📖 Venture Chronicles - January 2026

Overlooked #211

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of January.

I curated updates and insights around three themes:

Vertical Software

General Venture Capital

Entropy - other news and personal topics of interest

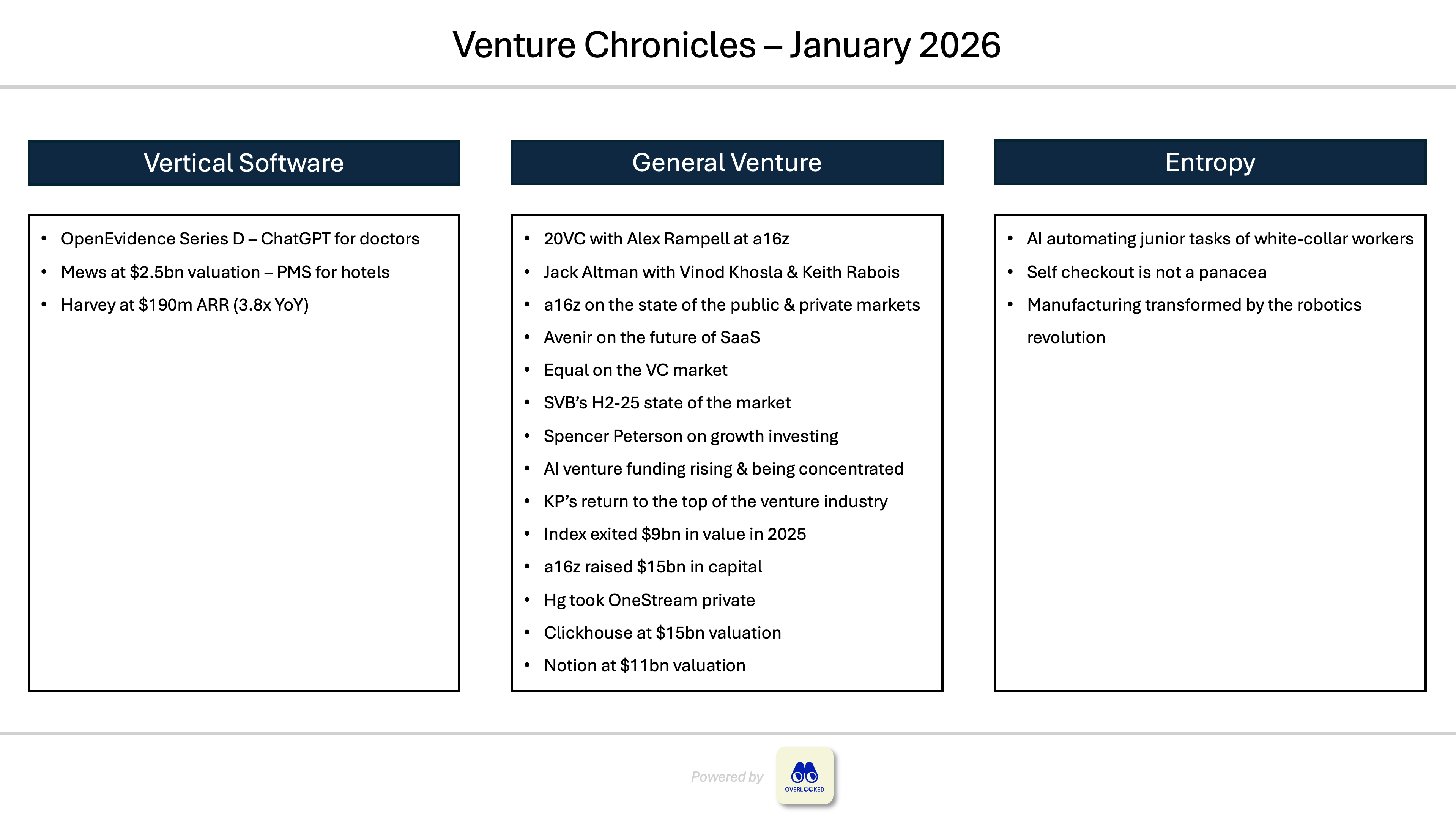

Vertical Software

OpenEvidence raised a $250m series D round led by Thrive and DST at a $12bn valuation. - CNBC, BusinessWire

OpenEvidence is a chatbot for doctors, with AI models trained on data and information from top scientific journals. It has reached a strong penetration and usage across doctors that it will start to monetise via digital advertising from pharmaceutical following Doximity’s playbook.

“OpenEvidence is the most widely used AI platform by doctors in the U.S., with more than 40% of physicians utilizing the tool.”

“While competition [from OpenAI & Claude] is emerging, Nadler said his company’s moat is its focus on physicians, quality of data and a first-mover advantage.”

“OpenEvidence said it topped $100 million in annualized revenue last year, mostly fueled by organic growth. Nadler said 95% of new users hear about OpenEvidence from another physician.”

Mews raised a $300m series D round led by EQT Growth at a $2.5bn valuation. Atomico, HarbourVast, Kinnevik, Battery and Tiger are all participating. - Mews, Hotel Dive

Mews is a cloud-based property management system for hotels disrupting Oracle’s Opera. It has 15k customers representing 132k hotels. In 2025, it processed $19.7bn in transaction volumes and grew its SaaS gross profit by 55%.

It will use the funding to add an AI layer to its platform, double down on financial services, keep expanding mostly in North America and Europe and pursue its serial acquirer strategy with 14 acquisitions to date.

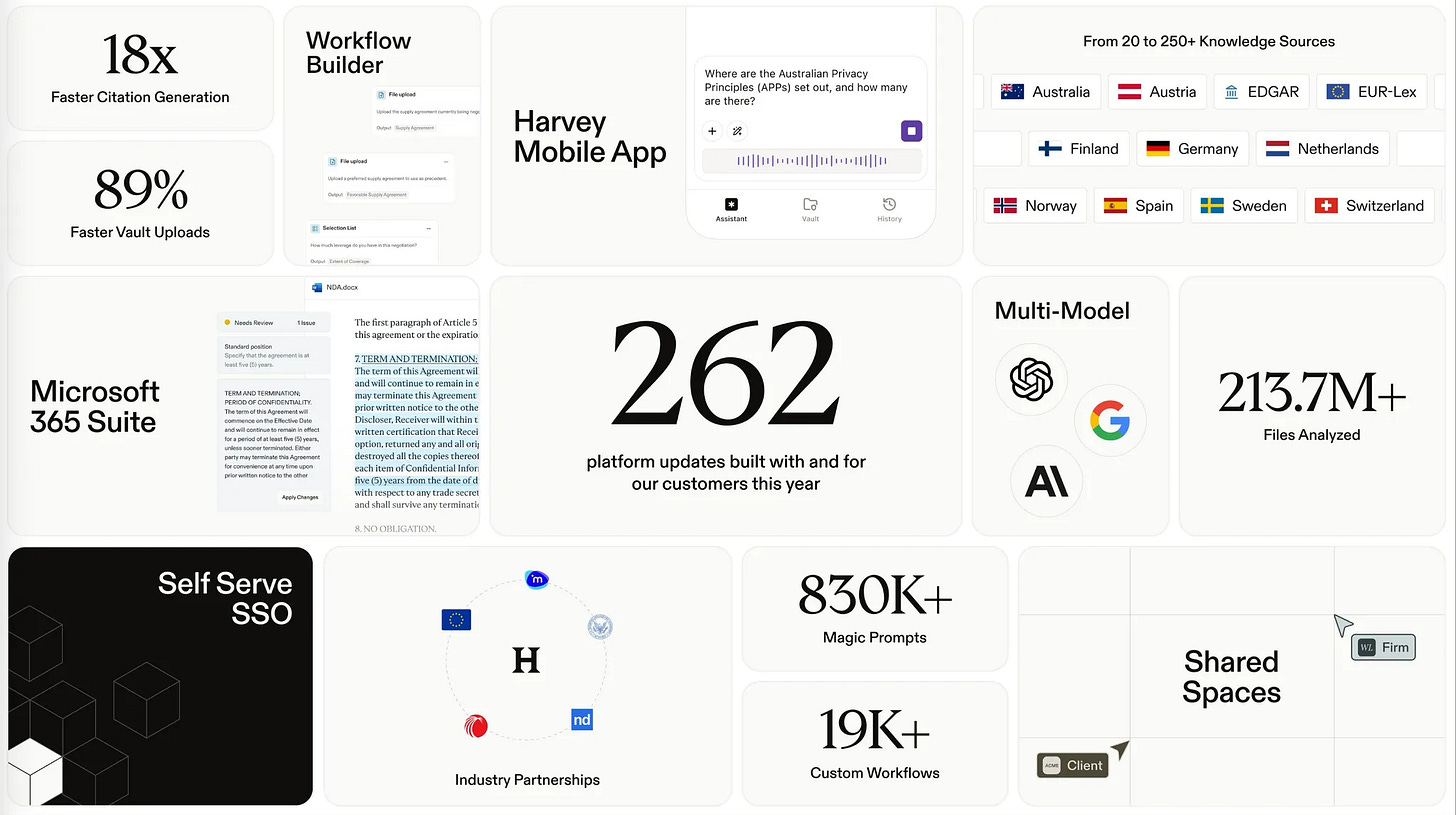

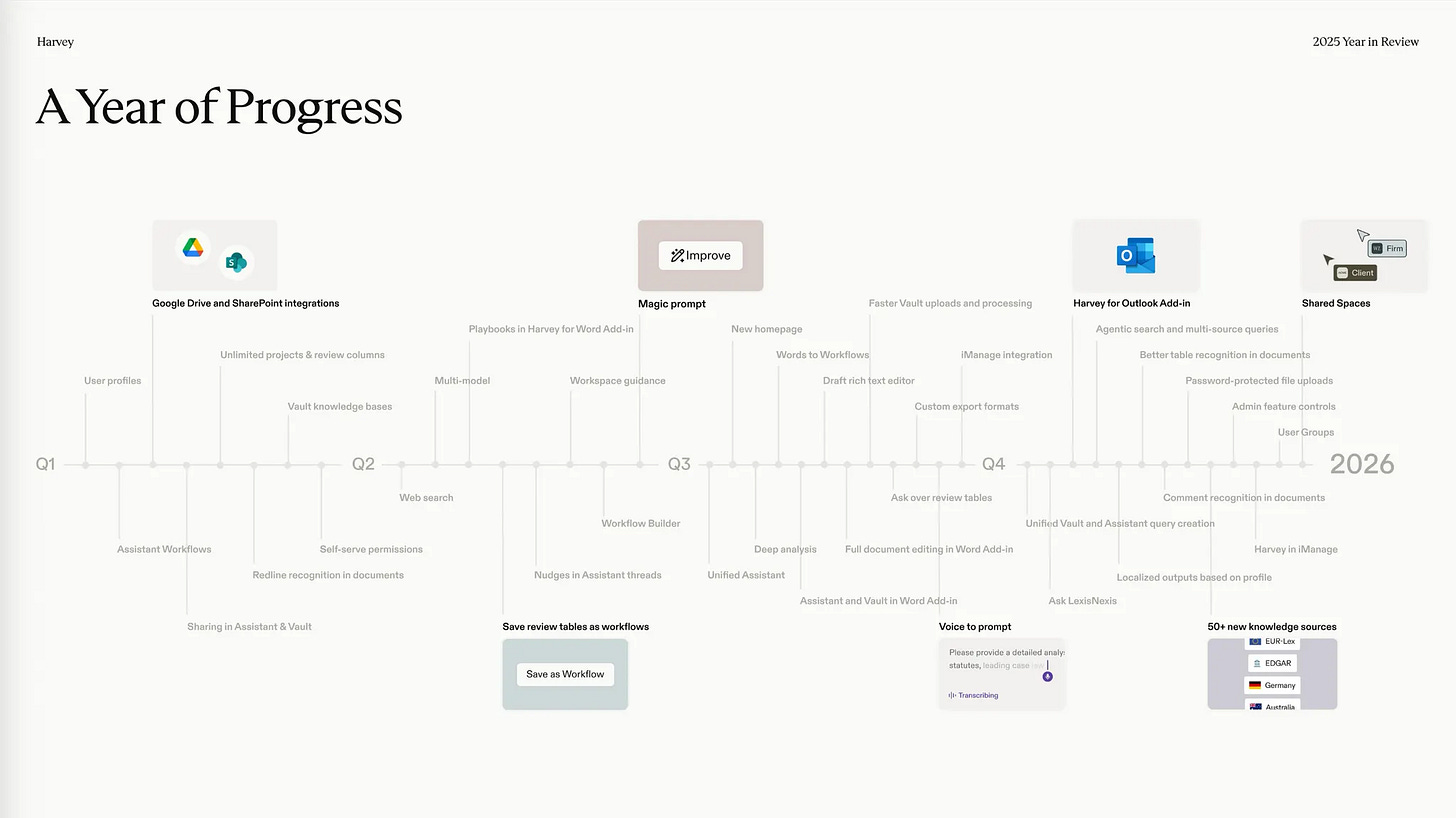

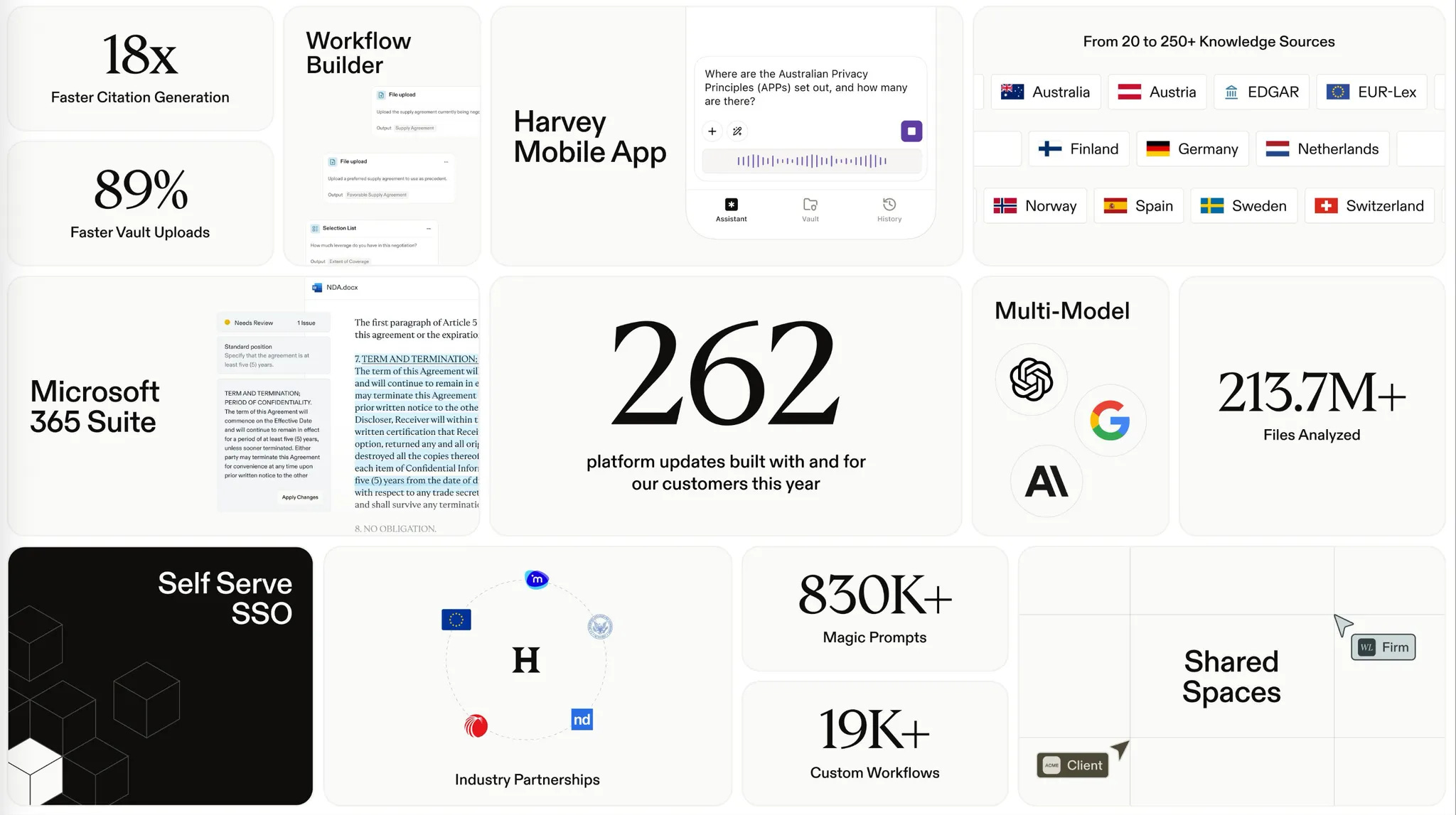

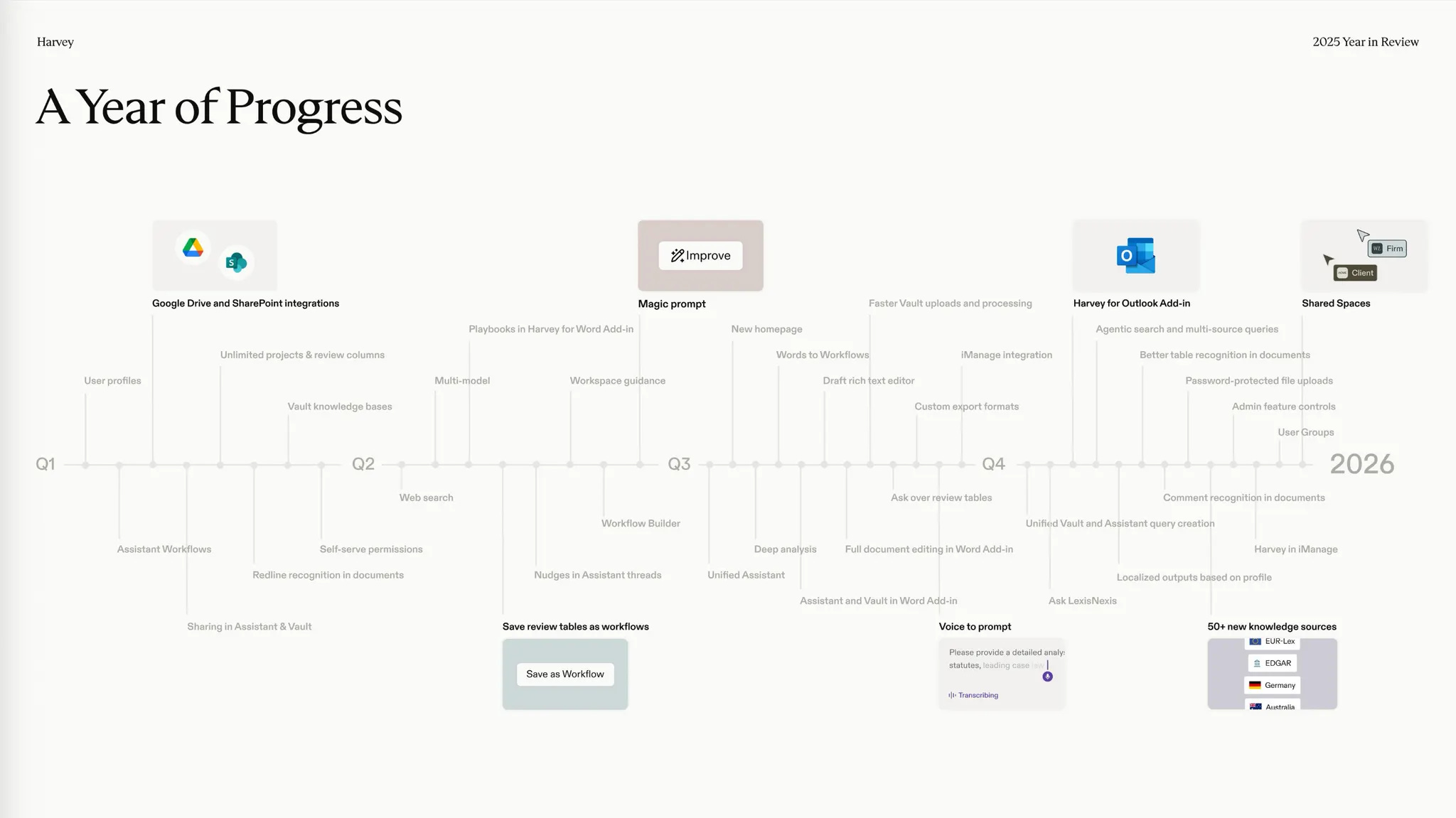

Harvey released its 2025 year in review report. It’s a legal AI operating system for law firms and in-house legal teams. - Harvey

KPIs: $190m in ARR (3.8x YoY), 1k+ customers (including 50% of top 100% US law firms), 92% monthly adoption rate, offices in 10 countries (including Spain, UK, Germany, Ireland and France in Europe), 500 FTEs.

