integration of AI into everyday workflows, Ramp itself has been highly human capital efficient, getting to $300m in annualized revenue with just c.500 FTEs.”

“Finance work moving from humans to autonomous AI agents portends a shift from seats in payroll in Rippling ($135m revenue in 2022) towards spend on tokens and SaaS in Ramp, blurring the boundaries to ownership over the full range of B2B spend. It’s still early for AI to replace high-cost services, but both dollars and margins will flow from services towards software and the finance team of the future will be strategic—not operational.”

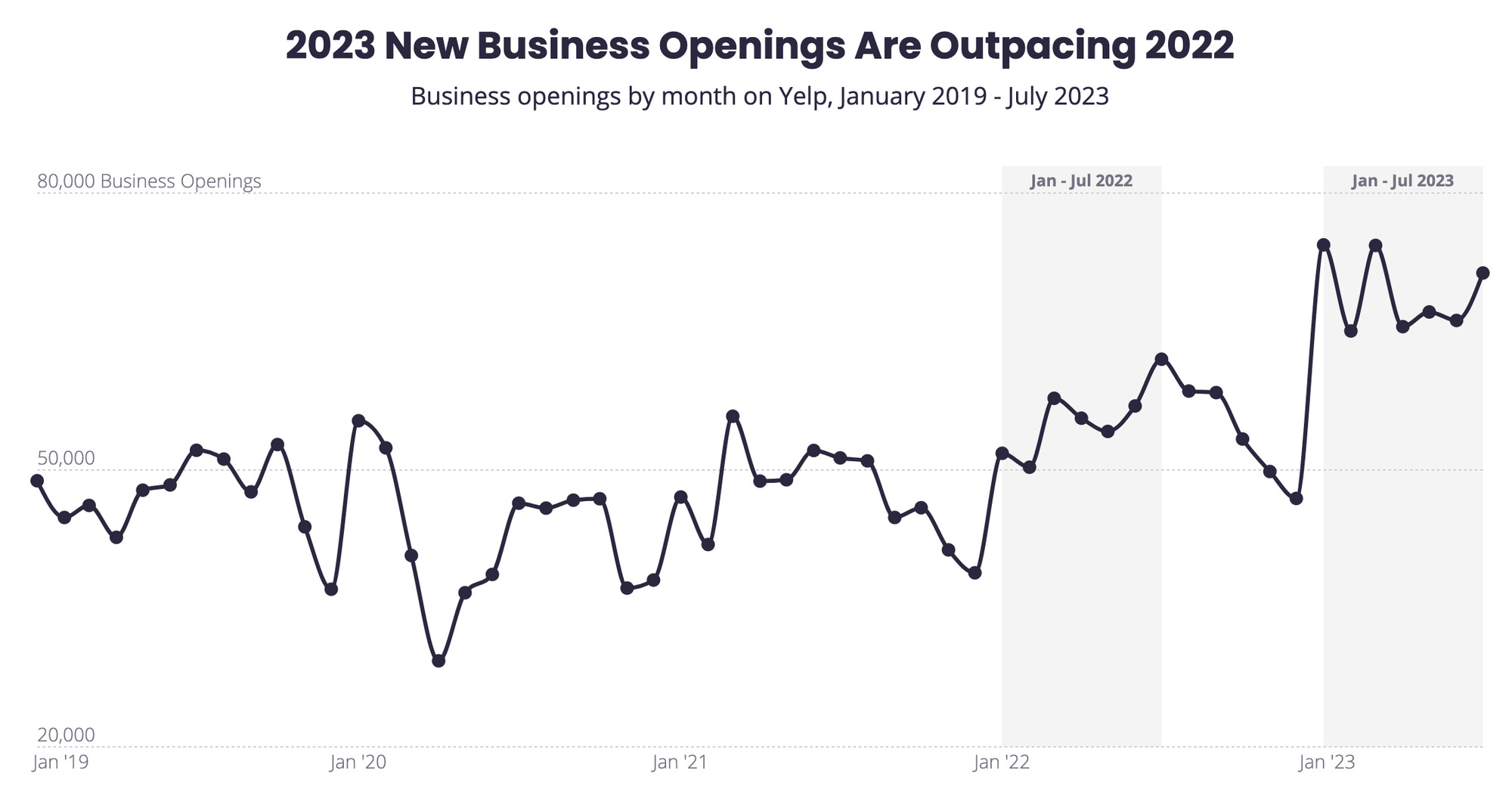

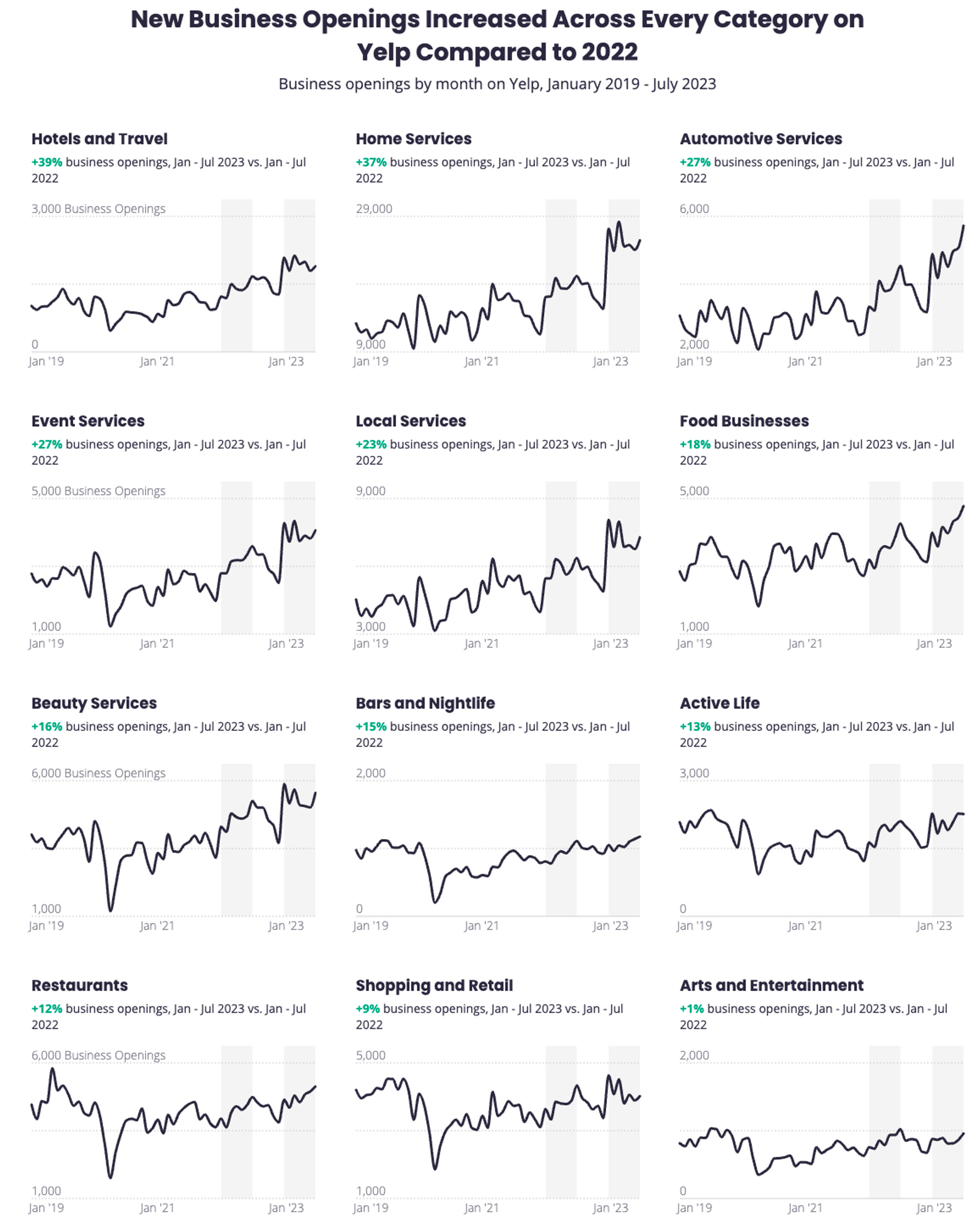

Saturday, Sep. 16th: Yelp published a report on small businesses openings in H1-2023. - Verticalized, Yelp

“National business openings on Yelp from January through July 2023 have surpassed openings from the same time period last year, a year which hit an all-time high for new businesses.”

“New business openings increased across every category on Yelp when comparing January through July 2023 to the same time period last year. Driving business opening growth nationally are hotels and travel (up 39%), home services (up 37%), auto (up 27%), event services (up 27%), and local services businesses (up 23%).”

Sunday, Sep. 17th: I listened to a podcast interview with Mark Leonard who created and who is leading Constellation Software. - Quartr

“I tend to wake up between 4 and 5 am. I have the same breakfast and read 2-3 newspapers.” (Financial Times, Wall Street Journal, The Globe)

“Our memories and knowledge has a half life. So the stuffs we learned 40y ago, little of it is being used by us today. We’re constantly replacing what we know by what is currently correct and we currently believe to be correct. You’ve got to be a lifetime learner. You’ve got to keep filling your mind with new ideas and knowledge. The old stuff becomes increasingly less relevant.”

“Creating a permanent capital vehicle for the vertical market software industry where you did not have to buy and sell the businesses. You can keep them forever. You can build relationships that lasted a lifetime. You can build businesses which intent is to be around as long as their clients were in existence. It’s a different perspective than the venture industry which is all about creating things you can sell to other people either as IPOs or as outright sales.”

“I realized that a couple of the vertical market software things that we’ve done were ideal except that they were small. They were not going to be big businesses that warranted significant capital and could be a big enough canvas on which to work [in venture]. So I came up with the idea of creating a holding for such businesses.”

Monday, Sep. 18th: Linear raised a $35m series B led by Accel at a $400m valuation (8.75% dilution). It's a project management software for developers (e.g., ticketing issues, roadmaps management, development cycles) going after Jira. The company has been profitable since 2021, having spent only $36k in online marketing and having hired only one salesperson. It also has only 50 FTEs. Linear will use the funding to accelerate its go-to-market and pursue product development (e.g., adding brainstorming, planning customer feedback, and post-launch analytics). - Forbes, Linear

“To me fundraising timing is about the company hitting an inflection point. Earlier this year, we saw our business hitting scale and we see the opportunity ahead.”

