📖 Venture Chronicles - June 2025

Overlooked #201

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of June.

Sunday, Jun. 1st: I read a great post on why it’s so hard to build a competitor to Bloomberg. - The Terminalist

“Since the early 90s, Bloomberg has always been on somebody’s kill list. Oddly, the list of potential Bloomberg Killers has grown every few years and has never crowned a king. Many on the list instead ended up as road kill to Bloomberg’s growth story.”

"Imagine that your ISP (connectivity), browser (interface), OS (orchestration), app store (functionality), search engine (directory), social network (chat), and media houses (news & data) were all run and owned by a single company. That would require the company to be AT&T, Apple, Google, Facebook & News+Fox Corp all rolled into one. Now, transpose this idea onto the world of finance, and you'll begin to grasp what Bloomberg does.”

“While data is one of the various value layers in which Bloomberg operates, it is the golden goose. The Terminal, a firehose of information, is a modern marvel that feeds on multiple data resources that Bloomberg has cornered (e.g. for bonds & FX, data on pricing, liquidity, and trades).”

“In a winner-take-all market (due to network effects), a trader would struggle to trade, discover price or uncover inventory without a Terminal.”

“Bloomberg’s chat service (IB for Instant Bloomberg) was the first time multiple user types in the financial value chain were electronically connected across institutions. Before IB, customers, trading partners, dealers, counterparties, sales & account managers sat on different internal networks and only communicated with each other via email or phone. As more users joined, IB became more attractive to the have-nots.”

“Every seasoned user of Bloomberg swears by it. Once past the initial learning curve, the environment, the steady UI/UX, the shortcuts, the keywords, the response times, the consistency, the lack of unexpected changes, and the slow, incremental updates all cultivate a sense of comfort, familiarity and ease for the user. Familiarity & stability are key design and engineering values at Bloomberg, as is their attention to detail.”

“One of the masterstrokes in business history and competitive positioning was the creation of Bloomberg News. News drives prices, and price movement drives engagement. Not only did the Terminal provide users with real-time pricing, but it also provided the stories that affected it.”

Monday, Jun. 2nd: I read a post from Sameer Singh on companies combining SaaS and network effects on the same platform. - Sameer Singh

“Many B2B SaaS startups are also fairly defensible because they benefit from high switching costs, i.e. those that are a “system of record” become “embedded” in the day-to-day operations of their customers’ businesses which makes it difficult for competitors to displace them.”

“B2B SaaS companies become even more attractive when combined with network effects to create greater structural advantages for startups.”

There are two broad ways to combine SaaS & network effects:

(i) Using SaaS to enhance a network effect-based model (Opentable, Treatwell). You come for the tool and you stay for the network which solves the chicken & egg problem that many marketplaces have.

(ii) Using network effects to enhance a SaaS model (e.g. Carta, Salesforce, Atlassian). Software is not used to bootstrap or strengthen a network. Rather, SaaS is used to tap into a pre-existing (and sometimes offline) network or a secondary developer platform/marketplace is used to extend the use cases of the core SaaS product.

Tuesday, Jun. 3rd: DJI is facing a potential ban in the U.S. due to national security concerns. The company is lobbying lawmakers to prove it doesn't pose a threat, as it plays a significant role in American life. Without a scheduled security review, DJI could be automatically banned by the end of 2025, impacting millions of users. - Rest of World

“The most immediate threat of a ban comes from a clause in the 2025 National Defense Authorization Act, a U.S. law that sets the annual military budget. Passed in late 2024, it requires DJI to clear a national security review or face an automatic ban by the end of 2025. No review has yet been scheduled, and the legislation does not specify which agency should carry it out.“

“The U.S. government has said its push to restrict DJI is rooted in fears that the company’s drones could collect sensitive data for China’s military or intelligence agencies. But given DJI’s edge in cost and capability over its rivals, a ban would be difficult to implement.”

“For DJI, the stakes are immense. It said in 2021 that North America was its biggest market, but has not provided updated sales data in recent years. The global drone market will be worth $57.8 billion by 2030, according to Hamburg-based consultancy Drone Industry Insights. First developed in a college dorm room in Hong Kong in 2006 by founder Frank Wang, DJI commands about 70% of global drone sales. Its top-performing and relatively low-cost models are widely used by the police, firefighters, emergency responders, and professionals in science and media.”

“DJI isn’t the only Chinese firm to come under scrutiny. Besides TikTok, the U.S. has made efforts to bar BYD’s electric vehicles with high tariffs, and imposed sanctions on Huawei’s chips on national security grounds.”

Thursday, Jun. 5th: Deel reached $1bn in ARR only 6 years after its inception growing 75% YoY and having been profitable for 3 years. - Deel, Reuters

“What began as a product to hire and pay contractors is now a full payroll and HR suite that serves 35,000 customers and 1.25m workers in 150+ countries. Today we’ve been profitable for nearly three years and achieved 75% year on year revenue growth.”

“Deel, which acquired Safeguard Global's payroll division for an undisclosed amount in March, allocated an M&A budget of between $200 million and $500 million this year, CEO Alex Bouaziz told Reuters. The San Francisco, California-based company is still aiming for a 2026 U.S. initial public offering, but it depends on macroeconomic conditions.”

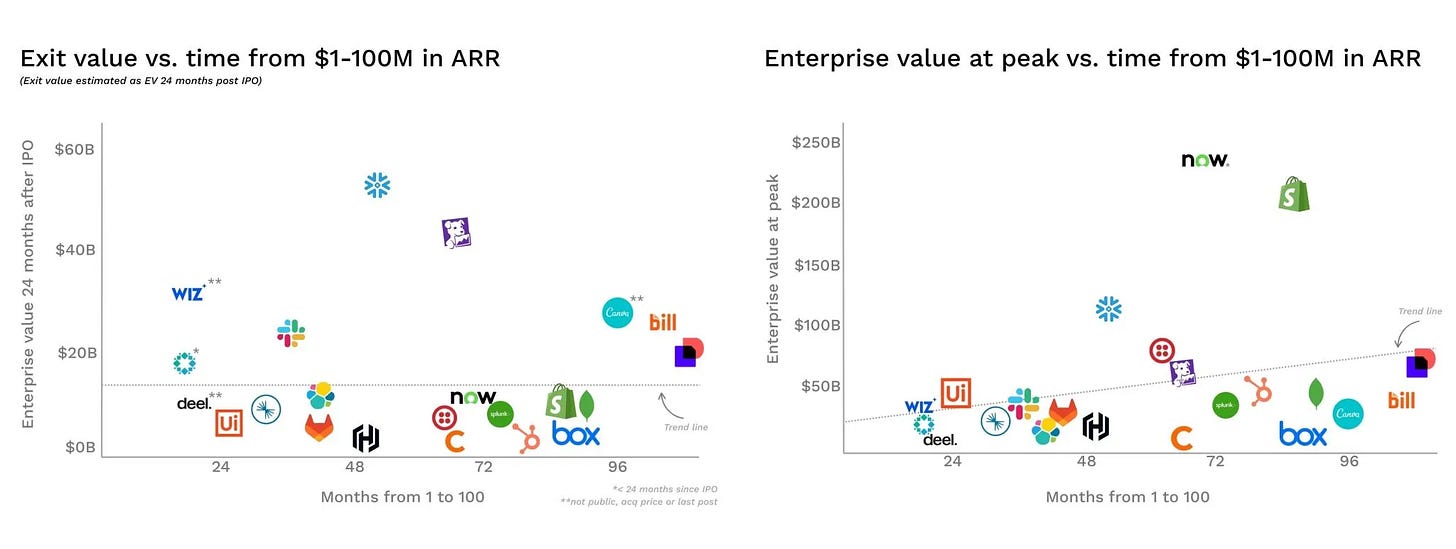

Friday, Jun. 6th: Reaching $100m in ARR doesn't guarantee a company's long-term success. There is no strong connection between how quickly a startup hits this milestone and its eventual value. - Maggie Basta

“There is actually no meaningful correlation between how quickly a generational startup gets to $100m in ARR and the magnitude of its eventual success.”

