📖 Venture Chronicles - October 2024

Overlooked #185

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of October.

Tuesday, Oct. 1st: Index dedicated an entire chapter to early hires in its guide on scaling startups. - Index

“Founders should prioritize “people-related” issues, spending up to 50% of their time on hiring, onboarding, and team organization.”

“Start with founder-led recruiting.” ”Hiring from your network makes hiring decisions less risky, and can give you strong conviction to compensate these individuals sufficiently to pull them in.”

“You should aim for 50–60% of early hires to have experience working for VC-backed tech companies.”

“Few startups hire an in-house recruiter ahead of raising a Series A, and only 10% of the companies we analyzed had hired a recruiter by the time their headcount hit 10.”

In the early days, “you have to be personally proactive in identifying, and engaging with, potential candidates. This founder-led recruiting strategy involves a mix between:

Secondary network—“friends of friends” including angels, investors and other people you know and trust,

Cold outbound—searching for specific profiles from specific companies on LinkedIn (you are advised to become proficient at using LinkedIn Boolean search), and then reaching out directly,

Inbound—cultivating an inbound flow of interested candidates through social media, blog posts, media presence, etc.”

“Analyzing the hiring patterns of successful startups offers templates for how to approach teambuilding, which vary by business model. On average, 4.5 of the first 10 hires are in technical roles, with 3 in GTM, and the remaining 2.5 split across G&A and Operations.”

“It’s critical to maintain a really high hiring bar early on. This will set the tone for all future hiring, which will ultimately determine your company’s success.”

“On average, one of the first 10 hires made by successful startups was at an executive level (C-suite or VP job title).”

“Most startups fail at hiring because they overvalue experience, and undervalue aptitude.”

“We recommend focusing on a Head of Talent or an experienced internal recruiter (five to seven years of prior experience) as your first hire into this area. The rule of thumb for triggering this hire is that you should have a plan (and funding) to hire more than 20 people over the following 12 months, with a sustained pace of scaling expected beyond that.”

“Your internal recruiter should report directly to the CEO, or alternatively to the COO.”

Wednesday, Oct. 2nd: Rich Barton is a successful tech founder known for creating billion-dollar companies like Expedia, Zillow, and Glassdoor. His strategy, called Data Content Loops, helps these companies dominate their markets by providing valuable information directly to consumers. This approach allows them to generate free user acquisition and build trusted brands in industries like real estate, travel, and job search. - Kevin Kwok

“Barton is a strong contender for the title of best consumer tech founder because of his repeated success. He’s founded three consumer companies each worth over a billion dollars with Expedia ($18.6B), Zillow ($8.8B), and Glassdoor (Said to have been acquired for $1.6B).”

“The Rich Barton Playbook is building Data Content Loops to disintermediate incumbents and dominate Search. And then using this traction to own demand in their industries.”

“In order to grow their demand high enough to become a beneficial flywheel, Barton’s companies use a Data Content Loop to bootstrap their demand and create unique content and index an industry online (homes for Zillow, hotels and flights for Expedia, companies for Glassdoor):

Expedia: Prices for flights and hotels that before you’d have to get from travel agent

Zillow: Zestimate of what your house is likely worth that before you’d have to get from broker

Glassdoor: Reviews from employees about what a company is like that before you’d have to get from a recruiter or the company itself.”

“His companies take power from the incumbents and give it to consumers. Instead of trying to hoard information, they are on the side of consumers and giving them more data transparency.”

”Glassdoor revealed how employees really felt about companies. Zillow shed light on what any house was worth. Expedia let people see the prices and availability of flights and hotels without talking to an agent. These were knowable things that people have always talked about with each other. There are few topics adults love gossiping about more than work, real estate, or travel.”

“They create common knowledge in their industries from information only middlemen had access to before, from public-but-hard to aggregate data, or from information collected from users themselves. These intermediaries, whether brokers or travel agents were misaligned. They controlled what information was shared with the public, but has an interest in withholding it. Instead of pushing increasingly more and higher quality information to the public, they maintained the status quo.”

“Before Zillow and Glassdoor, if you wanted to look up information about a specific home or company, there wasn’t a webpage for it. Barton’s companies created the definitive page for each house and company. Using a combination of data from authoritative sources (like all the various MLS systems) and user-generated data, they created high quality content unique to each company or listing. Being among the first to do this let them do a huge SEO land grab, which has been hard to displace since.”

Thursday, Oct. 3rd: French based consumer lending startup Younited will become a public company by merging with Iris Financial which is already listed on Euronext. Younited launched in 2012. Iris will invest €150-200m in Younited for a 40% stake implying a €375-500m valuation for Younited. After the acquisition, Younited will start lending from its balance sheet instead of raising capital from third parties. - BFM, Les Echos

Friday, Oct. 4th: David Peterson at Angular wrote about the issues associated with startups that are trying to “sell the work” instead of selling software. - Angular

Selling work has 3 core benefits: (i) opening up new vertical opportunities which were not addressable before because too challenging or unprofitable, (ii) aligning incentives with customers on an outcome based pricing and (iii) easier to sell a piece of a completed work than a productivity improvement.

“As is true for many service providers, any pricing power they have is based on their brand alone, and that isn’t enough to protect them from the deflationary impact of AI. Most of the benefits their customers imagined they were getting from AI (whether real or not!) got transferred right to their customers.”

“The continued competitiveness of open source models suggests to me that most of “the work” itself will eventually become a near-commodity. If that’s the case, then the clearing price for that work will continue to fall. In that world, only business models that don’t rely on making money by selling that work will succeed.”

Saturday, Oct. 5th: Harry interviewed Flo’s cofounder and CEO Dmitry Gurski. Flo is the leading women’s health mobile app specialised in period tracking with 70m MAUs, 5m paid subscribers and $200m in ARR. - 20VC

Dmitry Gurski grew up in the 90s in Belarus, a country left in ruins after the fall of the Soviet Union. His family had to grow their own vegetables in the garden because stores were empty. Dmitry started his career in book publishing, writing computer books and starting his own publishing house, ultimately becoming responsible for 2k educational books. When the App Store was launched, Dmitry decided to work on mobile apps, beginning with those whose content was based on books. After six years of building mobile apps, he started working on period tracking. It took multiple iterations before landing on a product with strong metrics.

“People accepted the idea to pay for subscriptions, and it was a huge cultural change.” “When we started monetisation, our dream was to monetise 5% of the American audience. Today, 25% of US women excluding teenagers are paying for Flo.”

“It’s good to have great competitors because you have an opportunity to learn from them. Great competitors speed up your execution pace and prevent you from becoming complacent.”

“When we launched Flo, I immediately understood that we had a chance to become a big business because our addressable market was obviously deep and retention was outstanding. I saw a long-term retention that I had never seen before.”

“Great retention is really rare in health and fitness. Retention does not depend on the product but on the use case. You can create the perfect fitness app it will always have a terrible retention because people will have the same churn rate as for physical gyms.”

“It's much more difficult nowadays than it used to be 10 years ago to get an initial audience organically even if your product is outstanding.”

For consumer mobile apps, simplicity is a key success factor. “For consumers, simplicity is more significant than anything else.”

Persistence is the key to success. “I don’t believe in talent. I believe that, all people are approximately the same. What makes people different is just hours of hard work, hard focused work.” “Most people, they just can’t work really hard for a very long time. And it’s what distinguishes successful people and less successful people.”

Successful founders must have a certain level of “craziness” to build a venture backed company. “Smart people work in McKinsey. Founders, they’re crazy. It’s not rational. Why would you do something with a 1% chance of success?”

Flo has a frugal company culture. “I never use business class. I would better pay one month of salary to a developer in Lithuania than waste this money for my comfort.”

Consumer subscription model is misunderstood by many investors. “Most investors just don’t understand this business model. They confuse it with SaaS and make very wrong conclusions because of that.”

Sunday, Oct. 6th: Revolut’s co-founder and CEO, Nik Storonsky, shared a guide on building high-performing teams. - Quantum Light

“A high-performance organization is A-player centric (top 15%-25%), focusing resources to retain and promote top talent while exiting under-performers as fast as possible.”

“Performance is a direct CEO mandate. Talent is a force multiplier for the whole company. It shouldn’t sit under HR, but it should be a core priority of the office of the CEO. We recommend setting up a small performance team reporting to the CEO, staffed with capable operators.”

“Performance is best articulated over three dimensions:

Deliverables, that measure ability to complete tasks assigned considering speed, quality and complexity

Skills, that are the technical competencies required for the role

Culture, that represents alignment with the company's overall values.”

Monday, Oct. 7th: HubSpot’s co-founder, Brian Halligan, shared valuable lessons on scaling the company. - Sequoia

“Perspiration vs Inspiration: In startup mode, the CEO role is 90% perspiration and 10% inspiration. In scaleup mode, the CEO role is 10% perspiration and 90% inspiration.”