Tuesday, Sep. 19th: Helsing raised a €209m round from General Catalyst and Saab at a €1.5bn valuation. It builds defense software for European governments. It uses AI for data processing and analysis to create a representation of a battlefield and assist in decision-making. It's an alternative to Palantir's Gotham platform. - FT, General Catalyst

“There is an urgent need to create new defense companies, in partnership with the existing ecosystem, and with responsible innovation at their core – in the service of deterring aggression and promoting freer, more democratic societies everywhere.”

“In June 2023, the German government selected Helsing and its partner SAAB to provide the new electronic warfare capabilities for the upcoming update of the Eurofighter. In August 2023, Helsing and its consortium partners won the contract to provide the AI backbone for the Future Combat Air System (FCAS) programme.”

“Helsing was selected for their first program of record (a contract that has been approved and budgeted by the government) just two years and two months from their founding, while Anduril won their first program of record just three years from their founding?”

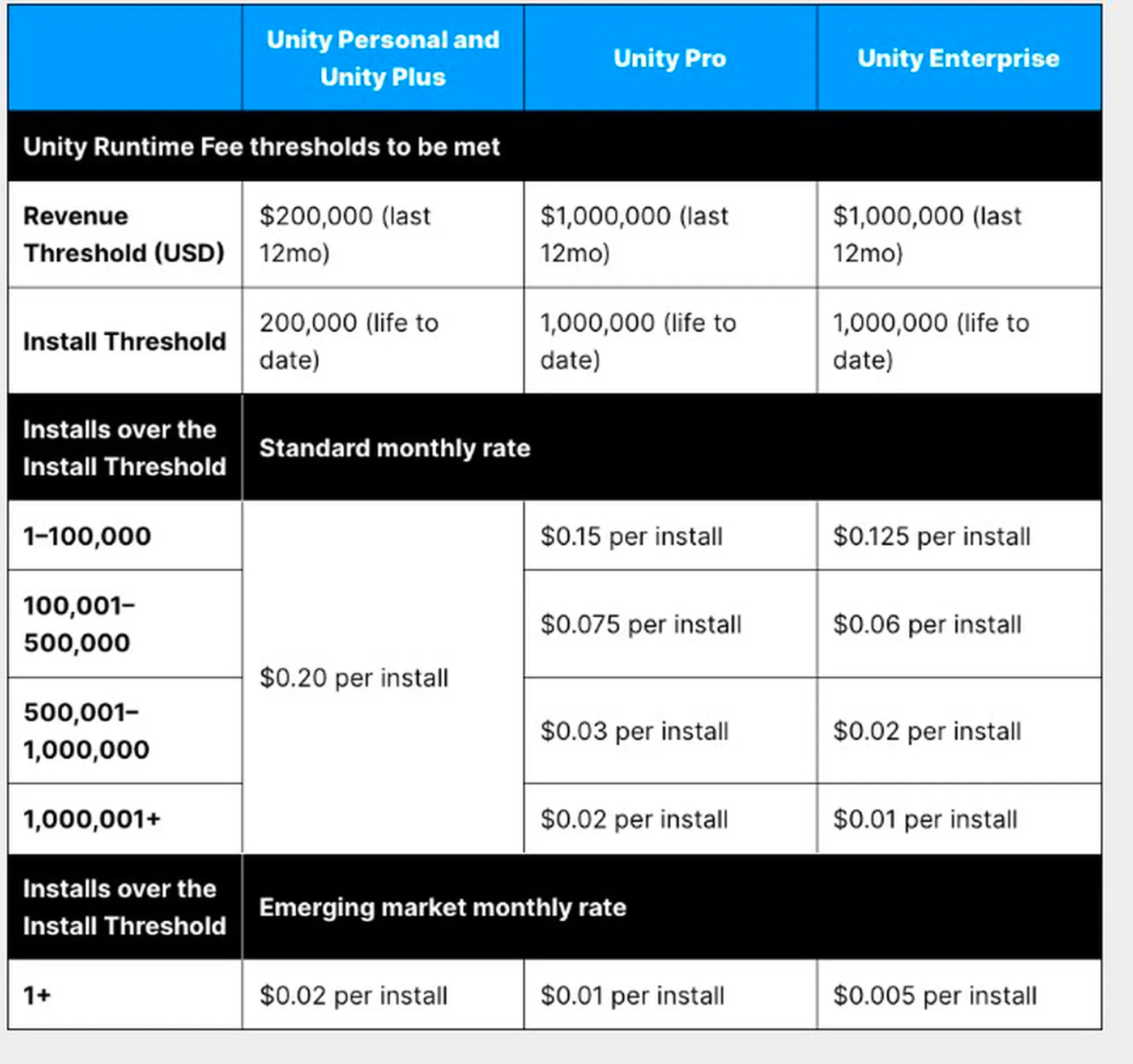

Wednesday, Sep. 20th: Unity changed its pricing model generating a strong backlash amongst its user base. Starting in 2024, game developers will now have to pay per download fee called Runtime Fee any time one of their games is downloaded after a certain downloads and revenue threshold. - The Verge, Unity, Game Developer, Games Industry

“Unity announced a pricing update which changes the pricing model from a simple pay per seat to a model whereby developers have to pay per install. This isn’t restricted to paid installs or plays; it applies to every plain install.”

“If you're starting a new game project, do not use Unity. If you started a project 4 months ago, it's worth switching to something else. Unity is quite simply not a company to be trusted. Across the last few years, as John Riccitiello has taken over the company, the engine has made a steady decline into bizarre business models surrounding an engine with unmaintained features and erratic stability.”

“A lot of those statements talked about trust, because trust is crucial for developers using a commercial game engine. Games can take years to build, and if a developer is going to commit to building a project in Unity, Unity needs to commit to supporting them over that span.”

“Unity lit money on fire for decades to buy a market advantage that overrules the basic economic incentives that supposedly ensure free markets work best for customers. It was successful in doing that because it's very hard for a sustainable business to compete against one that is fine losing billions of dollars.”

“We already know Unity management are big believers in AI, and if companies really can use the tech to cut headcount, they'll not only be paying fewer salaries but fewer Unity seat license fees. So if Unity expects its existing (unprofitable) model to be disrupted, it's naturally going to want to adopt a model better suited to the industry landscape of the future.”

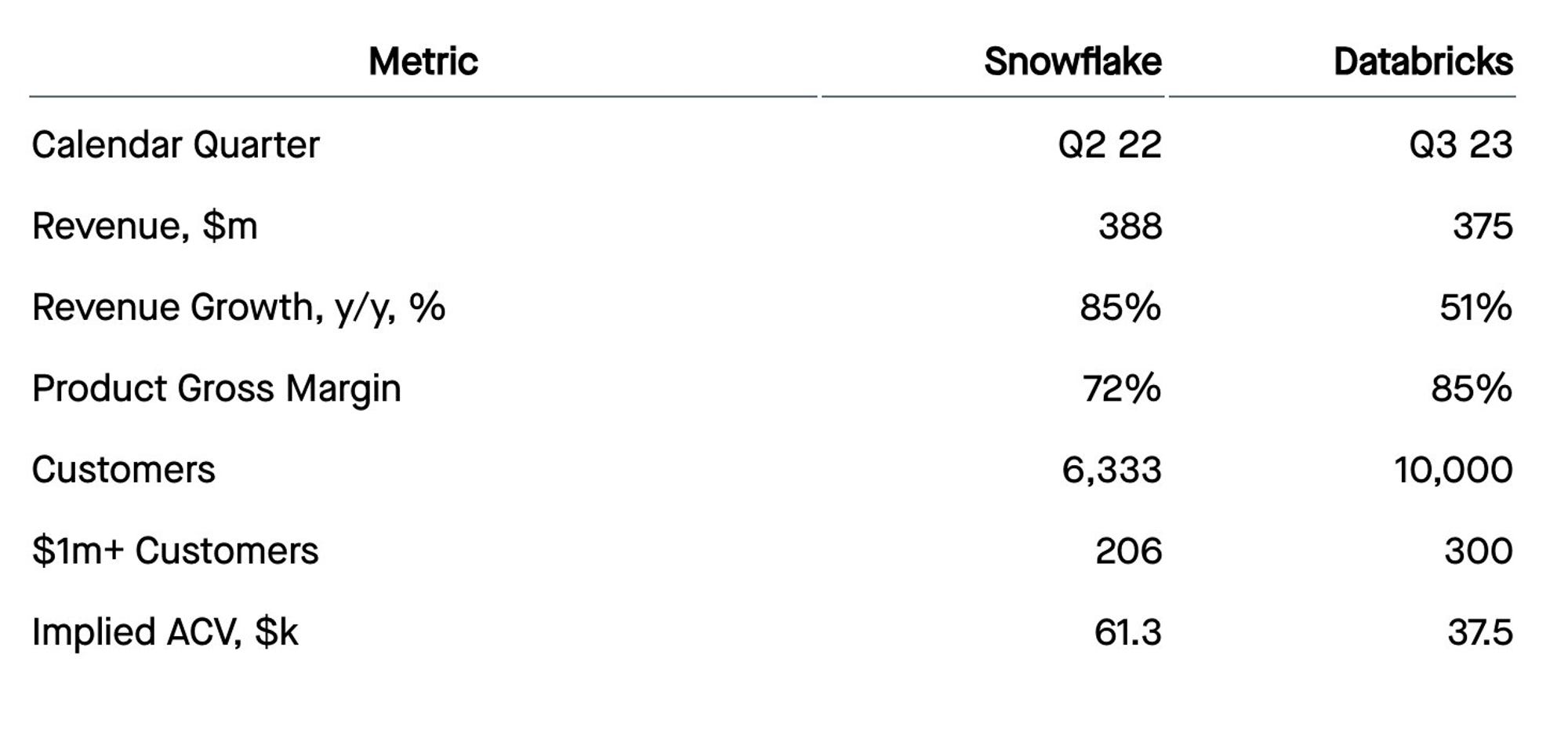

Thursday, Sep. 21st: Databricks raised a $500m series I at a $43bn valuation (vs. a previous $1.6bn round in Aug. 2021 at a $38bn valuation) from investors like T. Rowe, MS, Fidelity, Capital One or Nvidia. Databricks passed the $1.5bn ARR threshold in Jun. 23 with 10k customers including 300 customers making more than $1m per year. The company is planning to spend $1.5bn between 2022 and 2025 to grow at 50% YoY before reaching profitability in 2025. - Techcrunch, The Information, Forbes, Tom Tunguz

“Databricks’ product gross margins, which exclude any professional services work, top Snowflake’s by more than 10 points. Some customers run Databricks on their hardware (called on-premises or on-prem), whereas all Snowflake customers run on Snowflake’s cloud. Because Databricks doesn’t incur infrastructure costs when running on-prem, the business enjoys higher gross margins. If more Databricks customers move to the cloud, these figures may converge.”

