📖 Venture Chronicles - May 2023

Overlooked #147

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of May.

For 2023, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for May!

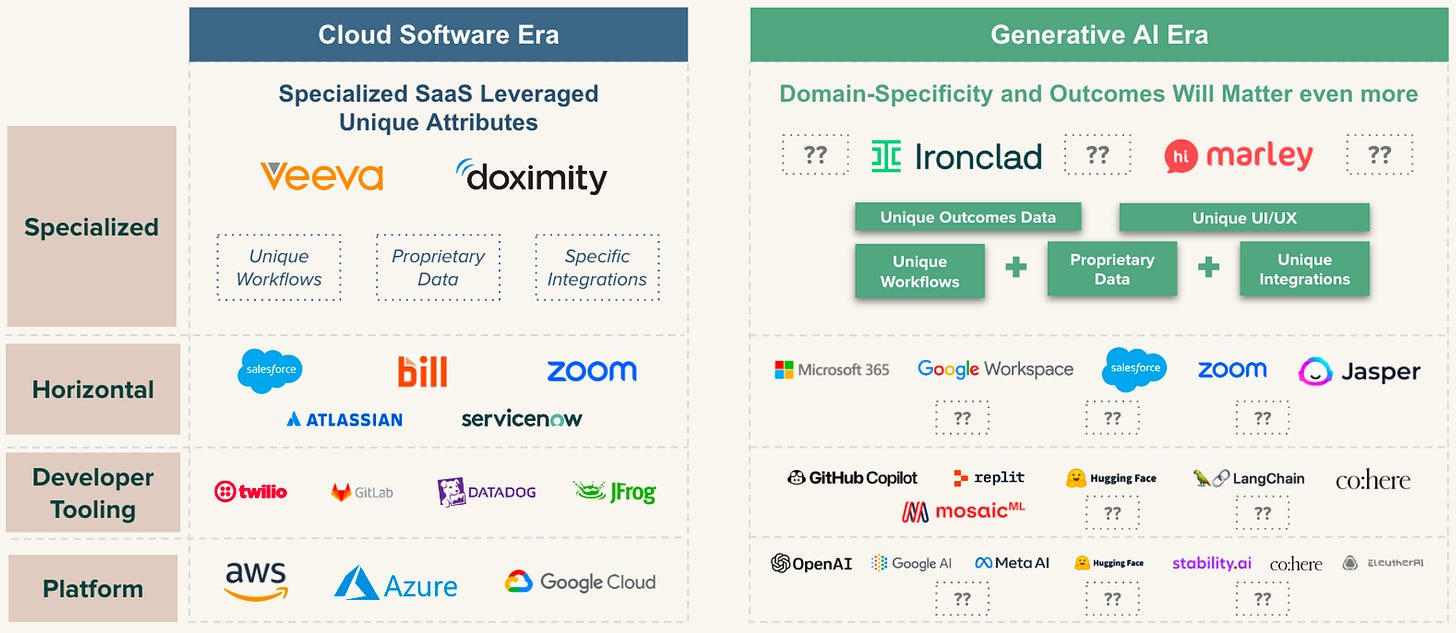

Monday, May 1st: Gordon Ritter at Emergence wrote about the impact of generative AI on specialised software. - Emergence

“What began as broad, horizontal software narrowed and became specific, and later became industry-focused. In this next age of technology [driven by gen. AI], specialized software and proprietary data are even more important than they were in the cloud era.”

“Today, generative AI applications are starting broad, just as early cloud companies did, but the key difference is that the underlying technology is closely aligned with Microsoft, Google, Meta, and others who are the largest players in tech. This is different from the cloud era in that Salesforce, Workday, ServiceNow, etc. were startups and built from the ground up. With big tech owning much of the broad horizontal applications, startups should focus on building in specific domains with narrow context.”

“I see two ways forward to build a lasting, defensible business: (i) major in generative AI’s emerging technical capabilities and hunt for a function or vertical problem that benefits from your insights, (ii) major in deep domain expertise and market relationships, and form a team to add in the technical knowledge.”

“In the age of generative AI, one lesson remains true: the tighter your context and industry, the wiser your model and product.”

Tuesday, May 2nd: a16z wrote about payment solutions in high-risk industries (e.g. gaming, sports betting, telehealth or cannabis). - a16z

“There’s now an opportunity to couple payments [in these high-risk industries] with a vertical-specific software layer to offer better compliance, wallets, tools for identity management and fraud detection, reconciliation, and more.”

a16z gives concrete examples of software based features that can be built: (i) reconciliation & dispute workflow tools for travel, (ii) geolocation for sports betting, (iii) built-in fraud prevention for sports betting.

Wednesday, May 3rd: I listened to a podcast titled Beyond 8 Figures with Mews’ CEO Matthijs Welle. Mews is a PMS catering to large independent hotels and small to mid sized chains. - Beyond 8 Figures

“We’ve got a coach for the individuals in the leadership team and then she coaches us as a group as well at the same time.” “Every three months we have this coach come bring us together into a room where we actually spent two days in the room getting to know each other again over and over.” “The level of trust that we’ve now built into our leadership is at a level where I think everyone gives each other feedback.”

The impact of Covid-19 on the hotel industry was profound. c.70% of Mews customers had to shut down their establishments. Mews had no choice but to lay-off 220 people amounting to 50% of its workforce. But, in retrospect, the pandemic presented an opportune timing for hoteliers to upgrade their technological stack.

Mews undertook a major shift in its go-to-market strategy transitioning from from the SMB segment to the mid-market/enterprise segment when most competitors tend to initiate and remain in the SMB segment.

“Oracle was the number one [in the midmarket/enterprise segment]. We’re there to take them out because they’re not doing a good job and they’re doing a disservice to hotels. I’m a hotelier and I deeply care about hotel experiences, they’re just holding our industry back. They’re holding it in hostage almost.”

Thursday, May 4th: I listened to a Colossus’ podcast episode with Bessemer’s partners Jeremy Levine, Kent Bennett and Brian Feinstein. It talks about how Bessemer operates and about their individual investment style. - Colosssus

Andrew Carnegie, Henry Phipps and Henry Frick invented the Bessemer process in the steel industry while building Carnegie Steel. The Bessemer process allowed for making steel in high volumes and at a low cost. J.P. Morgan purchased Carnegie Steel to build a monopoly in the steel industry under the US Steel umbrella. The acquisition made Carnegie Steel’s founders very rich. Subsequently, Phipps established a family office named Bessemer using its proceeds to invest in high risk and high growth opportunities. Initially, Bessemer focused on the industrial sector before transitioning into the IT sector in the 70s. The founding family continues to play an important role at Bessemer even if the firm has also third party limited partners.

Bessemer has 20 investment partners who operate in a “highly disaggregated and empowered manner”. This firm is not a consensus driven firm allowing partners to make investments even without a strong consensus amongst the partnership. Each partner grades potential deals on a scale from 1 to 10. The deal is validated as long as the average vote is above 5.5. Partners have autonomy over their investment decisions and are accountable for their track records. For entrepreneurs, there is no need for a meeting with the entire partnership and the lead partner can independently make follow-on investment decisions without seeking approval from the partnership.

“We encourage more autonomy than almost any other venture firm, both with respect to decision-making and investment style.” “Autonomy is important because conventional wisdom says you can't scale venture capital.” “We've cracked the code on how to scale to venture capital by enabling each individual partner to have that autonomy to pursue whatever investment areas they want to pursue and make the best decisions they possibly can.”

“The behaviour we have here is roadmap based, which means every partner will pick up over time, a number of essentially themes they're interested in, we call them roadmaps, and we go off and do a bunch of homework on those themes, typically, before we make our first investment, and we start talking to each other about them. […] When you bring in a company that's squaring a roadmap, your partners know that you're within a lane that you've thought a lot about.”

Bessemer’s best roadmaps come from (i) major technological shifts (e.g. cloud, LLMs) or (ii) learnings from portfolio companies which over-performed our expectations (e.g. user generated content: more content generates more traffic which generates more content | vertical software: “you can trade market size for market share”).

The partners favour investments in (i) products that are clearly better than alternatives at the time of the investment (“it must be a slam duck for customers buying them”), (ii) strong capital efficiency (investing in companies which don’t require money), (iii) clear path to market leadership.

