📖 Venture Chronicles - October 2023

Overlooked #160

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of October.

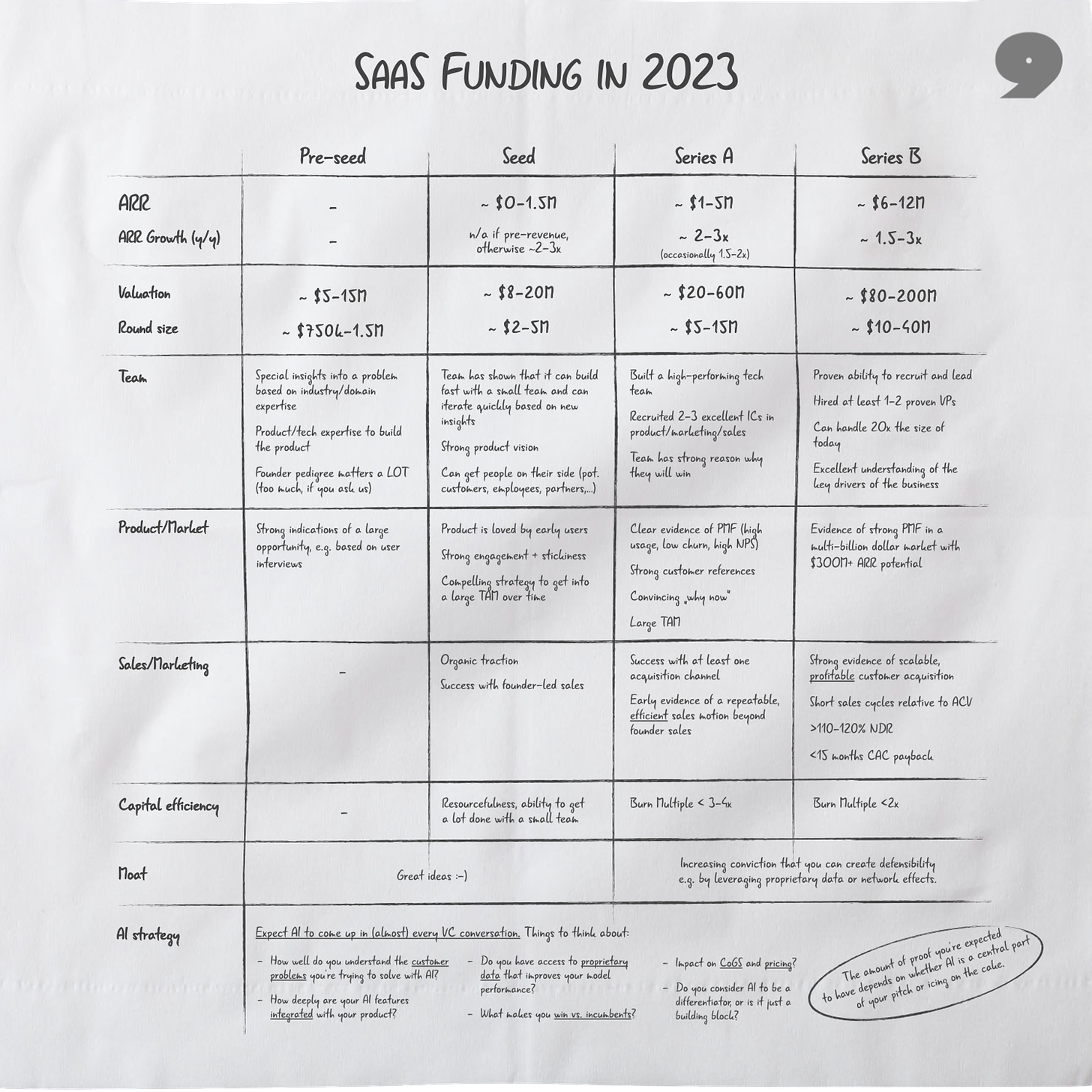

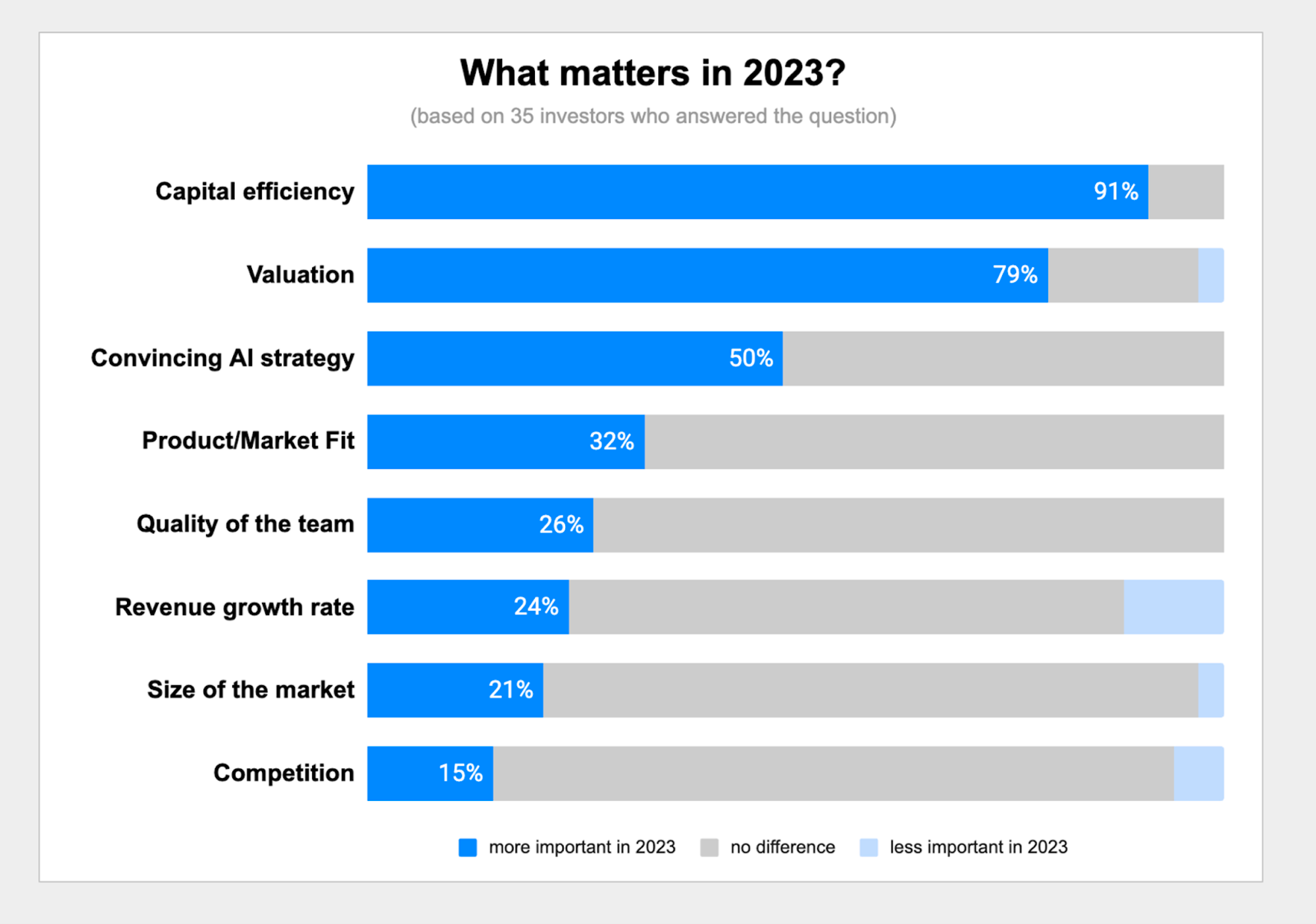

Sunday, Oct. 1st: Christoph Janz (GP at P9) published an updated version of his SaaS Funding Napkin. - SaaStr, Christoph Janz

“There seems to be a bifurcation in the market: significantly fewer startups raise an early-stage round, but those that do still do it on good terms.”

“If most Series A investors expect $2.5–3M or more in ARR (vs. the $1–2M from previous years), it has profound implications on how founders need to look at burn, runway, and their fundraising strategy.”

In the last 18 to 24 months, the amount of capital raised by startups has seen a 50-70% decrease. It is still on par with the levels observed in 2019. While this decline is substantial, it does not indicate a fundraising nuclear winter.

Compared to previous years, SaaS founders should place a strong emphasis on capital efficiency (e.g. on their burn multiple answering the question how much capital is required to add a dollar or ARR in your business) and have a clear strategy for integrating AI into their business operations. “Almost every investor cares much more about capital efficiency than before, and 50% of the respondents told us that a convincing AI strategy has become more important.”

Monday, Oct. 2nd: The Financial Times interviewed Niklas Zennström, who cofounded Skype before building a venture firm called Atomico. - FT

Atomico backed 130+ startups and has $5bn under management.

“I thought there was such potential in Europe for more companies like Skype to be created. Let’s break the [Silicon Valley] monopoly. We could build the same thing or even better in Europe.”

“He was raised by two idealistic leftwing teachers who met at art school. While he was young, his family moved to Uppsala, a beautiful university town some 40 miles north of Stockholm.”

“After failing to land a job at consultants McKinsey, he started working for the upstart telecoms company Tele2 in Copenhagen, which gave him a taste for taking on Europe’s “dinosaur” monopolies. But after a few years he was keen to break out on his own: “The whole dotcom thing was happening and I was like, ‘Shit, this is a lifetime opportunity. This is what I should do.’””

“Zennström and Friis hit on the idea for Skype while travelling around Europe and discovering that mobile phone calls were crazily expensive.” “In the first few weeks, Skype’s internet telephony service went “exponential” and 2 years later it had 52m users and estimated revenues of $60m.” “Such was the rate of growth that big US corporations started muscling in on the market, leaving Skype with some stiff strategic questions.” “The Skype team concluded that they needed the protection of a bigger partner and sold the company to eBay for $2.6bn in 2005. Zennström made even more money a few years later by participating in an investment consortium that bought Skype back from eBay and flipped it to Microsoft for $8.5bn in 2011, making him a billionaire.”

“What most excites him is the number of second- and third-time founders who have emerged. They have often learnt from the failures of earlier ventures and are now more experienced in building stronger businesses.”

“Former employees of Skype have founded 910 companies including 15 unicorns, or start-ups valued at more than $1bn.”

“Europe boasts more software engineers than the US, has 4 of the world’s top 10 universities and is the best place to launch a start-up focused on tackling big societal challenges, such as climate change.”

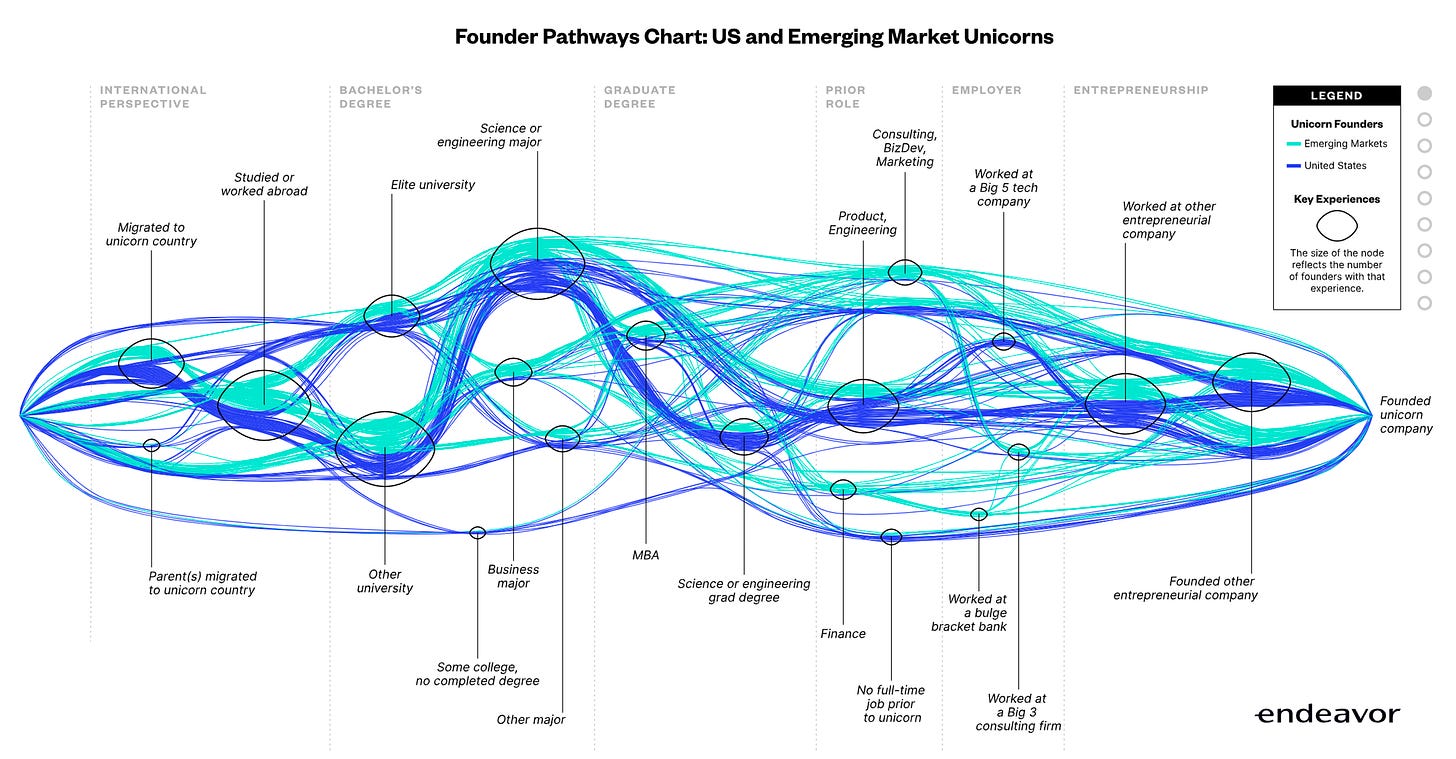

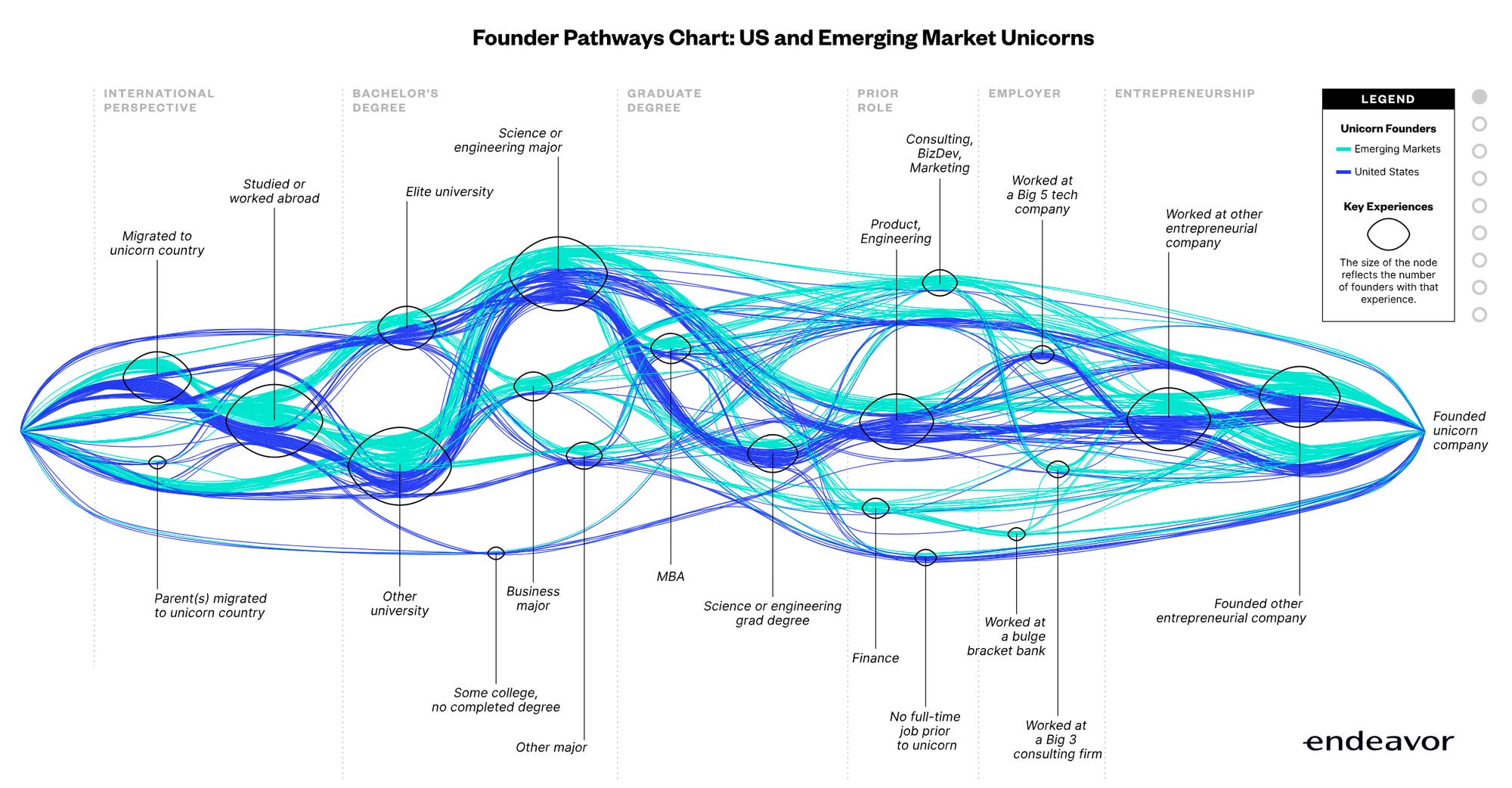

Tuesday, Oct. 3rd: Endeavor studied the career path of 200 unicorn founders (100 in the US and 100 in emerging markets). - Endeavor

Unicorn founders are global citizens. 55% of top US unicorn founders are immigrants or second generation immigrants. 60% of unicorn founders worked or studied abroad.

Only 1/3 of unicorn founders graduated from an elite university. Only 20% of unicorn founders worked for an “elite employer” (GAFAM, bulge bracket investment banks, top three consulting firms).

49% of unicorn founders previously built a company. 50% of unicorn founders also previously worked at a startup.

The average unicorn founder has 10y of work experience.