Friday, Sep. 22nd: Lenny Rachitsky wrote a guide for B2B companies to find PMF. - Lenny’s Newsletter

“The median time from idea to feeling product-market fit was roughly 2 years.”

“From a working product to feeling PMF typically took 9-18 months”

"Most companies got an alpha product out the door in 1-3 months. Unless you think you’re the next Figma, get your V1 out quickly.”

To get to PMF, you should follow the following steps: (i) get one company to love your product, (ii) get one company to pay (a meaningful amount of money) for your product, (iii) get more than one company to love and pay for your product, (iv) start noticing a shift from push to pull, and organic growth, (v) keep growing consistently.

Saturday, Sep. 23rd: Epic Games laid off 16% of its workforce (870 FTEs). - Bloomberg, Techcrunch, Epic

“For a while now, we’ve been spending way more money than we earn. I had long been optimistic that we could power through this transition without layoffs, but in retrospect I see this was unrealistic.” - Tim Sweeney

Fornite has 400m users. Tencent owns a 40% stake in Epic.

“We're cutting costs without breaking development of our core lines of businesses so we can continue to focus on our ambitious plans. We aren't cutting any core businesses, and are continuing to invest in games with Fortnite first-party development, the Fortnite creator ecosystem and economy, Rocket League and Fall Guys; and services for developers including Unreal Engine for games and enterprise, Epic Games Store, Epic Games Publishing, Epic Online Services, Kids Web Services, MetaHuman, Twin Motion, Quixel Mega Scans, Capturing Reality, ArtStation, Sketchfab and Fab.”

