📖 Venture Chronicles - July 2025

Overlooked #203

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of July.

I’ve decided to reformat my Venture Chronicles to make them easier to read. Instead of sharing one news item per day, I'll now curate updates and insights around three themes:

Vertical software

General Venture Capital

Entropy - other news and personal topics of interest

Let’s go!

Vertical Software

Clio acquired vLex for $1bn in a mix of cash and stock. - Clio, Techcrunch, Reuters

Clio is a vertical SaaS in the legal industry selling practice management software used by 200k+ legal professionals. It previously raised $900m in Jul. 2024 (primary & secondary) at a $3bn valuation. Clio also disclosed to have reached $300m in ARR.

vLex is a proprietary database of 1 bn editorially enriched legal documents (cases, statutes, regulations, journals) used by 2.8m users from 100+ countries. It built AI tools on top of this data to support on research and drafting. It competes with LexisNexis and Thomson Reuters.

It’s a way for Clio to double down on AI by acquiring a unique data-set and AI tooling built on top of it. Clio will integrate vLex’s AI capabilities into its platform. vLex started in 1999. It was a bootstrapped business that exited to Oakley Capital in 2022.

“It combines Clio’s legal operating system—trusted by more than 200,000 legal professionals—with vLex’s cutting-edge legal intelligence platform, which includes Vincent, its groundbreaking AI, built on the industry’s most comprehensive global legal database.”

“vLex is a valuable property because its database of legal documents can greatly improve AI models for lawyers. Data is one of the only long-term defensible competitive moats a company can have in the space.”

Thoma Bravo acquired Olo for $2bn in cash in another take-private of a vertical software company. - Thoma Bravo

Olo is a vertical SaaS company providing digital ordering, delivery, and payment solutions for restaurants chains. It works with 750 restaurants brands and 88k locations.

Since its IPO in March 2021 at a $3.5bn market capitalisation, Olo have had a rough journey as a public company having to shift the company from growth at all cost to a better growth-profitability balance and being too small to be interesting to investors.

It’s a great acquisition for Thoma Bravo for 3 main reasons: (i) it’s still a founder led company and Noah Glass is an amazing CEO, (ii) Thoma Bravo invests post-turnaround in a business that is both profitable and growing above 20% YoY, (iii) as a private company, there will be opportunities to aggressively expand Olo’s product surface with tuck-in acquisitions.

“The value of acquisitions by buyout firms YTD is up 11.7% to $580bn compared with the same period last year.”

AirGarage raised a $23m series B led by Headline. It’s a vertical software for parking facilities. It’s an operating system combining payment, dynamic pricing, gate-less operations and license plate-reading cameras to improve parkings’ efficiency. Founded in 2017, it raised $41m in total from investors including Founders Fund and a16z. - Axios

AirGarage has grown revenues by 10x since its series A in 2021 and it’s a cash flow positive business. It’s used by 300 parking facilities.

MaintainX raised a $150m series D from Bessemer and Bain at a $2.5bn valuation. It previously raised in Dec. 2023 at a $1bn valuation. It’s a vertical SaaS in manufacturing founded in 2018 streamlining equipment maintenance and operations. It serves 11k customers and manages 11m assets. It has 600 employees including 40% in R&D. - Reuters, Bloomberg

“It will use the new funds to accelerate research and development, to launch its business providing software to the US government, and to speed an expansion into South America and Europe.”

“The startup’s software works by gathering data from third-party sensors positioned on machines to measure vibration, heat and other indicators, helping it predict what is likely to break and how. The software also lets customers confirm equipment and parts are in stock, schedule maintenance and perform other back-end operations.”

General Venture Capital

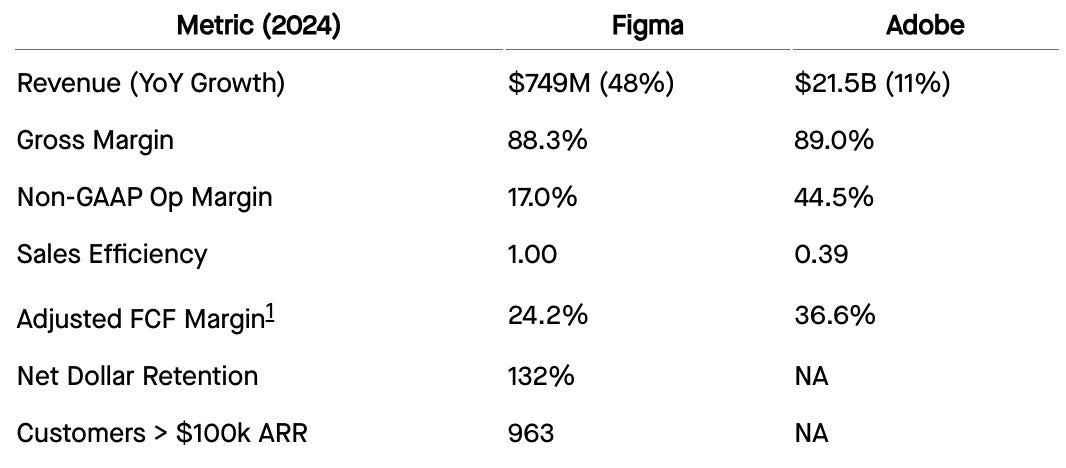

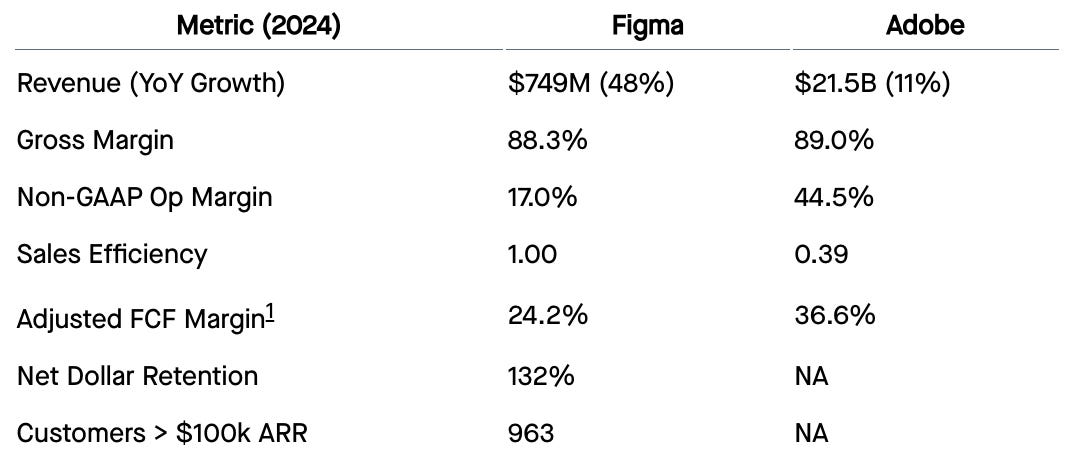

Figma went public in a blockbuster IPO raising $1.2bn (only $412m in primary) and closing its first day at a $60bn valuation after a 250% increase in share price. - Tom Tungunz, FT

“Figma is about 3% the size of Adobe but growing 4x faster. The gross margins are identical. The data also shows Figma’s Research & Development spend nearly equals Sales & Marketing spend. This is the PLG model at its best. Figma’s product is its primary marketing engine. Its collaborative nature fosters viral, bottoms-up adoption, leading to a best-in-class sales efficiency of 1.0. For every dollar spent on sales & marketing in 2023, Figma generated a dollar of new gross profit in 2024. Adobe’s blended bottoms-up & sales-led model yields a more typical 0.39.”

“Figma, with its 48% growth, would be the fastest-growing software company in this cohort setting aside NVIDIA. Applying our model’s predicted 19.9x multiple to estimate forward revenue yields an estimated IPO valuation of approximately $21bn.”