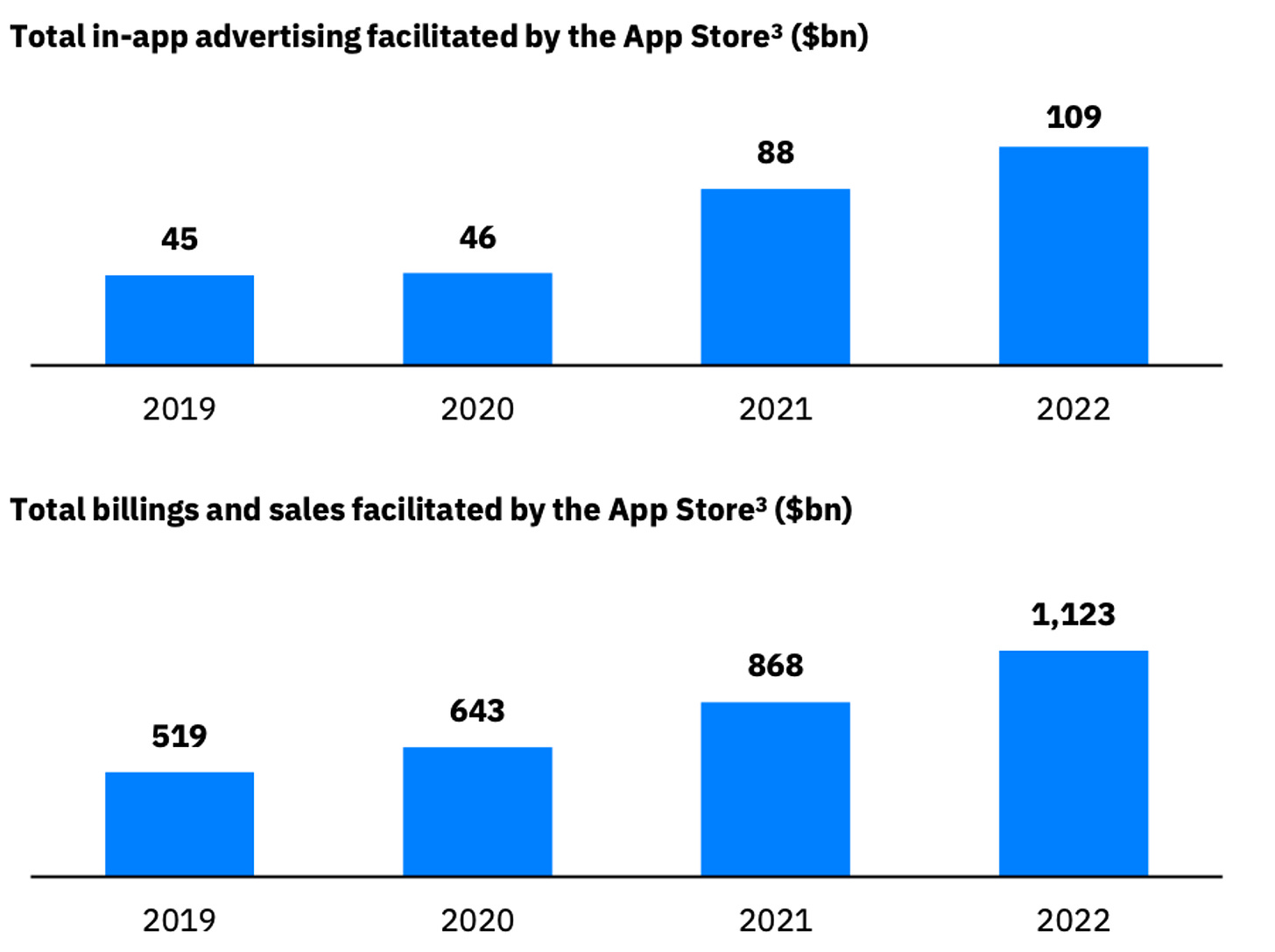

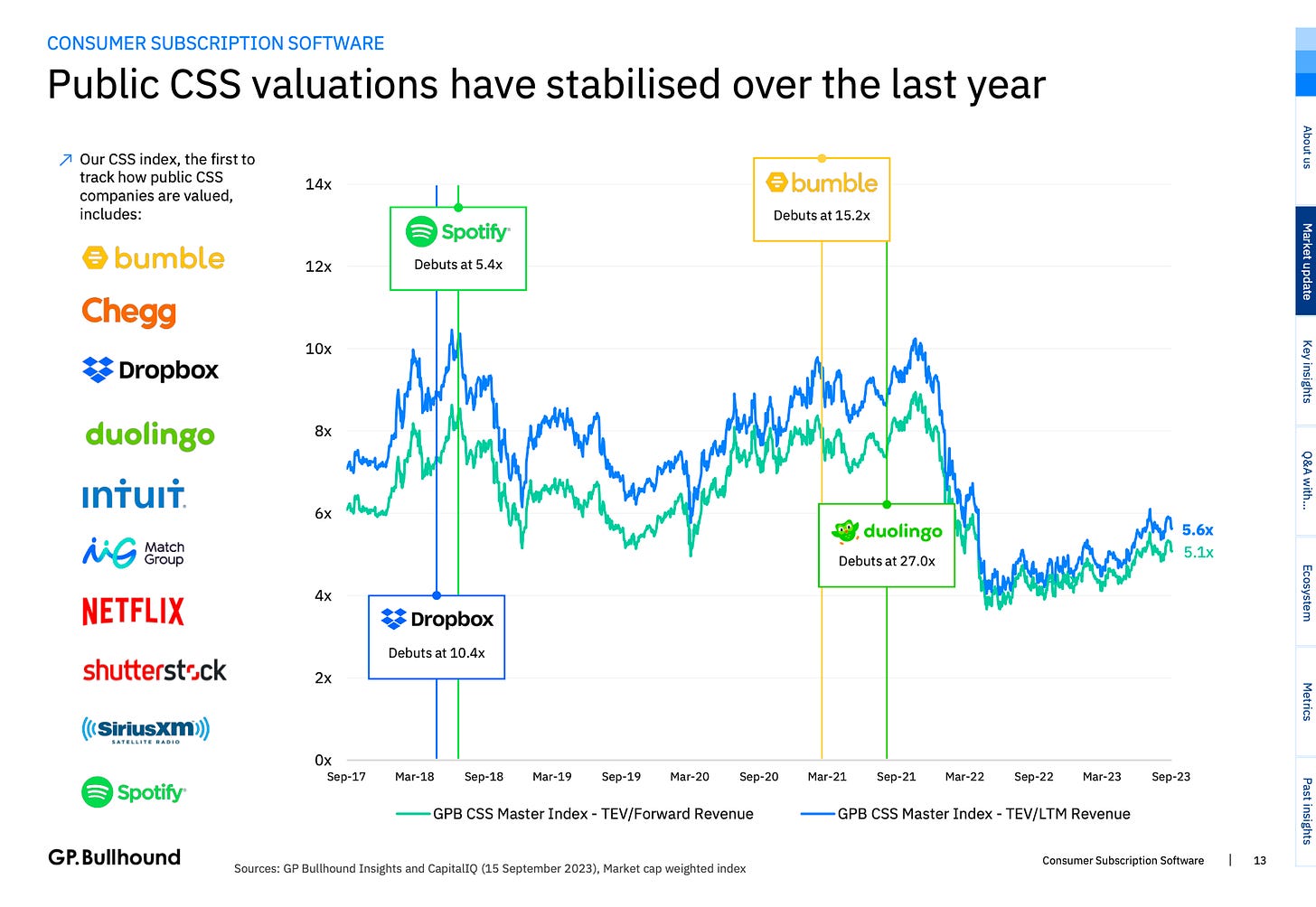

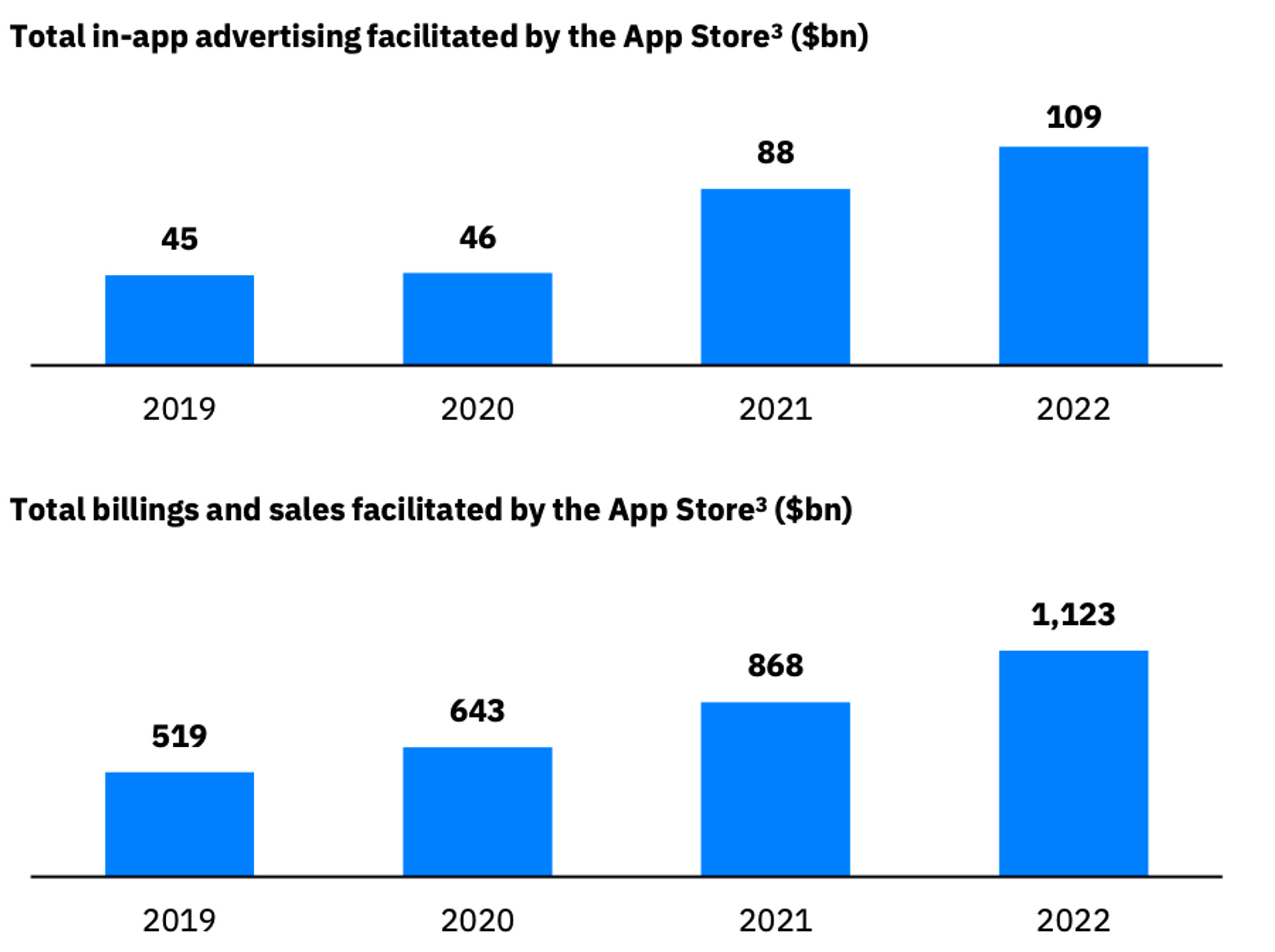

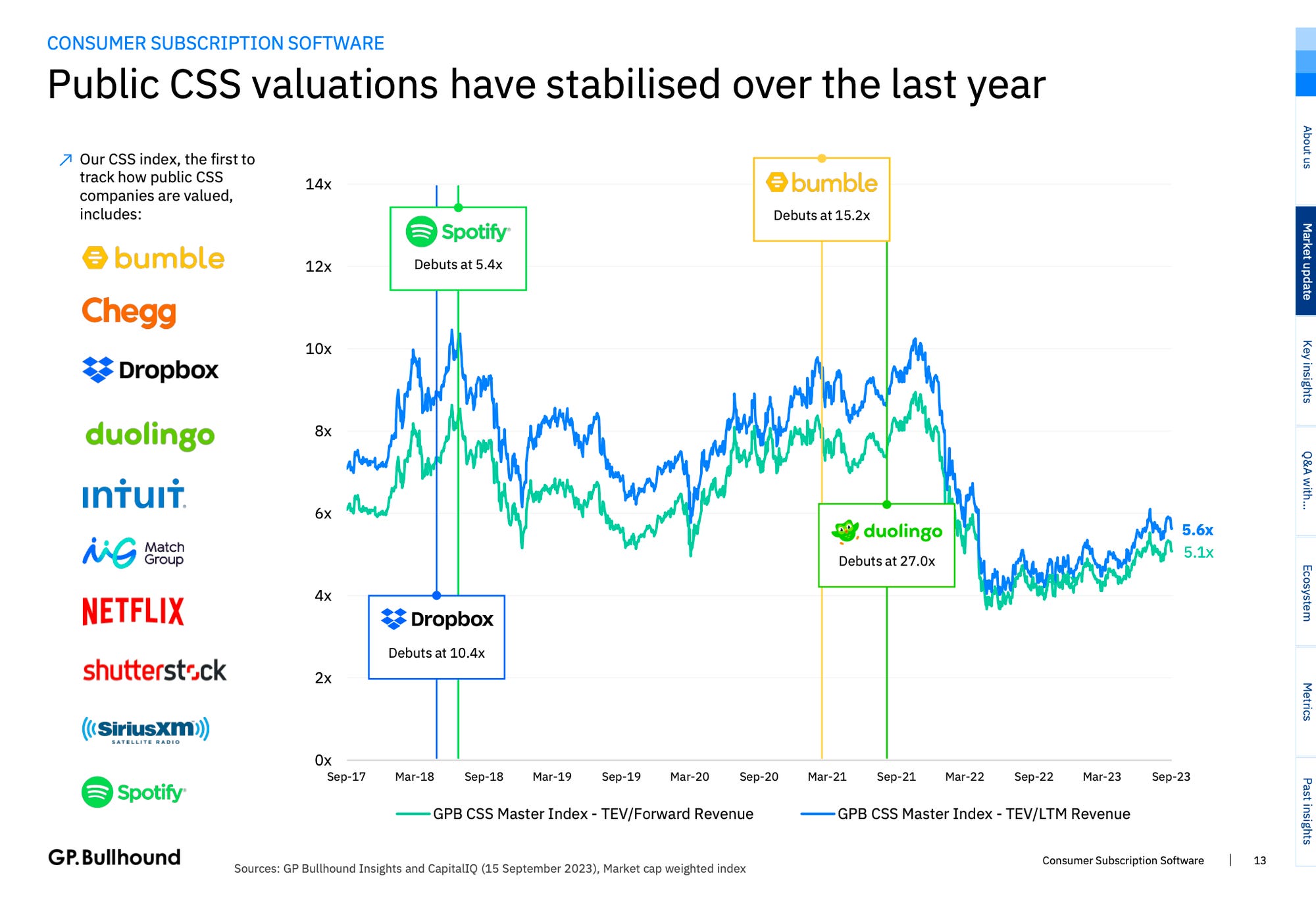

Wednesday, Oct. 4th: GP Bullhound published a new report on consumer subscription software (CSS). - GP Bullhound

Consumers spent $87bn on app stores in 2022. On average, we have 40 apps installed on our phones. Apple’s services revenues are expected to reach $95bn in 2023 (vs. $46bn in 2019). Publicly listed CSS are trading at 5.1x EV/ARR (vs. 8x on average in 2021). Several CSS companies could go public in the next 24 months including Discord, Strava and Chess.com.

Many CSS companies (e.g. Grammarly, Photoroom, Calm, Blinkist) are adding a B2B offering to sustain their growth and to reduce their churn rate. “CSS companies can deliver a uniform web and mobile experience, providing an edge over B2B counterparts typically focused on one platform.”

Thursday, Oct. 5th: Anh-Tho Chuong (CEO & cofounder at Lago) wrote a blogpost on how to win as an open-source company. - Lago

“What we’ve learned is that open-source tools can’t rely on being an open-source alternative to an already successful business. It’s not enough to succeed.”

“A great case for an open-source solution is when a transparency problem is present. What is a transparency problem? It’s when a solution being closed source creates distrust between the client and vendor.”

“One of the big benefits of open source is that it opens the development of niche features to the community. While the core product is typically maintained by a central engineering team, integrations or plugins are often built by community developers and then occasionally merged into the main branch. Conversely, closed-source solutions struggle with this because they rely on their engineering team.”

“Open-source projects—not just commercial open source—have served as a critical driver for the improvement of products for decades. However, some software is going to remain closed source. It’s just the nature of first-mover advantage. But when transparency and extensibility are an issue, an open-source successor becomes a real threat.”

Friday, Oct. 6th: Atomico raised $1.1bn for both its early stage ($600m fund) and growth stage ($750m fund) investment strategies. It was initially aiming to raise $1.35bn. The firm has made investement in 130 companies including Klarna, Medwise, Hinge, DeepL and Lilium. - FT, Bloomberg

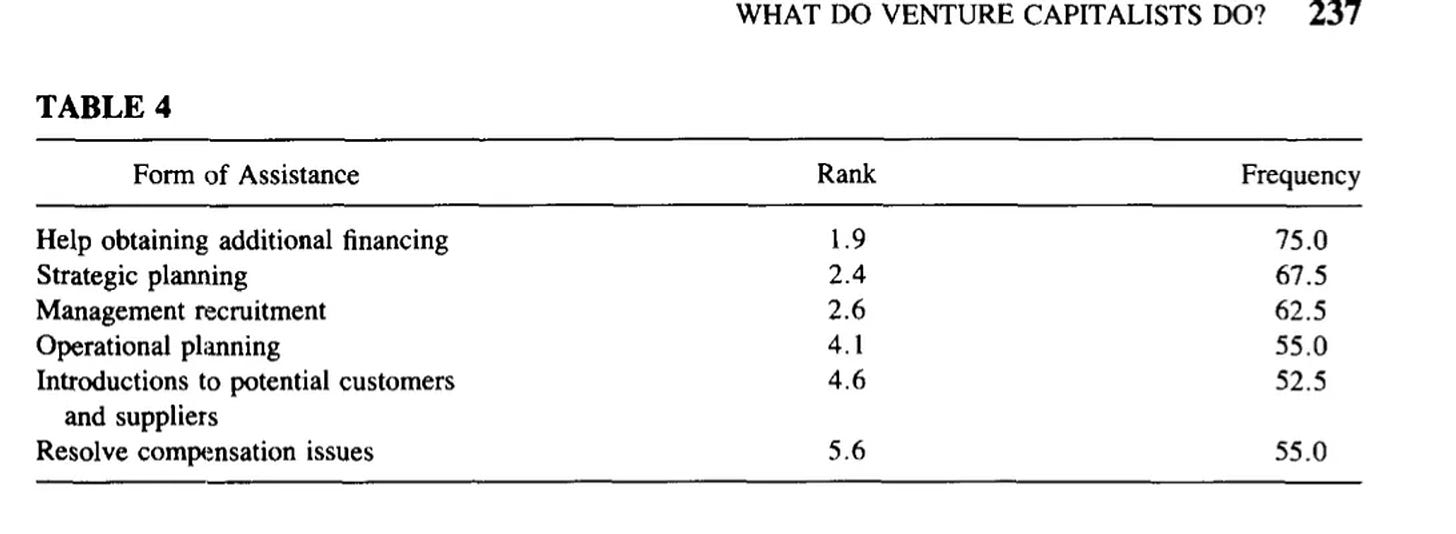

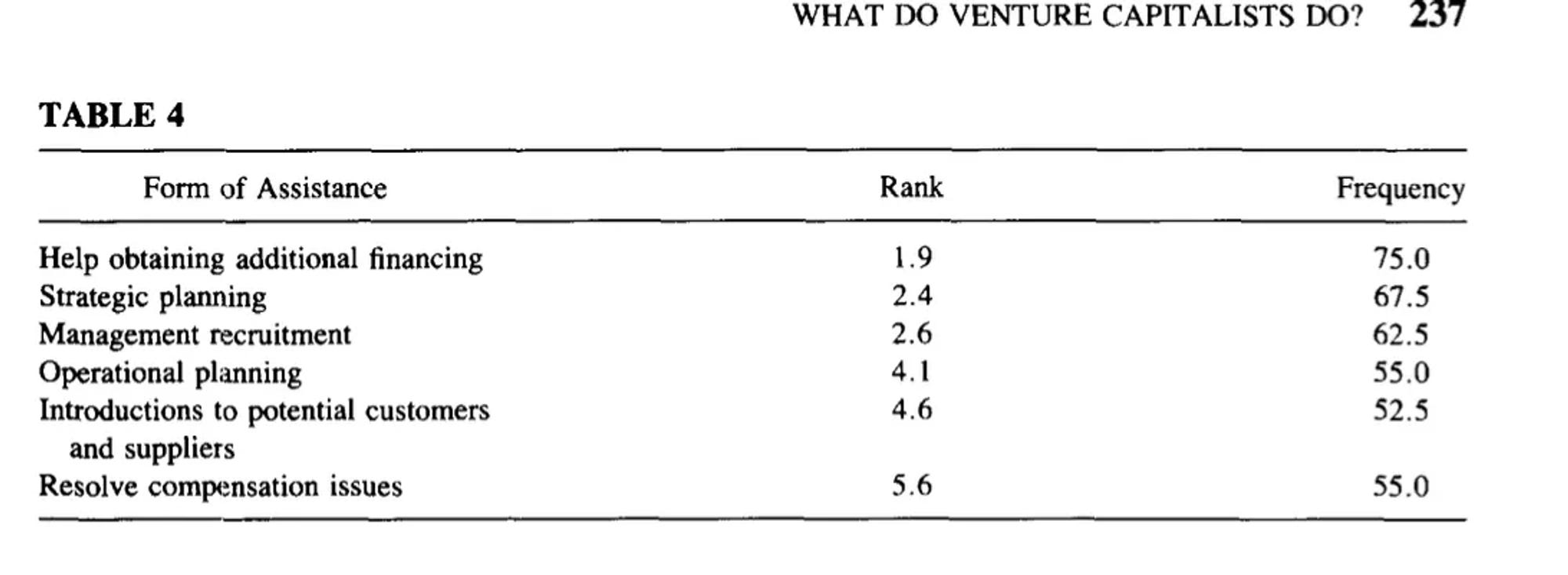

Saturday, Oct. 7th: I came across a post from The Generalist that discussed the daily routines of VCs, referencing a paper authored by Michael Gorman and William Sahlman in 1984. - The Generalist

VC partners typically oversee an average of 8.8 portfolio companies with board seats held in 5 of those companies. On a per-company basis, VCs devote around 80h per year working on-site with a company and an additional 30h on phone-related activities.

“Partners took a formal governance role in a large portion of the companies monitored, serving on an average of 5 boards [out of 8.8 companies monitored]. Some investors were considerably more hyperactive: one partner reported serving on 21 boards.”

“The majority of responding VCs reported spending more than 60% of their time per year either “assisting or monitoring” the companies they had backed.”

Sunday, Oct. 8th: I tuned in to a podcast episode from Colossus, which featured Copart, a B2B car marketplace that facilitates the end of life transition of vehicles between insurance companies needing to sell damaged cars and cars buyers worldwide. Copart manages the sale of c.3m cars annually with 2/3 of them being sold outside the original US state the vehicle is coming from and 36% of them being sold abroad. It generates $3.5bn in annual sales, it boasts a $40bn market capitalisation, it operates 250 locations and it has a 50% market share (30% market share for the 2nd player called Insurance Auto Auctions). - Colossus, Watchlist Investing

Copart collaborates with insurance companies, which constitute 80% of their supply, to inspect damaged vehicles and assess repair estimates to determine whether it's financially viable to repair the vehicles. If the repair costs exceed the vehicle's value, Copart takes charge of managing the sale of these vehicles.