“Manage your trust battery carefully: As a CEO, you generally start out with a fully charged trust battery. Over time you make calls—you get some right and get some wrong. If you get too many wrong in a row, you lose a lot of the charge in the trust battery with the organization and along with it some of your moral authority. My rule of thumb is that you get a few “CEO cards” to play that may be very bold bets or ones that your team disagrees with. You don’t have 52.”

“Keep your head in the sky and your feet on the ground: You need to paint a compelling vision of a terrific future for your company while at the very same time dealing head on with the very real problems you have today.”

“Your culture is your second product: At HubSpot, we have two products: one we sell to our customers (HubSpot’s CRM), and one we sell to our employees (HubSpot’s culture). Like your product, you need your culture to be unique relative to the competition (for talent) and you want your culture to be very valuable (for talent). Like your product, when your culture is unique and valuable, your company turns into a magnet that attracts and retains terrific talent. And also like your product, it’s never done—it needs continuous iteration.”

“My advice is not to sweat it too much if you need to replace leaders on your team as you grow. The company and the leader are likely both better off.”

“Recruit from companies just a few years ahead of you: I’ve found this applies to board members and executives. When we hire folks from companies that are several orders of magnitude larger than HubSpot (i.e. Microsoft, Google), there is an impedance mismatch. They are dealing with different issues at a different scale. We’ve had good luck with hiring folks who are at companies we admire that are just a few steps ahead of us.”

“Home grown talent is underrated: I’ve noticed that the VC playbook when a new round is done is to recommend “upleveling” some of the home grown talent. In some cases this might be right, but I think folks over index on it. If you look at the executive teams of some of the best companies (i.e. Apple, Nvidia, Amazon, etc) they are full of people who have been there a long time. HubSpot’s current management team has a lot of “home grown” talent.”

“When everyone is zigging, you should zag: Regardless of what you think of Peter Thiel’s politics, he wrote a really good book on startups called Zero To One. In it, he talks about how you need to be right about something that everyone thinks you are wrong about for a long time. This type of “zagging” worked for HubSpot three times.

First, we decided to focus on SMB (more M than S, btw) and stuck with it when everyone and their brother thought we should move to the enterprise.

Second, we decided we would move from a marketing application company to a CRM platform company, competing with Salesforce, when everyone and their sister told us we were crazy to try because they were too hard to compete with.

Third, we decided we would “build” (craft!) our CRM in-house as opposed to acquiring our way there when everyone and their cousin told us that we needed to follow ye olde CRM M&A franken-playbook.”

Tuesday, Oct. 8th: Hindenburg published a short-selling report on Roblox. - Hindenburg

Roblox is a $27 billion online gaming platform headquartered in San Mateo, CA. The company was incorporated in 2004 and is led by founder and CEO David Baszucki.

“Insiders have cashed out $1.7 billion in stock since the company’s 2021 direct listing. In the last 12 months, insiders have sold ~$150 million in stock, including ~$115 million by CEO Baszucki personally.”

“Our research indicates that Roblox is lying to investors, regulators, and advertisers about the number of “people” on its platform, inflating the key metric by 25-42%+. We also show how engagement hours, another key metric, is inflated by an estimated 100%+.”

“Our findings show that the company’s reported number of “people” regularly matches Roblox’s reported Daily Active Users (DAUs). But DAUs, according to Roblox’s own disclosures, “are not a measure of unique individuals accessing Roblox” because they can include numerous accounts run by a single person, such as alternate or bot accounts. Given these definitions, we believe Roblox intentionally conflates “people” with DAUs, consistently inflating the reported number of people on its platform.”

“We have more accounts registered to the U.S., multiple times over the population of the U.S.” ““Every time we see a user sign up, there’s a 60% chance that this sign up is from an alt [account]”

“Roblox forums detail how users regularly have dozens of alternate accounts to “farm” for goods on Roblox, avert bans and increase their follower counts, among other reasons.”

“In addition to alternate accounts, bots are rampant on the platform. For example, Roblox’s 7 most popular game, Adopt Me!, has garnered over 83,000 Change.org signatures to remove it from the platform due to extensive “botting” that “breaks” Roblox.”

“Beyond inflated key user metrics, our in-game research revealed an X-rated pedophile hellscape, exposing children to grooming, pornography, violent content and extremely abusive speech.”

“Roblox faces saturation in its top markets like the U.S. and Europe. It is now attempting to keep the appearance of growth alive by adding loss-generating users in markets like Asia, per a former employee. Profitability has plummeted despite reporting higher user metrics. The conversion rate of new daily active users to paying users has been in steady decline since 2020. Roblox is now hoping to drive incremental growth by pitching advertisers that ~79.5 million “people” spend an average of 2.4 hours per day on the platform.”

Wednesday, Oct. 9th: I watched Jason Lemkin interviewing Slice's CRO Lauren Padelford on scaling a vertical SaaS. - SaaStr

Slice serves independent pizzerias and generates over $100m in ARR. There are 30-40k independent pizzerias in the US, while large pizza chains like Domino’s and Pizza Hut collectively own around 20k pizzerias. Pizzerias generate $50bn in revenue. Slice provides software and services (e.g. marketing on their behalf, selling boxes) to help independent pizzerias run their businesses more effectively.

“We really vertically integrate the shop. We're looking at all the jobs to be done that a shop has. We help them do more of making great pizza and do less of running the shop.”

“To win SMBs as a vertical SaaS, you need to be the entire ERP to achieve the ROI they need.”

Vertical SaaS needs depth. Instead of point solutions, aim to become the "ERP" of your vertical, addressing all the customer's needs. “The true vertical would be the whole shop and that's what we're doing."

High ACV is crucial. Aiming for at least $10k annual revenue per customer is necessary to make the SMB model work. "You almost have to earn at least $10k a year from these very small businesses to make the math work."

“Pizza owners don’t want to find point solutions for everything they need. They want a single partner.”

As a vertical SaaS, you should own the majority market share and not only target a 10-20% market share as most horizontal SaaS do.

“Every shop that opens will just open in your platform just because you solved all the problems.” “You can open a pizzeria and immediately install the unfair advantage that Domino's has for your own local shop.”

“In sales, it's almost always a power law with 20% of the reps doing 80% of the number.”

To reach busy pizza owners, show value before pitching your solution. Help them succeed or connect with other owners to build community. It’s a long-term strategy, planting seeds for potential conversions down the line.

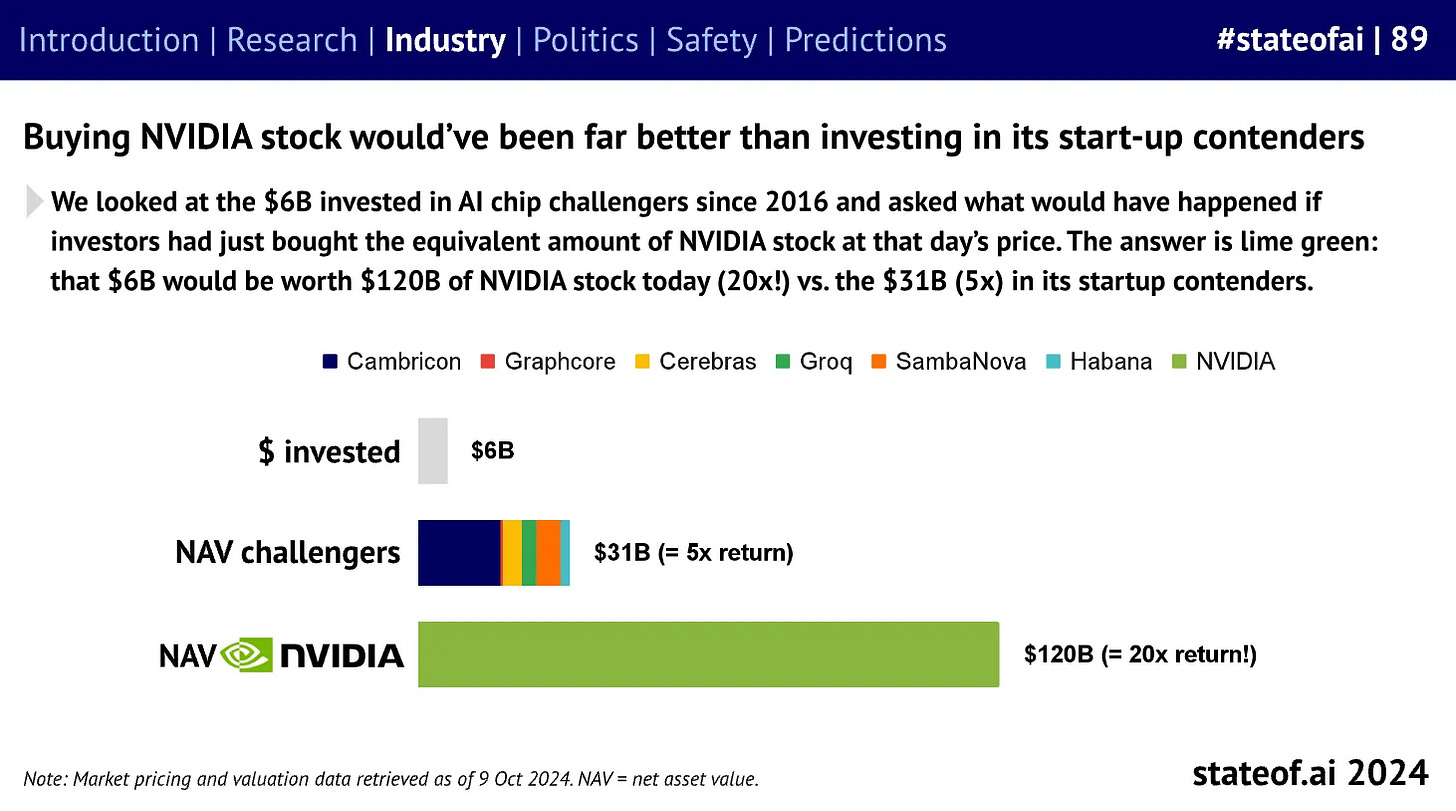

Thursday, Oct. 10th: Nathan Benaich at Airstreet published its State of AI Report for 2024. - Airstreet

“Frontier lab performance converges, but OpenAl maintains its edge following the launch of o1, as planning and reasoning emerge as a major frontier.”