“$100m is a milestone (albeit an important one), but it’s not the final destination.”

Speed is not the only playbook. Time to $100m isn’t destiny, and some of the biggest outcomes took longer to get there while others around them grew faster.”

Saturday, Jun. 7th: Thoma Bravo raised $34.4bn across a new set of funds (US buyout, US growth and Europe buyout). - Thoma Bravo, WSJ

“Thoma Bravo, a leading software investment firm, today announced the completion of fundraising for its buyout funds totalling more than $34.4bn in fund commitments: Thoma Bravo Fund XVI, a $24.3bn fund, Thoma Bravo Discover Fund V, an $8.1bn fund, and as previously announced the firm’s first dedicated Europe Fund, with approximately €1.8bn in capital commitments.”

“Thoma Bravo’s core fund is now the biggest global private-equity fund closed in 2024 or 2025, surpassing Blackstone’s $21bn fund and EQT’s $23.7bn vehicle.”

“The firm has invested in more than 535 software companies, and today, its software portfolio includes over 75 companies that generate approximately $30bn of annual revenue and employ over 93,000 staff globally.”

“Thoma Bravo was among those paying big multiples for companies at the peak of the market in 2021. But the firm has been able to profitably exit a number of them. It recently disposed of the last of its stock in Adenza, which it sold to Nasdaq in 2023 for $10.5 billion. The investment resulted in a 35% annualized return, according to people familiar with the matter. Together, Thoma Bravo said its flagship and Discover funds have returned a total of more than $30 billion to investors since the beginning of 2023.”

“You have to be buying companies, and you always have to be selling.”

Sunday, Jun. 8th: There is a growing number of startups that are going public below their last private valuation mark showing that the venture capital industry is purging the excesses of the 2020-2021 tech bubble. - Axios

“Venture capital's distribution blockade may be breaking down, at least a bit, thanks to some unicorns finally accepting that their ZIRP-era valuations were inflated.”

“Circle is expected to price IPOs this week, at a valuation below where it previously was valued by venture capitalists. Hinge Health and eToro both recently went public below their private valuations.”

“There's a cohort of companies that have decided to stop endlessly circling their destination. And they've been rewarded, often with upsized IPOs and strong aftermarket performance. Hinge and eToro, for example, are up 26.4% and 17.8% from their IPO prices, respectively.”

Monday, Jun. 9th: Harry interviewed Kyle Norton who is CRO at Owner, a vertical software selling to restaurants. Owner does website, online ordering, email, text message, marketing, custom branded, app listing management, all rolled into one platform. Kyle scaled ARR from $2.5m to $40m ARR in less than 3 years. - 20VC

“Revenue leaders need to see sourcing amazing talents as one of the most core components of their job.”

In your recruitment process, you should have a programmatic way to identify the right talent on a consistent basis in a way that you can then have somebody else do it. There are 3 components to evaluate: (i) DNA/mindset, (ii) sales craft, (iii) specific knowledge.

In SMBs sales, it’s 70% DNA/mindset. “I just want people who have a performance track record of excellence, and I don't care if it was sales or not.” “When you do things, do you do it at a really high level? Are you curious? Are you coachable? Are you an absolute grinder? Do you have resilience?” “I’m hiring people early in their careers—honestly, 70 to 80% of it comes down to their DNA. I can teach them the rest. I’m very confident in our sales training program.”

“Now, all of our new SDR and BDR hires are five days a week in office in Toronto.”

Owner’s sales metrics: (i) $8-9k ACV (mix SaaS + payments), (ii) 50% close rate at demo, (iii) SDRs/BDRs are booking 2 meetings a day, (iv) 60% inbound & 40% outbound/partnerships, (iii) 4 demos booked per day per AE and 3 held as well as 2-4 follow-up calls from previous pipeline, (vi) 2:1 BDR-to-AE support ratio, (vii) inbound account executives are closing $250k per month, (ix) many restaurants are closed in one call and the average sales cycle is under a week.

To find strong BDRs, go to a company which is not number one in its category and hire its the top 2-3 performing BDRs.

BDRs’ variable compensation is only get paid on closed won business. AEs only get paid when their customers go live.

“What drags on your total sales cycles is actually time to lose more often than it is time to win.”

“We’ve also made tremendous upfront investments—in RevOps, enablement, data, and BizOps. To an outsider, these teams might seem oversized for the current size of our team and our ARR. But we’ve built these systems and foundations to drive increasing efficiency.”

Tuesday, Jun. 10th: a16z shared a benchmark on the growth of early stage B2B AI companies. - a16z

“Pre-AI, a common benchmark for best-in-class enterprise startups was $1 million in ARR in its first 12 months.” “The median enterprise company in our sample set reached more than $2 million in ARR in its first year, raising a Series A just nine months post-monetization.”

“While the bar has been raised across the board, top performers are really pulling away. Many of these breakout companies continue to pick up steam through their first year, rather than seeing growth start to slow (as we often saw in the pre-AI era).”

Wednesday, Jun. 11th: Private asset managers are making alternative investments more accessible but sometimes with contestable fee structure - illustrated by Hamilton Lane - which are expensive and sometimes misaligned with long-term investor outcomes. - WSJ

“Giant firms like Apollo, BlackRock, Blackstone, Capital Group, KKR, State Street and Vanguard Group are all rushing to get individual investors to buy “alternatives,” including hedge funds, venture capital, and nontraded debt, equity and real estate.”

Hamilton Lane is known for buying chunks of private-equity funds in the secondary market at a discount to the net asset value. Post purchase, they mark up the value back to the original net asset value.

“Under the old contract, Hamilton Lane couldn’t collect more incentive fees because the gains on the fund’s underlying assets were unrealized. In fact, if the assets turned out someday to be worth less than Hamilton Lane says they are, the manager might never have earned some of those fees.”

“From now on, the incentive fee will be payable across the entire fund, not on each deal measured independently. The new fee is payable not just on realized gains, but on unrealized gains as well. That means Hamilton Lane no longer has to wait to sell each secondary holding at a gain of at least 8% to take its cut.”

Thursday, Jun. 12th: Dave Yuan wrote about the race in vertical software to become the system of action with AI doing the work when the previous generation of software was only helping to do the work. - Tidemark

“A system of action is the next step beyond the system of record, where humans, AI-assisted humans, and fully autonomous AI agents are able to act on data and trigger downstream workflows.”

“Historically, software helped a business run. It automated front-and back-office functions that weren’t the core activity of the firm itself. Generative AI is opening a new frontier—doing the work itself.”

““Doing the work” also creates an opening for native AI challengers to gain a foothold and “integrate & surround.” In industries where there are “Hero users” with strong agency to choose their own tools, “doing the work” can shift the locus of control.”

“Vertical SaaS has historically focused on running and managing a business, not doing the actual work of the business itself.” “The goal of vertical SaaS generally is to provide workflow software to owners and managers to operate the business consistently, efficiently, and profitably. And, because they sell to owners, they haven’t always needed delightful user experiences to be successful.”

“Hero users are those who: (i) are highly influential and valued because they are scarce or add unique value, (ii) are solo contributors or work independently and (iii) have agency within the company to choose and buy tools independently.”

“Well the system of record (i.e. the control point) is the logical incumbent. But if a native AI player is able to win the hearts and minds of the Hero users, they can flip the script and become the system where downstream actions are decided and triggered. They can usurp the system of record’s data gravity and become the system of action.”