“The supplier side is dominated by insurance companies, who supply 80% of Copart’s unit volume of vehicles. These are few, as the auto insurance industry in the US (CPRT’s largest market) include State Farm, GEICO, Progressive, and Allstate, together comprising half of the market. The remaining 20% or so come from banks, finance companies, charities, fleet operators, dealers, and individuals.” “On the buyer side sit literally hundreds of thousands of potential buyers that include vehicle dismantlers like LKQ, exporters, body shops, and individuals.”

Copart started as a specialised junkyard primarily focused on Chrysler parts. In a rapid transformation, the company invested in tech to digitise its operations including launching a bidding system and an inventory management solution.

Copart deries 20% of its revenues from a buyer fee ($150-200 fee per processed car) and the remaining 80% of its revenues from a seller fee (between 7% and 50% of the car’s value). On average, it takes Copart between 45 and 60 days to process a car through its system.

In the US, 12m cars are annually removed from operations because they were involved in an accident.

Copart is facing three main risks: (i) slowing growth (saturated market), (ii) failed international expansion and (iii) autonomous vehicles reducing the number of accidents.

Monday, Oct. 9th: Niek Tuerlings wrote on a mobile game genre called hybridcasual for Naavik. - Naavik

“Hybridcasual games introduce casual F2P audiences to RPG-esque progression mechanics; the best hybridcasual games are able to mature hypercasual players into full-fledged gamers.”

Niek highlights several tactics to make successful hybridcasual games: (i) high consistency between successful ads and core gameplay, (ii) arcade inspired core gameplay, (iii) focus on ads to IAP conversion, (iv) a deep yet accessible meta-game, (v) hiring casual games experts on staff.

“Hybridcasual games can be designed in three ways: (i) hybridizing a hypercasual game (Mob Control, Fight For America 3D, Dreamdale), (ii) hybridizing a casual game (Survivor.io, Collect ‘em All), (iii) starting out with a native hybrid approach (Pocket Champs).”

“When starting with a simple core game mechanic, the trickiest thing to do is adding substance to retain players mid- and long-term.”