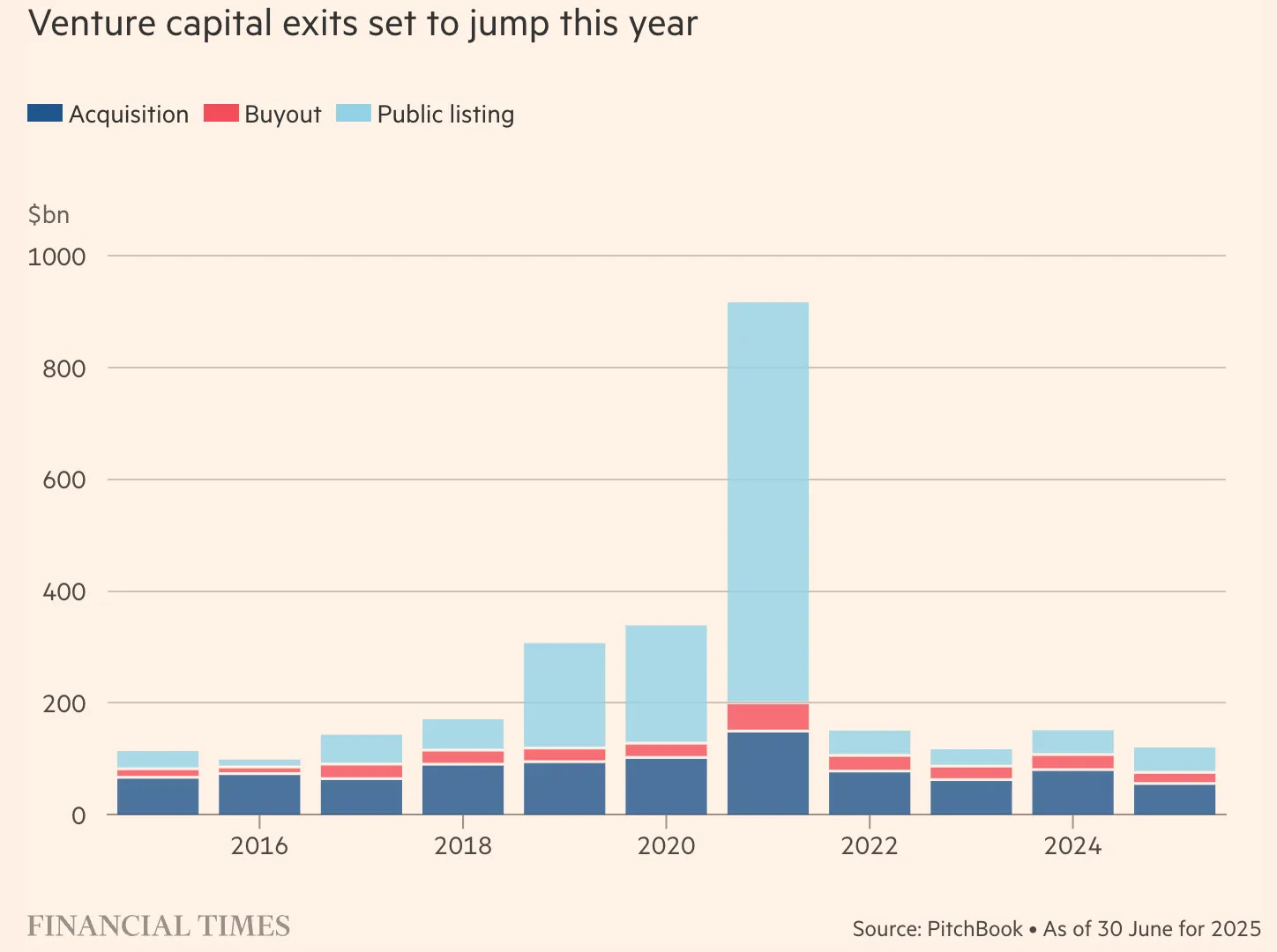

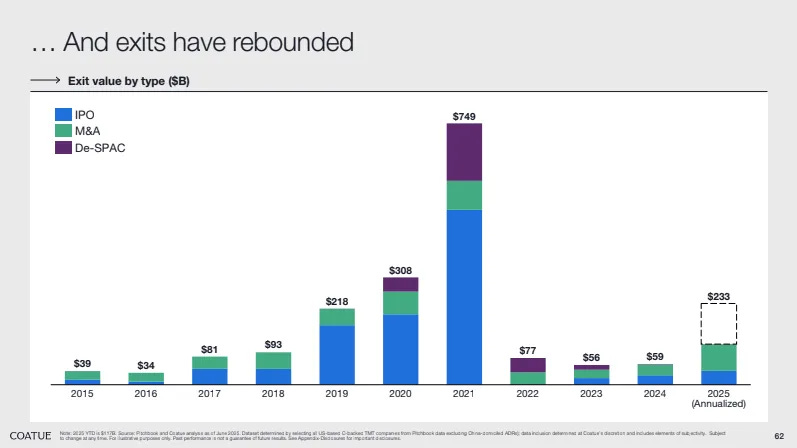

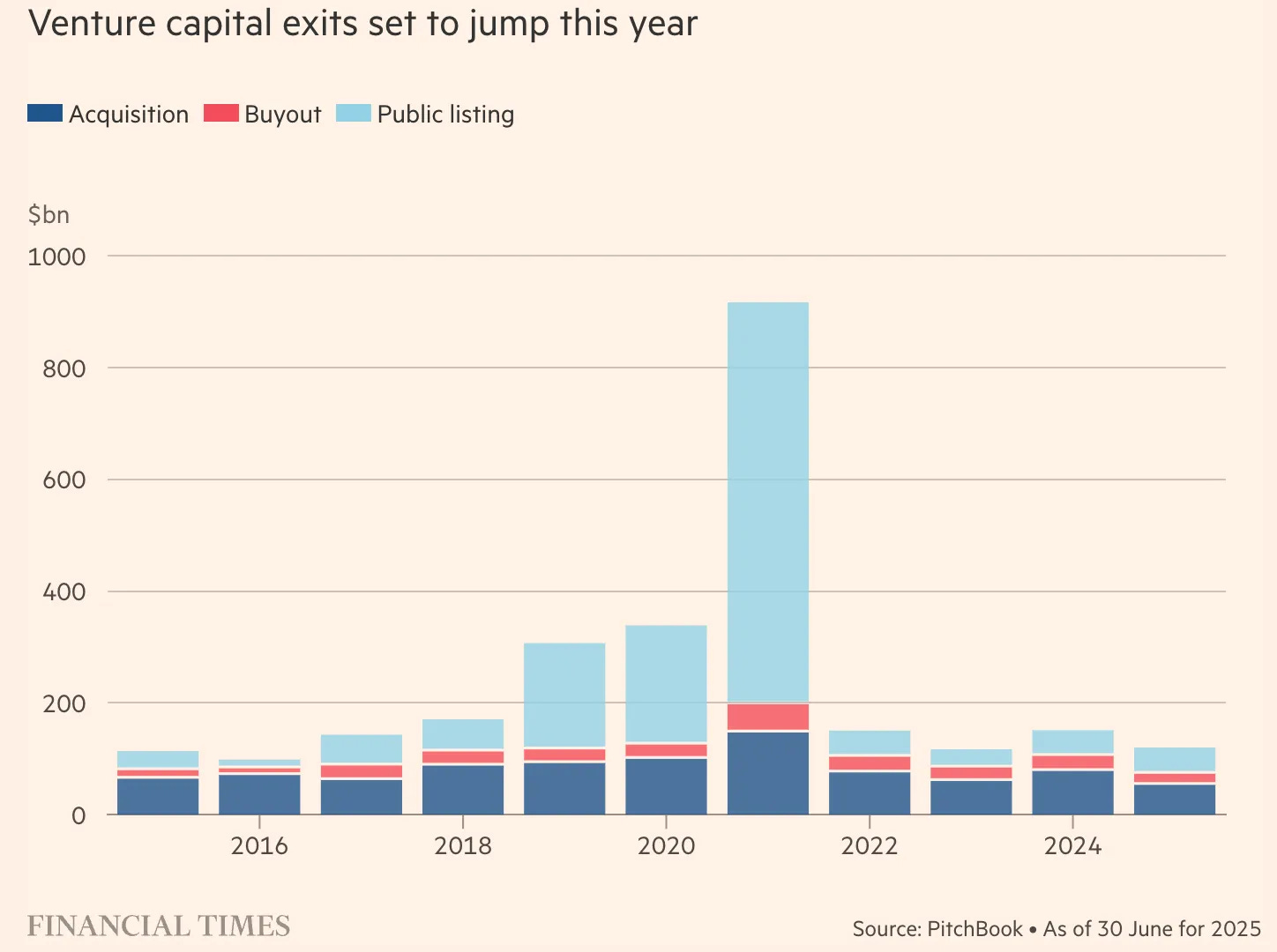

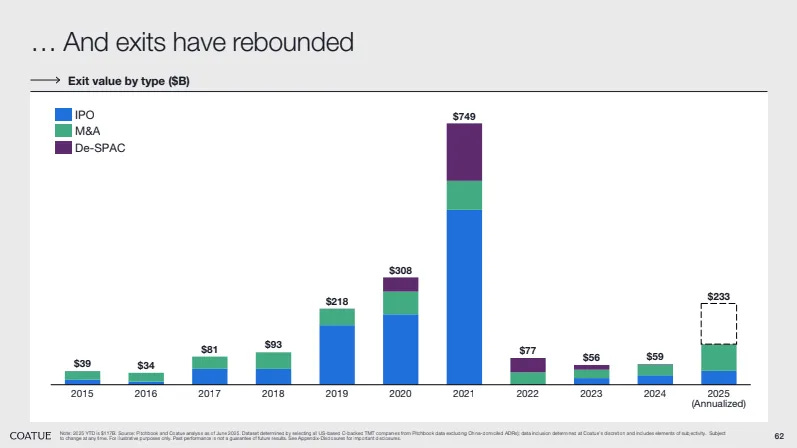

“Figma’s exit comes at a time when “exits” — events where venture investments are realised — are starting to pick up. Through public listings, acquisitions and buyouts, exits by venture reached $67.7bn in the second quarter of this year. That was a big jump from $38.5bn a year before and the strongest showing since the end of 2021.”

“According to hedge fund Coatue, exits fell to only 40 per cent of the value of new VC investments last year — a measure of just how little the industry was returning to its backers, relative to how much capital it is putting to work. With this year’s partial recovery, they have rebounded to roughly match new investments. But a healthy venture investing market, bringing steady returns for investors, would require the value of exits to reach twice the level of new investments, according to Coatue.”

“Another encouraging sign has been the willingness of some companies that raised money at the peak of the 2021 venture boom to bite the bullet and accept that they are worth far less today.”

Jack Altman interviewed Mamoon Hamid who is a partner at Kleiner Perkins. - Uncapped

Timing is everything in tech investing. "A lot of stuff that happened in the dot-com boom, the timing was just off. There weren't enough eyeballs or people ready to adopt these products and technologies. It took 5-7 years later for them to become mainstream behaviors.”

Small user base + high engagement beats large numbers. “If there's one learning I've had over my career, it's that small N, high engagement is a really good signal to invest in a company and get early.”

Look for founders with true intentions. "I'm looking for true intentions. Do you really want to be doing this for the next decade of your life? Are you doing it for money, fame, or power? Or do you just really want to solve problems that exist in the world?”

“Despite having lived through market cycles, you need to keep an open mind and some naivety. Otherwise, you're going to miss everything. You have to have a glass-half-full mentality and imagine the possibilities, the optimism of the technology shifts occurring in front of us. You have to keep an open mind and think about the "why now". The lesson is timing.”

“AI is to us the super cycle of all super cycles. We've been on a quest to invest in what we think will be generational companies.”

“If you look at that $100 trillion of GDP today, 60% of it is labor—human labor. AI is not just a new way of working or new productivity technology or new consumer apps. There's an element of labor—doing the actual work autonomously. That is a $60 trillion opportunity.”

“We created a job pyramid. At the top are highly skilled workers who are highly paid but fairly scarce—doctors, lawyers, engineers. If you look at the top 20 jobs in the US by pay, those are doctors, lawyers, and engineers. We thought about investing in co-pilots for these job types. Why co-pilots? Because two and a half years ago, they were nascent in terms of capabilities and would become more autonomous over time. But co-pilots because there are parts of these jobs that are very nuanced and the human brain needs to process those parts. But there are parts that AI can do—like scribing or taking notes as a physician when talking to a patient. We invested in Ambience for doctors and clinicians, Harvey for lawyers, Windsur for engineers—taking that layer-by-layer approach to different job types. That pyramid of highly skilled, highly paid making $200K+ a year.”

“Taking that pyramid structure, you go one layer below to jobs that are slightly less paid but still skilled—nurses, salespeople, financial analysts. Still very qualified, college educated. We found that some parts of those jobs you can do completely autonomously.”

“The end state, if you go down to the lowest paid and lowest skilled work, is physical labor. That's probably the hardest place to attack today. We're thinking much further out—robots, humanoids.”

“John Doerr has a drive like no other. When he sees something, he is relentless. He will not shake it off until he gets it. That's how he pursued Larry and Sergey as well as Jeff Bezos.”

“What made Kleiner so great and iconic and produced these epic returns was that we were early-stage specialists—a small partnership of early-stage technical people, practitioners who cared about the craft of venture capital, being in the trenches with founders, truly being their first partners and best partners.”

“Our mission statement is that we want to be the first call for founders who want to make history.”

“Can you live the KP culture, which is very much a servant culture? We're here to serve our founders. This is not about us as individuals. It's about our job to our founders—to work on their behalf tirelessly to help them become successful.”

“In a fund cycle, we invest in 35 companies. The math suggests we need two outlier outcomes and a couple more that are really great. Every partner has to deliver a company per fund that's a really good company. That becomes apparent from year four to seven, but you get multiple shots on goal.”

“Internally, our target is to see 60% of all Series As that get done by our peer group. Series A is what you care most about. We look at it religiously on a weekly basis—what Series As were announced, did we see it or not? Seeing means you actually met with the company, not just heard about it. You spent time on it and deliberately decided not to do it.”

“We keep a spreadsheet of all the losses and revisit them at every offsite. We look at whether we missed the good ones or not-so-good ones and what was missing in our playbook as to why we didn't win that investment.”

“For most of my investing career, I've been excited about productivity. I always saw that software in the cloud was a way better experience for productivity than desktop software.” It led Mamoon to invest in companies such as Box, Slack, Figma or Glean

“Slack’s engagement was insane—like 50% DAU/MAU, four hours a day inside the app.”

“I have a history of investing in companies that have been around for a while before I invest in them, but the new thing or the product they launch many years in is the thing that works.”

“If there's one learning I've had over my career, it's that high engagement is a really good signal to invest in a company and get early, get in earlier, not competitive, better pricing—all the things that come with better returns for our investors.”

“We have an early-stage fund today that's $800 million. The strategy there is we invest in about 35 companies per fund. In order to return a 5x on that fund, we need that to be $4 billion, which means that basket of companies has to be worth $40 billion and us own 10% of it for the math to work. The simple math: out of those 35 companies, you need to have two fund returners that get you pretty close to the 5x.”

