📖 Venture Chronicles - November 2023

Overlooked #163

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of November.

If you enjoy the “Venture Chronicles” series featured in this newsletter, I highly recommend downloading Capsule. Created by my friend Jérôme, it's a modern news app that I use daily to curate content for the newsletter. The app sources content from an international team dedicated to curating news, trends, and insights that are shaping the world in ways you may not have realized you needed to know. You can read more about Capsule on Techcrunch.

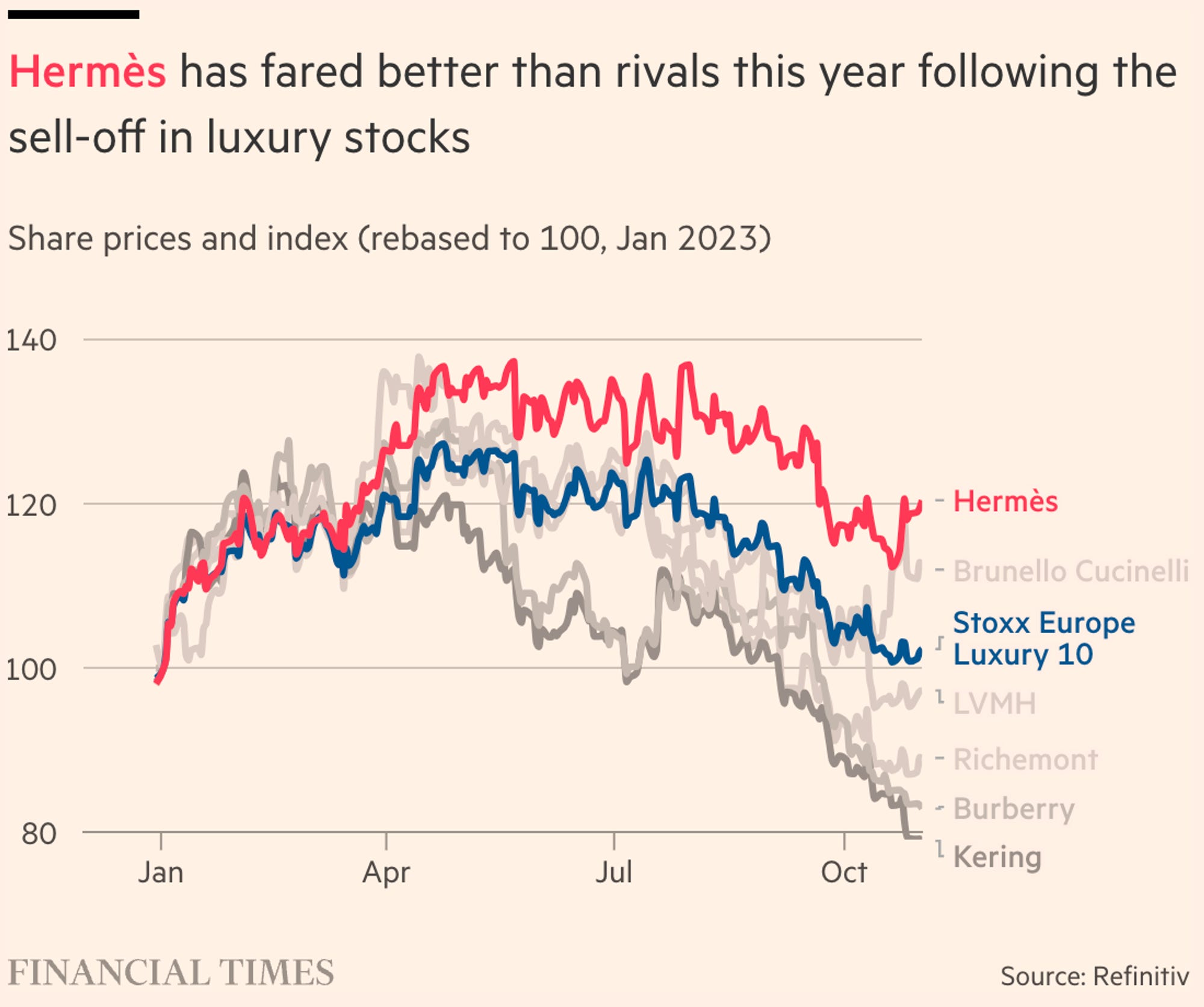

Wednesday, Nov. 1st: Hermès has shown greater resilience to the global economic downturn compared to its luxury counterparts. - FT

Unlike other brands, you cannot simply walk into a shop and purchase Hermès handbags (e.g. Birkin, Kelly). Instead, Hermès only offers loyal consumers the opportunity to buy these exclusive handbags. Consequently, many consumers purchase smaller Hermès items over several months to demonstrate their loyalty to the brand and to sales associates, in hopes of being selected to buy the coveted handbags.

"The global economic outlook may look uncertain but the market for Hermès’s top-tier goods remains strong thanks to its premium positioning, classic styling, wealthy client base and tightly controlled production.”

Hermès has outperformed other luxury brands, partly because its status as a higher-end brand provides greater insulation from market downturns. “The real luxury consumers continue to buy, maybe a little bit less, but what they don’t compromise is on the quality of what they buy. True luxury consumers don’t trade down.” “They may be growing less than others during peaks, but in that way they resemble Ferrari. They could have grown much bigger than they are but that’s how they manage to keep the brand exclusive.”

“Hermès’s lower exposure to tourist spending than rivals is a key factor. Local buyers make up more than 90% of its clientele in Japan and about 75% of its customers in New York City, according to one investor — an advantage during economic downturns as well as crises such as the pandemic.”

“The company has as much as 4-5 times more demand than it can supply for its products.”

Thursday, Nov. 2nd: Vinod Khosla (GP at Khosla Ventures) shared a list of innovations that could happen in the next decades. - Vinod Khosla

“These [predictions] have to do with how technology (AI and beyond) is the only lever by which we’ll reinvent societal infrastructure to give the resources enjoyed by 10% of the planet to the remaining 90%.”

“In 25y, there could be a billion bipedal robots. This would create a new industry larger than the current auto industry. From factory workers to farm workers and more, we could free humans from the bottom 50% of really undesirable jobs.”

Friday, Nov. 3rd: William Tancredi wrote about vertical SaaS for veterinaries highlighting four startups which are Maven (pet activity monitoring system), Digitail (modern veterinary software), Mascotte (remote & fractional support for reception) and Roo (veterinary relief marketplace). - Doc’s FIRE

“Many veterinary practice management systems fall short of “doing it all” and so practices end up cobbling together a variety of softwares to serve their needs in a fashion that resembles, at best, my ten-year old’s LEGO builds (charming and delightfully clever) and, at worst, Frankenstein’s monster (horrifying and hated by villagers).”

“Working as a relief doctor for Roo is useful as well because it allows me the chance to see how other hospitals solve problems similar to mine in different ways. It’s something like a professional exchange program.”

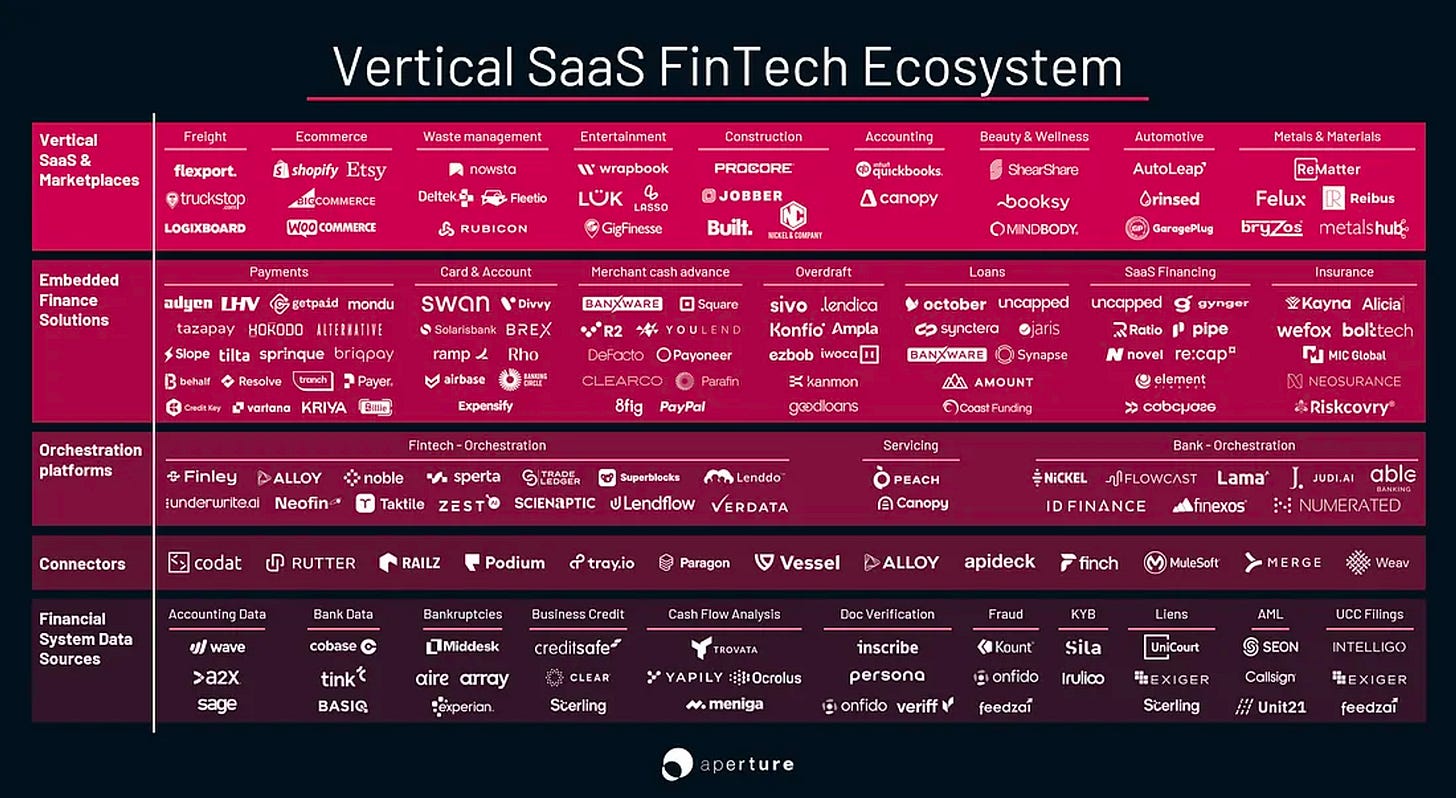

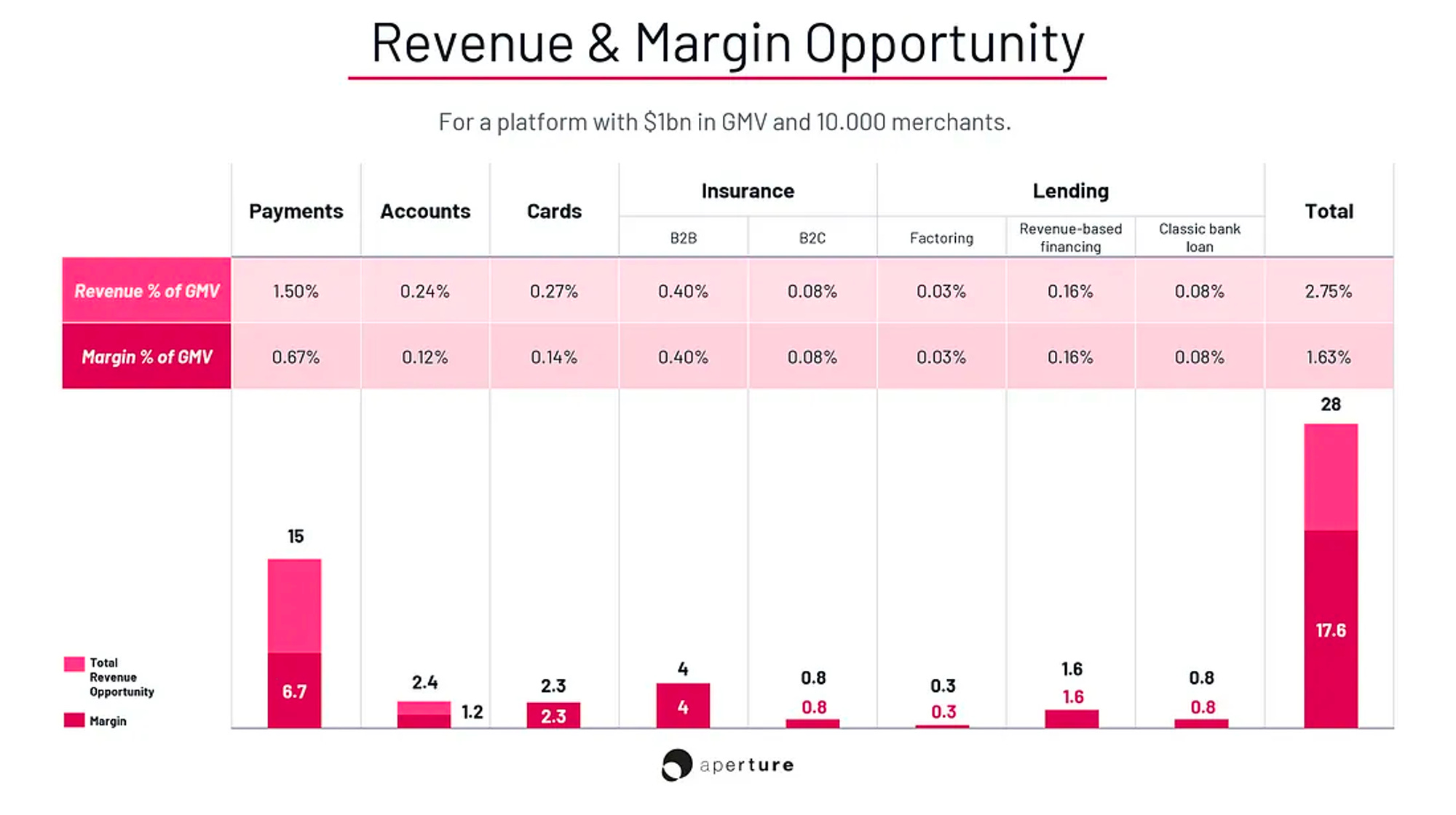

Saturday, Nov. 4th: Aperture published a market map of fintech enablers to add financial services into vertical SaaS and marketplaces. Aperture

“Vertical SaaS players like Toast piloted a genius scaling model: Offer the software for free and monetize through ancillary services — mainly of the financial kind.”

“By our estimate, a software platform with $1bn in GMV will likely be able to monetize up to 2.75% of that GMV using all the FinTech verticals we scored, which would lead to monetization potential of up to ~$28mn in additional revenue.”

“We believe that a good team to launch a [fintech] vertical is made up of the following: (i) a FinTech or vertical program manager, (ii) a FinTech analyst, (iii) a PM and (iv) 1–2 full-stack developers.”

Sunday, Nov. 5th: Hubspot, a sales and marketing platform, has acquired Clearbit, a B2B data provider. Clearbit has a database with 20m companies and 500m decision makers. This data is sourced through multiple private and public channels, including crowdsourcing. Hubspot plans to integrate Clearbit’s comprehensive B2B data directly into its platform, employing AI to make this data more actionable. This acquisition is a significant indicator of the consolidation within the sales tech industry. With this move, Hubspot positions itself to compete directly with industry giants like Apollo and ZoomInfo - Techcrunch, Hubspot

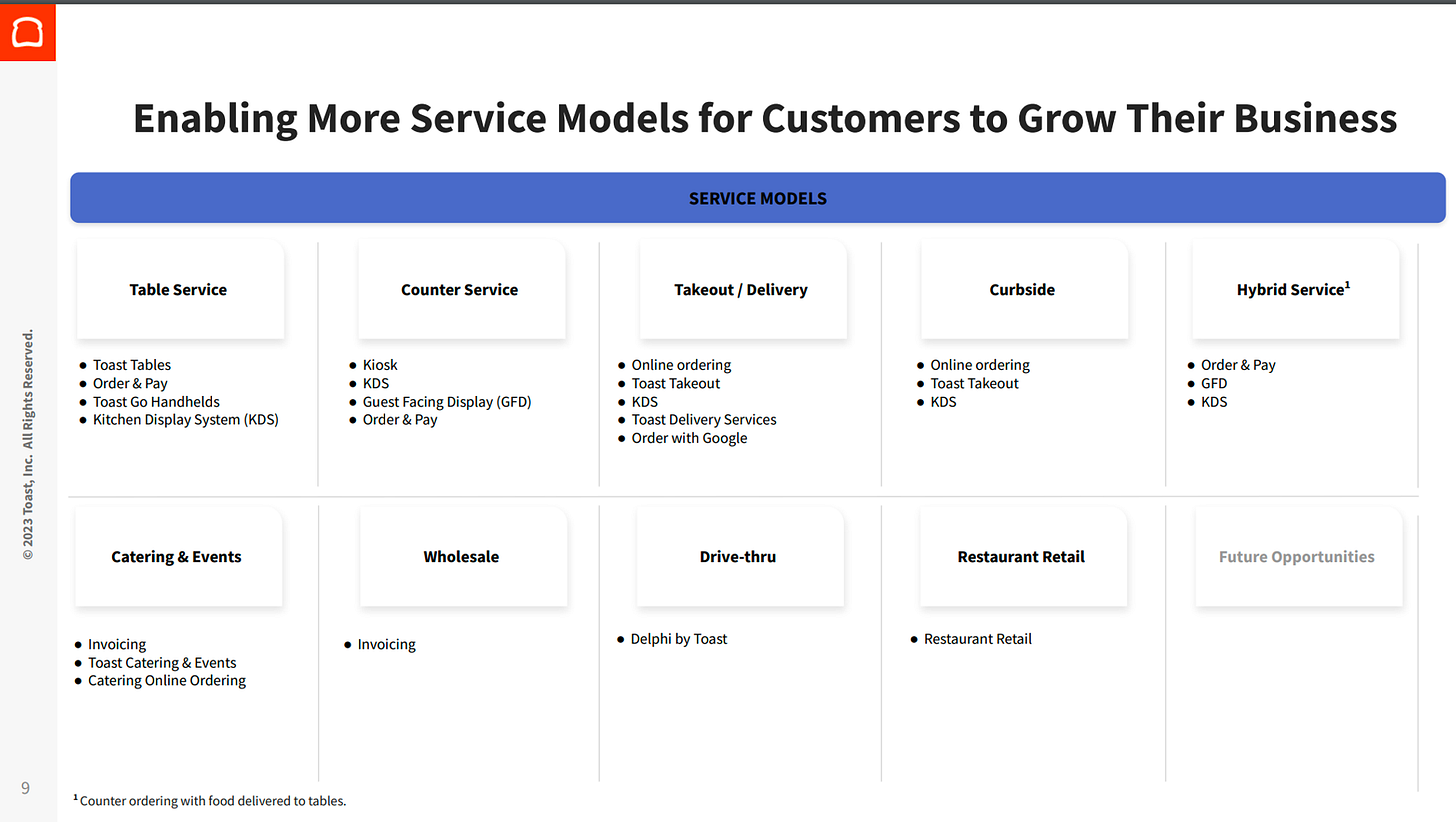

Monday, Nov. 6th: Sam Blond interviewed Toast’s CRO named Jonathan Vassil. - SaaStr

Jonathan joined Toast in 2017 as the SVP of Sales, at a time when the company had just raised its series B and was generating $20m in ARR. Today, Jonathan is CRO and Toast is a public company which is doing $1.1bn in ARR (Q2-23).

