🗞 Venture Chronicles - October 2022

Overlooked #129

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of October.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for October!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Saturday, Oct. 1st: The Economist wrote about the massive labour shortage that Germany is experiencing. - The Economist

Job vacancies reached 1.93m in Q2-22 (66% YoY increase) and c. 50% of German companies are struggling to hire enough skilled workers (vs. 30% in 2019). The German workforce is set to decrease by 15-16m people by 2060 (350-400k per year).

Several levers can be activated: increasing workforce participation rates, delaying retirement dates and leveraging immigration.

Sunday, Oct. 2nd: I listened to Acquired’s podcast on Benchmark. - Acquired

After Benchmark’s initial fund I success, distractions were coming from everywhere: (i) corporates were calling from all over the US to create joint ventures to digitize their business (e.g. Goldman Sachs, GM, ToysRUs), (ii) opportunity to expand Benchmark’s brand over the world, (iii) recruit other people in the team to process the massive inbound they started receiving and (iv) to raise bigger funds.

Bill Gurley was recruited as the sixth partner. Benchmark was trying to find a partner with a strong experience in venture. In terms of mindset, Benchmark was looking at investors that were both fiercely competitive on the ground and collaborative inside the partnership. Bill Gurley was known to have strong work ethics. He had started his career as an engineer at Compaq before joining Franck Quattrone to work on tech IPOs as a sell side analyst. He left to work in venture before being recruited by Benchmark.

With eBay, Benchmark discovered an mis-pricing in the venture market. They should not invest before product launch and product market fit as it was previously done. Instead, they should invest during a series A, into companies with a live product and early traction thus removing both product and market risks.

When you’re in a small equal partnership, you spend all your time on the field making new investments and supporting your portfolio companies. You don’t have to manage people or perform admin tasks.

After the success of fund I, Benchmark expanded globally. It raised a US $1bn fund, a $750m European fund and a $250m Israeli fund. It recruited local equal partnerships in the two new regions and gave them full autonomy. Benchmark US missed Google and Facebook because of these distractions. At some point, the US partnership decided to back pedal. It reduced the size of its next fund and closed its foreign offices (Benchmark Europe would end up becoming Balderton).

In my opinion, Benchmark’s most impressive fund is not its first fund which invested into eBay because (i) it benefited from the internet bubble, (ii) its performance is mainly driven by eBay and (iii) it was a small fund. I am much more impressed by Benchmark Fund VII. It was a $550m fund raised in 2011 which invested in Uber, Snap, Discord, StitchFix, Duo Security, Docker, Elastic, Nextdoor and WeWork. In 2018, the Wall Street Journal reported that this fund had a 25x multiple before fees.

Contrary to USV, Benchmark is not thesis driven. “Our job as a venture capitalist is not to see the future but to see the present very clearly” said Matt Cohler. Partners are great at picking founders as well as at picking businesses with compelling positioning and execution.

Benchmark is great at exiting its investments. For instance, they sold an important WeWork’s stake to Softbank when the company valuation was starting to get unsustainable. Moreover, Benchmark does not hold its stakes in the long term in companies which are going public. It prefers to pay back its investors as soon as possible.

Monday, Oct. 3rd: I read a McKinsey interview with Benchmark’s general partner Bill Gurley who invested into companies like Nextdoor, Grubhub, OpenTable or Uber. - McKinsey

When you’re laying-off employees, it should have a significant impact on your expenses (20-30% of your FTEs). In any case, you will have the negative cultural impact of a layoff and it’s better than making several rounds of layoffs (5-10% of your FTEs).

“The truth is that if you’re going to build something from scratch, this might be as good a time as you’ve had in a decade.” It’s the case because real estate is cheap and access to talents is getting better.

Benchmark is maniacally focused. “Around 85-90% of our funds are deployed on first-money and early-stage investments.” It does not have internal offices. It has not become multi-stage. It has not increased the size of its funds.

Silicon Valley is a powerful hub to start a tech company because (i) there is executive talent and (ii) everyone is working in the tech industry “creating a ton of serendipity outside the office”.

Tuesday, Oct. 4th: 83North raised a $400m fund XI. It’s a fund that deserves much more recognition in Europe. It has a Benchmark-style operating model with 4 equal partners and small & focused funds. 83 North has an impressive hit rate. It invested in 90 companies, of which 14 are now unicorns (inc. Celonis, Exotec, iZettle, IronSource, Marqeta, Mirakl or Wolt). 83 North invests in early stage and globally (US, Europe and Israël). It has 4 main pillars: (i) a boutique style operation with one deal per year and per partner, (ii) backing companies that are defining and leading global category leaders, (iii) building long term relationships with founders and (iv) an entrepreneur-first approach.- 83North

Wednesday, Oct. 5th: I read a post from Deconstructor of Fun unpacking Supercell’s success. - DoF

Supercell is unique in mobile gaming because it has repeatedly disrupted the industry creating new genres or redefining existing ones. It has published several games with over $1bn in lifetime revenues (Hay Day, Boom Beach, Clash of Clans, Clash Royale, Brawl Stars). It has built a well diversified portfolio across genres and it has published games with an incredible longevity.

Clash of Clans is Supercell’s best-seller. In April 2020, it had already generated over $6.5bn in lifetime revenues. Clash of Clans’ success in based on 4 key ingredients: (i) compelling and deep gameplay, (ii) a new social experience with Clan Wars in which players gather in guilds to cooperate against other guilds, (iii) a deep economy, (iv) strong live-ops with fresh content released regularly.

Supercell’s success is based on a distinctive culture in the gaming industry: (i) small development teams with a strong autonomy and extreme ownership on their games, (ii) a ruthless level of feedback from the organisation for games in development, (iii) an environment in which people are pushed to take risks or express their full creativity.