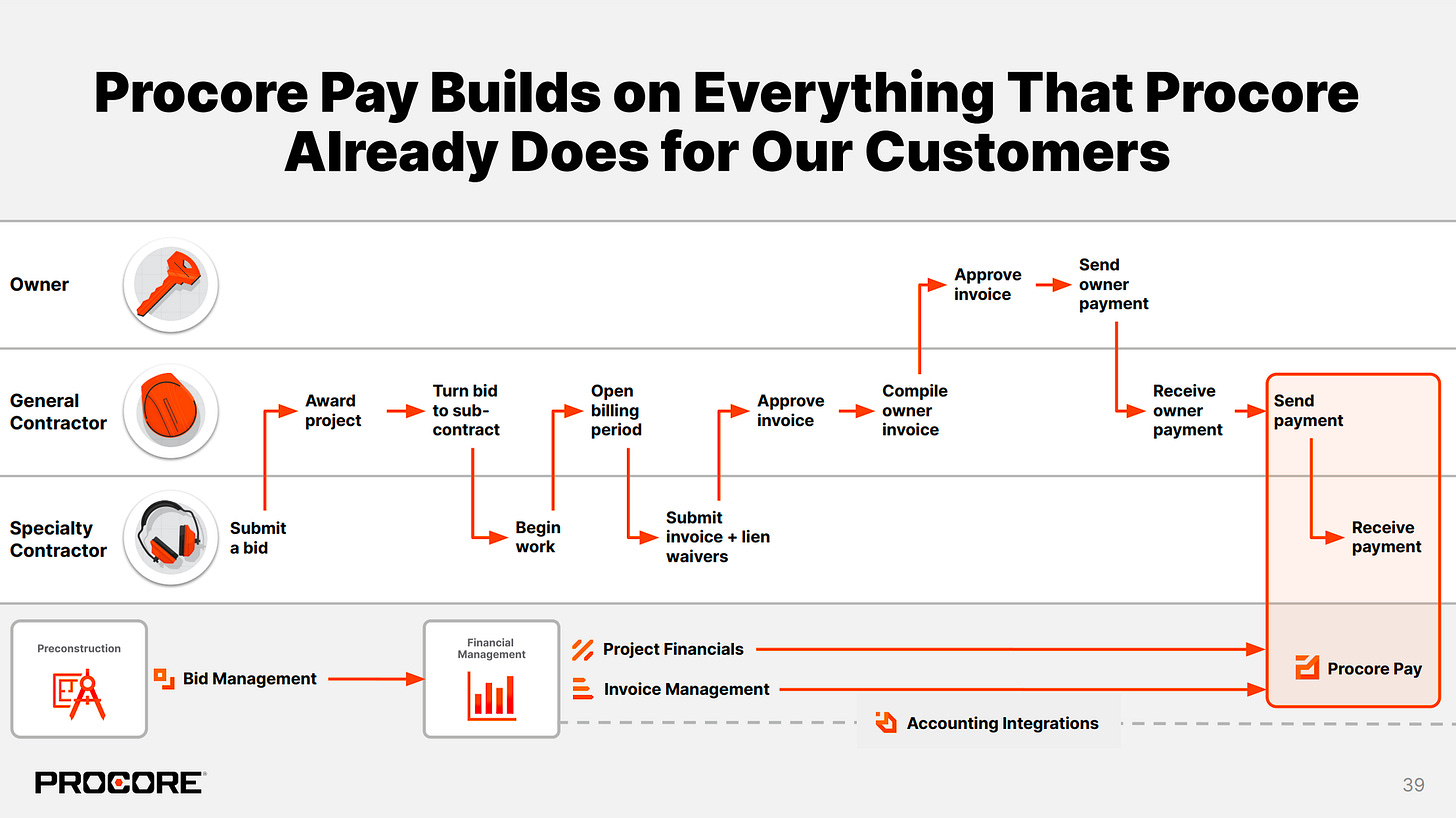

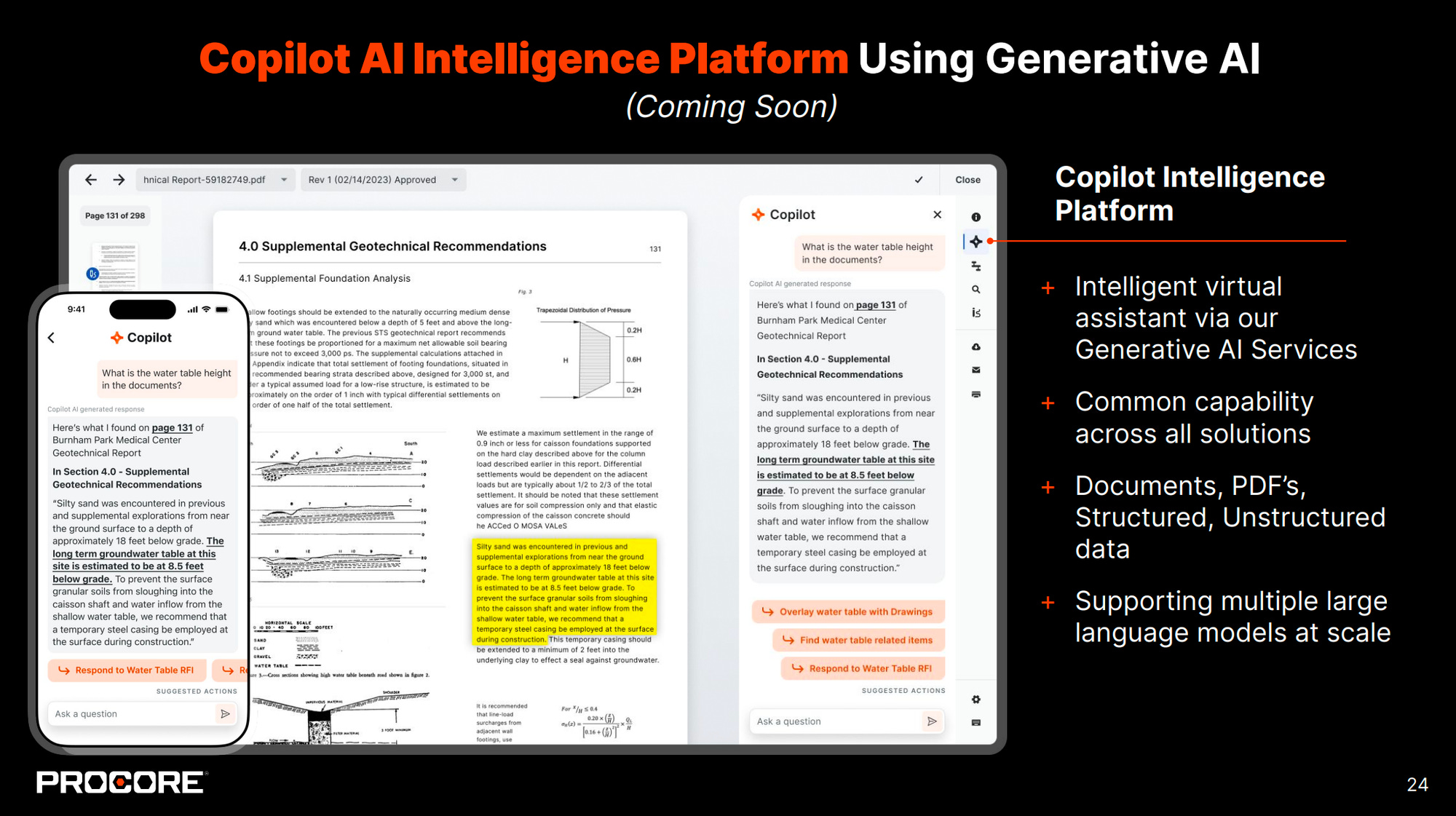

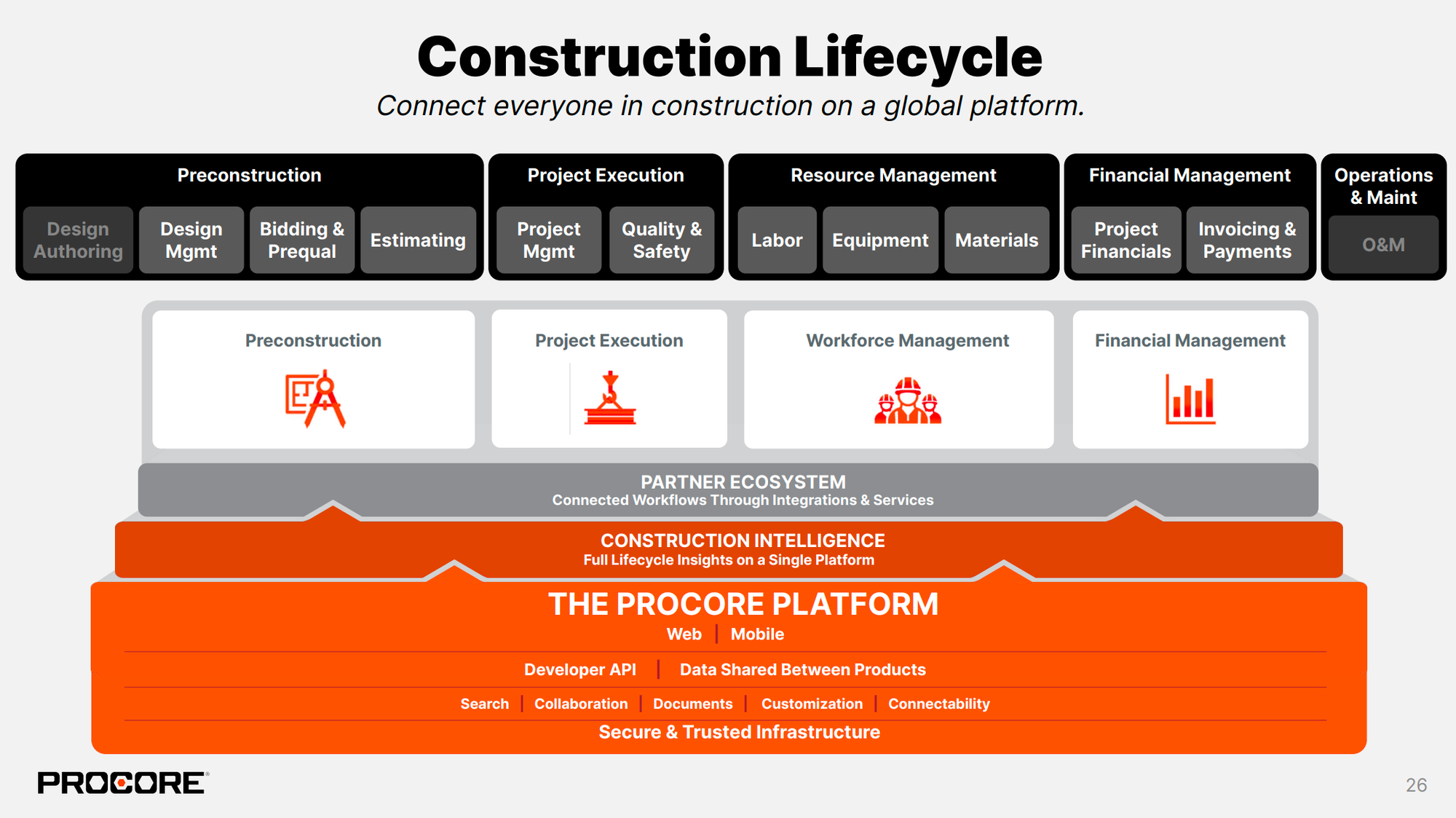

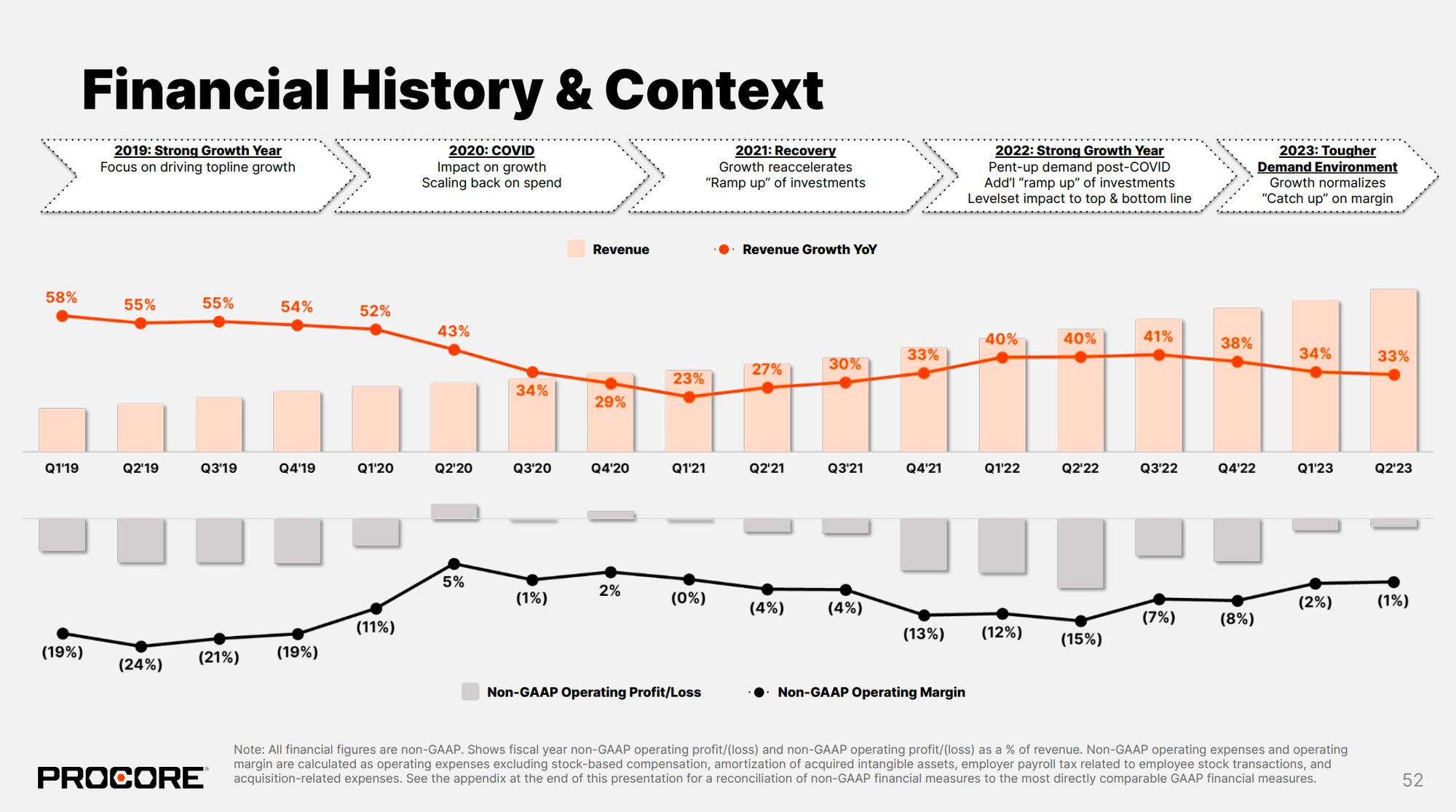

Sunday, Sep. 24th: I watched Procore’s investor day. The company shared more details on their expansion into financial services and on they plan to integrate generative AI to the platform. - Procore I, Procore II, Procore III

Procore launched its AI Copilot to automate time intensive and manual processes within the Procore’s platform. It will pro-actively surface important information to customers and it will help customers retrieve information on Procore. “You can have a conversation with Copilot, look for risks, look for updates, look for summaries, actually do advanced intelligence and reporting on the fly. And then actually, we can prompt you with things that you might need to do next based on what we've seen other users do in the system.”

“Part of building a generative AI and real-time intelligence in our product is being able to react in real time. A lot of companies will say they have real time, I would call it next-day action versus next best action. Next-day action is you're taking action based on intelligence, that's been processed the night before because you're having to batch things up and actually build it in the background and then start making recommendations to the customer. Over the past year, we've moved to an event-driven architecture platform. It allows every one of our products to basically push that data into that mesh and allows us to take action and build intelligence and actually start to inform generative AI across the board.”

