📖 Venture Chronicles - July 2024

Overlooked #180

Hi, it’s Alexandre. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of July.

Monday, Jul. 1st: Mary Meeker at Bond Capital published a presentation on AI’s impact on universities. - Bond

“The top five most highly valued global public companies are American technology companies – Microsoft, Apple, NVIDIA, Alphabet (Google), and Amazon. In spite of their already formidable size and influence, these companies are fighting like crazy for leadership in AI as their core businesses come under assault from one another...and from global competitors (including state actors)...and from entrepreneurs few have heard of (yet).”

“In the wake of ChatGPT and the AI explosion, we have likely reached a generational, fast and furious change across education. At their essence, AI and connected technology devices provide multimodal personalized output that can help users quickly get information and develop skills on their own terms. Tools that provide real-time feedback on engagement and skill development will continue to improve, enhancing the evolution of pattern recognition. AI will increasingly take over many rudimentary tasks, and the ways teachers teach, and their students learn will evolve.”

“AI can be an all-purpose education tool that many have imagined but have never had.” “It is what Alexander the Great had with his teacher, Aristotle. If Alexander was having trouble with a concept, I can imagine Aristotle slowing down for him...the goal was a “mastery of learning.”

“Five years ago, many would have said China was winning in AI. Since November 2022, however, the animal spirits of capitalism have been unleashed in abundant focus and investment. Many would now put America in the lead, thanks to entrepreneurship, capital, and most of all, rapid consumer and business adoption.”

“Universities have not traditionally thought of their students and alumni as customers – we believe that the evolution of learning, coupled with AI, may drive a shift towards the assessment of product offerings.”

“University costs are rising while the number of potential students declines. The average cost of four years of American university is $109K (public) / $223K (private). That compares with an average annual salary of $60K for students recently post-graduation. That starting imbalance means that the average borrower takes twenty years to repay student loan debt.”

“>75% of American K-12 teachers are optimistic about the potential for AI in their craft (although over 90% feel unsure of where to start, indicating that we’re still in early innings here).”

Tuesday, Jul. 2nd: I listened to a 20VC’s podcast episode with Danny Rimer who is a partner at Index. He invested into multiple successful companies including Figma, Discord, Dream Games, Etsy, Glossier and Patreon. - 20VC

At Index, every investor has a vote with a voting system that ranges from 1 to 4 and from 7 to 10, avoiding 5 and 6. An investment needs a certain threshold of positive votes (6.5 average) to pass through the partnership. The voting system is designed to ensure that the partner bringing a deal has enormous conviction in the company.

It’s extremely hard to have a deal pass if the partner bringing it only has a 7, unless it’s unanimous.

“The partner has so much conviction that they’re going to get us to be positive about it. The outlier is going to be welcome, but we’re going to look at the partner who’s bringing it to ensure that they really want to do this.”

Index was in a position to invest and passed on rounds in Spotify, Snap, Airbnb and LinkedIn.

Index has a thesis based approach in order to manufacture discipline within the team. “Creating investment theses are a way of making sure that we are building conviction and that we can support the conviction that we have.” “Everyone is encourage to have a major and a minor. Whether we're right or wrong is actually less important it's a way of sifting through opportunities and figuring out what we're looking for.” You start by doing a lot of work on your own to make sure that you’re actually committed and once it’s mature, you pitch it to the partnership to see if it’s a relevant thesis.

“If the person is extraordinary, throw all theses out the window and just back the back the founder - especially if they already have a really good instinct of the team that they're bringing on board.”

“As soon as we have signal superior to our peers that validates what we're betting on and that we can convince the team to take our money is as soon as we want to double down.”

Wednesday, Jul. 3rd: BlackRock acquired Preqin for £2.55bn in cash. Preqin is a private markets data provider known for tracking the financial performance of private equity funds and hedge funds. It covers 190k funds and 60k fund managers. Preqin is planning to reach $240m in ARR in 2024 growing 20% annually over the past 3 years meaning that BlackRock is paying a 13x EV/ARR multiple. BlackRock acquired Preqin in order to strengthen its private market tech capabilities integrating Preqin’s data into Aladdin which is BlackRock’s proprietary software helping investors to manage investment portfolios. - FT

Thursday, Jul. 4th: Revolut reached £1.8bn in sales in 2023 (95% YoY growth) from 38 customers (45% YoY growth) and reached £438m in profit before taxes. On the back of this announcement, Revolut is aiming to orchestrate a $500m secondary transaction at a £40bn valuation. - Revolut

In 2023, Revolut launched a range of new products, including eSIMs, Money Market Funds, RevPoints loyalty program, Robo-advisor, Ultra premium plan, joint accounts, group chat, and personal loans in several countries.

The customer base grew from 26.2m in 2022 to 38m by the end of 2023, marking a 45% increase. Revolut expanded into new markets such as Brazil and New Zealand, enhancing its global presence. As of Jun. 2024, Revolut reached 45m customers.

“Our monthly active customer base expanded by nearly 47%, highlighting the strength of our product portfolio and quality of service.”

“Over 70% of customers who joined Revolut in 2023 did so organically, or were referred by someone they knew.”

“In July 2023, we launched Ultra, our new award-winning top tier plan in the UK and EEA, offering more than £4,000 worth of annual benefits and exceptional perks across travel, lifestyle, and investing. In 2024, we launched eSIMs, allowing customers to buy phone data packages through the Revolut app, signifying our push into non-banking services. The value that our customers derive from these offerings is reflected in the notable uptake in our paid subscription products, with a 41% growth in retail customers opting for a paid plan.” Revolut also expanded into Brazil and New Zeland.

“In 2023, we saw a 68% rise in customers using Revolut as their primary financial services provider.”

“Credit has been one of our key focus areas; we have applied our superior product experience and competitive pricing with a view to becoming the first-choice provider for our customers. In 2023, we launched Personal Loans in France, Germany, and Spain, as well as credit cards in Ireland and Spain, increasing the number of countries where we offer credit products to nine. We carefully scaled our credit portfolio to grow our credit book from £204m in 2022, to more than £500m in 2023.”

“Revolut Business is designed to automate finance operations for companies around the world, with multi-currency accounts, global payments, and smarter spending tools. The segment continued to grow rapidly in 2023, with monthly active businesses increasing 66% year on year. By end of 2023, Revolut Business was onboarding 20,000 SMEs (small and medium enterprises) each month.”

Friday, Jul. 5th: Minecraft is expanding its intellectual property beyond gaming in response to a slowdown in the sector's growth. With 100m MAUs, the game has seen its revenues from consumer products, such as clothing and toys, double over the past two years. A movie adaptation is set for release in April 2025, and a Netflix series is currently in production. Additionally, Minecraft is exploring partnerships in merchandising, education, and content streaming to further capitalize on its brand. - Bloomberg

Saturday, Jul. 6th: Christoph Janz wrote an opinionated post against people arguing that SaaS is dying. - Point Nine

“When people talk about the end of software, oftentimes it’s because of a too narrow definition of software.”

Historically, when people were referring about the end of software they were talking about two adjacent ideas:

“The first alleged cause of death is that running a SaaS company is now like managing a fast-food franchise: high competition, limited differentiation, and low margins. The argument is that software development has become so easy that there’s no differentiation or defensibility in the product or the technology.”

“An adjacent argument relates to the fact that in the last 15 years, the SaaS business model has moved from obscure to obvious. The idea is that SaaS metrics have become so well understood that SaaS companies are perfectly priced. As a result, there’s no opportunity for outsized returns for investors and investing in SaaS companies will resemble investing in a broad index of stocks.”

Today, when the point is made with AI, it assumes that “software development will become so cheap that every market will become hyper-competitive” or that “software development will become so easy that the market for software products will shrink, and companies will develop more custom software based on exactly what they need.” The more radical view is to say that “all of the value will accrue to a small number of foundational model providers and hyperscalers. The idea here is that AI is going to replace software as we know it.”

Sunday, Jul. 7th: Goldman Sachs published a paper discussing the gap between Capex spending in Gen. AI and current benefits from Gen. AI applications. - GS

“The promise of generative AI technology to transform companies, industries, and societies continues to be touted, leading tech giants, other companies, and utilities to spend an estimated ~$1tn on capex in coming years, including significant investments in data centers, chips, other AI infrastructure, and the power grid. But this spending has little to show for it so far beyond reports of efficiency gains among developers.”

“Only a 25% of AI-exposed tasks will be cost-effective to automate within the next 10 years, implying that AI will impact less than 5% of all tasks.”

“To earn an adequate return on the ~$1tn estimated cost of developing and running AI technology, it must be able to solve complex problems, which, he says, it isn’t built to do.”

“Current capex spend as a share of revenues doesn’t look markedly different from prior tech investment cycles.”

“My prior guess, even before looking at the data, was that the number of tasks that AI will impact in the short run would not be massive. Many tasks that humans currently perform, for example in the areas of transportation, manufacturing, mining, etc., are multifaceted and require real-world interaction, which AI won’t be able to materially improve anytime soon. So, the largest impacts of the technology in the coming years will most likely revolve around pure mental tasks, which are non-trivial in number and size but not huge, either.”

“ServiceNow—a digital workflow software company— has reported an 80% reduction in the average time it takes to resolve a customer service problem thanks to AI technology.”

Monday, Jul. 8th: I listened to an Invest Like the Best’s podcast interview with Modest Proposal who is an anonymous online but who is a public and private investor. - Invest Like the Best

“The idea of putting multiples on temporary surplus generated from surging demand meeting inelastic supply, that's a thing that you just have to accept is reality. But if you're thinking over some duration, it seems unlikely that surplus will persist in the way it first emerges.” For instance, during covid, “soaring demand for everything digital in 2020 when the real world shut down wasn't going to persist unless the real world was shut down permanently and that did not happen.” The same is currently happening in AI with chips.

To assess the ROI on Capex invested in AI, you should aggregate both new revenue generation (high single digit billions as of today mostly from hyper-scalers and foundational models) and cost savings (hard to quantify but several success stories like Klarna’s use of AI for customer success). You would end up with a number that does not justify the $200bn Capex spent but it’s not that surprising in the early stage of an infrastructure platform shift.

“On-prem to SaaS was a pretty disruptive architectural shift, and the question in software today is, are there AI native companies that are going to utilize a modern architecture where data is queryable, real time by these models?”

“The Nasdaq 100 has returned 5x MOIC on a pretty consistent basis for the last number of years. jokingly ask my friends in the venture world, how many fund families do you know of that have multiple 5x MOICs?”

“I think that the endowment model and the allocation of assets into privates has gone too far and this is not self-serving as a public equity investor. The reasons now for capital to go into private markets is much less about risk reward, gaining the efficient frontier and taking advantage of opportunities. It’s much more based on institutional smoothing, return smoothing and volatility avoidance. I think these pools of capital have gotten on to the backside of the curve where it's probably detrimental to the extent to which assets are being moved into illiquid environments.”

Tuesday, Jul. 9th: Deconstructor of Fun published an analysis on the launch Supercell’s newest game called Squad Busters. The game had a strong start but quickly faltered, becoming Supercell's weakest launch since Boom Beach, with poor retention and revenue. The failure is attributed to skipping a soft launch, overestimating brand power, and ineffective pre-registration strategies, leading to low-quality downloads. - Deconstructor of Fun

“While Squad Busters initially drove massive download quantity, it quickly sputtered out, and poor download quality translated to lackluster active users and revenue.”

“Gathering all Supercell IPs under one roof was supposed to be Squad Busters' strength, but the result is irreverent. Supercell may have brand recognition, but brand equity remains questionable.”

