🗞 Venture Chronicles - September 2022

Overlooked #125

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of September.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for September!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Thursday, Sep. 1st: Snap announced a massive restructuring. It aims to reduce costs by $500m per year. It laid-off 20% of its employees. It will stop investing into projects like Originals, Minis, Games, Pixy will also shut down standalone apps Zenly and Voicely. Snap is refocusing the business around 3 key areas: community growth, revenue growth and AR. It wants to reach 450m DAUs and $6bn in revenues (inc. $350m from paid subs) in 2023. - Snap, Techcrunch 1, Techcrunch 2, The Verge

Friday, Sep. 2nd: I watched Block’s Investor Day presentation on the Afterpay’s ecosystem. - Block

As a reminder, Block acquired Afterpay in 2021 which is one of the 3 BNPL giants with Affirm and Klarna. On paper, Afterpay (20mm consumers, 140k sellers, €20bn GMV, €600m in gross profit, global presence in Australia, the US, UK, Spain and France) is the perfect brick to connect merchants powered by Square and consumers powered by Cash App which are the two main Block’s ecosystems.

Block will integrate Afterpay’s capabilities both in Cash App (esp. its BNPL engine and discovery/shopping platform) and in Square (offering BNPL to Square merchants).

It will also cross-sell Afterpay, Cash Pay and Square. Cash Pay can be sold to Afterpay’s merchants and Afterpay can be sold to Square’s merchants. Moreover, Afterpay is generating almost 50% of its GMV from enterprise customers which is a key growth area for Square.

Afterpay turns its consumer receivable book 15x per year generating a high return on capital and a low risk exposure.

Saturday, Sep. 3rd: I looked at Klarna’s H1-2022 financial report. - Klarna

Klarna has 150m active global consumers, 450k retail partners, 23m MAUs, 1.6m card holders ($6.5bn in total deposits), is present in 45 countries, generated $41bn in GMV (21% YoY growth) and $782m in operating income (18% YoY growth) in in H1-22.

In the US, Klarna has 30m consumers, 31 of the top 100 US retailers, and doubled its GMV in H1-22 compared to H1-21. It’s Klarna’s second largest market by revenue. Klarna used to be profitable for the first 14 years of its existence. It decided to burn cash to capture the US market and shift from a BNPL provider to a broader finance/commerce platform.

Klarna took harsh decisions since the beginning of the year: (i) raising a $800m down-round at a $6.7bn post money valuation, (ii) laying-off 10% of its workers, (iii) reducing credit losses.

“I know is that our business model is so much better in a tougher economic environment than the traditional credit card model. Credit card companies will hand consumers a $30k limit, and try to get consumers to spend, spend, spend, at the highest possible interest rate because that’s how they make money. Our business is very different. The average outstanding balance is $100. It’s only outstanding for less than two months, and paid off in installments. So consumers pay what they owe over a period of time - that helps their cash flow - and no more. In an environment where interest rates are rising, as a consumer you don’t want to be in the hands of credit card companies - your interests are not aligned with theirs.”

Sunday, Sep. 4th: I read McKinsey’s report on fintech in Africa. - McKinsey

Market leaders have 6 characteristics: (i) match their value proposition to local markets, (ii) quickly acquire a large base of users, (iii) have clear monetization strategies (either multiple revenue streams combined or one large revenue stream), (iv) understand & solve for Africa’s offline market, (v) collaborate with regulators, (vi) manage lower expected revenue per customer.

In 2020, African fintechs generated $4-6bn in revenues representing a 3-5% market penetration and with a potential to grow by 10% in CAGR by 2025. In Africa, 10% of transaction are digital (vs. 90% of transactions that are cash-based). In 2021, there were 5.2k startups in Africa (3x YoY) with almost 50% in the fintech sector. 65% of Africans remain unbanked or underbanked.

McKinsey distinguishes 3 paths for fintechs to scale: (i) scaling massively a non-financial product before adding basic and then more complex financial products, (ii) launching a specific B2C or B2B financial product solving a specific need on the market before expanding into other financial products, and (iii) starting with a local infrastructure product before launching a comprehensive suite of financial products locally and eventually scaling in other geographies.

