📖 Venture Chronicles - June 2023

Overlooked #149

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of June.

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

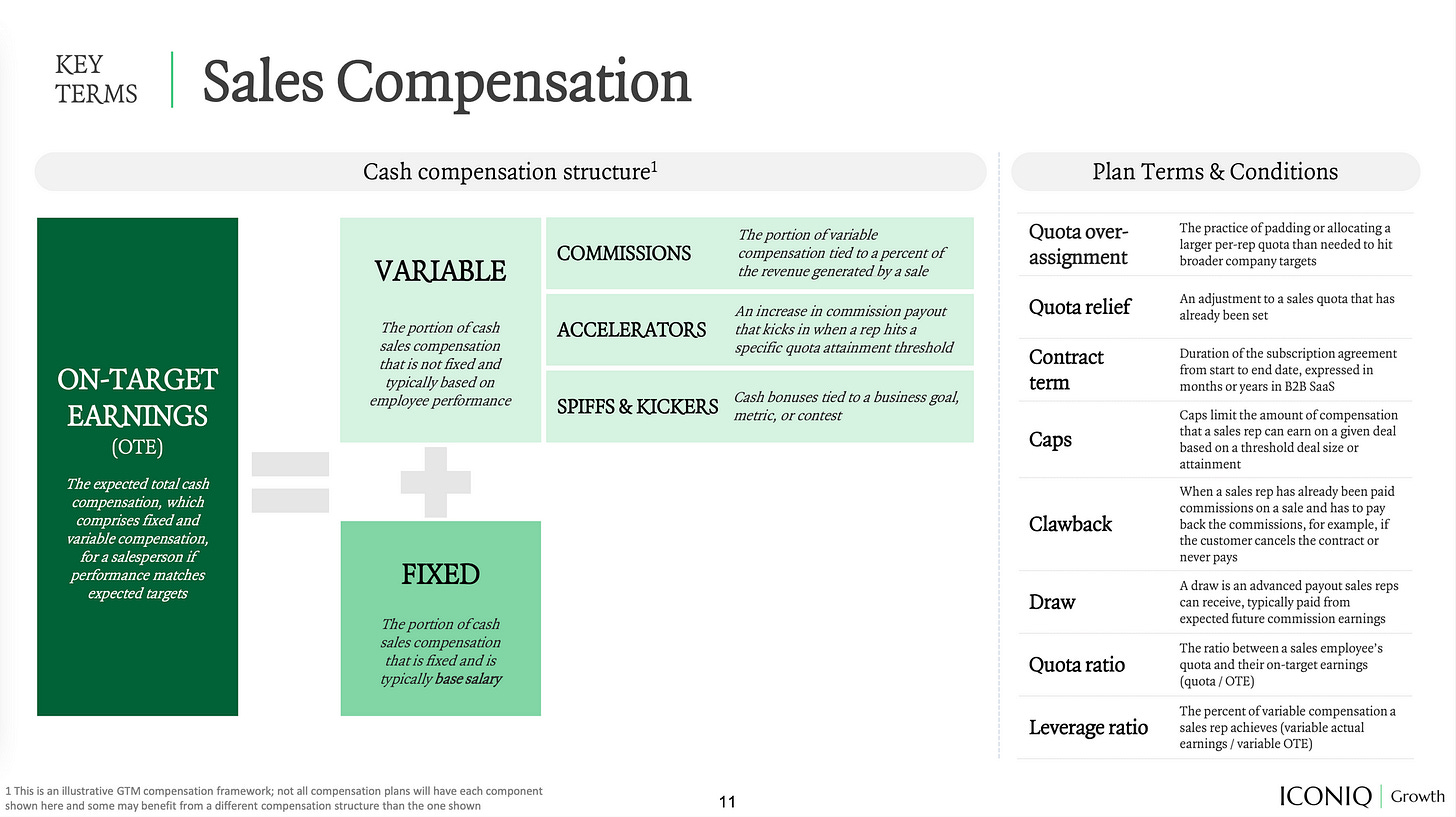

Thursday, Jun. 1st: Iconiq published a report on sales compensation. - Iconiq

Iconiq points to several emerging trends in sales incentives: (i) an emphasis quality over quantity favouring healthy deals with upsell potential, multi-year engagement and/or upfront payment, (ii) the use of a minimum attainment threshold to gradually phase out underperforming sales reps, (iii) the adoption of net dollar retention as the north star metric rather than new ARR generated, (iv) a preference for results over activities.

“82% of sales organisations offer accelerators and 71% offer SPIFFs to reward strong performance against quota or other objectives”. 53% of companies are using clawbacks (asking sales to pay back the commission if the contract is cancelled).

Friday, Jun. 2nd: Buy-Now Pay-Later (BNPL) player Klarna published its Q1-2023’s results. - Techcrunch, Sequoia, Klarna

Klarna signed Airbnb as a new customer strengthening its diversification in the travel sector.

Its quarterly GMV grew by 13% YoY to $19.7bn. It’s a significant achievement given that the e-commerce market contracted by 2% over the same period. Klarna managed to reduce its quarterly operating loss from $235m to $110m.

“It’s funny—when you look at Swedish students now, something like 70% want to start their own business. When I was in school it was more like 7%.” - Sebastian Siemiatkowski (CEO and cofounder at Klarna)

The company is now implementing AI throughout its product line in a bid to enhance its digital financial assistant and shopping recommendation engine.

“The power of AI is reshaping the shopping landscape, shifting the traditional Western model where the majority of purchases come from search rather than recommendations. Instead it's rapidly bringing us closer to the Chinese model, where a remarkable 80% of purchases are driven by recommendations.”

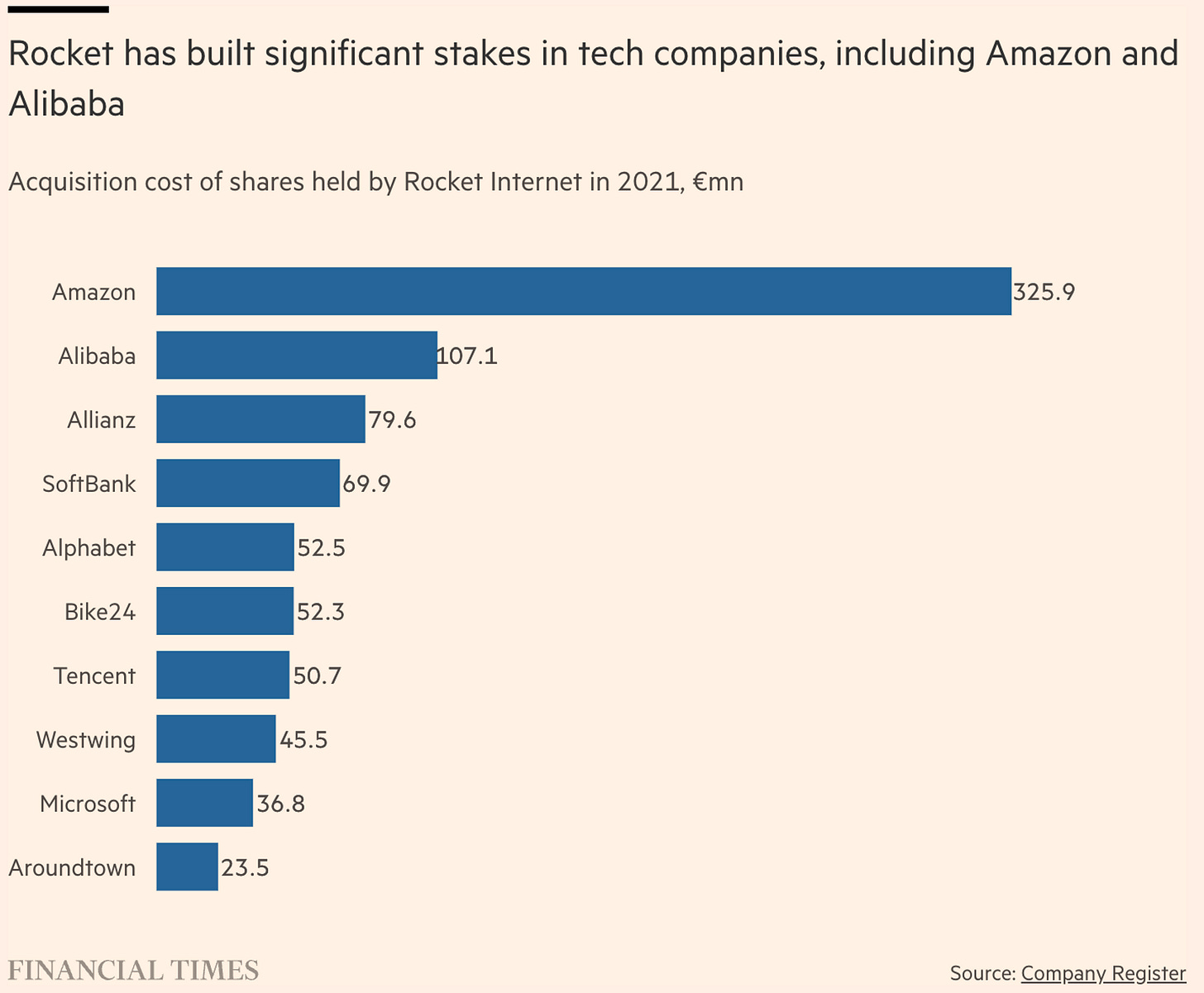

Saturday, Jun. 3rd: Rocket Internet has shifted its investment strategy, transitioning from investing in early stage startups to more conservative tech assets. Rocket used to have 130 employees. Today, it operates with just a couple of dozens. Both GFC (early stage fund) and Flash (startup studio/incubator) have been discontinued. GFC failed to raise a €1bn fund. Rocket failed to find a target for a SPAC vehicle it had raised. Today, Rocket invests primarily in public companies (Amazon, Alibaba, Softbank, Alphabet, Tencent, etc.) and in late stage private startups through debt financing (e.g. Revolut, SumUp). - FT

Sunday, Jun. 4th: In 2022, iOS mobile apps generated $1.1tn in revenues (29% YoY growth). The revenue was comprised of $910bn from physical goods, $109bn from in-app ads, and $104bn from digital goods. 4.8m people work for the AppStore ecosystem in Europe (2.4m people) and in the US (2.4m people). Apple rejected 1.7m app submissions in 2022. - Apple, Analysis Group

Monday, Jun. 5th: The average age of unicorn founders when they launched their companies was 35 years old. The majority of these founders started their ventures when they were between the ages of 20 and 50. My team and I have had several discussions about this topic, so it's enlightening to see the data. - Ilya Strebulaev

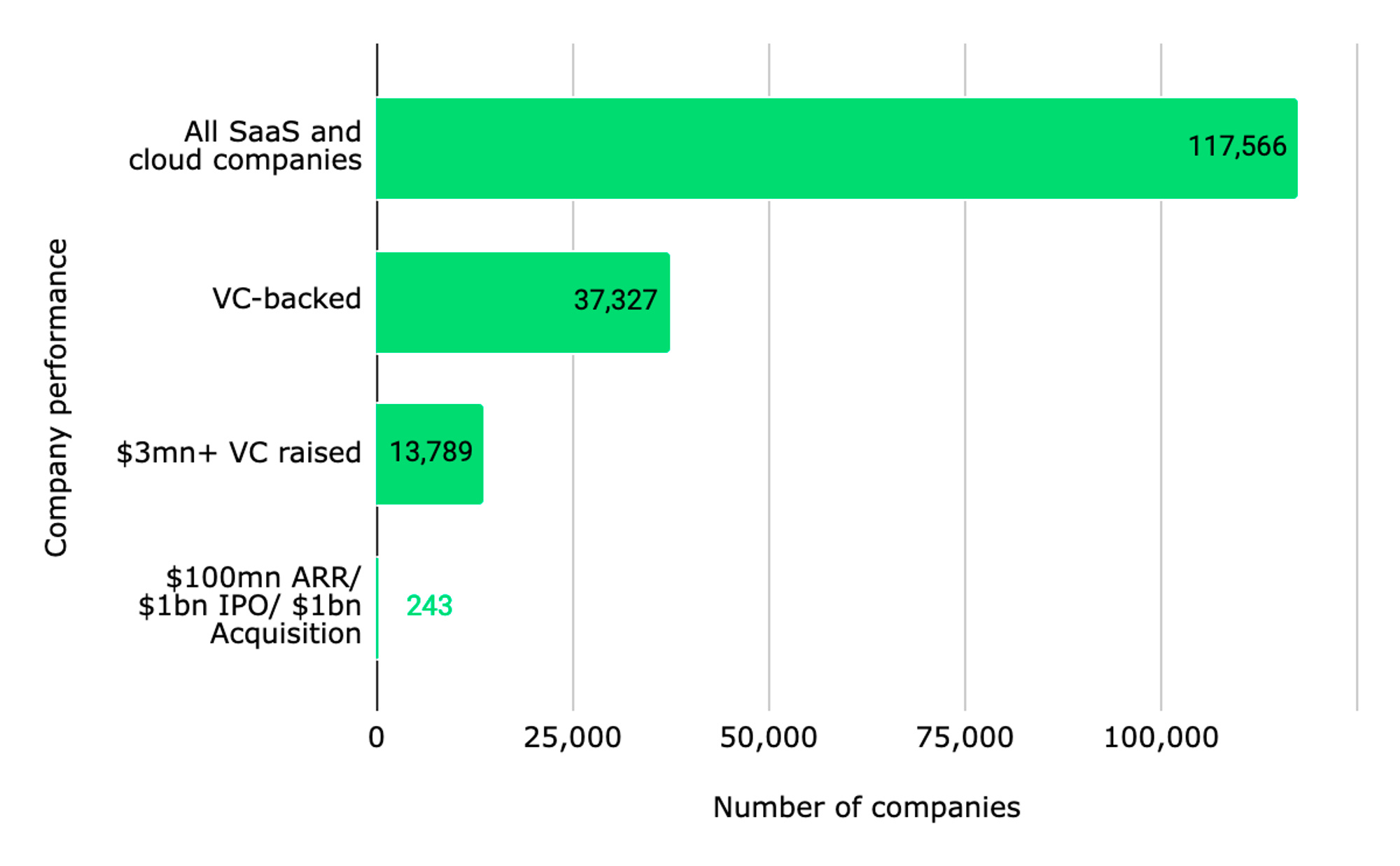

Tuesday, Jun. 6th: Stephen Millard at Notion published a study on scaling a B2B SaaS from $1m to $100m in ARR. - Notion

Merely 0.65% of VC backed SaaS companies manage to generate more than $100m in ARR or secure an exit valued at more than $1bn.

