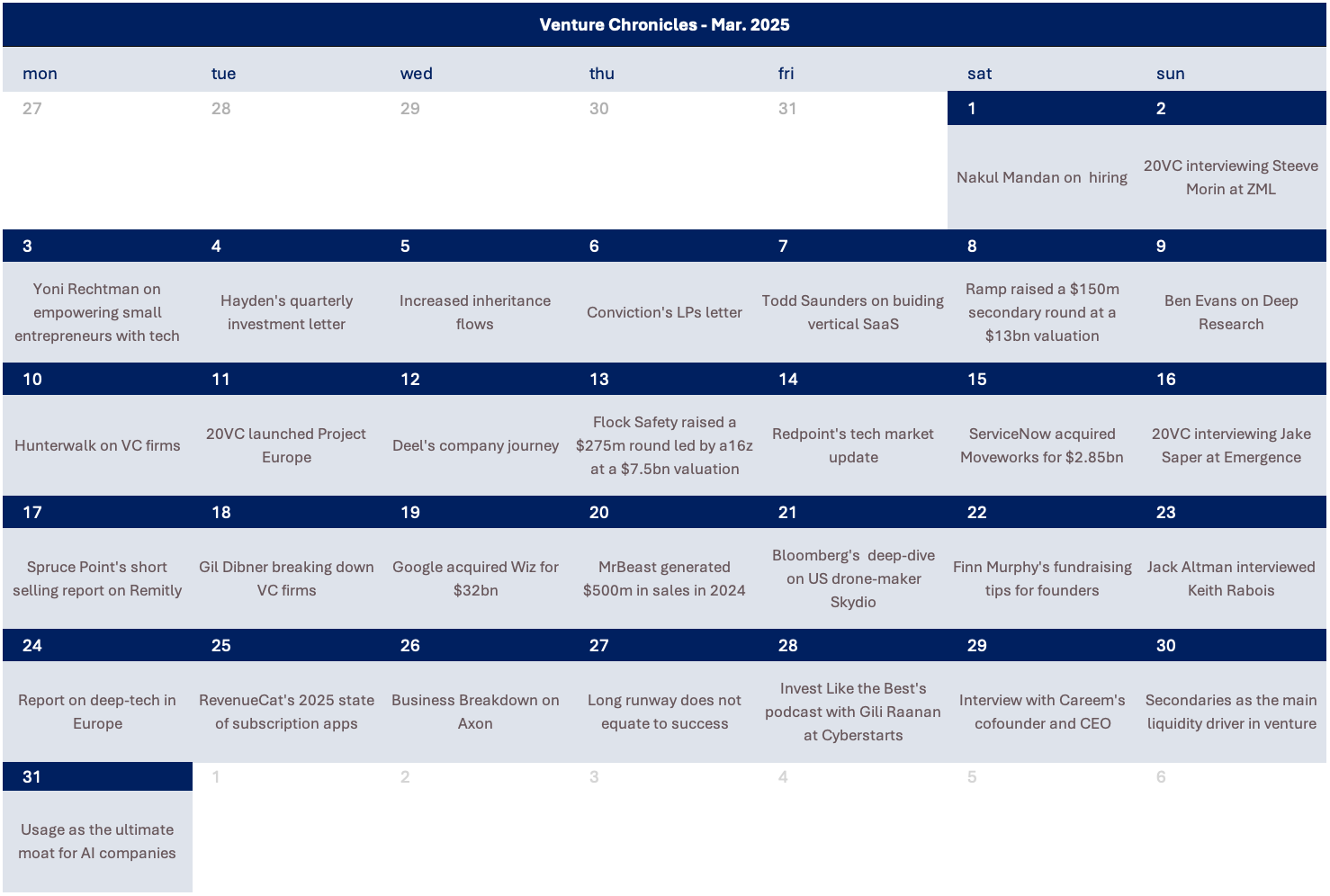

📖 Venture Chronicles - March 2025

Overlooked #195

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of March.

Saturday, Mar. 1st: Nakul Mandan wrote about hiring, arguing that the best founders are obsessed with finding and recruiting exceptional talent capable of having a transformative impact on their company. - Nakul Mandan

“In every team, a few players disproportionately move the needle. Your job as a founder is to stack your team with as many of these outliers as possible, knowing they’ll contribute 10x the value of an average hire.”

“There’s often not a deep internalization that good is the enemy of great. There are founders and execs who understand this, and there are founders and execs who simply don’t. The reality is that if your recruiting process and mindset is geared towards hiring good enough, you’re going to end up with a bunch of mediocre players on your team.”

“The high quality candidates are out there in the market, but to get in front of them, you’ll have to reach out to enough of them, you’ll have to pound the pavement in terms of getting intros to the best people you and your extended networks can get you.”

“The founders who build legendary companies internalize the power law of recruiting - they understand that a handful of hires will define the company’s culture, standard of performance and overall trajectory. They don’t settle. They don’t treat recruiting as a side task. They obsess over it. If you want to build something enduring, you have to become exceptional at recruiting. That means relentlessly sourcing, vetting, closing, and course-correcting. The founders who commit to this mindset dramatically increase their odds of success.”

Sunday, Mar. 2nd: Harry interviewed Steeve Morin who is the cofounder and CEO at ZML which is a AI inference stack allowing the deployment of AI models across various hardware platforms. - 20VC

“ZML is a ML framework that runs any models on any hardware uh and it does so without compromise.”

“Models now are not the right abstractions. If you look at closed source models, they're not really models they're more like backend. You’re not talking to a model but to a constellation of backends that produces a response.”

“You can get an order of magnitude more efficiency depending on the hardware you run.”

Today, companies are not switching to other hardware providers mostly because they are tied to the PyTorch/Cuda ecosystem. PyTorch is the ML framework used by people to train model. It was very much built on Cuda which is Nvidia’s software. PyTorch runs on other hardware but works not as well because of multiple small details.

Most GPUs in the market are Nvidia GPUs because all the stakeholders in AI are used to Nvidia’s ecosystem. There is a self perpetuating loop even if Nvidia does not have the most efficient hardware on all dimensions and the most efficient software.

What are the fundamental differences in terms of infrastructure needs between training and inference?

In training, more is better. Training is research. The recipe for success is speed of iterations. In inference, less is better. Inference is production.

If you do production, you want to avoid inter-connect between machines together.

“If you run around millions of instances of a model you cannot you know hack your way to do that.”

“Training on first principle is actually two paths forward and backward. Inference is running only the forward path.” Companies are trying to specialise because at scale duct tape for inference does not really work out.

“It's a problem that's growing because a lot of people are coming on a market with needs for inference. It wasn't the case you know a year and a half ago.”

“If you deploy inference, the number one thing that will get you is autoscaling. As your systems get more and more loaded, you want to provision them as you scale to avoid massive costs.” “You want to provision compute as you grow. You want to do it up and you want to do down.” It’s a classical problem in engineering but in AI we did not have the issue before today.

All chipmakers beyond Nvidia have a GTM problem because it’s very hard for companies today to maintain multiple AI stacks at the same time. The switching costs are super high from one provider to another and to make it worth to use a new hardware provider, you have to buy a lot of chips.

The right approach is to make the buy-in is zero. If it’s the case, you just buy what is best today. It means that you can freely switch compute from a hardware provider to another. ZML does this working with hardware providers to support their chips. You should only work with what is good at the moment and you can get into incremental gains. Today, it does not work and even if you have a 7x improvement on any metric, you won’t do it because the lock-in is too high.