General Venture

Harry interviewed Alex Rampell at a16z. - Alex Rampell

The death of the middle in venture. To succeed in VC, you must operate at the extremes: either as a large generalist with extensive resources & network effects (e.g. a16z, Insight, Lightspeed, GC) or as a small specialist with deep domain expertise (e.g. Ribbit in fintech).

Top founders can uniquely “materialize labor, capital, and customers.”

Materialize Labor: convince top talents to leave high-paying & stable jobs at top tech companies to join a high-risk startup with a significant pay cut.

Materialize Capital: unique storytelling skills to convince investors to provide capital to the business.

Materialize Customers: capacity to land the first five customers with a product that has no historical track record.

Top founders know everything about the history of their industry (e.g. Patrick Collison of Stripe, Brian Chesky of Airbnb).

The best entrepreneurs are often driven by a powerful, intrinsic motivation that goes beyond financial gain. Like the Count of Monte Cristo driven by revenge and redemption, they have a chip on their shoulder.

Startups should have hostages, not customers. The most durable software companies create systems of record that are so deeply embedded in a customer’s operations that switching is nearly impossible, effectively turning customers into “hostages.”

A good strategy for startups to compete with incumbents is to sell to newly created companies which are not held hostage by legacy software (e.g. Stripe in payments, Rillet in ERPs). It works well where the rate of new company creation is high.

Jack Altman recorded a podcast with both Vinod Khosla and Keith Rabois at Khosla. - Uncapped

Vinod and Keith critic the prevailing “founder friendly” paradigm in venture, which they believe is often detrimental to entrepreneurs. They believe that as long as they have the right to advice gained by operational or entrepreneurial expertise, investors should act as active consigliere to the founder or venture assistant actively engaged in company building.

For Keith the best founders are either: (1) top 1 basis point on a specific dimension (e.g. intelligence, tenacity, strategic thinking, people assessment) or (2) have a rare Venn Diagram of traits (e.g. Max at Affirm who is a world class technologist and business mind or Jack at Twitter/Square who is a world class designer, technologist and business mind).

Moreover, best founders have also (1) a very steep learning rate, and (2) a strong ability to surround themselves with A-players.

In AI, rapid learning prevails over experience.

