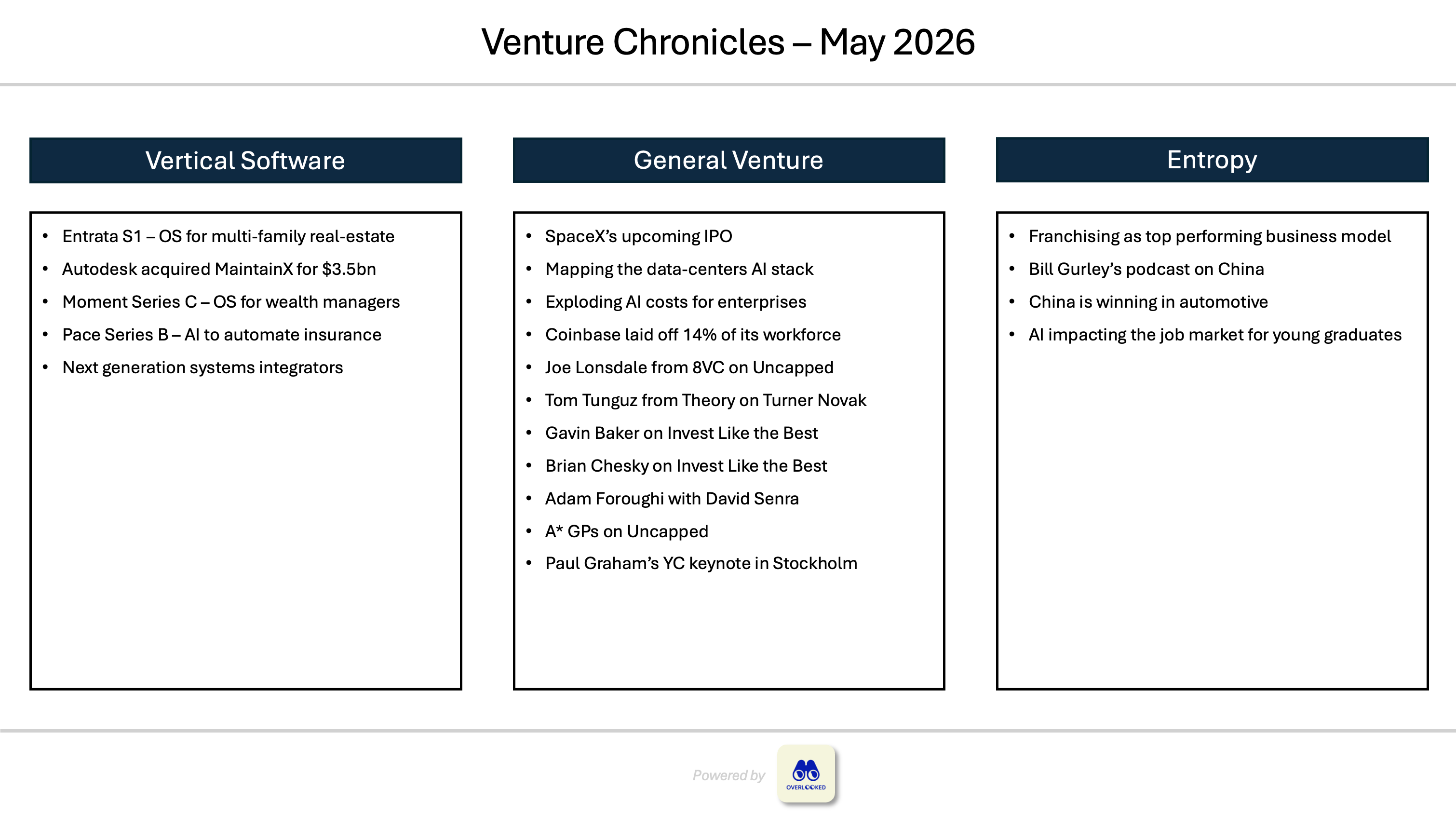

📖 Venture Chronicles - May 2026

Overlooked #219

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of May.

I curated updates and insights around three themes:

Vertical Software

General Venture Capital

Entropy - other news and personal topics of interest

Vertical Software

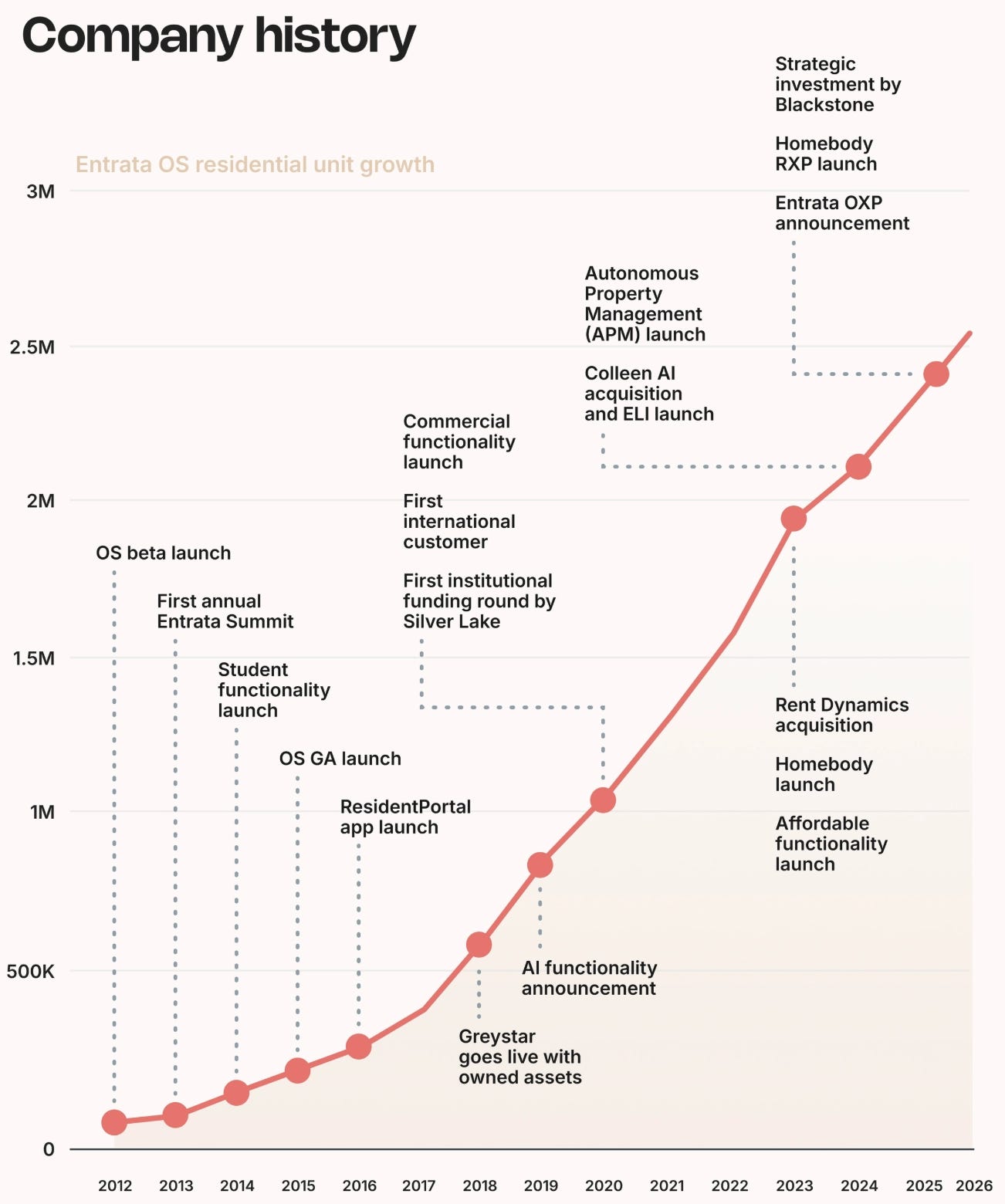

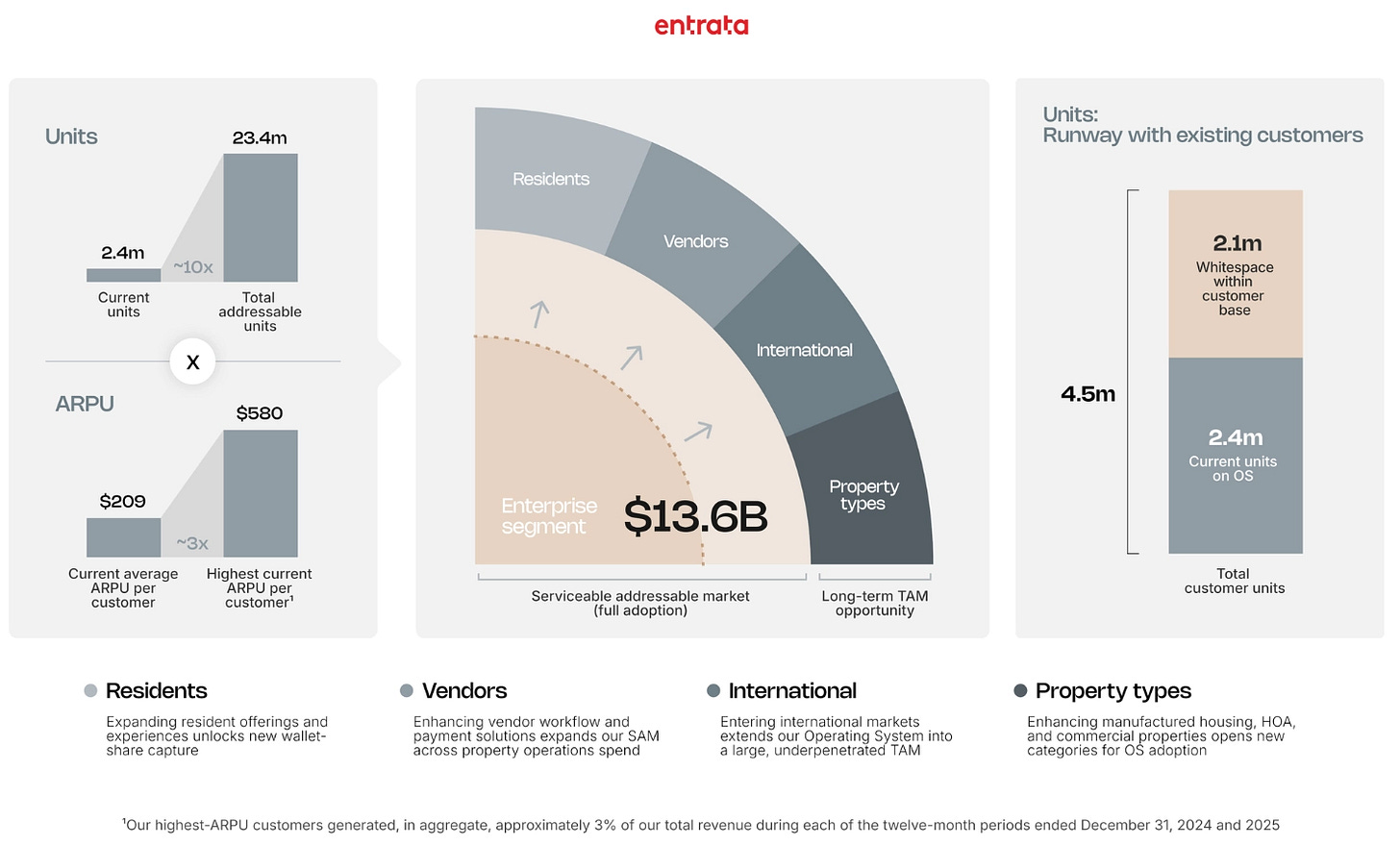

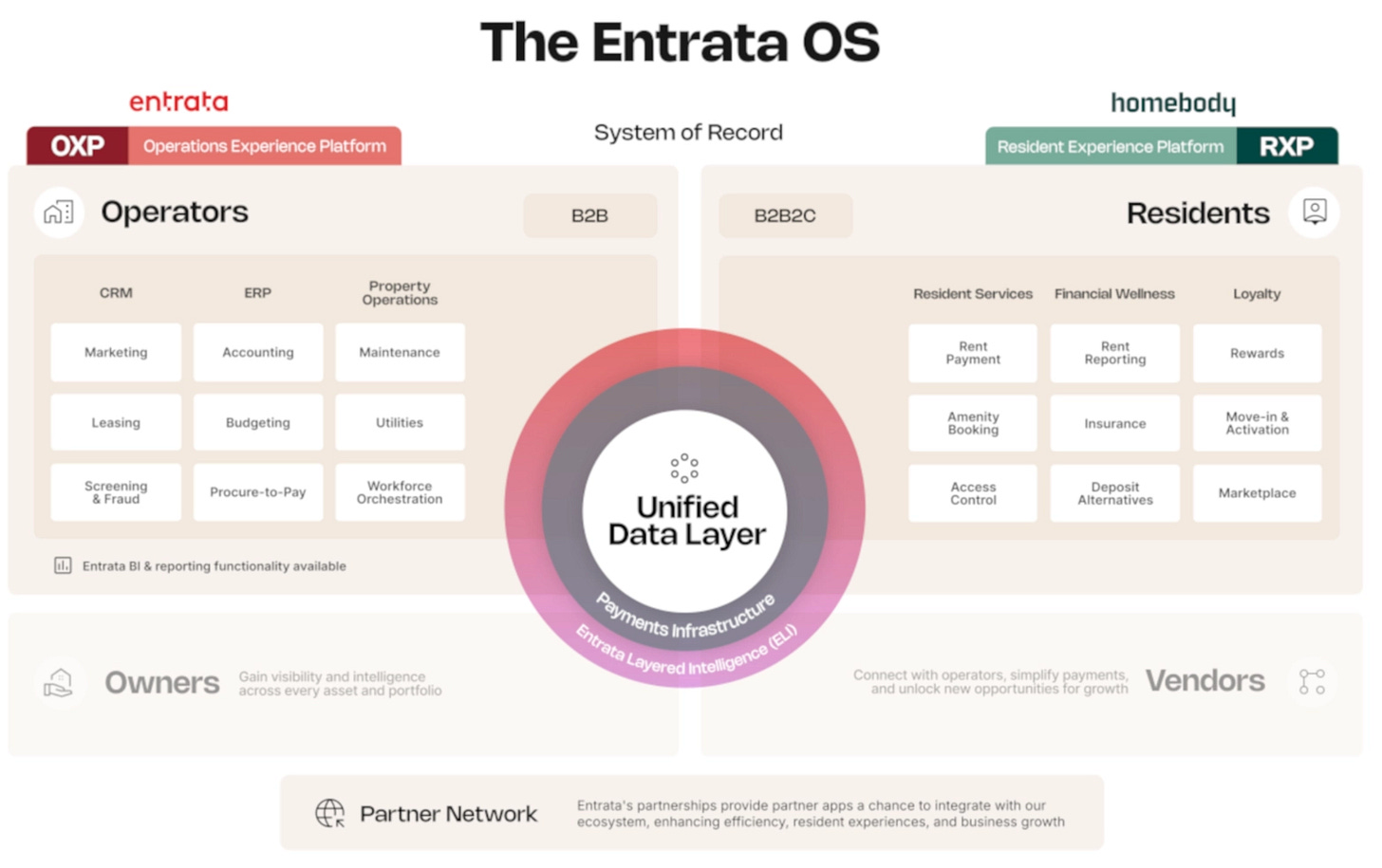

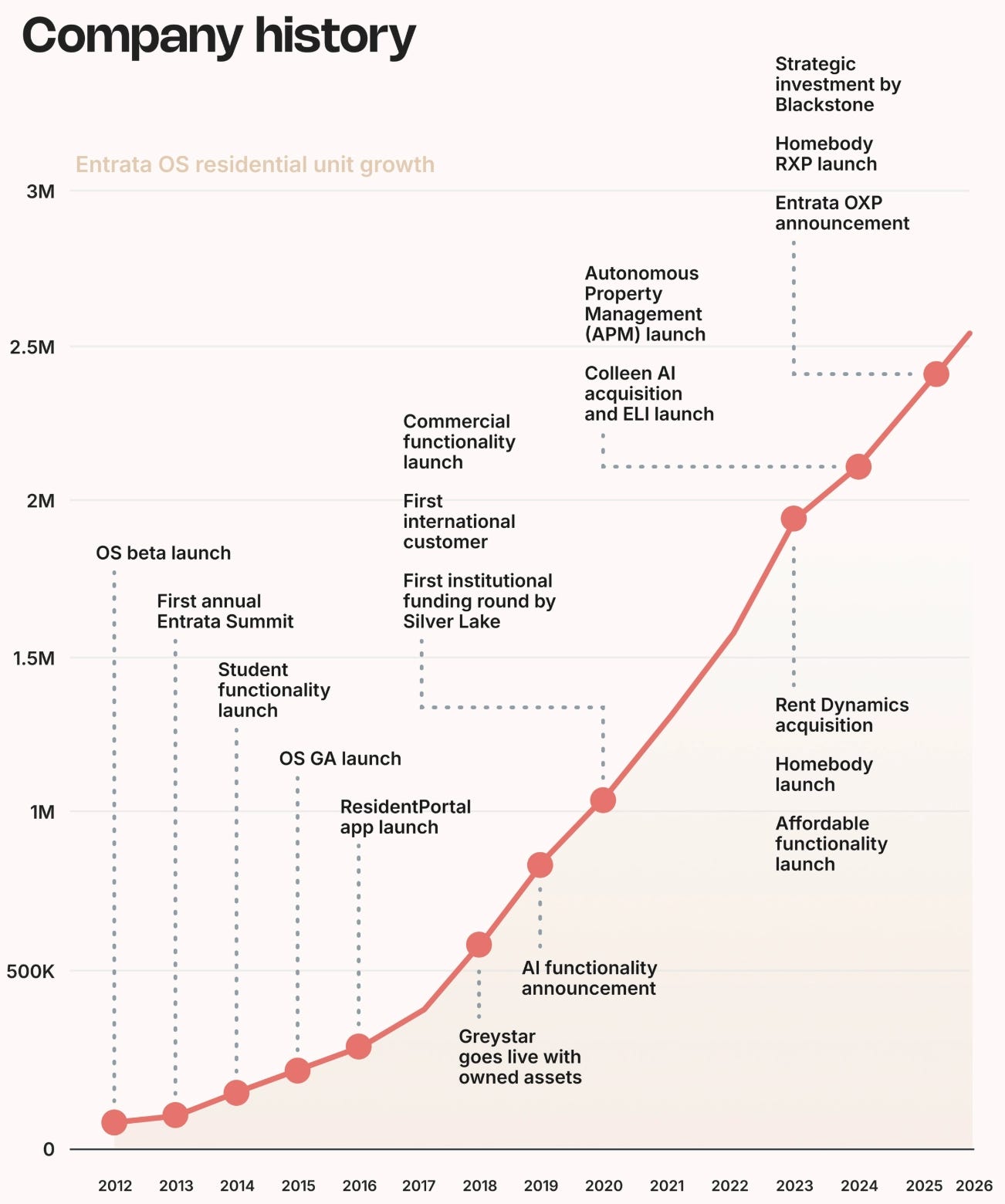

Entrata filed its S1 to go public. It’s a property-management OS for US multifamily real estate doing $574m in ARR growing 23% YoY and profitable. - S1

Entrata was founded in 2003 and stayed bootstrapped until 2021 when SilverLake started to invest in the business before becoming majority shareholder in 2022. In May 2025, it raised $200m from Blackstone at a $4.3bn post money valuation.

“Entrata’s technology empowers property owners and operators to run tens of thousands of thriving residential communities, delivering better experiences for millions of residents while strengthening the entire residential ecosystem.”

“Multifamily real estate is one of the largest and most complex industries in the world comprising housing types such as conventional, student, and affordable, yet for decades it has relied on fragmented tools and legacy systems that are not built for such an essential part of everyday life.”

“It’s a modern and autonomous OS that connects the broader residential ecosystem within a single platform, including owners, operators, residents, and vendors.” It includes ERP, CRM, property operations and resident engagement.

“As of March 31, 2026, we powered 2.5 million units, or roughly 10% of the U.S. multifamily market.”

“Our ability to scale with enterprise customers is evidenced by our 233 customers with ARR exceeding $500,000 as of December 31, 2025, compared to 183 such customers as of December 31, 2024, representing an increase of 27% in the customer count. These customers with ARR exceeding $500,000 represented 84% of total ARR as of December 31, 2025, compared to 81% of total ARR as of December 31, 2024.”

“The rental property ecosystem consists of a wide range of interconnected stakeholders (owners, operators, residents & vendors). Each of these stakeholders interact regularly and have unique needs that are essential to the ongoing success of any property.”

“Rising demand for rental properties has fueled increased investment in multifamily units, which are predominantly managed by enterprise operators.”

“We have a proven track record of acquiring new customers, and currently 4 of the top 10 NMHC operators and 10 of the top 50 are on our Operating System.”

Autodesk acquired MaintainX for $3.6bn in cash. It’s an AI-enabled computerized maintenance management and enterprise asset management for frontline industrial teams to perform work orders, inspections, asset condition data, maintenance histories. - Bloomberg

Founded in 2018, MaintainX is used by 11k companies and has 11m assets under management. It raised $245m in total. Last round was a $150m series D in Mar. 2025 at $2.5bn valuation. It’s on track to generate $135m ARR in 2026 growing 50% YoY.

Autodesk’s strategy is to bundle design, make and operate in a unique platform. MaintainX gives them the “operate” data layer they lacked.

