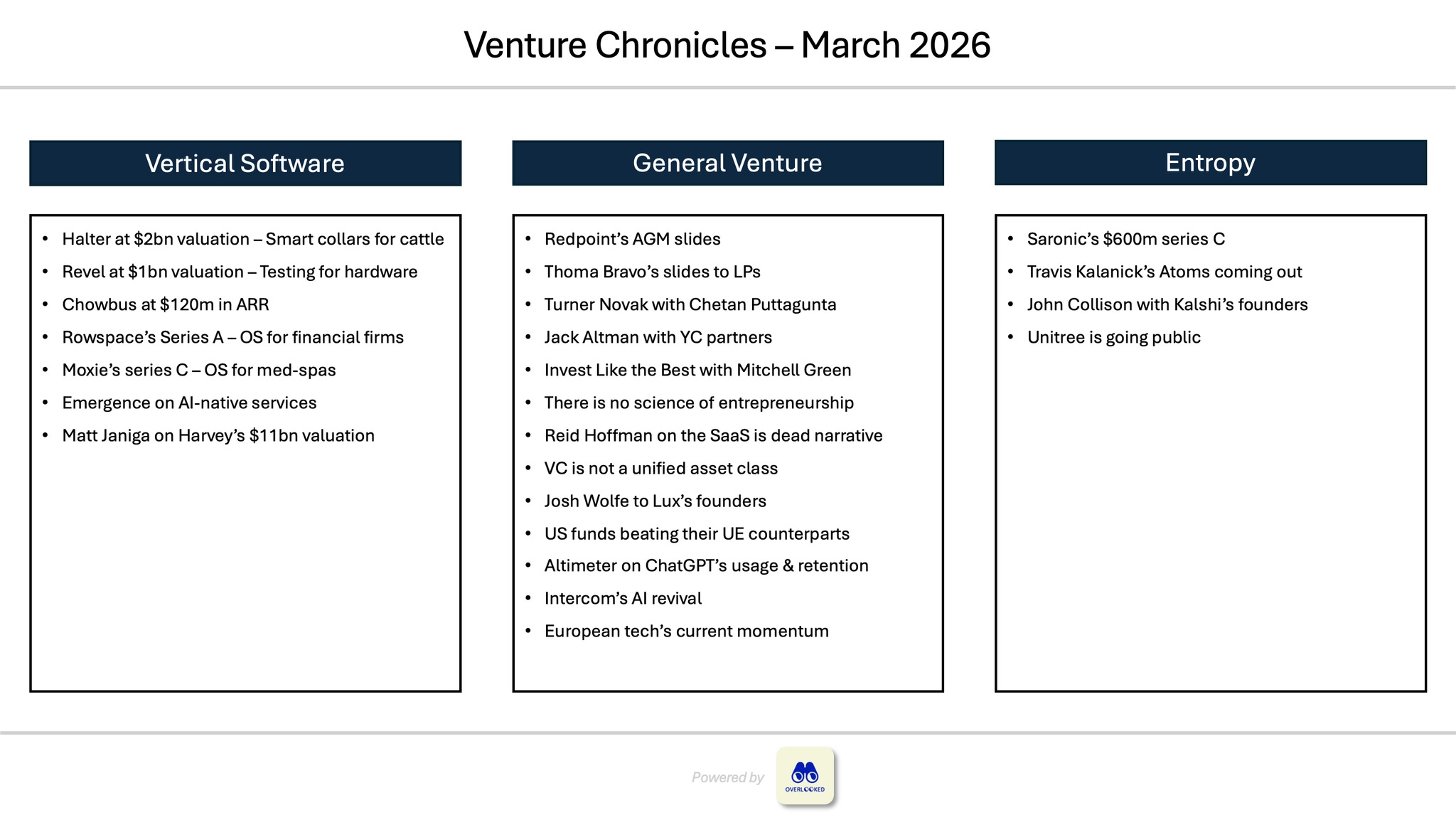

📖 Venture Chronicles - March 2026

Overlooked #215

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of March.

I curated updates and insights around three themes:

Vertical Software

General Venture Capital

Entropy - other news and personal topics of interest

Vertical Software

Halter raised a $220m series E round at a $2bn valuation led by Founders Fund. It’s an AI-powered smart collars for cattle used as virtual fencing as well as health and location monitoring. It previously raised a $100m round in Jun. 2025 led by Bond. - Bloomberg, Halter

“Halter serves more than 2000 ranchers and farmers across New Zealand, Australia, and the U.S., with a million of its solar-powered collars now sold.”

“Halter’s technology is designed to create a virtual fence for cattle and enable farmers to monitor the animals’ locations and health indicators through an app. Its collars, which are solar-powered, connect to farmers’ phones to allow them to manage pastures remotely — for example, a rancher can herd their cows using vibrations and audio cues from the collars.”

“The startup’s approach is part of a broader “precision agriculture” push, where farmers use technology to better manage their fields and reduce human labor needs. Many collars for cattle on the market focus on monitoring digestion, searching for any irregularities that could signal sickness or other issues, and on tracking breeding cycles.”

“Halter will deploy the new capital to grow its commercial and field operations across the U.S., New Zealand, and Australia, while expanding into other international markets, starting with Ireland and the U.K. later this year.”

Revel raised a $150m series B led by Index at a $1bn+ valuation. It builds software to test and control complex real-world hardware (e.g. rocket engines and nuclear reactors). It has already landed customers including Impulse Space, Radiant Nuclear, and Astro Mechanica. - NYT, Revel

“Revel’s software helps companies develop and command complex hardware systems, drawing on the experience of its founder, Scott Morton, who led software engineering for SpaceX’s enormous Starship rocket. He and his team developed programs to manage tests of the rocket after being dissatisfied with the status quo: decades-old software like LabVIEW, a 40-year-old program.”

“Its initial focus is helping customers test hardware, working with companies like Impulse Space, a spacecraft start-up, prototype more quickly.”

“The company is expected to move beyond running tests, Mr. Morton added, into controlling and observing complex hardware processes, potentially accelerating American manufacturers’ business operations.”

“Revel was initially used for rocket test stands, one of the most demanding environments in the world. Today, we’re expanding beyond testing into industrial control across the critical sectors and systems that keep society running — nuclear facilities, oil and gas refineries, water treatment plants, power stations, defense systems, data centers, and biomedical manufacturing.”

Chowbus raised a $81m series E led by Prysm and Left Lane. It’s an operating system for Asian restaurants in North America including POS, marketing, accounting, supply ordering and insurance. - PR Newswire, HPA

It generates $120m in ARR (9x growth over the past four years) and $4bn in annualised TPV.

Chowbus was founded in 2016 in Chicago, originally as a food delivery platform for Asian restaurants, before evolving into restaurant SaaS including a cloud-based POS.

“Chowbus plans to use the funds to expand its suite of AI-driven tools for marketing, automated accounting, and supply chain optimization; deepen service integration by moving beyond traditional SaaS to offer comprehensive business services that reduce overhead for restaurant operators, and pursue international expansion into Canada while strengthening support for the tens of thousands of independent restaurants currently using its POS and analytics platform.”

Rowspace raised $50m in a combined seed and series A rounds led by Sequoia and Emergence. It’s an AI platform allowing financial firms (PE funds, hedge funds) to turn their years of proprietary data into alpha. It provides specialized intelligence for investors to make faster, sharper decisions. - Fortune

“Manapat described Rowspace as the intelligence layer that sits on top of a firm’s data. The platform integrates all of an institution’s structured and unstructured data, whether in the form of documents or accounting systems or old PowerPoints, and performs reasoning in advance.”

“Rowspace’s focus is more on compiling and synthesizing a firm’s data in a secure way, and doing so with a financially literate team.”

“Rowspace is working with about 10 top firms with seven-figure annual contract values.”

Moxie raised a $25m Series C led by Viewpoint Ventures. It’s an operating system for aesthetic medicine. - AmSpa, BeautyMatter

Moxie is launching Scale Suite for multi-location practices to provide them with operational infrastructure, margin intelligence, and AI-driven compliance alerts.

“Today, Moxie supports more than 700 aesthetic practices nationwide. Moxie-supported practices grow 60% faster than the industry average, achieve 10% higher margins, and save more than $5,000 per month on products and supplies. The company maintains a 97% retention rate, and more than 20% of new practices join through referrals from existing Moxie-supported owners.”