“Foundation models demonstrate their ability to break out of language as multimodal research drives into mathematics, biology, genomics, the physical sciences, and neuroscience.”

“NVIDIA remains the most powerful company in the world, enjoying a stint in the $3T club, while regulators probe the concentrations of power within GenAl. More established GenAl companies bring in billions of dollars in revenue, while start-ups begin to gain traction in sectors like video and audio generation.”

“Although companies begin to make the journey from model to product, long-term questions around pricing and sustainability remain unresolved. Driven by a bull run in public markets, Al companies reach $9T in value, while investment levels grow healthily in private companies.”

“In April, Meta dropped the Llama 3 family, 3.1 in July, and 3.2 in September. Llama 3.1 405B, their largest to-date, is able to hold its own against GPT-40 and Claude 3.5 Sonnet across reasoning, math, multilingual, and long-context tasks. This marks the first time an open model has closed the gap with the proprietary frontier.”

“On novel tasks, where LLMs are unable to rely on memory and retrieval, performance often degrades. This suggests that they still often struggle to generalize beyond familiar patterns without external help.”

Friday, Oct. 11th: Sam Lessin and Yoni Rechtman from Slow shared valuable lessons on seed investing. - Sam Lessin, Yoni Rechtman

“The VC factory model is dead. People have watched and learned tough lessons on dilution mill — smart kids focus on capital efficiency and financial optionality vs. conveyor belt.”

“Evolution of software business model / death of 'selling software' and rise of software-leverage-to-gather-assets.....this is the clear 'shift in thinking' of the smarties.... Build the software to get the assets efficiently, the value isn't the software.”

“Diversification of downstream capital relationships as it becomes about asset acquisition, you need access to debt, etc. PE folks etc become way more relevant / building relationships there.”

Yoni loves pre-seed for 3 key reasons: (i) maximum flexibility to pursue the best plan because you can pivot as many times as you want, (ii) rare VC value added via collaborative due diligence and (iii) no time pressure.

Saturday, Oct. 12th: Dave Yuan wrote about franchise as an archetype for vertical SaaS companies. Franchises can serve as a model for vertical SaaS , offering business-in-a-box services to small businesses. Vertical SaaS can replicate franchise services like marketing, supply chain support, and demand generation. By bundling these, vertical SaaS can achieve higher revenue take rates and provide more value to their customers. - Tidemark

“Most Vertical SaaS companies get to 1% of GMV take rate, with the occasional high flyers getting to 3%. At Tidemark, we believe the industry has set its aims far too low. The ambitious founder can earn a much, much higher take rate.”

“A franchise is a company that sells “business-in-a-box” opportunities to entrepreneurs. In the typical franchise business model, the franchisor takes a revenue royalty in return for helping with aspects of the business. A 2018 report from FRANdata pegged the average revenue take rate to be 6% for franchisors across 29 industries, from pizzas to tax prep.”

A franchisor usually offers a bundle of services including (i) marketing support, (ii) in network demand generation, (iii) supply chain, (iv) operations playbook, (v) financing and (vi) IP.

Sunday, Oct. 13th: General Catalyst raised $8bn in capital with $4.5bn for its VC funds (seed, growth and healthcare focused funds), $1.5bn to incubate new companies and $2bn to develop strategic businesses. - FT, Tech.eu

“Behind the moves that we’re making is the fundamental observation that venture capital does not scale. There are the same number of outlier [companies] whether you make funds bigger or make funds smaller.” - Hemant Taneja

“The 25-year-old firm has launched a division to build companies, rather than simply fund them, and made a string of unusual investments. It announced plans to acquire a hospital system in Ohio this year, as part of Taneja’s push to embed technology into healthcare.”

“General Catalyst has also explored ways to hold companies for longer than the decade or so a traditional venture firm might. Those include considering strategies more familiar to private equity groups, such as launching a roughly $1bn continuation fund to hang on to start-up stakes and rolling up multiple small businesses in a sector to create one dominant player, according to people with knowledge of the plans.”

“General Catalyst has a deep history of hatching 45+ successful companies, including Commure, Crescendo, Demandware, Hippocratic, Homeward, Kayak, and Livongo.”

“This includes the Customer Value Strategy, which provides non-dilutive capital to accelerate growth, and the GC Transformation Flywheel, which connects innovators with adopters to drive industry transformation at scale.”

Monday, Oct. 14th: Stripe acquired of stablecoin infrastructure Bridge for $1.1bn. Bridge previously raised $58m from top investors including Sequoia, Ribbit and Index. - Forbes, Patrick Collison, Bridge, Sequoia

“Thanks to stablecoins, businesses around the world will benefit from significant speed, coverage, and cost improvements in the coming years. Stripe is going to build the world’s best stablecoin infrastructure, and, to that end, we are delighted to welcome Bridge to Stripe.”

“We’d like to believe that Bridge has played a small role in this transition. Shortly after launch, several cross-border payments companies integrated our APIs, proving that stablecoins could be used to make global money movement faster and cheaper.”

“Stablecoins represent an entirely new payments platform. Realizing the potential of this platform will be a decades-long journey. And as we’ve gotten to know the Stripe team, it’s become clear that we both share a vision for what’s possible with stablecoins and an excitement around the opportunity to create and build this future.”

“In 2023, when they shared their vision for a new stablecoin-based platform that would make all payments seamless with a single API, we were as excited about working with them as we were about their transformative idea.”

“Over the years, we have been fortunate to partner early with many companies that were later acquired and went on to change the world, including Instagram, YouTube, PayPal and WhatsApp. We believe Bridge will join that list of iconic companies that achieved their full potential after acquisition.”

“Bridge (FKA Shift Pay) is building APIs that enable businesses to allow users to pay with crypto easily and cheaply across different coins and chains.”

“Bridge aims to be a crypto native American Express, integrating with businesses to enable users to make purchases across the globe (across any chain) and settle in their native currency. Users can instantly transact in any crypto asset and pay for the purchase with the assets they already own. Eg: instantly buy an NFT with ETH, settle the transaction with USD; pay L2 gas fees in MATIC, settle in ETH.”

Tuesday, Oct. 15th: Turner Novak interviewed Slice’s cofounder and CEO, Ilir Sela. - The Peel

There are 80k pizza shops in the US who collectively manage c.$48bn in sales. 25% of pizzerias are owned by large chains (Pizza Hut, Domino’s). Pizza accounts for almost 50% of delivery orders in the US. 5k net new pizzerias opened in 2022 including 4.8k independent and 200 owned by large chains.

Much of Slice’s model is inspired by Domino’s in terms of their focus on digital and on making franchisees very successful.

You can make great margins from a pizzeria. It costs less $3 to make and the average retail price of a pizza in the US is $17.

“I would say over 30 family and friends have pizza shops” The Albanian community is very involved in pizzerias in the US because stopped in Italy before moving to the US where they worked in pizzerias and learnt the craft.

“Pizza owners are inheriting every business problem. They start off by wanting to make pizza and, and support their family but pretty quickly, they're inheriting financial jobs. They've gotta be the marketer, the technology person, HR, the whole thing. And it's incredibly lonely and it is incredibly difficult and challenging.”

“Slice was very important because I thought there could be a third way for people to operate in the industry. One way would be the franchise model. The second way would be purely independent. Third way would be working together as a team – having the support that is franchise-like, but remaining independent. So as we say in business, “for yourself, but not by yourself.””

“Slice brings forward the economies of scale and the capabilities that benefit the Domino's franchisees without having to trade off the independence.”

Slice started with commerce enablement (website builder & online ordering) to replace phone ordering. Slice launched Slice Register as second product, a point-of-sale system that helps shop owners manage all sales channels—online, phone, and in-person—by centralising information to streamline operations. Most recently, Slice launched The Goods which is a procurement arm to aggregate Slice’s pizzerias buying power to source and personalise packaging (e.g. pizza boxes, bags, plates, cups, napkins, etc.).