There have been several evolutions in vSaaS: (i) pure SaaS models (Procore), (ii) SaaS embedding payments and other financial services (Mindbody, Toast), (iii) AI driven vSaaS which makes software adoption viable for certain verticals.

Three categories of vSaaS opportunities exist: (i) greenfield opportunities (there are less greenfield vertical markets today than 10 years ago but increasing the take rate by combining business models can make some smaller vertical markets attractive), (ii) replacement cycle opportunity coming with a product 10x better and/or 10x cheaper, (iii) AI-based vSaaS that transforms services into software through AI (e.g. EvenUp and demand letters in the legal space).

Friday, May 5th: Shopify recently made a strategic decision to refocus on its core competency - serving as a premier e-commerce platform. This led to the company stepping away from its product expansion into logistics. It also sold its logistic fulfilment operations to Flexport (in exchange for a 13% stake in Flexport) and its warehouse robotics operations 6 River Systems to Ocado. - Shopify, WSJ

“Shopify finds it useful to talk about the difference between main quests and side quests internally. The main quest of the company is its mission, the reason for the company to exist. Side quests are everything else. Side quests are always distracting because the company has to split focus. Sometimes this can be worth it, especially when engaging the side quest creates the conditions by which the main quest can become more successful.”

“Shopify’s main quest is to make commerce simpler, easier, more democratized, more participatory, and more common.”

Saturday, May 6th: Semi Analysis published a leaked internal document at Google claiming that open source AI will outcompete any proprietary AI. - Semi Analysis

“The uncomfortable truth is, we aren’t positioned to win this arms race and neither is OpenAI. While we’ve been squabbling, a third faction has been quietly eating our lunch. I’m talking, of course, about open source.”

“Open-source models are faster, more customizable, more private, and pound-for-pound more capable.”

“People will not pay for a restricted model when free, unrestricted alternatives are comparable in quality.”

“Paradoxically, the one clear winner in all of this is Meta. Because the leaked model was theirs, they have effectively garnered an entire planet's worth of free labor. Since most open source innovation is happening on top of their architecture, there is nothing stopping them from directly incorporating it into their products.”

Sunday, May 7th: Gergely Orosz penned an insightful piece about the downfall of Fast. For contect, Fast was an e-commerce enabler offering one-click checkout to merchants. It secured a $102m series B in Jan. 2021 led by Stripe at a valuation close to $500m. However, by Mar. 22, it had to cease operations and layoff all its employees. - The Pragmatic Engineer

In 2021, Fast recorded a mere $600k in revenues while burning $10m per month.

“The Fast story should be a warning sign that a well-funded scale-up could be closer to bankruptcy than it seems.”

“Exploding [equity] offers because of “the inevitability of the Series C closing” was used as a tactic to close candidates at the end of 2021.”

“Fast did less than $300k worth of sales and below $6k in revenue on most days from January 2022 to April 2022. There were days with around $2,000 in revenue for Fast. This meant checkouts were completed in the low thousands. The biggest merchant on the platform would have 500-1,000 sales per day.”

“The average volume of Fast customers was low because most customers were from small businesses. And yet, every small business needed custom engineering work to be done, making integration slow.”

“Despite the warning signs, no employee within Fast expected bankruptcy to be on the table until The Information published their series of articles.”

“Affirm is hoping to take on a good part of Fast’s engineering team. In a deal negotiated by Fast’s engineering leadership, Affirm is extending offers to about 100 of the 150 engineers at Fast.”

Gergely shared several tips for prospective employees considering joining a new startup: (i) research the company and its founders, (ii) ask for numbers on sales & runway, (iii) conduct reverse interviews your future manager and founders, (iv) ask to talk about the lead investor, (v) speak to former employees.

Monday, May 8th: Bessemer published its 2023 State of the Cloud. - Bessemer

Tuesday, May 9th: PermitFlow raised a $5.5m seed round led by Initialized. It’s a US-based construction startup created in 2021. It assists developers, architects and general contractors in streamlining the construction permit application and management process. Today, the permitting process is mostly done manually with construction companies interacting directly with municipalities. PermitFlow offers an integration on the Procore’s marketplace. It will use the funding to expand its geographical presence in other US cities and to grow its team. - Techcrunch

Wednesday, May 10th: Boston Globe wrote a deep-dive on Toast and on its cofounders. - Boston Globe

Toast collaborates with 79k restaurants, employs 4.5k people and generates $3bn in sales. It has successfully disrupted established players such as Oracle and NCR. Toast’s cofounders previously worked together at e-commerce startup Endeca which was sold to Oracle to $1bn in 2011. “Endeca founder Steve Papa was so impressed by the trio when they worked for him that he invested $500k — and eventually a total of $10m.” Besides the POS, Toast added other features like real-time communication with the kitchen, mobile payment and payroll.

“The three friends hadn’t decided on a focus for their startup when they began meeting at coffee shops and bars, where they noticed inefficiencies — including waiting for their checks. They initially tried to build a mobile payment app, but pivoted to point-of-sale terminals when they realised how little technology had penetrated the restaurant industry.”

“Toast’s success opened doors for other startups aiming at specific markets with cloud software and payments features, including auto repair shop-focused Shopmonkey and laundromat server Cents.”

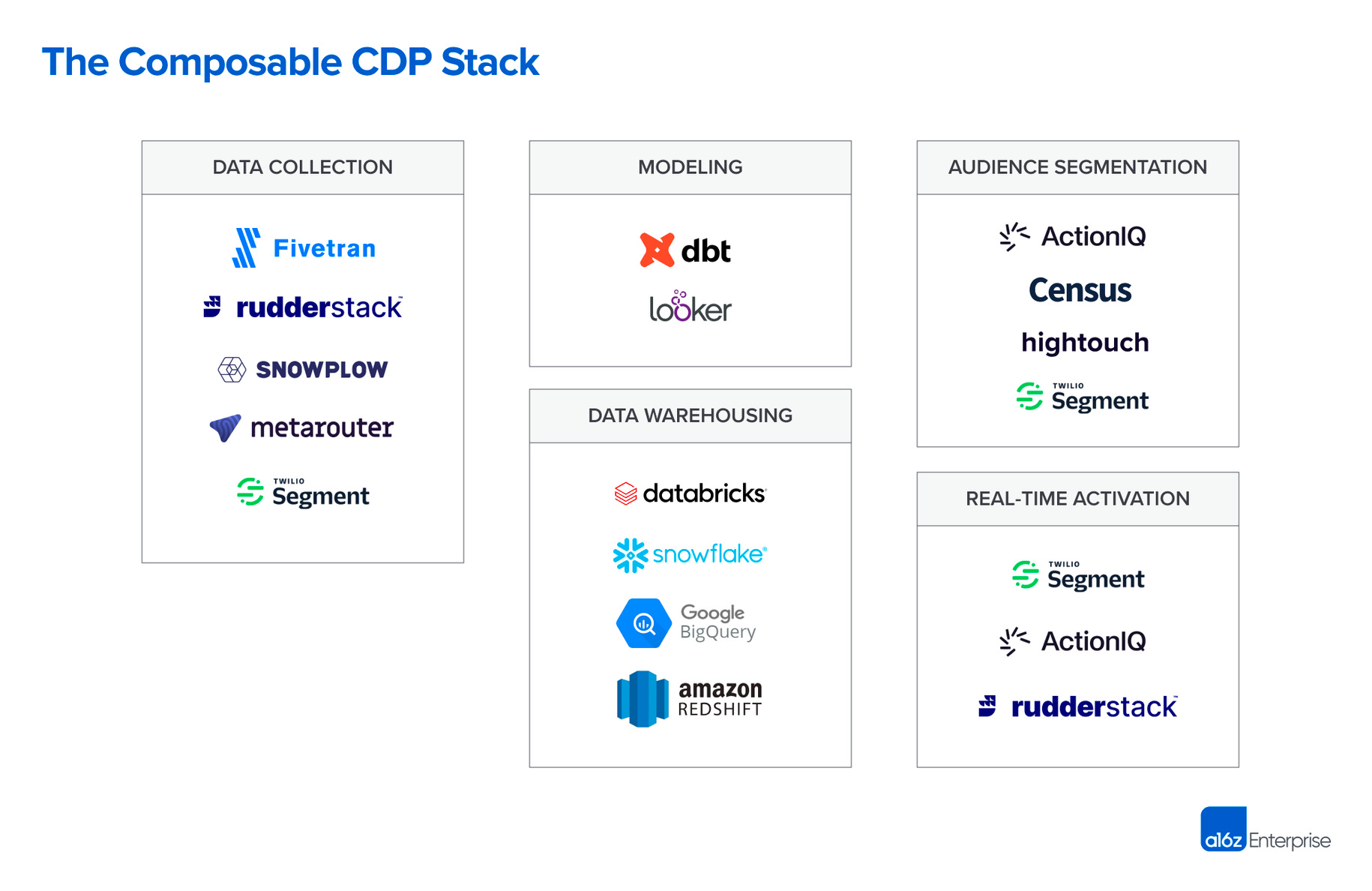

Thursday, May 11th: a16z wrote about the rise of composable Customer Data Platforms (CDP) like Hightouch or Census. - a16z

Composable CDPs are built on top of data warehouses. They don’t store customer data (which was historically the case for CDPs) and are data warehouse agnostic (vs. Salesforce and Adobe forcing their CDP’s customers to use their data warehouses). They have a no-code interface for business users to activate the customer data without SQL knowledge.

