📖 Venture Chronicles - November 2024

Overlooked #188

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of November.

Friday, Nov. 1st: French fintech Qonto is exploring a €200m secondary share sale at a €5bn to provide liquidity for employees and early investors. In 2022, Qonto previously raised at a €4.4bn valuation. Founded in 2016, Qonto offers financial services for 500k SMEs in France, Spain, Italy and Germany. It has recently expanded to new markets like Austria and Portugal. - FT

Saturday, Nov. 2nd: Yoni Rechtman at Slow wrote about moats for startups. - Yoni Rechtman

“Moats are important. Economic moats drive long term margins and profits for any business that gets big enough to attract jealousy and competition. Startups don't have moats. If they did they wouldn't be able to start up in the first place (with very few exceptions in extremely technical or regulated industries). But every founder should be thinking about the eventual moat from inception.”

Here are key questions to ask around moats: (i) when will your moat kick in? (ii) how much of a moat will you have/how strong will it be? (iii) what kind kind of moat will you have and could you even have more than one?

The main moats for startups are the following:

“Network effects or demand side economies of scale. The service gets better with more users. These can be stronger/global (Facebook) or weaker/local (Uber). Sometimes this is derived from unique data, sometimes from connectivity, sometimes from

Economies of scale. You get better pricing with size (Walmart) and/or can amortize capital investments over a big base that others can't (Buffet's OG local newspaper thesis). The other side of network effects

Regulatory. The government has picked you as a winner either explicitly (Boeing, x-Vegas casinos) or implicitly (any licensed FI)

Intellectual property. You have strong patents (biotech) or it's just near-impossible to replicate your technology (TSMC).

Brand. A close cousin of IP moats. People just love you for ineffable even if irrefutable reasons (McDonald's, Coke).”

Sunday, Nov. 3rd: Top financial institutions, including Blackstone and BlackRock, have lent over $11bn to neocloud companies (including CoreWeave and Lambda Labs) to enable them to buy more Nvidia’s GPUs and using these same GPUs as collateral. Several risks are associated with these loans including: (i) risk that GPUs are assets that depreciate at a faster rate than initially planned, (ii) risk that Nvidia’s chips started to be commoditised with the arrival of new entrants, (iii) risk that there is an oversupply of GPUs when the leasing contracts expiring lowering their resale value. - FT

“CoreWeave, the largest neocloud company, began amassing chips when it launched in 2017 to mine cryptocurrency but pivoted to AI two years later. The company now claims to be the largest private operator of Nvidia GPUs in North America, with more than 45,000 chips.”

“CoreWeave has raised more than $10bn in debt in the past 12 months from lenders including Blackstone, Carlyle and Illinois-based hedge fund Magnetar Capital. It announced a further $650mn credit line from Wall Street banks including JPMorgan, Goldman Sachs and Morgan Stanley this month.”

“The financing means CoreWeave is highly leveraged. When it announced its first $2.3bn debt financing in August 2023, which included about $1bn of loans from Blackstone, it had annual revenues of just $25mn and negative EBITDA of roughly $8mn, said two people close to the company. Revenues have since surged to about $2bn this year, one of the people said.”

“Some of CoreWeave’s largest lenders were persuaded to invest because of a large contract it had negotiated with Microsoft — the biggest backer of OpenAI — last year that would generate revenue of more than $1bn over several years, said several people with knowledge of the deal.”

Monday, Nov. 4th: I listened to Bill Gurley, Brad Gerstner and Jamin Ball discussing the excesses of the current venture market. - BG2

“The venture markets have transitioned from a high margin cottage industry to a institutionalised lower margin industry. That has a lot of implications for LPs, GPs and founders.”

“10-15 years ago, the funds were smaller and as a GP as an investor you'll make money on that guaranteed portion but not necessarily right as I called it get rich money. If you wanted to get rich you had to maximize your carry maxising the value of the underlying investments that you made. The incentives were aligned between founders and GPs.”

“Today, funds are much bigger and the 2% guaranteed portion of the compensation is enough to get rich as a GP.” “There's a path tog get rich for GPs where the outcome of the founders in their companies is irrelevant.”

“Large funds incentives are more about deploying dollars quickly as opposed to maximizing the value of those deployed dollars.”

“It leads to companies showing early traction to get flooded with investment dollars.”

“For founders there are implicit things you are signing up for by taking too much money at too high of valuation (e.g. not being able to sell the business for $100-200m and make significant money as a founder because of your preference stack).”

If you raise money, you will spend it. The money will not stay in the bank account and you spend that capital in a non optimal way. Constraints drive creativity.

“If you want to get maximum dollars deployed in a business, there may be only so many primary dollars you can get and so we started to see this desire to buy secondary shares - leading to founding teams taking big dollar off the table.”

“Out of the 1,400 private unicorns, 90% are going to have a down round to get through the system. The echoes of that 2020-2021 period have not reverberated that loud today.” “I'm seeing activity that is at at at at least no different than what we saw in the past.”

“You create a prisoners dilemma with your competitors where they feel forced to raise the same amount of money and now you have multiple overfunded companies in a single category. Capital is used as a weapon of economic destruction. You have excess capital causing excess competition and the natural market winner does not emerge as fast as they otherwise would.”

“Valuations represent discounted future expectations. If you raise at a massive valuation, it means that you increase everyone's expectation for what this company can achieve in the future.”

“The number of first time funds raising a second time fund has plummeted and the number of first time funds have plummeted. What's happening is you have the consolidation among a few big platforms like General Catalyst or Lightspeed.”

“The window for which you would evaluate whether someone can accurately or successfully deploy a multi billion fund might be 20 year. It’s beyond the lifetime of most GP’s career left to be done.”

“If you're investing just in growth stage there's only so many companies you can invest in that can give you power low outcomes. You are almost inherently widening the aperture to do more than what could be a power law outcome the larger you get.”

Tuesday, Nov. 5th: The Financial Times wrote about the AI impact in healthcare with multiple applications including imaging-based diagnostics, treatment personalisation, back-office automations as well as communication between patients and doctors. - FT

“Few industries are more ripe for creative disruption than healthcare, which consumes huge sums of public and private funding while still battling to meet demand from growing and ageing populations around the world.”

AI enhances diagnostic accuracy and consistency in medical imaging.

Potential exists for AI to minimize diagnostic errors and missed diseases.

AI aids in personalizing treatment and reducing patient risks.

Automation in healthcare administration is an untapped area for AI innovation.