“Squad Busters launched too early. Forgoing a soft launch deprived Supercell of the ability to assess even Day 30 KPIs. This decision remains puzzling, as there was no pressure to launch Squad Busters.”

“Squad Busters is a disciplined reminder of the importance of soft launching and a reality check on the strength of platforms and mobile-first IPs.”

“The pre-registration effect front loaded downloads, and for the first five days of Squad Busters launch, these exceeded portfolio highs before receding to portfolio lows.”

“While there’s no shortage of ideas to improve the title, these mostly reflect a game that launched too soon and thus too feature short.”

“While Squad Busters' launch fell short of lofty expectations, consigning the game to failure would be premature. Supercell course corrected Brawl Stars into a monster hit years after its launch.”

Wednesday, Jul. 10th: I listened to a 20VC’s podcast episode with Ara Mahdessian who is cofounder and CEO at Service Titan which is a vertical SaaS for the trades. - 20VC

What are your biggest lessons in terms of moving up market successfully and what it takes?

First, you need a maniac on a mission to lead the charge on going upmarket.

Second, you have to realise that there are different customer needs that need to be discovered and quickly solve for. You have to have very high product velocity to quickly build the incremental needs to go upmarket.

Third, you need to set a specific go-to-market motion to go after this segment. You need to be really good at understanding the purchasing process and the ROI case (asking potential customers the number of technicians they have, their current close rate as well as their average ticket and showing them the impact that ServiceTitan can have on these metrics as well as the overall revenue and profitability generation of the business).

“We didn't choose to be the premium option in the market. We just wanted to make the buying decision of buying Service Titan such a no-brainer by bringing a super strong ROI to our customers. We earned the label of being a premium solution in the market by building so much ROI into the product that it makes a life-changing difference in a contracting business.”

ServiceTitan’s strong brand has a significant impact on customer acquisition costs and the efficiency of good or market motion both in surfacing pipeline (word of mouth and referrals) and in increasing close rates. It also has an impact on the willingness to pay. You can charge more and the willingness to buy pro products goes up.

When is the right time to launch your second? As soon as the product you are currently building has great product market fit, you should start working on your second product.

Thursday, Jul. 11th: Yoni Rechtman at Slow Ventures published an investment thesis on the necessity to buy out companies in a given industry to digitise this industry. - Slow

“For many founders building vertical-specific software, combining with a incumbent to compete is the best way to capture value from their innovation/product.”

“No more easy wins: the runway for vSaaS has shortened. Further progress will require new GTMs and capital structures.”

“Introducing Growth Buyouts (GBOs) in which software company buys an operating company to compete directly in the market on the basis of proprietary technology and systems. You modernise the company and transforms the economics through software You become the best buyer in the category because you can underwrite the biggest, most consistent improves post-acquisition.”

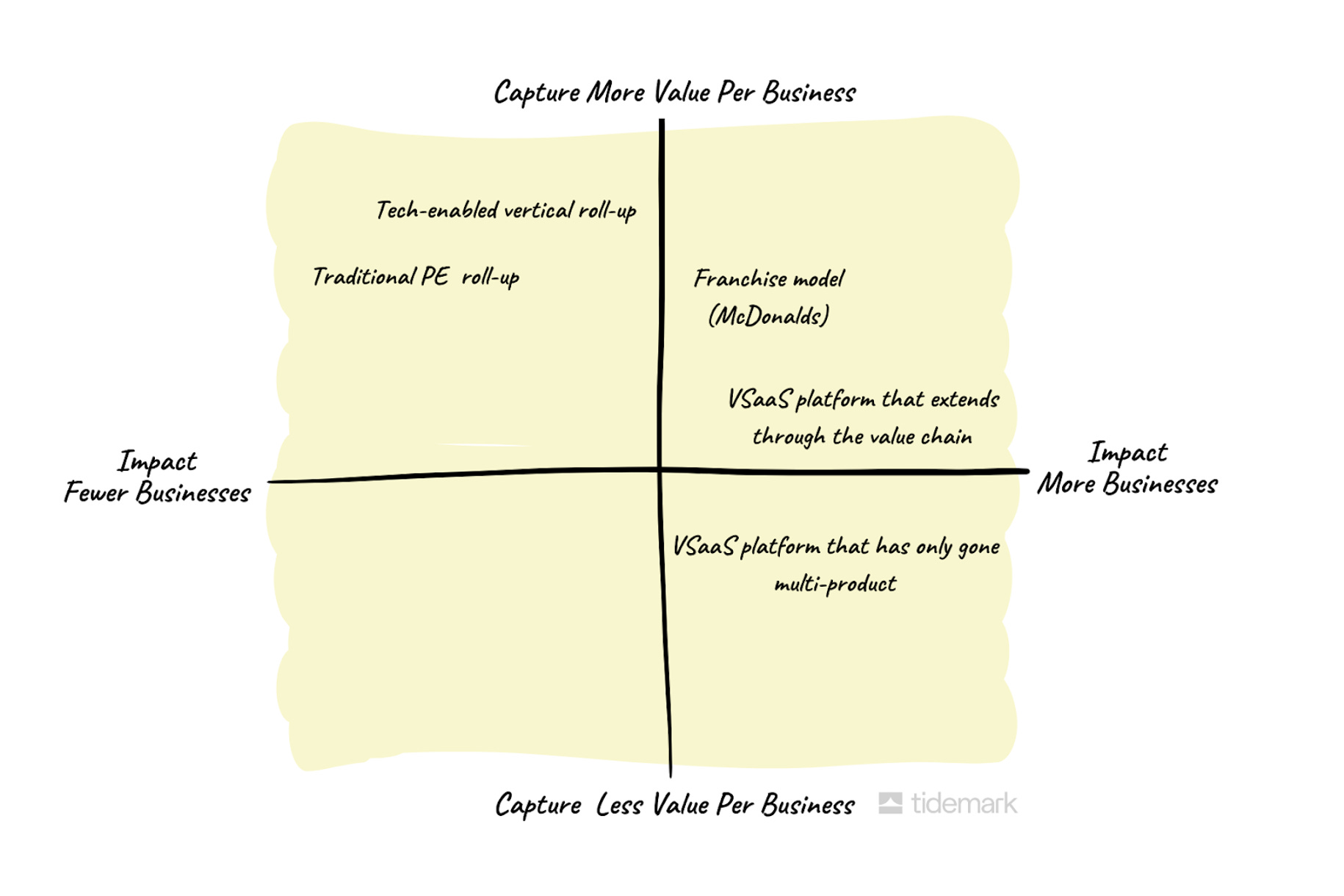

Friday, Jul. 12th: Tidemark published a paper on tech-enabled vertical roll-ups. - Tidemark

“In my opinion, these roll-ups mix conflicting strategies. Venture investing is about rapidly building enterprise value: build a product once and sell it many times at a 100% gross margin. Roll-ups are usually about financial engineering and cost-cutting.”

“A tech-enabled rollup is a tool (sometimes a very effective tool), not a strategy. The key leverage point is the technology, not in its own right (remember the WeWork principle), but as a tool to increase pro forma free cash flow. The other key leverage point is other people’s money—ideally debt—to scale and aggregate. This can work well if you buy fundamentally good companies (stable, high-margin, and recurring). It is better if they grow organically independently, or you can significantly grow them pro forma.”

“Another model slowly coming into vogue is the “tech-enabled vertical roll-up.” In contrast with the traditional Vertical SaaS Vendors capturing a fraction of the value they generate (but across a wide number of merchants), this strategy focuses on maximizing the value captured across just a handful of merchants. This is done by buying the merchants outright and then (often with the help of AI) implementing tech-powered improvements that create value. By virtue of owning the end business, all productivity gains from those improvements flow directly to the owner.”

“If you have, within a single entity, a software business that trades at a high multiple and a services business that trades at a low multiple, the public markets will usually just characterize the combined entity as a “high-margin services company.” These company’s multiples end up closer to their service peers versus their software peers. This is because the software component becomes captive to your services businesses (it can no longer be sold as a neutral platform to all merchants in the vertical). Thus, you sacrifice a high multiple business to enhance a low multiple services business. However, the new founders of these roll-ups are betting that: (i) AI opens up an opportunity to easily achieve huge efficiency improvements and operating leverage in any small business and (ii) pure software plays will only get more competitive and commoditized as AI increases in power, decreasing margins to the point where the profit pool flips to the merchant versus the software provider.”