“For first-party data, traditional CDPs deploy a proprietary tag or SDK to collect digital behavioural data (e.g., clicks, page views, etc.) in real-time. For third-party data, such as CRM or payments data, products that specialize in ELT pipelines with built-in integrations across a wide range of SaaS platforms have emerged as the clear best-of-breed option.”

Friday, May 12th: I read a post from Yoni Rechtman who is an investor at Slow Ventures arguing that vSaaS should become Group Purchasing Organisations (GPOs). - Yoni Rechtman

“Group purchasing organizations (GPOs) are syndicates of similar businesses that buy supplies together and use their collective purchasing power to extract discounts from vendors. GPOs take a cut of the discounts as revenue, charge a fee to participate, or both.”

“Forming a GPO is a network effect driven, high margin way for vSaaS companies to make money and actually drive value for their customers.”

“Because vSaaS companies typically have small ACVs and not network effects, they suffer from diseconomies of scale: CAC becomes dramatically worse over time as they run out of easy customers to win. GPOs-as-a-Service could fundamentally reverse this trend.”

Saturday, May 13th: Andrew Chen at 16z shared a retrospective on a16z’s gaming fund after one year in operations. - Andrew Chen

“Last year we were very focused on studios, web3, and infrastructure. This year we’ve continued to maintain that focus, but have really started to lean into AI. In Q1 alone, we met over 100 AI x Games companies. And in 2023, 80% of the Games Fund's investments have had a major AI component - either reinventing core gameplay or creating tools.”

“A major part of a16z's differentiation has been our Operating Team that helps companies. In fact the vast majority a16z's staff focuses on that, and it's a small minority that focuses on investing.”

Sunday, May 14th: Lux published its LPs’ Q1-23 report. - Lux

“We urge our Lux-family founders to “spend” to save: spend the time and effort now to save an additional 10-15% of costs, spot and eliminate weakness and weak talents, sharpen strategic focus today amid any headwinds and confusion to set yourselves to take the market - with full force.”

“In the battle between large, centralised AI companies and specialised, open organisations, the latter will take the lead in the years ahead.” “The future is likely to be specialised, fine tuned, faster and much cheaper smaller models for each individual business use cases.”

“This is especially important as the diffusion rate of new technologies accelerates. Back in 1999, it took Netflix three and a half years to reach 1 million users; in 2004, it took Facebook 10 months; in 2008, Spotify five months; in 2010, two and a half months for Instagram; and just last year, ChatGPT did it in five days. What about 100 million users? Google Translate, launched in 2006, took six and a half years, Uber took just under six years and ChatGPT reached 100 million users in an estimated two months.”

Monday, May 15th: Kustomer spun-off from Meta and raised a $60m round at a $250m valuation from co-led by Battery and Redpoint which were previously investor in the company. Meta had acquired the company in Nov. 2020 for $1bn. Kustomer is an omni-channel CRM that supports channels such as phone, email, text messages, WhatsApp and Instagram. The funding will be used to expand its team and integrate generative AI features into its platform. This move by Meta is part of a larger strategy to increase company efficiency and focus. - Techcrunch, Reuters, Kustomer

Tuesday, May 16th: I listened to a Colossus’ podcast episode with Instacart’s CEO Fidji Simo. She is truly impressive - one of the best French operators that we have in the tech industry. - Colossus

Fidji Simo grew up in the South of France in a family of fishermen and graduated from HEC. She started her career in the tech industry working at eBay between 2007 and 2011 in San Francisco in the strategy team. In 2011, she transitioned to Facebook where she spent over a decade primarily in product roles. She ended up leading Facebook’s mobile app after having worked/launched many projects (Facebook Live, Facebook video advertising, Instant Games, monetization of the newsfeed). In mid-2021, she joined Instacart as CEO. She also serves on Shopify's board and is a co-founder of the healthcare institute, Metrodora, which focuses on neuro-immune disorders.

Gen. AI will shift the e-commerce industry towards natural language. E-commerce is not a natural experience. “You already need to know exactly which products you want, go into a search box, type that product, select that product, add it to a cart.” In reality, people want to have a conversational way to buy goods (e.g. I have this budget, I need to feed x people, I like this and that, what do you recommend?). Ideally, you would have an engage that takes all your constraints and generates a meal plan with all the right ingredients in your cart.

“AI is going to make software development easy. It means that there's going to be fewer barriers to entry. So when I advise companies, I always tell them, focus on doing the hard things.” Instacart is a “unique translation layer between the digital world and the physical world.” “The hard thing that we've built is connecting to 80k stores across the U.S., connecting to 1.1k retailers and this ability to translate your intent of cooking something for dinner into products showing up at your doors within 2h because the physical world is still going to remain pretty difficult to navigate even in an AI-enabled world”

The grocery sector is the largest commerce category ($1.1tn market in North America). Yet, it is one of the least penetrated online (12% post pandemic, 3% pre pandemic). “It’s weird because I don't think you have many people who are saying that groceries in store is so much more enjoyable than going and buying electronics or buying fashion.” It happened industry incumbents resisted this transition. Covid was a tipping point and there is no going back for the grocery industry. Instacart has emerged as a major enabler in this digital transition with the Instacart app, with specific software built for retailers (e.g. Sprouts.com and Publix.com are websites powered by Instacart’s e-commerce engine) and with hardware in-store (cf. smart carts following the Caper’s acquisition).

“An omnichannel customer that shops with you both online and in-store is more valuable, more retentive, more profitable than an online-only customer or an in-store-only customer.”

Instacart consistently lost money on every order until it reached a volume of 100m orders. Achieving scale was a necessary step for Instacart to generate profits, as it enabled sufficient network density for orders batching.

Instacart is currently focusing on several strategic priorities: (i) assisting retailers in transitioning from in-store only to omni-channel, (ii) launching Instacart Health to scale food as medicine (make prescribing food as easy as prescribing a drug, 87% of healthcare costs come from diet-related diseases), (iii) grow ad revenues (selling its ad engine to other retailers including innovative formats like sponsored products, shoppable display and shoppable video ads).