“We have also a Select fund which is today $1.2 billion. Half the dollars typically go into our best companies like Figma, Rippling, and Glean, Harvey and others. We use it as a vehicle to double down into companies we're already on the boards of. Sometimes you can preempt it and do it very easily with the founders where it's easy for them, easy for us, and we want to give them more. The other half is things that we missed at the Series A or B. If we really kick ourselves, we'll do one to two of those a year where we missed out on the A and B and we're going to do it out of the growth fund.”

“I try to bring the best version of me to every meeting. It's not always possible, but I think of it as putting myself in the shoes of a founder. Typically pitching to VCs is the biggest thing you could be doing in that moment in time. It's intimidating. You're trying to raise capital. You're putting yourself out there. If I can make them feel just a little bit more comfortable and more respected and acknowledge the work that they're doing and all the blood, sweat, and tears that they're putting into this and the family sacrifice they're making and just empathize with that and have some humility around what they're trying to do, I think we can make that experience just better for all of us.”

Rob Go at NextView published a great post about the seed market. - Nextview

“Meanwhile, both mega-brewers and mega-VC funds have improved their offerings, and although craft players still exist in large numbers, the excess profits of this segment have been eroded to the point that most of these firms are not thriving.”

"As the VC industry has matured, two significant forces have emerged that have created massive problems for seed investors.” First, YC because “YC fundraising path tends to be orthogonal to the typical seed VC fundraising path.” "The second unstoppable force is the mega-funds. Some of these funds have programs similar to YC (e.g., A16Z speed run), so they capture an incremental portion of that same part of the market. But more significantly, the mega-funds are systematically targeting consensus founders and alumni, while offering unbeatable terms for initial funding rounds.”

“By consensus founders, I mean a) a repeat founder with some level of prior success, b) a star player of a top 50 company, or c) a super smart young person who is well networked into the tech elite.”

“Behind the formidable forces of YC and the mega-funds is a more fundamental shift in venture capital and in tech entrepreneurship overall. Over the last 20 years, one of the most controversial and non-intuitive tenets of investing went from being non-consensus to consensus. This is the idea of the power law.” “The best companies aren’t just 10X more valuable, they are 1000X more valuable. These companies aren’t just going to be unicorns, they have the potential to be trillion-dollar companies.”

“We are in an environment where exits are down overall, and the exits that do happen tend to be super-outliers. So investors may as well swing only for grand slams because it’s not like the hit rate of home run outcomes is significantly higher.”

David Kaye made smart comments on Superhuman’s acquisition by Grammarly. - David Kaye

Superhuman raised over $100m with its last round in Aug. 2021 at a $825m valuation. It has c.$35m in ARR and “ten of thousands” of users. The acquisition price was not disclosed but it should be way below Superhuman’s last valuation mark.

“Venture math is unforgiving. If you take big checks at big valuations, you're committing to building a business that can support those numbers.”

“Distribution beats everything. In a world where AI can replicate features quickly, your sustainable advantage comes from access to users, not cleverness of implementation.”

“The real story here is the user count disparity: Grammarly's tens of millions versus Superhuman's tens of thousands. Distribution trumps product.”

“What can't be easily duplicated is access to millions of users who trust your brand and use your product daily. Grammarly has that. Superhuman, for all its product excellence, remained a high margin but niche product.”

Mario Gabriele wrote a four-part deep-dive on Founders Fund. - Part 1, Part 2, Part 3, Part 4,

“Though LPs could not have known it at the time, in 2004, Clarium Ventures was the best-placed firm in Silicon Valley. That was thanks to two personal investments Thiel had made in the year leading up to the raise [Palantir and Facebook].”

“The firm became Palantir’s first outside investor, writing a $2 million check. It would grow to become a major financial and reputational winner for Thiel and his fund. In the years that followed, Founders Fund would invest $165 million into Palantir, making it the firm’s sixteenth-largest position by capital in. As of December 2024, the fund’s stake was valued at $3.05 billion, an 18.5x return.”

““Whenever you have these massive up-rounds led by smart investors, almost as a rule of thumb, they are undervalued. It’s because when these companies have momentum, people undervalue that momentum. When things change, they underestimate how much things have changed.” A willingness to concentrate on the fund’s winners would become a Thiel hallmark.”

“That “different way” was simple but provocative: Unlike the investors they’d worked with, Founders Fund would never move to oust an entrepreneur from their own company.”

“You found edge by visiting places other investors wouldn’t or couldn’t. Rather than search for Founders Fund’s next outlier among a crop of slick, nimble fast followers, Thiel would focus on hard tech, on the companies building in the world of atoms instead of bits.”

“Over the following 17 years, Founders Fund would invest a total of $671 million into SpaceX, making it its second most concentrated position behind Anduril. Returns data estimates that position to be worth $18.2 billion, a 27.1x multiple.”

“In 2010, Clarium alums James Fitzgerald and Andrew McCormack founded Valar Ventures with Thiel. It began with a simple, complementary premise: while Founders Fund focused on backing Silicon Valley’s elite entrepreneurs, Valar would search for outliers beyond California. Valar accumulated shares in accounting business Xero at just shy of $1.50 a share in 2010. By 2017, the $4 million invested was worth c.$54 million. As Thiel’s interest in New Zealand waned, and with opportunities abounding elsewhere, Valar’s focus shifted as the years passed. It progressively widened its aperture to include Europe and emerging markets. In 2013, it led a $6 million Series A in TransferWise (now Wise), which hit an $11 billion valuation at the time of its direct listing. Valar would also snag positions in neobanks Nubank and N26. In recent years, it has evolved once again. Because of Thiel’s PayPal credentials, Valar has always shown particular aptitude in fintech. Today it leans on this aspect of its identity, rather than narrowing in on particular geographies.”

“Thiel understands the importance of conserving talent. Once he decides someone meets his high bar, once he decides you are special, he is uncommonly proactive in ensuring that person remains in his orbit. If an investor wants to experience operational life, they should join Palantir or Anduril; if an operator wants to learn how investors think, they can take a stint at Clarium or Mithril or Founders Fund; if someone is ready to start a firm of their own, why not do it with his backing?”

“In 2010, Peter Thiel shared his view of the coming decade. The next decade is going to be about venture capital. Companies are going to be staying private longer, and more of that value is going to be captured on the private side.”

“One of Founders Fund’s greatest strengths over the years has been its ability to avoid these rebuilding periods by proactively refreshing its roster. Throughout its history, Thiel has been willing to move on brand-name investors, push out underperformers and weak cultural fits, and add talent to serve the firm’s current needs.”

““Brian [Singerman] is notorious for saying, ‘I’ve never opened a spreadsheet, because I don’t need to. This is a gut bet business.’ Honestly, it had been a lot of gut bets for us. We’d made the gut bet on Facebook, mostly based on Zuckerberg. We made the gut bet on SpaceX, largely based on Musk. We were an early-stage fund focused on early-stage bets. But we were beginning to scale.””

“Over the years, Founders Fund invested a total of $601 million in Stripe, making it the firm’s third-largest position by deployed capital. At a conservative valuation of $70 billion, Founders Fund’s stake is worth $3.9 billion, a 6.4x.”

“Spotify had recently raised financing valuing it at $270 million and was in no need of further capital, but Parker’s experience was too relevant to turn away. Founders Fund invested $16.5 million at a $330 million valuation, securing a 5% stake in the European firm. A total of $27 million invested yielded $239 million in distributions.”

Firstround wrote on how Shopify integrated AI into its business. - Firstround

“As it turns out, Shopify’s internal response had been years in the making. The memo certainly accelerated things, but the company had already been an early and eager AI adopter. Shopify’s VP & Head of Engineering Farhan Thawar brought GitHub Copilot into Shopify so early that he couldn’t even pay for the product yet.”

“Many companies grant org-wide access to the most basic AI tools, reserving the more powerful models and apps for only technical teams. Instead, Shopify allows anyone to use every tool and model. The thesis is that high-value use cases can come from anywhere in the company, and you have no idea which will emerge as the most impactful and most worthy of the good models.”

“Thawar can see the people getting value by using an internal leaderboard of who’s spending the most on additional Cursor tokens.”

“Shopify makes it easy for people to access, use and build with the latest tooling by putting everything in one place — the company’s internal LLM proxy, a tool that allows users to easily interact with a wide variety of models and switch between them through a single access point. In production, the proxy helps with scaling, tracking, and failover use cases as well.”

"Workflow: A site audit tool that changes how prospecting works. Shopify uses website performance benchmarking as an important tool in the sales process. When they claim industry-leading site speed to prospective merchants, they’ve got to analyze the prospect’s site and show how Shopify performs better. Previously, a human had to compile this data via site audits, which is time and labor intensive. Recently, a non-technical sales rep used Cursor to build a tool that generates detailed performance comparisons automatically. It pulls data from the prospect’s website, compares that against Shopify’s benchmarks and even provides talking points to assist in the sales process by tapping into internal documentation.”

“A sales engineer brought the MCPs of his most frequently used tools — GSuite Drive, Slack, Salesforce, and more — into a Cursor-built dashboard that prioritizes his tasks using real-time context from all these tools.”

“The Revenue Tooling team created an agent that answers multiple RFP questions at once. […] The agent gives solution engineers a way to generate fast, context-rich responses without manual toil.”

“Shopify is hiring more interns because they’re the ones who are using AI in the most interesting ways and have a beginner’s mindset by nature.”

Calvin French-Owen wrote about his experience working at OpenAI. Calvin cofounded Segment as a CTO before spending almost a year at OpenAI.- Calvin-French Owen

“The first thing to know about OpenAI is how quickly it's grown. When I joined, the company was a little over 1,000 people. One year later, it is over 3,000 and I was in the top 30% by tenure. Nearly everyone in leadership is doing a drastically different job than they were ~2-3 years ago.”

“An unusual part of OpenAI is that everything, and I mean everything, runs on Slack. There is no email. I maybe received ~10 emails in my entire time there. If you aren't organized, you will find this incredibly distracting. If you curate your channels and notifications, you can make it pretty workable.”

“OpenAI changes direction on a dime. This was a thing we valued a lot at Segment–it's much better to do the right thing as you get new information, vs decide to stay the course just because you had a plan. It's remarkable that a company as large as OpenAI still maintains this ethos–Google clearly doesn't. The company makes decisions quickly, and when deciding to pursue a direction, goes all in.”

“The thing that I appreciate most is that the company is that it "walks the walk" in terms of distributing the benefits of AI. Cutting edge models aren't reserved for some enterprise-grade tier with an annual agreement.”

“OpenAI is perhaps the most frighteningly ambitious org I've ever seen. You might think that having one of the top consumer apps on the planet might be enough, but there's a desire to compete across dozens of arenas: the API product, deep research, hardware, coding agents, image generation, and a handful of others which haven't been announced.”

“From start (the first lines of code written) to finish, the whole product was built in just 7 weeks. The Codex sprint was probably the hardest I've worked in nearly a decade. Most nights were up until 11 or midnight. Waking up to a newborn at 5:30 every morning. Heading to the office again at 7a. Working most weekends. We all pushed hard as a team, because every week counted. It reminded me of being back at YC.”

“If you're a founder and feeling like your startup really isn't going anywhere, you should either 1) deeply re-assess how you can take more shots on goal or 2) go join one of the big labs. Right now is an incredible time to build. But it's also an incredible time to peer into where the future is headed.”

Brian Singerman is raising a $500m new fund called GPx with $100m to invest in emerging GPs and $400m to double down in the breakout companies of these GPs. - Techcrunch

"GPx uses a two-pronged strategy. The firm will invest approximately 20% of the capital into funds managed by emerging VCs who are targeting pre-seed and seed-stage startups; the remaining capital will go toward partnering with emerging managers on leading later-stage investments (most likely at Series B) of their breakout companies.”