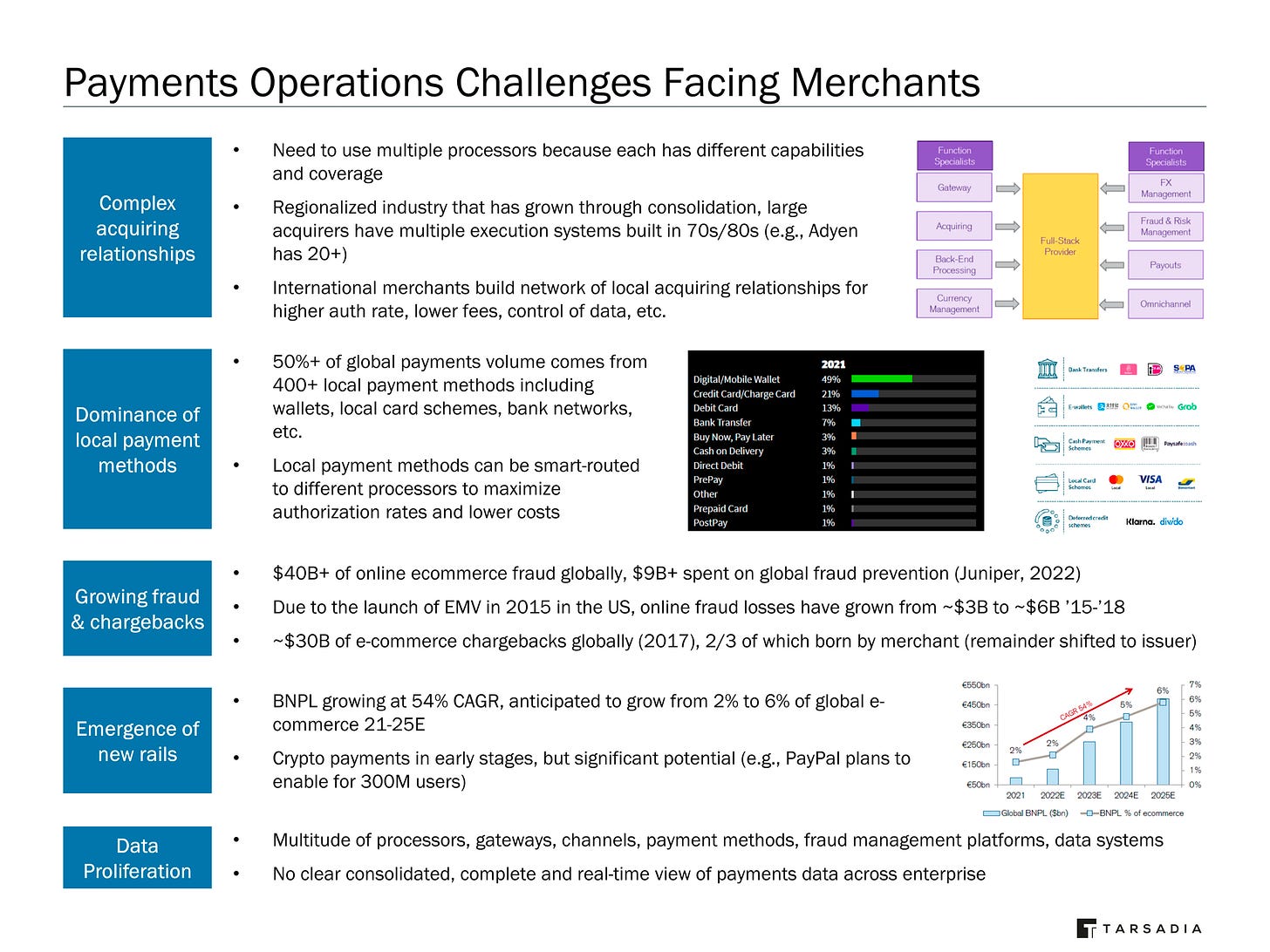

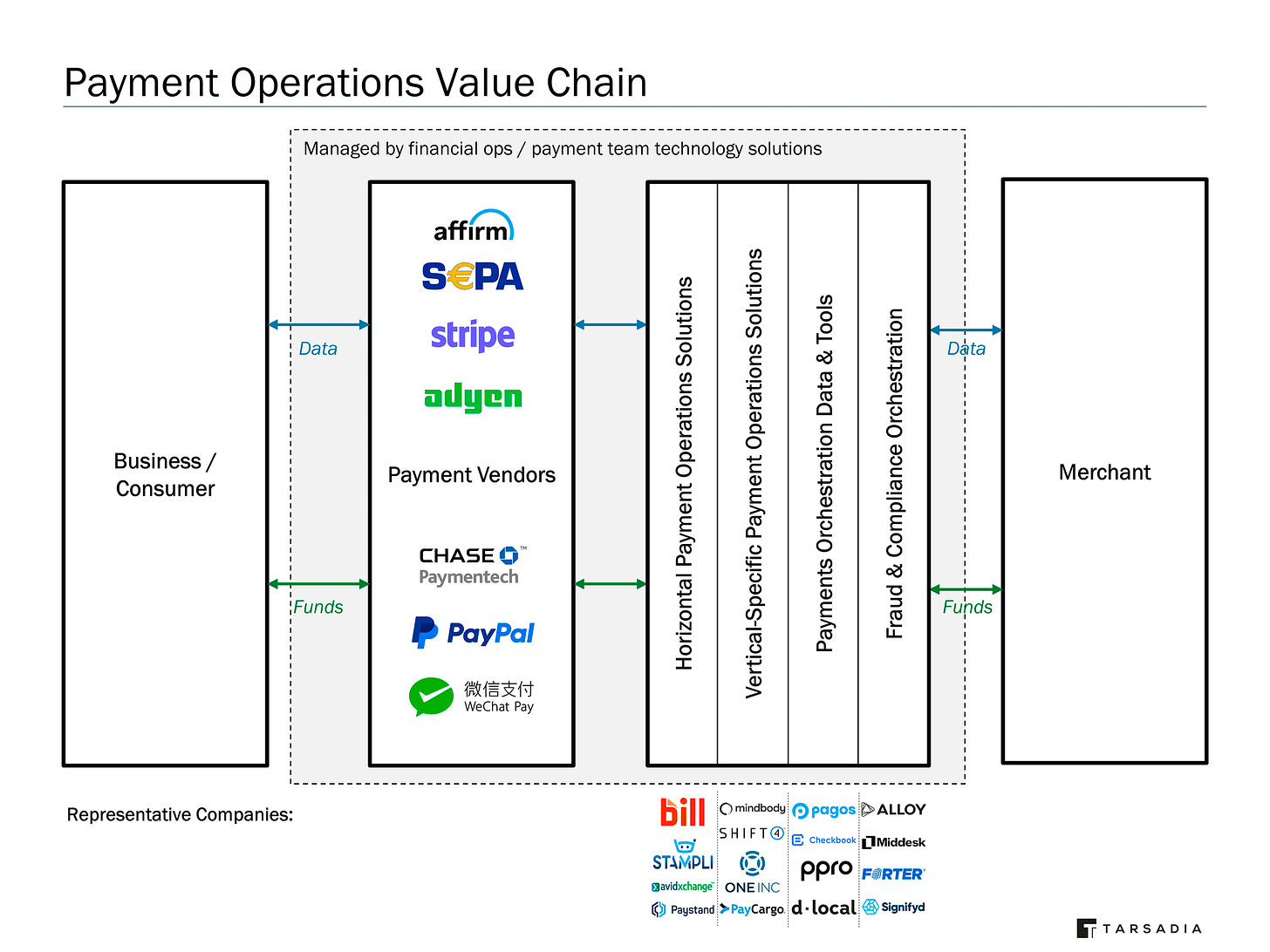

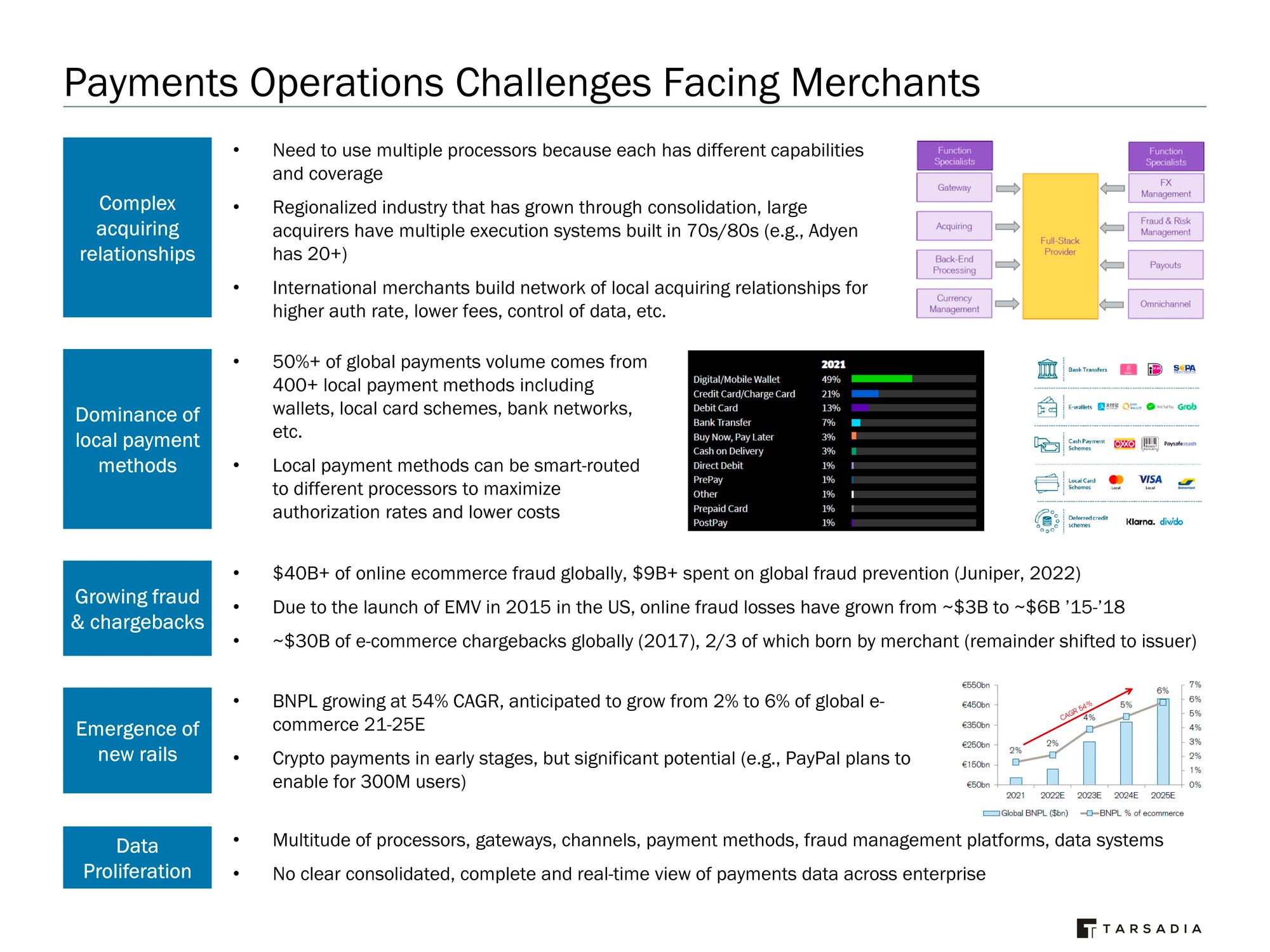

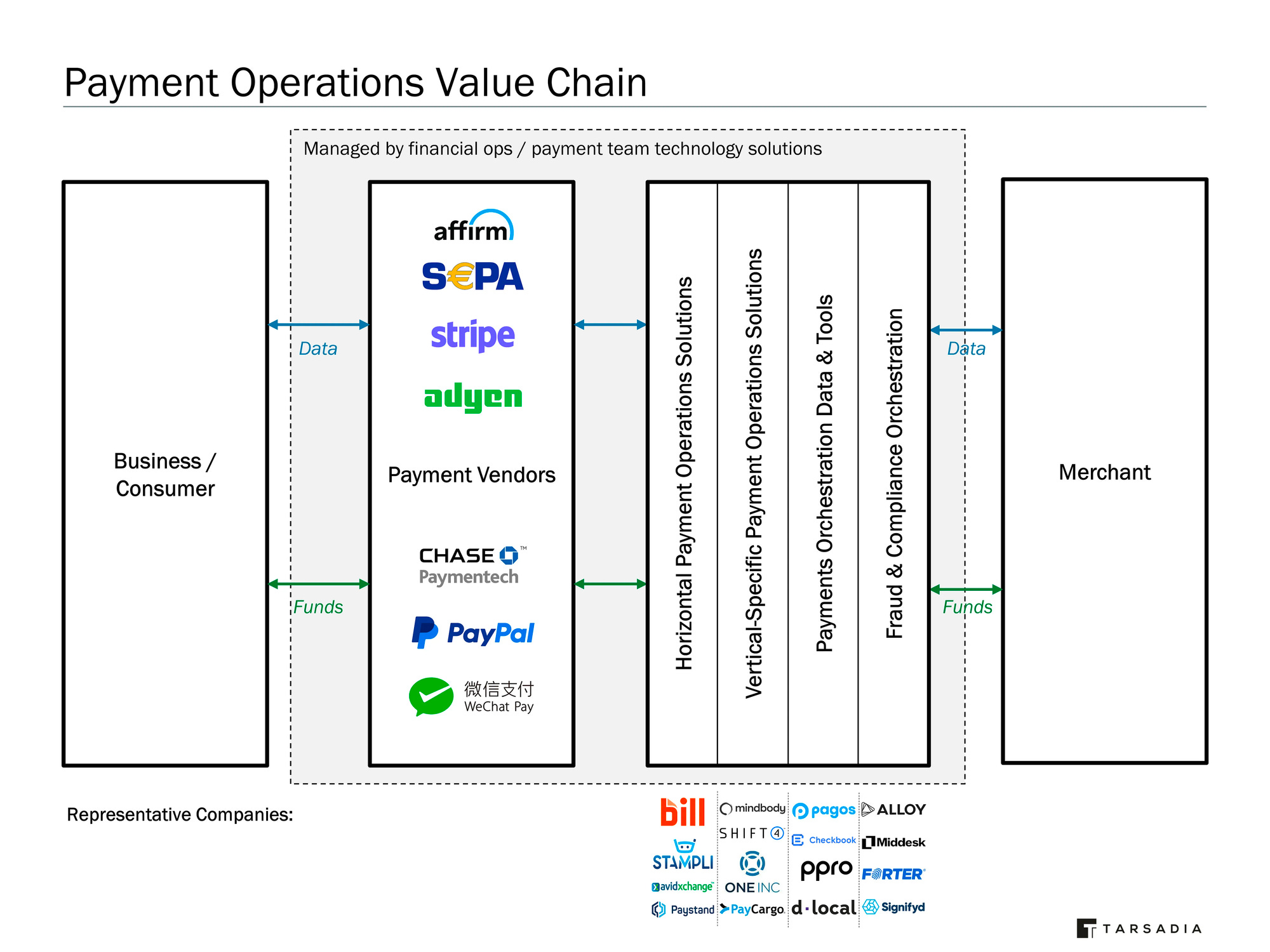

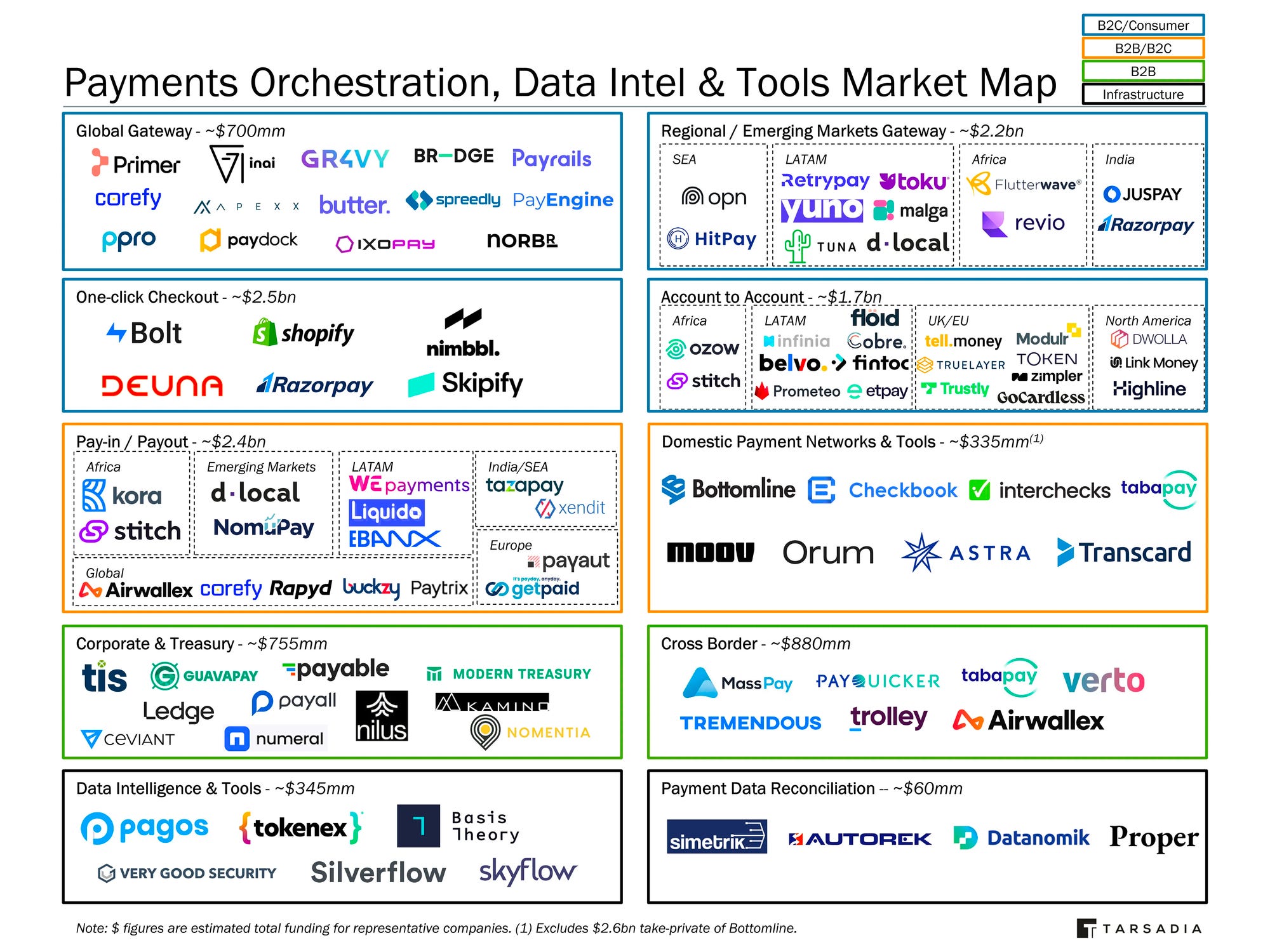

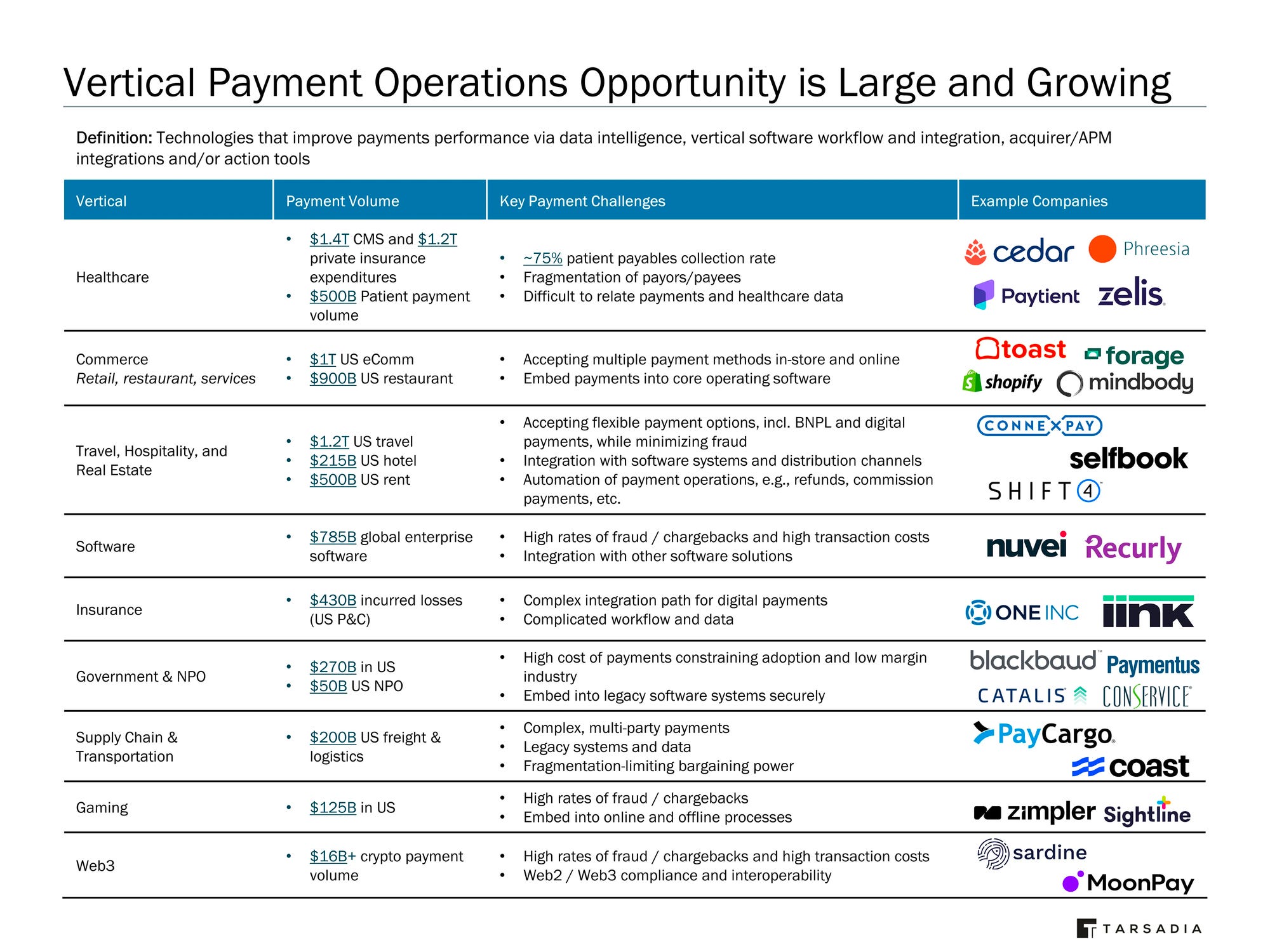

Tuesday, Oct. 10th: Darshan Patel wrote about payment operations software defined as an execution layer optimising payments performance by increasing conversion & reducing costs. He breaks down payment ops into 3 segments: (i) payment orchestration/data, (ii) fraud & compliance orchestration data, (iii) vertical specific solutions. - Tarsadia Investments

“We define payment operations technology below as the layer of software tools that sit in between the merchant and the payor, often embedding payments vendors within.”

“Unique workflow, data and/or integration needs often demand an industry-specific payment operations solution.”

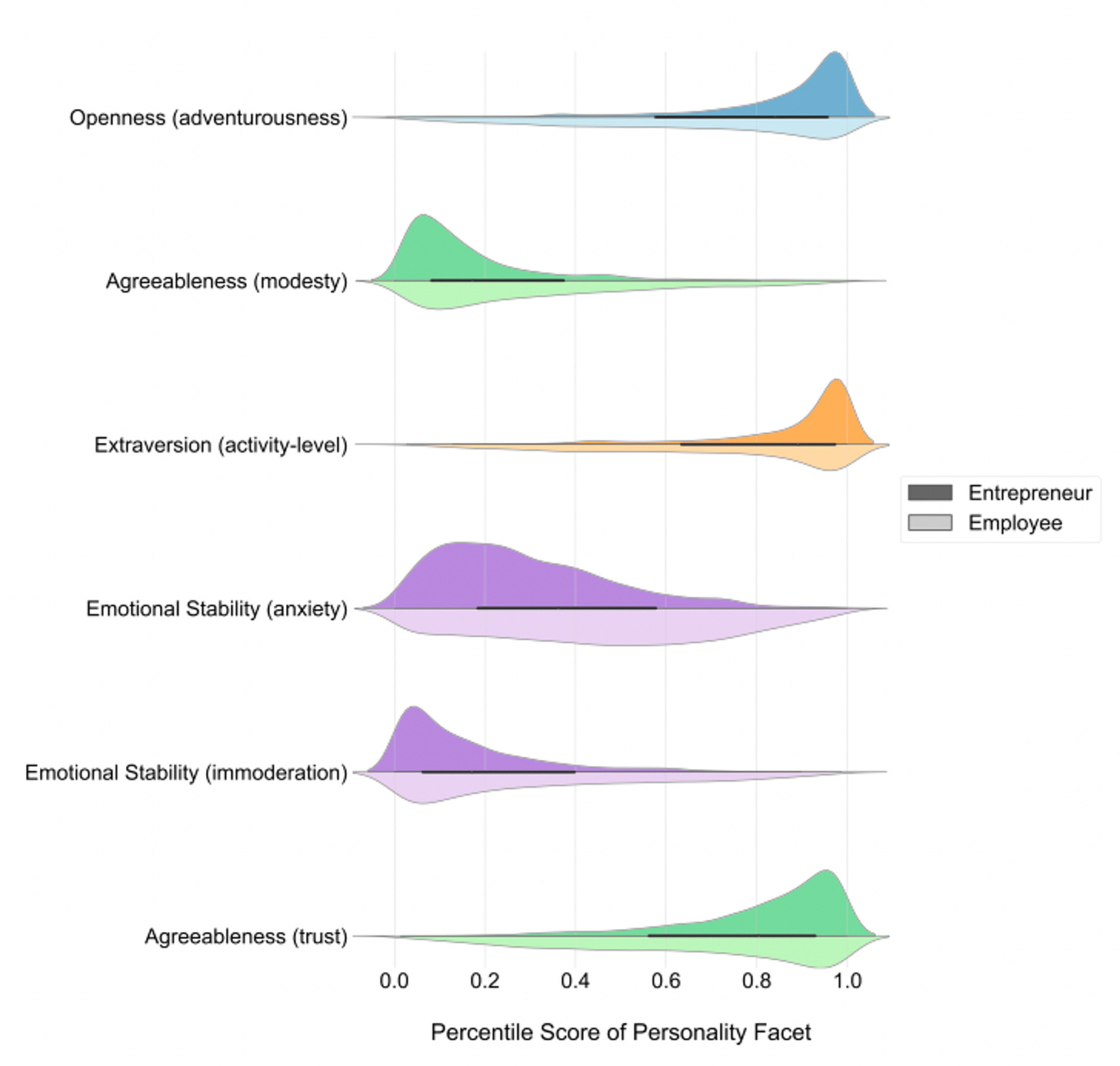

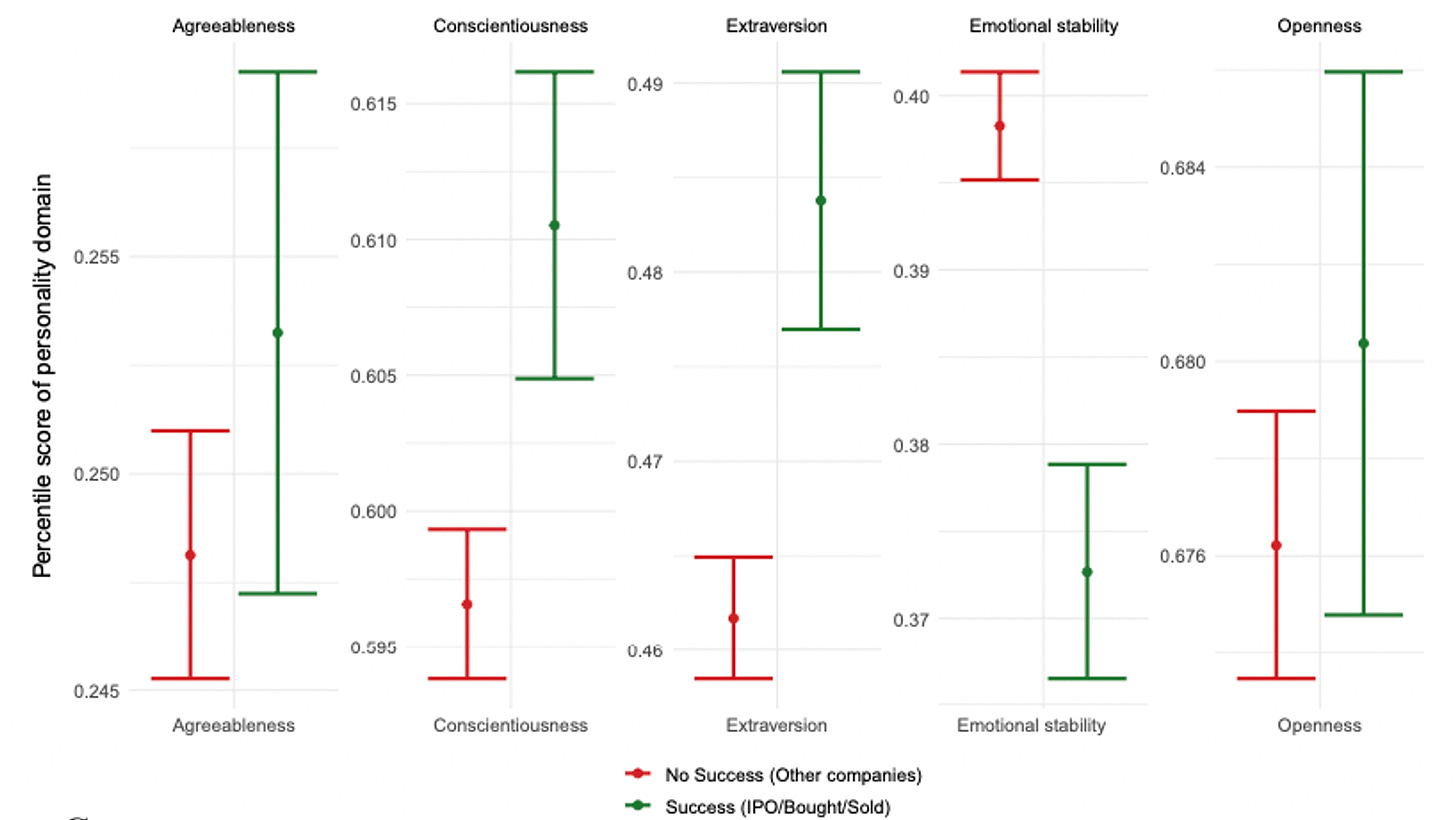

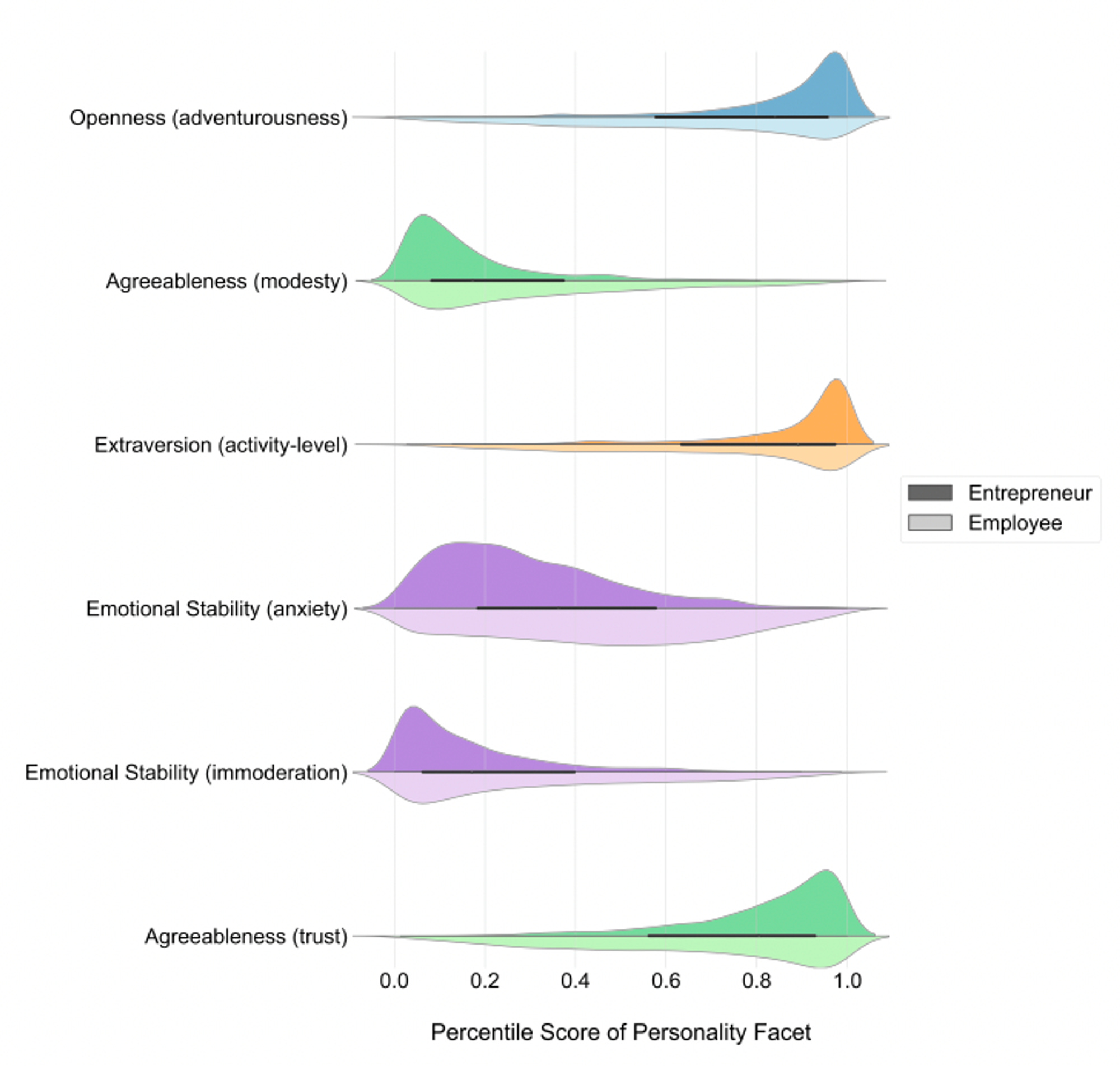

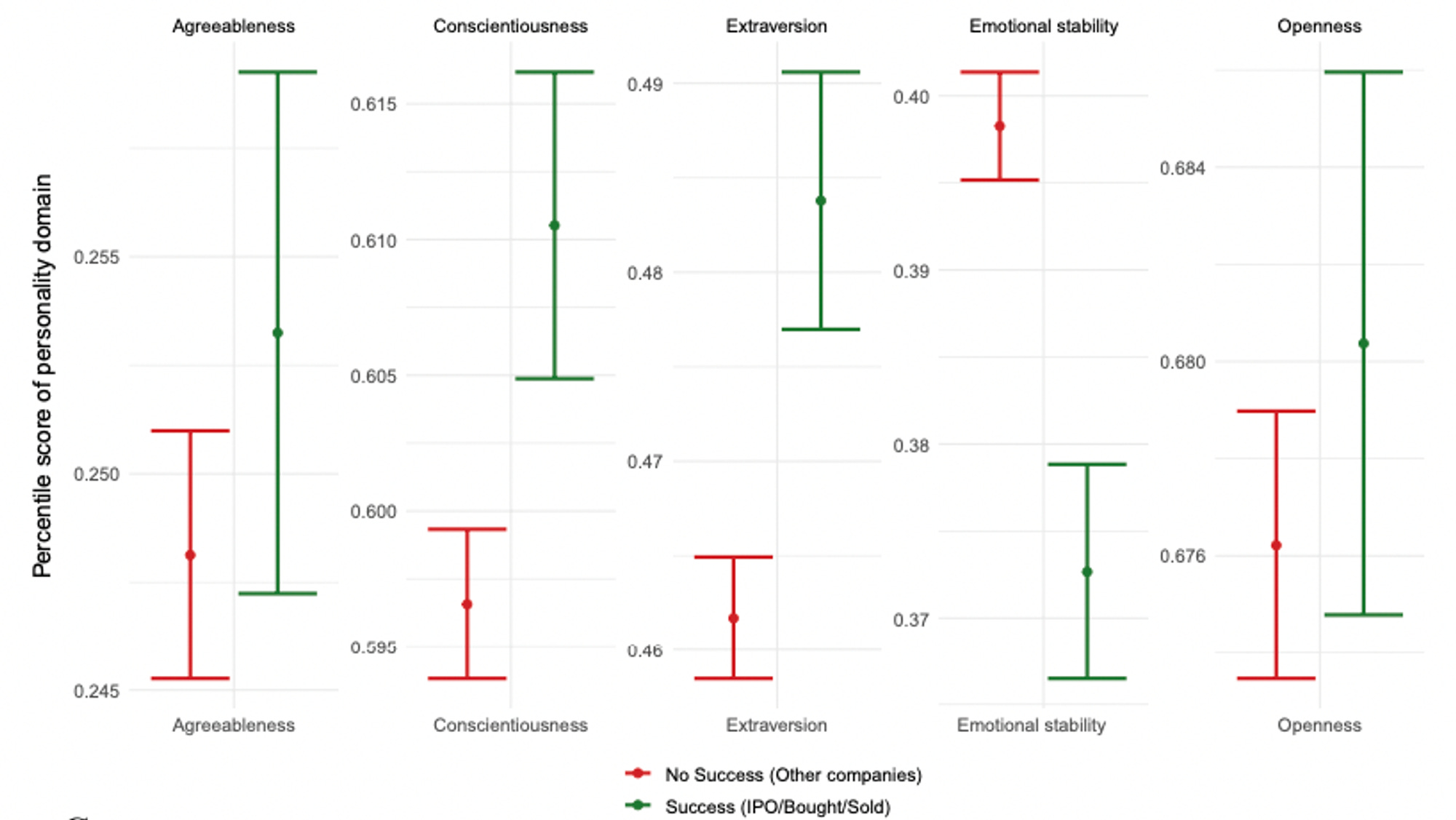

Wednesday, Oct. 11th: Nature published an intriguing research paper that analyzes the influence of founder personalities on startup success. - Nature

“We show that founder personality traits are a significant feature of a firm’s ultimate success.”

“Key personality facets that distinguish successful entrepreneurs include a preference for variety, novelty and starting new things (openness to adventure), like being the centre of attention (lower levels of modesty) and being exuberant (higher activity levels).”

“We have also shown that successful startup founders’ personality traits are significantly different from those of successful employee.”

It distinguishes several founder personalities including:

“Accomplishers: organised & outgoing. confident, down-to-earth, content, accommodating, mild-tempered & self-assured.

Leaders: adventurous, persistent, dispassionate, assertive, self-controlled, calm under pressure, philosophical, excitement-seeking & confident.

Fighters: spontaneous and impulsive, tough, sceptical, and uncompromising.”