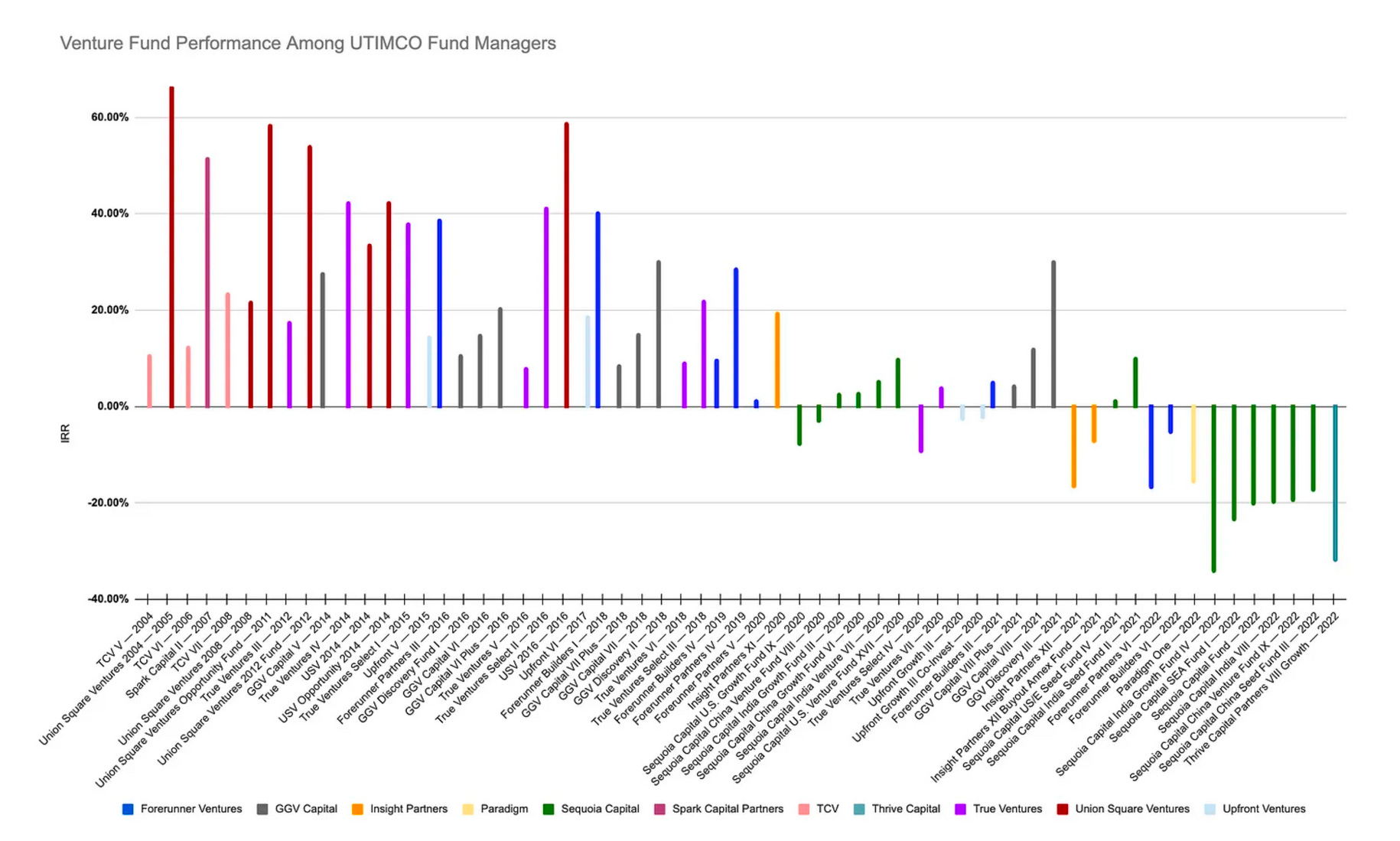

Wednesday, May 17th: Eric Newcomer shared the performance of venture funds backed by UTIMCO (University of Texas Investment Management Company) which is Texas’s public investment fund which has $65bn in assets under management. - Newcomer

USV returned $1.18bn to UTIMCO from $129m invested in different funds at an overall IRR of 59% and with remaining upside on all the vintages raised after 2004.

Thursday, May 18th: Faks raised €5m from Connect, Seedcamp and Cocoa. It’s a vSol for pharmacies. It aids pharmacies in managing their relationships with suppliers (100 suppliers on average per pharmacy) especially on after-sales related tasks (promotions, claims, expired products). Faks collaborates with 12k pharmacies in France (60% market share), 118 pharmacy associations and 700 pharmaceutical companies. It raised to consolidate its market position in France and to expand in other geographies. - EU.Startups