“Supercell’s strategy is not for everybody, as it requires extremely high design talent, creativity, and a risk-taking, long-term focused mindset.” As a result, “Supercell is one of the few companies that is best positioned to generate genre-defining hits in the mature mobile gaming market”

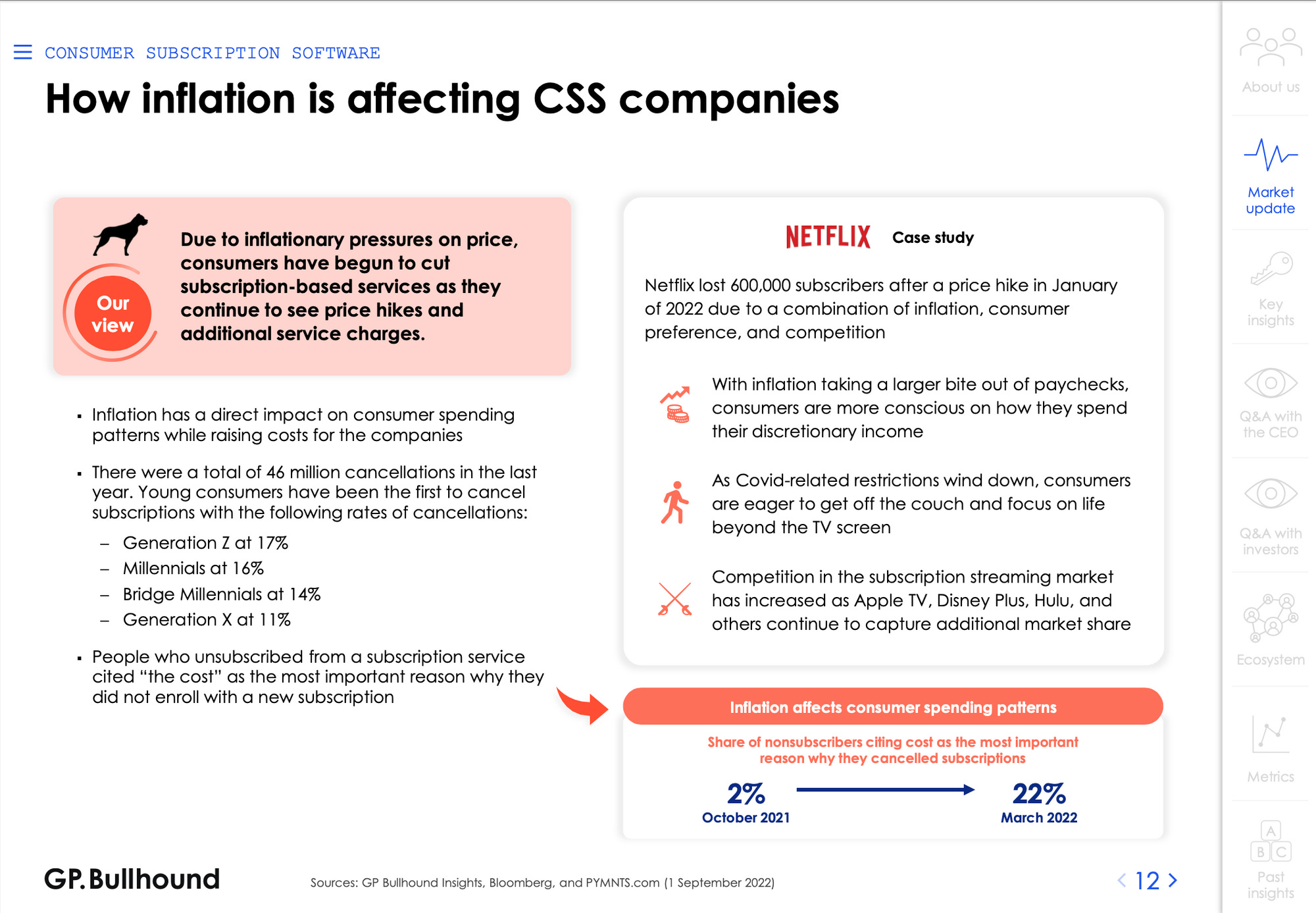

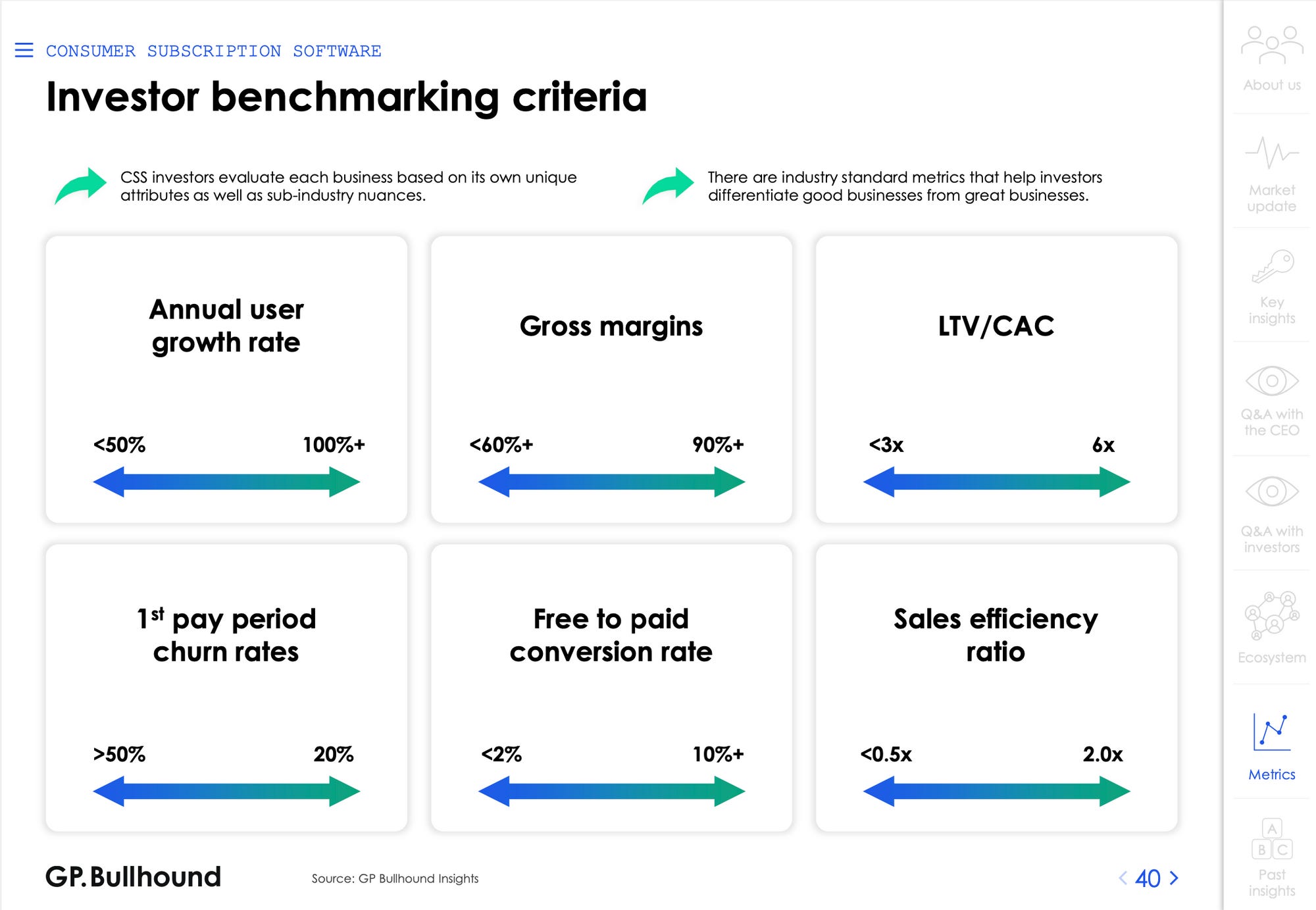

Thursday, Oct. 6th: GP Bullhound published a new report on Consumer Subscription Software (CSS). - GP Bullhound

Friday, Oct. 7th: Tiger Global is raising a new fund that is half the size than his previous one, and one of its key partners John Curtis is leaving to create his own fund. - Forbes, Tiger Global, The Information 1, The Information 2

Tiger is raising a $6bn fund (vs. $12.7bn for the previous one) with a 1st closing expected in January.

John Curtis is leaving and will launch its own investment fund in 2023. It is called Cedar Investment Management to invest in B2B companies in early stage (between series A and series C). John Curtis worked at Silverlake and Elliott before joining Tiger Global in 2017. At Tiger, he invested into 250 companies in 5 years (1 company a week) including companies such as Snowflake, Synk, Databricks, Toast, Hopin or Confluent.

Saturday, Oct. 8th: Casavo raised a €100m series D led by Exor with the participation of new investors Hambro Perks, Neva, Fuse Ventures and Endeavor Catalyst. Casavo also raised €300m in debt. Casavo started in 2017 in Italy with a Opendoor-like value proposition: making an offer to sellers within 2 days, refurbishing and reselling properties. Casavo grew its userbase 3x in 2021 and is on track to do it again in 2022. Casavo is already present in Spain and Portugal. It’s now opening the French market by acquiring digital broker Proprioo. It’s notable that an Italian startup acquires a French competitor to expand geographically. It’s another proof that the Italian tech ecosystem is maturing with startups raising large rounds and European leadership in their category. - Tech.eu, Techcrunch

Sunday, Oct. 9th: I listened to a Colossus’ podcast episode on Intuit. - Colossus

Intuit is a platform for prosumers and small businesses to manage their financials, pay their taxes and expand their business. It owns TurboTax, Credit Karma, Mailchimp and Quickbooks. It generated $13bn in sales in 2021.

In the US, taxes are filed using a self assistant system. 40% of US individuals fill their taxes without an accountant because it’s cheaper to do so. 30% of them do this with TurboTax which is seen as a solution to withstand an audit and maximize tax refunds. You fill a questionnaire and you pay TurboTax when you submit the tax returns to tax authorities. You only need to pay if you earn above a certain income threshold ($60 in average). It’s a one off yearly expense but the business generates highly recurring revenues because you pay your taxes every year.

QuickBooks is a book-keeping solution for SMBs and self employed (1-10 FTEs). It has a 90% market share in this category making it the de-facto standard. QuickBooks goes beyond accounting and offers products like payroll, invoicing, payments or inventory management. It has 6m customers (75m addressable customers). QuickBooks costs $70 per month.

CreditKarma is used monthly by 38m US consumers to monitor their credit score and see to which financial products they can apply to. It monetizes thanks to lead generation for financial products.