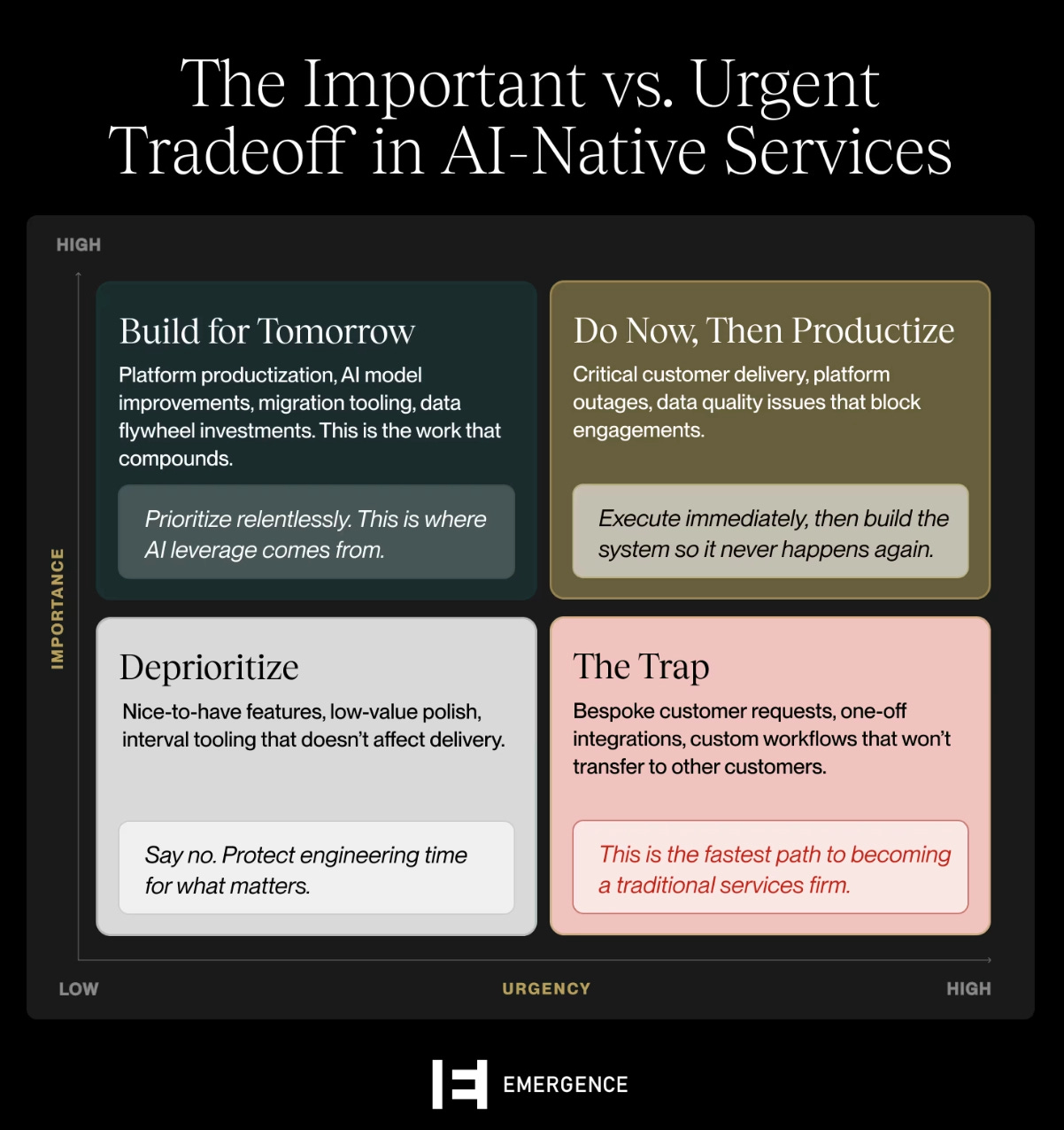

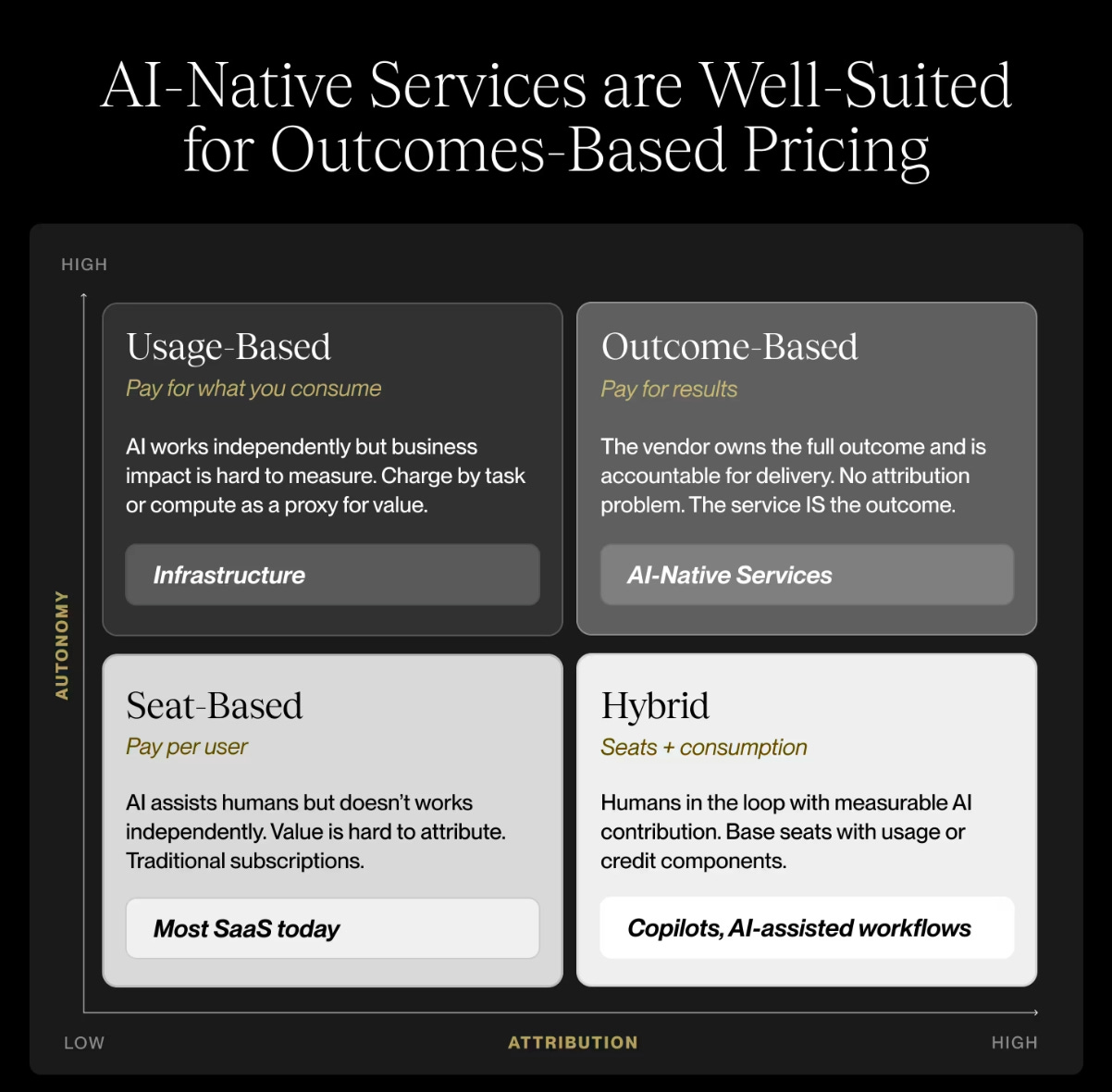

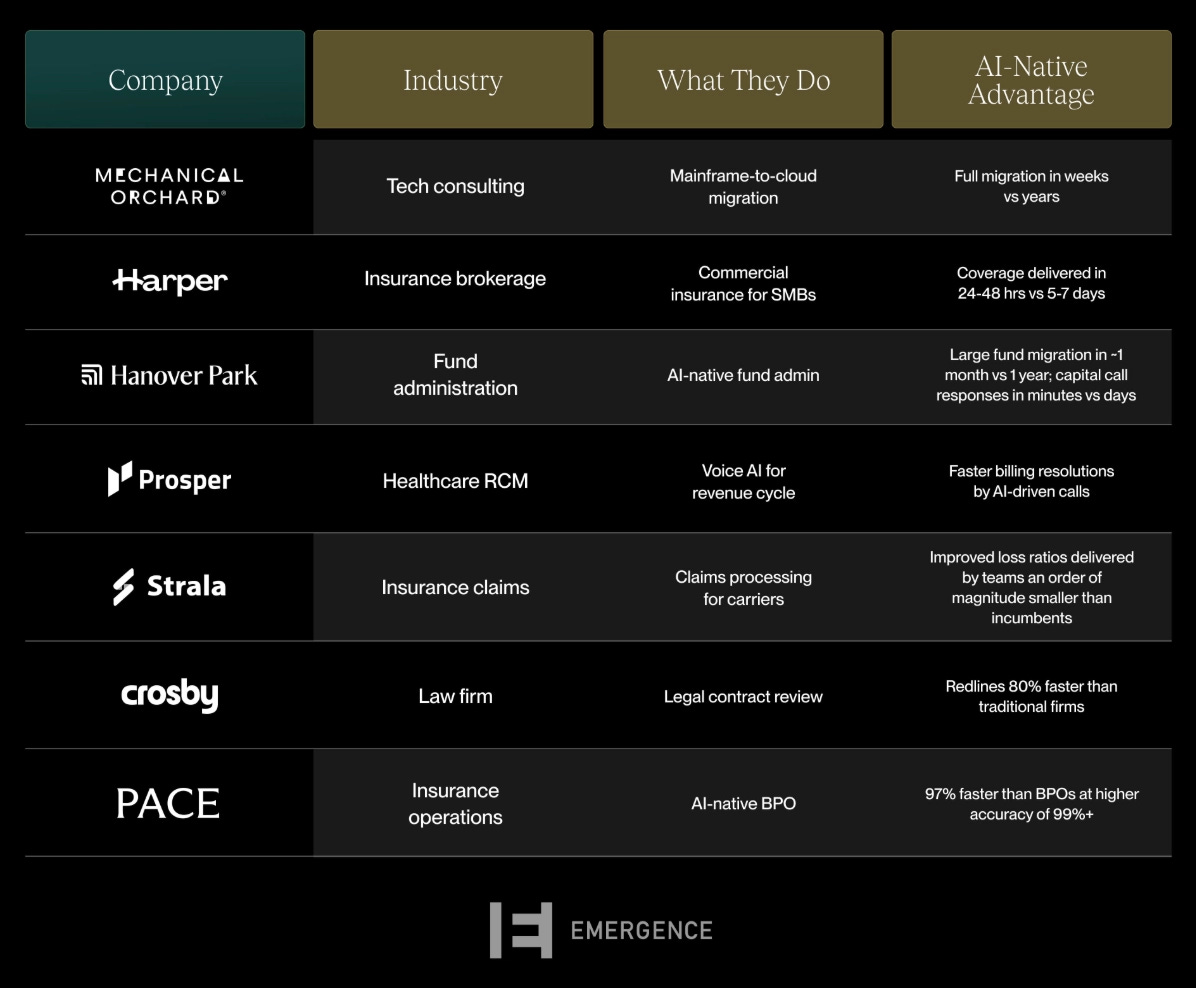

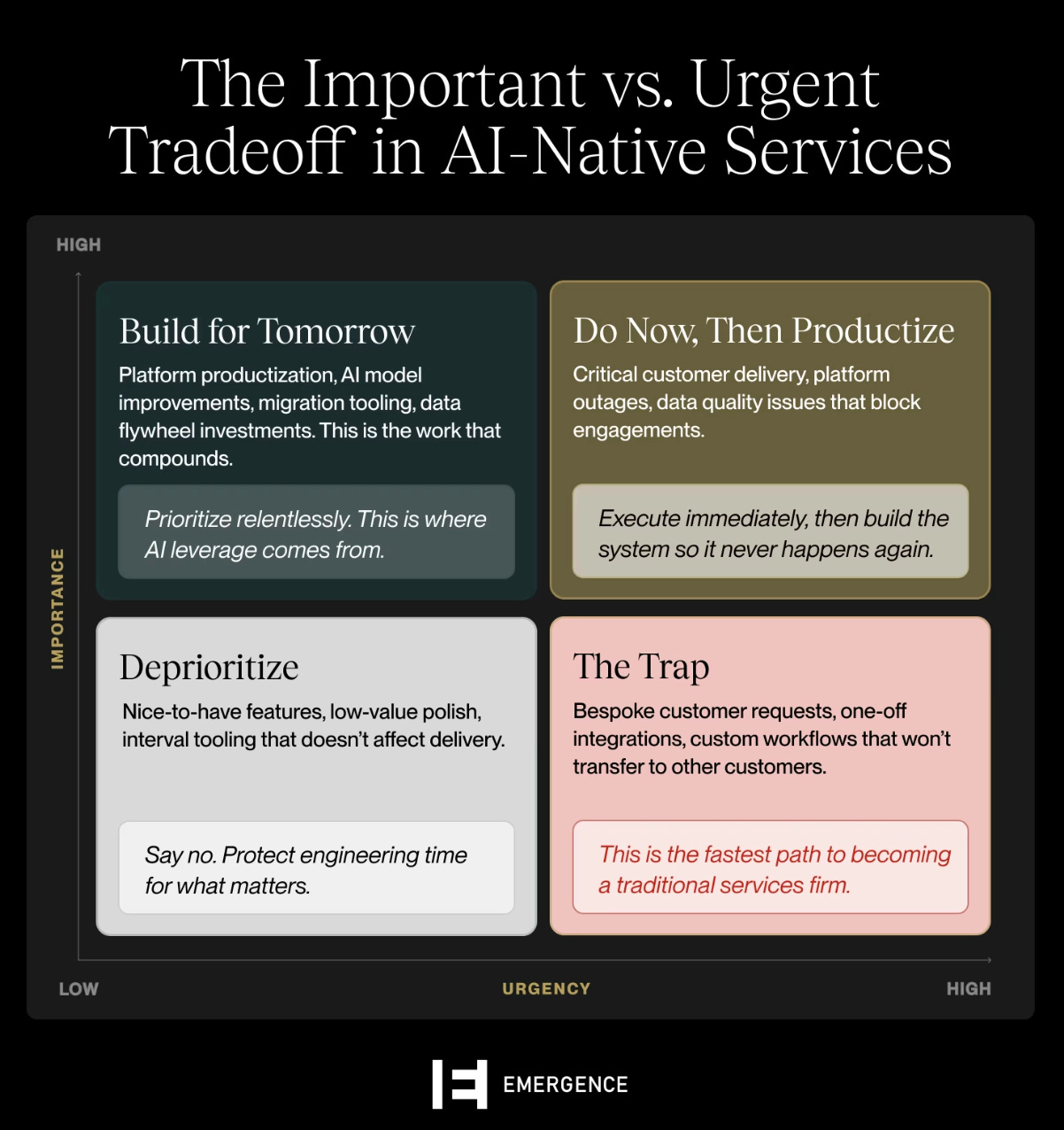

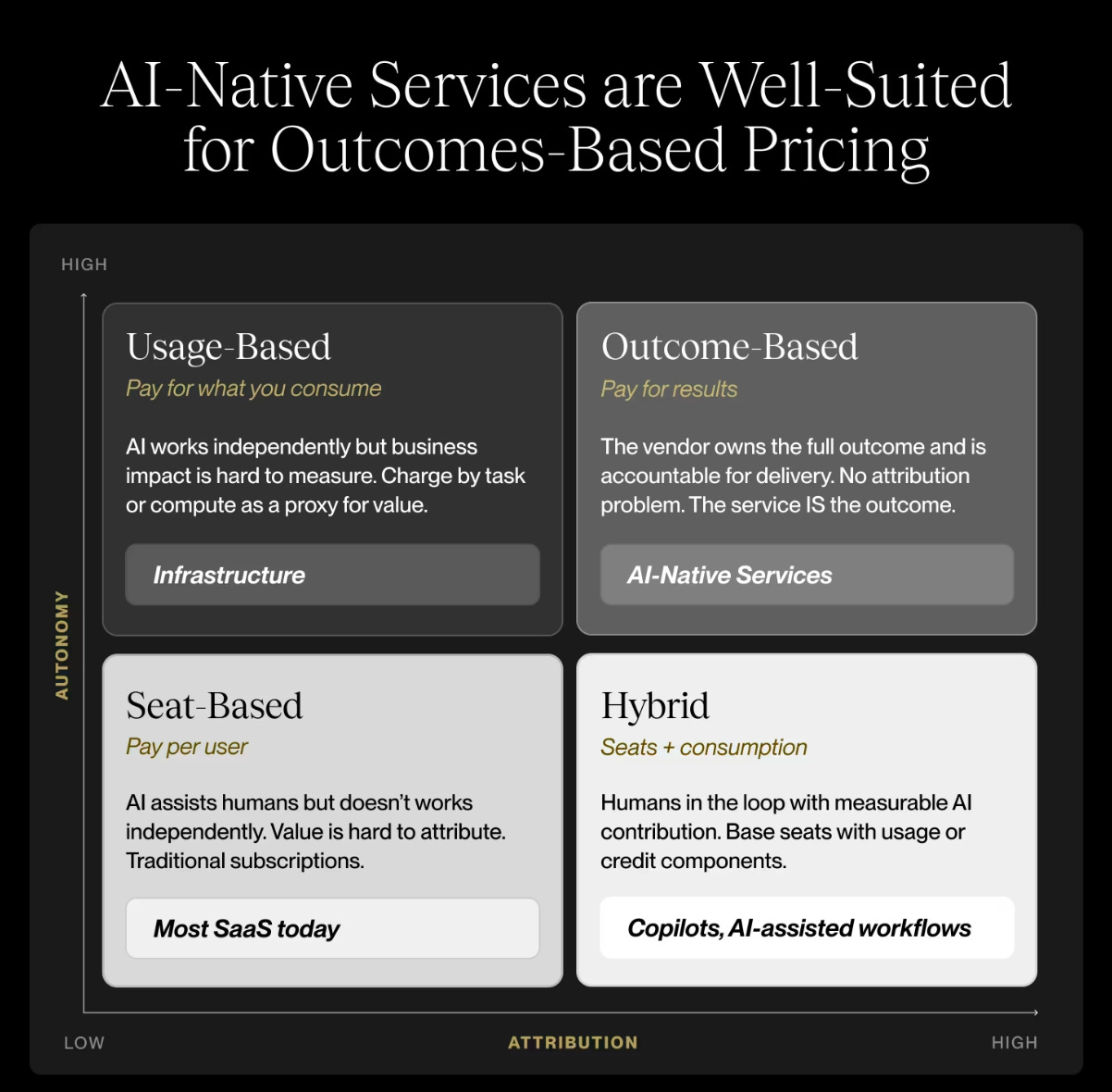

Emergence published articles on AI-native services. - Emergence 1, Emergence 2

“AI-Native Services will be a defining business model of the AI era.”

“Domain expertise is a must have. In traditional SaaS, you’re selling a product. In AI-native services, you’re selling yourself. Domain credibility isn’t just important; it’s existential.”

“PMF is a different beast in AI-native services. Strong revenue growth and net dollar retention can mask a lack of true AI enablement. Unlike SaaS, revenue growth and strong logo retention don’t prove product-market fit. You only truly have it when AI is doing a material share of the work at a high gross margin and delivering superior customer outcomes. Otherwise, you’ve built a good services firm financed with the wrong kind of capital.”

How do you know if you have Mirage PMF? (1) Flat or declining gross margin as revenue grows. (2) ARR/FTE is not improving. (3) Delivery is still human heavy. (4) Bespoke work is expanding.

“Focus on one or two jobs to be done. The more jobs you take on, the harder it becomes to productize your AI.”

“AI-native services succeed because they collapse software and services into one integrated system, delivering the full outcome the customer wants. By owning the full stack, they can guarantee the quality of the output. That structural advantage is why this model can deliver 5-10x improvements in speed or throughput while operating at 50%+ gross margins, and why the opportunity extends far beyond the categories that have gotten early attention.””

Matt Janiga at Modern Treasury commented Harvey’s latest $11bn valuation. - Matt Janiga

“Harvey feels like it competes with Lexis Nexis and Westlaw, which are the other two legal tools every major law firm has. I used Lexis’s AI tool a lot in my prior role. It was decent and seemed to improve over time. I assume Lexis will continue to improve it. It honestly competes with ChatGPT and Gemini more than Harvey.”

“The interesting thing is that Lexis and Westlaw have legacy businesses built on datasets of legal precedents and carefully curated regulatory materials like opinion letters and legislative history. They also offer other products that drive material revenue, like Lexis’s identity verification databases and value-added services. Harvey doesn’t have those things.”

“Law firms who adopt Harvey more will have to change their billing models.”