Wednesday, Nov. 6th: Bloomberg wrote about Italy-based consumer mobile apps roll-up Bending Spoons. In 2024, it will generate $700m in sales from 200m monthly active users. - Bloomberg

“Since buying Evernote last year, Bending Spoons has snapped up five other companies. That includes Dutch file-sharing service WeTransfer, which had shelved plan for an initial public offering that would’ve valued the company at €716m just a couple of years before its sale, and the assets of Meetup, a bankrupt events-listing business that briefly belonged to WeWork.”

In 2024, it failed to acquire Vimeo when it had a $690m market capitalisation.

Bending Spoons purchases “distressed businesses with a steady cash flow that sell subscription software. Then it brings in twenty-something coders and data scientists in Italy who add features and sometimes push the limits of what subscribers will pay.”

“Investors compare Bending Spoons to Constellation Software, which sells to an assortment of businesses including car dealerships and spas, and Barry Diller’s IAC.”

“When we acquire these companies, we do so to own them forever. We’ve never sold one. When you own something forever, there is a very big incentive to think long term.”

Thursday, Nov. 7th: Toast reported its Q3-2024’s earnings. - Toast

In the quarter, Toast added 7k net locations (127k locations in total, 28% YoY growth), reached $1.6bn in ARR (growing 28% YoY) and $113m in EBITDA.

“This fall we launched new products like Branded Mobile App and SMS Marketing.”

“28% of restaurant owners hope to open a new location over the next 12 months.”

40% of restaurants are very likely to add AI to their operations “selecting options including optimizing menu performance, making recommendations for guests, benchmarking their business performance against their peers, and optimizing pricing.”

“Over the 3 years, we've more than doubled our market share in the US, including recently signed mid-market brands, Metro Diner, Giordano's Pizza and Earl Corporation. We're still only at 14% penetration.”

Friday, Nov. 8th: Battery published its 2024 State of the OpenCloud. - Battery

AI is driving a shift to “services-as-software” as a business model, automating human tasks and emphasizing value-based pricing.

Public cloud providers (AWS, Azure, GCP) have seen a boost in revenue growth driven by AI.

Software companies have seen a stabilization in SaaS multiples around 7.5x EV/NTM Revenues on average and 12.7x for top quartile companies.

Private companies command higher ARR multiples than public ones, with a premium of 3.2x in 2024 YTD (23.4x EV/ARR vs. 7.3x EV/ARR), driven by expectations of growth and AI-related returns.