“MaintainX is used to manage inspections, work orders and the condition of assets across a wide variety of industries, including farming, manufacturing and food services. The San Francisco-based firm expects annual recurring revenue to grow more than 50% to more than $135 million in 2026, the companies said in the statement.”

Moment raised a $78m series C led by Index. It replaces fragmented investment management software with a unified platform that enables AI agents to handle portfolio construction, compliance scanning, trading and tax optimisation across multiple asset classes. - Business Insider, Memo

“Investment management software has historically been built as a patchwork of point solutions — separate platforms for fixed income, rebalancing, unified managed accounts, direct indexing, reporting, reconciliation, and other workflows — connected by the people working across them. Moment is an operating system designed to replace that patchwork with a single platform on which AI agents can operate end-to-end in a regulated environment. The platform unifies trading, portfolio management, and compliance across asset classes and currencies in a single operating system.”

Moment’s agents: portfolio construction, portfolio optimisation, surveillance, compliance, order & execution management.

“The platform now powers investment management for firms collectively managing more than $10 trillion in client assets, up from $300 billion less than 18 months ago.”

Pace raised a $46m series B co-led by Thrive and Sequoia. It helps insurance companies automate back-office work (submissions, renewals, servicing, claims). - Business Wire, Pace

“Since we launched last year, the world’s leading insurers have relied on Pace to autonomously complete more than a quarter of a million critical insurance workflows with AI agents. It’s how Prudential automates thousands of hours across customer acquisition. How Palomar resolves 90% of policy servicing tasks without linearly scaling customer service headcount. How Convex speeds up data ingestion for new business and renewals.”

“Whether it’s launching new products faster, onboarding more customers, or scaling infinitely to meet spikes of activity, the outcome is the same: we are helping the world’s leading insurers decouple the cost curve of operations from the growth curve of the business.”

“Pace’s purpose-built agents are engineered for your work across submissions, renewals, servicing, and claims.”

“We will invest this capital to help our customers scale their agentic workforce to tens of millions of operations tasks this year across the US, Europe and now globally.”

“When a major storm headed toward Florida, an insurance claims servicer called Ryze Claim Solutions had the obvious problem: thousands of new claims, one week, not enough people. The old answer was to find a small army of temporary claims processors and hope the paperwork did not drown them. The newer answer, according to Pace founder and CEO Jamie Cuffe, was to send in AI agents.”