Toast is a vertical software and embedded payment solution focused on serving the restaurant community across the US, Canada and the UK (85k restaurants).

“One of the greatest strengths of our go to market motion is the partnership between our sales organization and our marketing organization.”

“We understand our TAM at the deepest level. We've spent a lot of time understanding our market (e.g. the composition of the restaurant vertical, how restaurants make decisions).”

“What makes the restaurant vertical distinct and therefore our go to market motion distinct is really the density that you see with restaurants. There is no other vertical that's that has that many rooftops in the US or across the globe. We’ve leveraged that density to our advantage by generating social proof from our successful restaurants to convince restaurants in their surroundings.”

c. 75-80% of sales are driven by field-based sales representatives, each owning a specific geography. They meet restaurants face-to-face, serving as trusted advisors. The remaining 20-25% of sales are managed by inside sales teams, who focus on territories with lower density or areas where recruiting a field representative is more challenging.

Field sales are effective for Toast due to the high density of restaurants in targeted areas, and because Toast’s ACV includes SaaS and payments services significantly increasing the LTV of customers.

Tuesday, Nov. 7th: Procore disclosed its Q3-2023’s results. - Procore

In Q3-23, Procore made $248m in sales growing at 33% YoY (international revenues grew 30% YoY impacted by currency headwinds), reached 16k customers and returned to operating profitability.

Procore rediscussed several product announcements:

Procore Connectability: “all project stakeholders will be able to collaborate on a project [starting with drawings] and share data with one another, all while staying within their own accounts.”

Procore Copilot: “an extension of the project team, automating time-consuming processes, surfacing information in real time and suggesting next best actions.”

Procore Pay: “The real challenges stem not necessarily from the moving of money but from all of the complicated upstream workflows and processes that must come first. All of these processes exist in the Procore platform today. The beauty of Procore Pay as it essentially automates the last mile of the payments workflow. We now seamlessly facilitate the payments and lean labor process between general contractors and specialty contractors, thereby minimizing complicated paperwork and ultimately giving our customers full transparency into their entire payments flow.”

Procore acquired Unearth which is a geospatial information mapping product for construction that Procore will integrate into its platform to remove the friction of determining the location of materials, equipments and teams in a construction project.

“It is clear that the demand environment has become incrementally more challenging. The construction industry is not immune to broader economic conditions. We have continued to see heightened cautiousness from customers in response to external uncertainty around a potential downturn, which has translated to increased scrutiny and purchasing decisions.”

“We are seeing increased scrutiny on deals, causing sales cycles to elongate. Customers are taking longer to finalize purchasing decisions with more decision-makers involved and more layers of required approvals. As an example, deals that used to get approved timely by the internal champion are now requiring CFO approval and deals that used to require CFO approval may now require board approval.”

Wednesday, Nov. 8th: Hoxton Ventures wrote on the current macro-economic environment. - Hoxton

“In the public markets, seven technology companies – Apple, Microsoft, Amazon, Google, Nvidia, Tesla, and Meta (the “Magnificent Seven”) – have been responsible for most of this year’s gains. They make up only 28% of the S&P 500 Index but have contributed almost 65% of the S&P 500 Index YTD. If you exclude them from the S&P 500 index, the index would be negative.”

“Earlier this September, there were signs the IPO market might have come back. ARM, Klaviyo and Instacart all went public – successfully. But again, the reality is more complicated. All three sold only a small portion of their stock into the market. Klaviyo sold just 6%. It used to be customary for companies going public to float at least 10%. A small supply and good demand mean the stock trades well on day one. Then the stock weakens as IPO buyers take profits, leaving the companies to struggle to find longer-term shareholders. Like SPACs, this trick only works a few times before everyone realizes the game that is being played.”

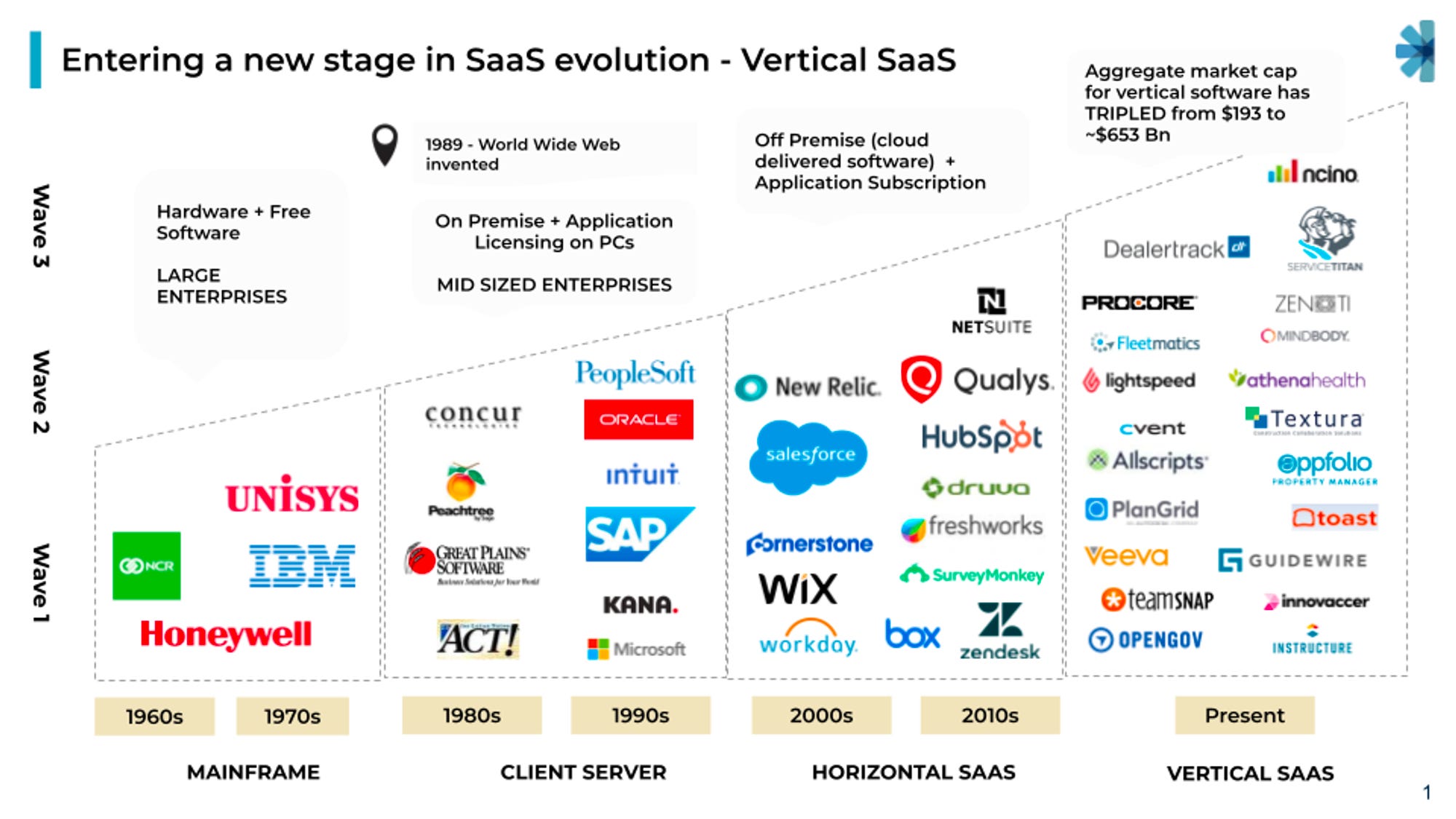

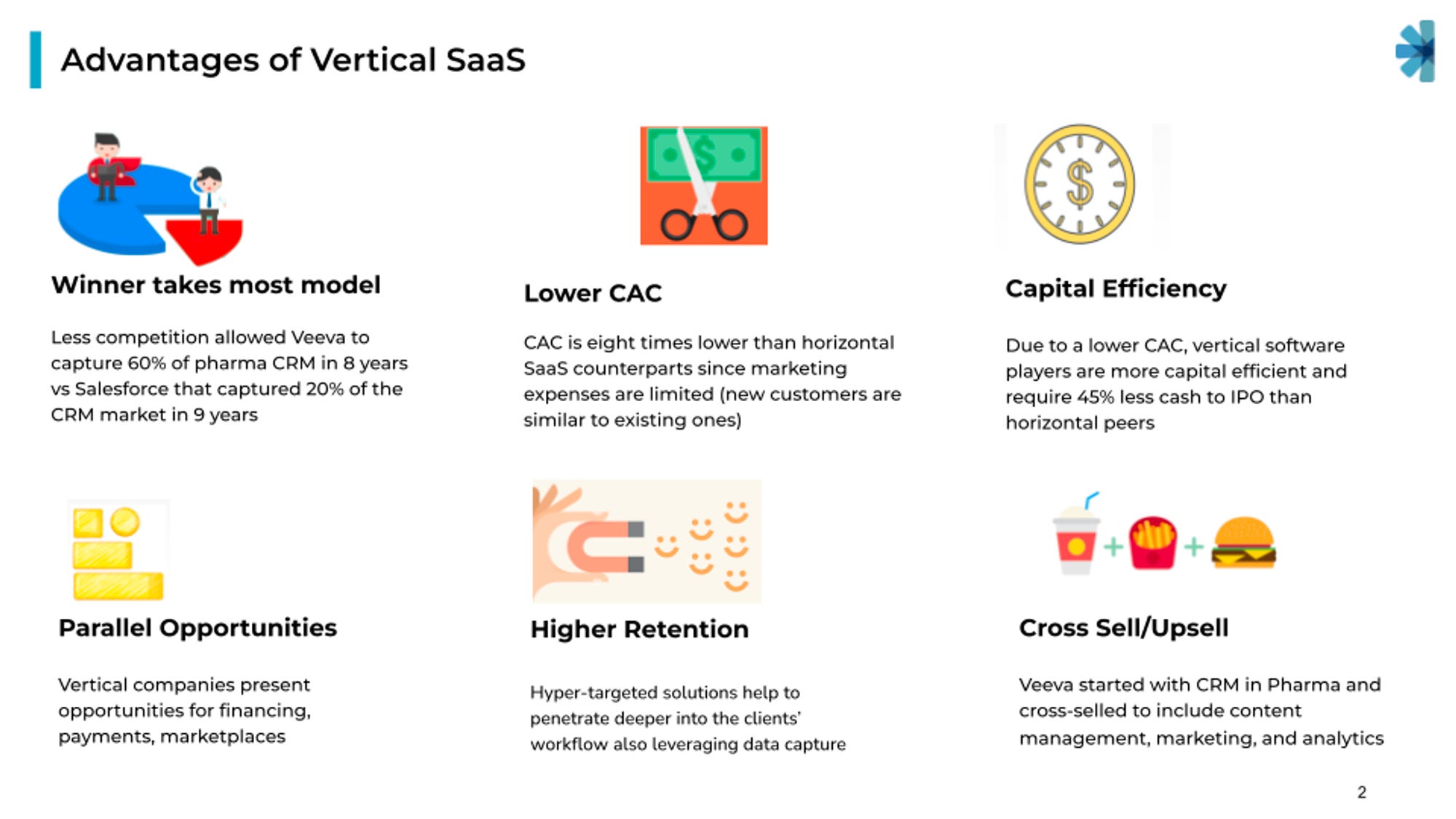

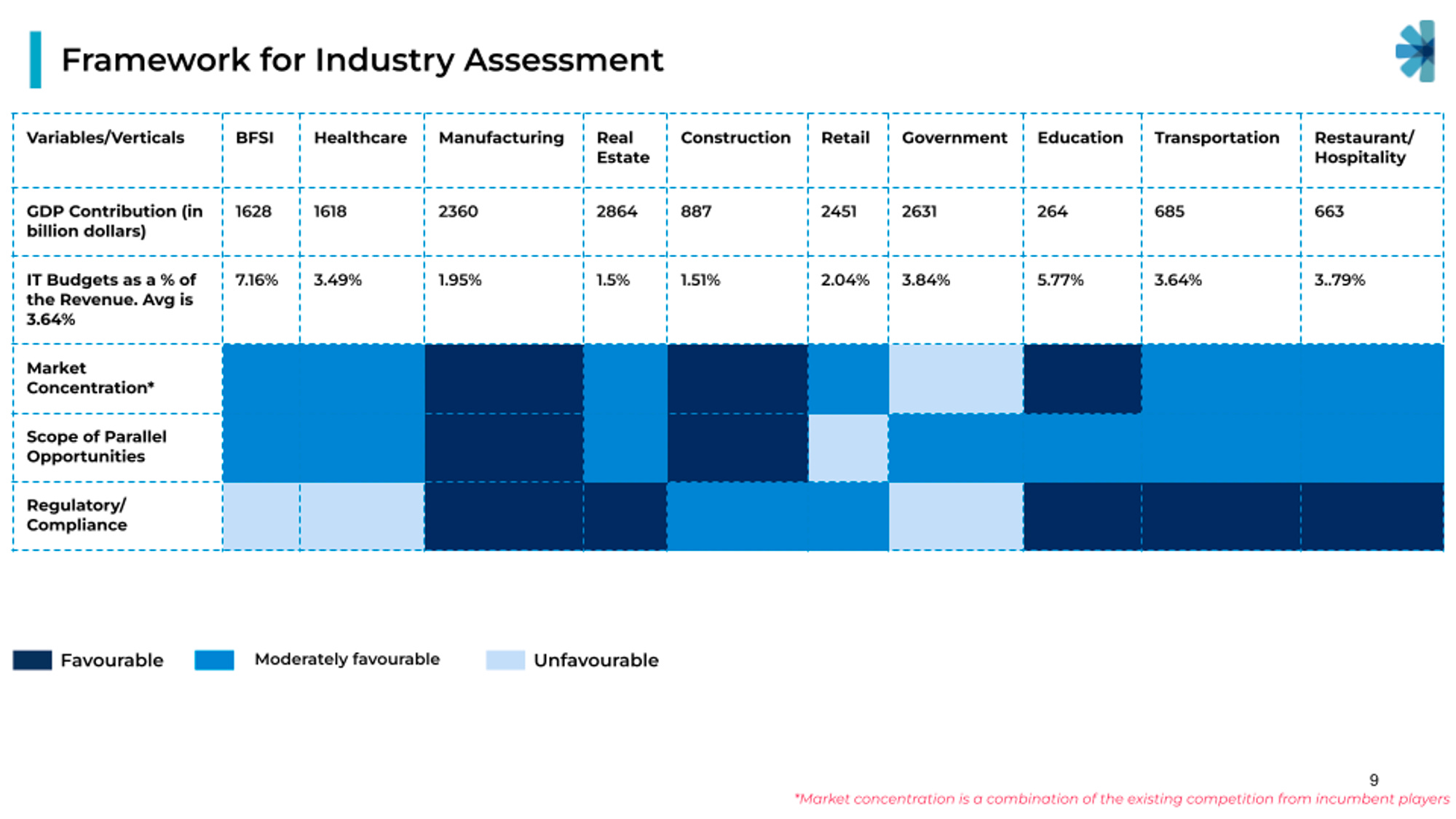

Thursday, Nov. 9th: I discovered a good paper on vertical SaaS published by Anirvan Chowdhury who is an investor at an Indian venture fund called Blume Ventures. - Anirvan Chowdhury

“We strongly believe with wider adoption of SaaS, the wave of vertical focused SaaS companies that started around a decade back, are not just here to stay, they could very well be the future of SaaS. This opportunity is not restricted to Vertical SaaS companies building for India like Classplus, but we believe there are going to be multiple plays such as Innovacer and Zenoti out of India building world class Vertical software for global markets.”

“When we are assessing vertical SaaS plays we generally like to look at companies through the lens of the a) overall GDP of the industry, b) software spends as a % age of revenue in that industry, c) market concentration (incumbents and fragmentation of vendors), d) scope of parallel opportunities, e) the extent of regulatory and compliance constraints.”

Friday, Nov. 10th: Jared Sleeper shared careers tips for emerging investors. - Sleeper Thoughts

“Understand that this recruiting game is different. Given the pyramidal shape of the [investing] industry, mid-career roles with high potential to convert into permanent roles are much harder to find- in part because people deliberately don’t leave them.”

“It will take longer to find a mid-career role because they open up rarely and idiosyncratically. If you’re looking to make a change, set a timeline based on your expected tenure in the role. If you’d budget two months to find a role that you’d expect to last three years, you should be comfortable taking six+ months (at least!) to find a role you hope will last ten+ years. It’s worth being patient and not creating artificial time pressure for yourself- the stakes are higher here.”

“I advise candidates to look for three key variables when they evaluate potential mid-career roles:

Platform: Does this firm provide you with the resources you need to develop your career? Does it have a good brand, capital, dealflow? Does it provide access to datascience and research? Is it a place you would want to be associated with for the next decade or more?

Person: Who will you be working for- aka which senior person is going to be championing my investments and (later) my career? Is that person known for being good to work with? Do you deeply respect them? Are they likely to stay at the firm for the long haul? This will almost certainly be your primary working relationship- it’s a huge decision.

Path: What is the path to taking risk (leading a deal, owning public positions, managing a portfolio, etc.)? Is there a clearly defined timeline? Who makes the decision?”

“Most risk-taking investors have a specialty that narrows their focus to a scope that allows for both excellence and moat-building. It could be a specific stage, sub-sector, geography, strategy or combination of the above”

Saturday, Nov. 11th: The Economist recently discussed a paradox in the US economy between a national economy recovering with a quarterly GDP growing 4.9% YoY and top public companies continuing to express a negative outlook on future prospects. - The Economist

“Plenty of bosses failed to excite investors despite bringing them sound results. The reaction to the performance of big tech was particularly discordant. Alphabet, Google’s parent company, heartily beat profit forecasts but saw its share price sink by 10% after investors were underwhelmed by how its cloud-computing division was doing. Meta’s warning on macroeconomic uncertainty meant that the social-media empire’s biggest-ever quarterly revenue figure went unrewarded by markets.”

“A boom in the third quarter notwithstanding, the future health of America’s consumers remains bosses’ principal worry.” Retail sales are growing solely due to price increases, rather than an increase in sales volumes.

“According to Bank of America, credit- and debit-card data show a downturn in spending in October, compared with a year ago. Last month Americans with student loans had to resume debt payments after a three-year reprieve.”

“Bosses were silent on a bigger long-term threat to earnings: higher interest rates. Eventually, however, big businesses’ debt piles will need to be refinanced at a higher rate of interest, which will squeeze profits.

Sunday, Nov. 12th: I watched OpenAI’s Dev Day Opening Keynote. - OpenAI

OpenAI launched ChatGPT in Nov. 22, GPT4 in Mar. 23, ChatGPT Enterprise in Aug. 2023, voice & vision capabilities for ChatGPT in Sep. 23, Dall-E 3 in Oct. 23.

OpenAI has 2m developers building on its APIs, 100m WAUs on ChatGPT and 92% of Fortune 500 companies using its products.