“The cool thing about multi-product companies, is that each product can be an on-ramp for the customer.”

“Slice started as a bootstrapped company. It was under the brand mypizza.com. The idea was to create a fourth brand to compete with the big chains with MyPizza being the brand representing all the independents.”

To get early customers, Slice did not directly pitch them online ordering. “[Pizzerias] all had a fax number on the physical menu that they would distribute, mostly aimed at companies so that some admin at a company would fax an order to a pizza shop.” These fax machines were generating 1-2 orders per day. Slice found a way to convert an online order into a fax order through an API. It came back to restaurants asking them if they were keen to receive many more orders on these fax machines entrenched in their habits instead of pitching online ordering.

“The franchise system is is pretty straightforward. You have a company that figured out a successful business model and put processes in place to a point where anyone can come in and replicate that same business model in some different geography, and then in exchange they get royalties.”

“Someone can apply to become a franchisee of Domino's. Domino's gives them the right to open up a Domino's location in a specific geography that's exclusive to them. They follow all of Domino's systems and processes, and they take advantage of Domino's brand marketing and buying power and community. And in exchange, they have to pay Domino's. I don't know if this is the exact number, but let's call it 5% or 6% of gross sales now. Some other things that can be in play is Domino's forces their franchisees to buy all of their supplies from Domino's. So 60% of Domino's revenue is the supplies they sell to their franchisees.”

Slice bootstrapped the business to $40m in GMV, $4m in revenues and $3m in profits in 2015 with less than 10 people in the team. He had an opportunity to sell the business for $18m and ended up raising $1m with Firstround at $15-20m valuation to bring Slice to the next step of its journey.

Slice launched a consumer app in 2017 and became Slice as a brand in 2019. In 2023, Slice generated $1.3bn in online GMV.

“We want to create an on-ramp, a platform so people can learn about what it's like to run a business, and then we want to be able to help them launch their new business.” “The goal is for you to be able to not only apply for financing [to launch your pizzerias], but what I would like to do is create an education platform.”

In the past 12 months, Slice has helped 4-5 locations to launch with white-glove service to find a place, buy equipment, build the brand, integrate tech and run their shop.

An online customer is worth 4x more than an offline customer. Online ordering AOV on Slice is $41 vs. $22 by the phone because you don’t have to order from memory. You can also do a lot of things to upsell your online ordering funnel. Moreover, you also get customer data to re-engage them via online channels (emails, SMS) which increases orders frequency.

Vertical SaaS have to turn on marketplace features and vice versa. Slice launched its own marketplace but its does not take a cut - just a flat fee per order.

Wednesday, Oct. 16th: Monzo’s cofounder and previous CEO, Tom Bloomfield, shared his interpretation of founder’s mode. - Tom Bloomfield

Great leaders maintain a close connection with the product and dive deep into specific details.

Successful CEOs balance detailed oversight with strategic delegation, ensuring leaders are effective and invested in the company’s core vision.

“The process of building and maintaining trust between a CEO and an exec involves the CEO repeatedly going incredibly deep on niche subjects, verifying that the exec really knows what’s going on in their department, and has a good grasp on the problems. As the exec builds trust, these deep-dives can become less frequent, but they never totally disappear. If the exec repeatedly doesn’t have a good grasp of the details as you dive deep into their domain, you quickly realize that you need to replace them.”

“I believe that great leaders have to be able to dig into the details, have an incredibly high bar for quality, and ultimately do great IC work themselves. Great managers have to manage the work - they should primarily be responsible for quality and speed of output. Managing people must be secondary to managing the product.”

Thursday, Oct. 17th: Gili Raanan’s venture capital firm, Cyberstarts, has achieved significant success by launching several multi-billion-dollar cybersecurity startups (Wiz, Fireblocks, Island, Cyera). However, it has come under scrutiny due to its adviser compensation program. Executives from major corporations, who stood to benefit from these startups, were part of a network that shared in Cyberstarts’ profits, prompting ethical concerns. In response to the growing criticism, Raanan recently suspended the profit-sharing component, drawing attention to potential conflicts of interest within their business model. - Forbes

“For some executives, there was more to it: compensation, potentially quite lucrative, in the form of profits from Cyberstarts’ blue chip early-stage funds. The execs who participated in Sunrise had the option to share in a pool of 4% of Cyberstarts’ own earmarked profits, known as carried interest, provided they took those calls and provided meaningful help, as determined by Cyberstarts.”

“Cyberstarts had written early checks to standout security companies including Wiz, the cloud security startup that recently turned down a $23 billion acquisition offer by Google; $8 billion-valued crypto security startup Fireblocks; $3 billion-valued enterprise browser business Island; and $1.4 billion-valued data security startup Cyera. Over the lifetime of one of the firm’s funds, participants could expect to see payouts of as much as $250,000.”

“Cyberstarts was suspending the compensation part of the program, effective immediately.”

“The executives who participated typically oversaw massive software and security budgets. Their organizations had the power to award exactly the type of large-sized contracts that could boost a fledgling startup’s financials and position it for success.”

“At worst, their own financial interests might cloud their judgment, or conflict with the best interests of their employer.”

“Of 54 advisers named on Cyberstarts’ own website in May, one-third have since been scrubbed.”

“In June, he’d told Forbes that about half of Sunrise’s advisers had opted into payments. But in October, he said the number was really only 20%, or about 15 people.”

“Last week, the firm announced its fourth seed fund, a $60 million vehicle bringing its total assets under management to $720 million.”

“[Gil is] a native Israeli who had served in Unit 8200, the elite cyber division of the Israeli Defense Force that has produced many of the country’s leading tech entrepreneurs, Raanan learned firsthand that technology alone didn’t lead to market traction.”

“After Sequoia’s Israel arm wound down in 2016, Raanan struck out on his own, launching Cyberstarts two years later in Mikhmoret, on the country’s central coast.”

“Since 2018, Raanan and Cyberstarts have achieved five exits, worth a combined $1.6 billion, without a single public flameout.”

“In addition to Chipotle, with its eight identified contracts, Forbes identified five contracts each signed with Cyberstarts startups at real estate giant Jones Lang LaSalle and pharmaceutical multinational Takeda, both of which have employed current or former Sunrise advisers. Mortgage lender New American Funding, security unicorn Armis and BNY Mellon, the world’s largest custodian bank, appeared to have signed contracts with four.”

“Cyberstarts “managed to crack the code” on achieving early product market fit. (Sequoia has since backed five Cyberstarts unicorns: Cyera, Fireblocks, Island, Wiz and Zafran.) “As a result, these businesses are often able to scale faster than usual,” Leone wrote.”

“As participants in Cyberstarts’ adviser network, called Sunrise, they were used to taking introductions from the firm to meet with its three or four new startup investments each year. The startups could receive product feedback and gain insight into what potential large-sized buyers needed. For the executives, mostly chief information security officers, or CISOs, the startup founders gave them the inside track on new technologies emerging from Israel’s elite hacking units.”

Friday, Oct. 18th: Adyen’s 2024 Embedded Finance Report highlights a $185bn market opportunity for SaaS platforms embedding financial services, with potential revenue growth of 3-4x. As demand from SMBs rises, only 20% of the market is currently served, leaving substantial growth potential. Embedded finance, such as payments, lending, accounts, and card issuance, allows platforms to centralize business and banking solutions, enhancing customer retention and revenue streams. - Adyen

Saturday, Oct. 19th: Jamin Ball at Altimeter wrote about misaligned incentives between founders and investors in venture capital. - Jamin Ball

“If we rewind the clock 15-20 years, fund sizes were significantly smaller. The 2% (annual management fees) part of the equation was nice, but if you wanted to “get rich” it was all about maximizing the 20%. In this path, the GPs and Founders win together - with large company exits. It was the singular focus of GPs and founders.”

“Fund sizes have ballooned significantly. So much so, that the 2% part of the equation is very meaningful given the size of funds! In the past, to “get rich” as in investor it was all about maximizing the 20%. Today, with fund sizes where they are, many are instead looking to optimize for the 2%. This means raising as much as possible, and deploying as much as possible (as quickly as possible).”

“In the past, the only path to “get rich” for GPs also resulted in a “get rich” path for founders. Today there is a “get rich” path for GPs where the outcome of the founders is irrelevant. Doesn’t matter how the underlying companies in a fund perform, you collect the annual management fees regardless.”

“Am I being offered more money at a higher valuation because the investor truly believes more than anyone else, or are they just playing a deployment game?”

“If your job as an investor is to always go find the next investment to deploy the next dollar, it gets really hard to actually slow down and work with each portfolio company / board you're on.”

“Ask yourself this question when deciding on who to work with. “Am I working with a 2% or a 20% venture firm?” The 2% firms are optimizing for deployment. The 20% are optimizing for large company outcomes.”