Monday, Sep. 5th: I listened to a Colossus’ podcast episode with Ravi Gupta who is partner at Sequoia. - Colossus

Ravi worked at KKR for 10y. He left to become CFO and then COO at Instacart before joining Sequoia as partner.

“You should keep the main thing the main thing.” You should prioritize and execute against one unique goal. If you chase too many objectives, you will end up not delivering them. You will end up valuing activity over progress. For instance, at Instacart, in 2015, the whole company had to focus on generating positive unit economics to save the business. At the time, the company was loosing $14 per order and was burning $12m per month. It worked out because the whole company was executing against this unique objective.

In venture, focusing on the main thing implies that you should make investments only in companies which have the potential to become one of the few dozens companies that will count in the next decade because venture is a business driven by the power law. Ravi had the following questions at the top of its notebook for every meeting with companies: “If you could only make one investment this year, would this be it? Would you tell your best friend that they should go work at this company and take options at the price of the round? Would you do that? Do you want to be in the board of this company in the next 10 years?”

In order to assess founders, Ravi Gupta combines several best practices: (i) caring about getting to know the person in front of you independently from wether you want to invest, (ii) bring founders in different settings that what they’re used to (e.g. going for a walk), (iii) willingness to ask the hard questions.

“I try to look for companies that are early and inevitable.” (e.g. Stripe, Faire, Benchling). Ravi also seeks founders who know their business in every details which is a good proxy to identify founders who really care about the business they’re building.

At Sequoia, “yesterday does not matter”. “We’re only good as our next investment.” Sequoia has a culture with 3 pillars: performance, teamwork and the mission to leave the firm in better shape than how you found it.

Tuesday, Sep. 6th: I listened to an Acquired’s podcast episode on Square (now known as Block). - Acquired

When Square started, it was extremely hard for a small merchant to get approved by a bank to open a merchant account and to process transactions. Square has a straightforward experience. You sign-up online, you receive a card reader for free by mai, you start processing transaction by paying a 2.75% flat transaction fee and you received transactions in your bank account in 1-2 business days.

In Square’s early days, Jim McKelvey and Jack Dorsey worked with Robert Morley who was professor at the Washington University in Saint Louis and who had a technology to read credit cards via a hardware to plug on a mobile phone. Robert Morley was never a Square’s official founder but he sued Square (for patent infringement and for forcing him out) in 2014 and found a settlement with the company in 2016 for $50m.

In the early days, Square was a credit card reader. It later evolved into a broader cloud-based point of sales.

Square introduced a business model innovation. It bundled software and hardware for free/at a very reasonable cost and was making its revenues from transaction fees.

Wednesday, Sep. 7th: Marie Brayer at Fly wrote about the current market situation. - Marie Brayer

“Entreprise software / cloud valuations should go back (maybe quickly, maybe in the next 12-24 months) to 10-15x for the good stuff and give everyone ”normal” laws of physics to work with. I don't expect 2021 50x valuations to re-occur though.”

“If your >2M€ fundraising in Q2/3 was very hard or failed, don’t take it too personally. Even if Jesus had been raising a 100M$ round in Q3 no one would have cared. Very few TS were sent overall in Q2-Q3 except for seed rounds.”

“Due to reporting lag, there is no “external” datapoint that can help you realize as a founder how inactive most VCs are right now but they are.”

Marie gives the following fundraising advice: (i) delay your funding round if you can, (ii) have a partner/GP intro to get a deal done, (iii) reduce your funding ask by 50%, (iv) be over-prepared (pitch deck, data-room, fundraising process), (v) pitch a new category over an existing category, (vi) growth is still the 1st metric that investors are looking at but you should also have strong unit economics, (vii) sell your product beyond start-ups and scale-ups.

