📖 Venture Chronicles - March 2024

Overlooked #172

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of March.

Friday, Mar. 1st: I read Josh Wolfe’s Q4-2023 letter to its limited partners. Josh Wolfe is a cofounder and managing partner at Lux Capital which is a venture fund investing in deep-tech. - Lux

“Recent optimism around the near-term fall in rates has incited the mania we last saw in 2021. Has venture learned its lesson? We see more and more investors feverishly funding futures closer to science fiction than the facts of science (to wit: fusion, quantum, longevity, space elevators, and more).”

“Too much attention and capital is currently allocated to venture ideas that are 10+ years out-and too little to maintenance of all the systems that already exist.”

“The mere prospect of lower rates on the horizon has caused many other generalist firms to venture further into the future: many are rebranding as "Al investors," or otherwise trying their hand at deeptech investing. Perhaps this is out of necessity, especially as these generalists' own previous domains-consumer, enterprise SaaS, fintech, e-commerce, and the like-have become increasingly crowded and competitive.”

“The concentration of capital in the 10 largest stocks of the S&P is the highest it's been since the 1970s Nifty Fifty. Investors are optimistic that Al products for the 'Magnificent Seven' will deliver top-line revenue growth, cost efficiencies, productivity gains, and contribution margin expansion. […] Meanwhile for the rest of the market, results are grimmer. Across all public companies, earnings fell more than sales growth, with margins compressing and record bond issuances increasing corporate indebtedness.”

“We expect a lot of dry-powder to prove wet (capital that will be used to shore up weak companies in underwater portfolios rather than invested into new ventures).”

“There will be many more dispiriting exits in venture, with soft landings for talent but hard landings for investors.”

“As much as 80% of financial transactions use FORTRAN or COBOL 60-year-old programming languages. Nearly half the banking system uses COBOL, and it runs 95% of the time you swipe your ATM card. “

Saturday, Mar. 2nd: Elad Gil revealed the unanswered questions he has regarding AI. Elad Gil is a solo-GP who become investor after a successful career as an operator at Google and as a founder in a company called Mixer Lab which was sold to Twitter. He spend a lot of his time in AI and has a podcast dedicated to the topic called No Priors. - Elad Gil

“Frontier LLMs are likely to be an oligopoly market. Current contenders include closed source models like OpenAI, Google, Anthropic, and perhaps Grok/X.ai, and Llama (Meta) and Mistral on the open source side.” “Frontier models keep getting more and more expensive to train, while commodity models drop in price each year as performance goes up.”

“As model scale has gotten larger, funding increasingly has been primarily coming from the cloud providers / big tech. For example, Microsoft invested $10B+ in OpenAI, while Anthropic raised $7B between Amazon and Google. NVIDIA is also a big investor in foundation model companies of many types.”

“Are cloud providers king-making a handful of players at the frontier and locking in the oligopoly market via the sheer scale of compute/capital they provide?”

Sunday, Mar. 3rd: Cox acquired a majority stake into Open Gov at a $1.8bn valuation. Open Gov is providing software for the public sector (budgeting, accounting, procurement, asset management, permitting), has 1.9k customers and is used by 1/3 of the US population. It generates more than $100m in ARR and it’s a profitable business. - Cox, Joe Lonsdale

“Our purpose was to bring transparency to state government by revealing waste, comparing performance, and spotlighting the most and least efficient areas.”

“As a founder of Palantir, I’d seen how the federal government had been grossly underserved by technology, but we’d stumbled on a different kind of gap here, compounded by much smaller budgets, minimal technical investment, and a fragmented market of tens of thousands of municipalities, which none of us really understood.”

“Initially we focused on the transparency and reporting workflows we’d discovered at California Common Sense [non profit cofounded by Joe Lonsdale], which required integrating with cities’ ERPs and enabling a variety of capability requests.”

“Through trial and error, we learned that most governments can pay for things that are already in their budget, for critical workflows they are already doing - such as permitting, licensing, budgeting, procurement, etc. Of course, there’s no rule that you can’t enable these functions in 10X better ways. This led us to identify existing processes we could translate to novel, cloud-based workflows. We found over 90 functional areas for which local governments buy software, and OpenGov covers nearly half of them today.”

Monday, Mar. 4th: Louis Coppey who is a partner at P9 wrote about the opportunity with AI to replace service businesses with AI-powered software businesses, expanding on Sarah Tavel’s thesis on selling work instead of software. - Louis Coppey

“Foundation models might perform well enough to build full-stack, AI-first service businesses that will ultimately look like software businesses.”

“Selling the work isn’t the same as selling AI-powered SaaS features. For both reasons, going after this opportunity might lead to a typical “Innovator’s dilemma”: an existing player would need to cannibalize its existing business to innovate.”

“A new player entering the market as a full stack AI-first service business can constrain the problem and hire service agents to:

Understand end users’ problems very well — iterating with employees will be much faster than iterating with customers,

Have “humans-in-the-loop” to get to the right level of quality of service,

Collect data that is highly specific to the industry and use case.”

“On the earlier stage side, below is a short list of ideas/companies we’ve seen more recently: automated SDRs, automated CS agents, automated development services, automated circuit design, automated accounting firm, automated law firm for tech companies.”

Tuesday, Mar. 5th: I read a great post on how startups beat incumbents. - A Smart Bear

“When we analyze how incumbents are vulnerable, we uncover opportunities that startups can exploit to win, where there’s often nothing the incumbent can do about it, despite their advantages:

Taking risks that cannot be quantified

Addressing a profitable niche

Doing delightful, valuable things that don’t scale

Unsurpassed customer service

Leveraging new technology

Having an opinionated personality

Doing things that aren’t zero-sum

Being worse-but-acceptable in most dimensions

Being low-cost against a profit center.”

“Every big-company advantage creates exploitable weakness.”

Wednesday, Mar. 6th: Photoroom raised a $43m series B round with Balderton and Aglaé at a $500m valuation. Additionally, it announced new Gen. AI features within Photoroom, alongside unveiling a new foundational model for commerce photography. The funding will be utilized to double its team size and enhance its Gen. AI capabilities. Photoroom is generating more than €50m in ARR, is profitable and its app has been downloaded 150m times (vs. 40m in 2022). - Matthieu Rouif, PR Newswire, Usine Digitale

“We saw limitations in the GenAI stack last summer. It was limiting in speed, architecture, and data. So we decided to train our model with an architecture that’s even faster, hence Photoroom Instant Diffusion name.”

“Photoroom's custom architecture will also increase the speed of image generation by up to 40%. This means users will be able to generate and iterate on its images much faster than on any other visual AI model.”

Thursday, Mar. 7th: Lenny Rachitsky interviewed Jason Lemkin on building and scaling a sales team. Jason Lemkin is the founder of SaaStr which is the largest community and the largest event for B2B SaaS founders. - Lenny’s Newsletter

When you acquire your first 10-20 unaffiliated customers as a founder, it's crucial to be honest about the go-to-market (GTM) strategy needed to sell your product. If a sales-led motion is what these customers require, you should deploy it, even if you don’t particularly enjoy sales and would prefer a product-led growth (PLG) motion. “I find too many folks that don’t like sales who will flee from customers requiring a sales led motion and I’ve never seen that lead to success.”

Most companies end up being hybrid between sales led and product led. “There's all different ways to combine a product-led or self-serve motion with sales-led. Too many founders in the beginning think it’s either or but it’s not.”

When is the right time for a founder to hire a first salesperson?

Founders should find a way to close at least the first 10 customers, even if they don’t particularly enjoy sales. Customers appreciate interacting with founders. In the early days nobody has a better understanding of the product and the market than founders. Even if a founder isn't skilled at sourcing or closing deals, they should excel in the middle of the sales funnel, adeptly discussing the product and the market.

Once you've signed your first 10 customers and find yourself dedicating more than 20% of your time to sales, indicating that it's effective, it's time to hire salespeople to scale up. It's advisable not to hire just one, but two sales representatives for an A/B testing approach. “These first two hires should be people you would buy your own product from.” You should do the efforts to interview at least 30 sales reps disregarding their past experiences. Out of these, around 20 will be terrible, 8 will be good, and 2 will be amazing in selling your product. It's essential to focus on those who are actively working to prepare interviews and who are great at selling your product, rather than being swayed by prestigious logos or impressive resumes.

“We're looking for pirates and romantics in the early days. We are not looking for folks with massive sales operations teams and enablement teams. You're looking for that quirky one that's got a few extra IQ points, that for reasons that make no sense has fallen in love with your little product that is so feature poor and does nothing, but they love it.”

These initial two sales representatives should possess a few years of experience in B2B sales and demonstrate maturity, as at this stage, there's limited time for babysitting (no onboarding or extensive training) and it’s crucial to trust them with the leads you provide.

“You need 2 sales reps hitting quota closing deals before you're ready to hire a manager for them. Almost all VPs of sales, their job is to take you from rep 3 to 300 and to scale something that is just start to repeat.” You will hire more experienced sales rep to learn from them and iterate towards scaling the GTM motion (e.g. spotting 10x features, spotting feature gaps).

When you hire a VP of Sales, they need to have a quota and close sales themselves at least for a little while (full quota, half quota or backfill the sales team). You want your VP of Sales in deals 20-30 hours a week when they start. You need a VP of Sales who actually want to do sales.

“The majority of VP of Sales don't want to do sales. It's my first screening question. That's why they got to carry a bag because it proves they actually still care about the craft. The best sales folks love sales. It's a craft. They also love money. Do not hire a sales rep that doesn't like money. Trust me on this one. There's 0% chance they'll work out either, but they also like the craft.”

“In the early days, if you’re not spending 20% of your time in sales and 20% of your time in recruiting you’re failing as a founder.”

How to interview salespeople both early sales hires and VP of Sales?

For VP of Sales, you should ask them what they want to do during their first 30 days. If they don’t to want to start by talking to customers, it’s a massive red-flag and it means that they no longer have the drive to work hard. In the early days, you don’t want them to spend time on processes (e.g. territory planning).

For early sales reps, you should ask them to sell you your product. They have to put the 2 hour work (e.g. watching webinars, reading customers testimonials) to be in a position to sell the product during their interview.

“The best reps will tell customers not to buy their product because they know that there is a mismatch between the scope of the product that they sell and the expectations of potential customers.”

How to set-up compensation and quotas for early sales reps?

