📖 Venture Chronicles - January 2025

Overlooked #192

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of January.

For French speakers, I recorded a podcast earlier this month with Sébastien Couasnon on Tech45 to discuss the findings of my report on the French tech ecosystem. You can listen to the episode here.

Monday, Jan. 1st: In venture, deal sourcing and selection offers quicker feedback loops that waiting for 7-10 years for successful exits. By optimising their deal sourcing processes and focusing on immediate feedback, VCs can better position themselves for long-term success, despite the inherent delays in realising financial returns. - Article

“While your ultimate reward signal (successful investments) is still delayed, you can construct dense intermediate rewards that provide much richer learning signals.”

“In these causal chains, there are a few things that are disproportionately rewarding, such as investing in a "supernode" (someone who has high degree connectivity in a prospective ecosystem) or being strongly opinionated in long-form about a non-consensus opinion.”

“Smart firms build attribution systems that track the complete causal chain: [Action] → [Network Node] → [Deal Flow] → [Quality Meetings] → [Competitive Access]”

“Early stage venture isn't just about maximizing expected value over a 10-year horizon. It's about learning which actions in your current state maximize the probability of encountering high-value states in your deal flow Markov Decision Process.”

Thursday, Jan. 2nd: Rick Zullo at Equal VC shared 2025 predictions on the public tech market and the venture capital industry. - Equal VC

“The stock market will see a correction of at least 15% with technology stocks taking the biggest hit.

I think valuations are stretched, risk tolerance is too high and the chances of economic decline are much higher than most folks think.

The magnificent 7 (Apple, Microsoft, Amazon, Alphabet, Tesla, Meta, and Nvidia) represent roughly 50% of the Nasdaq and more than a third of the S&P.

Revenue growth rate and Rule of X are the worst they’ve been as far back as this data is tracked, yet multiples are back in the 2017-2020 range. This means folks are paying the same price for lower growth and efficiency.”

“We’ll see more defections from big VC funds and more emerging managers “growing up”.”

I’m receiving a tremendous amount of preliminary interest from partners within these firms to figure out how to start their own funds.

It’s hard to go a single week without seeing a major departure from one of these firms.

It used to be that these firms were perceived as the safest sources of capital

I suspect that we’ll see some defections from multi-stage funds result in the formation of firms with this profile (as we saw earlier this year with Chemistry, a fund led by alums of A16Z, Bessemer and Index) and suspect that we will see other venture managers graduate up.

“A record number of funds will close up shop.”

While I believe more money will be deployed in 2025 than in 2024, I sense fatigue from LPs and emerging managers alike and believe a significant amount of emerging manager wind downs will occur.

I’m seeing most employers go back to the office at least 4 days a week and even a few VCs telling me that they refuse to fund companies that aren’t in the office.

Friday, Jan. 3rd: The venture industry in the US is undergoing a significant consolidation. Large & established firms are capturing the majority of LPs fundraising dollars, while a long tail of smaller venture capital firms is gradually disappearing from the market. - FT

25% decline in active funds between 2021 and 2024 (8.3k to 6.2k).

Total fundraising for GPs is back to 2018 levels.

Capital raised is concentrated on a small group of mega firms with 50% of the capital raised by US VCs concentrated into 9 GPs (inc. a16z, GC, Thrive, Iconiq)

Countdown Capital and Foundry Group have wound down operations.

Saturday, Jan. 4th: Hindenburg published a short-selling report on Carvana. Since then, the activist short-selling firm announced its closure after eight years of operations. - Hidenburg

“Carvana is a $44bn online car dealer founded in 2012. Its main business is an online platform that allows retail customers to buy and sell used cars. Despite facing bankruptcy risks in 2022 and 2023, Carvana’s stock spiked 284% in 2024, with investors believing the company’s worst days are behind it.”

“Carvana’s turnaround is a mirage.”

“Carvana’s main business is an online platform that allows retail customers to buy and sell used cars, which accounts for ~70% of its total revenue.” “The company offers financing, insurance and other services like car protection plans.”

“The company also runs a wholesale auction business, called ADESA, which it acquired in May 2022. ADESA has 56 locations where registered auto dealers can participate in auctions, either virtually or on-site. Carvana also acquires vehicles in these auctions.”

“In September 2023, amid fears of bankruptcy, the company “aggressively restructured”, working with creditors to slash $1.3 billion of debt. Since then, the company has focused on a “three-step plan” that includes (1) driving the business to positive EBITDA, (2) achieving positive unit economics and (3) returning to profitable growth.”

“Heading into 2025, signs of stress are increasingly evident in the U.S. auto loan market. Subprime auto loan delinquencies are currently higher than during the Global Financial Crisis of 2007-2008.”

“Investors seem to under-appreciate that Carvana’s business is capital intensive and reliant on the willingness of third parties to purchase the loans it originates.” “Financing is a key part of Carvana’s business model, with about 80% of customers financed by the company. Rather than keep these loans on its balance sheet, Carvana offloads the vast majority to third-party buyers. Over the last 9 months, Carvana sold $6.15 billion in loans to third parties, reporting gain-on-loan sales of $541m. Those gains accounted for 26% of gross profit over the last 9 months.”

“As we investigated Carvana, it became apparent that the company is skewed to non-prime and sub-prime borrowers, usually with low credit scores and few financing options available to them. Carvana has very few restrictions on lending, merely requiring that a loan applicant have annual income of $5,100, be over 18 and have no active bankruptcies.”

Sunday, Jan. 5th: I listened to an interview with Doctolib’s CEO Stanislas Niox Chateau. - GDIY

The importance of user-centricity. Doctolib is obsessed with its users (both patients and physicians). "For us, users and the product are everything. If we have a good product, if our users are happy, the rest will follow."

Integrating AI into Doctolib’s platform. Doctolib is heavily investing in AI to develop innovative solutions like a consultation assistant, which automatically documents consultations, and a virtual phone assistant, revolutionizing patient care and physician workflows.

AI will have a massive impact on healthcare. AI is poised to revolutionize healthcare more than any other sector. Healthcare generates vast amounts of data, and if AI can make this data accessible and actionable, it could dramatically enhance the quality of care.

Building a right to win before founding a company. Before stating Doctolib, Stan spent over six months visiting healthcare facilities to personally observe and understand the workflows, needs, and challenges of healthcare providers. This firsthand experience allowed him to identify the specific pain points that Doctolib could address.

Monday, Jan. 6th: Scott Galloway shared its predictions for 2025. - Scott Galloway

“The AI ecosystem is settling into three layers: applications (Duolingo, Netflix, Tesla), AI models (Anthropic, Gemini, OpenAI), and infrastructure (AWS, Google Cloud, Nvidia). Two companies dominate. OpenAI has doubled its annualized revenue to $3.4 billion in the past six months. And its ChatGPT accounts for 56% of premium LLM subscriptions, i.e., people pulling out their credit cards.”

“So far, the benefits of AI have accrued to existing players. The next set of winners will be firms that capitalize on service-as-a-software, i.e., taking human-intensive services and putting a thick layer of AI on top to scale with less labor. This is a fancy way of saying there will be more consumer-facing AI applications. The real cabbage, however, is in routinizing back-office functions (e.g., accounting, compliance, customer service, etc.).”