General Venture Capital

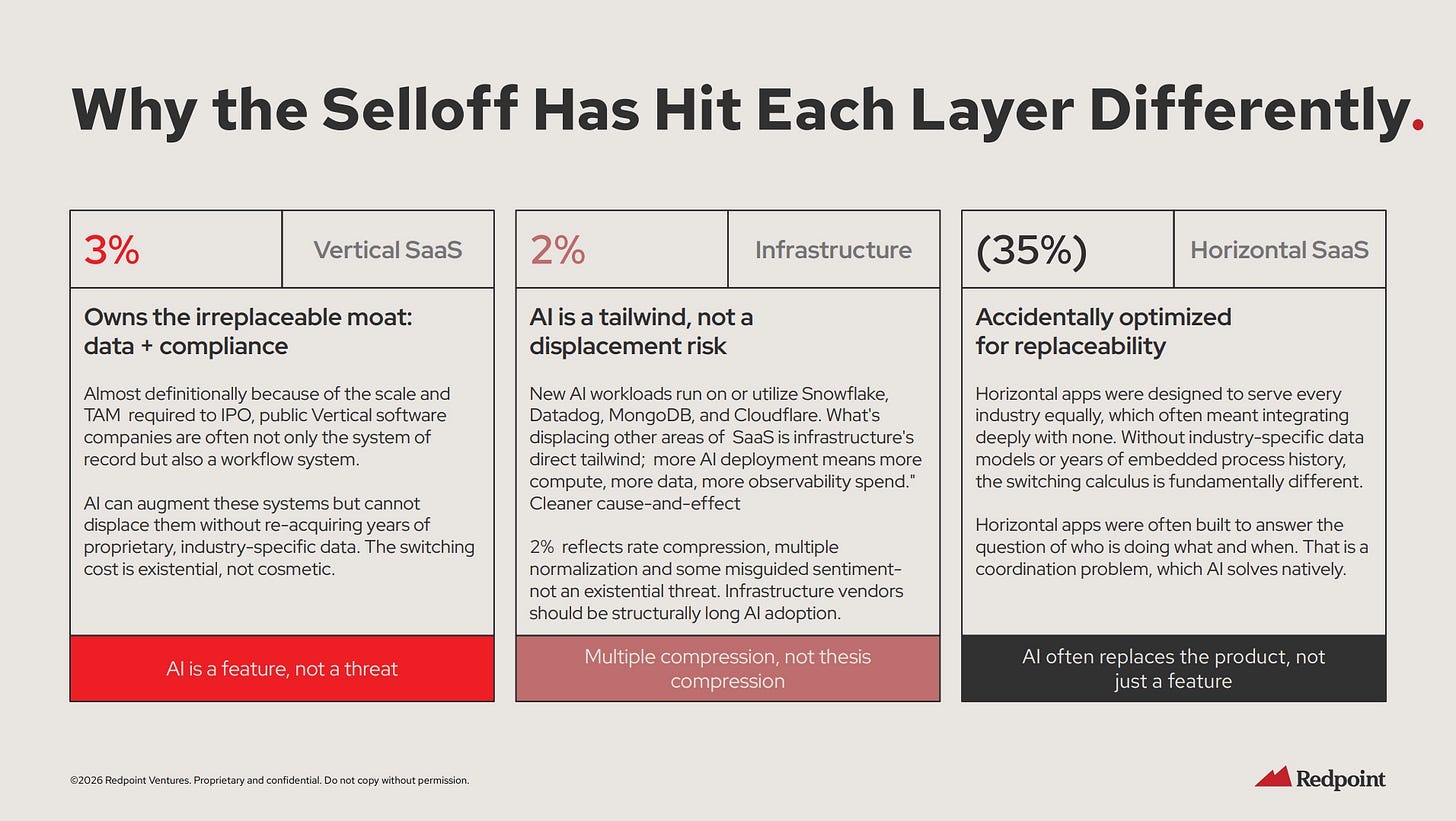

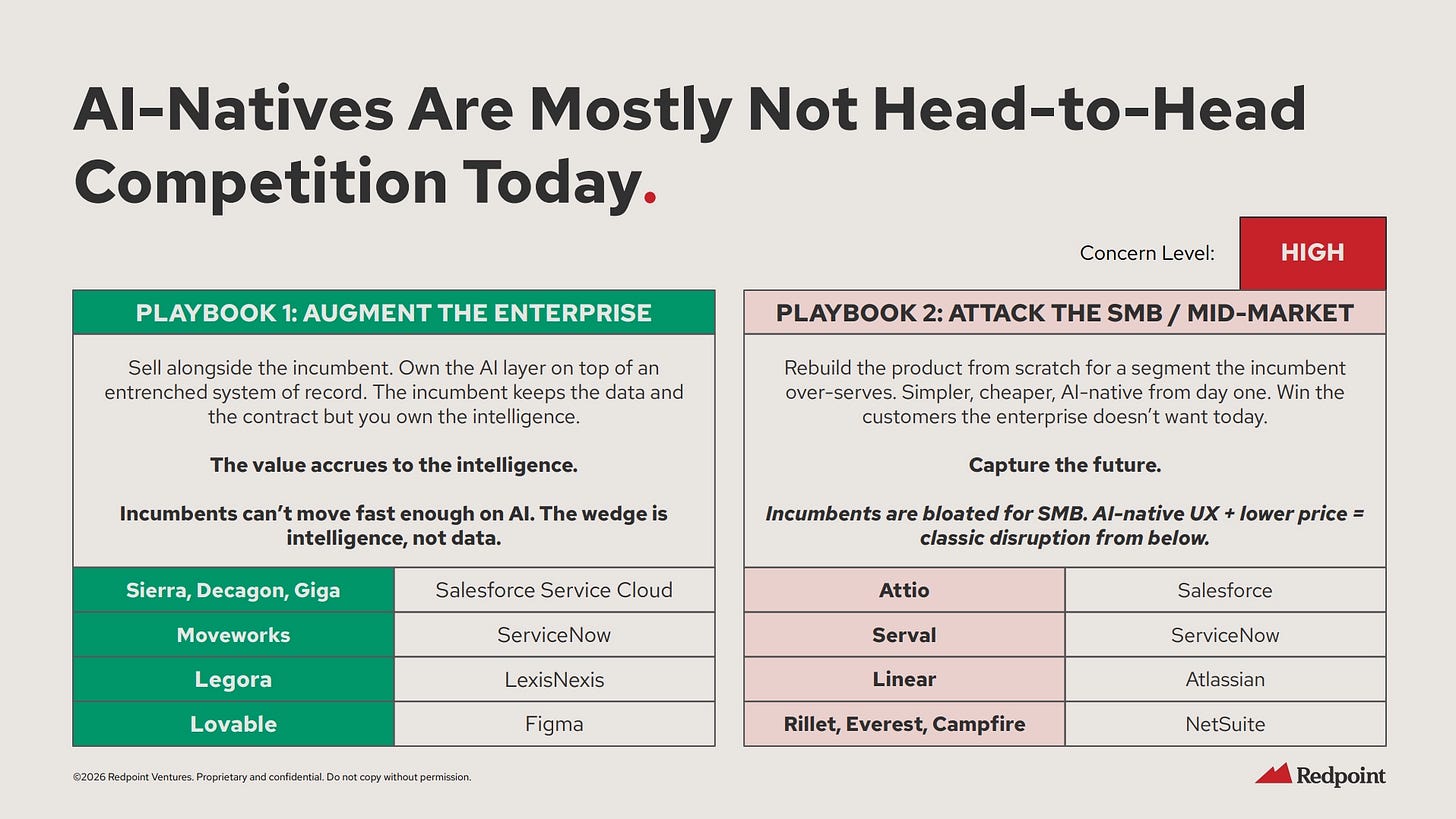

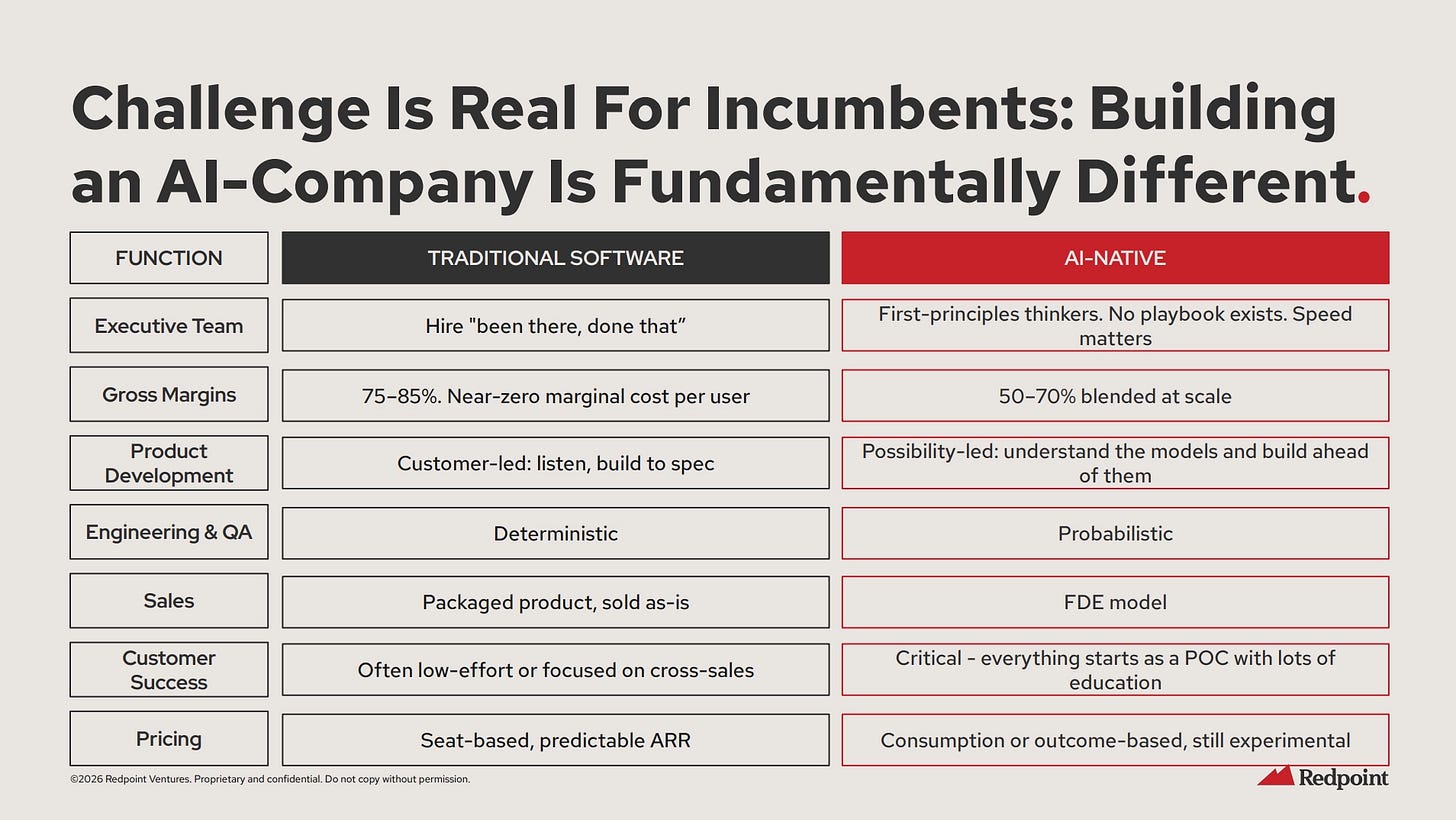

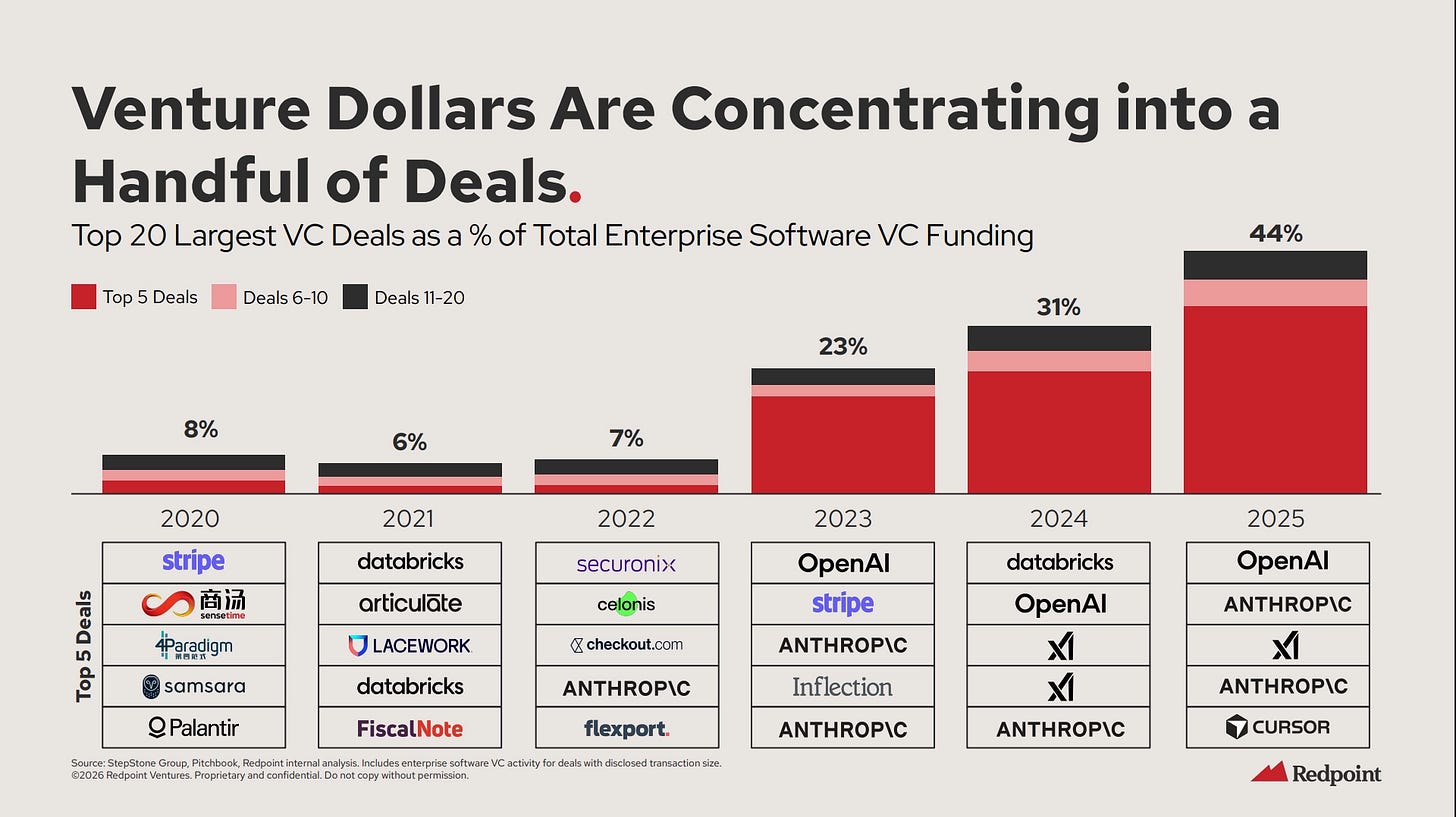

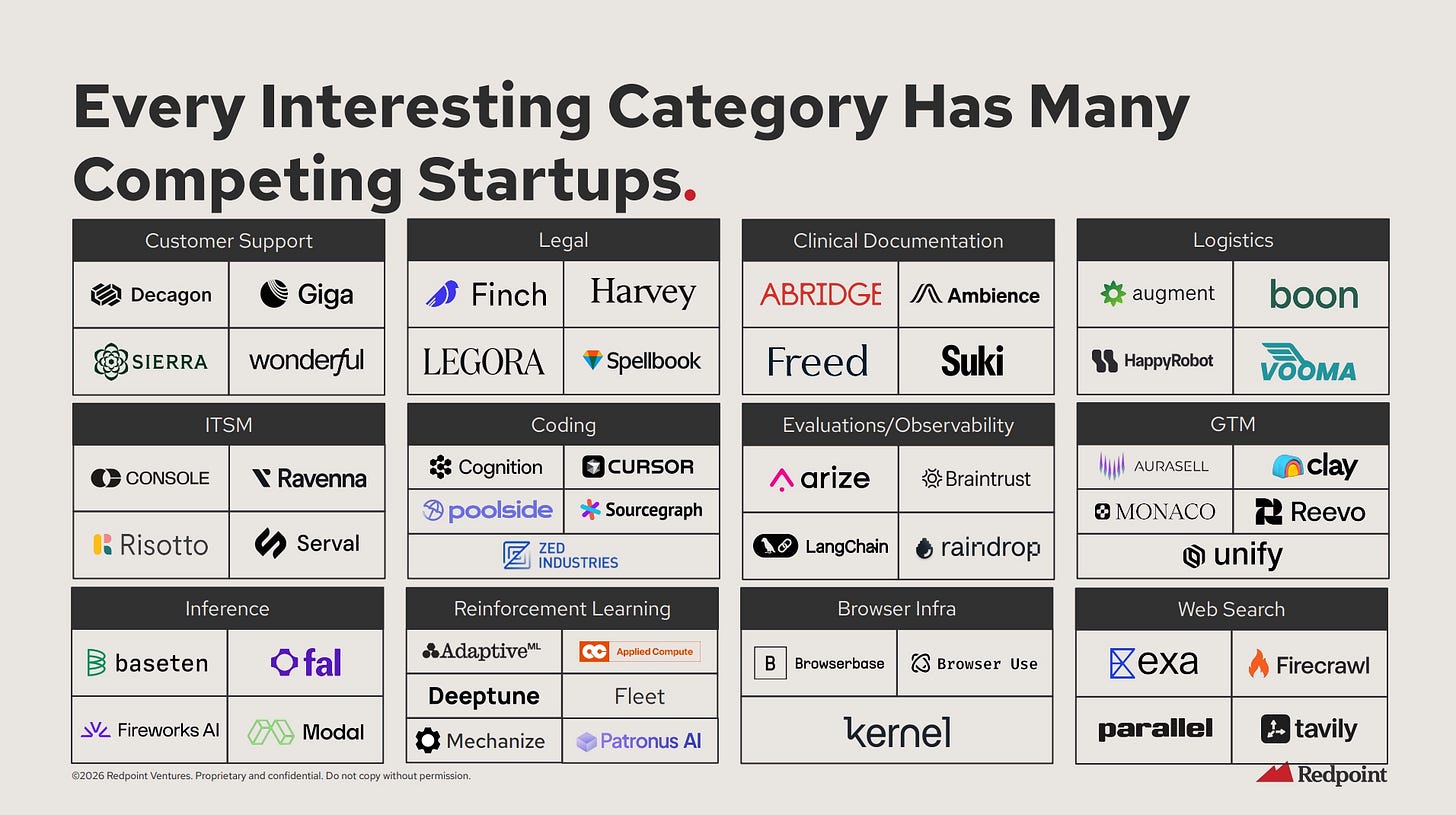

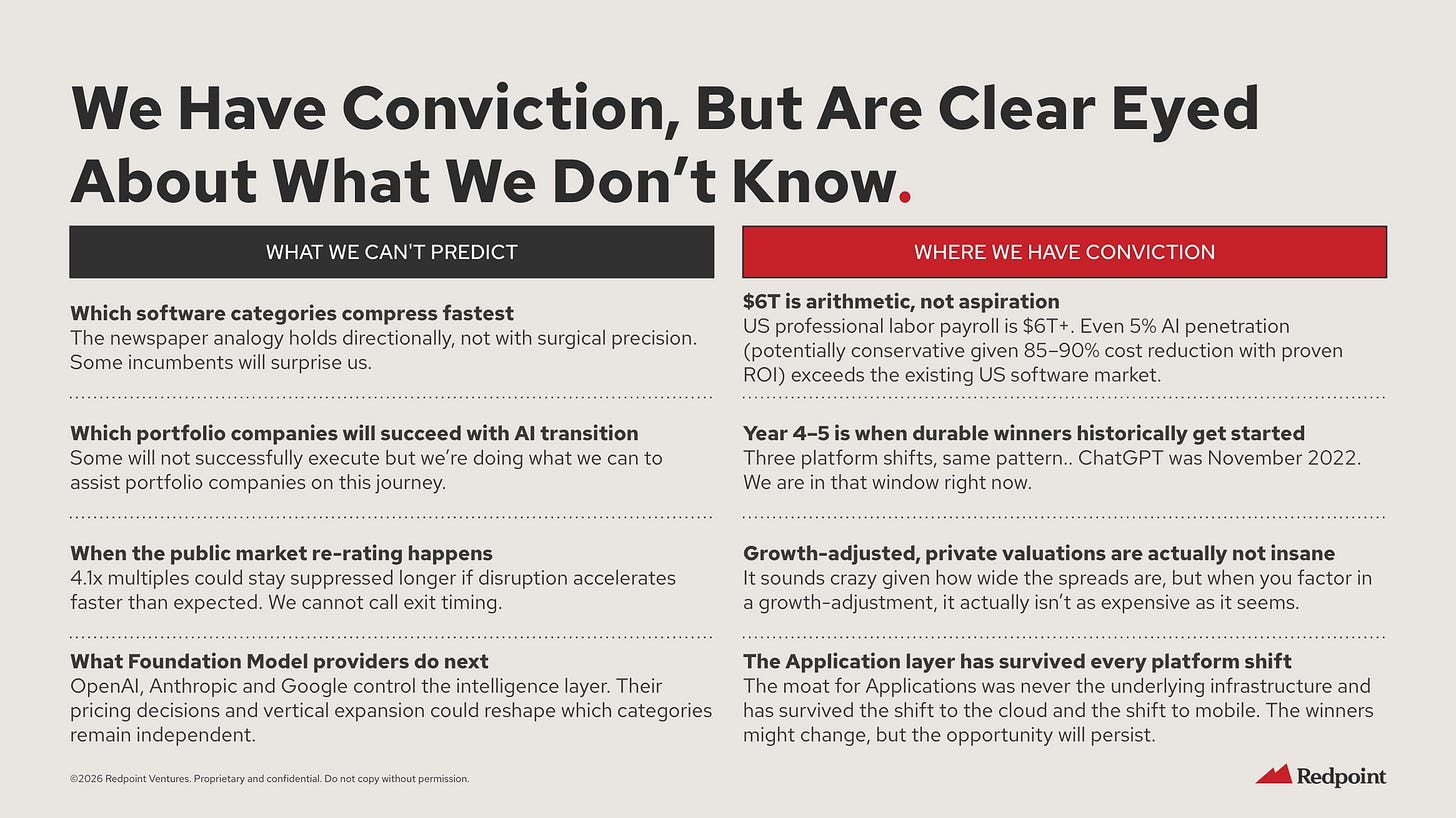

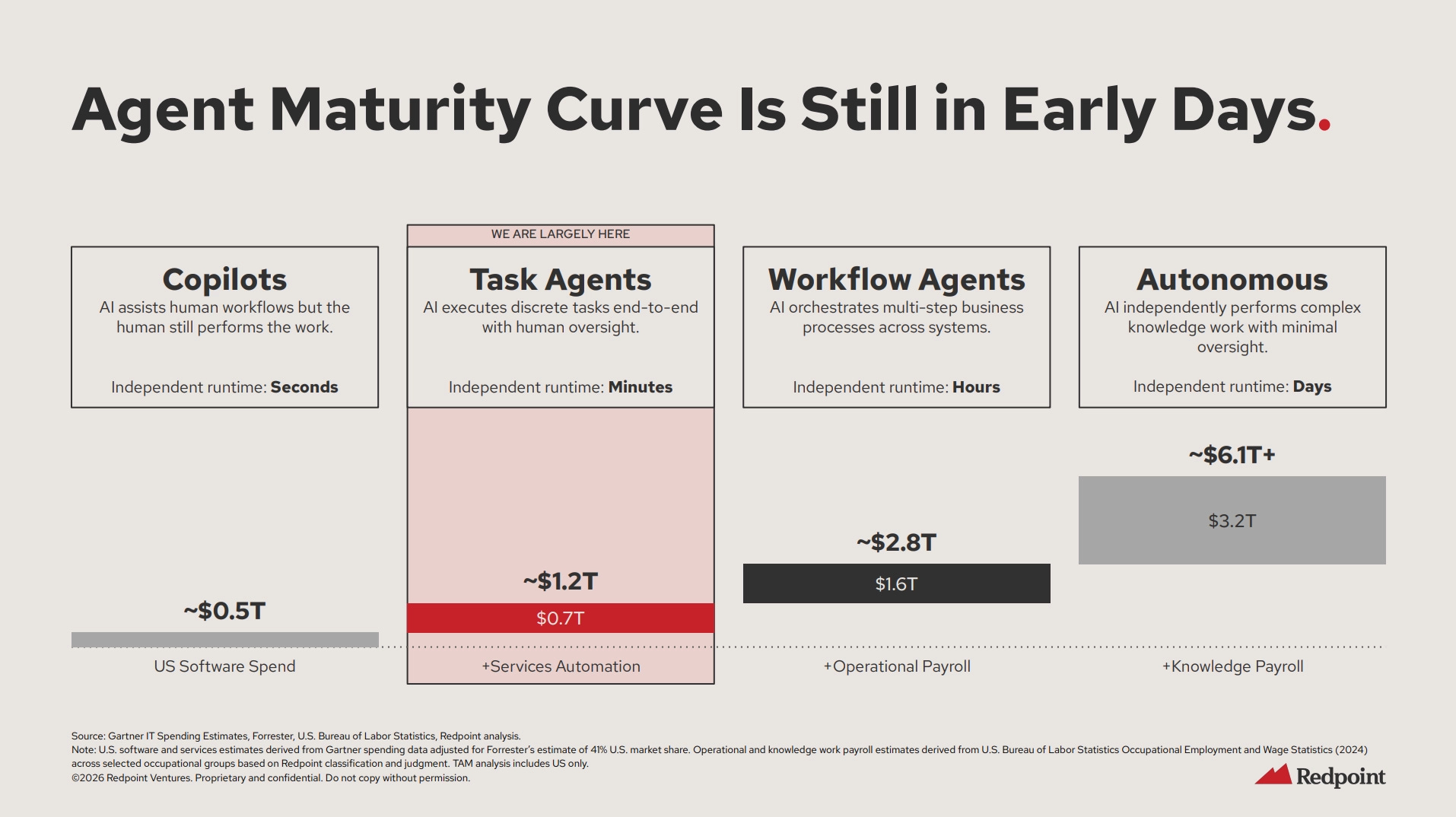

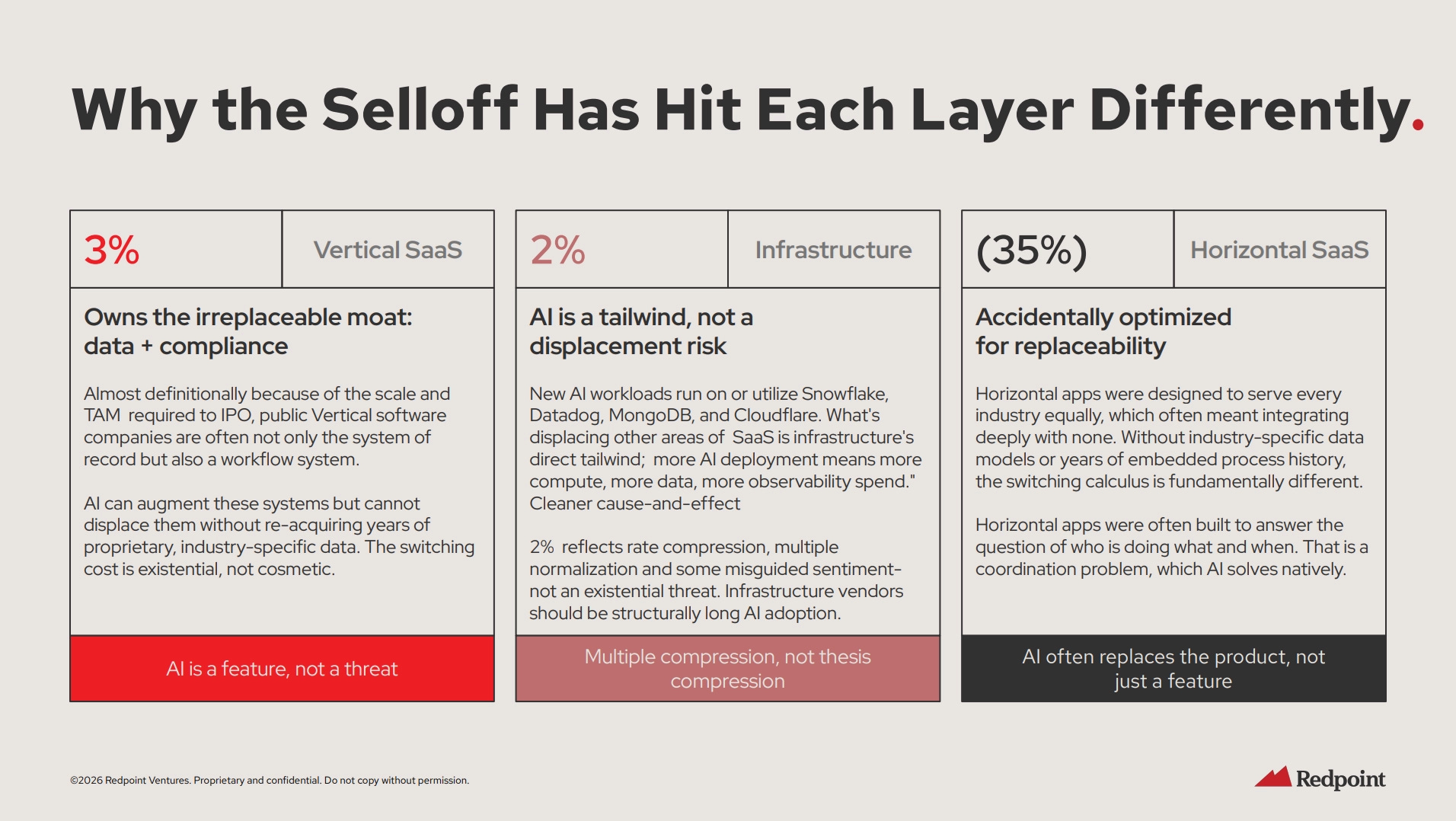

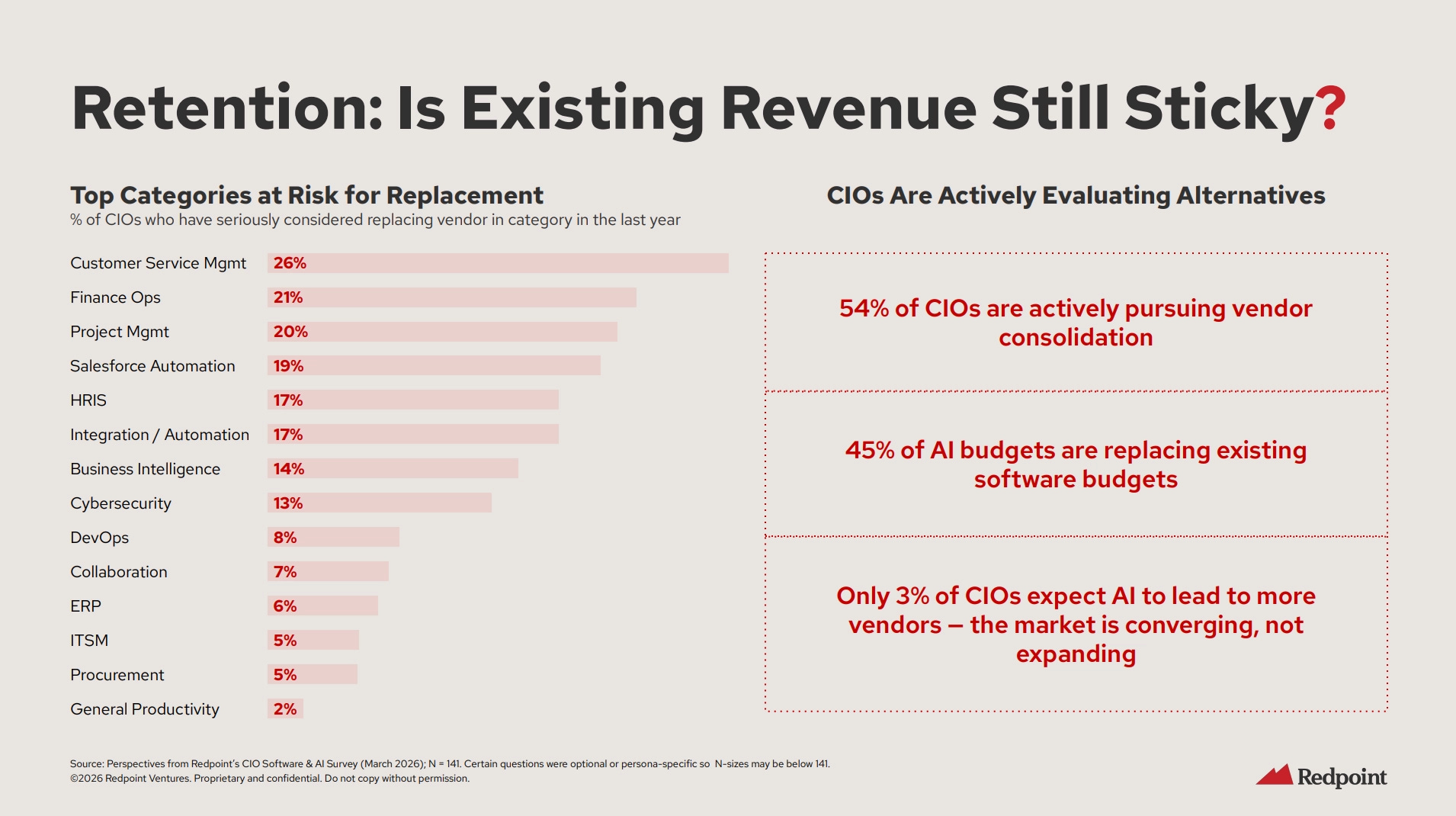