During the initial 3 months, sales reps should retain 100% of what they close. While this might not be sustainable at scale, it's essential for jumpstarting the business and investing in the sales team. This approach fosters a sense of accomplishment among sales reps and allows them to ramp up without excessive pressure.

Salespeople should receive compensation at market rates, typically divided equally between fixed and variable components. Ideally, a sales rep should generate 3-5 times their take-home pay in revenue. For enterprise sales, this multiple should be even higher, accompanied by a corresponding increase in compensation.

“You want your sales to make a lot of money. Your sales team has to eat.” If they make too much money, it does not matter. It means that you’re extremely successful as a business.

How to scale a sales organisation?

In sales, operating leverage is limited. Sales tend to scale linearly with new revenues, and there are even anti-efficiencies, with public companies often being less sales efficient than startups.

Building management within a sales organization is essential. For every 8 SDRs, there should be a manager, as well as for AEs. Additionally, 8 directors will require 1 VP.

SDRs typically hold entry-level positions, often fresh out of school, with an OTE (On-Target Earnings) ranging from $60k to $80k in the US. Their responsibilities include email outreach, cold calling, and occasionally screening inbound leads. SDRs pass qualified leads to AEs, who are responsible for nurturing and closing deals. SDRs are openers, while AEs are closers.

Upon hiring a VP of Sales after the initial two sales hires, the VP will begin seeking out 2 directors while simultaneously recruiting an additional 6 AEs whom they will manage directly. Directors' responsibilities can be segmented by geography, customer size, or sector.

When hiring a VP of Sales, it's advisable to select a candidate who represents a stretch—a professional who was previously a director and will receive a promotion within your organization. This approach is preferable to hiring someone who previously held the VP of Sales position but may no longer be suited for the role. A sign that the VP of Sales is effectively scaling is their ability to recruit or promote top directors within the organization to expand the sales team.

Friday, Mar. 8th: I listened to a 20VC’s interview with Adam Fisher who is a partner at Bessemer based in Israël who invested in companies including Wix, Fiver, and Habana. - 20VC

Investors should maintain a balanced relationship with entrepreneurs, reacting to both good and bad news with composure. This builds trust and transparency.

Adam prefers investing in companies with a unique approach rather than being one of many competitors. “I think there's two types of investors out. There are those that get comfortable when there's competition and they get comfortable because that gives them the sense that there's that there's investors out there willing to put money in and that there must be a market if multiple people see the same opportunity. I'm the other type. I get comfortable when it's only us but if we're right, we're going to be the leader.” “I think it's a better arbitrage opportunity to be the sole player or the first mover even in a smaller market - even in a niche market - than to be the number two or three in a large market. It’s like gladiators. Number two is still a looser.”

Category creation often happens in retrospect when a company identifies a new type of customer. “If you’re talking about creating a category from the get-go, you’re making a mistake. A lot of times, when we talk about category creation, it’s in retrospect that we see that a category was created. It was not started that way. It became an independent category. It’s typically not because that one company created it but because the multiple companies with very similar mindset are also moving in that same direction and and luckily you were ahead of the curve.” “I think where category creation makes sense is when founders have identified a new type of customer or a new type of buyer.”

“As much as I am willing to be contrarian, I'm not willing to invest in something that others are not going to fund. It’s a fine line. I need to find something that perhaps is not mainstream perhaps but is also not going to be dismissed by other investors as not interesting. Making sure that the next round of funding is accessible and doable is a critical part of my strategy.”

Sometimes, founders and investors think that they’re going after a large market but what they’re really focused on is a small subset of that market. “I personally like to invest in in smaller markets. First, there is unlikely to be competition. Second, if you price it right you can still achieve an exit that in that smaller market or niche. A niche that has no potential of expanding is problematic. I like niche areas where there are adjacent sectors (e.g. going upmarket, going into a second related product). It’s a fine way to grow into a bigger market.”

Founders should raise only what is needed and avoid overfunding companies too early. Excess capital distorts strategy and culture.

VC investors should invest in smaller markets if priced appropriately. Adjacent growth opportunities can expand the market over time.

Saturday, Mar. 9th: I listened to a podcast interview on World of DaaS with Sarah Tavel who is a general partner at Benchmark. - World of DaaS

In the past 25y, most software companies have been about improving the productivity of employees. At the end of the day, if you sell productivity improvement, the value of that productivity improvement for an employee is relative to the cost of this employee (e.g. you can extract more value from improving the productivity of a senior developer vs. a recruiter). You monetise by taking a percentage of the productivity gain generated by your software. You charge on a per seat basis.

The first wave of Gen. AI startups are still replicating this model with copilots to improve the productivity of employees (e.g. Github for developers). The challenge for startups with the copilot model is that you will always lose to incumbents which have distribution.

The idea with selling work is that you get out of the mental model of selling a 10% productivity improvement. Instead you think about the work to be done that employees are doing. You unbundle that work and see if there is an atomic unit of work that can be automated. Instead of selling software that you're trying to get employees in a company to adopt and you're actually selling that atomic unit of the work product itself.

EvenUp sells to personal injury lawyers. Any time these lawyers have a new case, they have to summarize the case in a document called the demand letter that will be submitted to the insurer and there is going to be a back and forth to figure out what the claim will settle for. The software way of selling this would be to sell a software product to the personal injury lawyers to improve their productivity. The way to sell work is to take all that work on the company side. You have human in the loop to do QA. You customise the output based on your brand. You do the summarisation to make the demand letter. You charge per demand letter produced instead of selling per seat. You sell the work product for much more money than you would have otherwise with a productivity gain software.

A useful test to see whether an idea could be sold as work is whether that work is already outsourced to a third party (e.g. a BPO). Instead of competing with another software company, you’re competing with a BPO.

When you build or invest in a company selling work, you need to be honest about your ability to fully/mostly automate the work you provide to avoid ending as a tech enabled services company. You should start from a place where you can automate at least 80% of the work and have a roadmap to get close to 100% in a reasonable timeframe.

A great place to start a company like this, it’s to look at what services BPO providers are providing and use AI to replicate their work at a fraction of the price and at a better quality.

Sunday, Mar. 10th: Europe has welcomed a new vertical SaaS unicorn, as Mews secured a $110m funding round at a valuation of $1.2bn. The round was led by Kinnevik, along with participation from existing investors Revaia, Goldman Sachs, Notion, and new investor LGVP. Mews has surpassed the $100m ARR threshold, experiencing a remarkable 60% YoY growth. The company has also achieved $8bn in gross payment volumes, up from $2.3bn at the end of 2022, serving over 5k (compared to 3.3k at the end of 2022) and managing 350k rooms. Additionally, Mews boasts a marketplace with 1,000 integrations and has acquired eight companies since its inception. The funding will be directed towards doubling down on geographical expansion, particularly in Germany, the Netherlands, France, the Nordics, and the US, as well as acquiring new companies and investing in R&D. If you want to read more about the company, you can read the deep-dive I published last year. - Techcrunch, Skift, Mews 1, Mews 2

“I really look forward to seeing our teams release the first of these features to make sure Mews is at the forefront of AI innovation.”

“Real momentum has built in the past few months, and we’ve reached a tipping point in several markets. We onboarded the early adopters a few years ago and started seeing pockets of success, but once you get past 10% market ownership, suddenly word of mouth spreads and lots of local brands start adopting.”

“Investors believe hotel software has hit a pivotal point as hoteliers switch from on-premise products to cloud-based tools meant to interact with other software and provide more dynamic selling opportunities for upsells and ancillaries.”

Monday, Mar. 11th: Alex Konrad at Forbes wrote a great portrait of Garry Tan who joined Y Combinator as president and CEO in January 2023. - Forbes

YC's model is facing challenges including several remote and larger batches reducing the quality of the program, alternative programs such as Sequoia's Arc and venture investors are more willing than ever to invest at the pre-seed stage.

“In the year-plus since, Tan has worked to win them over by reshaping YC in a “return to roots,” as he describes it. That has meant reconfiguring its batches, from admissions to groupings and social activities, to restore its status as a mecca for earliest-stage, technical (mostly nerdy) founders to learn the basics of company-building over three months.”

“By abruptly shutting down its Continuity fund, an eight-year-old growth-stage focused group within YC which held large investments into many of its brightest alumni companies, Tan took an unusual and decisive action. Celebrated by some as a prudent strategy, it stunned others in its coldness, leaving some founders — usually YC’s most prized assets and advocates — still disgruntled to this day.”

“He’s a great storyteller. He’s a real champion of founders, and a true believer. Founders gravitate to him.” - Brian Chesky about Garry Tan

“YC conducted a data analysis of Series A founders to break down the characteristics it should look for, and study why some did or didn’t apply.”

“YC would retreat from backing too many later-stage companies that had already raised funding and started making revenue, as well as non-software businesses.”

Tuesday, Mar. 12th: An engineer at Airplane wrote about its experience in a company that was acquired by Airtable and which product is being shut down. - Benjamin Yolken

“In the summer of 2023, the company hit some headwinds. First, although we were still adding customers, our revenue growth rate had noticeably slowed down. From what I understand, this was a trend across the entire SaaS tooling space that wasn’t unique to Airplane, but it still hurt morale and made us less optimistic about the company’s near-term future.”

“In addition, people on the team started quitting. Up until that summer, we had had zero employee attrition. Then, within a three month period, we lost 4 engineers and the company’s head of growth.”

“To top it all off, the CEO (who was also a co-founder) announced that he was leaving so that he could work on a personal, AI-related passion project. The CTO (the other co-founder) would be taking his place. His departure wasn’t a huge surprise- he had been very clearly burnt out and disengaged for months. But, it’s still never a good sign to lose the leader of your organization.”

“He then explained that the Airplane product would be shut down, but that most of us would be getting “extremely strong” offers from Airtable. However, we’d have to do interviews for leveling purposes, and the financial details wouldn’t be made available to us until later.”

“Based on these discussions, we put the pieces together and realized that this was an acqui-hire. Airtable wasn’t interested in our product, our technology, or our customers. They wanted our CEO to lead their new AI effort, and the rest of the company was baggage that would be accommodated to the minimum degree required.”

“As expected, customers were shocked and upset. Many had been using Airplane for critical workflows within their organizations, and they now had to replace huge chunks of internal tooling before the final shutoff on March 1.”