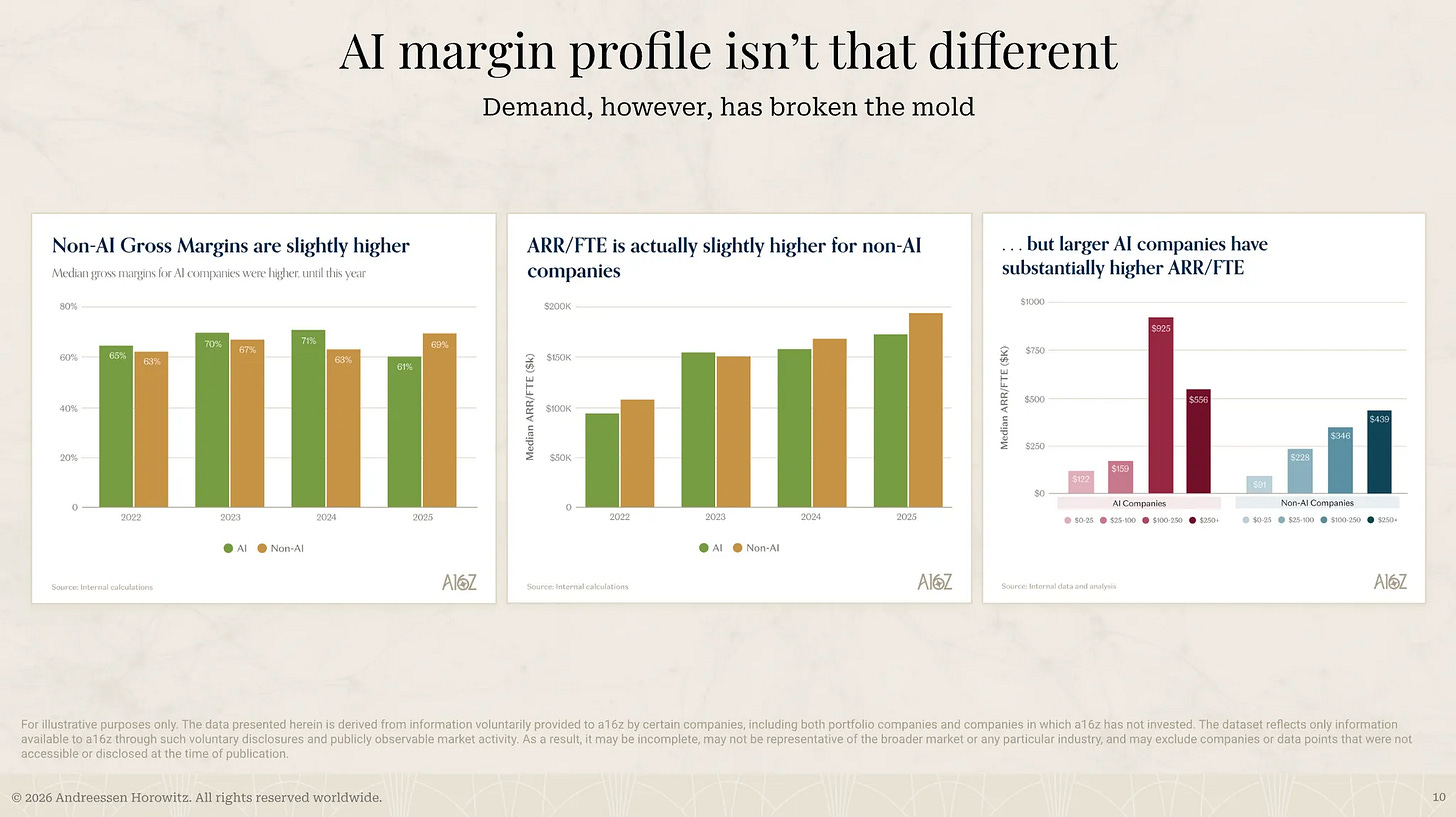

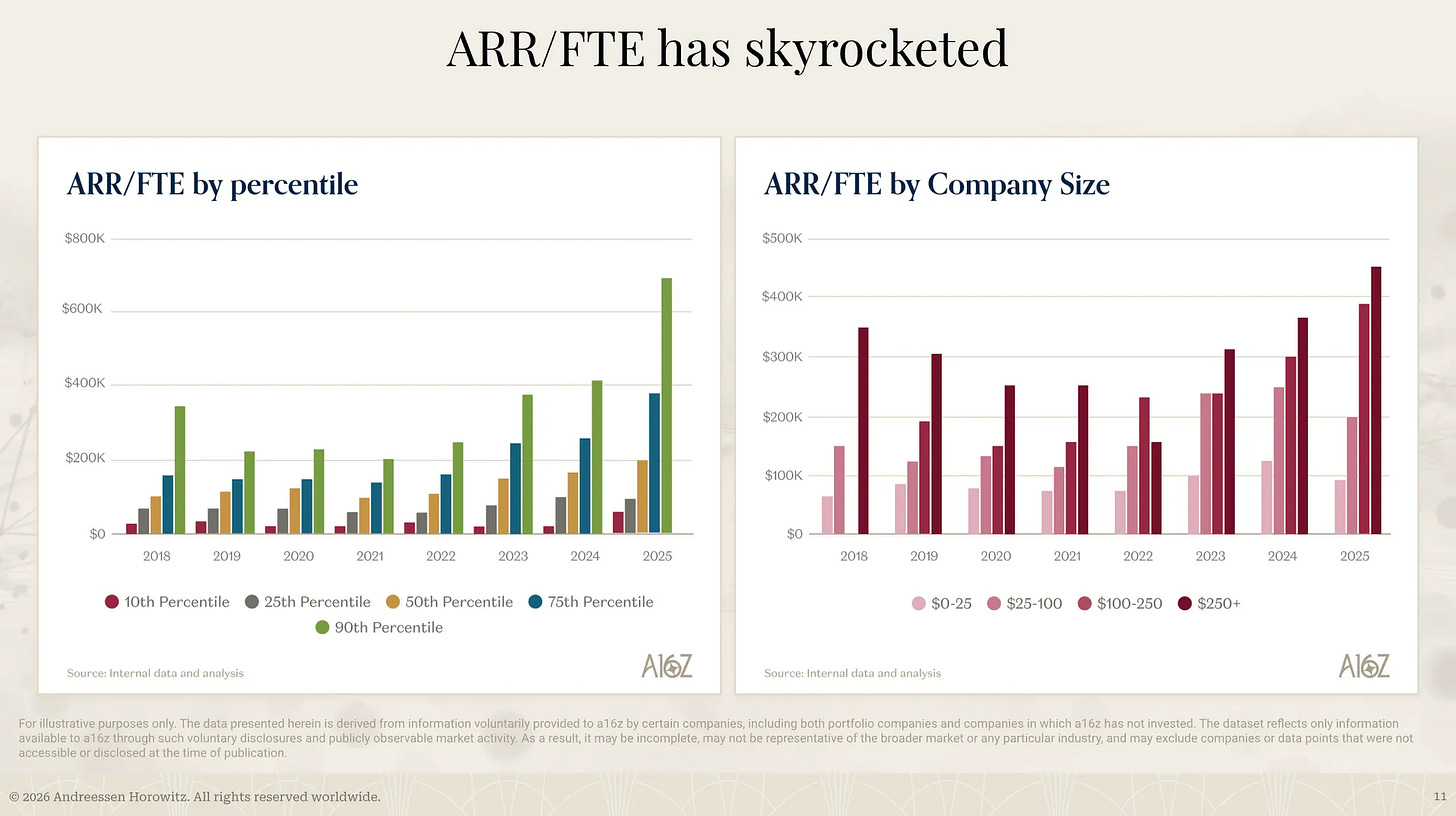

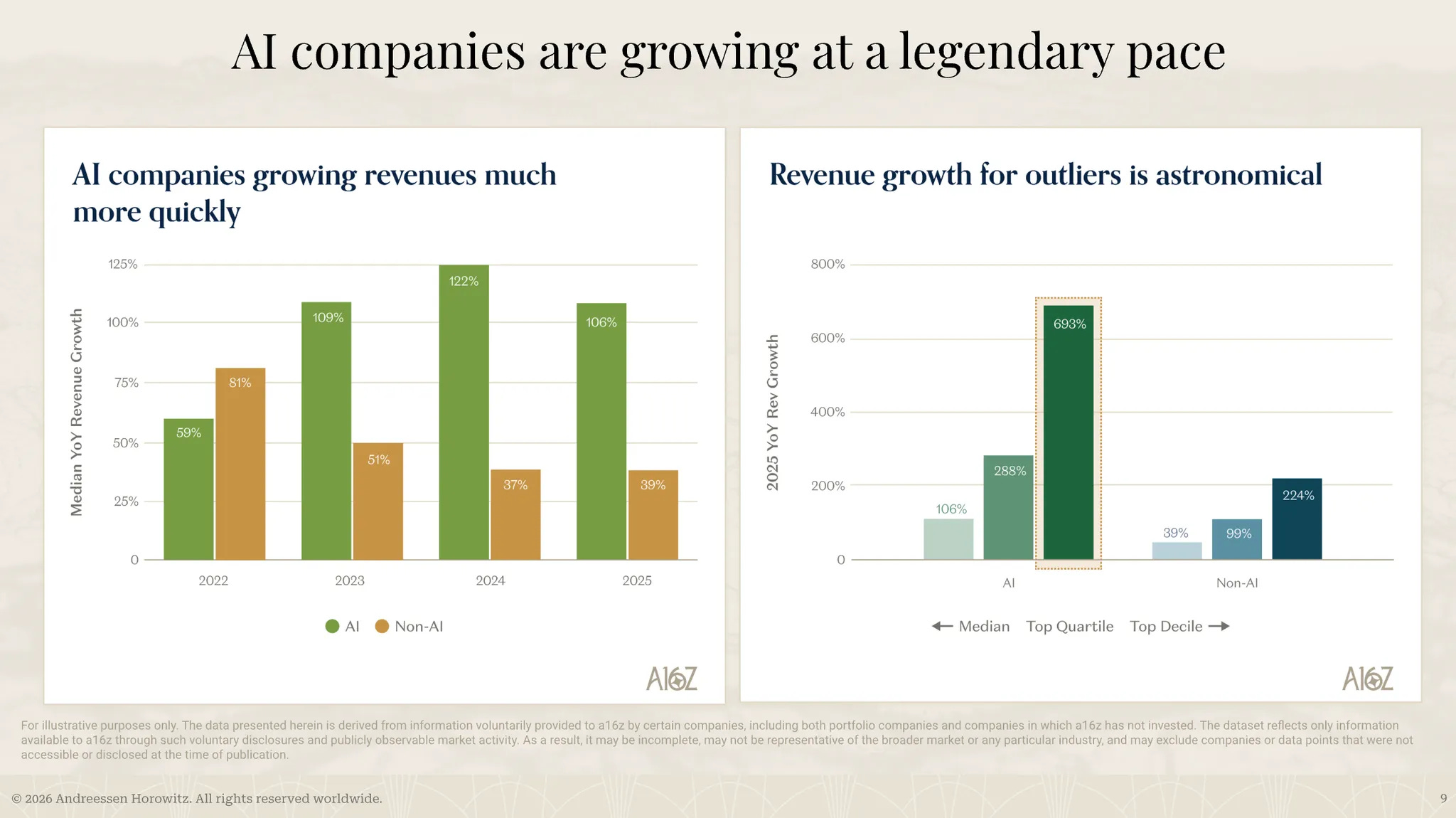

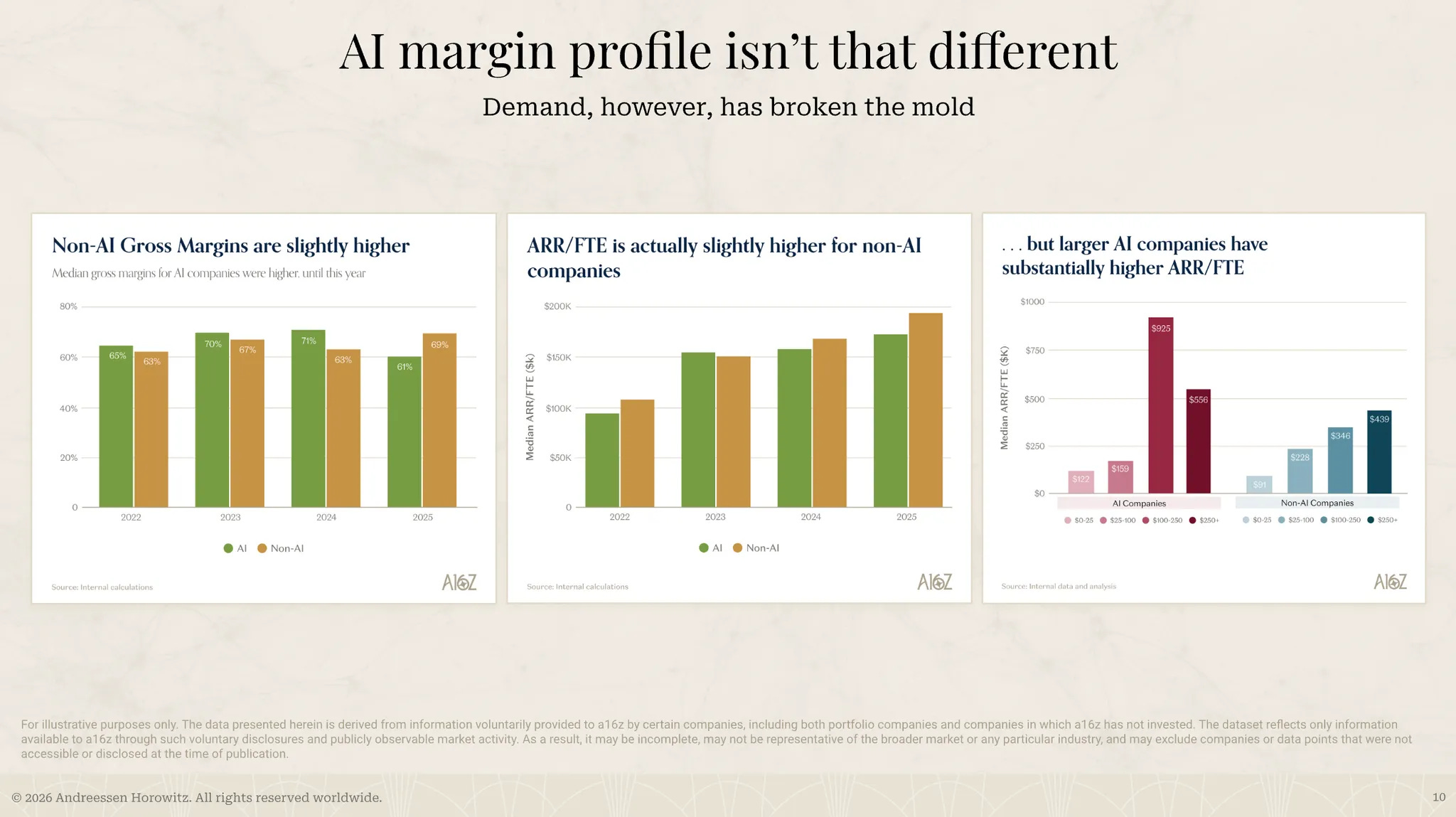

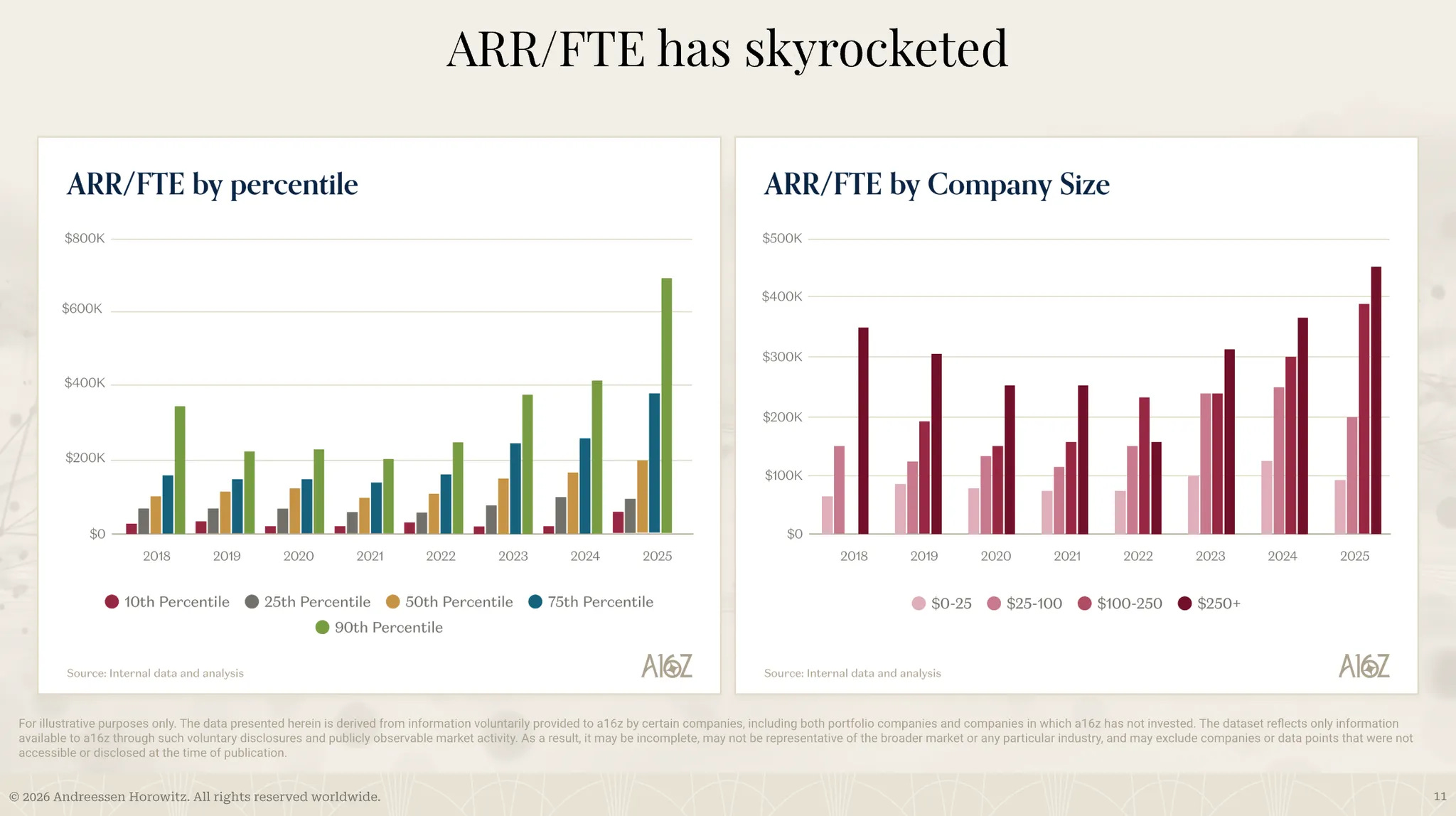

a16z published a presentation on the state of the tech public and private markets. - a16z