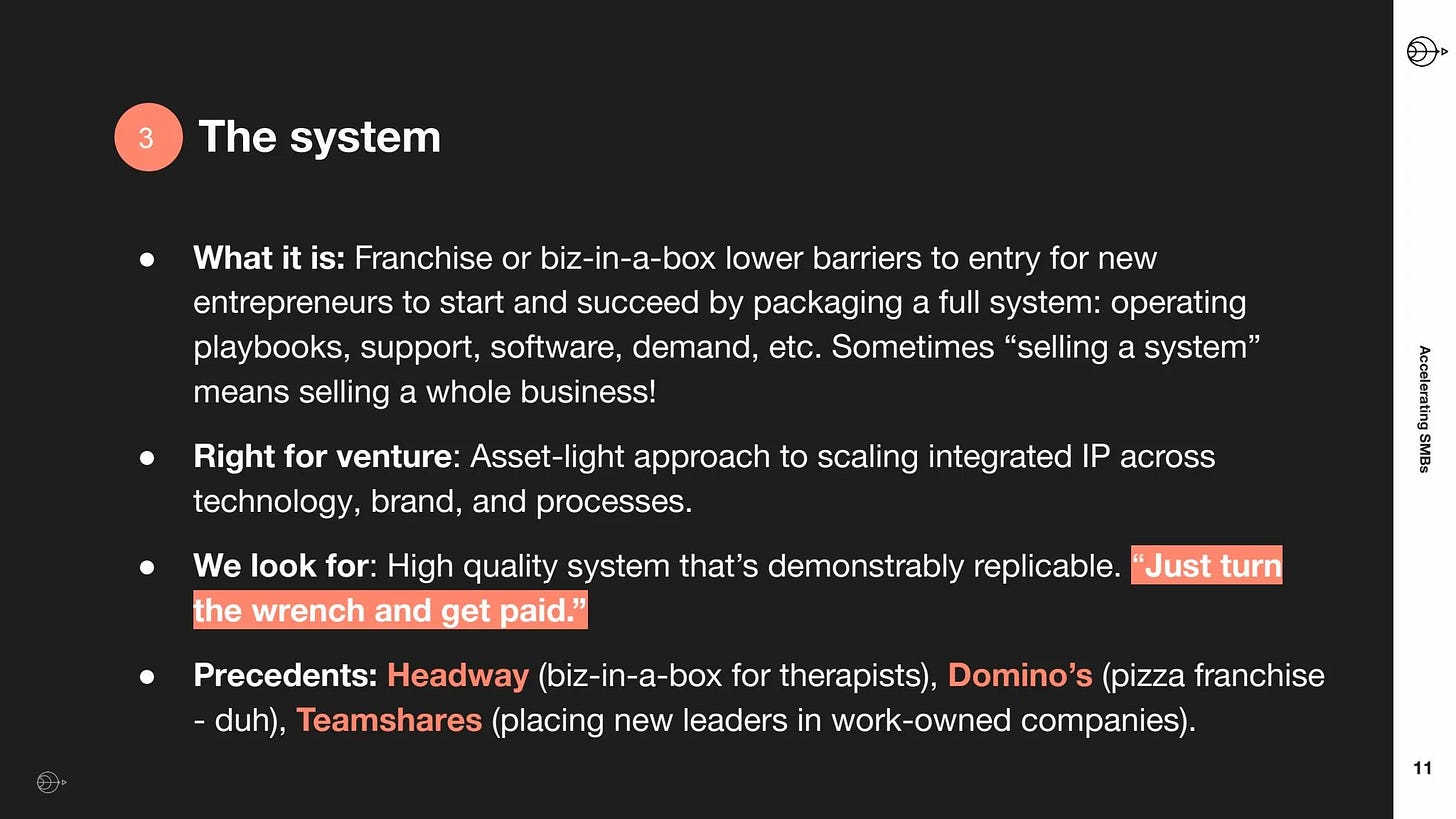

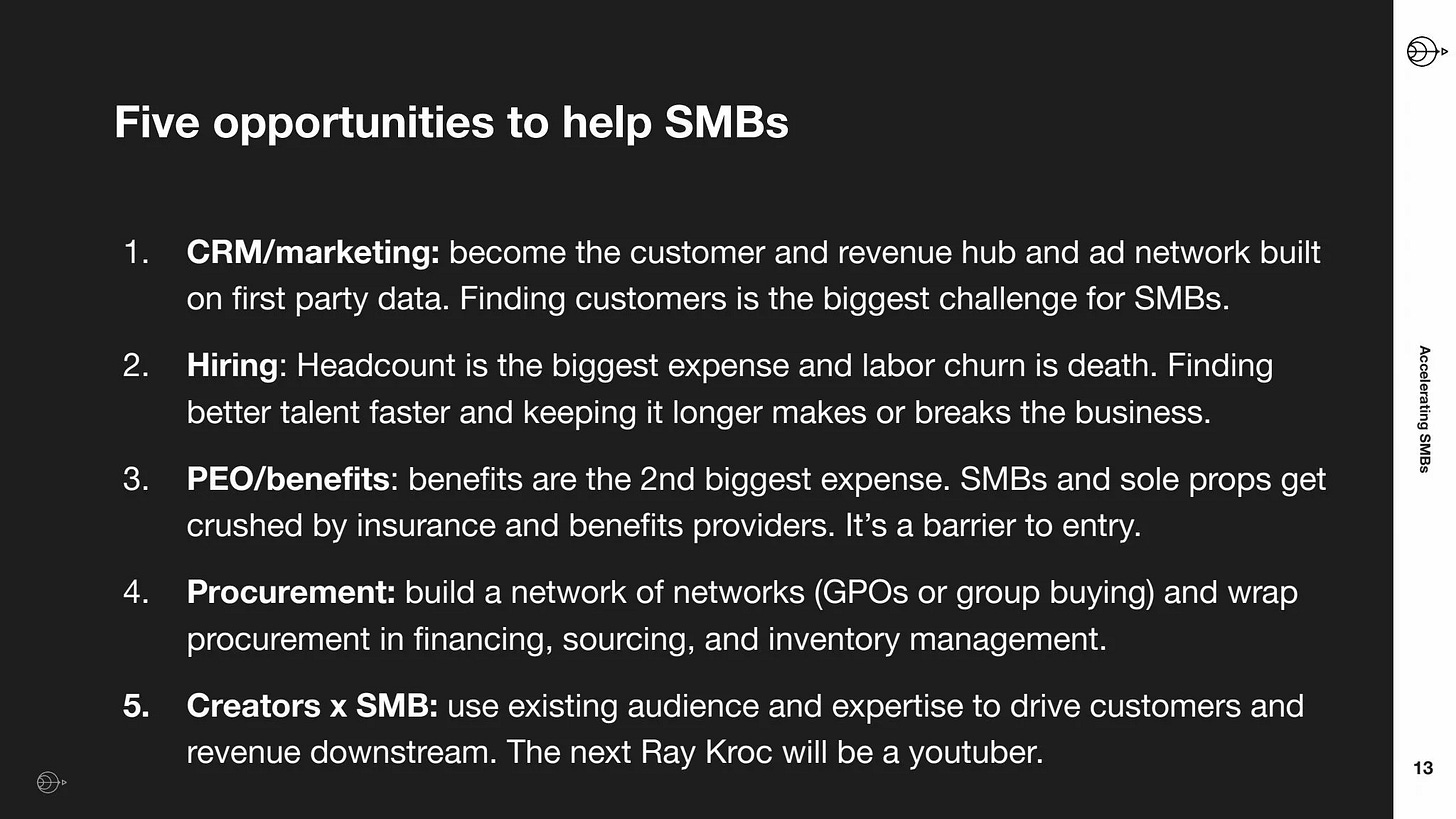

Monday, Mar. 3rd: Yoni Rechtman published a presentation on platforms empowering entrepreneurs in the real economy with 3 different models: vertical software, marketplaces/GPOs and franchises/business-in-a-box. - Yoni Rechtman

The entrepreneurial culture is shifting, with real-world jobs and SMBs gaining high status. It opens opportunities in venture to make money by helping people become entrepreneurs and build real businesses.

Private equity is negatively impacting small businesses by consolidating supply, squeezing customers, breaking the promise of self-reliance, and cutting talent off from wealth creation.

Tuesday, Mar. 4th: Hayden Capital published its quarterly investment letter. - Hayden

“The market began recognizing what we’ve been calling for a while – that Sea Ltd will be able to out-compete its rivals and capture the majority of ecommerce spend in Southeast Asia. And that Applovin’s true value lies in its advertising network (i.e. the algorithm), which is competitively advantaged by its breadth of data.”

““We’ve been wading into investments in earlier-stage businesses and relatively recent IPOs… Some may be wondering, have we completely lost our minds? Obviously, the answer is no instead, this segment of the market attracts us precisely because other investors have this fear, resulting in it becoming one of the most inefficient spots within our investment universe today.”

“Commonly, these businesses have a “mature”, profitable, existing business line, where all the profits are being reinvested into a “start-up” division or geography – thus depressing overall profitability or even pushing it into company-wide losses. The market tends to price these situations at the lower “overall” level of profitability, and even further punishing the valuation multiple given what’s viewed as risky capital allocation. But the market fails to appreciate that these are also distinct business lines. Assuming management is rational, the startup division (and its associated losses) can be easily shut down. And when that happens, the company’s “mature” business alone is probably worth equal or more than the existing stock price. This is the “worst case” / “lower boundary” scenario shown in the second chart above, and provides our partners with downside protection.”

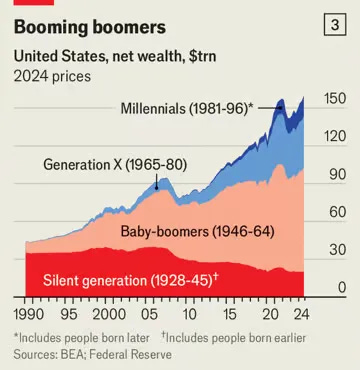

Wednesday, Mar. 5th: Inheritance flows are increasing, now averaging 10% of GDP across wealthy nations. This trend is driven by growing wealth, changing demographics, and slower economic growth. Baby boomers, who accumulated significant wealth, are now passing it on to fewer heirs. Inheritance taxes have decreased, allowing more wealth to be transferred. - The Economist

“So The Economist has gathered academic estimates on the annual “inheritance flow”—the value of what people pass on to heirs in art, cash, properties and the like—for a range of countries. In 1900 inheritances were worth over 20% of GDP in some countries, as people passed on vast stock portfolios and estates. The value of inheritances then fell in the 20th century, before more recently roaring back. By the end of the 2010s inheritances were worth, on average, 10% of GDP. This year people across the rich world will inherit on the order of $6trn.”

“In 2023, 53 people became billionaires by inheriting money, not far short of the 84 who did so by working.”

“Falling inheritance taxes also increase the share of a bequest that an heir can keep. In the early 20th century, revenues from death duties accounted for a sizeable chunk of the total tax take in America and Britain. But in the latter part of the century, politicians turned against the taxes.”