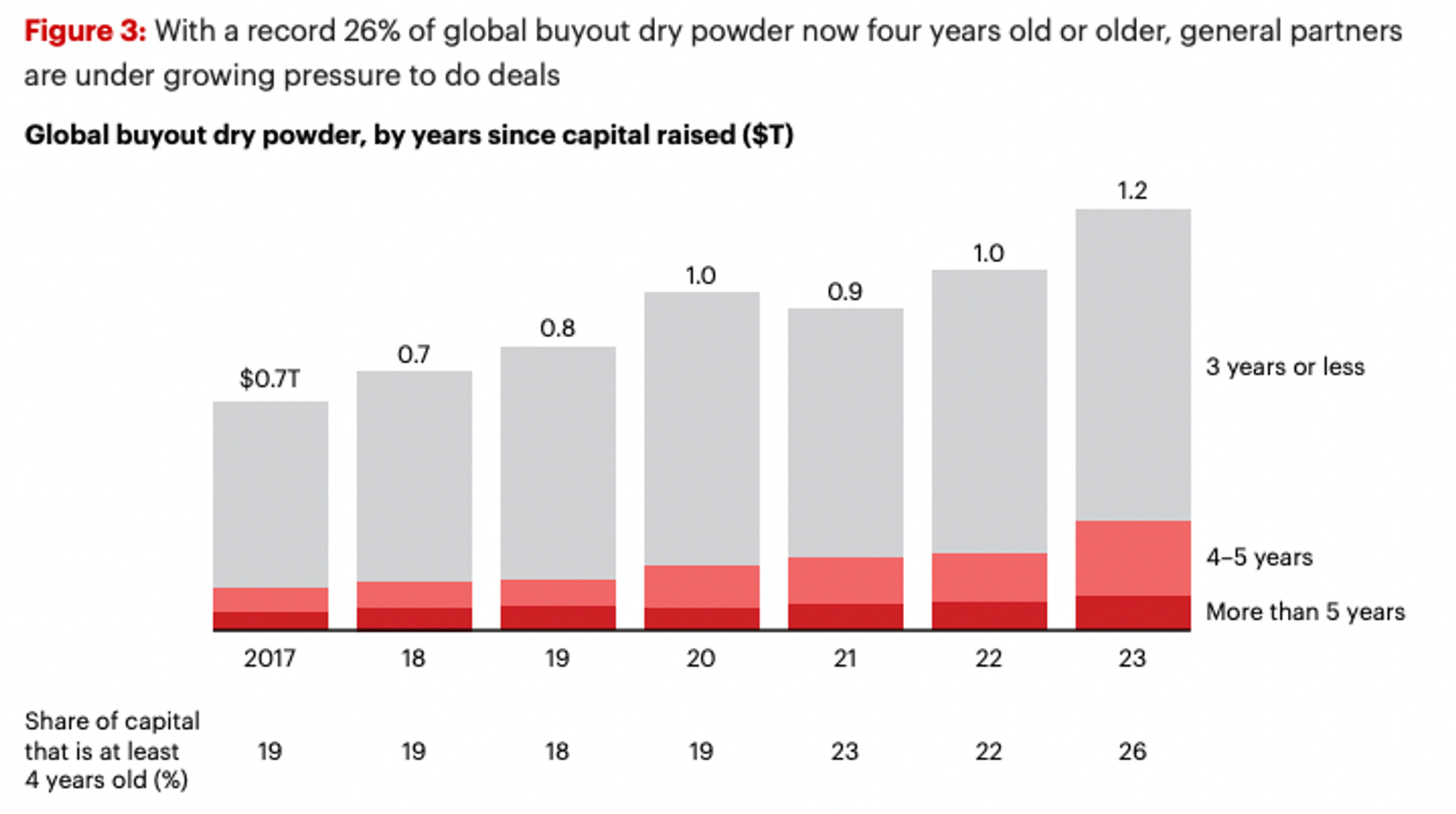

Wednesday, Mar. 13th: Bain published its annual report on private equity. - Bain

“It was truly a year of haves and have-nots. Just 20 funds accounted for more than half of all buyout capital raised.”

“The numbers are all very GFC-like: Deal value and deal count have fallen 60% and 35%, respectively, from their peaks in 2021. Exit value is down 66%, and the number of funds closing is off by nearly 55%.”

“Slower distributions have left LPs cash flow negative, crimping their ability to plow more capital back into private equity.”

“While capital flowed to the largest “reliable hand” buyout funds, fund-raising for most was as hard as it’s ever been.”

“The lack of affordable leverage cut the number of megadeals—those over $5 billion—by almost half, and the average deal size dropped to $788 million, down from the peak of $1 billion in 2021.”

Thursday, Mar. 14th: RevenueCat published a great report on subscription-based mobile apps with benchmarks from 30k apps on conversion rate, retention and monetisation. - RevenueCat

“We’ve seen the emergence of LLMs and generative AI as a mass consumer technology. We’re seeing almost every category of consumer app affected or, in some cases, disrupted by AI. While some are calling the era of mobile “over”, I contend that the AI era will be the second act of the mobile era. Mobile is, and will be, the primary platform for daily use of new and transformative AI technologies.”

“Many VCs aim for 50%+ Year 1 retention, yet RevenueCat’s data shows that the average is not just below 30% but is actually getting worse in 2023. Top decile apps can beat this average, but even established apps like Duolingo (with a 40% Year 1 retention rate) can’t retain half of their yearly subscribers. Monthly and weekly plans show the lowest retention rates, at 11.4% and 3.4%, respectively. That means 90-95% of paying subscribers will churn before the one-year mark. Even a leading app like Duolingo scores below 2-digits on this metric, at 9%. Shorter plans usually have higher price points, and do get intermediary renewals, but they still illustrate how brutal a challenge it is to retain consumers in the subscription app space.” - Thomas Petit

Friday, Mar. 15th: Stripe published its 2023 annual letter. - Stripe

Stripe’s customers processed $1tn in total payment volumes in 2023 growing 25% YoY and accounting for 1% of global GDP. Stripe was cash flow positive in 2023 and expect to remain so in 2024.

“Around 70% of online shopping carts are abandoned. We obsess over eliminating barriers to internet purchases. Our optimized checkout suite now includes over 100 optimizations, from the very large to the very small.”

“The average tenure of a company’s inclusion in the S&P 500 index has been shrinking over the past few decades: it was 61 years in 1958 and now sits at 18 years. This provides some empirical foundation for the basic intuition held by the CEOs of most large companies: reinvention is required. Our enterprise segment continues to grow rapidly, with more than 100 companies now processing more than $1 billion per year with Stripe.”

“Checkout and Payment Links are the most common products used by startups on Stripe, since they combine power with simplicity.” “Today, 1 in 6 new Delaware corporations incorporates with Stripe Atlas”

Saturday, Mar. 16th: Deconstructor of Fun wrote about the reasons why the gaming industry has struggled to grow significantly in 2023 despite the release of numerous blockbusters. - DoF

“The market looks to have bottomed out and is recovering at a projected growth rate of just 1.3%. The problem is that at the end of 2024, the market is still noticeably smaller than it was three years ago in 2021.”

“The miserable growth rate doesn’t make sense when considering all the fantastic titles that came out last year. Diablo, EAFC, Madden, Hogwarts Legacy, Baldurs Gate 3, Zelda Tears of the Kingdom… 2023 seemed like the year for consoles with all those blockbusters launching back-to-back. What happened was that selling and playing all of the blockbuster games of 2023 hurt live service games and stalled the growth of subscription services.”

“How high interest rates affect the game industry: (i) limited consumer demand for games, (ii) fewer new games in development, (iii) fewer investments into new studios, (iv) fewer exits through mergers and acquisitions, (v) focus on profitability instead of growth, which leads to layoffs.”

The Xbox Game Pass is not growing as expected its number of subscribers for several reasons: (i) no exclusive must play games, (ii) lack of time (i.e. most people play a couple of games per year and spend most of their time on Games as a Service), (iii) lack of accessibility as consoles/PCs cannot be played on the go.

“The downside of GaaS is that there are enormous risks. They cost the same as a AAA title, they don’t generate any launch week sales, and their costs only ramp up post-launch as the gigantic team creates content to retain players.”

Sunday, Mar. 17th: Ben Thompson interviewed Eric Yuan who is Zoom’s CEO and cofounder. - Stratechery

“Yuan was an early employee at WebEx, which was acquired by Cisco in 2007, where he became Vice President of Engineering. After failing to convince Cisco to rebuild WebEx around a better video experience Yuan left the company to do just that: Zoom Video Communications was founded in 2011, and IPO’d in 2019.”

What was the initial core thesis behind creating a new video-conferencing platform like Zoom? First, you need the best video quality. Two, it has to be extremely easy to use and you should not have any learning curve. Third, you need to support all form factors including mobile and tablets.

“Zoom product needed to be the best. So the reason was that, again, I’m still humble, but I do think I spend way more time than anybody else on talking with the customers.”

“I really wish there was no COVID. Zoom would be a much better company today and COVID, I did not think really helped us that much except for the brand recognition. For everything else, I feel like there was a negative impact to our business in terms of culture and growth and the internal challenge, or the competitive landscape. Everything else, I feel like it’s not good for us.”

“During COVID, within a short period of time, you had to hire a lot of people to scale up your business. But again, that’s not sustainable. Looking back, we also made a mistake, we should not have hired so many employees because that’s more short-term planning, and our solution was not sustainable, it did cause a cultural issue.”

How do Zoom think about moat creation? First, Zoom is not only a video conferencing product but it’s a full collaboration communication platform (phone, team chat, white board, note taking, email, calendar). Second, AI is embedded natively into Zoom and does not come at a big additional cost to the subscription.

Monday, Mar. 18th: GoStudent reached profitability and shared many insights on the company turnaround after its exponential growth during covid. - Techcrunch, Fortino

GoStudent has 11m families and 23k tutors on its tutoring marketplace. It sells 1m lessons per year. It reached profitability after having burn €89m in 2021 and €220m in 2022. In 2023, the company generated €250m in revenues with a double digit growth.

European families are spending €25bn on tutoring.

GoStudent scaled in France, Italy and Spain with its €8m series A. During covid, it expanded aggressively in 20 additional markets. In 2022, when the tech market started to crash, it drastically cut down its costs laying off 50% of its employees (from 2k to 1k employees) and exiting 9 unprofitable market.