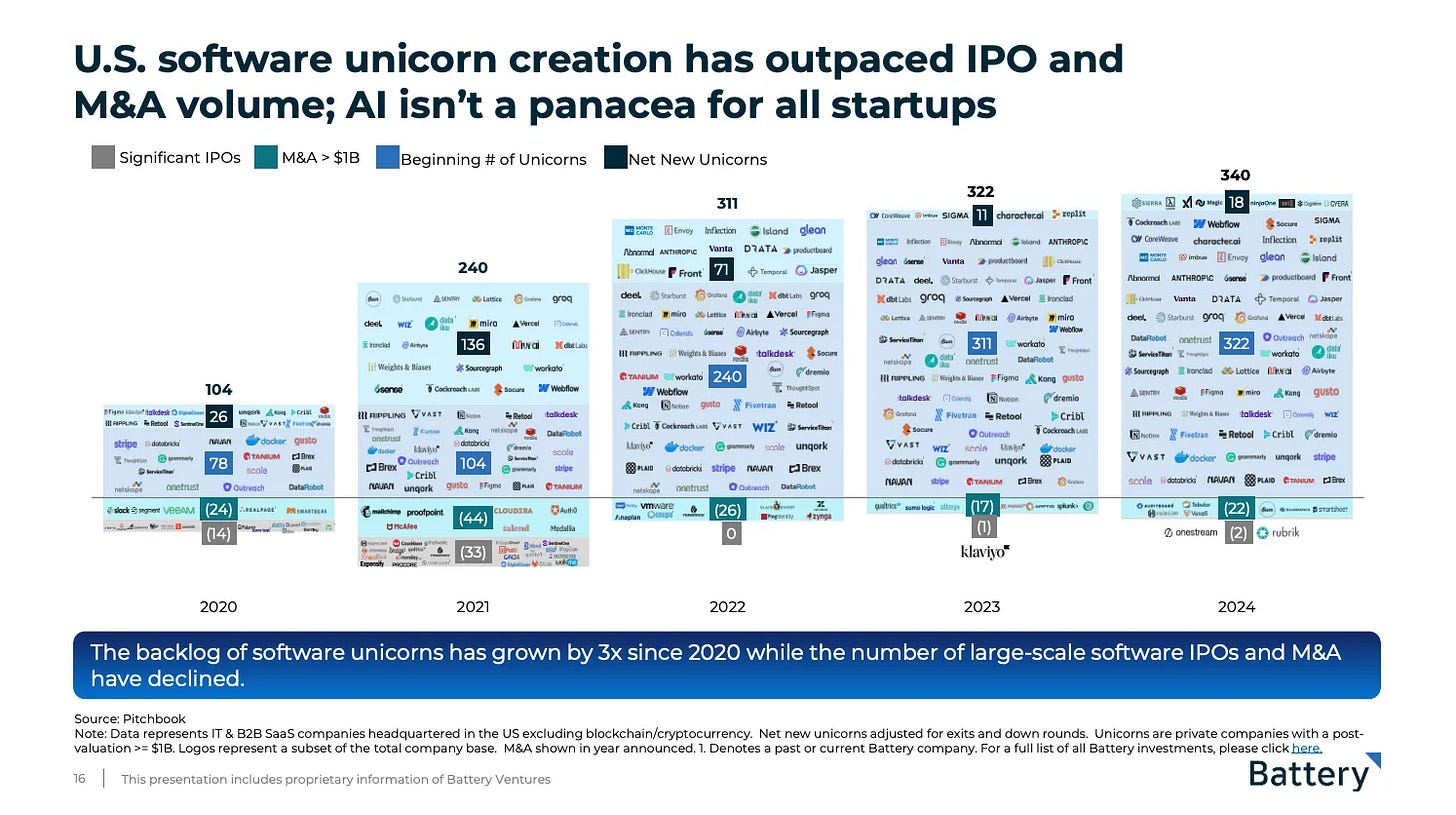

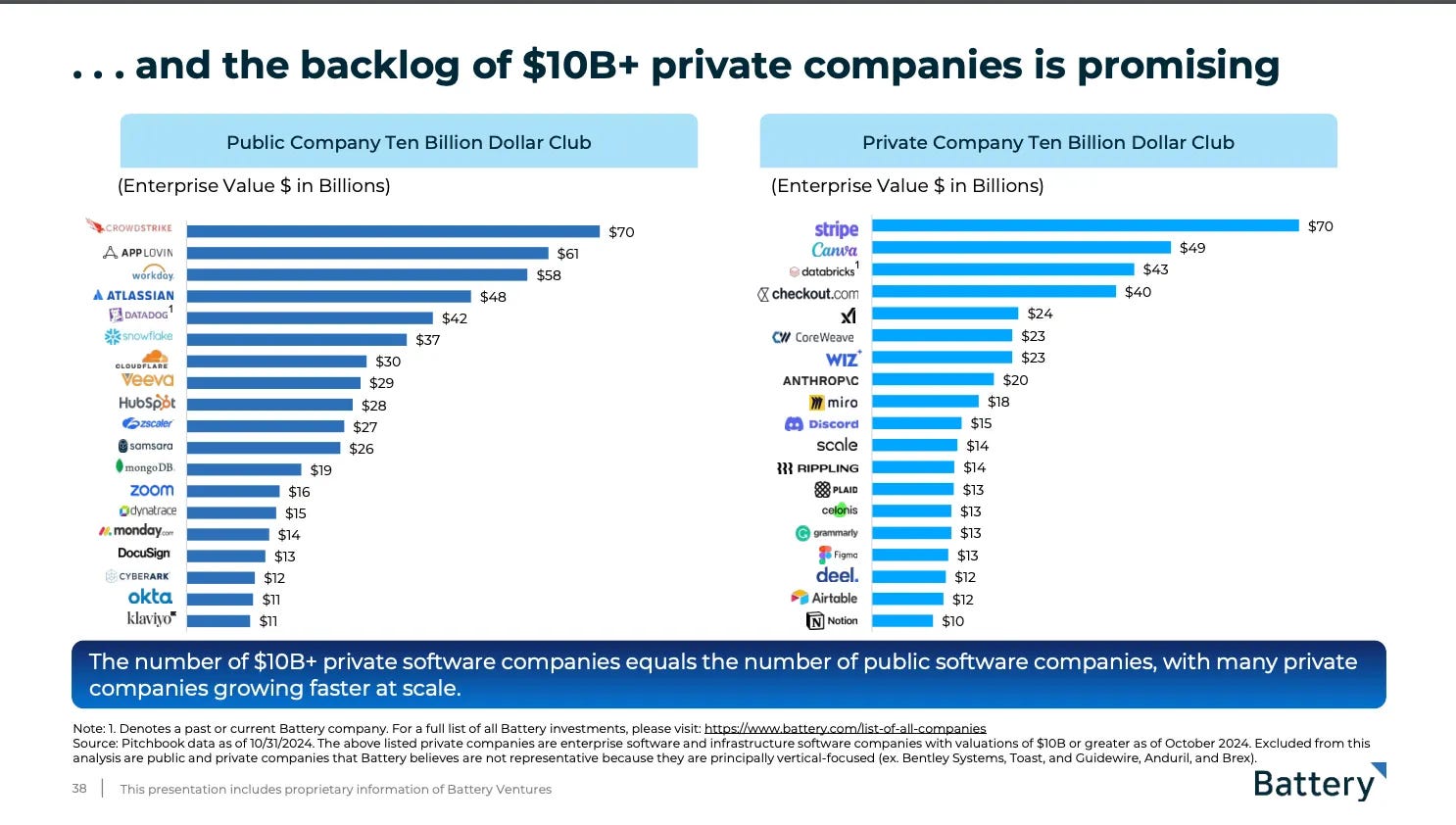

The creation of U.S. software unicorns has significantly outpaced IPO and M&A activity, with a backlog that has grown threefold since 2020. The number of unicorns increased from 104 in 2020 to 340 in 2024, while large-scale IPOs and M&As have declined.

Saturday, Nov. 9th: Yelp is going deeper into the auto vertical by acquiring a car repair estimates platform for consumers called RepairPal for $80m in cash. RepairPal helps 3.8k car repair shops to generate more leads from consumers looking to repair their cars. It generates $30m in sales and is breakeven. RepairPal . - Techcrunch

Sunday, Nov. 10th: Tara Seshan (ex. Stripe and Watershed) wrote on the graveyard of no-code and low-code (LCNC) platforms. - Tara Seshan

“None of the LCNC companies has been a breakout success.”

“However, there is some reason to be optimistic: public market competitors like Palantir, Microsoft’s PowerApps, and SFDC’s Force.com and Lightning Platform are doing well, and have specifically called out their LCNC tools as a part of their AI success stories”

“Great custom software is a competitive advantage. If the user-facing products set the current revenue run-rate potential, internal software sets the speed limit on improvements.”

“The “LCNC as feature” companies are more successful than the “LCNC as the whole product” companies.”

“I think there are two types of “tool builders” that can become $10B+ companies:

A very vertical specific tool builder (“Retool for trucking”) that can be deeply opinionated about the space.

A tool builder as a feature of a broader functional-specific platform that differentiates based on user experience and flexibility.”

“The vertical specific tool builder can command a higher price than the more domain agnostic tools. This is because it can come in with a very specific set of problems that it already solves, extremely tailored to the company in question.”

Monday, Nov. 11th: : Logan Bartlett interviewed Verkada's co-founder and CEO, Philip Kalazan. - Logan Bartlett

Verkada faced challenges in securing early funding due to its hardware component. “We went to every firm on Sand Hill Road and the hardware component throws people off. At the time, everyone only wanted to invest in pure SaaS models.”

Verkada prioritizes hiring individuals with a deep passion for building and problem-solving, even if they lack prior industry expertise. “We would rather hire the top knife salesman than a good software salesman. You'd rather teach someone amazing selling how to sell physical security software.”

Verkada's initial focus was on revolutionizing the video security market by leveraging cloud technology. “Cameras were getting pretty good and inexpensive to build a modern software-driven cameras solution.”

Verkada adopted a channel sales strategy from the outset, partnering with integrators to reach customers and scale its business. “As integrators have access to a lot of the market, we decided to play nice with them by making our product compatible with that selling motion.”

Verkada's product expansion strategy was driven by customer demand for integration with other building systems. As customers embraced Verkada's camera system, they sought to connect it with their existing access control, alarm, and other building management systems. “Customers were loving ou software solution that came with the camera so much that they wanted to integrate it with more of their building (e.g. alarm system, door access control system).”

Tuesday, Nov. 12th: I read Rail Vision’s 20F and investor presentation. - Rail Vision 1, Rail Vision 2

It was created in Apr. 2016. It raised $78m in total since inception including capital from Knorr-Bremse. It has (i) a $1.4m contract with Israel Railways for 10 systems, (ii) a $500k contract with a Latin America mining company and a (iii) up to $5m contract with a US rail & leasing company. It competes with Bosch, Alstom, Siemens and Toshiba.