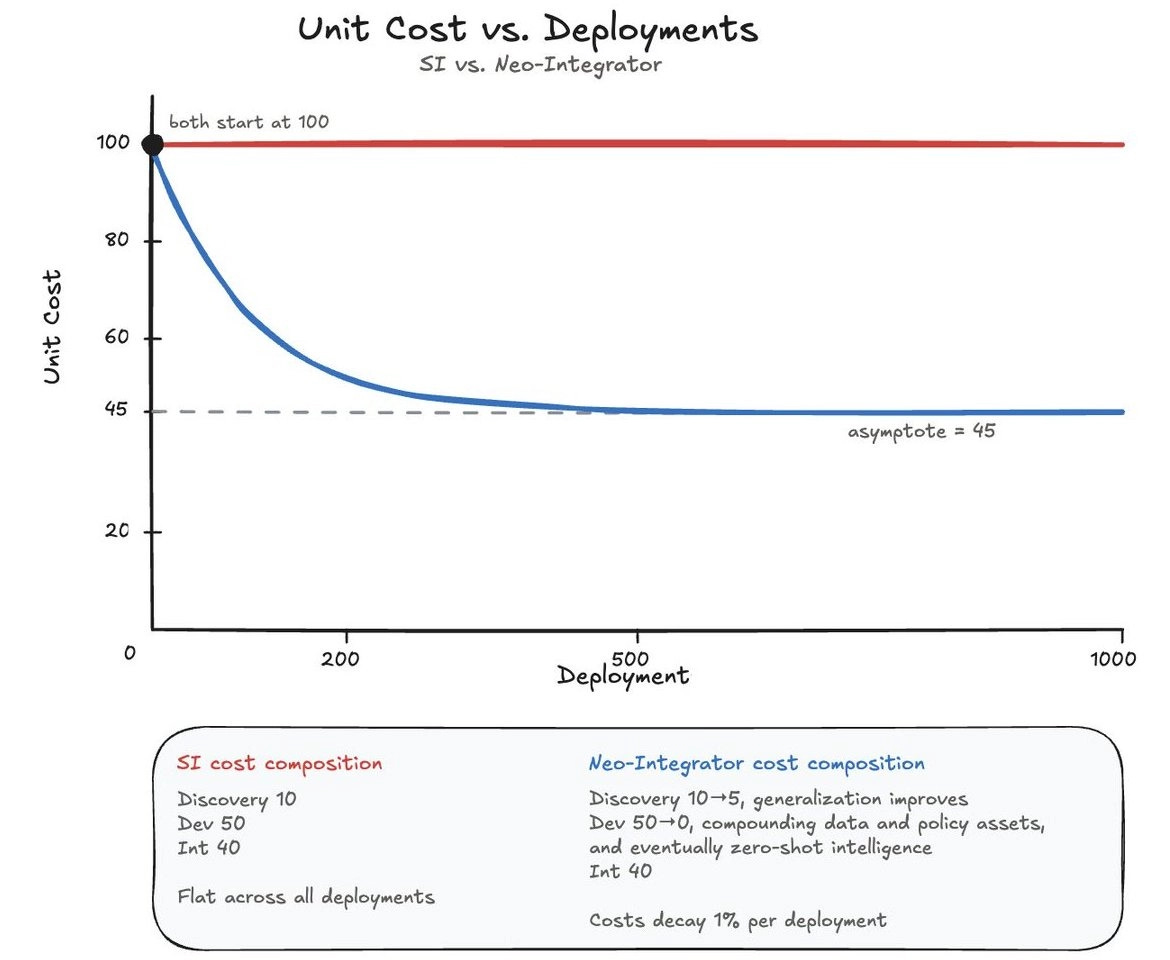

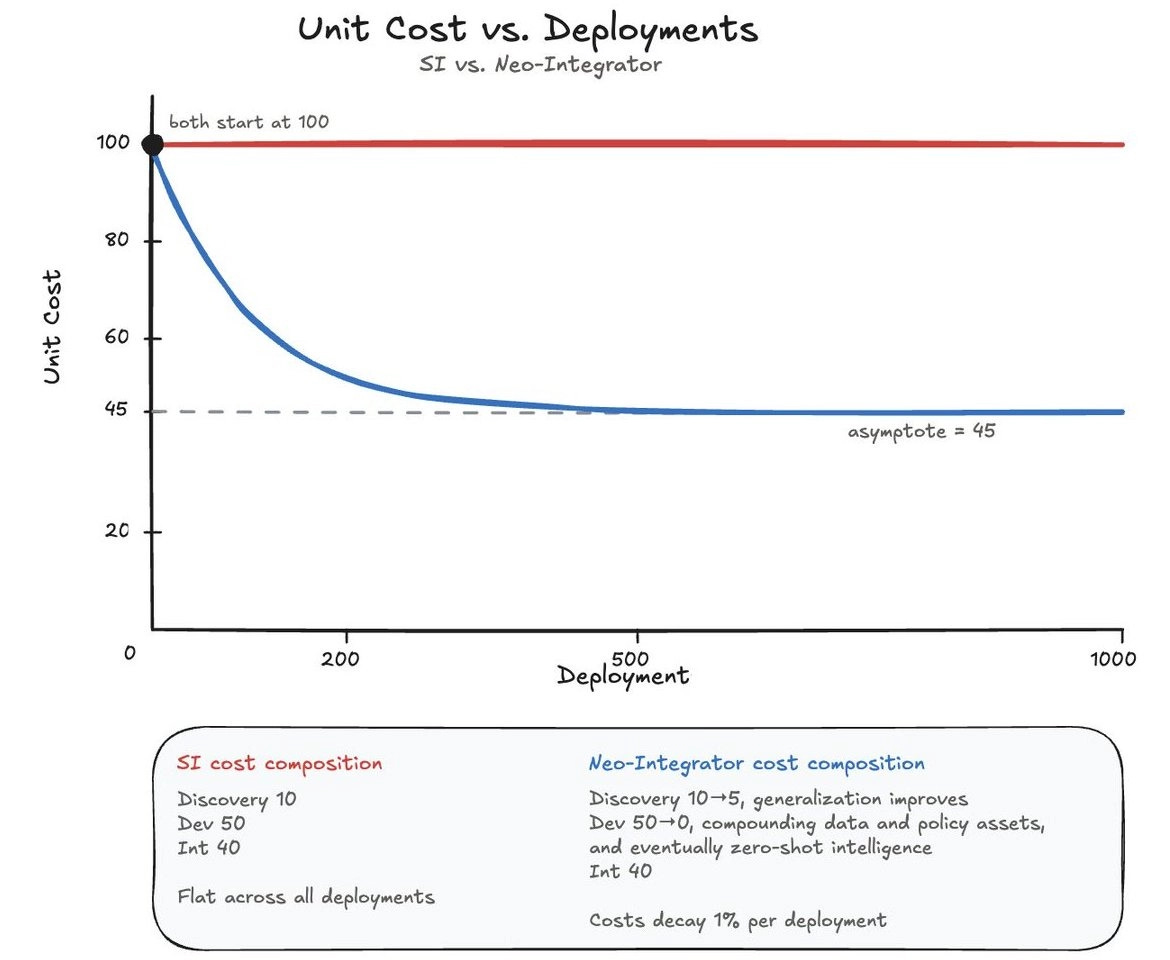

Avi Zurlo wrote about next generation systems integrators (SIs). SIs manufacturing services companies connecting different machines, software, robots, and production systems so they work together as one factory process. - Avi Zurlo

“SIs are the forward-deployed engineers of robotics and are responsible for ~70% of the 400k industrial robots deployed in the US today.”

“Their deployment work breaks into three phases: discovery (what to automate and where), development (designing the cell, writing robot paths, configuring vision, handling edge cases), and integration (mounting, networking, safety review, WMS/MES/PLC integration, operator training, debugging, maintenance). Today, development and integration dominate every project budget, ~50% and 40%, respectively.”

“The old development cycle for deployments was largely custom engineering: a technician writes the robot’s paths, tunes the vision system, handles edge cases. The new development cycle is teleoperation, data collection and processing, and model post-training. The labor mix shifts from scarce SI technicians and engineers get replaced by two cheaper, more available inputs: teleoperators who collect data and run supervised deployments, and ML engineers who own the policy lifecycle. In a foundation model regime, data and policy assets carry forward. Though their value is bounded by overlaps in embodiments, tasks, and environments, the marginal cost of development falls with each deployment.”

General Venture

I read several analyses on SpaceX’s upcoming IPO. - Stratechery, Ed Elson

“At $2 trillion, SpaceX would be the seventh-most valuable company in the world, more valuable than Meta, Walmart, JPMorgan, and even Tesla.”

“Only a few pages in and it’s already starting to feel like an ayahuasca trip.”

“Once you arrive at the financials you start to realize what the language is overcompensating for: awful numbers. The company generated $4.7 billion in Q1 2026, up only 15% from the year before (very low for an “AI company”). It also lost $4.3 billion, up 700% from the year before. That means the company is spending roughly twice as much as it makes.”

“I’d have no problem with SpaceX’s sh*tty financials if they were reflected in the valuation — but they’re not. The stock is set to be priced at 107 times sales, which would make it one of the most expensive stocks in history.”

“SpaceX’s AI unit is essentially a giant sinkhole. The segment generated less than a billion dollars last quarter while spending more than three billion.”

“Management believes retail is the answer. SpaceX is reserving 30% of its shares for retail investors, three times larger than the average IPO. The expectation is that die-hard Musk fans will buy the stock no matter what — a bet on the “dumb money.””