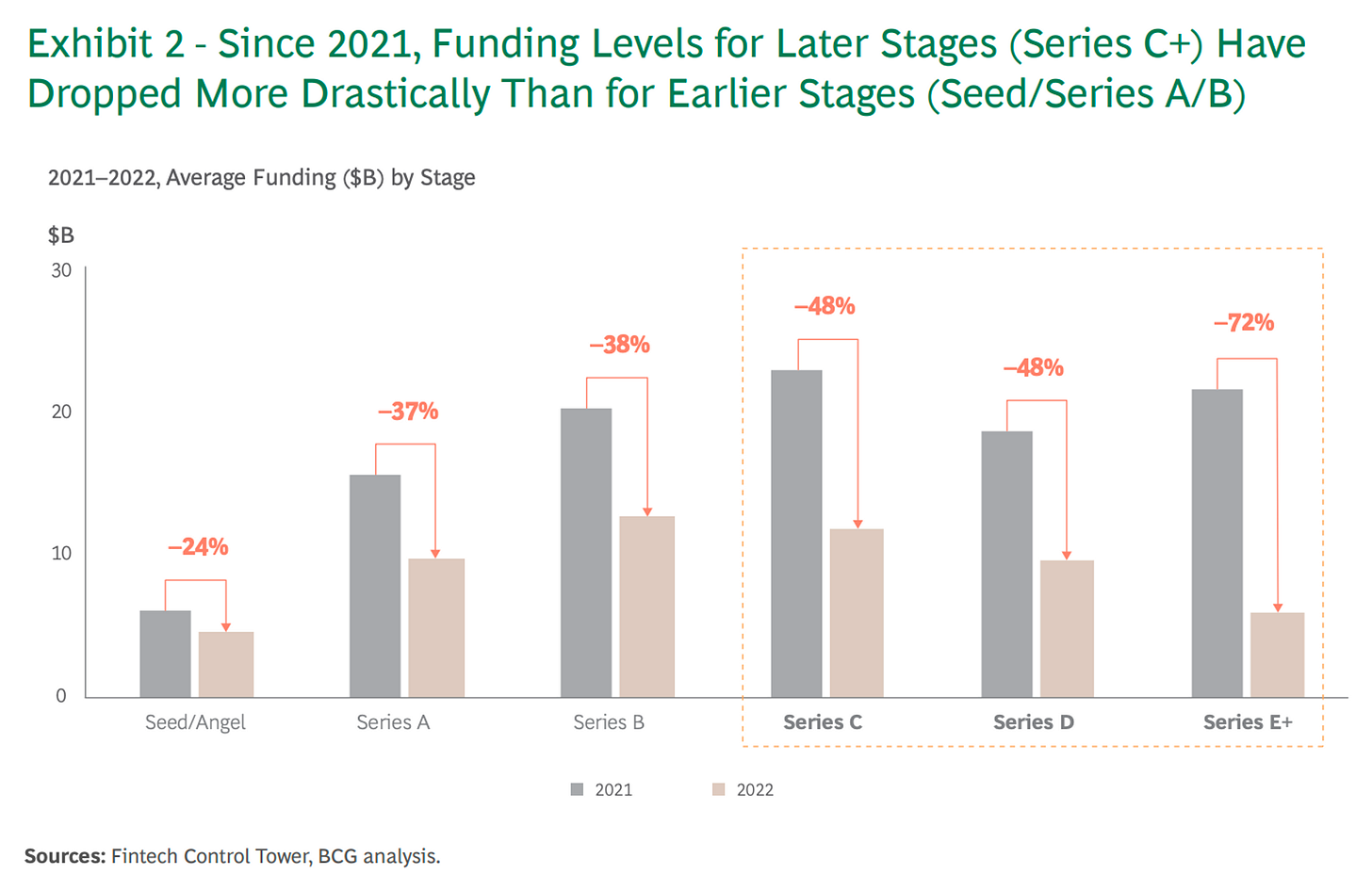

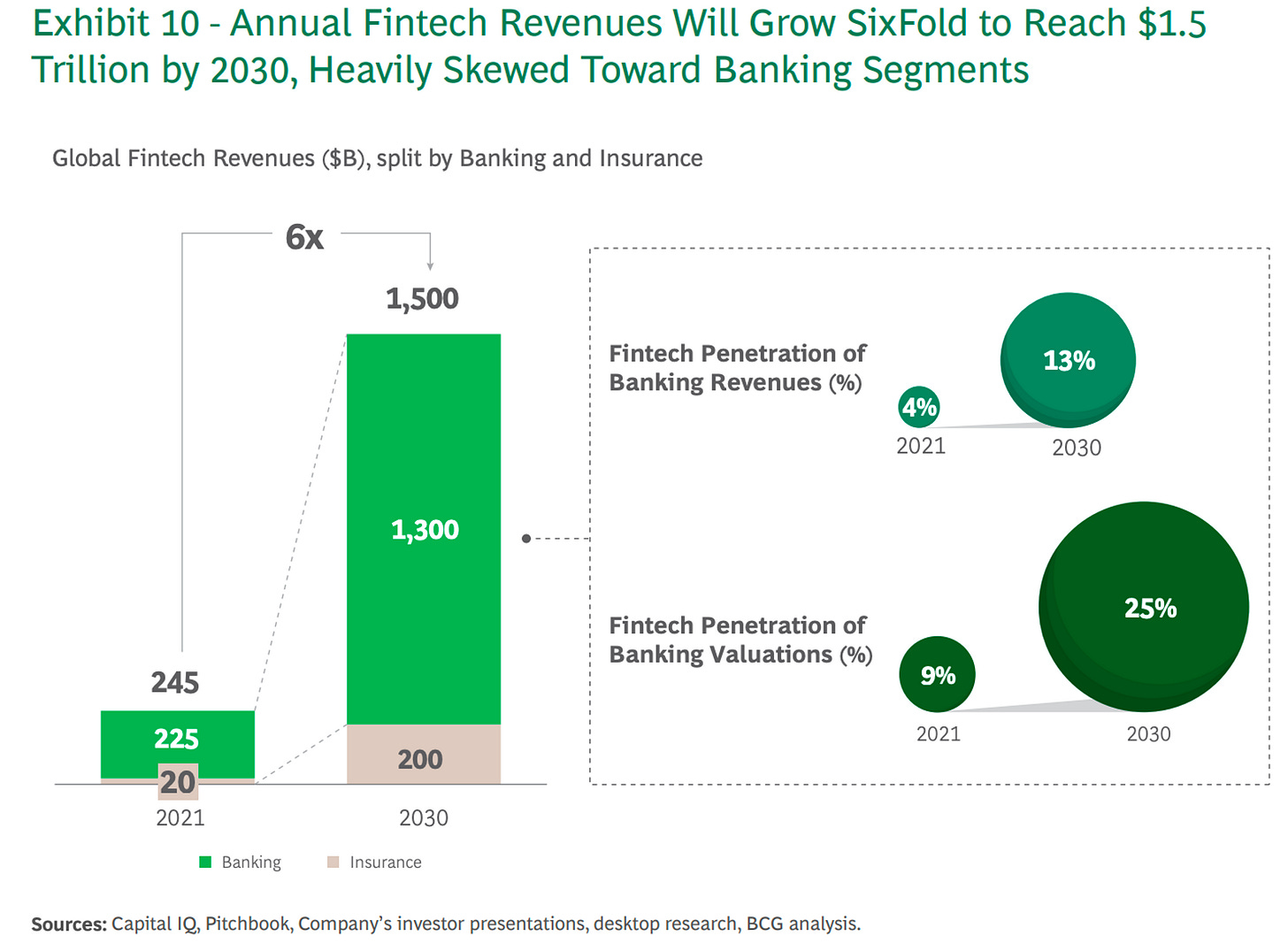

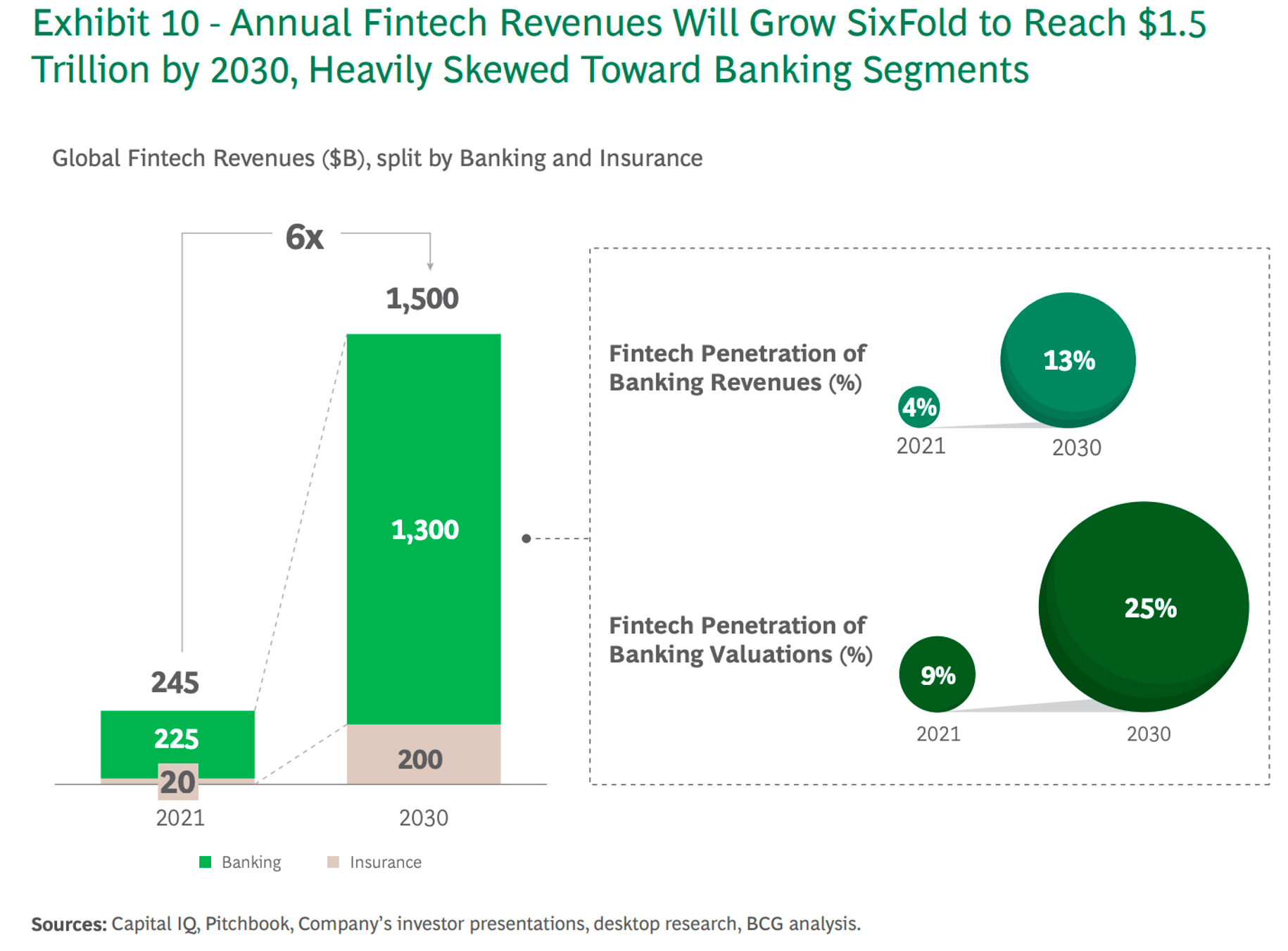

Friday, May 19th: BCG and QED published a report on fintech. - BCG

There are 32k fintechs globally which raised over $500bn in the past decade representing around 20% of the total amount raised in venture capital. In the last 12 months, fintechs’ valuations decreased by an average of 60%. Fintechs had to shift from revenue growth at all cost to improving unit economics and moving towards profitability.

“The financial services industry is one of the largest and most profitable segments of the global economy, representing $12.5tn in annual revenue pools and creating an estimated $2.3tn in annual net profits or additional value—based on one of the highest average profit margins across all industries of 18%.” By 2030, the industry is expected to reach $21.9tn in annual revenues growing at 6% CAGR.

Fintechs account only for 2% of the financial services sector annual revenues ($245bn). By 2030, fintechs’ revenues are expected to grow 6x to reach $1.5tn.

B2B payments will be a major growth driver in the fintech industry with specific subcategories such as cross border payments ($20tn annual volume in cross-border transactions & $120bn in transaction costs), real time payments (bank to bank transfers), payment plus (offering software solution on top of payment like billing, invoicing, tax automation, revenue recognition, treasury, card issuing or business financing).