Thursday, Sep. 8th: Misfits Market acquired Imperfect Food which is its most direct competitor in the US. - BusinessWire, Forbes

Both players are creating and leading what I called the “avoid waste upstream” category in the grocery sector. On the one hand, they partner with food producers and wholesalers to help them monetize food that is not suited to be distributed in retail (e.g. fruits that are too big or damaged pasta boxes) and that would have been otherwise wasted (30-40% of the food supply in the US). On the other hand, they sell to consumers boxes with food products at discounted rates compared to supermarkets (40% markdown) and accessible via a subscription. They started with fruits and vegetables before expanding into other grocery categories and launching their own private label.

The combination will have 500k members and will generate $1bn in sales post integration. Moreover, it’s supposed to reach profitability by 2024.

Misfits Market was founded in 2018 and raised at a $2bn valuation in Sep. 21. Impossible Foods was founded in 2015 and raised at a $700m valuation in Jan. 21.

It’s another proof-point that the digital grocery sector is experiencing a strong wave of consolidation driven by (i) declining growth rates with the return to normal following the covid boom and by (ii) the general race to profitability in the sector.

Friday, Sep. 9th: I listened Roelof Botha (GP at Sequoia) on Tim Ferris’ podcast. - Tim Ferris

When he joined Sequoia, Roelof used to write “10^9” on the corner of its notebook every Monday when the team was doing its partners meetings (entrepreneurs pitching the Sequoia’s partnership). To remind him constantly its objective to produce meaningful gains for the fund, he sets the objective to return $1bn to its LPs thanks to its investments.

He uses other reminders to track and be reminded about the key things he wants to accomplish for both Sequoia and his portfolio companies (top 3 actions to support them in the next 6 months).

In his career, Roloef did not take the path with the least resistance and took risky decisions. He studied actuarial science because it was the hardest program to get accepted and because it was a way to work outside South Africa. He left McKinsey and took a large salary cut to join PayPal.

Don Valentine has a 2x2 matrix about founders with one axe from not exceptional to exceptional and another from not easy to get along to easy to get along. Don said that the best founders were the ones who were exceptional and not easy to get along. It’s because you will need resilience and obsession to be successful. You will need to have the engine of personal frustrations to overcome the challenges to build a great business. You cannot just accept the reality and you will be hard to manage when the world does not fit what is your idea of the world.

Founder-market fit or founder-problem fit is a key success factor for startups. Roloef always asks founders: How did you come up with this idea? What is it about the current solutions that you must have evaluate that frustrated you and that you think are not good enough? What is your unique compelling value proposition?

Sequoia does pre-parade and pre-mortem before doing an investment. A pre-parade explicits what success implies for the company. A pre-mortem explicits what could go wrong for the company. Sequoia also does pre-parade and pre-mortem for its own company.

Sequoia’s main risk is to rest on its past successes. Sequoia’s internal motto is that: “you’re only as good as your next investment”. Sequoia should continue to keep meeting and investing in the next iconic companies as soon as possible.

Saturday, Sep. 10th: EQT raised a €2.2bn growth fund to back European entrepreneurs with tickets between €50m and €200m. It will invest in 20-25 companies predominantly into 4 sectors including enterprise, consumer/prosumer, healthcare and climate. It will target an ownership between 5% and 40% (which is usually high for a growth fund). EQT has already made 7 investments including Vinted, Mambu and Epidemic Sounds. - Tech.eu

Sunday, Sep. 11th: Tesseract raised a $78m round from led by Balderton and Lakestar with the participation of Accel, Creandum and Lowercarbon. It’s a climate-tech startup started by two former Revolut employees (Alan Chang who was 3rd employee and right hand-man to Revolut’s CEO and Charles Orr who led strategy at Revolut). Tesseract aims to decentralize energy production. It will acquire renewable energy assets. Instead of installing a solar panel, consumers will be able to acquire a virtual solar panel or wind turbine on Tesseract’s mobile app in order to get their electricity. - Sifted

Monday, Sep. 12th: I read a post from The Economist on the Visa-Mastercard’s duopoly. - The Economist

In the US, merchants pay $138bn in interchange fees every year. Visa and Mastercard are processing 3/4 of credit card transactions. They are extremely profitable generating respectively 51% and 46% in net margins in 2021.

With the shift away from cash to digital payment methods following the covid crisis, Visa and Mastercard are increasing their footprint. American consumers used their credit cards for 51% of their transactions in 2021 compared with 45% in 2016.