“Once you have acquired a meaningful community of these customers and they are finding daily delight in your wedge, you can “integrate and surround” the incumbent’s control point. Your goal is to integrate into the system of record. You’ll start with scrappy tactics: copy/paste, Chrome extensions, RPA. But when you reach scale, have your users demand integration for you. This is the moment you start beating down the incumbent and getting aggressive. Pull in or replicate core functionality from the system of record into your own product.”

`Friday, Jun. 13th: I listened to an Invest Like the Best’s podcast episode on the state of venture capital with Bill Gurley who was General Partner at Benchmark. - Invest Like the Best

Trend n°1: continued rise of mega VC funds.

“When I first started, everything was bespoke, most of the well branded funds were focused on early-stage. They didn't participate in late stage and the funds were modest compared to today. Today, many of the branded firms have moved from maybe $500 million commitment every three or four years to $5 billion, so 10x. And they're participating very actively in what we would call late-stage.”

Several historical VC firms have moved up market (GC, Lightspeed) and new parties have entered the late stage market with different approaches (Fidelity, Altimeter, Thrive, Softbank).

Trend n°2: zombie unicorns with c.1k companies which raised money at a valuation over $1bn during the ZIRP period and need to be purged from the system

“They've raised somewhere between $200 and $300 million each. And so you roll all that up, it's $300 billion.”

“There's a question as to what they're worth. The investment world doesn't seem excited about this group of companies. They don’t have super high growth rates, they are barely profitable and no-one in the system has an incentive to reset their valuation.”

When you raise that much money, a couple of things happen. First, you end up with too many participants in a single field where you would have had whittling earlier. It makes market expansion more difficult because there's three to five survivors instead of one or two. Second, companies end up misallocating capital doing too many things at the same time and subsidising growth.

Trend n°3: stalled IPO and M&A markets in recent years

“If you look at last year, 2024, the NASDAQ was up 30% and the window was closed.” “ Never in my history of paying attention to the capital markets or being in venture capital you have a successful NASDAQ market in a closed window.”

On the IPO side, (i) there is a massive IPO discount that banks force upon the market, (ii) the cost of going public is too high, (iii) there is enough money in the private market so that the best companies can stay private forever.

Trend n°4: LPs have a liquidity problem

“US colleges and universities issued $12 billion of debt, which was the third highest quarter ever. If you're using debt to fund capital commitments because your endowment doesn't have the liquidity it needs to pay out the 3 or 5% or whatever it is that they always had traditionally paid out.”

Harvard ($1bn) & Yale ($6bn) are in the market selling private equity assets in secondary.

Trend n°5: “The VC market never had a full correction post ZIRP here because AI came along and everyone got so excited”

“Despite the fact that the traditional LPs are tapped, VC firms were able to go find money elsewhere (e.g. Middle East, retail investors).”

Trend n°6: The best VC-backed companies (e.g. Stripe, Databricks) can decide to be private forever

“Why take on the additional burden of extra work and scrutiny and data disclosure, and show your competitors what you're doing and all this kind of stuff if functionally you have your own captive private market?”

“Late-stage firms turn around and go to the LP community saying companies are no longer going public when they used to. If you want exposure to that growth in these important high-tech companies, you have to invest in me.”

“The number of total public companies in the US is way down from peak. There are less IPOs because IPOs are extremely expensive with a 26% average underpricing and a 7% fee leading to a 33% cost of capital.”

“Coatue used to have a $5 million minimum for a commitment. They're taking it down to $25,000 or something, and they're going to work with an investment bank to place it.” VC and PE funds are trying to unlock retail investors as new source of capital.

“Founders are forced to play the game on the field. An overcapitalised market forces everyone to go all in and swing for the fences. I lived it in the Uber-Lyft situation. With AI, we're going to have that type of capital battle in every category under the sun.” “If your competitor raises $300 million and is going to 10x the size of their sales force, you will be dead before you know it.” “If someone is going to pay 30x revenue and force you to play a game that you're not comfortable playing by burning hundreds of millions a year, you should probably take a little off the table.” “It’s bad for the ecosystem that we are going to remove all the small and middle outcomes and just play grand slam home run ball all day long.”

Saturday, Jun. 14th: Euclid wrote on voice as the biggest opportunity to reinvent vertical software in the age of AI. - Euclid

“Conversational voice agents may represent the most significant opportunity in Vertical AI today. While many early voice AI breakouts have focused on speech-to-text transcription use cases (Abridge in medical scribes, Rilla in sales coaching, etc.), we believe the largest long-term opportunities will emerge from conversational, speech-to-speech uses.”

“Early conversational voice agents also possess a unique advantage in adoption: despite their shortcomings, phone-based communications remain mission-critical for nearly every vertical market.”

“Unlike AI implementations that demand significant systems integration or workflow redesign, voice agents can seamlessly join any phone-based communication.”

“From a market perspective, we’ve seen a few clear, consistent patterns emerge in voice agent adoption: (i) phone-centric: a vertical market where the phone is the preferred medium for customer-facing sales, support, ops, etc., (ii) measurable outcomes: calls are constrained in length and complexity, with a pre-defined range of outcomes, (iii) revenue-generating: customers can book more business, collect more money, or save on back-office costs.”

“The most ambitious Vertical Voice startups aren't stopping at single use cases. They're using voice as a wedge to capture broader platform opportunities within their target markets.”

Sunday, Jun. 15th: I read an investment thesis on Amplitude which is a digital analytics platform that helps businesses understand user behavior. - Un Tiro Al Aire

“AMPL isn’t just a SaaS player; it’s a royalty on the growth of its enterprise clients (27 of Fortune 100 and growing), thriving as they scale in the product-led growth (PLG) era.”

“The blurring lines between marketing and product teams—coupled with a shift to first-party data amid privacy crackdowns—supercharges AMPL’s total addressable market (TAM). Companies need a unified view of user interactions to survive in a post-third-party-data world. AMPL’s platform bridges this gap, positioning it to grab a bigger slice of enterprise budgets.”

“Regulations like GDPR and CCPA are killing third-party data. Companies must pivot to first-party strategies, and AMPL’s platform is tailor-made for this shift. As businesses race to adapt, adoption could accelerate, increasing revenue beyond the 12% ARR growth seen in Q1 2025.”

“Skates is building for 5-10-year horizons. His push into AI agents and marketing-product convergence shows solid ambition to widen AMPL’s moat.”

Monday, Jun. 16th: Mario Gabriele wrote on venture firm Founders Fund created by Peter Thiel in 2005. - The Generalist

“Since launching in 2005, Founders Fund has grown from a $50 million inaugural fund, with a novice investing team and little brand equity, into a Silicon Valley powerhouse, boasting billions under management and what looks like the best full-stack investing team in the industry.”

“Concentrated bets on SpaceX, bitcoin, Palantir, Anduril, Stripe, Facebook, and Airbnb have delivered a string of hit vintages even as fund sizes have grown. In its 2007, 2010, and 2011 vehicles, Founders Fund can lay claim to a trio of the asset class’s best-ever vintages, producing gross multiples of 26.5x, 15.2x, and 15x from $227 million, $250 million and $625 million, respectively.”

Tuesday, Jun. 17th: Bloomberg wrote on international athletes playing on Chess.com. - Bloomberg

“It’s also a testament to the growing popularity of chess among professional athletes and Chess.com’s unique role in democratizing the market for online play.”

“Athletes playing chess is not a new phenomenon. Professionals from the worlds of boxing (Lennox Lewis), basketball (Wilt Chamberlain), baseball (Barry Bonds), football (Jim Brown) and soccer (Johan Cruyff) have all been known to enjoy the game. No less an authority than grandmaster and five-time World Chess Champion Magnus Carlsen has repeatedly pointed out the strategic similarities between chess and soccer and basketball.”