“Autonomous trains are integrated with advanced systems to provide improved control over the train for stopping, departing and movement between train stations.”

“Autonomous trains, also known as driverless trains, are operated automatically without any human intervention, and are monitored from the control station when communication is available. In case of any obstacle incurred in the route, the obstacle detection system commands the train to stop and in parallel a message is sent to operational control center and to the attendant on the train if any, to further command the train.”

“We have developed unique railway detection systems for railway safety, based on image processing and deep leaning technologies that provide early warnings to train driver of hazards on and around the railway track, including during severe weather and in all lighting conditions.”

“Due to the braking distance required for a train to stop, train operators require advanced notice to stop a train in time and avoid an obstacle on the track. The braking distance of a passenger train traveling at a moderate speed (i.e., 87 mi/h) is between 600 and 800 meters; freight trains typically require a similar distance to safely brake – depending on the load size and speed of the train. Human operators, however, do not have the capacity to detect obstructions on the railway track, and halt a train within these braking distances. Our advanced technology is designed to address this human deficiency.”

Wednesday, Nov. 13th: Joe Lonsdale wrote on how AI companies disrupting services companies can leverage the Palantir’s playbook. - 8VC

“Unlike most software businesses, many Palantir’s engineers spent significant time working alongside our customers.”

“We iterated and extended our platform alongside our customers, improving their mission effectiveness by understanding their needs, and improving our products by abstracting those needs into universal components we could then apply to other problems. We ‘productized’ our services.”

“What’s been consistent throughout is that services have supported product revenue, not vice versa.”

“When serving the world’s most complex organizations, a special operations “services” mentality is what lets you build complete solutions that, in the end, are worth more to your customers than out-of-the-box products.”

“At 8VC, we’re seeing extraordinary results from integrating AI with best-in-class operations to transform the economics and scalability of B2B service industries.” “These startups have a similar offering to incumbent competitors, but use AI and a vertically-integrated technology stack to drive much higher margins and deliver unrecognizably better service (faster / cheaper / 24-7).”

“The best tech-services companies use technology to drive operating leverage in two ways: (i) create a unique value proposition with faster, cheaper, and better service quality than legacy providers, (ii) improve unit economics by removing big chunks of labor from COGS; both altering the margin structure and making the business easier to scale relative to incumbent competitors.”

“Buying an incumbent can help solve the “cold start” problem for companies operating in markets with high regulatory barriers or switching costs, and a relative lack of differentiation between service vendors. Reducing hiring and sales pressures can allow startups to focus on validating tech-driven margin improvements in the early phase of company building.”

Thursday, Nov. 14th: Vinod Khosla wrote about hiring in startups arguing that talent density is key in startup success. In the early days, founders should focus on hiring for value creation roles with people who are ambitious, risk taking and comfortable with ambiguity. - Vinod Khosla

“Candidates for value creation need to have a record of taking an idea from inception to successful execution, even if unrelated to the role.”

“Startups are born with zero value. Executives need to take big swings and big risks to disproportionately create and increase their company’s value. For a value creation role, you want an ambitious risk taker. The best candidates you interview will not need to have had this role previously in their career, but is used to ambiguity, a balance between focus and defocused exploration, risk taking. Learning on the job is ok and first principles, instead of experience based thinking, is critical.”

“However, after your Series B/C, you now have a business with real customers at a decent scale. The CFO of a later stage company is typically looking to protect the value that has been created. The company is now worth something.You want them taking measured risk.”

“The questions in a value creation interview should focus on understanding if they’ve implemented important initiatives at prior roles, and focus less on whether their prior experience lines up with this role. Smarts, first principles thinking, and creativity become more important than experience. But team building and leadership almost always trumps most other skills, especially in a CEO.”

“My bias is to find someone who hasn’t spent too much time in the industry to which the startup belongs.”

“Prioritize finding someone who is the absolute best team builder and a good leader.”

“When considering a startup exec, the most crucial factors for me are their quality of thinking and their ability to grow rapidly.”

Friday, Nov. 15th: Creating “businesses in a box” for skilled trades can empower technicians to become entrepreneurs, combining brand, software, training, and support. This approach promotes wealth-building without commodifying labor. By encouraging independence and aligning incentives, it fosters stable, profitable ventures for tradespeople and helps them avoid the pitfalls of PE-owned rollups. - Yoni Rechtman

“If you put together demand gen. (brand, marketplace, marketing, etc.) + operating capacity (software, capital, etc.) + services and support (training, accounting, etc.) you reconstitute the franchise value proposition.”

“Biz in a box for trades makes it possible for a technician to become an entrepreneur with little/no skills but the technical ones.” “You'll earn much higher take rates and much more stably than any of SaaS, services, or marketplace on their own.”

Saturday, Nov. 16th: Klarna has confidentially filed for a US IPO, which could value it between $15bn and $20bn, marking a shift after its 2021 $46bn peak valuation. Despite governance tensions, the fintech has narrowed losses, focused on U.S. expansion, and embraced AI for cost-cutting. - FT

“Klarna has been on a rollercoaster ride since it was valued at $46bn in a 2021 deal that made it Europe’s most valuable start-up. It was then valued at $6.7bn during its last official fundraising round in 2022, as investors sharply re-rated fintech companies in response to rising interest rates.”

“Although widely anticipated, Klarna’s choice of the US for its IPO is a blow for Europe’s capital markets, and follows a similar decision from compatriot Spotify to choose New York for its listing in 2018.”

The company has implemented cost-cutting measures, including workforce reductions and the use of artificial intelligence to improve efficiency. These steps have contributed to narrowing losses and moving toward profitability.