QuickBooks is an open ecosystem with an open API and a wide ecosystem of third party services integrated to Quickbooks (e.g. Square, Stripe, Bill.com, etc.). 40% of QuickBooks’ customers connect another app to QuickBooks.

Intuit acquired Mailchimp for several reasons: (i) many Quickbooks’ customers were hacking the product to use it as a CRM (4bn customer records stored on Quickbooks), (ii) when you start a business you pick a CRM before picking an accounting system which bring new customers quicker into the Intuit’s ecosystem to cross-sell them many products, (iii) Mailchimp has been successful at expanding internationally with 50% of revenues generated outside the US.

Monday, Oct. 10th: I watched a 2017 SaaStr interview with Peter Gassner who is Veeva’s CEO and founder. - SaaStr

Peter Gassner worked at Salesforce between 2002 and 2005 ending up VP of Technology before starting Veeva.

Veeva is building the industry cloud for life sciences. It started in 2007 as a pharmaceutical CRM on top of Salesforce. In 2010, Veeva started a 2nd product called Veeva Vault around content management before launching many more products to serve its customers’ need.

When you launch a 2nd product, it needs to be a product going after a bigger market opportunity than your 1st product and you need to shift your internal organisation from a single product organisation to a multiple products organisation.

Veeva is extremely capital efficient. Before its IPO, it raised $7m but only burned $3m. Veeva was quickly profitable because it signed massive enterprise deals and it charged for professional services.

“Execution matters most. I spend 90% of my time executing. What I’m going to do today, this week, this month, this year? Write down the plan, execute the plan and measure yourself against the plan. Over the long term, any good idea gets copied but execution is enduring. If you want to be great, you have to execute.”

Tuesday, Oct. 11th: Factorial raised a $120m series C at a $1bn valuation led by Atomico with the participation of GIC and past investors Tiger, CRV, K-Fund and Creandum. It’s a massive news for the Spanish ecosystem - Factorial being based in Barcelona. It has 7k customers in Spain, Portugal, France, UK, Germany and Latam. It has grown 200% YoY in the past 3 years. Factorial is a HR platform for SMBs with features including: employee onboarding/off-boarding, payroll, shift and holidays management, performance management, org charts, etc. It will use the funding to invest in product and commercial expansion. - Techcrunch

Wednesday, Oct. 12th: Katana raised a $35m series B led by Northzone with the participation of existing investors Atomico and 42Cap. Founded in 2017 in Estonia, it’s an ERP for manufacturers whose key features are inventory management, master planning, order management and traceability. It’s a cloud-based and open to external apps solution. It will use the funding for product development (apps marketplace, business intelligence, etc.) and recruitment. - Katana, Techcrunch

Thursday, Oct. 13th: I read a blogpost from ModernTreasury on payment operations which is the lifecycle of money movements for a company (e.g. initiating payments, accounting reconciliation, tracking sent & received funds, etc.).. - ModernTreasury 1, Modern Treasury 2

Implementing a payment ops platform has the following benefits: (i) saving money, (ii) delivering a better customer experience, (iii) reducing errors, (iv) spending more time on strategic matters.