“As venture capital concentrates in the largest funds, some of those firms’ best investors are no longer interested in being a part of a big machine. They are leaving the behemoth firms to launch their own investing outfits where they can be more nimble and specialized.”

“Early-stage VCs often try to exercise pro-rata rights in later funding rounds (Series A, B, and beyond), but their fund sizes typically prevent them from maintaining their percentage ownership in top-performing companies.”

“With GPx’s capital behind them, emerging funds will have an opportunity to not only exercise their pro-rata rights but also lead a later-stage round.”

Elad Gil argues that certain AI categories (LLMs, code, legal, medical scribing, customer service, search) are now crystallising around a couple of key winners. - Elad Gil

“We have now entered an era where the first set of AI markets have solidified and a likely set of winners have emerged.”

“The next set of markets that seem highly interesting and tractable to generative AI include, but are not limited to the below: (i) accounting, (ii) compliance (e.g. healthcare), (iii) financial tools, (iv) sales tooling & agents, (v) cybersecurity.”

“For the “new” market segments above, one core question is what has been preventing market crystalization? Part of it for some markets is the models need to advance in reasoning or fidelity. Beyond models, other things that may prevent adoption of generative AI in a market may include: (i) getting the GTM wrong, (ii) too much incumbent lock in, (iii) buyers are slow to move & adopt new solutions, (iv) right team has not showed up, (v) it can take time to build a meaningful product (6-12 months).”

Top venture funds like Thrive and GC are investing in private equity style roll-ups acquiring traditional businesses and integrating AI to drastically improve their unit economics. - FT

“Among those deploying the approach is Thrive Capital, a backer of OpenAI and Stripe, which is involved in a new $72mn funding round for wealth management start-up Savvy Wealth. The investment values the New York-based group at $225mn, according to people with knowledge of the matter. The funding will go towards buying up smaller advisory firms and hiring individual advisers, as well as embedding artificial intelligence into the group’s operations.”

“Where private equity firms typically make heavy use of debt and slash costs in a roll-up, VCs claim improvements to efficiency and margins will come from infusing technology into the companies.”

“General Catalyst-backed Dwelly is taking a similar approach to the British property rental market, acquiring three lettings agencies across the UK, and currently manages more than 2,000 properties. It plans to automate the process of matching tenants and landlords, property management and rent collection.”

I listened to Coatue’s Thomas and Philippe Laffont discussing tech public and private markets during East Meets West. - Coatue 1, Coatue 2

“AI is probably the defining and biggest tech trend that we're going to see.” “One of the reasons these trends get bigger they're built on top of each other.”