When examining companies that have achieved $100m in ARR, the median time to reach this milestone is 9 years. 65% of these companies manage to reach $100m in less than 10 years, while 20% do so in less than 6 years.

Notion breaks down company scaling into five stages: (i) $0-1m ARR: finding PMF, (ii) $1-3m ARR: moving beyond founder led sales validating an early GTM model and finding a first good ICP, (iii) $3-10m ARR: finding the GTM model and putting in place the playbook to scale it, (iv) $10-30m ARR: scaling a predictable growth playbook, (v) $30-100m ARR: introducing new product and entering new markets.

Wednesday, Jun. 7th: Deconstructor of Fun recently discussed Clash Mini, a Supercell game which is an auto-chess (similar to Riot Games's Teamfight Tactics). This game is the closest to a global launch among Supercell's lineup. Clash Mini, developed by Supercell's Shanghai studio in China, began its soft launch 16 months ago. Despite numerous iterations on Clash Mini, Supercell appears to struggle in finding a true product market fit, as evidenced by stagnant revenue per download and weak mid-to-long-term retention. This article is another story on Supercell demonstrating the difficulty that even top-tier mobile game studios face in producing multiple hits. - DoF

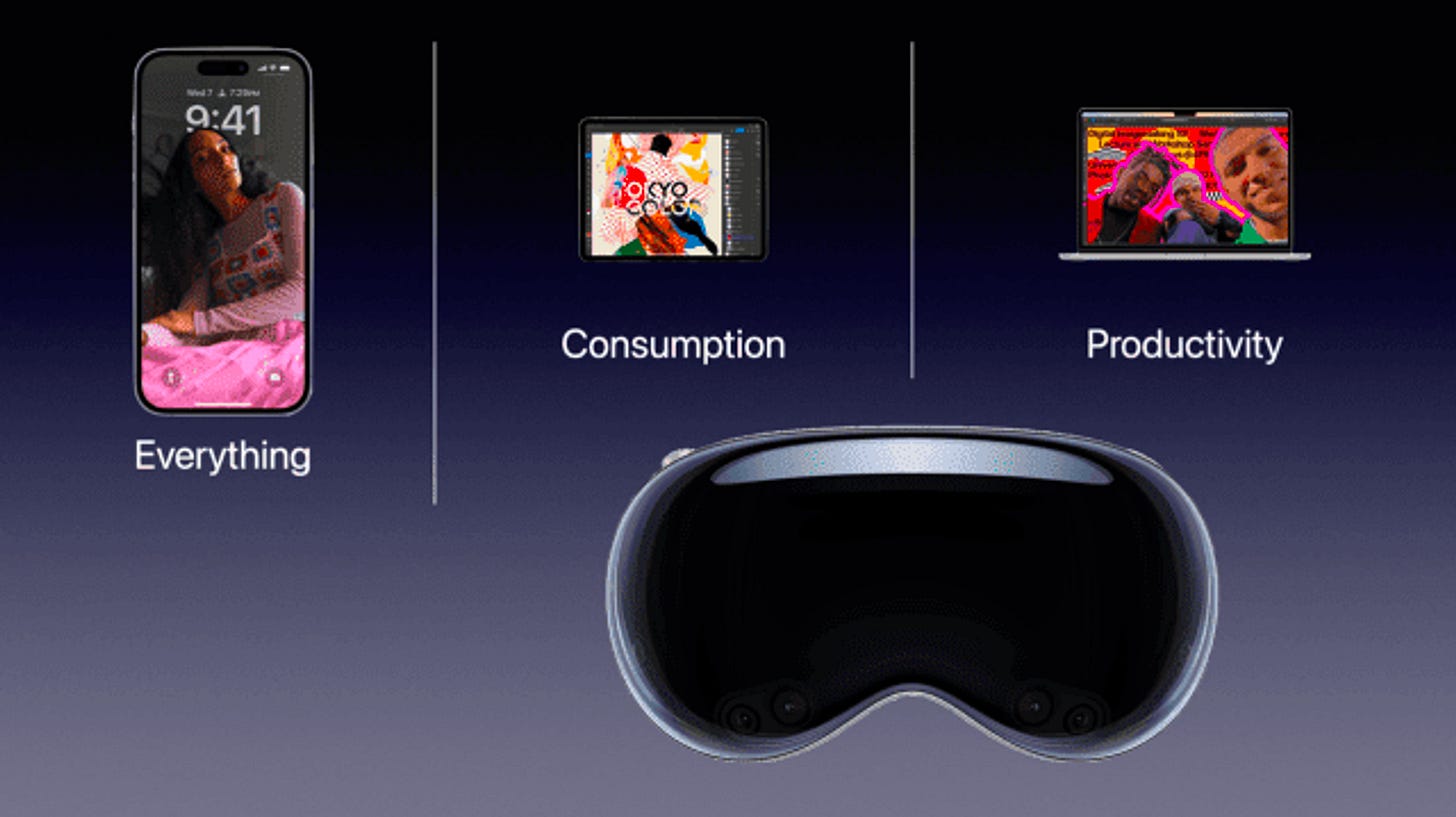

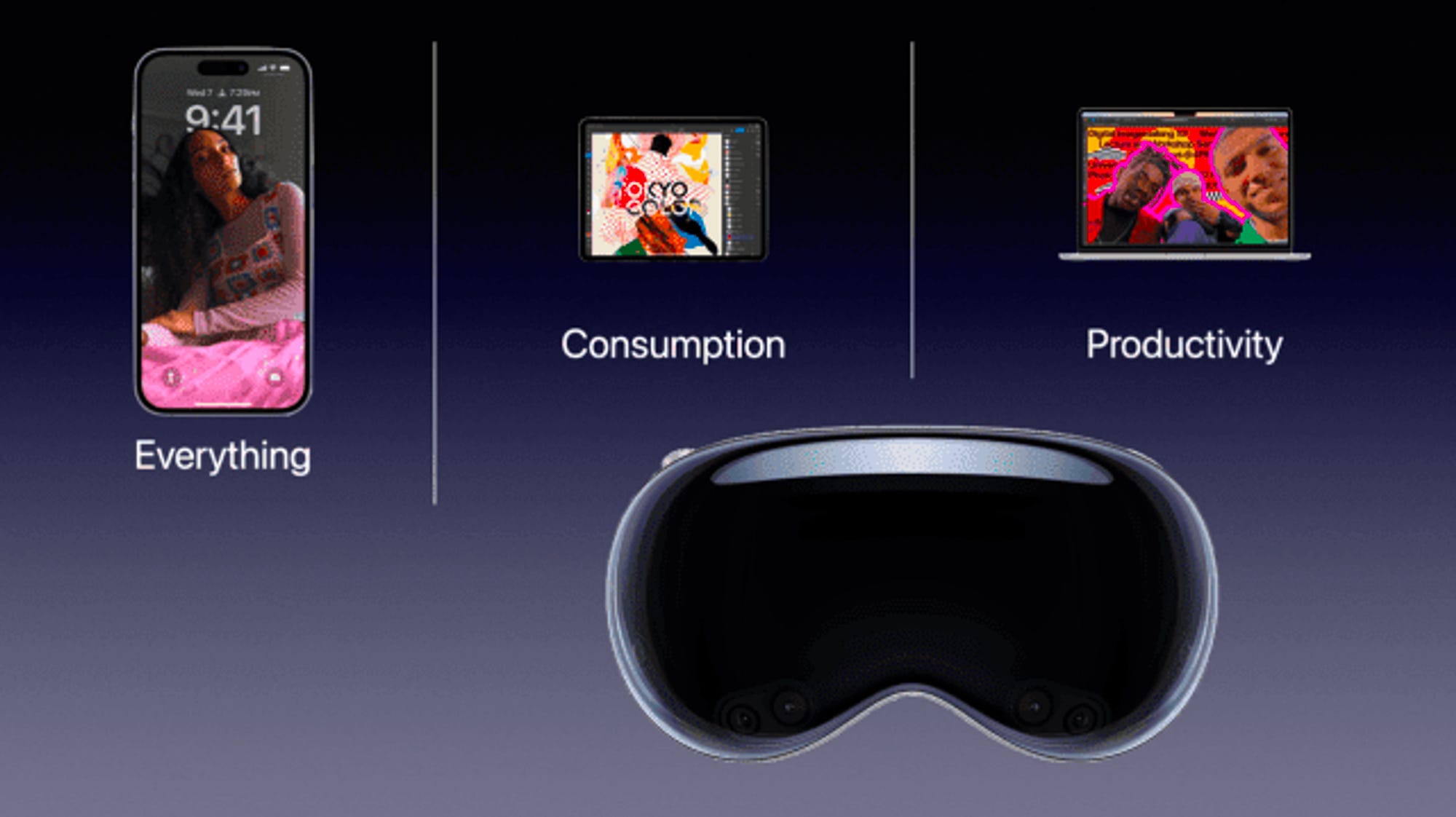

Thursday, Jun. 8th: I watched Apple’s 2023 WWDC. - Apple

Apple has unveiled a VR headset named Vision Pro with a dedicated spatial operating system called VisionOS. This VR headset can be operated through eye movements, hand gestures, and voice commands. Upon launch, users will have access to a range of applications, including Adobe Lightroom, Microsoft Office and Zoom, as well as 100 games from Apple Arcade. Native Apple applications, such as FaceTime, will also be available, allowing users to interact with others using 3D avatars. It is set to be released in 2024 and is priced at $3.5k.

In addition, Apple introduced a journaling application called Journal, which leverages on-device machine learning to create personalized suggestions based on user activities such as music listening, workouts, locations visited, and photos taken.

“Apple exceeded my expectations on both counts: the hardware and experience were better than I thought possible, and the potential for Vision is larger than I anticipated.”

“Apple Vision is technically a VR device that experientially is an AR device, and it’s one of those solutions that, once you have experienced it, is so obviously the correct implementation that it’s hard to believe there was ever any other possible approach to the general concept of computerized glasses.”

“I have been relatively optimistic about VR, in part because I believe the most compelling use case is for work. First, if a device actually makes someone more productive, it is far easier to justify the cost. Second, while it is a barrier to actually put on a headset — to go back to my VR/AR framing above, a headset is a destination device — work is a destination.”

The bull case for Vision Pro is to take market share in the productivity and the personal consumption space. “Vision Pro makes sense everywhere the iPhone doesn’t.”