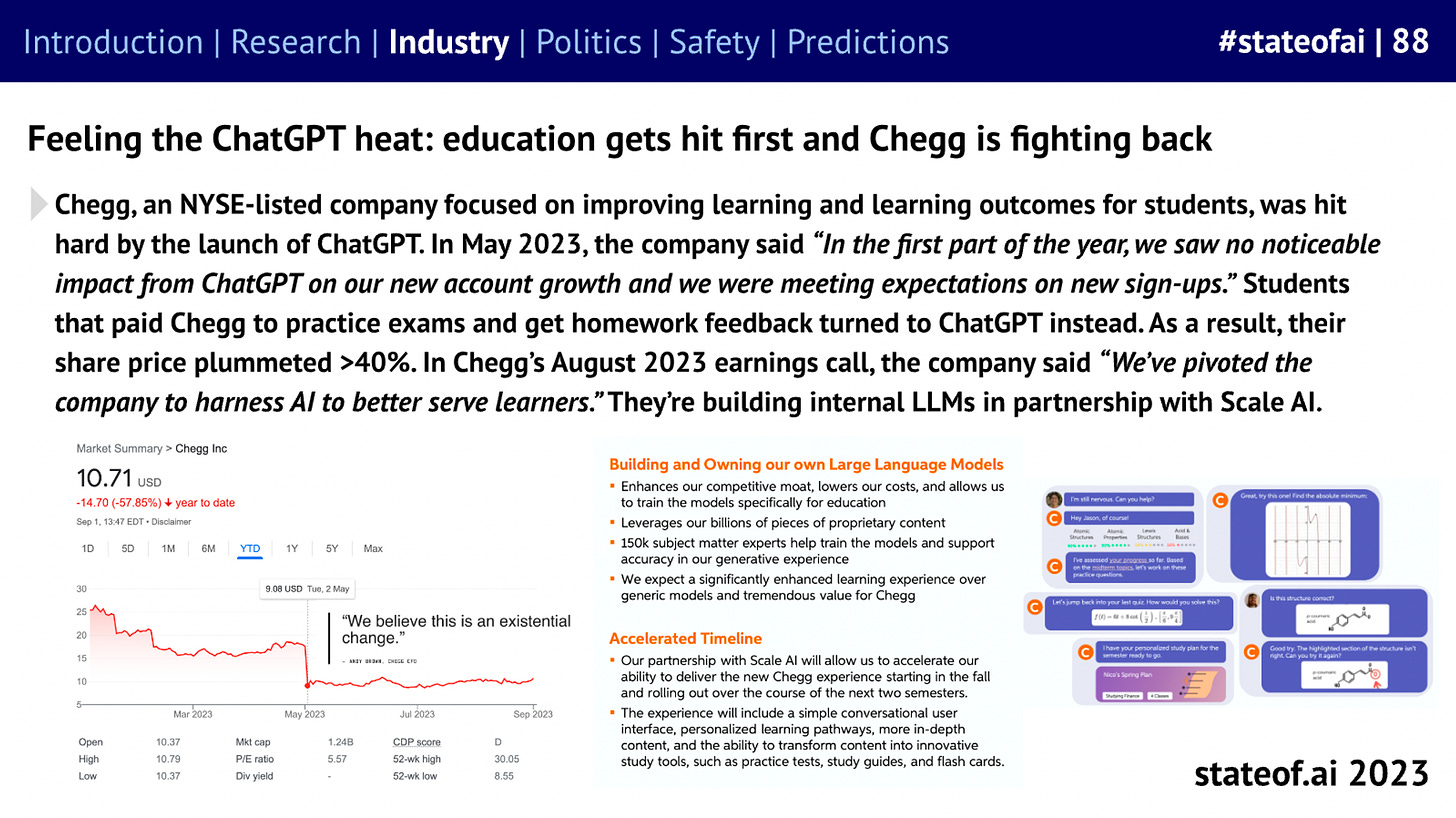

Thursday, Oct. 12th: Atlassian acquired Loom for $975m - $880m in cash and $95m in equity awards. Loom is an asynchronous video communication platform with 25m users, 200k customers and 7m monthly videos exchanged between its users. Loom was founded in 2016. It raised $200m+ in total including a $130m series C led by a16z at a $1.5bn valuation in May 2021. - Atlassian 1, Atlassian 2, Phil Haslett, Kleiner Perkins, Ed Sim, Vinay Hiremath

Atlassian is acquiring the company at a 35% discount compared to its latest private valuation. a16z will recoup its capital invested and earlier investors are making a great return on their investment (25x for seed investors, 12.5x for series A investors, 4.5x for series B investors).

Atlassian will deeply integrate asynchronous video into its collaboration products (Confluence and Jira). “By integrating Atlassian’s and Loom’s investments in AI, customers will be able to seamlessly transition between video, transcripts, summaries, documents, and the workflows derived from them.”

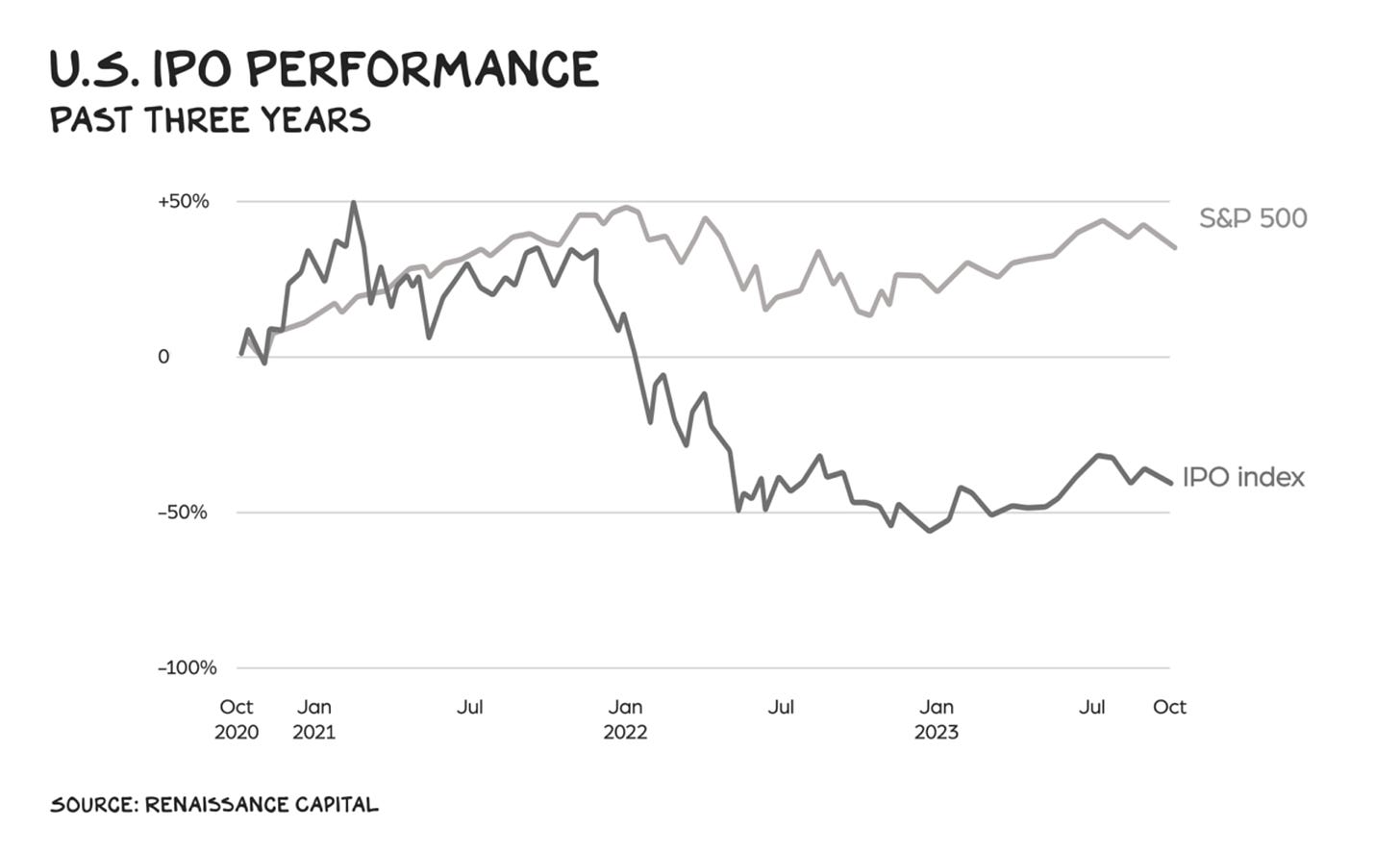

Friday, Oct. 13th: I read a post from Scott Galloway on the venture market. Thanks Naïm for the recommendation! - No Mercy/No Malice

“Of the 310 SPACs launched in the past three years, 10 have registered positive returns.”

“The traditional IPO construct is in structural decline, and that’s a symptom of a fundamental shift in the capital markets.”

“When capital piles in returns go down, and private market investors want to capture the upside previously leaked to public investors.”

“VC firms, who posted remarkable returns the first two decades of the millennium, needed a home with a backyard big enough to absorb billions in fresh capital. Tens of billions piled into pre-IPO growth firms. Never underestimate the market’s ability to create a product when consumers have cash in hand.”

“The problem isn’t that IPOs have become a pump and dump scheme (often they are). The problem is that they don’t matter. The center of gravity is shifting from public to private capital.”

“In 1980, 9 out of 10 tech IPOs were profitable. In 2021, it was 1 in 5. Among all venture-backed companies, in 1980, 78% were profitable; in 2021, 10%. Among the 13 VC-backed companies that went public in 2022, not one was profitable.”

“Historically, a company could be expected to grow long past its IPO, and the resulting share gains were available to anyone with a Schwab account and the foresight to buy in early. […] But if you don’t need the public markets for capital, why give up those gains to the unwashed masses?”

“Warren Buffett says the markets are a vehicle for transferring wealth from the impatient to the patient. The IPO markets are increasingly a(nother) mechanism for transferring wealth from young to old, poor to rich, and public to private.”

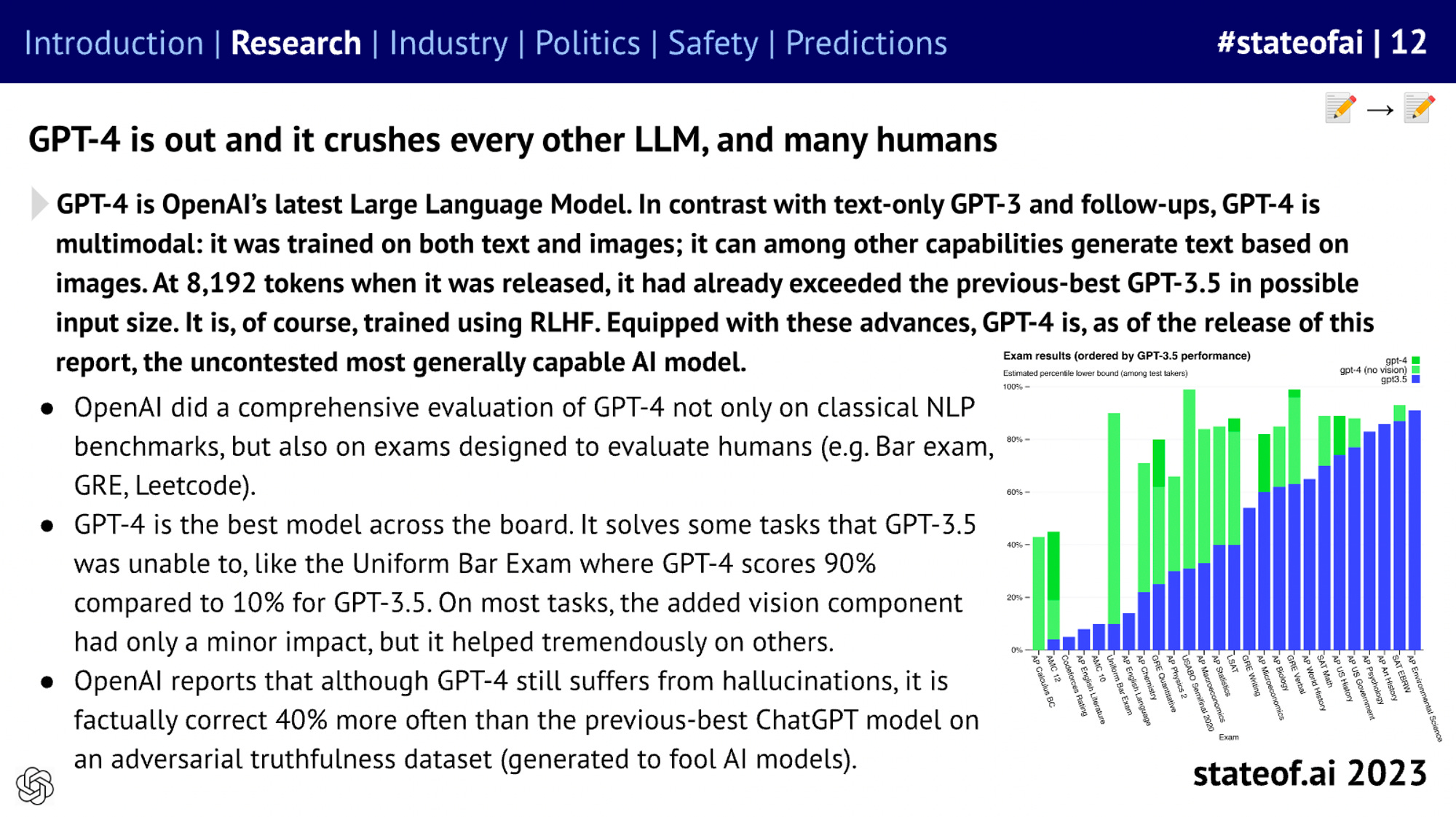

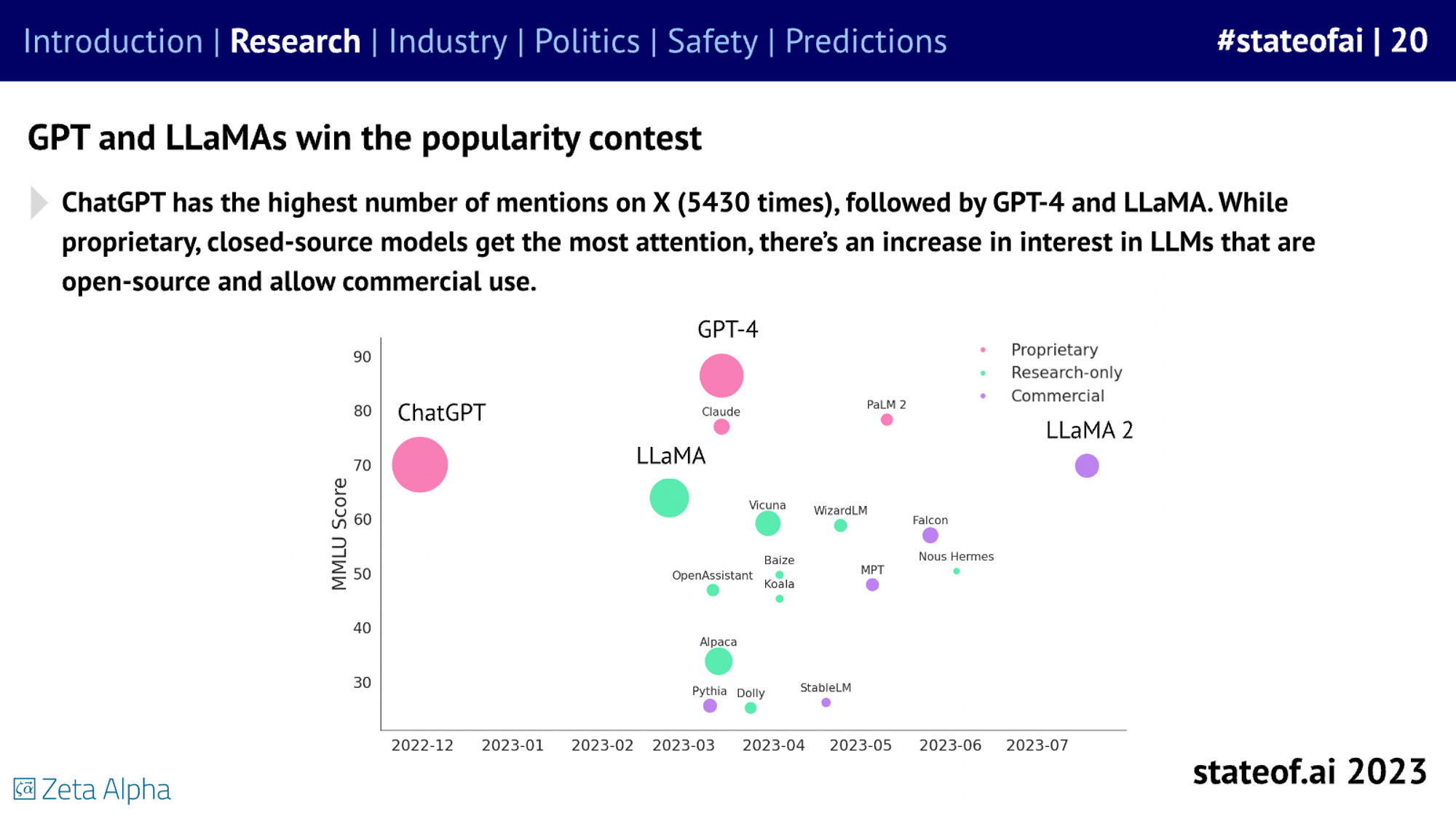

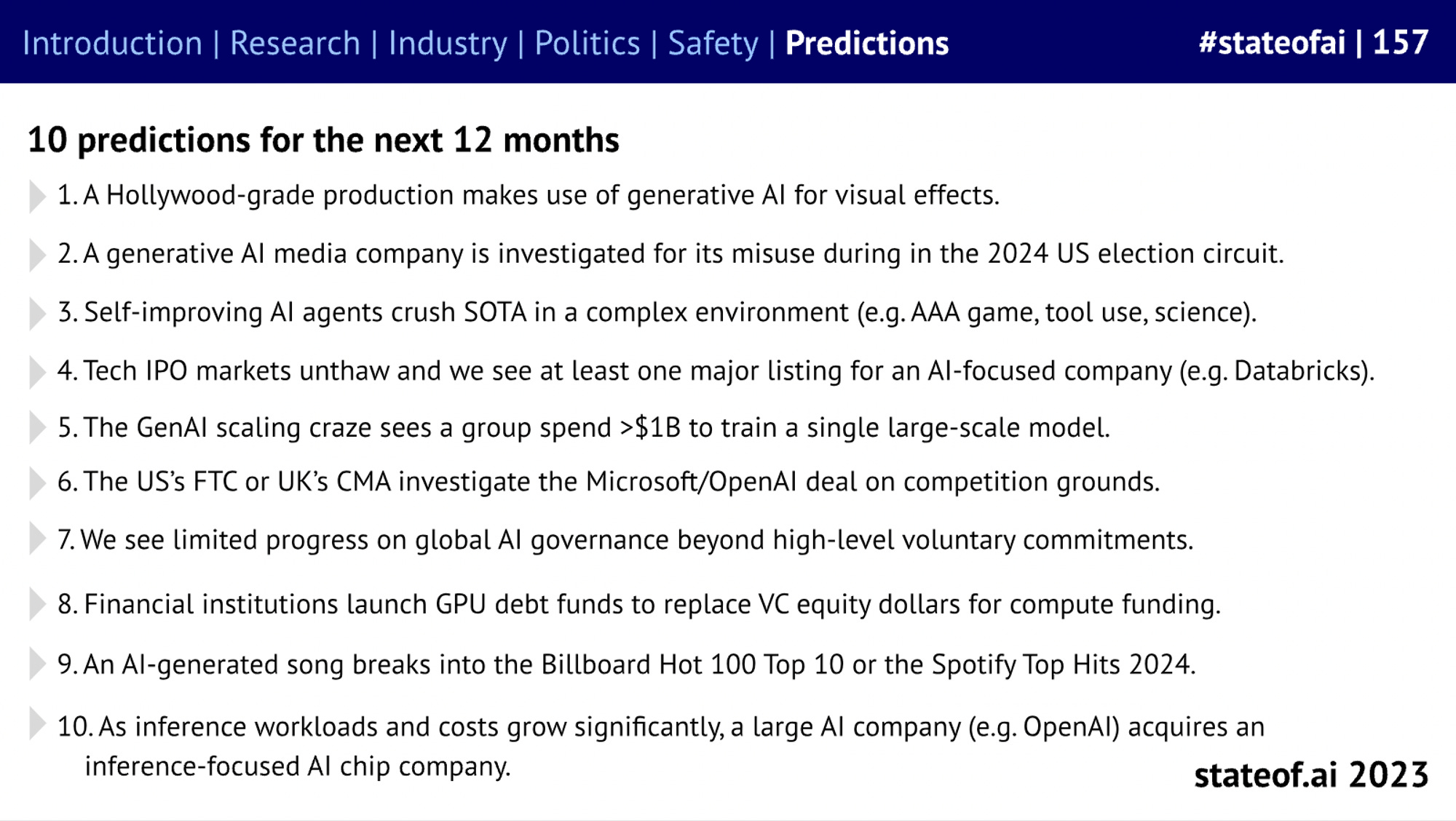

Saturday, Oct. 14th: Nathan Benaich published its 2023’s state of AI report. - State of AI

“GenAI saves the VC world, as amid a slump in tech valuations, AI startups focused on generative AI applications (including video, text, and coding), raised over $18 billion from VC and corporate investors.”

“Synthesia is now used by 44% of the Fortune 100 for learning and development, marketing, sales enablement, information security and customer service.”

Sunday, Oct. 15th: Metropolis raised $1.7bn to acquire SP+. Metropolis started as a vertical SaaS selling software to parking lots to streamline payments, automate operations and enhance customer experience. With SP+ and Premier Parking’s acquisitions, Metropolis is now buying out parkings to digitise them with its software. This playbook fits a personal thesis I have on vertically integrated vSol which will become necessary to bring digitalisation forward in certain sectors (cf. OneMedical in healthcare or Oyo in hospitality). - Yoni Rechtman, Metropolis

“At Slow, we increasingly believe that bringing software to industry remains among the biggest potential opportunities for software to orchestrate/accelerate GDP but only if you can think beyond traditional vSaaS and the GTMs and biz model thereof. Metropolis is a great case study of the "vertical SaaS buyout" where a software company buys and transforms operating companies. Metropolis gets to own all of the upside from its product and ensure its implemented properly instead trying to sell lots of small dollar contracts to hesitant SMBs. For software to truly eating the world we have to see beyond 80% gross margin pure software companies.”