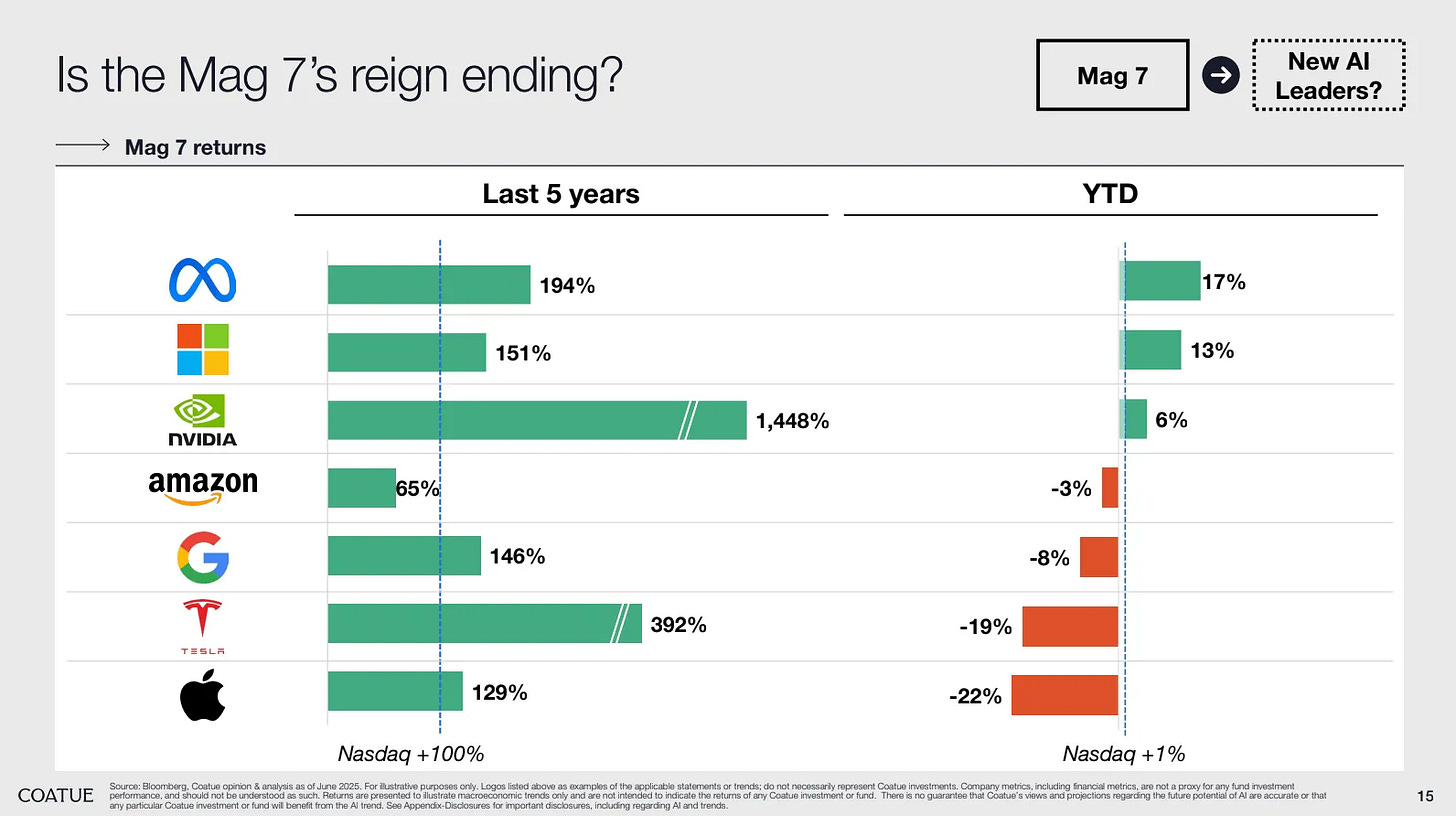

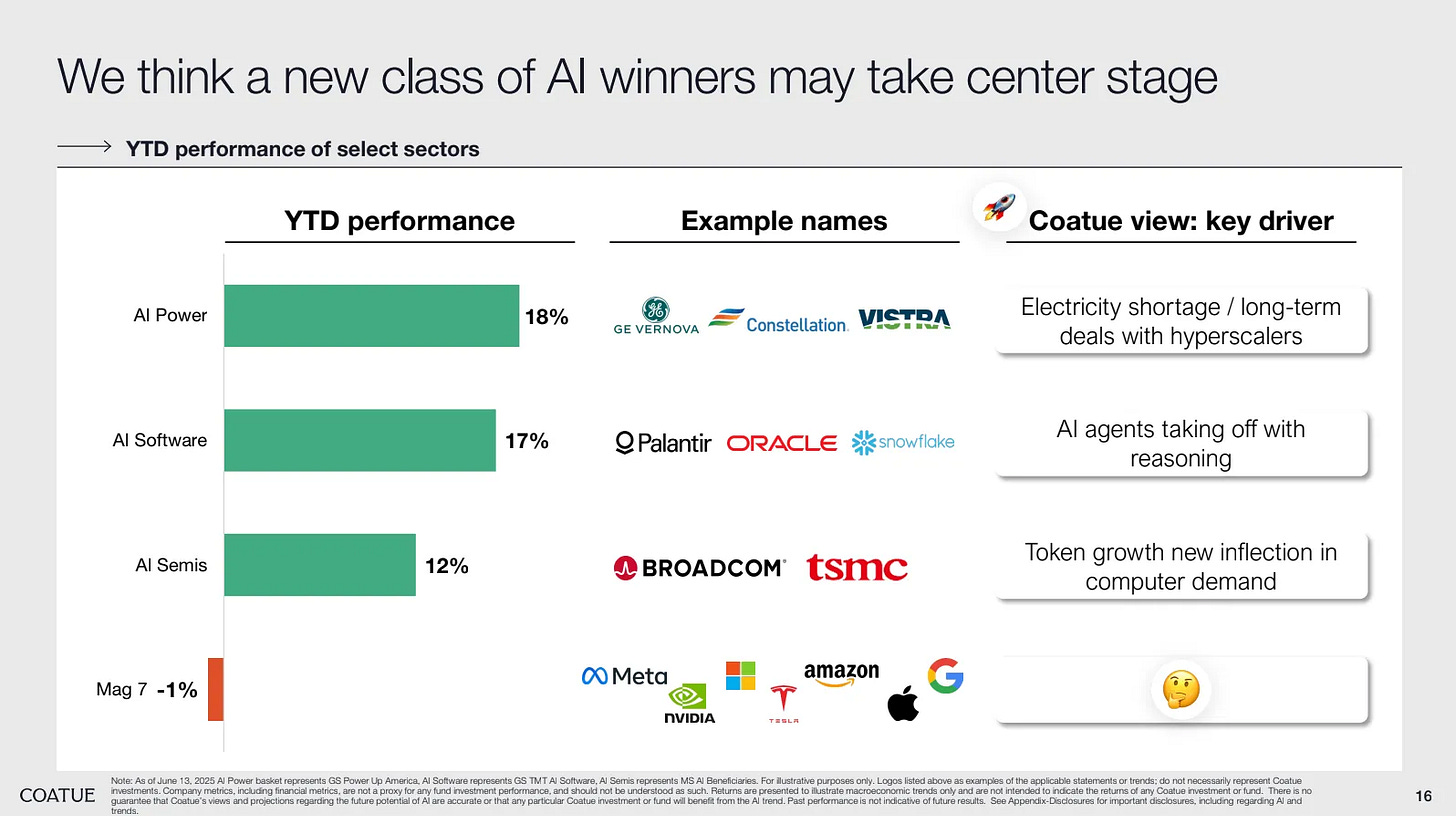

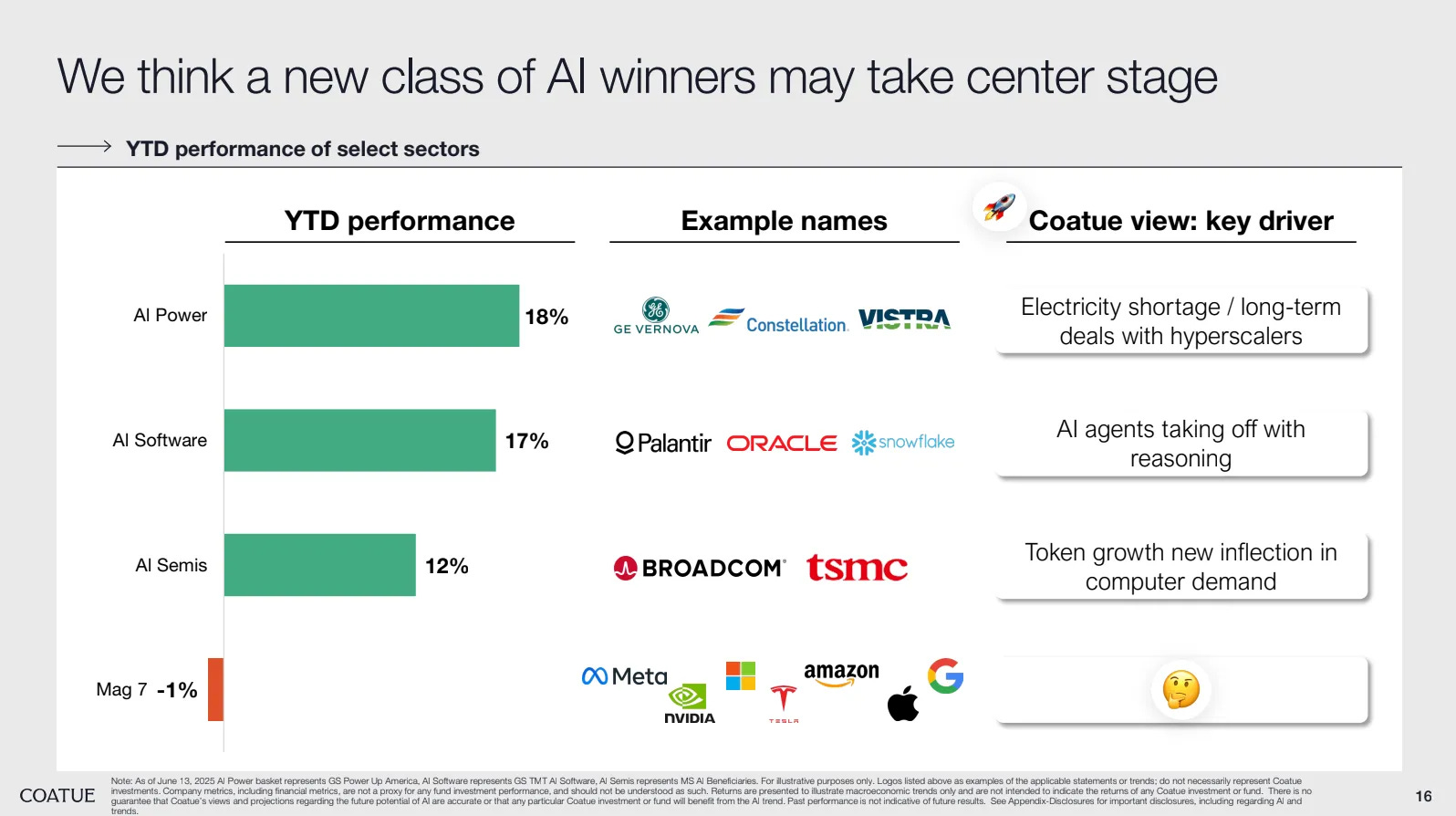

“The Mag 7 has actually underperformed this year but we have AI power, AI related software and AI semis are up on the year.” “On average, the Mag 7 was basically flat YoY. Yet, we saw tremendous value accretion to the top AI companies like OpenAI or Anthropic.”

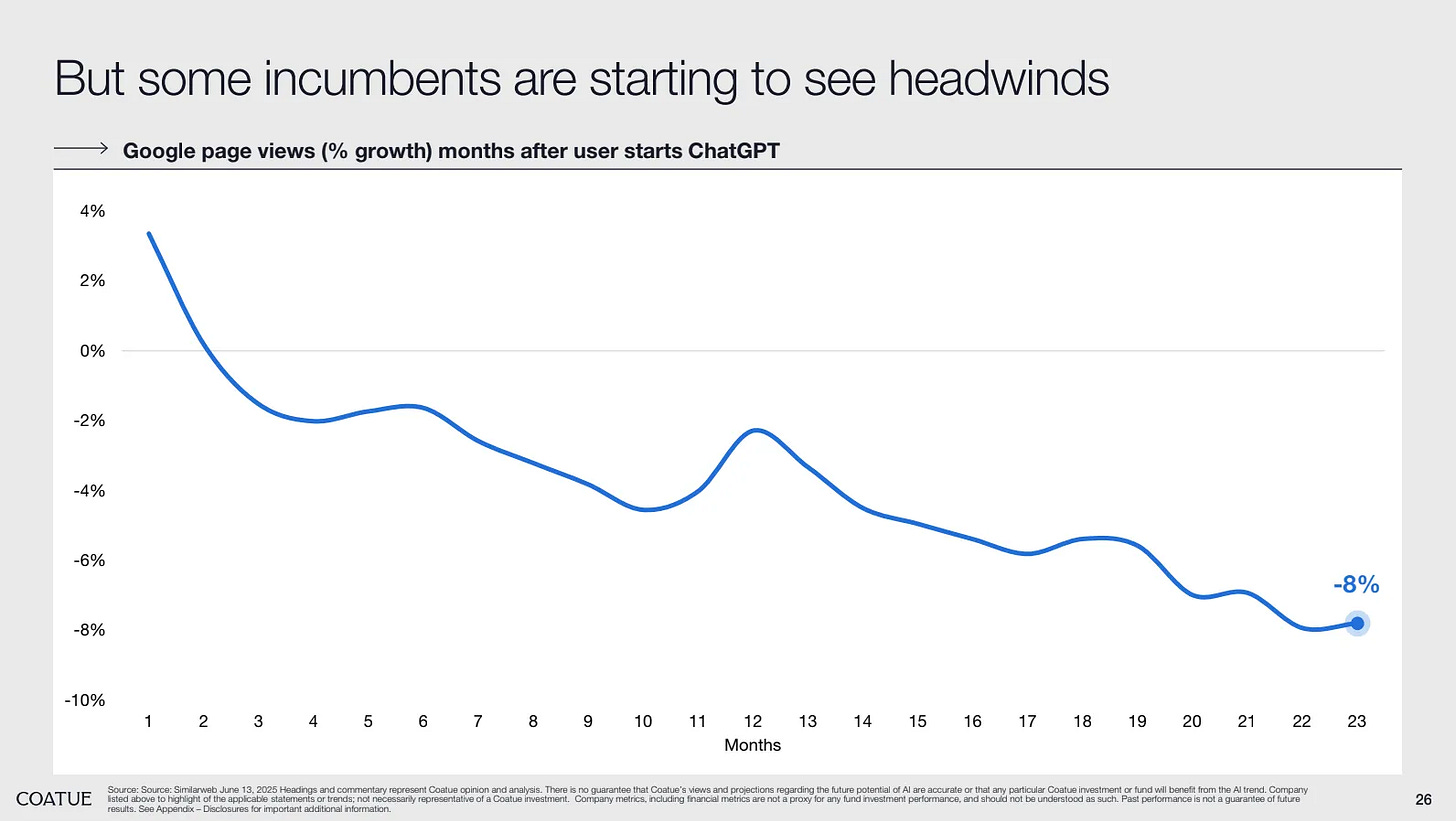

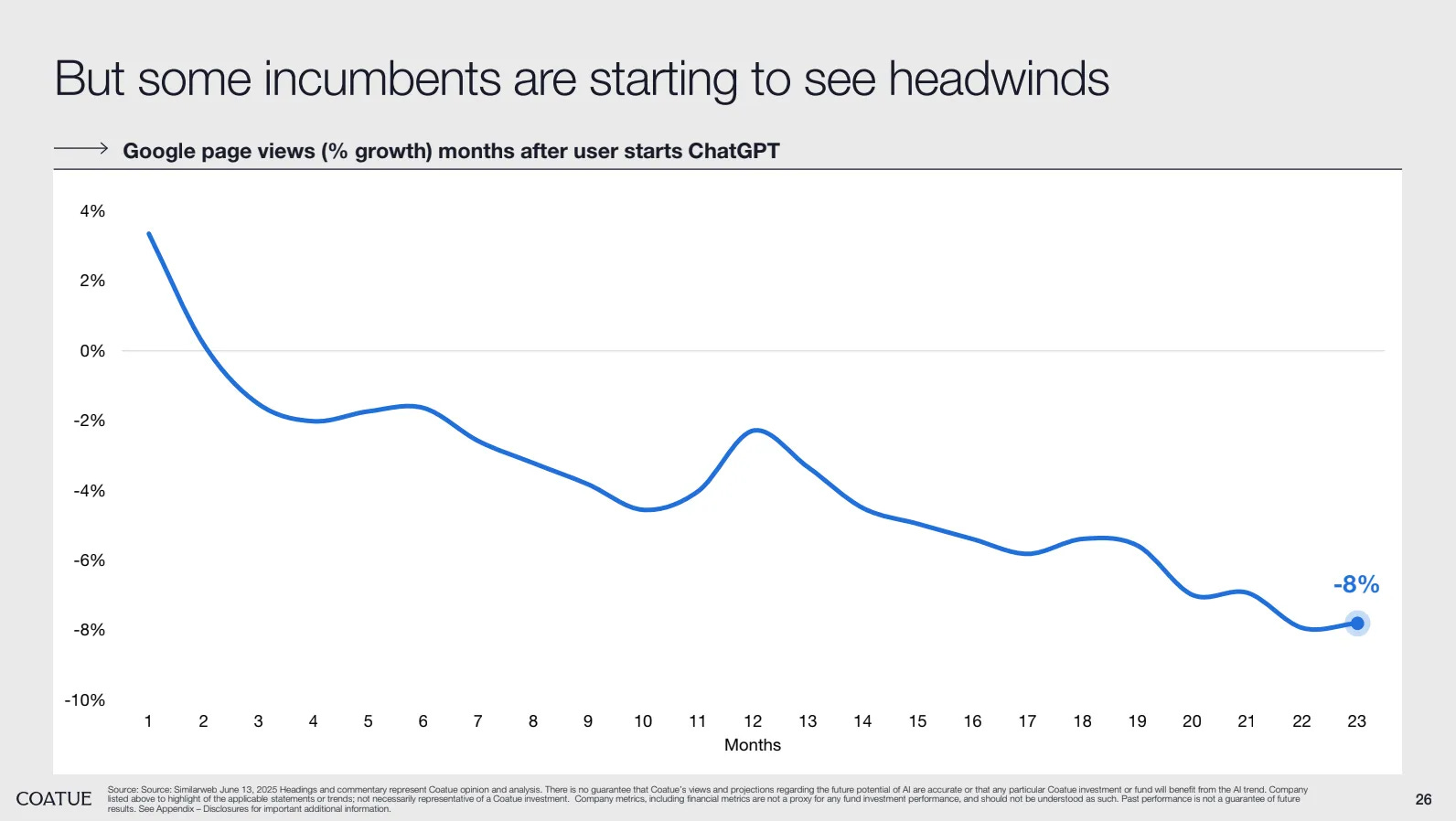

ChatGPT is starting to impact Google’s search business. Prior to ChatGPT, Google page views for particular user was growing 4% per year showing that we were consuming more Google overtime. But once a user starts paying for ChatGPT, his consumption of Google page views is decreasing going down 8% YoY after 23 months. “Major shifts just start one little step at a time and these one little steps end up becoming a gigantic move.”