“The rise of the inheritocracy reflects three factors: increasing wealth, changing demography and slower economic growth.”

“The second factor is demography. Baby-boomers have soaked up wealth, having come of age just at the point when house prices and stockmarkets started soaring. Germans aged over 65, who make up a fifth of the population, own a third of the country’s wealth. American baby-boomers, also a fifth of their country’s population, own half of its net wealth.”

“In the 21st century, the incomes of the top 1% of French inheritors are once again higher than those of the top 1% of workers.”

Thursday, Mar. 6th: I read Conviction’s latest letter to its LPs. - Conviction

“Our mission remains the same. We are the best business partners to the most important next-generation companies. As 2025 begins, our founding premise — that AI is a foundational innovation which changes the character of the technology industry — continues to hold.”

“Models are increasingly multimodal, going beyond text sequences to understanding and generating useful images, voice and video. This is already powering new applications in content creation (e.g. HeyGen, Pika), customer experience (e.g. Sierra, Decagon), and healthcare (e.g. New Lantern). We expect these capabilities to impact ecommerce/retail, advertising, social media, entertainment and gaming.”

“We have been surprised by the depth of the capital markets in funding the heavy investments in AI training to date, the aggressive participation of sovereigns and strategics, and even the rapid creation of large new financial vehicles to fund this effort. Unless investors become warier of diminishing returns and more competition, we would bet capital continues to fund the existing oligopoly.”

“In terms of aggregate capital deployment and price sensitivity, the market seems to have returned to 2021 territory. Upon further inspection, much of this investment has been concentrated into the labs, and a small number of highly pedigreed teams and growth-stage AI application companies.”

“Eating the service elephant. We are especially compelled by founders that demonstrate both unreasonable long-term ambition, often with the goal of building an “autopilot” that displaces work, and short-term practicality, in starting with a quickly-saleable “copilot” that assists human workers. In the cases of Harvey (legal), Latent (pharmacy operations), Collate (life sciences documentation) or Town (SMB tax), we’re backing founders we believe have intense curiosity for understanding the elephant, and good instincts for how to pick a juicy first bite and map a path through.”

“These interface changes have the potential to revolutionize the enterprise software world. Many of the pillars of enterprise software can be described as forms and workflow on top of a structured database. What happens when we no longer need to explicitly structure the data and the forms and workflow can be automatically generated and personalized?”

Friday, Mar. 7th: Todd Saunders shared advice for founders building vertical software companies. - Todd Saunders

3 key ingredients: (i) pick a niche where businesses are underserved, (ii) win trust before you sell & build a community while you’re doing it and (iii) make your product & service both irreplaceable.

“Win trust before you sell and build a community while you are doing it.” “Consistently communicate a clear and relatable message through both words and actions in the industry.” “Show up at industry events and put real faces to real names.”

“The goal isn’t just to sell software, it’s to embed yourself so deeply into the industry that customers can’t imagine operating without your product, and your people.”

Saturday, Mar. 8th: Ramp raised a $150m secondary round at a $13bn valuation from GIC, Khosla, Thrive, Stripes and GC who purchased shares from employees and early investors. It was previously valued at $7.65bn valuation in Apr. 2024. It started in 2019 with a corporate card but has become a broader financial platform including expense management, bill payments, procurement, travel and treasury. It serves 30k US customers (50% of them are using at least 2 products), generates $700m in ARR (vs. $300m in Aug. 2023) and processes $55bn in annualised payments (vs. $10bn in Jan. 2023). - FT, Pymnts, Techcrunch

Sunday, Mar. 9th: Benedict Evans criticised OpenAI’s Deep Research tool, highlighting its limitations in delivering accurate data. - Ben Evans

“LLMs are not databases: they do not do precise, deterministic, predictable data retrieval, and it’s irrelevant to test them as though they could.”

“We’re asking for a deterministic answer from a probabilistic question, and there it looks like the model really is failing on its own terms.”

“Are you telling me that today’s model gets this table 85% right and the next version will get it 85.5 or 91% correct? That doesn’t help me. If there are mistakes in the table, it doesn’t matter how many there are - I can’t trust it.”

“Deep Research will be mostly **right, but only mostly.”

“OpenAI and all the other foundation model labs have no moat or defensibility except access to capital, they don’t have product-market fit outside of coding and marketing, and they don’t really have products either, just text boxes - and APIs for other people to build products. Deep Research is one attempt amongst many both to create a product with some stickiness and to instantiate a use case.”

Monday, Mar. 10th: Hunterwalk categorizes new VC firms as “traditional but better”—refining familiar methods with unique talent—or “different & excellent”, which take standout, innovative approaches. - Hunterwalk

“VCs with identities, backgrounds and networks which are additive to the venture ecosystem to better serve founders, so while the structure of the playbook is duplicative, the people running the playbook aren’t – and that’s the key.”

“VC firms which aren’t carbon copies of anything else out there. In fact, they probably aren’t generally replicable. But they take advantage of their unique founding partners, very often the type of people who would reject – or not get hired by – ‘traditional VCs.’”

Tuesday, Mar. 11th: Alongside P9 and Adjacent, 20VC launched Project Europe. We gathered 170+ of the best European founders to back the next generation of European founders with a $10m fund. We will write €200k cheques into 18-25 years olds engineers building tech companies. - FT, The Economist

“There is a doom loop around Europe and we need to change that. The brain drain to the US is very real and it’s going to really damage the future of Europe unless something changes.”

“When we think about building the next generation of great European founders, we have to start with youth.”

“For decades, America’s immense investment in research lured Europe’s best scientific talent across the Atlantic. European policymakers now see an opportunity to reverse the flow.”

“Giving refuge to researchers from America is part of Europe’s new urgency about boosting science.”

“The EU spends about 2% of GDP on research and development, barely half America’s 3.6%. Most of the gap is explained by lower R&D spending by businesses. That calls for deeper capital markets to provide risk capital for innovative firms, and a more unified and less regulated market to allow them to scale their products. Project Europe, an initiative of over 150 European tech founders, helps talented young people in Europe who want to solve technical problems and start businesses. “Europe has all the ingredients, but we fail to bundle them,” says Matthias Knecht, one of the founders. He sees a deep frustration “that Europe doesn’t get its act together”.”

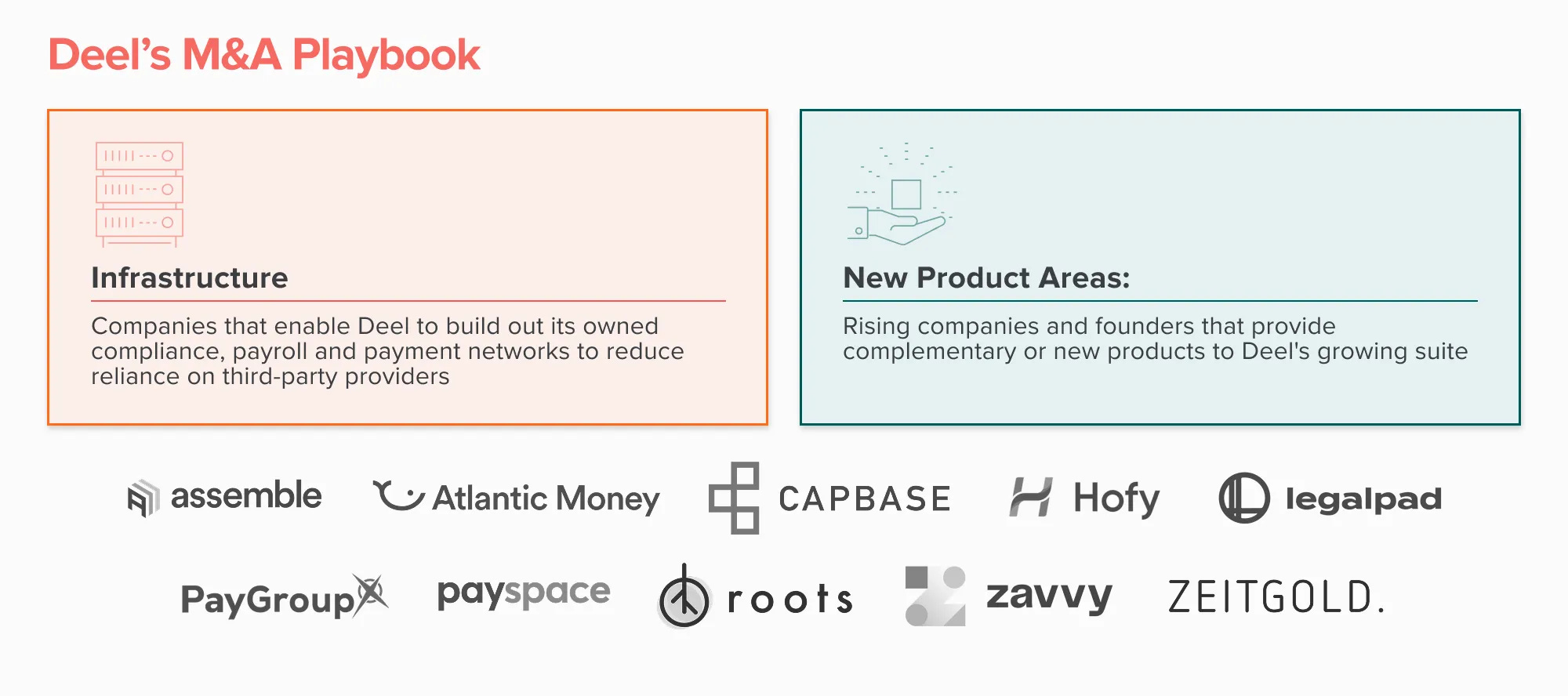

Wednesday, Mar. 12th: Asnish Acharya at a16z wrote a great post on Deel’s company journey highlighting 3 key success factors: vertical integration, unbundled platform to have multiple product wedges and M&A at the core. - a16z

“Anyone qualified should be able to work at any company without burdensome hoops and delay, no matter their location. With ambitions to create the universal payroll rails of the world Deel is working to become a foundational layer for global businesses.”