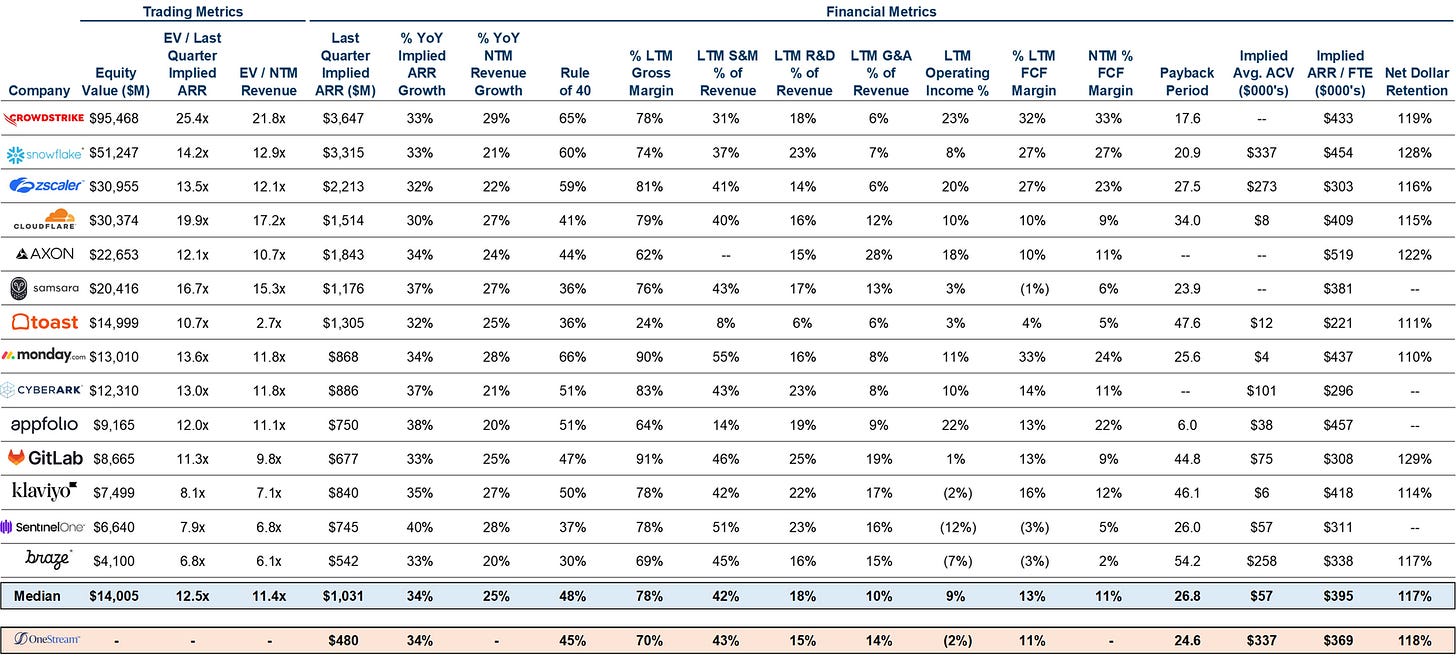

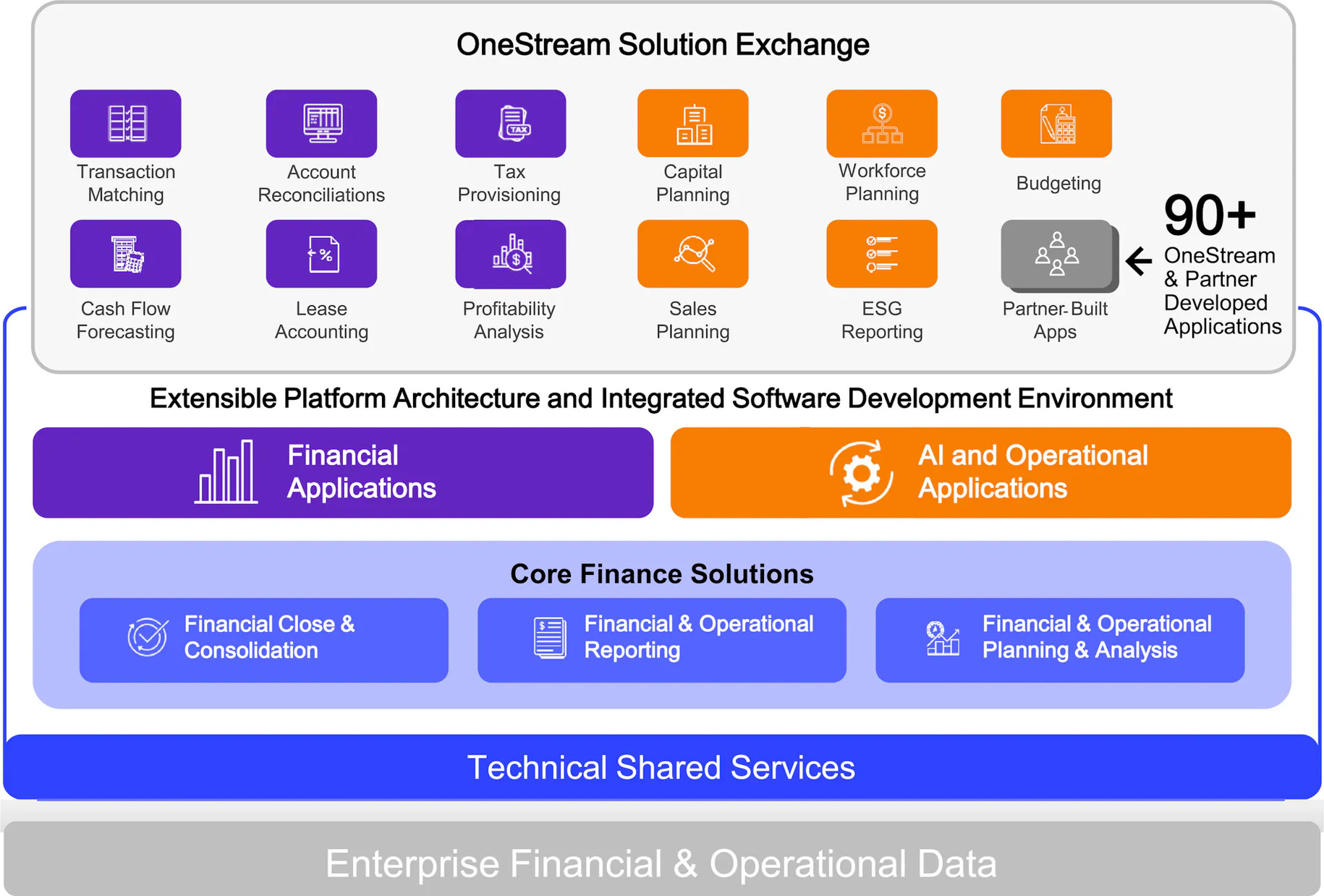

Saturday, Jul. 13th: OneStream filed to go public. It’s a cloud-based financial operations software generating $480m in ARR and growing 34% YoY from 1.4k customers. It started in 2012 and reached $100m in ARR in 2020. - Meritech, OneStream

“With the increase in the amount of data finance teams utilize across a business, there is a need for a single platform that reduces the complexity of financial operations and helps unify data (i.e. many integrations) across the corporate performance management processes, including planning, financial close, consolidation, reporting, compliance, and analytics.”

“OneStream focuses on mid-market and enterprise customers; their implied average ACV (annual contract value) was $337k as of last quarter, and they already have more than 75 of the Fortune 500 as customers. OneStream had a 118% net dollar retention rate and a 98% gross retention rate as of last quarter.”

“OneStream’s last reported round in 2021 was a $200m round at a $6bn valuation. The company is majority owned by KKR.” “In March of 2019, KKR invested $500m at a $1bn post-money to own 50% of the company.”

“OneStream’s initial subscriptions are typically 3 years but can range from 1 year to 10 years. The average sales cycle, from initial evaluation to payment, is 4-8 months but can vary significantly up to multiple years for some customers.” “Regarding sales efficiency, OneStream discloses their own sales efficiency and reports that the average number of months to recoup customer acquisition costs was 21.3 months in 2022 and slightly higher at 23.4 months in 2023.”

“Gross margins have increased slightly over the last 8 quarters from 64% to 69%. Software gross margins are in the high 70’s.”

“While OneStream operates in a market that has not yet moved to the cloud, OneStream also just recently transitioned to SaaS. To argue that OneStream is a bleeding-edge solution might be a harder sell.”

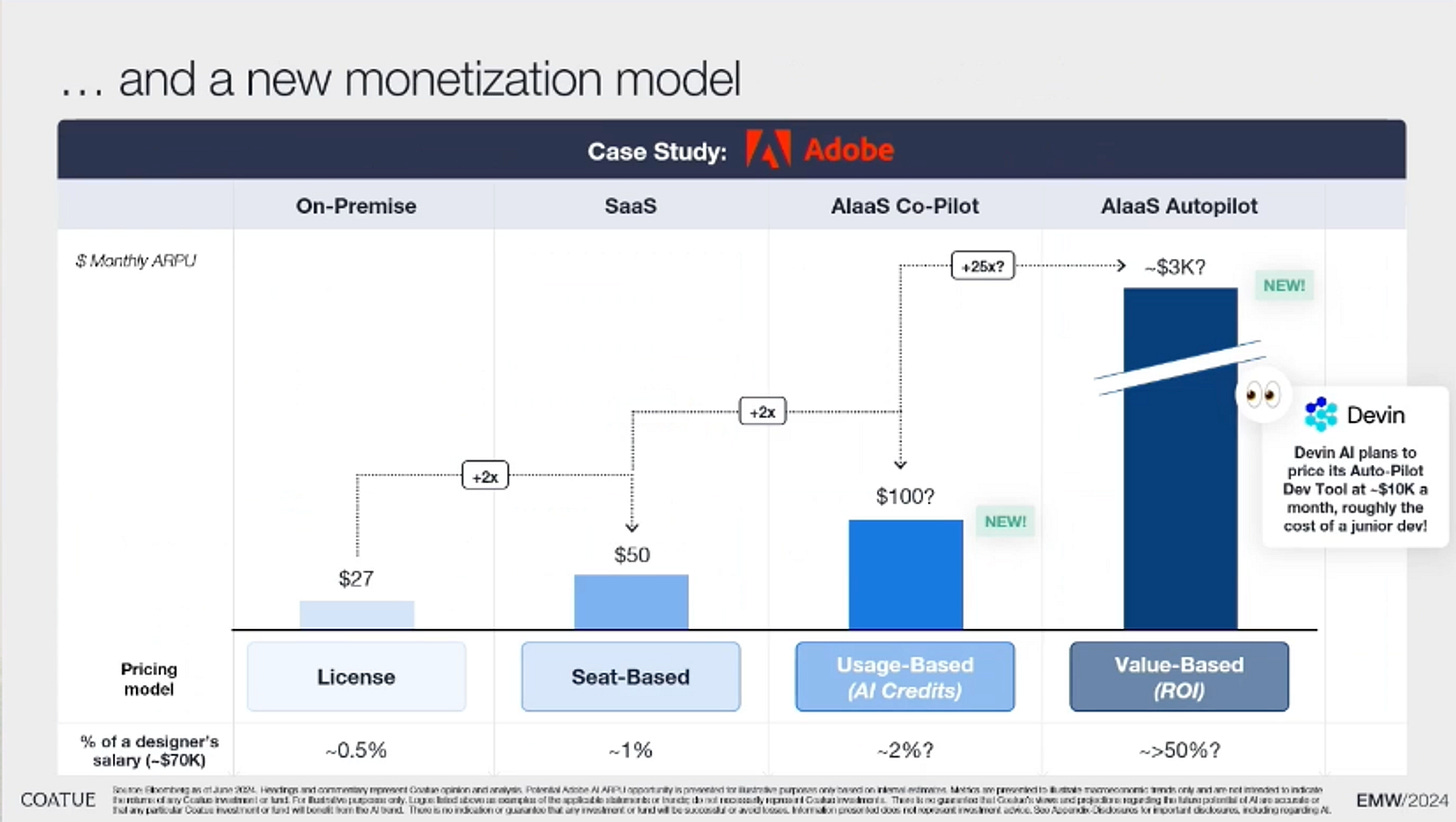

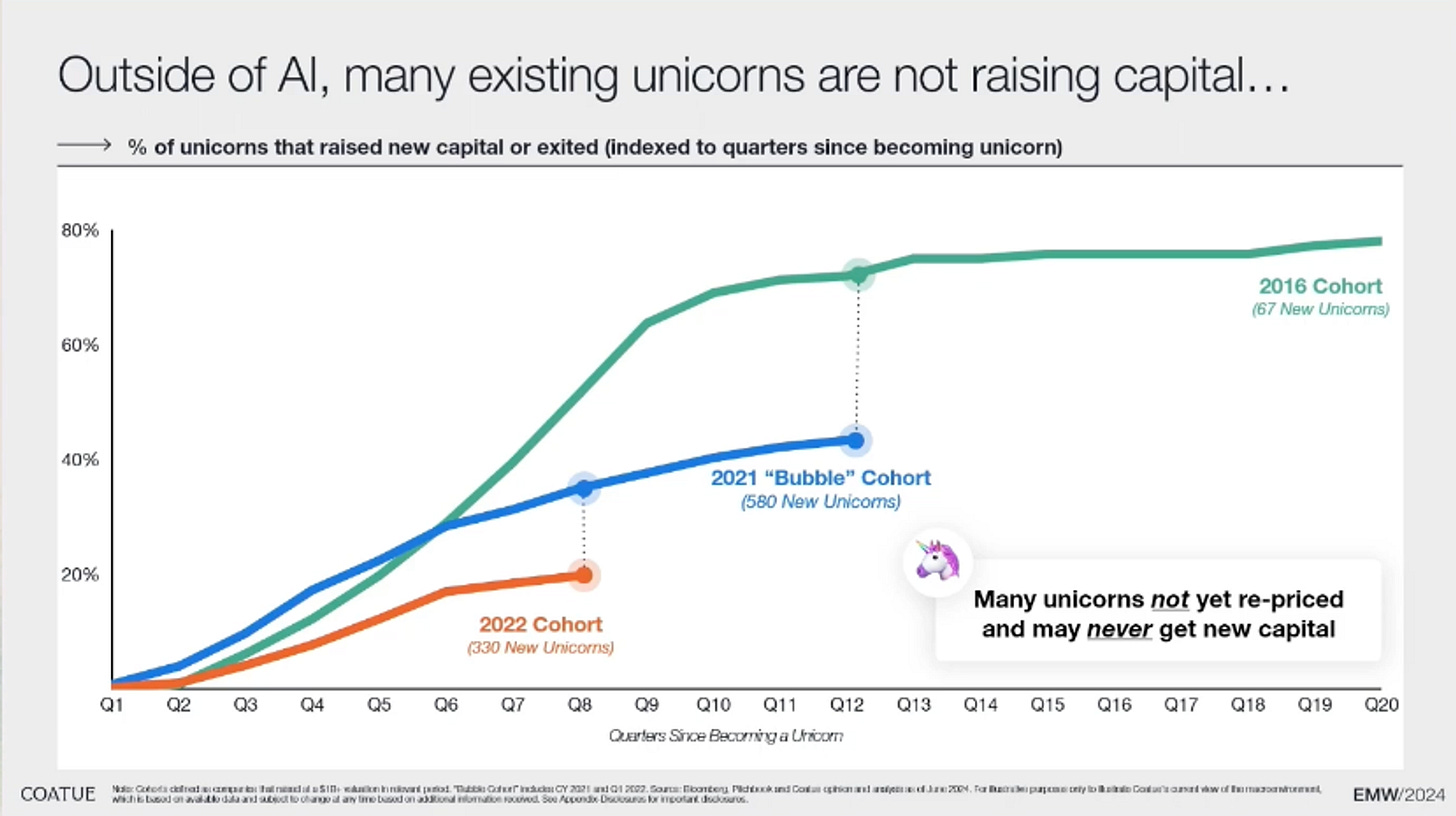

Sunday, Jul. 14th: I watched Coatue’s annual view on the state of the markets presented at East Meets West. - Coatue

There are several $1+ trillion companies which are concentrating a lot of the stock market value in the US ($50 trillion) and in the world ($110 trillion). These companies share several attributes: ecosystems with strong network effects, dominant market shares in their category and strong impact (1bn+ users for B2C companies and 80% of F500 companies as customers).