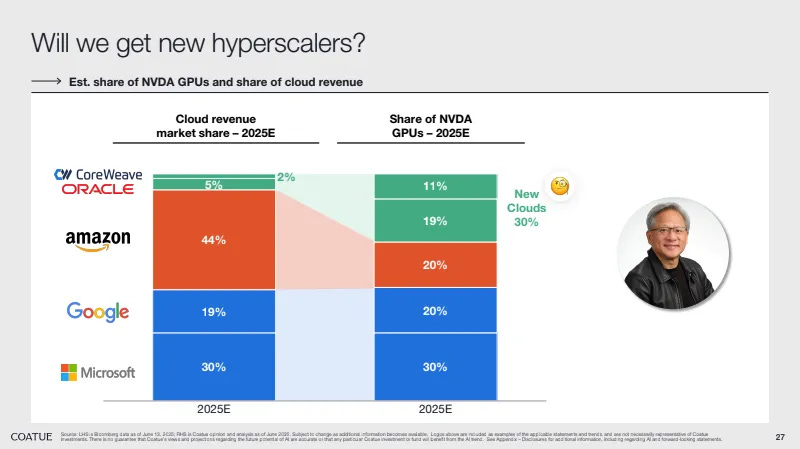

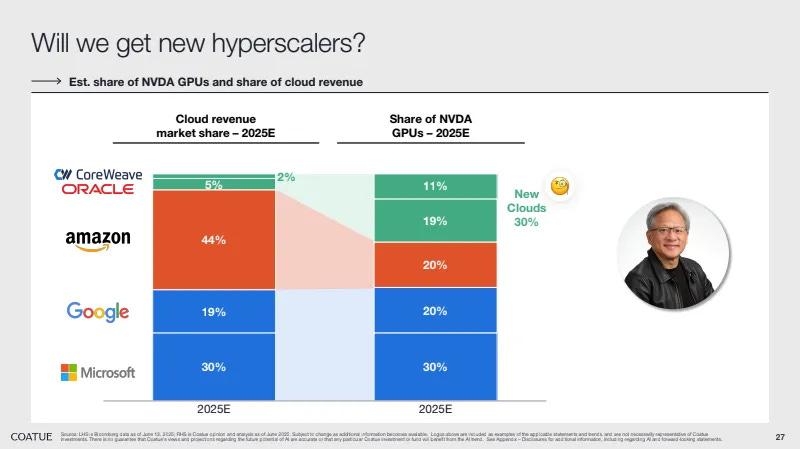

Coatue compared cloud revenue market share with the market share of Nvidia’s GPUs, highlighting the competitive dynamics as cloud providers ride the AI wave. Several key learnings emerged: (i) AWS is either potentially lagging in AI or pursuing a different hardware strategy than its competitors, (ii) Oracle is reinventing itself for the AI era, (iii) CoreWeave is entering the market as a pure-play AI cloud provider, (iv) Nvidia aims to diversify its customer base, fostering a shift from three dominant hyperscalers (Amazon, Google, and Microsoft) to a landscape with dozens of hyperscalers (including players like Anthropic and OpenAI) and (v) there’s a battle between those choosing to standardize on Nvidia and those opting for alternative hardware strategies.

We're starting to see a liquidity unlock in the private market both in terms of M&A and IPOs. In 2021-2022, the tech environment was broken with too much capital going in and not enough coming out. In the past 9 months, we have seen a rebound in IPOs, better IPOs that are performing well in the public market and large exits (ScaleAI’s acquisition by Facebook, Wiz’s acquisition by Google).

“A whole new market has emerged called ‘quasi public.’ These are companies valued at over $5-10bn that would have gone public 10 or 15 years ago because the private markets back then lacked the capital depth to support them.” “Retail investors should have access to these companies.”

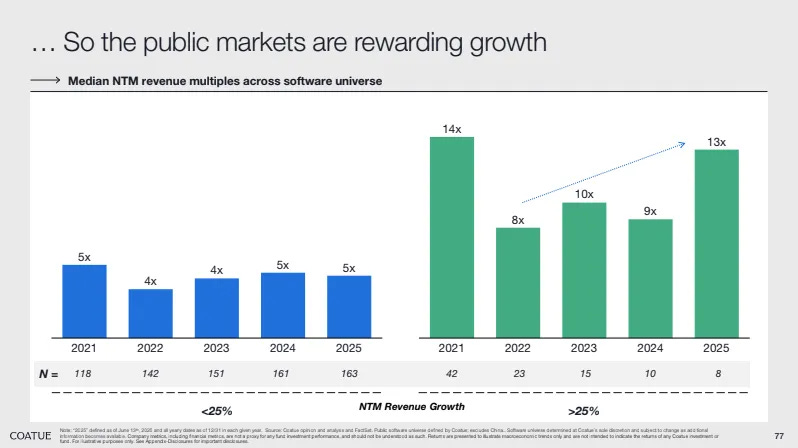

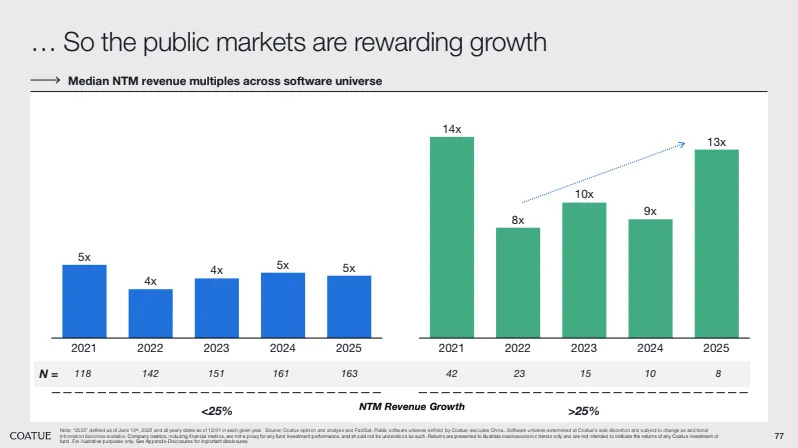

Growth has become more scarce in the public market and there is a big delta in revenue multiples re-rewarding growth.

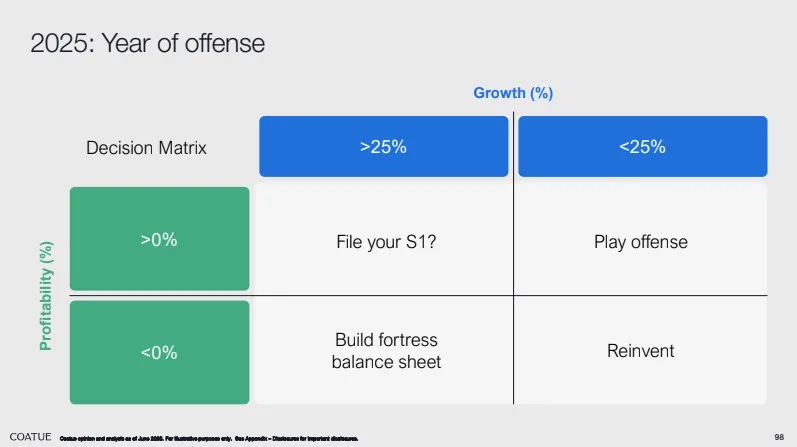

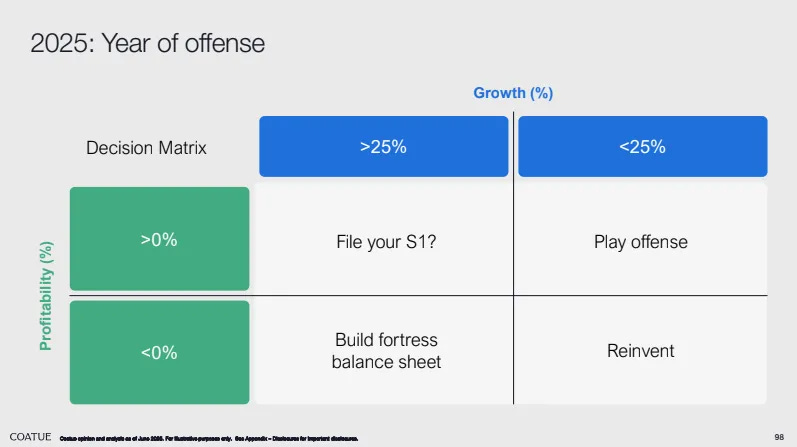

Companies growing in excess of 25% YoY, you should go public if they are profitable or you should strengthen your balance sheet if they are not. Companies that are growing less than 25% YoY but have become profitable should play offence to re-accelerate their growth incorporating AI in their business. If you’re not growing fast and you’re not profitable, you should completely reinvent yourself.

Boldstart raised $250m for its seventh fund to back technical founders selling to enterprise at inception. - Ed Sim, Boldstart

“This isn’t just venture. It’s a philosophy: (i) no pitch deck required, (ii) no metrics, just obsession and grit, (iii) just a bold technical founder and a future only they can see.”

“When you take our check, you’re getting one of the hardest-working partners in your corner. We will help you shape the narrative, land the first design partners, recruit early key hires, and accelerate your path to product market fit. That’s inception.”

“We are in the earliest stages of a platform shift that will surpass both cloud and mobile, and it is already beginning to reshape the enterprise. This next wave is not just about automation. It is AI-native, agent-powered, and autonomous by design. We are backing the core primitives of this shift: AI-native infrastructure, orchestration layers, secure identity, optimized compute, and semantic interfaces.”

“We don’t follow categories or market maps. We’ll help you create them.”

Mario Gabriele and Helsing’s cofounder Torsten Reil wrote about the European tech ecosystem. - The Generalist

“For too long, the continent’s most productive founders have chosen the latter path. They have failed to use their experience, network, and ability to take progressively bigger swings. Peruse a list of significant European exits and look up what the founders are currently doing, should you need more proof. You will find plenty running diversified venture vehicles or spinning up marginal products, and precious few attempting to build something truly ambitious.”

“It is perhaps even more concerning that founders who secure modest acquisitions seem content to quasi-retire. […] But by stepping away from entrepreneurship early, these founders deprive the world (and themselves) of what they might have built with the lessons learned from their first venture.”

“America does not seem to have this problem. Why? Because within the confines of Silicon Valley, it is socially damaging to take an early retirement.”

“Thanks to Facebook’s acquisition of Oculus, Palmer Luckey had a net worth of $700 million when he chose to co-found Anduril. Travis Kalanick could have retired after founding Uber, but chose to work on CloudKitchens. Jack Dorsey was well on his way to a mega-hit with Twitter when he launched Square. After co-founding both Twitch and Cruise, Kyle Vogt is building once again with The Bot Company.”

“Rather than pushing its most capable citizens to utilize their productive years effectively, the continent’s culture celebrates their complacency. Thanks to widespread expectations around work-life balance and norms that dampen rather than amplify ambition, many effective entrepreneurs receive much greater social capital once they’ve stopped building.”

“Europe is equal to these challenges, but only if it can rely on its best builders. We should not celebrate entrepreneurs who retire early—we should encourage them to go for it again rather than shelving their ambitions.”

Colossus published Ramtin Naimi’s portrait. He is 34 years old and cofounded a VC fund called Abstract - now managing $1.8bn. - Colossus

“At 13, he convinced his parents to lend him $2,000 to learn stock trading. When $2,000 proved insufficient for meaningful equity positions, he migrated to derivatives that could multiply his buying power.”

“Instead of college, Naimi launched a hedge fund straight out of high school. […] In total, he raised $3 million from 45 investors. He was the largest LP in his own fund, having poured his $500,000 of trading profits into it.”

“My personality is much more suited to being out hustling and meeting founders and learning about new technologies than sitting by myself for 15 hours a day.”

“He began reverse-engineering his path to seed investing. He meticulously researched power law outcomes—companies worth more than $5 billion—and made a counterintuitive discovery: multi-stage venture firms were better at seed investing than dedicated seed funds. “At the time, if you eliminated Uber and Roblox, whose seed rounds were led by First Round Capital, you couldn’t point to a single power law outcome within a venture timeline where the seed round was led by a seed-stage venture firm,” he explains.”