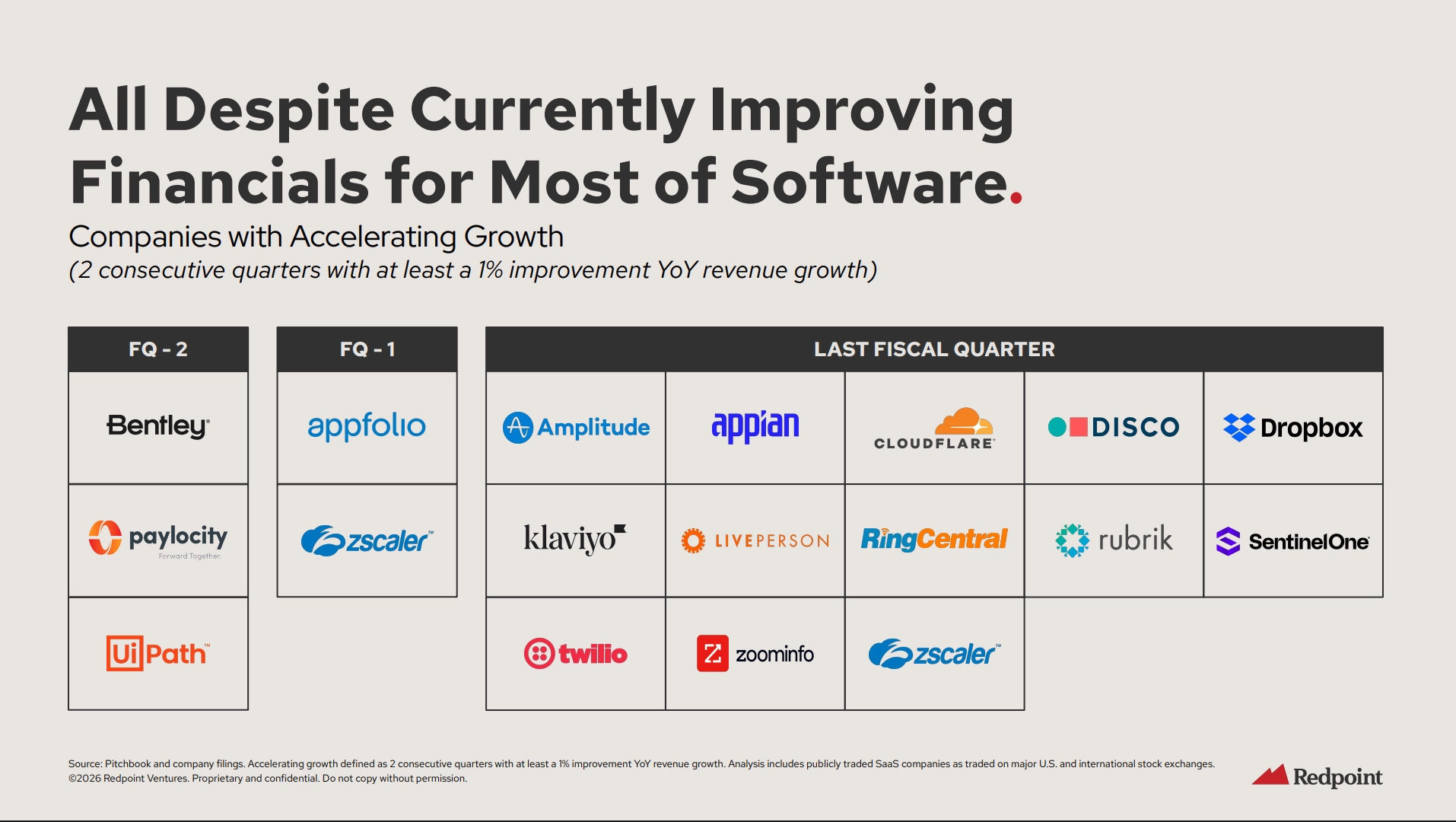

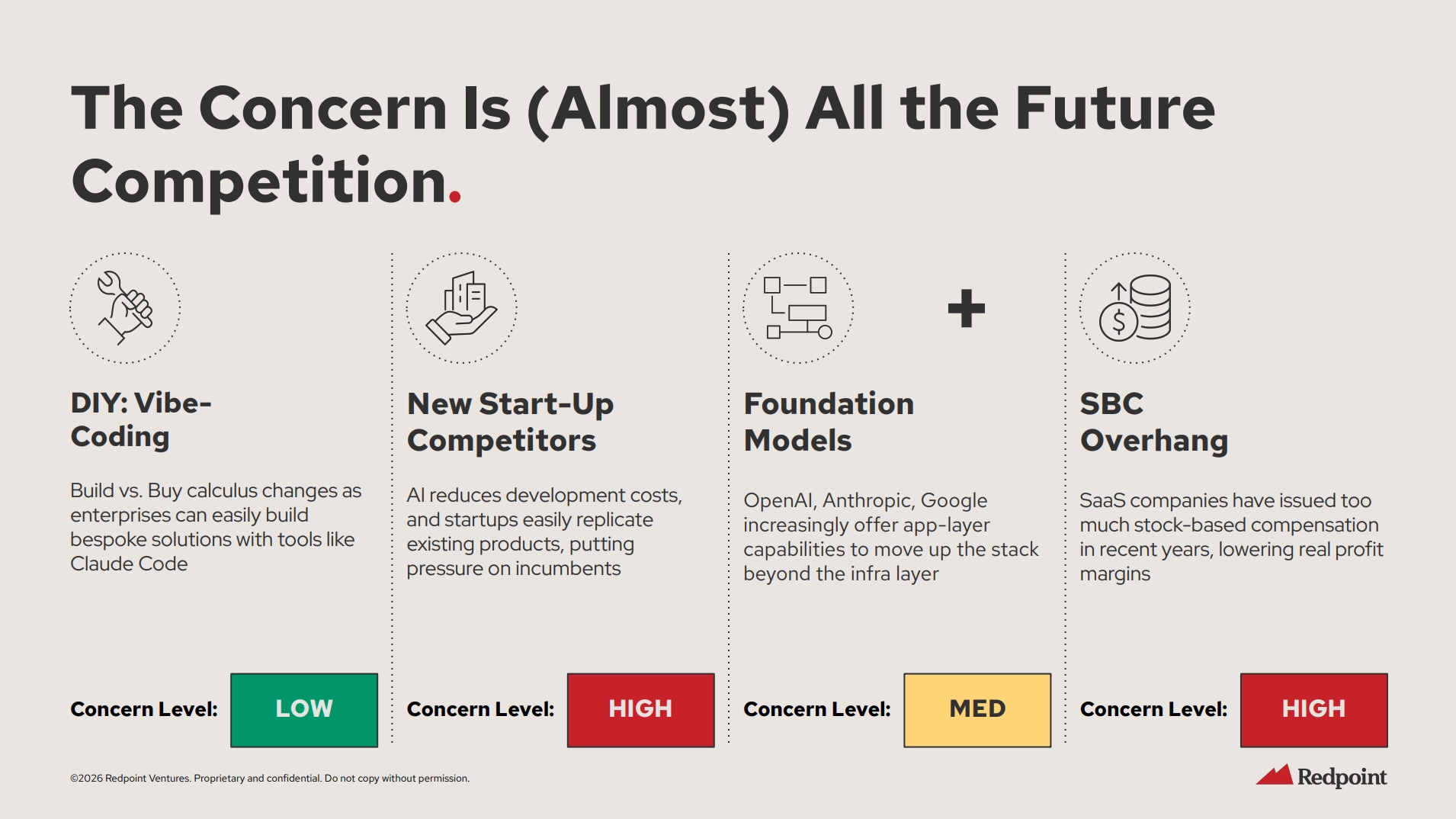

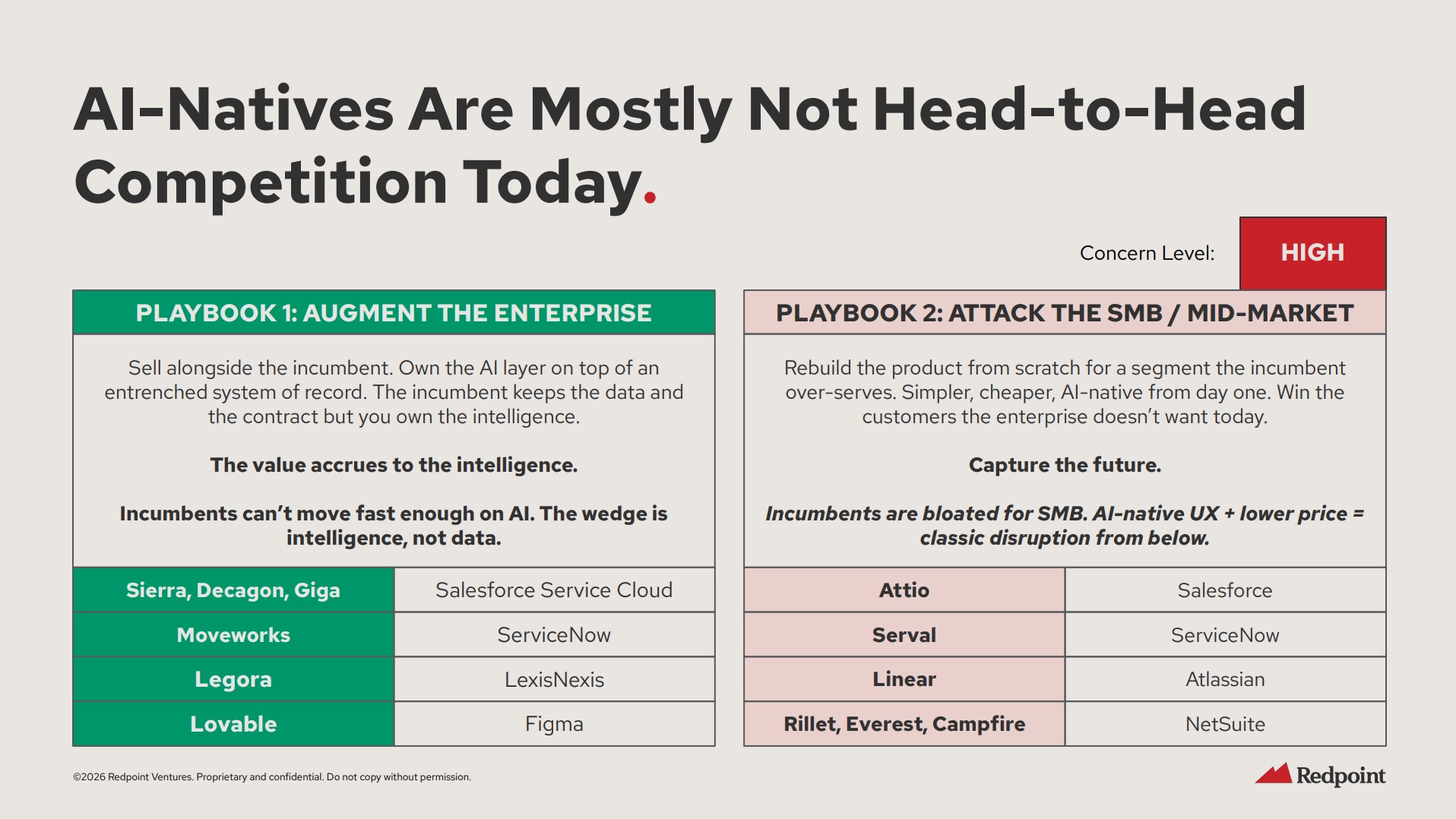

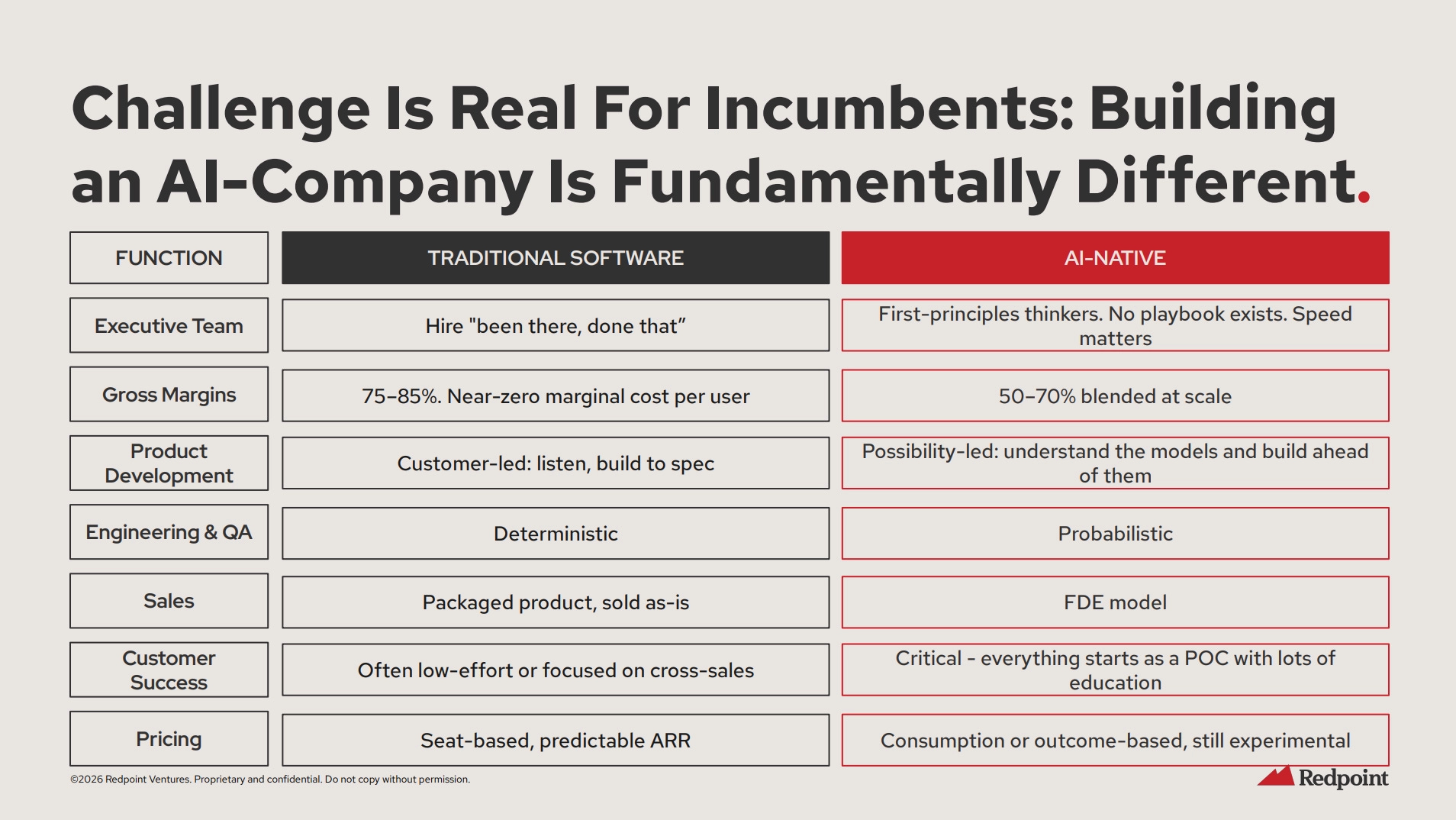

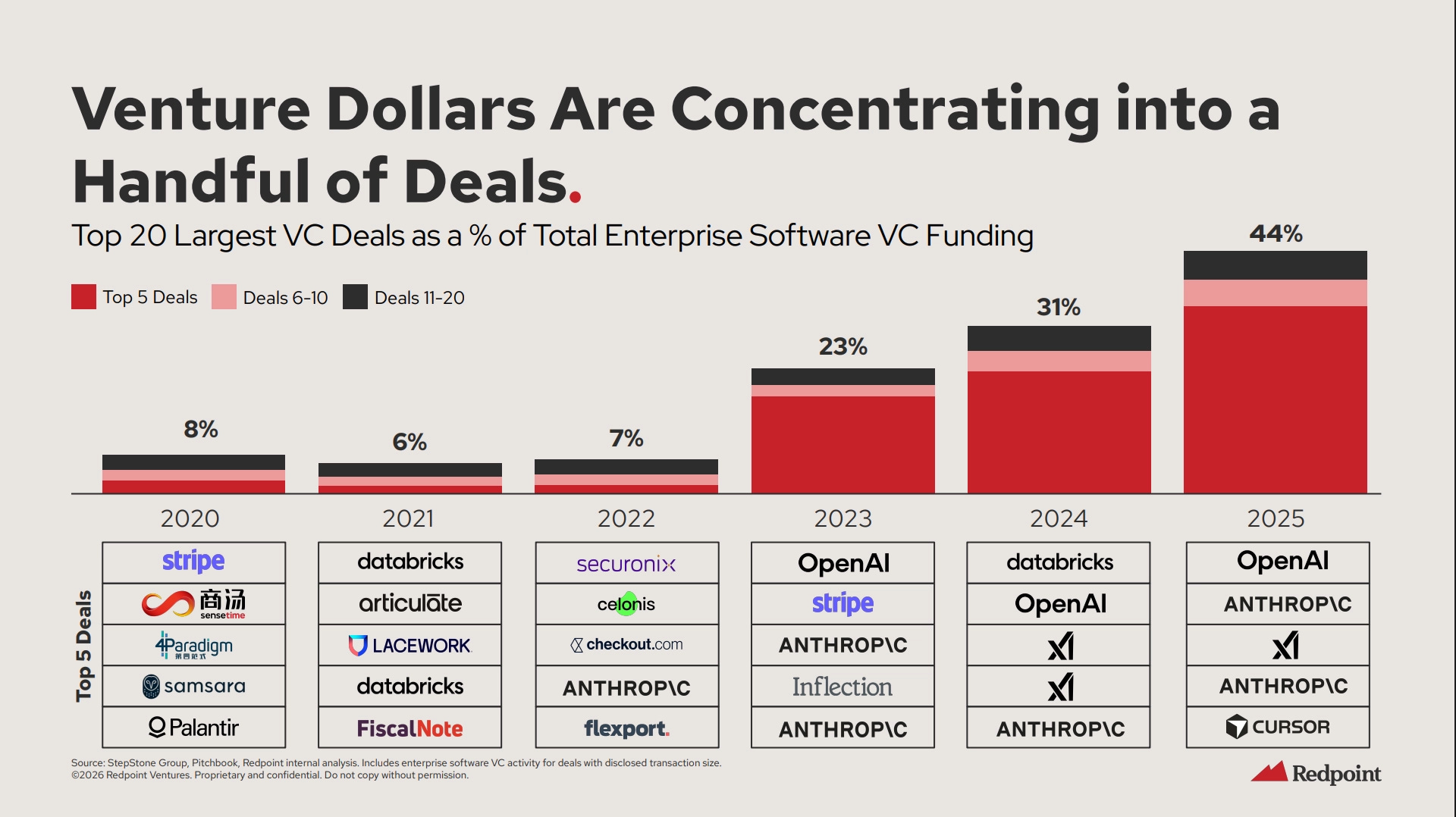

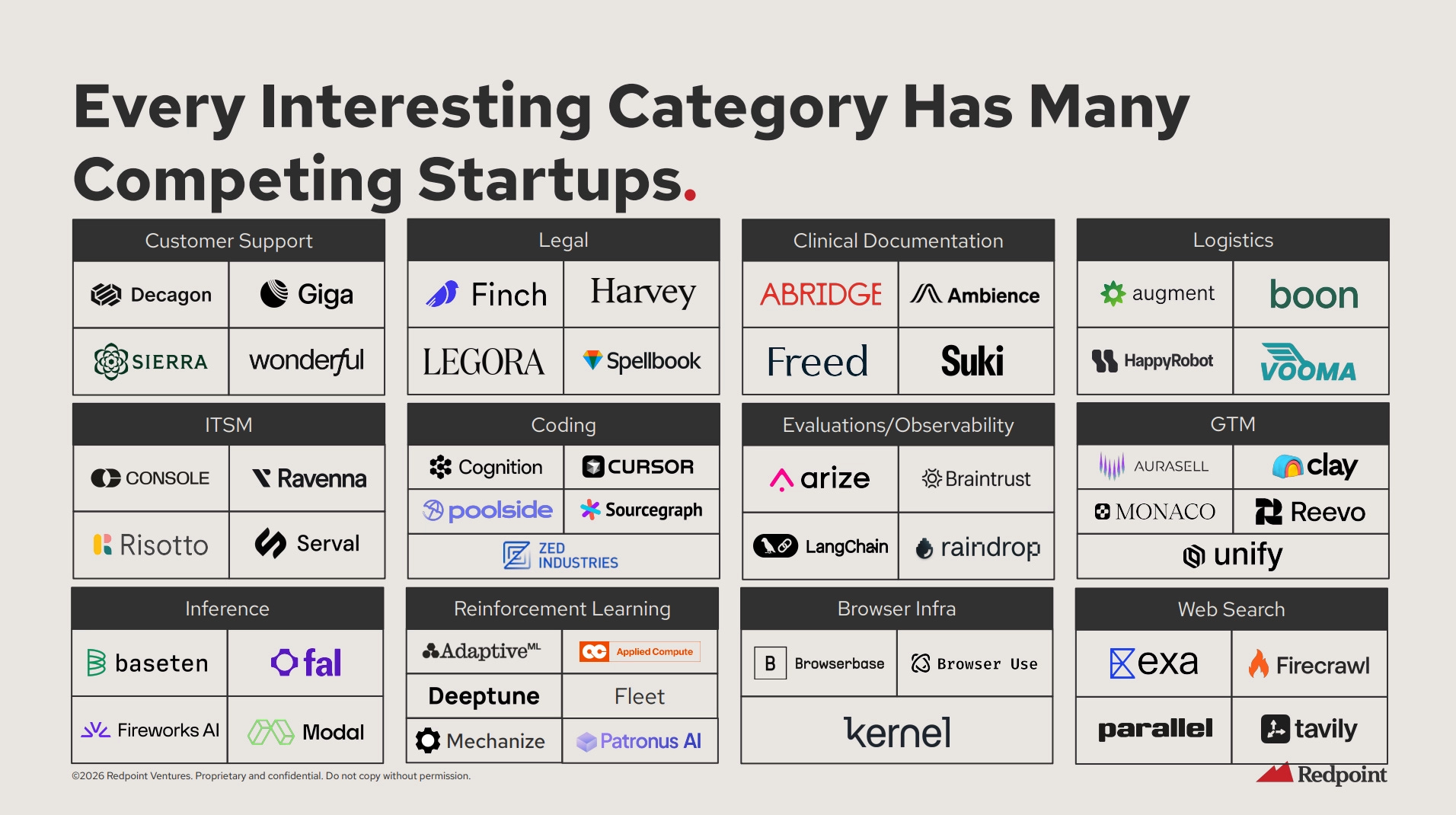

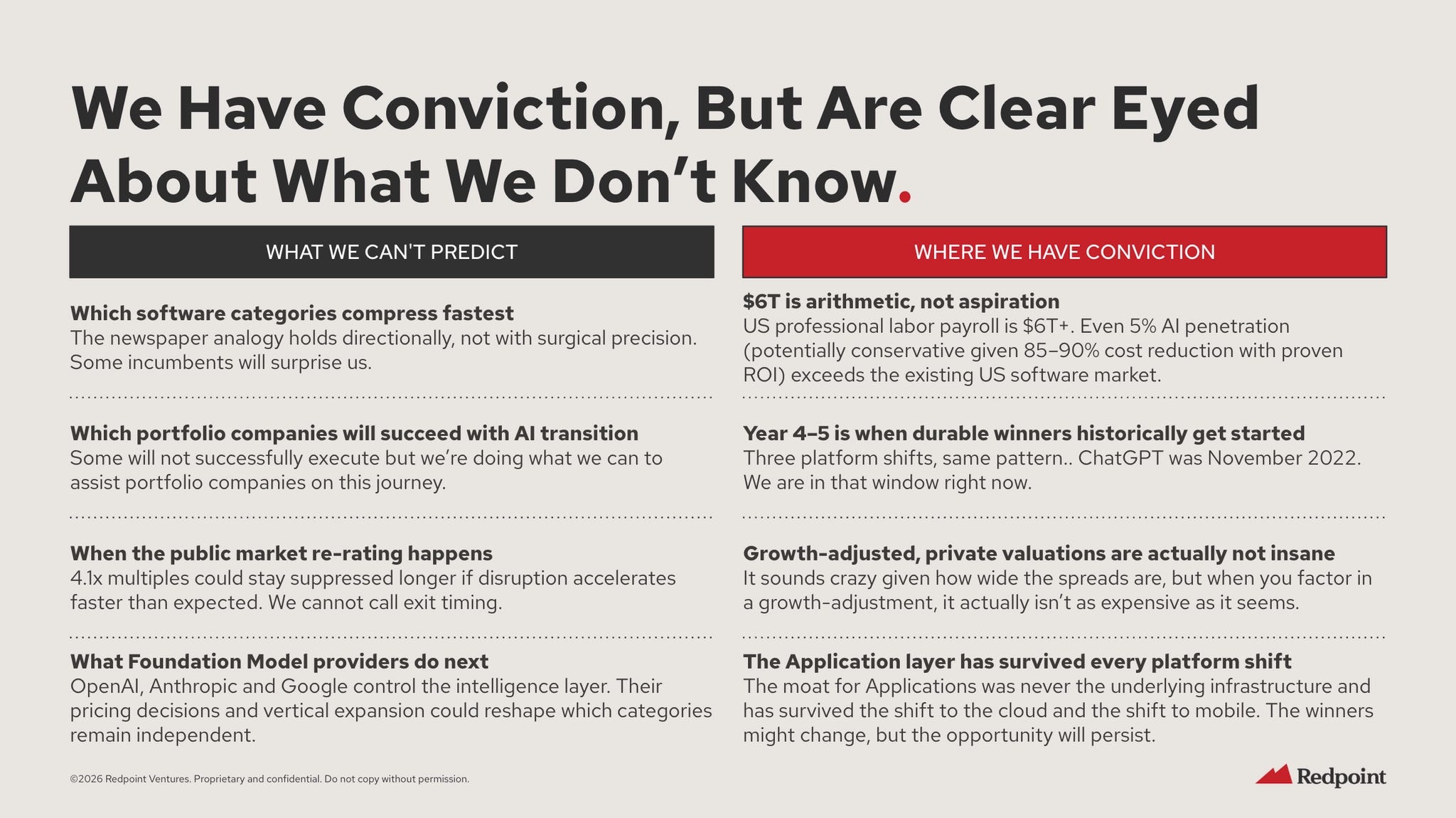

Redpoint publicly shared its AGM presentation on public and private markets. - Redpoint