On average, companies use 9.5 systems to manage payment ops (ERP, spreadsheets, billing tool, accounting tool, bank portals). 66% of the companies say that the finance team is wasting too much time on payment ops and 36% of companies say that they lose more than 1 work day per week on payment ops.

Friday, Oct. 14th: Instacart self repriced its valuation for the 3rd time to $13bn vs a $39bn valuation at its peak (vs. $24bn after the 1st cut in March and $15bn after the second cut in July). Instacart is trying to go public in the next quarters and needs to present a valuation that will be acceptable to the public market. It’s also a medium to issue stock options plans that are not unrealistically actionable for current and new employees. - The Information

Saturday, Oct. 15th: Talia Goldberg shared great lessons she learnt from his mentor at Bessemer, Jeremy Levine. - Talia Goldberg

“Play the game your way – Bessemer’s model encourages independent thinking and action. This means there is no “Bessemer” way of doing venture capital. Rather, a set of shared values, incentives, and resources, with partners that spike in different ways.”

“Be direct and transparent – even when the message is difficult or unpopular, you deliver it extremely clearly. You are upfront even when it isn’t in your best interest to do so, and you expect the same from others. You don’t oversell. This engenders trust.”

“Make and own mistakes – in an industry built on outliers, studying wins won’t teach you much. It is the mistakes that teach the most.”

Sunday, Oct. 16th: I read two interesting articles on vertical SaaS. - Protocol, Index

Following the success of vertical SaaS in several industries, Salesforce has launched verticalised CRMs integrating industry-specific workflows (e.g. manufacturing, financial services, healthcare, etc.).

“What investors missed is that you can capture significant market share in a vertical much more so than in any horizontal industry. In the CRM space, for example, Salesforce is dominating the market with about 30% market share. But in vertical software you can credibly get to 50% plus market share.” - Talia Goldberg

What are the drivers behind the rise of vertical SaaS? (i) the rise of mobile and cloud to have easy to use and accessible OS for business owners, (ii) the “Amazon effect” which increased consumers expectations, (iii) the rise of embedded finance to add financial revenue streams into vertical SaaS.

Vertical SaaS is an interesting category for the following reasons: (i) mission critical (OS for customer, single source of truth), (ii) bring productivity gains to customers (higher sales, lower costs, time savings), (iii) constantly upselling new products to an existing customer base.

Monday, Oct. 17th: I read an interview from Ben Thompson with Instacart’s CEO Fidji Simo. - Stratechery

“What I discovered when I joined Instacart was an opportunity that was much bigger than just online grocery delivery. What I saw was a massive trillion dollar category of grocery that was going to be disrupted by technology, and the ability to be a company that could become the technology backbone for that entire industry.”

Instacart aims at helping the grocery industry in its digital transformation across both online and in-store innovations.

“The online penetration of the grocery industry had been accelerated by COVID, but was going to continue for a long time. We went from the grocery industry being 3% penetrated online before COVID, to 10% post-COVID, but all of the categories of retail are in the 20 to 30% range. So for us, it’s really about getting on that ten-year journey of continuing to deepen that online penetration, which is something that has a lot of room to grow.”

Instacart started as a three-sided marketplace between retailers, personal shoppers and consumers to enable retailers to have groceries delivered to consumers via personal shoppers who would handle picking up the groceries in the store and deliver them. It expanded by building e-commerce digital operations for retailers which wanted to have their own e-commerce shop (e.g. Sprouts, Costco).

“Our key insight there is that even if we look five years from now, maybe in five years 30% of the industry is online, that still leaves 70% that’s going to be in-store, and customers are expecting more and more of a seamless experience across online and in-store.”

Instacart launched a smart shopping cart. During the week, consumers make their shopping list on Instacart. When they arrive to their grocery store, they scan a QR code and the list appears on the shopping cart. When they drop items in the cart, automatically the item is wrote-off the list thanks to computer vision. You don’t need to check-out and the smart cart will automatically debit your Instacart account.

For Instacart, it was key to be more aligned with retailers to thrive in the long-term. “The fact that Instacart can come to the table and say that we make the exact same amount of money and economics, whether it’s on our marketplace or on a retailer’s website, that makes us a strategic partner for retailers, because they realize that our incentives are entirely aligned with them. We grow our business when they grow their business and that’s very different from the relationships that we would have if we were just a marketplace. That’s really why this retailer enablement vision is so important as a core of who we are, we enable retailers, we don’t compete with them.”

“Advertising is obviously a massive opportunity for Instacart. We see ourselves as a platform by which CPG brands can advertise themselves and really have a platform that combines the best of online advertising — the measurability, the precision, and the targetability. We see the ability to move products off the shelves [in retail stores] and get them in the hands of consumers and when they see an ad.”

“How do we make all this way more affordable? […] Whether it’s bringing the food assistance program online, whether it’s bringing more discount and club retailers online, whether it’s rolling out new benefits for our Instacart plus membership program, new payment options, all of that has contributed to making the service more affordable.”