Monday, Oct. 16th: David Zhou wrote about the science of selling in venture. Thanks to Paul for the recommendation! - Cup of Zhou

“Generally speaking, don’t sell your fast growing winners early. Except when…selling on your way up may not be a crazy idea.”

“You might sell when you want to lock in DPI. Don’t sell more than 20% of your fund’s positions unless you are locking in meaningful DPI for your fund. For instance, at each point in time, something that’s greater than 0.5X, 1X, 2X, or 3X of your fund size.”

“You might consider selling when you’ve lost conviction. Consider selling a position when you feel the market has over-priced the actual value, or even up to 100% if you’ve lost conviction.”

“You might consider selling when one is growing slower than your target IRR. If companies are growing slower and even only as fast as your target IRR, consider selling if not at too much of a discount.”

“At USV, they “typically seek to liquidate somewhere between 10% and 30% of our position in these pre-IPO liquidity transactions. Doing so allows us to hold onto the balance while de-risking the entire investment.”

“Returning above a 3x DPI is tough. Don’t take our words for it. Even looking at the data, only 12.5% of funds return over a 3x DPI. And only 2.5% return three times their capital back on more than 2 separate funds.”

Tuesday, Oct. 17th: Northzone wrote a blog-post on vertical AI startups. - Northzone

“At Northzone, we believe that the burgeoning capabilities of generative models promise to reshape entire industries, and we’ve spent much of the last year looking at vertical AI platforms for markets like healthcare, manufacturing, real estate, wealth management, and more.”

“We are excited about (i) NLP use cases (ii) built by industry experts that (iii) serve large, tech-laggard industries with intensely manual workflows for rich text data that (iv) often sit across multiple systems of record.”

“We find that teams with deep industry expertise can move faster because they intuitively understand this trade-off and can shortcut some of the product discovery work that others must do. Coupled with their natural GTM advantage, we find that teams that lead with industry knowledge and are supported by AI talent typically find PMF the fastest.”

“The best vertical AI solutions will be like a functional worker who is also a team player: expert in their core task (summarization, for instance), but also diligent in updating the horizontal systems of record that the broader organization relies on”

Wednesday, Oct. 18th: I listened to a Colossus’ podcast episode on Wex with Mark Tomasovic, an investor at Energize Capital. Wex is a leading player in the fleet card market offering specialized credit cards for fleet operators to efficiently manage their fuel expenses while providing rebates and enhanced control. - Colossus

In the US, 400m gallons of motor gasoline are purchased everyday (inc. 60m for fleets) and there are 40m fleet vehicles. 20% of the fleet market is unaddressable because fleets purchase fuel outside the retail gas stations network (e.g. school buses having their own private fleet fuelling locations).

Wex has a 25-30% market share in the US fleet market with 18m vehicles and 600k fleets as customers. It generates $2.5bn in sales growing 25% YoY. 60% of revenues is coming from the fleet business unit. 40% of revenues is coming from B2B payments (travel & corporate expenses, health & employee benefits). Wex has a 35% EBITDA margin and the fleet division has a 50% EBITDA margin. Late fee makes up about 1/3 of their overall fleet solutions revenue.

30-40% of fleets are unequipped with fleet cards. Wex competes with Fleetcor which has 24m vehicles and 800k customers as well as with Voyager Bank Card. Wex, Fleetcor and Voyager Bank Card have a 50% combined market share.

For fleet owners, the value proposition is (i) to control spend from fleets (how much fuel has been purchased? what was the vehicle mileage? what were the ancillaries purchased?) and (ii) to get rebate on fuel prices compared to the retail price.

Wex has its own payment loop. It does not rely on Visa or Mastercard to process transactions meaning that Wex can capture a higher share of interchange fees compared to traditional credit card businesses.

In the mid-term, Wex is facing the following risks: (i) exposure to fuel price, (ii) pressure from investors to divest fuel related businesses (and Wex could be considered as such) and (iii) increasing interest rates putting pressure on margins (because Wex Bank’s cost of capital is increasing).

Wex has to properly manage the transition towards hybrid fleets and full EV fleets. Today, Wex captures $6 per vehicle per month on their gasoline fuel card product. On EVs, Wex estimates that it can capture between $5 and $20 per vehicle per month because EVs can be monetised in several ways (find charging locations, monitor battery performance, reimburse employees if they charge at home instead of at a fleet depot).

