🗞 Venture Chronicles - November 2022

Overlooked #132

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of November.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for November!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Tuesday, Nov. 1st: I listened to a Colossus’ podcast episode starring Steven Galanis, Cameo’s cofounder and CEO. - Colossus

The marketplace, started in 2016, enables people to book personalised video messages from a pool of 50k pop culture, sports and entertainment celebrities. Cameo helps celebrities monetise their social following in a brand positive way. Cameo’s has a 25% take rate on transactions.

There is a class of celebrities who is more famous than rich. For instance, 80% of NFL players go broke five years after playing their last game.

How does Cameo size its market? There are 2.5m celebrities that could be monetizable on Cameo and that this number will double in the next 5 years as there are new celebrities emerging everyday on the Internet.

Cameo is a managed marketplace with a customer support team working with celebrities on topics such as pricing, promotion strategy or referrals.

Celebrities have 7 days to shoot the video. It they don’t do it, fans are refunded. If a celebrity has completed its last 3 Cameo’s requests, there is a 97% chance that he or she will complete the next request.

Cameo has a unique viral flywheel. Celebrities promote their Cameo’s link on their social media, driving demand from fans for free for the marketplace.

Cameo has a Net Promoter Score (NPS) in the 70s and a 4.99 score on online stores. Customers only complain when celebrities do not record their videos or when they have to wait for 7 days.

Supply on Cameo is non-fongible (vs. drivers on Uber or restaurants on DoorDash).

Celebrities select their own pricing but the most optimised price is between $125 and $250.

Cameo has been working on different growth projects: (i) increasing repeat purchases by offering other products (e.g. Zoom calls with the celebrity), (ii) Cameo for businesses (products tailored to companies) (iii) add-ons to increase AOV (priority booking to complete the video in 24 hours, additional characters in the message given to celebrities), (iv) acquiring Represent which is a merchandising as a service offering for celebrities.

Wednesday, Nov. 2nd: Sønr published a ranking of the top 100 insurtechs. It includes several Eurazeo portfolio companies such as WeFox (n°3), Yulife (n°10), Descartes Underwriting (n°13), Qoala (n°45) and +Simple (n°82). - Sonr

Coalition was founded in 2017 in the US as a cyber-insurance MGA for small and medium enterprises. It raised $750m including a $250m series F from AllianzX in Jul. 2022 at $5bn valuation. It generates $740m in premium (3x YoY growth) and has 160k customers (3x YoY). Coalition struck a multi-year partnership deal with Allianz to get capacity for its operations both in the US and in the UK.

Descartes was founded in 2018 in France as a parametric insurer for climate risk. It raised $141m in total including a $120m series B at a $500m+ valuation. It works with several data providers such as ICEYE (flood hazard), Global Earthquake Model Foundation (open-source SaaS for hazard) and Reask (climate analytics & data company).

Thursday, Nov. 3rd: Merge raised a $55m series B led by Accel with the participation of existing investors NEA and Addition. Merge started in June 2020 in the US. It started as a payroll/HR/accounting API provider before becoming more horizontal, adding API integrations to other categories of products such as CRM tools, project management and ticketing systems. Its ARR grew by 12x in the past 12 months and it now has 3k customers (inc. Divvy, Appolo.io, Ramp, AngelList). - Techcrunch, Merge

Friday, Nov. 4th: I read a post from the Weekend Fund on how VCs win hot deals. There are 3 main takeaways: (i) have a relevant, differentiated and authentic pitch, (ii) do the job of an investor before investing (show founders that you can help them), (iii) offer a good founder UX (show up well prepared, be responsive, run a transparent process). - Weekend Fund

Saturday, Nov. 5th: I read a deep-dive from Mario Gabriele on Softbank. - The Generalist

In 2022, Softbank lost $40bn in value. It plans to lay-off c.30% of its investors.

Softbank started in the 1980s as a software distributor and a publisher of technology magazines. It went public in 1994 raising $140m.

After the IPO, Masayoshi Son started to use Softbank to invest in early stage startups.

In 1995, it invested $2m in Yahoo. 4 months later it invested an additional $105m into the company for a 33% stake. Yahoo went public 2 months later. Softbank further reinvested $250m into the company. In 1999, Softbank’s stake into Yahoo peaked at $8.6bn.

In 1996, Softbank and Yahoo did a 60-40 joint venture called Yahoo Japan which became the dominant local search engine and reached a $4.5bn valuation in 1999.

In the mid-to-late 1990s, Softbank ended up investing into 800 startups (inc. E-Trade, Geocities, ZDNet and Webvan).

In 2000, with the explosion of the tech bubble, Son personally lost $70bn in twelve months. He also made its best ever investment by investing $20m into Alibaba before the company was generating any revenue.

In the 2000s, Masayoshi Son rebuilt the Softbank empire around technology. He secured a licence for mobile spectrum. He bought Vodafone Japan for $20bn. He stroke a deal with Apple to be its exclusive distribution partner in Japan.

When the $100bn Vision Fund I was raised, it was 30x bigger than any other fund in venture capital. Masayoshi Son was the only decision maker on this fund. Staffing an investment team that has to work together has been a messy exercice. Investors were fighting for Masa’s attention. Finding good deals was replaced by finding deals that would please Masa.

Vision Fund I was supposed to invest in AI. It ended up pouring hundreds of millions into private market leaders to help them establish their leadership and invest in long term projects (which is not necessarily a bad strategy as “overcapitalizing the winner is the only legal way to establish a monopoly”) with a preference for atoms over bits (e.g. investments in WeWork, Uber, Oyo, Didi, Coupang).

For Vision Fund II, Softbank raised $56bn exclusively from its balance sheet because Masa did not want to be associated with Saudi Arabia anymore and because Fund I was underperforming. Softbank adopted a new strategym building a more diversified portfolio with smaller entry tickets.