Visa and Mastercard are facing 2 main threats: (i) regulations (e.g. in Europe interchange fees on consumer credit cards are capped at 0.3%) and (ii) alternative digital payment methods bypassing card schemes (e.g. AliPay, Grab or Mercado Pago).

In July 2022, Richard Durbin proposed a new regulation in the US called the Credit Card Competition Act which wants to break the links between banks and card networks. It will force banks to offer merchants at least two card networks to process transactions and one of them would have to be neither Visa nor Mastercard.

Tuesday, Sep. 13th: I listened to a Colossus’ podcast episode with Mitch Lasky, who is partner at Benchmark, on the gaming sector. - Colossus

Gaming is unfairly perceived by most investors as a hit driven and short lifetime business.

It’s a customer acquisition and a customer lifetime business. It’s driven by content (an aesthetic call has to be made beyond initial metrics) and network effects.

Modern changes in gaming: free to play, direct distribution, multiplayer, subscription based.

Platform-based publishing. In the past, physical distributors had the upper hand in the gaming value chain. Today, digital platforms like Fortnite/Epic Games, LoL/Riot, Steam or Xbox Game Pass have emerged as demand aggregator. As a result, they have an impact on the gaming value chain making it worth for them to internalize a portion of the content they sell on their platform. Moreover, game developers have to be on certains of these platforms (esp. Steam and Xbox Pass).

How monetization has changed in gaming? It moved from an inelastic pricing (buying a $70 game with a disk no matter how much you play the game afterwards) to an elastic pricing model (gave the game for free and push the monetization depending on their game usage).

Gaming is a $190bn industry - 55% from mobile, 25% from consoles and 20% from PCs.

The rise of mobile gaming has accelerated the shift towards free to play, has created many innovations around monetization, has given rise to dark patterns around advertising and has pushed acquisition budgets to an unseen level (25% of expected revenues spent on acquisition in the past and today it can be up to 90%).

Twitch is now a core component of gaming. Game developers are thinking about making their game streaming friendly and are integrating Twitch as a distribution channel in their go to market strategy.

What are the features making a game long lasting? Fun gameplays, durable replayable design patterns, strong game communities.

The best gaming communities are open to new members and are generating a lot of UGC (inside and outside the game).

Apple’s changes around IDF have a major impact on mid core and hard core mobile gaming user acquisition. They make it much more harder to target whales with Facebook’s direct response advertising. In reaction, companies are working on alternative approaches like becoming cross-platform to drive installs on PC thanks to partnerships with streamers while driving monetization on mobile.

Mitch is interested into location-based entertainment creating experiences bridging the online and offline worlds (e.g. Pokemon Go or Snap AR).

Wednesday, Sep. 14th: Kojo (ex. Agora) raised a $39m series C led by Battery. It’s a procurement platform for construction companies to help them manage their suppliers and get the best prices for the materials they need on construction projects (3-5% savings on construction materials which is massive in an industry with an average 5% profit margin). It started with electrical contractors and had now expanded to support contractors in areas like mechanical, concrete, drywall, roofing, flooring and site preparation. Kojo was founded in 2018 and launched its product in 2020. It powered 10k construction projects. It processes $1bn in construction volumes and it grew its ARR by 3.5x YoY. In 2021, it launched 3 products including inventory management, bills of material and invoice matching. Kojo is planning to add fintech features on the platform like payment processing and automatic invoice reconciliation. - Techcrunch, Battery

Thursday, Sep. 15th: Northzone raised a €1bn for its tenth fund. It’s a generalist fund (fintech, healthtech, SaaS, workplace software, consumer apps, entertainment) investing into category defining companies from seed to pre-IPO. - Northzone, Tech.eu

It started in 1996 in Stockholm as an early stage investor in the Nordics. It invested into successful companies like Spotify, Klarna, Kahoot or iZettle. Since then, it has expanded to become a pan-European fund.

Northzone has also an office in the US to support portfolio European companies expanding in the US and to make investments in the sectors in which the team has a strong expertise.