Despite Nvidia tripling in earnings, the P/E has not changed because earnings expectations have become massive.

“Everybody says buy low and sell high. I’ve done well for 25 years buying high and selling low. The reason is that when you buy high, you buy the winners and you let the market gives you some direction. You buy companies companies that are working and the market are giving you some feedback. Sometimes, when you sell low, you get rid from the losers.”

In 2024, AI has been responsible for 2/3 of the S&P returns with 1/3 of this coming from Nvidia alone.

We spent $10 trillion in 70 years in the CPU based infrastructure and we are going to spend $10-20 trillion in a GPU based computing architecture. We’re going to depreciate and wipe out the old infrastructure to build a new one.

“I worry about the power of these $3 trillion companies. I think it’s a perverse effect of regulation. The FTC and others want to protect small companies. They’re not allowing large companies to buy small companies. That makes the future of small companies much worse because now you only have less ways to win.”

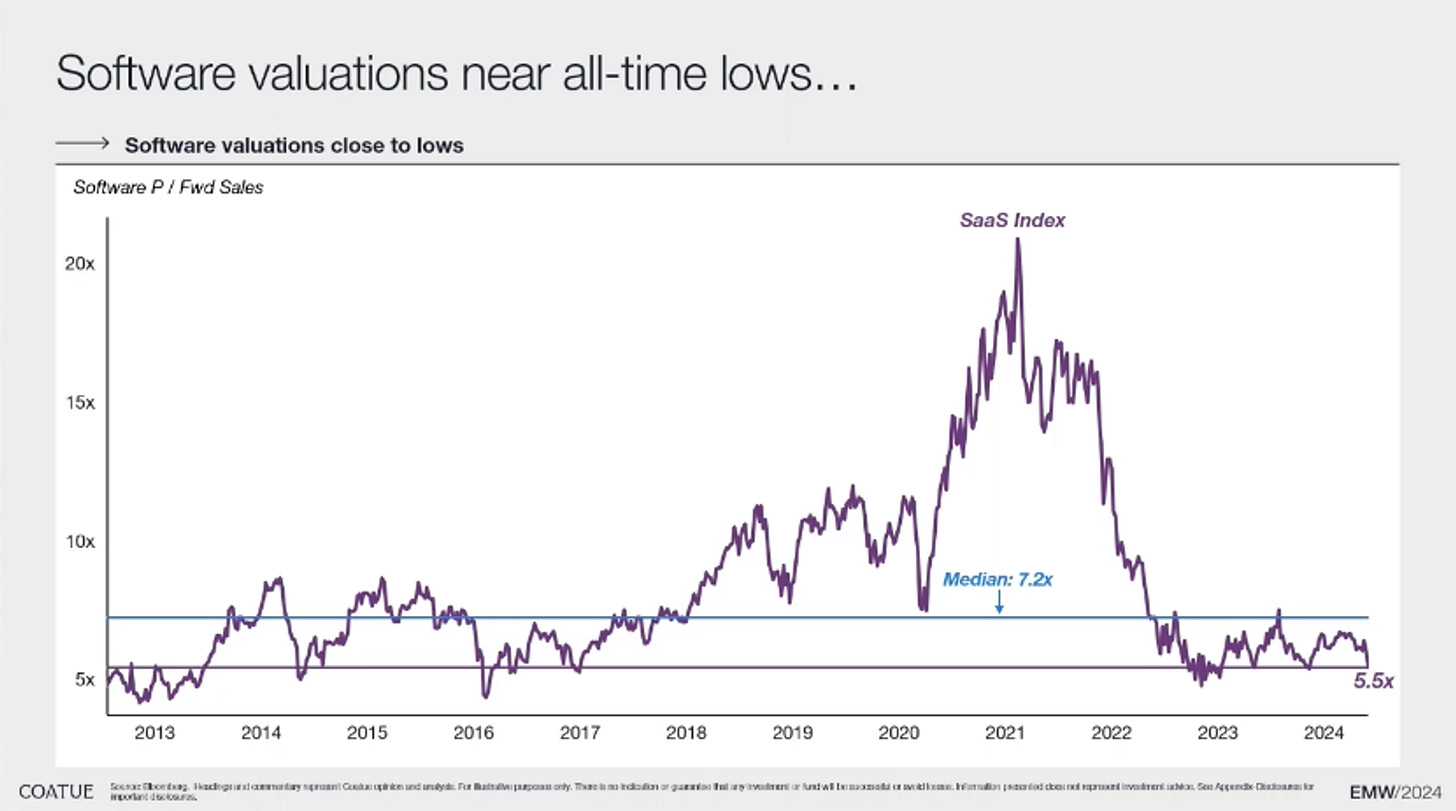

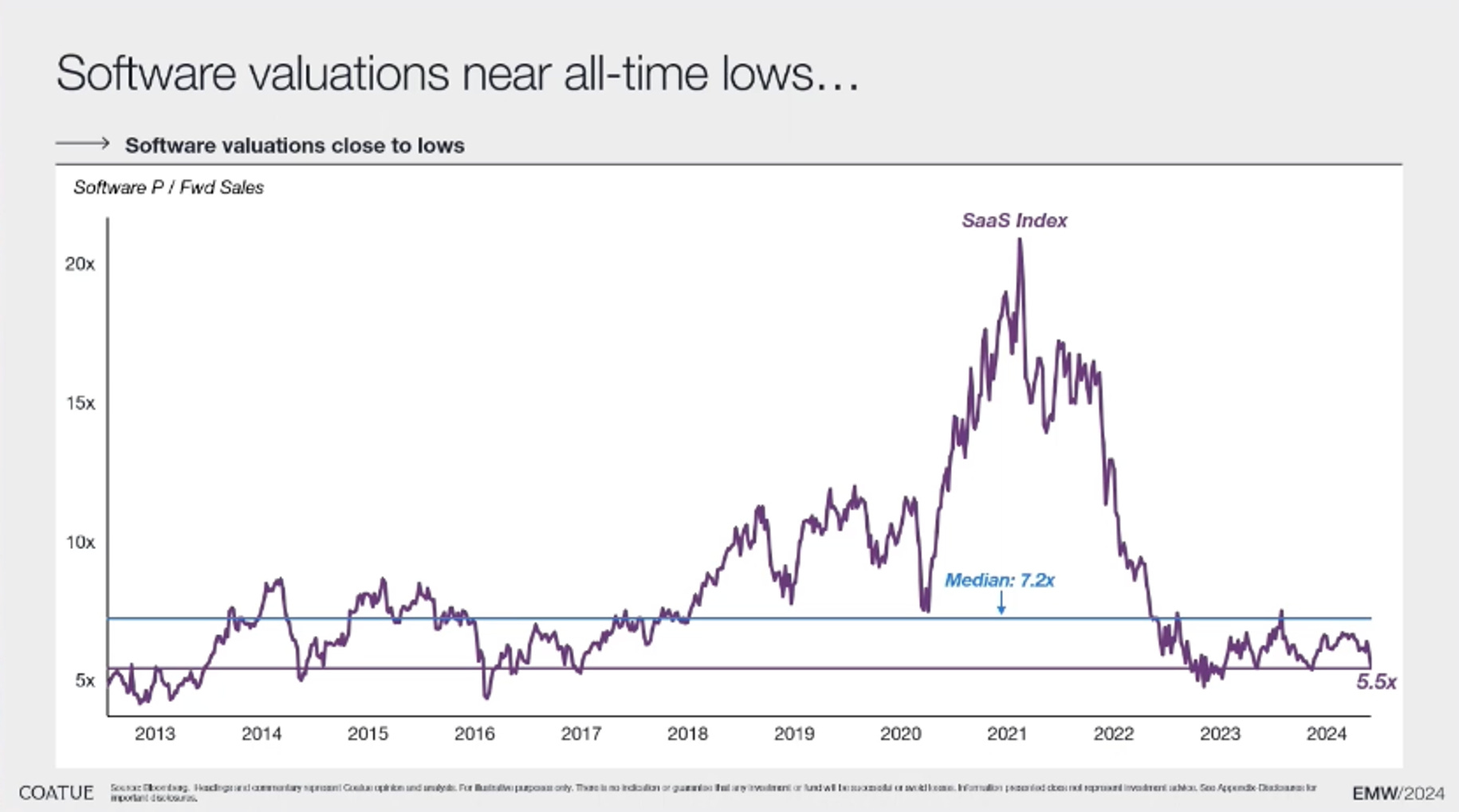

Software companies are trading at 5x EV/NTM on the public market partly because sales growth has massively slowed down. Software will come back but it’s naturally delayed because the market favoured infrastructure companies in the early days of the AI revolution.

The venture funding cycle is normalising post the ZIRP era in 2021. AI is a bubble within a burst in venture. AI accounts for 3% of total deals but 15% of total capital raised.

We’re creating more unicorns than exits. It can’t go on forever.

Why are there no more IPOs?

The public market is now mostly driven by passive index and ETF investing favouring larger companies while institutional active investors are on the decline.

Private valuations could still be higher than public markets. Private companies are afraid to review their last private valuation mark.

Public investors have a lot of alternatives with companies in the public market having scale, growth, profitability and attractive valuations.

Private equity is a new partner for the unicorn economy. Private equity is willing to pay rich revenue multiples and which is willing to buy a profitable growth story.