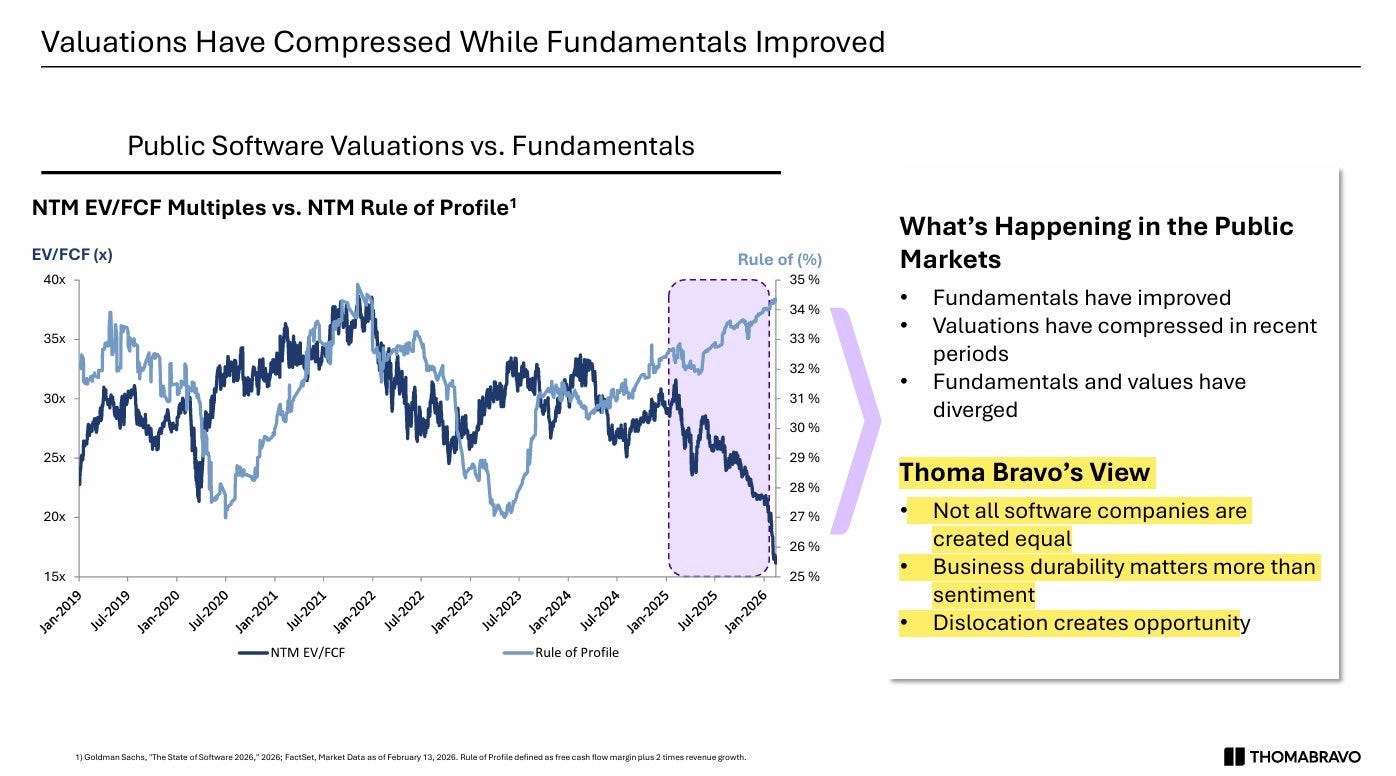

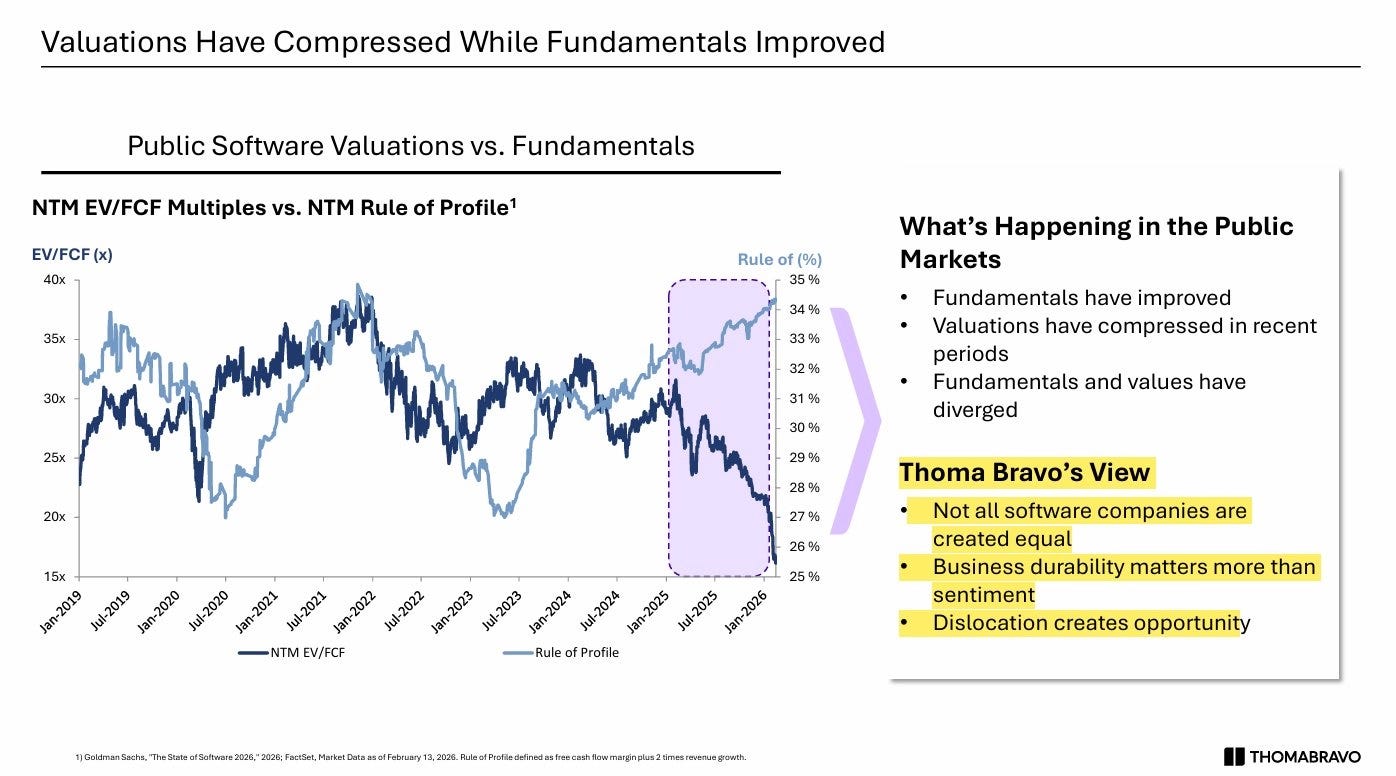

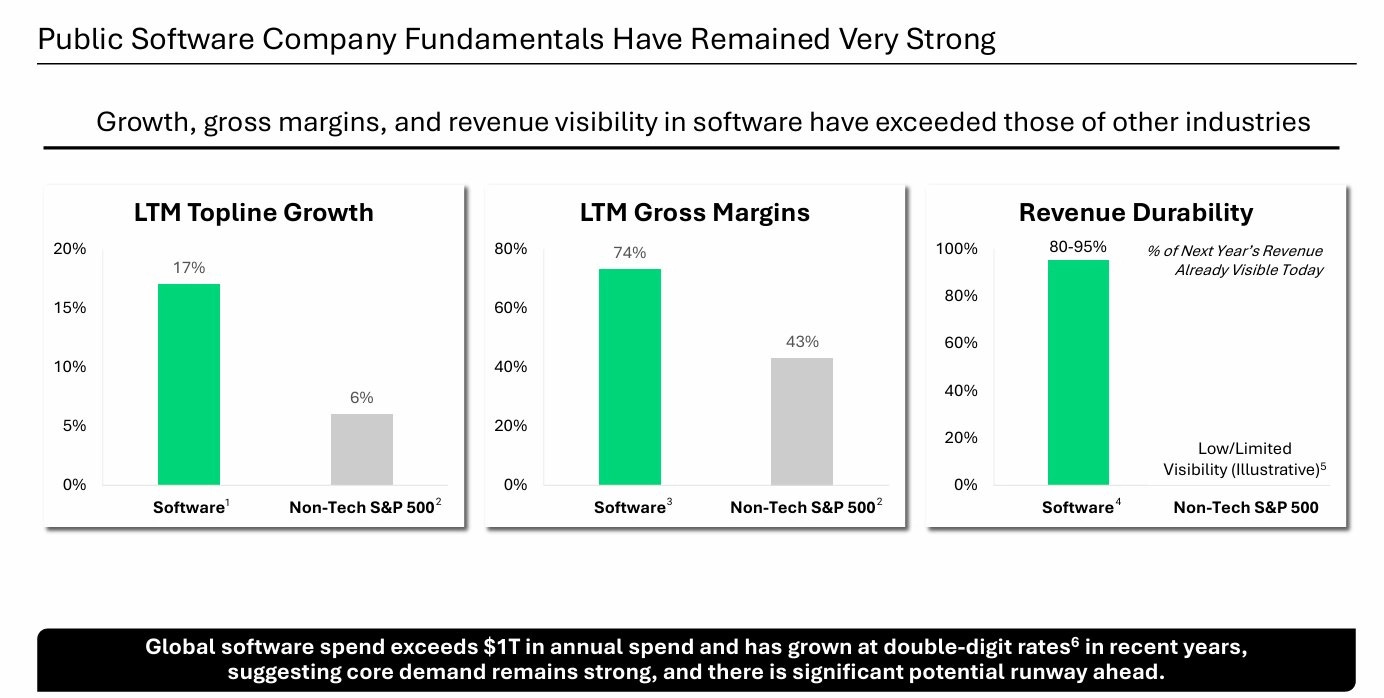

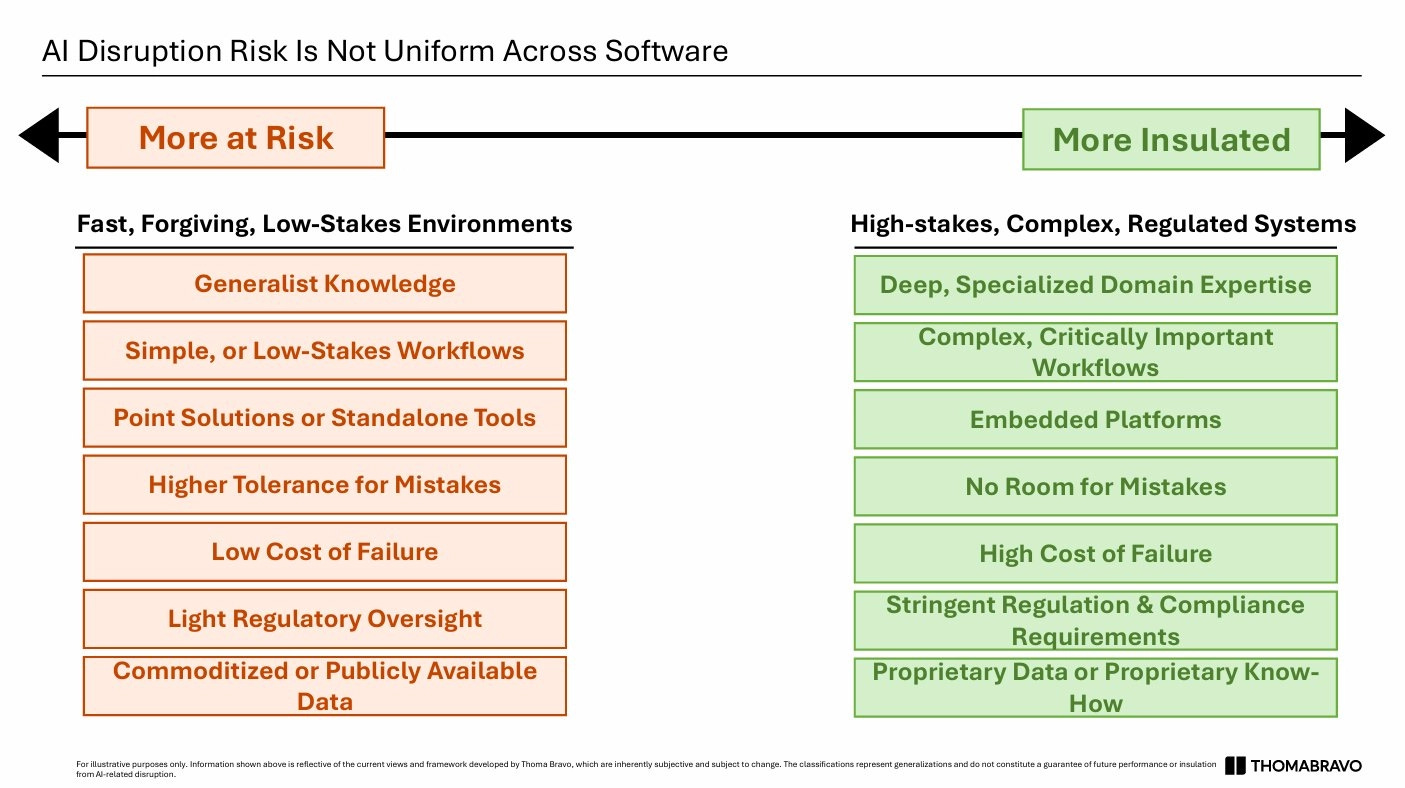

Thoma Bravo publicly shared slides it sent to LPs arguing that public markets are wrong on software companies. - Thoma Bravo

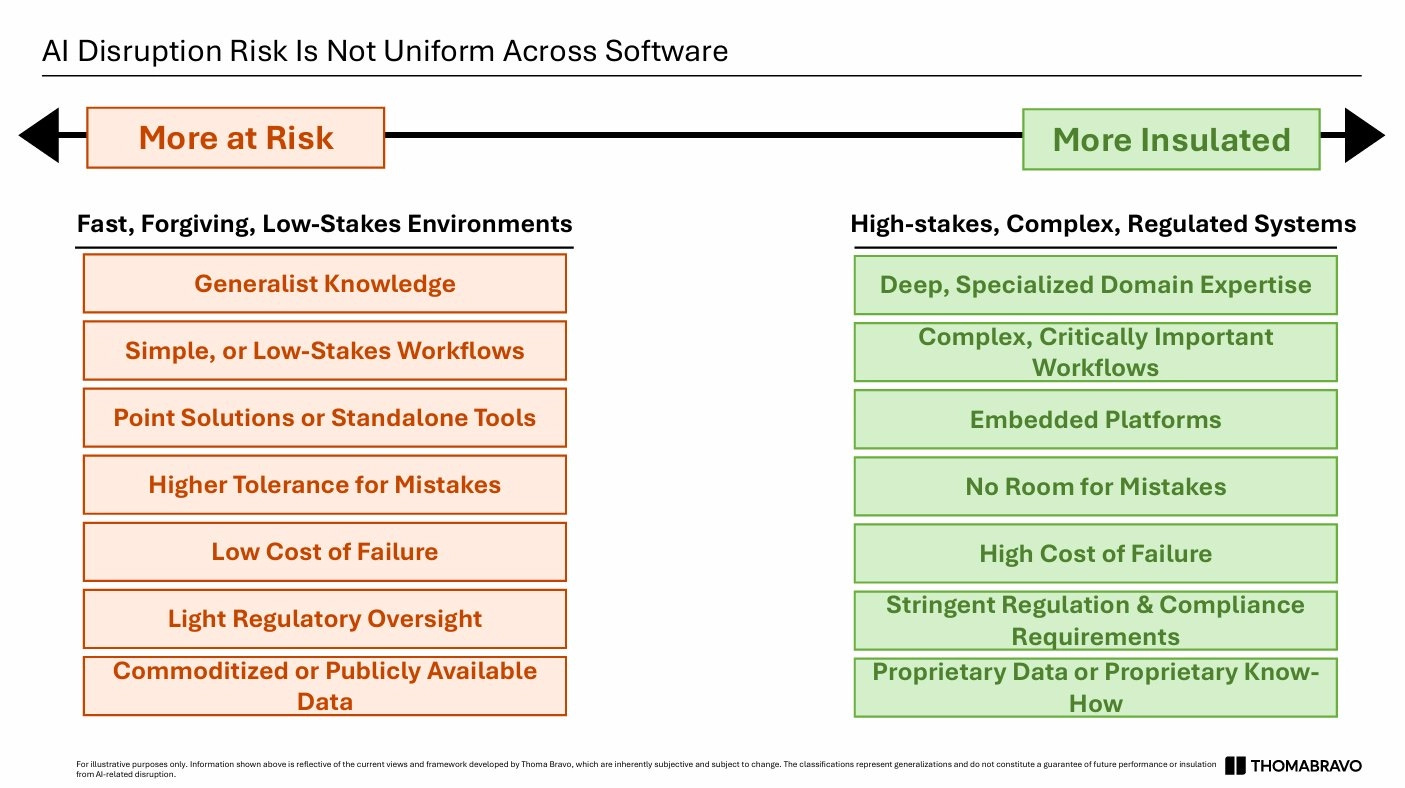

Thoma Bravo draws a line between two types of software companies. More exposed: simple workflows, generalist knowledge, light regulation, easy to replace. More protected: zero tolerance for errors, deep domain expertise, heavy compliance, proprietary data, embedded across customer systems.

“Looking backwards a bit, year-over-year revenue growth for the public software space decelerated from 2022 to 2025, not because of AI but largely because interest rates spiked and software seats had been oversold. Meanwhile, the practice of stock-based compensation as a percentage of revenue was higher than revenue growth in certain software sectors, as noted in a Feb. 2026 report. The market was complacent about these factors until it wasn’t, and now we believe it’s overcorrecting, re-pricing on AI disruption fears that aren’t fully visible in actual software business performance. The moment creates a major buying opportunity for those disciplined enough to act on it.”

Turner Novak interviewed Chetan Puttagunta at Benchmark. - Turner Novak

Learnings from Manus

Manus moved from zero to $100m ARR in eight months. Including consumption revenue, it reached a $125m run rate within that period.

It had initially product market fit on 3 use cases: (1) deep research (generating highly detailed reports beyond the capability of standard chatbots), (2) coding (used by non tech users to build websites, mobile apps & prototypes), (3) slides (leveraging deep-research capabilities to showcase them into slides).

Manus succeeded by breaking a single task into approximately 1,000 sub-tasks. For each sub-task, the system uses multiple models (Anthropic, OpenAI, and Gemini) in parallel to ensure completion.

Software history is defined by enabling technologies that lower the barrier to entry and increase the volume of applications by orders of magnitude.

“What is happening at the application layer with AI is a fundamental shift that is on the same scale of on-prem to cloud.”

Jack Altman interviewed YC partners. - Uncapped

YC serves as a “vortex” that identifies talent and normalizes the “weird” experience of starting a company. It’s a “Disneyland for transformation,” taking earnest, technical individuals and turning them into “formidable” founders.

Teams as small as 10 people (e.g. Giga) are now capable of out-executing large incumbents and well-funded competitors (e.g. Sierra, Decagon).

YC is filtering for founders with (1) agency (problem solving skills), (2) tenacity (”tireless gardener”) and (3) taste (building a product loved by users).

YC now operates as a collection of autonomous “mini-YCs” or pods. Each partner runs a group of ~30 companies, similar to the size of early YC batches.

Colossus interviewed Mitchell Green at Lead Edge. - Colossus

Lead Edge has 18 junior analysts cold-calling c.9k companies per year. It screens these companies against 8 criteria (revenue >$10m, >25% YoY growth, >70% gross margins, recurring revenue, capital efficiency, profitability, no customer concentration, 90%+ gross retention). c.900 companies meet 5+ criteria. It does do diligence on 150-175 to make 5-7 deals per year.

Lead Edge has 800 LPs (95% of them are world-class executives and entrepreneurs) which are actively leveraged across the entire investment lifecycle (sourcing, due diligence, post investment).

Lead Edge has a unique portfolio construction. It targets 2-5x returns per deal in 3-7 years to reach 2-2.25x net and 20% net IRR at the fund level. They avoid write-offs and only lost all their money in one deal ever.

70% of capital deployed is special situations or secondaries. Lead Edge invested in Zoom via LP positions in a fund that held Zoom stock because they couldn’t lead a round (company didn’t need money) and couldn’t buy secondary (Sequoia blocked it).

“If you tell an entrepreneur you’re gonna do something, then actually do it. There are so many people that say they’ll do things that just never do them. If you’re known as a person that does what you say you’re gonna do, it goes a long way.”

There is no science of entrepreneurship as any method for building a startup, once widely known, stops being an unfair advantage. - Jerry Neumann

“If everyone follows the same bestselling startup techniques, everyone ends up building the same company and, with no differentiation, most of those companies fail. The truth is, anytime someone insists on a method for how to build a successful startup, you should do something different.”

“What the chart shows is that between 1995 and the present, the percentage of companies surviving for one year is essentially unchanged. The same is true at two years, five years, and 10 years.”

“The precipitous drop in seed-funded companies raising further capital does not support the idea that venture-backed startups have become more successful over the past 15 years. If anything, they seem to fail more often.”

“Once everybody uses the same theories, maybe they stop conferring an advantage. Strategy is about doing something different from your competitors, after all.”

“When new startup methods are quickly adopted by everyone, no one gains a relative advantage, and success rates stay flat. To win, startups must develop novel, differentiating strategies and build sustainable barriers to imitation before competitors can catch up.”

“A genuine science would embrace the dynamism rather than try to eliminate it. It would recognize that competitive differentiation is the mechanism by which startups create durable advantage, that homogeneous strategies cannot produce differentiation, and that the usefulness of any novel approach has a half-life inversely proportional to how fast it spreads.”

“If you do what everyone else does, you get what everyone else gets.“

Reid Hoffman at Greylock wrote about the “SaaS is dead” narrative. - Reid Hoffman

Margin erosion is not death. The old operating 40-50% margin SaaS model is weakening, but the leap from “disrupted” to “dead” is wrong.

Software is not just code generation. Most people misunderstand software businesses as lines of code generated once. They are living systems requiring maintenance, verification, security, compliance, and ongoing refinement.

The new moat is AI-native domain depth. A CRM company that ships deeply intelligent agents tuned to sales workflows, with purpose-built backend libraries, has a strong moat. Generic prompting won’t replace that.

Business model shift ahead. Expects moves toward prepaid token budgets (utility model), similar to the on-prem to cloud SaaS transition. The world expanded then; it will again.

Classic moats still hold. Network effects, customer relationships, data advantages become more valuable when AI can build on them. Customer lock-in deepens when AI has been trained on years of specific workflows.

Jevons’ Paradox applies. As the cost of building software drops, demand for software will expand.

VC is not a unified asset class. What people call VC is actually four distinct activities conflated under one label: (1) seed investing, (2) traditional venture (contrarian experimentation against uncertain hypotheses), (3) supercharged growth investing, and (4) small-cap growth tech stocks repackaged as private rounds. - Kyle Harrison

“Despite the dozens of scout programs and angels and incubators and accelerators and hacker houses and bootcamps, there is still raw untapped potential in the world of the entrepreneurially minded. There are still people with the intellectual horsepower and cultural grit to shape the future, they just lack the familiarity with how to “play the game.” Seed investing can still offer these people a supportive on-ramp.”

“What most of the capital deployment we have today would fit into is a very odd bucket that feels akin to old-school growth investing, but it is supercharged.” “The underwriting case for those businesses is momentum rather than fundamentals.” “The danger of this kind of “growth investing” is this: what can go up fast can go down just as fast.”

“Seed investing is a game of people. The idea, candidly, doesn’t really matter very much. Seed investing is about finding exceptional people with exceptional gumption who will run through walls to shape the world around them. You can support these people, you can help round some of their roughest edges, you can help them become more legible to downstream capital. But, ultimately, it is 99.99% about the people.”

Josh Wolfe at Lux shared a memo its its founders. - Lux

“We send notes like this not because something is wrong, but because the cost of preparation is trivially low and the value of being positioned well is asymmetrically high. This isn’t a macro call. It’s a set of observations about correlated risks that are worth your attention. And a set of practical suggestions regardless of whatever happens next.”

“Markets rewarded Block’s 50% workforce reduction with a 20%+ stock gain. Other companies may have been wanting to do layoffs and see highly publicized RIFs as providing PR cover. They may see it as a way to boost their stock price. So it creates incentive structures that might ripple through partners or customers. Having concentrated relationships at a partner or customer, where that person or sponsor or their team gets laid off would be a wise risk to hedge against. An actionable thing is to check-in and meet more people on teams and work for wider relationships. If you make revenue that correlates to customer headcount, it’s wise to model what happens if there are surprise layoffs.”