“Before chess migrated online, athletes who played were regarded as anomalies — jocks doing nerd things. Then the smartphone came along, giving rise to short-format versions of the game. Apps such as Chess.com put the ancient game in everybody’s pocket and allowed casual players to be matched up instantly with opponents of equal skill. That shift changed the commitment needed to play and, in turn, the perception of chess itself.”

“Online chess is mostly free from such entanglements, allowing athletes to have encounters with regular people without the interference of celebrity.”

“Between June 2020 and December 2022, accounts on the site jumped from 35 million to 100 million. (It had taken 14 years to bring in those first 35 million.) And unlike pandemic darling Peloton, Chess.com didn’t suffer in popularity when lockdowns ended. The site recently announced its 200 millionth signup, and monthly active users are holding steady at 35 million. Chess.com routinely hosts 25 million games per day.”

“The privately owned company, founded in 2005 by Allebest and Jay Severson, makes most of its money from subscribers, who pay $5 to $15 a month for features such as unlimited play and postmatch analysis. Allebest says annual revenue is more than $100 million.”

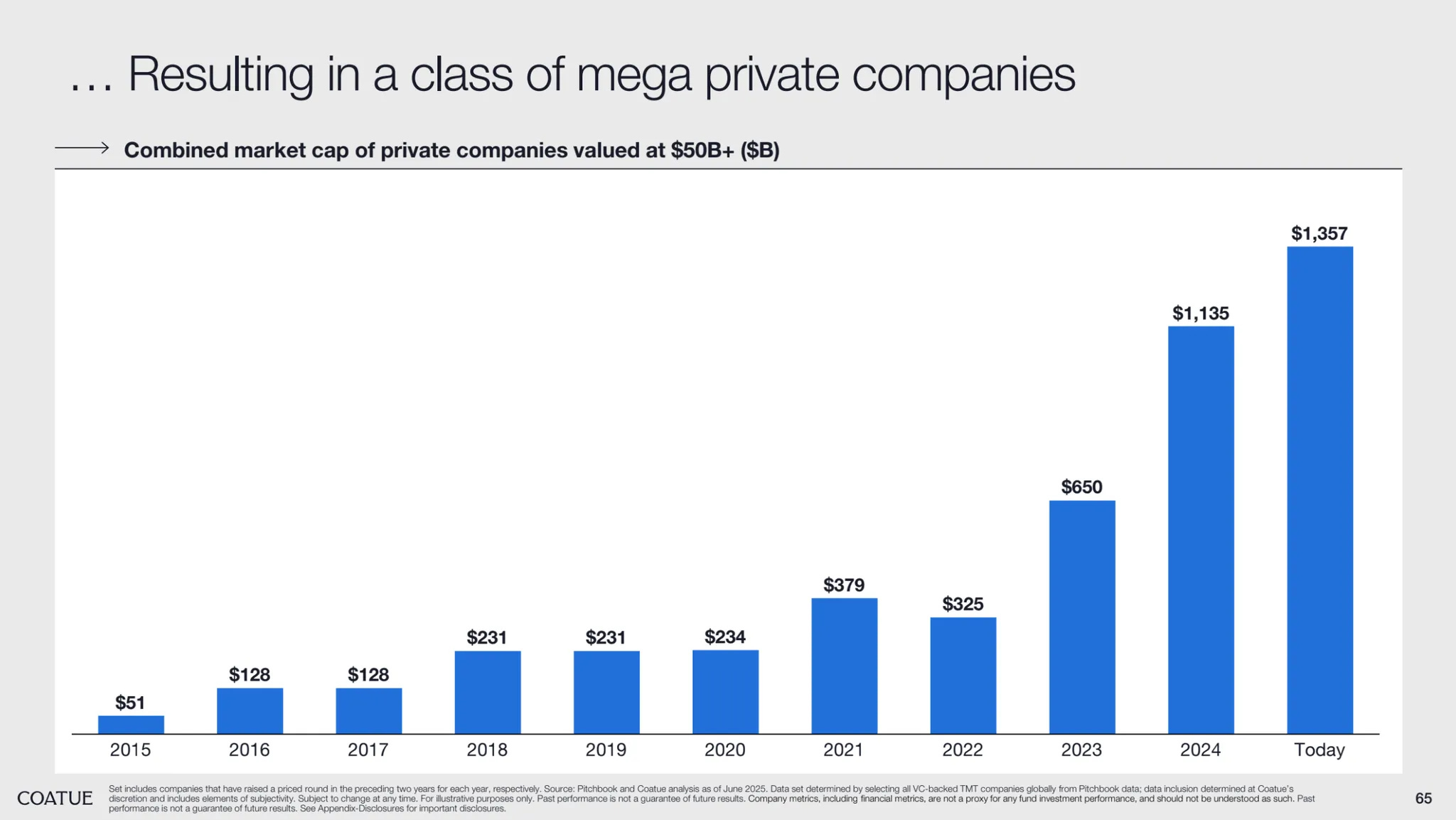

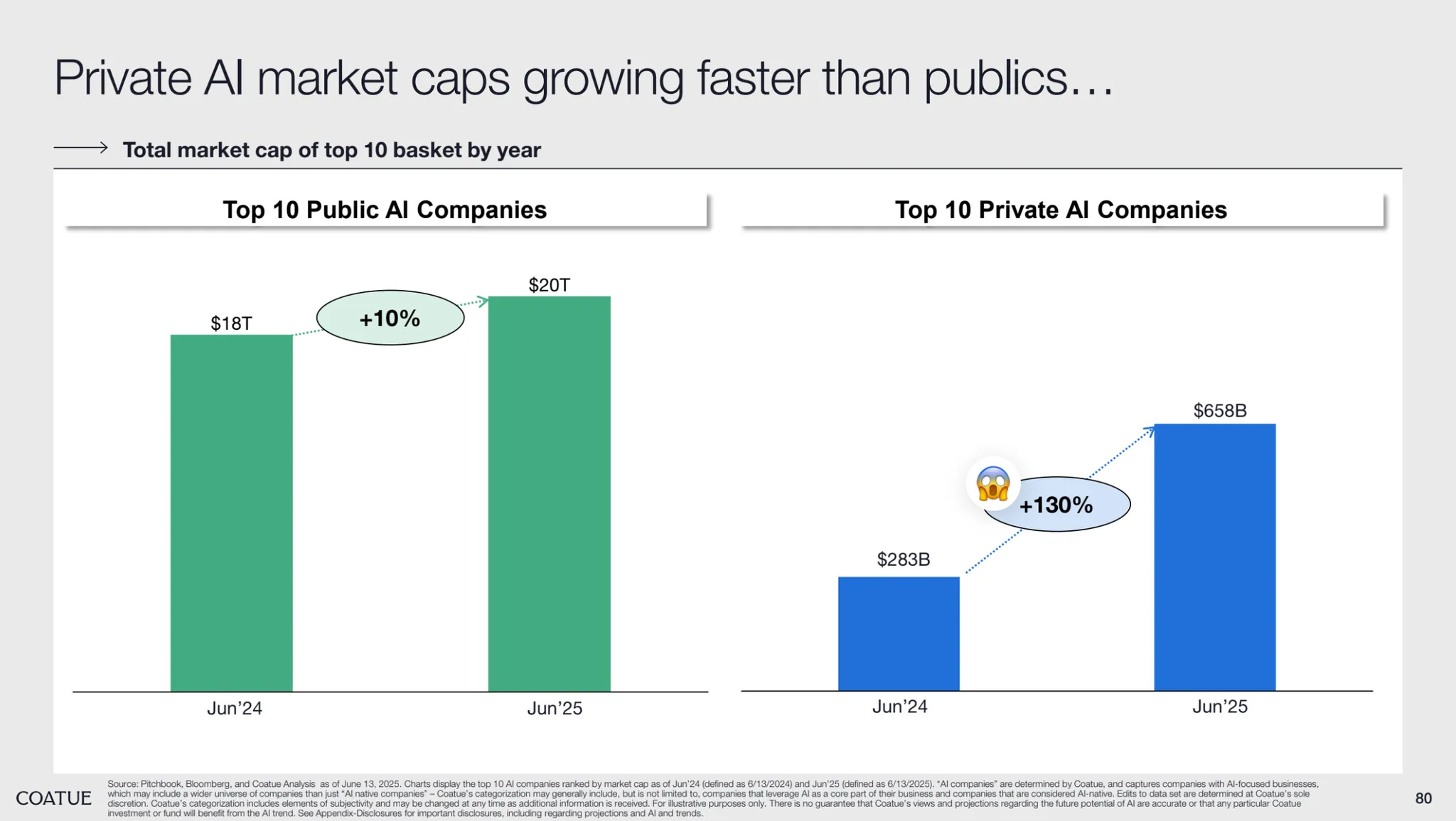

Wednesday, Jun. 18th: Coatue published its annual East Meets West presentation on public and private markets. - Coatue