“Since being founded in 2019, the company has grown from a simple EOR business to offer horizontally and vertically integrated global payroll, HR, finance, compliance, mobility, and IT support wrapped in one platform: a global operating system for work.”

“In 2019, the pair started Deel as a global contractor platform, facilitating all payments for international workers in one place. Their employer of record (EOR) service — initially an experiment launched in Canada and the UK at the request of a client — allowed companies to quickly and compliantly hire workers around the world, without setting up their own local entities. As workforces became increasingly distributed during COVID, the demand for Deel’s first prodcut exploded.”

“This realization — that vertical integration could unlock a truly differentiated product — is something numerous successful startups have learned over time. This model results in a far more responsive and reliable product for customers.” “In 2024, for example, Klarna replaced Workday with Deel’s HRIS and payroll service, which provides a single control center for its global workforce.”

“Many of Deel’s 36,000+ customers — Shopify, Klarna, Hermès, Coinbase, and Reddit among them — have originally been inbound customers for one IC or one EOR, then expanded their business over time.”

“Deel’s services are unbundled by default. In contrast, many SaaS platforms and enterprise software suites — including Salesforce and Workday — often bundle their services or impose high costs for accessing individual modules or product features. Customers often come to Deel when they have a particular problem that needs to be solved, whether a task seemingly small, but essential, like obtaining a single O-1 visa for an executive, or complex, like replacing their entire global payroll operation. Unlike most companies that rely on a single entry point to land customers before cross-selling to additional products, Deel has multiple, modular wedges — distinct entry points that serve as natural on-ramps for customers across different needs. This flexibility allows Deel to meet customers where they are, whether through EOR, contractor payments, mobility services, or other solutions, rather than forcing them into a predefined sales motion.”

“As M&A has become a more important part of the business, Deel has operationalized and streamlined the process; one internal team is focused specifically on people integration, pre- and post-acquisition.”

Thursday, Mar. 13th: Flock Safety raised a $275m round led by a16z at a $7.5bn valuation. - Bedrock, Flock, Techcrunch, Reuters

“Flock makes computer vision-enabled video surveillance technology used by law enforcement as well as businesses, property management companies, and so on. It’s best known for its automatic license plate recognition tech, but Flock also makes gunshot detection tech marketed to schools, and recently acquired public safety drone company Aerodome.”

“Flock plans to launch U.S.-manufactured drones in 2025, as it builds out a 100,000-square-foot manufacturing facility in Georgia.”

“It now serves over 4,800 law enforcement agencies and nearly 1,000 businesses across major retailers and healthcare systems. Enterprise businesses account for about 30% of its revenue.”

“After we failed to mobilize fast enough to be involved in Flock’s Series A fundraise, Geoff decided to hop on a plane to Atlanta with a singular mission: convince Garrett to raise more capital from Bedrock.” “He pivoted from being pitched on Flock to pitching Flock on raising more capital from Bedrock right away. It was a longshot; they really didn’t need the money. But we were persistent, and Flock ultimately agreed to raise a $10 million Series A-1 round led by Bedrock at a then ‘totally insane’ $60 million valuation; a near 3X valuation step-up to the Series A that had closed just a few months earlier.”

“Today, Flock Safety is valued at 125x Bedrock’s entry valuation, and has grown from effectively pre revenue when we initially invested to over $300m in ARR today [growing 70% YoY]. Along the way, we have invested over $164 million into the Company across multiple Bedrock funds and multiple Flock financing rounds.”

“Flock has set itself apart by pioneering a specific and proprietary playbook for engaging local, municipal, and state level government agencies and organizations. This innovative approach has enabled the Company to serve unique local market verticals that no other private technology company has accessed at scale.”

“Flock’s systems are natively built in the cloud – and Flock has embraced an open ecosystem approach – so they have been able to knock down the barrier of inter-jurisdictional data sharing.”

“Flock has raised less than $1 billion in total private primary financing to reach its current extraordinary scale – despite having a significant hardware component (and hardware in general tends to be more capital intensive).”

Friday, Mar. 14th: Redpoint published a general tech market update looking both at the public and private markets. - Redpoint

Saturday, Mar. 15th: ServiceNow acquired Moveworks for $2.85bn in a combination of cash and stock. Moveworks is an AI platform to find answer and automate tasks across different systems used by companies. It also a platform to build and run AI agents. - ServiceNow, Fortune, Techcrunch

In Sep. 2024, Moveworks disclosed to have passed the $100m ARR threshold. Moveworks was cofounded in 2016. It released a product in 2019 for enterprise customers to automate high level IT support before expanding into other functions (HR, finance, facility management). It raised $315m in funding with a last round at a $2.1bn valuation in 2021.

“The acquisition will combine ServiceNow’s agentic AI and automation strengths with Moveworks’ front‑end AI assistant and enterprise search technology to unlock new experiences for every employee for every corner of the business.”

“ServiceNow has nearly 1,000 AI customers and has surpassed $200m in ACV for its Pro Plus AI solution as of Dec. 31, 2024.”

“ServiceNow is already one of Moveworks’ more than 100 technology integrations, and the companies have approximately 250 mutual customers.”

“In initial integration phases, ServiceNow and Moveworks will deliver a unified, end‑to‑end search and self‑service experience for all employee requestors across every workflow – all from a single entry point. As domain specific AI agents proliferate to accomplish tasks across HR, CRM, finance, IT, and more, ServiceNow’s powerful agent orchestration capabilities will connect, analyze and manage AI agents, ensuring agents work in harmony across tasks, systems, and departments.”

“While ServiceNow’s AI agents primarily automate specific back-end tasks, Moveworks had built an “elegant front-end” AI assistant that can perform a wide range of different tasks.”

“Enterprise search tools have also emerged as an important new battleground among software companies in the AI age because finding the right data from within a company’s knowledge base is critical to both “retrieval augmented generation” and and also to having AI agents that can accurately and effectively perform tasks.”

“ServiceNow knows it can’t just be a system of record anymore. The future belongs to software that’s AI-native, not just AI-enhanced. Enterprises don’t just want workflow automation; they want intelligent automation. Moveworks gives ServiceNow a serious AI leg up.” - Krishna Mehra

Sunday, Mar. 16th: Harry interviewed Jake Saper who is GP at Emergence. - 20VC

Zoom’s investment in 2014: Zoom was doing $2m in ARR with extremely strong product led growth metrics. Emergence wrote a $20m ticket at $200m valuation out of a $250m fund. It was competitive because of the early growth and the fact that the company was profitable. Eric at Zoom picked Emergence because Emergence committed to help Zoom to build a proper enterprise sales motion on top of his product led growth motion. Zoom generated $2.5bn in proceeds for a fund which generated 16x in DPI.

“I don't think any venture firm makes all their money on having a prepared mind. I do think that having a prepared mind can help you to get to conviction sooner and faster than others.” “We broadly develop prepared minds from the portfolio company investments we make. For example, what is happening at Chorus that informs a broader thesis on voice AI beyond its specific sales use case? How can these insights shape our broader investment strategy?”

“Most private equity outcomes don't generate incredible returns for the VCs. Most transactions done by PE funds are done at 3-5x ARR. So you can get your money back or get 2-3x returns which are not meaningful for a fund. Salesloft was an exception acquired for 20x ARR at a $2.5bn valuation.”

“Just because something breaks out right after you invest or early on doesn’t guarantee it will succeed. A breakout can indicate market pull, which is crucial, but it doesn’t necessarily mean the company will endure.”

“You want people desperate for your product. Otherwise, it’a nice to have. It’s not necessarily a desperate problem if your buyer hasn’t tried to hack together a solution, purchased an inferior product, or spent countless hours dealing with it themselves.” “The things I want to hear in customer calls are things like “if my boss stopped paying for this I'd quit” or “if my boss stopped paying for this I'd pay for this out of pocket”.”

“It is still possible to be non-consensus, right, and get a good price. However, there are increasingly more consensus deals, and you want to have exposure to both.”

At Emergence, 9/10 early stage investments have raised a follow up round. 5/10 have raised at a valuation above $1bn. 1/10 have gone public.

“There are certain founders who aren't looking for the product we sell. We sell a low volume, high-touch product. There are some founders who really want that and other don’t want.”

“If I were to posit a replacement for the “triple triple double double” phrase maybe it's something like “quadruple 120”. You should be growing very quickly, quadrupling year-over-year but also have a net dollar retention over 120%.”