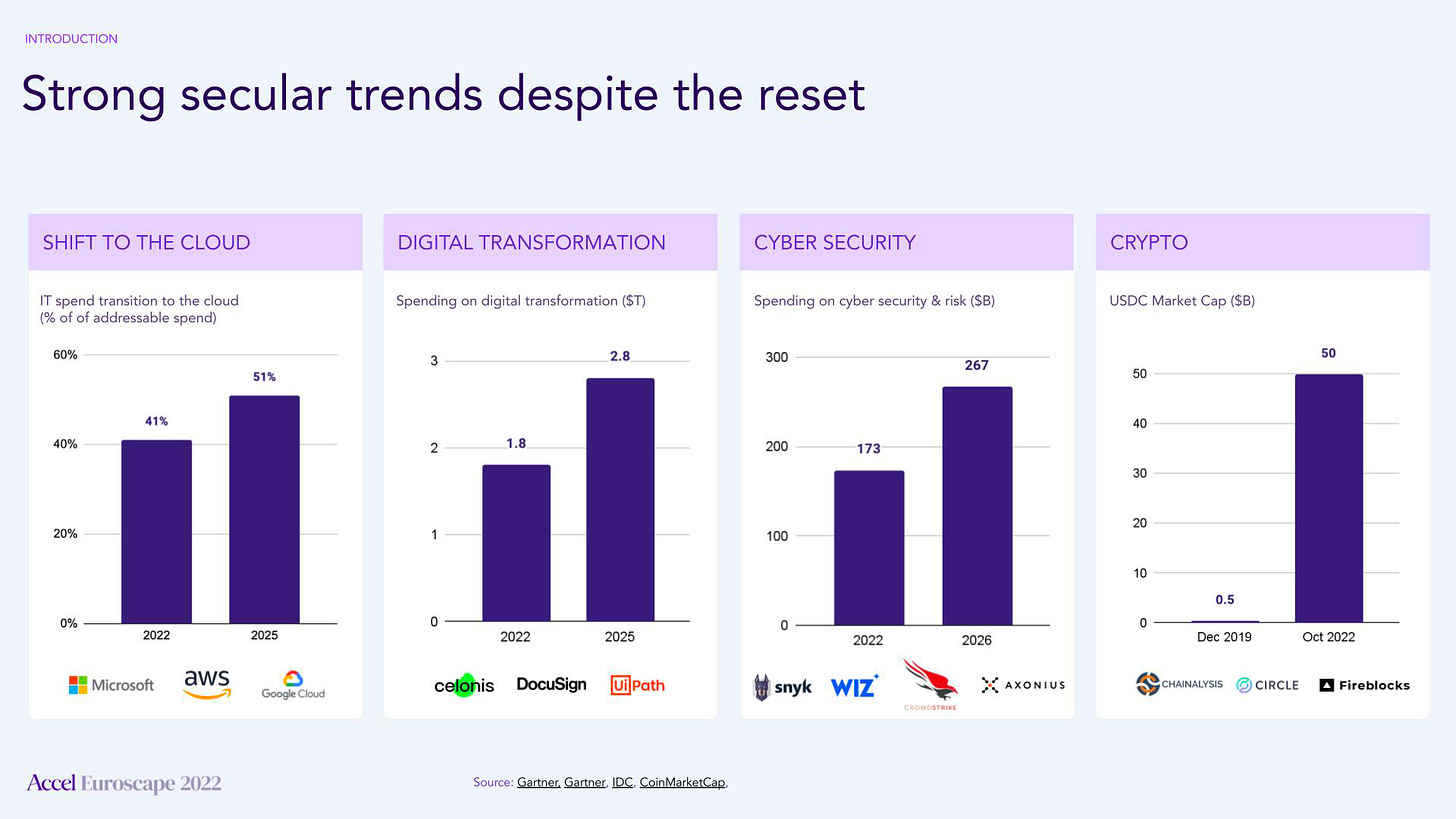

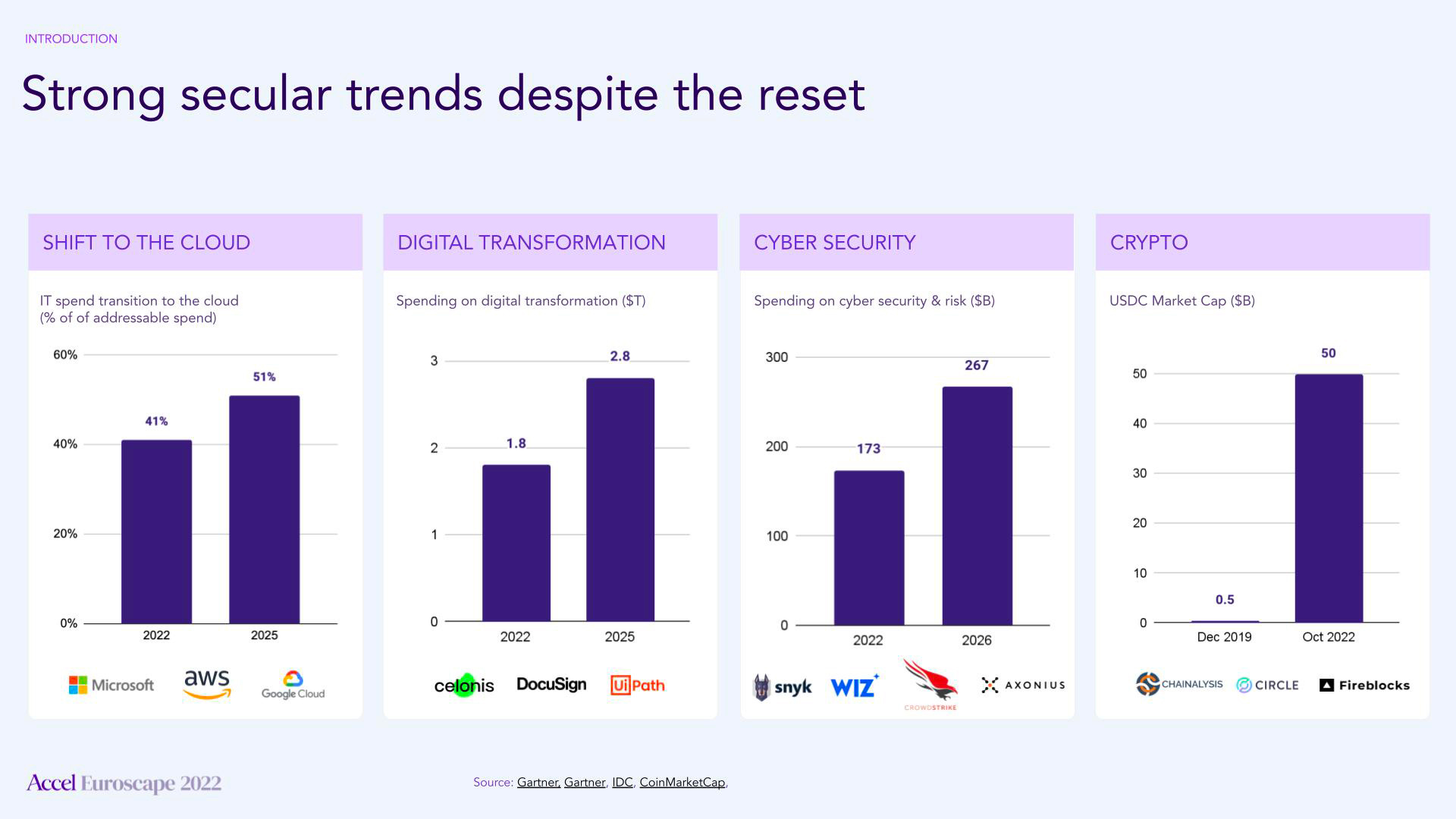

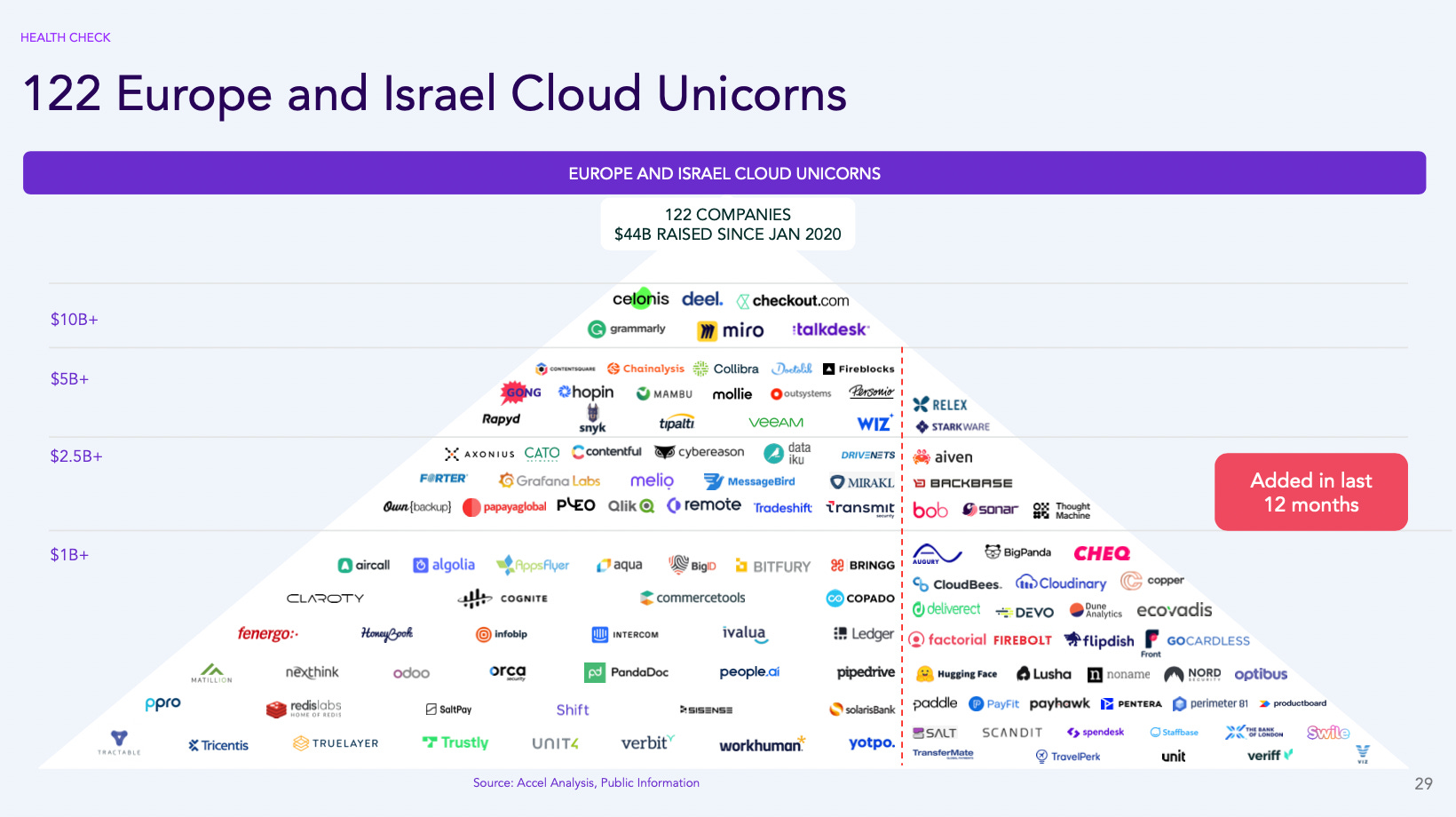

Tuesday, Oct. 18th: I read Accel Euroscape’s 2022 edition. - Accel 1, Accel 2

We’re still at the beginning. In 2022, only 40% of the workloads transitioned to the cloud. It should increase to 51% by 2025.

In Q3-2022, total funding in Europe and Israël decreased by 42% YoY. There is a lag between financings and announcements. In reality, the funding market started to dry up in Q2-2022.

Top 10 highest multiple SaaS companies are trading on average at 15x EV/NTM Revenues, with a 40% NTM Revenue growth and a 14% FCF margin. Companies over the rule of 40 are also trading at 9x EV/NTM Revenues compared to 4x for other companies.

There are 122 unicorns in Europe with c.50% which are generating less than $100m in ARR.

Wednesday, Oct. 19th: We’re delighted to share that Eurazeo co-led a €30m series together with BPI in Paris-based startup Aqemia (💙). Existing investor Elaia also participated. Aqemia creates a modern drug discovery platform based on quantum-based algorithms to accelerate the preselection of molecules which are potential candidates to become drugs. Without Aqemia, pharmaceutical companies and biotechs need to test hundreds of molecules in vitro which is a long and expensive process. Aqemia is using its platform by collaborating with pharmaceutical companies like Sanofi, Janssen and Servier and to build its proprietary drug pipeline with a first focus on oncology and immuno-oncology. - BusinessWire

Thursday, Oct. 20th: I listened to a Colossus’ podcast episode with Lauren Taylor Wolfe on Wyndham Hotels (WH) which is the largest hotel franchisor group with over 9k hotels across 20 brands (inc. Microtel, Super 8, Days Inn, Lakita, Ramada, Wyndham) in 80 countries. - Colossus, EaglePoint

WH has an asset light mode: 97% of hotels are franchised and Wyndham collects a royalty fees on topline revenues, 2 hotels are owned and operated by Wyndham, 300 hotels are owned by third parties but operated by Wyndham.

WH is dominant in the economy space with selective service hotels in which the offering is extremely basic centred around the night-room, the lodging and the breakfast but without any additional services.