“From 2019 to 2022, we scaled our core business model to more than €100m in revenue and it was amazing, crazy growth from zero basically within two years.”

GoStudent conducted 3 different rounds of layoffs. In 2023, it reduced burn by 70%.

“If the digital transformation brought along by Covid-19 lifted many boats, that was particularly true for edtech, and even more so for GoStudent. The company went from having to convince parents of the merits of online tutoring to becoming the go-to solution for schoolchildren in need of educational help.”

“Most GoStudent’s tutors are university students and this younger demographic makes it easier for them to click with pupils while serving as role models, too.”

In 2024, GoStudent has 3 business priorities: (i) remaining cash-flow positive, (ii) staying true to its goal of putting students first and (iii) showing how AI allows GoStudent to scale its business in a capital-efficient way.

“Their AI model in customer service answers the most common queries, halving the number of tickets and resulting in a saving of €3-4m annually.”

Tuesday, Mar. 19th: Ibotta submitted its S1 to go public. It’s a cash-back business in the US grocery space with its own cash back mobile app and a platform for retailers to offer digital promotions to consumers from CPG brands. Ibotta started in 2012 with its cash back mobile app and expanded in B2B only in 2020. - Ibotta, Techcrunch

It generated $320m in revenues in 2023 (52% YoY growth) with a 26% EBITDA margin. It works 850 customers representing 2.4k CPG brands. It gave back $1.8bn in cash back to customers.

“87% of consumers’ grocery purchases are influenced by offers, discounts, and promotions.”

“We are pioneers in success-based marketing: we only get paid when our client’s promotion results in a sale, not when a consumer merely views or clicks on the promotion.”

“We receive a large volume of item-level purchase data through our POS integrations with 85 different retailers.“

“In addition to providing digital offers for retailers, Ibotta also makes the same offers available on its own digital properties, which include Ibotta D2C. Since 2012, over 50 million Americans have registered for our free app.”

Wednesday, Mar. 20th: I listened to a 20VC’s podcast episode with Gili Raanan who is founder and GP at Cyberstarts which is a seed fund specialised in cybersecurity based in Israël. He also worked 15 years for Sequoia before building his own venture fund. - 20VC

“That characteristic of a smart and somehow lazy child you know was one of the driving forces behind my career.” “I think that laziness in the right combination is a wonderful trait.” “It makes you think about efficiency.” “You think about not repeating task you don't like. You focus on the things you really like and you're really good at.”

“In every successful company there was at least one board member who is the first call for the CEO and who is in the room whenever the important decisions are being made.”

In my interview with Michael Moritz to join Sequoia, “I had to talk about what drove me and what was my motivation. It was a very different interview. It taught me a lot about what's important when you like to get to know someone. You get to know someone not by looking at the inventory of their accomplishments but when you understand why they pick to do what they do.”

“When I talk to entrepreneurs today I like to understand them and you know that understanding would help me predict their behavior going forward.”

“Once you manage to create a brand for yourself, you create an amazing cycle where the best entrepreneurs like to partner with you, the best executives like to work for your portfolio companies and all other investors like to invest in your portfolio companies. The game becomes easier.”

On performance, Sequoia has an endless hunger. The firm is never satisfied. You could invest in Google but the next day, you run a meeting and you’re asking how you can improve. You're never happy with the status quo.

“The moment you're happy is when you start to lose. The moment you start to believe that you are experienced and that you're simply amazing in what you do is the moment you start to make mistakes. Questioning yourselves, beating up yourselves for anything that you could do better and chasing real greatness I think that's the only the only ways to to stay on top of the game.”

“In the early days I was looking at markets, at TAM, at technology and differentiators, I simply realised that all of that is bullshit. Everything will change in a venture except the team.”

“As time went by, I became more and more purist in my approach. When I started Cyberstarts, I decided that I would not even ask [founders] about market or technology or product. I meet with a new team which I don't know and we spend an hour you know speaking about their childhood and their mother. That’s enough to pick amazing teams.”

“I listen to their life story. I try to understand why they did what they do, why they moved from station A to station B. I'm looking for early signs of them being unique or simply excellent in something. I’m looking at whether they've gone through real life difficulty: have they gone through something that's really difficult and manage to be successful? I'm looking for the individual who was a socially isolated child. I'm looking for people who went through real difficulty in life and became successful.”

Cyberstarts employs a company-building process called Sunrise, which kicks off after selecting exceptional teams to collaborate with. Founders engage in extensive discussions with 60-70 Chief Information Security Officers (CISOs) from Fortune 500 companies over a three-month period. They inquire about the pain points these executives would prioritize solving if they had $100m allocated to engineering investments over the next three years. This approach addresses the market timing question effectively, as companies express their immediate needs and challenges. Following this phase, founders embark on another three-month round of interviews, presenting a solution thesis to the same pool of CISOs for feedback and gauging their willingness to become customers. Subsequently, a 1st version of the product is developed within 3-4 months, and commercialization efforts commence.

“The Sunrise process is an amazing process because unlike the traditional first year experience of a startup, you take all the hypothetical objections you might face as a company in the next three or four years and bring them to present.” You ask all the tough questions during your interviews: why would you buy our solution vs. a product from Palo Alto Networks? how would you price our product? what is the right distribution channel to sell this product? It allows companies from Cyberstarts to scale at a faster pace than regular startups because you get a more streamlined business by asking all the hard questions in advance.”

21 companies went through Sunrise. 17 companies raised a series A. 7 companies are unicorn. 1 company is a decacorn (Wiz).