“If we apply comparable market multiples to each of SpaceX’s three business lines (space, connectivity, and AI), we arrive at a sum of parts valuation of $550 billion. That would be a reasonable valuation of SpaceX.”

“Starlink is the consumer-facing business of SpaceX, generating $8.7 billion in revenue last year and $4.4 billion in profit; while it’s not totally clear exactly how SpaceX accounts for launch costs, obviously Starlink benefits greatly from the fact that it has access to SpaceX’s launch capacity. That launch capacity has resulted in over ten thousand active satellites in low Earth orbit, delivering low latency high speed Internet anywhere in the world — including in the air. That’s the carrot for airlines; the stick is the prospect of everyone else having the same service, and customers making flight decisions based on the quality of Internet access available.”

“Everything about this IPO is absurd. SpaceX is seeking a $2 trillion valuation on a mere $18.67 billion in revenue with $4.9 billion in losses last year, and growth actually slowed from 35% to 33%. That slowdown happened despite the addition of xAI (and thus also X), which tipped the company from a small profit to that massive loss, thanks to $5.1 billion in AI R&D expense. That R&D, keep in mind, went towards building a model that is in 5th place, and whose entire founding team recently left the company.”

“There is no reason that space data centers would look like data centers on earth. What makes far more sense is to think about an individual satellite as something akin to a rack.” “The big shortcoming for a rack-satellite is power and its dissipation, but going from 25kW to 135kW is certainly within the realm of possibility — and given that you don’t need much of the cooling and power distribution usage on earth, something closer to 100kW might deliver similar performance.”

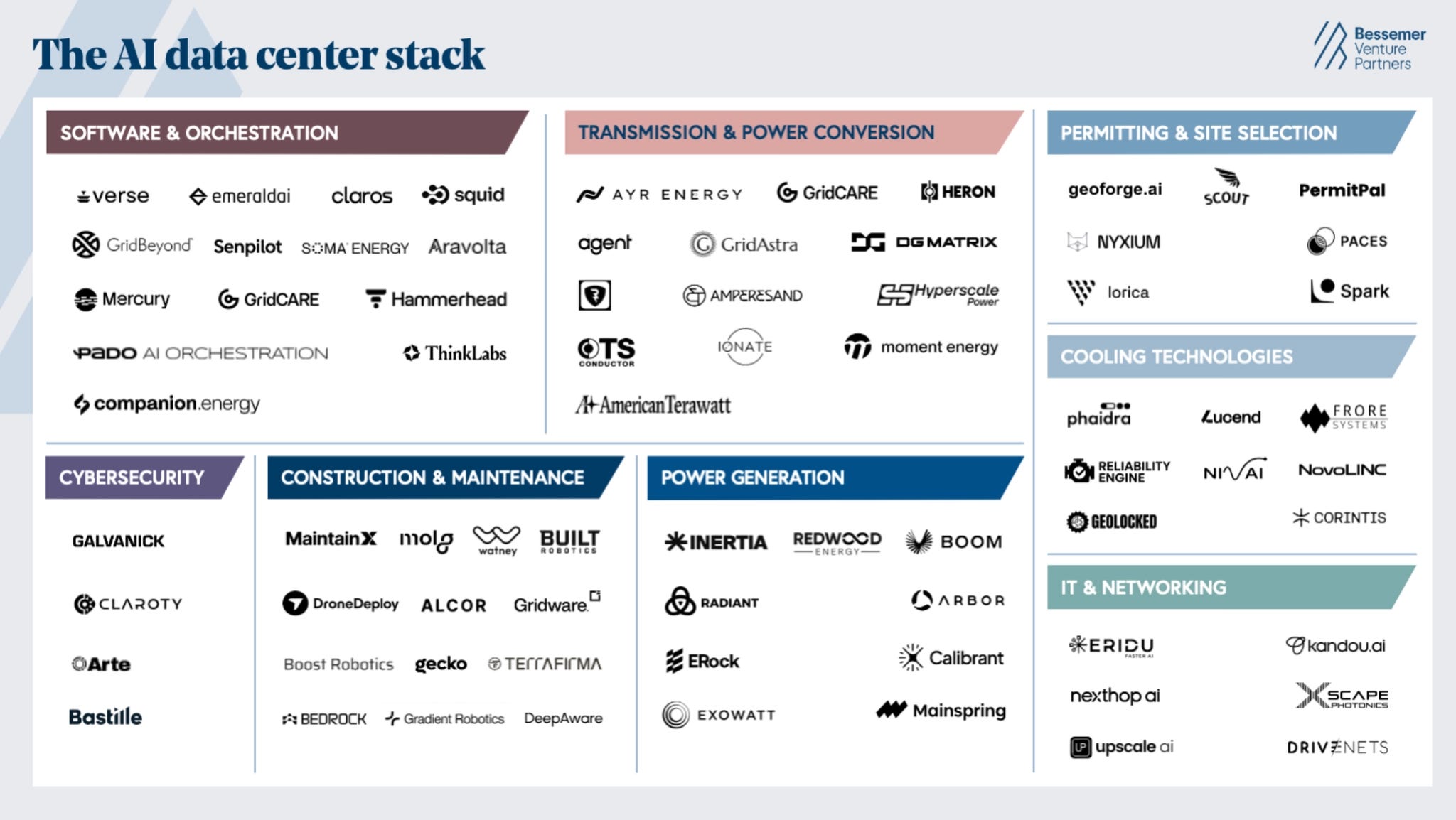

Bessemer published a market map on the data center AI stack. - Bessemer

“As of early 2026, 190 GW of hyperscale data center capacity has been announced across 777 projects. This includes ~148 GW planned, ~21 GW in construction, and ~12 GW already operational. Global data center electricity consumption is projected to more than double by 2030, and in the U.S., data centers will soon consume more electricity than all energy-intensive manufacturing combined.”

“Data centers can be constructed within 12-18 months, but connecting them to the grid currently takes five to seven years. Of the 110 data center projects that were slated to come online in 2025, more than a quarter were delayed due to power, permitting, and construction constraints.”

“We believe the hardware and software layers that make those [AI data centers] developments possible are still in their early innings, leaving significant room to venture into the enabling technology stack.”

“Paces is another player in the space unifying grid, permitting, and environmental data into a single platform that helps developers identify viable sites and catch flaws before committing capital.”

“While grid-connected sites still account for the largest share by project count (45%), on-site generation and hybrid approaches together account for close to half of all announced capacity. This reflects the broader “Bring Your Own Power” (BYOP) movement, where data centers generate electricity on-site behind the meter (BTM) to sidestep waiting years in the interconnection queue for grid access.”

“Hyperscalers and frontier labs are willing to redesign around alternative cooling technologies because overheating directly affects the useful life of hardware and performance per watt.”

Enterprise AI costs are exploding as usage-based pricing replaces all-you-can-eat subscriptions, pushing companies from “use as much as possible” to rationing, tracking ROI, and steering workers toward cheaper models. - WSJ, FT

“Use of artificial intelligence by big companies is exploding—and the soaring cost has some of them pumping the brakes in a way that could complicate AI’s triumphal march across the economy.”

“Some enterprises have hit their annual budget in just three months or reported seeing their AI spending bills double or triple.”

“Top technical executives at Uber Technologies, Meta Platforms, Microsoft, Salesforce, DoorDash and other companies have all talked about new efforts to ensure AI use contributes to productivity or have taken steps to reduce the availability of some tools for certain employees.”

“That would potentially hurt Anthropic or ChatGPT maker OpenAI as they take steps toward public listings this year.”

“All-you-can-eat subscriptions amounted to a subsidy by the model-makers, which often lost money on the intensive activity of power users. Exhorted to embrace the wave of change, employees at some companies engaged in tokenmaxxing, or using as much computing as possible in order to be seen as AI-forward—a practice that continued even as the model companies shifted to usage-based pricing.”

“Higher costs may eventually steer users toward cheaper models that cost a fraction of the price, but many companies remain wary of such AI systems because several of the cheapest options were developed in China, according to executives. Anthropic, OpenAI, Google and others also offer cheaper versions of their flagship models, and Factory and others have developed systems to help companies triage queries and steer some tasks to cheaper options.”

“Salesforce introduced a system for tracking how token use ultimately contributes to positive business outcomes.”

“Amazon has shut down an internal leaderboard that tracked employees’ use of AI tools after workers tried to boost their scores with unnecessary activity that increased the company’s computing costs.”