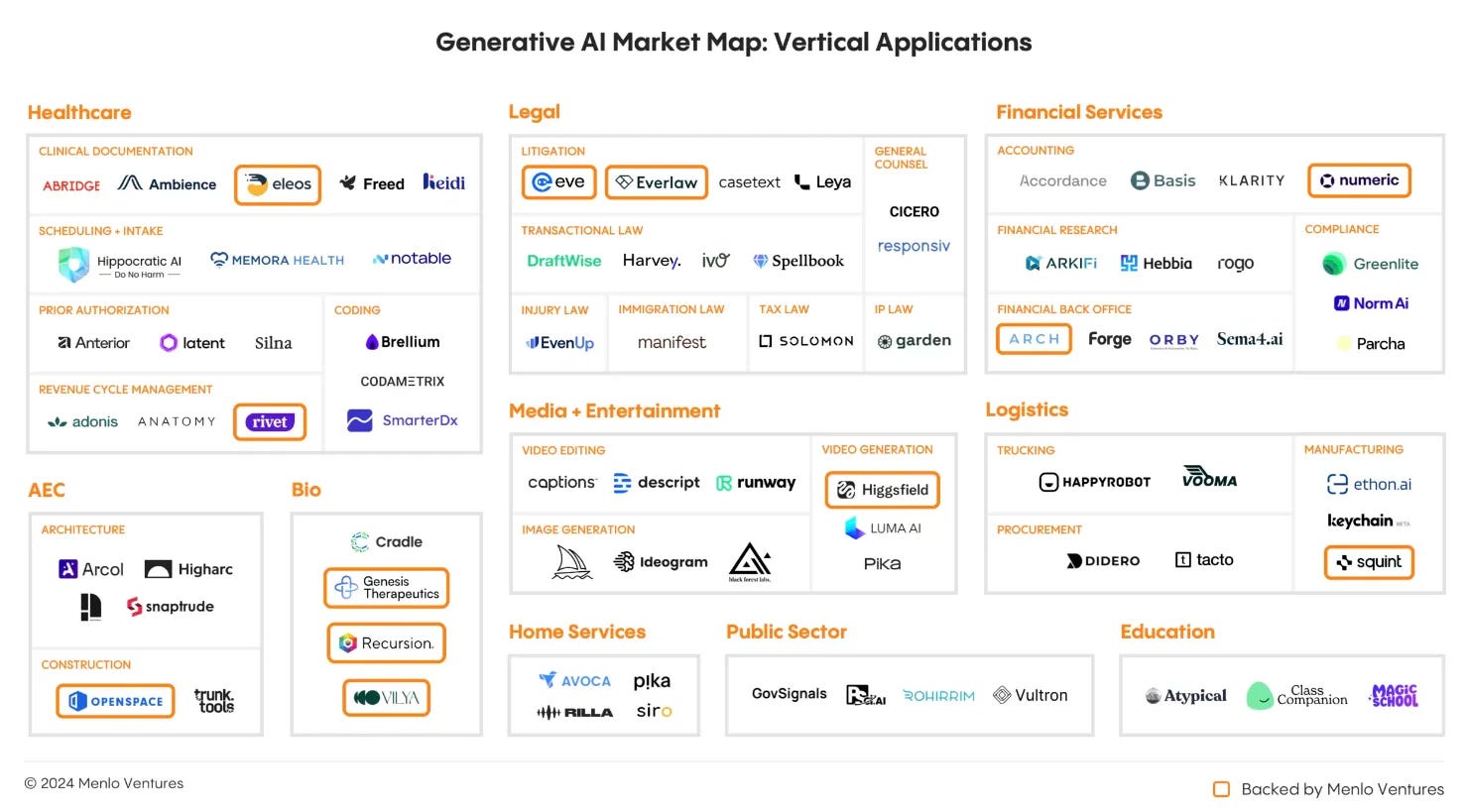

Sunday, Nov. 17th: Pete Flint at NFX wrote about the AI impact on vertical SaaS. - NFX

“AI is about to make the vertical SaaS pool 10x deeper.”

“Many horizontal B2B SaaS companies are vulnerable to unbundling right now. With a great UX, powerful vertical specific features and AI that significantly cuts cost or delivers exceptional value, startups may be able to complement or displace legacy systems.”

“AI empowered vertical companies are going to unbundle and dominate compared to horizontal SaaS.”

“The cost of building software has become significantly cheaper, particularly for features that are well understood and established.””

“AI excels in all the ways that horizontal ERPs are weak. It delivers uniqueness at scale: instant, customizable solutions for every business/person. It performs even better in a pool of industry-specific documentation and unique data.”

“We may see an “unbundling” of major B2B SaaS categories, like ERPs, or CRMs, by verticalized, AI-powered solutions.”

“Large, horizontal companies may have more data in general. But they’re unlikely to have the highest quality, contextual data that truly delivers insights to each specific vertical.”

“Software led rollup: rather than trying to sell a new approach from scratch, buy the distribution, then infuse technology from there.”

Monday, Nov. 18th: Klarna published its Q3-2024 financial results. - Klarna

“Since launching Klarna balance and cashback in 12 markets just three months ago, we've seen strong adoption, with 1.6m consumers actively using Klarna balance and over 1m consumers collectively earning $5m in cashback rewards.”

“Currently, over 1,000 merchants are running active cashback offers, achieving sales increases of up to 30% for participating brands. This has contributed $200m in GMV and fueled growth in Klarna’s affiliate revenue. Brands like Walmart are among those leveraging cashback to enhance customer engagement and boost sales.”

Year to date, Klarna’s revenue increased by 23% to $1.85bn compared to the previous year. It also achieved an adjusted operating profit of $142m for the first nine months of 2024 implying a 7.7% operating margin of 7.7%.

Tuesday, Nov. 19th: Francis Santora wrote about entry prices in venture. - Francis Santora

“Since one company will probably provide most of the returns, I want every investment to be able to return the fund. Think of it like shooting a target. If a bet can’t return the fund, I just wasted a precious bullet.”

“So far this year, my average entry price has been $11.6 million post-money. A 70x on that is much easier to underwrite to. I don’t even need an investment to be a unicorn. $800 million will do me just fine. Don’t get me wrong, getting to a $800 million valuation is extremely difficult. But it’s a whole lot easier than hitting $35 billion.”

Wednesday, Nov. 20th: Nabeel Qureshi shared valuable insights on startup sales in a post, drawing from his experience as the first salesperson at GoCardless. - Nabeel Qureshi

“Your job is not to sell, your job is qualification. The actual “selling” process goes extremely smoothly if you’ve qualified the person correctly.”

“The #1 rule of doing a sales call is: be quiet. You should aim to be talking for about 20% of the time, with your customer talking about 80%. If you didn’t get this ratio, it wasn’t a good sales call. Sales is fundamentally about listening, not about talking.”

“Not only should you have a structure laid out in front of you on a notepad/paper, butyou need to lay this structure out verbally from the outset. The structure we used was: (i) introductions, (ii) current process, (iii) pain points & Ideal solution / requirements, (iv) your solution and (v) next steps & timeline.”

“Always follow up same-day. No excuses. Do not leave your follow-ups till tomorrow. Just get it done then and there, it shows you’re on top of things and the signalling value is super important, plus lags are the death of sales so you always want to take care of your end of things as quickly as is humanly possible.”