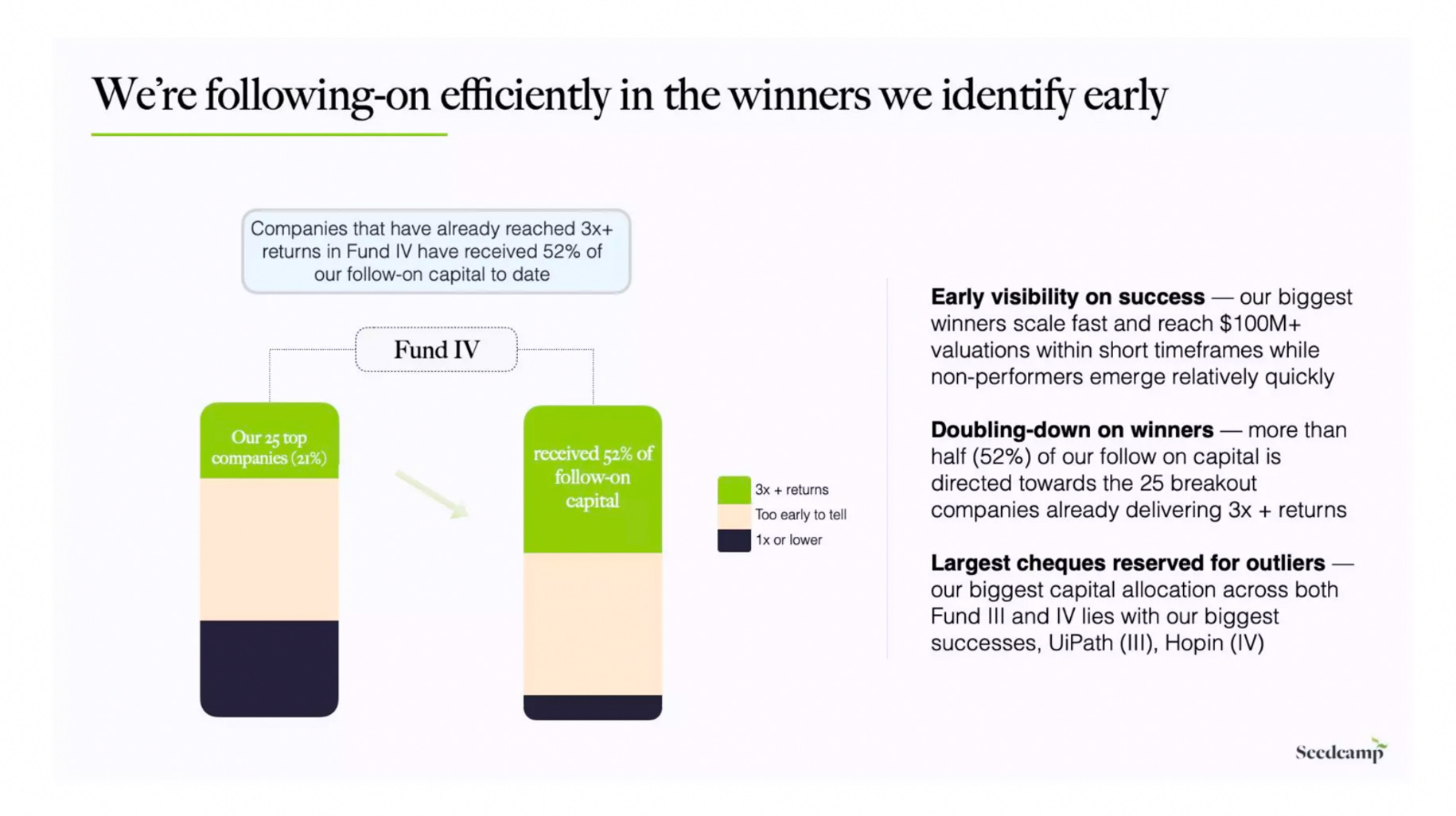

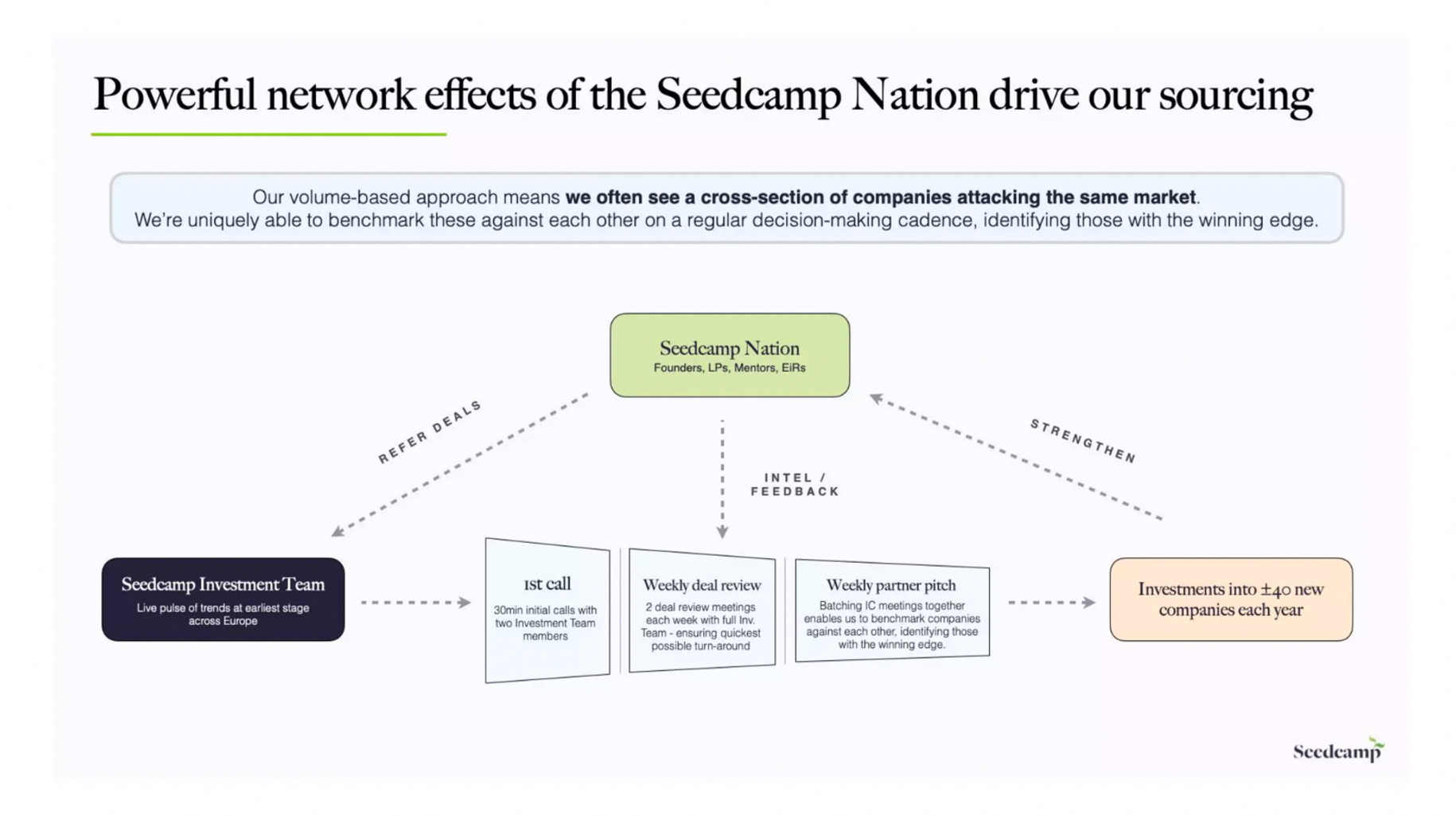

Saturday, May 20th: Seedcamp raised $180m for its sixth fund. Seedcamp invested into 460 companies and minted 9 unicorns. Its new fund is twice bigger than the previous fund. It will write tickets up to $1m from angel to seed rounds into 100+ companies. - Seedcamp

Sunday, May 21st: Zip raised a $100m series C at a $1.5bn post-money valuation in a round led by internal investors YC, Tiger and CRV. It was previously valued at $1.2bn after a $43m series B led by YC Continuity in December 2022. Zip is operating within the procurement space and started with an intake solution to streamline the approval process for new employee expenditures. With this latest funding round, Zip announced its expansion from Intake-to-Procure to Intake-to-Pay building a full Procure-to Pay platform atop its Intake-to-Procure solution and thus directly competing with incumbent solutions. - Techcrunch, Forbes