Monday, Mar. 17th: Spruce Point published a short selling report on Remitly which is a publicly listed remittance company. - Spruce

“We find evidence that the Company has used dubious customer testimonials and doctored Trustpilot reviews. According to the CEO, his business is ultimately about trust and the top listed frequently asked question among its immigrant customers is “Why should I trust Remitly?”. Moreover, we believe there is ample evidence to distrust the Company’s accounting, financial reporting, governance and equity growth story. We lay out the case that Remitly is exhausting its ability to pull revenue and cost levers to improve its financial performance as the shift to digital payments accelerates and it may have weakened its compliance protections to prevent fraud in pursuit of lower quality and/or riskier customer growth.”

“Remitly ceased disclosure of metrics we believe are important such as number of transactions, long-term customer value to acquisition cost calculations (LTV/CAC) and overhauled its flywheel depiction despite minimal business shift.”

“We disagree and believe its business faces long-term displacement risk from stablecoins and short-term disruption from U.S. immigration policy tightening.”

“Spruce Point interviewed a former Remitly employee who was with the Company for over 2 years and worked on front line product development. In addition to existential risk related to stablecoin, the executive references multiple concerns such as new competition (e.g. TapTap Send and Nubank) and how Remitly has struggled to expand and innovate in the same period that Wise has introduced many product extensions.”

“I'm hearing from consumers that they're getting ads from various companies with very similar messaging. For them then the question really becomes again, the pricing and then considerations on the product side.”

Tuesday, Mar. 18th: Gil Dibner at Angular broke down VC firms into 5 different categories: (i) < $50m pre-seed funds specialised in a vertical or a geography, (ii) $100-250m inception funds with concentrated portfolios and with a first-check building mindset, (iii) $250-500m emerging series A funds competing to build the next generation of legendary venture funds, (iv) $500m-$1bn funds that are too large to rely on inception investing to generate returns and that are struggling to compete with super-scale platforms, (v) super-scale platforms that are LPs money magnets. - Angular

On super-scale platforms: “They operate more as asset aggregators than as traditional venture capital firms, deploying large amounts of capital across a range of venture, growth, and PE-style investments. Their performance targets (both per investment and on a fund level) are far lower than traditional early-stage venture. For them, a 2x return on a given investment is perfectly acceptable.”

On emerging series A funds: “Like the inception funds, these firms are company builders by nature, but they bring deeper pockets and a stage-focused approach. They are highly engaged with their investments, active on boards, and maintain concentrated portfolios. Competition among them is intense, however, because there are few if any undiscovered opportunities at the Series A stage.”

On dedicated pre-seed funds: “We believe many of these firms are struggling to adjust to market conditions. Larger rounds wreak havoc on their economics and render them less attractive to founders. Lower graduation rates and the growing need to bridge companies to Series A can be very challenging for subscale firms due to limited (or non-existent) reserves.”

“Many VCs will try hard to blur these swim-lanes, but founders should be cautious about letting that happen. The old adage “your fund size is your strategy” has never been more true. Many funds who have grown tremendously in size find themselves forced to shift strategies.”

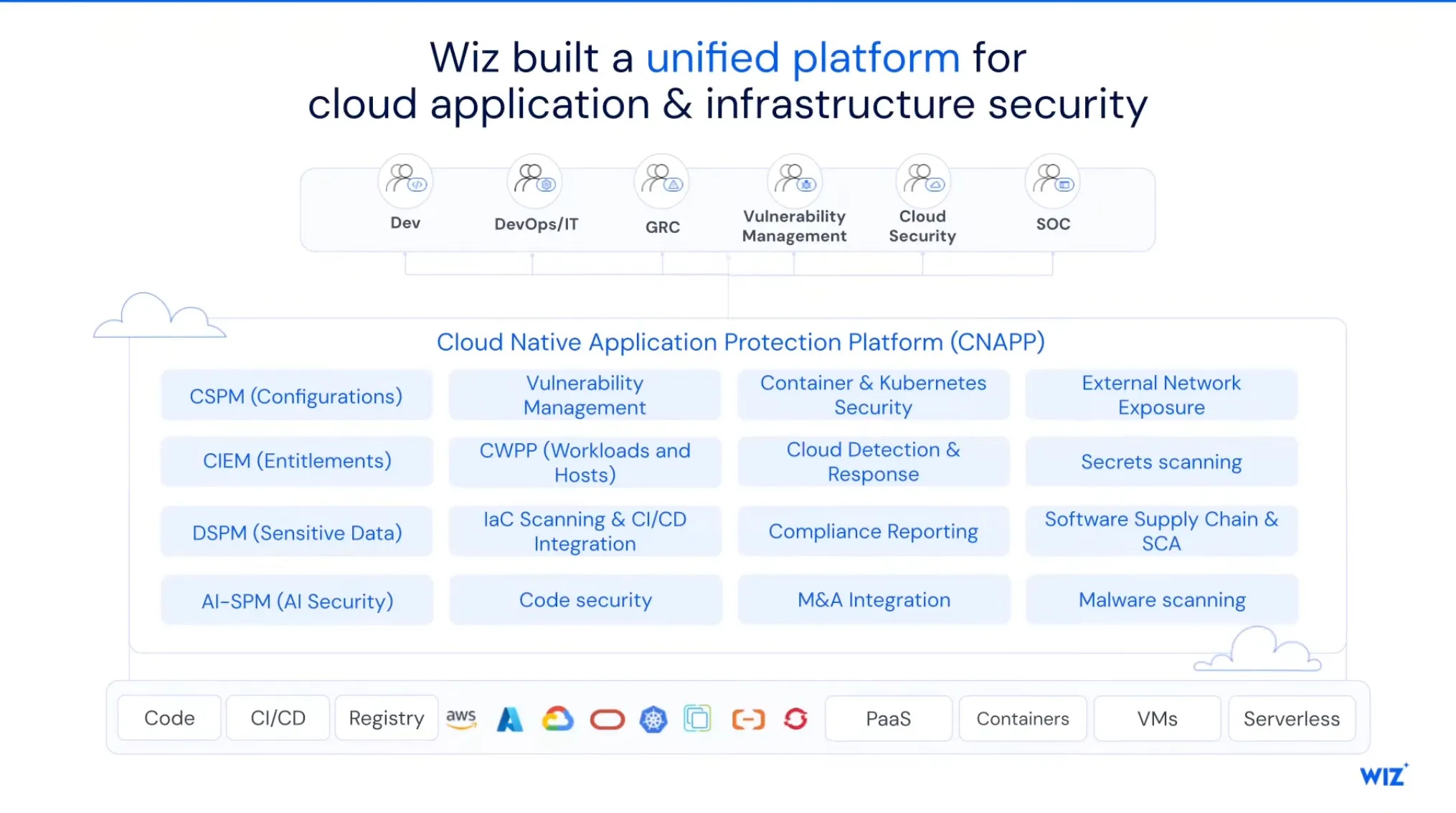

Wednesday, Mar. 19th: Google acquired Wiz for $32bn in an all-cash deal to strengthen its capabilities in cloud security. It’s Google’s largest acquisition to date surpassing its $12.5bn purchase of Motorola in 2012. - Wiz, Reuters, Google

“Five years ago, my fellow cofounders and I set out to create something security and development teams would love. We embarked on a significant mission: to help every organization secure everything they build and run in the cloud – any cloud.”

“Alphabet will buy fast-growing startup Wiz for about $32 billion in its biggest deal ever, the Google parent said Tuesday, as it doubles down on cybersecurity to sharpen its edge in the cloud-computing race against Amazon and Microsoft.”

Google initially offered $23bn for Wiz in 2024, but the deal fell through as Wiz pursued an IPO in a regulatory environment that was not favorable to strategic exits. Negotiations resumed recently, leading to this agreement.

Thursday, Apr. 20th: In 2024, MrBeast generated $500m in sales and burned $60m. Its chocolate brand Feastables generated $250m in sales and $20m in profit while its media business generated $250m in sales and lost $80m. Over the past four years, MrBeast raised more than $450m with his latest valuation reaching $5bn. He is looking to raise a couple hundred million dollar to expand into new areas including gaming, beverages and wellness. - Bloomberg

“MrBeast, whose real name is Jimmy Donaldson, has spent the past few years leveraging his fame on YouTube and other social platforms to build businesses that have nothing to do with media. In addition to Feastables, Beast Industries is a shareholder in the snack brand Lunchly and the owner of Viewstats, a software firm that sells digital tools to fellow content creators.”

“The average video for MrBeast’s main channel now costs between $3 million and $4 million.”

“Amazon paid MrBeast about $100 million to produce the first season of Beast Games, one of the most expensive deals in the history of reality TV.”

Friday, Mar. 21st: Bloomberg published a deep-dive on US drone-maker Skydio. - Bloomberg

“Like the machine gun and the tank before them, drones are remaking battle, and since Russia’s 2022 invasion, Ukraine has become the world’s laboratory for drone warfare. Quadcopters bought for a few hundred dollars and loaded with explosives have been transformed into lethally efficient guided missiles. Ukrainian pilots wearing virtual-reality headsets steer them into combat, stalking and killing Russian infantrymen from above and destroying multimillion-dollar tanks and armored personnel carriers. The Russians have responded with drone units of their own. At this stage of the conflict, the weapons are responsible for the majority of the casualties on both sides.”

“A military-industrial complex of small domestic drone companies, aided by US funds, has sprung up in response, but the country still has to import much of its supply.”