“Amazon had started to use a metric called “normalised deployments”, evidence of engineers regularly using AI to create useful code, to measure the success of its AI tools and adoption of the technology rather than outright token consumption.”

Coinbase laid-off 14% of its workforce. It’s an adjustment to the crypto current bear market and to become more AI-native in how the company operates. - Reuters, Brian Amstrong

“Today I’ve made the difficult decision to reduce the size of Coinbase by ~14%.”

“AI is changing how we work. Over the past year, I’ve watched engineers use AI to ship in days what used to take a team weeks. […] We are adjusting early and deliberately to rebuild Coinbase to be lean, fast, and AI-native.”

“Fewer layers, faster decisions: We are flattening our org structure to 5 layers max below CEO/COO. Layers slow things down and create coordination tax. The future is small, high context teams that can move quickly.”

“No pure managers: Every leader at Coinbase must also be a strong and active individual contributor. Managers should be like player-coaches, getting their hands dirty alongside their teams.”

“We’ll also be experimenting with reduced pod sizes, including “one person teams” with engineers, designers, and product managers all in one role.”

Jack Altman interviewed Joe Lonsdale from 8VC on Uncapped. - Uncapped

“Palantir is kind of the center of the AI world in terms of what’s working, in many ways.” What Palantir figured out (FDE motion, workflow-ontology extraction, knowing where to apply LLMs) became the center of the broader AI playbook.

“When I wrote the check into Anduril, multiple people told me they would never work with me again. You had to be willing to go completely against the cultural zeitgeist and be excommunicated which is sometimes the most valuable thing to do.”

“There will be about a dozen neo defence primes that completely crush it. I don’t think there’ll be that many more. There are already probably eight or nine really crushing it. Anduril is the biggest one and will make the most money.”

“In the ‘90s, about 80 defence companies merged into eight primes. Then the tech wave hit, and all their core tech talent left. They don’t have computer-science talent and don’t understand what it is.”

“At 8VC we track thousands of talented engineers - I’ve done this for 15 years — and none of them were going into the primes. The few that did left quickly because they’d be rejected, get no upside, no cultural building.”

“When we talk about investing in AI, we talk about six levels: energy is the base, then chips, then data centers, then models, then software infrastructure, then apps and services.”

“You need a lot of young people on your team who are friends with the best programmers and in the talent networks. It’s going so young, even accelerator programs are getting extremely young. These kids who are 18 but AI-native and have been programming a long time.”

Turner Novak interviewed Tomasz Tunguz from Theory Ventures. - The Split

AI is a three-layer stack: data center + chip + model. Full vertical integration takes 7-10 years and will only make sense for the top 5 AI companies.

Google has all three.

Anthropic has only the model (Netflix-on-AWS). For Anthropic, the play is run as fast as possible, win share with model quality, then decide later about vertical integration.

xAI has data center + model but no chip yet.

Six markets are owned by incumbent AI roadmaps (OpenAI, Anthropic): agentic coding, health, finance, legal, software/infra automation, security.

“75% of all US GDP growth this year is AI.”

Token efficiency doubles roughly every year. Google has said for two consecutive years that it generates 80% more tokens per GPU-hour than the year before.

Model performance is converging: initial advantages on specific benchmarks (agentic tool calling, math, knowledge retrieval) are getting subtle. Ultimately distribution, workflow capture, and adoption matter more than raw model quality.

Agentic coding is the king PMF because it sits at the intersection of: huge tech spend + huge labor spend + infinite demand + closed-loop testability (code either runs or doesn’t).

Tomasz Tunguz is spending time into 3 areas:

Online advertising,

Specialised inference (e.g. real-time/fast inference, image/video inference, long-running background-task inference),

AI-native email (rebuild the email layer around agents reading/triaging on your behalf).

Patrick O’Shaughnessy interviewed Gavin Baker from Atreides Management. - Invest Like the Best

Anthropic has burned ~80% less capital than OpenAI to reach similar revenue scale and is likely already cash-flow positive.

Anthropic has deprecated Claude’s intelligence by ~70% on Opus (fewer tokens per question) to manage compute scarcity.

If Anthropic could wave a wand and get unlimited compute, they’d be at $100–200B run rate today vs. the $50B constrained number.

Watts shortage in AI will start to ease in 2027–2028 as turbines and alternative power come online. The new bottleneck is zoning, approvals, and political backlash, not energy.

New game theory for AI labs: a prisoner’s dilemma over whether to release frontier models via API. If everyone abstains, Chinese open-source falls behind; if one defects, they capture revenue and pull ahead.

Elon’s Terafab will work. It’s a joint venture with Tesla and SpaceX to produce AI chips. The Intel partnership delivers 50 years of process knowledge from just a few quarters behind the frontier. The A-teams at ASML, KLA, Lam, and AMAT will show up because of Elon’s hardware reputation — same reason TSMC originally caught Intel. And Elon will relocate Taiwantown, Japantown, Koreatown next to the fab to recruit the best engineers.

AI just shifted from all-you-can-eat to usage-based pricing. This is why OpenAI and Anthropic will exceed $200B in ARR this year. Sad consequence: the real frontier is only visible to enterprise customers; everyone else is on lobotomized rate-limited versions.

Turner Novak interviewed Ali Partovi at Neo. - The Split

Neo turned $120–150M into $1.2bn+ across two consecutive funds, both on track for 10x+ DPI. Cursor and Kalshi were two of the major drivers (Kalshi in Fund I, Cursor in Fund II).

Allocate ~90% of attention to people, ~10% to idea/business plan. Smart founders course-correct away from bad ideas quickly. Dumb ideas don’t survive contact with a brilliant operator.

The #1 trait Ali looks for in a founder is magnetism: would their friends follow them? It comes in different flavors (quiet/Michael Truell-style or flamboyant), and there’s no checklist, but you feel it.

Other key traits: risk tolerance, willingness to do what peers are afraid of, and “mischief”: a healthy disregard for arbitrary rules, first-principles thinking. Not dishonesty; integrity is a hard prerequisite.

Childhood entrepreneurship is one of Ali’s strongest predictors. Tony Hsieh sold worms in 4th grade, Alfred Lin arbitraged pizza in his Quincy House dorm. Selling anything in person trains rejection tolerance and “I can make something people want.”

Beyond people, the only non-people criterion: “if it succeeds, it has to be huge.” Ali explicitly looks for ideas that will probably fail as that filter selects for ambition. Incremental ideas (10% better coffee lid) get filtered out.

“Smart people don’t pursue a dumb path very long before correcting it.”

“”The fear of failure drives a lot of first-time founders into ideas that will probably succeed, but those are usually the incremental ones.”

“Risk minimization is a huge mistake. You should always be looking to maximize reward, which means look for where the risk is and steer toward it.”

The “people not ideas” thesis was forged by missing PayPal and Google. As a 26-year-old at Link Exchange, Ali knew Max Levchin (then 22, the firm’s best contractor engineer) was a genius — but passed on his Palm Pilot infrared-payments idea because the concept was absurd. Same with Google: he knew Craig Silverstein was a top-3 CS mind at Harvard, but thought “the 11th search engine” was hopeless. Both became defining misses. The realization: smart founders course-correct fast; bad ideas don’t survive contact with brilliant operators.

Mapping the future of a sector causes you to miss teams that don’t fit your map. Cursor pitched CAD autocomplete; Kalshi pitched prediction markets at a time when the US market consisted of one nonprofit and was legally questionable. Both were misses for thesis-driven funds.

Invest Like the Best interviewed Brian Chesky, who is cofounder & CEO at Airbnb. - Colossus

Founders are born, CEOs are not. Founder instinct is innate, but the CEO job is counterintuitive. Almost all of your founder instincts about what to do as CEO are wrong. The danger is learning on the job through trial and error, because by the time you correct a mistake the mis-hire has built an empire that takes years to unwind.

Covid forced Brian to move to founder mode. By 2019, with 7,000 employees, he felt like he was driving “a car without a steering wheel.” Losing 80% of revenue in eight weeks forced him into total control. He reviewed every detail of the company for two to three years, working ~100 hours a week.

It’s better to give ground grudgingly than delegate first & intervene second when something goes. Start hands-on, teach by doing, and let go over time.

AI founder mode will be even more intense than founder mode. Information that used to require 35 hours of meetings a week is now available on demand. The shape of management changes: fewer layers, asynchronous over meeting-based, every manager must remain technical.