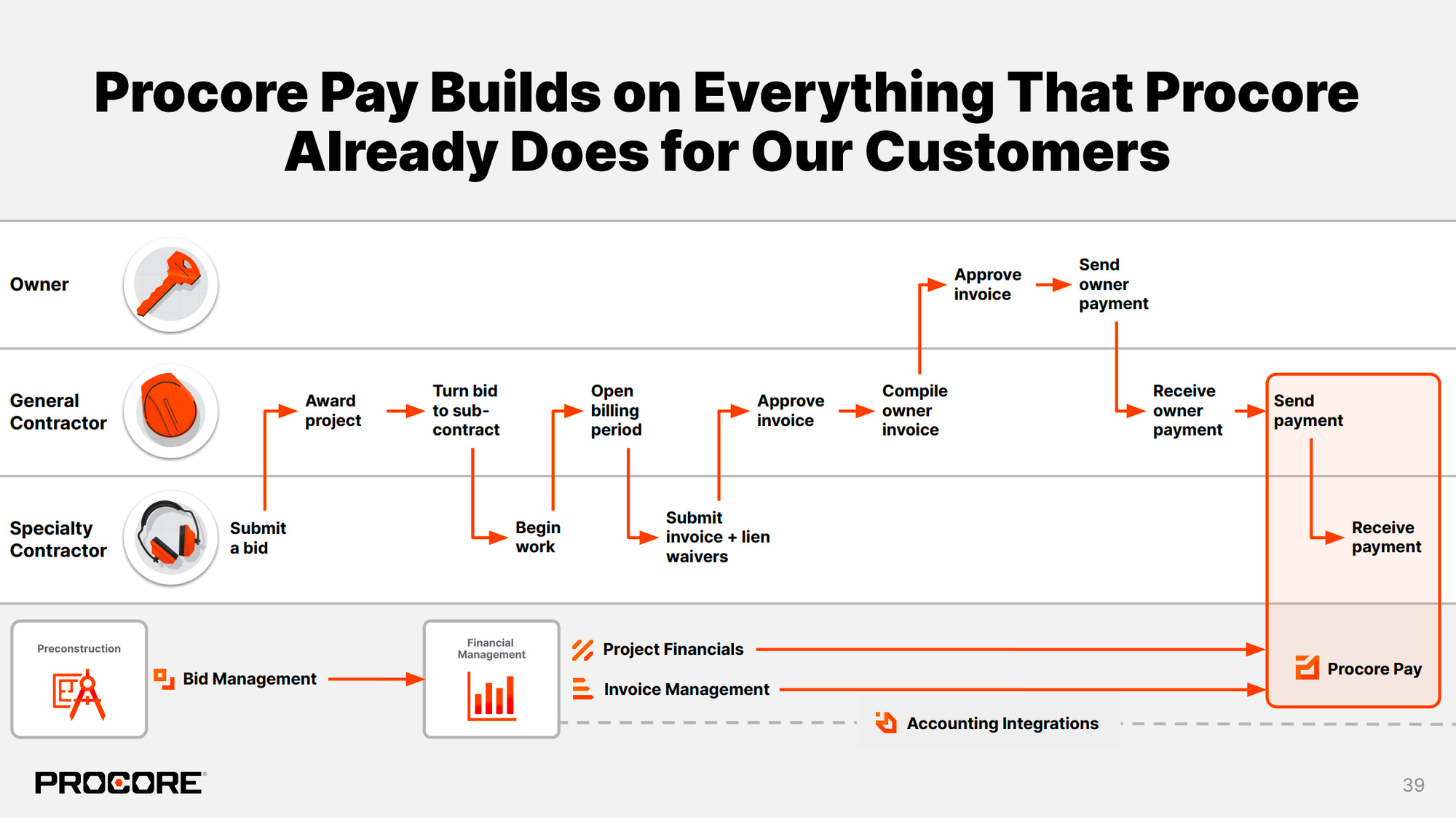

“I'll give you a good example of how the platform we're building makes us faster than a startup. When we built Procore Pay, it needed a workflow engine, which we had as a component in our platform. It needed enterprise-grade permissions, which were a component we had in our platform. We needed a way for subcontractors to log in and connect their bank account. That's good because we have a Procore construction network where they can log in. And so we just need to have a bank account connection in there. And so when we stand up a new solution for customers, like Procore Pay, we truly can be faster than a start-up at this point, thanks to the maturity of our platform. Our platform still has a long way to go, and we can be even faster, but it's really powerful to see those LEGO blocks of a platform start to stack up.”

“Tooey [Procore’s CEO] always tells me stories of climbing up poles at a job site trying to hang an Internet router in 2004 or 2005 before mobile caught hold.”

“Assuming Procore Pay receives anywhere from a 5 to 25 basis-point take rate on annual construction volumes (e.g. global volumes of $3.8tn), we estimate an incremental TAM opportunity of $2-$10bn in Payments alone, 2-10x Procore’s current revenue base.”

“Procore introduced new products such as Procore Copilot (in development, GA likely 12+ months out), while also expounding on its product-market fit and monetization roadmap for FinTech initiatives such as Procore Pay, Risk Advisors (insurance) and Materials Financing (working capital management).”

“On Procore Risk Advisors, we came away encouraged by the early momentum, namely that Procore has already had 150+ “first meetings” with customers, built relationships with 30+ carriers, and early customers are observing meaningful reductions to insurance premiums due to Procore’s extensive construction risk data.”

In H1-23, 40% of Procore’s new logos came from companies with collaborators who were using Procore for free before converting into paying customers.

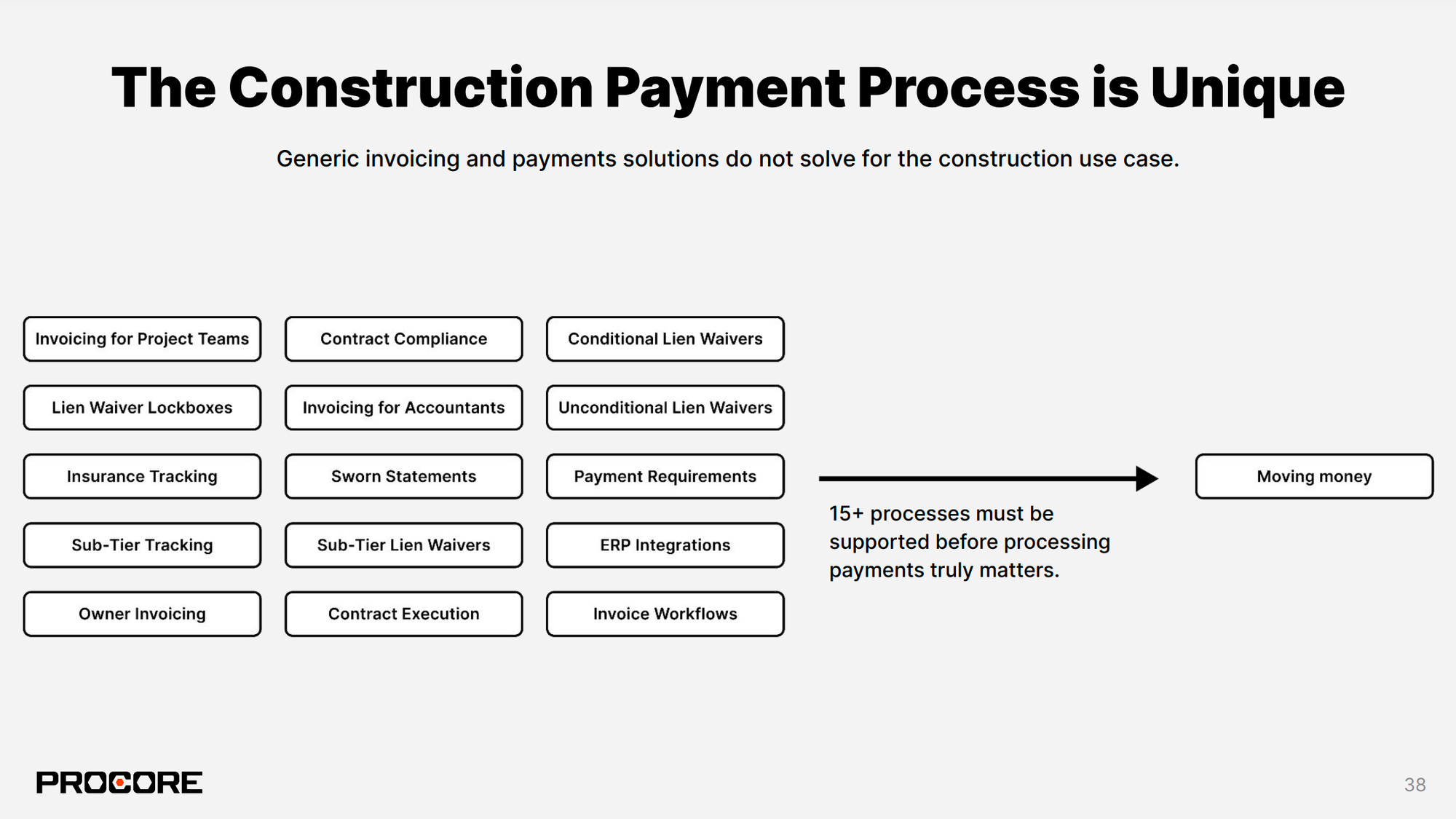

“Every month, the subcontractor has to effectively compile what we call a payment application for the GC. The sub is going to pull together 10-15 different documents specific to the requirements of the project, the GC and the owner. On the other side, the GC will have to review these documents before approving the payment. The owner will do the same with the GC payment application which aggregates all the payment applications from subs involved in the project.” The main pain point around payments in the construction industry is more documentation management than replacing checks with electronic payments.

“The invoicing process in construction is very unique to construction with things like schedule of values, retainage, lean waivers or certificates of insurance.”

Processing payments is the last mile of a broader getting paid process for subs which starts earlier with bid process, project execution, invoice management and accounting integrations. Processing payments as a standalone product does not work. You need to handle all the business workflows surrounding payments which Procore does with its platform.

Procore made Procore Pay generally available. It previously ran a pilot during one year with two dozen GCs of all size. Procore will start to sell it to GCs which are already paying customers of Procore’s invoice management module in the US. Procore estimates that it will take between 6 and 24 months to fully ramp-up a customer on Procore Pay. Procore will sell to the CFO who is a new persona to address for Procore’s go to market team.

On Procore Risk Advisors. Procore acts as an insurance broker leveraging its unique relationship with customers and its unique dataset to improve insurance delivery and underwriting in the construction industry. Procore secured capacity from insurance partners. It compared performance data between Procore customers and non Procore customers to prove that Procore customers are performing better and are less risky than their peers making them attractive for insurance partners.