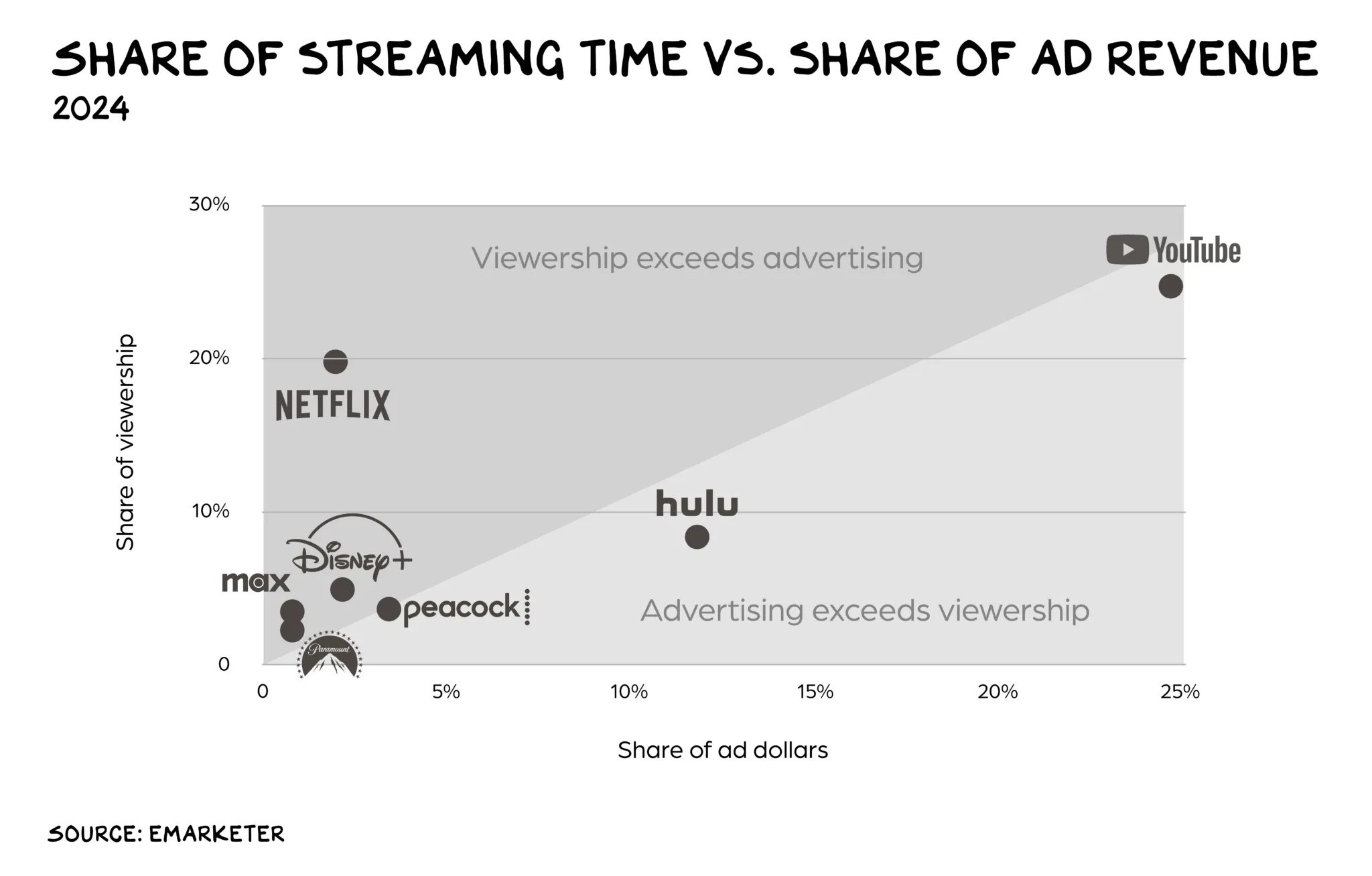

“Netflix didn’t win the streaming wars, YouTube did. Last year, YouTube, which spends zero dollars on content — it shares revenue with creators instead of paying them — became the first streaming platform to reach 10% of all television viewing. […] In the U.S. and U.K., one-third of kids aged 8 to 12 said YouTube was their No. 1 career choice; movie star didn’t make the list. Also, YouTube is the number 1 podcast platform, adding a tailwind no other streamer has. If Alphabet were forced to spin off YouTube, the company would likely be worth half a trillion dollars, vs. Netflix’s market cap of $350bn.”

“A historic amount of cash is on the sidelines. Since 2003, private equity’s dry powder, i.e., the committed capital not yet allocated, increased 8x to $4 trillion. Corporate cash holdings total $4.1 trillion. Context: U.S. GDP is around $27 trillion. Setting aside whatever grievances Trump may hold against specific tech and media companies, the perception is that his administration will likely be more friendly to M&A. Some predictions re who will be on top of some big transactions: Comcast, Uber, and (see above) Musk. Also, I believe someone will take Intel and/or Boeing private.”

Tuesday, Jan. 7th: VC is no longer a unified asset class. Like in private equity, there are multiple segments based mostly based on fund sizes with different risk-reward profiles. - Venture Unlocked

“Many LPs still use a monolithic lens to assess venture capital, which results in the ongoing comparison of "large vs. small" VC funds, which misses the point—these aren't just different fund sizes; they're fundamentally different economic products with unique risk-return profiles and business models.”

Samir breaks down funds into several categories: small cap (below $250m), smaller mid-cap ($250-500m), larger mid cap ($500m-1bn) and large cap ($1bn+).

“The evolution of venture capital mirrors that of other private market segments. Just as institutional investors wouldn't compare a large buyout fund to a small-cap niche specialist in private equity, we need to move beyond simplistic "large versus small" comparisons in venture capital.”

“Small-cap funds offer the potential for exceptional returns but demand both high-risk tolerance and exceptional manager selection capabilities. Mid-cap funds provide a balance of upside potential and portfolio construction flexibility, while large platforms deliver more predictable outcomes with stronger downside protection.”

“Building a successful portfolio of small-cap funds requires significant resources to meet managers (I think to invest in 5 managers per year, investors should be meeting 200-300 managers) along with a deep evaluation of individual managers on whether they have a definable edge when it comes to sourcing, picking, winning, etc. This is necessary to avoid getting small-cap beta returns where investors are not likely to get compensated for the additional risk versus larger funds.”

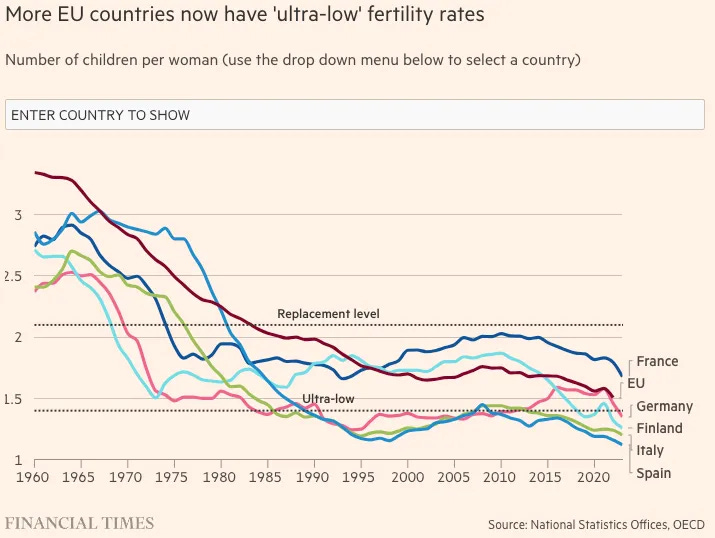

Wednesday, Jan. 8th: EU countries face a demographic crisis as fertility rates fall below the “ultra-low” threshold of 1.4 children per woman (e.g. Germany, Finland, Italy, Spain), driven by delayed parenthood, economic uncertainty, and changing social attitudes. - FT

“The fall in birth rates partially reflects the “postponement of parenthood until the 30s”, which involves a “higher likelihood that you will not have as many children as you would like because of the biological clock”, said Willem Adema, senior economist at the OECD.”

“With young people reaching milestones, such as buying a house, later in life, the average age of EU women at childbirth rose to 31.1 years in 2023, a year later than a decade ago. The figure rises is 31.4 in Germany, and over 32 years in Spain, Italy and Ireland.”

“The norms of what it means to be a good parent and how intensive you should participate in that are such that quite a few young people say: ‘Well, in addition to the fact that I don’t need children to be happy, it would also be a very difficult job for me to do, and I’m not sure that I can take that responsibility’.”

Thursday, Jan. 9th: I watched an All-In podcast episode on 2025 predictions. - All-In Podcast

2025 will be “the year of the robot” with autonomous hardware/robotics companies getting strong momentum both in B2C and B2B.

In 2025, it will be hard to be a government service provider with the Trump’s administration cutting public services costs. "You do not want to have the United States government at any level as over 35% of your revenue".

In 2025, there is going to be a title wave of M&A after four years of not being able to get anything done - starting with Intel & Boeing that could be acquired as well as independent frontier AI labs that start struggling to compete with integrated cloud providers (Amazon, Microsoft & Google) which have a structural cost advantage.

In 2025, large enterprise software providers will struggle.

AI agents will replace many white-collar jobs, which are the main target market for enterprise software.

Legacy software companies do not have the resources (their own models or computing power) to properly compete in the AI agent space.

There will be a war between the “software industrial complex” (large, inefficient enterprise software companies that rely on outdated technology and expensive sales tactics) and AI startups coming up with better products sold at a fraction of the cost undercutting the pricing of legacy software providers.

Friday, Jan. 10th: Sam Altman wrote about OpenAI’s journey. - Sam Altman

“We ended up mercifully calling it ChatGPT instead, and launched it on November 30th of 2022. We always knew, abstractly, that at some point we would hit a tipping point and the AI revolution would get kicked off. But we didn’t know what the moment would be. To our surprise, it turned out to be this. The launch of ChatGPT kicked off a growth curve like nothing we have ever seen—in our company, our industry, and the world broadly. We are finally seeing some of the massive upside we have always hoped for from AI, and we can see how much more will come soon.”