Thursday, Nov. 21st: Odoo raised €500m in a secondary round at €5bn valuation led by Sequoia and Capital G who acquired shares from existing investors Summit Partners, Noshaq, and Wallonie Entreprendre. Odoo is a Belgium-based open source ERP. It has 13m users and adds 7k new customers per month. It is growing 40% YoY while being profitable. It aims to generate €650m in billings in the next 12 months and €1bn in 2027. It has 80 proprietary apps (accounting, CRM, manufacturing & marketing) and an app store with 50k apps developed by its ecosystem of developers and partners. - Techcrunch

“ERPs are traditionally expensive and resource-intensive to implement, often failing to meet the actual needs and evolving requirements of SMEs.We have developed a unique value proposition that is playing a pivotal role in the market.” - Fabien Pinckaers (founder & CEO at Odoo)

Friday, Nov. 22nd: Menlo published a report on the adoption of Gen. AI within enterprise companies. - Menlo

“AI spending surged to $13.8bn this year, more than 6x the $2.3bn spent in 2023—a clear signal that enterprises are shifting from experimentation to execution, embedding AI at the core of their business strategies.”

“When deciding to build or buy, companies reveal a near-even split: 47% of solutions are developed in-house, while 53% are sourced from vendors. This is a noticeable shift from 2023, when we reported that 80% of enterprises relied on third-party generative AI software—indicating an increasing confidence and ability for many enterprises to stand up their own internal AI tools rather than rely primarily on external vendors.”

“Rather than relying on a single provider, enterprises have adopted a pragmatic, multi-model approach. Our research shows organizations typically deploy three or more foundation models in their AI stacks, routing to different models depending on the use case or results.”

Saturday, Nov. 23rd: The FT wrote a portrait on Thrive Capital. - FT

“As OpenAI raced to raise almost $7bn last month, one investor was always on hand. Thrive Capital stayed close to the AI start-up’s co-founder and chief executive Sam Altman and contributed over $1bn to a funding round that valued the artificial intelligence group at $150bn.”

“It also typifies the approach Kushner has developed since launching Thrive 14 years ago: get close to founders, remain loyal through crises and concentrate funds in a small number of companies.”

“Thrive is attempting to manage both, writing cheques for multibillion-dollar start-ups its team believe can still multiply 10 or 100-fold in value.”

““They are trying to prove you can have a $5bn fund and be a boutique,” says the managing partner of another New York venture firm.”

“Kushner launched Thrive in 2010 when he was a student at Harvard Business School and raised a first fund from institutions in 2011.”

“That was followed a year later by an investment in Instagram which put Thrive on the map. The firm doubled its money inside a week, when Facebook swooped for Instagram in a $1bn deal. Kushner also launched health insurance start-up Oscar Health in 2012. The company went public at close to $8bn in 2021, though its market capitalisation is roughly half that today.”

“Venture at scale is not new: Andreessen coined it,” says the New York-based rival. “But Andreessen has become [luxury conglomerate] LVMH while Thrive is trying to prove they can be Chanel.”

“Loyalty to founders is one reason Thrive has continued writing cheques for companies that have grown to a scale most VCs would balk at, and why it is willing to stay invested much longer than the typical decade or so.”

“Most VCs split funds between dozens of start-ups, but the vast majority of a Thrive fund will go to just 10-15. The firm has put 10 per cent or more of earlier funds to work in single companies, including workplace messaging app Slack, GitHub, Instagram and Stripe.”

“The firm has “become the master of the secondary market.” “Thrive has built its stakes in companies including Stripe, OpenAI and GitHub by buying up employee shares. The firm is currently buying $1bn in stock from employees at data intelligence firm Databricks.”

“Diversification is for people that don’t know what they’re doing. Investors are paid to know what they’re doing.”

Sunday, Nov. 24th: The Economist wrote on Sequoia’s challenges to constantly remain one of the best performing venture firms. - The Economist

“In contrast to some other VC old growths like Kleiner Perkins, whose reputation for spotting the next hot startup has wilted in the past decade, it has managed to thrive more or less continuously for half a century.”

“It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most responsive to change.”

“Responding to change has included hatching a “growth fund” to bankroll larger startups that would once have gone public (in 1999), expanding into China (in 2005) and India (a year later), and creating a hedge fund (in 2009) and a wealth-management arm (in 2010).”

“Two years ago Sequoia launched its Arc programme for young startups. In 2023 it parted ways with its Chinese and Indian units.”

“With lots more cash chasing roughly the same supply of startup talent, industry-wide returns have duly disappointed.”

“According to Cambridge Associates, an investment firm, the LPs of American VC firms have made compound annual returns of 1.45% in the past three years, compared with 41% in the three years before and less than the 8% they could have earned in public markets.”

“Sequoia is also contending with smaller “seed” investors, often ex-entrepreneurs, getting between old-school VCs and the next generation of founders.”

Monday, Nov. 25th: Rick Zullo wrote about the differences between marketplaces, brokers and storefronts. - Equal Ventures

“Marketplaces are able to create economic leverage in the value chain, by bringing ALL buyers and sellers to a centralized hub. We deliberately callout ALL, as multi-homing (the concept of a market participant operating across multiple competing solutions) is strongly disincentivized on these platforms. Due to a variety of different factors, buyers/sellers experience high switching costs (the concept of experiencing significant losses in productivity when moving from one platform to another) and/or increasing marginal utility (ie. deriving incrementally higher benefit from each marginal interaction) that strongly disincentivizes multi-homing behavior. ”

“Brokers differ from marketplaces in their lack of captivity. While there are incremental advantages to consolidating business behind a single transaction facilitator (i.e. moderate switching costs), buyers and sellers freely multi-home across providers. The products/services being facilitated by brokers are often unique, but non-exclusive as sellers frequently list the same product across multiple providers (whereas this practice is punishable on marketplaces like eBay).”

“Brokers largely try to differentiate themselves via the quality of their services (resulting in higher operating expenses, but perhaps higher willingness-to-pay) and finding long-tail buyers and sellers where the transactions are more difficult to discover and curate. These are often the only places where they can yield margin as the more liquid supply in the market gets transacted incredibly efficiently (as in commodity markets).”

“Brokers can be great businesses, but they are businesses of tactical execution given the constant pressure of the market. This generally results in lower persistency of profitability and lower margins in the market.”

Tuesday, Nov. 26th: Harry interviewed the founder of Lakestar, Klaus Hommels. - 20VC

“One of my rules was to pause investing for three months after a big success. Success can make you overconfident. You start to believe you can walk on water, which leads to mistakes. Pausing gave me time to regain humility and clarity.”