A franchise lasts 10-20 years. Franchisees pays (i) a 5.5% royalty on room revenues to use the brand, (i) a 3-4% royalty also on room revenues that the brand will spend on marketing & technology, (ii) an access fee when a loyalty member is coming to the property (it’s worth it because loyalty members stay twice as long and spend twice as much as non loyalty members, WH has 89m loyalty members, the loyalty program is cross-brands). It costs $5m to build an hotel ($3.5m can be funded in debt) and you can renovate an hotel for $25-40k to be compatible with a WH’s budget brand. An hotel generates $1.3-1.5m in annual sales with 40% EBITDA margin (post WH royalty fee) and with a $60k annual royalty fee paid to WH (at 80% margin). For an hotel’s owner and operator, it’s a tradeoff between paying a royalty fees to a brand like WH or being dependent on OTAs for acquisition (70-80% of bookings coming from OTAs which charge a 15-20% commission).

WH’s hotels can be profitable with a 30-40% occupancy rate compared to 50%+ for luxury or upper upscale brands.

To drive top-line growth, WH has 2 main drivers: (i) increasing the number of hotels and (ii) increasing the RevPAR (Revenue Per Available Room). WH has a 94-95% annual hotel retention rate. WH grows its number of hotels by 8% every-year. RevPAR is growing 3-5% every year.

“We generate our earnings from [a] percentage of revenue fees from thousands of hotel owners and our income is not dependent on incentive fees or hotel level profits. We generate substantially all of our EBITDA from hotel franchising activities [and] our margin on non-pass through revenues [is] in excess of 75%.”

“Approximately 80% of the U.S. population live within a ten-mile radius of one of our hotels, and our roadside signs generate more than 500 billion annual drive-by impressions in the United States alone.”

WH is driving 70% of bookings in the US via its central reservation system, 20% via OTAs and 10% via walk-ins.

Friday, Oct. 21st: eFounders wrote a great post on its startup mafia. - eFounders

“The eFounders mafia generated 40 eFounders alumni who founded 46 companies which raised $430m.”

The eFounders is bringing the following unfair advantages to its mafia: (i) a strong network, (ii) the right mindset to build a product iterating continuously, (iii) high execution standards, (iv) finding your next business idea, (v) a consistent and cadenced execution, (vi) an international environment, (vii) ambition.

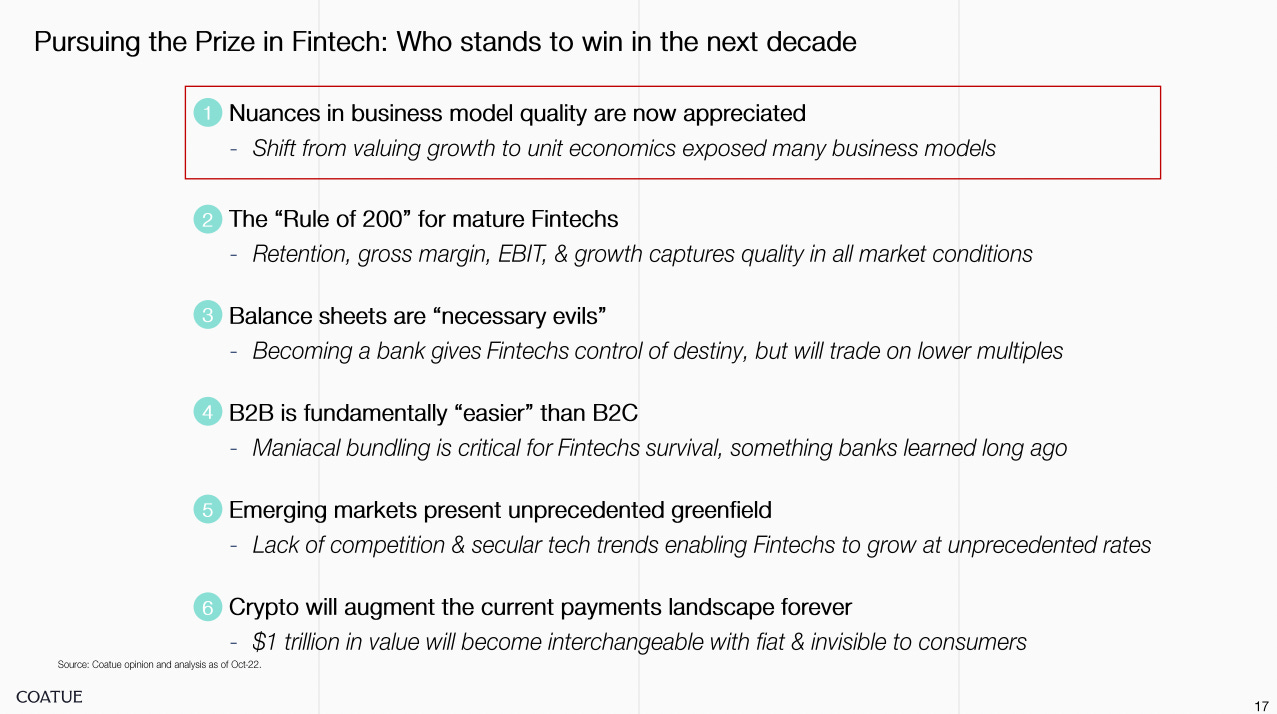

Saturday, Oct. 22nd: Jared Franklin (investor at Costanoa Ventures) wrote about the future of fintechs after the tech market meltdown that we’re currently experimenting. - Jared Franklin

In 2021, the fintech sector reached its popularity peak with (i) many fintechs going public (e.g. Coinbase, Nubank, Robinhood, Toast, Marqeta, etc.), (ii) the fintech unicorns’ count jumping from 75 in 2020 to 167 in 2021 and (iii) large acquisitions (Square buying Afterpay, Intuit buying Credit Karma).

In the 2010s, the rise of fintechs was driven by several factors: (i) the global financial crisis creating a catalyst for innovation, (ii) the combination of new technologies (cloud/mobile), (iii) the rise of fintech infrastructure and (iv) sponsor banks partnering with fintechs.

“But 2021 was an anomaly. It was an end cap on a fun period of fintech becoming cool. Late-stage private market valuations still need to reset, and that ripple effect needs to play out. What was considered cool before won't be as cool going forward. […] Consensus fintech isn't performing.”