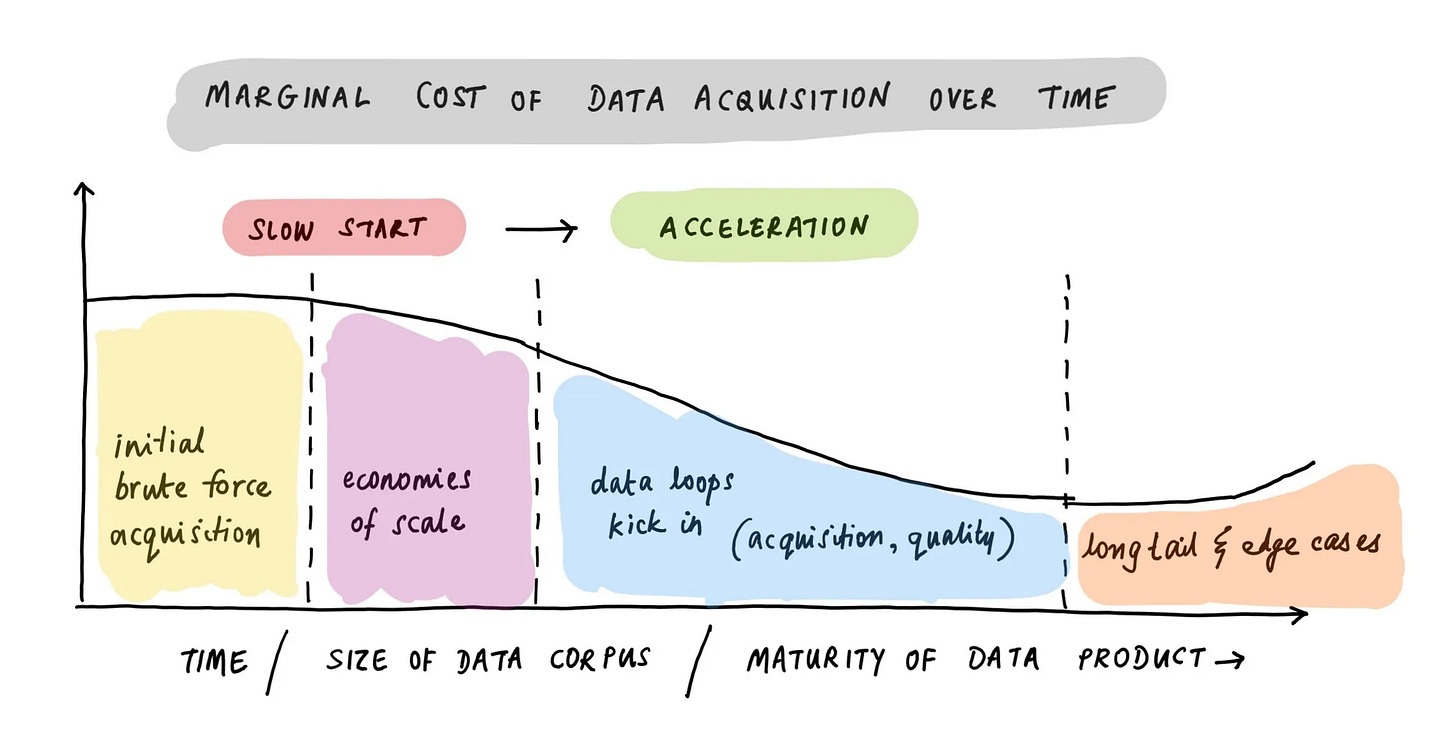

Sunday, Oct. 20th: Abraham Thomas wrote about the economics of data businesses. - Pivotal

“Successful data businesses are all built around a unique or proprietary data asset.” “Whoever controls the data, captures the value. Intermediaries get squeezed. A common failure mode is to build a business on top of somebody else’s data.”

“Businesses send their counter-party data to Dun & Bradstreet, in order to access D&B’s B2B credit database — which is based on aggregating all these counter-party reports.”

“If your data product is substantially similar to existing products, then one way to be ‘better’ is to offer a dramatically lower price. But this doesn’t work for data! The concept of minimum viable corpus means you need to be above a certain size and quality, else your data is almost worthless. And the very particular economics of data acquisition (brute force, economies of scale, data collection loops) mean that it's hard to build an MVC that’s dramatically cheaper than the incumbent offering. So ‘disruption from below’ rarely works.”

“Typically, a successful new data product is not a variation on the existing data; it’s a brand new data asset from a completely different source, exploiting a completely different set of loops.”

Data businesses rely on unique, proprietary data as their primary product, with various acquisition methods such as brute force collection, affiliate partnerships, and customer data loops.

Owning and controlling unique data is essential, as dependence on external data sources can limit value capture. Transforming and combining datasets creates proprietary value.

Data businesses require significant upfront investment but grow faster over time, benefiting from network effects, economies of scale, and increased data relevance, ultimately creating high barriers to entry.