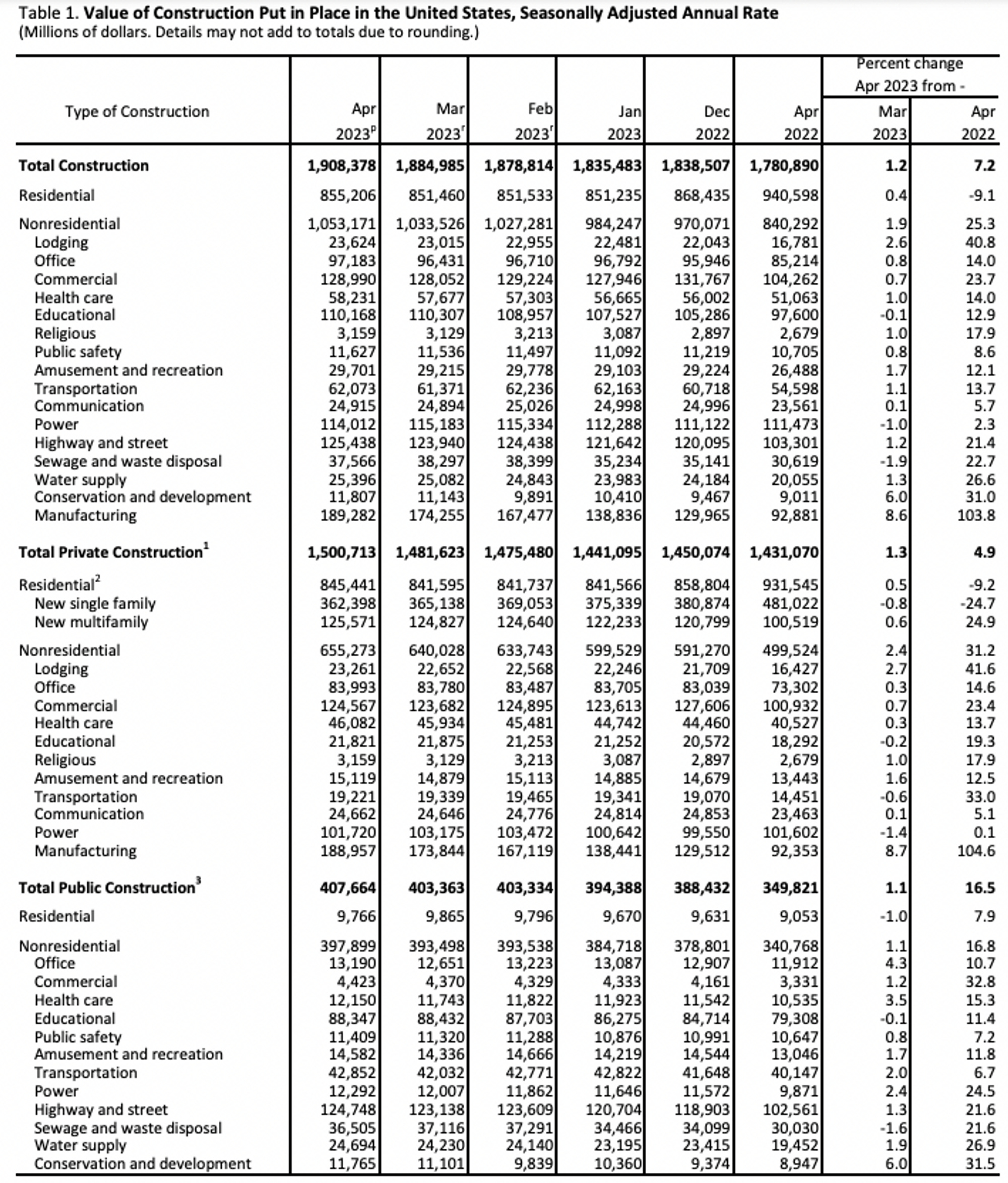

Friday, Jun. 9th: Procore published its Q1-23’s results. - Procore

Construction is divided between residential and non residential. Within the non-residential sector, there are 70 subcategories spanning a wide range of areas, including lodging, commercial real estate, healthcare facilities, educational institutions, office buildings, public infrastructure, and transportation projects.

On March 2023, Procore unveiled a new insurance product called Procore Risk Advisors as part of a broader push into financial services. “Insurance in construction is complicated, cumbersome and expensive, all stakeholders on a project are contractually obligated to have relevant coverage for each individual project they work on.” Procore Risk Advisors, acting as a digital broker, can occasionally assist with underwriting by leveraging proprietary data on its customers and the broader construction industry. “In terms of monetization, there are currently 2 avenues. The first is through serving as a broker by which we sell policies from third-party carriers and earn a brokerage commission, which varies by policy type. And the second is through serving as an underwriting agent for select policies, whereby Procore partners with the carrier who is taking on the claims risk in their evaluation of the policy, providing additional industry expertise and enhanced data in exchange for a share of the premium. It's important to note that in both of these cases, we take on 0 balance sheet exposure to claims. Because to be clear, we are a distribution partner for the insurance carrier who bears the risk of the insurance claims.”

“50% of the construction companies we talk to every day are coming from analog pen and paper greenfield opportunities and is not a competitive dynamic.”

Saturday, Jun. 10th: The Wall Street Journal recently published an article on the challenges startups face, focusing on their struggles with pivoting, efforts to sell their businesses, and in some cases, their eventual shutdowns. - WSJ

“The Mass Extinction Event for startups is under way. It’s like the entire industry went out drinking and is now suffering the consequences.” - Tom Loverro (IVP)

The bull market artificially boosted startups’ survival rate. For instance, Hustle Fund invested in 101 pre-seed startups in its first fund. 90 were alive 1y ago. This number is now down to 60.

“Roughly 16% of companies have had a successful acquisition or went public within seven years of raising their first venture capital fundind, according to data on close to five thousand U.S. companies that raised first funding between 1995 and 2013."

Sunday, Jun. 11th: I watched a talk by Sam Blond at SaaStr where he shared his go-to-market learnings from his time as the CRO at Brex. During his tenure, he successfully scaled Brex's ARR from $0m to $400m. - SaaStr

When starting, focus on warm outbound strategies leveraging personal networks of people around your companies rather than cold outbound.

When Sam joined Brex as the 18th employee, the company was operating stealth mode, with a beta product and all employees maintaining a stealth presence LinkedIn. The website only hinted at an upcoming product launch. To acquire customers during the beta phase through outbound efforts, Brex relied on leveraging personal networks rather than engaging in mass outbound strategies using tools like Outreach and ZoomInfo. These tools are more effective once an established brand is in place. Instead, Brex capitalized on its association with YC, initially reaching out to companies in the same YC batch before expanding outreach to other YC-affiliated companies.

When launching your product, it is important to leverage multiple channels to maximize visibility. In Brex's case, they transformed their stealth website into a marketing website and initiated a PR campaign that coincided with a fundraising announcement. The team proactively reached out to influential individuals in their networks to generate public conversations about the launch. Additionally, Brex sponsored podcasts and launched a billboard campaign in San Francisco. The strategy revolved around creating repetition and utilizing various marketing touchpoints to target their Ideal Customer Profile (ICP) within a condensed timeframe.

When sponsoring events, it is crucial to invest heavily in event marketing to stand out from other sponsors. Brex implemented several creative strategies to differentiate themselves. They sponsored the credit cards given by hotels to attendees, which allowed them to promote their product while attendees accessed their rooms and made purchases. Furthermore, they sponsored burritos for people waiting in line, enhancing their brand visibility and creating a positive association. To add a touch of entertainment, Brex hired a magician to perform tricks within the venue, providing a memorable experience for attendees.

Brex implemented an outbound campaign known as the "champagne campaign." They allocated $20k to send 300 handwritten notes, personally signed by Brex's CEO, along with a bottle of champagne to startups in the Bay Area that had recently secured funding within the past six months. The purpose was to congratulate these startups. Following the reception of the package, Brex would then send an email to the founders to request a meeting. Remarkably, this approach yielded a 75% response rate to the email and a subsequent 75% closing rate after the demo. Ultimately, Brex successfully converted 169 customers from the initial 300 bottles of champagne.

Account Executives (AEs) should engage in outbound activities. Many early-stage startups encounter a bottleneck in demand generation, and having AEs contribute to outbound efforts can significantly alleviate this challenge. At Brex, 50% of revenues were generated through outbound efforts led by AEs, compared to 30% from outbound SDRs and 20% from other channels. In contrast, in most startups, AEs typically focus solely on closing leads generated by SDRs and the marketing team, without actively engaging in outbound initiatives. However, AEs possess a unique understanding of what constitutes an excellent demo and which target customers are most suitable. Their experience allows them to naturally identify and target the right type of companies, resulting in higher closing rates. Moreover, AEs often have prior experience as SDRs and are typically more experienced and proficient than recently recruited college graduates in the SDR role.

SDRs compensation should be tied to revenues and not sales qualified opportunities. Incentivizing SDRs solely on qualified opportunities may not lead to the generation of high-quality opportunities. Instead, SDRs should be motivated by the revenue outcome. When Brex implemented this shift, it observed increases in both ACVs and conversion rates. Charlie Munger famously said: "show me the incentives, and I'll show you the outcome.”

It is crucial to establish revenue targets as soon as you hire dedicated sales personnel. The target would be set with a 90% degree confidence that it can be reached in order to create a culture. You aim for 70% of your sales reps to reach their quotas. It is essential to demonstrate that success is the norm within your organization. Brex holds weekly meetings to celebrate the wins of the week and to keep the sales organization motivated and on track.

Expanding revenue within the existing customer base should be prioritized earlier than expected and with ample resources. Brex has developed a sales farming team that is larger than its hunting team, emphasizing the importance of nurturing and growing existing customer relationships.

Monday, Jun. 12th: I listened to a Founders’ podcast episode on James Dyson’s autobiography called Against the Odds - Colossus

James Dyson created thousands of prototypes before successfully manufacturing a significantly superior vacuum cleaner compared to his main competitor, Hoover. "I didn't find -- I didn't fail. I just found 10,000 ways that didn't work.”

"My own success has been in observing objects in daily use, which it was always assumed could not be improved. By lateral thinking, it is possible to arrive empirically at an advance. Anyone can become an expert in anything in 6 months, whether it's hydrodynamics for boats or cyclonic systems for vacuum cleaners.”

“The best kind of business is one where you could sell a product at a high price with a good margin and in enormous volumes. For that, you have to develop a product that works better and looks better than existing one. That type of investment is long-term, high-risk, and not very British, or at least it looks like a high-risk policy.”

“I've been a misfit throughout my professional life, and that seems to have worked to my advantage. Misfits are not born or made. They make themselves. And a stubborn opinionated child desperate to be different and to be right encounters only smaller refractions of the problems he will always experience, and he carries the weight of that dislocation forever.”

You should have a straightforward marketing message when you’re marketing something new. Dyson’s vacuum cleaner was also a great dry cleaner but it was never marketed like this. “You simply cannot mix your messages when selling something new. A consumer can barely handle one great idea.”

Tuesday, Jun. 13th: Eli Dukes wrote on integrating payments into vSaaS. - Verticalized

There is an opportunity for payment processors to make a vSaaS roll-up and to embed payments into the acquired vSaaS with incredible unit economics because your payment stack is vertically integrated. It’s a playbook used by PE-fund Advent with Xplor which is a combination of a vSaaS and a payments platform serving 82k businesses processing $27bn in payments.

“Toast and Shopify infused the vertical SaaS category with a TAM-expanding thesis: Payments can catapult vertical SaaS companies to become multi-billion dollar categories. And for most companies, payments are also the starting point in the pursuit of additional fintech revenues. Getting a customer to switch to your payments product gives you a clear line of sight into other organic growth opportunities.”

“There is meaningful room for unit economics improvements on payments - quite literally next-to-free margin improvement by consolidating several 1-5B GPV vSaaS companies under a single payfac.”

“Square has realized that the vertical solutions increase profitability and GTM efficiencies. It’s why they are pursuing rapid verticalization around three anchor verticals: retail, beauty, and restaurants.”

Wednesday, Jun. 14th: Marc Andreessen wrote about AI arguing that AI will save the world. - a16z

“What AI offers us is the opportunity to profoundly augment human intelligence to make all of these outcomes of intelligence [e.g. longevity, learning, financial decision, parenting outcomes, job performance] much, much better from here.”

“Productivity growth throughout the economy will accelerate dramatically, driving economic growth, creation of new industries, creation of new jobs, and wage growth, and resulting in a new era of heightened material prosperity across the planet.”

“Every child will have an AI tutor that is infinitely patient, infinitely compassionate, infinitely knowledgeable, infinitely helpful. The AI tutor will be by each child’s side every step of their development, helping them maximize their potential with the machine version of infinite love.”

“The single greatest risk of AI is that China wins global AI dominance and we – the United States and the West – do not.”

“Big AI companies should be allowed to build AI as fast and aggressively as they can – but not allowed to achieve regulatory capture, not allowed to establish a government-protect cartel that is insulated from market competition due to incorrect claims of AI risk.”

“Startup AI companies should be allowed to build AI as fast and aggressively as they can. They should neither confront government-granted protection of big companies, nor should they receive government assistance. They should simply be allowed to compete.”

“Today, growing legions of engineers […] working to make AI a reality. […] They are heroes, every one. My firm and I are thrilled to back as many of them as we can, and we will stand alongside them and their work 100%.”