“Building up a company at such high velocity with so little training is a messy process. […] Mistakes get corrected as you go along, but there aren’t really any handbooks or guideposts when you’re doing original work. Moving at speed in uncharted waters is an incredible experience, but it is also immensely stressful for all the players.”

“We’ve also seen some colleagues split off and become competitors. Teams tend to turn over as they scale, and OpenAI scales really fast. I think some of this is unavoidable—startups usually see a lot of turnover at each new major level of scale, and at OpenAI numbers go up by orders of magnitude every few months. The last two years have been like a decade at a normal company. When any company grows and evolves so fast, interests naturally diverge.”

“In 2025, we may see the first AI agents “join the workforce” and materially change the output of companies.”

Saturday, Jan. 11th: Addepar is raising $250m from 8VC, Valor and WestCap at a $3.5bn valuation. It will use the funding to provide liquidity to existing investors and early employees. It’s a vertical software in the finance industry. It sells wealth management and investment software to 1.2k financial institutions including MS, Jefferies and HSBC accounting for $7tn worth of assets. The company generates hundreds of millions of dollars in revenues and is expected to be cash flow positive in 2025. It previously raised a round at a $2.1bn valuation in Jun. 2021. - Bloomberg

Sunday, Jan. 12th: The Atlantic wrote about the rise of social isolation in America, with an increasing number of people spending time alone. - The Atlantic

Over the past two decades, in-person socializing has drastically declined, further amplified by the pandemic.

This societal change is evident in various aspects of life, such as dining, entertainment, and general socializing. For example, solo dining has increased, with many people opting for takeout rather than dining out, signaling a preference for solitude over communal experiences. This trend is also reflected in entertainment, as people increasingly consume media at home rather than in theaters.

The real issue is not loneliness itself, but rather the lack of response to the biological urge for social connection, which has profound implications for mental health and social cohesion.

Monday, Jan. 13rd: Jason Cohen wrote on the shift from exploring to reach product market fit to scaling execution post product market fit. - Jason Cohen

“Founder arrogance peaks once the company achieves some success, having entered the vaunted Product/Market Fit. It was such a hard scrabble to get here, against all odds, and now it’s actually working!”

“What Arrogant Founder doesn’t realize is that the needs of the company dramatically change after Product/Market Fit. Everyone and almost every thing at the company must change and adapt. Including the founder.”

“The “Execute” modality is required to answer the new challenges including (i) hiring & managing (vs. only building), (ii) having a good balance between de-risking & bringing new innovations to the market, (iii) bringing predictability in your business.

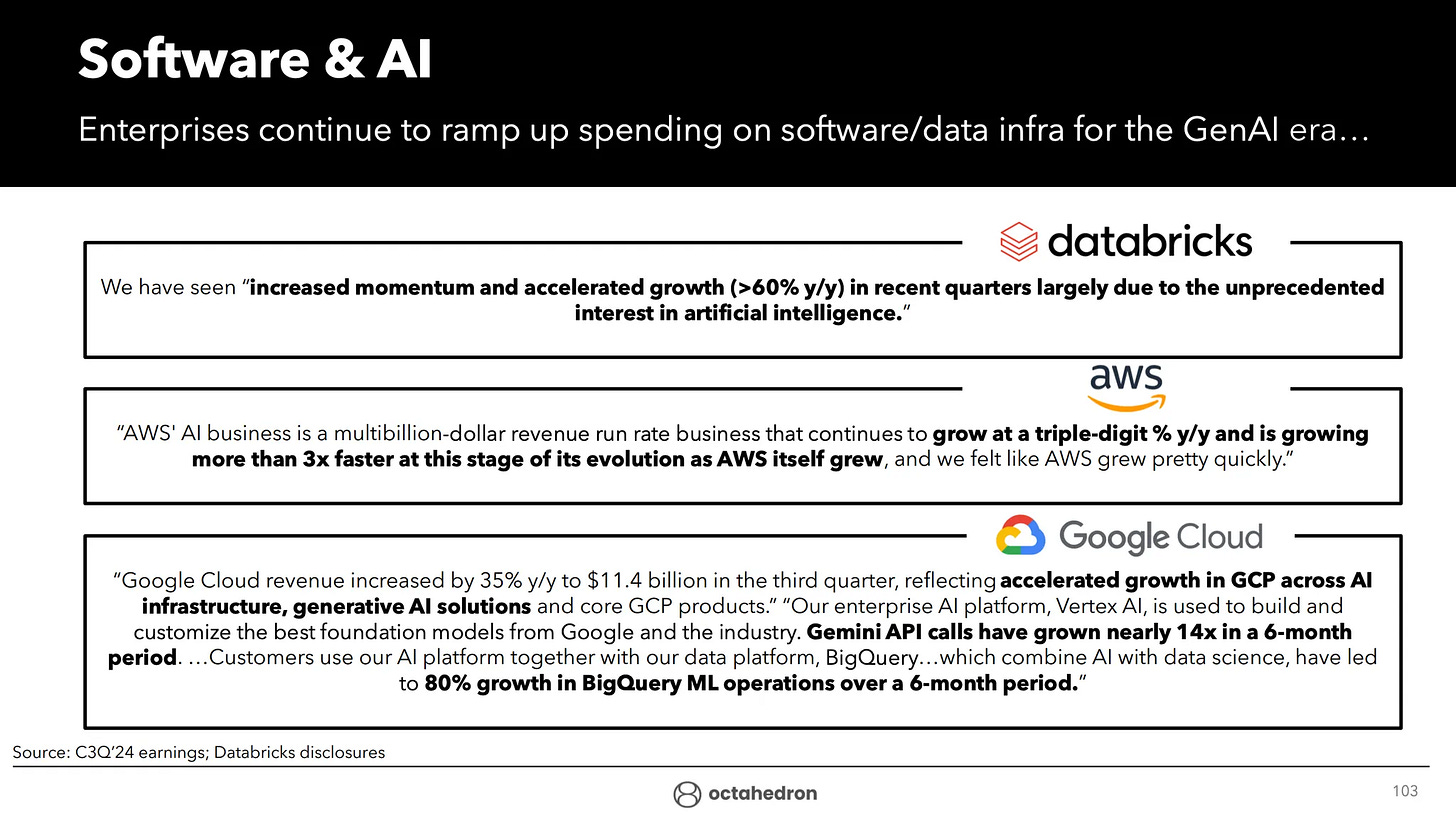

Tuesday, Jan. 14th: Octahedron Research published its Q4-2024 market analysis report covering macroeconomic trends, digital advertising, on-demand services, e-commerce, semiconductors, and fintech.

Software companies like Salesforce and ServiceNow are positioning themselves for the next significant wave of GenAI development: AI agents and the infrastructure needed to support them.

Salesforce is heavily promoting its Agentforce platform, highlighting its ability to automate tasks, analyze data, and interact with customers 24/7, freeing up human employees for more strategic work.

ServiceNow emphasizes its Xanadu platform, which aims to govern the deployment of agentic AI across the enterprise, enabling businesses to manage and control their AI agents effectively.

Wednesday, Jan. 15th: Matthew Mandel at USV wrote about deep-tech as the next frontier for venture capital. - Matthew Mandel

“Modern venture history begins with General Georges Doriot’s American Research and Development (ARD) Corporation. ARD invested in a wide range of novel technologies, from off-shore oil and radiation detection to, most importantly, minicomputers.”

“Venture capital returns are driven by outlier investments. By investing in companies with capped downside and unlimited upside, venture funds maximize their returns by making high variance bets each with the potential to pay for the failures in the rest of the portfolio, potentially many times over.”

“Over the last thirty years, venture has come to be more narrowly associated with software startups.”

“Venture became the way to finance the search for product-market fit for capital efficient, easy-to-iterate-on, quick-to-grow startups that could ideally defend themselves once they found product-market fit via network effects. We might call this dominant model the “lean startup” model.”

“Although the lean startup model has been successful over the last thirty years and has become near-synonymous with venture capital, it’s less well-suited to the mature era of the internet we’re in today and offers an overly restrictive conception of where venture capital can be profitably directed.”

“Venture’s historical success was investing in frontier-pushing technologies, and so as the lean startup opportunity compresses, the frontier might be the best place for investors to explore.”

“There are very large markets that lean software companies haven’t and won’t transform: energy, manufacturing, defense, life sciences, telecom, semiconductors, etc. While lean software will continue to make life easier in these industries by improving workflows, the only path to radical improvements to their core products is through fundamental innovation in relevant fields like mechanical engineering, electrical engineering, chemistry, biology, etc. This is the territory of deep tech startups.”