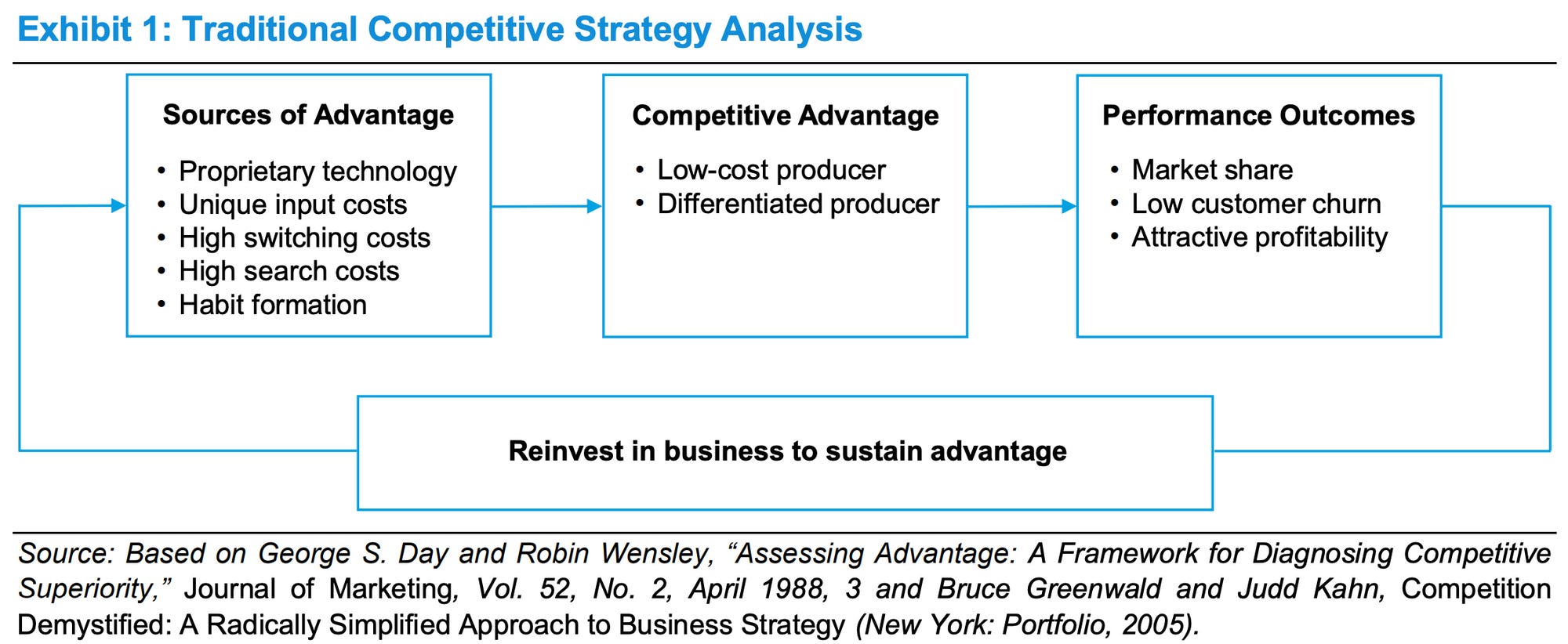

Sunday, Nov. 6th: Morgan Stanley shared a broker note on competitive advantages. - Morgan Stanley

“We define sustainable competitive advantage as a company’s ability to generate returns on investment above the cost of capital, and higher than its competitors, for an extended period.”

“A traditional approach to assessing a firm’s competitiveness considers the potential sources of advantage, determines whether those sources translate into a competitive advantage, and validates the existence of competitive advantage by examining measures of performance, including market share and profitability.”

There are 3 levers to increase the willingness to pay: (i) network effects (value of a product/service increasing as more people use this product/service), (ii) complements (good/service consumed with another good/service like Android and Google Search) and (iii) branding.

“Achieving a sustainable competitive advantage is difficult for a business that competes in an industry where there is instability in market share. As a general observation, market share instability tends to be high as an industry emerges. During this phase competitors jockey for market fit and new competitors join the fray. Market shares then become more stable as the industry shakes out.”

“A company can create an opportunity to enhance market power by increasing willingness to pay and decreasing willingness to sell.”

Monday, Nov. 7th: I read a cyber-insurance report published by the French government. - Direction Générale du Trésor (in 🇫🇷)

In France, cyber-insurance remains a small market. It generated €219m in premium in 2021 mainly driven by large corporations. Companies with more than €500m in revenues generated 75% of the cyber insurance premium in 2021. The cyber-insurance market grew by 119% between 2019 and 2021. In 2021, 54% of French companies suffered from a cyber-attack. In 2021, 92% of claims captured only 7.4% of cyber-insurance premiums. 84% of large companies have a cyber-insurance compared with 9% for medium businesses and less than 0.3% for small businesses. Cyber-insurance had a 84% loss ratio in 2019, 167% in 2020 and 88% in 2021.

Several factors explain this market size: (i) SMBs are not aware of the cyber-risk they’re facing and do not know how to evaluate cyber-insurances, (ii) incumbent insurers and reinsurers are not able to correctly price the cyber-risk and are scared that cyber-attacks are a systemic risk, (iii) the national regulatory framework around cyber-insurance is not clear enough (e.g. silent cover, how to deal with ransom-wares?)

There are several categories of cyber-attacks: (i) malwares, (ii) phishing, (iii) Denial of Service, (iv) man-in-the middle (capturing communications that are not supposed to be captured), (v) zero-day (exploiting a vulnerability that has not been corrected in a software).

The cyber-risk is hard to measure for incumbent insurers because (i) it’s a recent risk with a limited history to use as a baseline to underwrite insurance policies, (ii) it’s a risk that is constantly evolving, (iii) it’s hard to have a real count of cyber-attacks because companies don’t want to tell the world they’ve suffered from one.