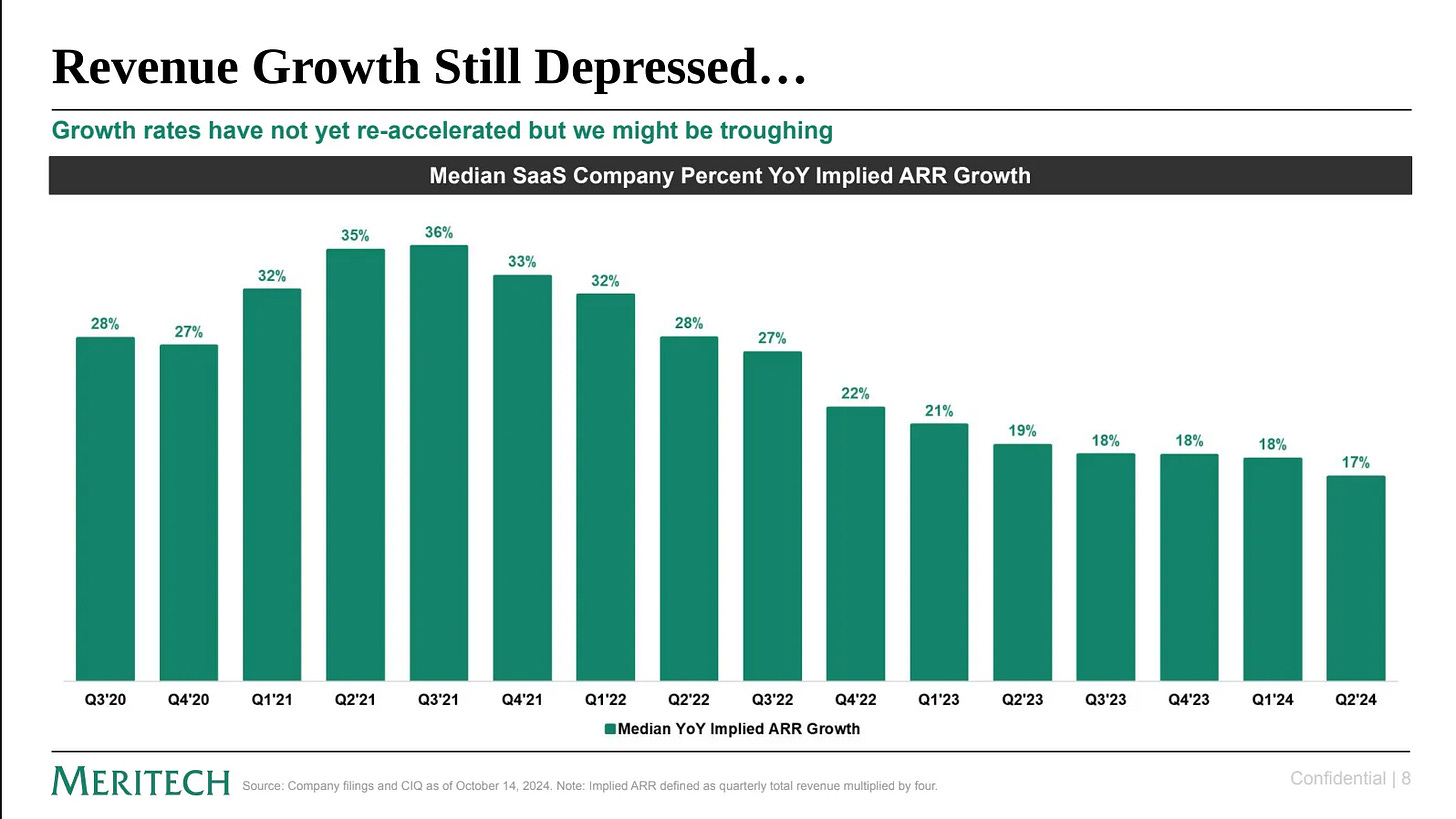

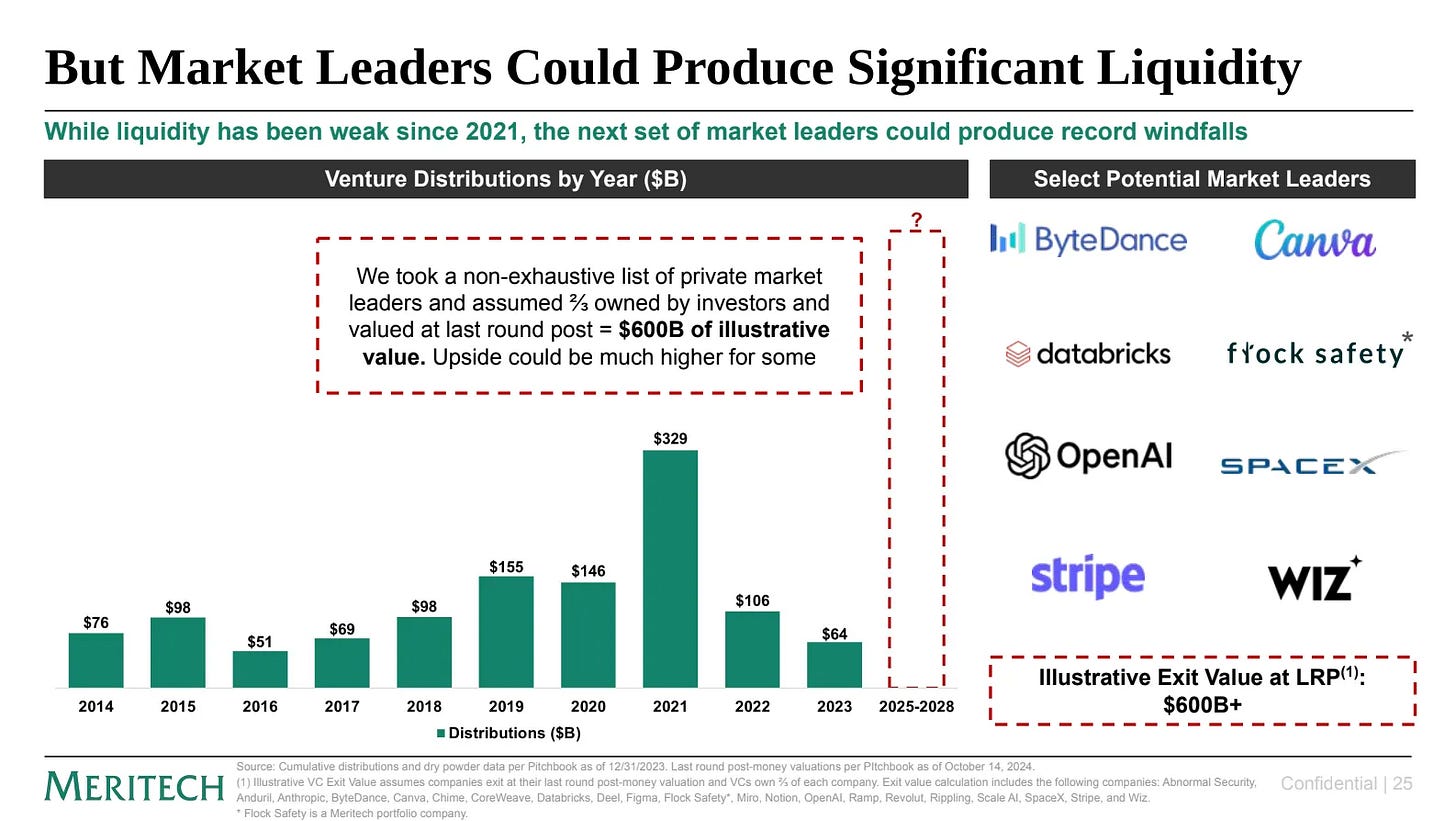

Monday, Oct. 21st: Alex Clayton publicly shared the presentation on the tech market that he prepared for Meritech’s LPs annual meeting. - Meritech

Equity markets are at an all-time high (24% YTD increase) but it’s mostly driven by large tech companies (e.g. Amazon, Apple, Arm, Google, Meta, Microsoft, Nvidia).

Median multiples for publicly listed SaaS are below historical norms (6.1x EV/NTM revenues vs. 8.2x before the post covid boom).

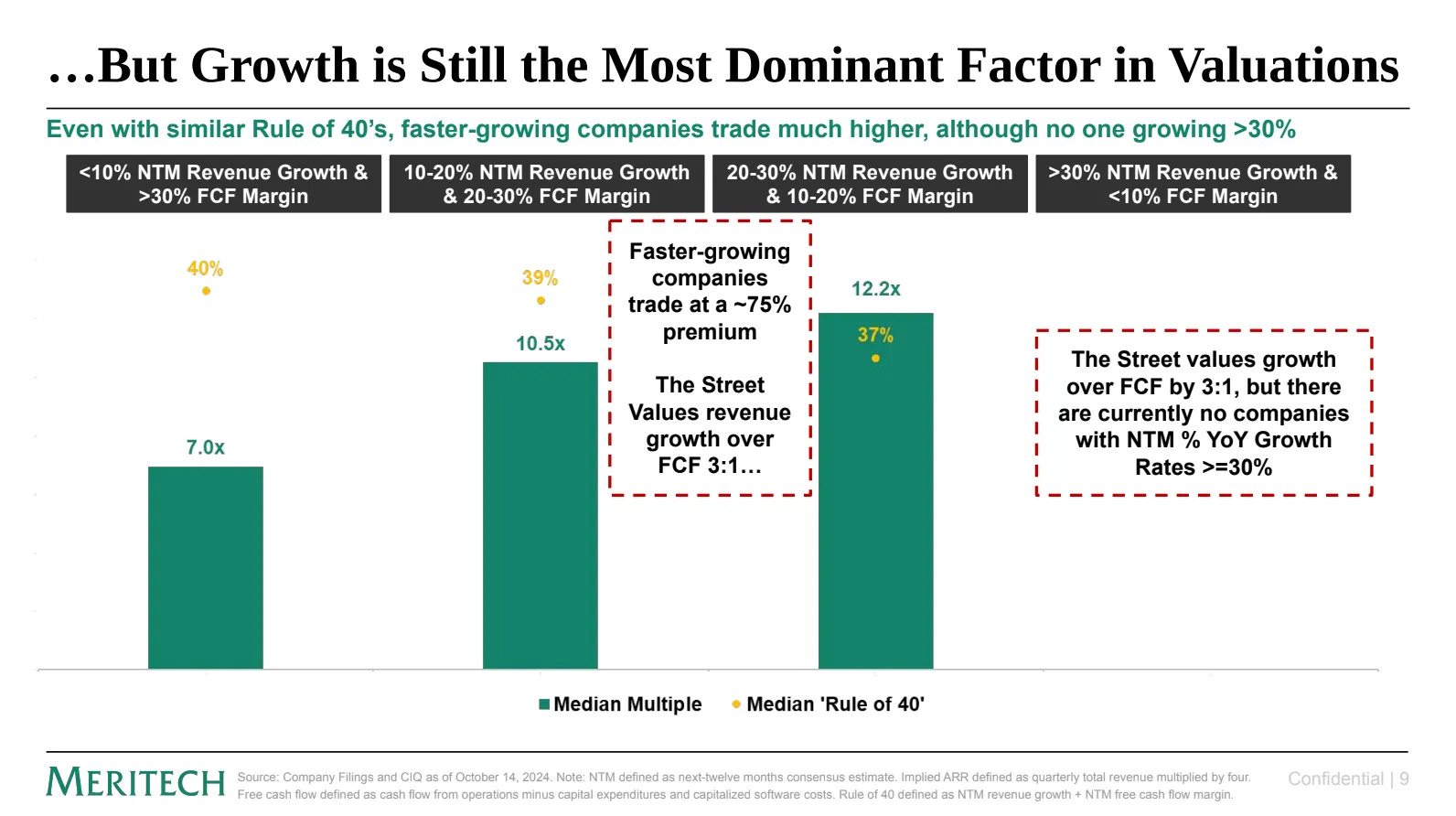

Growth is still the most dominant factor in valuation for public SaaS companies. Wall Street values growth over FCF by 3:1.

“SaaS market leaders are larger and more valuable than ever before with little to no AI revenue (yet) while the overall index has struggled. AI could make them bigger.”