“In fact, there’s something about deep tech startups that is profoundly aligned with the venture model. Venture capitalists may have mistakenly developed a preference for companies that can persist on little capital as they iterate in search of product-market fit. Deep tech startups largely can’t do that. Early stage capital usually only lets them test one or two technical hypotheses. But, if a deep tech startup can crack whatever technical challenges they face, they should be uniquely positioned to upset a massive industry and rapidly gain market share. Such extreme binary outcomes reflect the core truth of venture: because downside is capped and upside is unlimited, all that matters is the size of the wins, not the recovery on the losses. The safety that venture investors have come to appreciate about investing in lean software might prove to be antithetical to the power law that undergirds the asset class.”

Thursday, Jan. 16th: ElevenLabs raised a $180m series C co-led by Iconiq and a16z at a $3.3bn valuation. It also brought strategic on board including LG, Deutsche Telekom, Hubspot, NTT and RingCentral. - Techcrunch, Sifted, Concept

“ElevenLabs has emerged as a major player among those providing synthetic voice technology. Dozens of major publishers and content creators across verticals like media and gaming, as well as a number of other tech startups, are all using ElevenLabs’ technology to power their voice and audio features.”

“In addition to a focus on improving its AI models, the company plans to use the funding to grow its conversational AI builder with an ambition to reach more consumers directly and through partnerships.”

“The company also wants to double down on creating AI-powered conversational agents by supporting legacy communications like telephony and better integrating different kinds of knowledge sources. This is partly why it is partnering with telcos in this round.”

“Its tool converts text to speech, featuring emotion and intonation, allowing clients like publishers and content creators to turn written material into audio.”

“ElevenLabs currently has more than 200 employees, according to LinkedIn. Its product and research teams are primarily based in Europe, in the UK, alongside Poland and Hungary, while its US footprint is mostly made up of sales and partnerships teams.”

“In just two months since launching their Conversational AI tool, developers have built over 250,000 conversational AI agents using their technology.”

“The Series C funding will accelerate ElevenLabs' research into more expressive and controllable voice AI while expanding their tools for developers and businesses globally.”

Friday, Jan. 17th: Chinese social media are monetising users via ecommerce when their Western counterparts rely only on advertising. - Rest of World

“Chinese apps have made social shopping mainstream, in contrast to Western social networks which focus on advertising.”

“A key driver behind the success of Chinese apps is that they have integrated e-commerce into their platforms, blending entertainment and networking with sales to monetize their famously addictive algorithms.”

“All of China’s major social platforms have a component of shopping built into them.”

“In 2023, TikTok’s Chinese sister app, Douyin, said its platform sales exceeded 2 trillion yuan ($2 billion).”

“Although TikTok only launched TikTok Shop in 2023, American users’ social commerce content helped boost ByteDance’s non-China revenue by 60% last year, despite regulatory pressures. Last year, TikTok said it topped $100 million in Black Friday shopping revenue in the U.S.”

“Instagram feels like a stage where everyone’s watching and judging. But TikTok felt like a casual hangout where you could just be yourself.”

Saturday, Jan. 18th: In 2024, private equity firms accelerated activity in Europe driven by discounted valuations for large companies - especially in the public market where there is a strong valuation gap between US and European stocks. European buyouts over $1bn rose 78% to $133bn (vs. 29% for the rest of the world). Major transactions included Hargreaves Lansdown’s $6.9bn deal, Thoma Bravo’s $5.5bn acquisition of Darktrace, and Brookfield’s acquisition of Neoen. - FT

Sunday, Jan. 19th: Kent Hendricks wrote a fascinating blog post about 52 things he learnt in 2024. - Kent Hendricks

“Employees who use Firefox or Chrome have a 15% higher retention rate and report more satisfaction at work than employees who use Internet Explorer or Safari. This is because they’re less likely to accept the default way of doing things.”

“ChatGPT caused a 2% drop in the number of freelance jobs posted on Upwork.”

“Legalization of online sports betting generates an 8% increase in credit card debt among sports betters. The poor are disproportionately affected: low income households spend 32% more on betting than high income households.”

“People overestimate others’ dishonesty by about 13.6%.”

“Men are more likely to order two hamburgers at McDonald’s when they order with a screen. When they order from a human, they tend to order only one.”

“Each additional negative word in a news headline drives 2.3% more clicks.”

“People know whether or not they want to buy a house in just 27 minutes, but it takes 88 minutes to decide on a couch.”

“Waymo self-driving taxis generate 88% fewer property damage claims and 92% fewer bodily injury claims than human drivers. After driving 25.3 million miles, Waymo Driver had nine property damage claims and two injury claims, compared to 78 property damage claims and 26 injury claims from humans who drive an equivalent number of miles.”

“Among luxury brands, an increase in the size of the logo by one point on a seven-point scale results in a $122.26 price decrease for Gucci and a $26.27 decrease for Louis Vuitton.”

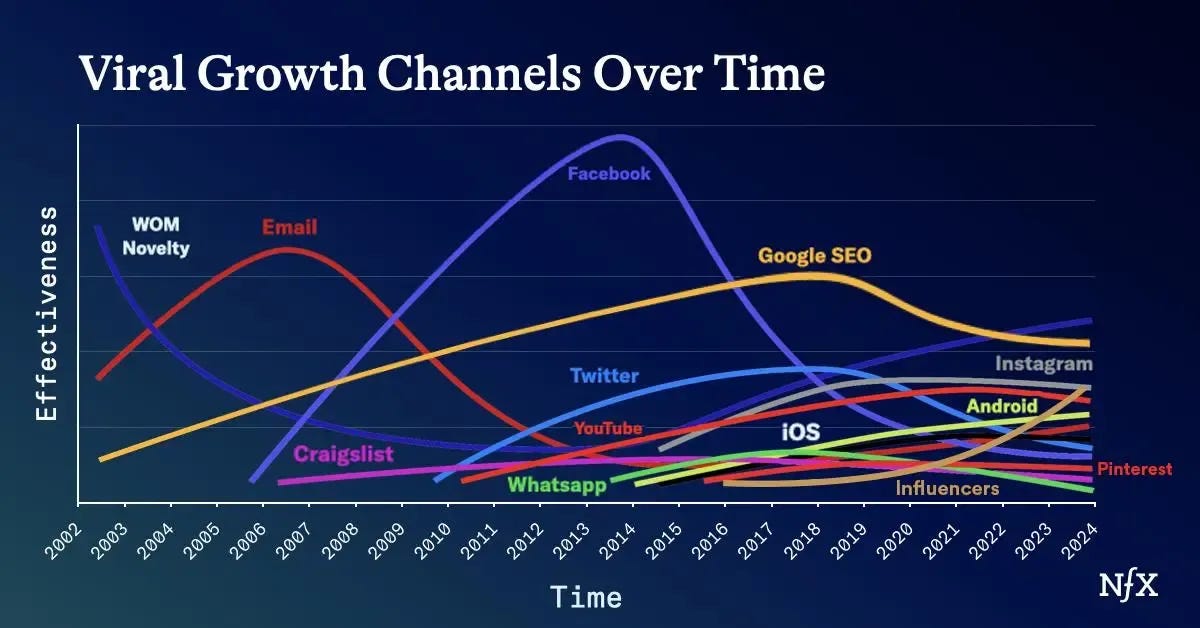

Monday, Jan. 20: NfX wrote about consumer startups. Since 2014 (post mobile phone maturity), the window to launch new consumer businesses has largely closed, making it difficult for new companies to succeed. Today, AI is now creating fresh opportunities. - NfX

“Consumer software is doing great for public market investors today but hasn’t been great for founders starting something new, nor for Seed and Series A investors investing.”

The consumer window closed for 2 main reasons: (i) “the hardware interfaces to software (e.g. internet browser for computers, mobile touch for mobile) haven’t changed in a long time and (ii) “for what can be done on these interfaces, the psychological and emotional needs of consumers are largely taken care of” by major consumer platforms (Meta, Google, Snap, X, Netflix, Linkedin, etc), (iii) “incumbents can block you because they have all the defensibilities: network effects, scale, brand, and embedding” and (iv) “incumbents own, or have clogged, the growth channels”, (v) “incumbents will actively copy or block any startup that gets momentum”, (vi) “incumbents get laws passed that benefit them”.”

“You need to leverage AI. It’s a fantastic wedge that – still today – few startups other than OpenAI have used to discover new consumer behaviors, delights, needs, wants, and loves. It’s still sitting there for you to grab. The technology window for consumer AI is still early with all its openness and creativity.”

“You have to build network effects into your product from day one to give you a chance against the incumbents.”

