📖 Venture Chronicles - January 2024

Overlooked #167

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of January.

Monday, Jan. 1st: Howard Marks published a new memo called Easy Money. - Howard Marks

“Declining and ultra-low interest rates had a huge but underrated influence on the period in question. They made it: (i) easy to run a business, with the stimulated economy growing unabated for more than a decade; (ii) easy for investors to enjoy asset appreciation; (iii) easy and cheap to lever investments; (iv) easy and cheap for businesses to obtain financing; and (v) easy to avoid default and bankrupt. In short, these were easy times, fueled by easy money.”

“Low interest rates encourage risk taking, leading to potentially unwise investments.” “The ultra-low returns on safe assets cause some investors to take additional risks to access higher returns. Thus, these investors become what my late father-in-law called “handcuff volunteers” – they move further out on the risk curve not because they want to, but because they believe it’s the only way to achieve the returns they seek.”

“I love Hayek’s word “malinvestment,” because of the validity of the idea behind it: in low-return times, investments are made that shouldn’t be made; buildings are built that shouldn’t be built; and risks are borne that shouldn’t be borne.”

Tuesday, Jan. 2nd: I listened to a Colossus’ podcast episode on Visma with Nic Humphries who is executive chairman at Hg Capital which owns 50% of Visma and which initially invested in the company in 2006 at a $450m valuation. Today, Visma is worth $21bn. In 2023, it generated $2.5bn in revenues and $800m in EBITDA. It has 15k employees and offers HR, accounting and payroll products in the Nordics, Benelux and Baltics. - Colossus

Visma is the European equivalent of Intuit. It provides daily mission-critical use software for small businesses (e.g. bookkeeping or payroll).

Visam is highly countercyclical because it provides business-critical software that companies require to operate effectively. “It’s pretty much the last thing you turn off before you turn off the lights on the business and appoint a receiver.”

“When you build a business that has established [a brand and a reputation for being extremely strong at compliance] within a particular geography, it's often a go-to product for the customers because they know it works, they know they're not taking any risk with regulatory compliance.”

“The business has continued to do a succession of relatively small tuck-in M&A transactions, essentially using M&A to add high-quality SaaS products around those core bookkeeping and payroll applications. And so it makes about 30 to 40 relatively small acquisitions per year.”

As the Nordics are more advanced in terms of digital adoption (internet penetration, mobile penetration, SaaS/cloud adoption, AI/ML adoption) compared to other European countries, it allows Visma to see the future 5 years in advance and deploy it in other European geographies.

Visma does not force a heavy integration of the companies it acquires. It lets its entrepreneurs run their historical business independently. Visma streamlines financial reporting, cash flow management, cybersecurity and development practices but product and go-to-market continue to be fully driven by acquired entrepreneurs. “The number one thing that we have to maintain as we scale is keep that entrepreneurial spirit because that's what's actually driving the superior organic revenue growth.”

Visma reinvests its cash back to the business to fund the SaaS product development and to invest in accretive M&A. “Visma believes it can acquire high-quality, high-growth SaaS businesses at prices that are attractive to the entrepreneurs that are selling, but also accretive to its model going forward.”