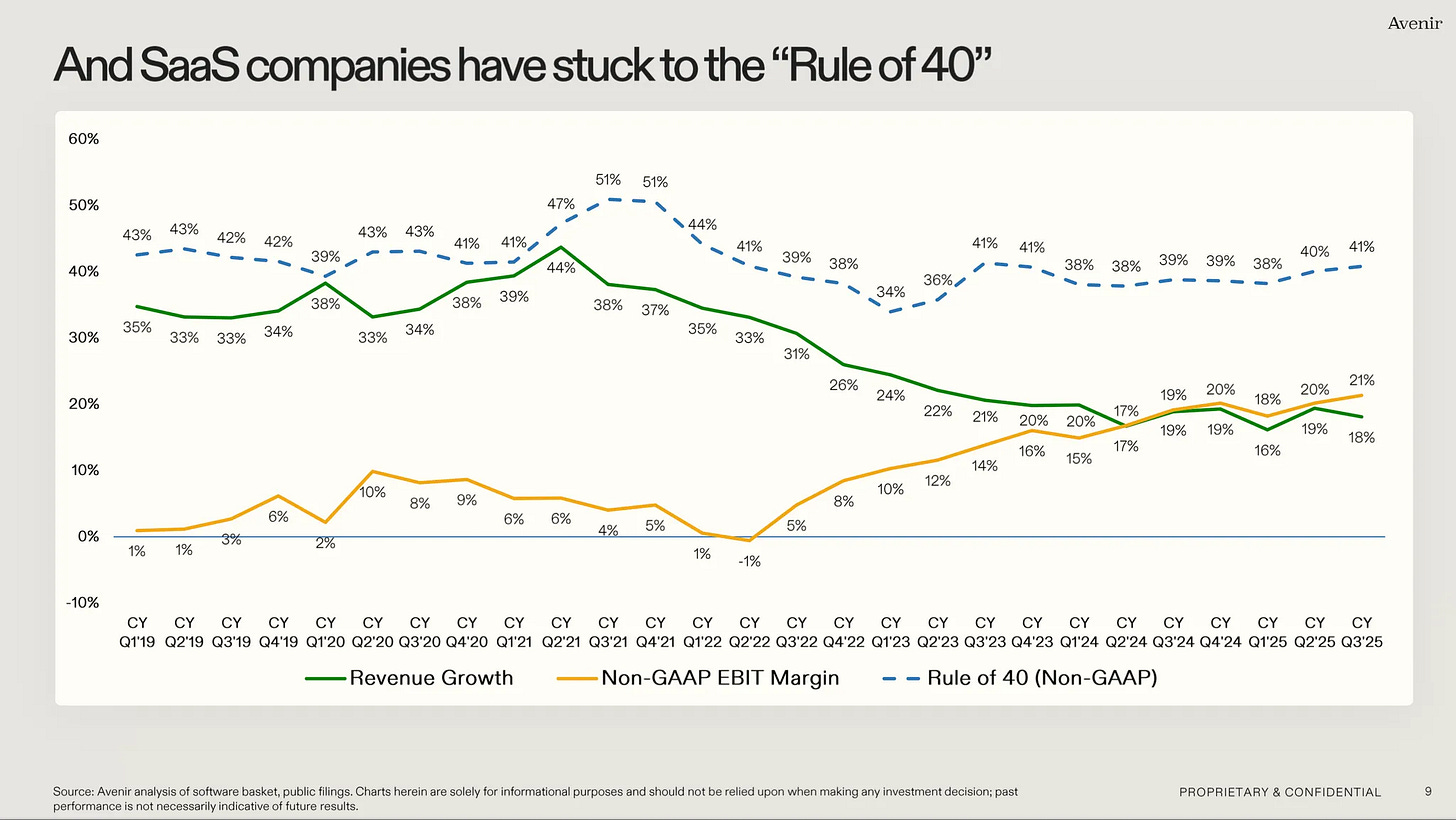

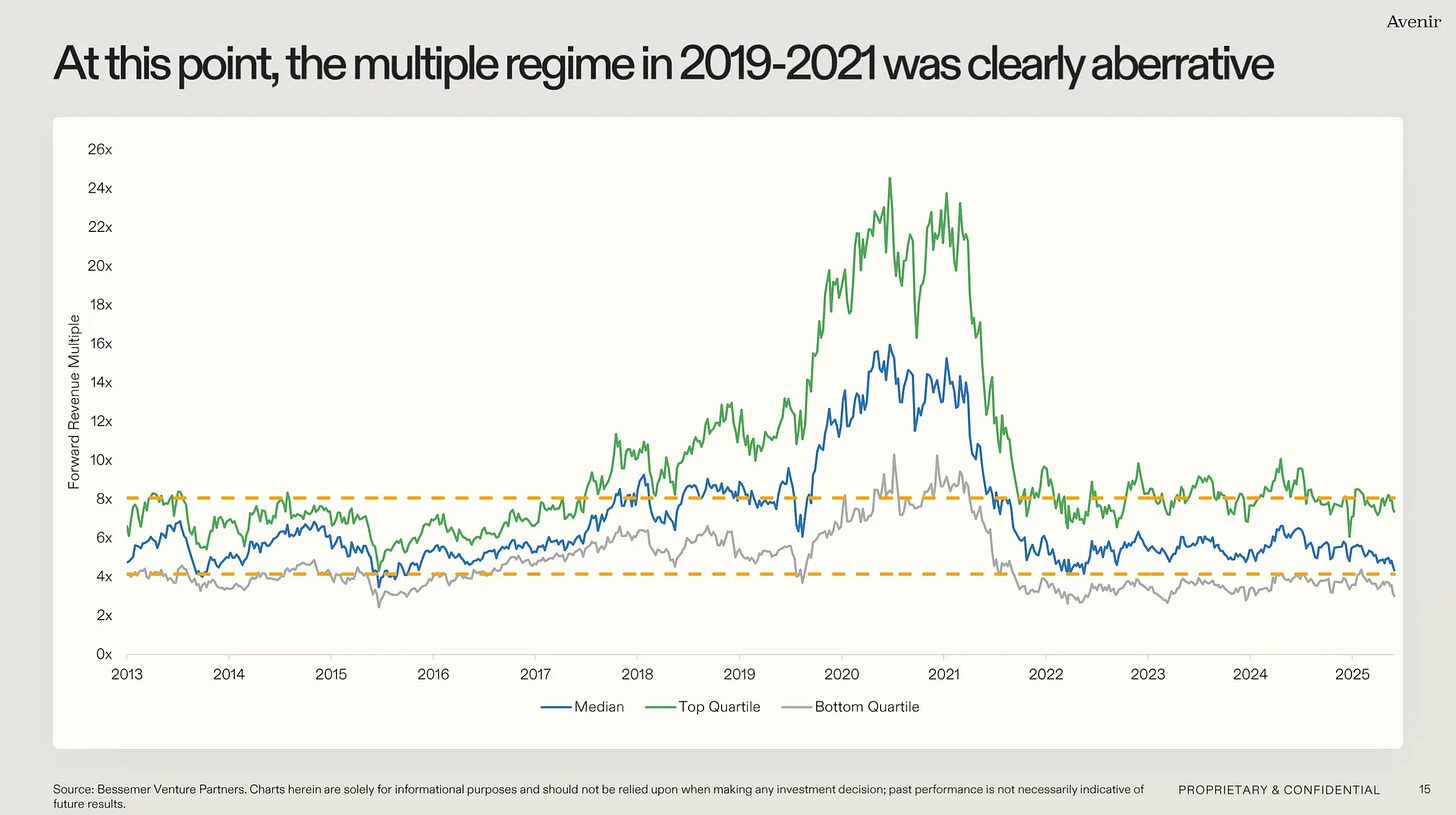

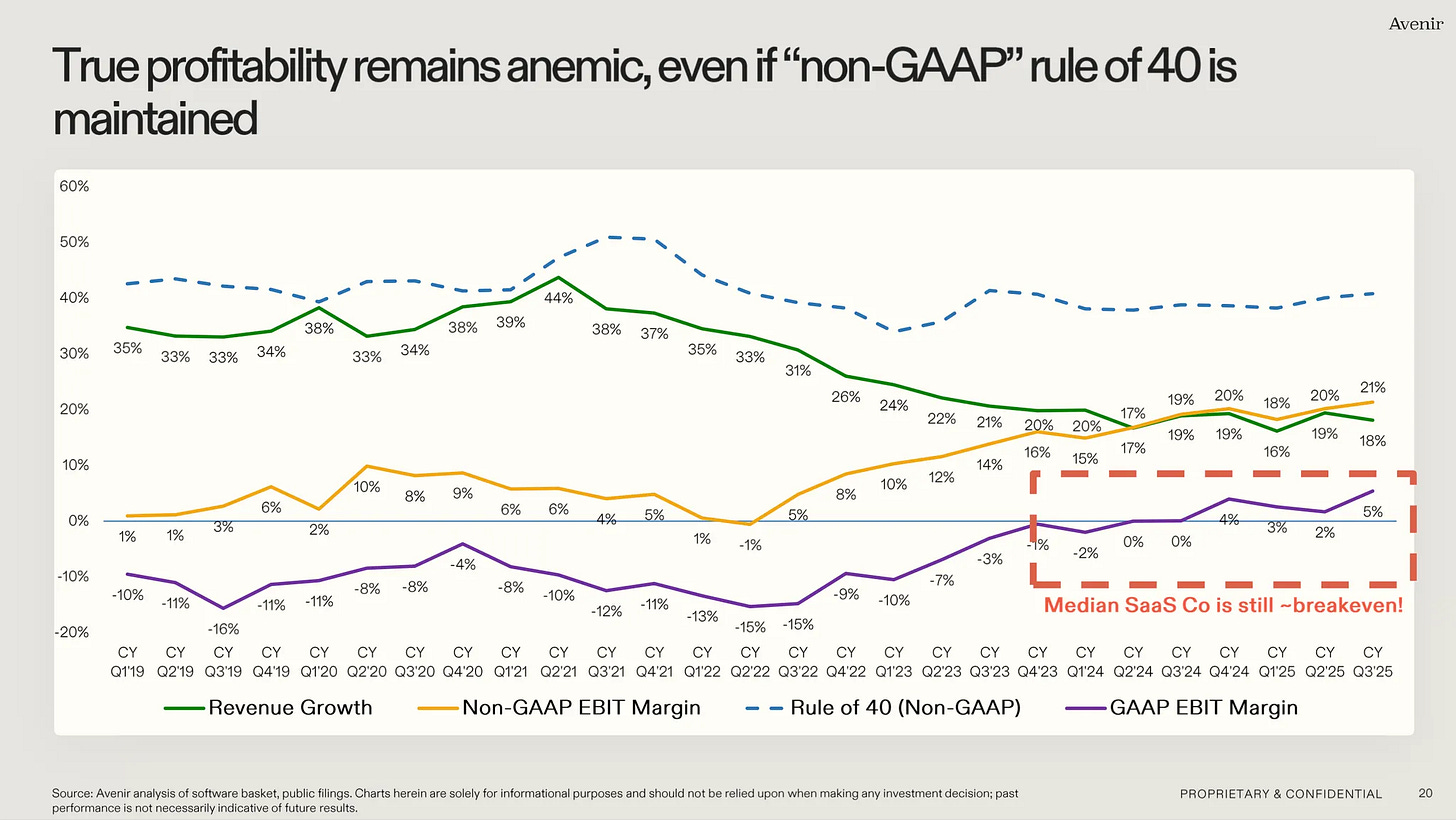

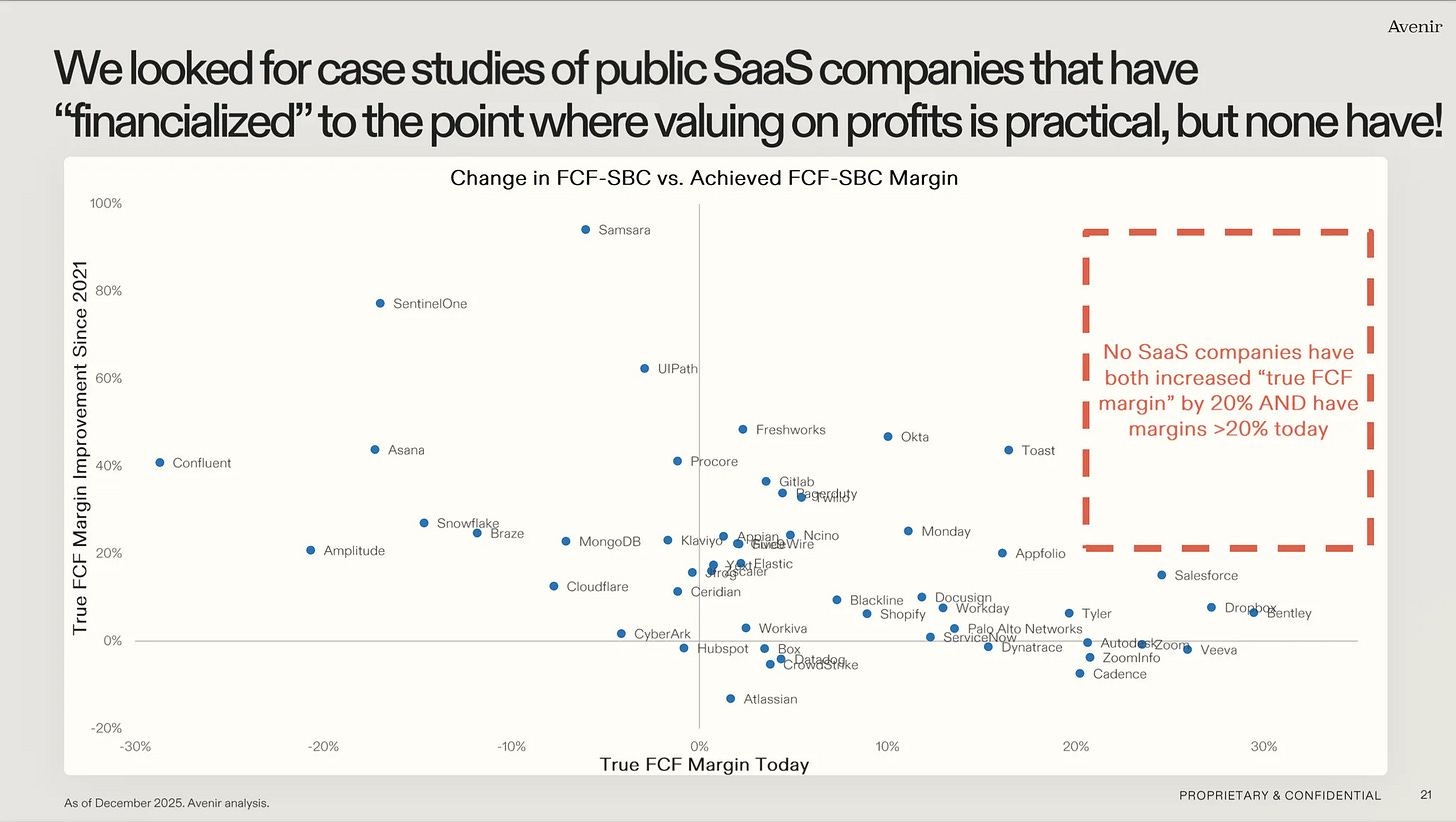

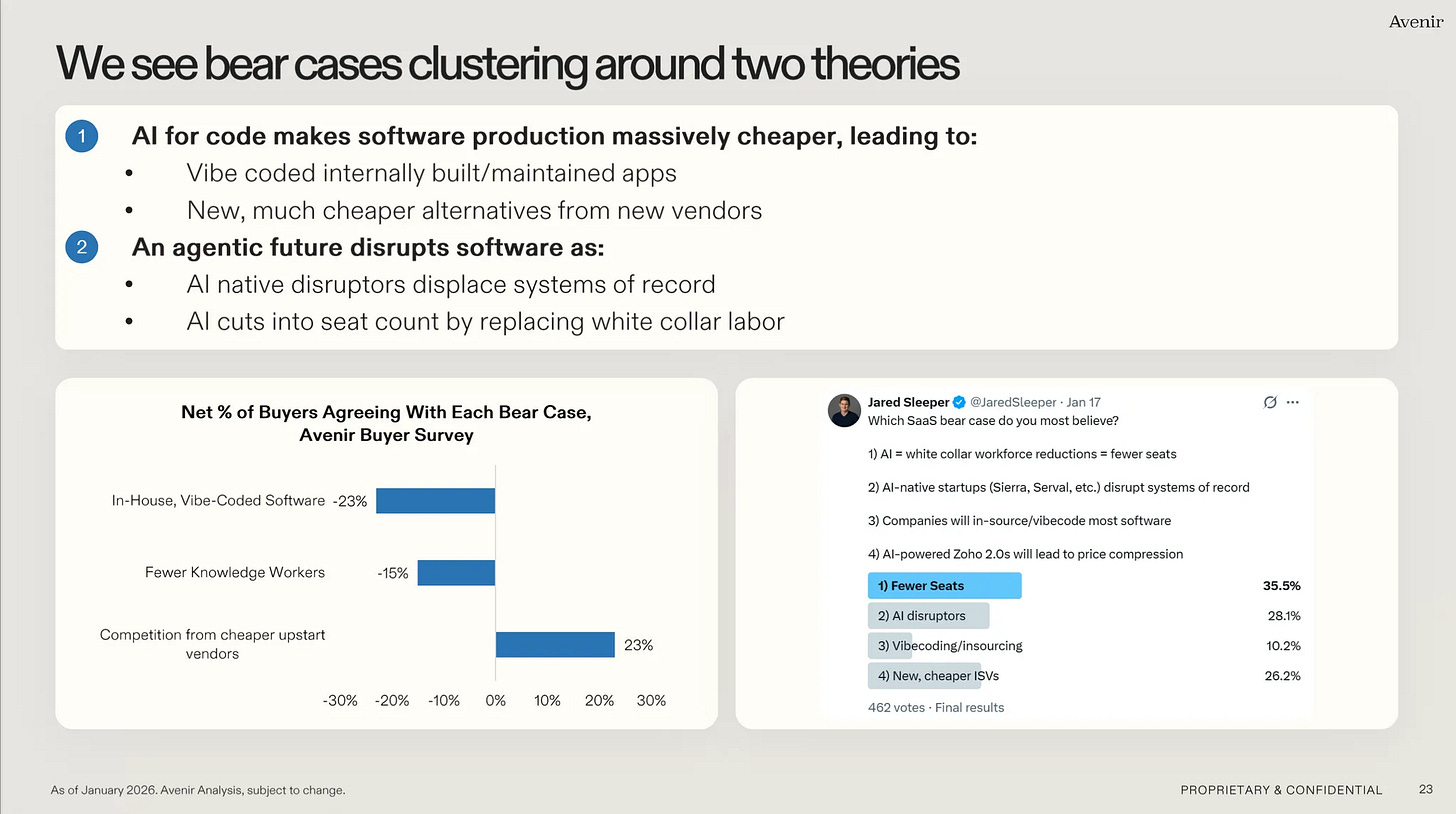

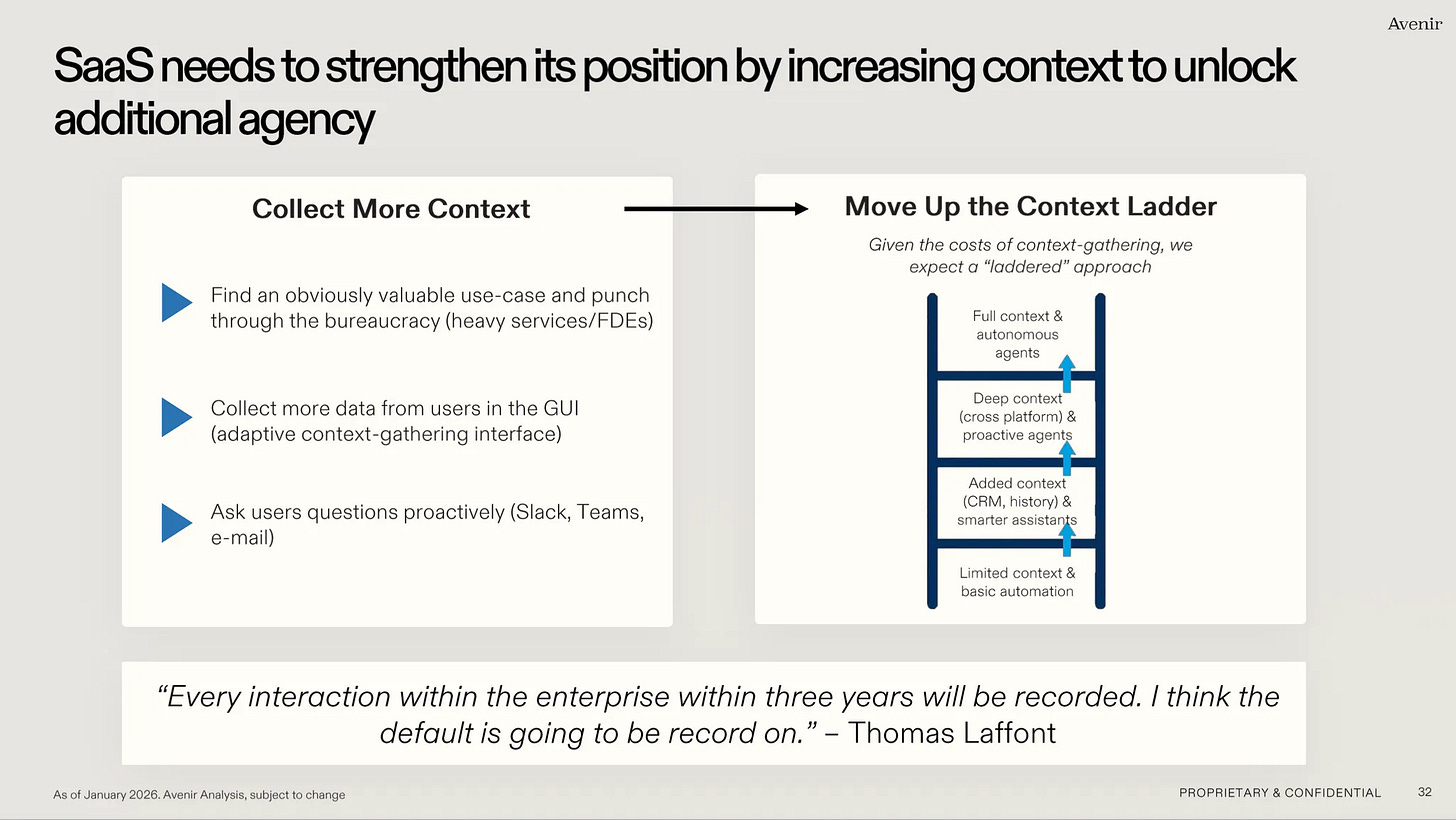

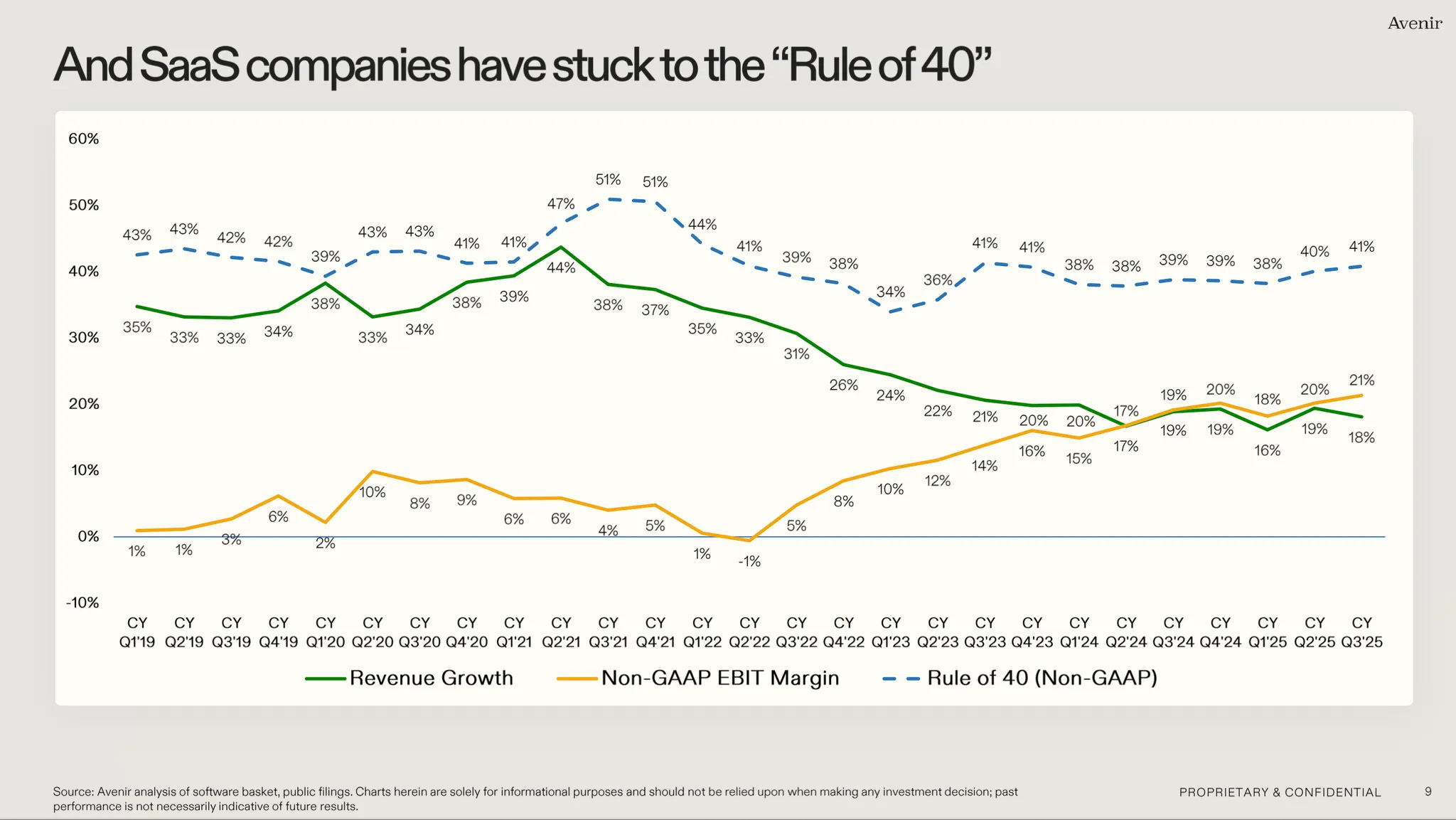

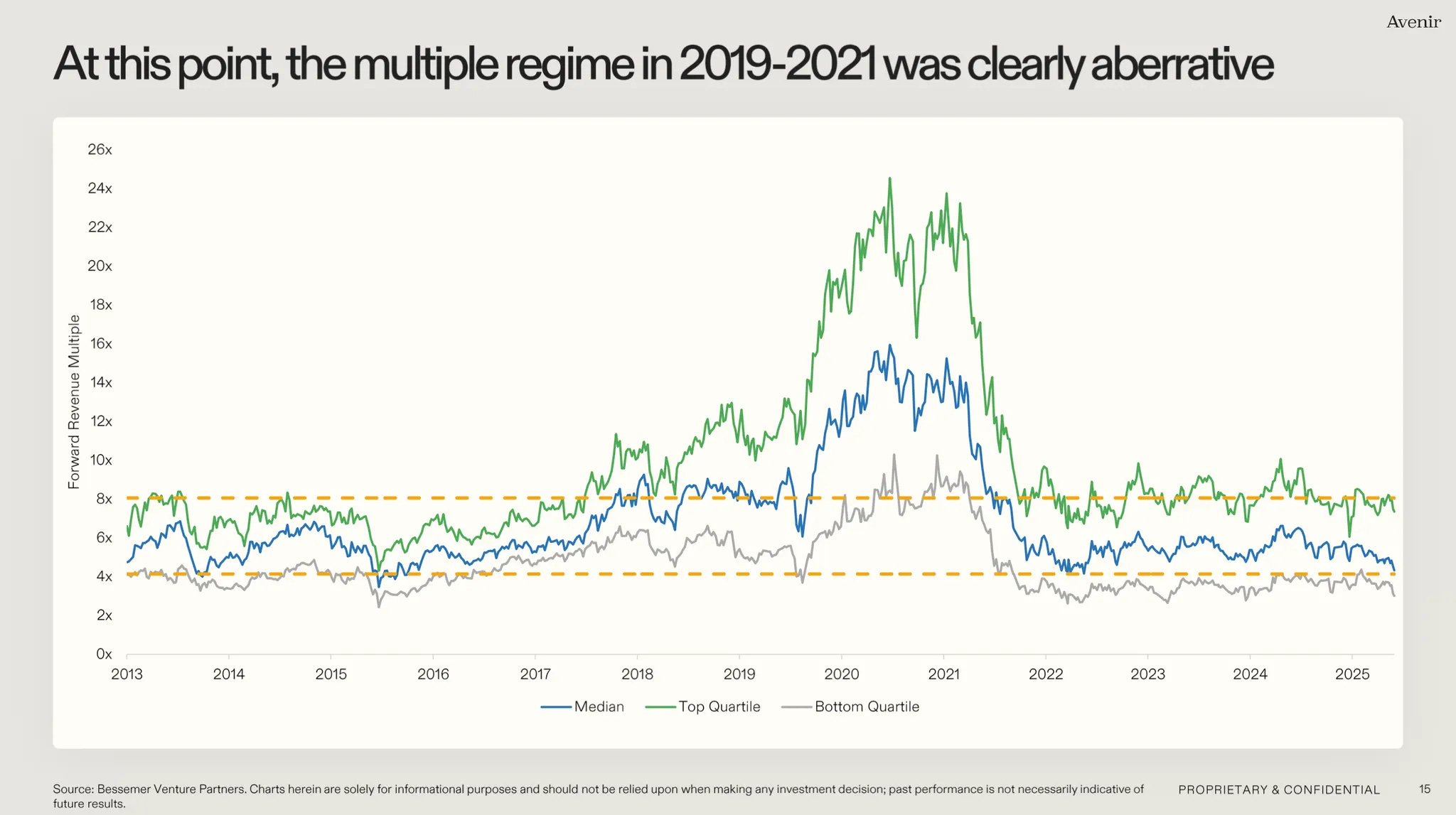