Thursday, Jun. 19th: Nathan Benaich and Nikola Mrkšić argued that it’s a fallacy to roll-up services firms and reshape their unit economics with AI believing that the generated entity will have software multiples. - Fortune

“Generative AI will transform low-margin service businesses into high-margin software companies. Several well-known platform venture firms have committed billions to this strategy and have begun to make their bets.”

“On paper, it’s brilliant arbitrage. In practice, it’s a mirage. It rests on a fundamental category error: confusing operational improvement with business model transformation. Yes, AI can make workflows more efficient. No, that doesn’t turn a services company into a software company.”

“Consider Concentrix, often cited as a BPO transformation success story. Despite a major push in launching their gen-AI products in 2024 and now having deployments at over 1,000 customers, the company’s EV/EBITDA multiple remains stuck in the low single digits, and its EBITDA margin is still hovering around 10%. The market’s message is clear: Automating workflows doesn’t change your fundamental business model.”

“Efficiency improvements that reduce billable hours directly cannibalize revenue. As PolyAI discovered, BPOs promise innovation to win contracts, then revert to maximizing billable hours to protect margins. It’s a business model fundamentally at odds with automation.”

“Services businesses aren’t inefficient by accident. They’re inefficient by design. The inefficiency is the product. Clients pay for flexibility, customization, and someone to blame when things go wrong.”

Friday, Jun. 20th: I read a detailed investment thesis on Grab. It’s a Southeast Asian super app offering ride-hailing, food delivery, payments, and financial services. - Amit

“I believe Southeast Asia is going to be a monster emerging market in the next decade and Grab will be able to consistently compound their network effect by 20% every year.”

“The company currently is trading at 47% cash, meaning for every dollar you buy of Grab, you are buying 47 cents of pure cash.”

“The biggest issue with Grab is that their margins are not good. My argument against that was as the company gains operating leverage, their margins will increase, and the cash on the balance sheet will cushion most of their efforts to get that margin expansion with their topline revenue growth.”

“Now, there are 700m people in the SEA region. This means their penetration is less than 6%. Many of these people are just entering into the digital age, which means they will need a bank (Grab offers that) mobility, and deliveries – along with all of the other things the app provides which is the superapp thesis.”

“Two incredibly large opportunities for Grab are advertising and financial services. Their financial services business is growing about 40% YoY and is not profitable yet on an adjusted ebitda basis but the company is guiding for them to be breakeven by 2026. Advertising is another huge opportunity – as of Q1 2025, they had 191K active advertisers which is only 3% of their 6M merchants. Their take rates on ads is about 1.7%, increasing YoY, but still relatively small.”

Saturday, Jun. 21st: Adnan Esmail, former SVP of Engineering at Anduril, shared insights about the company’s engineering culture. - Colossus

“Anduril was never just a job; it was part of my identity. My badge still worked, I continued on in an emeritus role, and I still spent around 15 hours a week working with the engineering team I’d helped build.”

“When I joined Anduril in the fall of 2018, I was employee #20, the company was valued at $250 million, and we had lofty, but hypothetical, ambitions of reinventing the defense ecosystem. Less than six years later, the 4,000-person, $28 billion company has deployed 30-plus products with thousands of fielded systems, and changed the arc of American defense technology.”

“While the threat from China wasn’t yet front-page news, Palmer and his team had already recognized the need for better defense technology to deter a great power conflict and to maintain American hegemony. They understood that America’s technological edge in defense was eroding, and that traditional defense contractors were too glacial and bureaucratic to meet the challenge.”

“It reflected our approach: get to a minimum viable demonstrator, something that creates end-to-end capability, then iterate ruthlessly.”

“Each product therefore had to embody our chief working principles: move fast with purpose; question everything; take ownership; keep it simple; hold high standards; and design with deployment in mind.”

“Every project at Anduril had a directly responsible individual (DRI)—a single owner accountable for the outcome from end to end. Sometimes ownership meant taking extraordinary measures when the stakes were high.”

Sunday, Jun. 22nd: Traditional systems of record are responding to AI disruptors building on top of their platforms by either acquiring these innovators or restricting access to their data. - Tom Tunguz

“Systems of record are recognizing they cannot “take their survival for granted.” One strategy is to acquire: the rationale Salesforce gives for the Informatica acquisition. Another strategy is more defensive - hampering access to the data within the systems of record (SOR) (e.g. Salesforce shutting down access to Slack’s API). Unlike the previous software era where SORs built platforms on top of themselves to develop broader ecosystems (in Salesforce’s case Veeva & Vlocity), the AI shift does seem to be more defensive.”

Monday, Jun. 23rd: AI’s value capture is shifting from commoditized models to interfaces where users interact, decide, and generate feedback. Startups capturing domain-specific interfaces—like legal tech, logistics, or procurement—gain an edge, as these become decision hubs and data sources. - Merantix

“The real leverage is moving to the interface layer (as in: how people are actually interacting with AI). This is where users make decisions and generate the feedback that improves the system.”

“We’re witnessing interaction move from something active and controlled to something embedded and passive.”

“Interfaces are no longer just access points. They define how we unlock the value of backend AI systems, where a good user interface allows the true potential of AI functionality to be unlocked.”

“Everyone is realizing that the interface is the control point. While one might think that reality favors incumbents, this also creates a huge startup opportunity.”

“By embedding themselves in the day-to-day work of operational teams, they gather data that improves the product, reinforce habits that are hard to unlearn, and position themselves as the primary system of record.”