Thursday, Jun. 15th: Sequoia made the decision to split its firm into three separate entities: US/Europe, China and India. There are several reasons behind this strategic move: (i) a complex geopolitical environment, (ii) competition among portfolio companies, (iii) concerns about brand dilution, (iv) difficulties in maintaining a centralised back-office as Sequoia was expanded globally. Personally, I believe that this decision highlights the challenges of scaling venture capital as an asset class and that geopolitical tensions between China and the US directly impact the venture capital landscape. - Forbes

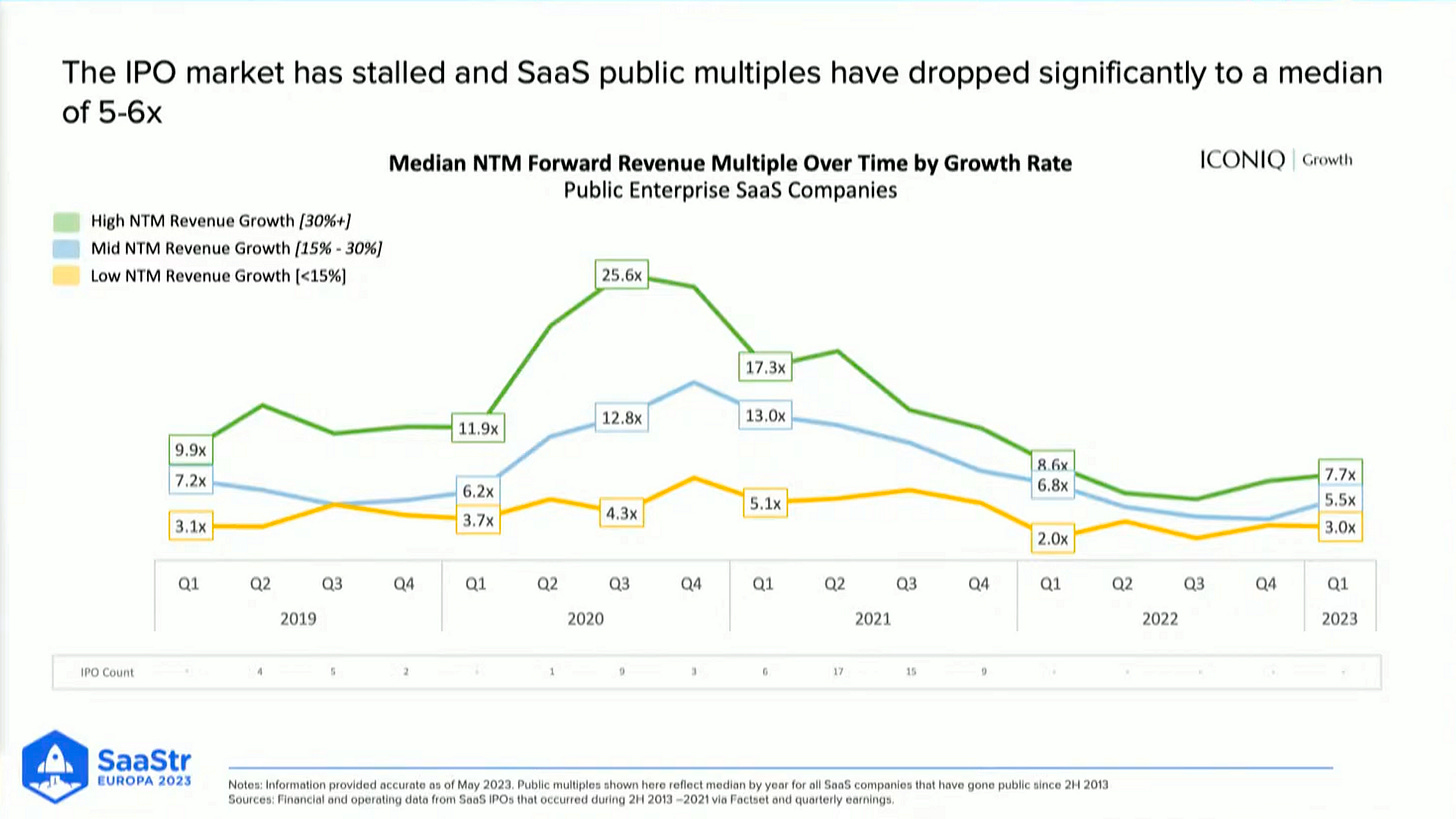

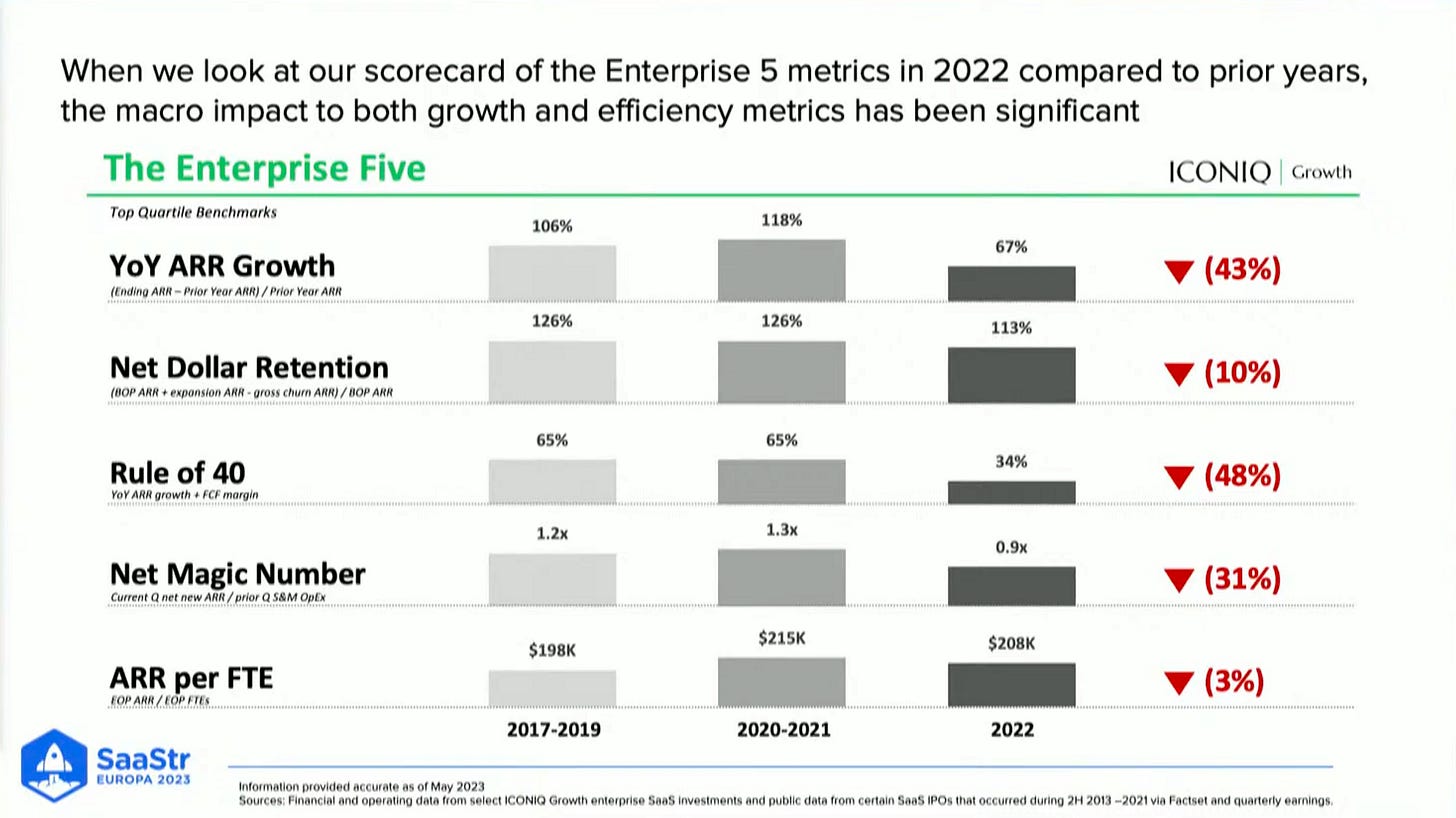

Friday, Jun. 16th: At SaaStr, Iconiq Growth shared some metrics that shed light on scaling efficiently for both private and public companies. - SaaStr

“The balance of focus on growth vs. efficiency has shifted with the rule of 40 becoming increasingly correlated to public multiples.”

“Performance across SaaS businesses declined in 2022 with topline metrics seeing the greatest impact. Efficiency metrics also deteriorate as many companies did not scale back costs sufficiently to account for macro headwinds.”

Most companies missed their top-line plan in Q1 with vertical SaaS and GTM sectors being the most impacted.

“Cash conversation will be critical this year. Companies have median runways of 25 months.”

“Many companies are embracing AI to accelerate both their product & internal organisation productivity.”