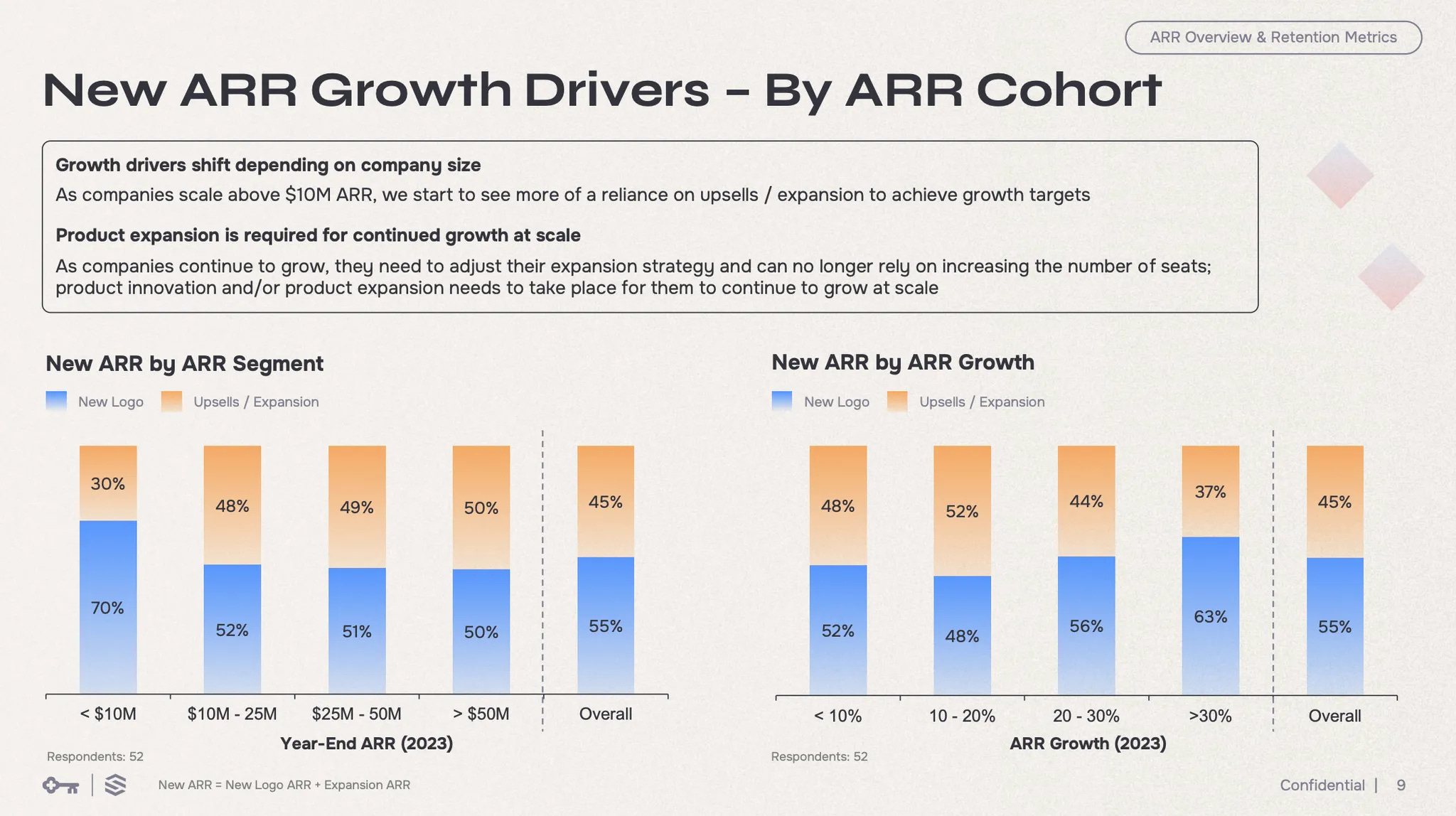

Tuesday, Oct. 22nd: KeyBanc and Sapphire published the 2024’s edition of their SaaS annual survey. - KeyBanc

“ARR growth is expected to slightly decelerate to ~19% in 2024 after companies already experienced growth deceleration in 2023 from ~22% to ~21%.

“Both gross retention and net retention have remained and are expected to remain relatively consistent at ~90% and ~101%, respectively.”

“Sales quotas have also increased from ~$675K in 2022 to ~$750K in 2023 and 2024, indicating that expectations have become greater for sales teams.”

Wednesday, Oct. 23th: Keith Rabois made a presentation on how to hire in startups. - Keith Rabois

“The most important and useful advice I ever got from a board member in 23 years of working in tech was, when I was at Square, Vinod Khosla said to me, the team you build is the company you build.”

“At PayPal we had this philosophy, where we didn't allow for general managers. We didn't hire a single person in the company whose skill was managing people. If you were going to lead a design team, you had to be the best designer. You're going to lead the engineering team, you had to be the best engineer.”

“The most important concept is you cannot hire the obvious people.”

“Peter Thiel told me that you can't hire anybody over 30. By time you're 30, everybody on the planet knows how to assess you pretty accurately because there's enough data points on your resume back then and as a startup you will not be able to outspend large tech companies that are very profitable or have infinite money.”

“The first day anybody starts, have them write down on a piece of paper the 5 or 10 most impressive people they know, and definitely do it on the first day and then go reach out to those 5 or 10 people.”

“We call gene pool engineering: find the places where the people have the skills you want the most currently work. And then go to LinkedIn and go surf all of the profiles of the people that work at those three companies, let's say, and send them an email from you as CEO.”

“I think the best reason to announce a financing is actually for recruiting. I don't believe that financing announcements typically generate customers. There are rare exceptions, but you shouldn't announce the financing because you think you're going to get customers. It does help bring talent to you. More importantly, it may help you close.”

“How do you assess people that don't have the classic experience? The most important lesson was it wasn't that I couldn't evaluate people because I picked all three really well. It was that I couldn't evaluate strangers.”

“I can definitely tell you the people who created the most value in the history of PayPal, are the weirdest people that worked at PayPal. Max Levchin earlier this yearjoked with me on stage that I was the most normal person that worked at PayPal. So think about that. I'm the most normal person of 300 people. So, he meant it as an insult. I took it as a compliment.”

“The other way to cheat is hire interns. I don't think you can do it too early. So I think you do need a critical density of people that have some experience in a job somewhere, but interns have more upside than anybody you're going to hire. Because what happens to the best interns is they become founders. Some fraction of those founders become really famous, and then you're never going to hire them. But if you intercept them when they're 16 to 20 years old, they don't know that they're yet ready to found a company and be the next Mark Zuckerberg. So you want to hire them as early as possible.”

“There's two reasons you hire. One is value creation. Then, there's value protection. So experience is not your friend, typically, when you're trying to create value. If I'm trying to create value, if this is the way I'm going to compete with the rest of the planet. I probably don't want anybody who has experience. Out of 254 people at PayPal, there were exactly two people who knew anything about financial services.”

“Should you hire someone who walks in the door and says, I want to found a company in two years? My answer is yes. The way I look at it is, first of all, these people have more potential. And then secondly, my job is to make sure the company is so interesting, so valuable and such a challenge for any of the employees that they don't want to leave.”

“I'm trying to do is figure out what someone's strengths and weaknesses are. What I like to do is basically try to match what this person is motivated by and what they're talented at to the problem I have. Is this person I’m about to pull the trigger on or could pull the trigger on, do you have an unfair advantage in solving this specific problem? So what I'm trying to figure out is does the person have a super power or strength that might make it more probable than not that they can solve the problem I'm suffering through.”

“It's kind of arrogant of me to assume that you wake up and have some interest in Stripe. It's my job to convey why Stripe is the most compelling thing that you could do with your life.”

“Almost no one maps the importance of recruiting as 1st priority for founders to their time allocation. It doesn't have to be perfect mapping, but you want it to be as close as possible.”

Thursday, Oct. 24th: The Economist wrote a great paper on GLP-1’s potential ability to transform healthcare. - The Economist

GLP-1 drugs revolutionize multiple health areas. Originally developed for diabetes, GLP-1 receptor agonists are now approved or in trials for treating cardiovascular disease, obesity, sleep apnea, and even conditions like Alzheimer's, addiction, and inflammation-based diseases due to their broad cellular and brain impacts.

Beyond healthcare, GLP-1 drugs influence industries from food to aviation due to their potential to reduce obesity and calorie consumption; these effects may lower healthcare costs but also require public health systems to adjust to preventive uses and manage high drug costs long term.

“These drugs [GLP-1] seem to activate basic protective mechanisms in cells, such as reducing inflammation and clearing out junk, thereby keeping organs healthier. They also have powerful effects on the brain, through which they can both further influence the health of the rest of the body, and even affect behaviour.”

“At first glance, the wider effects seen from GLP-1 drugs might look like ancillary benefits from their effect on weight. That does happen, of course, but research shows that it is not the full story. A study of more than 17,600 overweight and obese patients from 41 countries who took semaglutide found that participants lost about 10% of their body weight and had a 20% reduction in serious adverse coronary events, strokes, heart attacks and all-cause mortality.”

“Cost looms large in any discussion about these drugs, as well as the need to take them for a lifetime. Both concerns are likely to prove temporary. In years to come the growing level of competition and the arrival of generic copies will lower prices and broaden access.”

“If the average United Airlines passenger were to lose 10lbs (4.5kg), it would save the airline $80m a year in fuel costs.”