Tuesday, Jan. 21st: Insight raised $12.5bn for its 13th flagship tech fund and a structured opportunity fund falling short of its $20bn target due to challenging fundraising conditions. Despite this, the firm achieved over $8bn in exits in 2024, including Recorded Future’s $2.65bn sale to Mastercard and WalkMe’s $1.5bn sale to SAP. The firm plans investments from $5m to $500m in software and internet-focused companies, including acquisitions from VC firms under liquidity pressure. - Techcrunch, Insight

Wednesday, Jan. 22nd: Lenny's Rachitsky recently published the results of a survey of 6.5k readers, detailing their preferred tech stacks. - Lenny

“The Jira paradox and Linear’s insurgency. 68% of participants use Jira, but it also tops the “we wish we could use a different tool” list. Enter Linear: the fastest-growing alternative to Jira, and already used by over 10% of participants.”

“Miro continues to stay ahead of FigJam for virtual whiteboarding, just barely. But FigJam is gaining ground (because everyone’s using Figma…).”

“AI tools have become as essential as having a laptop. A whopping 90% of respondents use ChatGPT regularly. This is the most significant shift in the product team tool stack in recent memory. More participants use ChatGPT than Gmail (76%) or Slack (71%).”

“Notion is playing a clever game. It’s become the second-most-popular project management tool and the fourth-most-popular docs, and it’s gaining traction as a CRM tool. Participants consistently praised its flexibility (“It’s my go-to for … anything”) and how it enables teams to build a shared understanding.”

“Bundling is powerful, but it can get you only so far. Some of the most-used tools, like Jira, Microsoft Teams, and Google Slides, are all bundled within their respective corporate stacks, which locks people in for the long term and creates a massive switching cost. Thanks to the bundle, they end up “winning,” but we’re seeing some of these products top the “least valued” and “most interested in switching from” lists, so it may be only a matter of time until a better-crafted and well-executing startup (e.g. Linear, Figma Slides) finds a wedge in and eats their lunch.”