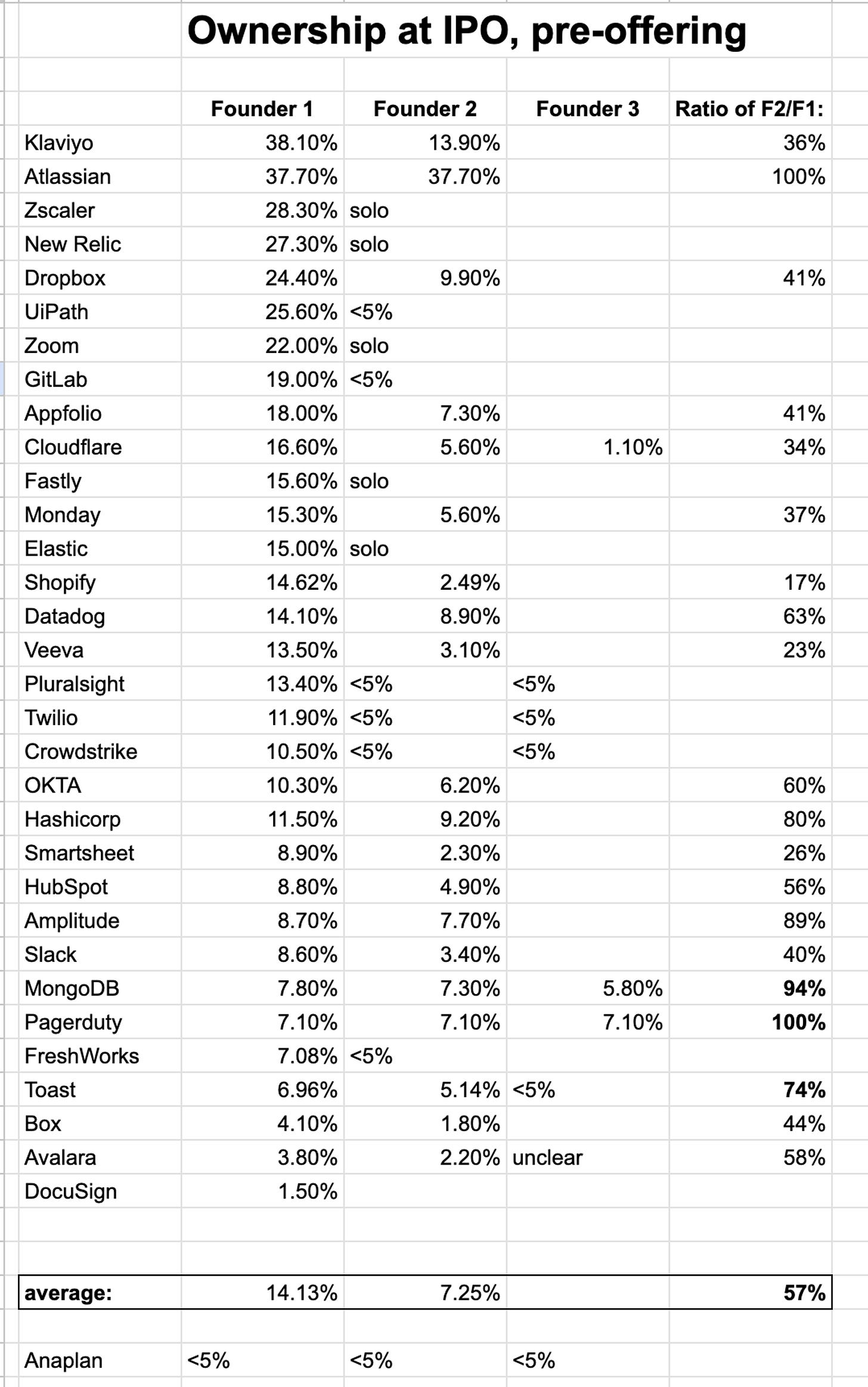

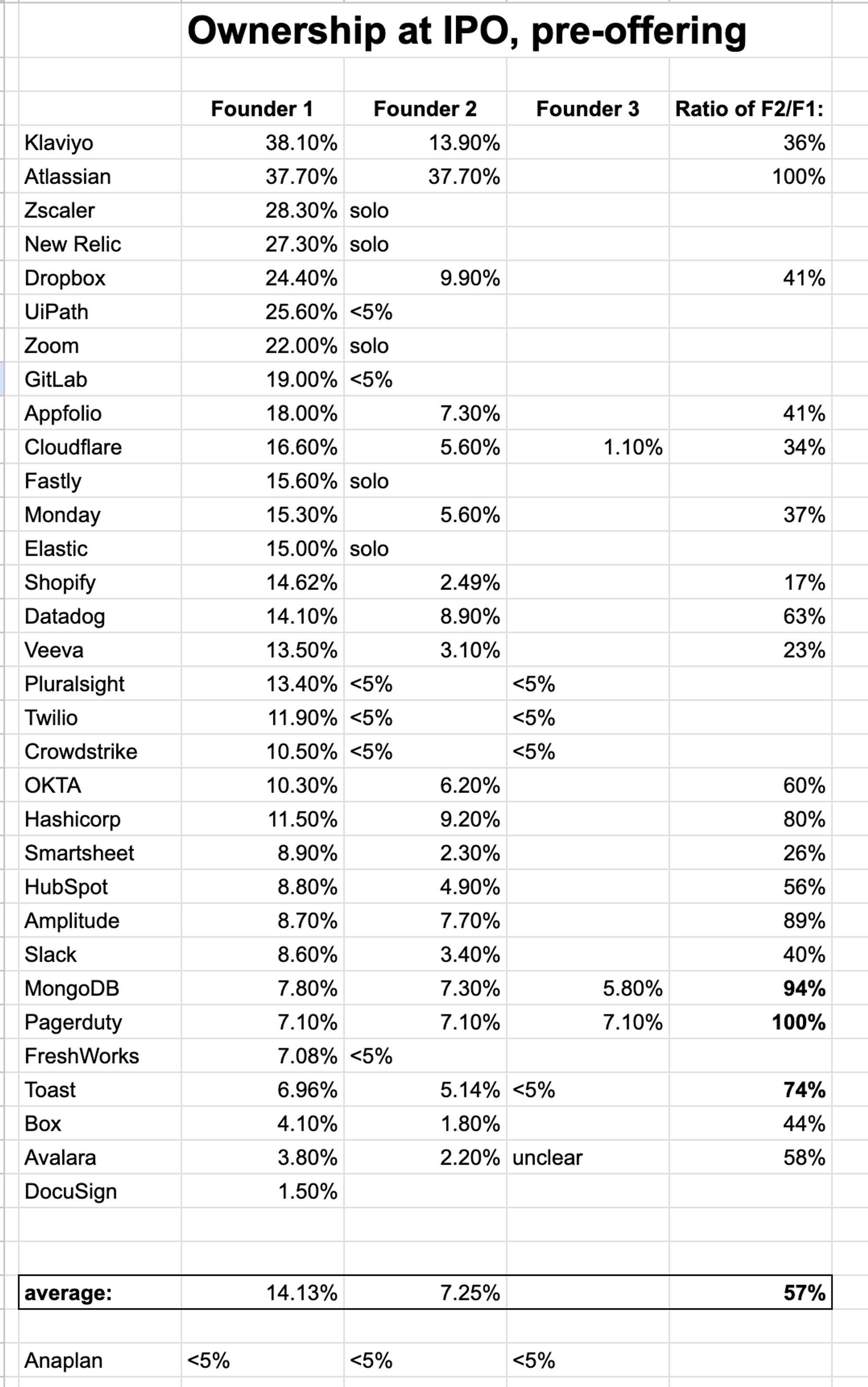

Thursday, Mar. 21st: I found great benchmarks on founders’ ownership at IPO. - Jason Lemkin, Meritech

“On 122 companies tracked by Meritech, 76 had founders who were still the CEOs at time of S-1 filing, & 46 had non-founder CEOs. The median for founder & CEO is 14.1% while the median for non-founder is 4.2%.”

Friday, Mar. 22nd: I read a post from Chris Dixon comparing early career choice to the hill climbing problem in computer science. - Chris Dixon

“How can smart, ambitious people stay working in an area where they have no long term ambitions?”

“There is a natural human tendency to make the next step an upward one. He ends up falling for a common trap highlighted by behavioral economists: people tend to systematically overvalue near term over long term rewards. This effect seems to be even stronger in more ambitious people. Their ambition seems to make it hard for them to forgo the nearby upward step.”

“People early in their career should learn from computer science: meander some in your walk (especially early on), randomly drop yourself into new parts of the terrain, and when you find the highest hill, don’t waste any more time on the current hill no matter how much better the next step up might appear.”

Saturday, Mar. 23rd: The Economist wrote about the impact of AI in healthcare. - The Economist

“In Europe analysts predict that deploying AI could save hundreds of thousands of lives each year; in America, they say, it could also save money, shaving $200bn-360bn from overall annual medical spending, now $4.5trn a year (or 17% of GDP).”

“Although AI has been used in health care for many years, integration has been slow and the results have often been mediocre. There are good and bad reasons for this. The good reasons are that health care demands high evidentiary barriers when introducing new tools, to protect patients’ safety. The bad reasons involve data, regulation and incentives.”

“Each year roughly 800k Americans suffer from poor medical decision-making.”

“The foundation models that power “generative” applications like ChatGPT have some serious drawbacks. Whether you call it hallucinating, as researchers used to, or confabulating, as they now prefer to, they make stuff up.”

“The shortage of health-care workers is predicted to reach nearly 10m by 2030—about 15% of today’s entire global health workforce. Artificial intelligence will not solve that problem on its own. But it may help.”

Sunday, Mar. 24th: Jack Altman (CEO at Lattice) shared a post arguing that AI is opening the door to disrupt existing systems of records (e.g. ERPs, CRMs) thanks to killer applications (e.g. automated sales reps, automated bug catcher and fixer) leveraging Gen. AI breakthroughs. - Jack Altman

“One of the most important concepts in software startup strategy is killer apps. Each platform ecosystem is surrounded by a set of applications of varying degrees of importance - the best of those are the killer apps.

In sales the system of record is the CRM, the database in which all customer data lives. Salesforce of course built many important applications around it, and integrates with thousands more. HubSpot began with applications around inbound marketing before backing into the CRM later. In HR you have the HRIS. Lattice started with one important HR application, performance management, before building several more, and then eventually an HRIS. When the iPhone first launched it spawned a huge number of new applications, some of which it built itself and some which were built by third parties.

Today we'd consider the killer apps things like messages, maps, musics — in most cases, there are both native and external products offered. One of the reasons Al is so important for the software landscape is because it shuffles the deck of possible killer apps. It opens up entirely new functionality that was simply impossible to build before; an automated sales rep, a robot bug catcher and fixer, a support agent that can triage many cases automatically.

This change is critical for two reasons. First of course, it opens up a bunch of new potential businesses. Second, and perhaps more importantly over the long term, it creates important new wedges, which gives the potential to unseat the major players over time and build new systems of record.”