Monday, May 22nd: Pigment raised a $70m round led by Iconiq at a $850m post money valuation valuing the business at a 85x EV/ARR multiple. Pigment is a modern FP&A platform directly competing with incumbent Anaplan. It targets mid-market and enterprise customers. Zip and Pigment’s funding rounds illustrate the current trend is growth stage investing. There is not a lot of growth capital deployed into startups but when it does occur, it tends to be invested into assets perceived as recession proof and suited to the new paradigm. Zip and Pigment share key characteristics such as being focused on the mid-market/enterprise segment, combining SaaS & financial services as revenue streams, disrupting PE backed incumbents (with Thoma Bravo behind both Anaplan and Coupa) and offering software aimed at reducing expenses (FP&A and procurement). - Sifted

Tuesday, May 23rd: QED raised a $650m early stage fund and a $275m growth stage fund to back fintech companies across the globe. QED invested in companies like Credit Karma (led the series A), Klarna, Nubank (led the series A), Remitly (led the series A) or AvidXchange (led the series B). QED was established in 2007 by Nigel Morris and Frank Rotman who also cofounded Capital One Financial Services in 1994. QED invested into 28 unicorns out of 200 investments. QED’s growth fund is largely dedicated to provide follow-on financing to its early stage companies at series B and series C. However, it also has the flexibility to invest opportunistically in companies that it may have missed with its early stage fund. In early stage, QED will make 35-45 investment with a $15m average investment. - Bloomberg, Techcrunch 1, Techcrunch 2, QED

Wednesday, May 24th: Instacart generated $740m in ad revenues in 2022 growing at a 30% YoY and representing almost 30% of its total revenues. The integration of advertising has become a common strategy for many marketplaces aiming to boost sales and margins, but Instacart has elevated this strategy to a new level when compared to, for instance, Amazon, which only generates 10% of its revenues from ads. - The Information

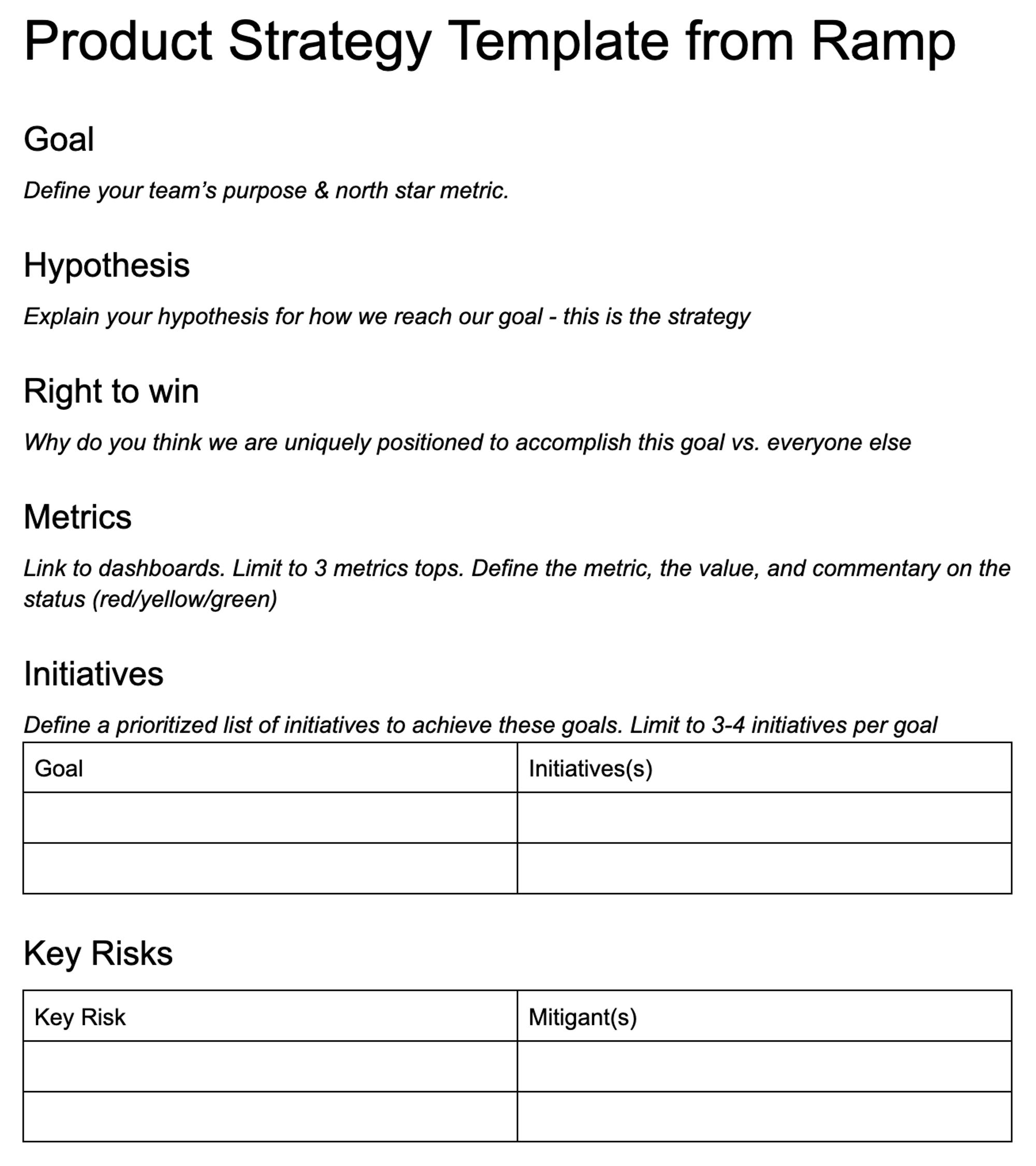

Thursday, May 25th: Lenny Rachitsky discussed with Geoff Smart who is Ramp’s VP of Product how the company builds product. It’s a noteworthy conversation because Ramp is known for being one of the startups with the highest product velocity. - Lenny Rachitsky

“Our entire planning process is optimised toward product velocity. In essence, we believe that doing is better than planning. Any second you spend planning is a second you don’t spend doing.”

“Teams are organised based on customer or business outcomes above all else. The team needs to be accountable for something big. That lights a fire behind a team and makes them want to run through walls. Years ago, we gave a team the mandate to drive 50% of our sales qualified leads by automating outbound emails. And they did. We gave a team three months to build a competitor to Bill.com. And they did. Big goals, tight timelines, and fully autonomous resourcing (remove as many dependencies as possible) were the common ingredients.”

“Keep teams small so they move fast. We don’t like having more than 5 to 10 engineers on a given team. For example, we spun up a new team to build our Bill Pay product. That pod became four subpods as we grew, and we spun out one of those subpods fully to own workflows across Ramp.”

“Sell your first customer. Oftentimes, PMs throw products over to sales to sell without actually having gone through the motions of positioning, pitching, listening, and iterating. I task my PMs to find, pitch, and close the first 5 to 10 customers for their products. This forces them to work with customers from the start and iterate until they get it right. If you can’t find 10 customers, you haven’t built something people want, and we are not going to waste the time of the go-to-market teams. We also believe PMs need to learn to sell, period, whether it’s the company vision, the product, or new candidates.”

“Take the bets with asymmetric upside. If an outcome has a 98% chance of failure and a 2% chance of massive benefits for the business, take the bet.”