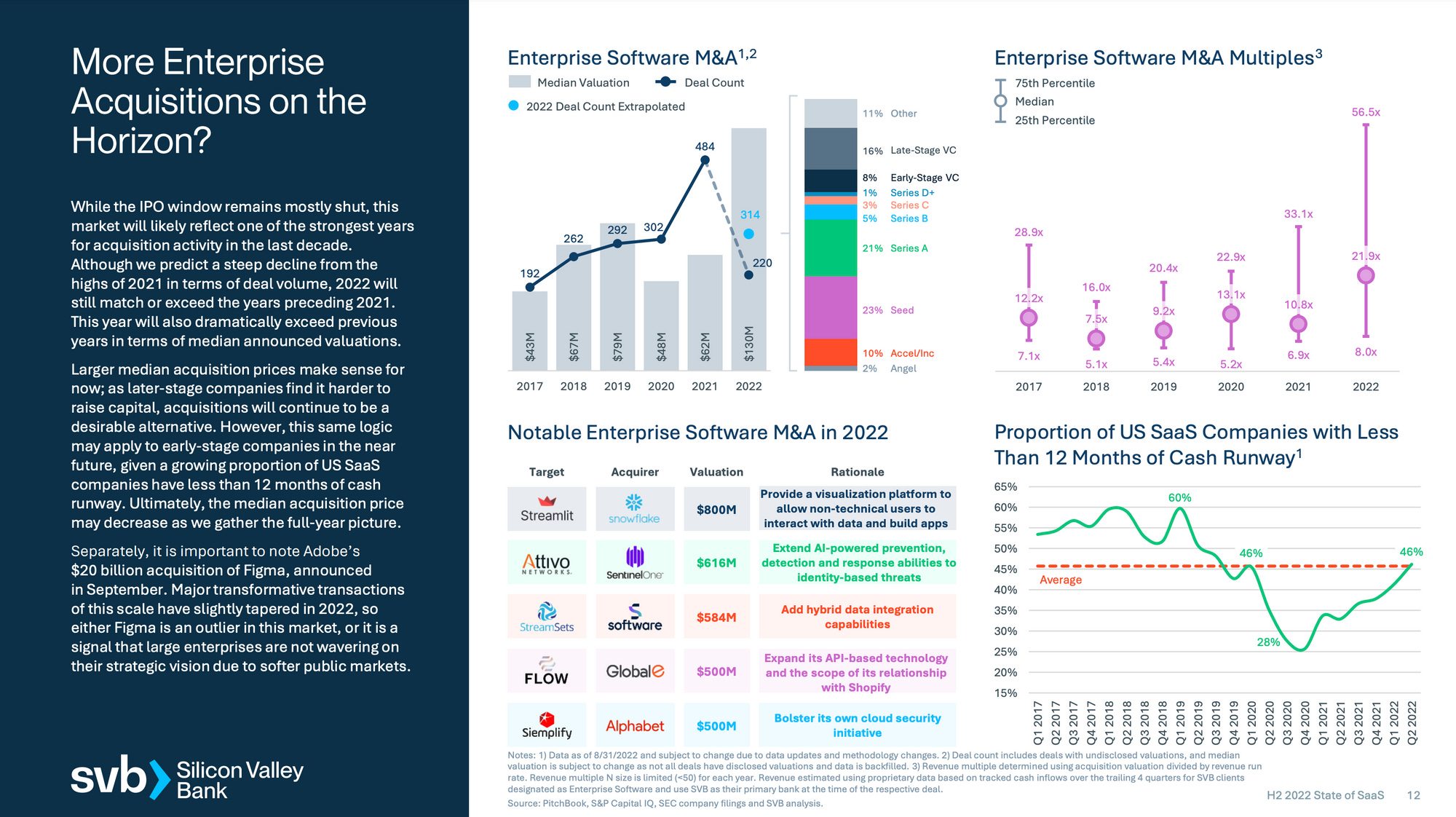

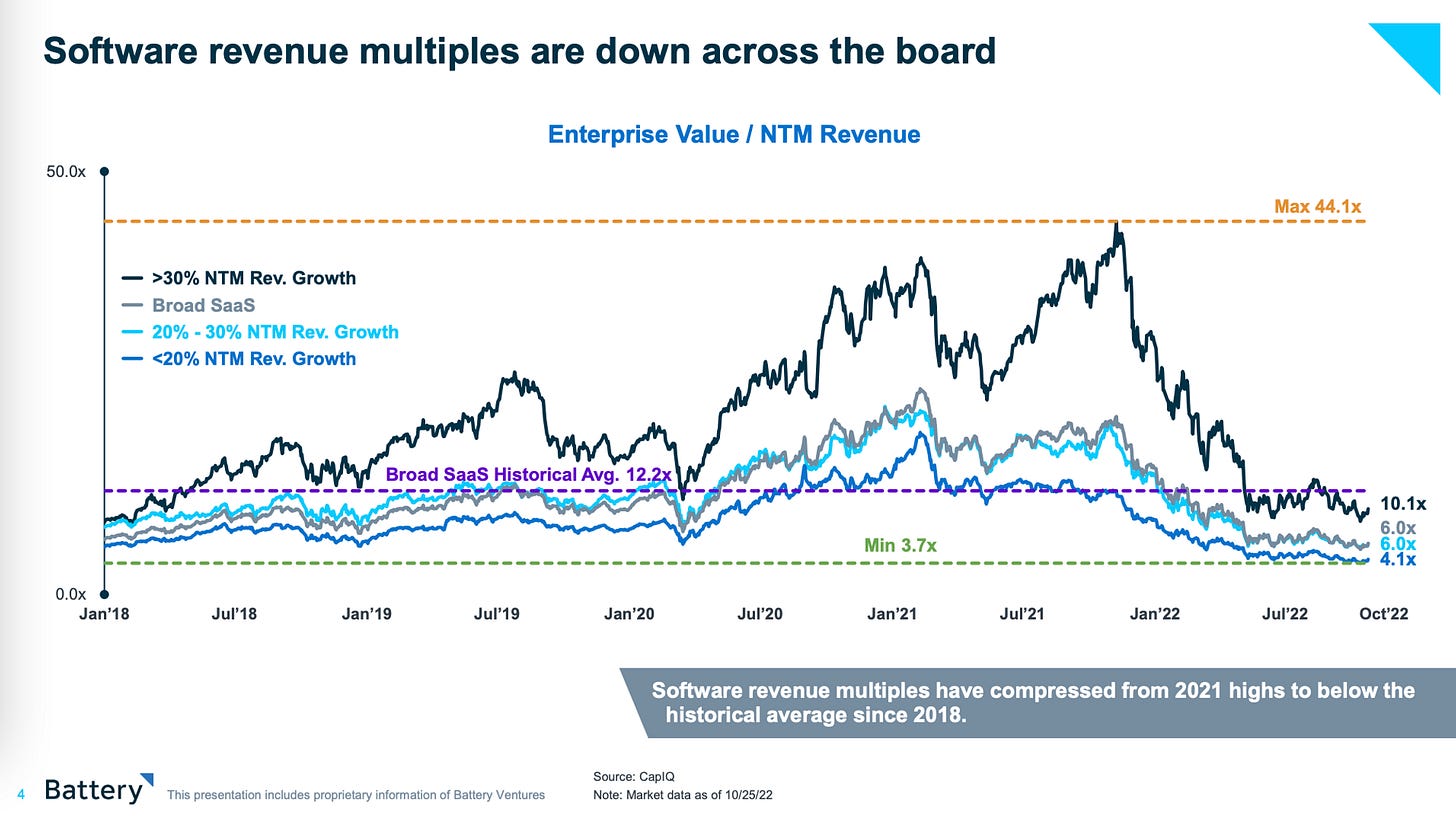

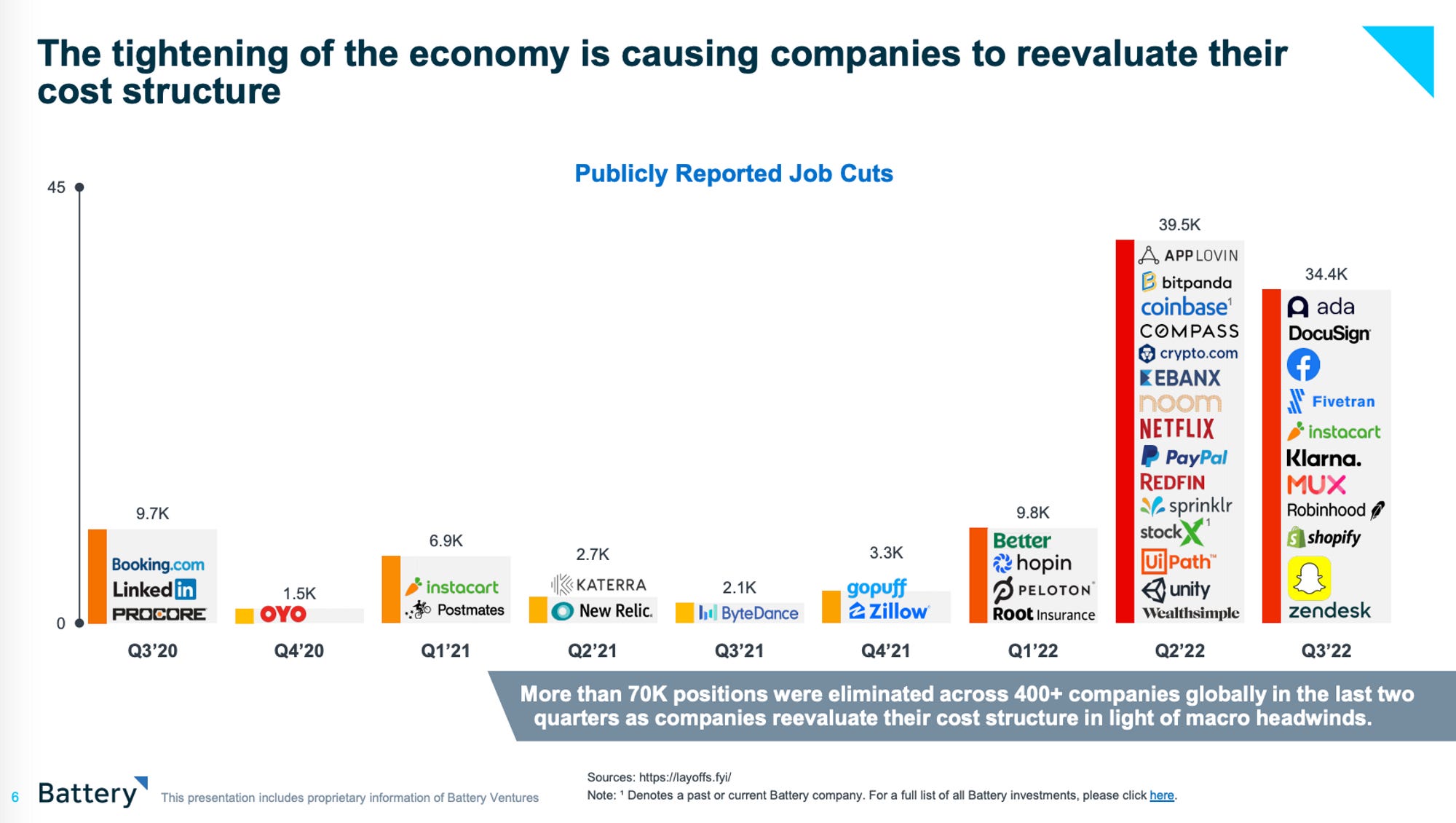

Tuesday, Nov. 8th: Silicon Valley Bank published a 22-slide deck on the health of US SaaS companies. - SVB

Wednesday, Nov. 9th: Battery published a 45-slide deck on the state of cloud infrastructure and open source software. - Battery

During the past 4y, public SaaS companies traded at a 12.2x EV/NTM revenues on average. Today, they trade on average at a 6.0x EV/NTM revenues. SaaS companies with a forecasted growth rate above 30% for next year are trading at an average 10.1x EV/NTM revenues.

400 companies have cut 70k+ jobs in the past 6 months. Companies are reviewing their cost structure to adapt to the new macro-environment.

“On a combined basis, cloud represents 28% of Amazon, Microsoft and Google’s enterprise value, up from 17% in the year prior.”

I like Battery’s best-in-class and long term P&L for SaaS companies: 30% ARR growth, 130% net retention rate, 90% gross retention rate, 25% EBIT margin, 25% S&M expenses (as % of revenues).

Battery is looking at how ML has moved from prediction to generation and how it’s impacting many workflows.

Thursday, Nov. 10th: The Economist wrote a great paper comparing top tech companies (Google, Meta, Amazon, Apple and Microsoft) and large private equity houses (KKR, Blackstone, Apollo) to past conglomerates like GE, Johnson & Johnson, 3M or Kellogg. - The Economist

Conglomerates are “case-studies in underperformance, misaligned management incentives and poor capital allocation.”

Returns on capital were divided by 2 during the past 5y for large tech companies. Public market investors tolerated this underperformance as long as the core business was still defensible and cash generative. Today, it’s no longer the case as cloud and advertising are under pressure due to increasing competition and a looming recession.