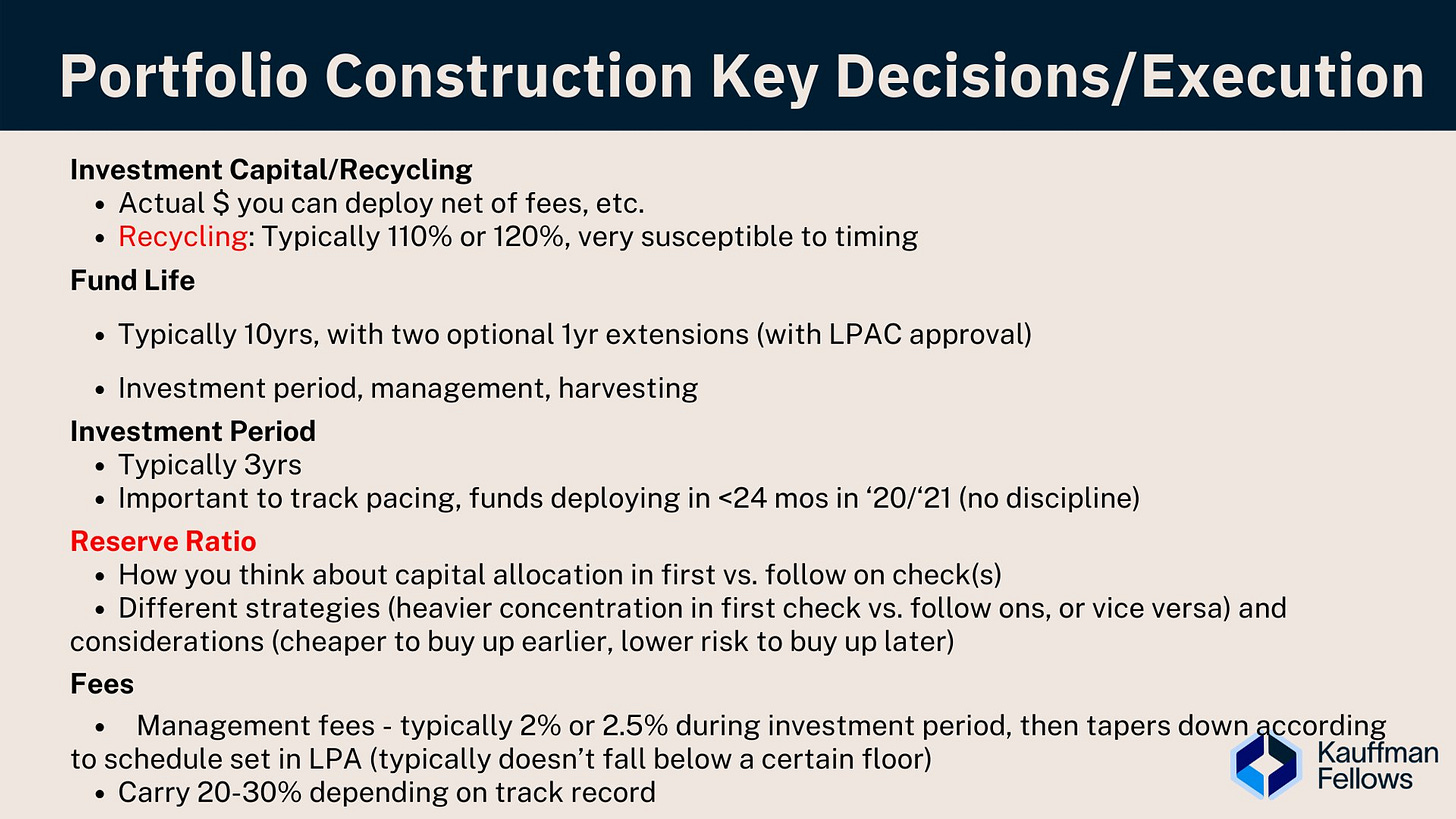

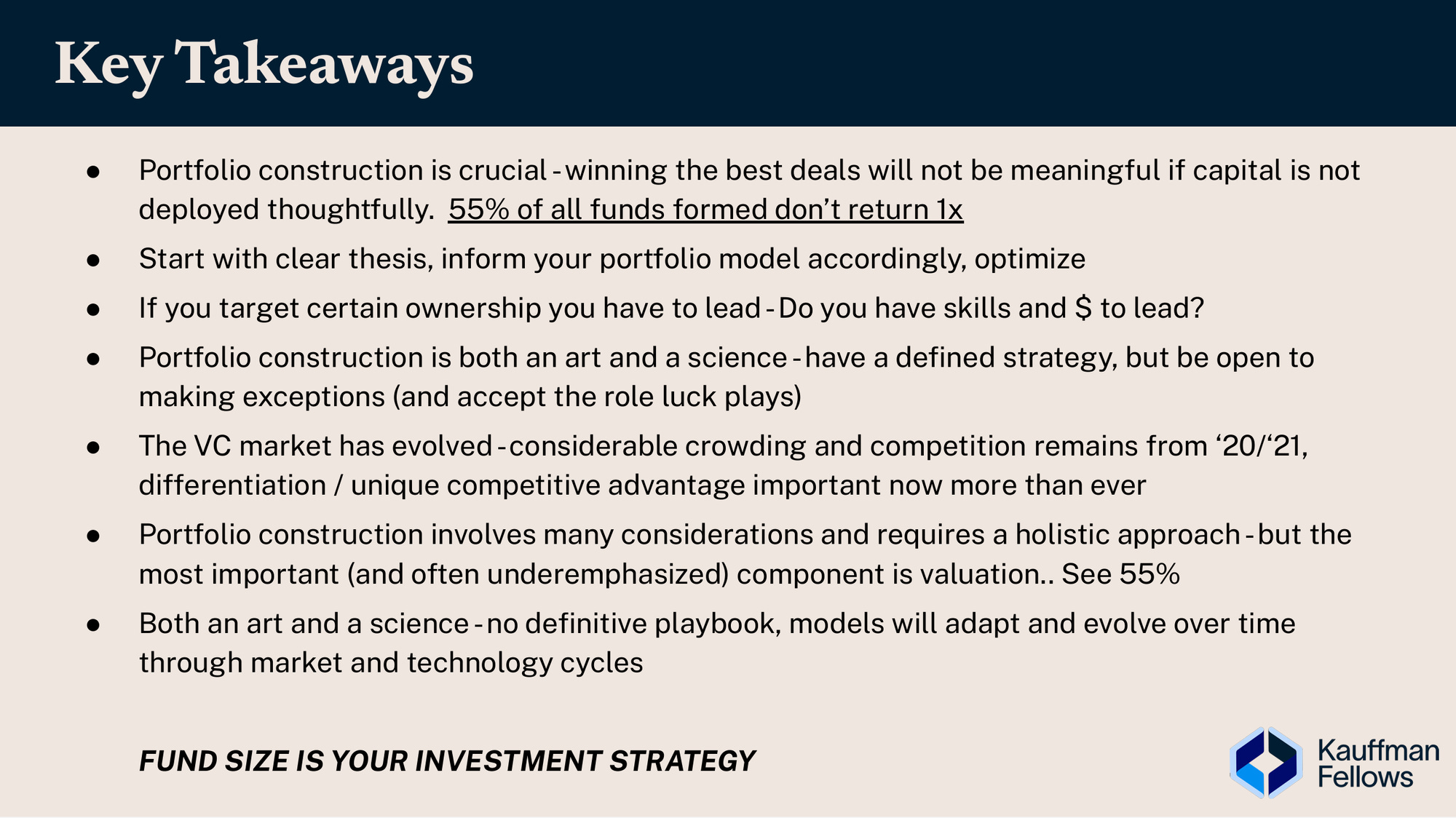

Monday, Mar. 25th: Bonfire’s cofounder Mark Mullen shared a slide-deck on portfolio construction for VC funds. - Bonfire

Tuesday, Mar. 26th: The Economist discussed the concept of the Magnificent 7, contending that it has lost its meaning. Companies are no longer following the same trajectory on the stock market, and they are not all perceived as winners in the AI revolution. - The Economist

“The band has broken up. One feature of the storming bull run that began on October 27th is that the Magnificent Seven have stopped charging as a pack.”

“Last spring the narrative was obvious: the Magnificent Seven would end up as the winners from the AI gold rush.”

“A year ago generative ai so enthralled investors that tech giants were assumed to be winners by default. Now that automatic benefit of the doubt is being withdrawn.”

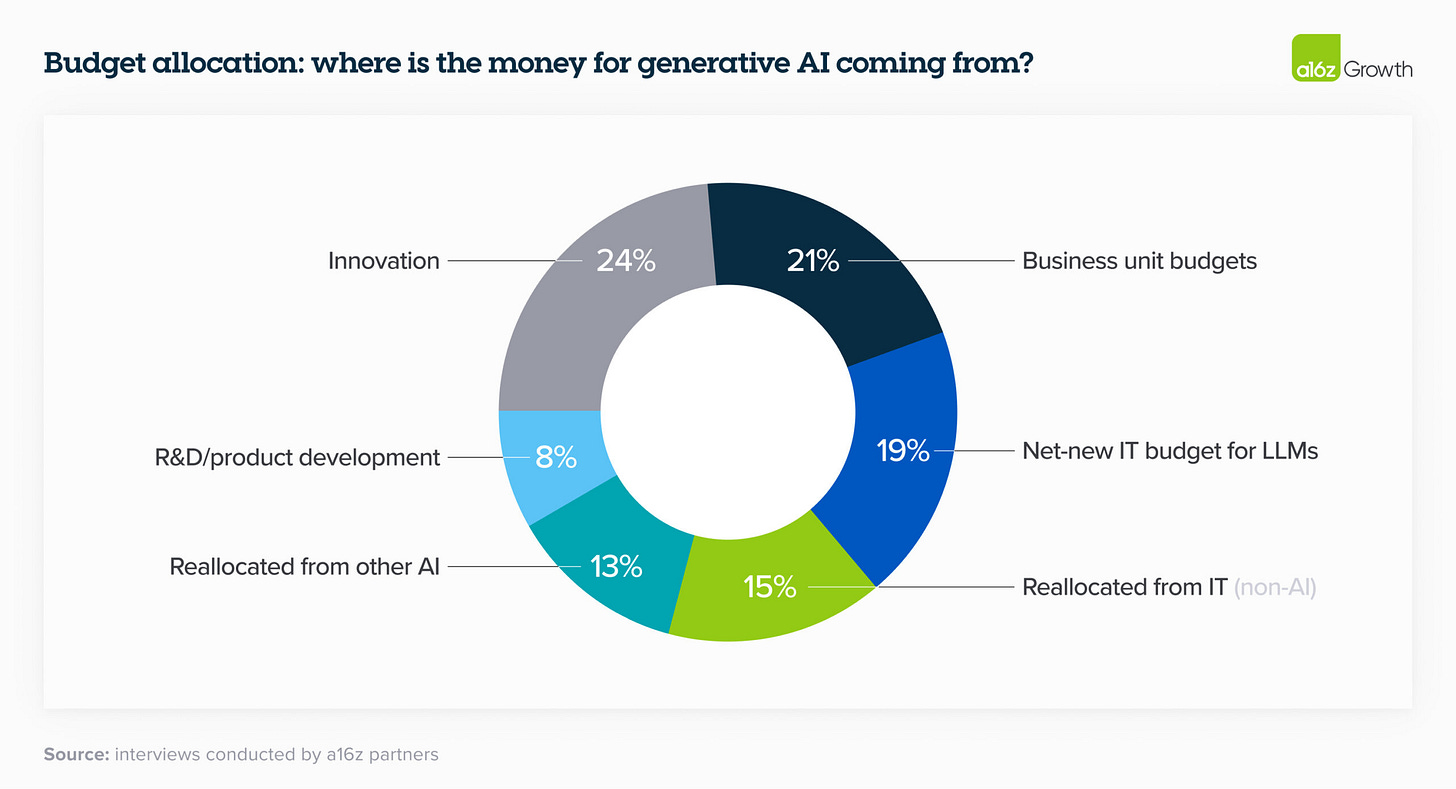

Wednesday, Mar. 27th: a16z shared their learnings of surveying F500 enterprise leaders on how they think about Gen. AI. - a16z