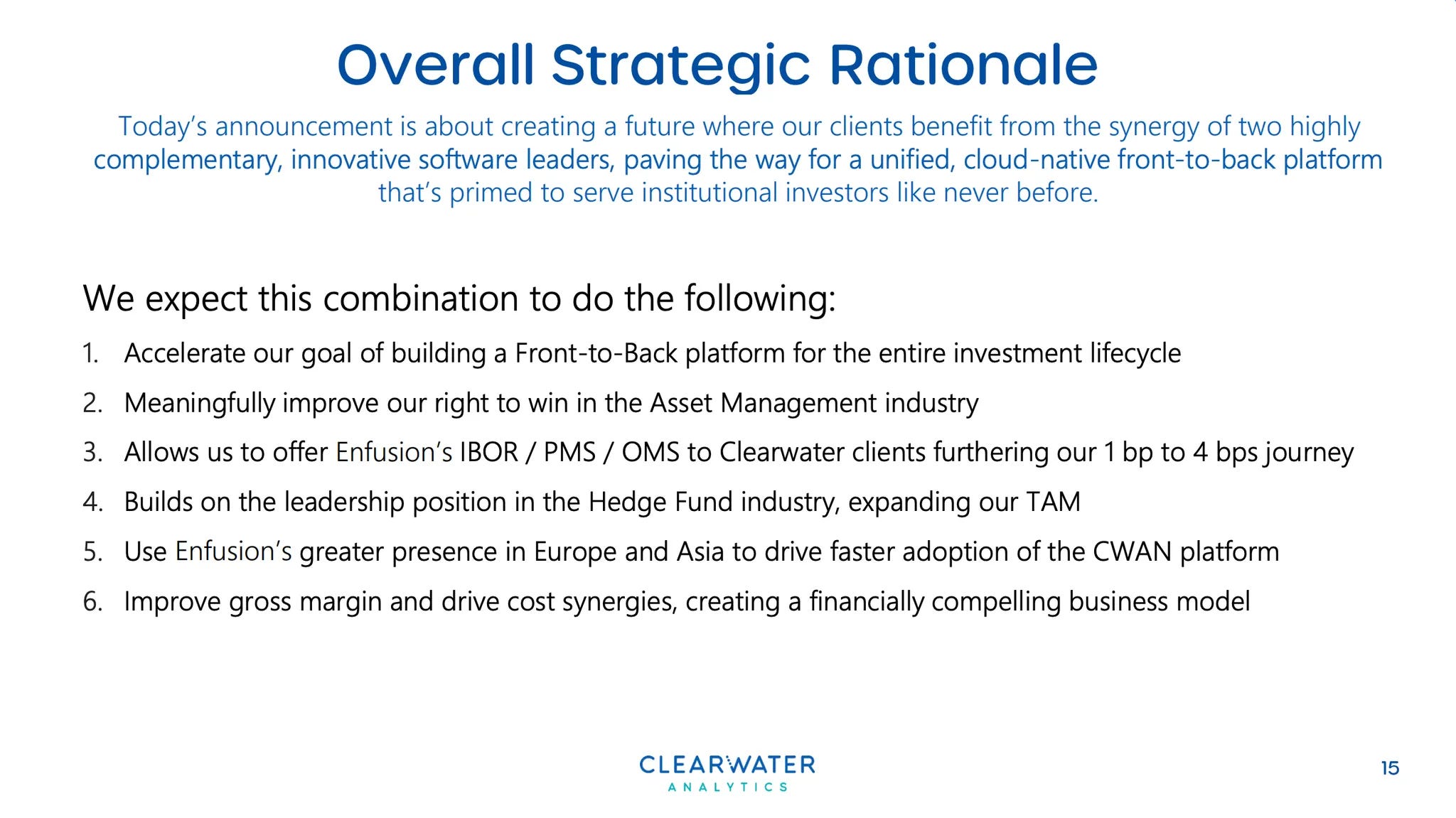

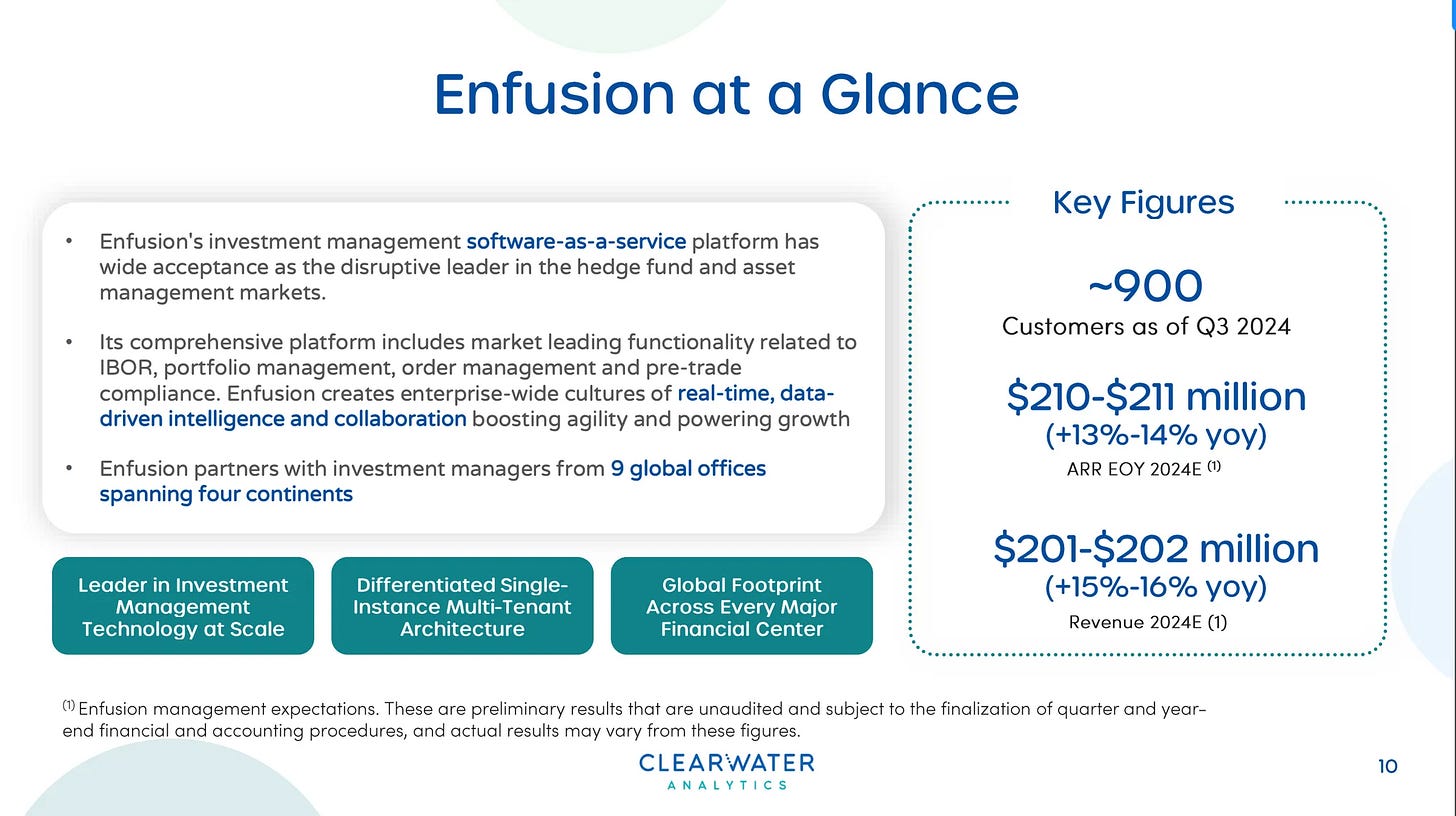

Thursday, Jan. 23rd: Clearwater has agreed to buy Enfusion for $1.5bn. Enfusion is a vertical software for hedge funds and investment managers generating $210-211m in ARR (growing 13-14% YoY) from 900 customers ($233k ACV). The acquisition accelerates Clearwater's vision of building the first cloud-native front-to-back platform for the entire investment management industry. Enfusion's front-office capabilities, including IBOR (Investment Book of Record), portfolio, and order management, will be integrated with Clearwater's middle and back-office solutions. - Clearwater