Monday, Sep. 25th: Airtable laid off 27% of its workforce (c. 240 FTEs). In Dec. 2022, Airtable had already laid off c. 250 FTEs. The company is adapting drastically to the new paradigm, no longer rewarding growth at all costs. To be ready to go public, Airtable is cutting costs and refocusing on expanding ACV with large customers. Airtable had previously raised in Dec. 2021 at an $11.7bn valuation and is on track to generate $150m in ARR in 2023 (78x EV/ARR multiple). - Forbes, Anand Sanwal

Tuesday, Sep. 26th: Flexpoint raised a $2.4m seed round led by Garuda Ventures. It’s a verticalized fintech offering a payments automation platform for Managed Service Providers (outsourcing services in fields like accounting, IT, marketing, etc.). MSPs will onboard their customers on the platform. Customers will be able to access a branded payment portal to track all their invoices and make their payments (via multiple payment options, including installments and deferred payments). MSPs will have a unified platform with all their customers, with automations to accelerate payment collection and to remove manual accounting reconciliation. They will also be able to access financing to grow their own business. - Business Wire

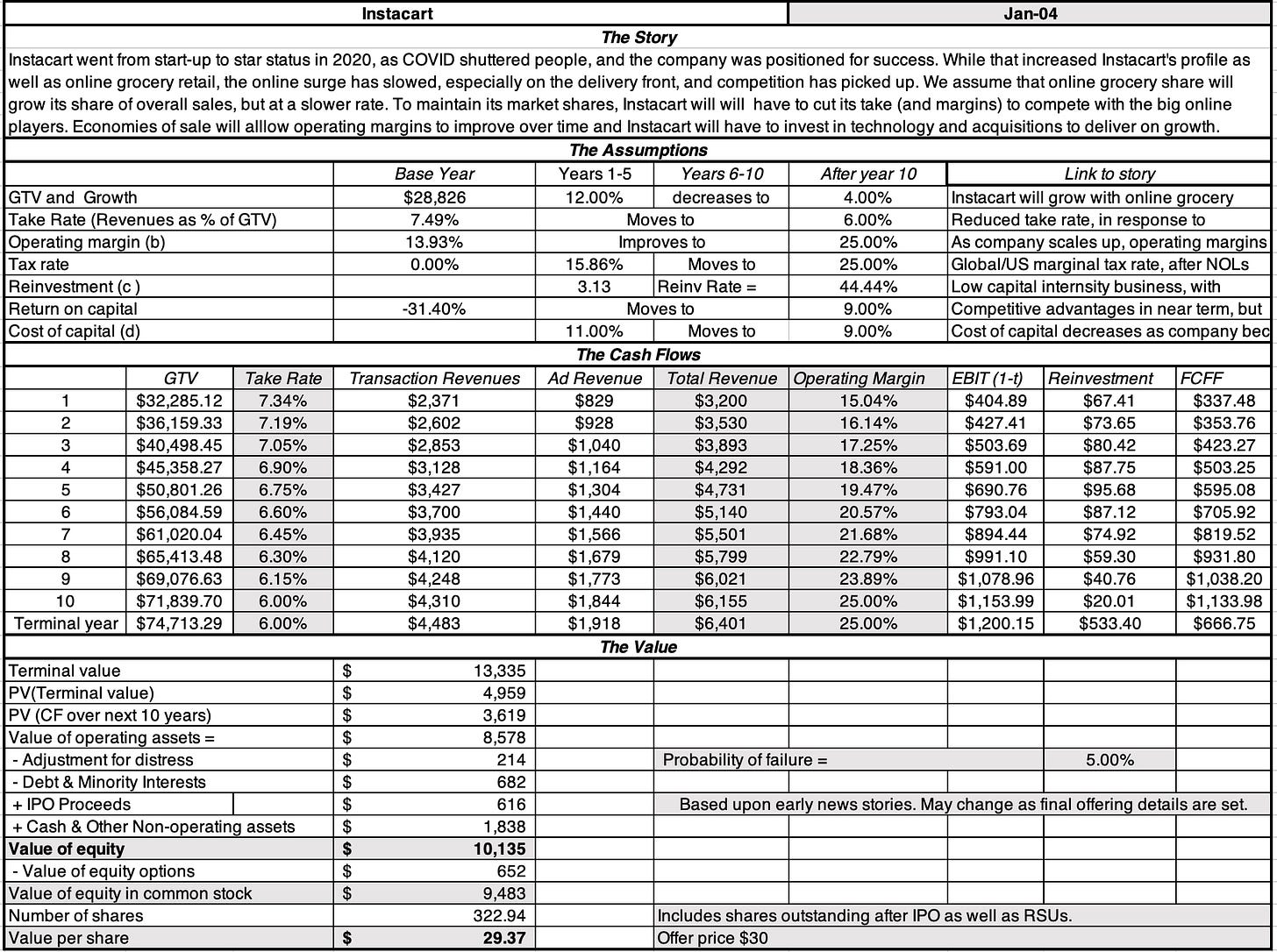

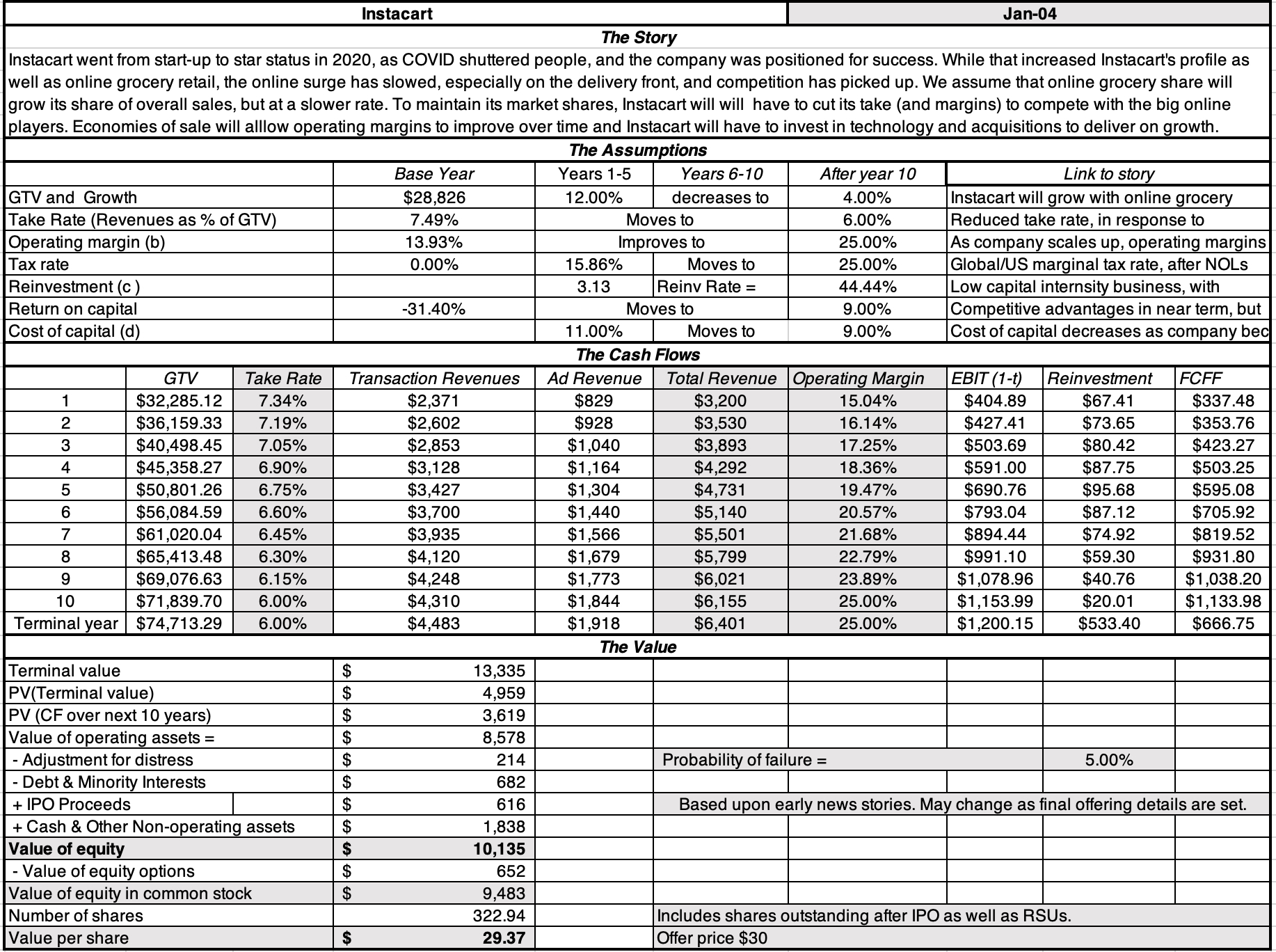

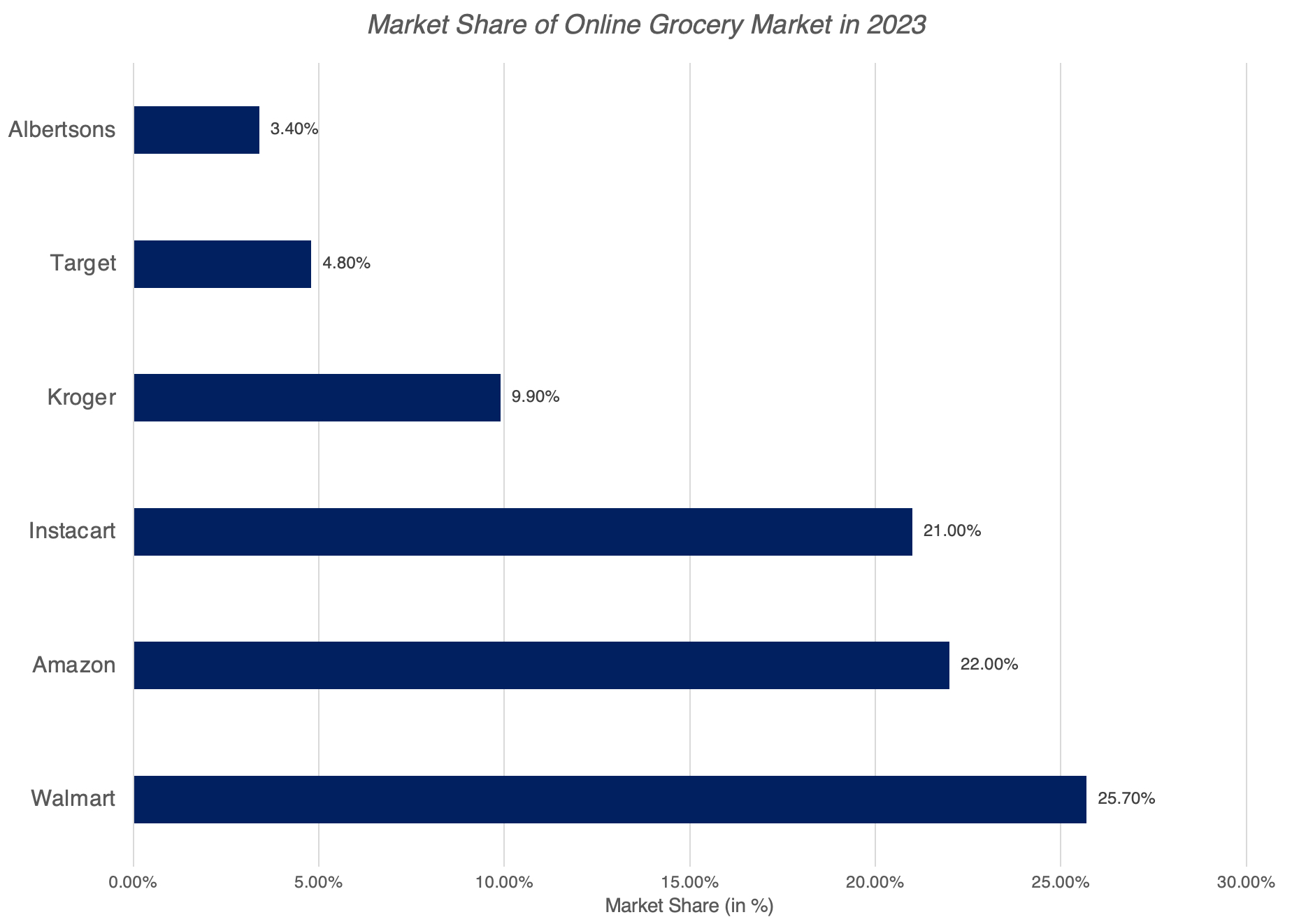

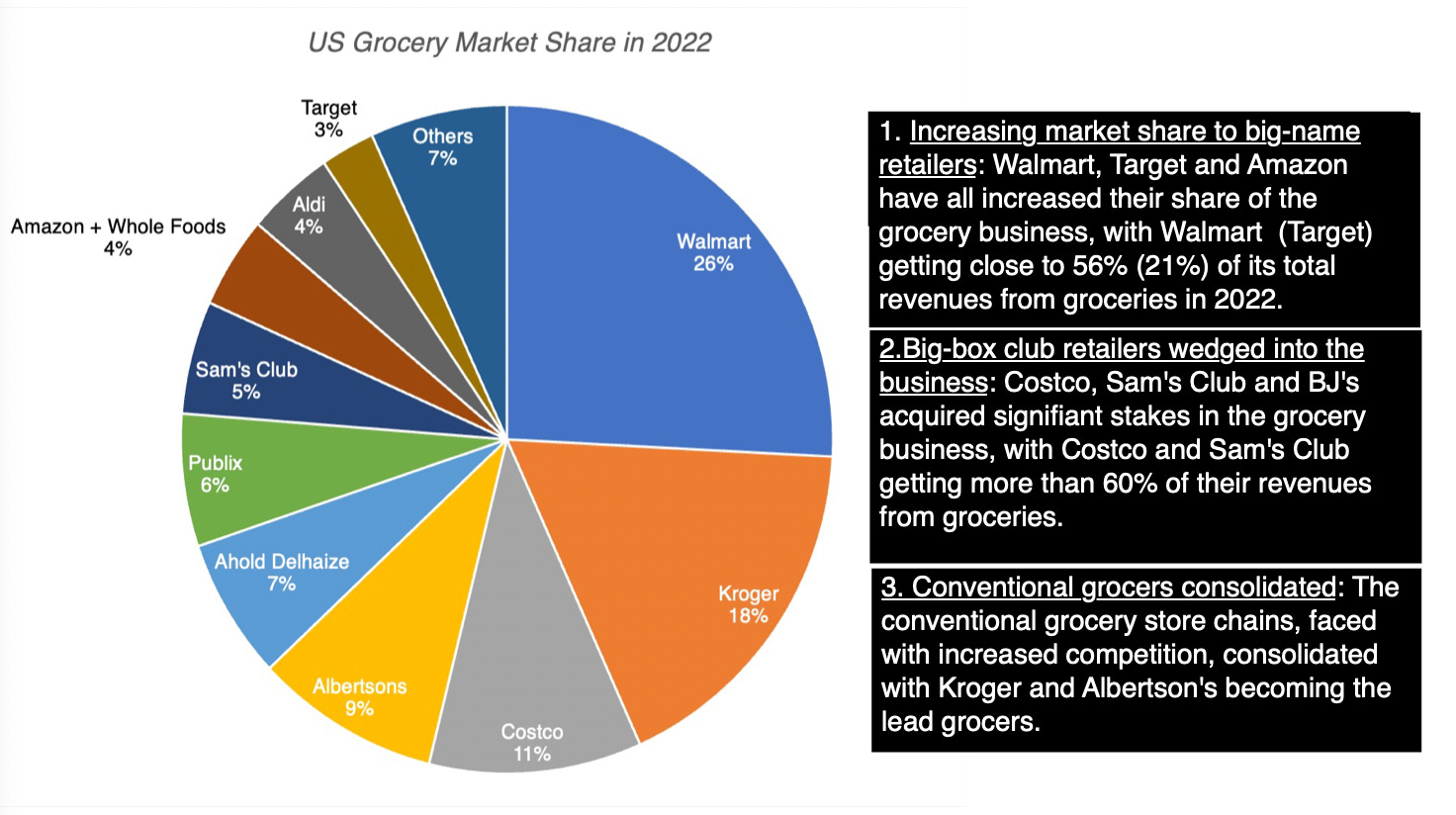

Wednesday, Sep. 27th: Instacart went public raising $660m at a $9.9bn market capitalisation. I previously wrote a deep-dive on Instacart ahead of its IPO that you can find here. Several interesting articles or comments were published when the company went public. - Forbes, Aswath Damodaran 1, Aswath Damodaran 2, Bessemer, Apoorva Mehta, Ravi Gupta, Jeff Jordan

“In 2015, we were losing $15 on every order. We had less than a year of cash. We went all in on fixing our unit economics and set seemingly impossible goals for the team. Over the next year we broke down every aspect of our business. And along the way we went from losing $15 an order to making $3 an order.” - Ravi Gupta

“The company’s early performance was impressive, and even more impressive was that almost all of the consumer-side growth was organic. Their GMV had almost tripled over the preceding 3 months and the early performance of their new markets exceeded that of their early markets.” - Ravi Gupta

“a16z has long had an investment theory that we should invest behind strengths of a business model and opportunity, not lack of weakness. Instacart is a case study of this. Focusing on the former was key to our investment decision.” - Jeff Jordan