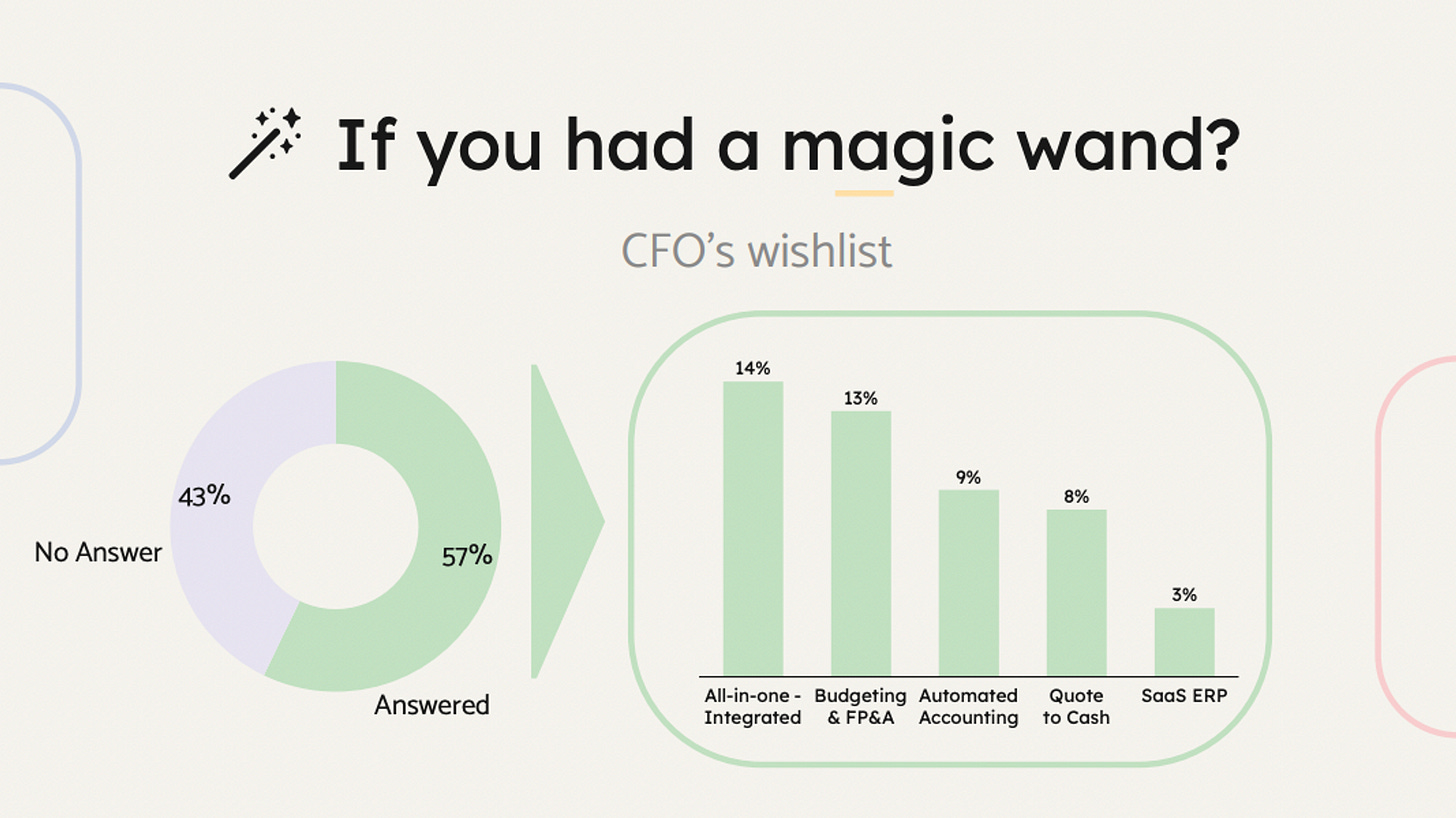

Friday, Nov. 11th: Charles Tenot interviewed 200+ finance executives to learn more about their tech stack and top priorities. - Charles Tenot

FP&A, treasury management and ERP are the top 3 tools that they want to set-up or replace in 2023.

The most outdated tools they used are accounting systems, FP&A, treasury management and ERPs.

It’s noteworthy that finance executives want to consolidate their tech stack - especially for SMBs (”integrated solution for SMBs”, “a fully integrated product such as SAP but for SMBs).

Finance executives want their software to be integrated, automated and simple.

Saturday, Nov. 12th: Elad Gid wrote a blog post on how startups should think about 2023. - Elad Gid

“Interest rates are typically inversely correlated with the multiples ascribed to growth stocks - as these stocks are often valued on future discounted cash flows, and the discount rate ascribed drops (or grows) with the interest rate.”

Covid drove a broader tech adoption in B2B and B2C. With covid ending, long term growth is being normalised (e.g. ecommerce).

The tech industry started a hiring spree in the past 2y for both large tech giants (GAFAM) and startups (hiring ahead of PMF and commercial traction).

“The more likely outcome [in 2023] is more interest rate hikes globally, a recession, and the first real wave in this cycle of private tech company failures, deep layoffs, down rounds, M&A, and other activity.”

It’s a mistake to assume that you should layoff 10-15% of your team. “10-15% seems to be the number that reflects big enough that I can tell myself and my investors or board I am doing it, but not so big that it causes truly uncomfortable conversations for the team.” “One venture firm I know is encouraging companies to assume they should cut 50%of its workforce and then use financial modeling to prove otherwise”

“During the COVID era, due to pre-emption and excess capital, many companies raised at least one “free round”. In other words, many companies received a bolus of money 12-18 months before they would have historically been able to based on progress and traditional valuation metrics”.

M&A activity in tech is picking up. In 2023, M&A activity will increase even more and the power between acquirers and targets is likely to shift towards acquirers.

Sunday, Nov. 13rd: Eric Newcomer interviewed Vinod Khosla. - Newcomer

In 2004, Vinod Khosla founded Khosla Venture after having cofounded Sun Microsystems and having worked at Kleiner Perkins. Khosla invested into companies like Square, Affirm, GitLab, DoorDash, Stripe and OpenAI. It manages a $1.4bn venture fund and a $550m opportunity fund.

“He told me that he thought higher interest rates — whether that meant 2%, 4%, 8%, or 16% — would be “irrelevant to venture capital.” For venture, he said, “You want very high rates of return. That means everything north of 30 to 50% is sort of the range you want your returns from an investment to be.””

“When many people in the venture business were paying high prices, our goal was not to be at the top quartile competing nor at the bottom quartile. We would like to be in the middle.”

“Khosla understands from experience just how important ownership is to maximizing venture capital returns. Big ownership positions in Juniper Networks and Cerent Corp were key to Khosla’s billion dollar returns as an investor at Kleiner Perkins.”

“My view is most experts are experts in a previous version of the world, not the one that's happening, or the ones entrepreneurs want to create.”