OpenAI recently launched GPT-4 Turbo, featuring several key enhancements:

it supports a longer context length,

it offers enhanced control for developers, including options like JSON outputs and reproducible outputs (which allow for more precise management of model behavior)

it provides access to improved knowledge retrieval capabilities, enabling the integration of information from external documents and databases into OpenAI projects, and updating the knowledge cut-off date from March 2021 to April 2023 (with a near-term goal of achieving real-time updates),

it introduces new modalities, including access to Dall-E 3, a Text-To-Speech model, and GPT-4 Turbo with vision via APIs,

it allows for greater customization, with more fine-tuning options for recently released models and custom model development based on proprietary company data,

it offers higher rate limits.

“We're introducing Copyright Shield. Copyright Shield means that we will step in and defend our customers and pay the costs incurred, if you face legal claims or on copyright infringement, and this applies both to ChatGPT Enterprise and the API.” “We do not train on data from the API or ChatGPT Enterprise ever.”

OpenAI is also working hard to reduce the price of its API making GPT-4 Turbo 2.75x cheaper than GPT-4 (cutting cost for both prompting tokens and completing tokens).

“The shape of Azure has drastically changed and is changing rapidly in support of these models that [OpenAI is] building. Our job, number one, is to build the best system so that [OpenAI] can build the best models and then make that all available to developers.” - Satya Nadella

OpenAI introduces GPTs which are tailored versions of ChatGPT for a specific purpose. “You can build a GPT, a customized version of ChatGPT for almost anything with instructions, expanded knowledge, and actions, and then you can publish it for others to use.” “We know that many people who want to build a GPT don't know how to code. We've made it so that you can program a GPT just by having a conversation.” GPTs will be accessible via a marketplace and OpenAI will share a portion of its revenues to the most popular GPTs.

Monday, Nov. 13th: I listened to a Private Equity Deals’ podcast episode on RealPage’s public to private acquisition by Thoma Bravo with Scott Crabill who is managing partner at the private equity firm. - Private Equity Deals

Thoma Bravo is a private equity firm specialised in software with $115bn in assets under management and 400 transaction completed across platforms and add-ons. Thoma Bravo was founded in 1998. It made its first investment in software in 2002 and transitioned to invest only in software in 2008. It has offices in San Francisco, Chicago and Miami. It has 200 employees including 85 investment professionals.

Thoma Bravo has four different software funds: (i) a flagship fund for large software companies, (ii) a discover fund for lower mid-market software companies, (iii) a credit fund and (iv) a growth equity fund.

RealPage is a tech platform that enables real estate owners and property managers to efficiently operate residential assets. In 2021, Thoma Bravo took the company private from the public market for $10.2bn.

RealPage is focused on residential units (vs. commercial units) that can be broken down into multi-family apartment buildings, single family rental units, student housing, affordable housing, military housing and vacation units.

RealPage started by targeting property managers automating core back office business processes around property management (e.g. accounting, budgeting, document management, lease management, procurement, facilities management). It expanded by adding products for property owners like revenue management (data analytics product that helps in decision making around pricing of rental units) and business intelligence (see in real time how their properties are doing). It also added products for renters which have become a big part of the business (online payment, rental insurance, utility billing management, rental portal) and products for prospects (lead generation, CRM, virtual tours).

RealPage was founded in 1998 with the acquisition of Rent Roll. In 2001, RealPage released its core property management system called OneSite. It went public in 2010 after having acquired 14 point solutions to have an all-in-one platform for property managers. In 2008, Apax invested in RealPage to fund some acquisitions and owned 20% of the business at IPO. Between 2010 and 2020, it made c.30 additional acquisitions being successful at acquiring and integrating businesses and funding acquisitions thanks to a mix of debt, capital increase and cash from the balance sheet.

What were the attractive features for Thoma Bravo when they acquired RealPage? First, it’s a successful vertical software meaning that it has high barriers to entry and that it’s a mission critical platform. Second, the real estate market is massive ($500bn in rental payments in the US, $20bn TAM for software) and has strong tailwinds favouring a platform like RealPage (2-3% YoY unit growth, 3-4% YoY rents growth, shift from owning to renting, low digital penetration of technologies like IoT and AI). Third, RealPage was a clear market leader being positioned as number 1 players in terms of market share in the enterprise and mid-market segments.

What were the issues that Thoma Bravo saw when evaluating RealPage’s acquisition? First, the company was planning to go through a management transition with the founder and CEO ready to step down. Second, RealPage is the result of many acquisitions creating a lot of complexities (e.g. lack of integrations between products acquired, no streamlined org. chart and IT stack). Third, in Dec. 2020, the macro-context was highly uncertain (covid recovery, recession risk, real estate market impacted).

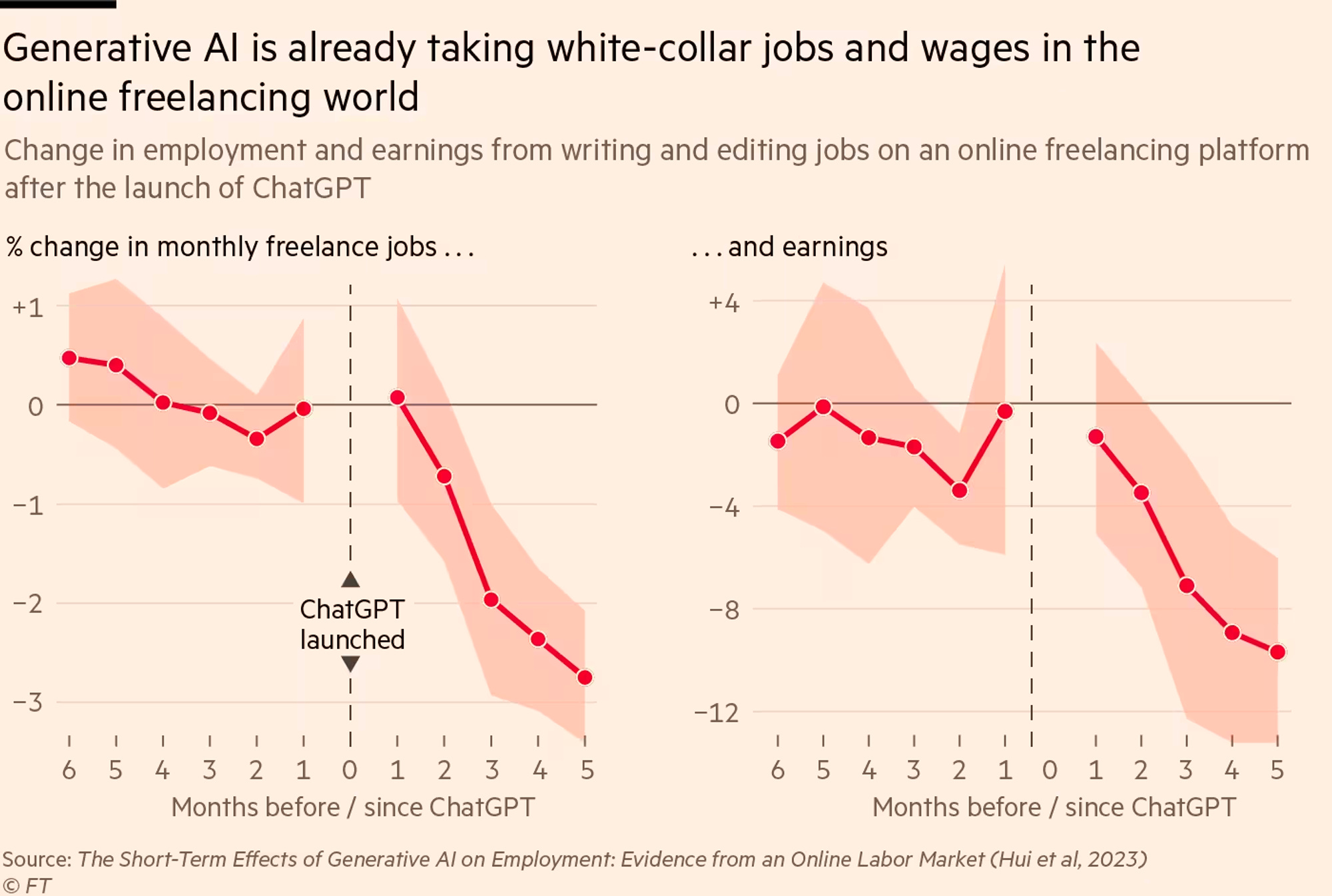

Tuesday, Nov. 14th: The Financial Times wrote about the impact of gen. AI on white collar workers. - FT

“The jobs most at risk from the new wave of AI are those with the highest wages, and that someone in an occupation that pays a six-figure salary is about three times as exposed as someone making $30k.”

“Within a few months of the launch of ChatGPT, copywriters and graphic designers on major online freelancing platforms saw a significant drop in the number of jobs they got, and even steeper declines in earnings. This suggested not only that generative AI was taking their work, but also that it devalues the work they do still carry out.

“The more multi-faceted the role, the less risk of complete automation. The gig-worker model of performing one task for multiple clients — copywriting or logo design, for example — is especially exposed.”

“Not only did AI-assisted consultants carry out tasks 25% faster and complete 12% more tasks overall, their work was assessed to be 40% higher in quality than their unassisted peers. Employees right across the skills distribution benefited, but in a pattern now common in generative AI studies, the biggest performance gains came among the less highly skilled in their workforce.”

Wednesday, Nov. 15th: Gil Dibner (GP at Angular) wrote a great post on venture claiming that venture needs to go back to its roots with the end of entrepreneurship by autopilot. - Gil Dibner

“There are still many opportunities for large successful disruptive companies. But there will be fewer of them because there are no large mega-waves right now to ride.”

“Over the past two years, we have been more focused than ever on path to profitability, breakeven, and sustainable growth. We don’t underwrite anymore to an imaginary Series A round.”

“We are investing in companies that are truly unique and totally awesome. So unique and awesome that they are succeeding with customers even as venture investors fail to understand them. So unique and awesome that they just might not need to raise again. Instead of underwriting to the idea that some other investor will understand these companies and mark them up, we find ourselves underwriting increasingly to at least one of two other things: (1) breakeven and/or (2) our own convictions.”

“We are not completely convinced that the venture factory is completely shut down. We do continue to occasionally find a company where we think the next step is likely a traditional Series A. It’s just that we increasingly find ourselves backing companies that are building optionality around other pathways to success.”

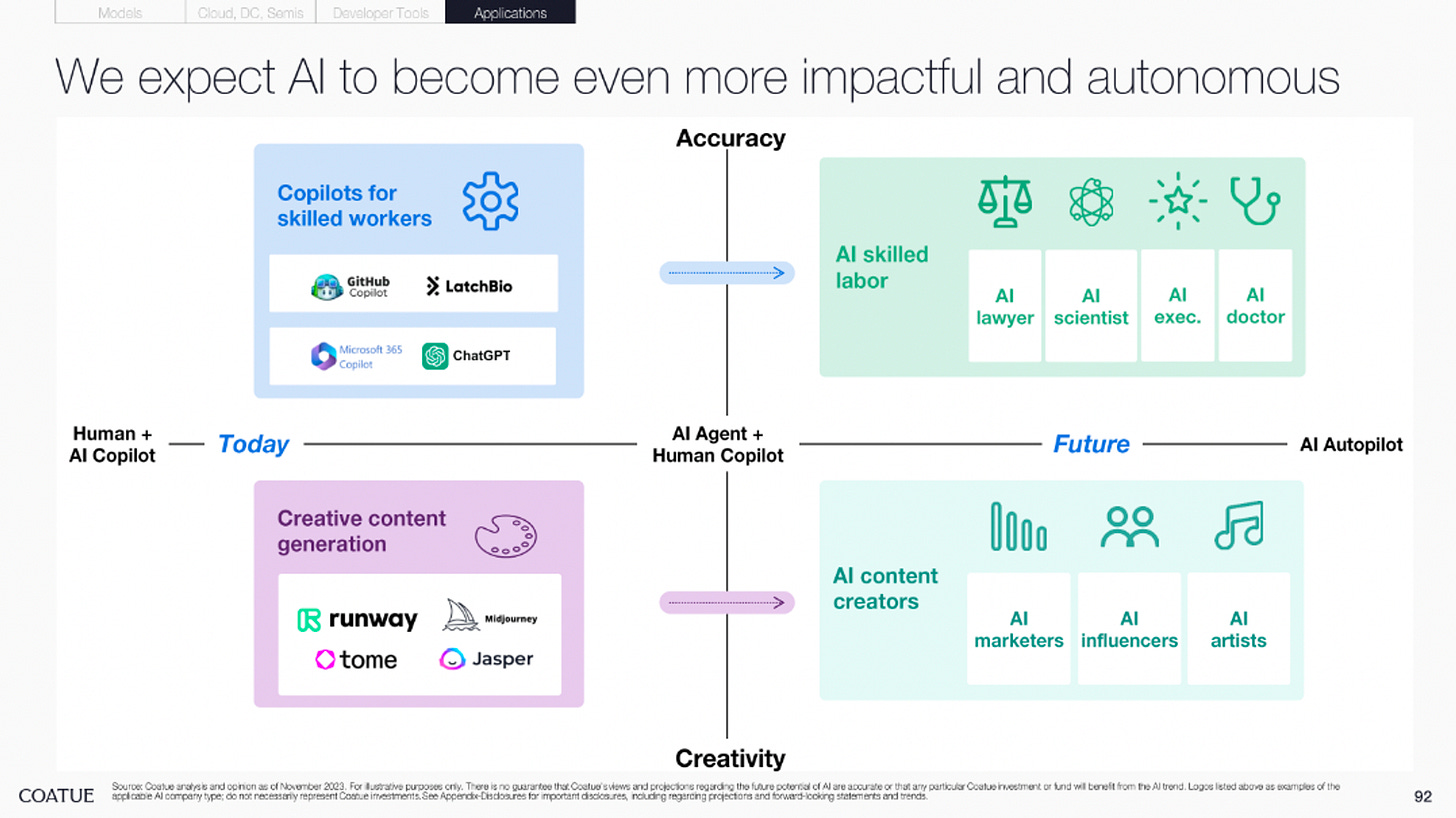

Thursday, Nov. 16th: Gil Dibner (GP at Angular) broke down Gen. AI companies into three thought provoking categories: (i) thin and ephemeral (ii) big and weak and (iii) small and strong. - Gil Dibner

Thin & ephemeral. “They are characterized by an attempt to solve a very narrow business (usually horizontal) problem with nothing more than a prompt to an LLM, usually a third-party API.” “These may be a quick way to make a buck from a customer or ten, but they don’t seem like sustainable businesses in most cases.”

Big & weak. "These may be a quick way to make a buck from a customer or ten, but they don’t seem like sustainable businesses in most cases.” “The founder is planning to ingest essentially all enterprise information sources (emails, logs, code, configuration files, salesforce records, SaaS APIs, you name it) and intends to enable all the users (business users, developers, and everything in between) to do just about everything from asking a question (a la ChatGPT) to creating a full-blown application (Github Copilot but on a massive dose of steroids and redbull).”

Small & strong. "These startups are “small” because there is usually a clearly defined ICP, almost always in a vertical where the founders have deep domain expertise.” “These startups are often “strong,” in my view because they tend to have a pretty robust layer of application functionality built on top of the data and AI layer that underlies them.” “In short, their verticality is their key source of product clarity and business defensibility. These companies utilize AI and often have LLM capabilities as well, but these are mere building blocks that help underpin a much deeper and more robust application.”