It has a network of 300 entrepreneurs to support their founders. It claims to have a “full-stack” positioning preserving significant reserve to invest in multiple rounds in portfolio companies.

Friday, Sep. 16th: Adobe is acquiring Figma for $20bn (50% in cash, 50% in stock). Figma is a UX/UI product design platform. It has become a market standard out-executing both AdobeXD and Sketch. Figma is on track to generate $400m in ARR by the end of 2022 growing at 100% YoY with a 150% Net Dollar Retention, a 90% gross margin and positive operating cash flows. The main rationale behind Adobe’s acquisition of Figma is to remove an existential threat to preserve its monopoly on the design tool market. Besides, Adobe wants Figma to support its efforts to bring its creative products suite to the new design tooling paradigm created and led by Figma (web-first, multiplayer, easy to use, freemium). - Adobe I, Adobe II, Figma

Saturday, Sep. 17th: I read a post aggregating interesting business frameworks. - Aishwarya

“A specialised tool will always beat a generalised tool overtime. A Swiss Army knife is very useful when you are space constrained. It is less useful when you need a dedicated screwdriver to assemble a room full of furniture. Similarly, products with a generalized value proposition will inevitably be cannibalized by more specialized competitors.”

“Elasticity of demand approaches zero as you ascend Maslow’s hierarchy of needs. Assuming that items are not subject to scarcity pricing of utility value (i.e. there is a pandemic and toilet paper is out of stock), consumers have an increasing willingness to pay any price as you move up Maslow’s Hierarchy of Needs. Self-actualization has virtually inelastic demand. Self-expression also has highly inelastic demand.”

“Market risk vs. execution risk. Market risk is where the demand for the product is unknown. Execution risk is where the demand is well understood, but the hard part is in the delivery of value against existing competition. Any company that is pure execution risk without any market risk is not a suitable venture investment.”

“Why “Why now?” Venture capital is a very specific instrument that is purpose built to fund companies that are capable of explosive value creation over compressed periods of time. Concurrently, the invisible hand is a constant force that continually reduces the ability of any one company to generate outsized value. That means that venture capital is particularly well suited to finance companies that are capitalizing on “dam-breaking” moments—sudden changes in technology and regulation (and to a lesser extent, capital markets and societal shifts). […] Without a sufficient answer to the question of “Why Now?”, any venture capital invested into the company or category is subsidizing company building that would be better served by alternative capital instruments (with a lower cost of capital, i.e. debt, etc.). […] The reason why we have not recently seen additional mobile-first social companies emerge is because we are well into the half-life decay of the smartphone. The vast majority of the capturable enterprise value in the mobile social space was done in the first few years after smartphone saturation (Snapchat was founded in 2011).”

Sunday, Sep. 18th: TCG invested $100m into Night Capital in order to buy D2C brands that can be scaled by leveraging Night Media’s network of content creators. Night Media is a company founded by Reed Duchscher who is managing content creators including MrBeast and Night Capital will be a subsidiary of Night Media. Instead of relying on paid marketing on Meta and Google, D2C acquired brands will be able to build a unique distribution edge thanks to Night Media’s network. - The New York Times

Monday, Sep. 19th: Mark Suster (GP at Upfront) wrote about the future of venture capital in a world that will have fully integrated the tech public downturn. - Mark Suster

We’re entering a new normal in which public SaaS companies will trade at 10x EV/NTM Revenues. Valuations in private markets are progressively resetting to adjust to this new reality. It will take 6-24 months.

In the US, VC funds have $290bn in dry powder. This capital will be deployed but it will deployed patiently only in companies with adjusted valuation expectations.

Upfront has a “super focus” investment strategy writing $2.0-3.5m seed tickets from $200-300m funds and targeting a c.20% upfront ownership. It has been extremely consistent in executing this strategy across multiple funds.

Upfront has strong industry expertise (healthcare, fintech, computer vision, marketing tech, gaming infra, sustainability, applied biology) with a partner leading each expertise. It allows Upfront to have an edge against competitors.

“In any given fund 5–8 investments will return more than 80% of all distributions and it’s generally out of 30–40 investments. So it’s about 20%.”