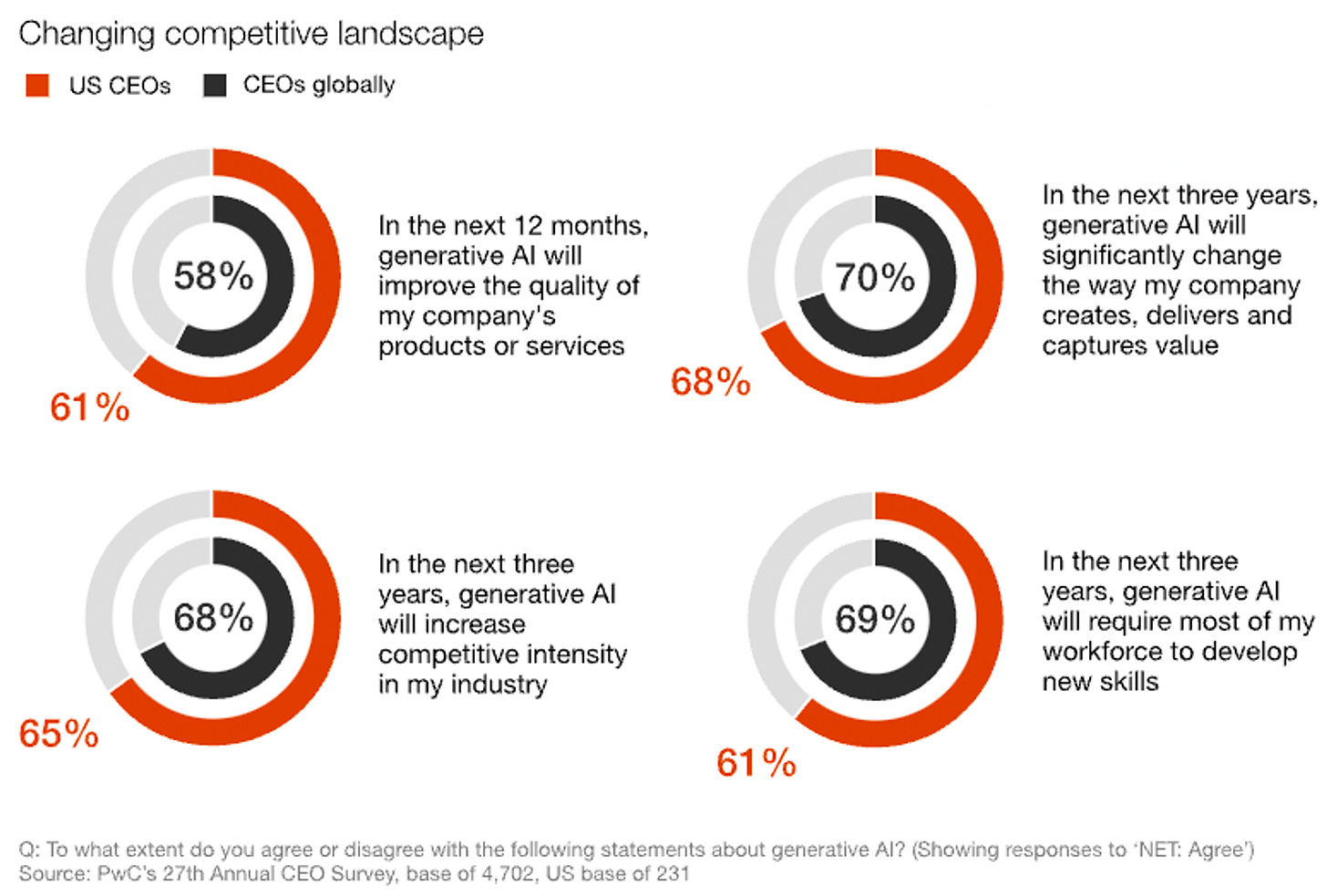

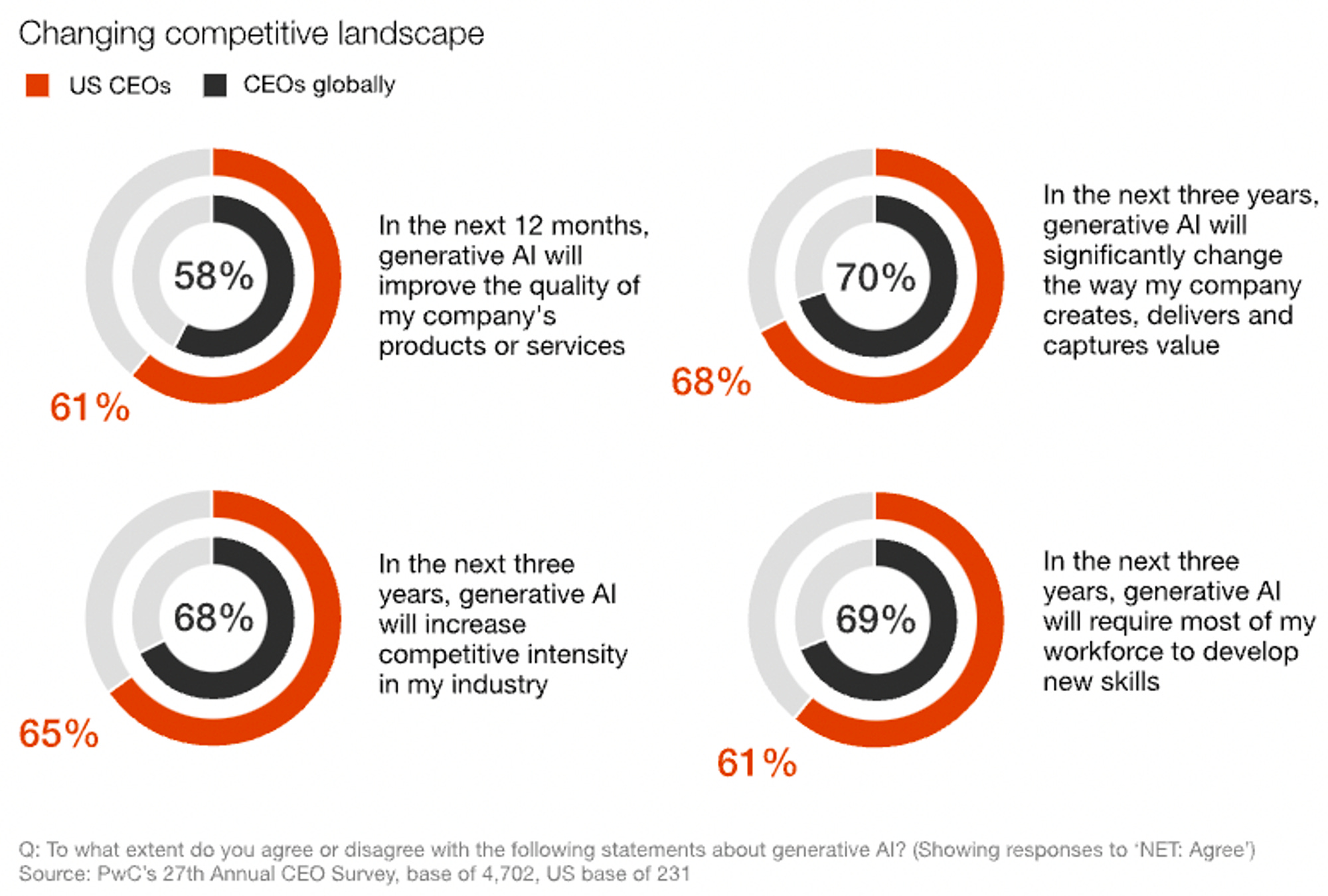

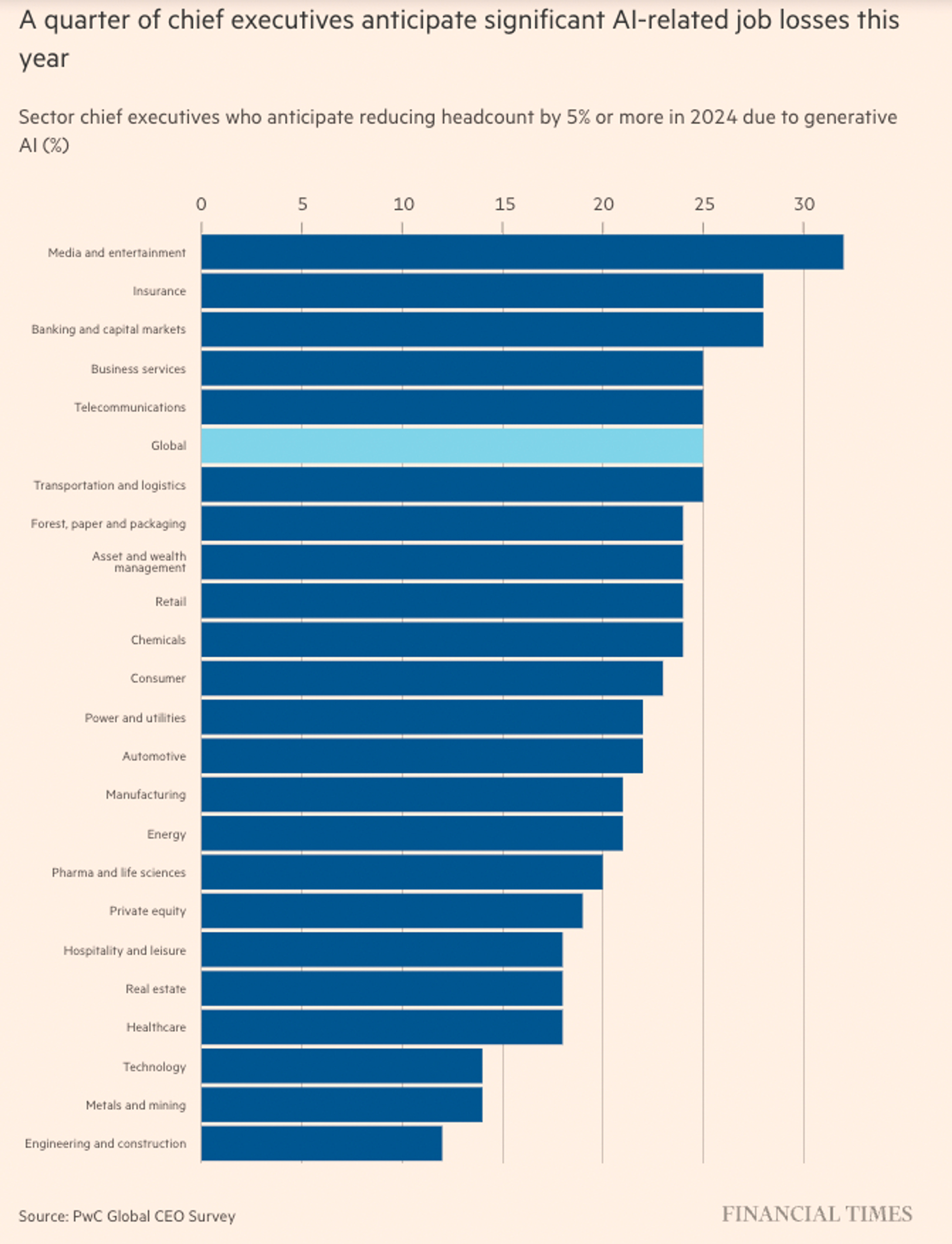

Wednesday, Jan. 3rd: 25% of global CEOs believe that productivity gains from generative AI will allow them to reduce their headcount by 5%. - FT, PwC

46% of CEOs expect the use of Gen. AI to boost profitability in the next 12 months while 47% of them say that the technology will deliver little to no changes.

32% of CEOs said that their company adopted Gen. AI across their company in 2023.

61% of CEOs except that Gen. AI will improve the quality of their products and services.

Thursday, Jan. 4th: I discovered an awful story involving a vertical SaaS in the UK, used by the UK Post Office, whose faulty payment system led to the wrongful prosecution of over 900 postmasters between 1999 and 2015. The disaster stemmed from errors in the Post Office's Horizon IT system, developed by the Japanese company Fujitsu. - The Economist

“The Horizon system falsely reported shortfalls in the accounts of various Post Office branches, leading to the prosecution of sub-postmasters who were held responsible for these discrepancies.”

“In the Netherlands an automated system for predicting child-benefit fraud malfunctioned; more than 1,000 children were taken into care before the prime minister, Mark Rutte, was forced to resign.”