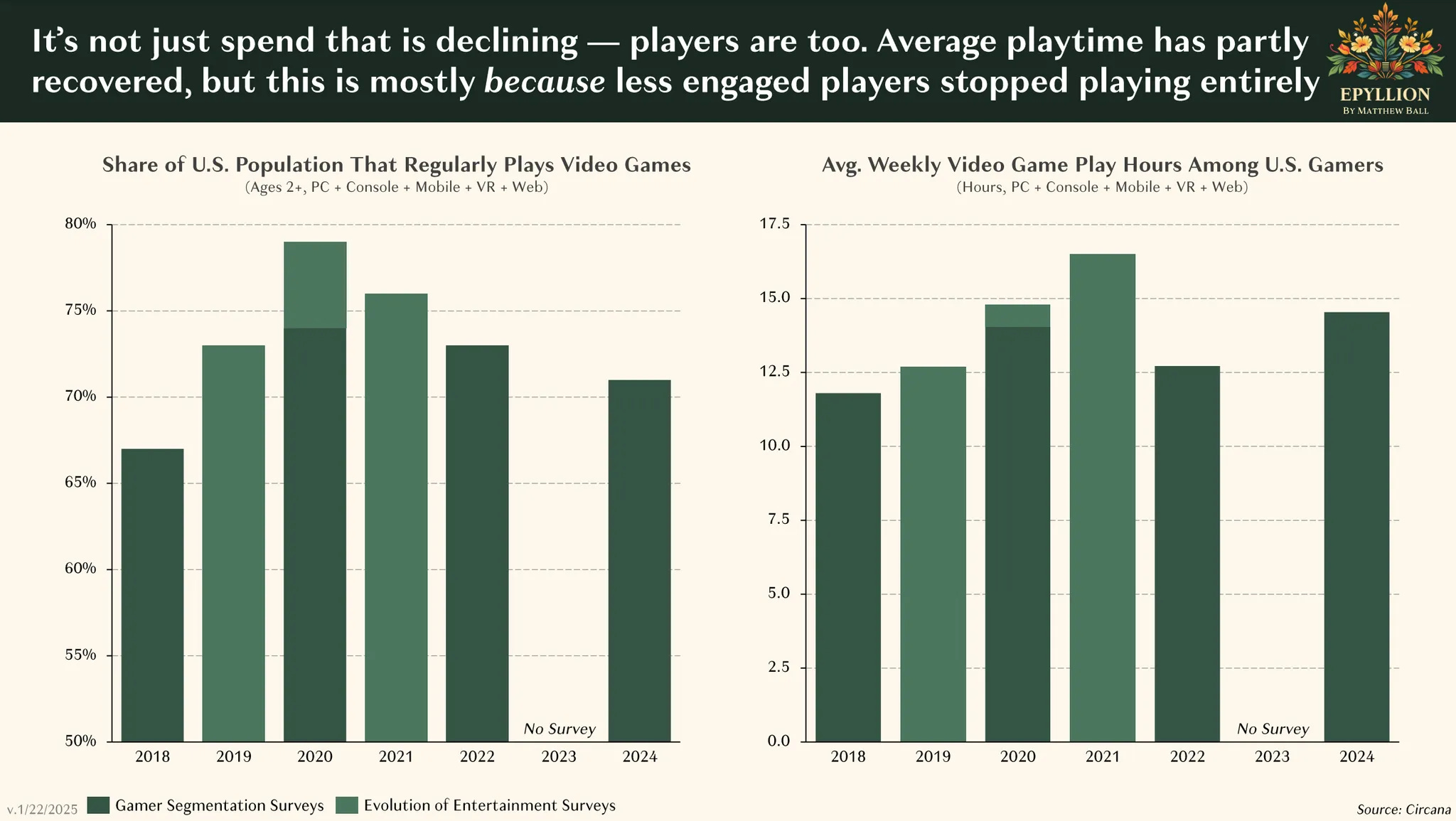

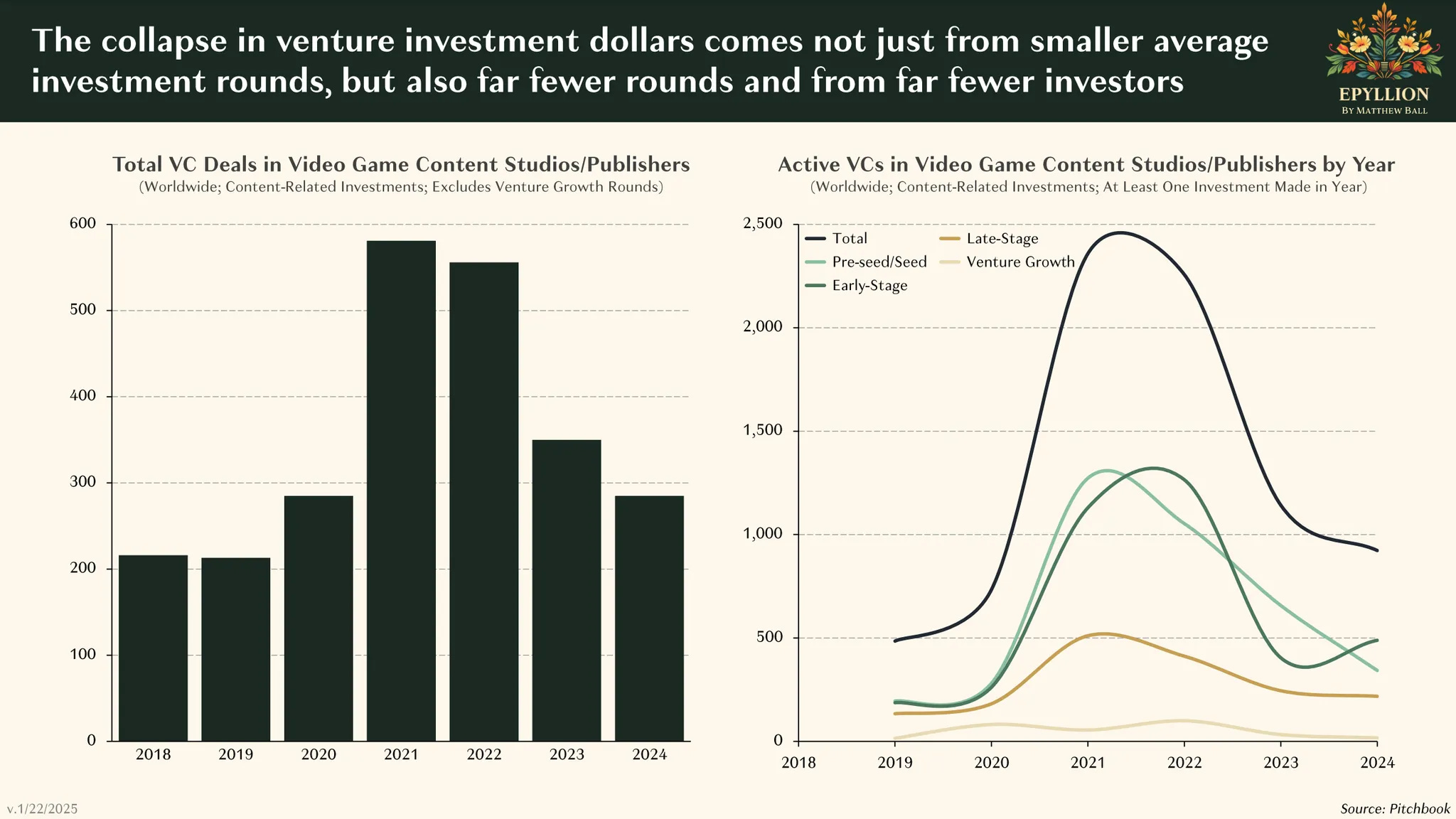

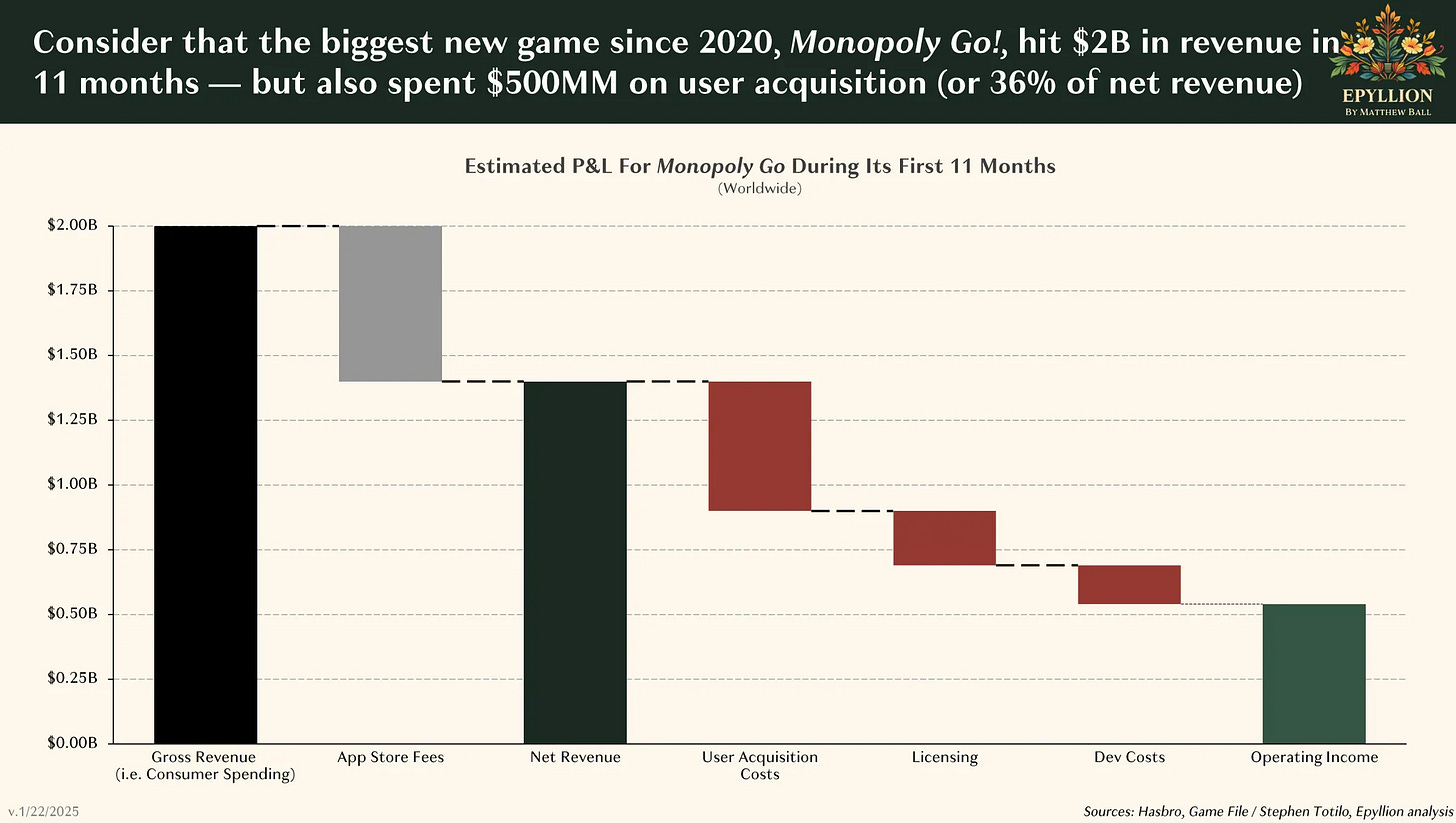

Friday, Jan. 24th: Matthew Ball published a presentation on the state of the gaming market in 2025. - Matthew Ball

Saturday, Apr. 25th: Clément Delangue (Hugging Face’s CEO) and Matt Hartman (ex. Betaworks) cofounded Factorial as a venture capital firm leveraging technical founders to support in sourcing, picking, winning and supporting companies. - Techcrunch

“Factorial’s model relies on a network of technical founders, each one focusing on sourcing their own deals from their own networks and areas of expertise.”

“Clement Delangue, CEO of AI startup Hugging Face (which Hartman backed while at Betaworks), was Factorial’s first sourcing partner. Now the firm is announcing some of its other partners: Giphy co-founder Alex Chung, Venmo co-founder Iqram Magdon-Ismail, Hugging Face co-founders Julien Chaumond and Thomas Wolf, Fast Forward Labs co-founder Hilary Mason, and Beme co-founder Matt Hackett.”

“In the case of Factorial’s sourcing partners, Hartman said they could write checks individually, and they do often invest their own money alongside the firm. But when they bring deals to Factorial, they can make bigger bets (the firm typically invests $500,000) and then receive half the carried interest from those deals.”

“Hartman is not yet disclosing the size of his first fund, but he’s targeting 30 startup investments.”

Sunday, Apr. 26th: I listened to a Business Breakdown podcast episode on Kaspi which is Kazakhstan-based super app integrating payments, e-commerce, financial services, and government solutions. Thanks Paul for this one! - Kaspi

Kapsi is a leading financial technology company based in Kazakhstan. It operates as a “super app” offering a comprehensive range of services, including:

Payments and digital wallets: Kaspi provides a payment network, peer-to-peer payment solutions, QR payments, and business-to-business (B2B) payments.

E-commerce: its marketplace works like Amazon or Alibaba, providing a wide range of products, from electronics to groceries, with fast delivery options.

Financial Services: it includes buy-now-pay-later (BNPL) options, loans, and financial services for consumers and merchants.

Government Services: Kaspi enables digital access to various government services, such as registering a business, renewing licenses, or obtaining documents like birth certificates.

Customer centricity. Kaspi focuses on enhancing user lives with seamless, high-quality services. NPS guides product development and improvement through feedback. With strong user engagement, 67% of monthly users interact with the app daily.

Super App strategy. Kaspi integrates multiple services—payments, e-commerce, financial services, and government services—into one app, creating a closed ecosystem that enhances user convenience and loyalty. Its success with the super app model demonstrates the value of interconnected services and network effects, where one service promotes and supports another.

Metrics:

$2bn net income (+25% YoY)

$20bn market cap

Every business vertical achieves profitability, even new ventures like groceries, which became profitable within 12 months

14m MAUs (70% of the country’s population) and 67% of MAUs visit the app daily

Kazakhstan transitioned from 10-15% cashless in 2016 to 90% today, with Kaspi as the driver

Monday, Jan. 27th: a16z announced the closure of its London office, just a year after its 2023 opening, to refocus on the US market. The firm's initial London expansion was aimed at tapping into the UK's crypto industry amidst increasing regulatory scrutiny in the US. In the UK, a16z invested in companies like Arweave, Aztec, and Improbable. The firm's renewed focus on the US market is likely driven by the recent shift in the US crypto regulatory landscape. - FT

“One UK official downplayed the US investor’s reduced ambitions in the country, saying: “They were never really here.””

Tuesday, Jan. 28th: Lightspeed led a $2bn funding round in Anthropic at a $60bn valuation. It also participated in other AI mega-rounds including Databricks’ latest round at $62bn valuation and xAI’s latest round at $50bn valuation. - Bloomberg

“For venture capitalists, there is rising pressure — particularly on those that missed the chance to back the top AI companies at lower prices — to align themselves with the leading players before it’s too late, investors said.”

“Lightspeed is best known for savvy investments in consumer technology, fintech and enterprise software, making early bets on companies like Snap, Affirm Holdings Inc. and Rubrik Inc. Despite its track record, the firm has yet to become as much of a household name as some of the most famous tier one VC players. With its aggressive AI bets, insiders say these deals could permanently elevate its standing — if they succeed.”

“In December, it parted ways with its two lead consumer investors and said it was adjusting its consumer investing strategy to better suit the “age of AI”.