Brian thinks the next 12–24 months will see a consumer AI renaissance. Today, founders don’t build in consumer for 4 main reasons: (1) fear that ChatGPT will kill it, (2) no proven consumer business model (subscriptions, ads, and e-commerce are all hitting local maxima against free competitors), (3) Silicon Valley moves in trends, and the trend is enterprise, (4) consumer is genuinely harder (more hits-driven, requires excellence in design, marketing, culture, press, not just sales and tech).

“Two types of people will not survive the age of AI. Pure people managers. And people who are rigid and don’t want to change.”

Hiring is the job. Founders should spend 50% of their time hiring.

Build pipelines, don’t run searches. Searches give you ten résumés. Pipelines mean constantly meeting people and mapping the talent ecosystem.

Start with the result you admire and work backwards to the people behind it.

Co-hire two layers deep.** He is the co-hiring manager for the top 200 people at Airbnb.

Hire so high it’s reaching. “Your executives should hire people so good they wouldn’t work for them without my help.”

Hiring vs. managing is one for one. The more time you spend hiring, the less you have to spend managing. Great hires are self-managing.

David Senra interviewed Adam Foroughi, who is cofounder & CEO at AppLovin. - David Senra

“I would have given up a quarter of the company for a million bucks. The VCs said no, and the same VCs put a lot of money into our competitors a year later. That was very motivational.”

“I never wanted to lose the best talent. At any given moment I want the best talent in the most important roles. If you don’t do that trade, your best people start their own businesses.”

“Make the advertiser an arbitrageur. If they spend a dollar and know with certainty they’ll make more than a dollar back, the only constraint on scale is the cash in their bank account.”

AppLovin’s first product was an app-recommendation app. It was a terrible app, but the recommendation engine had crazy conversion. They scrapped the app, packaged the engine as an SDK, and sold it to mobile gaming companies.

By 2018 Facebook’s ad model was visibly more potent because they had advertiser-purchase data (pixels on every site, billions of conversion events). AppLovin couldn’t get advertisers to share that data. So AppLovin bought the advertisers: 14–15 mobile gaming studios were acquired specifically to feed in-game purchase data into the ad model. With in-house studios & customers, AppLovin ended up training its model on 50%+ of mobile gaming ad spend. At this point, it sold its gaming division to Tripledot fully realigning AppLovin with its customers.

A players don’t tolerate B players. If you let a B player get hired into a critical role, your best engineer quits within months and starts a competitor. Therefore: cut early, cut often, and put extreme leaders in roles where they have no patience for anything sub-A.

The mobile gaming audience asset (~1bn daily users, average ad watched 35 seconds, middle-aged) can be leveraged not only for gaming ads but also for e-commerce and broader SMBs (e.g. discovering your next restaurant on a AppLovin’s powered mobile game).

Jack Altman interviewed Kevin Hartz & Bennett Siegel from A Capital* on Uncapped. - Uncapped

“There are two ways to make a billion dollars. One is the Benchmark way — partner with a generational Series A. The other is put a billion dollars into a company and double your money as it goes public in three years. One is a lot easier than the other.”

A maps talent, not markets. The investing operating system is to identify high-density nodes of talent (top universities, Palantir, Stripe, Jane Street, top accelerators) and work the social graph outward.* High-quality people hang out with high-quality people.

Palantir has the highest per-capita rate of unicorn founders. Reason: every Palantir employee was a “mini CEO” — they had to build, ship, and find product-market-fit themselves. Plus there’s a non-consensus mindset implied by wanting to work at Palantir in the first place.

50% of A’s seeds are “pseudo-proprietary.”* Meaning A* was first to reach out, had a prior relationship, an informed insight, or some thesis going in — not a cold round process. The pseudo-proprietary half has disproportionately generated returns. Shotgun marriages (3-day round processes with new founders) have higher volatility.

Concentration is everything in seed. A* runs a reserve-heavy model: >50% of fund dollars are deployed after the initial seed check. Out of ~40 seed investments, 3–5 companies end up with the lion’s share of capital. If all you’re writing is the first check at seed, it’s exceptionally hard to drive fund-returning multiples.

Hardware now offers a structural moat. A vibe-coded app can be cloned in minutes. A sensor in the physical world cannot. That’s why A* is increasingly drawn to hardware-enabled and sensor-grounded plays despite the historical pain in hardware investing.

Paul Graham did a YC Keynote in Stockholm. - YC

Every era has a single global center for any intense human pursuit: Paris for painting in 1870, Göttingen for math in 1900, Hollywood for movies in 1950, Silicon Valley for startups today. The answer to “should I go?” has been “yes” for thousands of years.

Entrepreneurs get 4 benefits by building in SF:

Talent density: more people and better ones, all clustered together.

Serendipitous meetings that can change the trajectory of the business.

Quicker fundraising.

Respect at home: local investors automatically upgrade their view of you once you’ve left.

The biggest benefit is not what Silicon Valley does for you but what it does to you. In the valley, you finally measure yourself against known big fish — a Brian Chesky, a Sam Altman — and the typical reaction is “this guy isn’t a different species; I could do what he did if I worked that hard.

YC is engineered to compress Silicon Valley into 3 months. It’s a “super valley within the valley,” with maximum founder density, instant colleagues, and investors who have to decide on minute-level timescales.

YC’s data shows founders who return home post-batch are about half as likely to become unicorns.

Entropy

Franchising is the engine that has minted more American millionaires than almost any other business model. - The Economist 1, The Economist 2

Franchising now accounts for c.850k US outlets run by c.250k owners. It thrives because aligns incentives dividing labour between a brand-focused franchisor and a locally-savvy franchisee.

The model has flourished under good regulation (mandatory FDD disclosure since 1979) but is endangered by bad regulation, chiefly “joint-employer” rules that would make franchisors liable for franchisees’ workers centralising the system, gutting its advantages, and ultimately hurting the workers it employs.

“One in eight businesses with at least one employee in America is a franchise—roughly double the share in its closest international rivals, such as Japan and Germany.”

“All kinds of establishments, from Dunkin’ Donuts to the UPS Store and most Marriott hotels, are franchised. Lately the model has been spreading into new areas—such as boutique fitness, home services and child care—thanks in part to private-equity investors that have become enthusiastic franchisors.”

“Some 95% of McDonald’s 14,000 American outlets are operated by franchisees, and the chain has plausibly created more millionaires than any firm in history.”

“Franchisors, who typically maintain control over things such as menus and opening hours, gain a network of motivated entrepreneurs prepared to put down their own capital, allowing the company to scale quickly. In return, franchisees are given the opportunity to run their own business with the security of an established brand.”

Bill Gurley recorded a podcast on China with Dan Wang and Patrick McGee who both wrote books on the country. - Bill Gurley

“China is at the engineering state — very liberal-minded, including about the population. The US is the lawyerly society, which can sometimes create wealth but is more interested in protecting existing institutions.”

“The Chinese have learned pretty much everything good about America and replicated most of it, except for the political system. They are far more capitalist than the United States is.”

“I don’t know if Chinese manufacturers will ever make money, but I came away not wanting to invest in any manufacturing business in the rest of the world.”

“China is going to make about 45% of global manufacturing by 2030. That’s similar to where America was at the end of World War II.”

The Western corporate worldview says product design and retail are high-margin and the manufacturing “middle” is the low-margin grunt work. Once China dominated that middle, nobody else can profitably manufacture against them and it’s easier for China to climb the value chain and do product design. The result: dominance in solar, EVs, the lithium-ion battery chain, and increasingly drones, consumer electronics, and active pharmaceutical ingredients.

China has become the global epicentre of automotive innovation. - The Economist

“To stem their loss of market share, carmakers around the world are looking to become more like their Chinese competitors—and not just when operating in China.”

“The market share of foreign firms in China has almost halved in five years, to around 30% in 2025.”

“In Europe over the past five years, Chinese brands have gone from almost nowhere to nearly 9% of all sales.”

“Chinese cars are cheap. They are also packed with whizzy technology.”

“Production processes designed around EVs, combined with deep vertical integration and a greater willingness to improve vehicles after they are released via software updates, mean it takes 24 months at most in China [to bring a new model to the market vs. 40-80 months for Western counterparts].”

“Even Renault, which does not sell cars in China, is now using the country to hasten its innovation: its latest Twingo model, though designed in France and manufactured in Europe, was developed in China to save time and money and glean know-how.”