“Model customer concentration against headcount compression. If any customer category exceeds 20% of revenue, scenario test it. The procurement effects from layoffs typically lag, maybe by one to two quarters. Having a sense of any exposure now gives you time to diversify and prepare.”

“Confirm compute capacity in writing. If your growth depends on scaling cloud infrastructure, verify your commitments and understand where your workloads physically run. We can see scenarios where there is a glut of availability and lots of capacity…and scenarios where there’s chaos and confusion and disruption.”

“Extend runway if you can do it cheaply. Some of our companies are really well capitalized, others are waiting for milestones to justify a new round. If a small bridge or tranche draw is available on reasonable terms, it’s worth considering. This is not at all about raising a full round at a discount or even flat. It is about sanity checking having breathing room at low cost, if you need it. Also worth checking syndicate strength as some funds may have invested in you out of older funds and may not have reserves to keep funding.”

“We’re not at all predicting what happens next. We’re observing that the number of correlated risks seem higher than usual, and that the companies which consistently outperform in the Lux family and beyond are the ones that maintain a good margin of safety as a matter of discipline in advance of (and not in response to) fear.”

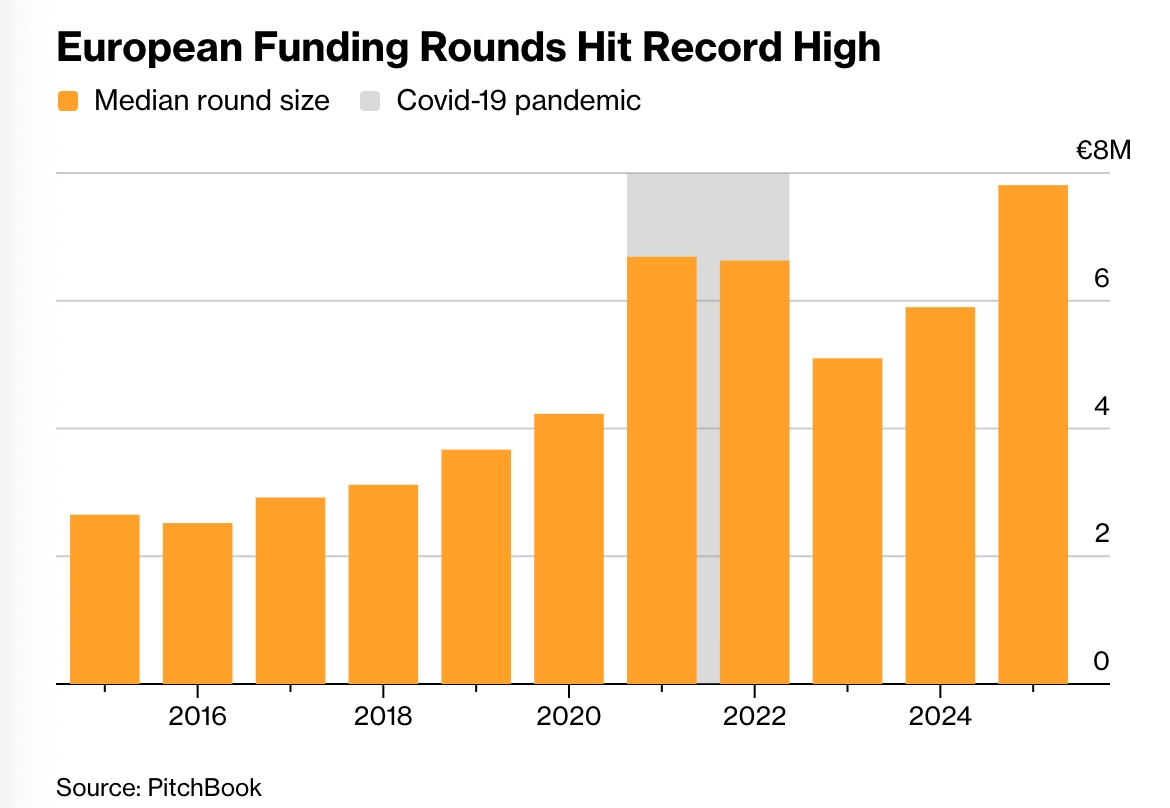

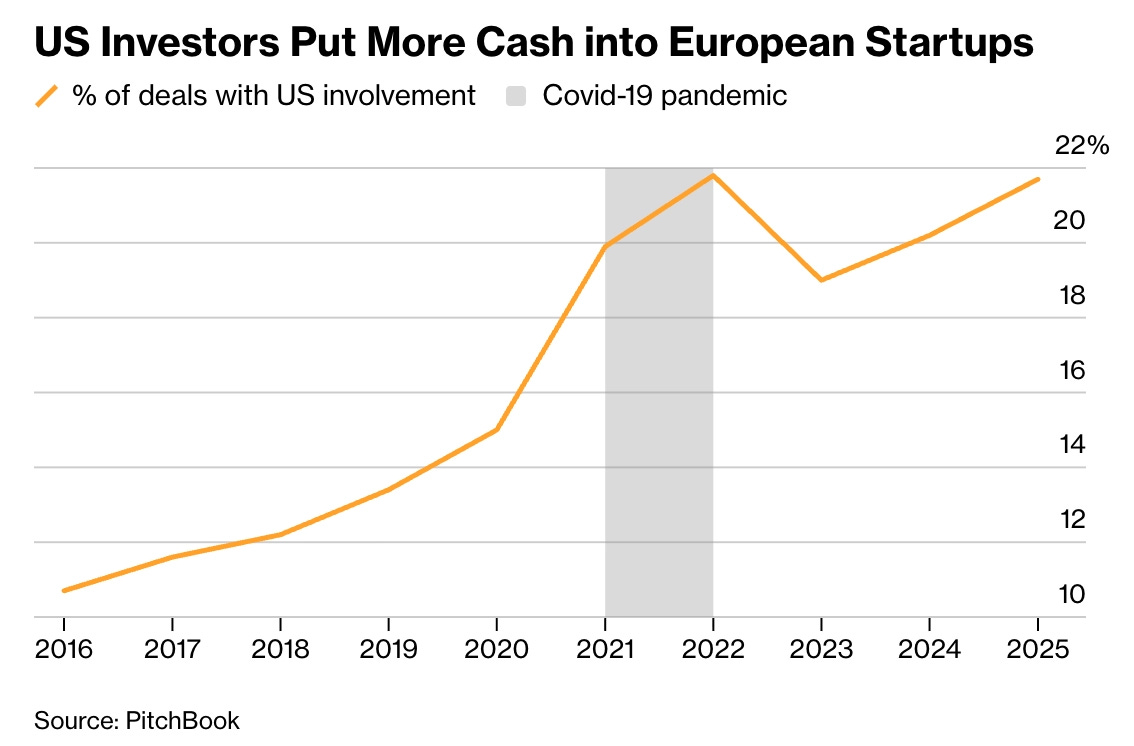

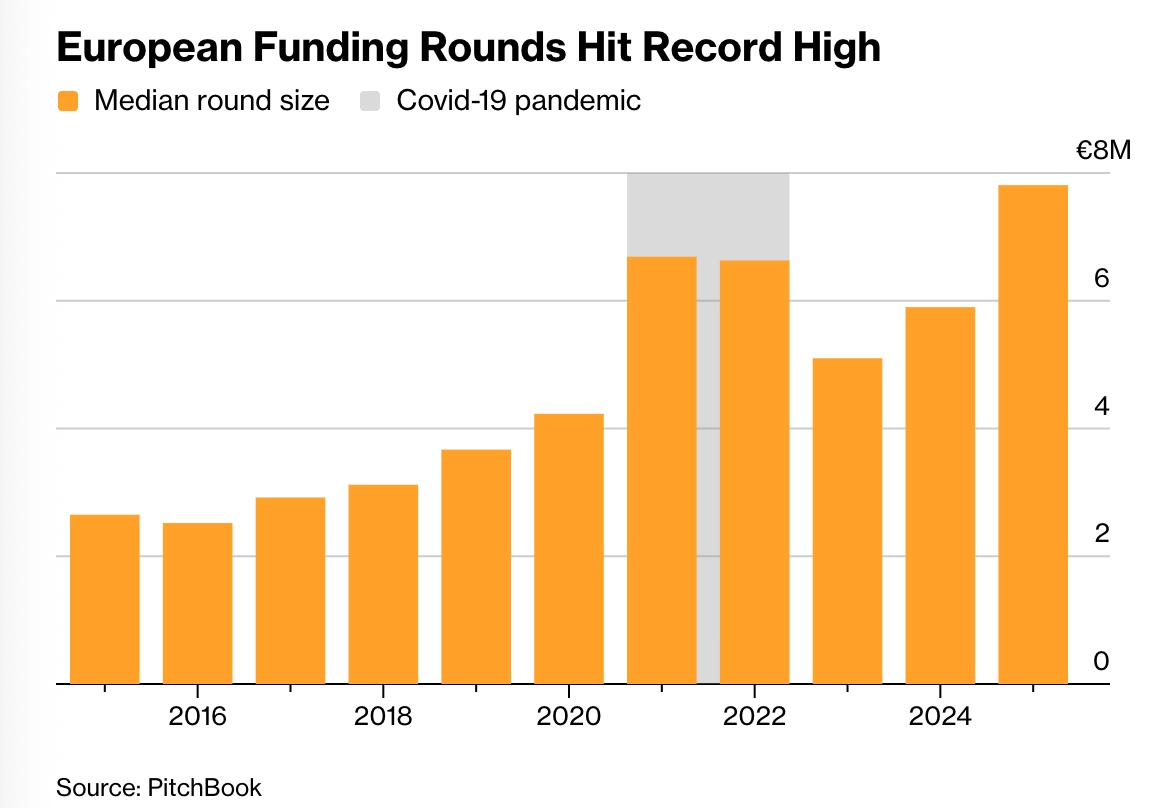

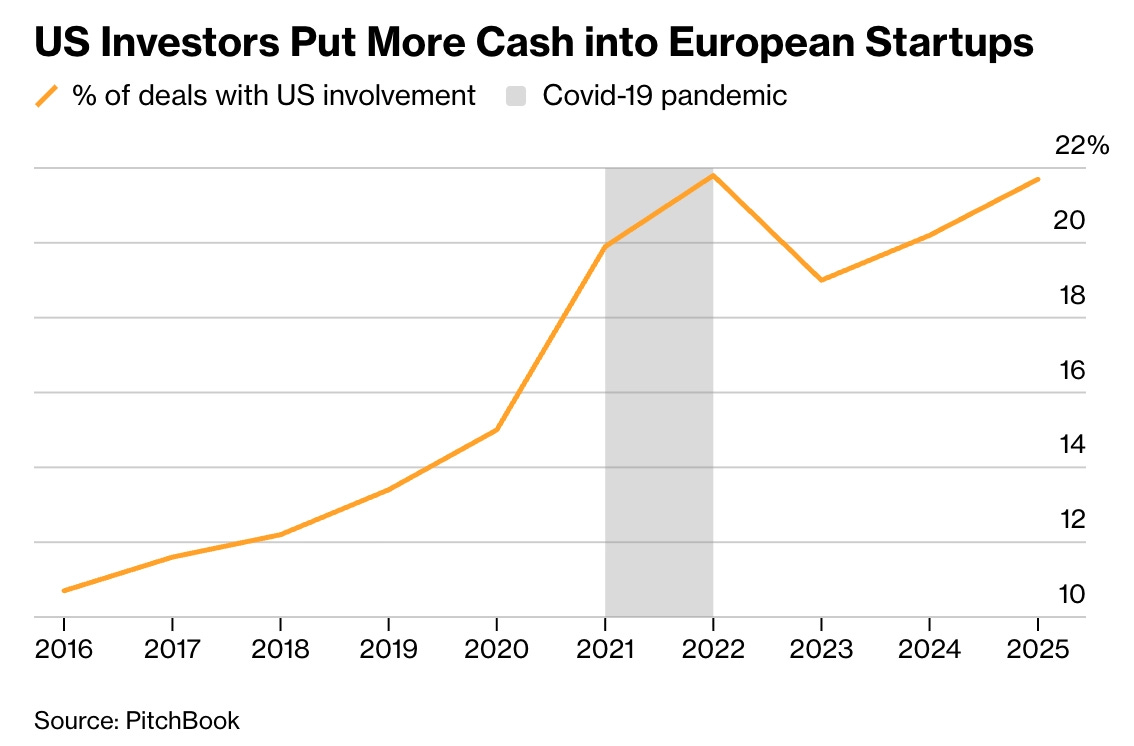

Bloomberg wrote about US funds inflating funding rounds size and valuation in the best European startups. - Bloomberg

“European funding rounds have never been bigger. Months-old startups without a product are surpassing $1 billion valuations, once a symbolic milestone attained after years of grind and multiple funding rounds.”

“US cash is driving the trend, with American investors at peak participation in European funding rounds. US backers are in a fifth of rounds, up from a tenth a decade ago.”

““I flew to Stockholm six or seven times to meet Anton,” said Ben Fletcher, a partner at venture firm Accel who recently moved to London from San Francisco, referring to Lovable Chief Executive Officer Anton Osika. “They weren’t raising at the time, but when they wanted to raise, we had a term sheet ready.” Accel led the latest funding rounds for n8n, Lovable and Legora.”