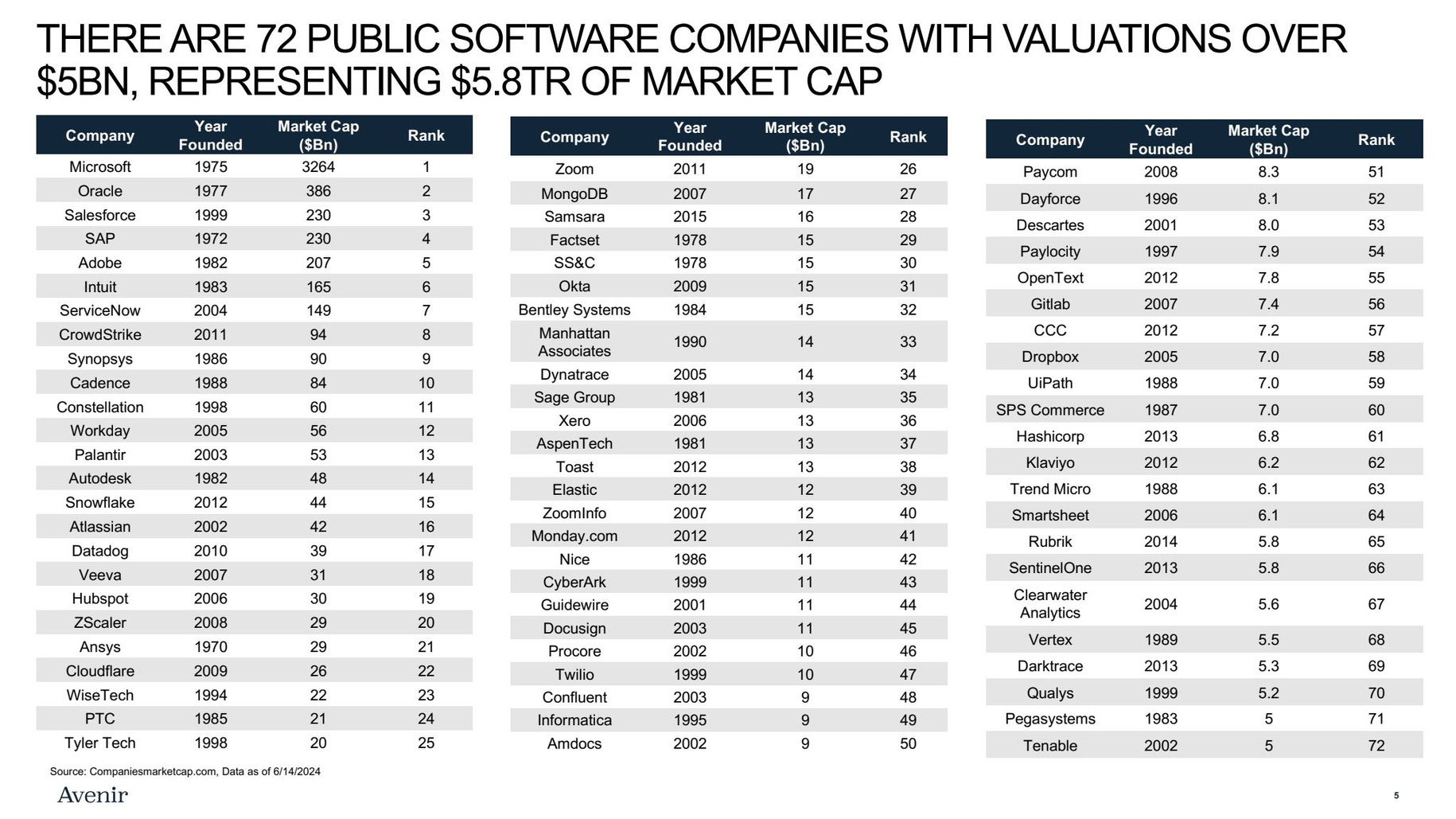

Monday, Jul. 15th: Avenir published a presentation on the state of software. - Avenir

Microsoft accounts for c.40% of global software market cap. There are only 6 other software companies trading above $100bn in market capitalisation: Oracle, Salesforce, SAP, Adobe, Intuit and ServiceNow.