“Instead of competing with these giants, Naimi decided to align with them. He chose to become a seed investor that treated multi-stage firms as partners rather than competitors, accepting smaller ownership stakes in exchange for access to higher-quality deals.”

“He analyzed the backgrounds of founders backed by top-tier VCs, identifying patterns in education, work experience, and career trajectories. He built a LinkedIn scraper to track roughly 7,000 people who fit the profile. “Anytime one of them changed their job title to founder, I got a push notification.””

“The breakthrough came via AngelList. Naval Ravikant’s platform allowed anyone to raise SPVs for individual deals—no permission required, just quality deal flow. When Naimi posted his first opportunity, Ripple, he raised $470,000 within four hours. “I was like, holy shit, what was that? This is incredible. I can’t believe this actually works.” The economics made it even sweeter: He would earn 15% carry on every SPV he syndicated through the platform.”

““At first it was almost unbelievable. Every week, this random dude would send lists of 15 companies backed by tier-one firms. He wasn’t a founder, and hadn’t worked at a tech company; it came out of nowhere.” But the deal flow proved real, and Naimi quickly became one of the platform’s top investors.”

“For six months, Naimi represented roughly one third of AngelList’s total volume. Between August 2016 and June 2017, while technically employed by Core, he invested in 47 seed-stage companies either via an SPV raised on AngelList, or as an angel. Two of them—Solana and Ripple—went on to have coin market caps worth more than $100 billion each. A third, Rippling, is now valued around $17 billion. He also caught early rounds of future unicorns like Clay, Cherry, Material Security, and NewFront. His SPV investments have already returned just under $100 million to investors.”

“Marc Andreessen, Chris Dixon, David Sacks, Keith Rabois, Michael Ovitz, Kevin Hartz, Bill Ackman, Stanley Druckenmiller, and Kevin Warsh bought 20% of his management company, Abstract, for $10 million in upfront cash. Naimi was 26 years old with a theoretically worthless company that had maybe $10 million in total assets under management.”

“The strategy required reimagining traditional venture capital portfolio construction. Abstract’s model focused on “relative ownership” rather than absolute ownership: If he could get 5% ownership in deals where Andreessen Horowitz got 15%, he might have one-third their ownership, but out of a fund that was one-fifteenth the size, his LPs got 5x more exposure to those companies than they would as investors in Andreessen’s fund. Naimi executed this strategy perfectly 22 times in the early days: tier-one co-lead, 15% for them, 5% for Abstract. But the division of labor chafed. “I was doing all the work and only getting 5%,” he recalls. The solution was to start leading deals himself while still keeping the tier-one firms involved as co-leads at slightly reduced ownership levels—typically around 10%, which he discovered was the threshold below which top firms would walk away from seed deals.”

“Since that initial $100 million fund in 2018, Abstract has raised capital at an accelerating pace: $270 million in 2021, $300 million in 2023, and $500 million in 2025.”

“Half of Abstract’s funds rank in the top decile for their vintage; the other half in the top quartile. The portfolio includes seed and early-stage investments in breakout companies like Neon (bought for $1 billion), Replit, Krea, xAI, Partiful, Hebbia AI, Garner Health, Crusoe AI, and Polymarket.”

“Beneath the polished surface runs a culture of almost manic urgency. At 10:30am, Naimi opens his sugar-free Red Bull. The four-person investment team meets every morning at 11—not weekly like most firms—to review every deal in the pipeline. Everyone works from the office five days a week. Response times are measured in minutes, not hours.”

"The culture reflects Naimi’s belief that venture capital is ultimately a service business where execution excellence creates sustainable competitive advantages. When Abstract competes with larger, more established firms, speed is a differentiating factor—even when it seems there’s nothing to do.”

Yoni Rechtman at Slow Ventures wrote about the second and third order impacts of the AI revolution: abundance of digital outputs (code, image, video and text), personalisation everywhere, automating white collar work and direct oversight of blue collar work. - Yoni Rechtman

“Direct oversight of service/blue collar work. AI can’t do this work but it will/can make observability and realtime feedback newly possible. You can use AI to scale management in the field.”

“Middle market companies will struggle. Neither nimble enough to win on speed and execution nor big enough to win on scale and reach, they’ll be caught in the valley of death. Many will get aggressively consolidated into bigger platforms.”

“Retention will go down and competition will go up for software. Between tons of new entrants and competition from internal tools, retaining customers will be a constant challenge. Switching costs will be much lower because you’ll often just be swapping agents vs changing workflows/tools.”

“AI will kill outbound sales and it will be too inefficient to keep running the same growth playbooks. Lots of tools to make content, lots of slop, lots of competition, etc. Outbound sales will be the new banner ad; it’ll be part of a halo strategy, not a pillar to directly drive revenue.”

“Pure software businesses go from bad early bets to bad bets overall. You’ll need NFX, virality, real brands, proprietary distribution, and/or high touch services to differentiate software and build durable enterprise value.”

“Consultants and connectivity will be huge winners. More vendors to manage, switching out vendors more frequently, and evaluating more vendors for each purpose all as a result of competition, lower trust, and more open/available industry knowledge and best practices. The people paid to manage complexity (whether consultants, integration businesses like Merge and Mulesoft, or app stores) will be huge winners and will take on lots of new forms.”

Finn Murphy wrote a post criticising seed investors claiming that they’re playing the game on the field. - Finn Murphy

“If you are trying to be great, blowing with the wind feels like a sure fire route to the median.”

“What’s most important is not being good at the game - it’s figuring out what game you’re playing in the first place.”

“Once you figure out the game, the goal is figuring out your edge on that field - what can you do that puts you out ahead of everyone else?”

“For founders and to some extent, VCs, the current meta, ‘game on the field’ is Attention and how to convert it into Velocity. How do you grab it, maintain it and then harvest it.”

“The Attention game for companies plays across into investing. Increasingly the winners in every market segment are being crowned earlier and earlier - everyone wants to be in the winner so the sooner you can manifest that aura, the better. ”

“You have to observe the field - adjust to the new rules - but play it your own way.”

John Luttig at Founder Fund wrote about the AI talent wars. - John Luttig

“The talent mania could fizzle out as the winners and losers of the AI war emerge, but it represents a new normal for the foreseeable future. If the top 1% of companies drive the majority of VC returns, why shouldn’t the same apply to talent? Our natural egalitarian bias makes this unpalatable to accept, but the 10x engineer meme doesn’t go far enough – there are clearly people that are 1,000x the baseline impact.”

“Trust can no longer be assumed as an industry baseline. The social contracts between employees, startups, and investors must be rewritten.”

“From the Big Tech point of view, if AI is a $10T+ revenue opportunity, and your research team sized scales sublinear to revenue with a cap of a few hundred researchers, is the difference between spending $5M/year/researcher and $10M/year and $20M/year enough to stop you? $10B per year in researcher comp is less than a quarter of Meta’s annual capex. No matter the odds of ultimate product-market fit, the sunk cost is too large to turn back now.”

“For non-urgent hires, athlete scouting could translate nicely to AI labor to spot young talent before it runs up in pricing.”

“With trade secret leakage risk and money big enough to tear teams apart, vanilla at-will employment contracts don’t protect either side. The industry needs a SAFE equivalent for tech talent.”

“In the tradeoff between money and mission, the money has gone parabolic. Founders use both to magnetize top talent to their companies, but as the capital opportunity cost increases, only the strongest missions can justify the economic sacrifice that candidates make.”

“The labs feel the talent war most directly, but all startups now require extreme resource aggregation to make AI R&D bets. When the opportunity cost of top talent is higher (both founders and engineers), it becomes harder to coordinate top talent around an early-stage bet. SSI, Thinking Machines, and Physical Intelligence all required massive funding rounds for a shot on goal.”

“A startup industrial complex around the Seed → Series A → Series B progression emerged in the 2010s to support the growth of software companies. Some companies still follow this pattern successfully: Harvey, Abridge, Glean, and others. But I believe that going forward, an increasing share of startup successes will have a “fat pitch” founding story: incubations with stacked founding teams, high institutional credibility on day one, and uniquely powerful missions. Modern successes like SpaceX, Anduril, and OpenAI could not be built as lean startups. They are too long-horizon and capital intensive to work through the traditional apparatus.”

“Investors must be more flexible than prior generations. The best companies won’t map to the predictable fundraise sequence of the past 20 years.”