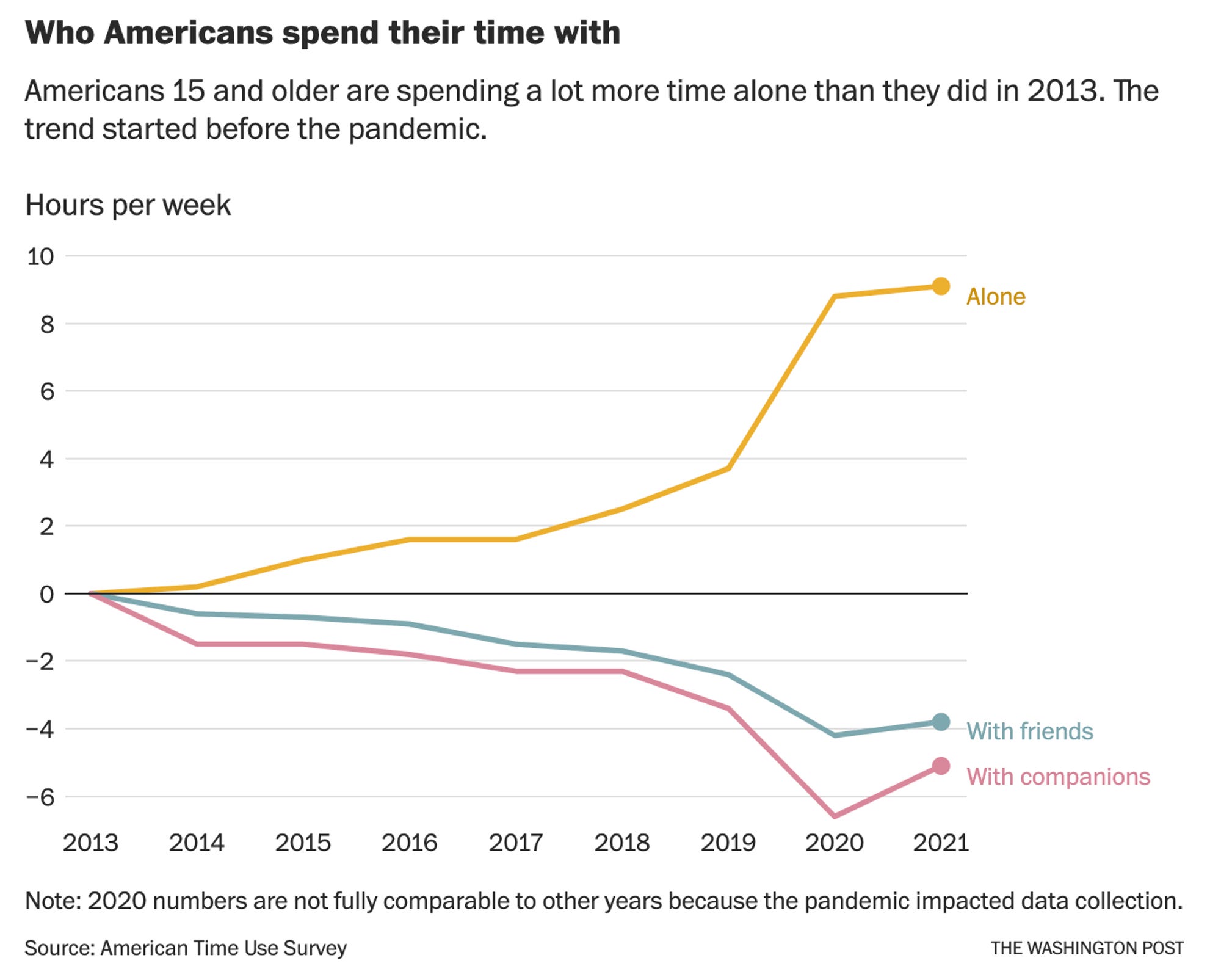

Monday, Nov. 14th: Americans are increasingly spending more time alone and less time with their friends and family. - Washington Post

“Relative to 2010-13, the average American teenager spent approximately 11 fewer hours with friends each week in 2021 (a 64% decline) and 12 additional hours alone (a 48% increase).”

“Spending less time with friends is not a best practice by most standards, and it might contribute to other troubling social trends — isolation, worsening mental health (particularly among adolescents), rising aggressive behavior and violent crime.”

Tuesday, Nov. 15th: Bending Spoons is acquiring Evernote. - Evernote, Alberto Onetti, Techcrunch

Evernote is a popular note taking app. It was founded in 2000. It raised over $205m from investors like Sequoia and NEA. At some point in its history, it reached $100m in recurring revenue and was valued at its peak around $1bn. Since 2015, Evernote has been struggling with a plateauing/declining growth and many waves of layoffs.

Bending Spoons is an Italian-based mobile apps studio which recently raised $340m in fresh capital. Bending Spoons will try to use its expertise and technology to try to revive Evernote one more time.

Wednesday, Nov. 16th: Pelico raised a $18.5m series A round led by 83North and Serena with the participation of existing investors ISAI and La Famiglia. - Business Wire, Tech.eu

Pelico is a vertical SaaS for the manufacturing industry. It builds an operations management system for factory teams. It includes features such as business intelligence, forecasting and AI-based recommendations. Pelico has a short time to value. For instance, with Collins Aerospace it reduced logistic cycles by half in just 6 weeks leading to a 72% reduction in parts shortages.

Pelico will use the funding to (i) recruit 50 employees in Europe and in the US and (ii) to double down on product development in order to support more use cases.

Thursday, Nov. 17th: Index raised $300m for its second seed fund called Index Origin II. - Index, Techcrunch

“It is a highly collaborative fund, with seed-specific support, that works alongside solo GPs and angels, to help companies be best positioned for success.” It invests mainly in Europe and in the US.

“Extraordinary entrepreneurs succeed regardless of the macro dynamics. They don’t start a business based on rallying markets and trending VC investments but instead are driven by a singular mission and complete conviction. In fact, uncertain times have time and time again produced some of the most successful companies. From Airbnb to Adyen, Slack to Skype, Google and Spotify, innovative companies have always been founded or grown during a downturn. They operate in an environment with fewer competitors, where startups produce better, more resilient teams with a greater focus and agility than legacy players.”

Index has refined its support for seed companies with a focus on (i) hiring the first employees, (ii) helping founders with introductions for their customer discovery and for finding their first co-design partners, (iii) providing a network with operators with a strong expertise on fields like product, sales, ops or engineering and (iv) a library of resources dedicated to seed founders.

Friday, Nov. 18th: I listened to a 20VC’s podcast episode with Brian Singerman who is a partner at Founders Fund. - 20VC

To be a great venture investor, you need to be equally excellent at (i) sourcing companies, (ii) picking companies and (iii) getting into the best companies. When you have a strong venture brand, it helps with winning the best deals but it does not prevent you from becoming bad at sourcing and picking the best companies. It’s key to constantly re-invent yourself in venture to keep thriving over the long term (e.g. keeping your network fresh).

Venture is about upside maximisation. You don’t care about doing a good deal financially speaking (e.g. low valuation or structured round). You should only care about investing as much money as possible at the best possible prices into the best companies. The best companies are founded by the best founders who are building things in outsized markets and which can have long term moats.

Top investors have one unique moat that makes them better than any other investors in sourcing, picking and/or getting into the best companies. They develop this moat to make sure that nobody will ever catchup with them.

Saturday, Nov. 19th: I read a company deep-dive done by Contrary Research on Faire which is a B2B-wholesale marketplace copied in Europe by Ankorstore. - Contrary Research

In Europe and in North America, there are 2m independent retailers generating $2.5tn in sales. Faire has 500k retailers and 85k brands.

“Typically, independent retailers have to undergo a fairly manual wholesale process to be able to discover and purchase new merchandise. Retail owners travel to in-person trade shows and work with brokers to acquire new merchandise from brands. In addition, retailers buy a new product without really knowing whether it will end up driving new customers and revenue to their store.”

In wholesale, small retailers are usually required to pay upfront for inventory. Faire offers financing, which enables retailers to buy the inventory now and pay for it only 60 days later even if they have sold the inventory in the meantime.

The company has cross-side network effects: brands will refer retailers and vice versa.

“Faire takes a 25% commission on orders made by new customers, 15% on repeat orders, and no commission on orders from retailers whose brands did business before using Faire’s marketplace.”

Between 2017 and 2021, Faire experienced a 3x YoY growth and reached $1bn in GMV on its marketplace.

Going forward, Faire is activating the following growth levers: (i) expanding in new geographies (Europe, Australia), (ii) opening new product categories (e.g. furniture, food, pets, etc.), (iii) expanding upmarket serving larger retailers.

Sunday, Nov. 20th: Ben Thompson interviewed Opendoor’s founder and CEO Eric Wu. - Stratecherry

Opendoor is currently testing whether its home-buying model can work in a downturn. In Q3, it recorded massive losses because it sold inventories at steep discount and it laid off 18% of its workforce.

“I had this view of the world that it should be possible to buy and sell a home in a few taps, in a few clicks, with just your mobile device.”

“There are certain types of businesses that require two to three miracles or maybe they’re effectively running two to three different startups, and so there wasn’t just one thing.” In the early days, Opendoor had 3 main challenges to crack: (i) building the pricing engine, (ii) accessing to capital, (iii) building vertically integrated operations from sales to support."

“If you talk to anyone who’s been through a real estate transaction, I would venture to guess that 95% of them are dissatisfied with the experience.”