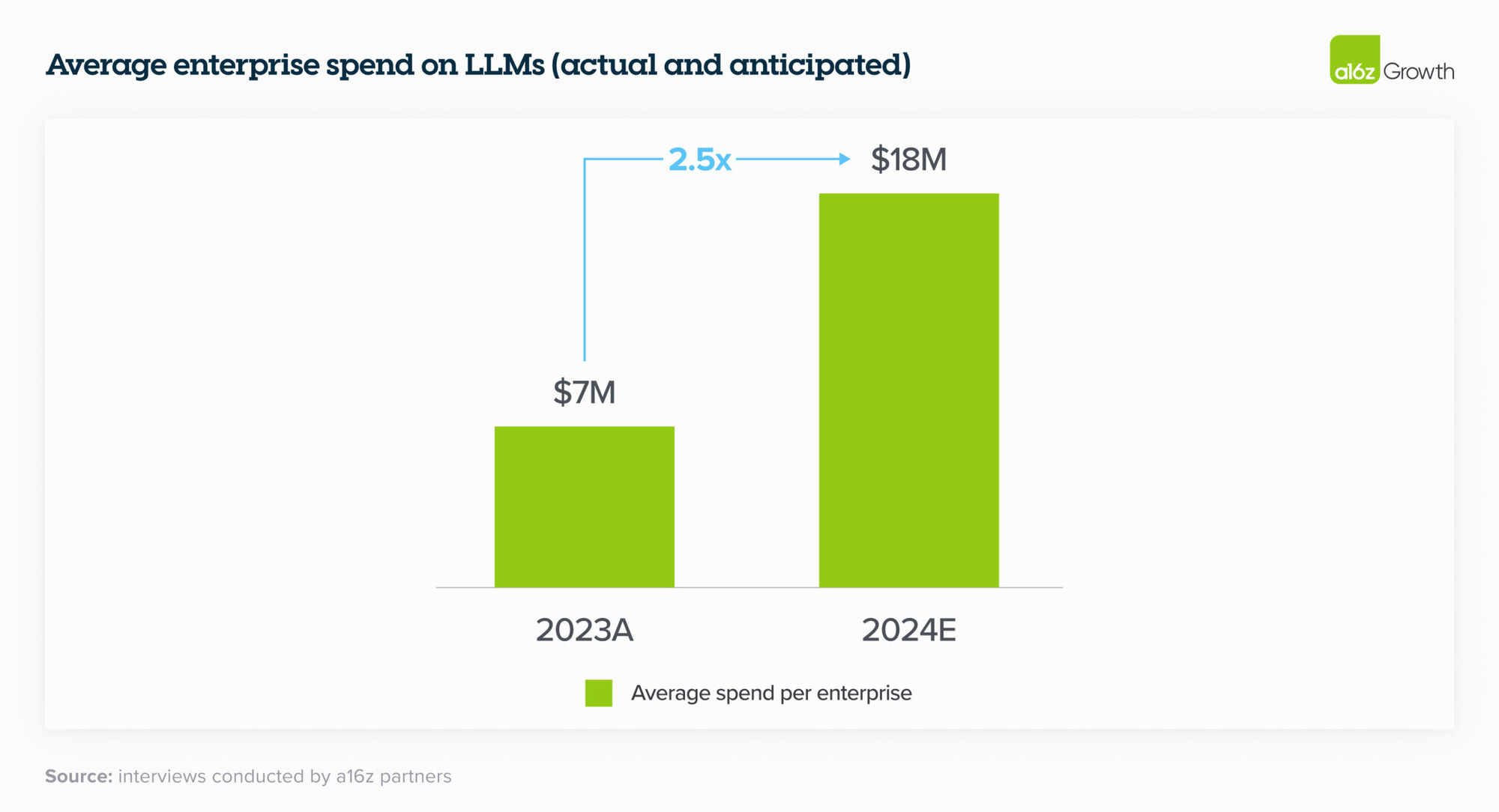

“In 2023, the average spend across foundation model APIs, self-hosting, and fine-tuning models was $7m across the dozens of companies we spoke to. Moreover, nearly every single enterprise we spoke with saw promising early results of GenAI experiments and planned to increase their spend anywhere from 2x to 5x in 2024 to support deploying more workloads to production.”

“Last year, much of enterprise GenAI spend unsurprisingly came from “innovation” budgets and other typically one-time pools of funding. In 2024, however, many leaders are reallocating that spend to more permanent software line items; fewer than a quarter reported that GenAI spend will come from innovation budgets this year.”

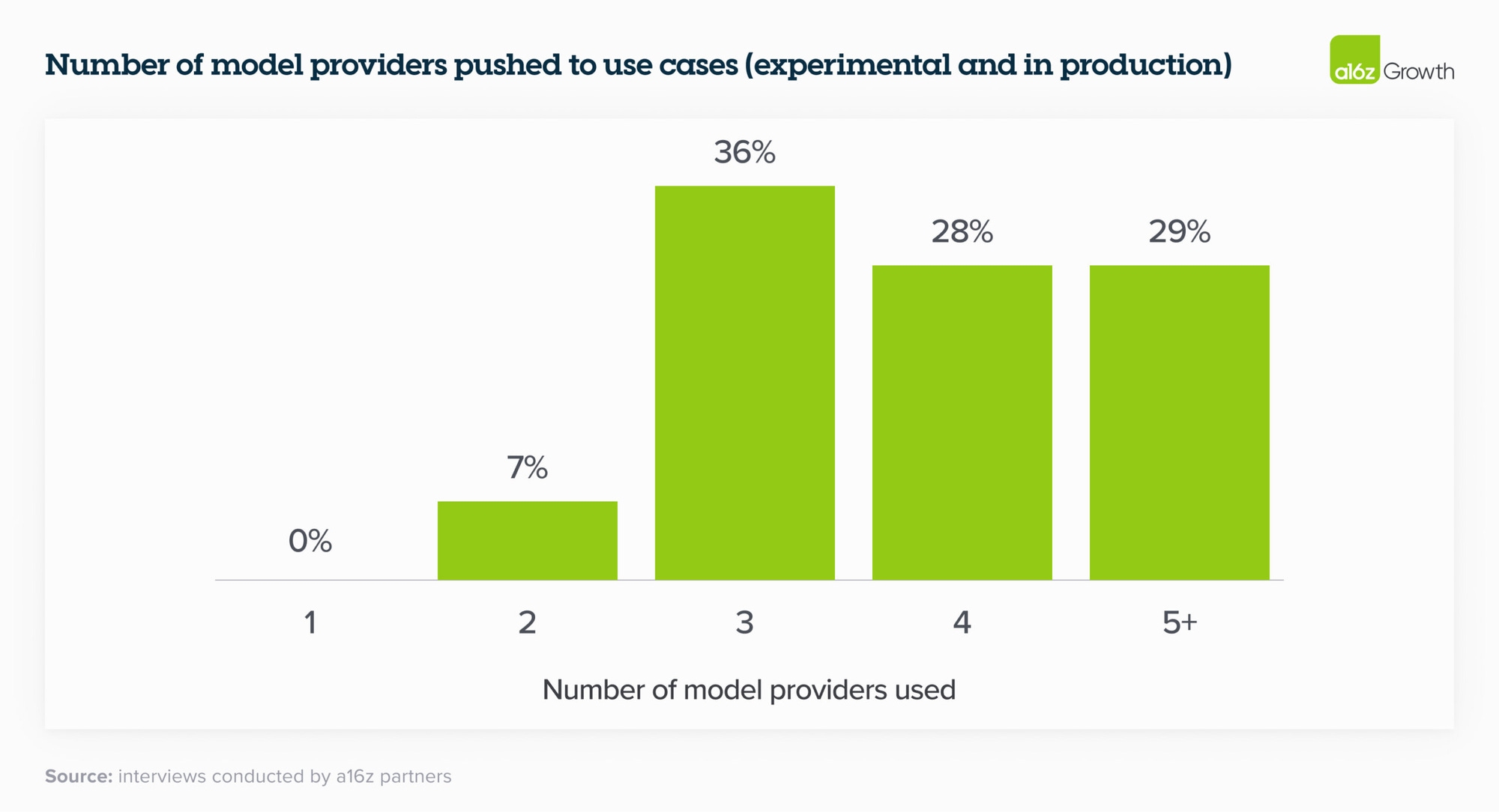

“Just over 6 months ago, the vast majority of enterprises were experimenting with 1 model (usually OpenAI’s) or 2 at most. When we talked to enterprise leaders today, they’re are all testing—and in some cases, even using in production***—***multiple models, which allows them to 1) tailor to use cases based on performance, size, and cost, 2) avoid lock-in, and 3) quickly tap into advancements in a rapidly moving field.”

“Most enterprises are designing their applications so that switching between models requires little more than an API change.”

“Enterprises are excited about internal use cases but remain more cautious about external ones. That’s because 2 primary concerns about genAI still loom large in the enterprise: 1) potential issues with hallucination and safety, and 2) public relations issues with deploying genAI, particularly into sensitive consumer sectors (e.g., healthcare and financial services). The most popular use cases of the past year were either focused on internal productivity or routed through a human before getting to a customer—like coding copilots, customer support, and marketing.”