“The potential for technology to improve the public sector is vast. But those in charge of government institutions cannot blindly rely on computers. When humans say there is a problem, they must listen.”

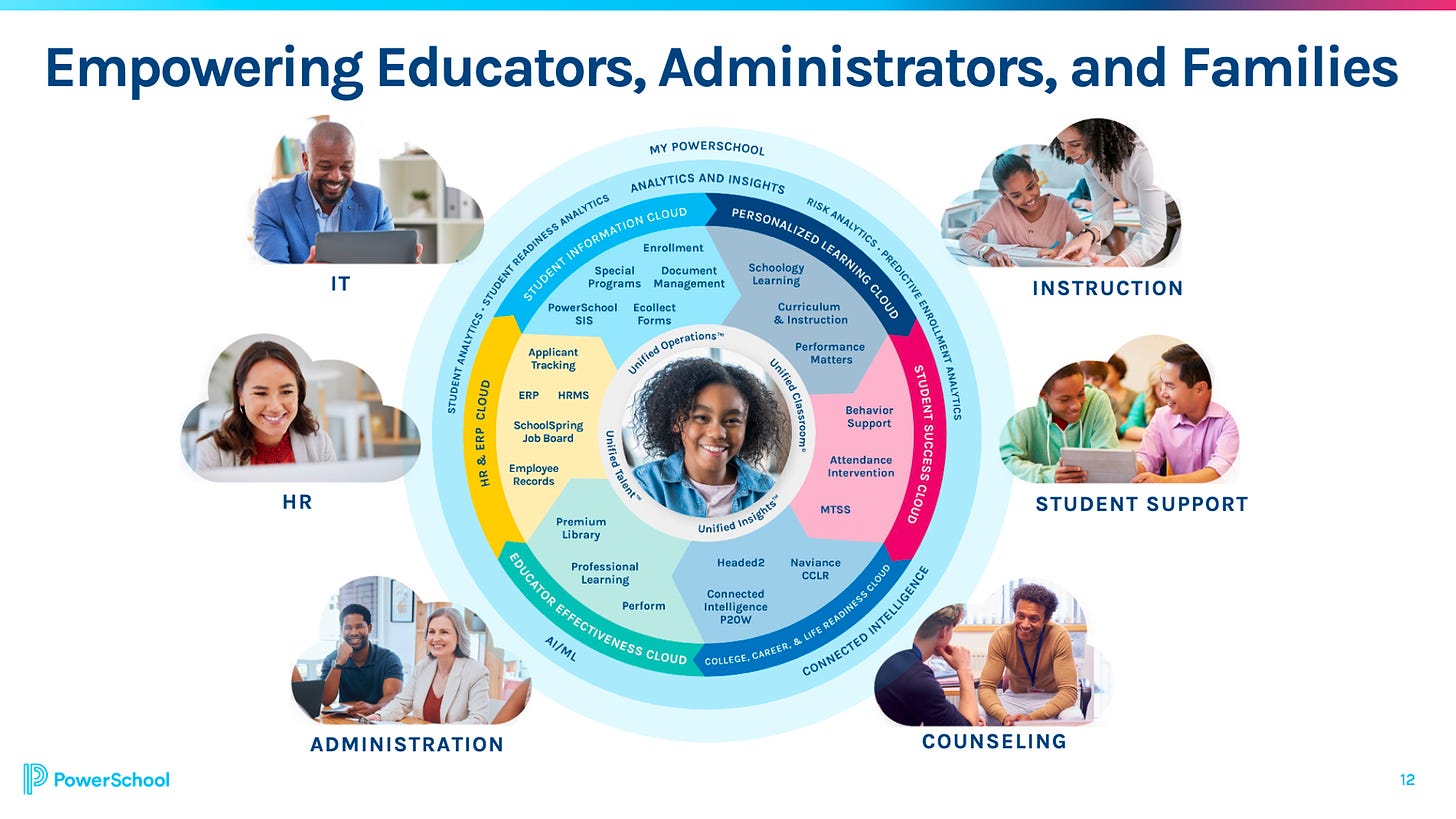

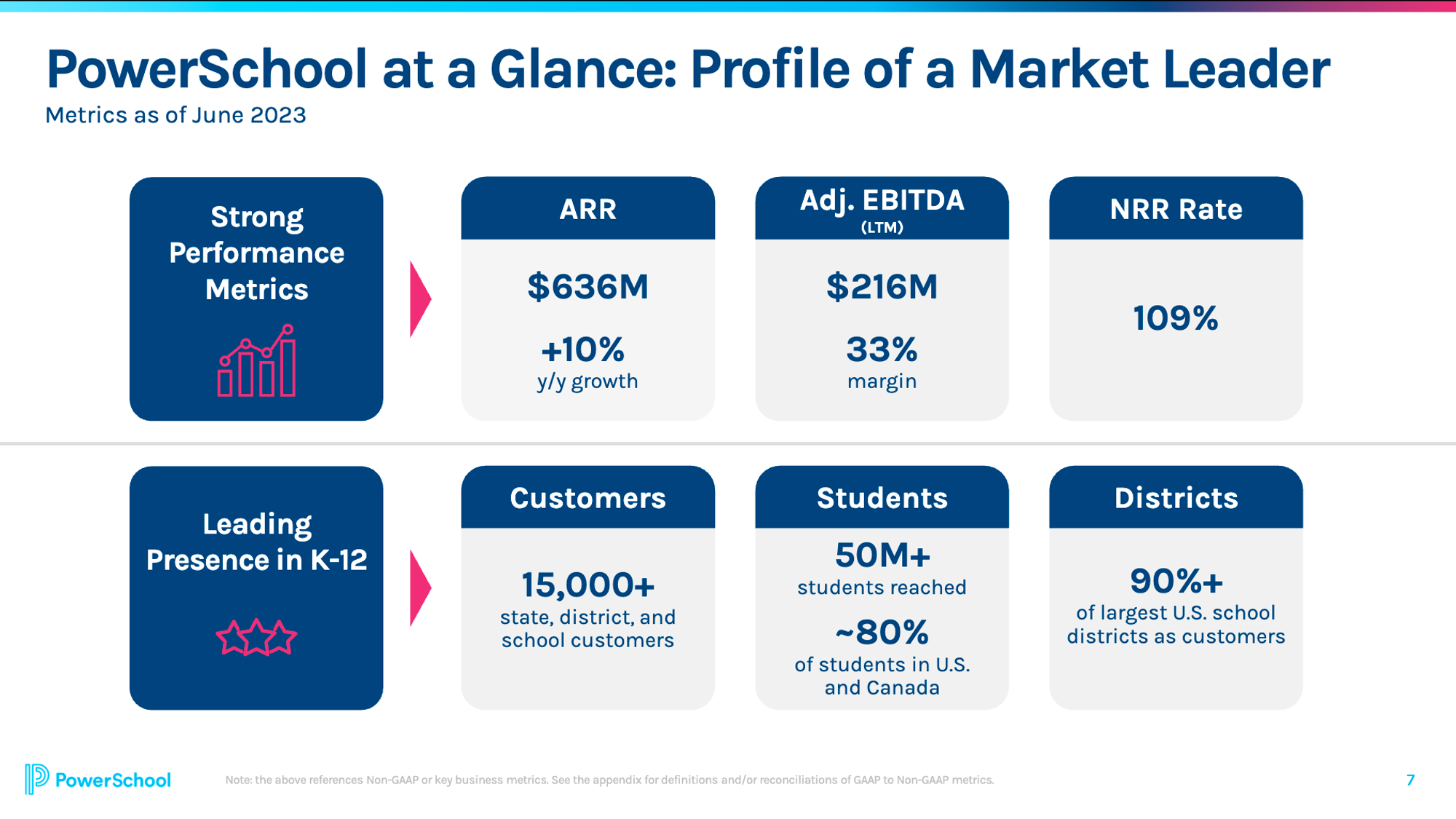

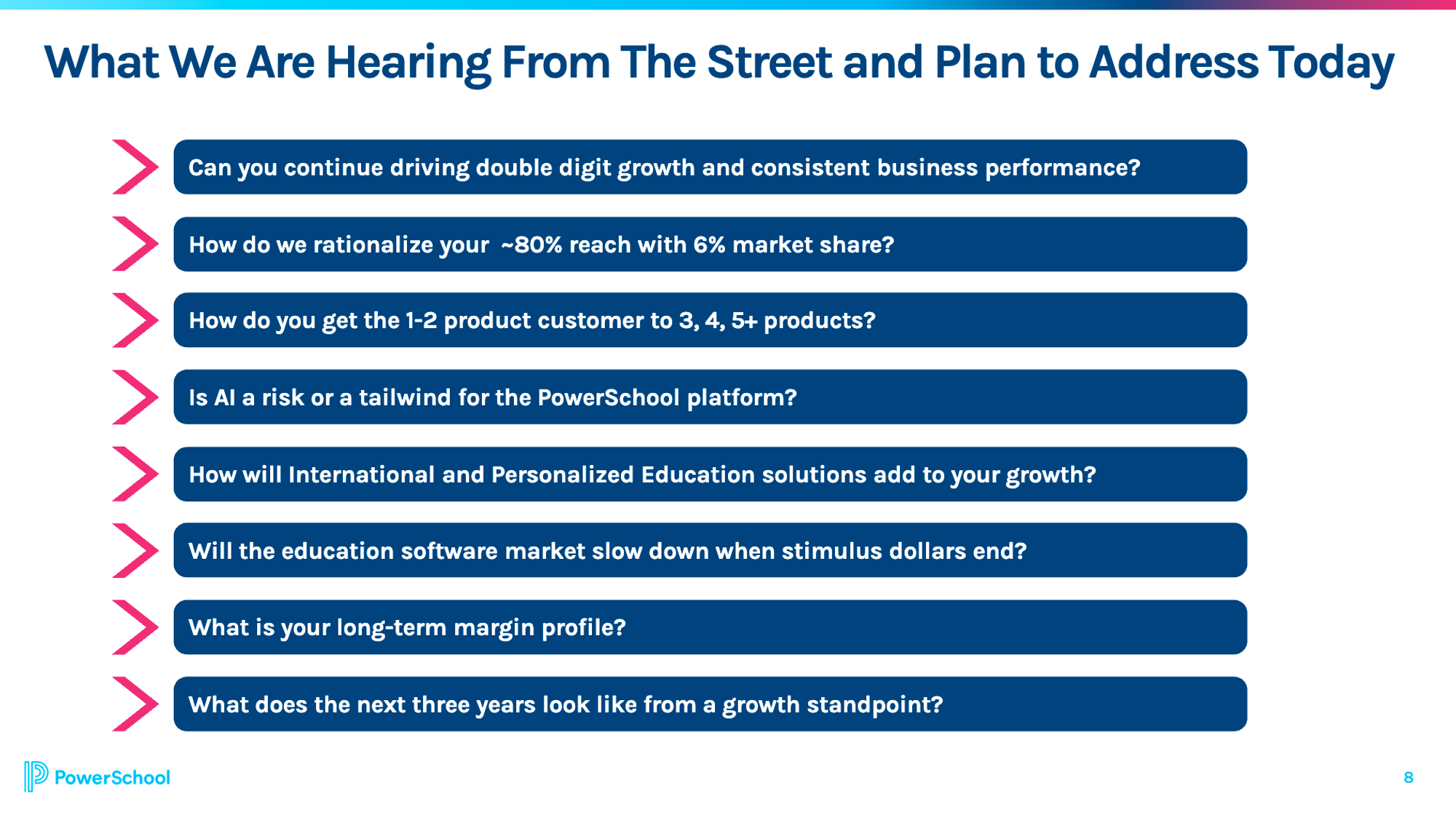

Friday, Jan. 5th: I read Goldman Sachs’ initiation coverage on PowerSchool which is a vertical SaaS in the education sector selling a Student Information System in North America.

“Founded in 1997, California-based PowerSchool is a provider of cloud-based software solutions to K-12 schools and school districts. PowerSchool’s product suite covers a wide range of use cases including state reporting and compliance, talent acquisition, registration, grading, assessments and analytics, among many more. Importantly, included in the company’s 12,000 customers are 45mn+ students, representing over 70% of the U.S. and Canada’s K-12 students.”

“PowerSchool’s primary offering is in Student Information Systems (SIS) in North America, and the company has built a significant competitive moat. PowerSchool introduced SIS in 1987 and has established leading market share at 32% over the last 34 years. SIS are in many ways the technology backbone of educational institutions, creating a foundation to build additional modules and technology on.”

“With SIS as its signature product, PowerSchool has built out a complete platform of software for K-12 schools across four additional solutions: Unified Classroom, Unified Talent, Unified Administration and Unified Insights, through a combination of organic development and acquisitions.”

“PowerSchool’s M&A strategy is best in class given its execution of 12 deals over the last 6 years to build a complete suite of integrated products for educators and administrators at a time when schools have a higher propensity to buy technology suites.”