Entropy

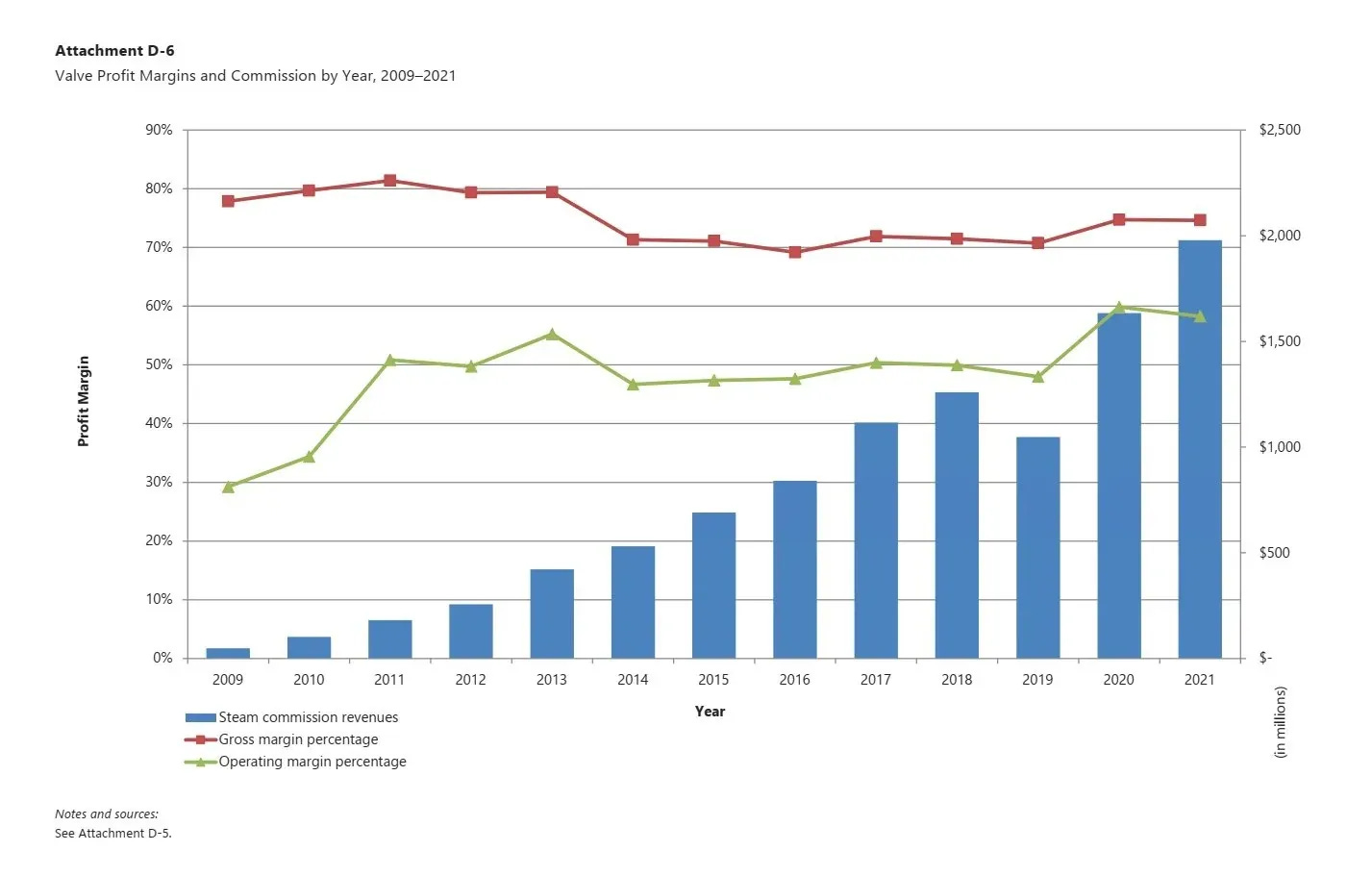

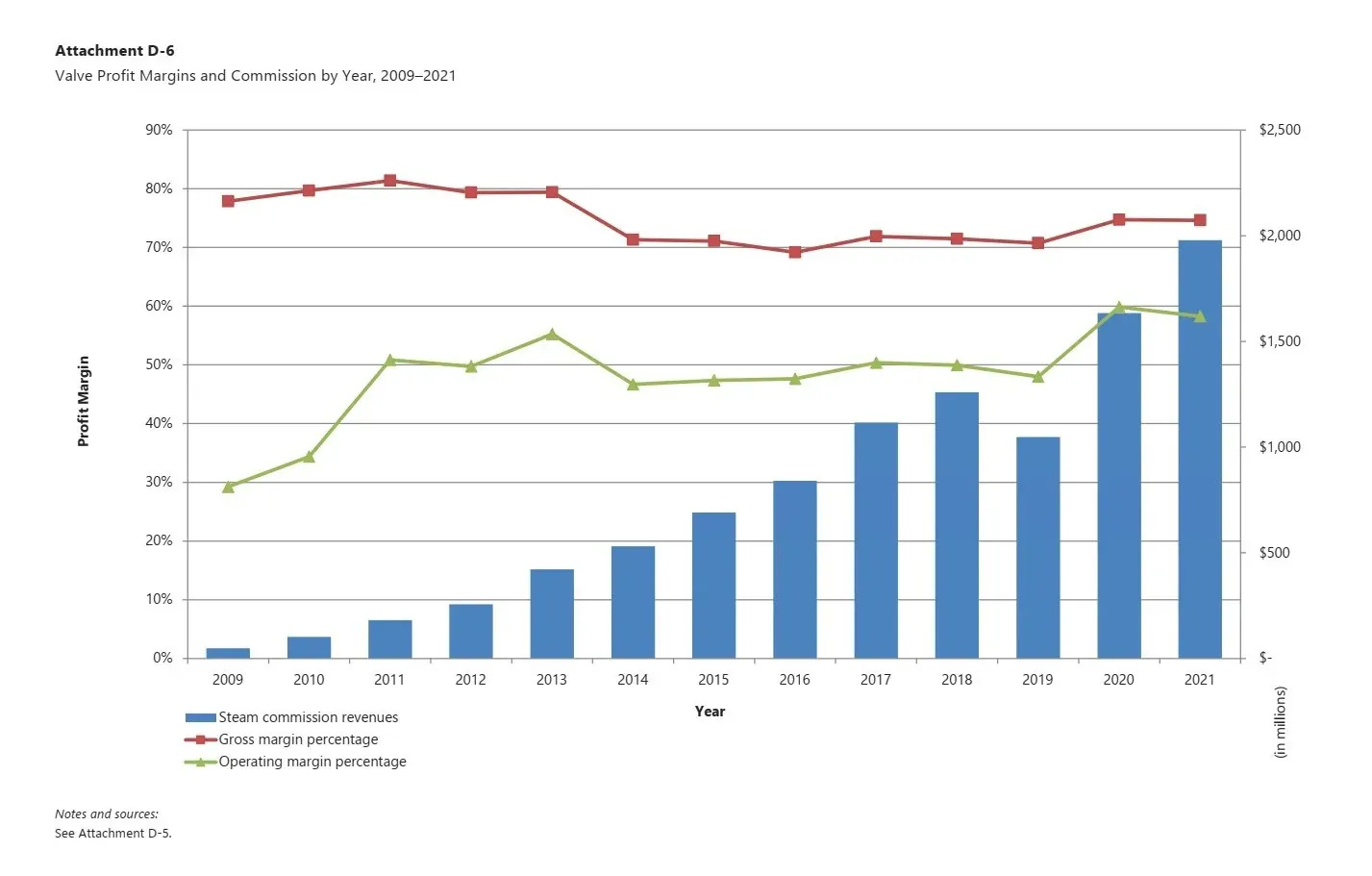

The FT published a deep dive on Valve, the gaming company behind Steam, the world’s largest online PC gaming store. - FT

“Valve games have been few in number, but their influence is huge: Half-Life and its sequels for their storytelling; Portal for its creativity and humour; the Counter-Strike series for its role in the emergence of esports; Left 4 Dead for its use of artificial intelligence to create dynamic co-operative gameplay. However, its most influential title is arguably Team Fortress 2, the game whose cosmetics system brought microtransactions — where players pay small amounts to unlock in-game content — into the mainstream. In doing so, it created a business model that has, for better and for worse, powered the mobile games revolution of the past two decades.”

“Valve has even managed to find some success in the notoriously tricky hardware market. Its handheld console — which looks roughly like a military-grade Nintendo Switch — has sold “multiple millions”, the company claimed in late 2023, with market research firm IDC estimating it hit 6mn sales by early this year.”

“But its financial engine, powering almost all its other achievements, is Steam. […] But its financial engine, powering almost all its other achievements, is Steam.”

“It also introduced a social overlay that allowed players to communicate more easily while playing different games.”

“Steam has established a dominant position in the PC games industry, with analysts assuming it accounts for perhaps 70 per cent of all sales of such games. The platform has more than 100,000 titles available for download, dwarfing its competitors, and levies a typical 30 per cent commission on sales of games and their (often extensive) add-ons.”

“Steam had 170mn global active monthly users in May, up from 153mn the year before.”

“Steam had an operating margin of about 60% and made $2bn of commission revenues, for about $1.3bn in profit just from Steam commissions in 2021.”

Ferrari is trading and operating much more like a luxury brand than a traditional car manufacturer. It epitomises Italian luxury maintaining strict exclusivity and leveraging high margin personalisation. - The Economist

“Last year Stellantis sold 5.7m vehicles; Ferrari fewer than 14,000. Yet Ferrari’s market capitalisation, at €76bn ($90bn), dwarfs that of Stellantis, at €25bn. Among carmakers, only Tesla, Toyota and BYD are more valuable.”

“Ferrari, which has an order book that is full for two years, had an operating-profit margin of 28% last year, compared with low single digits for most big mass-market carmakers.”

“The maker of high-end sports cars has succeeded in boosting sales while adhering to the maxim of Enzo Ferrari, who founded the firm in 1947, that it should sell “one less car than the market demands”.”

“Ferrari also now offers far more opportunities for personalisation, from custom paint-jobs to added carbon fibre and lavish interiors. These can add 20% to the price of its cars, which Barclays, a bank, reckons will set back buyers an average of more than €500,000 next year.”

“Chinese consumers, who have lately tightened their purse strings, account for just 8% of Ferrari’s sales, compared with as much as two-fifths at Hermès. And Ferrari relies almost exclusively on the very rich, who are more insulated from downturns.”

Cloudflare introduced a pay per crawl beta products allowing AI crawlers to crawl websites in exchange of a payment for access. - Cloudflare, Decoder, Techcrunch

“[News organisations, publishers and large-scale social media platforms] would like to allow AI crawlers to access their content, but they’d like to get compensated.”

“Instead of a blanket block or uncompensated open access, we want to empower content owners to monetize their content at Internet scale.”

“Google increasingly answers questions directly on its own platform, keeping users from clicking through to external sites. Prince says that six months ago, Cloudflare observed that 75% of Google searches ended without a single click to another website. With the introduction of Google's "AI Overview" feature, he estimates that number could now be as high as 90%.”

“For AI companies, the numbers are even more lopsided. Six months ago, OpenAI crawled 250 pages for every visitor it sent to a source. Now the ratio is 1,500:1. Anthropic's ratio is even more extreme at 60,000:1.”

"Users trust AI-generated summaries and rarely check the original sources - a trend backed up by early research. For content creators, this means a steep drop in both reach and revenue.”

“For the last year, Cloudflare has launched tools for publishers to address the rampant rise of AI crawlers, including a one-click solution to block all AI bots, as well as a dashboard to view how AI crawlers are visiting their site.”

“Website owners in the experiment can choose to let AI crawlers, on an individual basis, scrape their site at a set rate — a micropayment for every single “crawl.””

“At scale, Cloudflare’s marketplace is a big idea that could offer publishers a potential business model for the AI era — and it also places Cloudflare at the center of it all.”

LSA wrote a great article on the French baking sector. - LSA

France's 28k bakeries generate €10.6bn annually, with 55% of revenue now coming from snacking rather than traditional bread sales.

Traditional players like Paul, Brioche Dorée, and La Mie Câline face intense competition from new market entrants and changing consumer habits.

All major chains are prioritizing attracting under-35 consumers who represent the future of out-of-home dining consumption.

Chains are redesigning stores with contemporary aesthetics, digital ordering terminals, and expanded coffee/snacking offerings to compete with coffee shops.

Traditional players are doing major investments in airports and train stations, with Brioche Dorée winning 13 new airport locations and industry-wide SNCF partnerships.

Chains expanding globally - Paul le Café in Europe, La Croissanterie in Africa, with international representing 53% of Paul's revenue.

They need to maintain affordability (€10 menu ceiling) while upgrading quality and experience to compete in saturated market.

The Economist wrote about Stanley’s water bottles. - The Economist

“For Gen Z, a water bottle is both a necessity and a fashion statement. Social media are awash with videos of tumblers. The hashtag #WaterTok has 2.5bn views on TikTok.”

“Youngsters connect their water bottles “to their outfit and to their lifestyle”. They festoon their cups with all kinds of accessories, including stickers and keychains. Some buy straps, snack trays and backpacks for their beakers.”

“An obsession with “self-care” helps to explain the flood of interest, as many believe that water is the secret to glowing skin and mental acuity. This has led to people drinking more, a trend dubbed “hydration inflation”.”

“The desire for Stanleys is so great that a secondary trade is thriving: limited-edition cups resell for as much as $800.”

The Economist wrote about consulting being disrupted by AI. - The Economist

“Between the start of 2015 and the end of 2024 Accenture […] generated a total return (including dividends) of around 370%, handily outdoing not just the S&P 500 index but also Goldman Sachs and Morgan Stanley, rival redoubts of advisory smugness.”

“Revenue and operating profit both rose a touch faster than expected year on year, to $17.7bn and $3bn, respectively.”

“Having made a fortune telling others how to adapt to newfangled tech, from the internet to cloud computing, it now faces the selfsame predicament in the age of generative artificial intelligence. As semi-autonomous gen-AI “agents” sweep the world, who needs consultants?”

“Clients will require as much help with gen AI as they did with earlier tech innovations, or more, and that Accenture is perfectly placed to provide it.”

“42% of companies abandoned most of their AI initiatives. A year ago the figure was just 17%.”

“AI is being integrated into their offerings so that it works straight out of the box—and keeps working as AI agents automatically update and upgrade IT systems in accordance with users’ commands. Newcomers like Palantir are embedding their own engineers with customers.”

“Already the pace of Accenture’s new gen-AI contracts is slowing, from $200m a quarter last year to $100m in the past three months—not exactly reassuring for what are the early days of a ballyhooed technological revolution.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