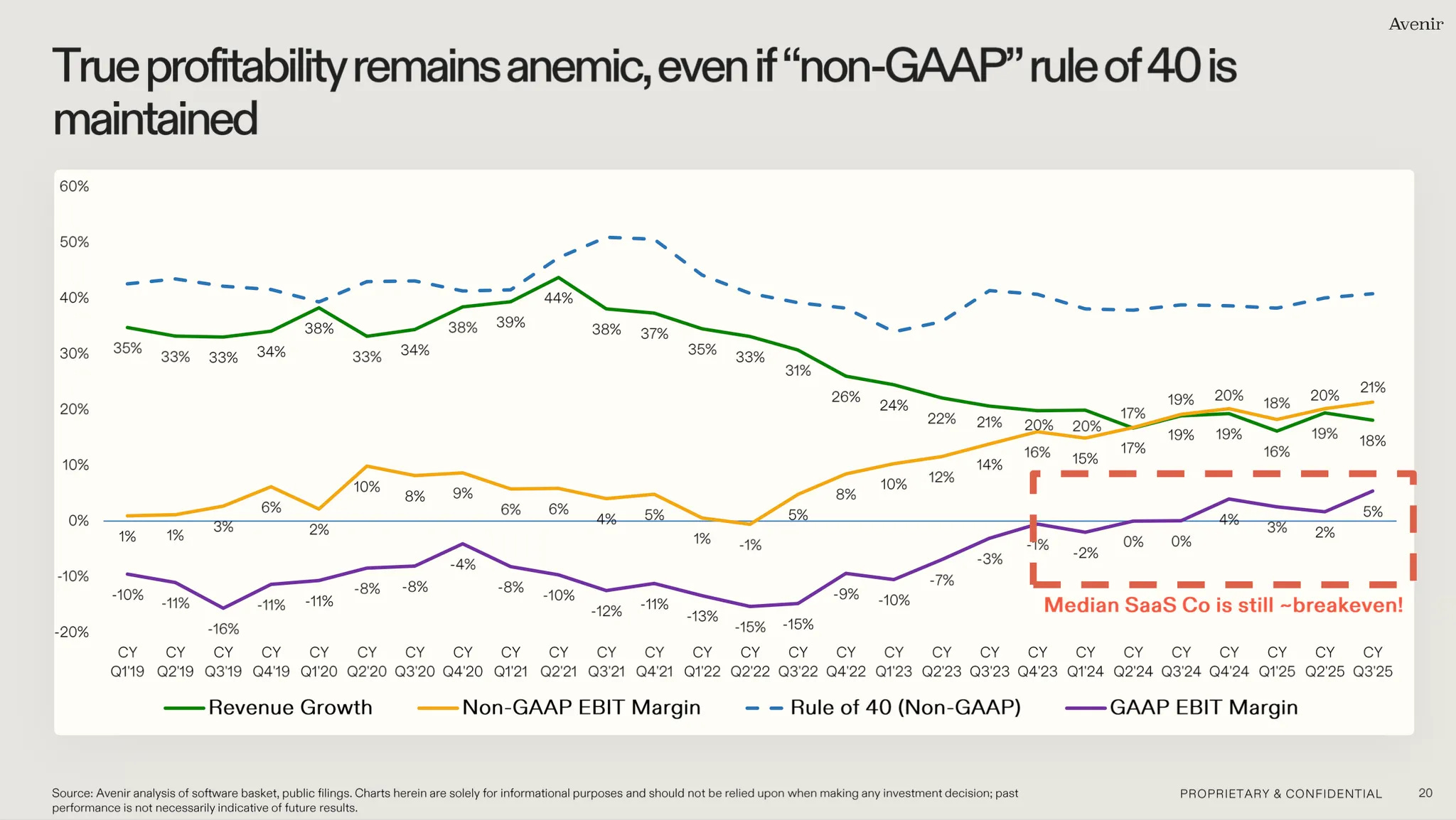

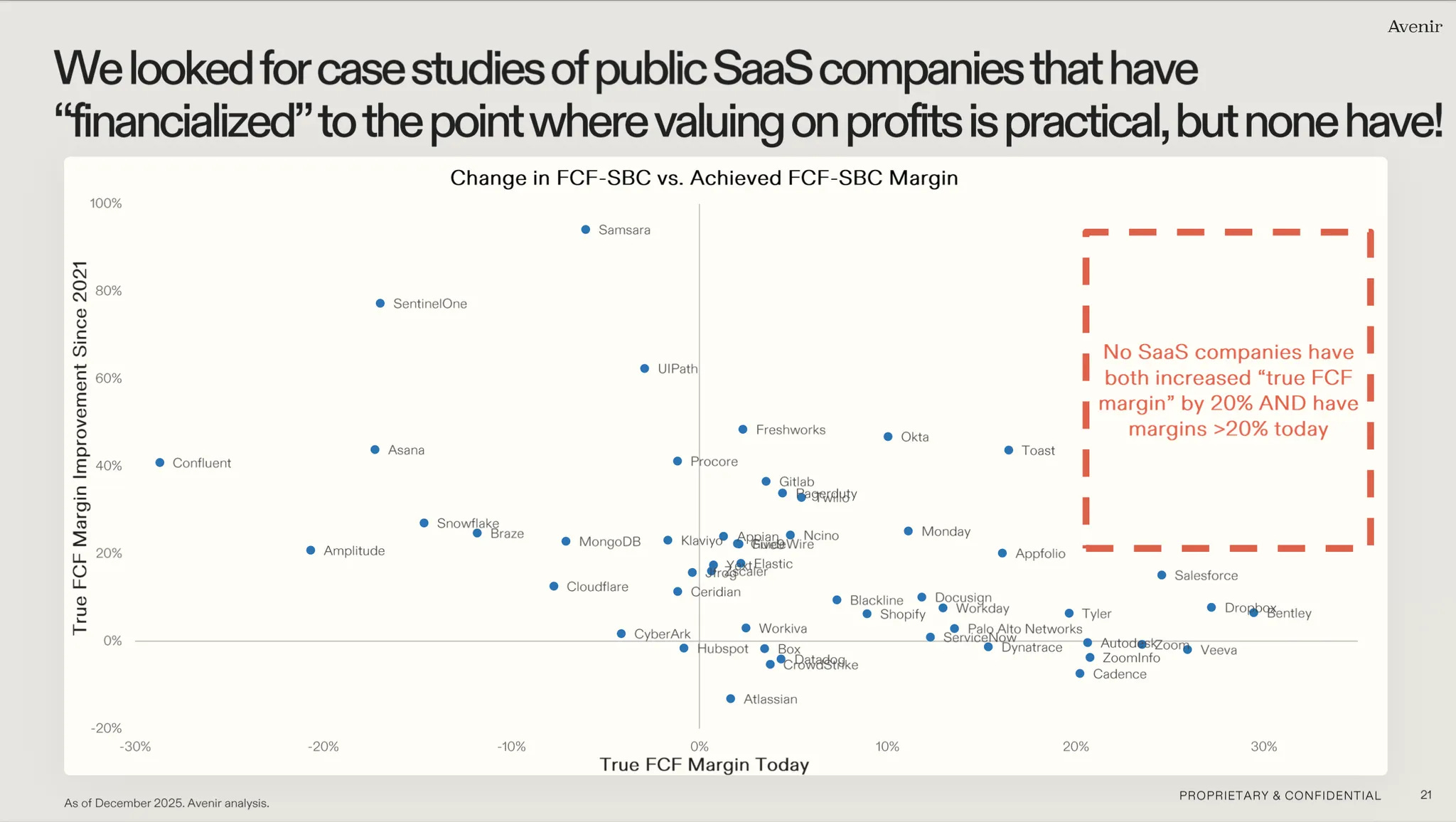

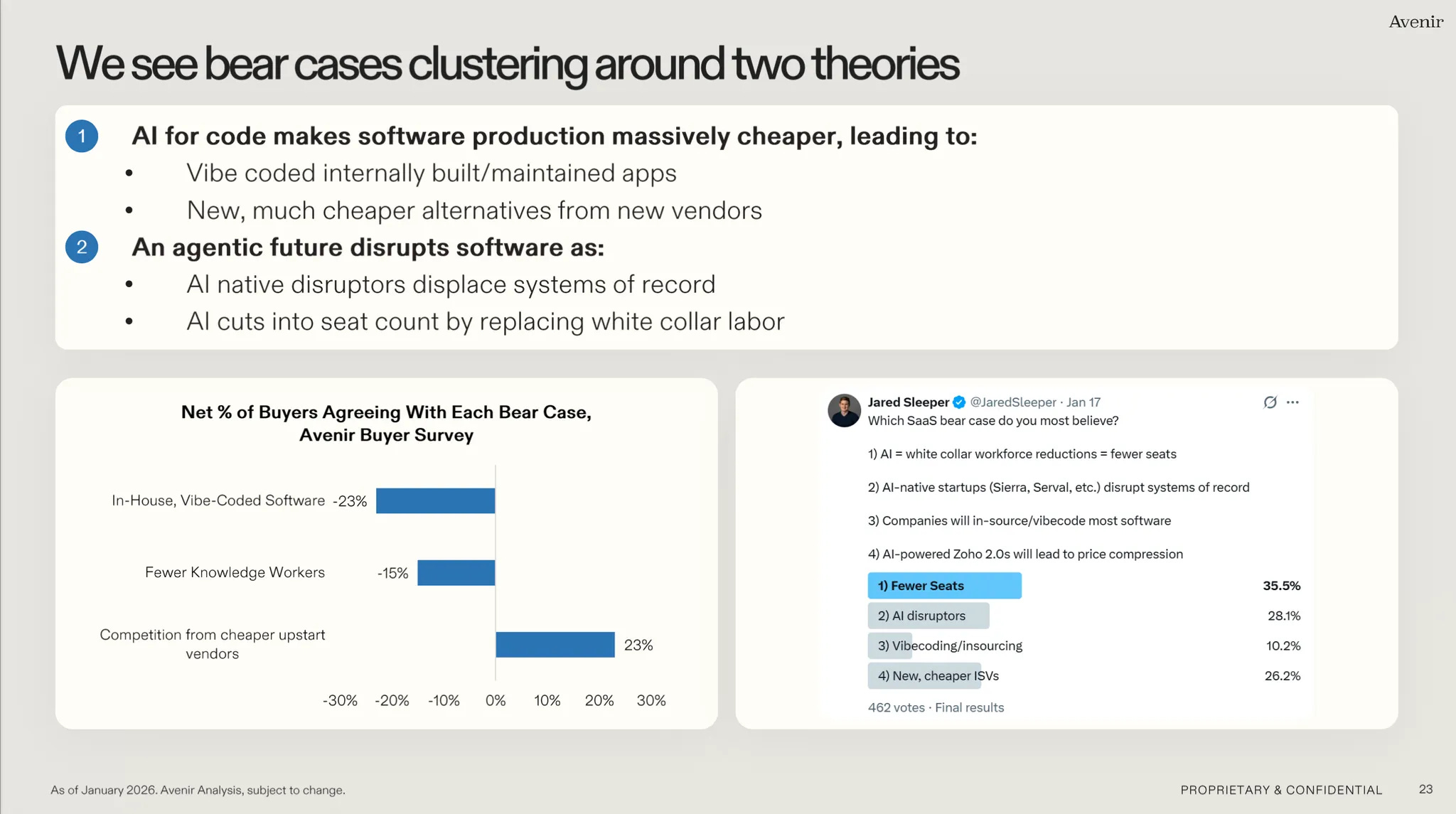

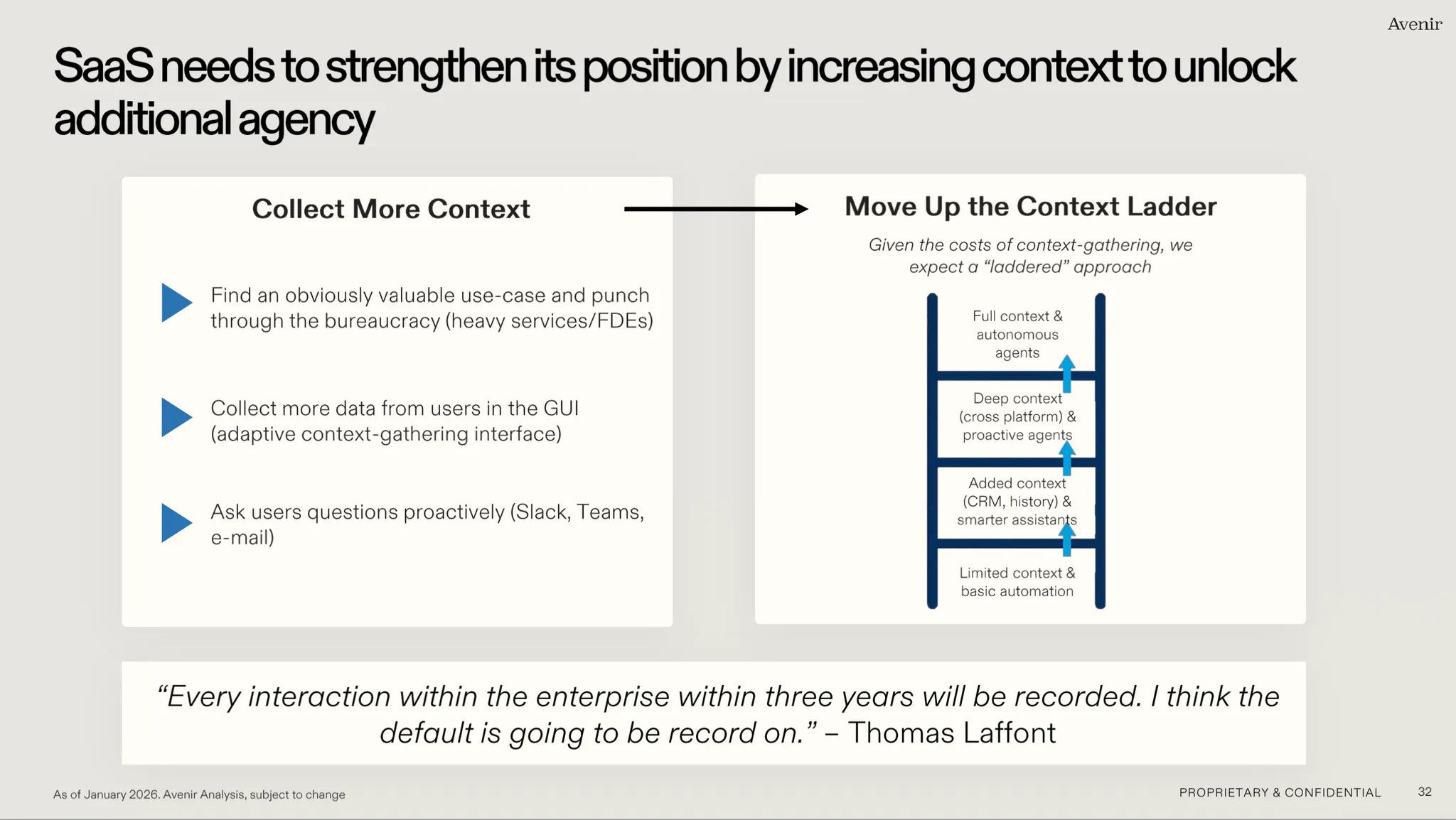

Jared Sleeper at Avenir shared a presentation on the future of SaaS.

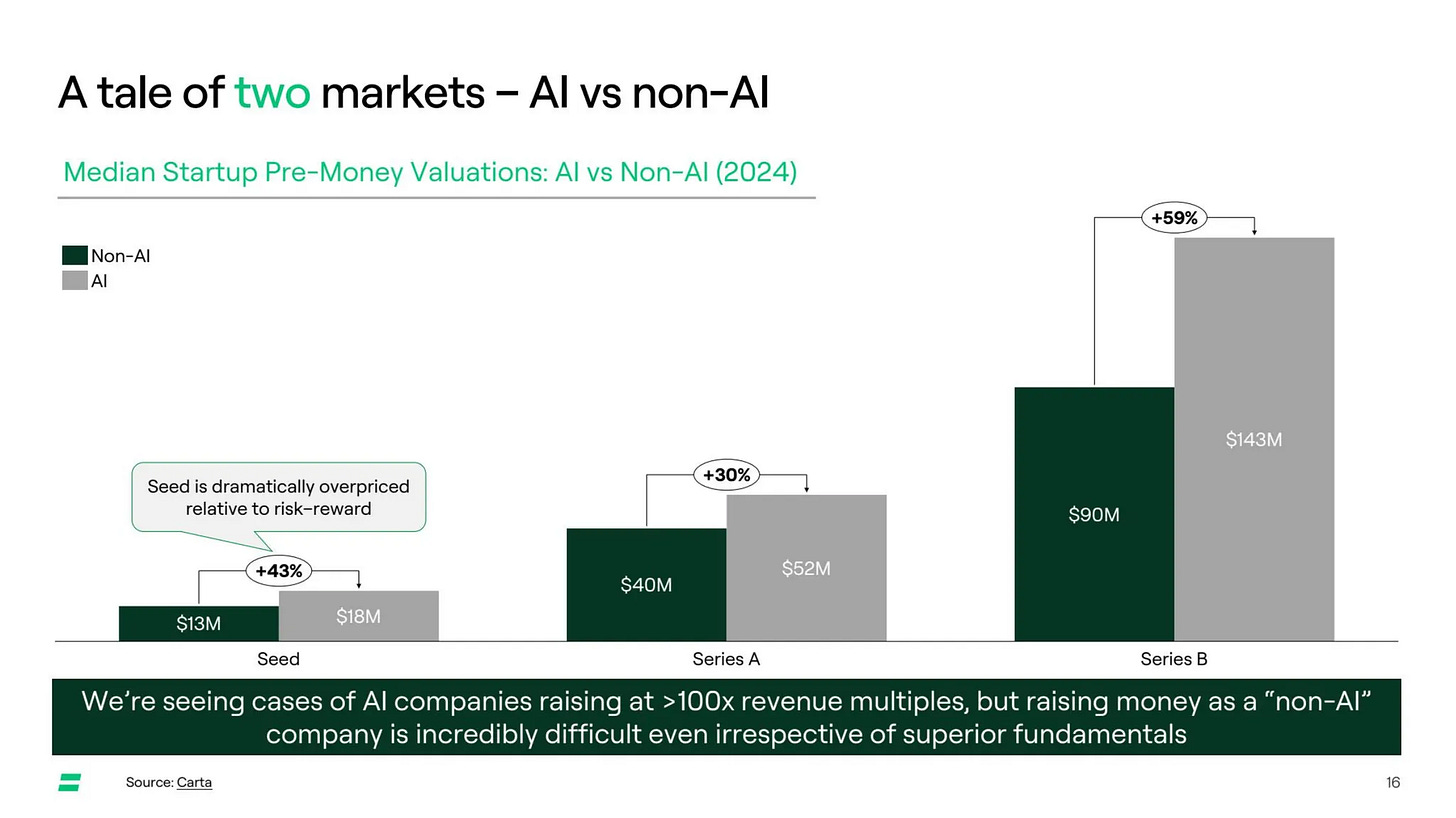

Rick Zullo at Equal Ventures published a deck on the state of the venture market. - Equal