Contrary to most marketplaces, Opendoor started by acquiring sellers instead of acquiring buyers. “The strategic decision was that if you can start to win supply, you can over time leverage that inventory to actually connect the dots with demand.”

Why Zillow failed at launching an Opendoor-like value proposition? It’s next to impossible to “make the transition from being a high margin media company to a vertically integrated low margin platform”.

“Given the shift in the market, we certainly made a forecasting prediction that has not been accurate about the slope of the change in the past three months. And to give you some context, the market moved from positive 7% appreciation per quarter to negative 1% in three months, and that is actually steeper than what happened during the Great Financial Crisis.”

Opendoor has low customer acquisition costs because “if you’re able to provide an online offer in minutes, homeowners and, importantly, home sellers, will start their journey with us.”

Monday, Nov. 21st: I read a post from fDi Intelligence on the tech ecosystem in Milano. - fDi Intelligence

5k multinational companies have an office in the Milan area with 520k employees in sectors such as energy, manufacturing, life science or professional services.

“In 2012, the Italian Start-up Act was launched, aimed at supporting the creation and growth of technology companies, which included a 30% tax credit for seed and early stage investors.”

“Culturally speaking, Italy and France are extremely similar, but Italy is about seven years behind France in terms of VC investment.”

“Milan is 7th-cheapest place to hire software developers ($76k) — more expensive than hubs like Tallinn, Estonia ($36k), but still cheaper than London ($105k), Berlin ($102k) and Paris ($116k).”

In Feb. 20, Klarna acquired a local fintech based in Milano called Moneymour partly in order to open a local hub in Milano.

Tuesday, Nov. 22nd: Greta Anderson who is investor at Balderton wrote a blog post on startups for restaurants. She noticed the following startups trends: (i) CPG and meal kits, (ii) self managed delivery (e.g. Flipdish, Deliverect), (iii) working capital financing (iv) kitchen robots, (v) staffing and benefit tech (e.g. Wagestream, Brigad), (vi) QR codes (e.g. Sunday), (vii) restaurant OS software (e.g. Ordio, Haddock). - Greta Anderson

Wednesday, Nov. 23rd: Balderton published a guide for founders on building and managing a B2B sales team. - Balderton

It has the following chapters: (i) selling, (ii) building a sales organisation, (iii) managing a sales organisation, (iv) renewing/expanding existing contracts, (v) using marketing to build your sales pipeline, (vi) using partners to improve reach & win rates, (vii) planning.

On selling: (i) in the early days, founders should push themselves to go out and sell their products, (ii) the perfect talk/listen ratio is 43% talking and 57% listening, (iii) ask open ended questions which reveal far more information than closed ended ones.

Thursday, Nov. 24th: a16z wrote about how to build a paid membership program. - a16z

Paid subscriptions are becoming mainstream for consumer businesses. It’s used/experimented by companies like Amazon, Costco, Twitter, Snap, Youtube, Discord, Disney and Meta. In China, it’s already mainstream for consumer companies to have successful VIP membership programs.

Looking at Chinese models, a16z unpacked 4 useful frameworks to have in mind while designing a subscription program: (i) a mix of earned and paid perks, (ii) an intricate leveling and points system, (iii) a balance of flexing (social expressions visible for the rest of the community) with functionality (utilitarian benefits), (iv) partnerships with other companies (cross-partnership with other non competitive consumer companies to increase respective customer base).

In China, “paid memberships get you an initial baseline membership package, but additional benefits are only unlocked with increased usage.” “For $3.50 USD a month, Weibo VIP members can edit their posts, have fun stickers next to their comments, access VIP emojis, and much much more. But continued usage of Weibo unlocks more features such as pinning more than one post.”

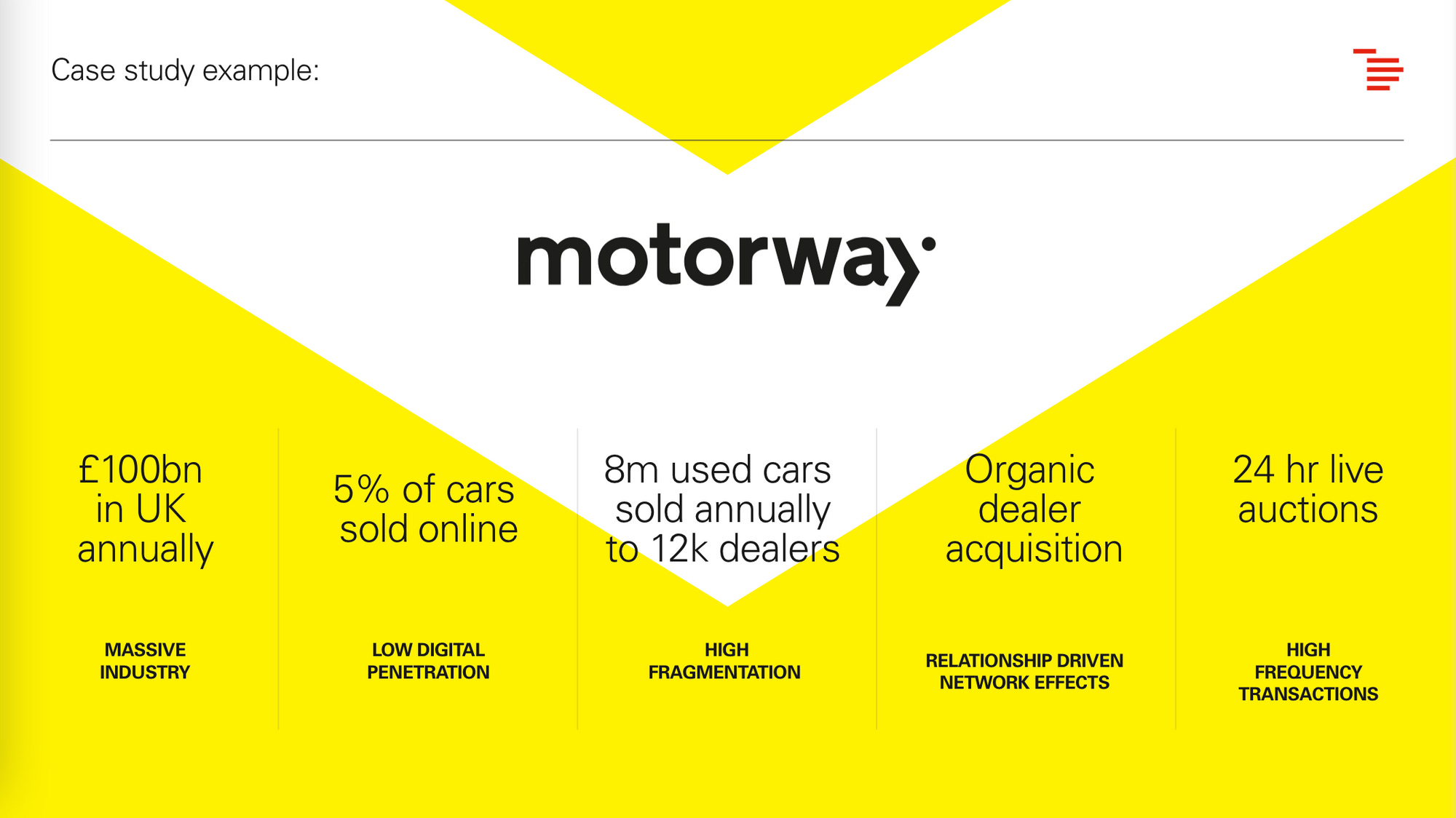

Friday, Nov. 25th: Georgia Stevenson at Index published a presentation on verticalised marketplaces. - Index

Horizontal B2B marketplaces (e.g. Alibaba, Amazon Business, SAP Ariba, Faire, Ankorstore) will be unbundled like their B2C counterparts.