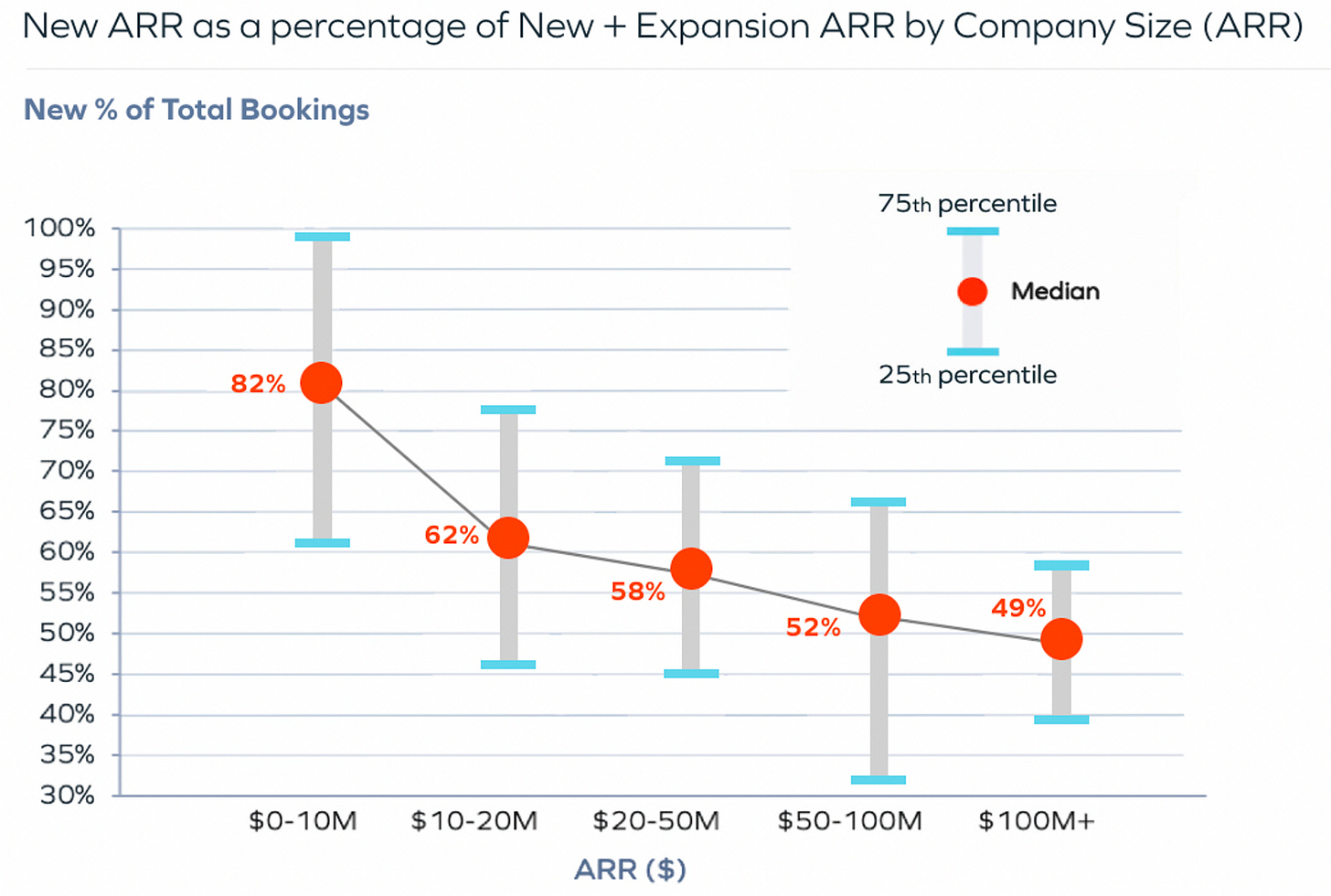

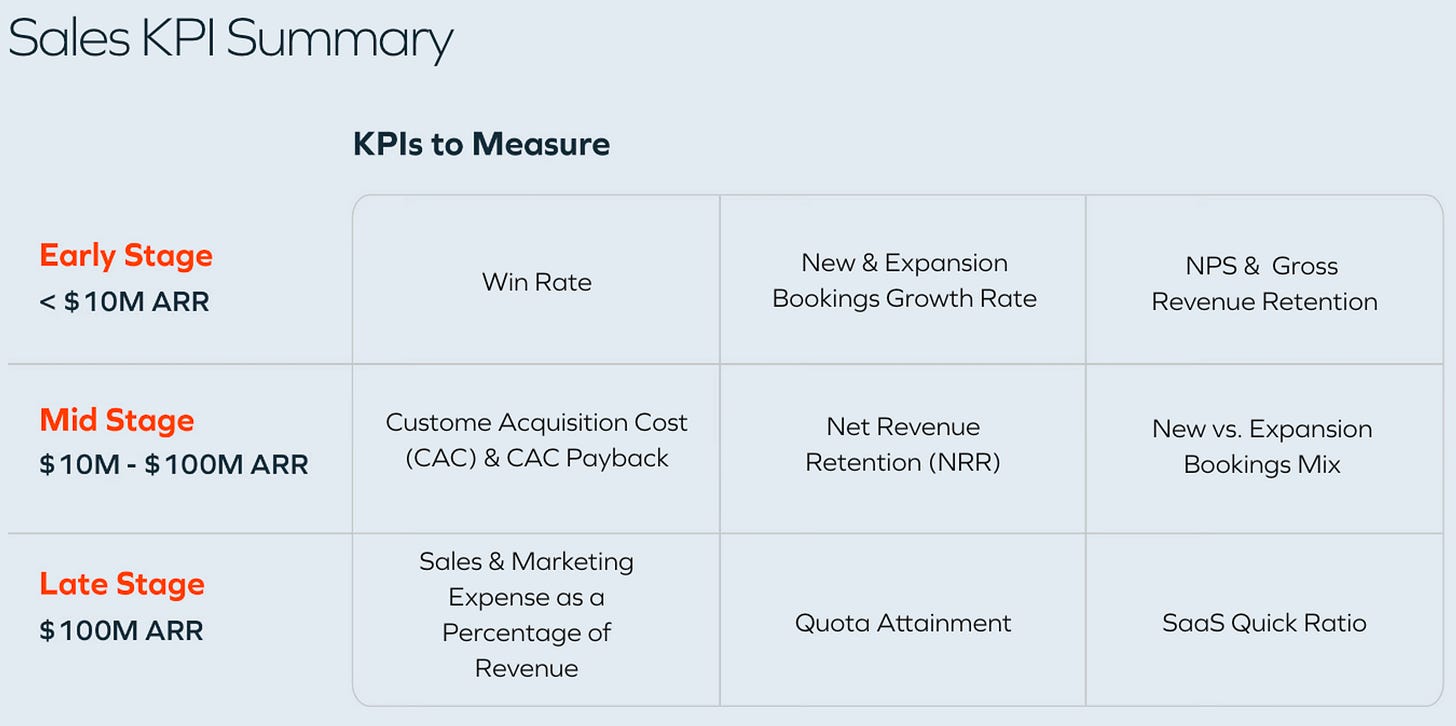

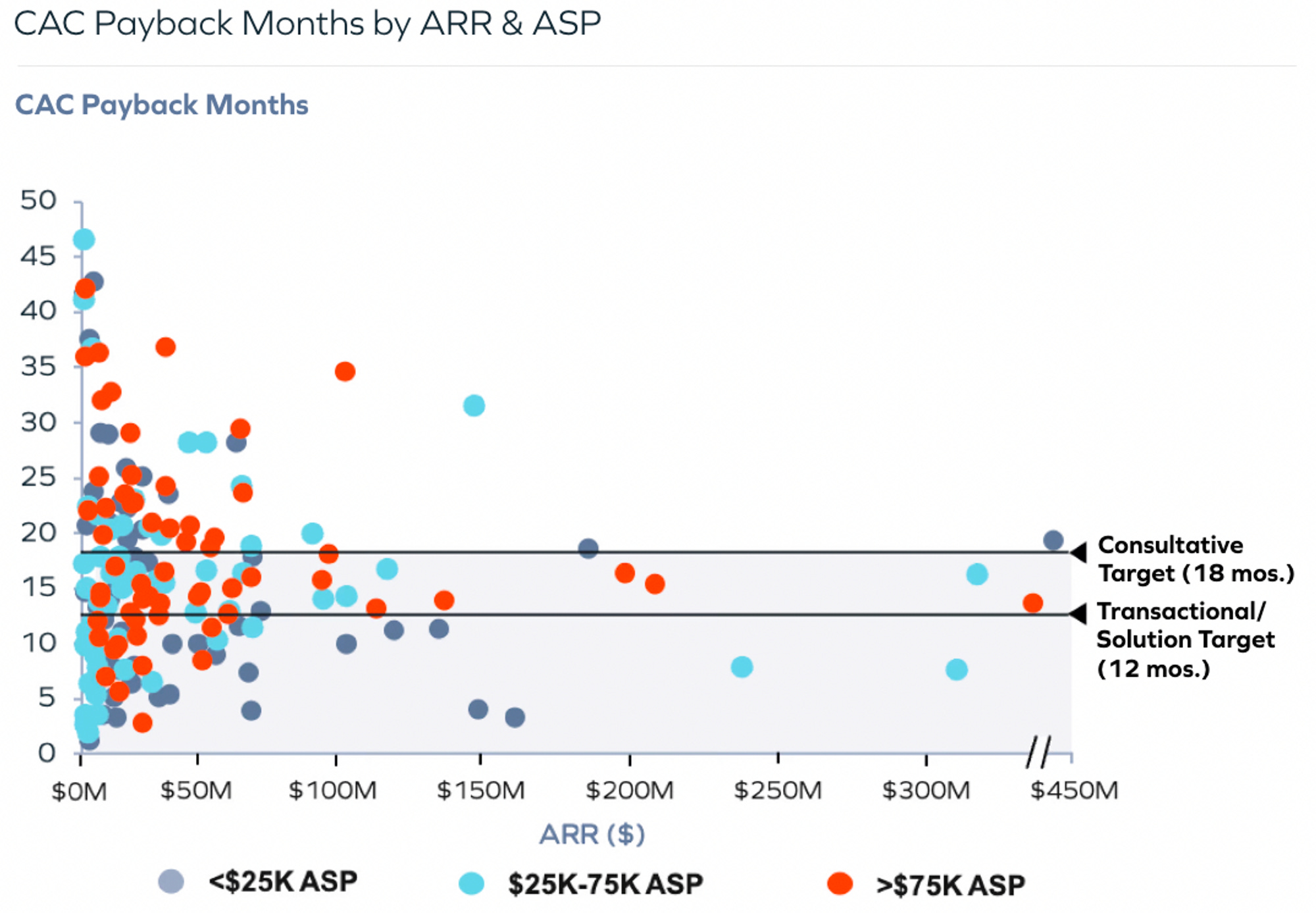

Saturday, Jun. 17th: Insight published a report on the sales-related metrics that companies should track as they grow to $100m ARR. - Insight

At early stage (below $10m in ARR), startups should track win rate (proportion of sales opportunities that are won, should be between 20-40% for new logos), growth in new and expansion bookings (should be above 100%) as well as NPS (should be greater than 50) and gross revenue retention (% of revenue retained from the prior year without including the impact of upsell or cross-sell, should be above 65%).

At mid-stage (between $10m and $100m in ARR), startups should track CAC & CAC payback, net revenue retention and the mix between new and expansion bookings.

Sunday, Jun. 18th: Jerry Chen at Greylock wrote about the new moats in an AI-first world. - Greylock

“To paraphrase Darwin: What is not the strongest (largest, most capitalized, or most well known) of companies that survives but the most adaptable to incorporating AI.”

“AI is becoming the platform technology of today, and this new LLM wave could potentially disrupt the hierarchy among incumbents. Case in point, through the integration with OpenAI’s ChatGPT, Microsoft’s long-maligned Bing may finally disrupt Google’s search moat.”

“There is potentially a world where big models address most of the complex problems, but smaller models solve specific problems or power applications at the edge like your phone, car, or smart home.”

“While the rise of AI is exciting, in many ways we have come full circle in our quest to build new moats. It turns out that the old moats matter more than ever. […] The value of the application is how to deliver the value. Workflows, integration with data and other applications, brand/trust, network effects, scale and cost efficiency all become drivers of economic value and the creator of moats. […] AI doesn’t change how startups market, sell, or partner. AI reminds us that despite the technology underpinning each generation of technology, the fundamentals of business building remain the same.”

Monday, Jun. 19th: After filing for bankruptcy, Luko is being sold to Admiral, a UK online insurance specialist, for €14m. This includes a €3m earn-out for the founders based on their performance. Luko is a French startup which had raised €70m across multiple funding rounds with prominent investors such as EQT and Accel, resulting in a last valuation of approximately €250m. Luko aimed to disrupt the home insurance market. Venture investors have been completely wiped out as the company had €45m in debt with TriplePoint and BNP, which will be partly repaid. Luko had acquired two companies (Coya which was a home insurance startup in Germany and Unkle which was a broker specialised in rental guarantees) which must now be sold separately. Prior to filing for bankruptcy, Luko faced challenges in raising external capital and finding a buyer for the company. B2C online insurance is notoriously difficult due to high customer acquisition costs, low profit margins and limited willingness to pay. Similar companies in the public market, such as Lemonade or Root, have experienced significant declines in their market value, making it extremely challenging for private consumer insurance firms to secure the next round of funding. Unfortunately, Luko found itself backed into a corner due to these circumstances. - Les Echos (🇫🇷), Maddyness (🇫🇷)

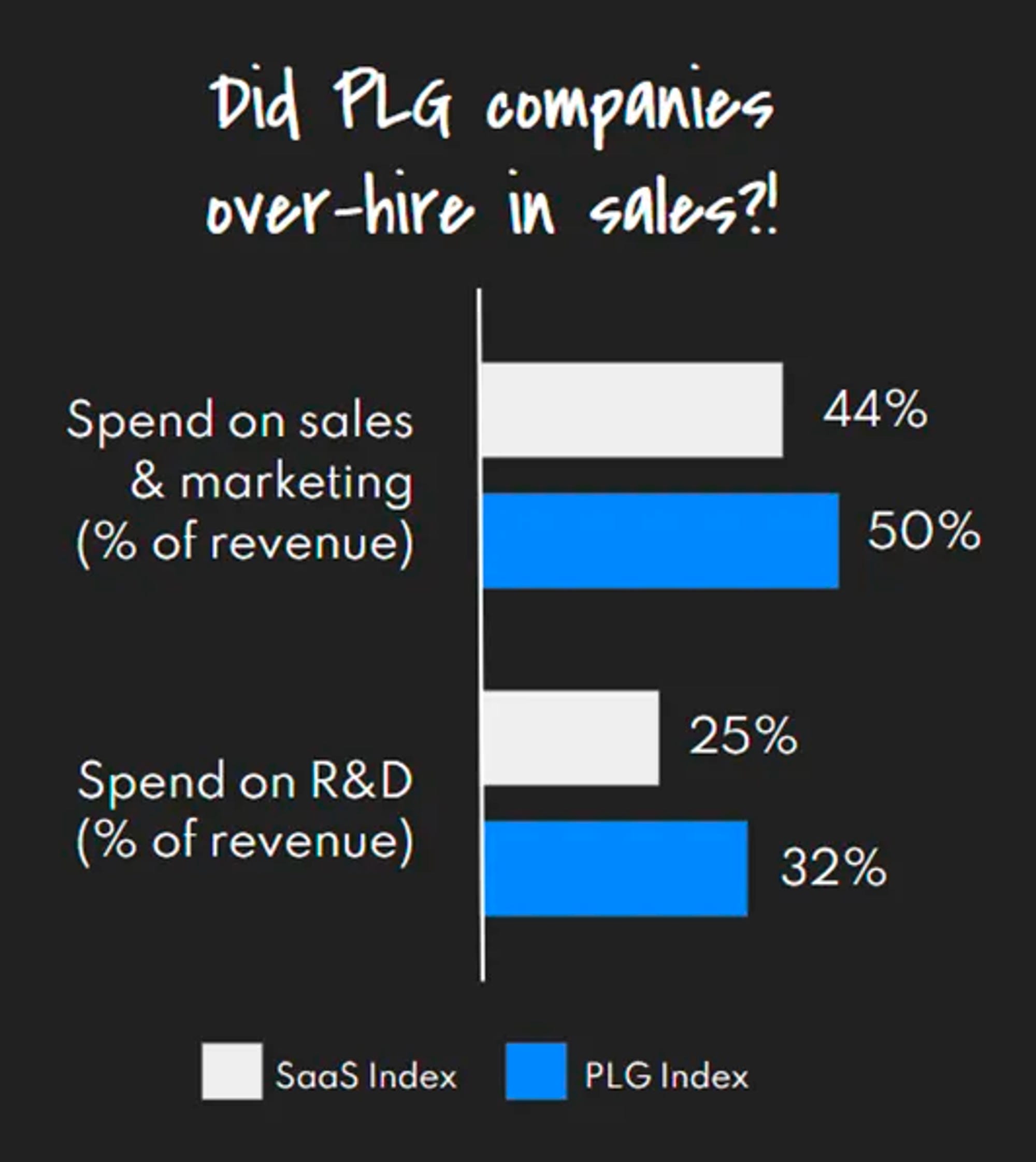

Tuesday, Jun. 20th: Kyle Poyar from Openview wrote an article discussing how PLG companies incorporate sales into their GTM strategy. - Growth Unhinged

It’s incorrect to assume that PLG companies do not have sales teams. Openview has demonstrated that publicly listed PLG companies actually allocate a higher percentage of their revenues to sales & marketing spend compared to traditional SaaS companies.