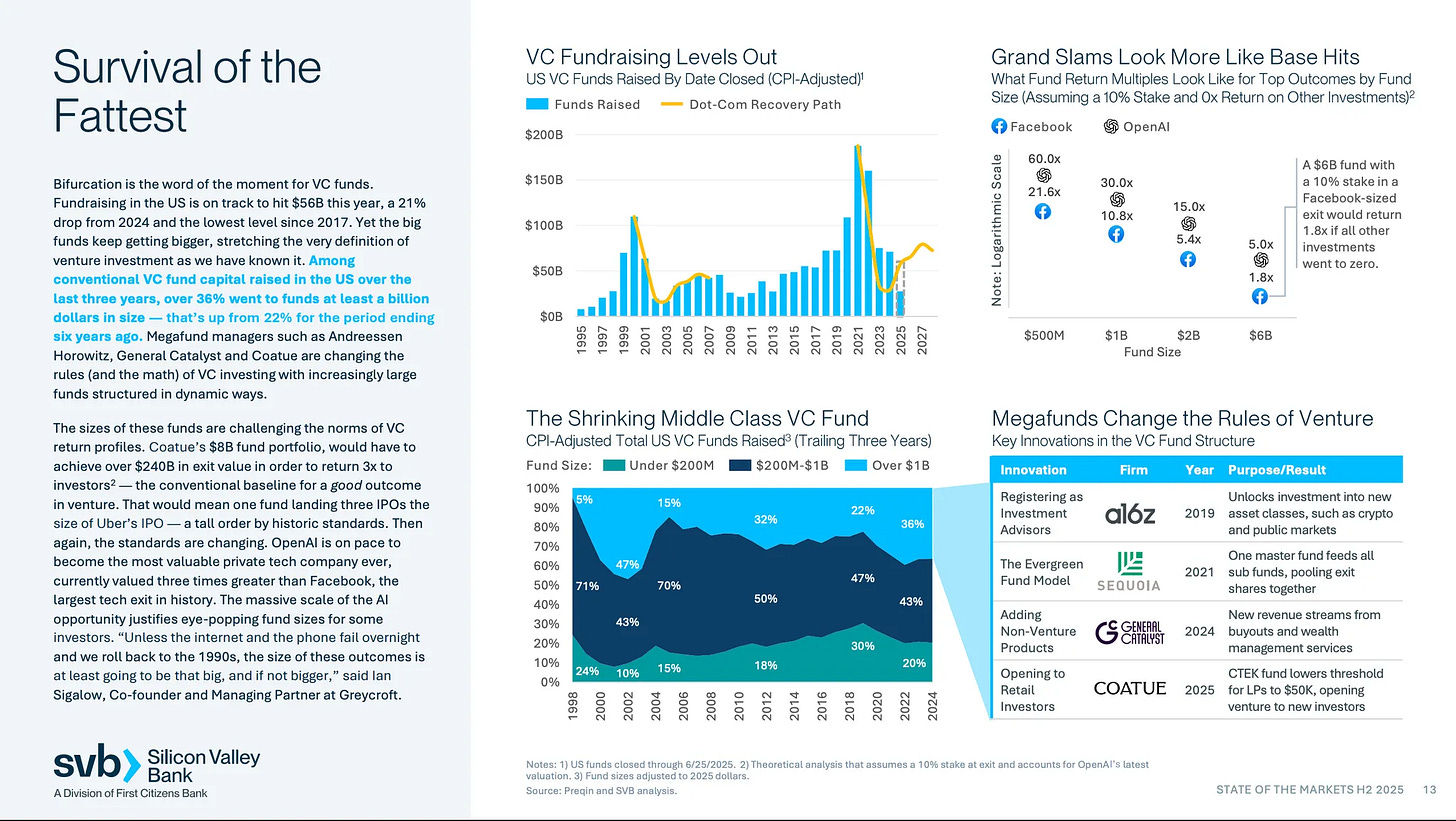

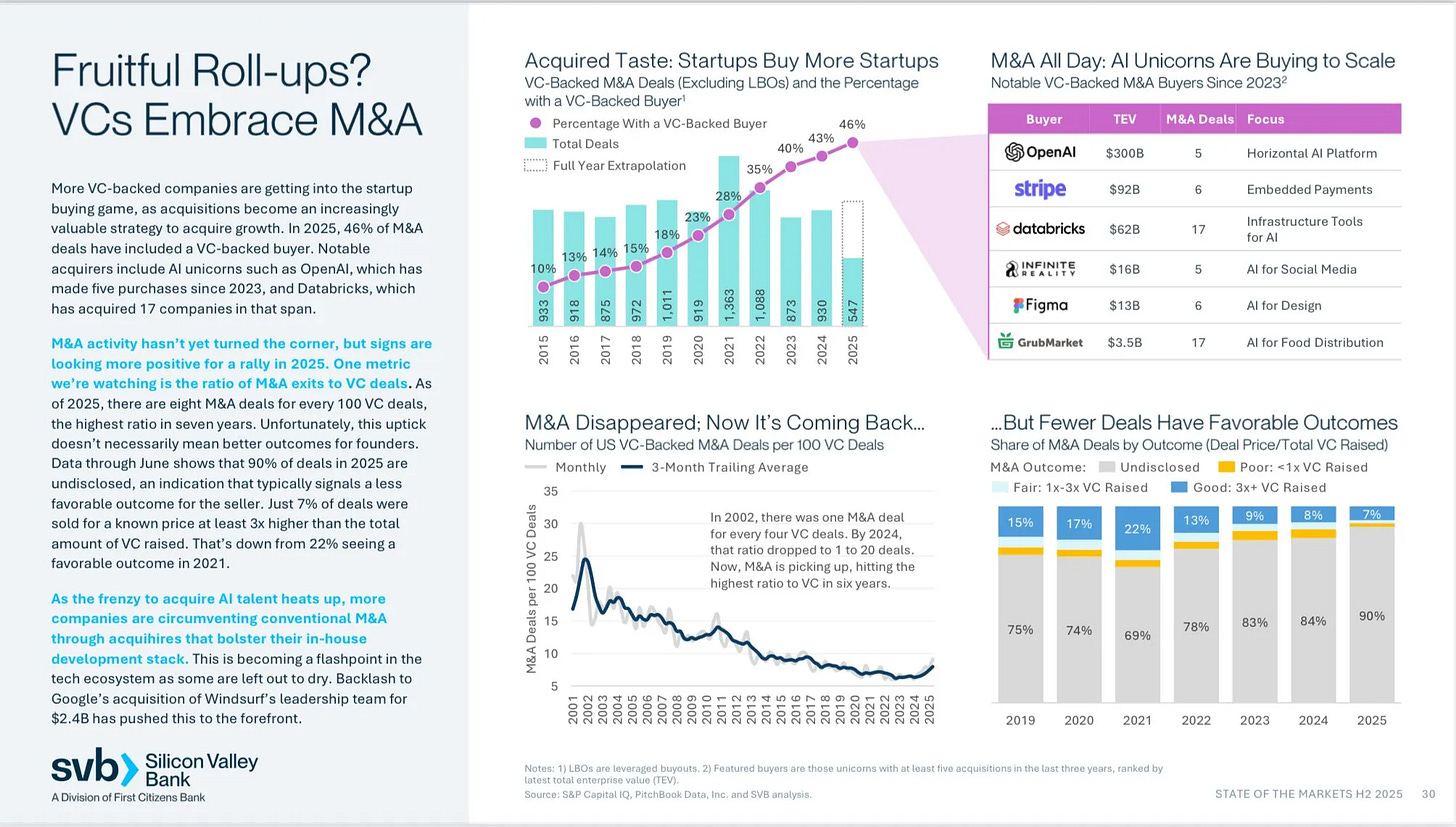

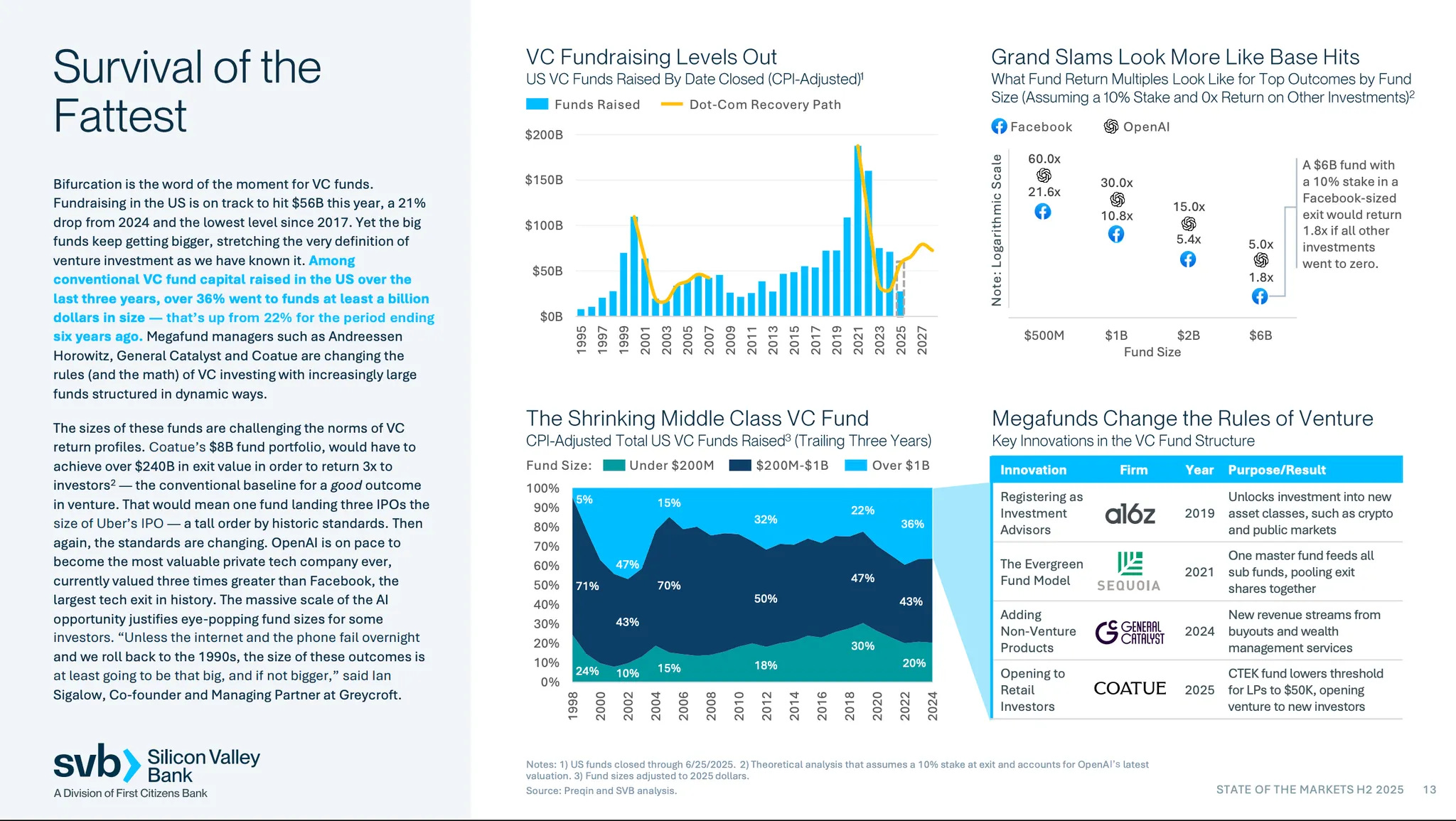

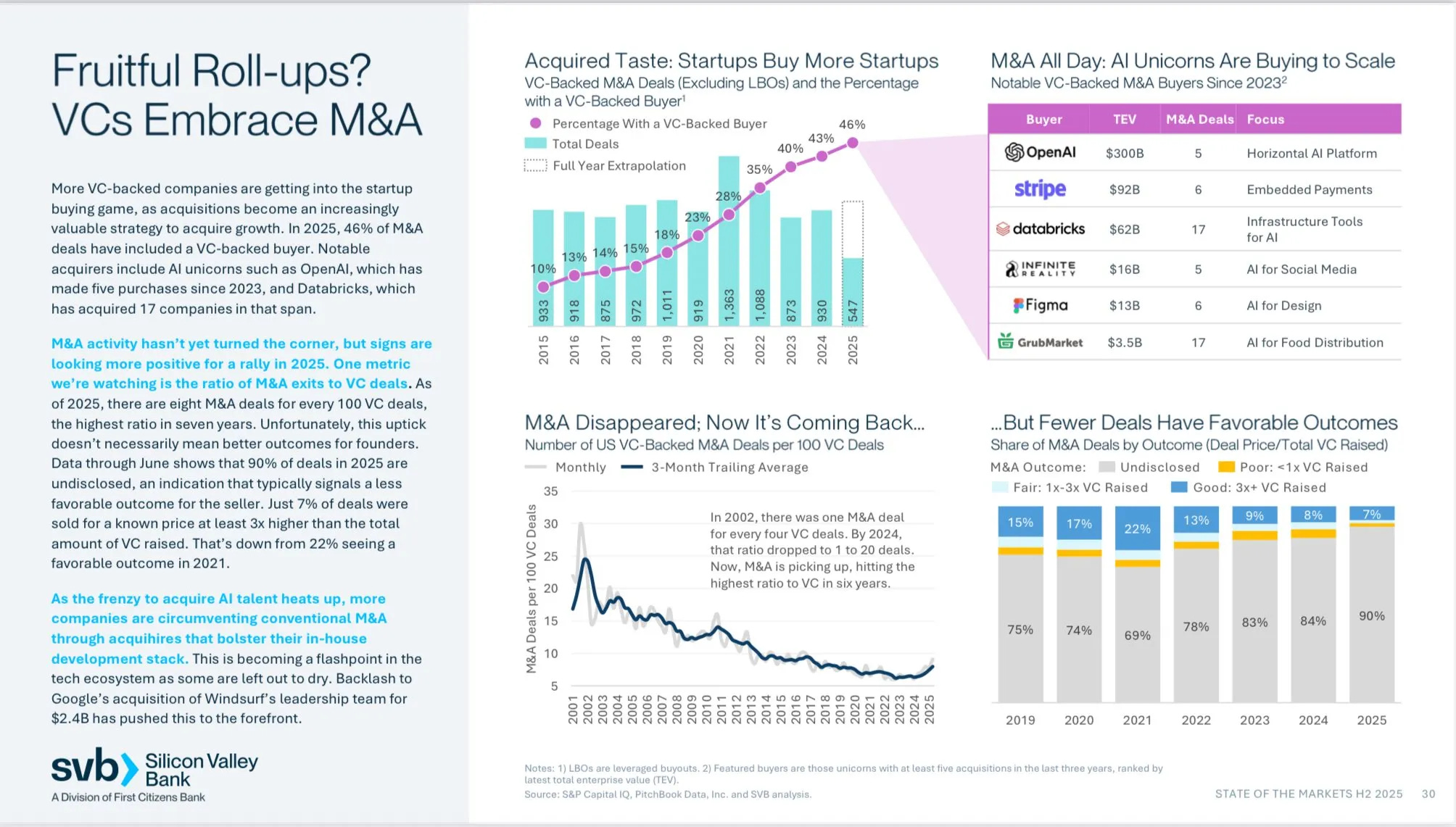

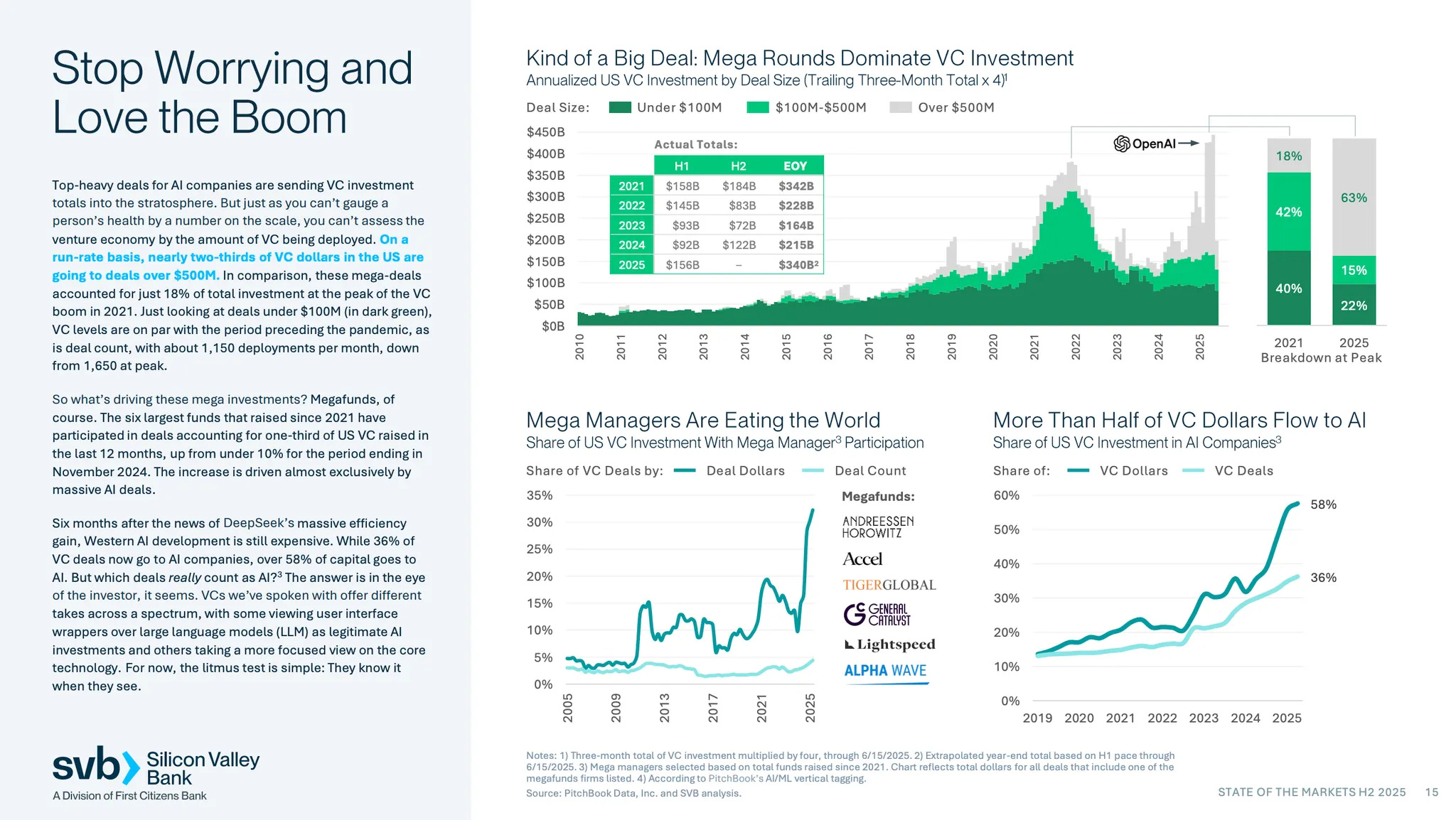

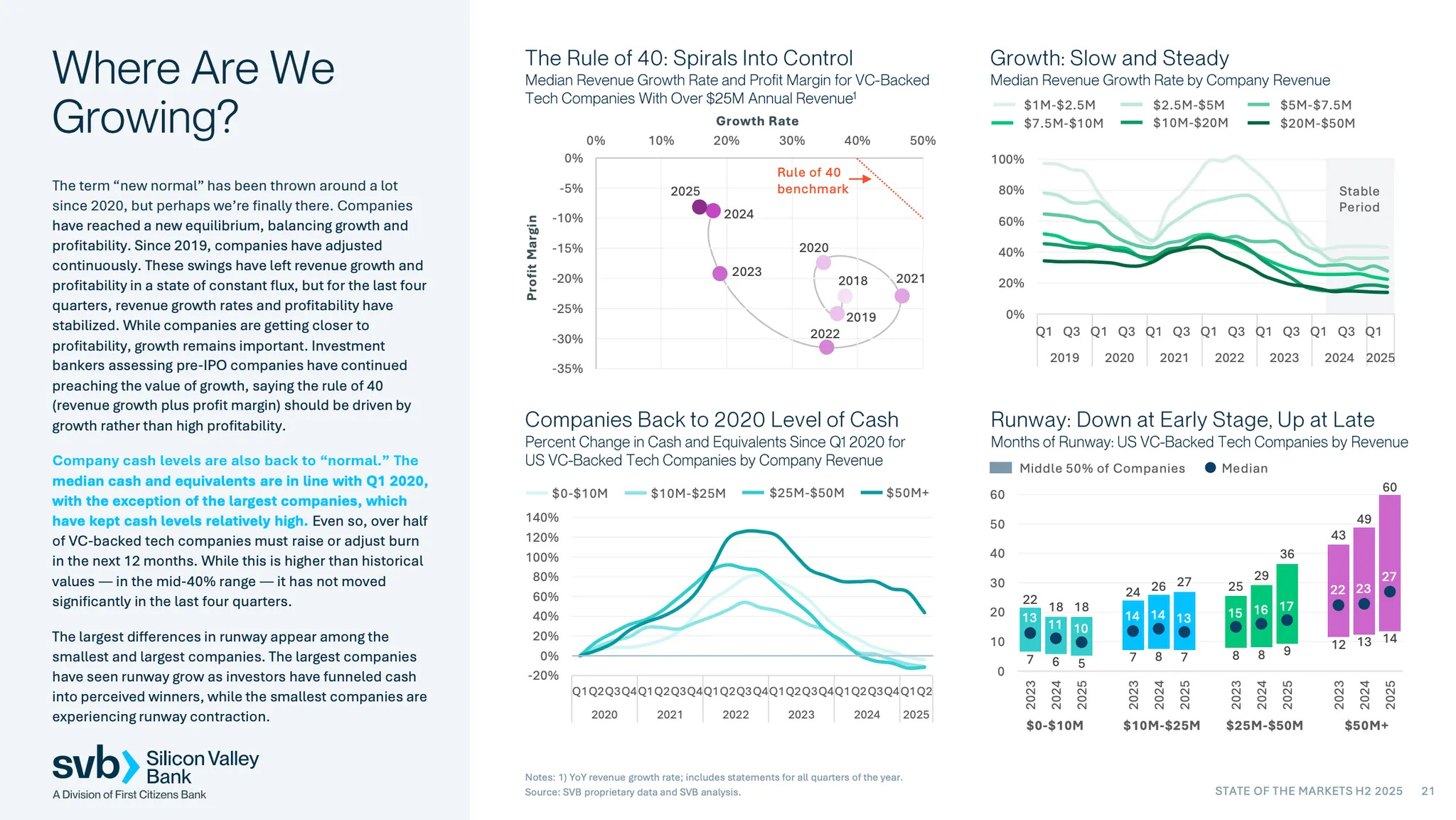

SVB published a H2-2025’s State of the Markets. - SVB

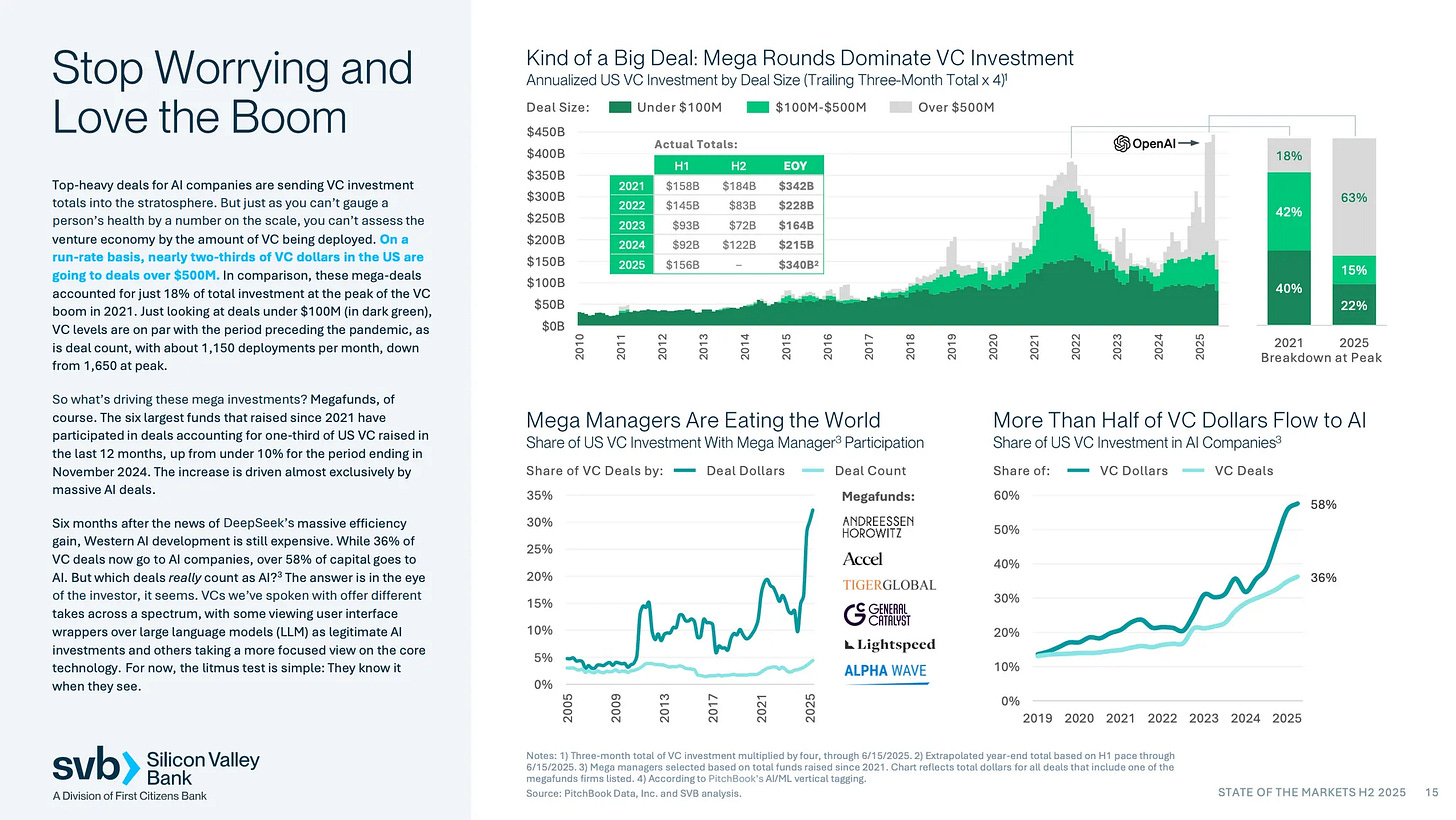

36% of capital raised by VCs in the US went to $1bn+ funds.

36% of deals and 58% of capital deployed in 2025 in the US went in AI.

2/3 of venture dollars in the US went to $500m deals (vs. 18% at the peak of the bubble in 2021)

Spencer Peterson at Coatue shared learnings on growth investing. - Spencer Peterson

“The Path to Platform: the greatest source of privates alpha is identifying a platform company before it’s a platform. Every investment thesis is really just “the path to this being a Platform”... what’s wild is how compressed the timeline has become: platforms used to take a decade to emerge, but now signals show up in just a few years (why some Series B valuations are so high!)”

“Great founders share a trait, rate of learning: the best founders are, without exception, learning machines. They just keep getting better in a way that almost runs away from you (especially if you’re a schmuck investor like me).”

“Diversification is a tax: concentrate winners! Diversification is not your friend: this is a known fact in venture.”

“Decision Quality > everything: for all the hustle culture, busy calendars and “value add resources” at funds .. all the leverage is in decision quality. Great decisions compound. Avoiding losing compounds. It feels bad (but is correct) to say 95-99% of “passes” don’t matter in power law investing. Know when you’re around a BFI and get the decisions right!”

AI venture funding is surging but is highly concentrated: a reduced number of funds are pouring cash in a reduced number of companies perceived as AI winners. - FT

“There is little doubt that billions of dollars of investment in AI start-ups will be vaporised over the next few years. But that’s all part of the plan. The venture capital industry’s standard operating procedure is to chuck capital at promising new technologies and see what sticks.”

“In particular, investors piled into AI companies, which attracted 48% of total venture funding with the adjacent field of robotics drawing record financing, too.”

“The latest investment frenzy differs from previous funding waves in being so heavily concentrated on one sector. “

“The top 10 most valuable private companies, including OpenAI, ByteDance, Anthropic and SpaceX, have been sucking up funding mega-rounds and are collectively valued at $2tn. The top 10 most active VC funds, including General Catalyst, Andreessen Horowitz, Sequoia and Accel, are heavily focused on AI.”

“One other significant difference today is how the Big Tech companies are reshaping the start-up universe given their overlapping roles as suppliers, customers, competitors, funders and acquirers.”

Fortune published a great piece on Mamoon Hamid’s push to return Kleiner Perkins to the top of the venture industry. - Fortune

“Hamid had helped build one of Silicon Valley’s buzziest new VC firms, Social Capital, leading a string of wins including investments in Box (one of 2015’s biggest IPOs) and Slack (at the time valued at $5.1 billion). Kleiner Perkins on the other hand, was widely viewed as an institution in decline.”

“Kleiner Perkins was not just any firm to Hamid. The firm had been the inspiration that led him to a career in venture capital, and John Doerr, the legendary Kleiner rainmaker who made early bets on Google, Amazon, and Netscape, had been his role model.”

““What came across to me about KP was this combination of having this great brand, but having a lot of the energy and the hunger of being a startup firm—nothing was taken for granted,” says Parker Conrad, cofounder and CEO of Rippling, which Kleiner backed in 2019.

“The new Kleiner is smaller and more focused than its previous incarnation—more boutique than mega. Now, as the AI boom inflates funding rounds and valuations to nosebleed levels, and raises the stakes for the VCs betting on startups, Hamid has the chance to show whether the firm he’s rebuilding can be truly competitive and define Silicon Valley’s next big chapter.”