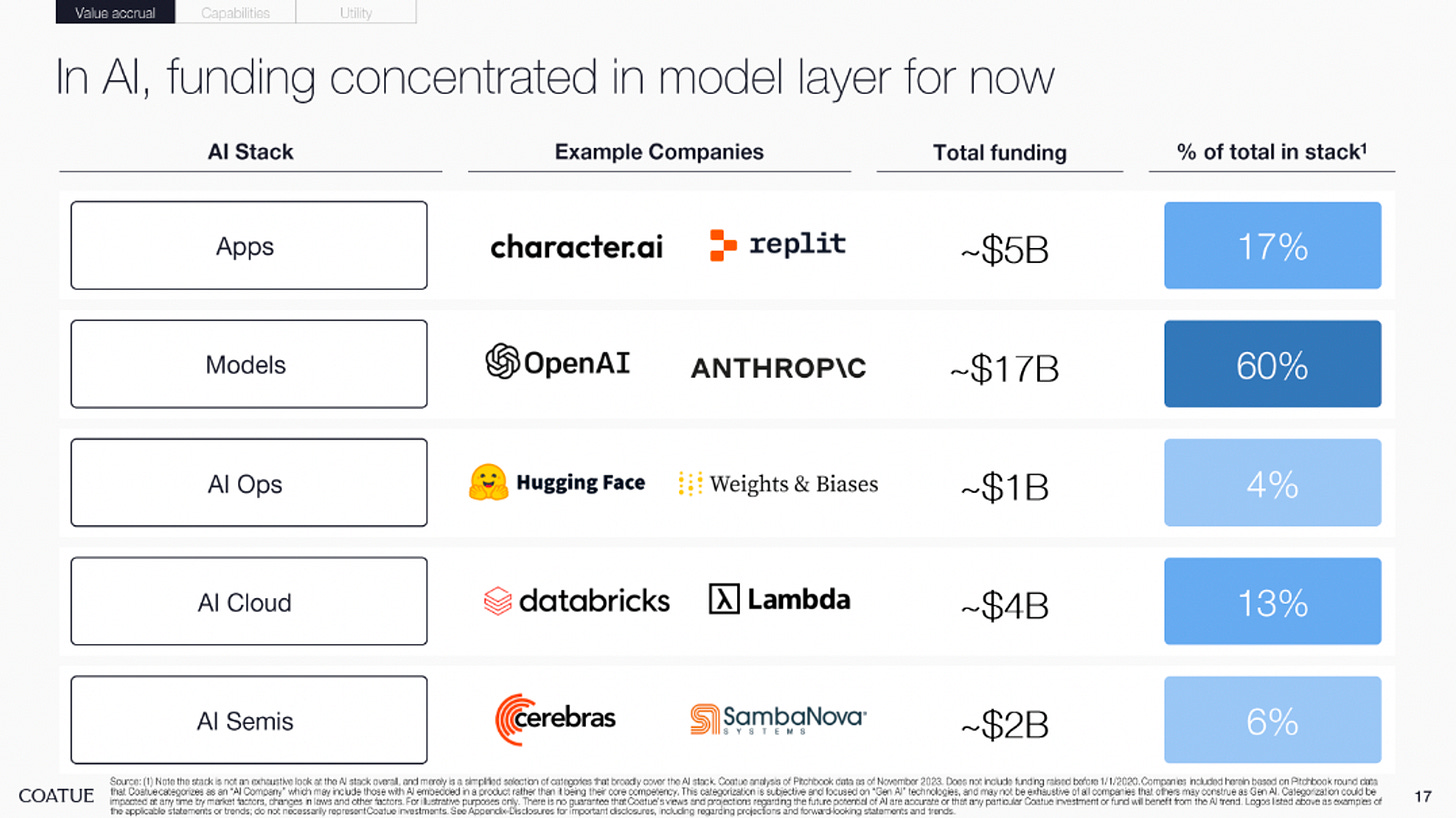

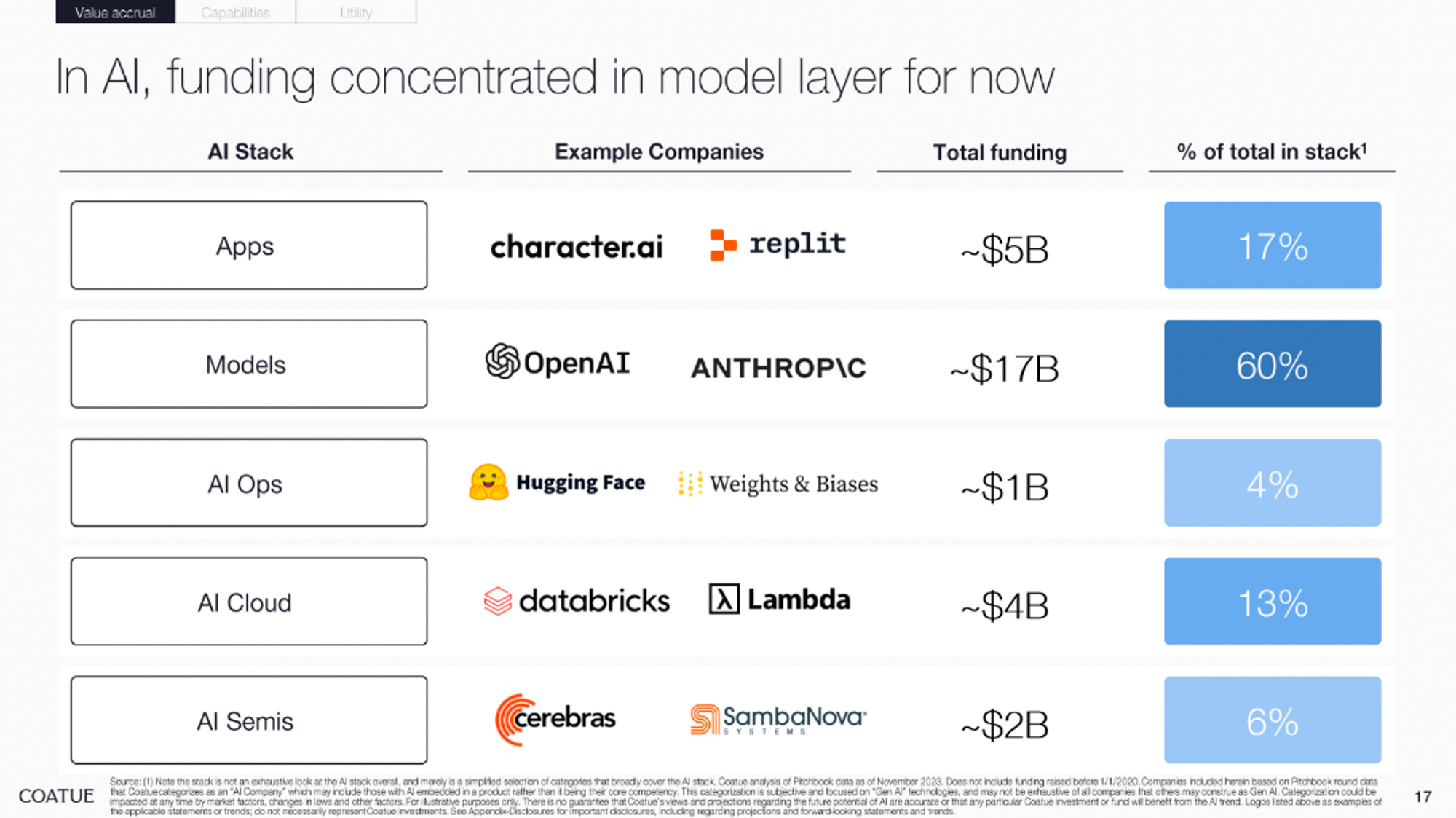

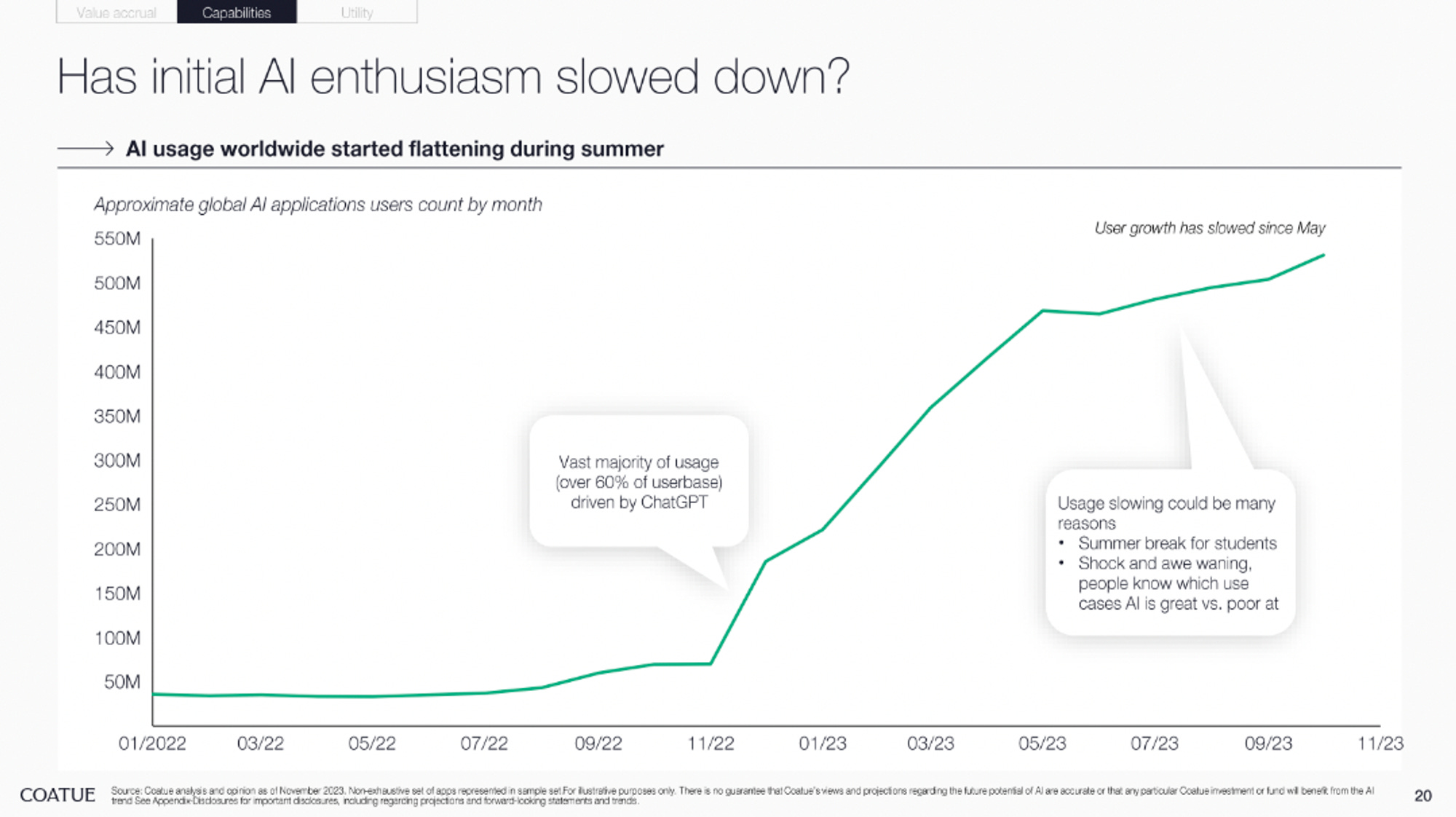

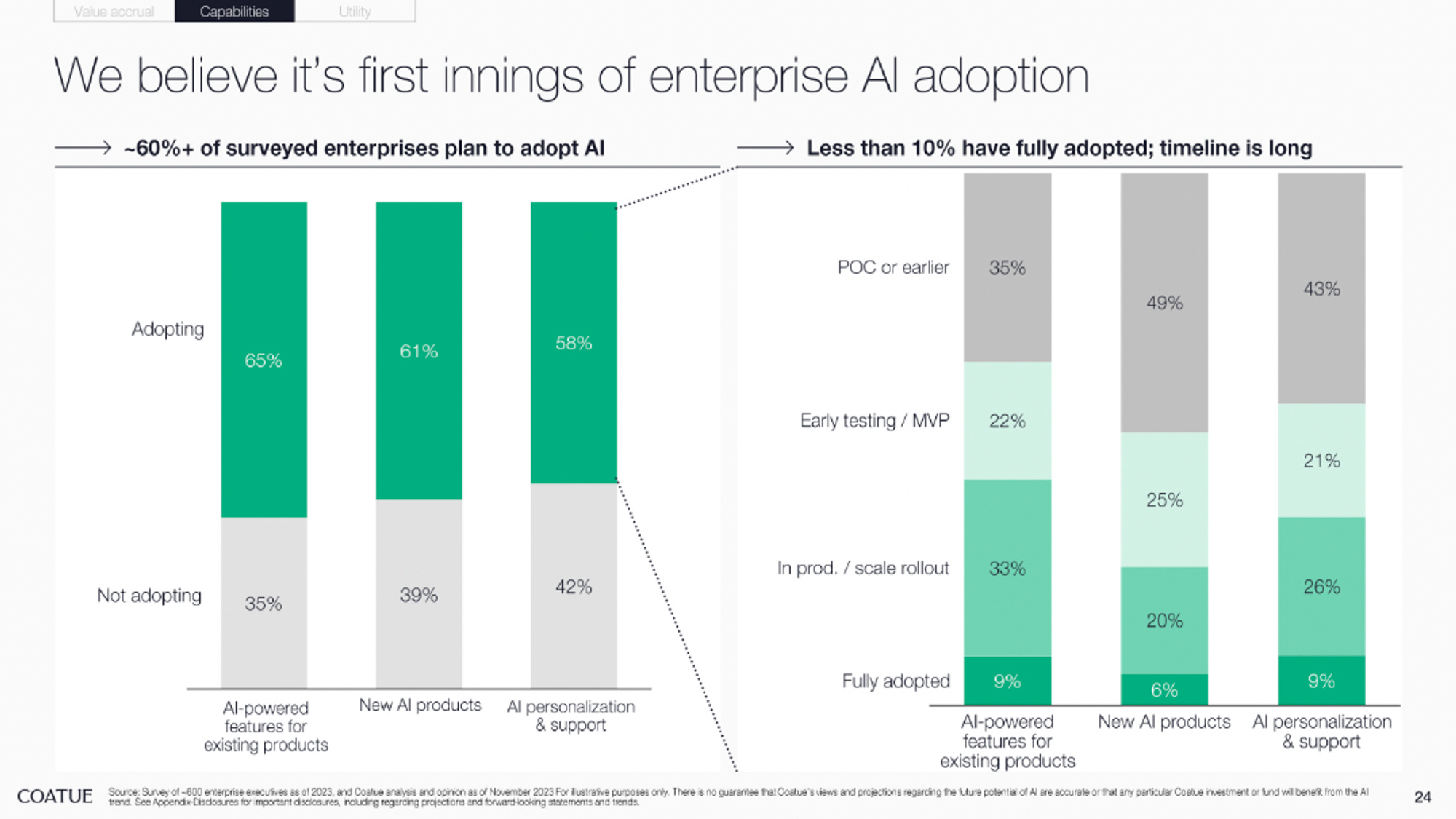

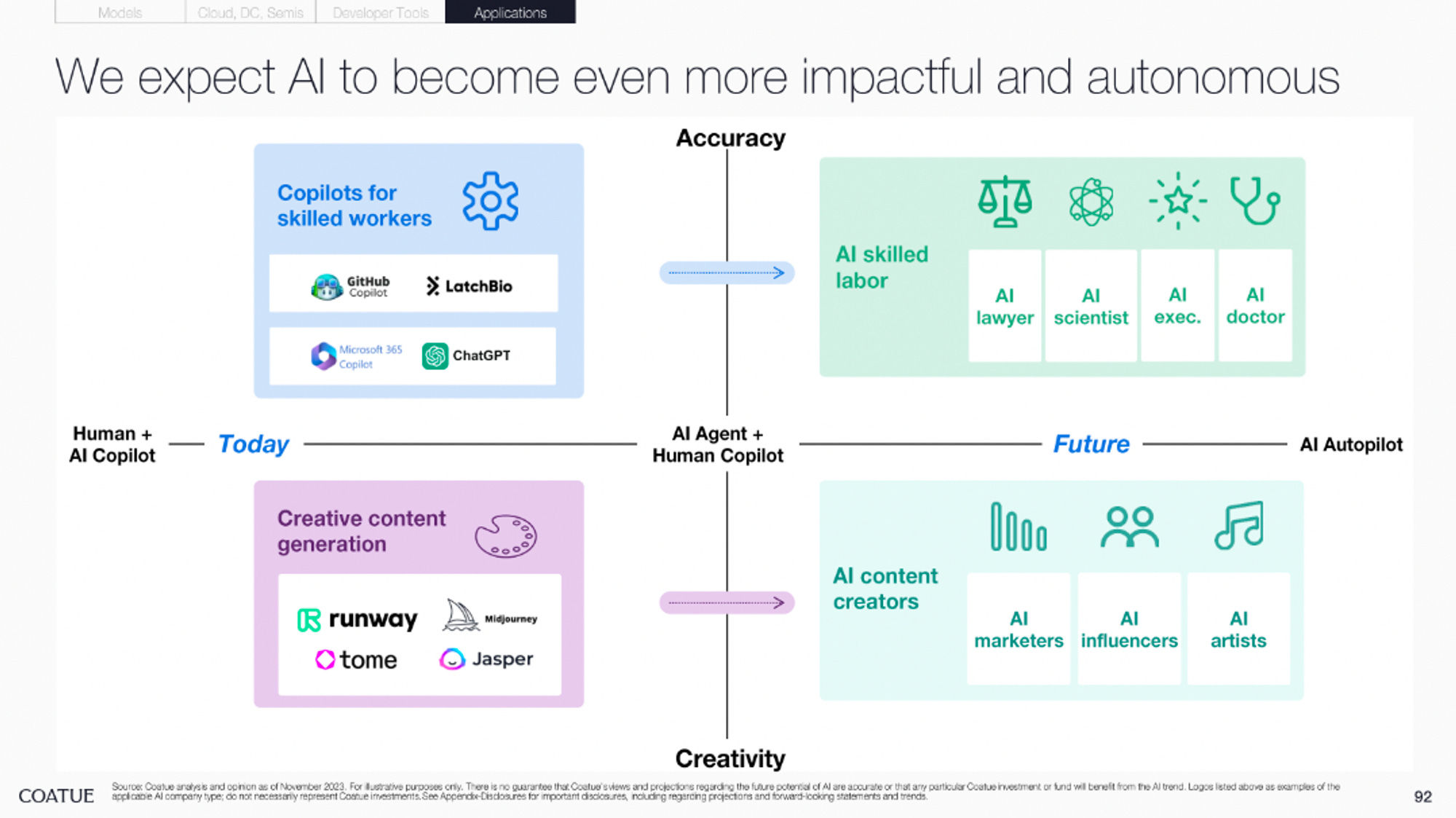

Friday, Nov. 17th: Coatue published an extensive presentation on AI, arguing that it already has a massive impact on our economy and that this influence will only grow in the coming years. They also suggest that AI will lead to significant venture outcomes. - Coatue

Coatue highlights several key trends in AI: (i) the use of natural language to program, language for programming, debugging, and deploying apps, (ii) on-device AI (e.g. on the iPhone), (iii) private datasets are poised to unlock new use cases, including personalized medicine for pharmaceutical companies and on-demand content for entertainment companies, (iv) multi-modality.