“I'm always intrigued by the technology or by the founder. This doesn't scale with money so much.”

“I do want to fall in love with the founder and the the business because at the end I look at myself as an outsourced business development guy. I do spend a lot of times on my investments so I do need to like everything with it.”

“I do not get involved in a lot of companies.”

“The progress of a society is defined by the way how they it handles risk.” “Today, the only regulatory compliant way of financing innovation is venture. In Europe, we are at 0.5% of GDP so we are under financing innovation by factor of 8 in comparison to the levels that made us wealthy in 1950-70s when banks were funding innovation yielding to companies like Bosch, Porsche or Siemens.”

In the US, 10-13% of assets managed by pension funds are invested into venture compared to 0.02% in Europe.

“I do believe that if you see the right companies you should take yeah a lot of risk and over proportional risk in those.”

“The good companies I would still do them even if they were 30% more expensive. I’m in not in buyout where buying at a right price makes a difference. I’m in venture where right judgement makes a difference. Even if you mis-priced an asset by 20-25% in the early days, it does not make a difference at the end.”

“Revolut is the biggest blessing that we currently have in the European ecosystem.”

Wednesday, Nov. 27th: David Girouard (CEO at Upstart) shared tips for making speed fundamental to your company. - Firstround

“I’ve long believed that speed is the ultimate weapon in business. All else being equal, the fastest company in any market will win.”

“I believe that speed, like exercise and eating healthy, can be habitual.”

“A good plan violently executed now is better than a perfect plan next week. The process of making and remaking decisions wastes an insane amount of time at companies. The key takeaway: when a decision is made is much more important than what decision is made.”

“We’re deeply driven by the belief that fast decisions are far better than slow ones and radically better than no decisions. […] There are decisions that deserve days of debate and analysis, but the vast majority aren’t worth more than 10 minutes.”

“I’m always shocked by how many plans and action items come out of meetings without being assigned due dates.”

“It’s always useful to challenge the due date. All it takes is asking the simplest question: “Why can't this be done sooner?” Asking it methodically, reliably and habitually can have a profound impact on the speed of your organization.”

Thursday, Nov. 28th: Delian Asparouhov, partner at Founders Fund and cofounder at Varda Space wrote about key life learnings. - Delian Asparouhov

“It’s aways possible to learn. What started as going to an initial aerospace conference at age 23, led to starting Varda at age 27, which led to now having a deep grasp of the entire field, both technically and as an industry.”

“Everything in life compounds. Compound interest exists in personal relationships, knowledge, and finances. It’s hard to appreciate this fact when you’re at the beginning of the curve. As long as you let those early investments ride and continue to double down on your winners, those early efforts can have massive outcomes.”

“The world of people who change the world is quite small. Arriving in Silicon Valley in 2012 I was overwhelmed by how much there was to learn about who actually built large tech companies and how it was done. Now, a decade later, I realize that the set of players relevant today has a massive overlap with those a decade ago. Not a whole lot changes.”

“If you’re not scared, you’re not pushing. If you don’t proactively take on some existential dread every few years, you probably aren’t pushing yourself hard enough.”

“Your physical space matters. I tell founders after we lead their seed round, that the most important decision they will make for the first year of the company, is their choice in office lease. If you don’t have a top-tier office, top-tier talent will subconsciously be averse to joining you.”

Friday, Nov. 29th: Plural’s funding partner Ian Hogarth wrote about what it takes to build a trillion-dollar startup in Europe. - FT

Europe lags in tech leadership due to bureaucracy, limited founder-led capital, and premature exits of promising companies.

Experienced founders are vital for high-risk innovation in areas like AI, fusion, and quantum computing.

“There are only seven examples of trillion-dollar tech companies in the world — Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla. All are American. None are European. Going a level down, Europe has four $100bn-plus tech companies compared with the US’s 33.”

“I believe that the growth of the technology industry in Europe is core to creating a more prosperous and resilient society.”

“Europe needs to celebrate and support experienced founders who are building and investing in the highest-risk, highest-reward ideas.”

“Like any profession, being a tech start-up founder is a kind of craft — and the longer you do it, the more you refine the craft.”

“For their second or third company, [serial entrepreneurs] will often tackle harder challenges. The deepest reason is that having founded a start-up, you know how hard it can be — so if you’re going to try again, you’re even more committed to tackling a mission that is inspiring enough to justify the lows that you know will inevitably come.”

“In Silicon Valley, more than 60% of the partners at top venture capital funds were previously founders and chief executives; in Europe, by contrast, the figure stands at a dismal 8%.”