“Hamid and Fushman quickly sought to reboot the Kleiner culture, instituting firm-wide offsites for the first time (including the front desk); nixing cubicles in favor of an open office plan that promoted collaboration; and introducing a mission: “Be the first call for founders who want to make history, and partner with them as company builders in pursuit of that goal.””

“Hamid and Fushman replenished the ranks with new blood, even as the firm has made a point to stay small (there are currently five partners at Kleiner versus the 10 there were right before Hamid joined).”

“In his first deal at Kleiner, Hamid led Figma’s $25 million Series B. And last year, Figma went public at a $19.3 billion valuation, in one of the highest-profile IPOs of the year. Even as Figma’s stock has taken a hit, at the current price the multiple from the initial investment is roughly 90x, and is right up there with Kleiner’s best-ever returns, including Amazon, Google, and Juniper, the firm says. Not including Figma—or any of the firm’s other promising AI-era investments like Vlad Tenev’s Harmonic, Ilya Sutskever’s Safe Superintelligence, Synthesia, Glean, Anthropic, and Applied Intuition—Kleiner has now returned $13 billion to its LPs since 2018.”

“The firm is also now invested in some of the AI era’s brightest stars, from AI medicine startup OpenEvidence, valued at $12 billion, to legal AI company Harvey, valued at $8 billion.”

“The rumored new fund is expected to be slightly larger than Kleiner’s last set of funds in 2024, which included the $825 million KP21 fund focused on early-stage investments and the $1.2 billion KP Select III, aimed at “high inflection deals” (basically, follow-ons and deals with startups Kleiner has built relationships with).“

““We’d rather stay small than have more people who dilute the brand out there,” he says on the topic of expanding the firm’s ranks. The firm’s partners are “meeting with founders, and they’re providing an impression of what Kleiner Perkins is. And if that’s not the right impression, we’d rather not have it.””

Index had an amazing year in 2025 exiting $9bn in value from Wiz, Dream Games, Scale, Figma, Nexthink and Wealthfront. As a comparison, Index raised $15bn from LPs over the past 30 years. - Bloomberg

“Index has evolved into possibly the most successful venture capital firm out of Europe.”

““It’s the only European VC who managed to win in the US,” said Julien Codorniou, a former Facebook executive and partner at 20VC, a prolific startup investment firm in London. “It wasn’t a given.””

“If regulators sign off on Google’s Wiz acquisition, Index will net around $9 billion in realized gains and unsold shares from its six exits in 2025, according to public filings and a person familiar with its financials. The firm has received about $15 billion over the past 30 years from external investors.”

“Venture firms don’t typically make big changes while they’re on a hot streak. But several years ago, Index leadership decided that once investing partners reach their mid-50s, they must make room for a new generation.”

“Initially, Rimer felt competitors didn’t take his obscure European firm seriously. “Those were the days,” he said.”

“Shah, a New York-based Index partner, said the firm was gifted at “marrying Silicon Valley and Europe” by pursuing startups with transatlantic ties, like Datadog, whose French founders launched their company in the US.”

“In 2024, research company Cambridge Associates reported that the average DPI for funds begun in 2012 was 1.5 — or $1.50 returned for every dollar invested. Index’s 2012 fund, which included stakes in Figma, had a DPI of 11 as of last year, according to two people familiar with the figures. A $780 million growth fund Index raised in 2015 returned a DPI of 5.1, those people said.”

“So far, Index has taken a relatively cautious approach — the firm hasn’t funded any trendy AI coding startups and, prior to this summer, had only invested in two longshot rivals to OpenAI: Canada’s Cohere and France’s Mistral. Now, it looks to some as if the firm is playing catch-up. Achadjian, Mignot and Shah all recently led investments into early AI startups. In September, Index joined a financing round for Anthropic at a $183 billion valuation, a deal that gives it exposure to a leading AI developer but isn’t likely to yield an 11x return.”