Tuesday, Sep. 20th: Bain wrote about the key success factor for companies building embedded finance solutions. - Bain

Bain defines “embedded finance as a nonfinancial software platform providing an adjacent financial service, for which it takes some degree of economic ownership”. It distinguishes the following segments: banking, payments, lending, insurance, tax, accounting, payroll, benefits and procurement within marketplaces.

Thanks to embedded finance, financial services are increasingly integrated into software products (e.g. ecommerce with Shopify, food delivery apps with Uber, wellness with Minbody). “End users increasingly prefer the convenience of using payments, lending, insurance, and other financial services embedded in their day-to-day software, rather than accessing standalone services from traditional financial institutions.”

By embedding financial services, software platforms are able to improve the value proposition for their customers: (i) a better customer experience, (ii) cost savings because financial services is bundled with software and (iii) increased access to financial services thanks to superior underwriting.

Platforms leveraging embedded finance are the best positioned in the value chain compared to fintech enablers because they own the relationship with end customers and can leverage competition between enablers to increase their share of the embedded finance profit pool.

Wednesday, Sep. 21st: I listened to a Colossus’ podcast episode with Trina Spear who is the CEO and cofounder at FIGS which a D2C brand selling scrubs to healthcare professionals. - Colossus

FIGS disrupted the category with a vertically integrated approach in which it manufactures and distributes medical apparels when the market was usually split between manufacturers and retailers. As a result, manufacturers did not have the customer feedback loop on their products which led to poor customer satisfaction.

FIGS designed healthcare uniforms that were both technical (like apparel for athletes) and comfortable.

In this industry, manufacturers used to be screwed by other players in the value chain: giving away 60% of the price to retailers and 8-12% in royalties to brand owners. With a vertically integrated model, you can reinvest margin dollars into product innovation, marketing and community building.

FIGS has built a lovable brand in an industry without brands. Healthcare professionals were wearing scrubs like if they were a complete undifferentiated commodity.

Word of mouth was a strong growth driver for FIGS because healthcare professionals talk to each other all day long in the hospitals and healthcare professionals wearing FIGS scrubs are walking billboards.

FIGS is a non-seasonal apparel business and has streamlined SKUs with 13 styles accounting for 80% of revenues. It makes the business super efficient and it makes the collaboration with manufacturers and fulfilment centers extremely convenient.

Going forward, FIGS is working the following growth levers: (i) geographical expansion beyond the US, (ii) product expansion beyond scrubs (e.g. fleeces, vests, underscrubs, leggings) which are still generating 80% of sales, (iii) gender expansion to better serve men (25% of healthcare professionals).

Thursday, Sep. 22nd: Yann Ranchère wrote about SoftPOS. - Yann Ranchère

“SoftPOS or Software Point Of Sales allows merchants to use a phone or device as a card payment terminal without needing additional hardware. This might seems like a small change, but it has a massive impact on embedded Finance for SMEs.”

Small merchants no longer need a specific hardware to act as POS to process transactions. They can use their mobile phones which are much more powerful than traditional POS and which have now the right encryption capabilities to process payments.

“With Software POS, it will be possible for a software solution to onboard a user instantly to accept card payments In Real Life. It opens a new set of opportunities for verticalized SaaS solutions for services businesses or any merchants acquiring payments In Real Life by fundamentally reducing the existing friction.”

“With Software POS, traditional card payments will be more easily blended within a complex payment flow, whether alternative rails, inventory management, payment split, etc.”

Friday, Sep. 23rd: 1M Robotics raised a $16.5m series A led by Ibex with the participation of Target Global and Emerge VC to create automated nano-fulfilment centers for last-mile delivery. It sells to quick commerce players and retailers wanting to add fast delivery to their offering. It will use the funding to expand into new geographies, grow its team and sign other enterprise customers. - The Robot Report, Techcrunch

Saturday, Sep. 24th: Robin Dechant (cofounder and CEO at Kwest) wrote about the European workforce crisis. - Robin Dechant

The European workforce is expected to shrink by 13.5m people until 2030 (4% of the workforce). It’s even more problematic in some countries like Germany, Italy or Poland. For instance, in Germany, the country is expected to lose 4m workers by 2030 and 8.7m by 2040.