“Skydio is particularly proud of the craft’s ability [of its X10D] to pilot itself, even without a radio connection and without GPS. The drone uses its navigation cameras, at altitudes up to 300 meters, to produce a real-time topographical map of the landscape below, relying on that to fly autonomously if other options fail.”

“For Skydio the meeting was a chance to get invaluable feedback—and to make amends. As everyone in the room was aware, the company’s track record in Ukraine had been disappointing. An earlier Skydio model, built to US Army specs, had been shipped over by the thousands, but many had proved defenseless against the anti-drone radio jamming now routinely used on Ukrainian battlefields.”

“Bry likes to say drones are evolving “from toys to tools to infrastructure.” Outdoor photographers and filmmakers were some of the first to rely on the technology; now firefighters and police officers do, too—in search-and-rescue operations, vehicle pursuits and potentially violent standoffs. Electric utilities send drones along power lines to look for damage, commercial shipowners use them to inspect their vessels, and structural engineers use them to spot warning signs of failure in the country’s aging bridges and dams.”

“The vast majority of the drones in the air today—in the US and everywhere else—are Chinese, most of them made by one company, DJI. As drones grow more important, Chinese dominance of the industry has heightened concerns about who controls the flows of data they collect—and who ultimately controls the craft themselves. Supply chains, too, can be weapons: Ukraine’s military is constantly having to find creative ways to acquire the Chinese drones and components on which its war effort depends, since the Chinese Communist Party, a Russian ally, restricts their sale to Ukraine”

“DJI models also tend to be much cheaper than their non-Chinese competition. That reflects efficiencies of scale and the company’s mostly automated assembly line, along with the lower cost of skilled labor in Shenzhen, where its offices and factories—and the offices and factories of many of its suppliers—are located.”

“The rise of drones has coincided with the worsening of relations between the US and China.”

“Bry believes the most exciting near-term possibilities for his company are closer to home, as more and more cities buy X10s for their police and fire departments.”

Saturday, Mar. 22nd: Finn Murphy at Nebular wrote a great post giving fundraising tips to founders. - Finn Murphy

“Most VCs would like to deny the role that hype plays, but everyone knows it's importance. Generating gossip and FOMO isn’t 100% of successful fundraising but it is often the difference between a fast process or a long death march.”

“For the love of christ find another founder [as a sherpa]. Game has changed and the sought after founder acting as your consiglieri is the power move in the game today.“

“The main driver of favourable terms in any fundraising is competitive pressure and the fear that if they don't move fast and put forward good terms then another fund will.”

“The biggest thing that surprises founders who transition to becoming investors is usually the realisation that VCs talk to each other. Like a lot.”

“Angels are another great avenue to ensure folks hear about your company and upcoming rounds. Line them up early and gradually tell them to introduce you to funds.”

“There is always an archetype of deal / founder that draws significant investor interest - you may not be able to be that archetype but you can associate with those types, build networks with those founders and tell your story aligned to the wider narrative.”

“The best way to drive investor interest in between funding rounds? Don’t speak to them without purpose. Every interaction needs to be planned and the information you share with them must be managed.”

“Controlling the information about your company that is out in the wild is not about deceiving your potential investors. It’s about managing their perception of the business and maintaining the magic of something new with limitless potential.”

“The challenge right now is that a lot of companies have told stories of near vertical growth and if you're not in that bucket it's harder than ever. But it's worth knowing a lot of that vertical growth is not quite what you think it is, but in your own positioning you have to be aware of that. Not all revenue is created equal, but it can certainly look that way in a slide deck.”

Sunday, Mar. 23rd: Jack Altman interviewed Keith Rabois. - Uncapped

“In venture, the returns are mediocre. The only way to produce great returns is to have a competitive advantage. Mine is to underwrite undiscovered founders when they have nothing but a keynote deck.”

“Every founder who really succeeds has a superpower that puts them into the top 10 basis points in the world on some trait (e.g. most tenacious, greatest salesperson, most disciplined).” “Ideally, this trait has to match the company.” “The other possible alternative is a Venn diagram overlap that you never see. For instance, Max Levchin is a world class technologist and a world class business strategist.”

“90% of the best stuff I’ve ever invested in, I was totally sure about (e.g. Palantir, Airbnb, Youtube, Ramp, Trade Republic). So if the fund were smaller, I’d probably just stick to the ones I felt really damn good about.”

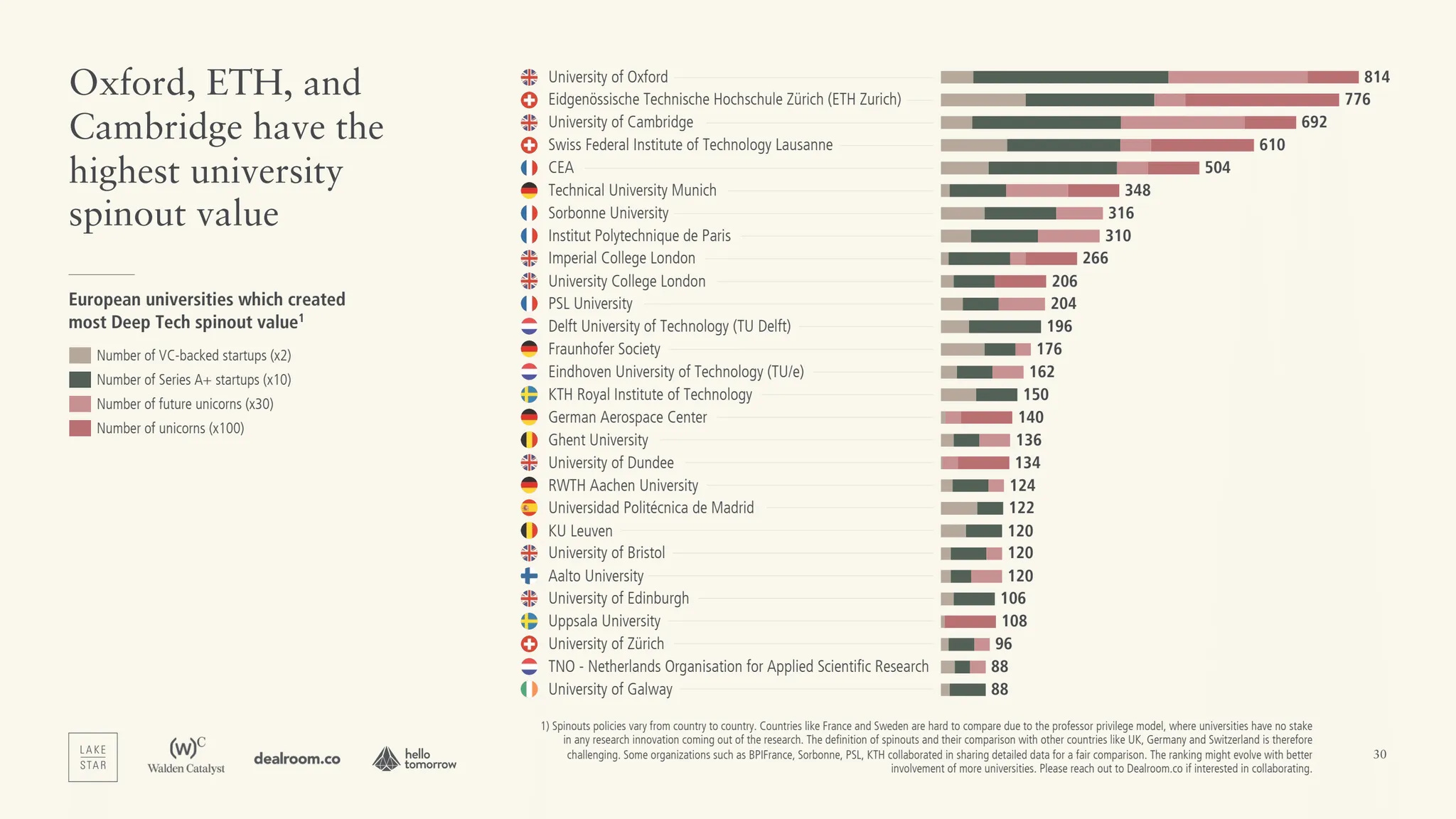

Monday, Mar. 24th: Lakestar, Walden and Dealroom co-published the 2025 edition of their report on deep-tech in Europe. - Lakestar

Tuesday, Mar. 25th: RevenueCat published its 2025 state of subscription apps report. - RevenueCat

Wednesday, Mar. 26th: I listened to a Business Breakdown’s podcast episode on Axon with Daneille Menichella who is portfolio manager at Sands Capital. - Business Breakdown

“Axon sells a public safety technology ecosystem that includes three main product groups, TASERs, body-worn cameras and other sensors, and evidence software, amongst a host of other software services, including virtual reality training.”

“What makes Axon special is it has this existing pretty resilient customer base through TASER customers, where there really isn't an alternative.”

“We have a business that has shifted from a predominantly hardware sales model to an increasingly software-driven subscription model with 95% subscription sales, 122% net revenue retention, increasing margins as a result of more software, and the ability to generate higher cash flows in the future.”