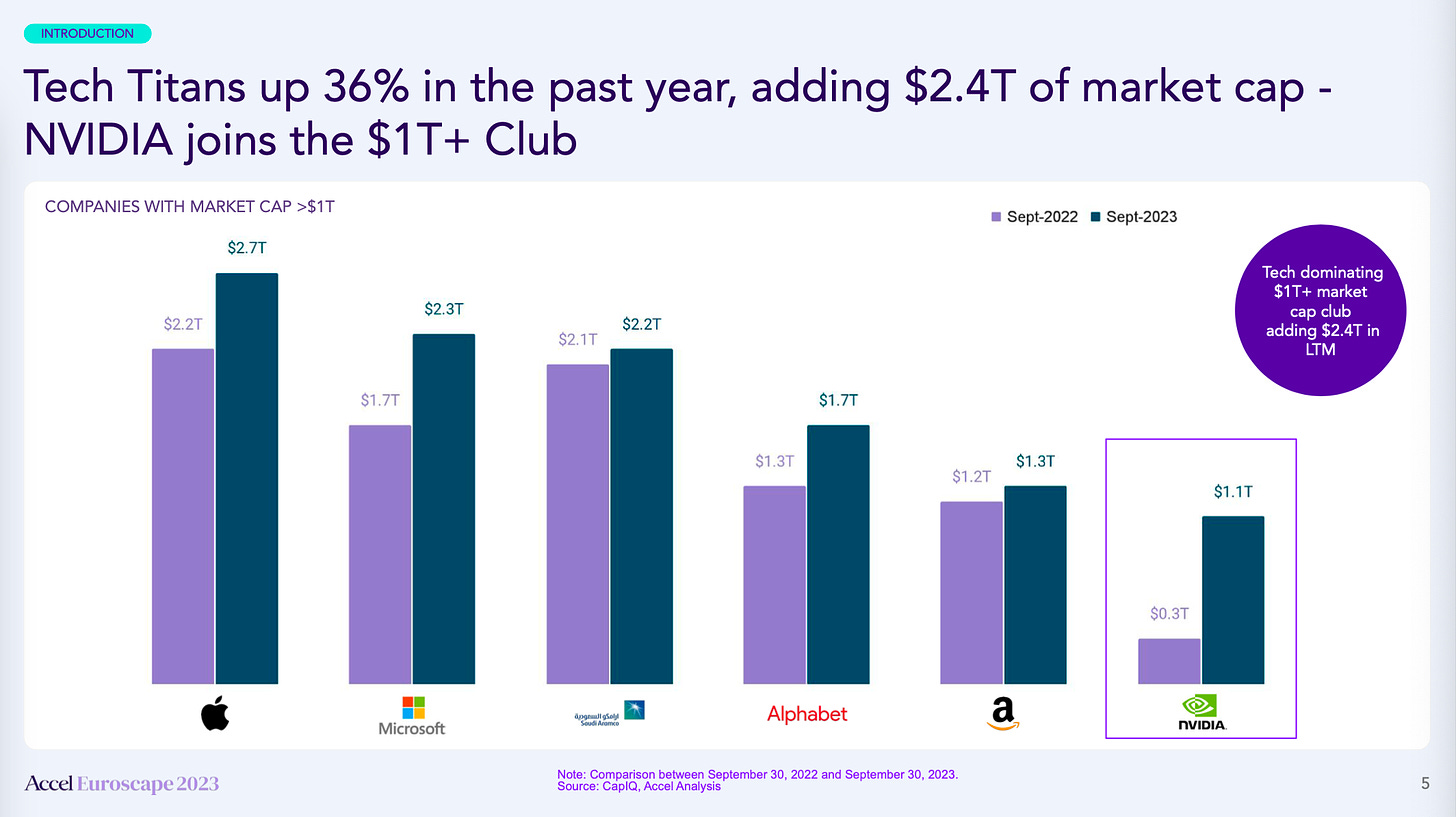

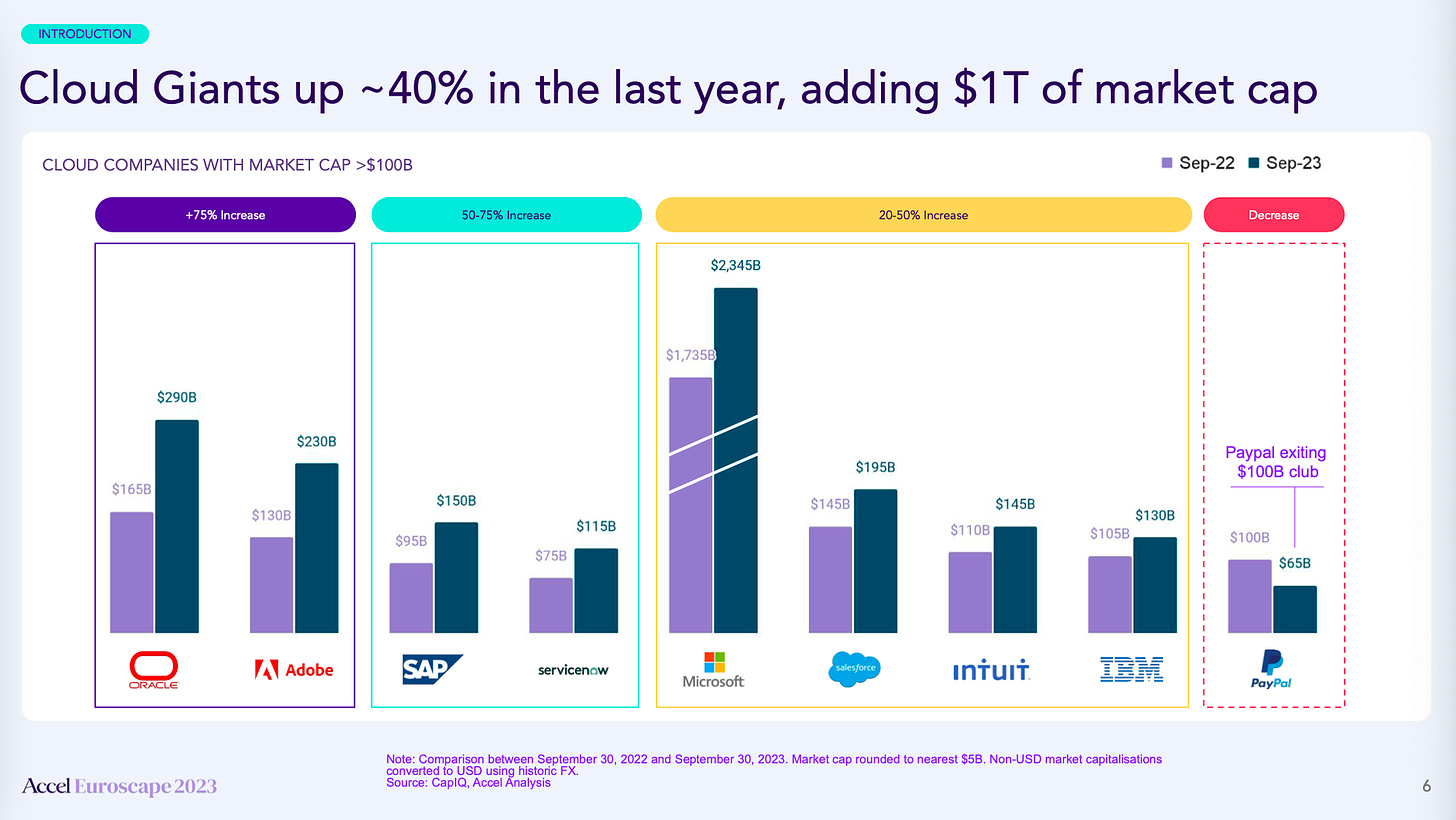

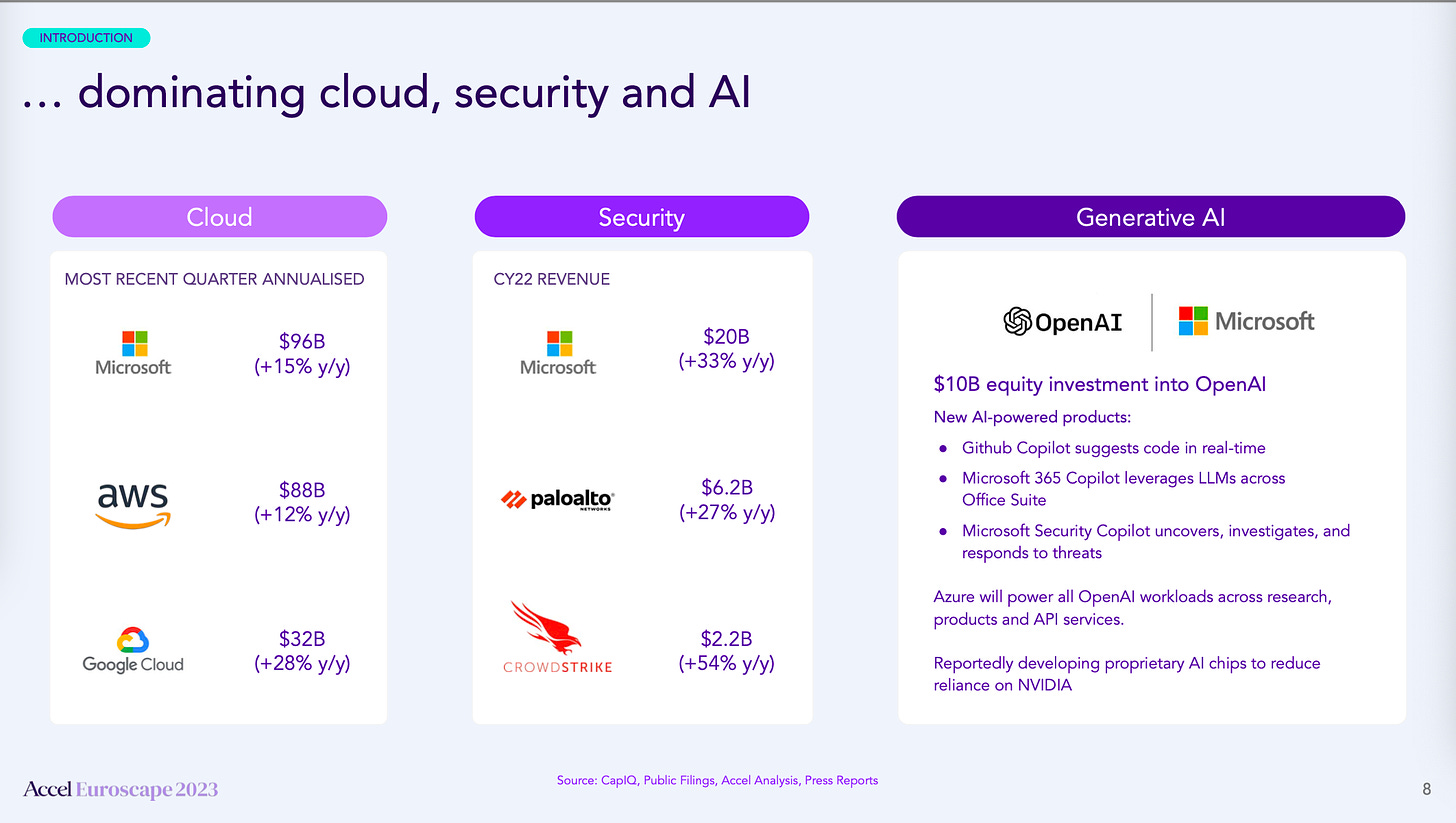

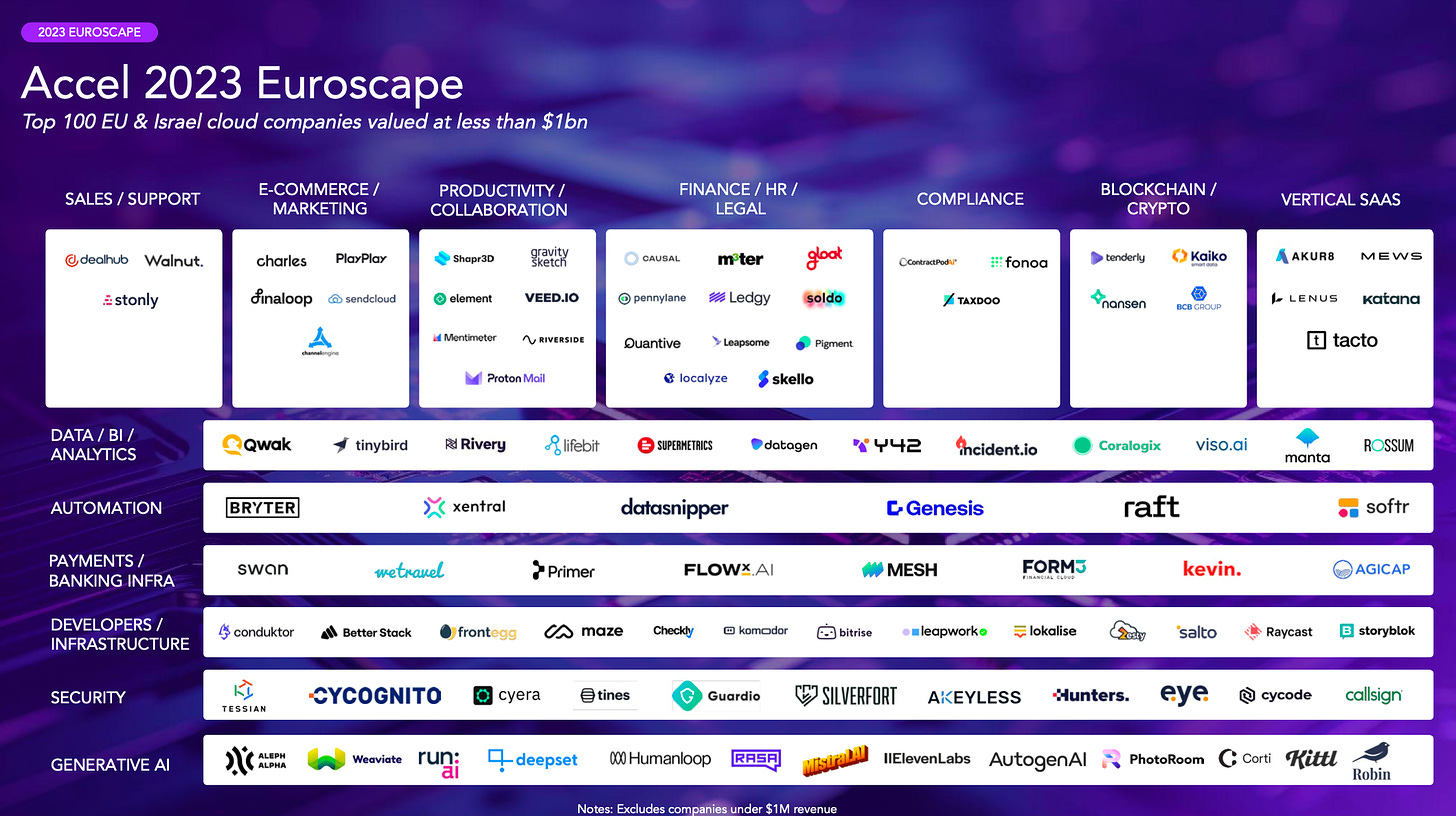

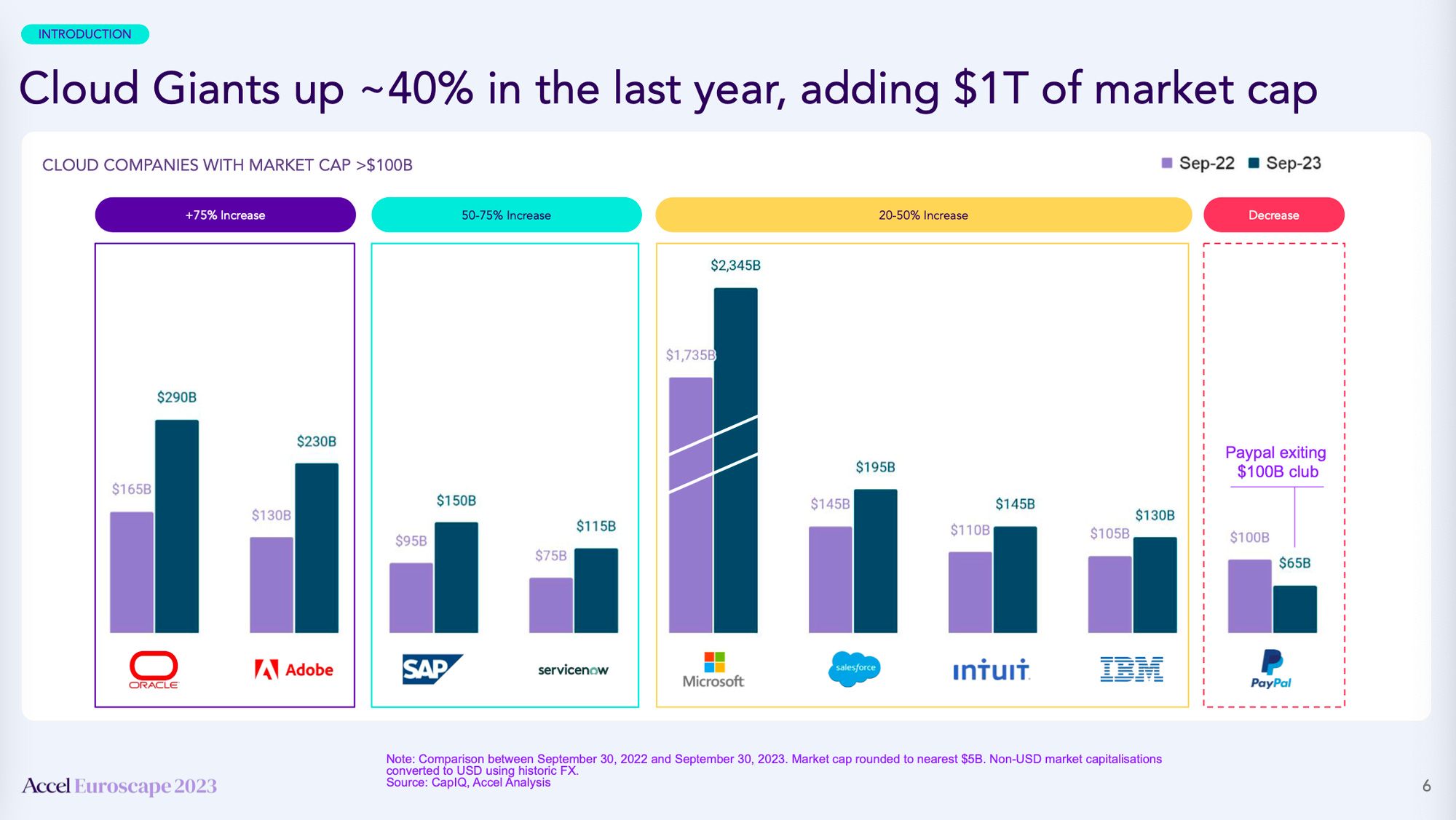

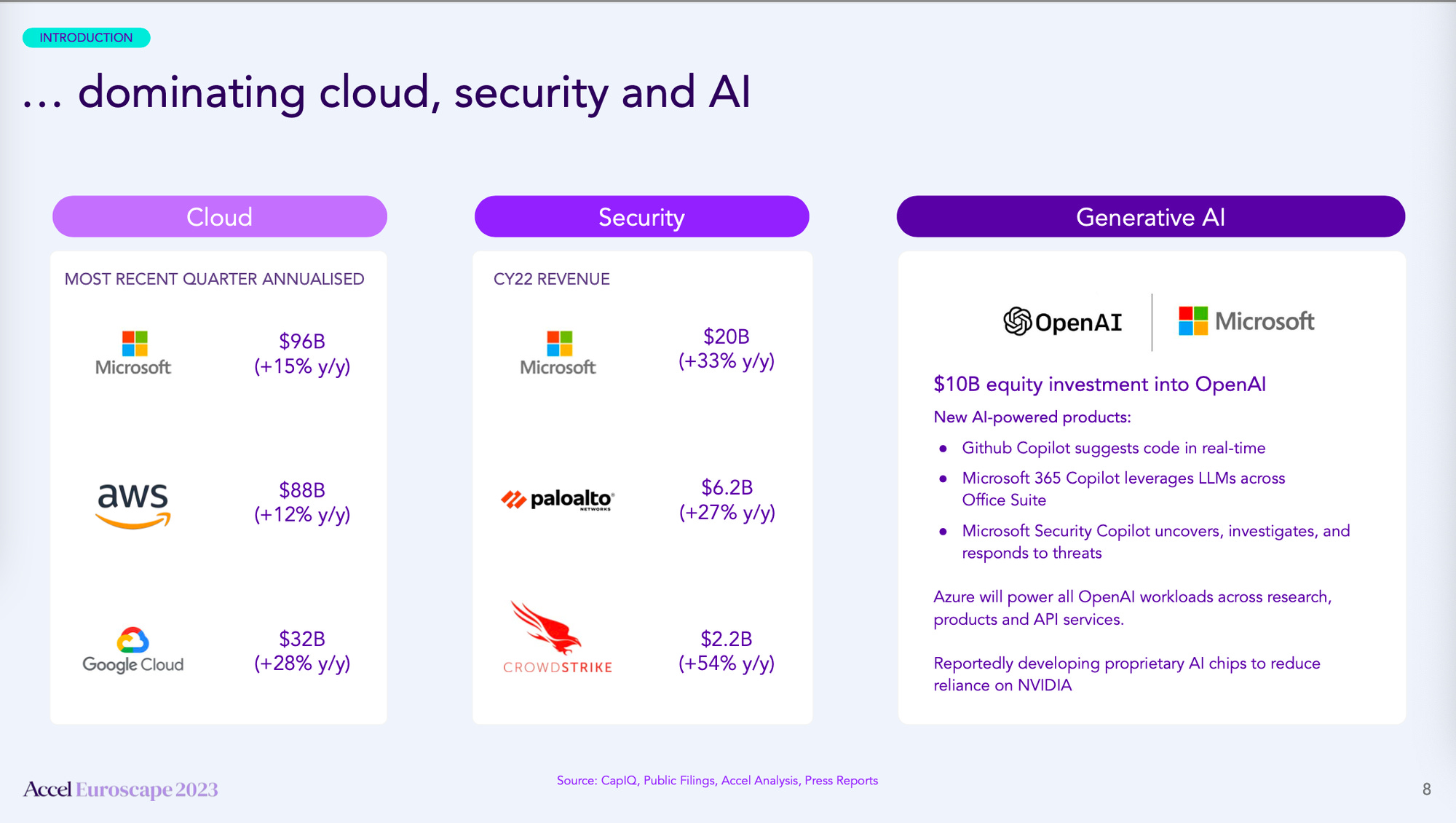

Thursday, Oct. 19th: Accel published its 2023 Euroscape report highlighting top trends in SaaS and a list of 100 European SaaS companies to track. - Accel

The public tech market is recovering mainly driven by tech titans (Apple, Microsoft, Alphabet, Amazon and Nvida) and large cloud players (Oracle, Adobe, SAP, Service Now, Salesforce, Intuit).

Microsoft is dominating 3 core SaaS markets: cloud ($96bn in ARR), security ($20bn revenues in 2022) and AI ($10bn investment into OpenAI, Github Copilot, Microsoft 365 Copilot).

Friday, Oct. 20th: Sam Lessin (GP at Slow) wrote about the current state of the seed investing market. - Sam Lessin

“The entire game of seed investing has very very quickly and violently changed in the last 18 months. There is a lot to be excited about; however, seed investors who do not recoginze the new world of today and change how they operate quickly are going to have a very bad time.”

“It has never been easier for super small lean teams to build serious businesses with extreme capital efficiency and getting profitable early. There will be more software and community driven 'billionaire' founders of tightly held companies in the coming years than ever before & seed investors are ideally positioned to provide the single 'shot' of high risk capital for liftoff and do very very well backing these shots.”

Saturday, Oct. 21st: Digital freight forwarder Convoy is ceasing operations, despite having raised $1bn in funding, including a recent round at a $3.8bn valuation. Previously, Convoy had gone though two rounds of layoffs (decreasing its workforce from 1.5k to 500 FTES) and failed to sell the business to a strategic acquirer - Freightwaves, Geekwire, Adam Keesling

“What happened and what does it mean for other supply chain tech companies? In short, it was a liquidity crunch: Convoy has taken on debt, and a change in both capital markets and a massive freight recession created the perfect storm for a shut-down”

“Convoy is a digital freight brokerage. They connect companies shipping stuff (shippers) with companies who have trucks and transport that stuff (carriers). Because there’s no physical product in freight brokerages (“asset-light”), they can scale quickly, which is what happened over the past several years. While physical constraints weren’t limiting growth, financial constraints were limiting growth. They could get shippers to sell them shipments quickly (which they passed off to carriers), but the shippers wouldn’t part with cash for that shipment right away (perhaps on 30, 60, 90 or longer terms).”

“In short, we are in the middle of a massive freight recession and a contraction in the capital markets. This combination ultimately crushed our progress at the same time that it was crushing our logical strategic acquirer – it was the perfect storm.”

“Alongside this unprecedented freight market collapse, the dramatic monetary tightening we’ve seen over the last 18 months has dramatically dampened investment appetite and shrunk flows into unprofitable late stage private companies. Add to that, amidst these freight and financial conditions, M&A activity has shrunk substantially and most of logical strategic acquirers of Convoy are also suffering from the freight market collapse, making the deal doing that much harder.”

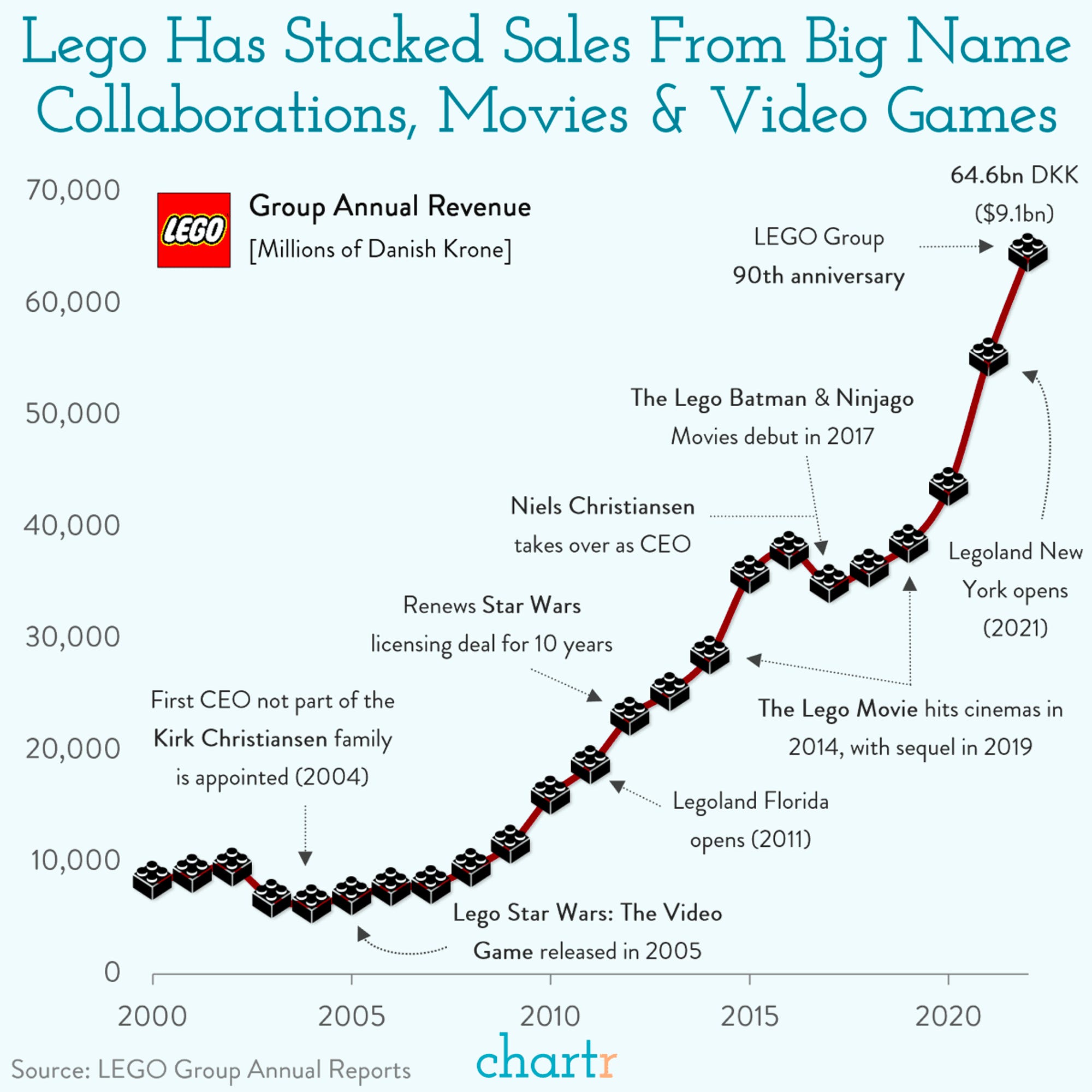

Sunday, Oct. 22nd: Chartr published great charts on Lego. - Chartr

“Lego has an enormous legion of AFOLs (Adult Fans Of Lego). Whether driven by nostalgia, the need for stress relief, or just wanting to show people a self-completed 7,541-piece Millenium Falcon, more adults are discovering, or rediscovering, the joy of Lego.”

To grow its sales, Lego has distributed its IPs in multiple media formats including movies (The Lego Movie) and video games (Lego Star Wars). It created a virtuous circle between physical Lego sales and its media and entertainment empires.

Monday, Oct. 23rd: US-based multi-stage firm General Catalyst acquired German-based seed fund La Famiglia. La Famiglia will become General Catalyst’s seed investing platform especially in Europe. Both firms co-invested into companies including Helsing, Stripe, Applied Intuition, Maven and Ramp. For General Catalyst, it’s a medium to expand its footprint both in Europe and in the seed market after having opened an office in Europe in Dec. 2021. Bundling and unbundling waves are also applying to venture. In summer, Sequoia broke down its operations into three different firms. Today, GC is joining forces with La Famiglia. In a venture market under pressure, it’s not surprising to see stakeholders being reshuffled. - Sifted, Techcrunch, GC

“We’ve probably reached the end of the SaaS curve. There’s probably going to be a redistribution of market share. If we think about what this next wave of innovation is going to be, it’s probably going to be anchored more in a shift from bits to atoms.” - Jeannette zu Fürstenberg

“Global resilience is a key theme for us, and Jeannette has a genuine passion for bringing that thesis to Europe. She has been a steadfast champion for a vital European tech ecosystem and has activated its closer partnership with industrial leaders.” - Hemant Taneja

Tuesday, Oct. 24th: US-based startup **iink raised a $12m series A led by Headline**. It’s a verticalised fintech automating payments in multiparty property insurance integrating into a single platform mortgage servicing banks, insurance carriers, contractors and property owners. It was founded in 2017 and it was operating as a service business until 2022. The company will use the funds to increase the size of the team, to expand its customer base and to double down in automations. - Techcrunch, Headline, GlobalNews

“The property insurance claim payout process in the US is a painful, and often manual, process that involves multiple parties, physical checks, and insurance proceeds split across numerous bank accounts. These manual workflows result in policyholders waiting unnecessarily for their homes to be repaired and liveable. It is expected that nearly $500 billion in property payment claims will be paid out this year, with most of these transactions still taking place via paper checks.”

“The company was built to initially be a workflow tool that automates the collection of digital signatures across these various stakeholders and then disburses the claim payout funds.”

“The company’s near-term product roadmap positions iink as a verticalized operating system for contractors, providing a digital wallet, embedded insurance, and debit card for contractors to pay for supplies. The longer-term vision is to build a closed-loop payment network between the insurance carriers, the mortgage lenders, the homeowners, and contractors, to move insurance payments from physical checks to digital payouts.”

“It’s an area that is ripe for digital transformation and iink has perfectly positioned itself as a conduit for carriers, banks, contractors, and property owners to communicate and keep the restoration process moving.”

Wednesday, Oct. 25th: Bloomberg wrote about the Thiel’s fellowship. Thiel’s fellows have built 11 startups which are valued over $1bn including Ethereum, Luminar, Upstart, Figma and Scale AI. - Bloomberg

“11 of the 271 recipients of the Thiel Fellowship have founded unicorns so far, an impressive accomplishment that doesn’t even take into account the inspiring innovations of other fellows and the many exciting projects yet to mature.”

“In 2011, Peter Thiel launched a controversial education program to pay college students $100,000 to drop out.”

“By giving people like his younger self a little money, some prestige and access to a network, he’s helped create innovative, valuable companies. The results of the Thiel Fellowship demonstrate that colleges likely block or delay the success of the most promising students.”

“[Thiel] sees the current higher education system as a perverse credentialing machine that forces students away from impactful careers in favor of ones like consulting and banking, which offer the surest path to repaying exorbitant loans.”

Thursday, Oct. 26th: Matt Brown wrote about ghost markets. - Matt Brown

“Ghost markets (e.g. B2B payments or freelancers market) seem real. They have a seemingly enormous TAM and a clear story about how tech will disrupt it and create a huge company in the process. Bottom-up and top-down analyses validate the opportunity. It’s the topic du jour on Twitter and TechCrunch. So a wave of companies is funded to go after it, and then… the opportunity vanishes into thin air.”

“People fall for ghost markets because they misunderstand vertical and horizontal markets. Vertical markets are defined by WHO is buying. Horizontal markets are defined by WHAT is being sold. The common misunderstanding comes from the subtle but critical point that no market, company, or product is entirely vertical or horizontal. Every market is defined BOTH by WHAT they sell and WHO buys it.”

“A ghost market is a vertical market that’s too vertical or a horizontal market that’s too horizontal. It’s a market that is defined so broadly in one dimension and excludes the other dimension entirely, so that it seems large and attractive but is in fact non-existent.”

“I think ghost markets appear most often when someone outside the market applies a label to the customer or to the solution which is entirely accurate, but also entirely useless. The problem with ghost markets isn’t that they’re wrong; it’s that there’s no opportunity there.”

Friday, Oct. 27th: The Atlantic wrote about the growing importance of the private equity industry in the US economy. - The Atlantic

The number of US public companies decreased from 8k in 1996 to 4k in 2023 in a country which added $20tn in GDP and 70m in habitants over the same period.

“The thing about public companies is that they’re, well, public. By law, they have to disclose information about their finances, operations, business risks, and legal liabilities. Taking a company private exempts it from those requirements.”

“In 2000, PE firms managed about 4% of total U.S. corporate equity. By 2021, that number was closer to 20%. In other words, private equity has been growing nearly five times faster than the U.S. economy as a whole.”

“Indeed, from 1980 to 2000, an average of 310 companies went public every year; from 2001 to 2022, only 118 did. The number briefly shot up during the coronavirus pandemic but has since fallen.”

“The secrecy in which private-equity firms operate emboldens them to act more recklessly—and makes it much harder to hold them accountable when they do.”

“Nearly a century ago, Congress concluded that the nation’s economic system could not survive as long as its most powerful companies were left to operate in the shadows. It took the worst economic cataclysm in American history to learn that lesson. The question now is what it will take to learn it again.”

Saturday, Oct. 28th: I listened to a 20VC’s podcast episode on seed investing with Ed Sim who is general partner at Boldstart. - 20VC, Ed Sim 1, Ed Sim 2

“This is the new race to be first — finding those special people, working with them well before incorporation, and arming them with capital to run fast.” […] “[Founders] will also need to partner with a fund with the right size who is big enough to lead any of these rounds, but also small enough that they get 1:1 attention — which means firms with concentrated portfolios.”

Ed Sim distinguishes 3 types of inception rounds which are defined as funding rounds that occur at the time of incorporation after having engaged with founders well before they incorporate helping them to iterate on the idea, recruit talents and validate market hypotheses:

Discovery rounds (below $2m) for first time founders exploring new sectors and who just need a bit of funding to hire their initial team and refine their ideas,

Classic rounds ($3-5m) for first or second-time founders. These founders might be capable of raising more, but they recognize that necessity is the mother of invention,

Jumbo rounds (above $6m) for repeat founders with have had a prior exit and are now building their next company, often reimagining an existing market with a large TAM. Jumbo rounds have emerged because of multi-stage funds are super-sizing classic rounds to deploy capital.

“[Every fund is] trying to go earlier and earlier and get pole position for future - it's super competitive out there at earliest stages.”

“Too much cash too early has a net impact on 99.9% of companies unless the founder is an exceptional capital allocator.”

“There are some smart second time founders that we just backed at inception raising $3-4m because they want the pressure to create quickly, they want hire great initial talents and they want to be able to raise the next round easily.”