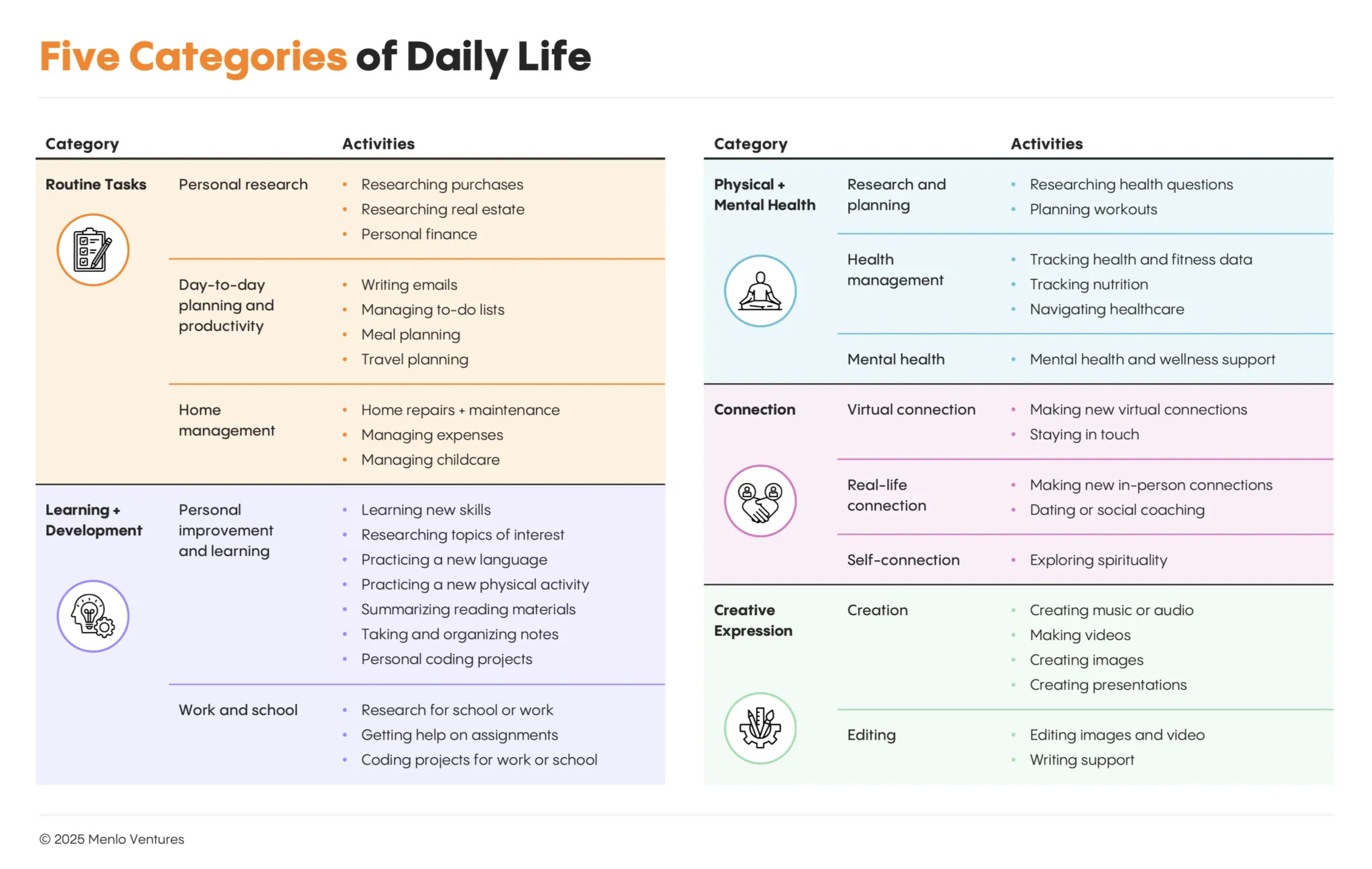

Tuesday, Jun. 24th: Menlo published a report on consumer AI. - Menlo

“More than half of American adults (61%) have used AI in the past six months, and nearly one in five rely on it every day.”

“Even ChatGPT, with its first-mover advantage, only converts about 5% of its weekly active users into paying subscribers”

“Parents are among the most engaged AI users, turning to AI for everyday help. Top use cases: 34% for managing childcare, 28% for researching topics of interest, 26% taking and organizing notes.”

“In the future, AI will take over entire workflows. Today’s AI handles discrete tasks like drafting text or generating images. The next generation will run complex workflows from end to end.”

“In the future, specialised tools will go mainstream. Nearly two-thirds of Americans now use AI, and the first wave dominated by general AI assistants is well underway. Starting this year, expect specialized tools to gain traction and move into the mainstream.”

Wednesday, Jun. 25th: New-Zealand based Halter raised a $100m Series D led by Bond at a $1bn valuation. It’s a vertical software for agriculture equipping cattle with solar‑powered, GPS‑enabled smart collars connected to a mobile/web app and field towers. These collars use sound and gentle vibration cues to establish “virtual fences” and enable remote herding. The system also tracks individual cows’ location, health, and heat cycles, while delivering pasture‑management insights in real time. It will use the funding to double down in its US expansion and to expand its product to become a digital operating system for farms. - Reuters, Axios

Thursday, Jun. 26: I listened to an Acquired’s podcast episode on Epic which has become the digital backbone of the US healthcare system. - Acquired

Epic serves 607 customers (32k hospitals, 42% market share of US hospitals) and adds 10–15 health systems per year. 42% market share of US hospitals. It generated $5.7bn in revenue in 2024, growing at 13% CAGR over 5 years and with 30–35% EBITDA margin. It has 14k employees.

Epic has no sales department. It has only developers, implementation managers, and technical specialists.

Epic provides its software for free to medical schools to train future users.

Hospitals in the US are consolidating to improve bargaining power with Epic and insurers.

Cosmos is a recent product launched by Epic aggregating anonymized data from 295m patients.

Epic is long-term oriented and under-monetizes compared to its dominance.

MyChart, launched in 2000, gives patients access to their medical data online.

Many healthcare providers struggle with failed implementations — Epic is known for getting it right, earning a reputation as the gold standard.

Epic’s deal with Kaiser Permanente’s for $4bn in total costs ($400m to Epic) was a game changer in the company’s growth trajectory.

Epic started with ambulatory/outpatient modules before moving into inpatient.

Epic has built its own programming language on top of its database.

Sequoia managed to purchase Epic’s shares in secondary.

Epic only raised an initial $140k angel round (50-50 equity/debt).

Epic helps hospitals maximize revenue via optimized billing.