“Each subsequent model aimed to make the TASER better and more likely to be able to ultimately replace a gun with bullets in terms of reliability. We're still not there yet. We're close though, after seven models, and we now have the TASER 10, which was introduced in 2023.” “One, range, the officer shot the TASER from too far away and have failed to reach the target. And two, lack of follow-up ability. The TASER was shot, the target was missed. Previously, TASERs only had two shots to get it right. So the latest TASER, the 10, helps solve those problems and more. It has increased range up to 45 feet. It has 10 shots to get it right.”

“In TASERs, Axon is in 92% of U.S. state and local agencies.” “Overall, in the U.S., when you think of all the other end customers, whether it be federal, corrections, private security or enterprise, U.S. TASER penetration is only about 35%.” “Body cameras for all the mandates and cries for more accountability from over the past five years or so, penetration reaches only 14% in the U.S. And then the big one there is the 4% penetration in software and cloud.”

“What police officers ultimately found was they felt safer wearing the body camera. They felt as though if they weren't doing anything wrong, if they were good police.”

When I think about growth of the company, I think it predominantly comes from four key categories: (i) new versions of existing products with more & better value added features, (iii) software that's capable of doing more with less time and resources from teams, (iii) new products that can be sold to new & existing customers (e.g. virtual reality training, Axon Respond, Axon Air), (iv) expansion outside the U.S. with international only accounting for 20% of revenues.

Draft One is a “a software program that leverages generative AI and takes body-worn camera audio to produce high-quality draft report narratives in seconds. The output is a report that is standard, more clear, more concise, more consistent.” “Right now, an officer sits behind their desk up to four hours of their eight-hour shift. So that is meaningful time that they can get back on the street, they can interact with their communities, they can stop crime.”

“The lowest subscription starts at about $15 a month per user, and that's for single software seat per month. Right now, the highest bundle is about $325 per seat per month. And that's for what Axon calls the Officer Safety Plan 10 plus premium. That's the gold standard, and that includes the TASER 10 and cartridges, the latest body camera, training, software and cloud.”

“Most contracts are on a five-year term, but there are some shorter, some that are 10 years or more. But let's talk about the five-year contract for the Officer Safety Plan. I think that probably is the best example. In year one, the officer will get a body camera and a TASER, including cartridges and training. And that includes virtual reality hardware and cloud software. The cartridges, training, software and cloud are continuous, meaning they get access to it over each of the five years. Then in year three, the officer will get a new body camera. So the expectation is that at the start of the next contract, the officer will get the new TASER and another new body camera.”

“TASER is a monopoly. I call the body camera segment a duopoly. That's not really true. There's a lot of players, and it's very fragmented. There are two key players, there's Axon and there's Motorola.”

“When you look at the top 50 municipalities in the U.S., Axon's market share is probably closer to 90%, so significantly large.”

“You have about 60% gross margin. The expectation or my expectation is that increase is about 500 basis points by the end of the decade, and that's really coming from slight improvement in the manufacturing of the current TASER 10 as they input some automated processes and you ramp up some economies of scale there, but also your software and your cloud margin is able to increase as well.”

“It's dominant market leadership, some monopoly in TASERs. Body cameras technically isn't, but in reality, there's only two big players, and we believe Axon's market share is twice that of the other player. It has an entrenched and sticky customer base and access to the most data in this field, which should help Axon benefit from generative AI faster than any potential competitors while offering a strong ROI to their customers, customers who every day are being challenged to do more with less resources.”

Thursday, Mar. 27th: Long runway doesn’t guarantee success. Early-stage startups should focus on achieving meaningful goals quickly, rather than conserving cash. Value diminishes after 12–18 months without progress. It’s better to take risks, spend wisely, and prove traction early. If it works, revenue will follow and extend runway. - Yoni Rechtman

“Sitting on cash won’t improve your odds of being right.”

“It’s much better to be conclusively right or wrong in a short period of time than spend years to produce a null, inconclusive result.”

“For really early companies, there is generally diminishing marginal expected value after 12–18 months. If you haven’t done something important in 18 months, the 19th month is very unlikely to be any different.”

Friday, Mar. 28th: I listened to an Invest Like the Best’s podcast episode with Gili Raanan who is the cofounder and GP at Cyberstarts. - Invest Like the Best

“AI will redefine cybersecurity. It will replace the old ways cybersecurity solutions were architected. The old systems of building rule-based systems and behavior-based systems so the good guys can fix misconfigurations or patch buggy software systems are gone. Founders will have to create cybersecurity companies that are AI-first and AI-native just to have a chance to build lasting, important cybersecurity companies.”

“My conclusion back in 2018 was that the venture model is completely broken.”

“Investors have spent an endless amount of time asking about markets, products, and technologies—questions for which founders at the very early, seed stage clearly don't have the right answers. Whatever they tell the investor would change within a few weeks, then change again and again. And everyone is simply playing a game and dancing the dance.”

“When I founded Cyberstarts, I made one very important commitment: to completely avoid questioning the market, the technology, the product, or the competitive advantage—and to focus on one thing only, which is the person ahead of me.”

“I'm looking for people who are not straight lines, who didn't have a perfect start in life and managed to overcome it and become successful, even though they didn't have a perfect starting point.”

“Cyberstarts is one simple thesis: one sector and a commitment to deliver real value to the founders we partner with, the clarity of that thesis, and the fact we focus solely on a single sector and own it.”

“Cyberstarts has more than $700m under management across five funds, four seed funds, and one continuation fund. The portfolio value today, cumulatively, is around $45 billion, which is 50% of the worldwide market cap of private cybersecurity companies. That means that we seeded 50% of the worldwide market cap for private companies in cybersecurity, and that's under seven years.”

“I learned that what's important in the story is not the what, it's the why. It's not about what you did; it's about why you did it, why you chose to do that, why you pick job A instead of job B, and why you pick that partner in life instead of another partner. It's always about the why. So it's not just about a unique, heartbreaking life story. It's about spending time with an individual and understanding the way they make decisions, the way they analyze situations, what drives them, and what really makes them tick.”

“Starting with the technology and then searching for who has a problem that the technology solves is the wrong order. The process should be completely reversed. We should first look at what the important pain points in a market are, identify the customers who are willing to spend money on solving that problem, and then build a solution for them.”

“One of my most favorite questions is, "Who's the vendor you hate the most?" Because if you don't like a vendor, that's a big motivation for you to displace that vendor.”

“Another important observation is that words are cheap. So don't look at what the customer says; look at what the customer does.”

“My approach is that it is expensive to build important companies. Important companies are typically not cheap. When I hear founders receiving advice like "keep down valuations, make sure you don't raise too much money," my approach is that your first priority as a CEO is to have enough money to build the right product and hire the right sales teams. That's expensive. So in order to raise enough money, the valuation should be high as well, because no founder would sell 50% of the company in Series A, nor in Series B. So I'm all for raising a lot of money, assuming you've built the right product and have the right team to scale and take on the opportunity.”

“I always speak with founders about their superpowers. What do they perceive as their superpower? […] It's fascinating to listen to the way they perceive themselves. I found out that some of the best founders are completely unaware of their superpowers. In many cases, the superpower they claim they have is not necessarily the real superpower they possess, but it shows you the way they view their weaknesses—because the superpower they are aware of, they pay attention to, having developed it in compensation for something else.”

“When you sell a product, you're going to face four personas. The person that has the pain point, the person who has the budget to pay for a solution to solve that, the person that has the authority to decide on the product or solution, and the fourth person is the one who would actually use the product. Now, as a startup, if those four personas map into a single person in real life, that's a mega hit. And that was the case of Wiz. If those four personas are mapped into four real people, there's one real person that has the problem, one real person that has the budget, one real person that has the authority, and a fourth person that actually uses the product. Don't do that. Go and pivot. And if you map into two people, that would be a very nice company. If you're mapped into three people, that's borderline.”

“Wiz managed to build a product that, during the first call with a prospect, allowed them to ask for the AWS credentials. And within the call, show them real value for their own organization rather than in a demo environment.”

“While we spent the first 12 months building a product, the next four quarters were quite unusual. The company closed with $1 million in ARR in the first quarter of selling the software, $2 million, approximately $8 million, and then $25 million in the fourth quarter”

“I learned at Sequoia many years ago that the expensive deals, the pricey companies, are pricier from day one. They're always expensive. They're expensive at the seed round, they're expensive at the A round, they're expensive at the B round. The worst reason for a venture capitalist to pass on an opportunity is for price. Because it's part of those companies' DNA—pick a company. All of those companies were expensive. Airbnb was expensive. Instagram was expensive. So if you're going to pass on an opportunity just because of price, you're going to pass on all the good companies.”

“He would source people whose hobby is writing code. He would source people that, on a weekend, assuming they are married and have kids and have a couple of hours of quiet time, would not read or watch a Netflix series or listen to music. They would go and write code. Those are the people you like to hire. When you have a hundred of these guys, it's like having 300 or 400 terrific engineers because you know the rule that a great software developer is probably 10 times better than a good software developer.”

“My recommendation is to really find your passion and do something that's not just about wealth generation or work—do something that's a life project for you. When I look at cybersecurity, cybersecurity is not an investment area; it's not an area of interest for me. It's a life project. It's really important for me.”