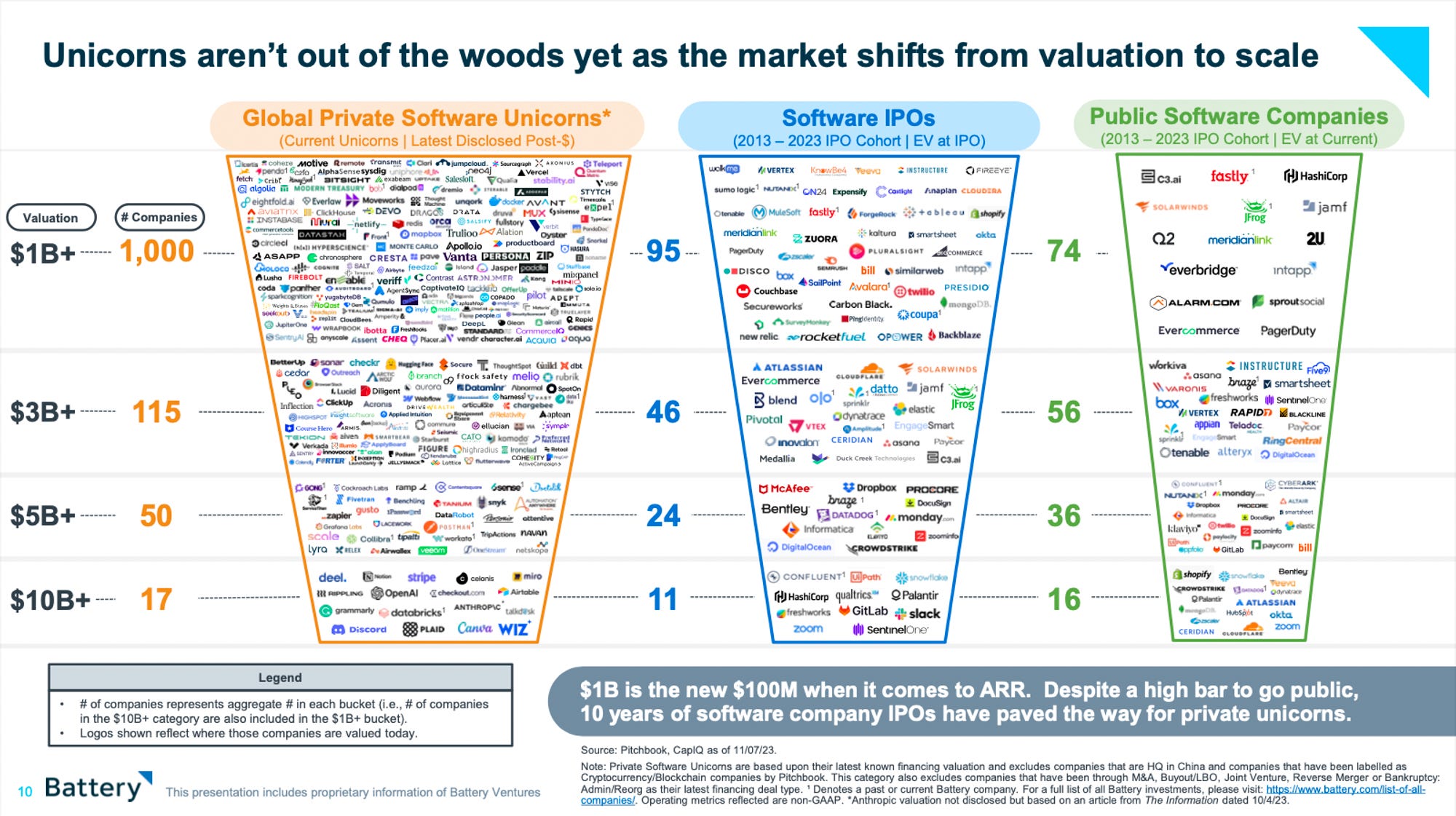

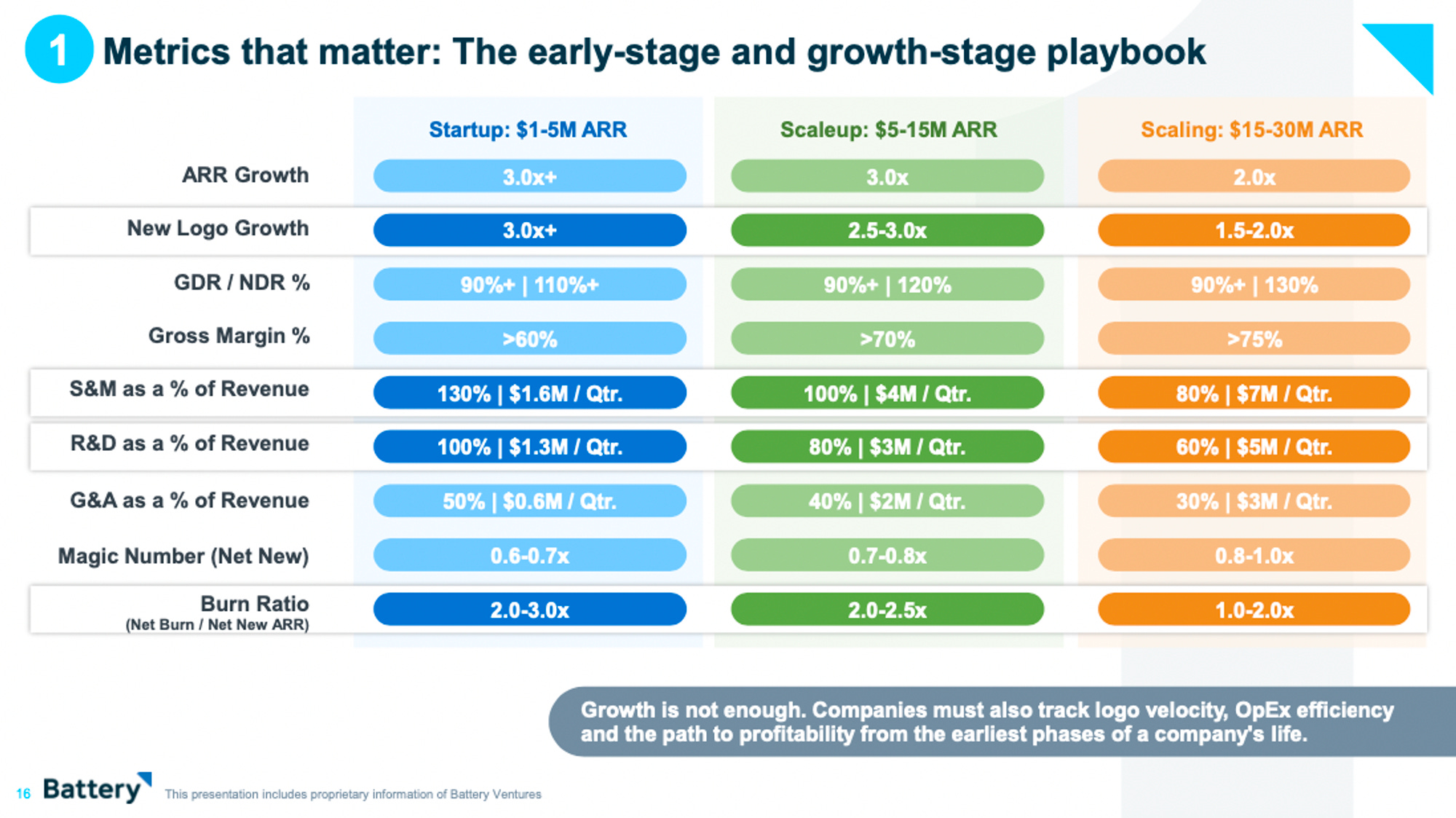

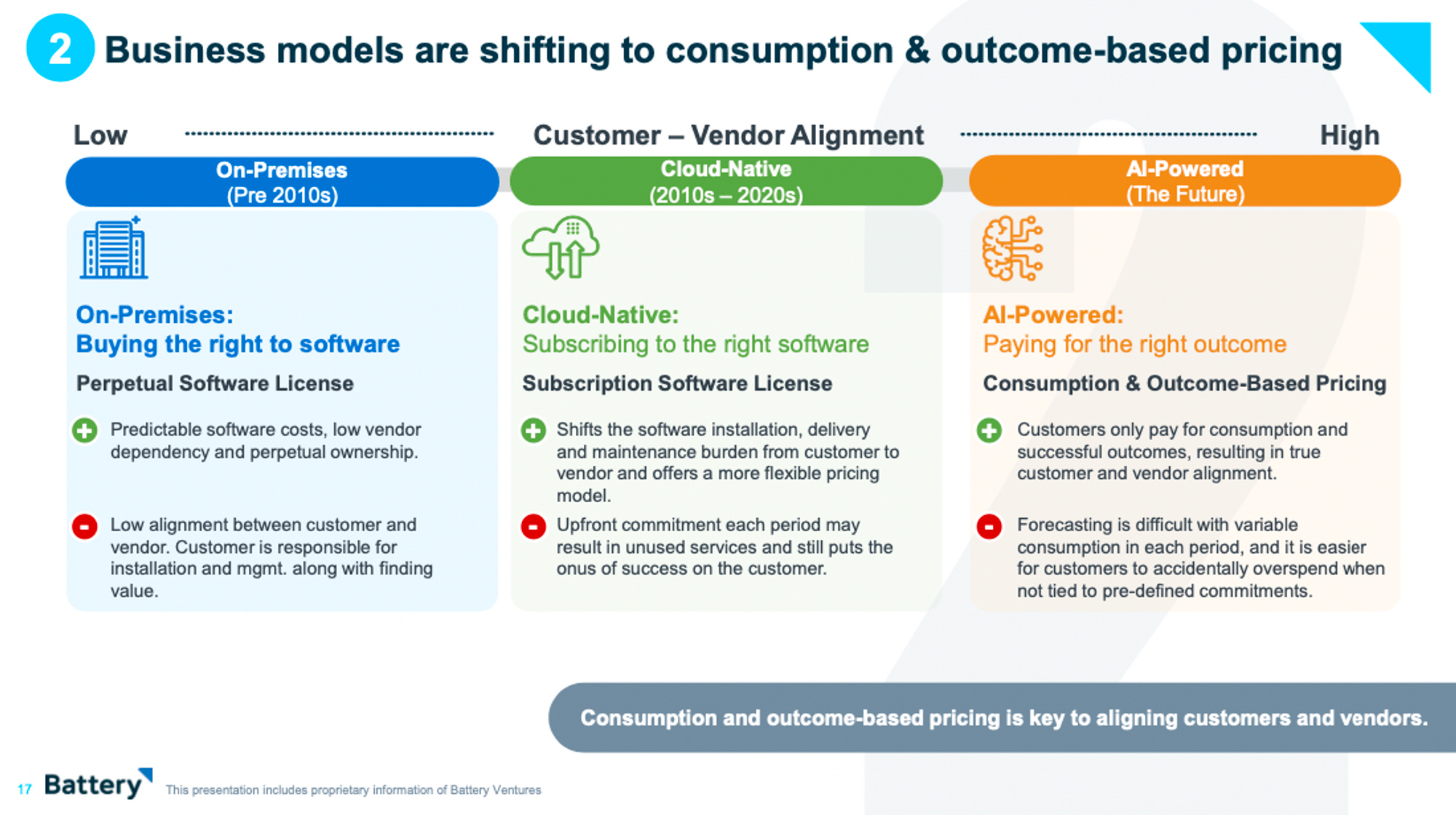

Saturday, Nov. 18th: Battery released its state of the open cloud. - Battery

“We see the technology landscape quietly pivoting toward a horizon brimming with promise as more enterprise-tech companies revert to fundamentals, seeking to balance growth and profitability and capture new efficiencies with AI.”

“We recommend that early-stage and growth-stage software companies focus closely on logo velocity. We know that as companies mature, they rely on expansion revenue to drive growth. However, logo velocity helps to ensure that there is a large enough customer base to fuel future growth, but also aligns sales to balance new ARR and expansion ARR from day one.”