“China speed is the result of a culture of long hours and an industry that has been built from the start around software-infused EVs. Restructuring legacy carmakers that have relied for decades on petrol power and mechanical engineering will be tough.”

“To avoid falling irrecoverably behind Chinese competitors in EVs, incumbent carmakers may have little choice but to strike partnerships. But in doing so, they run the risk of ceding expertise in the areas that will define the future of the auto industry. That would leave them at the mercy of the rivals they fear the most.”

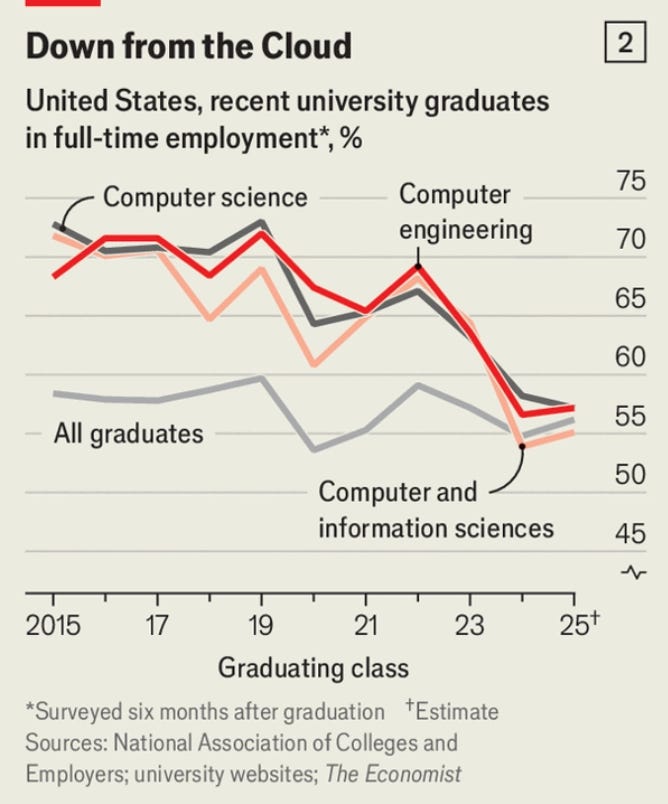

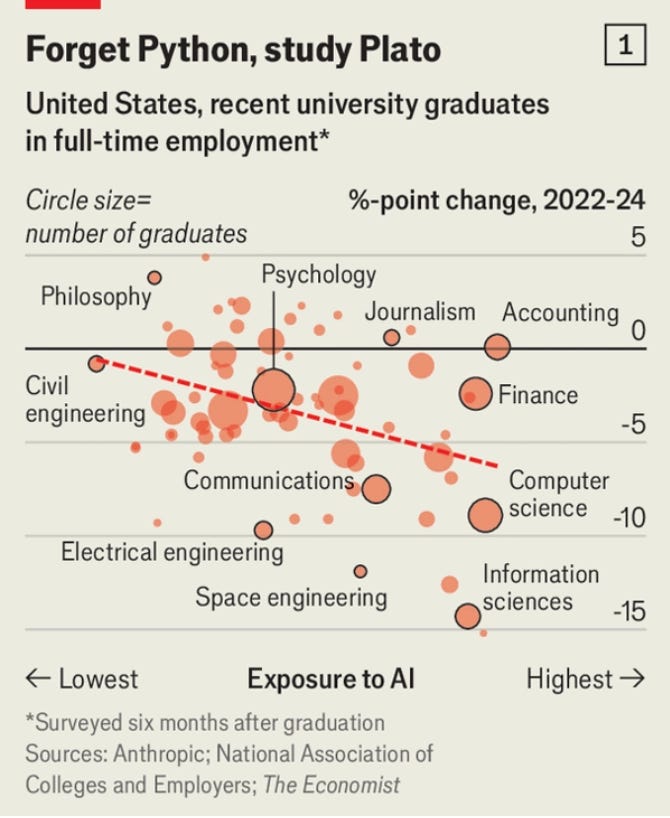

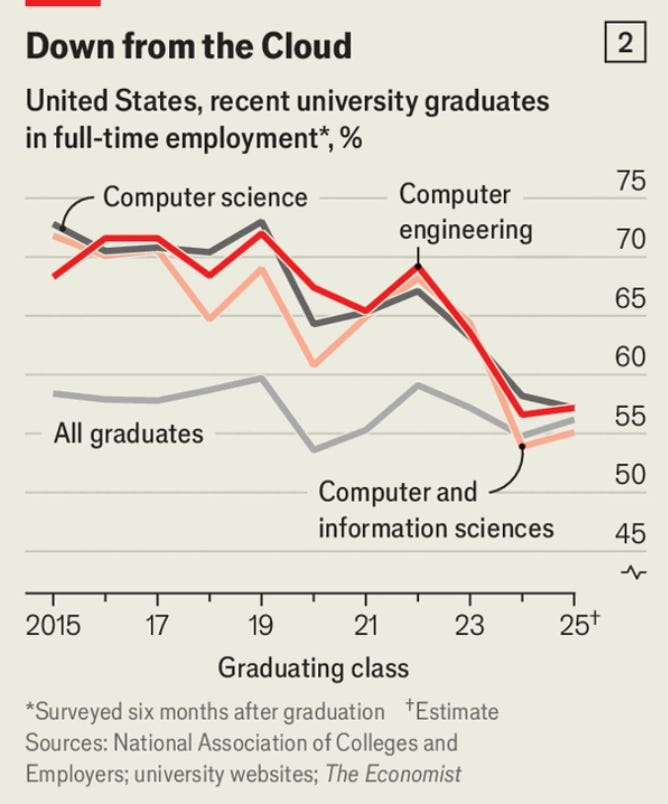

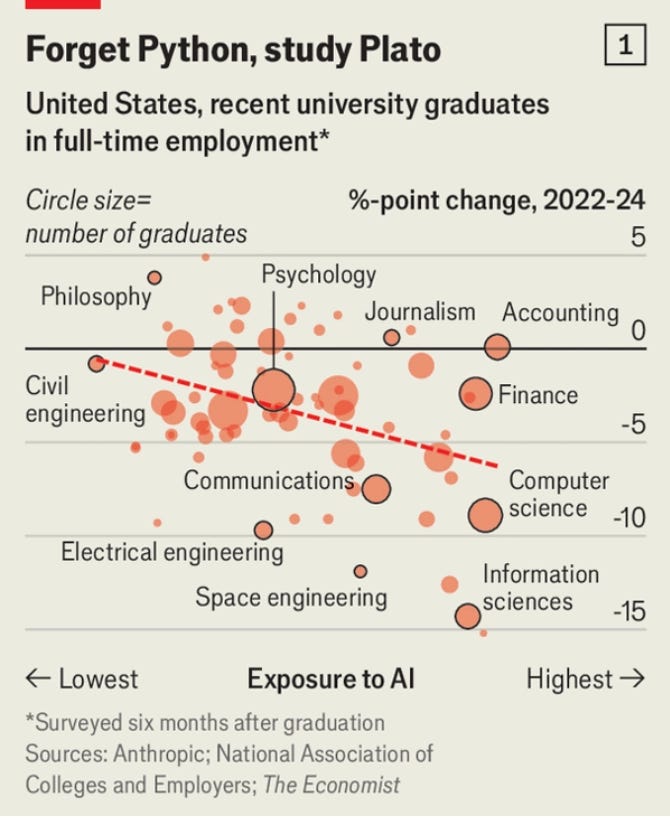

AI is impacting the job market for young graduates. - The Economist

“Our analysis suggests AI may indeed be harming some graduates’ job prospects.”

“Recent graduates are likelier to be unemployed than the average American.”

“Less than a fifth of [recent graduates] think this is a good time to find a good job—the lowest share in over a decade.”

“More than half of employers say they have considered replacing entry-level workers with the technology.”

“We found that graduates in fields more exposed to ai have suffered markedly worse outcomes. Between 2022 and 2024 graduates in the least-exposed quintile—studying subjects such as education, philosophy and civil engineering—saw their average full-time employment rate fall by just 1.5 percentage points. Those in the most exposed quintile—including computer science, computer engineering and information science—suffered a 6.6 percentage-point drop.”

“The rate of full-time employment fell from nearly 70% to 55% in three years—notably, the three years following ChatGPT’s release in 2022. Prior to that, it had been stable.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

i feel like you guys are one of the more contrarian European voices. tbh would be interesting to track which European founders raised in dollars vs euros