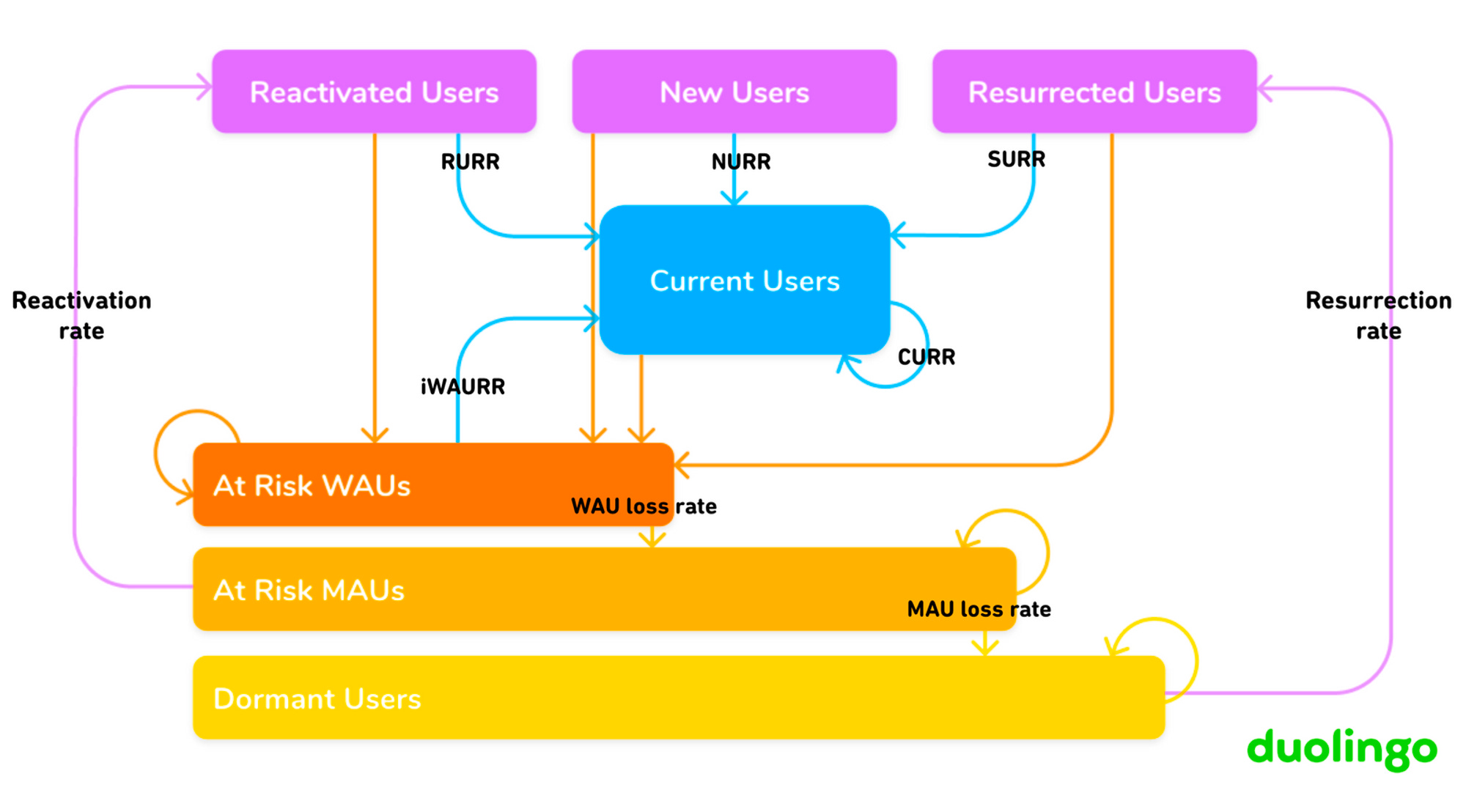

Friday, May 26th: Duolingo wrote about how it optimised its growth of DAUs by optimising certain sub-metrics impacting DAUs like the retention of daily learners. - Duolingo

c.80% of Duolingo’s users were acquired organically. 7% of Duolingo’s MAUs become paying users.

Duolingo’s core growth strategy is to build the best learning app and to offer it for free knowing that it will generate a strong word of mouth and that a significant percentage of the user-base will become paying users.

Duolingo classify its users into different buckets and tracks with sub-metrics how users are moving from one bucket to the other. All sub-metrics don’t have the same impact on Duolingo’s DAU growth. Duolingo discovered that increasing the retention rate of current users had the most impact on DAUs.

Saturday, May 27th: Harry Stebbings interviewed Nico Wittenborn from Adjacent on 20VC. - 20VC

Nico began his venture career at P9 for 4y (seed in SaaS) before joining Insight for 3y in New-York (series A in SaaS and consumer). He invested into companies like Revolut, Chainalysis, Oura, RevenueCat and PhotoRoom. He started his own VC firm in Nov. 2019 called Adjacent to invest mostly in consumer subscription companies.

Both SaaS and consumer subscription products tend to have high-margin, recurring and global reach from day 1. Consumer subscription apps usually exhibit higher customer churn than SaaS, but after the 1st year, the retention is as good as SaaS targeting to SMBs. Moreover, top consumer subscription apps have a model in which CAC is instantly recouped (because high share of annual subscriptions) so if you have a market that is large enough, you don’t care to lose 50% of your subscribers after one year.

Most consumer subscription products start with mobile apps but it’s not the only product surface that they can exploit. For instance, Photoroom is a mobile app, a web product and an API.

Adjacent has a fund strategy that does not rely on $10bn+ exits. Instead, $2bn+ exits should be able to return the Adjacent fund multiple times. Adjacent makes 75% of its investments at seed as lead investor and the rest at series A as co-lead investor. It invests in 20-25 companies per fund with tickets ranging from $1-7m aiming for average ownership of around 10% (which allows Adjacent to co-lead rounds with other funds). For consumer subscription products, seed investment is the best stage for maximizing upside and minimizing downside. These products can be extremely capital efficient reducing dilution for seed investors and offering more options for future funding (e.g. raising a growth round or staying profitable).

“At seed, you don't need a board. I think because you're chasing product market fit, most of the time I'm in your way [as an investor asking for a board]. The best thing I can do is share learnings from the other companies, be a strategic thought partner and then make introductions to other founders that have faced similar issues or solve things that you are facing right now. And there's some financing related things and stuff like that. But that's really how I see my role.”

To get into Revolut, P9 had to break down all its own rules. It was outside the scope (mobile consumer app) and the company did not need money (having just raised a round from Balderton). P9 had to persuade

Revolut to accept investment at a higher valuation than the round with Balderton resulting in a valuation and ownership stake that was far different from what P9 was accustomed to.

Sunday, May 28th: I listened to a Colossus’ podcast episode with ZoomInfo’s founder and CEO, Henry Schuck. - Colossus

ZoomInfo has a database of 130 million contacts. It helps sales and marketing teams to find and contact new potential customers. It aggregates information on companies and decision makers in companies. It collects signals to know when is the right moment to contact a company or a decision maker (e.g. new funding round, new hiring, etc.). The platform also allows users to establish workflows to engage with potential customers identified by ZoomInfo across multiple digital channels, including email, phone calls, and display ads.

In Q1-21, ZoomInfo employs 2k FTEs, 20k customers and $600m in ARR. ZoomInfo bootstrapped for 7 years reaching $25m in ARR with 50% in EBITDA margin. It raised external capital in 2014 from TA Associates (mix of primary ans secondary). It made multiple acquisitions before becoming public in Jun. 2020.

In early stage companies, the best salespeople are the one with high cognitive ability because as they need to figure out many things to successfully sell your product. However, it ceases to be the case beyond a certain stage, once tooling and processes are in place. Apart from this distinction, top salespeople possess a deep understanding of your products and your customers' needs. They also demonstrate tenacity in preparing calls, following up, and taking necessary actions to advance a deal through the pipeline.

Monday, May 29th: Tilman Langer at P9 wrote on distressed funding rounds. These encompass not only down-rounds but also rounds that offer additional legal protections to investors (e.g. liquidation preference going beyond 1x non participating, upgrading lower-ranking shares existing investors have when they participate to a new round, exit-driven price adjustments, adjusting the valuation based on the performance of the company). Excessive legal protection for investors is dangerous because (i) it increases mis-alignement between founders and investors and (ii) it complicates future funding rounds (it creates a precedent for next round, it can deter a new investor to join). - P9

Tuesday, May 30th: Accel published a report on unicorns’ startup mafias in Israël and in Europe. - Accel

59% of companies founded by a member of a unicorn’ startup mafia have secured VC funding. 54% of them stay in the same city as the unicorn they were working for.

The media amount spent by employees at a unicorn before building their own startup is 28 months.

Wednesday, May 31st: Boldstart published a board deck template and board deck best practices for SaaS companies selling to enterprise customers. - Boldstart 1, Boldstart 2

A board deck should cover the following sections: user story (why the company exists), CEO’s highlights & lowlights, cash, product updates (product roadmap and delivery against the roadmap), sales update with a pipeline review, marketing update (ICP definition, lead generation machine), team update, asks to your board members and metrics.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Great read - thanks for collecting these. Would be interesting to get 1-2 sentences adding your thoughts on each of them though. Enjoy reading your other posts so that would be v.interesting