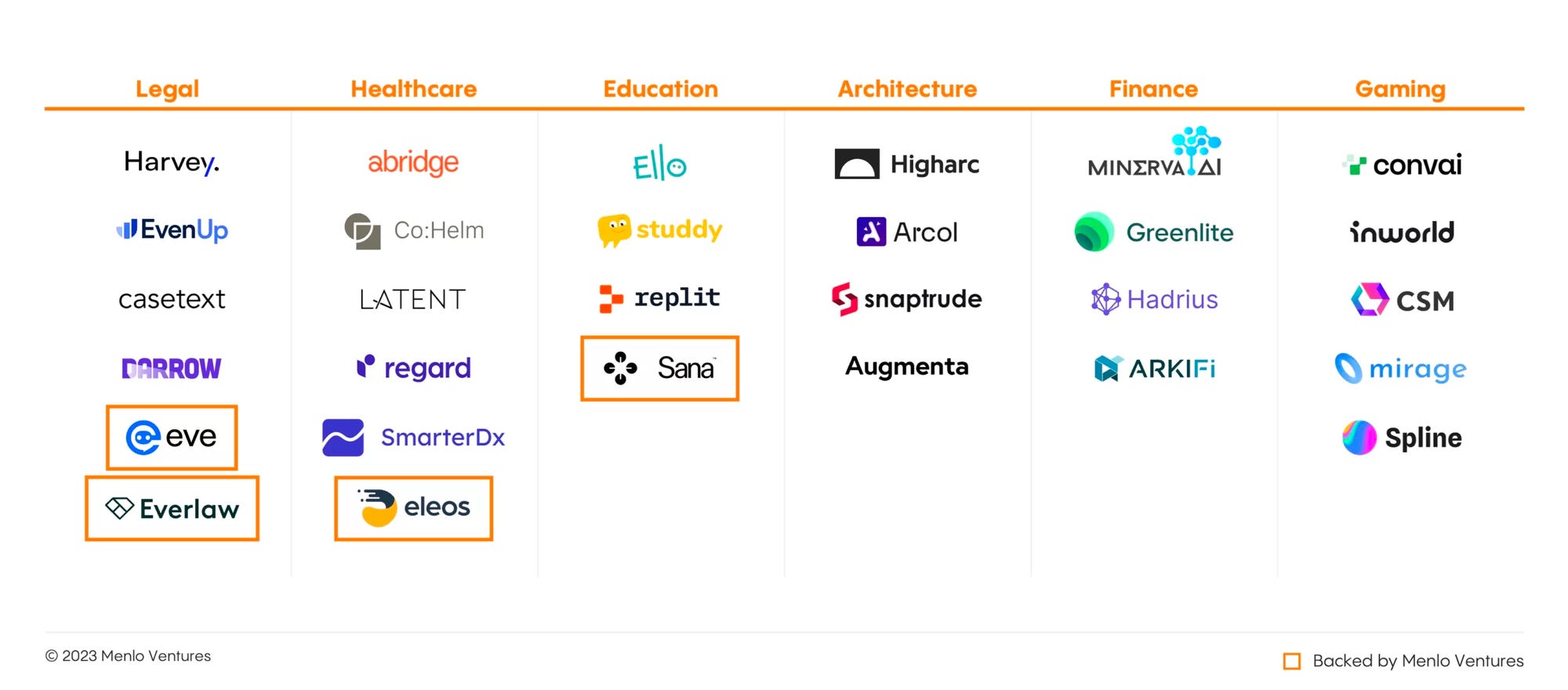

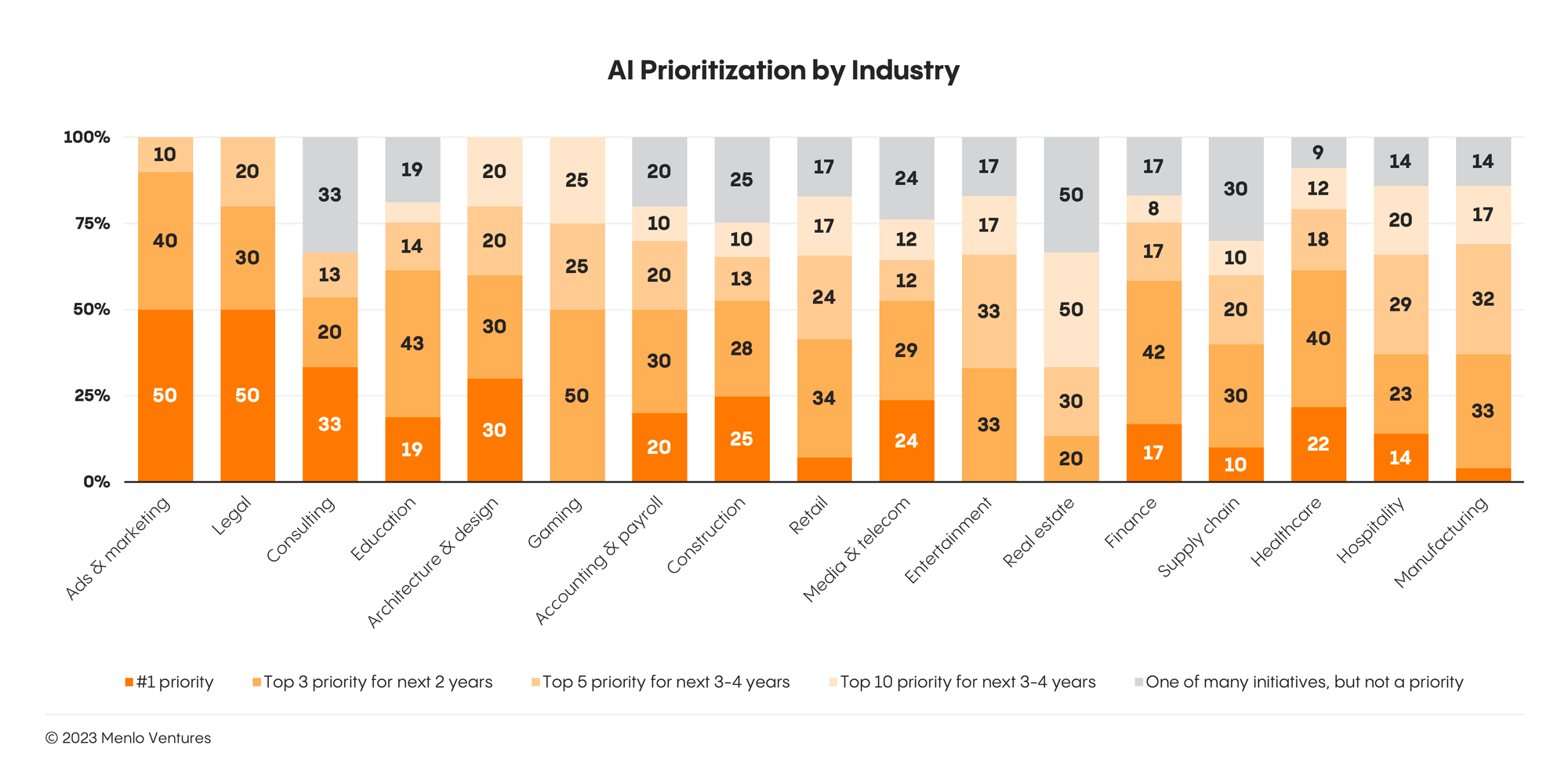

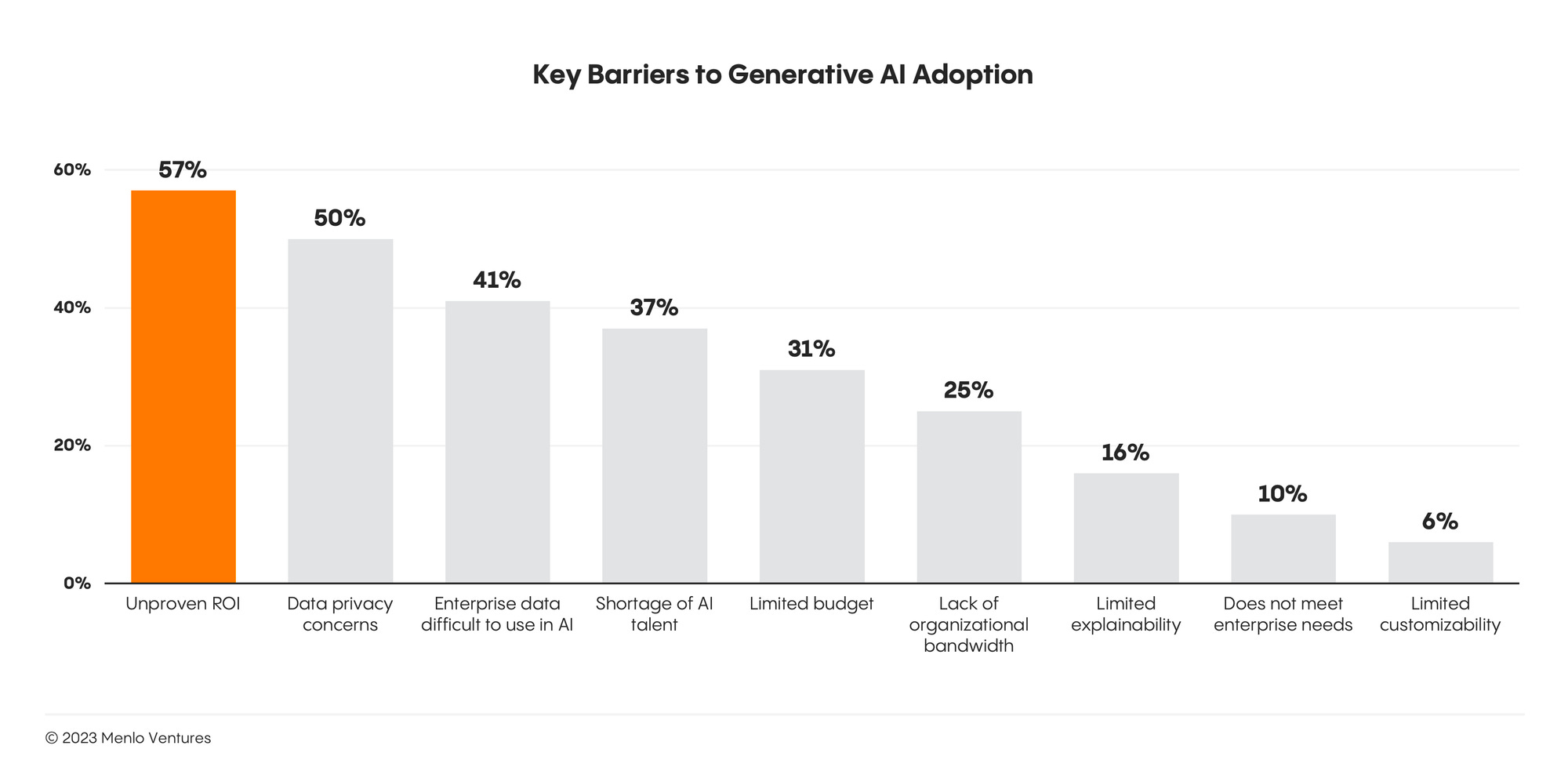

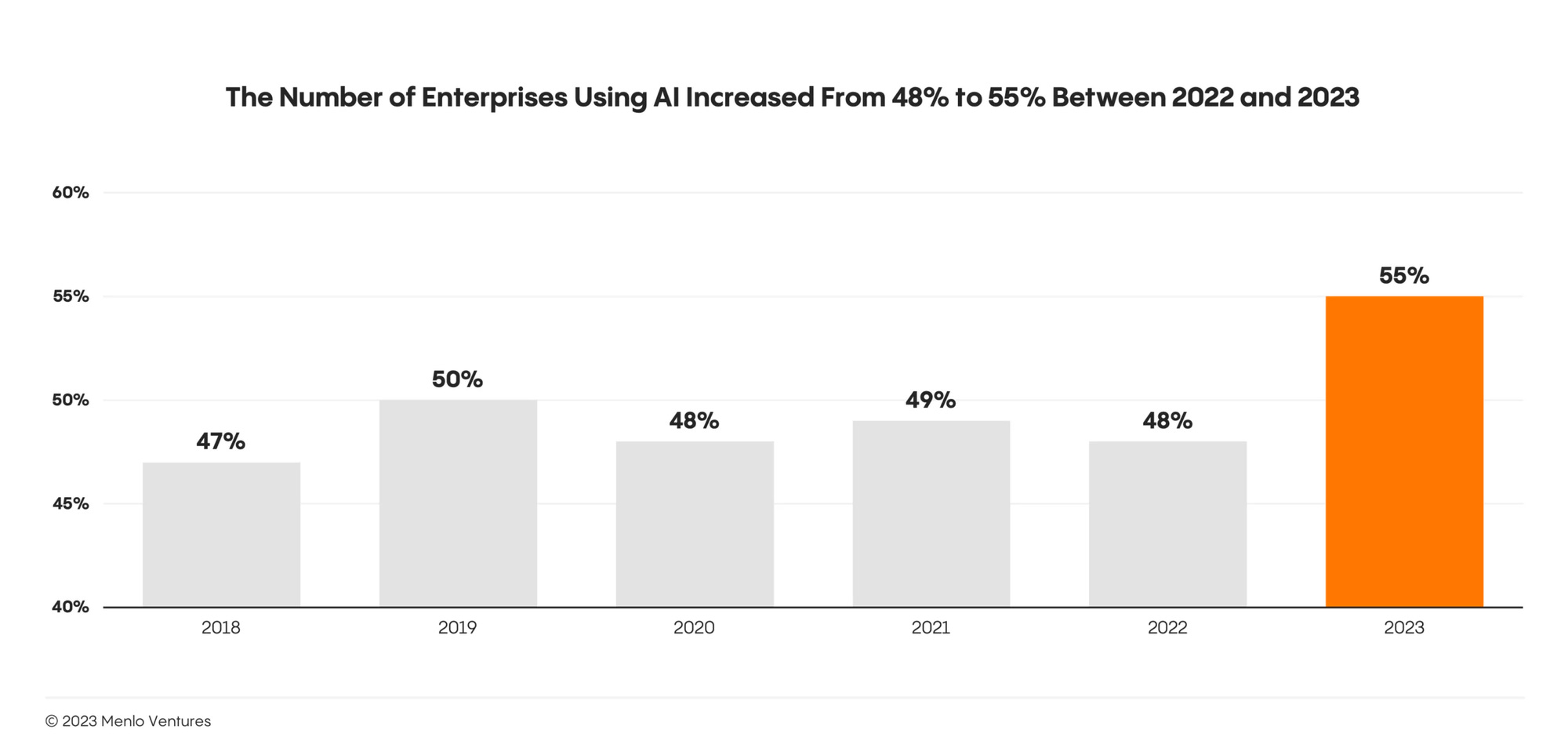

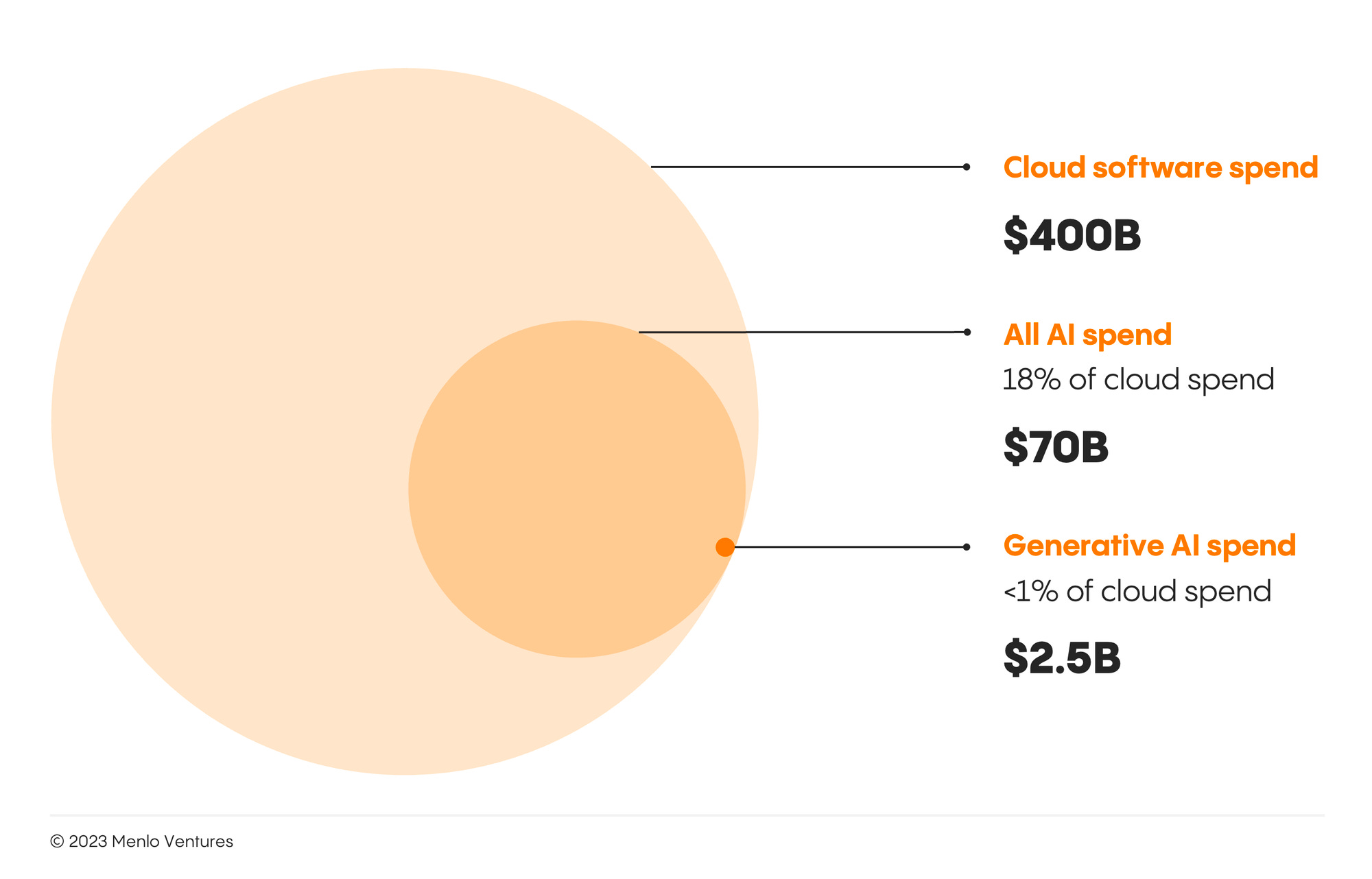

Sunday, Nov. 19th: Menlo surveyed 450+ enterprise executives in US and in Europe to ask them about the impact of generative AI on their company. - Menlo

“Despite the hype, enterprise adoption of generative AI will be measured, like early cloud adoption. The rise of ChatGPT inspired comparisons between the emergence of generative AI and the introduction of mobile technologies and the internet. But, although consumers quickly—and enthusiastically—embraced generative AI, we expect enterprise AI adoption to be slower, resembling early enterprise adoption of cloud computing.”

“The current market favors incumbents who, in contrast to their younger competitors, maintain powerful advantages in scale, distribution, brand, and engineering resources. We expect the incumbent advantage will hold for the next few years until new and more powerful AI approaches, like agents and multi-step reasoning, become prevalent.”