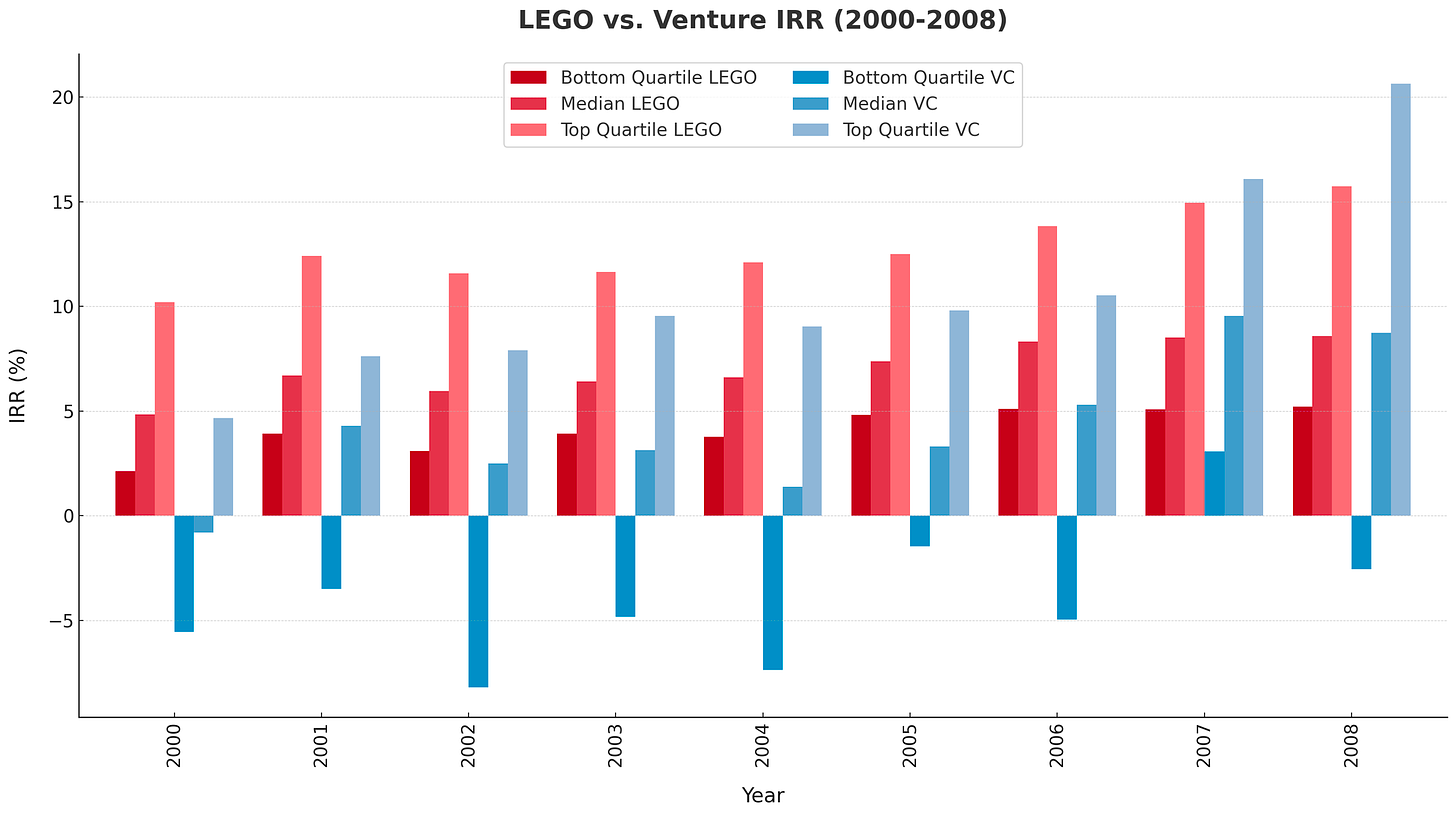

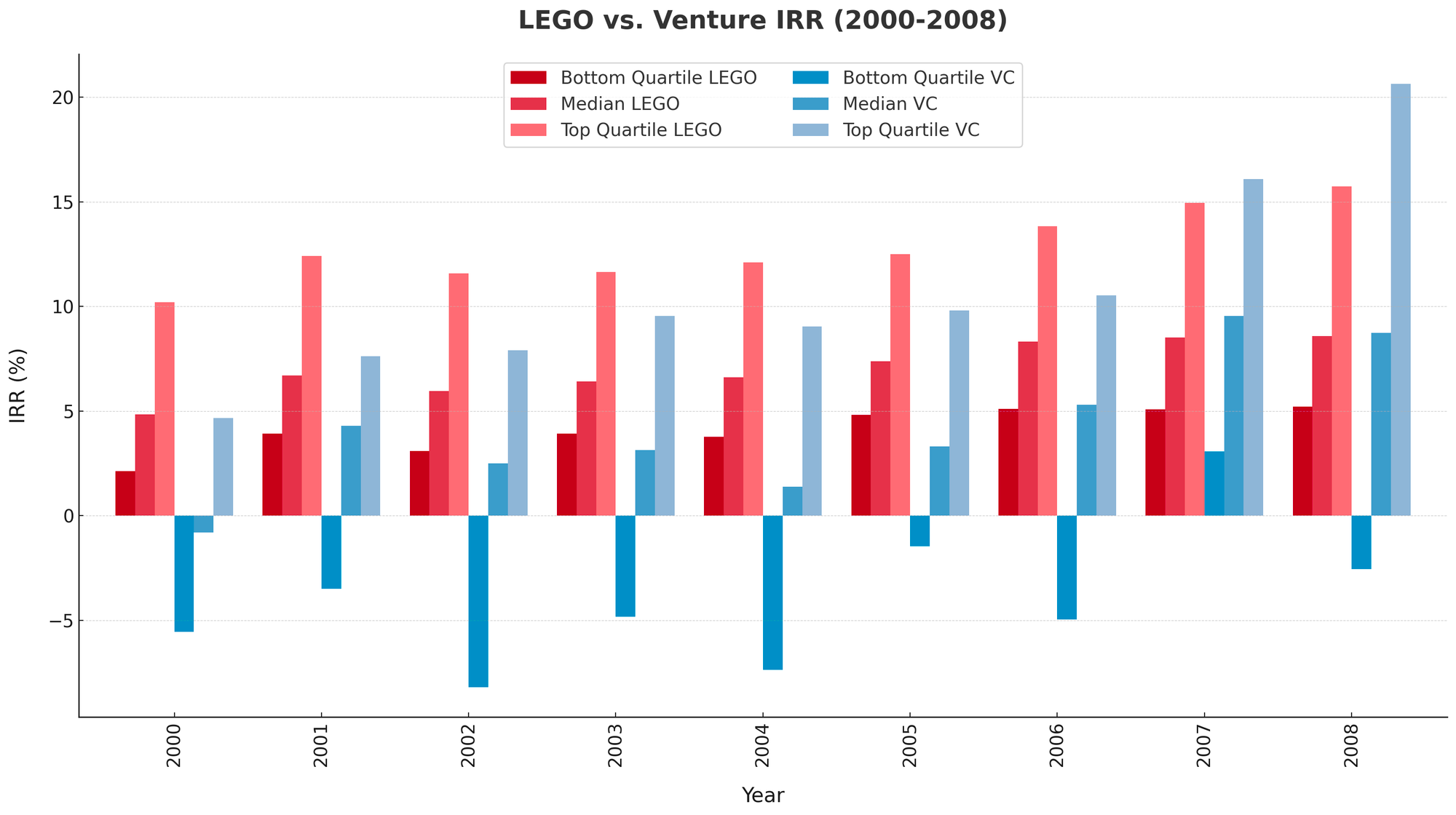

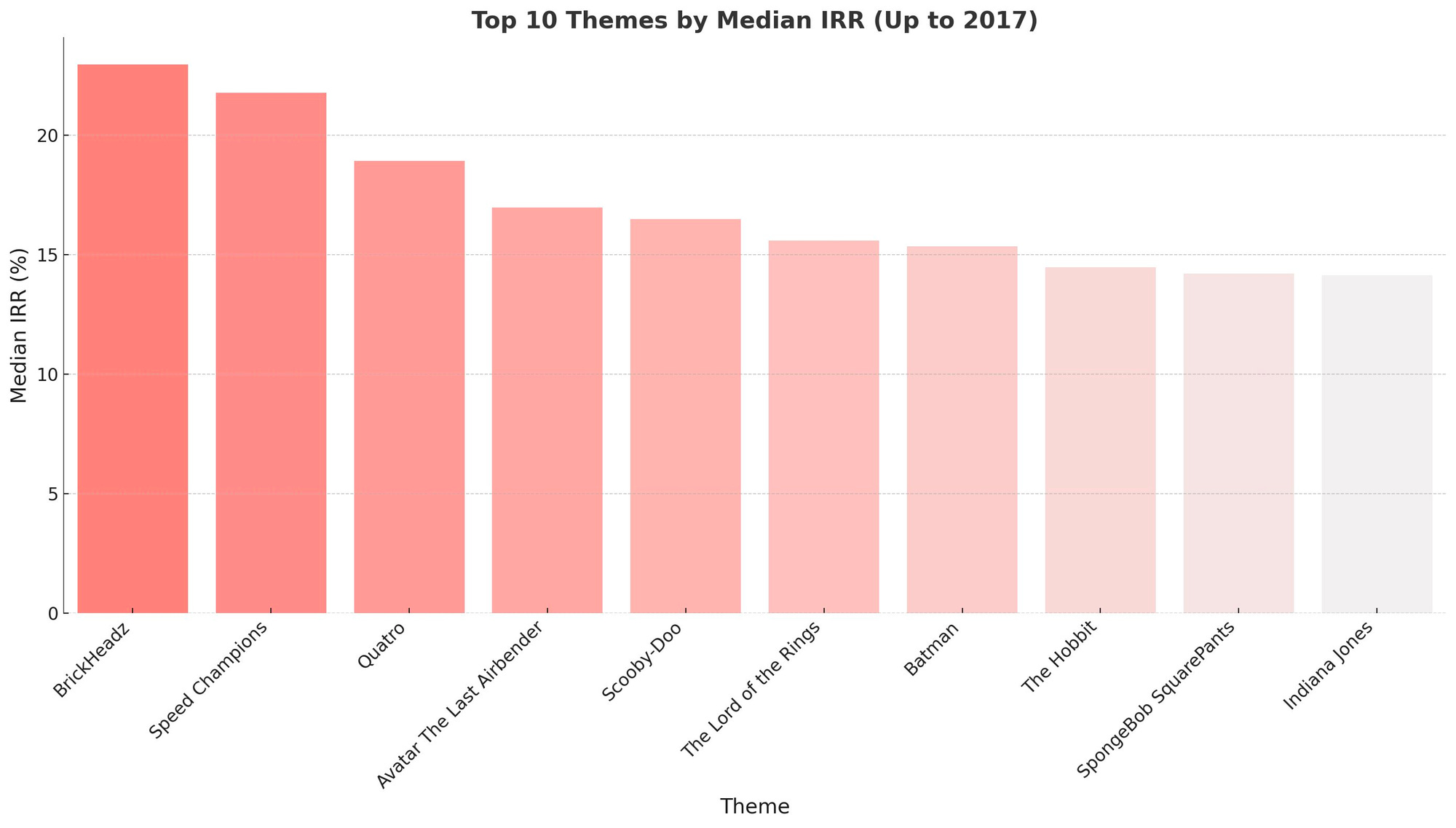

Sunday, Oct. 29th: Will Manidis (founder and CEO at ScienceIO) authored a post in which he compared the performance of venture funds and Lego. He used data on second hand Lego pricing from 10k different sets. - Will Manidis

“In most years, random [Lego] purchasing rivalled the returns of the median venture fund. If you just blindly bought certain themes, you can consistently generate double digit IRR across all vintages.”

“Buying Lego durably produce 10%+ IRR. Top decile sets will return 30%+ constantly over a decade.” “It is easy to predict these IRR drivers (e.g. sets that appreciate in year n-2 are likely to hold that IRR for years, representing basically free annuities).”

“Is there enough liquidity [to legitimately compare Lego and venture funds]? I did the math, and the Lego secondary market is of similar scale if not greater scale than some national economies. You could easily move tens of millions if not hundreds of millions of dollar of volume in this market. Certainly not the scale of venture capital, but you can make some money here.”

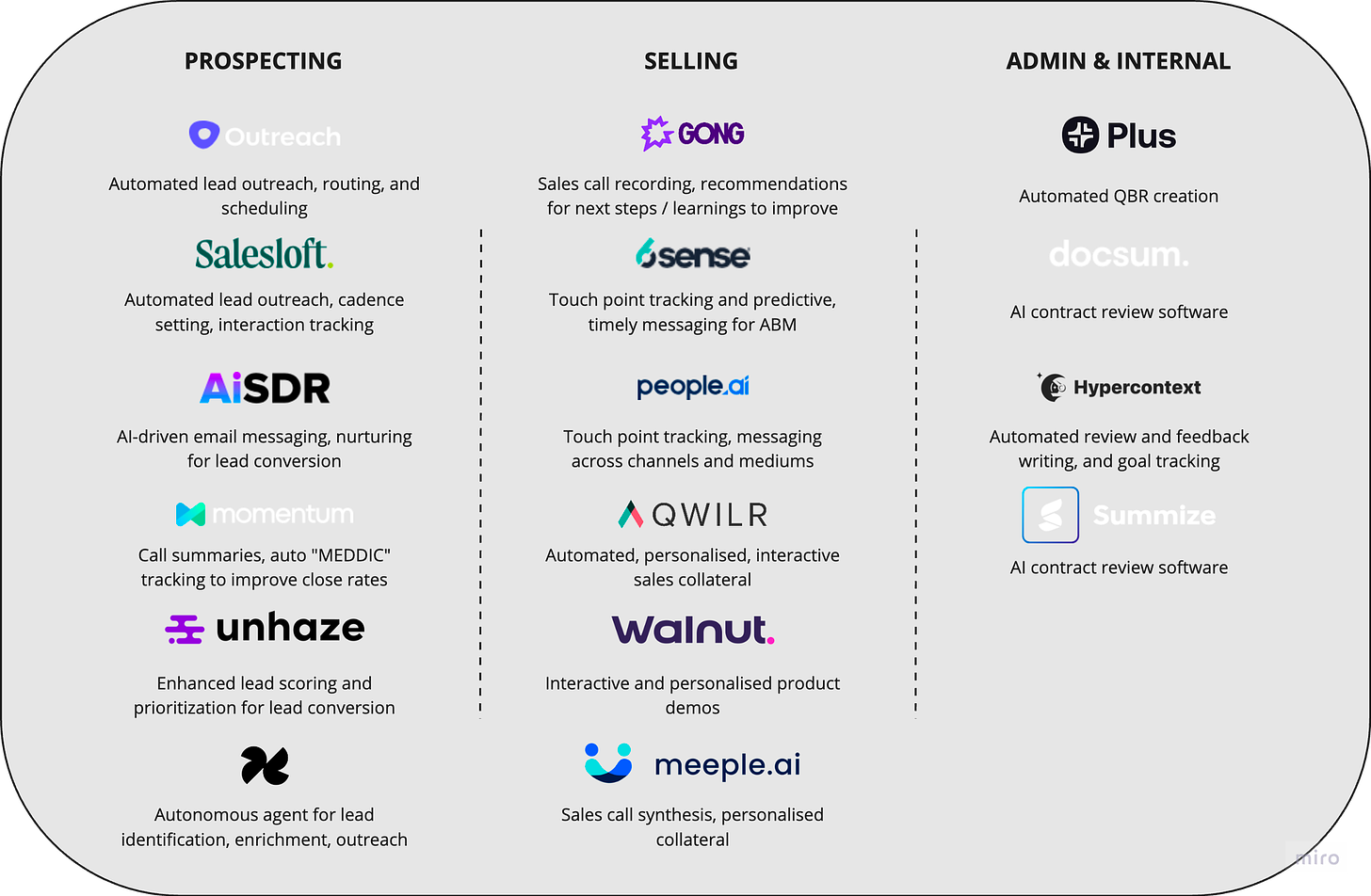

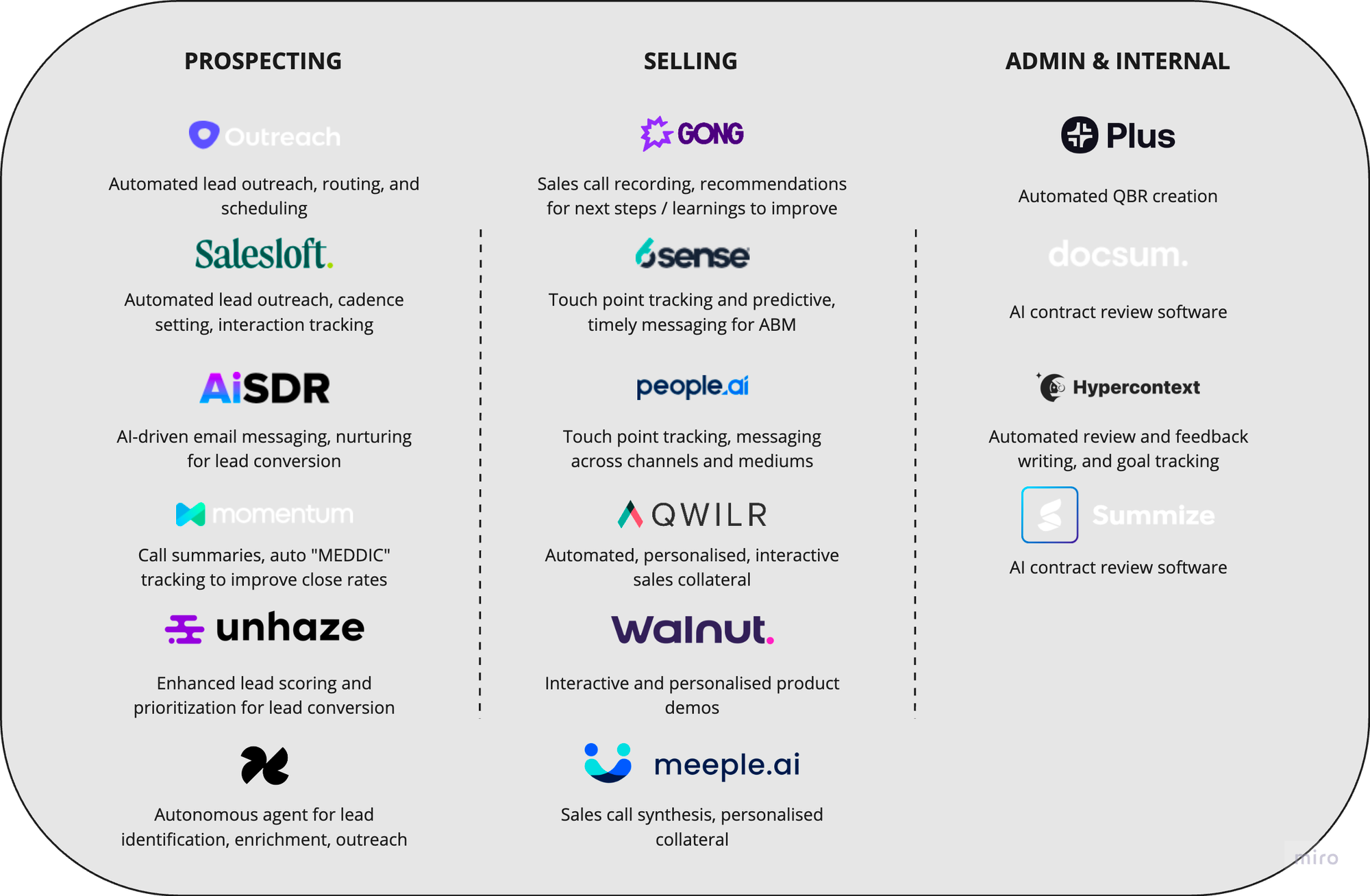

Monday, Oct. 30th: Akshat at Moonfire wrote about the B2B sales tech stack. - Moonfire

“Sales leaders are thinking about how we can create 10x SDRs with the good ones, and eliminate the ones that can’t become that with AI-driven tooling.” - B2B CRO consultant

“The majority of the feedback from our interviews sees outreach as the biggest time saver in the near term – if it works. The problem is that there is significant scepticism among sales leaders that AI can be as good as the human touch.”

“Internal processes and other administrative work that salespeople do surrounding the sale can’t all be eliminated (at least in the near term), but much of it can be improved with AI. The feedback we got from our interviews suggested that prepping, populating templates for internal meetings, and closing paperwork and contracts are all areas where AI can play a role.”

“A vision not just to a BDR productivity tool, but to becoming a BDR replacement. Specifically to prospecting, products with a forward-thinking approach aiming to eventually eliminate the BDR/SDR function will more effectively land over the long term with mid-to-senior level sales leaders, who don't want to train high-turnover BDRs on new tooling every year.”

Tuesday, Oct. 31st: The Economist wrote about upcoming AI regulations. - The Economist 1, The Economist 2

More than 50% of Americans are more concerned than excited about the use of AI.

“Another driver of AI-rulemaking diplomacy is even more surprising: the model-makers themselves. In the past the technology industry mostly opposed regulation. Now giants such as Alphabet and Microsoft, and ai darlings like Anthropic and Openai, which created ChatGPT, lobby for it.”

“Most firms also agree it is models’ applications, rather than the models themselves, that ought to be regulated. Office software? Light touch. Health-care AI? Stringent rules. Facial recognition in public spaces? Probably a no-go. The advantage of such use-based regulation is that existing laws would mostly suffice. The AI developers warn that broader and more intrusive rules would slow down innovation.”

“The European Parliament wants model-makers to test LLMs for potential impact on everything from human health to human rights. It insists on getting information about the data on which the models are trained.”

“If [regulators] go too fast, policymakers could create global rules and institutions that are aimed at the wrong problems, are ineffective against the real ones and which stifle innovation.”

“New regulation could easily entrench the incumbents and block out competitors, not least because the biggest model-makers are working closely with governments on writing the rule book. A focus on extreme risks is likely to make regulators wary of open-source models, which are freely available and can easily be modified; until recently the White House was rumoured to be considering banning firms from releasing frontier open-source models. Yet if those risks do not materialise, restraining open-source models would serve only to limit an important source of competition.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