“In total, Lightspeed has already invested $2.2bn in AI deals, a figure that doesn’t include its latest Anthropic investment.”

“It’s nearing the end of a fundraising expected to bring in $7 billion, a person familiar with the matter said.”

“The recent proliferation of AI megadeals also speaks to a broader shift in VC: a departure from the traditional strategy of early-stage investments, where firms acquire larger stakes at lower valuations. Now, VC firms are paying a major premium, and betting that a small number of AI companies could ultimately be worth over $1 trillion.”

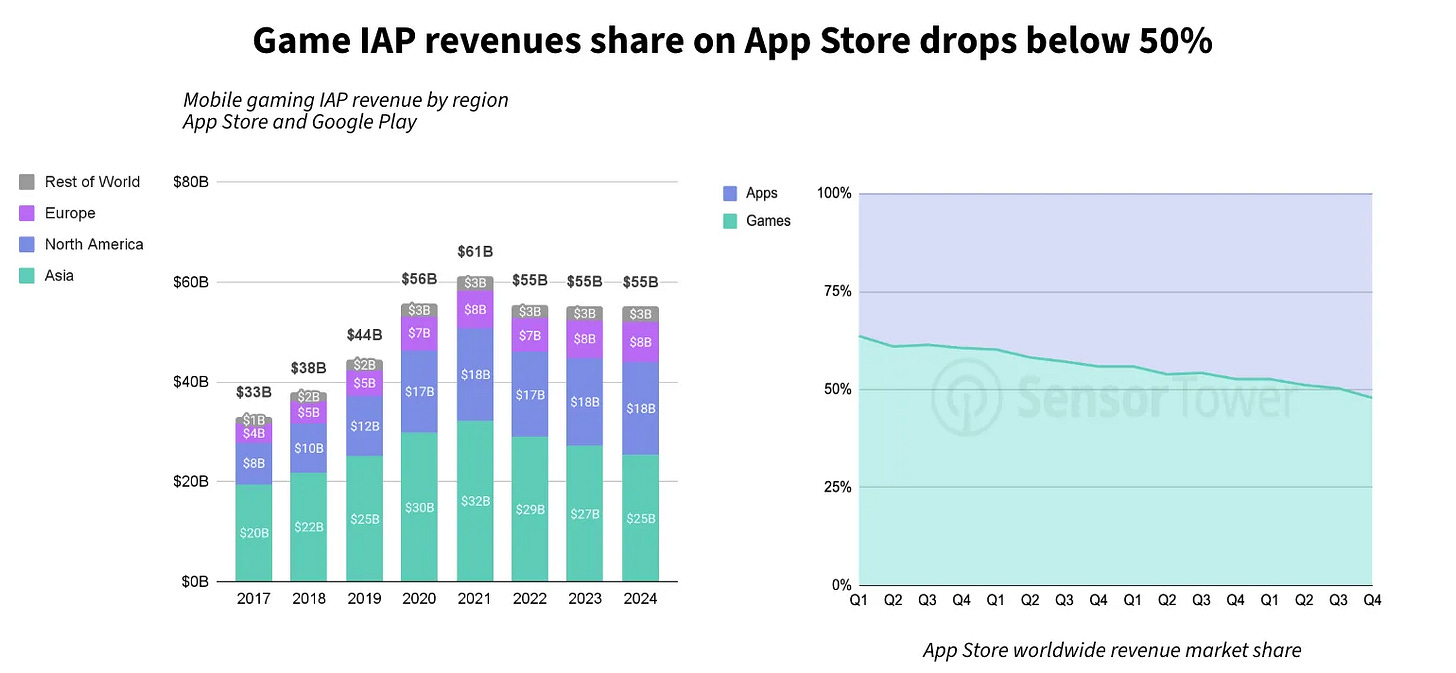

Wednesday, Jan. 29th: Deconstructor of Fun published its annual mobile gaming predictions for 2025. - DoF

“Competition for media consumption has intensified with streaming, shopping, and social media platforms taking an ever larger portion of consumers’ screen time - and wallet. As a result, apps account today for more than 50% of all in-app purchase revenues growing past the stagnated mobile gaming revenues.”

“2025 will be a better year for games than the year prior. The real issue is that the pie is not growing. The mobile market has finally matured after a decade of double-digit growth. Game companies achieve growth by ‘stealing players’. Today we are living in a market where a “winner-takes-all” approach prevails. Only those with the deepest pockets can fully utilize it.”

“Subscription service funding dry out. For the past couple of years Netflix, Apple, and Microsoft offered big checks to grow their game catalogs. But unfortunately, those days are coming towards the end.” “Xbox Game Pass has missed its sales targets now three years running.” Subscription gaming does not work for 3 key reasons: (i) most of the engagement on all platforms goes into free to play games, (ii) expensive back catalogs these services have amassed of 2-5-year-old games are not as attractive, (iii) no incentives for the best developers to launch on these platforms.

Thursday, Jan. 30th: IFS, a European provider of vertical software for the manufacturing industry, achieved €1bn in ARR in 2024 (+32% YoY). The company also added 350 new customers, including industry giants like Comcast, E.On, Miele, and Rolls-Royce. IFS offers cloud-based ERP, enterprise asset management, and service management solutions to diverse manufacturing segments, such as aerospace, defense, and energy. - IFS

In 2024, IFS acquired 2 businesses: Copperleaf (asset management and asset investment planning) and EmpowerMX (aviation maintenance software provider).

Friday, Jan. 31th: The FT recently reported on Mistral's challenges in competing against US and Chinese rivals in the global AI race. - FT

“Mistral was founded on the idea it had discovered more efficient ways to build and deploy AI systems than its bigger competitors.”

“Its biggest US rivals now have war chests that are 10 times bigger.”

“Arthur Mensch insists that Mistral is not for sale and indicates that it hopes to go public one day.”

“One investor in Mistral is less bullish in private. “They are starting to see the writing on the wall,” says the person. “They need to sell themselves.””

“Aleph Alpha, once Germany’s hope for an LLM domestic champion, pivoted away from LLMs last year, leaving Mistral as the only consequential player in Europe.”

“If Mistral fizzles, then Europe’s businesses and consumers will have little choice but to depend on a handful of American — or Chinese — platforms.” “[Tech] sovereignty for Europe is more important now than it ever was before.”

“What was even more frustrating was that much of the research going into LLMs was actually being done by European scientists,” says Samuelian-Werve, a respected figure in global tech circles.

“With 100 times less [computing power than US rivals], we’ve been able to make models that are pretty much on the frontier,” Mensch tells the Financial Times.

“Technical benchmarking sites, such as RankedAI.co, place Mistral among the world’s top 10 model developers. But newer rivals, not least China’s DeepSeek, are threatening to overtake it.”

“DeepSeek’s latest model as a jaw-drop moment. It’s going to change the economics of the whole industry.”

“They say that DeepSeek’s breakthrough only validates Mistral’s founding strategy that cutting-edge AI can be built for far less. They also highlight the control, privacy and neutrality that Mistral offers to corporate customers, in contrast to DeepSeek, which collects a lot of data and adheres to Chinese censorship.”

“It has raised too much to fade quietly into the background, yet not enough to keep up in the global AI race. It has around 150 employees, compared with thousands employed by its US rivals.”

“Maher predicts that Mistral will go the way of Adept and Inflection — promising AI start-ups whose talent was “acquihired” by Big Tech.”

“It’s extraordinary what they have been able to achieve, but they are the last gasp of the old paradigm — trying to play the scale game with a tenth of the resources of their rivals”

“As such, the company is rapidly expanding its Silicon Valley offices, both to attract engineering talent and to sell to US customers.”

“Mistral won early fans in the software developer community because its “open source” origins means some of its models are available under a licence that allows users to examine the “weights” that shape the output or make derivative works. But Mistral’s more advanced models, such as a well-received new programming tool, are only available commercially and it has struck cloud distribution deals with Microsoft, Amazon and Google.”

“One such customer is the French defence ministry, which recently signed a deal with Mistral after benchmarking its open-source models against those from Google and Meta.”

“Mistral also has several prominent French companies as customers, such as bank BNP Paribas, the shipping company CMA-CGM, and the telecom operator Orange. But Mistral insists that it is global: a third of its revenue now comes from the US, where its customers include consumer giant Mars and tech companies IBM and Cisco. European customers include online retailer Zalando and enterprise software maker SAP.”

“Its annualised revenue run rate — a measure that extrapolates from its most recent monthly performance — is in the tens of millions of dollars.”

“A study by Menlo Ventures, a Silicon Valley VC firm, ranked Mistral fifth in the enterprise AI market, with a market share of just 5 per cent last year — less than half Google or Meta’s share and far behind OpenAI.”