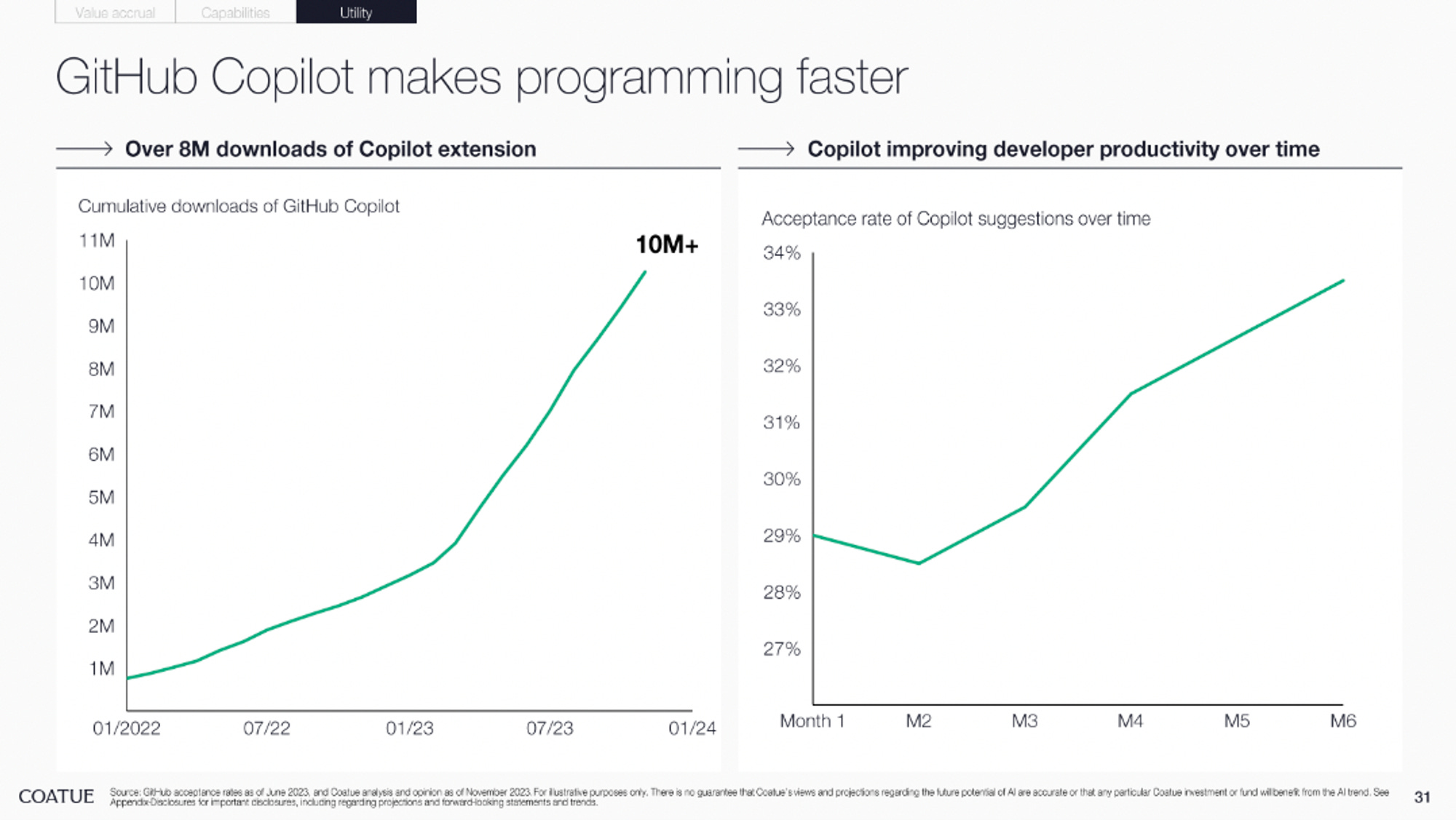

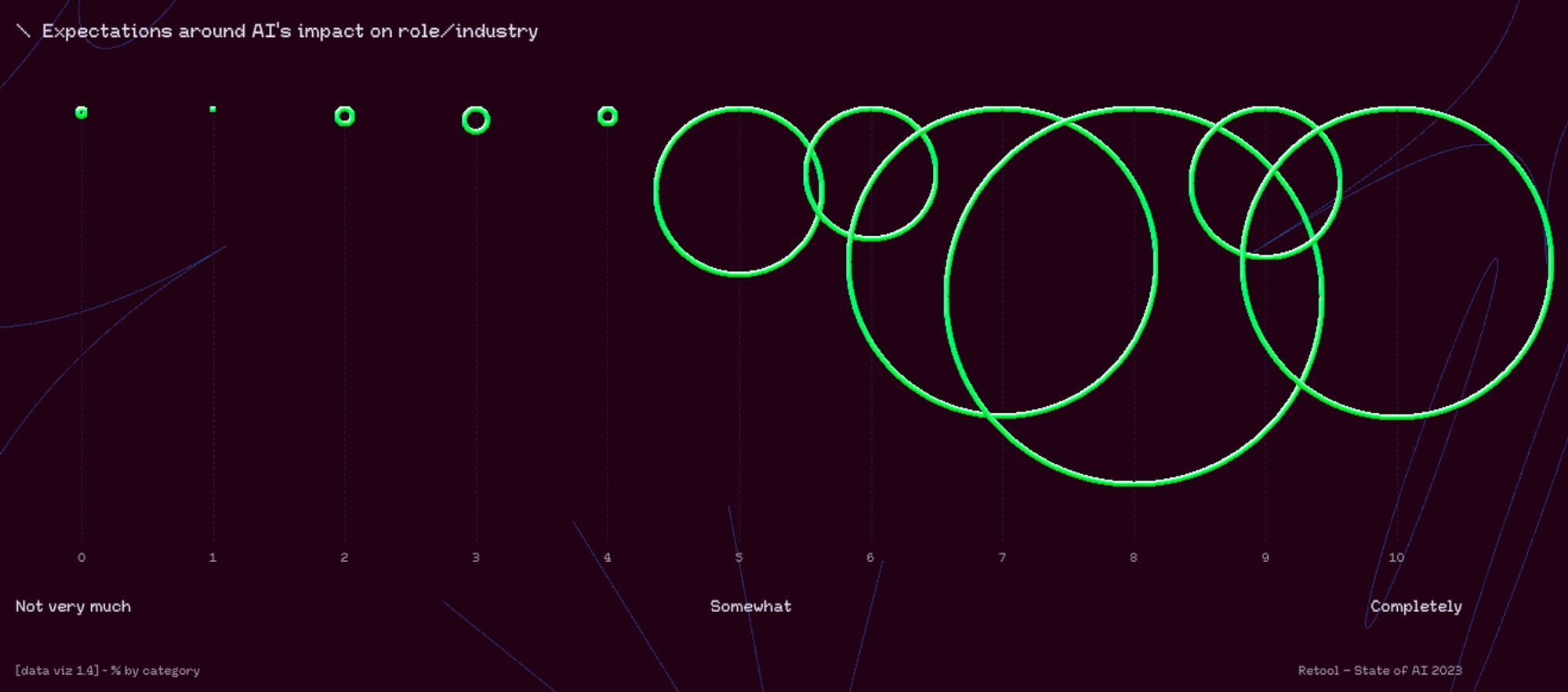

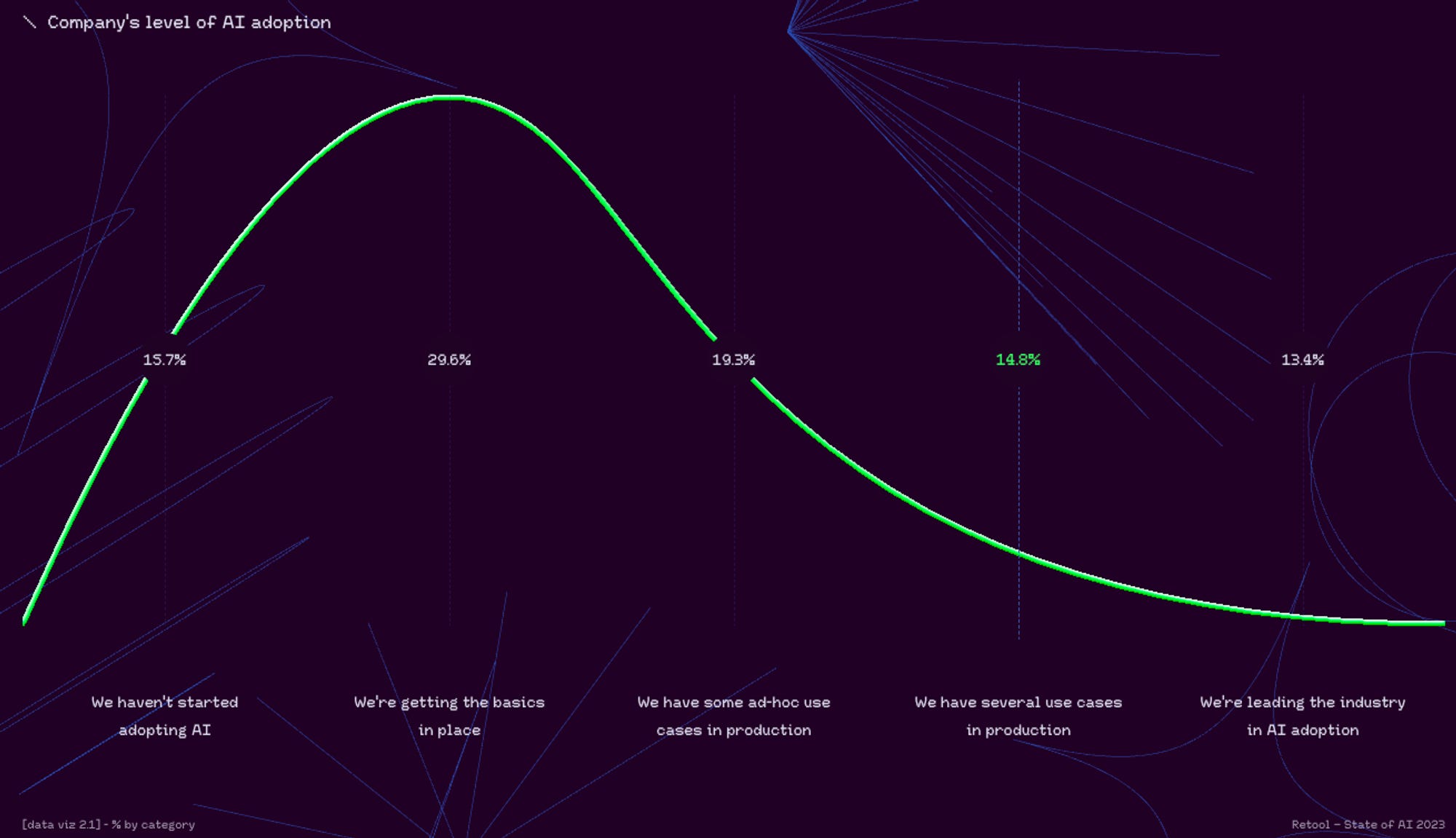

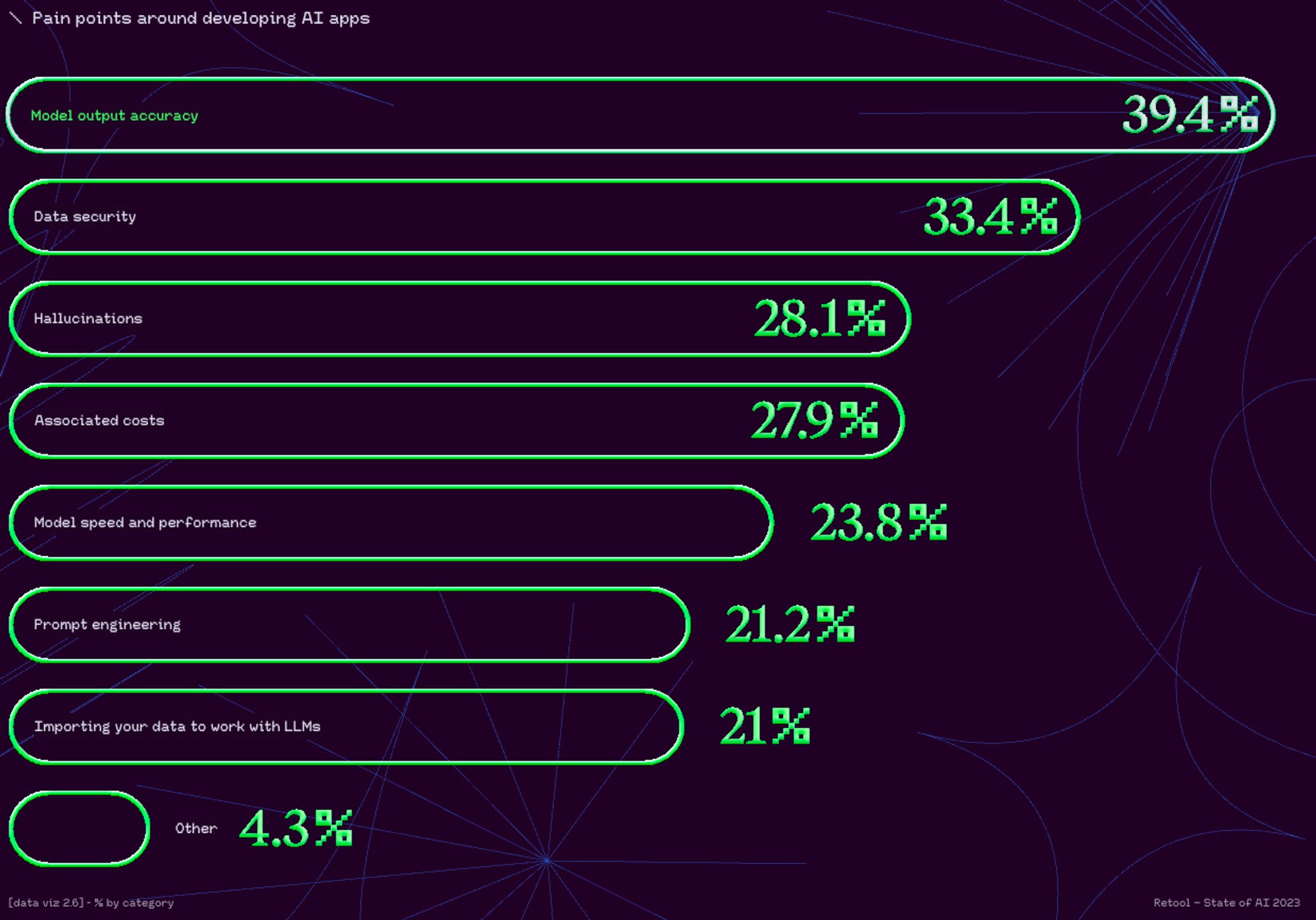

Monday, Nov. 20th: Retool published a report on how AI is used in production by companies surveying 1.5k tech people. - Retool

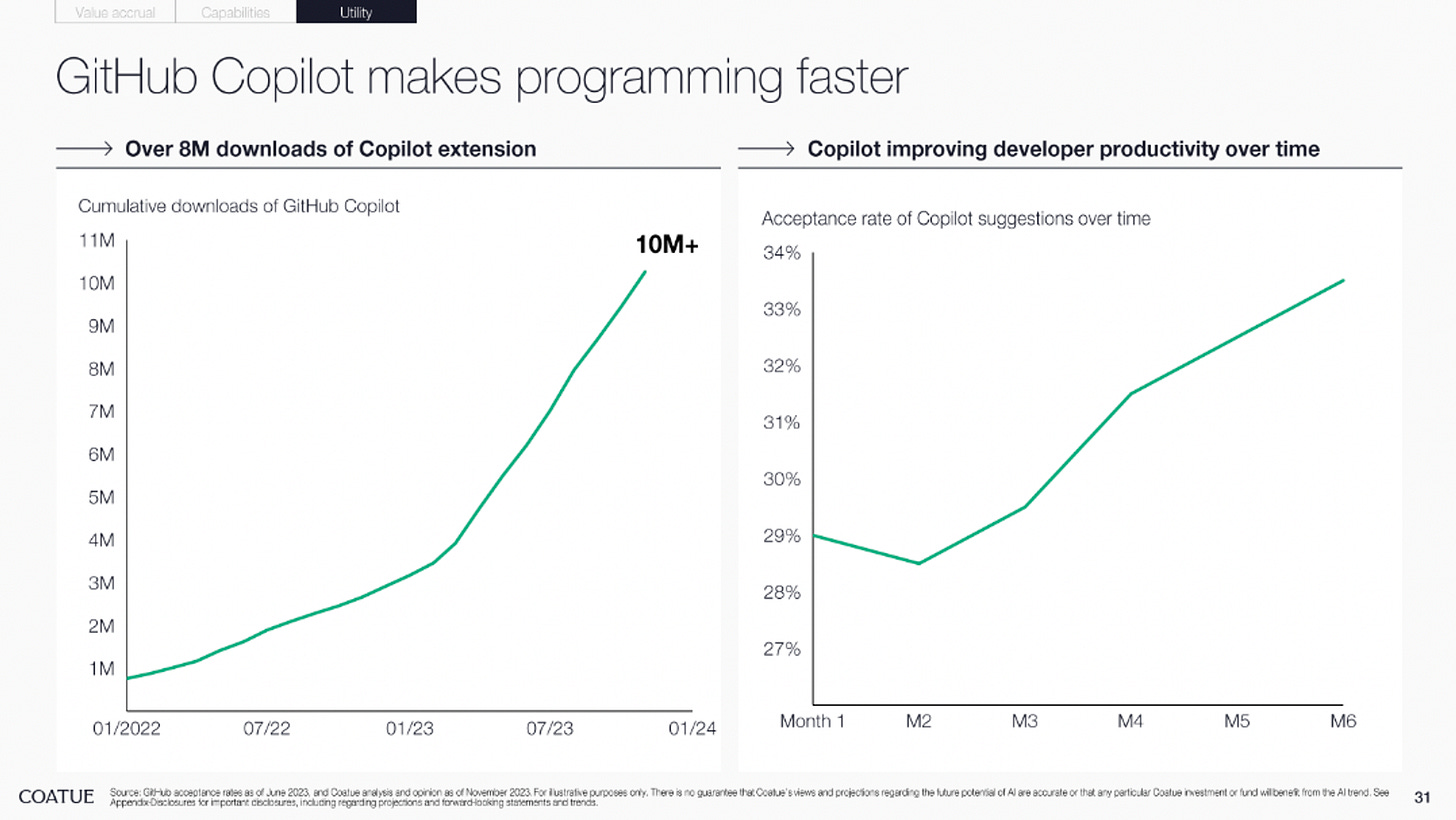

57.6% of developers have reduced their use of StackOverflow since 2022, including 10.2% who have stopped using it altogether. The predominant reason cited for this shift is the emergence of tools like GitHub Copilot and ChatGPT.

66.2% of respondents said that their companies have at least one internal use case live and 43.1% at least one external use case live.

Tuesday, Nov. 21st: Amo recently launched its first social app called ID. It also announced a $18m funding round at a $100m valuation. This round was led by Newwave, with participation from Coatue and DST. ID is a social network designed for interactions with close friends, positioning itself as an alternative to existing social networks that have evolved more into media platforms. Each user on ID is provided with a white canvas, which can be customized with text, photos, and links, and can be filled by either the user or their friends. Additionally, the app features a spatial graph showing all your friends and their connections. Once a user has caught up with their friends' updates, the app will automatically close. - Techcrunch

“The World Health Organization now calls it the loneliness epidemic. And if they say that it’s an epidemic, it’s because it’s actually infectious. In other words, if you’re isolated, your loved ones are too because you’re unreachable. So during the two hours you’re on TikTok, they have no one to talk to. And at the same time, the human needs that the social consumer space can fulfill are no longer covered by these products, whereas they used to be. In the early days of Facebook, I don’t know if you remember, profiles were sort of a mash-up. There were drawings, games, photos, text. You’d write long comments, it could be a poem… And on the other hand, it was a reminder that you mattered to these people.” - Antoine Martin (Amo’s CEO)

Wednesday, Nov. 22nd: Ed Suh who is a venture investor at Alpine wrote an interesting post about being contrarian in venture. - Ed Suh

“VC is an industry with immensely long feedback cycles (7+ years). But practically, practitioners at all levels need to demonstrate short term progress (2-3 years at a time) to develop their careers. […] At all levels, there is immense pressure to show portfolio progress in 2-3 year increments.”

“Aside from exits, which are virtually impossible to come by that early, markups are the interim markers that supposedly demonstrate positive progress. What kinds of companies tend to get higher markups faster? The ones that are perceived to be the "hottest". The speed & magnitude of early markups is more indicative of sector FOMO than fundamentals.”

“What kinds of companies don't raise follow-on rounds as easily? The truly contrarian ones: the ones in unsexy spaces, the ones with off the beaten path founders, the ones that take longer to break out. They're the ones that might have to bootstrap, get profitable faster, and take non-traditional capital in the early days. Eventually, their outstanding metrics speak for themselves, but it can take years in the wilderness before that happens.”

”Everything is harder on the contrarian path. The companies are funkier. They're hard to sell to follow-on investors. They're chronically under-resourced. Everyone doubts the category.”

“The funny thing about VC is while virtually everyone is keenly aware of the returns potential from being contrarian and right, it's extremely difficult to overcome the narrow 2 year view.”

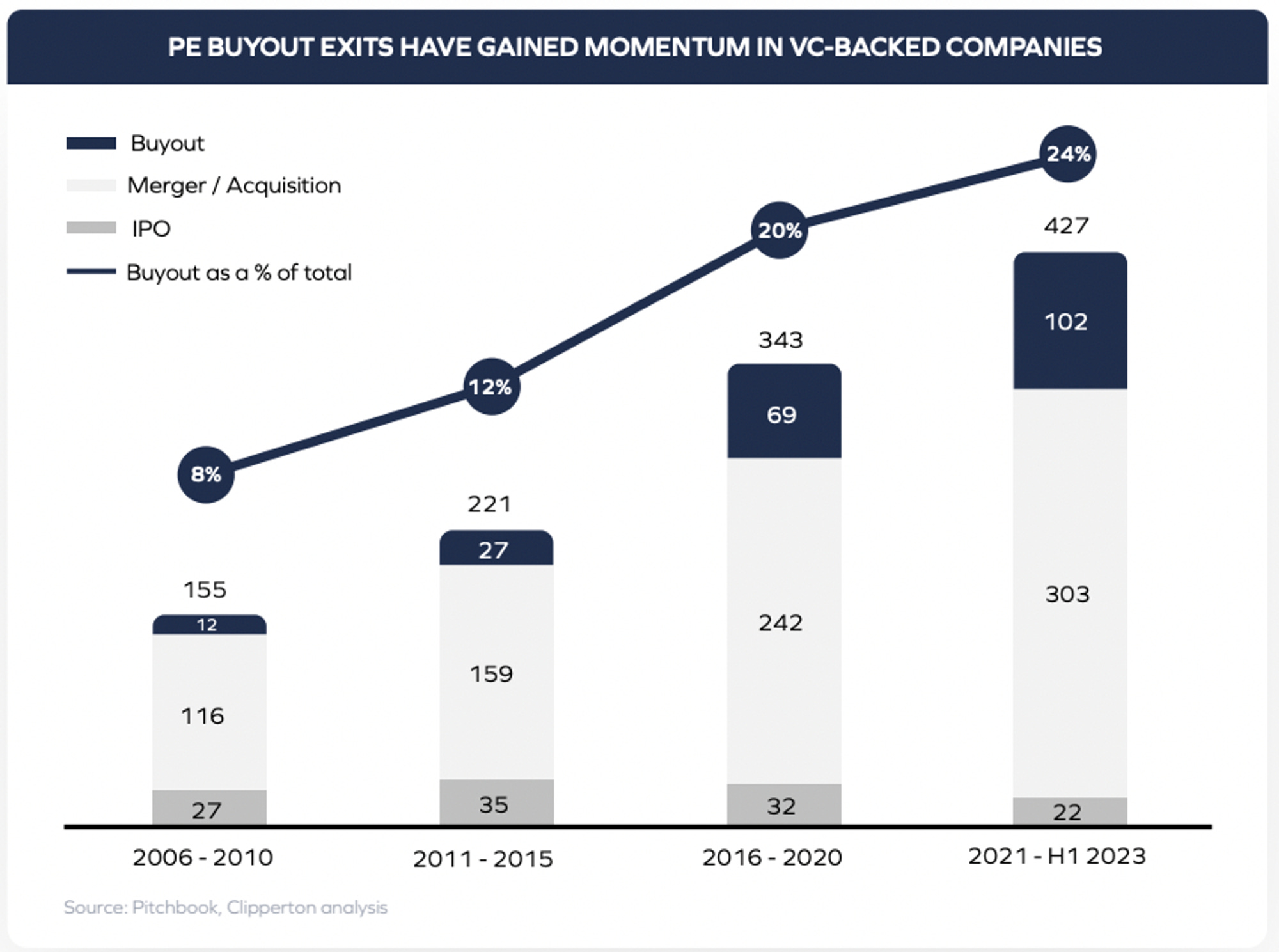

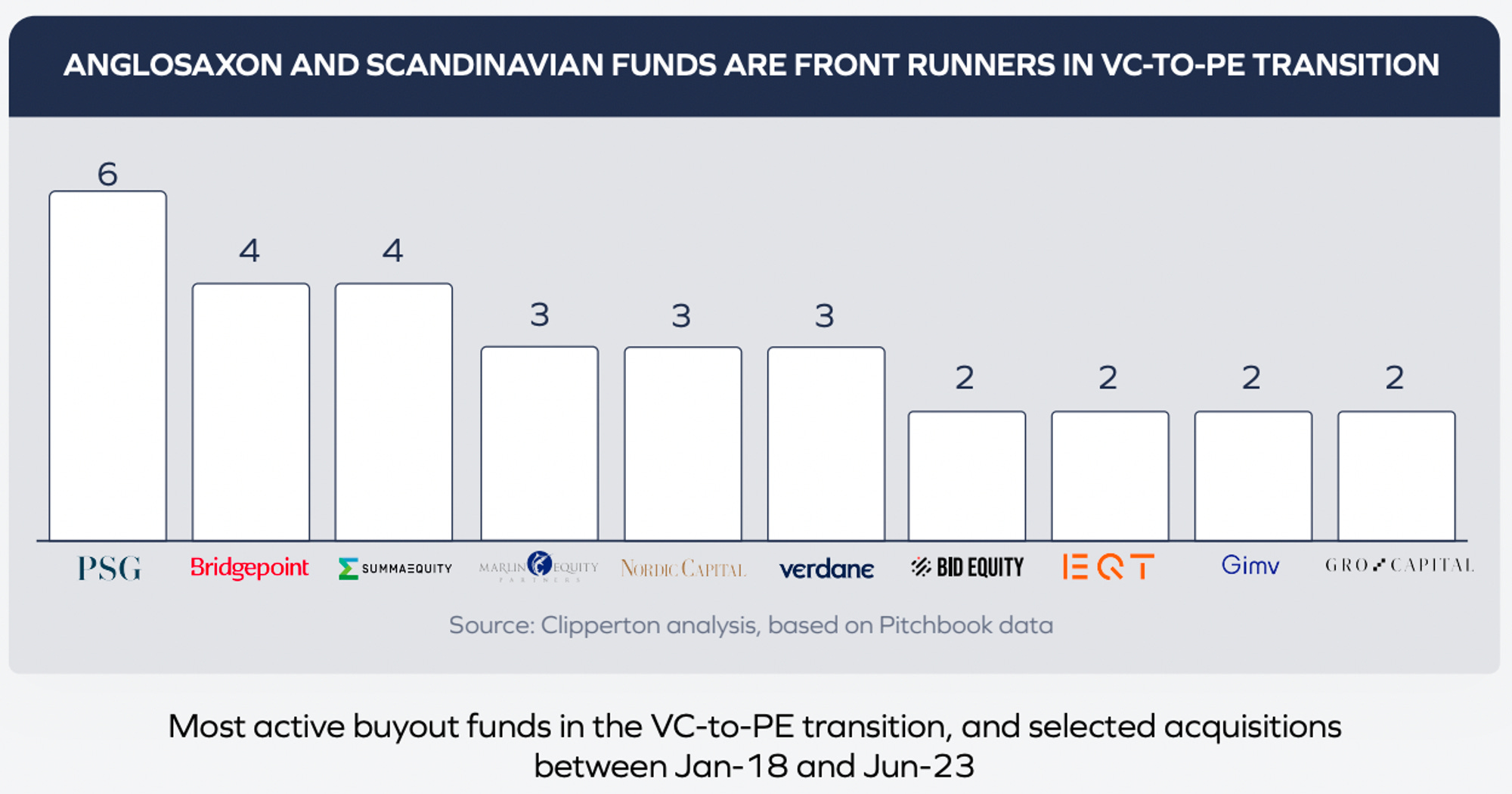

Thursday, Nov. 23rd: Clipperton published a guide for startups aiming to breach the gap between VC and private equity. - Clipperton

“Since 2006, buy-out deals have grown from 8% of VC-backed exits in Europe to 26% in 2023.”

“For European software businesses valued above €30M, PE funds actually accounted for 80% of all exits in 2022.”

There are multiple benefits both entrepreneurs and VC investors to partner with PE funds: “i) maintain a degree of independence, allowing teams to uphold their vision and strategic direction; ii) high chance of success (vs M&A deals with strategic acquirers and IPOs which tend to be more hazardous); iii) high level of flexibility (to decide who gets to cash out, stay on board, partial cash-out, etc); iv) compelling structured incentives for managers (PE deals are often accretive in terms of cap table for the management team); v) on-board a financial partner to drive a consolidation play through external acquisitions.”

“To qualify for an exit via a private equity firm, VC-backed companies need to display specific attributes that appeal to PE firms: they should be profitable or mature enough to provide a clear path to profitability, show capital efficiency, steady growth display, and have a robust customer retention track record along with a solid plan for external expansion.”

Friday, Nov. 24th: Nintendo has developed 17 of the top 20 best sellers in the video game industry. The company has created outstanding IPs including Pokemon, Zelda, Animal Crossing and Mario. These IPs are continually leveraged in new games and other formats (e.g. Super Mario Bros Movie or an upcoming film based on Zelda). - FT

“It can probably be argued that Nintendo has the biggest pool of underutilised IP in the world. One of the debates around Nintendo is the extent to which they become more commercial… Do they find a way for these movies to matter more financially? Do these movies translate into more software sales in aggregate?”