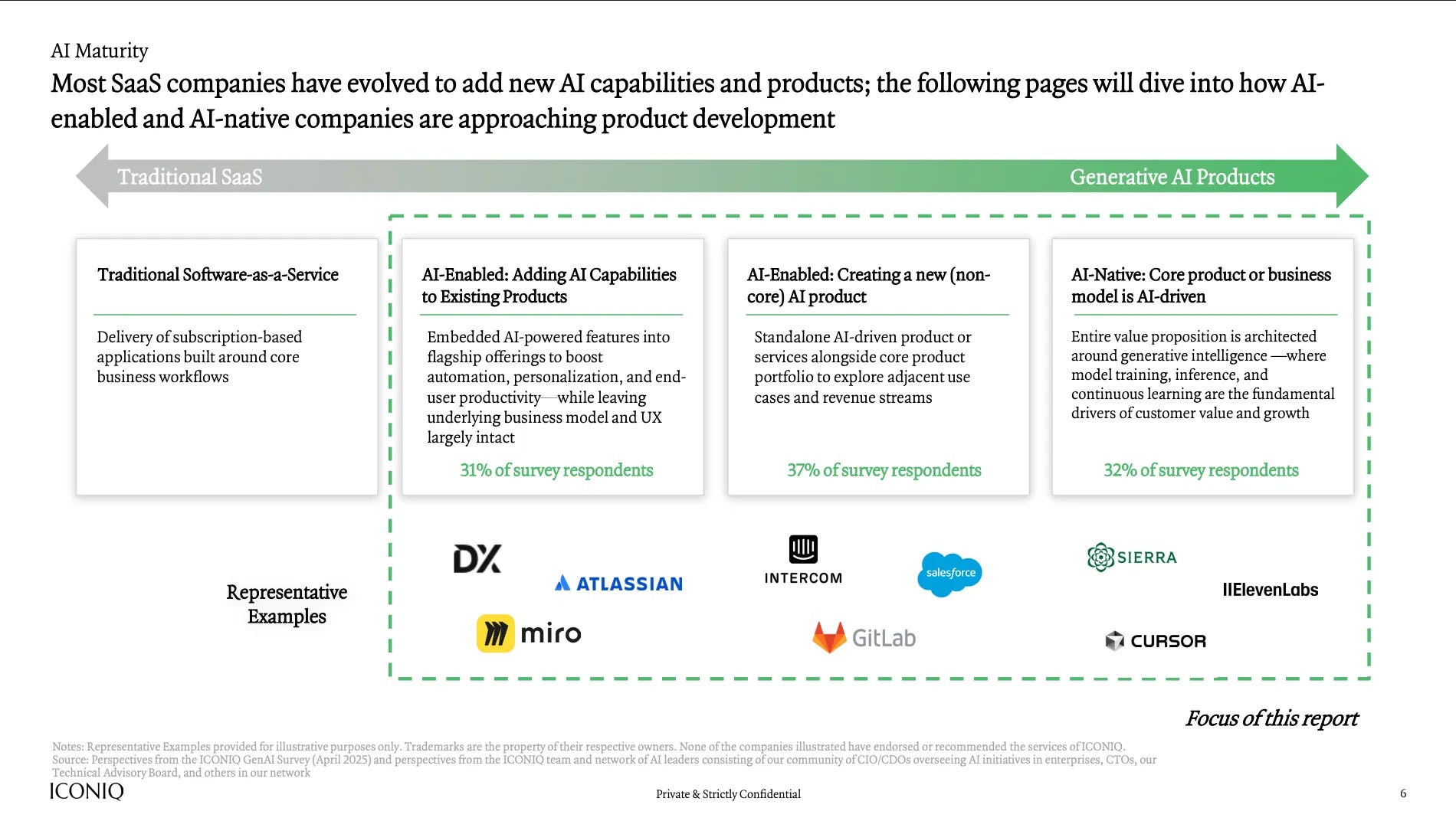

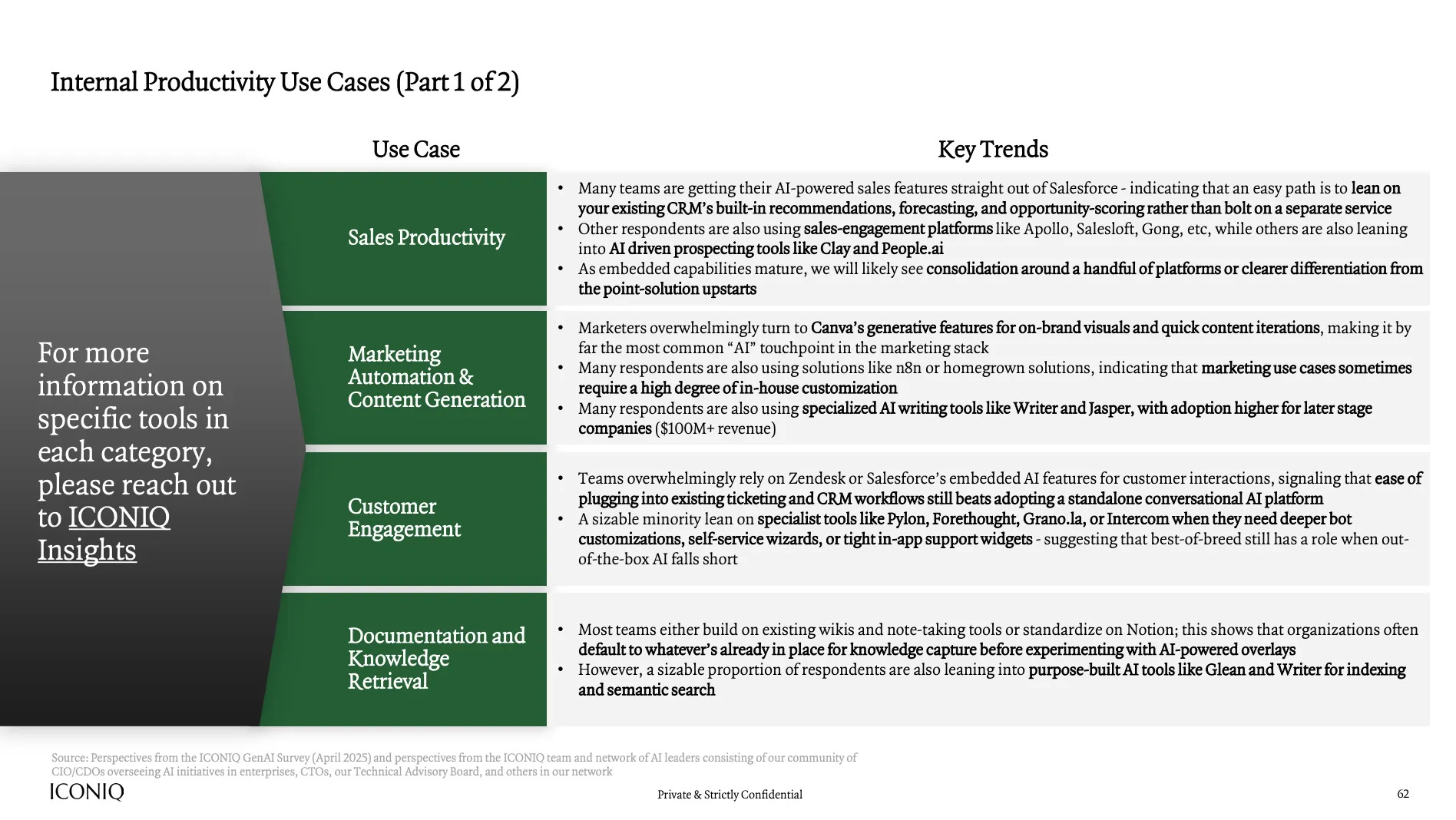

Friday, Jun. 27th: Iconiq published a state of AI report. - Iconiq

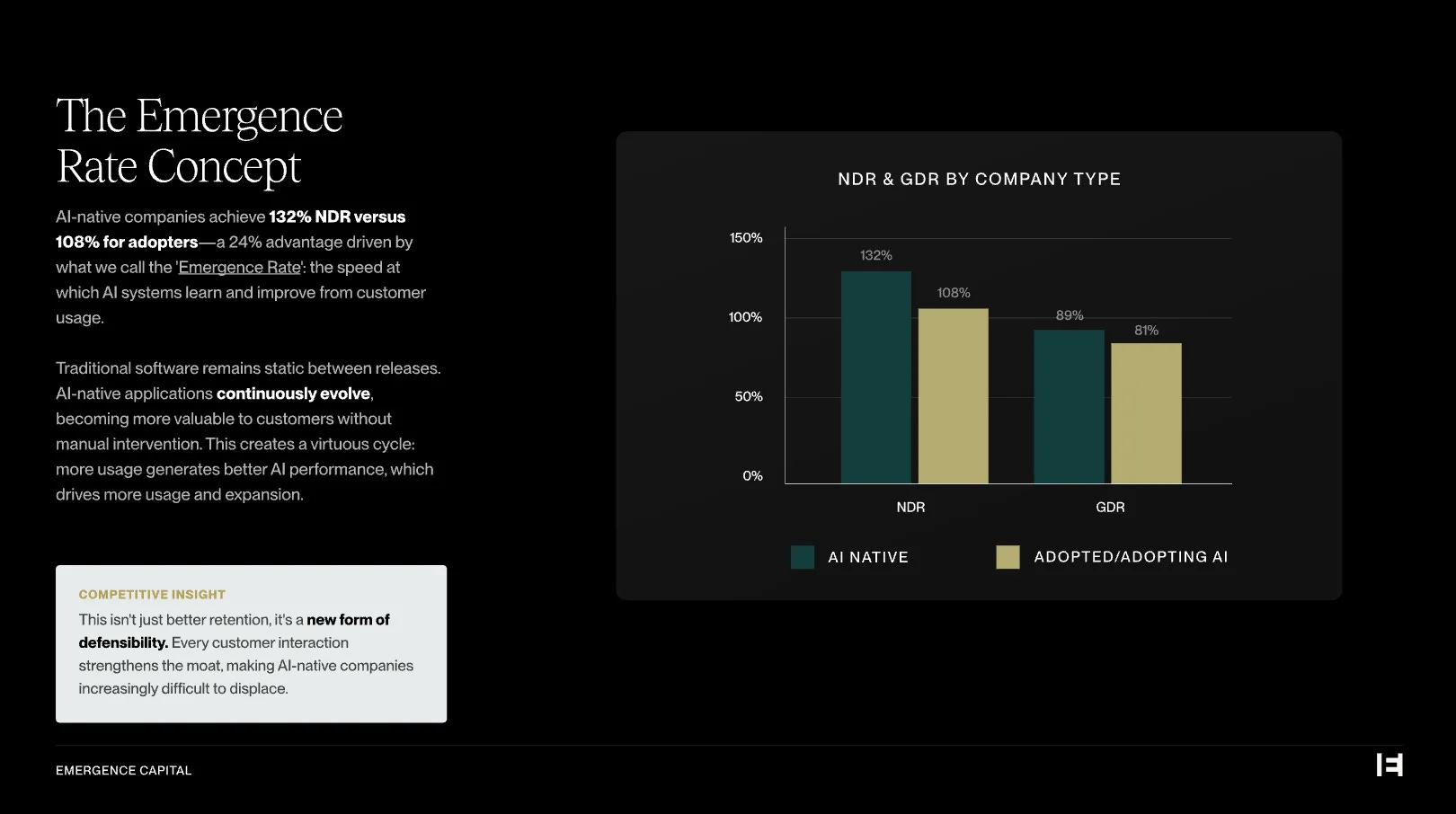

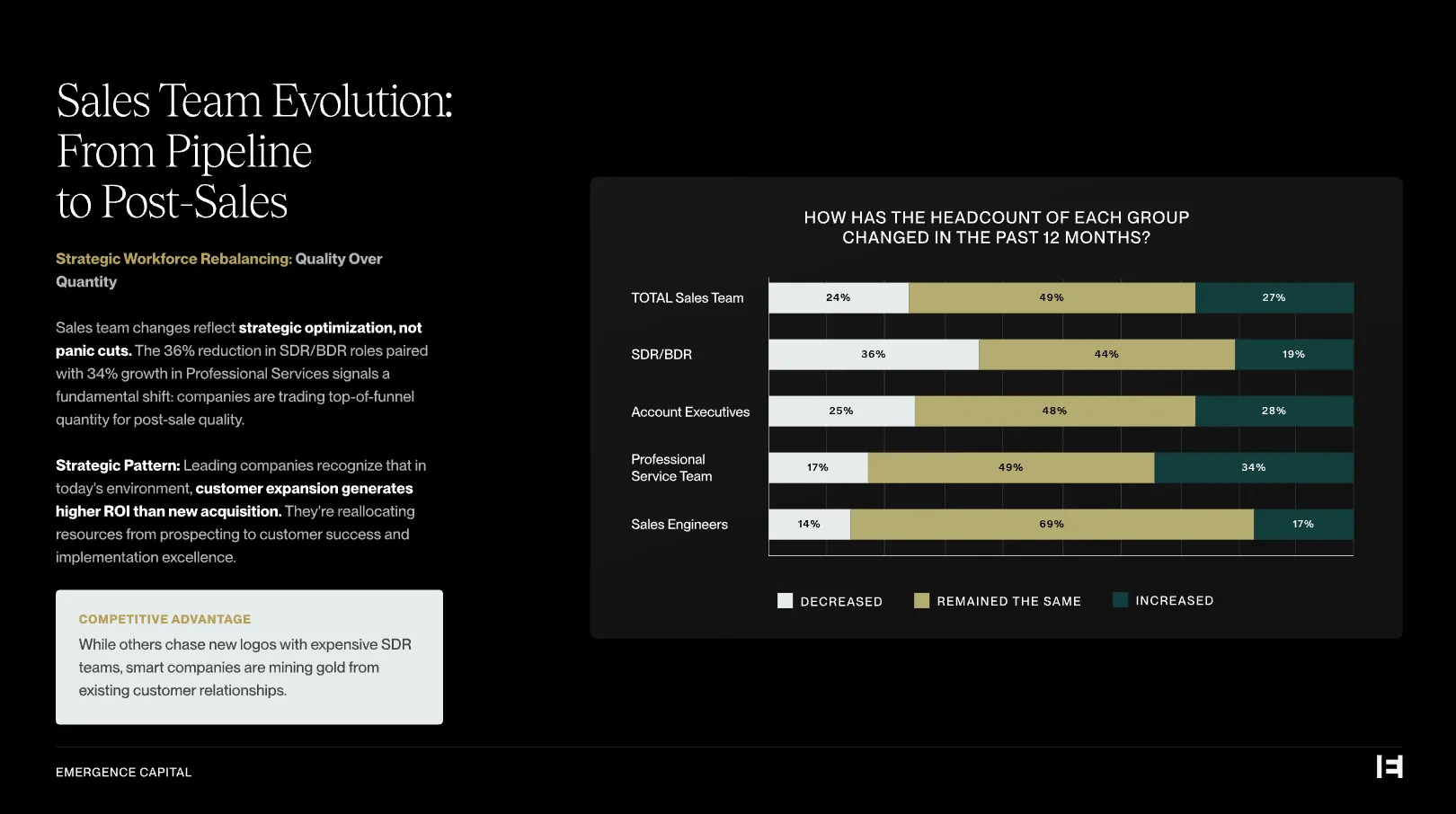

Saturday, Jun. 28th: Emergence published a report on how SaaS companies are navigating the AI disruption based on a survey of 560+ B2B SaaS companies. - Emergence

AI-native firms see higher Net Dollar Retention (132% vs. 108%), attributed the compounding value created as AI systems learn from user data.

At $50m ARR, expansion bookings (vs. new bookings) account for 58% of growth (67% for $100m+), fundamentally changing business models to focus on customer success and multi-product expansion.

Gross Dollar Retention drops during the $5–50m ARR phase as companies are aggressively new bookings without always having the right customer success infrastructure to retain/upsell new customers.

Sunday, Jun. 29th: Abridge raised a $300m series E led by a16z and Khosla at a $5.3bn valuation nearly doubling its February 2025 valuation of $2.75bn following a $250m Series D. It’s an ambient‑listening AI app that transcribes medical conversations and generates structured clinical notes. Abridge has been deployed across 150+ health systems in the US (c.50 % increase since February) and should process 50m clinical conversations in 2025. - WSJ

“The technology is lauded for reducing physician burnout—an increasing problem for overworked doctors—and allows them to spend more time focused on patients without needing to scribble notes after hours.”

Monday, Jun. 30th: In Q1-2025, Olo increased revenues to $80.7m (21% YoY) adding 2k new locations to reach 88k total locations. It plans to add 5k total locations in 2025. Olo is a vertical software for restaurants powering digital ordering, delivery integration, and customer engagement for multi-location restaurants. Its ARPU increased by 12% YoY to $911. It has a 111% net dollar retention and a 98% gross dollar retention. It had a $2.4m operating loss (-2.8% of sales). - Olo

“We made early progress on our 2025 priorities scaling Catering Plus, ramping Olo Pay card presence and increasing the number of Olo flywheel brands.”

“In the first quarter, although built on the momentum we sustained over 2024, we exceeded the high end of our revenue and non GAAP operating income guidance ranges.”

“Today, we have more than 70 brands using Olo Order and Olo Pay to generate digital transactions.”

“We're announcing that Chipotle, a new top 25 brand for Olo, will pilot multiple Olo modules across a subset of locations to support their catering channel. It's a great validation of our platform's strength and modularity as Chipotle will use Olo to power its catering channel as a complement to their in house tech.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