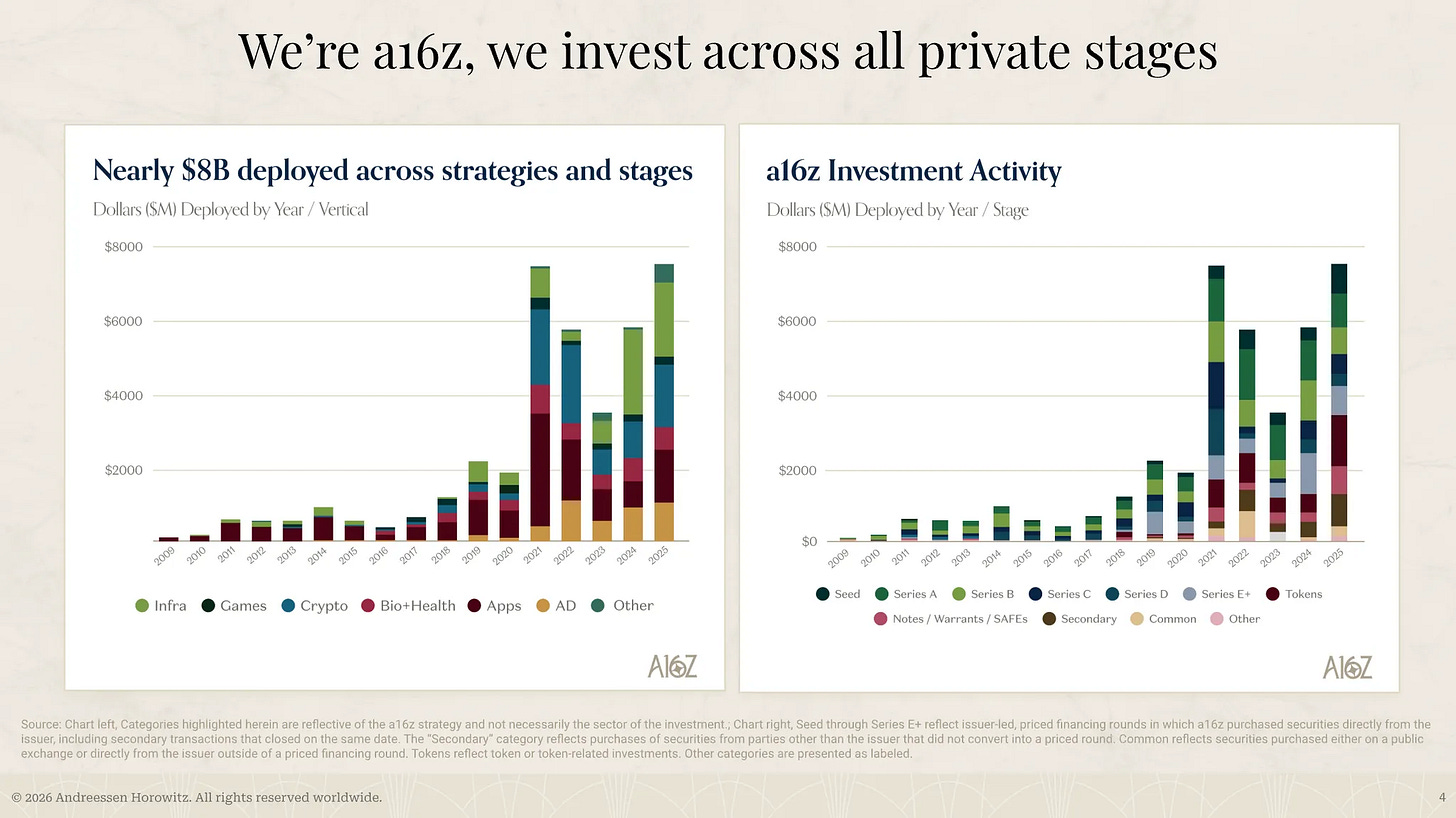

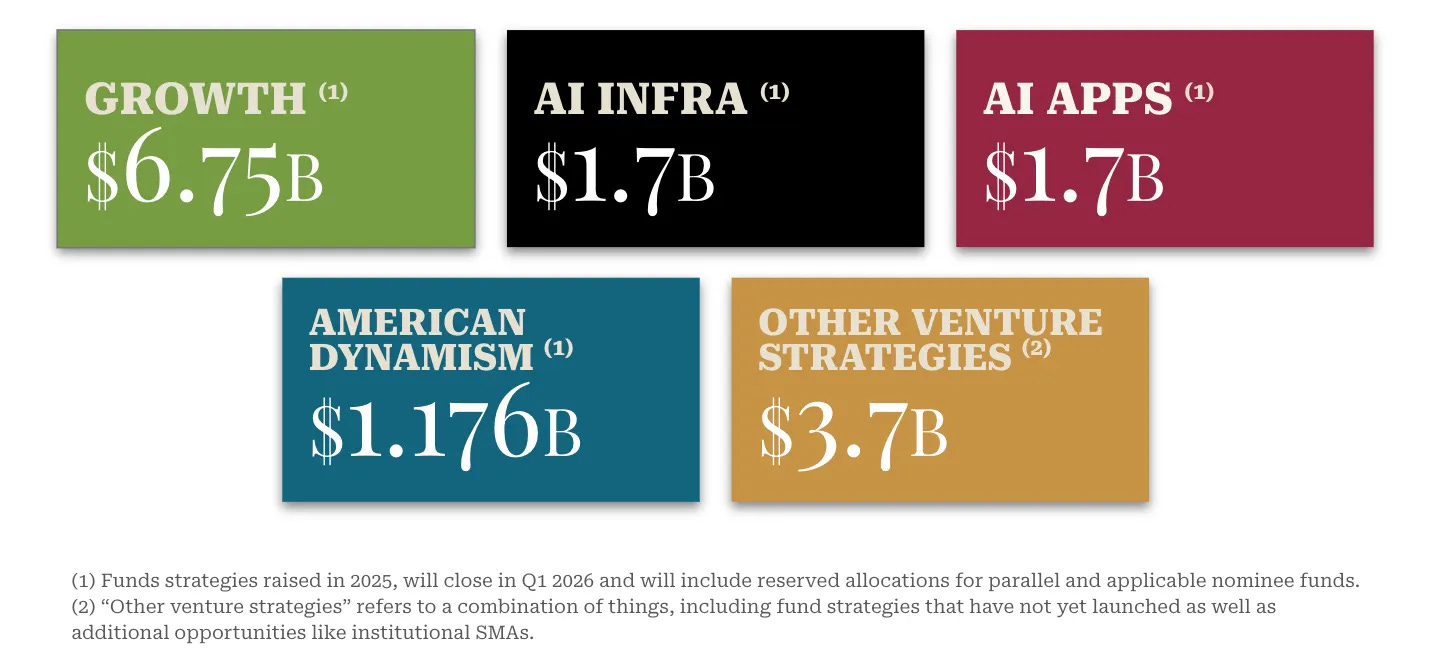

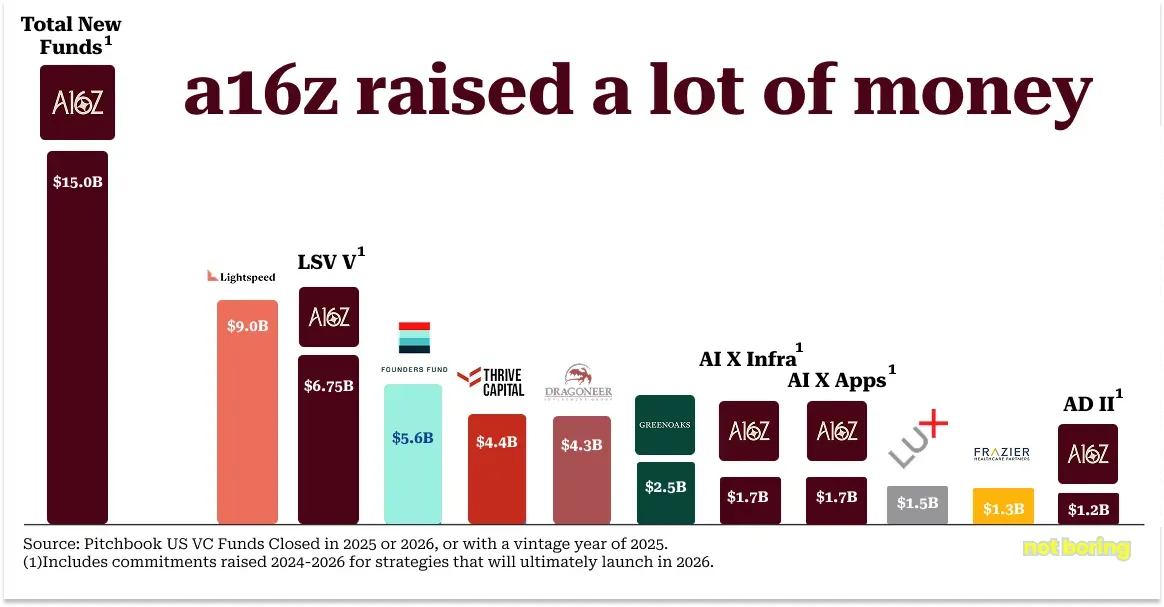

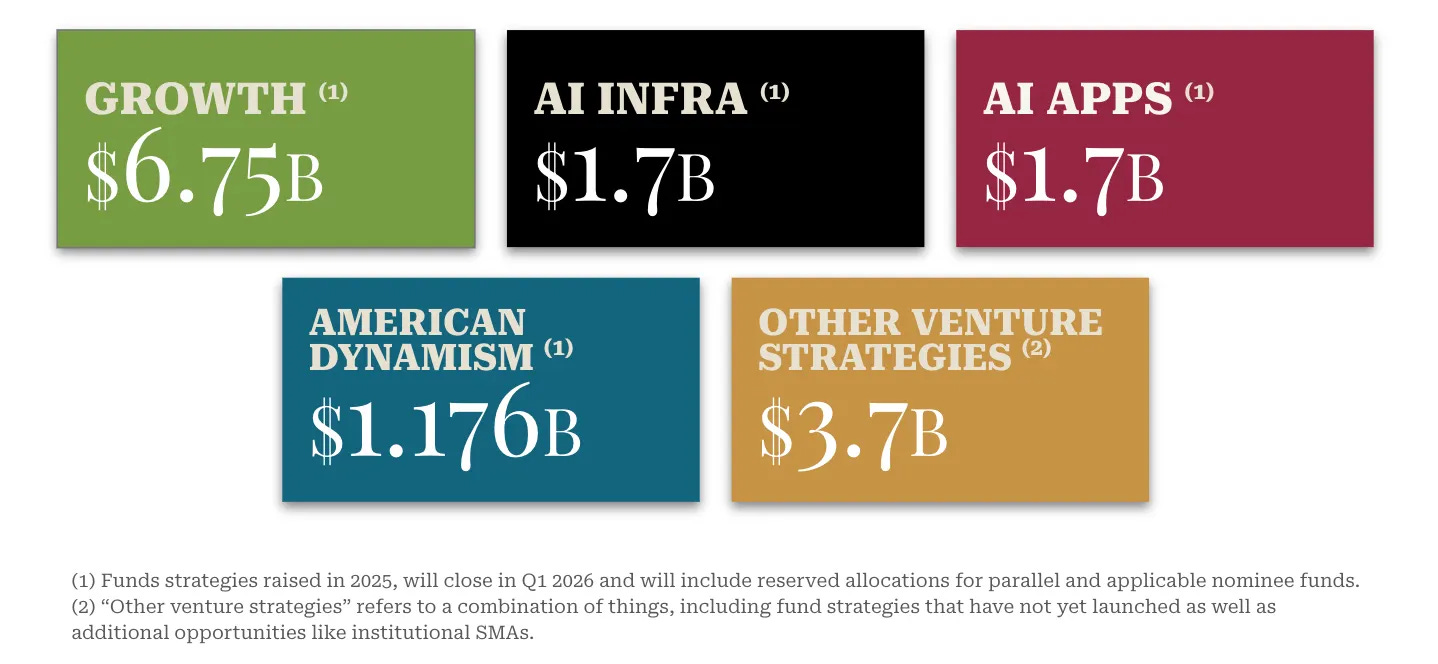

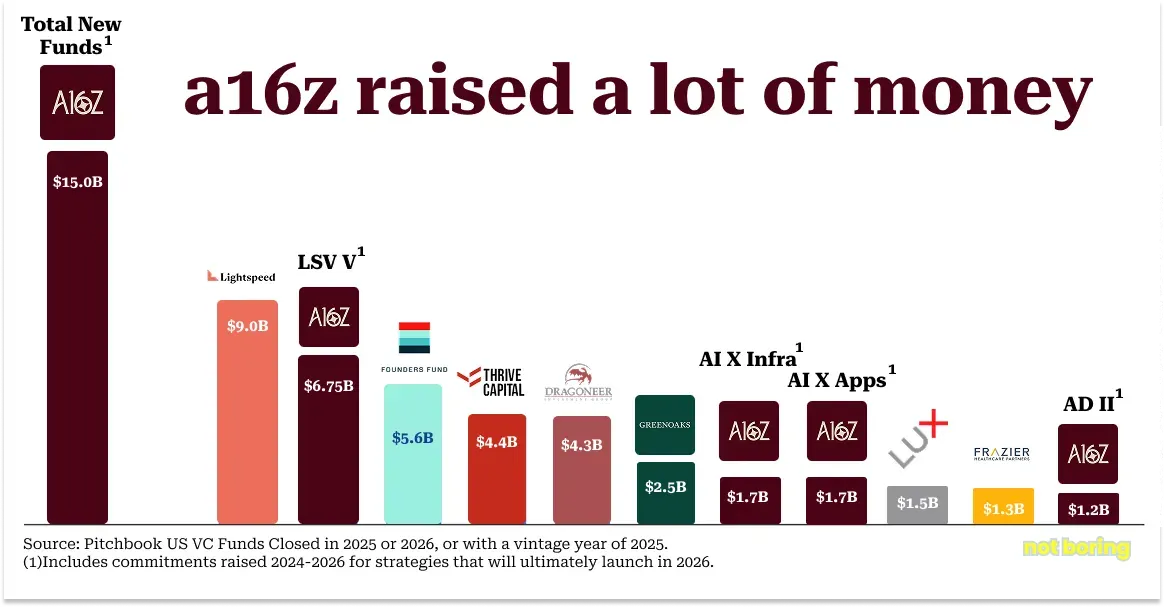

a16z raised $15bn in capital for its different strategies: $1.2bn for American Dynamism, $1.7bn for apps, $700m for bio & healthcare, $1.7bn for infrastructure, $6.8bn for growth and $3bn for other venture strategies. a16z raised 18% of the total amount raised by GPs in the US. - a16z, Not Boring

“As the American leader in Venture Capital, the fate of new technology in the United States rests partly on our shoulders. Our mission is ensuring that America wins the next 100 years of technology.”

“In the worst VC fundraising market in five years, a16z accounted for over 18% of all US VC funds raised in 2025. a16z raised more than the next two funds - Lightspeed ($9B) and Founders Fund ($5.6B) - raised in 2025, combined.”

“Today, across all their funds, a16z is an investor in 10 of the top 15 private companies by valuation: OpenAI, SpaceX, xAI, Databricks, Stripe, Revolut, Waymo, Wiz, SSI, and Anduril.”

“Its AI portfolio includes 44% of all AI unicorn enterprise value, also more than any firm.”

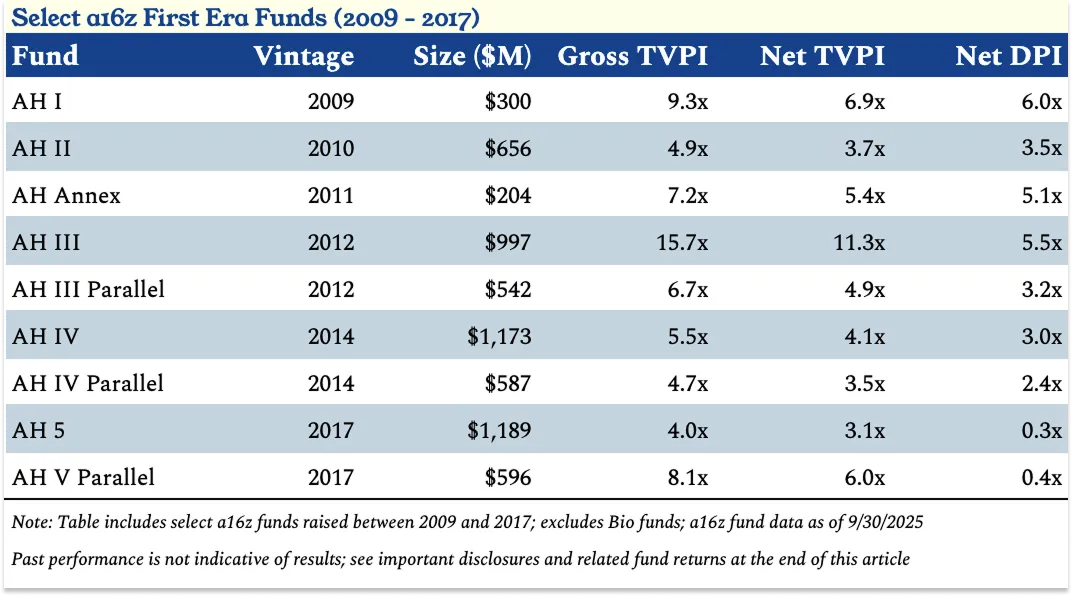

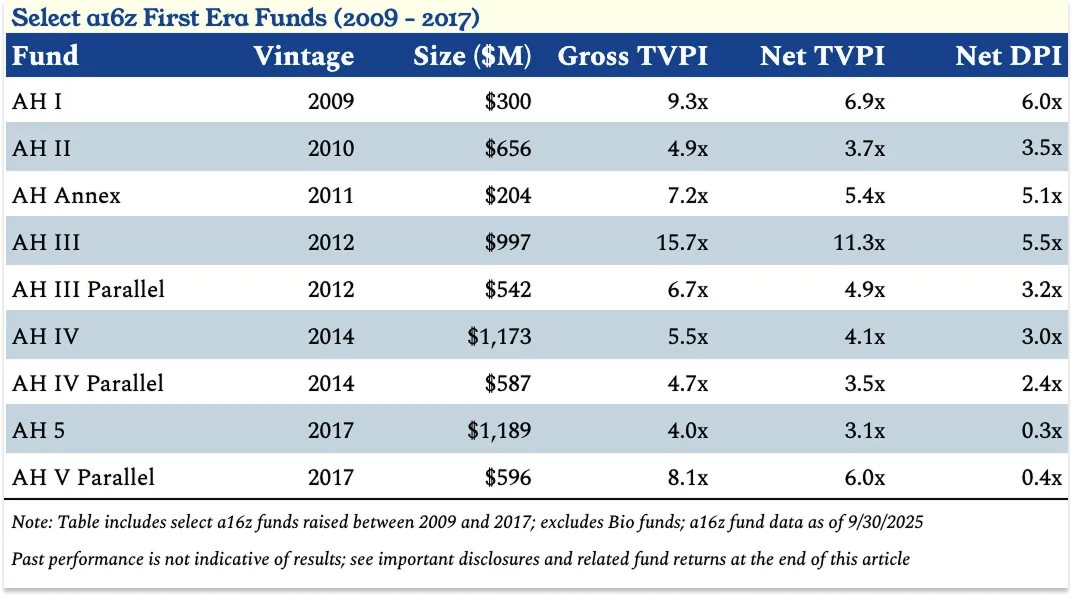

“Marc and Ben raised a $650 million Fund II in September 2010, and proceeded to make large late-stage investments in companies like Facebook ($50 million at $34 billion), Groupon ($40 million at $5 billion), and Twitter ($48 million at $4 billion), betting the IPO window would open.”

“AH III [$1bn fund], is a monster fund: sitting at an 11.3x Net TVPI (total value to paid-in capital after fees) as of September 30 2025, and when you include the parallel fund, it’s at a 9.1x Net TVPI. AH III includes Coinbase, which resulted in distributions of $7 billion gross to a16z LPs across the funds it’s in, Databricks, Pinterest, GitHub, and Lyft (although not Uber, proof positive that one sin of omission trumps every sin of commission), and I believe is one of the best performing large venture funds of all time”

“There is perhaps no bigger investing sin at a16z than investing in second best. If you miss a winner early, you can always invest in a later round. If you invest in second best, you lock yourself out from investing in the winner. This is true even if the eventual winner isn’t yet born.”

“Ben upped the check size and a16z led Databricks’ Series A at a $44 million post-money valuation. It owned 24.9% of the company. This initial encounter - Databricks asking for $200k, a16z going much, much bigger - set a pattern. When a16z invests in you, they believe in you.”

“A Firm is about delivering exceptional returns, and building sources of compounding competitive advantage. How do we get stronger with scale, not weaker?”

Hg agreed to take OneStream private at a $6.4bn valuation. Tidemark and General Atlantic will co-invest alongside Hg. OneStream is an enterprise financial software platform for consolidation, reporting, planning and forecasting. It’s another take-private of a solid SaaS business that was underperforming in the public market. - Bloomberg

Prior to its IPO, it was majority owned by KKR. OneStream went public at a $6bn market valuation and underperformed in the public market with a market cap that slipped to $4.5bn before the take-private.

OneStream is generating $600m in ARR growing 27% YoY and has a 98% gross revenue retention.

Clickhouse raised a $400m series D led by Dragoneer at a $15bn valuation. It’s a high-performance and cost-efficient alternative to Snowflake and Databricks especially for companies needing real-time analytics. - Clickhouse

Clikhouse’s managed offering has a 250% YoY ARR growth and 3k customers (Meta, Tesla, Capital One, Polymarket, Ramp, Vercel, Lovable).

ClickHouse acquired Langfuse, an open-source platform focused on observability and testing for LLMs.

It also launched a native Postgres service to help unify transactional and analytical workloads on a single platform.

“As AI systems move from experimentation into production, the demands placed on underlying data infrastructure are increasing. AI-driven applications generate significantly higher query volumes, operate with tighter latency requirements, and require continuous evaluation and observability.”

Notion closed a $270m secondary round at a $11bn valuation led by GIC, Sequoia and Index to provide liquidity to existing and former employees. - Notion, Fortune

Notion generates $600m+ ARR with 50% coming from AI products. In 2025, the company managed to re-accelerate its growth driven by the adoption of AI features on its platform.

Entropy

AI is automating junior tasks in marketing, HR, finance and CS, shrinking the number of entry-level roles with 5.8% US unemployment among recent graduates aged 22 to 27 (vs. 4.1% for the overall workforce), and -8% YoY in UK graduate recruitment. FT

“Global hiring remains 20% below pre-pandemic levels, job switching is at a 10-year low and AI is disrupting how we work.”

“Unemployment among new degree-holders is rising faster than the broader population.”

“AI can absorb much of the workload once assigned to early-career staff or to office-based roles such as marketing and communications and customer service.”

“Since the post-pandemic hiring boom, from 2023 to 2025, the legal, property and accounting sectors experienced the steepest declines, while previously growing areas such as consulting and human resources reversed course.”

“For many, the social contract feels broken: a traditional academic route no longer guarantees passage into a graduate-level job.”

Self-checkout is not a panacea for retailers and comes with trade-offs. - The Economist

“Self checkout machines are worse at what it does than humans, threatens jobs and increases the potential for crime.”

“The ratio of staff to customers is much lower for self-checkout machines than it is on assisted lanes. The lure of cost savings in a highly competitive industry gave supermarkets a strong incentive to stick with them even as customers griped at doing something new.”

“It will, however, be a long time before assisted lanes disappear entirely. When queues build up and stores need to speed up transactions, human cashiers are better. And customers’ preferences vary greatly. Older folk still tend to like cashiers; younger ones are less keen.”

“Employing fewer cashiers cuts costs, for example, but also opens the door to more shrink. So lots of self-checkout machines have weight-sensitive surfaces where you have to place each scanned item before proceeding to the next one; some retailers install exit gates that only open for people who have paid. Measures like these deter shoplifters, but at the cost of slowing down customers.”

“Real-world constraints mean that technologies often take small steps rather than great leaps. Self-checkout technology is no different.”

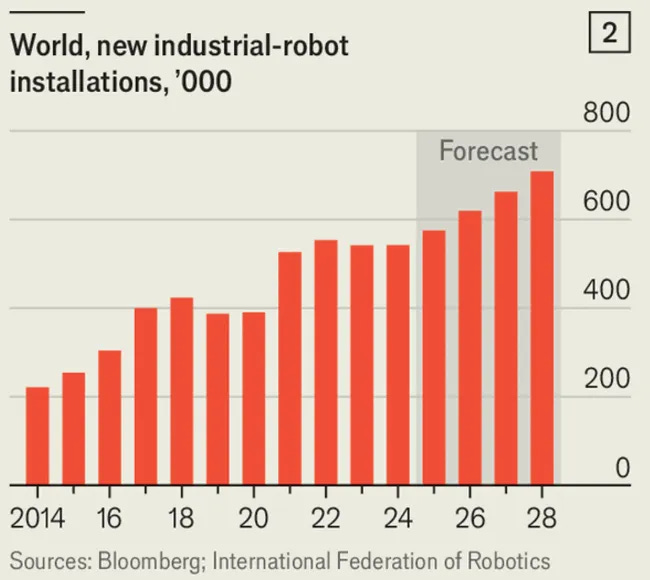

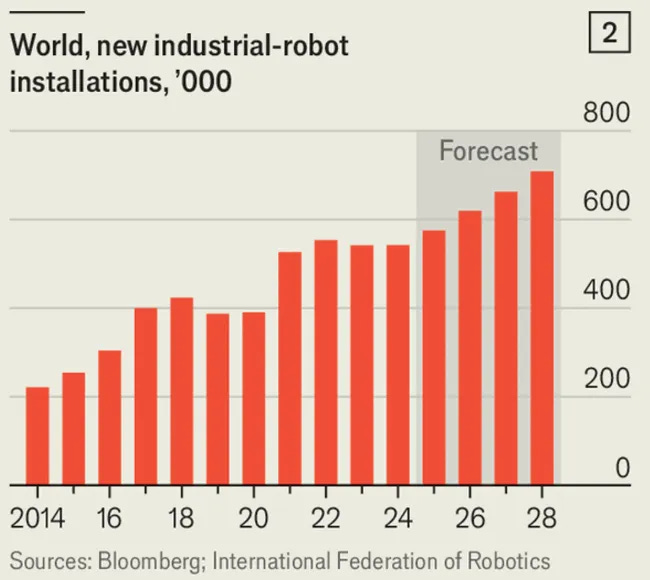

The AI revolution in robotics is transforming manufacturing, pushing factories towards greater automation and flexibility. - The Economist

“There were around 4.7m industrial robots operational worldwide as of 2024—just 177 for every 10,000 manufacturing workers. Having risen through the 2010s, annual installations surged amid the pandemic-era automation frenzy, but flattened off afterwards, with 542,000 installed in 2024.”

“Analysts see 2026 as an inflection point. The IFR reckons that annual robot installations will increase to 619,000 this year.”

“Partly that reflects tailwinds brought by the reduction of interest rates in the West over the past 18 months. But it is also a product of deeper structural forces. Western policymakers have turned to subsidies and tariffs to encourage manufacturing back to their shores; factory construction soared during Joe Biden’s time in office. With populations ageing, many manufacturers are struggling to find enough skilled operators to man their assembly lines, leading to rising demand for machines.”

“Advances in industrial software are helping overcome many of the challenges that have previously hindered efforts to automate production.”

“Siemens’ Amberg factory, which makes 1,500 variants of machine controllers, today produces around 20 times what it did when it opened in 1989, but with approximately the same number of workers.”

“Robots were once rigidly designed for one activity. […] Now the machines can be reprogrammed for another job with a tweak to their code.”

“Generative AI promises to take this transformation a step further. Until recently, precisely modelling the actions of a robot was often impossible owing to the many variables involved, a problem known as the “sim-to-real gap”. Simulations tended to break the moment lighting or the shape of an object changed. Supersized AI models, trained on vast amounts of data from sensors and cameras, may help solve that. As simulations become more accurate and detailed, it may be possible to program robots to approach a physical task much as a human would, perceiving, understanding and then reacting to the situation.”

“With each robot able to perform a wide array of tasks, shop floors may no longer need to be designed around lengthy assembly lines. Combine that with falling hardware costs and many firms may soon find it viable to spread their manufacturing across a network of smaller plants.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