Verticalised marketplaces are more likely to emerge because of major infrastructure improvements: (i) a shit to API driven architecture, (ii) integrated B2B payments & lending and (iii) seamless shipping.

When evaluating markets, Index is looking at the following characteristics: (i) massive industry, (ii) low digital penetration, (iii) high fragmentation, (iv) relationship driven network effect, (v) high frequency transactions. On the traction, Index wants to see: (i) efficient sales cycles, (ii) high GMV net retention, (iii) high engagement rate. On the product, Index is looking for: (i) intuitive product, (ii) solving a hard data problem, (iii) an end to end management of the transaction (searching, matching, bulk buying, financing, logistics).

Saturday, Nov. 26th: I listened to a Colossus’ podcast episode with Parker Conrad who is Rippling’s founder and CEO. Rippling is an employee management platform using employee data as a system of records to improve HR, IT and finance processes. - Colossus

A compound company builds a constellation of interoperable products with more value as a bundle than as independent products. It’s not a new concept. Microsoft, SAP, and Oracle are compound companies.

With the transition to the cloud, many compound companies were unbundled by point solutions that were faster to create in the new cloud reality. But, it was a transitory period. The ideal state for software is a world with compound companies with deeply integrated products as well as bundled contracting and pricing. Salesforce and Rippling are part of this newer generation of compound companies.

Rippling builds products which are always based on employee data and a set of underlying platform capabilities called middlewares (workflow automation, role based permissions, custom policies, approvals, routing, reporting & analytics). Products are interrelated making Rippling’s platform capabilities much more powerful than point solutions.

Salesforce is a system for managing business process and workflow that relates to customers and customer data. Rippling has the same concept for employees and employees’ data.

Compound companies have 4 main critical advantages compared to over-focused companies: (i) products are deeply integrated with each other, (ii) middleware capabilities will be always more powerful than the ones of standalone companies, (iii) once users know how to use a product from a compound company, they can easily use all other products, (iv) a compound company has pricing and contracting advantages because it can amortise sales and marketing expenses on many more SKUs.

Rippling has many former founders in its team. Rippling tells them that they are going to build a product inside Rippling while accessing Rippling’s funding, infrastructure and distribution. When they join, these former founders have to recruit on their own their core team of 3-4 engineers without the support of the recruitment department.

Sunday, Nov. 27th: The Economist wrote about the car industry shift from hardware to software. - The Economist

“Immutable objects that do not change after they leave the factory are turning into dynamic platforms for applications and features which can be updated “over the air”. Rather than deteriorate with age, such “software-defined vehicles” can improve over the years.”

Historically, most software in cars were developed by carmakers’ suppliers for their car’s parts and carmakers were mostly integrators. With the increasing reliance on software, this model is becoming unsustainable for car manufacturers.

It’s a new paradigm that will be extremely hard to seize for historical car manufacturers: (i) they have to become software centric and (ii) they have to shift to an iterative world in which their cars will be updated every day vs. every 4 year when they release a new model.

Stellantis launched a “Data and Software Academy” to retrain 1k employees and increase its number of engineers to 4.5k people by 2024.

“Each of these changes—to digital technology, organisation and business models—is a big shock on its own. Together they amount to a handbrake turn for an industry characterised by inertia.”

Tesla “was conceived as a software company that happened to make cars”.

Monday, Nov. 28th: I listened to a Colossus’ podcast episode with Brian Singerman who is partner at Founders Fund. - Colossus

When evaluating a business, Brian is looking for 3 things: (i) moat (does the company has an existing moat? e.g. unique team to execute the idea, unique international network effects at Airbnb), (ii) market (is the market large enough to have a meaningful impact on my fund?), (iii) execution (does it have a founding team that can execute from moat to market?).

“I love things that aren't easily cloned by the talented software companies we have in Silicon Valley.”

You have to master 4 skills in venture capital: (i) do you see the right deals? (ii) can you pick the right deals? (iii) can you get into the right deals? (iv) how do you help the company after you're in? (least important part because the founders can do it themselves).

“An A-plus founder knows how to own the weaknesses and knows how to account for them via some other way” (e.g. having somebody in the team that is really good that will be working on these weaknesses).

“When I'm hiring for somebody junior, I want to know what they're thinking and that they're thinking differently. My favorite question is a pretty standard one: What's your favorite company and why? What company do you love that other people don't? What company do you hate that other people love?”

Tuesday, Nov. 29th: Fabrice Grinda wrote about the current macro-economical environment. - Fabrice Grinda

“Being bearish about the global economy is consensus right now. As usual, I am contrarian, but in this case, my contrarian take is that the consensus is not bearish enough.”

Fabrice highlights 9 factors driving the bear sentiment he had on the current market: (i) interest rates may go higher than people expect for longer than people expect, (ii) the strong dollar is creating a sovereign debt crisis in emerging markets, (iii) high gas prices are going to cause a recession in Germany, (iv) there is another euro crisis looming with many countries with high debt to GDP ratios, (v) real estate prices are about to fall, (vi) structurally higher geopolitical risk, (vii) continued conflict between Ukraine & Russia will keep grain, gas & oil prices at a high level. All these factors could lead to a major global recession.

“In the meantime, the only place to invest right now is in early-stage private tech startups. Early-stage valuations are reasonable. Founders are focusing on their unit economics. They are limiting cash burn to not have to go to market for at least two years. Startups face lower customer acquisition costs and much less competition. While exits will be delayed and exit multiples lower than in the past few years, this should be compensated by lower entry prices and the fact that winners will win their entire category.”

Wednesday, Nov. 30th: Bill Gurley at Benchmark wrote a good list of red flags that could indicate a risk of corporate malfeasance. - Above The Crowd

It includes: (i) bull markets, (ii) lack of a legitimate board (e.g. no board, friends & families on boards, no experience in investing in private markets), (iii) super voting stock, (iv) aversion to audits, (v) unique way to present financial data, (vi) an atypical legal advisor, (vii) an odd corporate location, (viii) large secondary transactions (above $1-5m), (ix) overlapping corporate interests, (x) a too good to be true situation.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Nice work! Thank you for shaping your thoughts in such an enjoyable read!