Sunday, Oct. 23rd: In H1-22, Apple recorded a 30% Apple Watch’s attach rate to its iPhones. The Apple Watch launched in 2015. It has become a great tool to monitor and improve your health with key features such as sleep tracking, fall detection, ECG generation, blood oxygen saturation detection, body temperature sensing for ovulation tracking, etc. The Apple Watch helps Apple to lock consumers into its ecosystem and to push forward certain key strategic priorities such as selling services and going deeper into the healthcare space. - Counterpoint

Monday, Oct. 24th: Evan Amstrong wrote about the limitations of the current venture capital ecosystem. - Napkin Math

“We have now reached a point in the startup ecosystem where for large VC funds, a startup achieving a billion-dollar outcome is meaningless. To hit a 3-5x return for a fund, a venture partnership is looking to partner with startups that can go public at north of $50bn dollars. In the entire universe of public technology companies, there are only 48 public tech companies that are valued at over $50bn. Simultaneously there are close to 1,000 venture funds all trying to find these select few. This is a huge problem. It is likely that many of the funds deployed over recent years will be some of the worst-performing of all time.”

“Limited partners’ fund managers are generally compensated on a salary basis and are not incentivized to take risky bets. […] Yale, looking to deploy $9.4bn into venture capital, is only going to be putting their money into the Sequoias and Benchmarks of the world.”

“It isn’t just limited partners who are being ill-served by the venture capital product—entrepreneurs are getting hosed too. Since VCs typically only have 20-30 companies per fund, they end up doing a large degree of “pattern recognition” for their portfolio companies, resulting in a small subset of ideas being funded. The people behind these ideas almost always end up looking the same: white, Ivy League, and elite.”

Tuesday, Oct. 25th: Kyle Harrison wrote about hype cycles in the venture industry and the recent hypes (micro-mobility, social audio, NFTs, generative AI). - Investing 101

“The investors who always seem to be adapting their personalities to "the current thing" are taking part in a ritual that is indicative of some of the things that aren't great about venture capital.”

“There is a fine line between being obsessed with investing in the current thing, and the next thing. [Investing in the next thing is] about finding the early inflection points, and being ready with a prepared mind to invest in the things that can most effectively ride those inflections.”

There are 3 characteristics to “independent-mindedness: (1) curiosity, (2) resistance to being told what to think, and (3) fastidiousness about truth.”

Wednesday, Oct. 26th: Spotify published its Q3-22 earnings. Spotify has 456m MAUs (20% YoY growth) and 195m subscribers (13% YoY growth). The company is moving forward in its vision to create an expansive audio platform going beyond music streaming including other formats such as podcasts, audiobooks or audio-related games. - Spotify

Thursday, Oct. 27th: Timothy Motte wrote an insightful piece on Airlift’s failure. Airlift is a Pakistan-based quick-commerce startup started in 2019 which raised c.$100m including a $85m series B co-lead by Harry Stebbings and Josh Buckley before it went bankrupt in July 2022. Airlift started in 2019 in the ride-hailing sector before pivoting into quick-commerce during the pandemic. It grew massively in a national market under-penetrated by digital services and raised a massive series B in Aug. 2021 on the back of this growth. In the following months, everything became harder for Airlift: (i) the funding environment changed especially for emerging markets and capital intensive models, (ii) post-covid, certain consumer purchases shifted back to offline and (iii) the company blitzscale its growth without an appropriate mindset (disconnection between the HQ and warehouses, overpaying employees) and without controlling costs. Timothy argues that this failure helps the ecosystem to move forward: (i) it gathered strong talents on the same project, (ii) it removed the barriers of raising massive capital with international investors, (iii) it cast a light on Pakistan as an eldorado for startups to digitize its economy and (iv) it provided a case-study on mistakes that should not be reproduced going forward. - Realistic Optimist

Friday, Oct. 28th: Marcelo Cortes (CTO and cofounder at Faire) wrote a great post on maintaining engineering velocity as you scale. - Y-Combinator

He has 4 guiding principles: (i) hiring the best engineers, (ii) building solid long term foundations from day 1, (iii) tracking metrics to guide decision making, (iv) keeping teams small and independents.

“What makes this even harder is you often have to play the long game to get the best engineers signed on. Your job is to build a case for why your company is the opportunity for them. We had a few amazing engineers in mind we wanted to hire early on. I spent over a year doing coffee meetings with some of them. I used these meetings to get advice, but more importantly I was always giving them updates on our progress, vision, fundraising, and product releases. That created FOMO which eventually got them so excited about what was happening at Faire that they signed up for the ride.”

Faire organised its engineering team with a pod structure “to ensure that every team was able to operate independently but with all the context and resources they needed.” Faire had certain interesting guidelines for its pods: (i) pods operate like small startups, (ii) each pod should have no more than 8-10 employees (5-7 engineers, 1 PM, 1 designer and 1 data-scientist), (iii) “if you only have one product, assign a pod to each well-defined part of the product.”

Saturday, Oct. 29: McKinsey published a paper highlighting common success factors behind startups valued over $1bn. It highlights 5 characteristics: (i) is the team experienced and complementary? (ii) is the market large enough? (iii) is there a strong market momentum? (iv) does the technology work at scale? (v) does the business has a sustainable traction (i.e. found PMF, scale rapidly and have a path to profitable unit economics)? - McKinsey

Sunday, Oct. 30th: Coatue released a white paper on the future of fintechs. - Coatue

Monday, Oct. 31st: Brad Stone wrote an amazing post on GoPuff’s rise and current fall. - Bloomberg

“Gopuff had an Amazon-like approach of storing and stocking products in its own mini warehouses staffed by full-time employees, then using contractors to deliver products to people’s doorstep for $1.95 an order.”

“Its founders, Ilishayev and Yakir Gola, each now 29, got to know each other when they were undergrads at Drexel University, where they started an online business selling hookahs and other smoking paraphernalia to other college kids (early slogan: “Puffin’ has never been this easy”). It wasn’t until 2015 that they entered the booze business, charging an additional $2 fee per order for alcohol, and gradually expanded their assortment and ambition.”

“In recent months it’s laid off almost 2,000 employees, withdrawn from parts of Europe, shelved grandiose plans for new categories, raised fees on customers, and halted a planned initial public offering as its valuation has plummeted.”

“There were a few problems with this. Customers tended to exploit free shipping to make relatively small purchases—say, cookie dough ice cream and a pack of smokes—which wasn’t enough for the company to recoup delivery costs. But the fatal flaw, then and now, was the belief that an online delivery service could command the same veneration and stock multiples of purer technology companies”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Great post.

👏👏