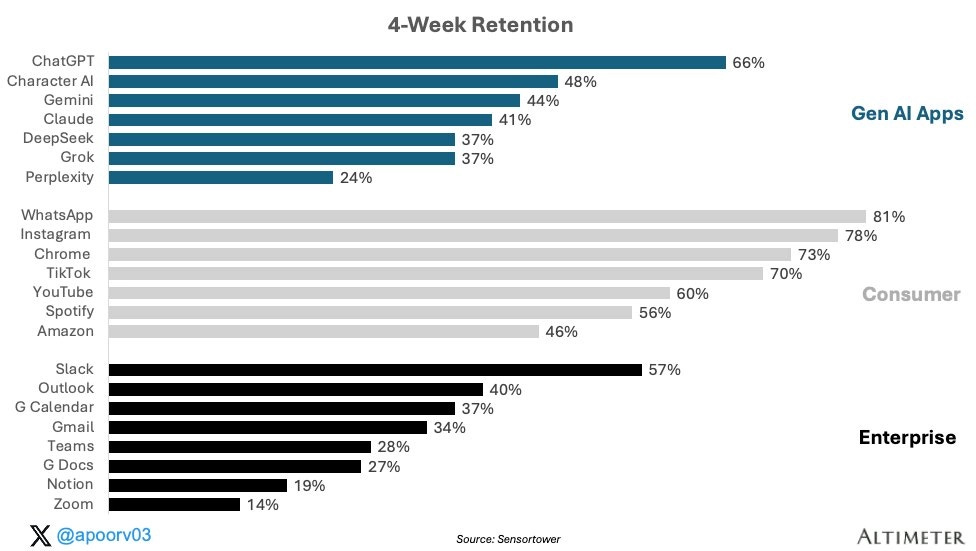

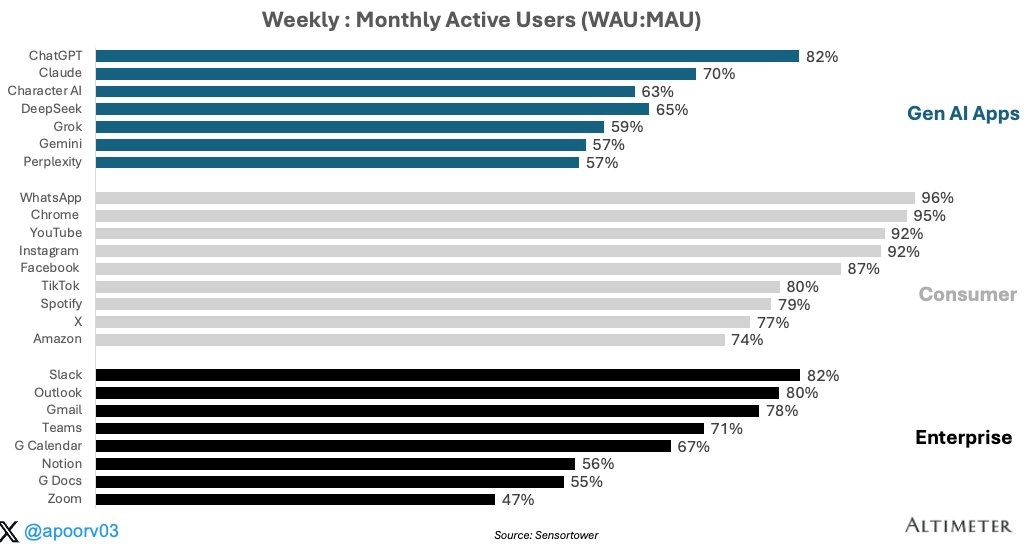

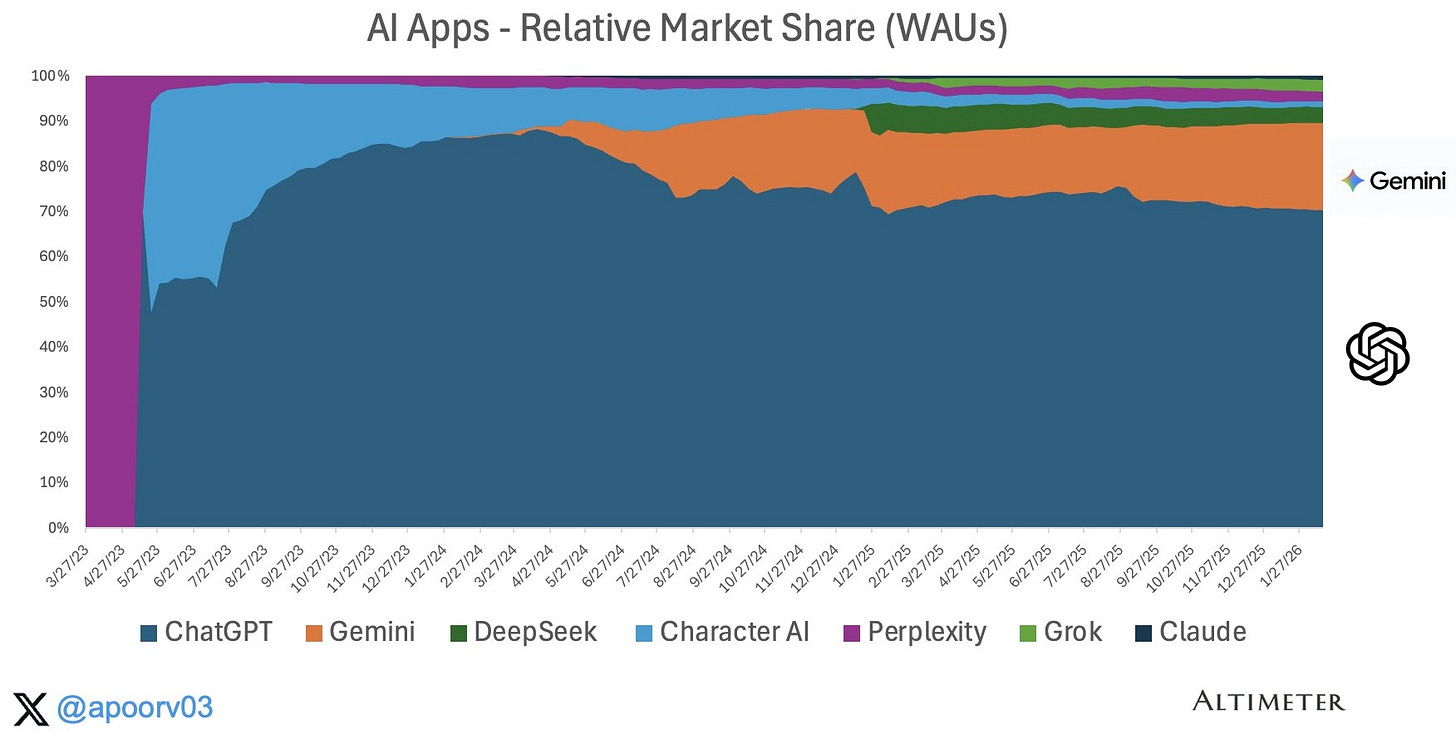

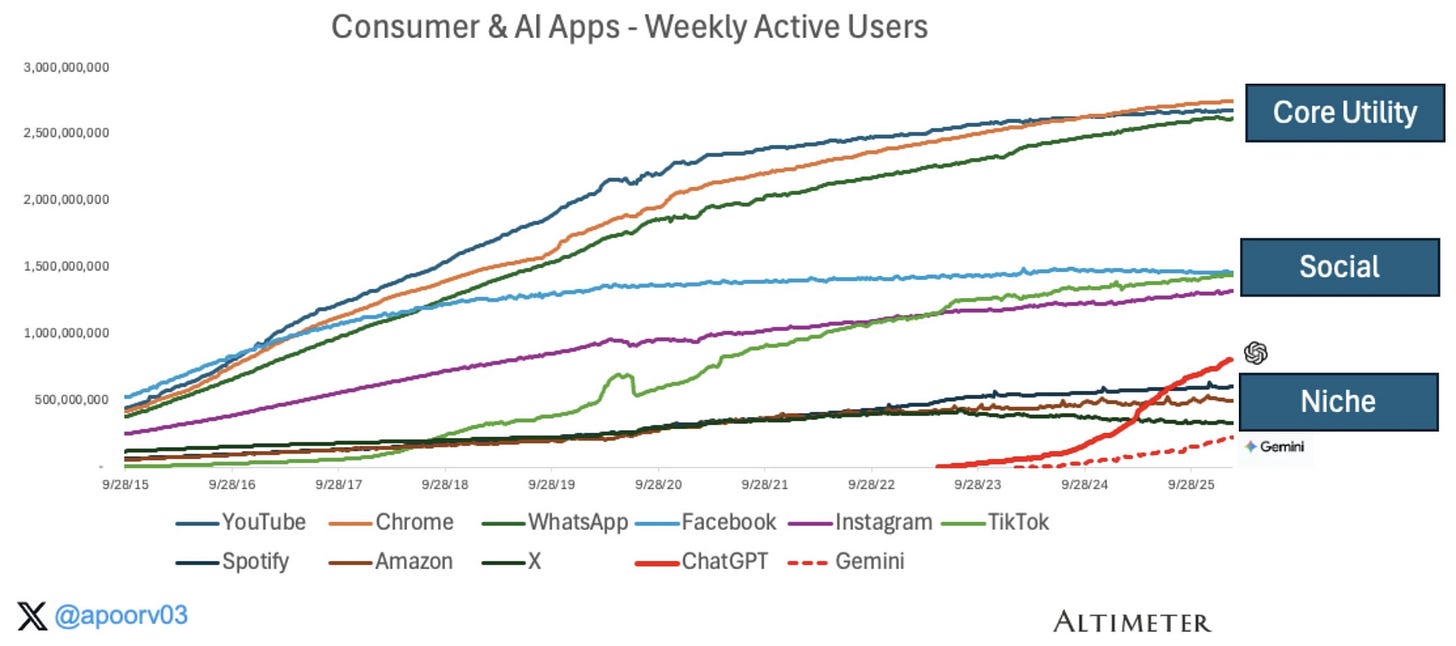

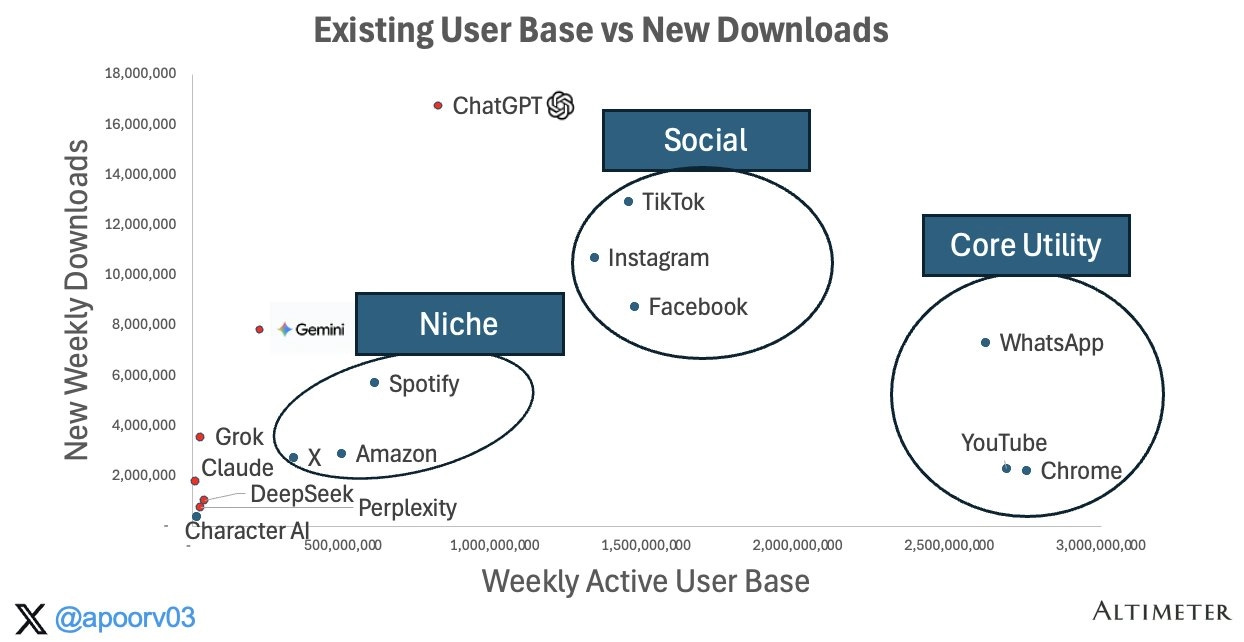

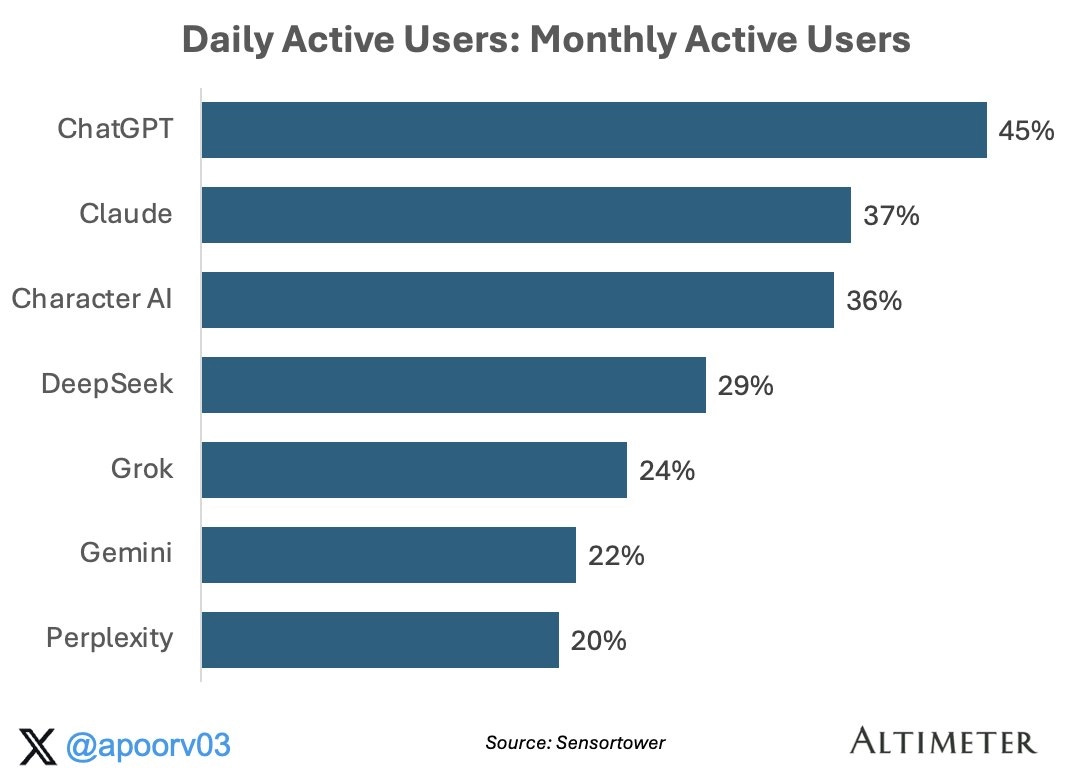

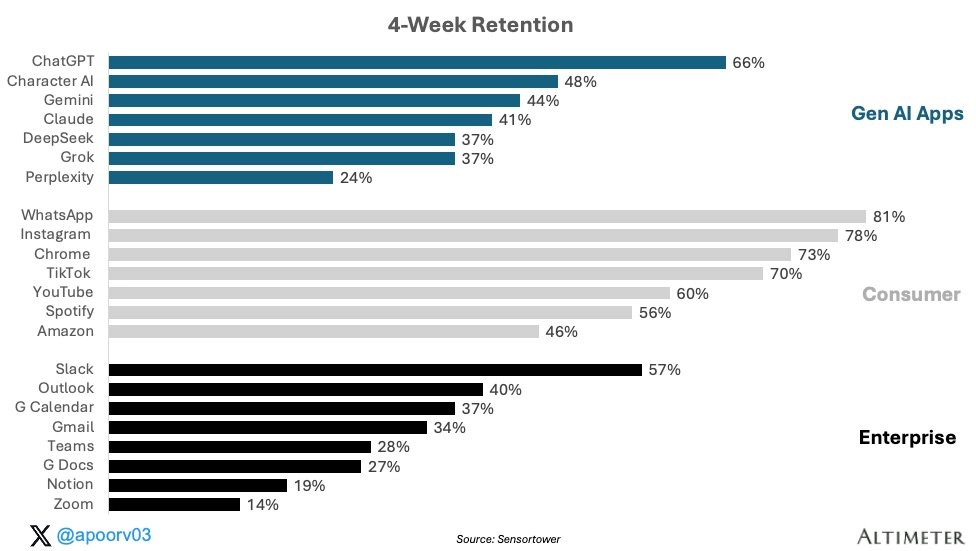

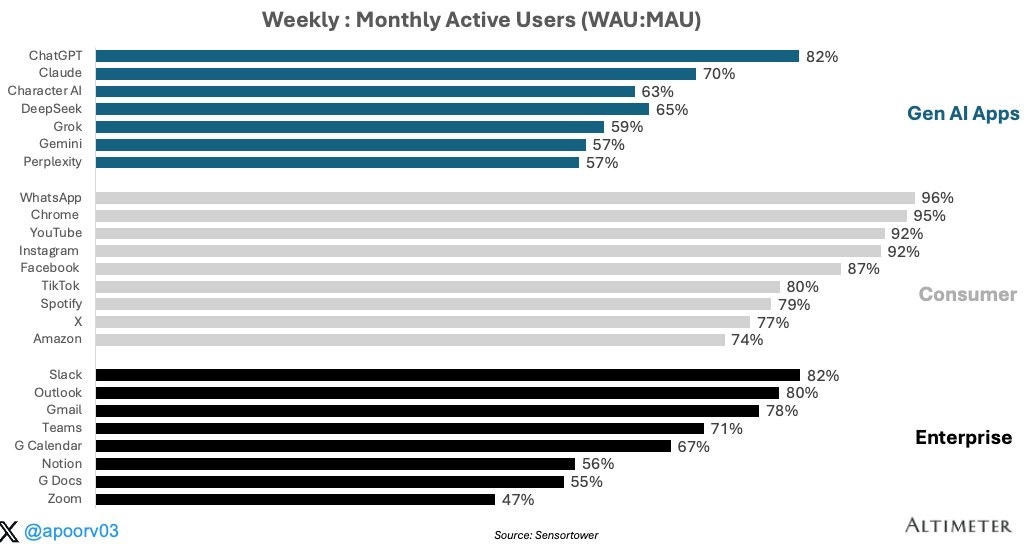

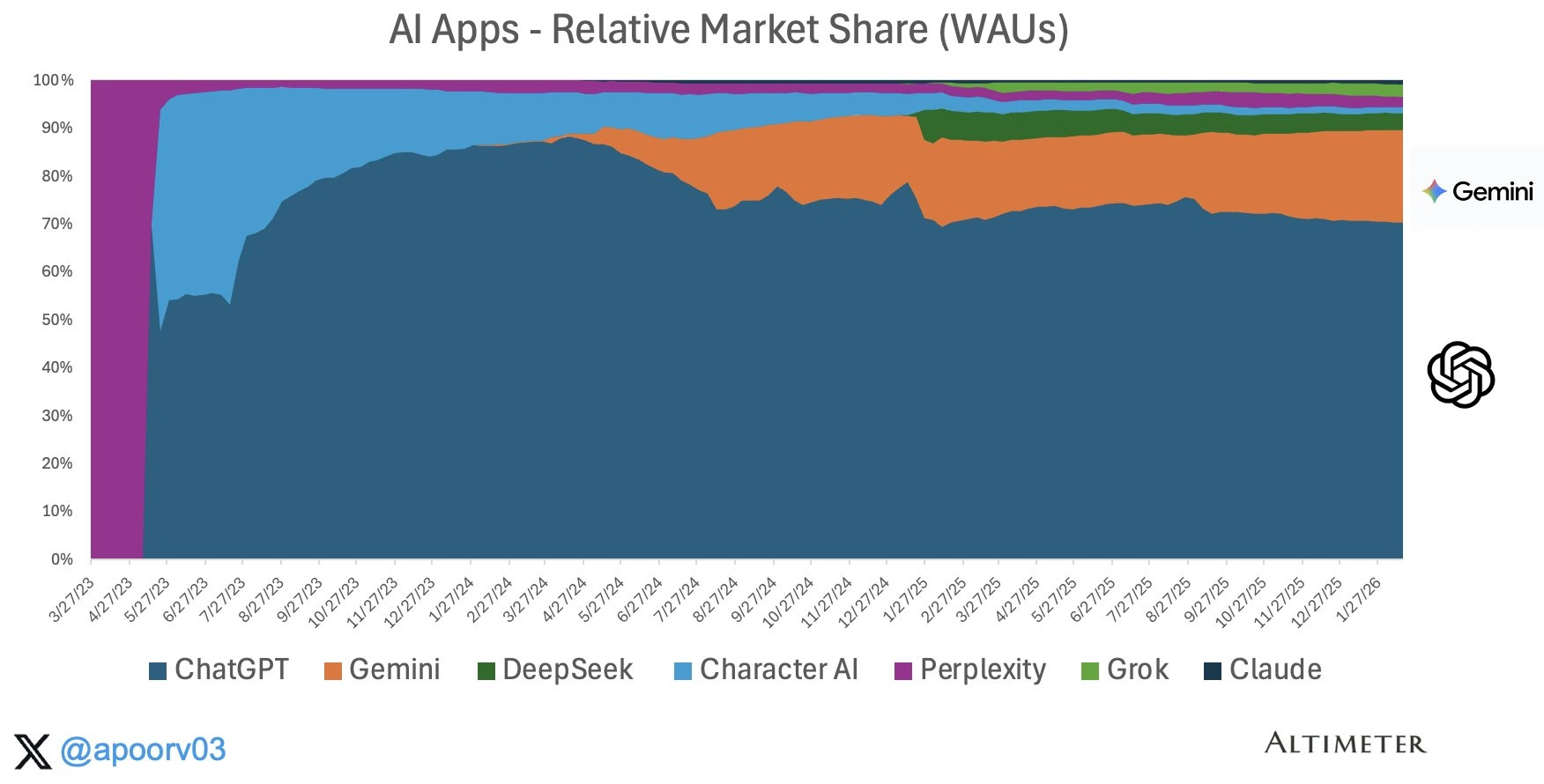

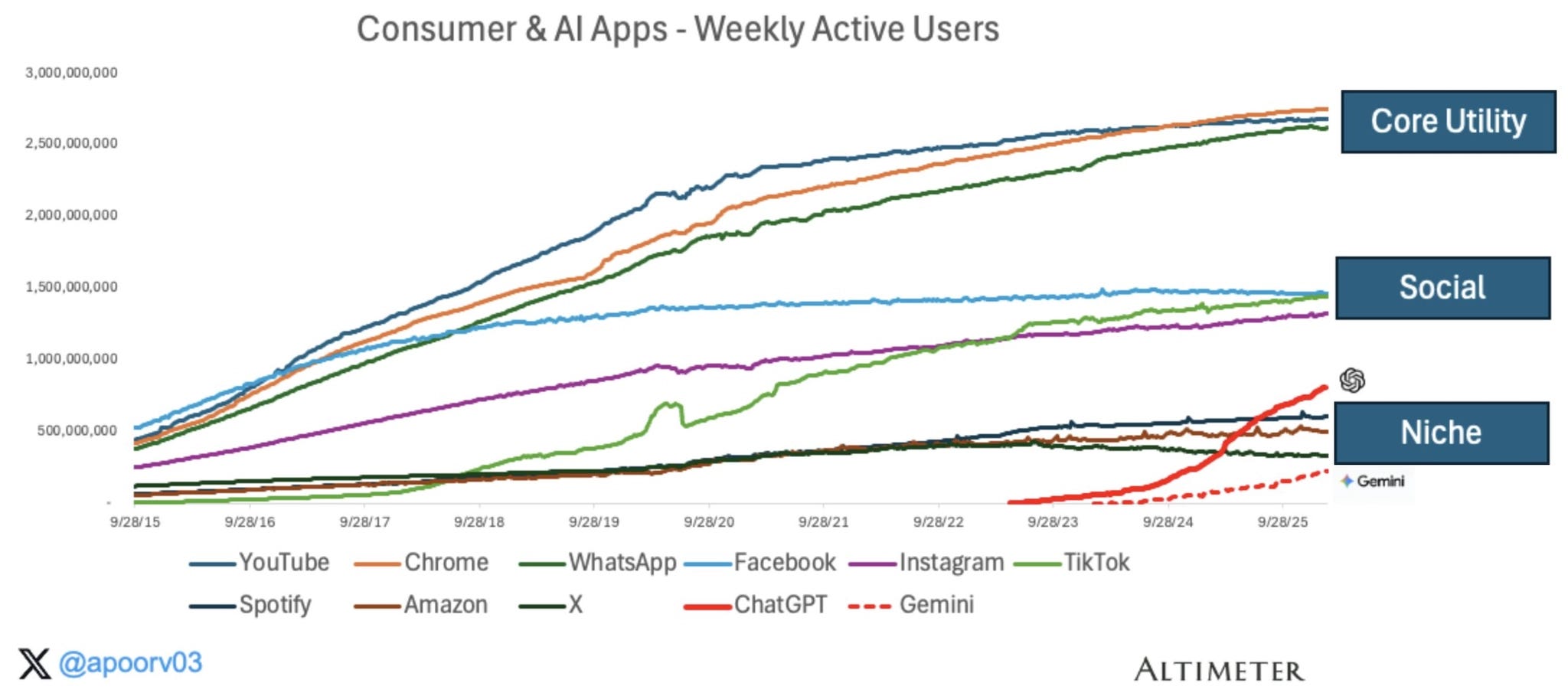

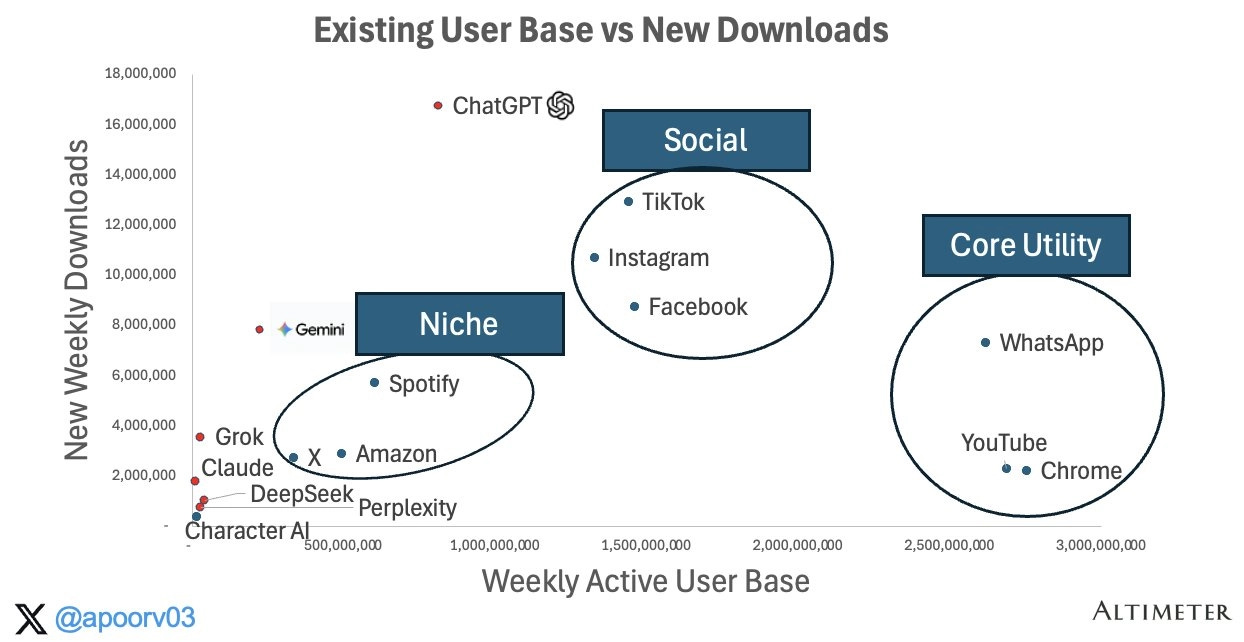

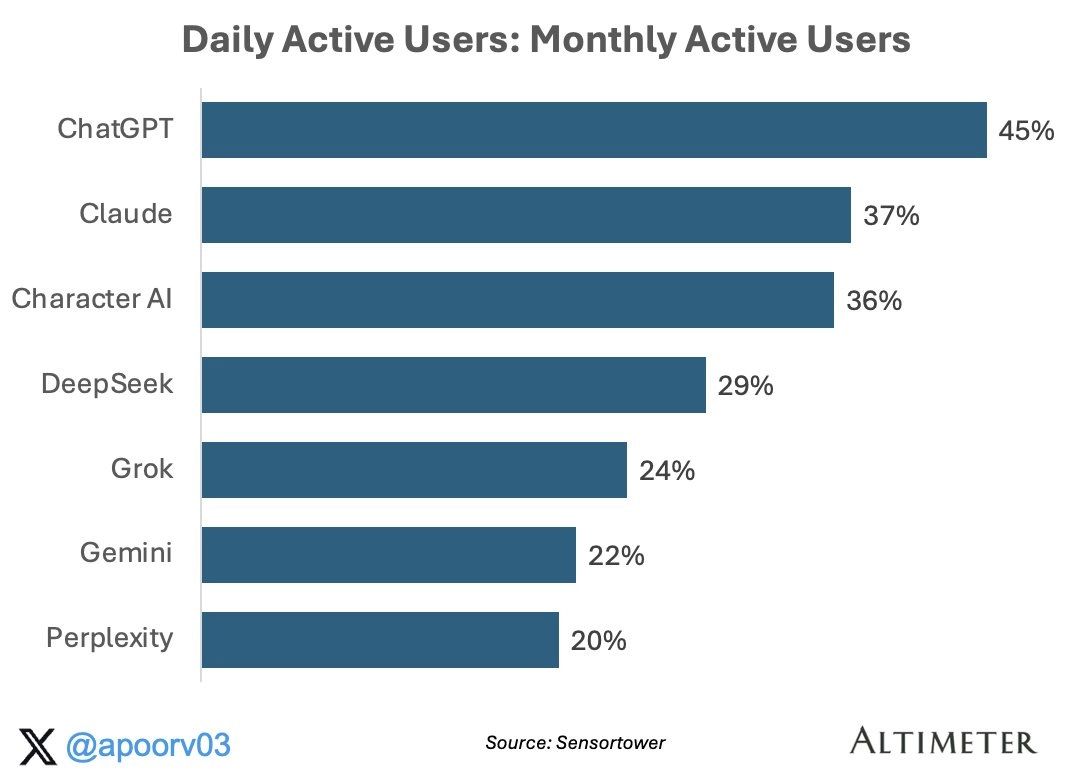

Apoorv Agrawal at Altimeter wrote about ChatGPT’s usage and retention patterns. - Apoorv Agrawal 1, Apoorv Agrawal 2

“Today, AI apps have crossed 1bn WAUs and ChatGPT alone accounts for 900m of that.” “Total AI app WAUs have gone from ~100M in January 2024 to over 1.2 billion in February 2026. That is a roughly 20x increase in two years. No app category in history has scaled this fast.”

“ChatGPT is the only AI app with both the installed base and new user momentum to become a core utility, like WhatsApp and Chrome are today.”

“ChatGPT is not just the largest AI app. It is also the stickiest. And it is getting stickier.”

“ChatGPT has better engagement than most enterprise apps (Slack, Gmail, Outlook) and matches the engagement levels of consumer staples like Facebook, Spotify, and X.”

“Three years ago, ChatGPT’s Week 4 retention was closer to 40%. It has climbed to 66% today, a roughly 25 percentage point gain. Most apps see retention set early and stay flat or decline as the user base matures and more casual users come in. ChatGPT has done the opposite: as its user base has grown 10x, retention has gotten better. The most likely explanation is product improvement. Each major release has given users a new reason to come back.”