Kyle shares a 5-step playbook: (i) start with the customer journey, (ii) validate that sales is incremental, (iii) identify product signals to drive engagement (what product activity is the most predictive of future revenue generation?), (iv) define the right sales plays, (v) be thoughtful about comp & operations.

Several sales plays could be implemented by PLG companies like: (i) creating a feedback loop between CS and sales when a customer reached out to the support team, (ii) warm outbound to users which are already on the free or self service plans, (iii) inbound hand raisers with specific touch-points in your website/product (e.g. ask for a demo).

“Sales will be closest to the customer. Product-led companies tend to be data-driven rather than customer-driven. Sales’ experience can bring PLG companies closer to their customers.”

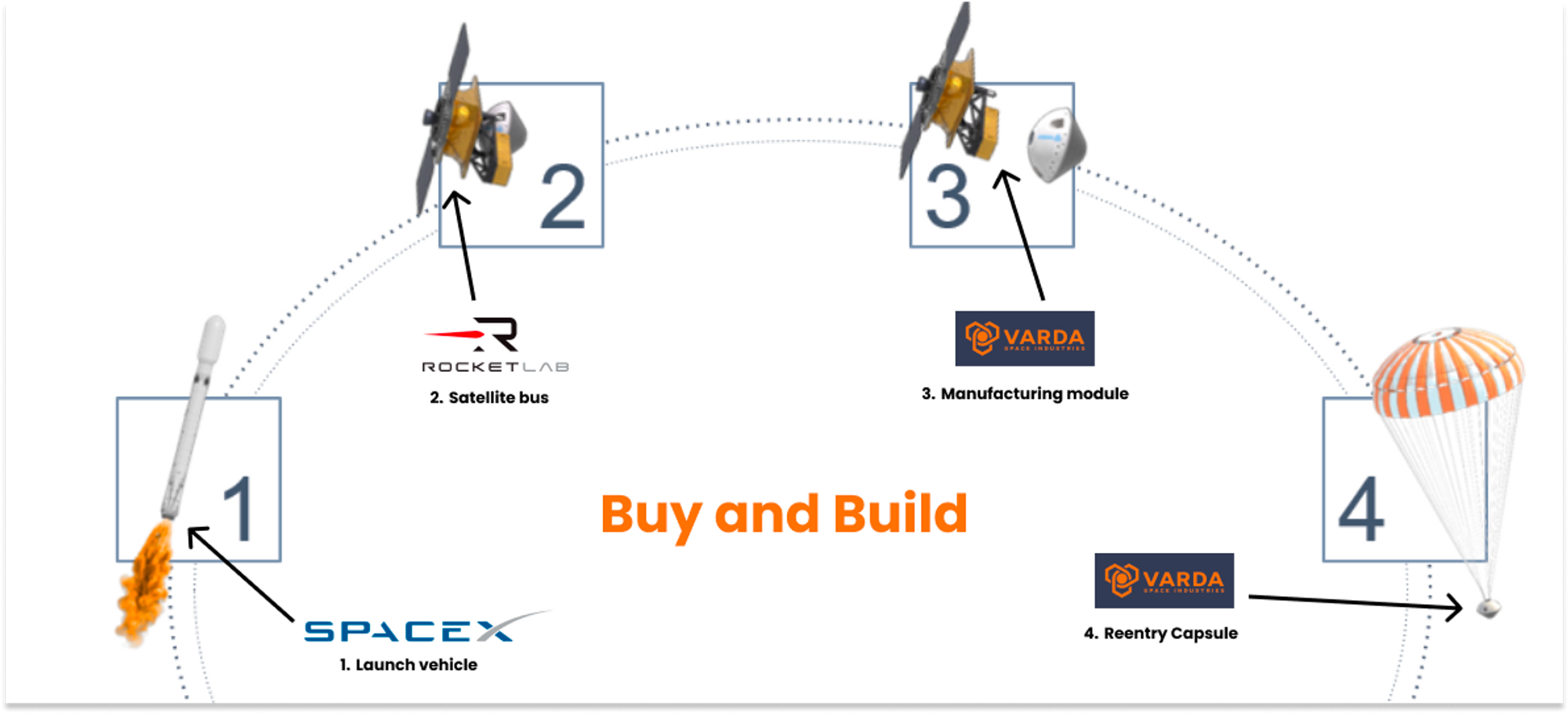

Wednesday, Jun. 21st: Not Boring published a piece on Varda. It develops factories in space. Certain products are easier to manufacture in a zero-gravity environment. Varda can dispatch a production facility into space by hitching a ride on commercial launch vehicles. Once in orbit, the production facility commences operation. After the product is manufactured, it is returned to Earth using Varda's re-entry vehicle. - Not Boring

As the cost of satellite launches decreases, it's starting to become commercially viable to manufacture products in space.

Thanks to SpaceX, “the number of objects launched into space annually has increased 10x, from 222 in 2015 to 2,163 in 2022”. “The existence of SpaceX and the dramatically cheaper and more frequent launches it offers makes space businesses not only possible, but economically viable.”

“To be successful, the company needed to excel at three key things - manufacturing in space, getting the payload back to Earth, and selling to both commercial and government customers.”

Varda raised a $9m seed round in Dec. 2020 co-led by Founders Fund and Lux. Varda collaborates on a $60m program with the US department of defense for its re-entry vehicle in order to do hypersonic testing for the US Air Force.

To build a successful deep-tech company, you need (i) to know the milestones that investors want for your next rounds and execute against them and (i) to generate revenues in its first three years.

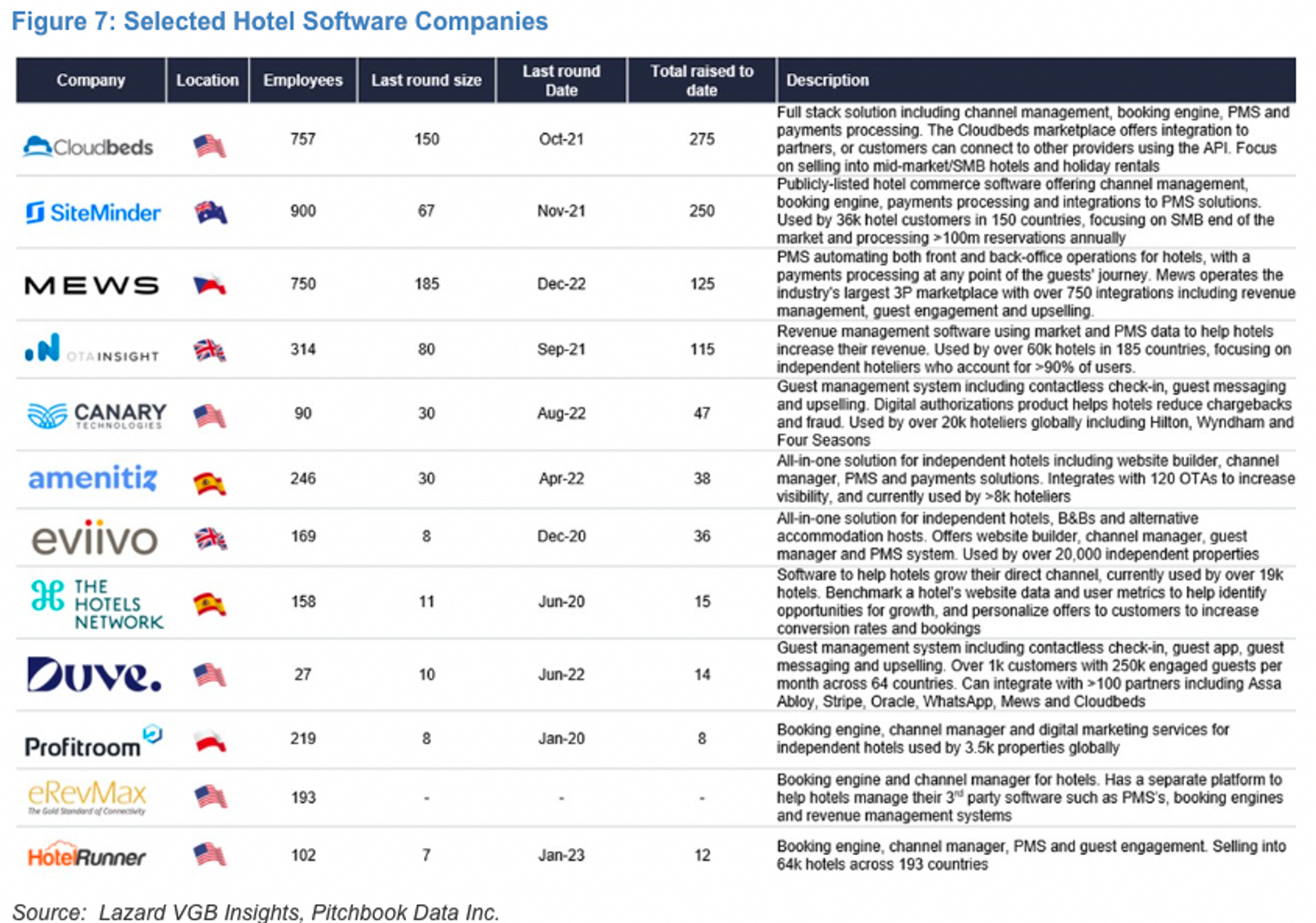

Thursday, Jun. 22nd: Lazard has published a report on hotel management software. Special thanks to Hadrien for sharing this!- Lazard

The hospitality sector allocates approximately 3.5% of its revenue towards software expenditures. Lazard estimates the global hotel management software market, encompassing hotels, alternative accommodations, and travel experiences, to be worth $10bn.

The market growth is driven by multiple factors including: (i) the shift to the cloud, (ii) the SMB adoption of software tools, (iii) tightness in the labour market, (iv) the fight with OTAs which have now a penetration rate above 50%.

“Trends in consumer behaviour and growth in personalisation and experiential travel have increased the need for end-to-end guest engagement.”

Friday, Jun. 23rd: Nelly raised a €15m series A led by Lakestar. It’s a German fintech serving the healthcare industry. Currently, it works with 450 healthcare practices. It digitises admin and financial tasks associated with a practice visit, thereby saving payment fees and admin time. It’s a growing trend in vSol to see fintech being used over SaaS as a Trojan horse to digitise an industry. - EU Startups, TechFundingNews

“91% of independent healthcare professionals express a desire for reduced documentation and administrative tasks.”

“Nelly aims to address this problem by introducing a digital solution for patient admission, invoicing, and payment.”

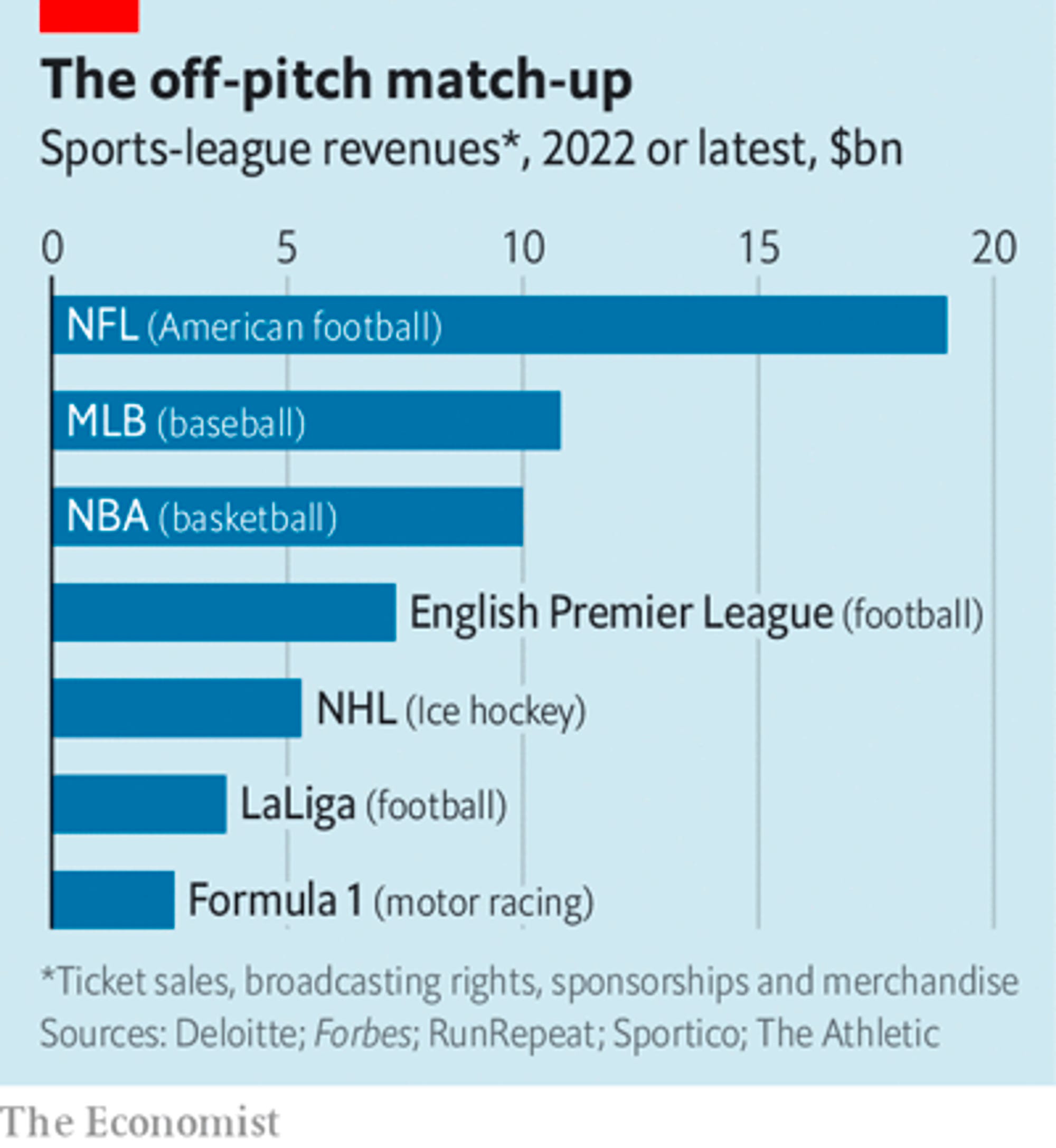

Saturday, Jun. 24th: The Economist recently published an article comparing the closed-league sports systems in America with the open ones in Europe. - The Economist

The U.S. sports system promotes greater predictability in club business performance. This is because clubs are not threatened with the risk of relegation to lower leagues, which could potentially devastate their finances. Additionally, mechanisms like the draft system and salary cap contribute to long-term parity among clubs.