“While there’s a lot of excitement about spreading the IP now, there could be a backlash if it is unsuccessful. Commentators will be writing about how video game companies should focus on making video games and license out the IP [instead] to experts on film, TV and merchandise production.”

Saturday, Nov. 25th: Leo Polovets wrote a post arguing that deep-tech is a great area to build in as an entrepreneur and to invest in as an investor. - CodingVC

“Deep tech is the best place to invest and build right now” because: (i) there are many $1bn+ deep-tech exits, (ii) deep-tech companies have similar capital intensity to traditional tech companies, (iii) the rate of good exits in deep tech is 2x higher than for traditional sectors.

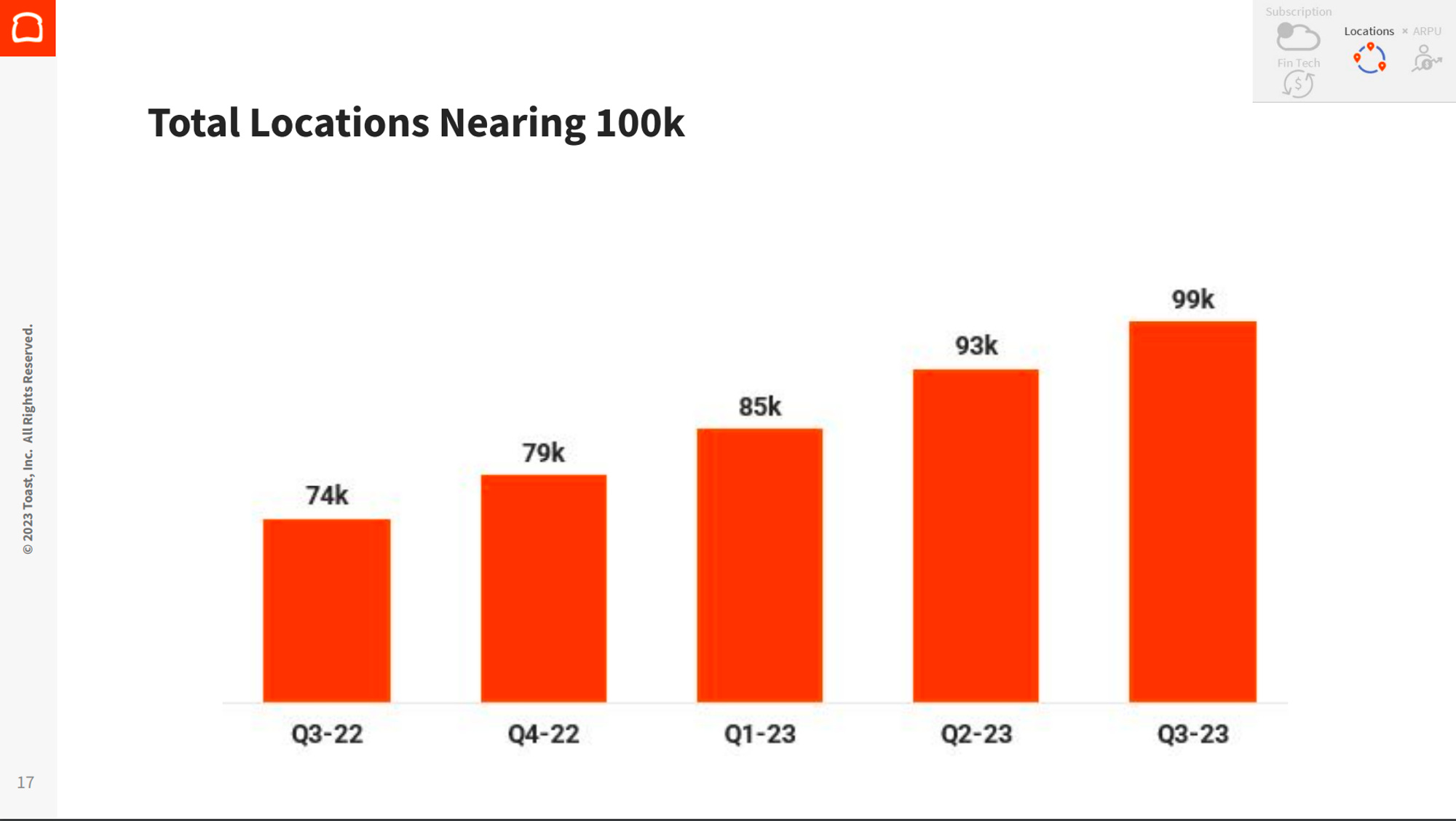

Sunday, Nov. 26th: Toast published its Q3-23’s results reaching $1.2bn in ARR growing at 40% YoY and adding 6.5k locations. It launched a dedicated solution for coffee shops and bakeries to expand into adjacent verticals to restaurants. It also delivered its second EBITDA positive quarter. - Toast

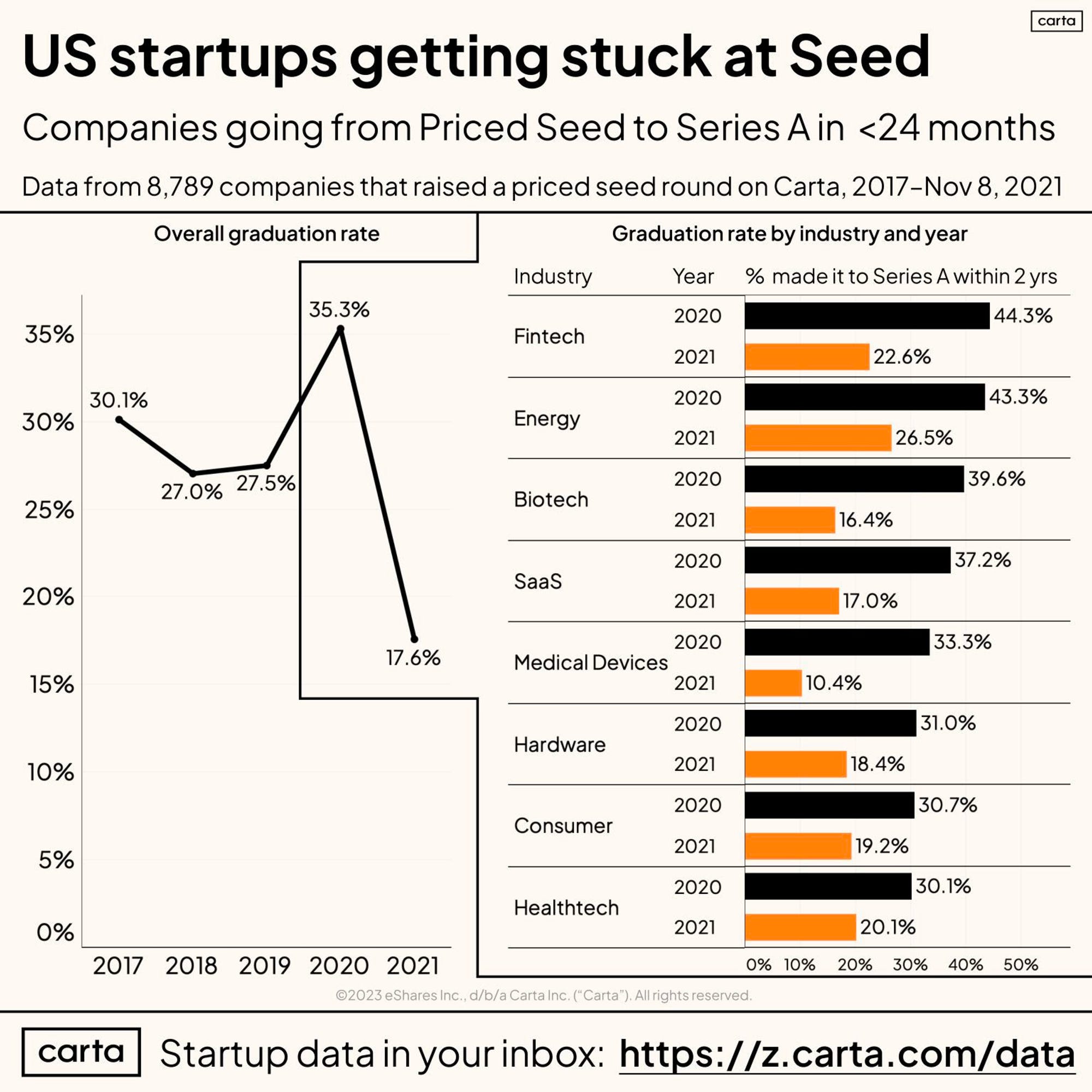

Monday, Nov. 27th: Carta published a graph indicating that the graduation rate from seed to Series A funding has been divided by 2, with fewer than 18% of companies managing to raise a Series A round less than 24 months after securing seed funding. - The Split

Tuesday, Nov. 28th: I read an interview with Investment Group of Santa Barbara’s (IGSB) founder called Reece Duca. - A Letter a Day

IGSB is an investment firm based in Santa Barbara. It does not manage outside money. It has concentrated investments with 80% of their assets in 2-4 companies. It aims to find exceptional companies knowing that it’s extremely hard to find them.

“The most important thing in the investment business is to keep everything absolutely as simple as you possibly can. We think complexity is the biggest barrier to high performance in the investment business.”

“If we had outside investors, and even today, there are not too many investors who have models that would have concentrated investments in public and private and doing the things that we do as part of our everyday model.”

“We think that risk comes from not knowing your companies (vs. concentrating your investments in 2-4 companies). We could de-risk it by knowing our companies better than anyone else would know them.”

“We don’t want to own a 5-10% position in a private company but more around 30-50% because our hypothesis is that if we are going to commit to a private company, we are going to spend a massive amount of time on that company, knowing the industry, and trying to help the management team and be the agent for knowledge transfer.”

There are a small number of exceptional companies. A study from the Arizona State University looked at the performance of 26k public companies between 1926 to 2016 and concluded that only 1k companies were able to create excess returns over the risk-free rate.

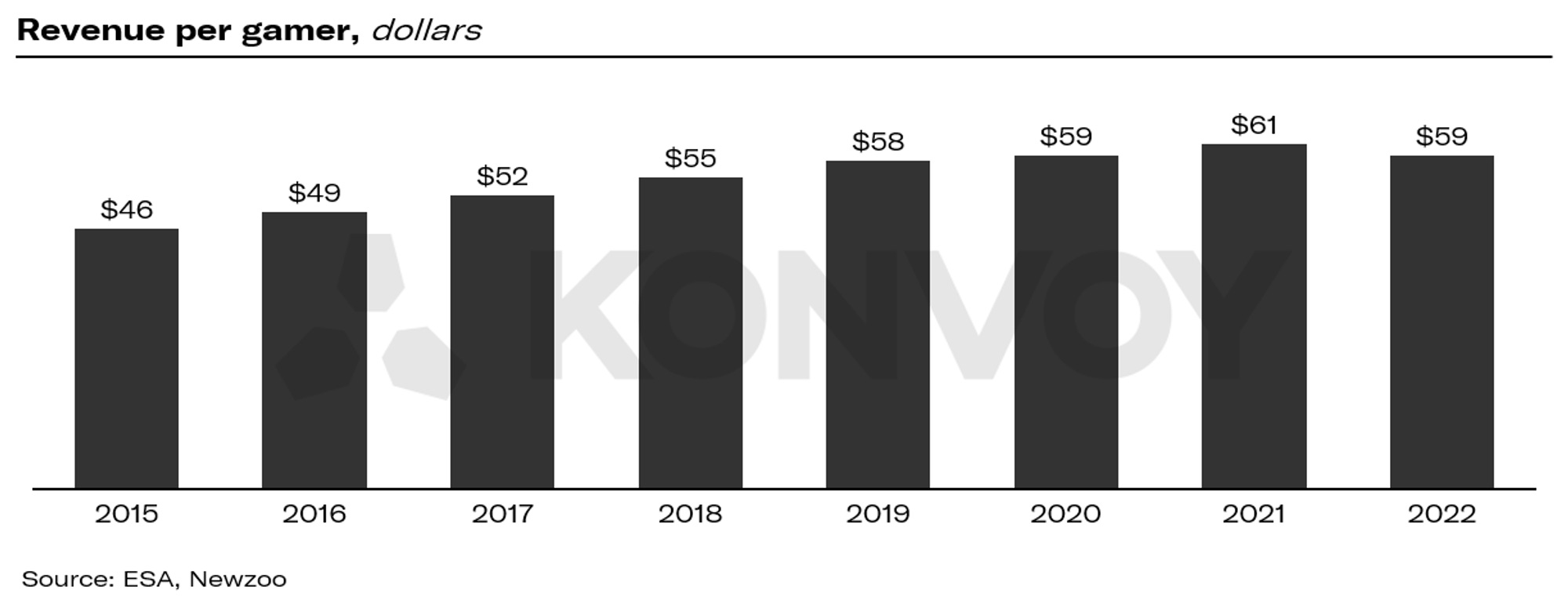

Wednesday, Nov. 29th: Konvoy's analysis of revenue per consumer in the gaming industry reveals that this figure has remained flat over the past few years and is underperforming compared to all other entertainment categories. Several factors contribute to this trend, including the explosion of mobile gaming in emerging markets, the rise of free-to-play games, and studios' reluctance to raise prices for fear of upsetting gamers. - Konvoy

“The growth in the numbers of gamers (6.4% annually) is outpacing the revenue per gamer growth (4.1%) by a factor of 1.5x. In short, we are adding gamers faster than the industry is figuring out how to efficiently monetize them.”

“It is clear that gaming is an incumbent not only of entertainment, but also culture more broadly. Today, gaming is monetizing gamers at ~$59/gamer per year and there is much room for improvement, especially on the price per hour of entertainment at ~$0.07 vs Spotify ($0.18/hr), Netflix ($0.28/hr), or Disney+ ($0.49/hr). We estimate the gaming industry is missing out on an additional $10-30bn in revenue per year given that the revenue per gamer at $59/year has been flat since 2019.”

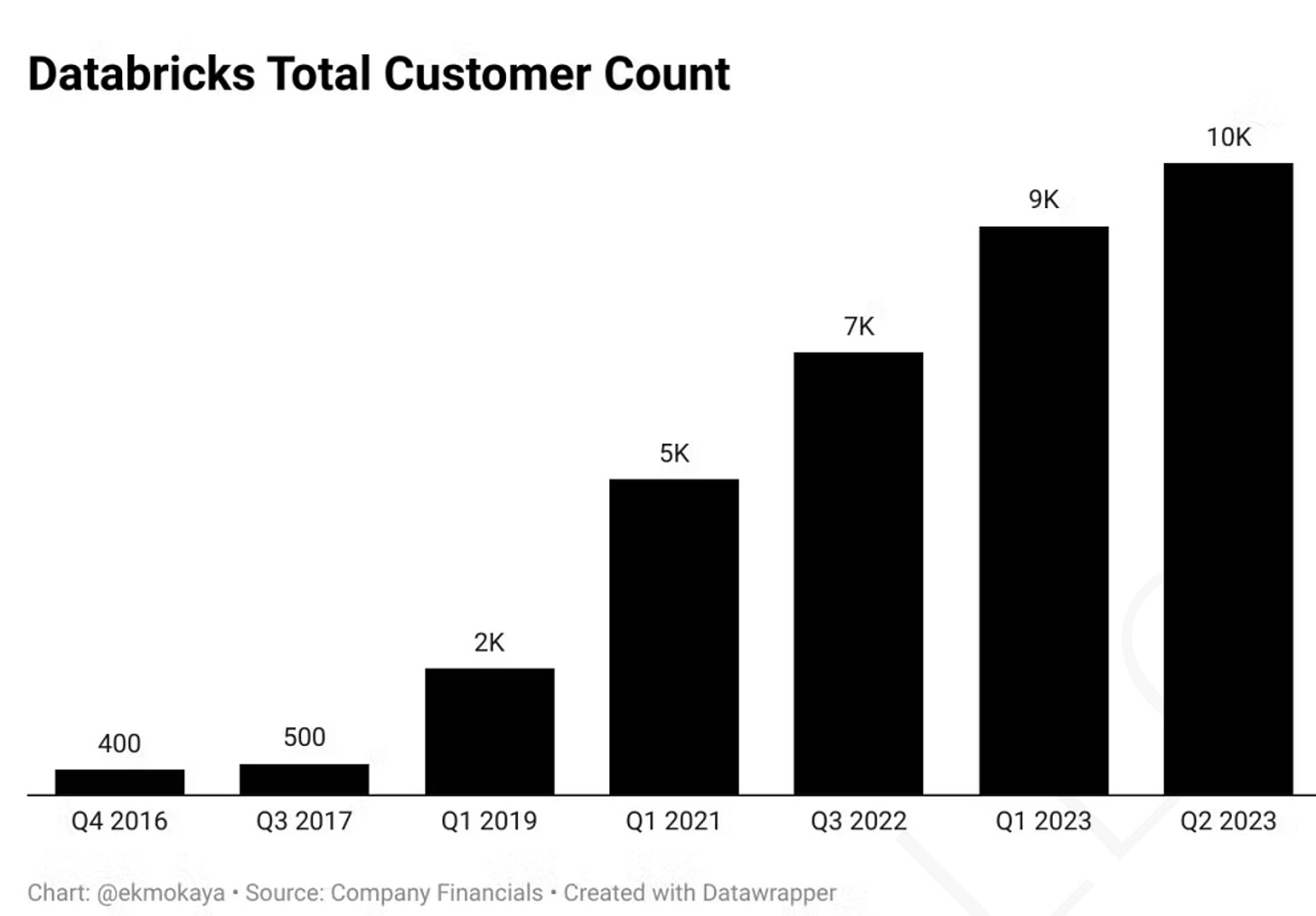

Thursday, Nov. 30th: I listened to a Colossus’ podcast episode on Databricks with Yanev Suissa who is an early investor in the company with SinWave Ventures. - Colossus 1, Colossus 2

“Databricks seeks to simplify and democratize data by combining the best features of data warehouses and data lakes.”

“Databricks Lakehouse Platform is the world’s first and only lakehouse in the cloud and runs on every popular public cloud offering. It's a unified, scalable platform built on open source and open standards: Apache Spark (large scale data processing framework), Delta Lake (secured data sharing across organizations) , and MLFlow (manage the entire ML lifecycle & deploy LLMs).”

Metrics: 9k+ customers, 1.2k+ partners (cloud providers, consulting firms, tech & data companies), $1.5bn in revenues growing 50% YoY, 300 customers generating $1m in revenues, 85% gross margin on SaaS (vs. 56% for Snowflake), $43bn valuation ($500m round done in Sep. 2023).

Databricks is a data processing platform processing both structured data (data organized and formatted in a predictable way to be stored in a spreadsheet or a database making it easy to search, process & analyse data) and unstructured data (movement-based data or data that is not in a defined set of columns and spreadsheets). Databricks started in unstructured data processing before adding structured data processing when Snowflake was doing the inverse path.

Databricks has three core products: (i) streaming analytics to deploy Apache Spark, (ii) lakehouse to process both structured and unstructured data to compete directly with Snowflake (in 18 months, this product went from $0 to $200m in revenues) and (iii) AI platform to run AI models and used them on your proprietary data (from the Mosaic’s acquisition).

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