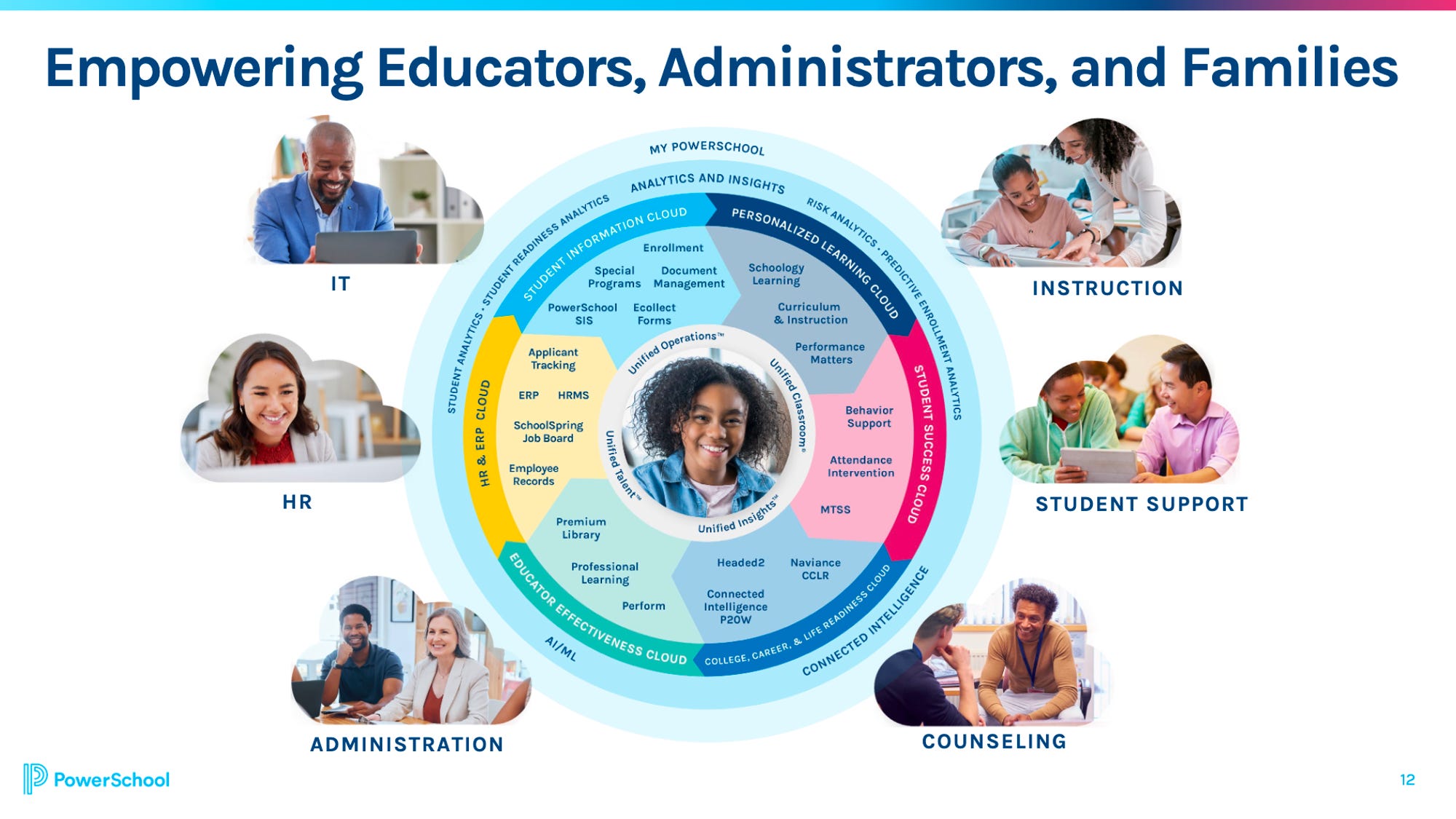

Saturday, Jan. 6th: I watched PowerSchool’s latest investor day. - PowerSchool

PowerSchool aims to generate $1bn in sales in 2026 (13% CAGR between 2023 and 2026). The growth will be mainly driven by cross sell and international expansion (targeting 10% of total sales in 3-5 years vs. 2% today). It also aims to have a 36% EBITDA margin (vs. 33% in 2023) thanks to gross margin expansion.

“The company still has significant runway with ~30% penetration in SIS (student information systems), 25% in Applicant Tracking, 20% in Enrollment, 20% in LMS (learning management systems), 20% in Professional Development, and ~10% in all other products.”

“PowerSchool's international strategy is focused on regions with large and growing K-12 student populations including 1) Middle East & Africa, 2) India, 3) Latin America, and 4) Southeast & Other Asia.”