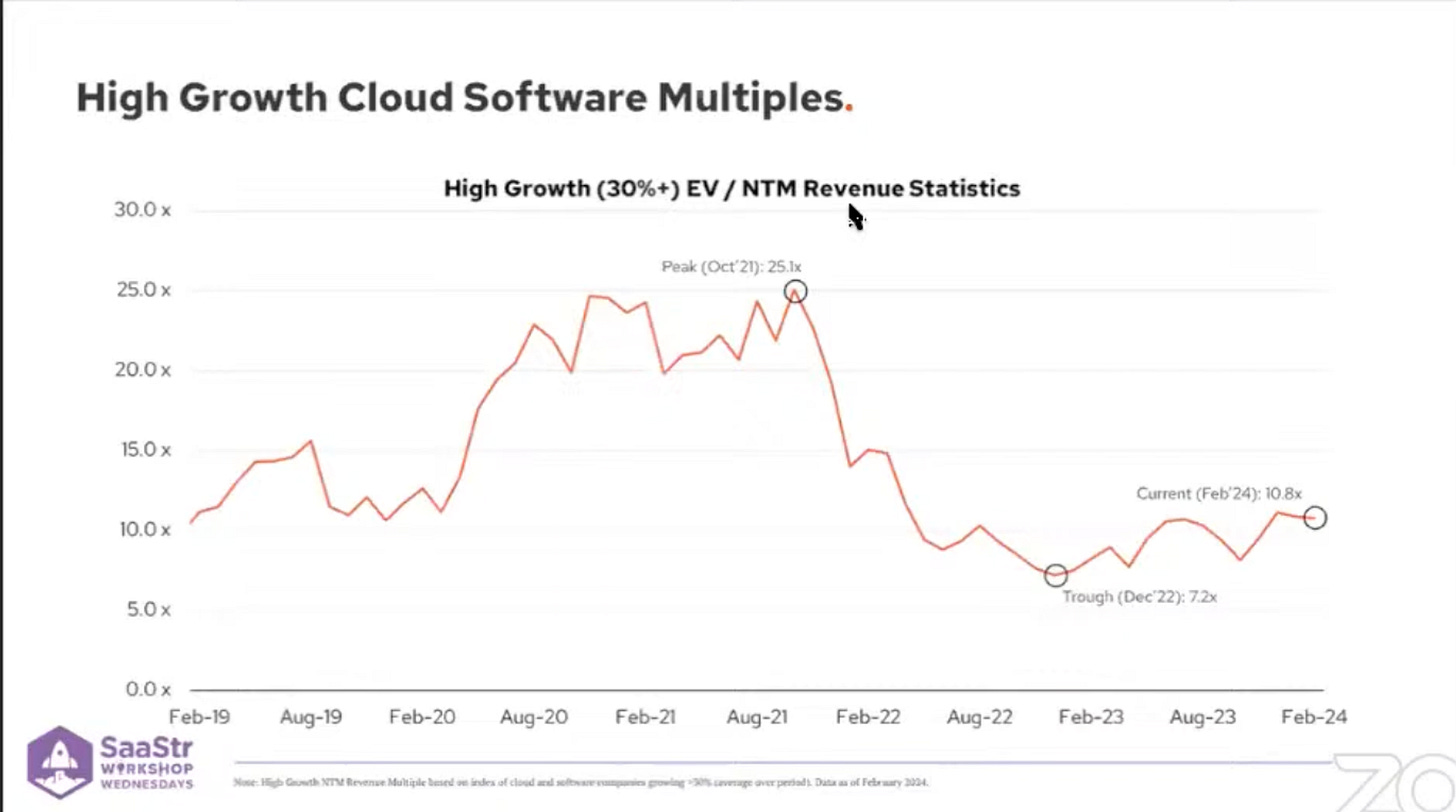

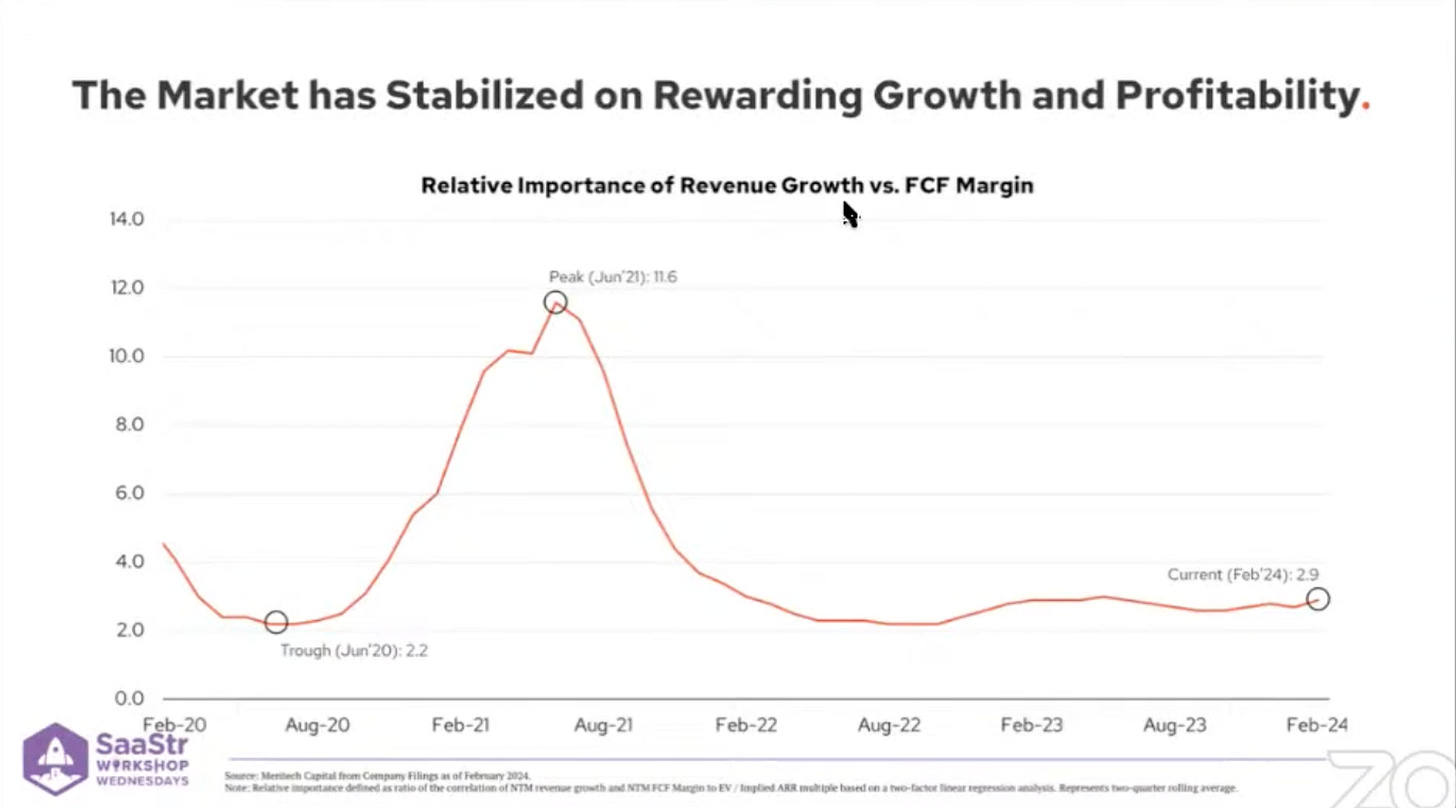

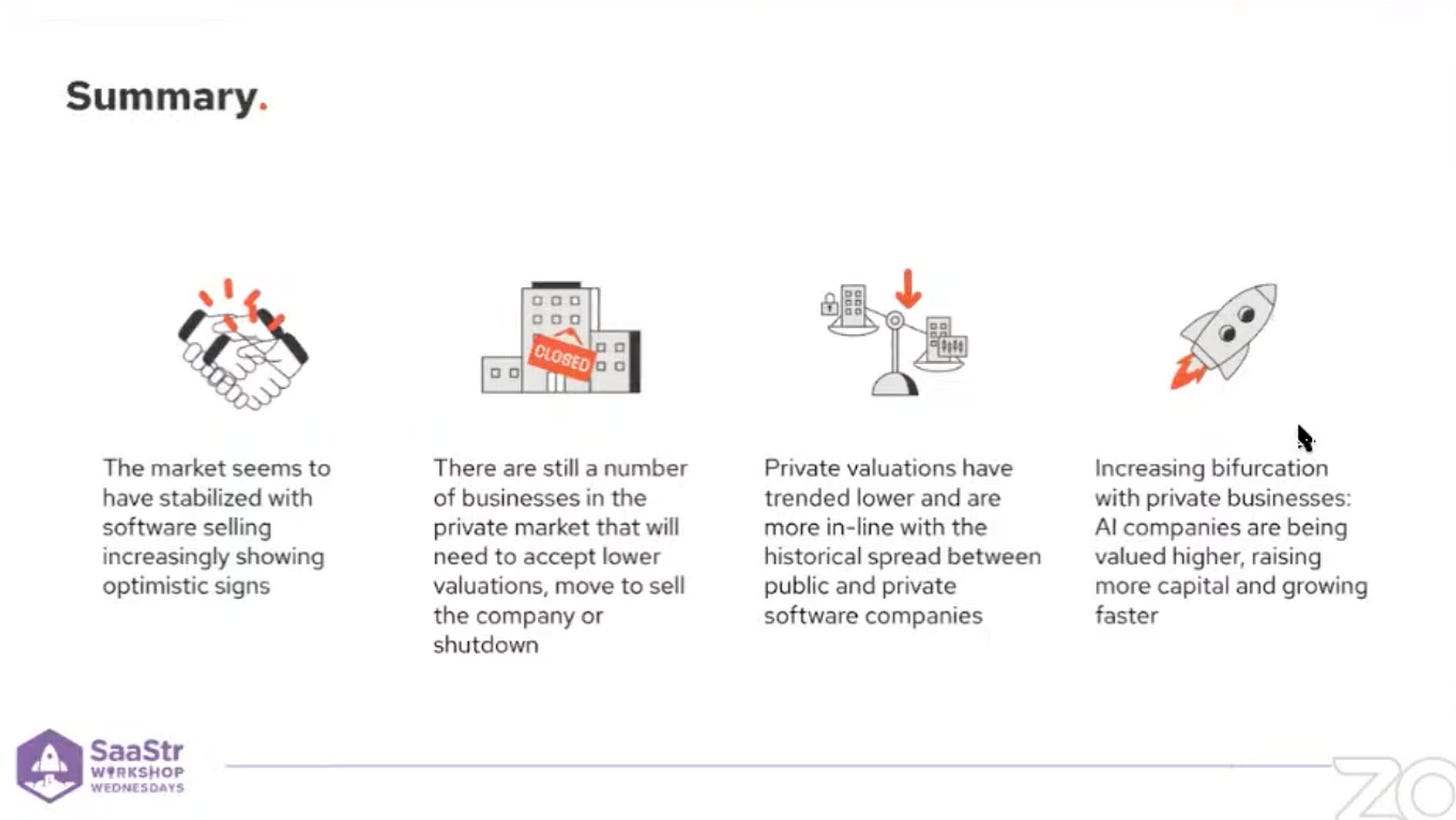

Tuesday, Jul. 16th: I watched a market overview shared by Logan Bartlett at Redpoint. - SaaStr

The NASDAQ is at an all-time high but this is largely driven by the magnificent seven.

High growth cloud software companies are trading 8-10x EV/NTM Sales which is in line with the 2008-2018 historical average.

A percentage increase of growth has always been worth more than a percentage of profitability. Today, 3% in growth equal 1% of profitability margin.

There are 3 situations in the private market: (i) some companies have held off on raising subsequent financing to grow into their valuations, (ii) some companies have raised down rounds resetting expectations on the real value of the business and (iii) and some companies have shut down.

Wednesday, Jul. 17th: Google was in advanced conversations to acquire cybersecurity startup Wiz for $23bn. In the end, Wiz rejected Google’s offer. It would have been Google’s largest acquisition to date. It was a strategic move by Google to enhance its cybersecurity offerings, strengthen its cloud computing division, and compete more effectively with rivals like Microsoft and Amazon in the cloud security domain. - Techcrunch, Eric Flaningam, WSJ

Wiz was founded in 2020. It reached $350m in ARR in 2023 being one of the fastest growing tech companies. It was planning to reach $1bn in ARR by the end of 2025. As of today, Wiz is doing $500m in ARR growing 120% YoY implying a 46x EV/ARR multiple. Wiz raised $1bn at a $12bn valuation in May 2024.

“GCP’s security portfolio is strong across analytics & managed services (Mandiant), SecOps/SIEM (Google Chronicle), and monitoring/governance (Cloud Monitoring, Dataplex). Wiz is the top cloud security company and fills a lagging area in GCP’s roadmap.”

Wiz has 4 cofounders which are owning each c.9% of the company. Index is the largest investor shareholder with a 11% stake followed by Sequoia with 10%, Insight with 9%, Greenoaks with 5% and Cyberstart with 4%.

“The deal talks provide a glimmer of hope for hundreds of other private tech companies looking for an exit path. While giants such as Microsoft and Nvidia have been on a tear, much of the startup sector outside of artificial intelligence is in shambles thanks to slowed venture funding, a chilly IPO market and regulatory scrutiny that has discouraged acquisitions.”

“The four [cofounders] met over two decades ago when they worked in the Israel Defense Forces cyber intelligence division called Unit 8200. Veterans of Unit 8200 have also founded other highly valued cybersecurity companies including Palo Alto Networks, Check Point and Fireblocks.”

“They soon pivoted to software that helps companies scan and identify security risks from dominant cloud platforms such as Azure and Amazon Web Services, betting that customers would want more protection than the tech giants provide themselves.”

“Raanan's not-so-secret weapon is his extensive network of cybersecurity pros, which he uses to connect his companies with potential customers. The rapid growth of Cyberstarts' portfolio has been powered by an advisory group of more than 50 chief information security officers at companies including Scotiabank, AT&T, Aetna and Zoom Video Communications. The Cyberstarts CISO group meets quarterly to discuss cybersecurity trends and provide feedback to the startups, who can then tailor their products to the needs of those companies. What makes the group unique is that Raanan seeks their input even before his portfolio companies have started building a product, rather than hawking existing products to the CISOS. The security executives advising the startups also get a sweetener: a small piece of the profits Cyberstarts generates from its funds. As a result, the security executives often become the first buyers of software from the Cyberstarts companies, which helps them grow faster. Products developed by young.”

Thursday, Jul. 18th: Sequoia offered its LPs to buy up to $861m of their Stripe’s shares at a $70bn valuation. Stripe’s valuation peaked at $95bn after a funding in 2021 and recorded a $65bn valuation during another secondary sales for employees in February 2024. - Bloomberg, Mostly Borrowed Ideas, Axios

“While Adyen raised ~$300m to build a company worth $30bn, Stripe raised ~$10bn to be allegedly worth $70bn. I say allegedly because they both process similar payments volume, but one is barely profitable whereas the other (Adyen) has ~50% EBITDA margin.”

“Sequoia's partnership with Stripe began in 2010 when Sequoia first invested at the seed stage. Across all funds and financing rounds, Sequoia Capital has invested a total of $517 million in Stripe. As of the most recent 409A valuation in July 2024, with a share price of $27.51 and a total valuation of $70 billion, Sequoia's entire position is valued at $9.8 billion.”

“As a business, Stripe is unusual in three respects. First, it is durable across economic cycles, a fact which we have seen directly. Second, while many products increase efficiencies or save costs, Stripe is one of the few that delivers direct revenue acceleration for its customers. One study by the company found an 11.9% average uplift among customers who adopt their Optimized Checkout Suite. Third, Stripe is useful both to the world's smallest companies and to the very largest (including Hertz, Alaska Airlines, and Amazon), yielding a compelling market opportunity. Testifying to these factors, Stripe handled $1 trillion in payments in 2023. We are enthusiastic about the company's ten-year prospects and Stripe's mission to increase the GDP of the Internet.”

“We are contemplating a transaction where new purchasers, including the Expansion Fund, Sequoia Capital Fund, Sequoia Heritage ("Heritage"), and Sequoia Capital Global Equities ("SCGE"), will commit to buy up to $861 million of Stripe shares held in select Sequoia funds raised between 2009 and 2012 ("Legacy Funds") at the most recent, July 2024, 409A valuation. We explicitly focused on these Legacy Funds, which were organized over a decade ago, given the normal ten-year life of venture funds. Limited partners of the Legacy Funds will have the option to hold or to sell all or a portion of their Stripe shares.”

Friday, Jul. 19th: Tekion raised a $200m round at a $4bn valuation led by Dragoneer. It’s a cloud based dealership management system cofounded in 2016 by Jay Vijayan who was chief information officer at Telsa. Tekion does not try to replace existing dealerships with a car marketplace but is providing them with software and financial services in order to offer a more efficient car buying experience to consumers. Tekion is making $100-200m in sales. In 2023, Tekion registered a 97% YoY growth rate. It has now 2k dealerships as customers. It works with customers including Absurdy Automotive Group, Longo Toyota and Lexus. The capital will be used to expand Tekion's product offerings for dealer partners and OEMs, accelerate implementation timelines, and enhance customer support. - Bloomberg, Tekion