There are 4 main levers to mitigate the problem: (i) immigration, (ii) education to empower people with the skills they need for their jobs, (iii) create better employment and wage opportunities, (iv) invest in tech & automation.

Several solutions can be brought by governments: removing frictions for worker immigration, favouring apprenticeship, increasing minimum pay, making work more flexible to increase the pool of workers.

Sunday, Sep. 25th: Louis Coppey (partner at P9) wrote about modern creative tools trying to unbundle Figma. - Louis Coppey

In May 2012, Adobe made the transition from on-premise to cloud by launching Adobe Creative Cloud (Adobe CC) and by starting to monetize via SaaS. In one-year, Adobe reached 700k subscribers and $233m in ARR.

Adobe CC is a platform with 20 creative tools that can be broken down into format outputs (photos, videos, UX/UI design, 2D design, podcasting, motion design). On each format outputs, startups are competing with Adobe.

Adobe estimates that the market for creative tools is a $40bn opportunity divided between creative professionals ($20), communicators ($15bn) and consumers ($6bn). It’s a fast growing market driven by the fact that everyone is now a creator and that “communicators are creatives without technical skills but significant content production needs and a high willingness to pay”.

To unbundle Adobe, startups can (i) address underserved segments to increase the TAM (democratizing the access to creation or empower communicators to become creators), (ii) make creative software collaborative, (iii) go after new platforms like mobile phones or tablets, (iv) make AI-based creative tools to automate the creative process, (vi) create viral growth loops by making creatives easily sharable.

Monday, Sep. 26th: P9 raised P9 VI which is a €180m fund to invest into B2B SaaS and marketplaces at seed stage with €0.5-5.0m tickets. It invests mainly in Europe and 25-30% in North America. I believe that P9 is an extremely successful seed investor for a couple of reasons: (i) small and partner-led investment team with investors who are independent thinkers, (ii) laser focus on B2B SaaS and marketplaces, (iii) pricing discipline and pricing power when they invest into companies, (iv) quality stamp on portfolio companies (a P9 startup is most of the time a company which has hired strong executives, which has great internal processes in place and which is already plug and play to work with series A investors). - Christoph Janz

Tuesday, Sep. 27th: Milan-based subscription apps targeting creators studio Bending Spoons raised a $340m round. It started in 2013. It has reached 500m downloads, has 90m MAUs and is generating $100m in ARR with its apps. It will use the funding to grow its apps, to launch new apps or to acquire other apps. Bending Spoons’ main app is a video editor app called Splice. - StartupItalia, Bending Spoons

Wednesday, Sep. 28th: Stockly raised a €12m series A co-led by Eurazeo and Daphni. Stockly is creating a new category in e-commerce. It builds a decentralised network of shared inventory to help brands, merchants and marketplaces to automatically buy or sell inventory to other network’s participants. At the moment, Stockly is focused on solving the ecommerce out-of-stock's pain point for merchants and marketplaces (e.g. GoSport, Decathlon or Galeries Lafayette). Stockly will use the funding to grow its team to 50 employees and to expand its network of brands, merchants and marketplaces - Overlooked, Techcrunch, Usine Digitale (🇫🇷), Les Echos (🇫🇷)