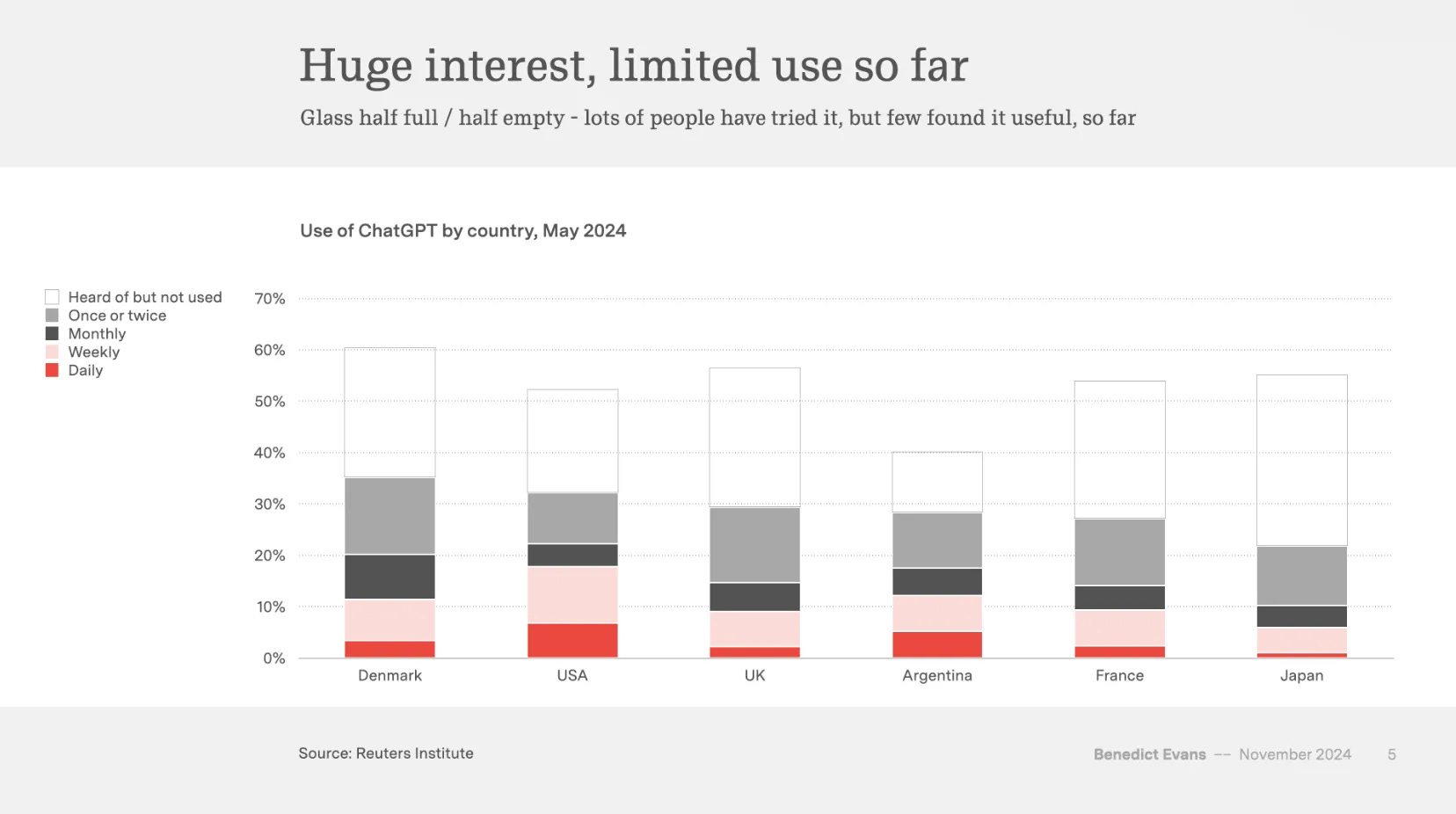

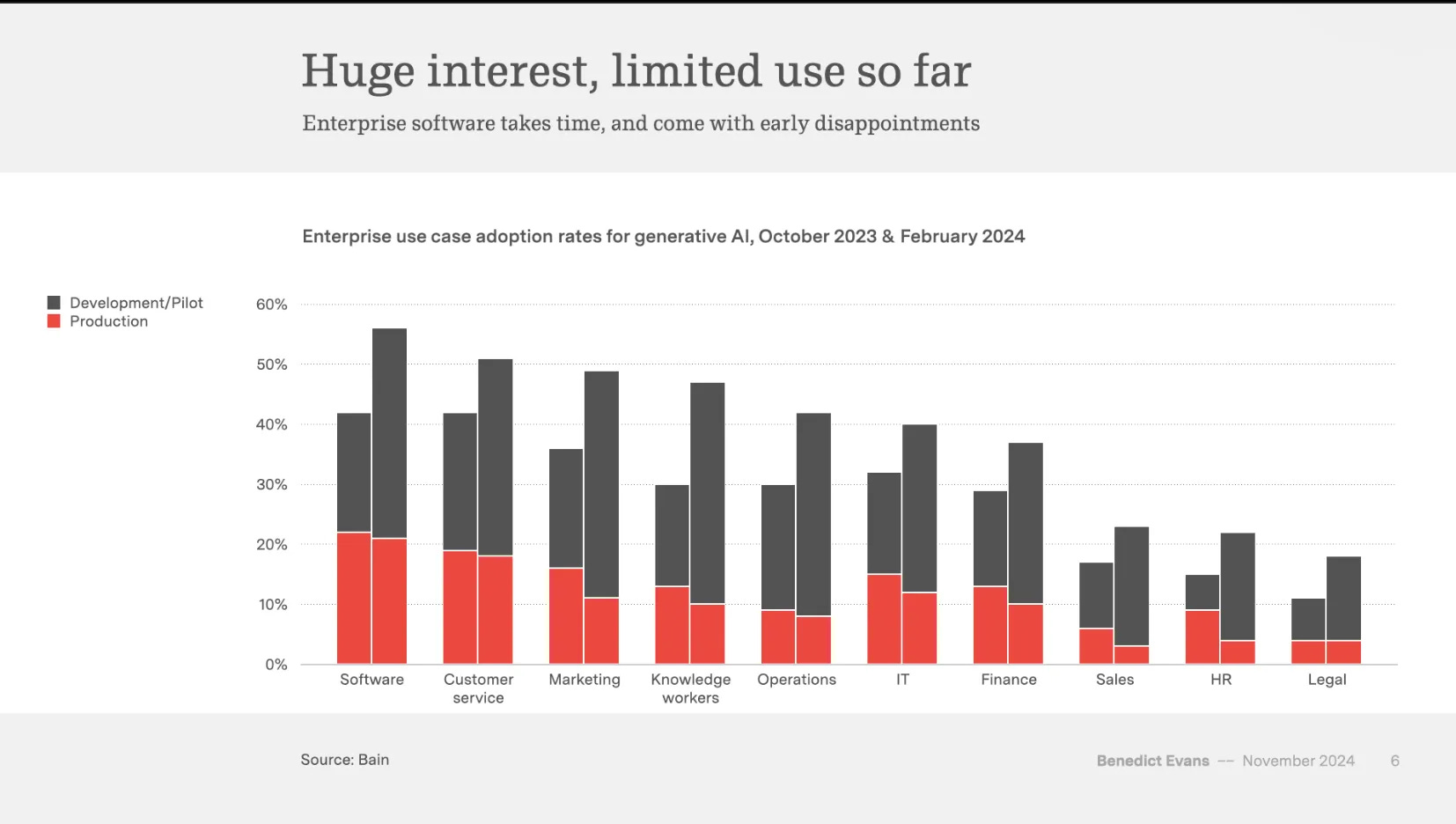

Sunday, Nov. 30th: Ben Evans shared a presentation on AI during Slush. - Ben Evans

ChatGPT has garnered widespread attention but the majority of users engage with it only briefly, failing to incorporate it into their routines.

Early adopters in software development, marketing, and customer support have already seen efficiency gains. However, limitations like hallucinations and probabilistic inaccuracies make AI unsuitable for contexts requiring high precision, such as law or medicine.

Deploying generative AI involves rethinking workflows and product design. Ben distinguishes between incremental improvements, such as adding AI features to existing products, and transformative changes that redefine markets.

Ben draws an analogy to past technologies like image recognition and databases, which were once considered AI but are now just software. Over time, LLMs will likely follow this trajectory, becoming commoditized and losing their association with “intelligence.” For example, tasks like rewriting emails or summarizing reviews may become as mundane as spell-checking.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