“More than a decade ago, I was sitting in my apartment in San Francisco bemoaning the fact that the only thing I had in my refrigerator was hot sauce. Don’t get me wrong, I love hot sauce, but you can’t exactly make it a meal. My empty refrigerator was an ongoing problem - and a source of inspiration. It was 2012 and I could shop for everything online except groceries. That was a lightbulb moment for me, and I got started coding the first version of the Instacart App.” - Apoorva Mehta

“Many grocery stores they partner with are supportive of this model (although they have a complex range of different agreements) - Trader Joes is the only exception. This partner support could obviously wane over time if these stores felt threatened or commoditized.” - Bessemer’s internal email in 2014

“People are so jazzed about the product that 93% of users say they’ve been telling their friends about the product and 62% of new users in the last few weeks came organically through WoM. A very Uber like acquisition dynamcis.” - Bessemer’s internal email in 2014

“A lot of people have said that perhaps I was pushed out of the company. The reality is, if I wanted to be the CEO of Instacart, I would be the CEO of Instacart.” said Apoorva Mehta who cofounded Instacart as CEO before stepping down in July 2021.

“As it’s told, Mehta started the company 11 years ago after he opened his fridge and found nothing but a bottle of Sriracha. Co-founders Max Mullen and Brandon Leonardo joined 8 months later. After building the app, Mehta missed the application deadline for elite startup incubator Y Combinator by two months. Desperately emailing YC partners, he eventually got a response from Garry Tan, who told him he could try and apply, but it would be nearly impossible to get admitted. Mehta turned in his application and afterwards sent Tan a case of beer using Instacart. Shortly after, he was admitted to YC’s 2012 spring batch.”

“We believe the Trojan horse to build this business starts with the basic needs – food & water (aka grocery stores). We believe Instacart has the key tenets of successful big-idea companies: 1) Huge market; 2) fabulous / missionary founder; 3) great products / service… augmented with the key ‘right product, right place, right time’ mojo.” said Mary Meeker when she led Instacart’s series C at Kleiner Perkins.

“Mehta, who was born in India and moved to Libya with his parents as a baby, immigrated to Canada when he was 14. He did a four-month stint at mobile device maker BlackBerry while studying at the University of Waterloo, then landed at Amazon as a supply-chain engineer after graduating in 2008. It was at the e-commerce giant that Mehta honed the operations skills that would be foundational to getting Instacart off the ground.”