Friday, Oct. 25th: Sierra raised a $175m funding round led by Greenoaks at a $4.5bn valuation. Iconiq and Thrive also participated. The company reached $20m in ARR less than a year after its public launch, implying a 225x EV/ARR multiple. Sierra leverages AI agents to automate customer service for enterprise customers, including WeightWatchers, Casper, Sonos and Sirius. It to outperform alternatives in reducing hallucinations and enables customers to personalise their responses based on their corporate brands. Sierra was cofounded by Bret Taylor former co-CEO at Salesforce and chairman of the board at OpenAI. - Reuters, Techcrunch

Saturday, Oct. 26th: Chemistry is a new US-based early stage fund that recently raised $350m for its first fund to invest in series A rounds in B2B companies focused on fintech, infrastructure, developer tools and future of work software. The firm was cofounded by experienced and successful partners from top VC firms, including Index, a16z and Bessemer. Ray Kurzweil (ex. Bessemer) invested in companies such as Launch Darkly, Intercom, PagerDuty and Twitch. Mark Goldberg (ex. Index) invested in companies including Persona, Pilot, Plaid and Bridge. Kristina Shen (ex. a16z) invested into ServiceTitan, Piva, Tennr, Wrapbook and Decagon. - Techcrunch, Chemistry, Forbes

““It’s incredibly rare for people to come together who are in the right stage of their career to do this,” Shen said. “It felt obvious.””

“Chemistry will look to make concentrated, hands-on bets with the fund, with each partner backing about two or three companies in each of the next three years.”

“Chemistry’s pitch: offer founders the experience and track records they’d expect from a bluechip VC firm, with the extra attention that can be difficult to consistently receive from a larger fund.”

““We were particularly impressed with the very thoughtful approach from having three different people with different DNAs, coming from different fund styles, that could work together,” she said. “That felt very powerful.””

“Many emerging managers or first-time funds start small, collaborating with bigger players before moving up to competitive lead checks. But Chemistry is sized to go head-to-head from the start.”

“The idea for Chemistry started with a question – what would a venture firm look like if its success was fully aligned with its founders’ success? For months, we workshopped the answer. It would bring together experienced GPs from top venture firms with complementary networks and investment styles. It would out-hustle the legacy firms that have grown distracted by scale. It would be led by a lean team that brings founder energy and clean slates to the office every day.”

“All three of us will actively support each investment. We are the portfolio services team, working in the trenches with our founders.”

Sunday, Oct. 27th: SilverLake and GIC are taking-private subscription management software Zuora for $1.7bn in an all-cash transaction expected to close in Q1-2025. Zuora generates $416m in ARR (implying a 4.25x EV/ARR multiple) growing 9% YoY with 11% FCF margins and 104% NDR. - Techcrunch, SaaStr

“The idea behind Zuora was a platform for orchestrating a businesses’ various billing systems, with an emphasis on subscription management. Over the past decade, Zuora has slowly expanded its offerings through mergers and acquisitions, purchasing subscription invoicing and billing startup Frontleaf, subscription experience platform Zephr, and revenue recognition software provider Leeyo.”

“It’s not ahuge multiple, and in that sense, it’s a reminder that growth matters more than profitability today. But it’s also great to see PE continue to believe that can re-ignite growth in SaaS and make 3x+ their money here.”

Monday, Oct. 28th: I read an old Earlybird blog post about their $1 million seed investment in UiPath’s 2015 seed round. - Earlybird

“We had our first meeting with Daniel Dines in July 2014 and were blown away with the technology vision, and Daniel’s passion for and immersion in his product.”

"We at Earlybird Digital East led the 2015 round with a $1m investment.”

“In the following two years, while UiPath focused on their product roadmap, we looked to help them secure a lead investor for their upcoming Series A round, which finally came together in April 2017.”

“Along the way, the company grew its ARR from $1m to $100m in 21 months, a pace never seen before in enterprise software.”

“For the first time, a company hailing from Romania was vying for global leadership in a major category, and executing a global growth strategy, with revenues spread out quite evenly around the world. A group of Eastern European engineers was beating its US- and UK-rooted, better-funded, competitors.”

“To provide some context, the stereotype of the Eastern European techie was that of a hacker. Teams lacked the polish and presentation skills that you’d expect to find in a team in Silicon Valley, London or Berlin.”

Tuesday, Oct. 29th: Max Levchin wrote on Affirm’s approach to building a meritocratic culture. Key principles include fostering high performance, encouraging disagreement, leading by example and running towards problems. - Max Levchin

“High performance culture is pretty easy to define: a culture of individuals doing productive work for the company in the most efficient way possible and helping others do the same, while generally having a good time.”

“Affirm is a meritocracy: your talent, skill, and willingness to put it all to work define you here. We solve multivariate optimization problems – a certain minimum intellectual capacity is required. Demand excellence from yourself and from your teammates, don’t settle. Work-life balance tends to take care of itself if you love your work.”

“Run towards a problem; don’t assume someone else will take care of it.”

“An occasional heroic act that helps Affirm win is a good thing, not a sign of poor planning. Constant heroic acts required for Affirm to survive is a sign of poor planning.”

“Time is the scarcest resource we have, be mindful of how you use yours, and your team’s.”

“Post-mortem everything: the successes, the failures, and the near-misses – and learn.”

“If you disagree, you must speak up, even escalate – especially before a decision is made.”

Wednsday, Oct. 30th: Euclid wrote about the future of vertical software. There is a shift from traditional SaaS to hybrid business models that capture broader value streams beyond tech spending (e.g. integrating transactional and industry specific revenue streams). - Euclid

“It has now become clear, however, that a seat-based subscription OpEx is not the universal path to technology adoption across industries. The next chapter of successful vertical software is seeing the incorporation of substantial business model innovations, taking into account the idiosyncrasies of each vertical to minimize friction of adoption.”

“In many traditional industries, tech spending has often plateaued between 2-5% of overall industry revenues. However, business model expansion has enabled new vertical startups to capture value from the 95% of non-tech spending, including sales & marketing, materials, freight, payment processing, labor, recruiting, training, insurance, banking, and many others.”

“Amidst this evolution of vertical software, we see two distinct species emerging:

Vertical Integration: the startup is the sole customer of the software, scaling revenue through tech-enabled services and/or roll-up strategies.

Synthetic Roll-Ups: a concept we introduced in our piece on AI Roll-Ups.”

"The Synthetic Roll-Up playbook is simple but powerful:

Identify an impactful constraint to revenue growth for your vertical and solve it.

Drive growth with an easy-to-adopt wedge and aggregate businesses.

Become the all-in-one solution for vertical, leveraging scale and first-party data to layer in more products and services over time, increase revenue per customer, and build a compounding moat.”

Thursday, Oct. 31st: Procore published its Q3-2024’s results. - Procore

It grew revenues by 19% YoY in the quarter reaching $1.2bn in ARR with 9% operating margin and 94% gross revenue retention rate. International revenues in the quarter grew 26% YoY.

It added 225 customers in the quarter reaching 16,975 customers including 2,261 with $100k+ ACVs.

“We are on track to expand operating margins by 900 basis points for the full year.”

“In Q3, we began communicating as well as implementing the go-to-market changes we previously announced. The two primary focus areas of our go-to-market evolution are: moving to a general manager model that’s going to localize our go-to-market motion and better serve the regions in which we operate and introducing new technical roles to support all buyer personas and realizing the full value of the Procore platform.”

“Our international teams have long been advocating for a local go-to-market approach to drive a more connected customer experience.”

“We are investing in our sales teams, part of which involves bringing on a couple of hundred net new go-to-market resources with the intent of hiring quickly to get them ramped and productive. We’re only about 1 quarter in, but we are pacing well. All general managers and their leadership teams are expected to be in place by the end of the year.”

“When we support our customers with a tailored approach and ample technical resources, it generates improvement in retention and expansion rates”

“With over 2 million construction professionals around the world collaborating on our platform, we have an unmatched corpus of construction data. This data allows us to provide customers with actionable insights that are not limited to one product or workflow but rather span projects and portfolios, giving our customers a comprehensive view of their projects and their businesses. We believe that because Procore is the only truly connected platform in the industry, we are the only solution that can fully harness the power of AI for our customers. You simply cannot maximize the benefit of these technologies if data is stuck in silos.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

je confirme ! :-)

Amazing newsletter as always, thanks for the gems!

A few topics particularly stood out to me:

1.Sierra: The level of execution is incredible. Reaching $20M ARR in less than a year is a masterclass. Bret Taylor proves once again that he knows how to play at the highest level and build visionary companies. And that 225x EV/ARR multiple? Absolutely impressive.

2.Chemistry: No surprise they raised $350M for their first fund. The track record of their past investments is a true Hall of Fame, and it’s exciting to see what their next moves will be.

3.UiPath: That ARR growth from $1M to $100M in 21 months never fails to blow my mind every time I hear it.

4.Roblox: The Hindenburg report also sent chills down my spine. Listening to the Gamecraft podcast, I had a much more optimistic view of this ecosystem—and the company itself.

5.Bridge: A fantastic exit for Stripe (once again, Index involved). Raising $58M and exiting at $1.1B shows that the exit-to-funding ratio can be stellar when the team executes well.

6.Recruitment: I loved the point on Index’s guide and Keith Rabois’ presentation.