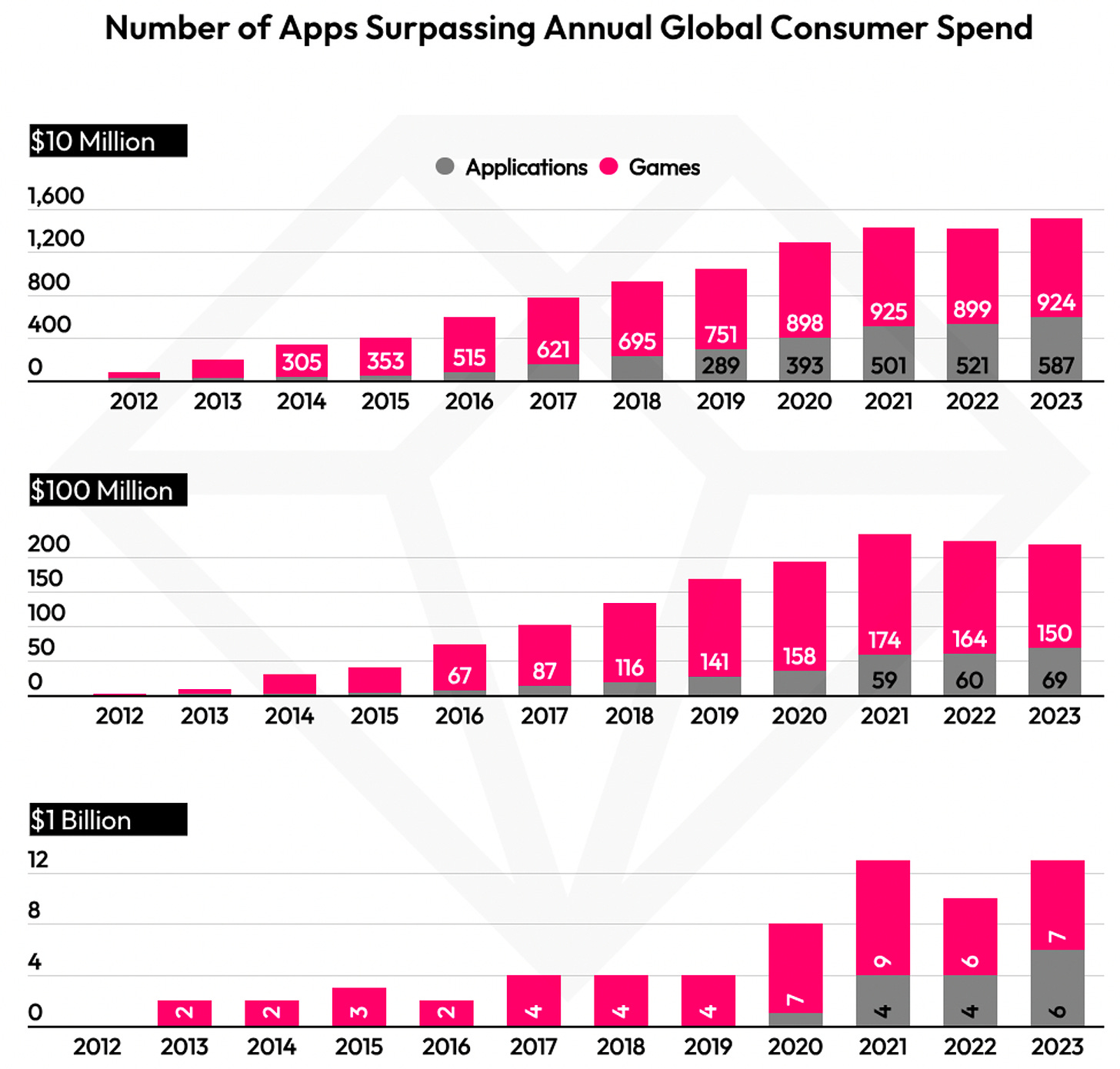

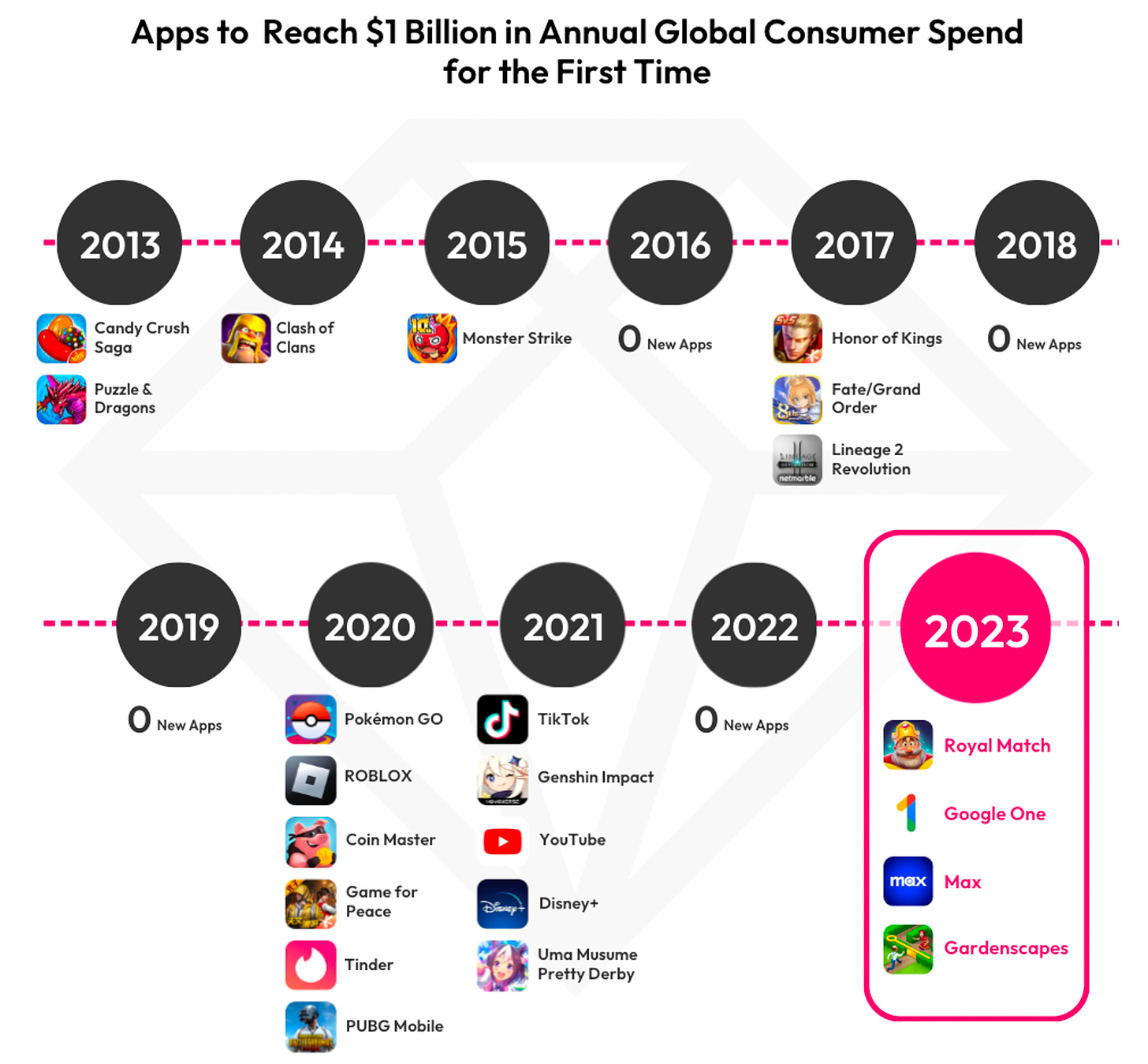

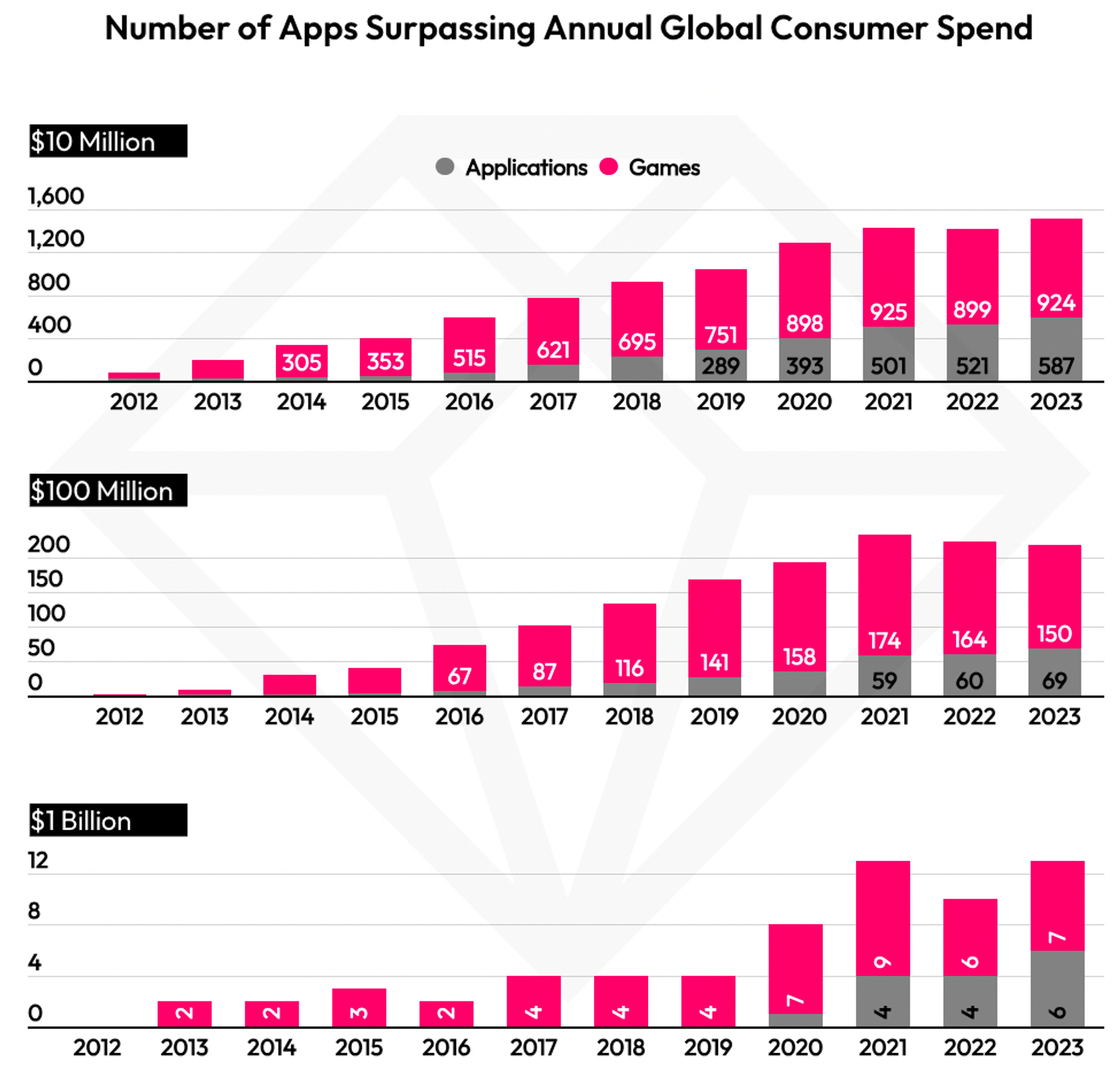

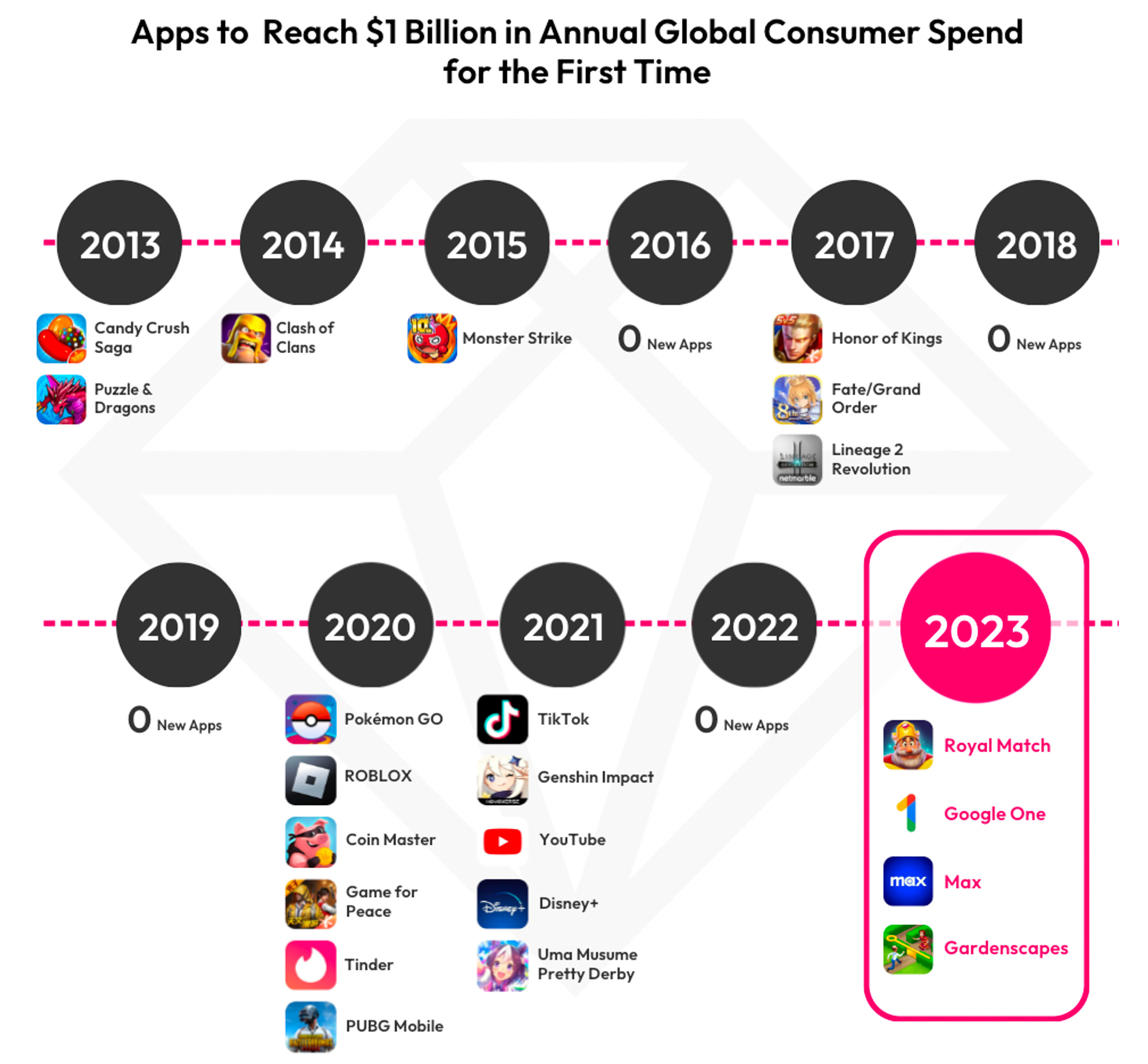

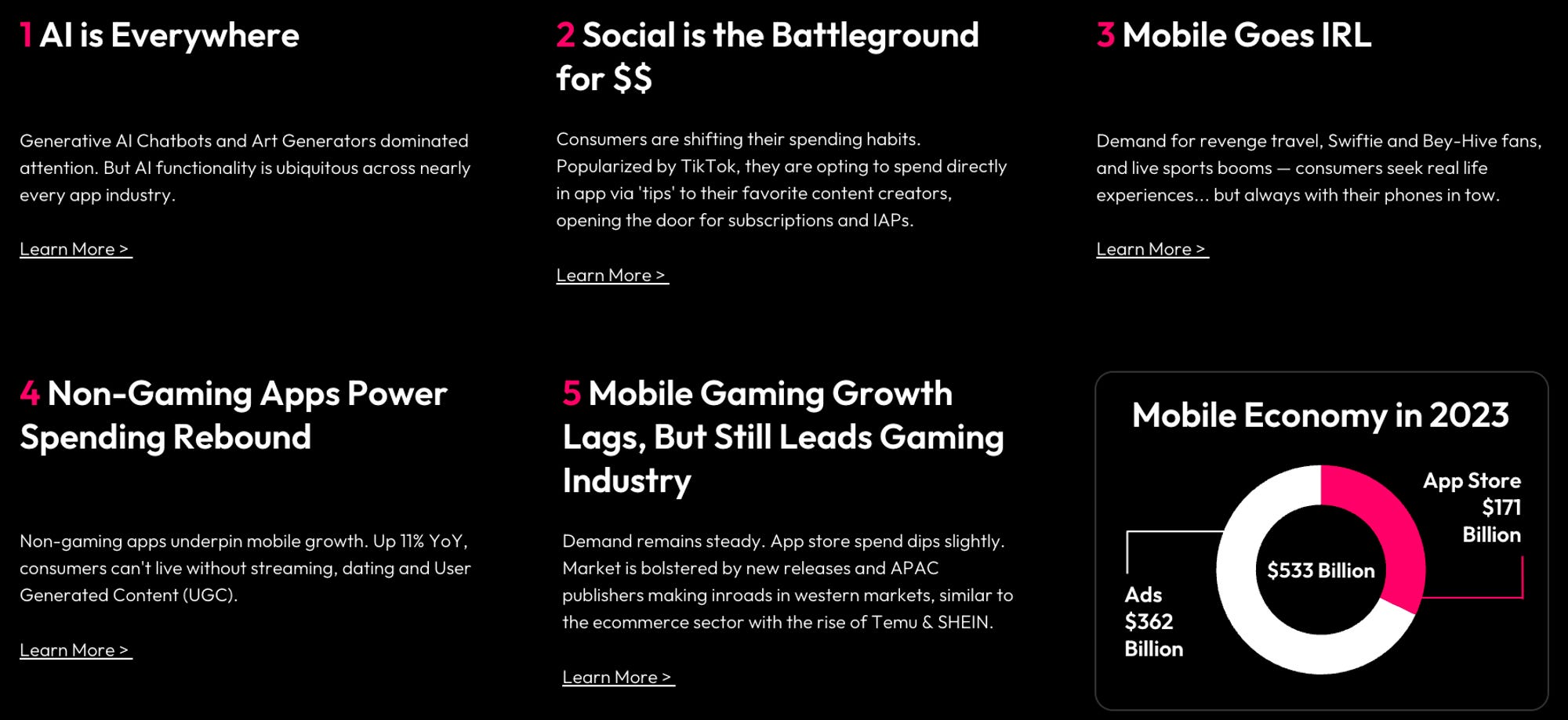

Sunday, Jan. 7th: Data.ai published its 2024 state of mobile with many insights on mobile apps and mobile games. - Data.ai

On average, we spend 5 hours per day on our mobile. In 2023, the mobile ecosystem registered 257bn downloads (1% YoY growth) and $171bn in spendings (3% YoY growth).

Ad spent on mobile is expected to reach $402bn in 2024 (11% YoY growth, $362bn in 2023).

150 games and 69 apps are making more than $100m in sales per year. 7 games and 6 apps are making more than $1bn in sales per year.

4x strategy games ($8.17bn), MMORPG ($7.17bn) and team battles ($7.05bn) are the mobile games’ genres generating most revenues.