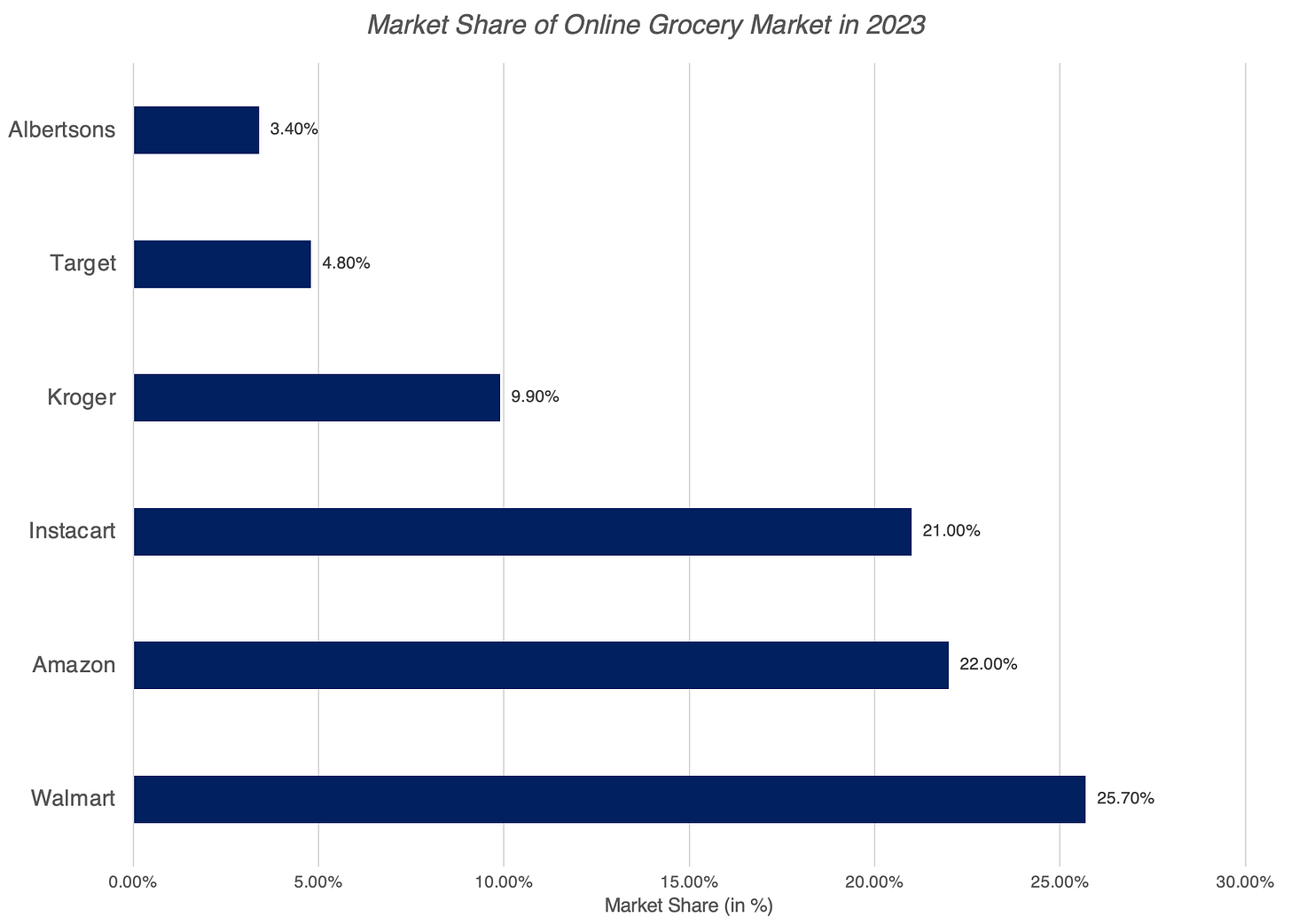

“Customers get the time-savings and convenience from having grocery shopping (and delivery, if chosen) done for them, but they pay in the form on both delivery fees and a service charge of 5-10% of the bill, depending on the store picked and the number of items in the basket.”

“For grocery stores, Instacart is a mixed blessing. It does expand the customer base by bringing in those who could not or would not have shopped physically at the store, but stores often have to pay Instacart fulfillment fees, which they sometime pass through as higher prices on products. In addition, grocery stores lose direct relationships with customers as well as data on their shopping habits, which may be useful in making strategic and tactical decision on product mix and pricing.”

“If you are an intermediary in a business with slim operating margins, as Instacart is, the low operating profitability of the grocery business will limit how much you can claim as a price for intermediation, in service fees.”

“The fact that the grocery business is dominated by a few big names will also play a role in the Instacart valuation story, by affecting the bargaining power that Instacart has, in negotiating for its share of the grocery pie.”

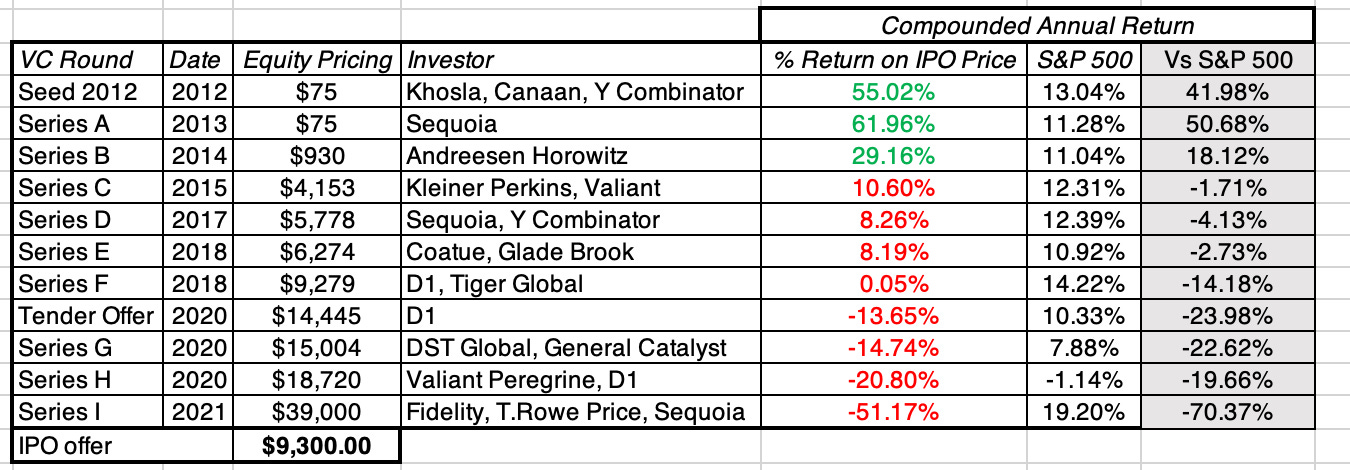

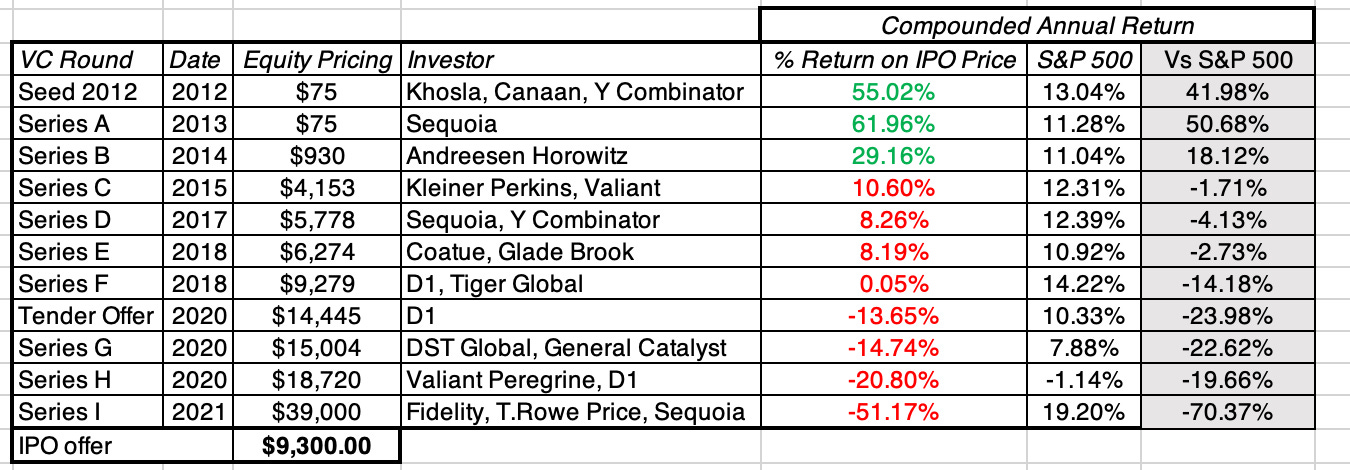

“The earliest providers of capital to the company will walk away with substantial profits, even if the company's market cap ends up at $9 - $9.5 billion, as indicated by the offering price. The seed capital providers (Khosla, Canaan and Y Combinator) will have earned at 55% compounded annual return on their investment, at the IPO offering price, well in excess of the S&P 500 annual return of 13.04% over the same period. Every subsequent round earns a lower annual return, and all investments in Instacart made after 2015 have underperformed the S&P 500 significantly, and the NASDAQ by even more.”

Thursday, Sep. 28th: Dawn raised its fifth fund. It’s a $620m fund to invest $10-40m tickets into series A/B in European B2B SaaS. 50% of the fund was raised from existing LPs. Dawn has already invested into 3 companies with this new fund including Fonoa (tax compliance platform), CoverGenius (embedded insurance) and FlowX (financial institution legacy systems updatder). Dawn has previously backed companies like Mimecast iZettle, Tink, LeanIX, Collibra, Dataiku or Quantexa. - Tech.eu

Friday, Sep. 29th: Spruce Point wrote a short sell report on Samsara. - Spruce

“Founded in 2015, the Company embraced the Internet of Things (IoT) hype cycle and originally focused on developing wireless sensors targeting the largest industrial processes and customers. Yet, like many IoT companies, after several product “pivots” Samsara has maintained its grand vision while finding market acceptance in only a small handful of niche applications.”

“These narrow, fleet-focused applications [in the trucking industry] account for nearly all of Samsara’s revenue and, importantly, are sold as a bundled solution including both software and commodity hardware. Originally priced separately, Samsara switched to a bundled subscription offering to boost annual recurring revenue (ARR) scale and growth prior to its 2021 IPO.”

“While Samsara management speaks little about its hardware products and operations (sometimes even acting as if they don’t exist), we believe the Company cannot escape their negative business model impacts.”

“We highlight that Samsara eliminated its past disclosure in its SEC filings that its LTV:CAC ratio is above 8x. Also, using ratios above and below that level as an input, our attempt to backward solve for implied ARR churn suggests an estimated deterioration from 4% to 8% per quarter over the past four years, a level likely higher than investors expect. We also see numerous drivers of increasing churn rates ahead, including commoditization, low switching costs, increasing competition, SMB- heavy customer base, macroeconomic pressures, and Samsara’s historical focus on customer acquisition over retention”

Saturday, Sep. 30th: Zach Weinberg shared an interesting list of great founders characteristics. - Zach Weinberg

“Can speak to the market/competition/strategy in specifics + they know tiny product details without having to ask an employee (aka they are not satisfied with high level facts).”

“They immediately jump at any opportunity to meet someone who could be a good future employee, they will chase down an intro.”

“Can give very specific examples and lots of them (either product or customer or sales process).”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Beaucoup d'éclairages passionnants dans cette édition. Merci.