“American sporting socialism, then, appears to lead to more competitive contests than Europe’s winner-takes-all approach.”

“As a result, American teams, which partake in the bonanza, fetch higher valuations. Over the past decade the value of the average NFL and NBA teams has grown by more than 300% and 600%, respectively, compared with a rise of 170% for America’s booming stock-market.”

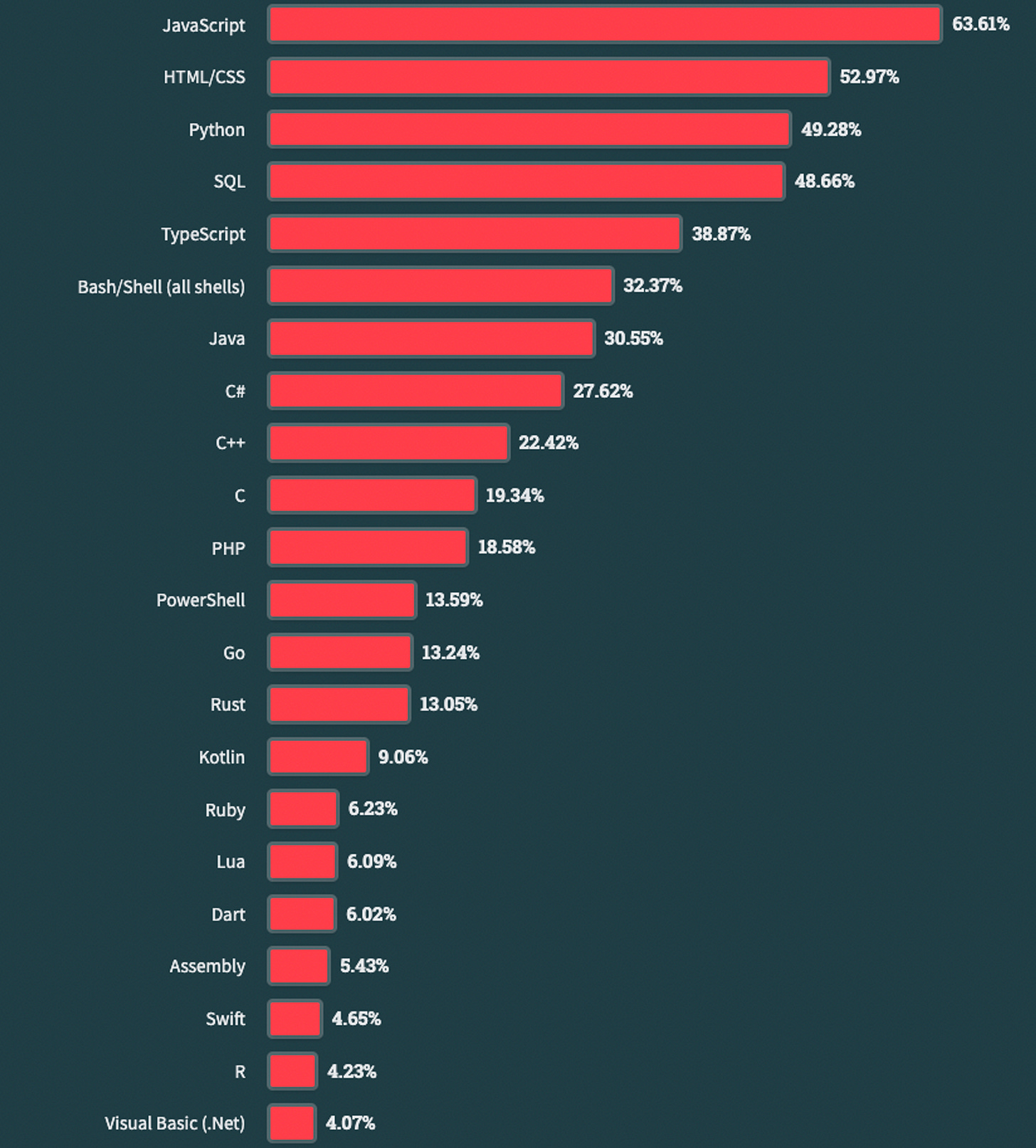

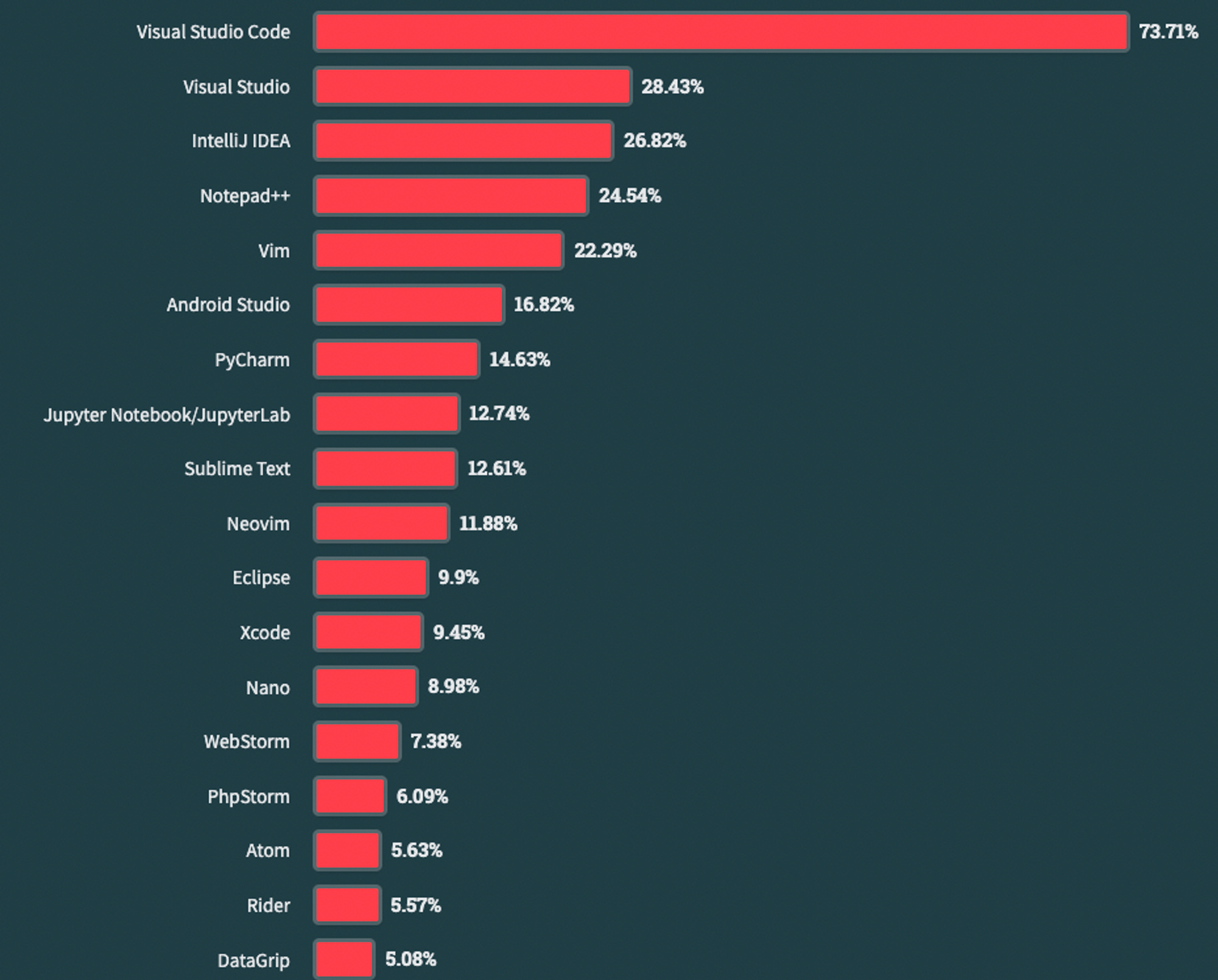

Sunday, Jun. 25th: StackOverflow published its 2023 Developer Survey. - Stack Overflow

“70% of all respondents are using or are planning to use AI tools in their development process this year.” 55% of developers are using GitHub Copilot. AI is mostly used to write code, to debug code or to document code.

“Hybrid is here to stay for larger organizations; over half of employees in 5,000+ organizations are hybrid. The smaller organizations are most likely to be in-person, with one out of five organizations with fewer than 20 people report being in-person.”

JavaScript, HTML/CSS and Python are the three most commonly utilised programming languages.

Among developers, AWS, Microsoft Azure, and Google Cloud are the most commonly utilized cloud platforms.

Visual Studio Code is the preferred IDE used by developers, ranking above Visual Studio and IntelliJ IDEA.

Monday, Jun. 26th: 20VC has co-created and co-raised a $5m fund named 20SALES, which will be managed by 8 women possessing in-depth B2B go-to-market expertise gained from working at companies such as Amplitude, Salesforce, MongoDB, Slack, Airtable, Vanta, Dropbox, Segment or Webflow. The fund plans to invest in pre-seed, seed and series A B2B SaaS companies with $100k ticket sizes. Harry Stebbings will serve as an advisor to the fund while the women managing it will do so part-time. I think it’s a fund with a clear, strong and differentiated value proposition for founders. I like the focus on GTM and the fact that it’s managed by active operators who can offer real time insights from the field. - Techcrunch