Saturday, Mar. 29th: I read an interview with Mudassir Sheikha who cofounded Careem on the company evolution from ride hailing to a vertically integrated super-app. - Rest of World

“The second chapter involved integrating Careem into the Uber ecosystem, a period of transition from a purely ride-hailing company to more than 15 services — including food delivery, bike rentals, financial services, and grocery delivery — on a single app.”

“Its third and current phase, initiated by a strategic spinout of all non-ride-hailing services from Uber at the end of 2023, marks a resurgence of Sheikha’s renewed focus on the future.”

“Sheikha wants to transform Careem into “a digital butler for everyday life.” For Sheikha, the concept of a digital butler transcends the transactional nature of super-apps. It focuses instead on a personalized and intuitive user experience, where Careem takes direct responsibility for the quality of its services, distinguishing it from platforms that merely connect users with third-party vendors. Under Sheikha’s leadership, Careem has adopted a strategic approach to expansion, prioritizing depth over breadth.”

“We see the destination as being a consumer internet or a consumer digital platform, which allows people to consume services that they need to use on a daily basis to make their lives simpler and more productive. We started with ride-hailing, so the first things we did were for ride-hailing. Deliveries were next. We started with food delivery, then grocery delivery, and pharmacy delivery. And then payments.”

“Then payments became another leg, which we now call CareemPay. Initially, it was just paying our captains — or drivers. We realized they were sending money back home, so we needed to make it easy for them. They needed to pay their bills, pay for their prepaid cellphone cards. We’re just following our customers in some path that is adjacent to the capabilities we’re building over time.”

“I’m not going to simplify your life if I’m going to burden you with the responsibility of selecting the right services and then working with all kinds of vendors to get the right quality of service.” “Today, we own our own grocery stores, and we own the end-to-end experience of the customer.” “The big difference is we stand behind the services that people consume.”

“The biggest issue is that markets are different. Egypt is different from Pakistan, which of course is very different from the UAE or Saudi Arabia.”

“One of the small contributions that Careem has made is the cohort of 600-plus “Careem mafia” — former Careem employees who have launched their own startup ventures. That’s the largest cohort of entrepreneurs in the region.”

“There’s generally a view that the world is going to adapt to you versus you adapting to the world. In many cases, it happens because there’s no substitute: The world adapts to you. But when there are substitutes, there is Careem and others that start in these markets, then we adapt to our customers and that just gives us the edge.”

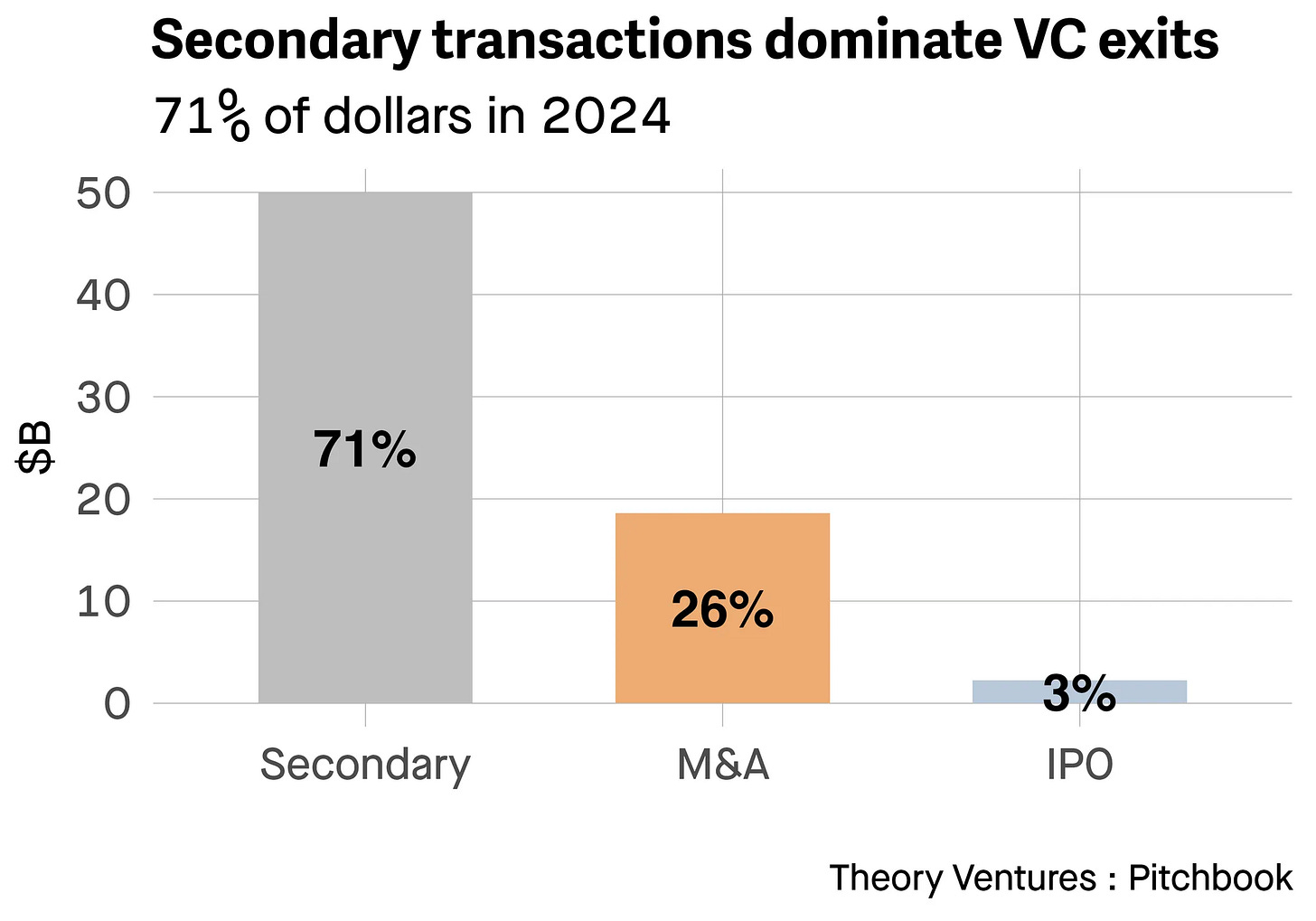

Sunday, Mar. 30th: Secondaries are now the main driver of liquidity in venture capital. - Tom Tunguz

“71% of exit dollars in 2024 came from a new avenue : secondaries. Historically, IPOs and M&A have been the dominant exit paths for venture backed companies. Some years IPOs dominate, other M&A dominates, but in 2024 secondaries captured the super majority.”

“There has been a huge challenge in liquidity since 2022 with the IPO market effectively silent, and M&A also stymied. In response, capital markets respond in a way they always do. They flood capital where there’s opportunity. And now the primary path to liquidity within venture are secondaries.” “This mirrors the private equity industry.”

“As in private equity, we should start to expect secondaries to become a permanent and significant part of venture capital liquidity for both employees of companies and also investors. With the target ARR required to achieve an IPO growing from $80m in 2008 to approximately $250m today, secondaries will become a permanent fixture in venture capital markets. It’s not just a temporary anomaly, but a structural evolution in how venture capital will function and ultimately evolve to look a bit more like private equity.”

Monday, Mar. 31st: Konstantine Buhler argues that usage is the ultimate moat for AI companies. - Sequoia

“Over the past few quarters we've seen some of the fastest growth in venture history. Many companies are racing to 100m or more of ARR in record time. A question that perpetually comes up is the depth of those companies' “moats.””

“Each new technological revolution has new potential moats in them. In the advent of telephony, we saw a very powerful moat - the network effect.” “This AI era poses a new question: can usage be a moat. In particular, can the data collected by customers using a product create a sustainable moat.”

“The intent behind ChatGPT was less to create a gangbuster consumer product and more to get this kind of usage data feedback. The theory was that if they created a consumer product that everybody could use, then they would be able to see the kind of questions that people would ask and get feedback about good or bad results. In my opinion, a mistake that they made was not allowing for edits in the responses, which would have provided even higher quality data in the feedback loop and an even deeper moat.”

“As companies race toward extremely high revenue targets. Perhaps their moat is really in the feedback loop - in usage. More data can mean a better AI product.”

“If they have raced past that point, it will be extremely hard for others to enter the market because the product is orders of magnitude better and the competitor would have to convince other users to use an inferior product for sufficiently long to get enough training data to improve. That is very unlikely for any self-respecting customer.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Hello Alexandre,

I hope this communique finds you in a moment of stillness. Have huge respect for your work.

We’ve just opened the first door of something we’ve been quietly crafting for years—

A work not meant for markets, but for reflection and memory.

Not designed to perform, but to endure.

It’s called The Silent Treasury.

A place where judgment is kept like firewood: dry, sacred, and meant for long winters.

Where trust, patience, and self-stewardship are treated as capital—more rare, perhaps, than liquidity itself.

This first piece speaks to a quiet truth we’ve long sat with:

Why many modern PE, VC, Hedge, Alt funds, SPAC, and rollups fracture before they truly root.

And what it means to build something meant to be left, not merely exited.

It’s not short. Or viral. But it’s built to last.

And if it speaks to something you’ve always known but rarely seen expressed,

then perhaps this work belongs in your world.

The publication link is enclosed, should you wish to open it.

https://helloin.substack.com/p/built-to-be-left?r=5i8pez

Warmly,

The Silent Treasury

A vault where wisdom echoes in stillness, and eternity breathes.