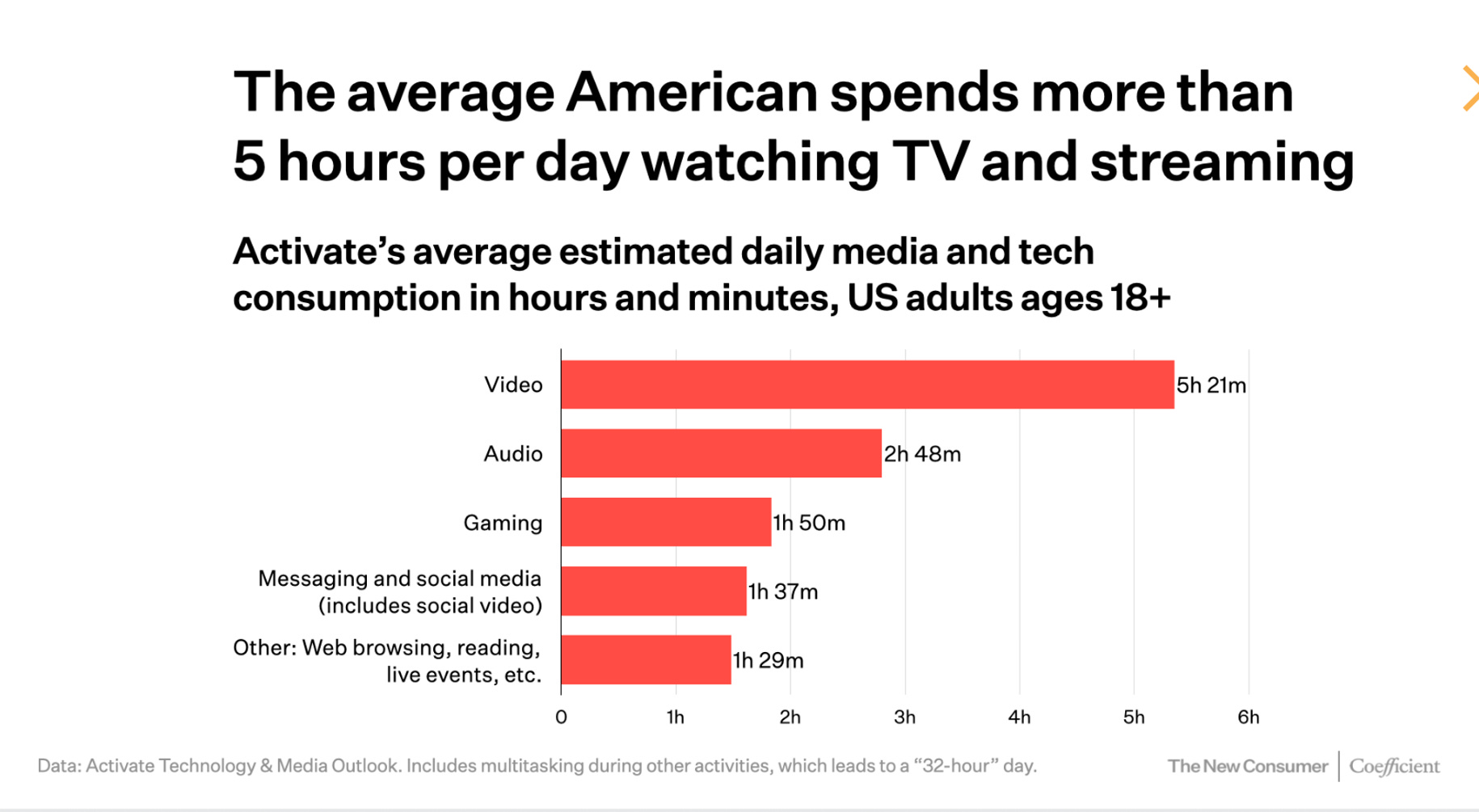

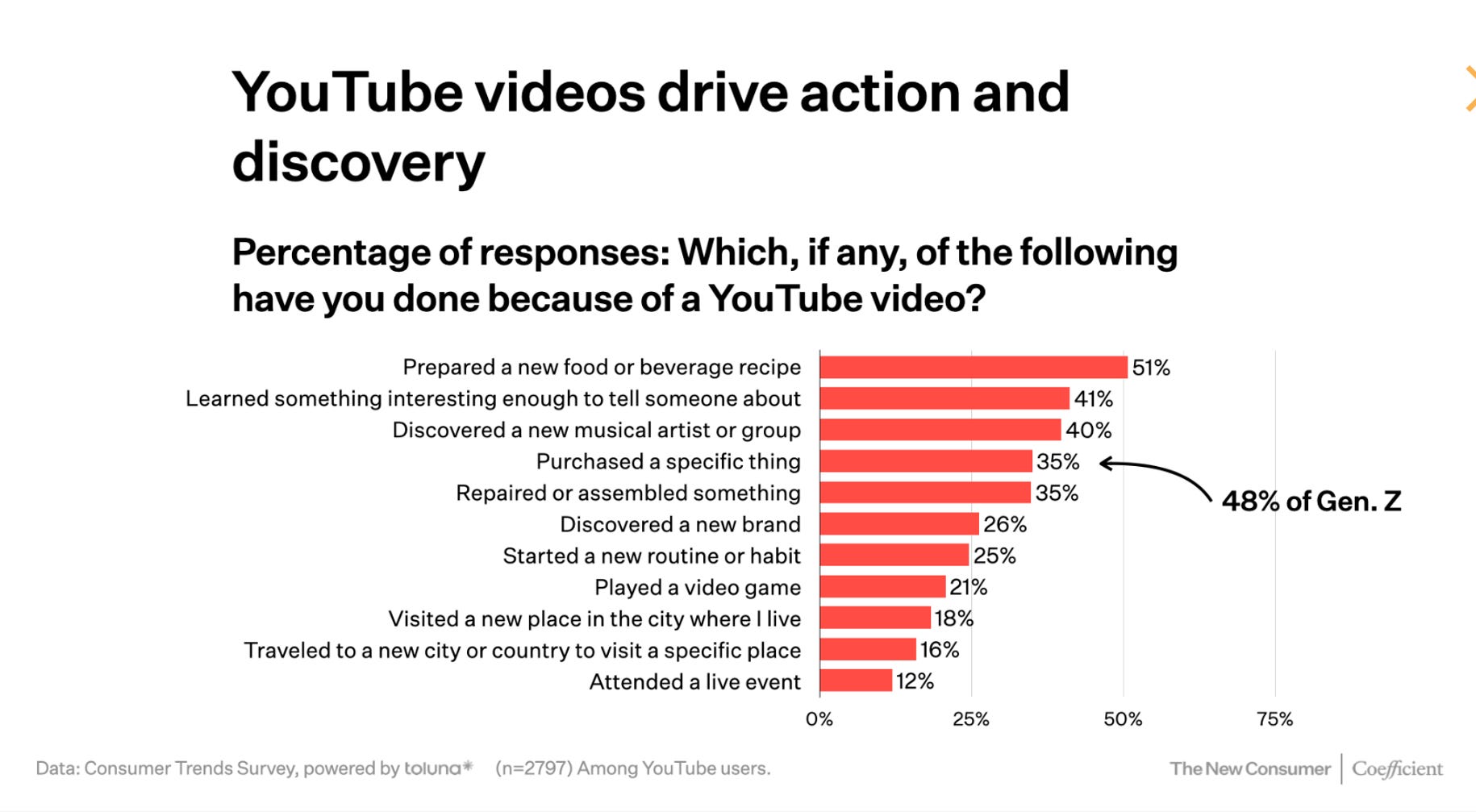

Saturday, Jul. 20th: I read The New Consumer’s most recent report on consumer trends with noteworthy insights on content consumption and on GLP-1. - The New Consumer

Sunday, Jul. 21st: The FT wrote about the current challenges faced by VC firms in achieving profitable exits from their investments. With market conditions making IPOs less viable and strategic acquisitions slowing, VC firms are experiencing extended holding periods for their portfolio companies. This situation is causing liquidity issues and pressuring fund performance. - FT

“Until they cash in a lot more of those unrealised capital gains, many venture capital firms will find it hard to show the kind of strong cash returns needed to persuade their backers to put up fresh capital.”

Big acquisitions have also become scarce. As a result, billion-dollar “exits” by US tech start-ups number only 16 so far this year, compared with 211 in all of 2021, according to Crunchbase.”

Monday, Jul. 22nd: Iconiq officially announced its seventh flagship fund raising $5.75bn to invest in growth stage companies all across the world. - Iconiq, Fortune

Iconiq Growth started in 2013. It invested into 140 companies. 27 companies went public for a total market capitalisation of $1.5tn.

“While the last few years have been remarkably dynamic across the technology landscape, rapid change gives rise to tremendous opportunity. We believe great companies are forged during times of transition, and we are entering a new golden age of inspiring ideas such as in artificial intelligence.”

“To further extend our portfolio companies’ success, we continue to invest in our platform and distinctive capabilities including revenue generation, talent acquisition, data-driven operational insights, technical advisory, and go-to-market advisory.”

“The Iconiq wealth management firm manages some $60 billion in assets for fewer than 300 families—with more than $80 billion in total across both the wealth management firm and venture fund. The typical family client has more than $250 million to invest with the firm and more than $1 billion in assets. Iconiq Capital has some 500 people on staff—working on everything from tax planning to real estate to philanthropy—with 80 people focused on Iconiq Growth, the venture capital arm.”

“Less than 20% of capital in Iconiq Growth’s latest fund came from wealth management clients.”

“Each introduction between a customer or mentor is documented in Salesforce, typically used by companies to track their sales leads. Each executive hire they help with is noted. Each event a founder attends is listed. All these data points are tracked, tallied, and shared with founders they work with. Last year, there were more than 1,150 intros made and the team helped with more than 90 executive or board searches, according to the firm.”

“As its investors have built deeper relationships with tech founders, the firm has put more and more focus on investing at the earlier stages. About half of the time, it makes its first investment when a company is at its Series B stage and the startup is making about $10 million in annual revenue. That’s when a company has found traction in the market, but still has plenty of room to grow, and when Iconiq thinks its customer introductions could help boost its top line.”

“Its first fund in 2013 returned net multiples of 2.7 times the invested capital; the 2014 fund did 5.5 times; the 2017 fund did 5.4 times, and the 2019 fund has so far returned 1.9 times on its investments.”

Tuesday, Jun. 23rd: I read an old short selling report from Spruce Point published in Sep. 2021 on Lightspeed Commerce which is building an all-in-one platform for retailers and restaurants. - Spruce Point

“We find irrefutable evidence that LSPD overstated its customer count by 85%, while GTV, a measure of payment volume through its platform was overstated by at least 10%.”

“After its IPO, LSPD laid out its organic growth plan and listed “attracting new merchants” as its first objective in its year end conference call. On the following call it reported 2,000 net new merchants on its system. Thereafter, LSPD stopped disclosing net new merchant adds and it began a string of acquisitions.”

“Hardware margins have recently turned negative and deferred revenue quality has deteriorated. Hardware sales, formerly a profit center, is now a cost center as competition gives it away for free.”

“Speaking with former employees, we find evidence that not all acquisitions have gone smoothly or met internal expectations, while some acquired platforms have been sunsetted.”

“LSPD promoted a “payments” solution in 2014, which to the best of our knowledge, didn’t appear to gain much traction. Now post-IPO in early 2019, LSPD introduced a new “Lightspeed Payments” and has been heavily promoting its upside to investors.”

“LSPD has not actively pointed out multiple changes to its ARPU KPI disclosure. We had to figure this out by close examination of its filings and statements. The CEO once referenced that ARP of $3k-$5k was necessary to build a company and attract investment. When LSPD stopped disclosing ARPU in Q1 2021, it was only at $245 per month ($2,940/annually).”

“COVID-19 has accelerated the movement from physical to virtual store locations and ecommerce. Whereas LSPD started primarily with POS solutions for brick and mortar retail and hospitality, it has had to acquire its way into providing ecommerce solutions (SEOShop and Ecwid). Conversely, Shopify’s expertise and core competency has always been centered around ecommerce. We believe it has more easily expanded into POS offerings to compete with LSPD. It recently introduced a brand new POS system, and was offering it for free.”

“It is because Shopify and Square give free hardware. Lightspeed is going to have to change, and they are going to have to give away free hardware. They are still using printers that haven’t changed in the last two and a half decades. When you look at the decrease in software ARPU and take into account the negative margin on the hardware, ARPU as a whole has dropped significantly”

“In fact, we believe many acquisitions have been companies that have peaked, restructured, and/or seen declining growth. Thus, we would classify many as “legacy” platforms that failed to scale.”

“My biggest fears about their very aggressive M&A strategy is integrating these companies, not only the financials but integrating systems and how they are going to support all these different products. It is just too much. With all the acquisitions they probably have 6 restaurant POS offerings. It’s just not scalable.”

“Terminal activation is definitely a problem. They had a deal where they would give a free terminal with payments. Basically, with anything that is free, they would ship the terminal and then it would sit in the box under the customers desk and never get activated because there was no incentive.”

Wednesday, Jul. 24th: Vanta raised a $150m series C at a $2.45bn post money valuation led by Sequoia. It previously raised in 2022 at a $1.6bn valuation. Vanta operates in the compliance space. It started in 2018 by automating compliance to popular security certification such as SOC2 and ISO27001 before expanding into a broader Governance, Risk and Compliance (GRC) platform. - Cristina Cacioppo, Bloomberg, Vanta

In the past year, Vanta doubled its number of customers to 8k customers including companies like Atlassian, Quora and ZoomInfo. In Jan. 2024, it passed the $100m ARR threshold. Since then, its growth rate has accelerated especially outside the US.

“We’re building AI and LLM-enabled features for our customers first, not for ourselves. Questionnaire Automation is actually really good – 80-90% answer approvals! – and Trust Center chat quite useful.”