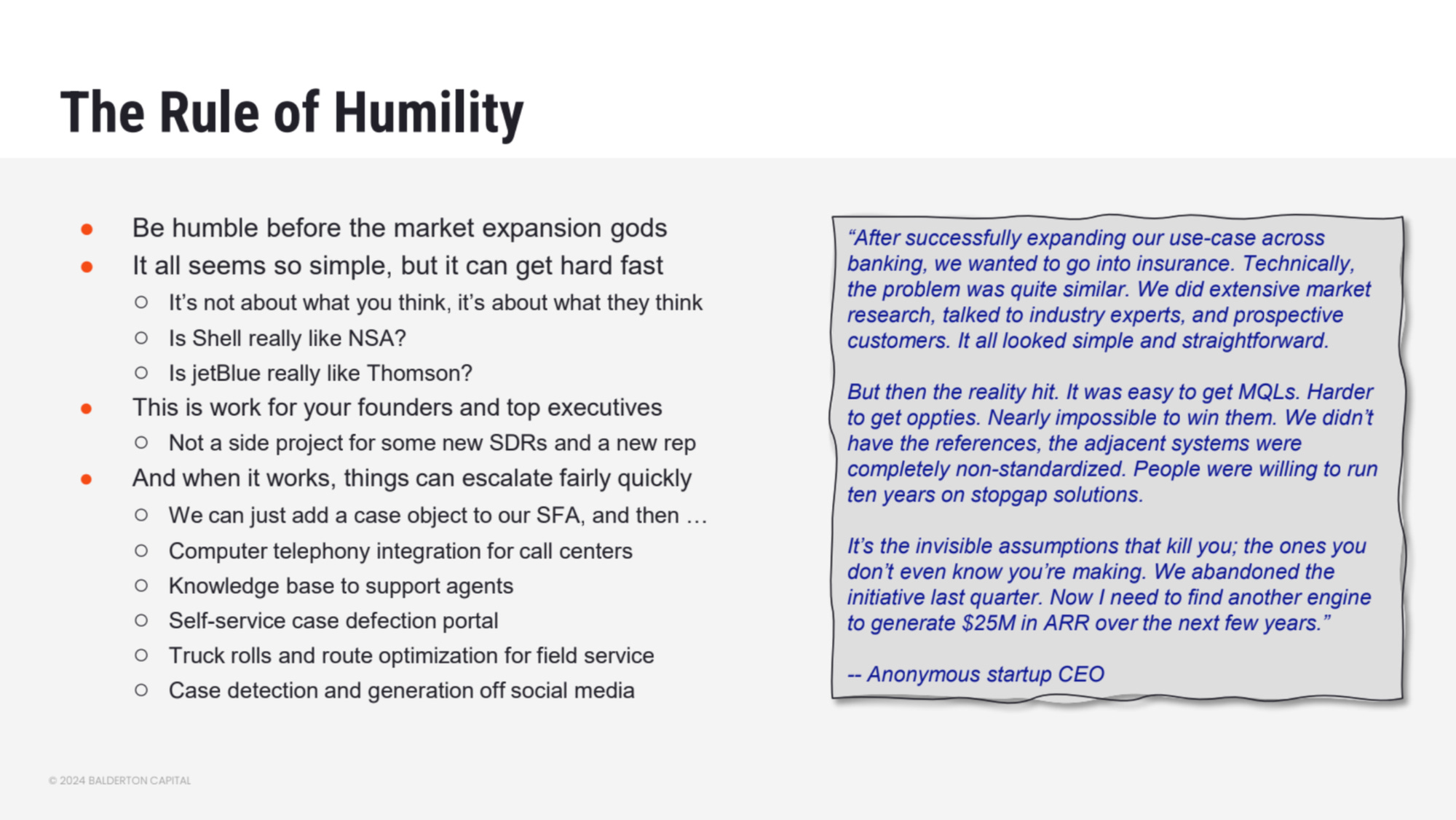

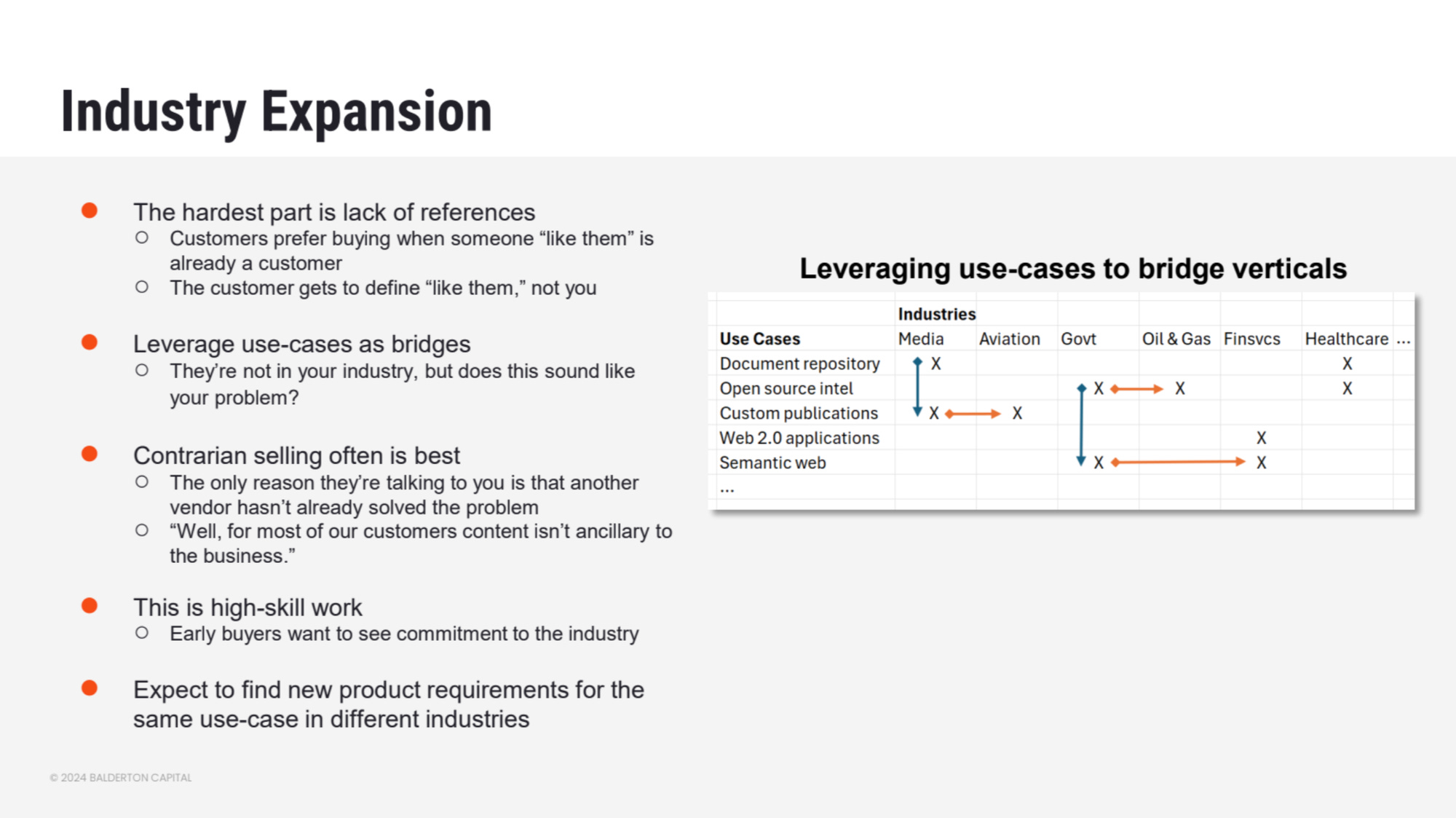

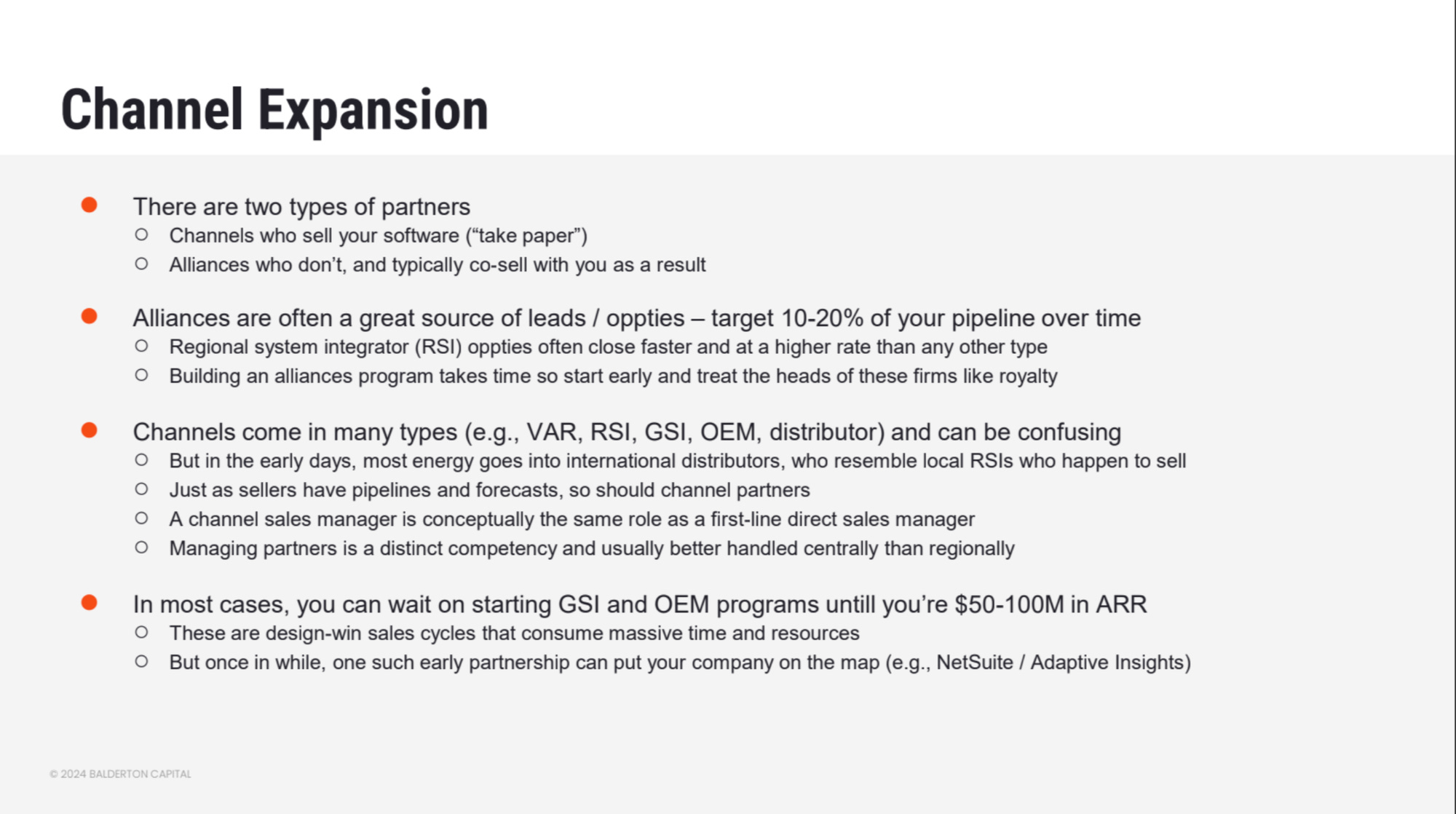

Thursday, Mar. 28th: Dave Kellog shared a presentation on efficient TAM expansion for startups. Dave Kellog is an entrepreneur in residence at Balderton. - Dave Kellog

Friday, Mar. 29th: PipeDreams raised a $25.5m series in the US from Canvas Ventures and Plural to roll-up HVAC and plumbing companies (100k businesses in the US) and augment them using software. PipeDreams is building software to help acquired companies around scheduling and marketing. - Techcrunch

It targets companies with more than $2.5m in revenues and 10 technicians focused on the residential repair and service businesses. PipeDreams is keeping the brand and the acquired team in place.

The marketplace model in this vertical “isn’t sticky as consumers can just seek out professionals directly after finding them through a marketplace.”

“PipeDreams is also addressing the skills shortage in the HVAC and plumbing industries, as Gen Z is less interested in learning trades than generations before them. The company launched an apprentice program in Q4 to allow people to get trained on the job. It’s had five students so far with plans to expand.”

Saturday, Mar. 30th: Thoma Bravo outlined the opportunity to acquire software companies in the public market during their annual meeting. Since 2008, there has been a tenfold increase in the market capitalization of public software companies. However, the average EBITDA margin of software companies has not significantly increased. This situation creates an opening for private equity funds, which can acquire these businesses and implement operational improvements.

Sunday, Mar. 31st: Fabrice Grinda wrote about what FJ Labs is looking for in B2B marketplaces. - Fabrice Grinda

“In most industries we have digital penetration below 5%, and it’s often below 1%. In most categories, there is no online catalog. There is no online pricing. There is no connectivity to the factories to understand manufacturing capacity and availability. There is no online ordering. There is no online payment, no order tracking. Insurance and financing cannot be ordered online. Whether it’s at large enterprises or small businesses, much is still done via pen and paper.”

“Baby boomers are retiring, leading to a shift in preferred purchasing behavior. Baby boomers preferred picking suppliers through RFPs (requests for proposals). Millennials, however, are digital natives and prefer ordering on online marketplaces.”

“We want small business owners to be able to do the jobs they love while the marketplace does everything else.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

So much value in one newsletter 🤯 Thanks for sharing. I particularly loved the insight by Smart Bear that startups win partly because they do illegal things and get away with it.