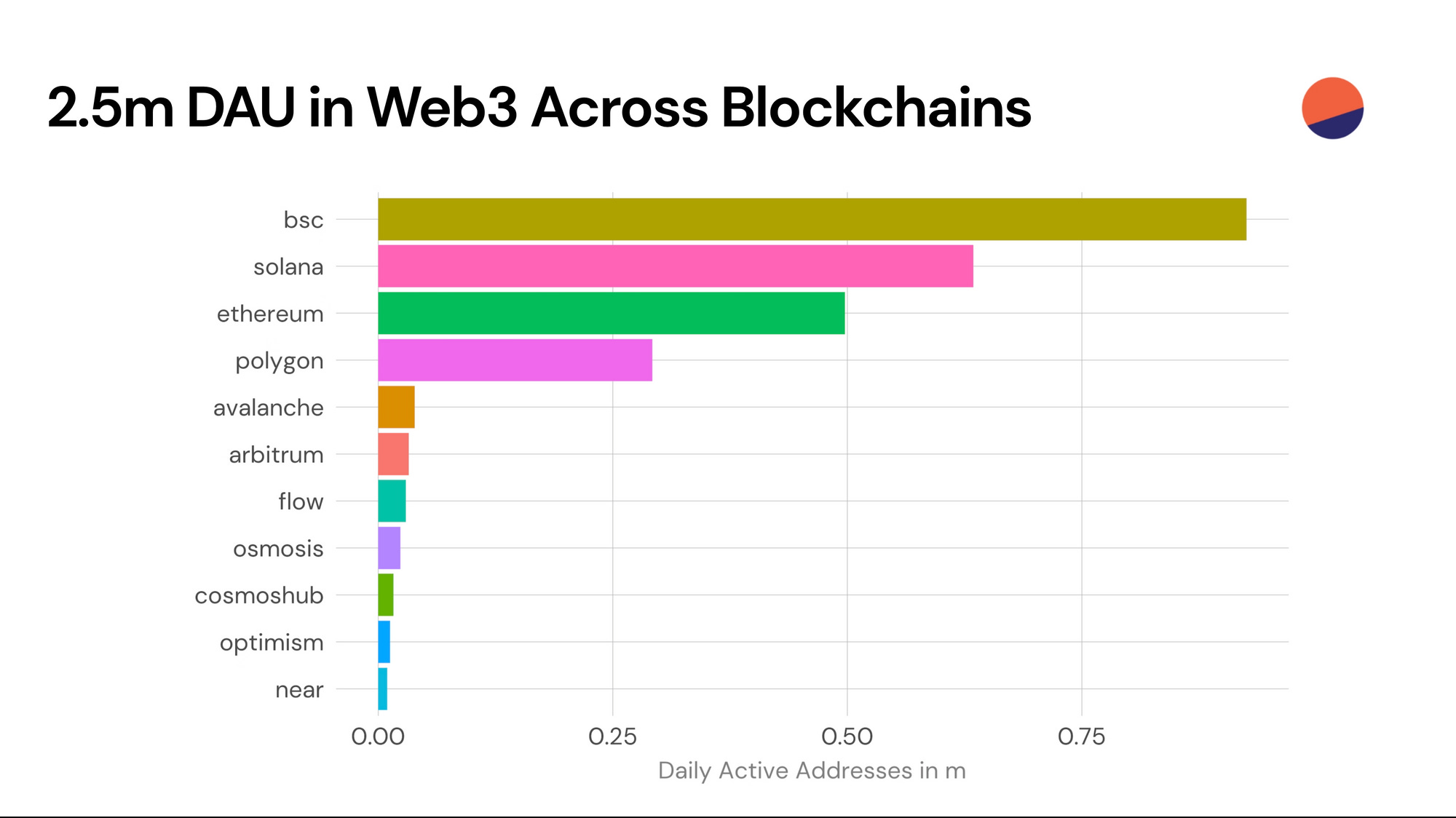

Thursday, Sep. 29th: Tom Tunguz published a presentation on the state of Web 3 in 2022. - Tom Tunguz

Some metrics: 2.5m wallets are daily active in the web3 ecosystem, centralised exchanges manage 100m active wallets, NFT volumes have fallen 97% from the top, layers 2 account for 30-40% of transactions on the Ethereum blockchain and consume only 2% of total gas and 5k developers push code to web3 every week.

Friday, Sep. 30th: Openstore raised a $32m funding round led by Lux Capital at a $970m valuation. It launched in 2021 in Miami as an e-commerce roll-up play in the Shopify ecosystem. Its sweet-spot is to acquire US-based D2C brands generating $1-10m in annual revenues. Openstore creates liquidity for merchants in the Shopify ecosystem. In the short-term, Openstore acquires, integrates and optimises brands selling on Shopify. In the long-term, it aims to create a unique e-commerce experience “bringing the experience of spontaneous discovery back online.” - Techcrunch

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