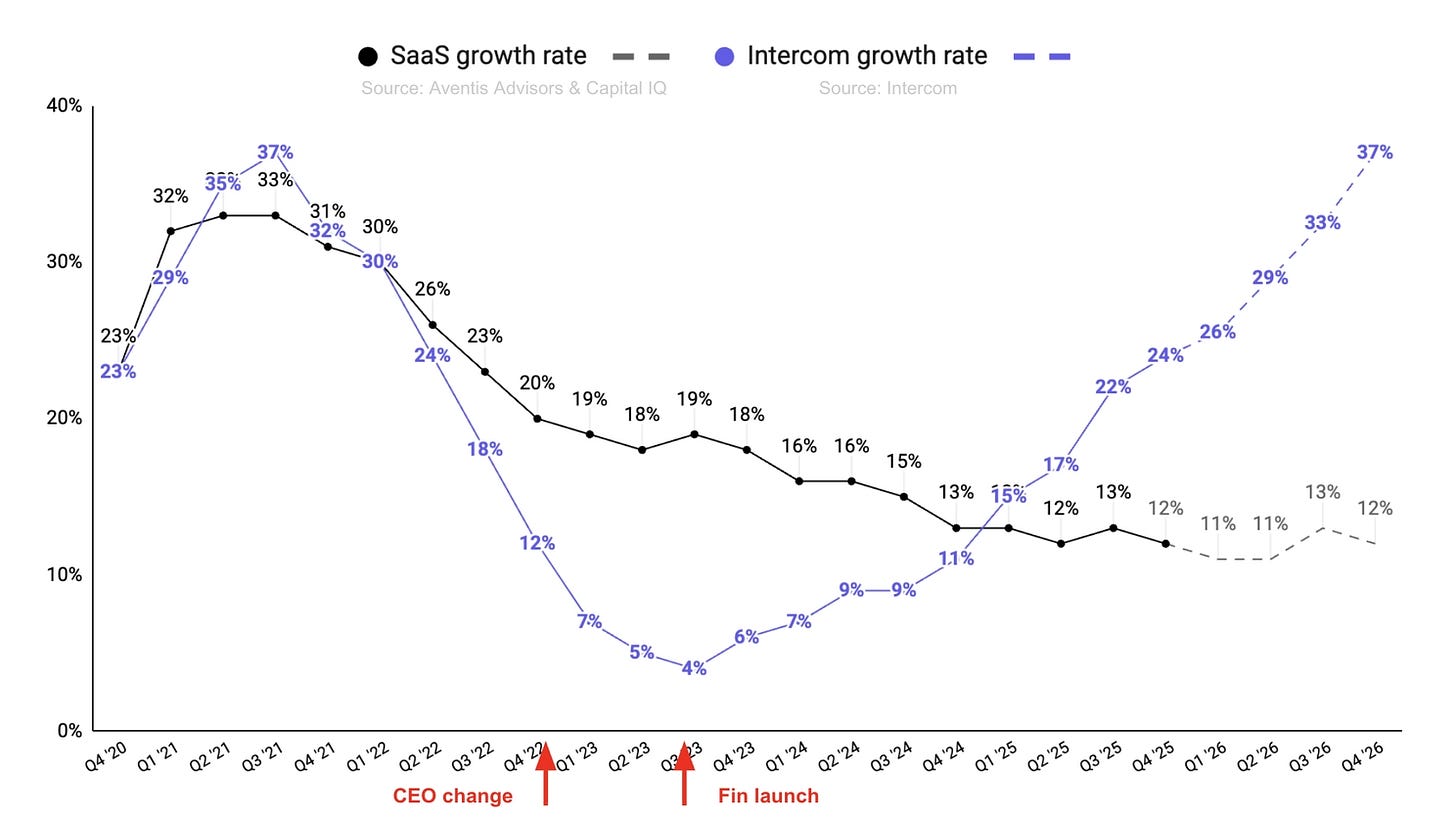

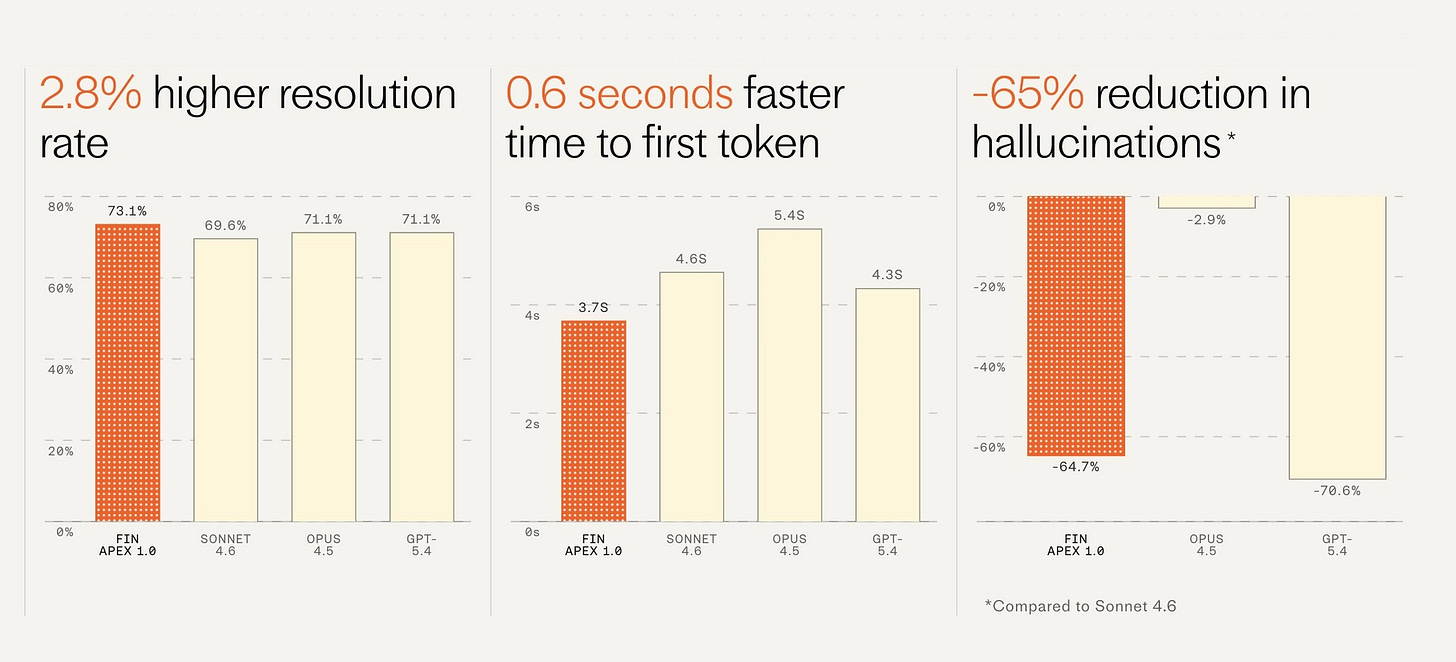

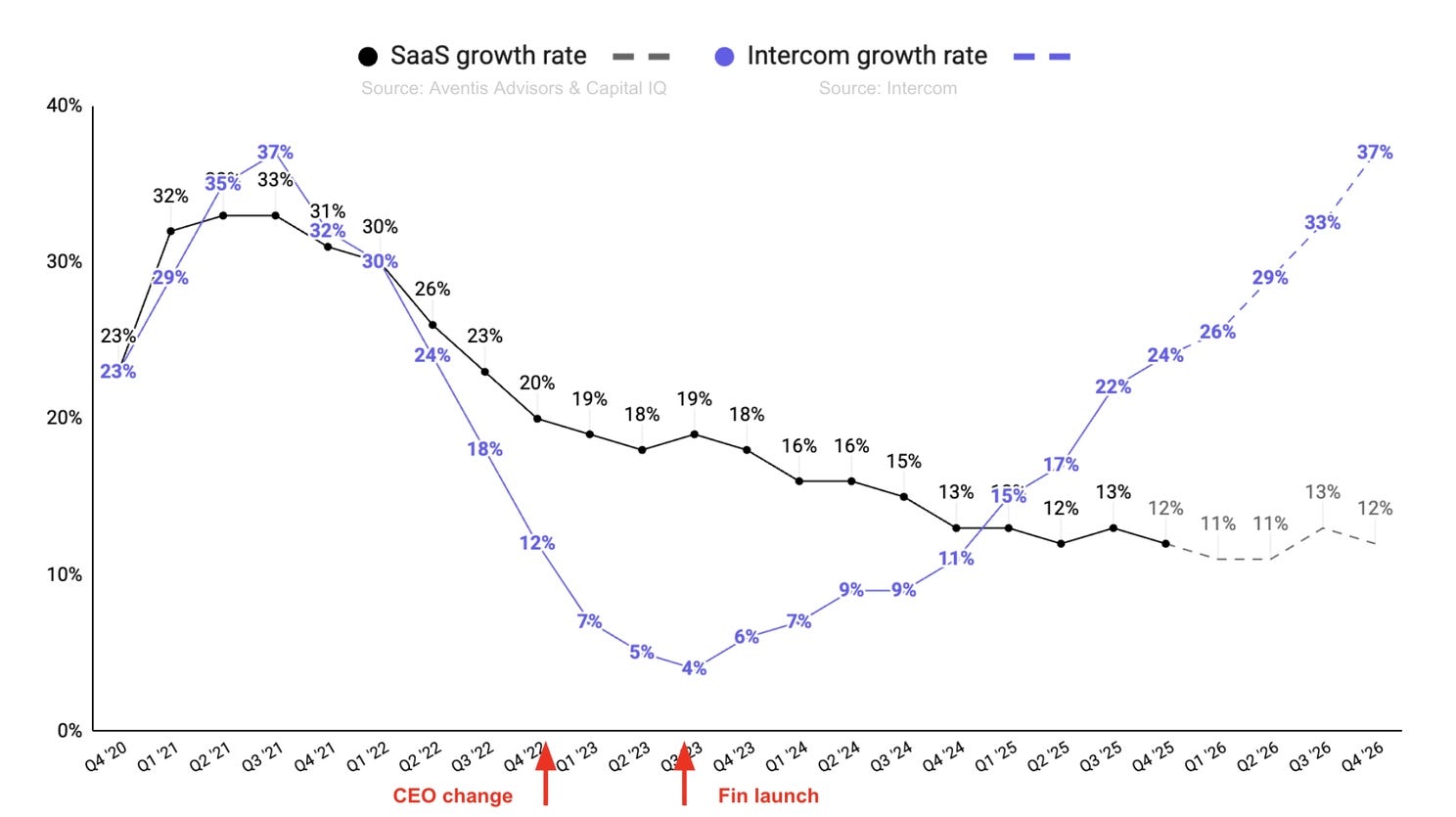

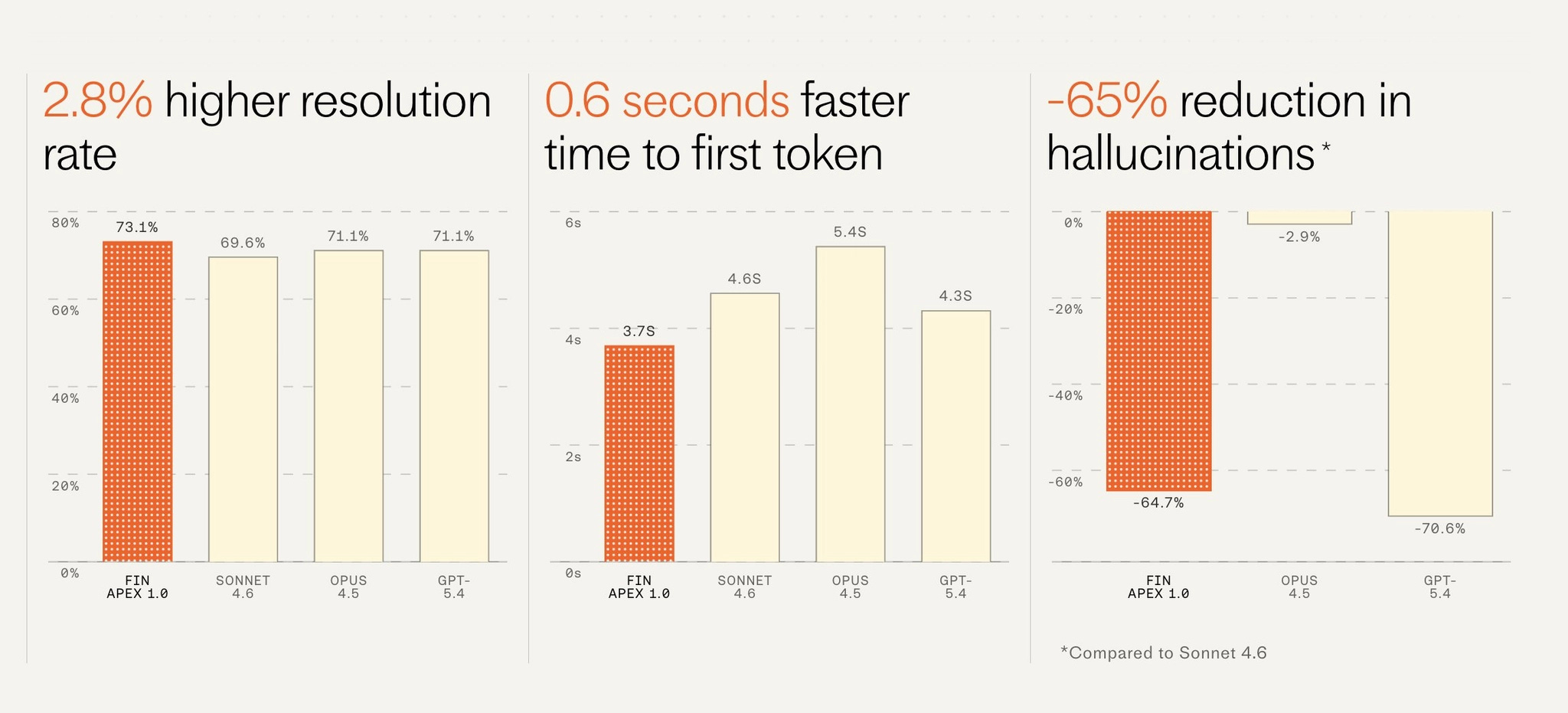

Intercom revived growth by embracing AI agents, killing its legacy SaaS model, changing pricing and culture, and accepting cannibalization. It also launched a custom model for its AI customer support agent that beats top general models on customer service across performance, speed, and cost. - Eoghan McCabe 1, Eoghan McCabe 2

“We did know that in the face of disruption, a force not new to tech in any way, the only way to have a place in the future is to destroy your past.”

“Three years ago, our future was looking pretty bleak. I jumped back into the CEO role after a two year hiatus while sick, when we were heading quickly towards negative growth.”

“We’re now at $400M ARR overall, with Fin about to pass $100M. But most remarkably, while growth rates amongst our peers have continued their decline, we’ve doubled our overall growth rate each year for the past two years, and are now on our way to being the fastest growing, large software company (per our knowledge), private or public, in the world. This is structural acceleration that comes from the aggregate of two businesses, one being the hypergrowth business Fin growing at ~3.5X and about to be half of our revenue early next year.”

“The tough pill you must swallow is that if you can’t become an agent company, your crud app business has a diminishing future.”

“We moved our R&D focus to be nearly 80% on Fin, while that business was still a single digit percent of our revenue.”

“We actively managed our entire customer base to a new, risky pricing model—we invented “outcome based pricing” that everyone in the agent space now talks about—that focused monetization on our helpdesk and agent combo, while reducing pricing for everything else, killing ~$60M ARR in the process.”

“The shift from on-prem to cloud wrecked many companies, but the change was not nearly as fast. And while it proved quite difficult for the previous generation to adapt quickly enough to keep up with my own, the shift in approach, skillset, go-to-market, and more was not nearly as dramatic. But, still, this shift is possible. Little, old, left-for-dead 15 year old Intercom did it. You can do it too!”

The Economist wrote on European tech’s current momentum driven by policy support, returning talents from the US and success stories in AI, deep-tech & defence. - The Economist

“In January, Lovable’s annualised recurring revenue hit $300m, up from $1m 14 months earlier.”

“Europe has long been a laggard in creating tech giants. Today Europe (ie, the European Union, Britain and Norway) is home to just six of the world’s 100 most valuable tech companies. America has 56; China, 16.”

“European enterprises are also “realising that they can’t afford to entirely depend on foreign providers”, says Arthur Mensch, the boss of Mistral, a French maker of AI models.”

“This month the commission is due to publish a plan to unify Europe’s segmented capital markets, which will help startups raise money.”

“Britain, France and Germany are tweaking rules to encourage pension funds to invest more in risky assets, such as young tech firms.”

“Mr Trump’s disdain for foreigners, and recent lay-offs by American tech giants, are driving talent to Europe. People working in Europe for American firms have also formed a talent reservoir. Data from Revelio Labs, a workplace-data firm, show the brain drain has reversed. Lovable, for one, has recruited executives from American software companies.”

“Fewer European firms are being sold to America. Dealogic, a data provider, notes that in 2011-13 American firms made 12% of acquisitions of European tech firms by number and 35% by value. In 2023-25 the shares were 9% and 17%.”

“Region’s established tech tycoons are helping youngsters make fortunes. Nikolay Storonsky, founder of Revolut, a fintech company, has backed Spiko, a French startup in the same sector, and Biorce, a Spanish medical-technology firm. Daniel Ek, Spotify’s founder, is a big investor in Helsing, a German defence-tech firm. Former staff of Klarna, a Swedish fintech star, have created more than 60 startups, according to Dealroom, another data provider, and Accel, a VC fund.”

“Mr Trump’s demand that Europe do more to defend itself is also spurring high-tech arms-making in a region that had little of it. In 2015-17 VC investment in European defence tech was barely 1% of North America’s. By 2023-25 that had risen to 6%. The International Institute for Strategic Studies, a think-tank, says that Europe’s defence spending rose by 42% from 2023 to 2025; America’s defence budget, though far bigger, was unchanged.”

“On February 25th the budget committee of Germany’s legislature called for “moderation” in defence spending and cut the expenditure on contracts with Helsing and Stark Defence, a rival.”

Entropy

**Saronic raised a $600m series C led by Elad Gil quadrupling its valuation to $4bn**. It’s a US defence startup building autonomous surface vessels. The round will fund the construction of Port Alpha, a next-generation shipyard designed to manufacture larger vessels. Saronic previously secured a c.$400m contract from the US MoD for its Corsair USV platform. - PR Newswire, Saronic

Travis Kalanick rebranded the company he launched after Uber from City Storage Systems to Atoms and is expanding its vision to create robots for the food, mining and transportation industries. - Om Malik, Bloomberg, Techcrunch, Atoms

“I left Uber in 2017 heartbroken. I had been torn away from an idea and a movement that I had poured my life into. I had lost my bearings as I found the world increasingly operating by the rules of perception not reality. It was only days after the death of my mother and the near death of my father in a boating accident when an investor decided to come out from the shadows and exploit this vulnerable moment to wrestle control of this idea away. I bled, but I did not perish. I got back up and fought my way back into the arena, back to my calling. Back to building.”

“I often get the question from entrepreneurs or executives, “What should I do next?” My answer has always been “become deeply self aware and when the right thing comes, you will know it. If you know yourself, your next thing, your new idea, your work soulmate will reveal itself.” When I told my friends, family and colleagues about my plans for what was next, they were really excited that I was “coming back.” The thing is, I never left.”

“Kalanick is remaking his real estate company, City Storage Systems, which owns ghost-kitchen operator CloudKitchens, and renaming it Atoms, according to a manifesto posted on the new company’s website. In addition to its work on food, Los Angeles-based Atoms is expanding into robotics technology for mining and automotive transport.”

“Kalanick wrote on the Atoms website that the company will make “specialized robots with productive jobs that bring abundance to their owners and society at large.” That will include “infrastructure for better food,” he wrote, as well as “more productive mines to power Earth’s industries” in addition to “wheelbase for robots” in transportation.”

“It was good to see him share his very clear, coherent and convincing vision of the physical world and how AI and robotics dovetail with that world.”

“At Uber, Kalanick consistently framed external forces such as regulators, competitors, the press, and board members as the problem. The company’s internal failures were always someone else’s move on the chess board.” “That pattern held. The company, and by extension Travis, was always being persecuted by people who didn’t understand what it was trying to do. The mission was always too important for ordinary rules to apply.”

“The Atoms manifesto is pretty much the same playbook. The unnamed investor, though everyone knows who it is, who timed his power grab during a family tragedy becomes the defining event of his departure. Gone are the issues and problems at Uber.”

“The second real argument is about specialized versus generalized robots. The humanoid is for bespoke, low-volume, human-designed spaces. The specialized machine is for industrial scale. This distinction matters, and not enough people covering robotics are making it clearly.”

“City Storage Systems, the company Kalanick has been running quietly since being pushed out of Uber, is being renamed Atoms. It is going after three major verticals: food, mining, and transport robotics.”

“The coverage of Atoms has largely worked exactly as designed. The vision is treated as the news. The rebranding is treated as a launch. The Horatio Alger story, knocked down, wandered, returned stronger, is irresistible to a media world that rewards narrative over nuance and speed over depth. You gotta fill airtime and make people buy your subscriptions.”

John Collison interviewed Tarek Mansour and Luana Lopes Lara at Kalshi to discuss prediction markets. - Cheeky Pint

Kalshi spent three years pre-revenue navigating CFTC approval before launching in 2022. “Financial services or healthcare, I think you can’t ask for forgiveness... we thought the biggest question to be answered was not, ‘Is this going to grow?’ It was ‘Can we do this legally in the US?’”

Kalshi sued its own regulator to bring elections to its prediction market. The CFTC pocket-vetoed election markets twice (end of ‘22, end of ‘23). Kalshi won because the CFTC can only block a contract if it falls within specific prohibited categories (war, terrorism, assassination). Elections didn’t fit.

Prediction markets have existed intellectually since the 1950s. The difference now is the pain is acute. “There’s a meaningful and accelerating rise of distrust in traditional sources of information. And so, you need a new one... the incentive structure for a prediction market is truth.” Critically, 80% of users are just consuming information — checking odds, not necessarily trading. The product solves an information problem first, a trading problem second.

$10.4bn in volumes in Feb. 26, 11x in 6 months.

Kalshi is a true marketplace with compounding network effects: more liquidity retains users, retains users attracts market makers, market makers deepen liquidity. The three drivers reinforce each other.

The product roadmap is a four-variable problem: breadth, market structure, margin, liquidity.

Breadth of markets (compute, insurance, collectibles)

Market structures (binary → futures, swaps, options)

Margin systems (currently broken — you tie up 100% capital upfront)

Liquidity

Current margin system is broken for certain markets (e.g. hurricane insurance — it makes no capital sense to sell those contracts today). Fixing margin unlocks parametric insurance, compute futures, and institutional flow.

Kalshi argues to be structurally different from sportsbooks. Sportsbooks make money on losers. They give bonuses to losing customers to hook them back. Kalshi makes money on transaction fees. They want winners as winners make markets accurate.

Unitree is going public in China. Founded in 2016, Unitree is building the “DJI of robots” producing both humanoid and quadruped robots. - Rui Ma

“Unitree shipped over 5,500 units last year, occupying 32.4% of the global humanoid market.”

Unitree generated $248m in revenues in 2025 (growing 335% YoY) and $42m in net profit (17% profit margin).

Unitree is vertically integrated (producing motors, control systems & hardware), benefits from Chinese hardware supply chain enabling for fast iterations and provides prices that are very hard to compete for Western counterparts.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