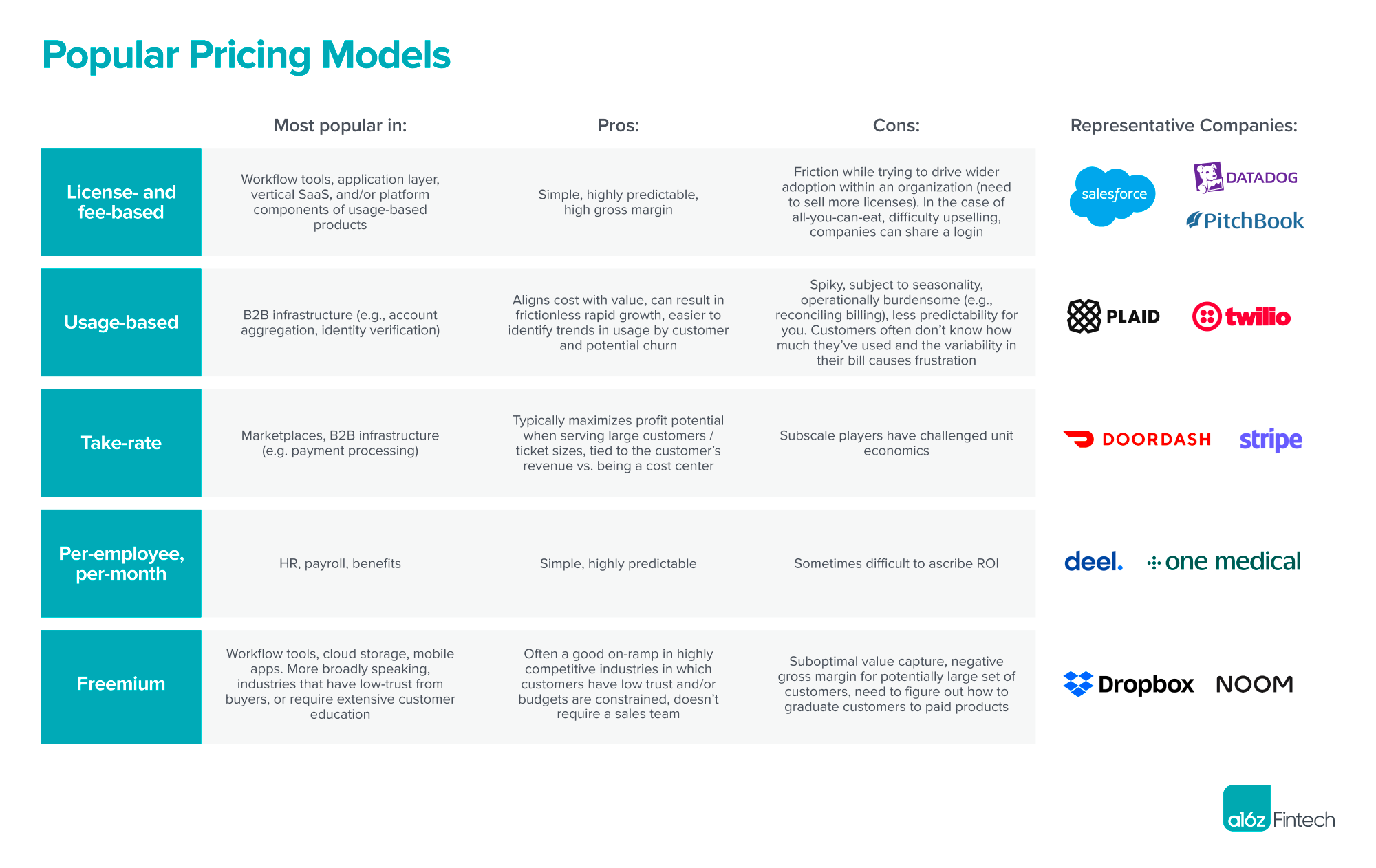

Tuesday, Jun. 27th: a16z wrote about pricing for B2B fintechs. - a16z

“Most B2B fintech companies employ a combination of these mechanisms [license based, usage based, take rate, per employee per month, freemium] to ensure business model resilience. Payments companies, as an example from our take-rate category, typically combine a flat dollar-based charge alongside a percent-based fee when processing a payment (e.g., $0.30 + 2.9%).This allows them to preserve their unit economics when handling a large number of small-dollar payments. They might also charge their customers “platform fees,” which are basically flat monthly SaaS fees, for the privilege of accessing the technology in the first place, or they might charge an implementation fee to help drive commitment and therefore initial adoption.”

“One overarching theme that we’ve seen is: don’t overcomplicate things. In the early days, the owner of pricing should be the person with the best intrinsic sense of the value being offered by the product. Any explicit pricing work done should be to ensure that you’re directionally right, and you shouldn’t distract yourself with optimizing for the incremental 1 or 2% improvement at the margins. As you scale, pricing can and should become more of a science that’s ripe for all the A/B testing and scatter plotting needed to ensure you’re accomplishing your most important priorities.”

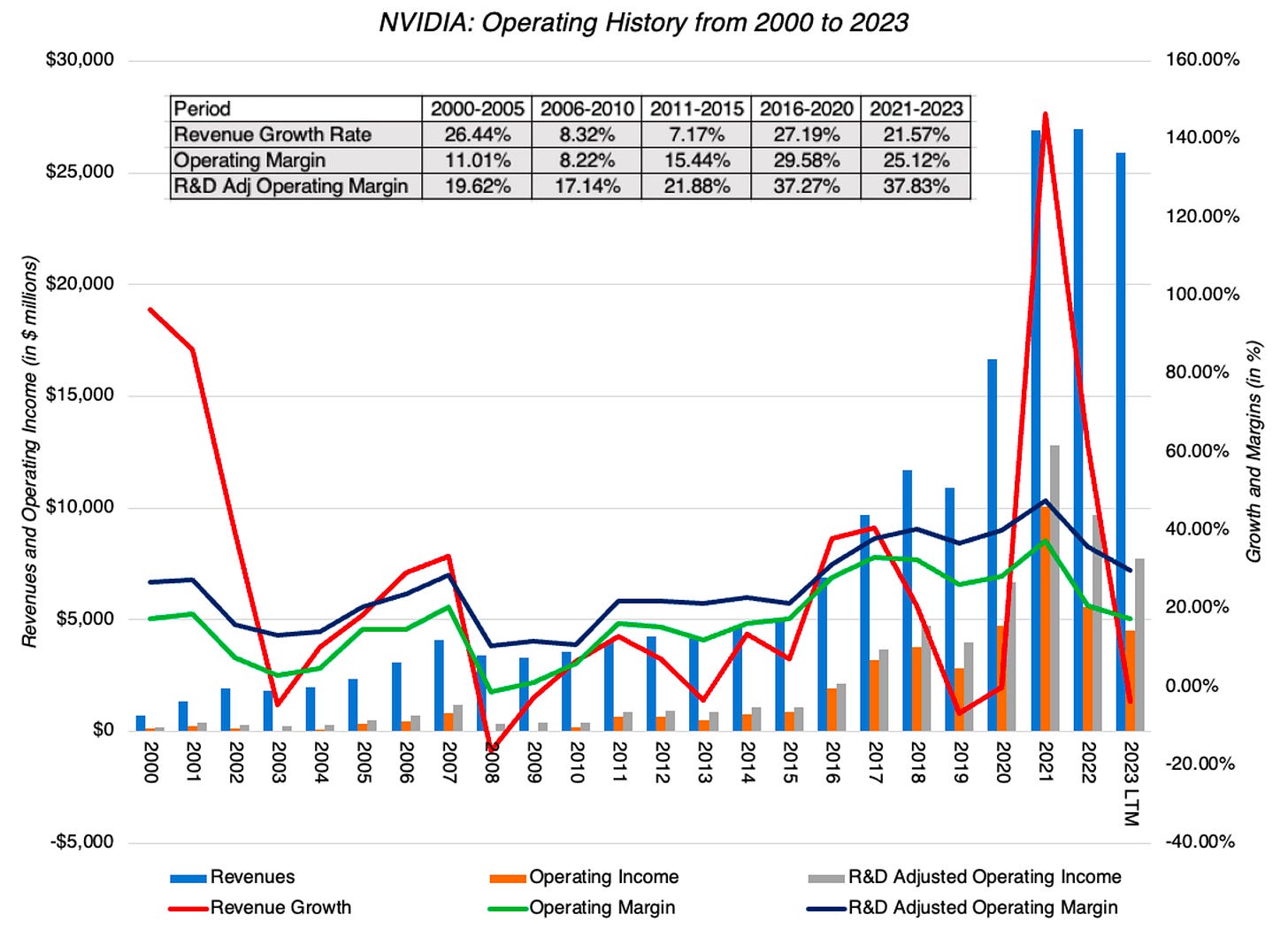

Wednesday, Jun. 28th: Aswath Damodaran has revised his valuation of Nvidia, aiming to reconcile its current public market capitalization with the ongoing hype around AI. - Aswath Damodaran

Nvidia was founded in 1993 by Jensen Huang. It went public in 1999. It became an important player in the semiconductor space thanks to correct bets in the gaming and crypto markets.

“There are two impressive components to NVIDIA's history. The first is that it has been able to maintain impressive growth, even as the industry saw a slowing of revenue growth (3.97% between 2011-2020). The second is that this high revenue growth has been accompanied not just with profits, but with above-average profitability, as NVIDIA's gross and operating margins have run ahead of industry averages. NVIDIA has clearly embraced a strategy of investing ahead of, and going after, growth markets for the chip business, and that strategy has paid off well. Thus, its current dominant positioning in the AI chip business can be viewed as more evidence of that strategy at play.”

“The company had near-death experiences, at least in market value term, in 2002 and 2008, losing more than 80% of its market value. […] Even the biggest winners in the market have had periods when investors have turned intensely negative on their prospects, making them attractive as investments for value-focused investors.”

“Where does AI fall on this spectrum from revolutionary to incremental to minimalist change? A year ago, I would have put it in the incremental column, but ChatGPT has changed my perspective. That was not because ChatGPT was at the cutting edge of AI technology, which it is not, but because it made AI relatable to everyone.”

“It is indisputable that each of the revolutionary changes of the last four decades has created winners within the space, but a few caveats have also emerged. The first is that these changes have given rise to businesses where there are a few big winners, with a few companies dominating the space, and we have seen this paradigm play out with software, online commerce, smartphones and social media. The second is that the early leaders in these businesses have often fallen to the wayside and not become the big winners. Finally, each of these businesses, successful though they have been in the aggregate, have seen more than their share of false starts and failures along the way.”

“The driver of NVIDIA's success has been its high-performance GPU cards, but it is very likely that the businesses that bought these cards and drove NVIDIA's success in the last decade will be different from the businesses that will make it successful in the next one. For much of the last decade, it was gaming and crypto users that allowed the company to set itself apart from the competition, but the bad news is that both of these markets are maturing, with lower expected growth in the future. The good news, for NVIDIA, is that it has two other businesses that are ready to step in and contribute to growth. The first is AI, where NVIDIA commands a hefty market share of what is now a relatively small market, but one that is almost certain to grow ten-fold or greater over the decade. The other is in the automobiles business, where more powerful computing is seen as the ingredient needed to open up automated driving and other enhancements. NVIDIA is only a small player in this space, and while it does not enjoy the dominance that it does in AI, a growing market will allow NVIDIA to acquire a significant market share.”

“Even if you buy into the argument that AI will change the ways that we work and play, it does not necessarily follow that investing in AI-related companies will yield returns. In other words, you can get the macro story right, but you need to also consider how that story plays out across companies to be able to generate returns.”

Thursday, Jun. 29th: Kerrisdale Capital published a short-selling report on Carvana. - Kerrisdale

“Despite the stock’s fall from all-time highs, Carvana shares are worthless. Comparisons to tech/e-commerce platforms are nonsensical. Carvana should be valued like any other publicly traded auto retailer, and specifically one that is poorly capitalized and more cyclical due to a lack of diversification and subprime exposure. We view the equity as a zero and investing at current levels is a worse deal than buying a clunker from a slick used car salesman.”

“The company inspects and reconditions all owned vehicles offered for resale utilizing in-house logistics to deliver cars directly to customers. Customers in certain markets can also pick up their vehicle at one of Carvana’s 33 car vending machines – multi-story glass towers that store purchased vehicles – a silly marketing ploy emblematic of how the company lit investor capital on fire during the tech bubble.”

“The used car market is large and fragmented. Though it represented the lowest mark in a decade, there were an estimated 36.2 million used vehicle transactions in 2022. As of 2021, the top 100 used car retailers collectively held 11% market share, with the largest commanding only 2.3%.”

“While Carvana management tries to paint its peers as old-fashioned slow movers, the reality is that the industry is overrun not only by scrappy local players constantly sacrificing profit to guard market share, but also sophisticated multibillion dollar behemoths actively building out their own data analytics and software capabilities to adopt the most cutting-edge tech-enabled industry standards.”

“Carvana depends heavily on the sale of these finance receivable [lending for car purchases via financing partners] for a substantial portion of gross profit and EBITDA.”

“Carvana is a “controlled company” with a dual-class share structure. Class A shares hold economic interest and carry one vote. Class B are effectively similar but enjoy 10:1 super voting rights and are 100% owned by the Garcias (Ernest the CEO and his father). The Garcias together have approximately 88% voting power.”

“There’s not a depth of auto experience in the Carvana executive team…Everything they’re experiencing is for the first time…they don’t know what they haven’t seen yet.” — Former Carvana senior manager

“Many of the consumer-friendly offerings that helped Carvana rapidly gain share are no longer unique. […] Carvana has had to adopt the less consumer friendly practices of dealers it once derided, in order to generate more profit. Over the past year, Carvana has dramatically narrowed the size and breadth of inventory (reducing customer selection) and added return fees, incentivized pick-ups, and begun charging a higher delivery fee when a customer wishes to purchase a vehicle that is further away (reducing customer convenience).”

Friday, Jun. 30th: This Week in Fintech published a report on the future of money movement. - This Week in Fintech

“We believe that the future of money movement is real time, transparent, and multi-rail – in which no single solution dominates globally, but rather specific rails gain prominence for particular industries and use cases. Achieving this vision will require a focus on both infrastructure and the operating and user experience layers that sit on top of these rails. Simplicity for the end user is vital, and the best infrastructure will be invisible; money will just work.”

New payments rails should have the following characteristics: (i) improvements in cost, transparency & speed, (ii) interoperability, (iii) effective governance & compliance, (iv) modern security layers, (v) risk controls and (vi) value added services.

“For 50 years, ACH has been one of the primary rails for US payments, surpassed by credit cards only in 2010. In February 2019 alone, ACH payments per day exceeded 100 million. But it has struggled with a central issue: settlement times. ACH transactions are still processed today on the same computer tapes rolled out in the 70s, which run once a day, and normally take a few more days to settle between banks. In 2016, the Automated Clearinghouse Association (NACHA) rolled out same-day ACH for credit (also called push payments), and in 2017 for debits (pull payments). But same-day still doesn’t mean instant, and many banks still charge consumers to cover same-day ACH fees.”

“Payments innovations typically gain traction when performance and incentives align with needs of their target users, and improvements over alternatives justify the switching costs.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