Thursday, Jul. 25th: Clio raised a $900m series F at a $3bn valuation led by NEA with the participation of new investors including GS, Sixth Street, CapitalG and Tidemark. Existing investors TCV, JMI, T. Rowe and Omers also participated. It previously raised a $110m series E at a $1.6bn valuation in Apr. 2021. Clio is an cloud based operating system used by law firms. Its product is used by 150k law professionals. A significant portion of the round is secondary. Clio went from $100m in ARR in Jun. 2022 to $200m in ARR as of today while having been EBITDA profitable for multiple years. - Techcrunch, Clio

“This year, we’re also introducing Clio Duo, our generative AI solution that will assist lawyers with routine tasks and provide insights into how to run more efficient practices.”

Friday, Jul. 26th: I read a Bowery’s interview with Jonathan Rath who is CEO and cofounder at Archy which is a vertical SaaS for the dentist industry in the US. - Bowery

“Archy is an all-in-one platform for dental practices - we handle scheduling, charting, treatment planning, imaging, billing, insurance claims, and revenue cycle management.”

“Our big differentiator is we have put these solutions that previously existed all into one platform. If a new dental practice were to launch tomorrow, they can sign up with Archy and be pretty much done with building out their tech stack; we have removed the need for a dental office to sign up with 5 or 10 different applications just to get off the ground.”

“Another differentiator is that we are cloud-based; 90% of the dental industry is still using on-prem servers to run their practice. This typically means they need to use an IT services company that can manage their server and their backups which is another added cost.”

“Today, most dental practices have a server somewhere in a closet in their office and then they have an outsourced IT management company which handles all IT operations.”

“In addition to a server, a typical practice usually has some core practice management software, and, at a minimum, separate pieces of software for imaging and patient engagement. If they are more advanced, they may also have a patient-facing online booking platform and some kind of BI reporting tool for running basic analytics. Like most businesses, dental practices will also have an HR platform for managing employees and some kind of payroll solution. These are just the basics - some practices may have even more in the way of software - but that is the typical stack.”

“Our ideal customer right now is a dental practice which operates out of a single location. It does not really matter how many dentists work there, they could have 1 provider or 15. Multi-location practices are our next focus and should be launching soon.”

“Another good example is payroll, we did not build a payroll company - these are big, complicated businesses on their own. Instead, we partnered with Gusto and we use their white-label API. This leads to real benefits in terms of efficiency for the practice, but there is no way we were going to build our own payroll company given all of the tax regulations and compliance.”

Saturday, Jul. 27th: Equal Ventures shared a venture investment thesis on backing tech enabled businesses consolidating insurance brokers. - Equal Ventures

“There is an opportunity to create a next-generation aggregator consolidating the long-tail of broker agencies into a single platform. This platform could grow incredibly fast by leveraging digital solutions that have proven to significantly cut transaction costs and expand EBITDA margins.”

Sunday, Jul. 28th: I listened to a 20VC’s podcast episode with Jason Lemkin on recent tech news. - 20VC

On Wiz walking away from a $23bn acquisition by Google:

It was not an expensive offer to pay 46x EV/ARR. This is a company which has gone from nothing to €500m in ARR in 4y. It’s meaningful to use ARR multiples only if you talk about companies growing at the same rate as top public companies. Wiz will be at $1bn in ARR in 12-18 months which would imply a 23x multiple which is comparable to what we see in the public market for top cyber security companies like Crowdstrike before its recent incident. “I don't think it was that expensive. That's why they could comfortably say no.”

For Google, looking to acquire businesses like Wiz or Hubspot makes sense in order to find the new platforms that have scale and that can have a positive impact on the mid to long term growth of the overall business. Wiz has strong synergies with Google Cloud and could help Google Cloud to be more competitive against Microsoft and Amazon.

“Offering 2x the last round is the clearing price to acquire a growth stage company that is doing well.”

For Wiz, it was not worth the risk of being blocked by the regulators knowing the trajectory of the company and its intention to IPO in the next couple of years. The regulatory antitrust company could kill the company and at best it’s a massive distraction for the company and the team if it does not go through.

For early stage investors in Wiz, they did not care if the deal was accepted or not because if not, they will have an opportunity to sell in secondary at this valuation in the following 12 months.

On liquidity in the venture market:

“If large M&A deals are blocked by antitrust, you know the majority of the liquidity in venture is blocked.”

Tech investors are investing today assuming that liquidity will come back in the market in the next couple of years but so far it has not been the case.

“This is the hardest time of my entire career. Tech multiple are down. Liquidity is tough. At the same time, you have now companies like Wiz or OpenAI that are executing at an unseen pace. Your job as a venture investor should only to find and be in these companies. And the founders of these companies don’t care about where we are in the macro cycle. They start their business whenever they want. There is one Wiz per year in the world and your job as a venture investor is to find it.”

“There are one or two entrepreneurs that will change an industry every year your job is to invest in them. It's it's very simple.”

“We’re praying we’re hoping liquidity comes back but we’re investing like there’s almost as much liquidity as 2021.”

On requirements to go public:

“I think you need $500m in ARR growing 30% YoY to go public. You could do it at $200m in ARR growing 50-60% YoY because it means that you will land at $500m growing 30% but the reality is that most $200m ARR companies are not growing at that pace.”

On Crowdstrike:

This incident shows “it’s incredibly important to global security and infrastructure and the numbers are still amazing.”

“Prior to this incident, CrowdStrike was arguably the most attractive SaaS and cloud company.”

CrowdStrike has benefited from customer loyalty. It’s going to be a rough NRR year. GRR will stay high, but upsell will be brutal. CrowdStrike needs customers to love their product so much they want to buy more. It’s not just about being multiproduct, it’s about customer love.

“I think almost upsells are going to have to go on hold for like three quarters. Upsell is not just about being multiproduct. It’s also having folks love your product so much that they want to buy more products from you. If you messed up with your customers, they may not love you as much as before.”

“Everyone gets one pass. In the end, this was not a security incident that would have put the entire business in jeopardy. If CrowdStrike is still the best solution despite this issue, they get one pass. A couple of customers will churn but most of them will forget and restart to buy more from Crowdstrike in 6-12 months.”

On Clio’s funding round:

“This whole payments fintech thing is their big accelerator. It took them 15 years to get to $100m, but they doubled in 2 years due to managing legal payments.” Moreover, revenue growth is still accelerating.

“Cleo is a company founded in 2007 with a great CEO everyone in legal Tech love. The fact that he could commit as the founder for this long and finally hit it is just heartening.”

Monday, Jul. 29th: I listened to a 20VC’s podcast episode with Saam Motamedi who is a General Partner at Greylock. - 20VC

“We are in an exuberant AI bubble. I could argue it’s even crazier than what was happening in the 2021-2022 tech peak.” “Companies that have a little bit of revenue growth are raising at 100-200x revenue, whereas top public names trade at 15-20x forward revenue.” “That dislocation does not make sense to me unless you believe that these companies fundamentally have much more persistent growth than prior generations of software companies.” It has been the case so far for OpenAI but it won’t be the case for many Gen. AI startups.

Gen. AI can disrupt the three pillars of a SaaS which is its data model, its delivery model and its interface opening the door to create a new generation of horizontal SaaS. “If you think about what have been the largest outcomes in SaaS, most of them are deep systems of record for important horizontal functions.” “I would argue that you can only go after the core when the data model profoundly changes, the delivery model profoundly changes and when the interface changes.” “You need disruption on these three buckets for the opportunity to be real. Otherwise, it’s just incremental.

“Open AI is ruthless and the quality of their execution is just incredible. We should expect them to continue executing and shipping amazing products. My mental model to understand where Open AI is going to play in the future is that there are some applications that are foundational primitives and workflows on top of Gen. AI that Open AI will want to own. It includes content generation, writing, editing as well as coding.”

“We do think there are some applications where you need to own the model because the model needs to be tied to the application.”

“One of the distortions of the 2020 to 2023 period is we all forgot about the power law. We all forgot that very few companies matter, but the companies that matter end up being much larger than we think.” “All that matters is are you backing the team that has a chance of building an iconic and enduring company? Those teams are really scarce. So when you find one of those teams, I really don’t believe you should be passing on price.”

“We make very few investments at Greylock. Each partner might make one to two investments a year. And many of them start as very small checks. The last two investments I made over the last 12 months, one was a $6.5m check and the other was a $5m check. But our constraint is not the capital. Our constraint is our time. Because when we make these investments, we sign up to be accountable and in service of the founder forever. Like, it’s not an option for us. And so we actually, on the $6.5m check, I spent 90 days getting to know the founders in our offices before we wrote that investment, where I was working with them every single day.”

“I would say that great money is made being contrarian and being right. There are multiple ways to do that. I think the common way people do that is they find companies or markets that others aren’t all over and they invest in them. And then a year later, it’s clear that thing’s really working and they benefit from cheap follow-on capital. But another way you can be contrarian and right is to take a really competitive situation and say that you’re willing to pay twice the price anybody else is willing to pay because you actually are such a believer in this thing that you’re willing to price it at twice the price that other people are paying.”

Tuesday, Jul. 30th: Massimo Giunco wrote about Nike’s failed strategy to streamline its organisation to become a D2C brand. - Massimo Giunco

John Donahue joined Nike as a CEO in Jan. 2020 and launched a transformative plan based on 3 key pillars: (i) Nike will eliminate categories from the organization (brand, product development and sales), (ii) Nike will become a DTC led company, ending the wholesale leadership and (iii) Nike will change its marketing model, centralizing it and making it data driven and digitally led.

“Things seemed to go well at the beginning. Due to the pandemic and the objective challenges of the traditional Brick & Mortar business, the business operated by Nike Direct (the business unit in charge of DTC) was flying and justifying the important strategic decisions of the CEO. Then, once normality came back, things slowly but regularly, quarter by quarter, showed that the separation line between being ambitious or being wrong was very thin.”

“As announced by the quarterly earnings releases, the inventory level on May 31st, 2021, was 6.5bn $. On May 31st, 2022, it was 8.5bn $. On November 30th, 2022, it reached 10bn $. Nike didn’t know anymore what to produce, when to produce, where to ship. Action plans to solve the over-inventory issues planted the seed of margin erosion, as Nike started to discount more and more on its own channels.”

“Many consumers - mainly occasional buyers - did not follow Nike (surprise, surprise) but continued shopping where they were shopping before the decision of the CEO and the President of the Brand. So, once they could not find Nike sneakers in “their” stores – because Nike wasn’t serving those stores any longer -, they simply opted for other brands.”

Wednesday, Jul. 31st: Christoph Janz shared lessons on Clio’s journey to $200m in ARR. - Christoph Janz

“Today, Clio is used by more than 150k legal professionals, has crossed $200m in ARR, is endorsed by more than 100 law societies and bar associations worldwide, and has more than 1,100 employees.”

“Some of the best companies don’t follow the T2D3 path. The reality is that very, very few companies can sustain this type of explosive growth over an extended period. Attempting to force it often leads to failure. The good news is that growing a little slower is not the end of the world. If you have a great product with high NPS, low churn, and an excellent position in your market segment, you have a decent chance of getting to $100M in ARR even if your growth rate starts dropping significantly below 100% year-over-year at around $10M in ARR. It just takes a few more years.”

“Except for the first few years, Clio never grew at 100% year-over-year. However, Clio has unusually high growth persistence, i.e. its growth rate didn’t go down much with increasing scale.”

“Clio began as practice management software for solo lawyers, offering a simple solution for time tracking, billing, and document management. Sixteen years in, it has become a true industry operating system, powering not every aspect of the legal process including client intake, client communication, court filings, accounting, and much more.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

I really enjoy these and have been doing so for almost a year. Each time I read it, I can't help but feel they'd really improve if you added one liner take aways. Your other writing is great but I think you'd benefit from it as well as us.