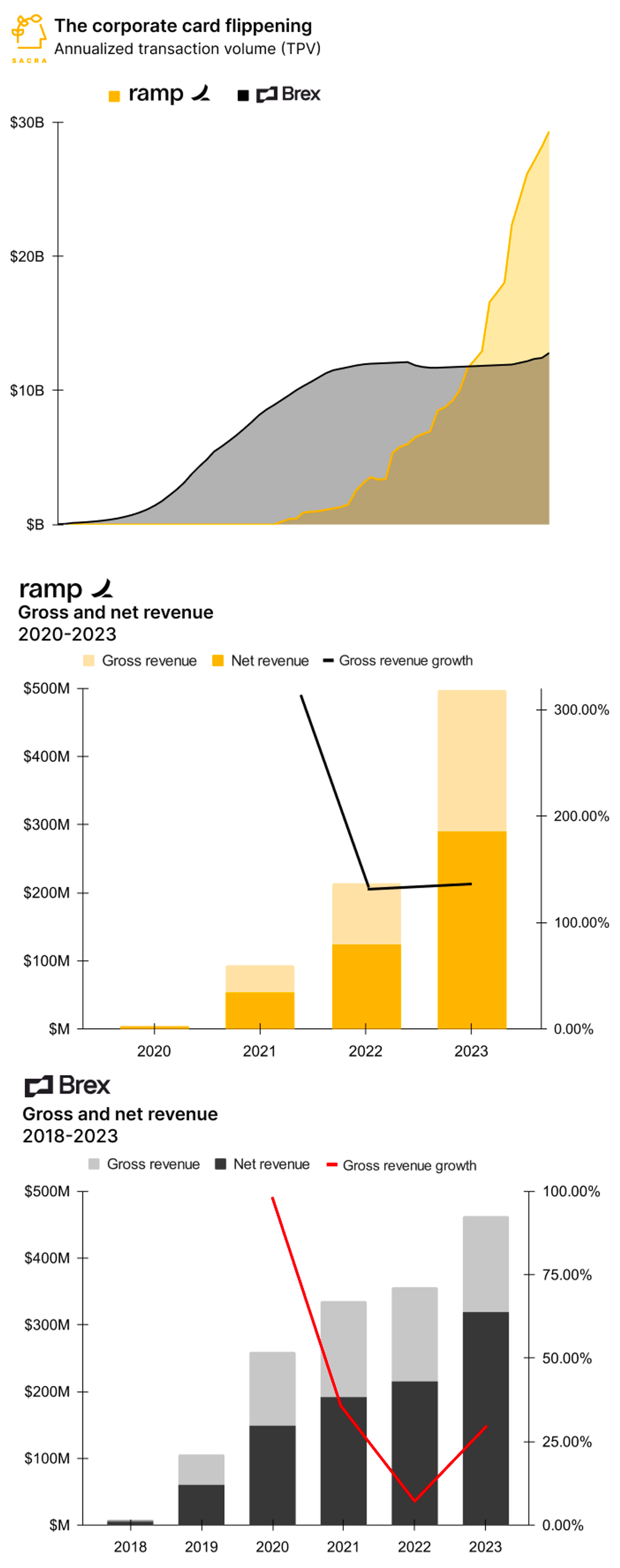

Monday, Jan. 8th: Brex laid off 20% of its workers. Brex burned $17m per month in Q4-23 (vs. $22m per month in Q4-22). In Q3-2023, Brex reached $283m in ARR growing at 1% QoQ and 40% YoY. In 2023, Brex refocused its customer base towards mid-market and enterprise customers. It also benefitted from the SVB’s failure to attract new customers. It aims to be cash flow positive and potentially go public in 2025. - Fortune, The Information

Tuesday, Jan. 9th: I listened to a This Week in Startups’ podcast episode with Bill Gurley and Brad Gerstner on the state of the tech market. - This Week in Startups

“2023 was the year that ZIRP funded startups finally started to die. ZIRP technically ended in Mar. 22 but startups started to die at scale only in 2023 due to the lagging nature of the venture funding market.”

c.1.5k companies died in 2023 (as Carta represents 50% of the market) which is the largest death toll for startups since the dot-com crash.

1.2k companies are expected to run out of money in 2024. It will force many companies to go out to fundraise, to go public, to be acquired or to shut down.

The venture industry is inherently cyclical driven by powerful waves in which it takes risk on very slowly and then risk off seems to happen overnight. In the upward part of a cycle, investors take more risks, valuations expand and founders/investors are less conservative on unit economics and profitability.

“What is different about this crash compared to previous crashes is that so many of the large startups had accumulated so much capital that the effects of the wave crashing are delayed rather than immediate.”

In 2021, most growth companies accumulated 2-3 years of cash. The day of the reckoning is happening when these companies are running out of cash. Moreover, valuation multiples have collapsed meaning that the vast majority of growth companies will raise at the valuation below what they previously had. It takes founders and investors a long time to process this information and build a strategy around it.

The rules have changed dramatically in venture when you compare today and 2020-2021 around the amount of risk you can take and the profitability profile that you should have. There is a chance that most companies will not be able to adapt to the new rules of the game.

“AI is living with an exemption and is acting like things were in venture 2-3 years ago.”

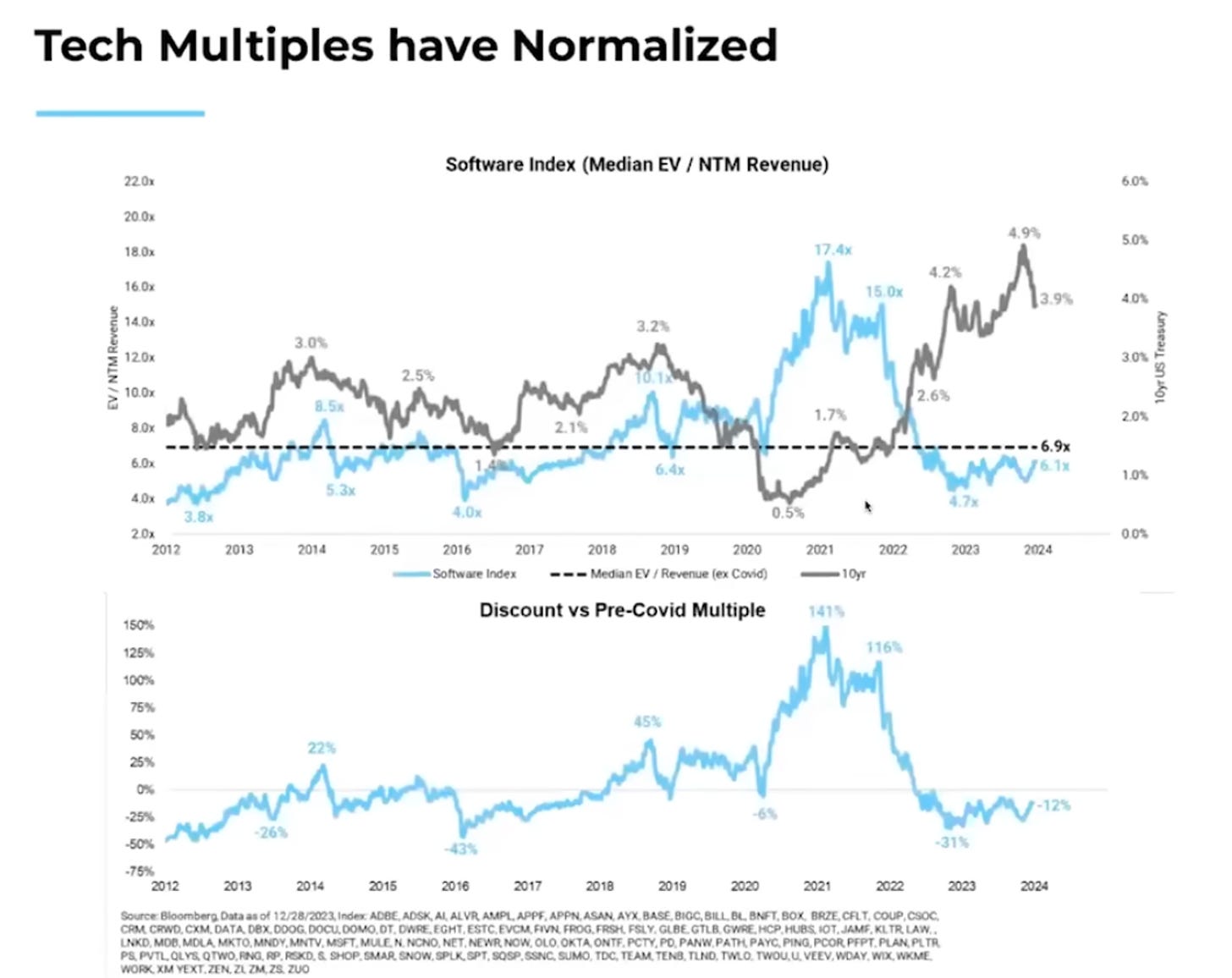

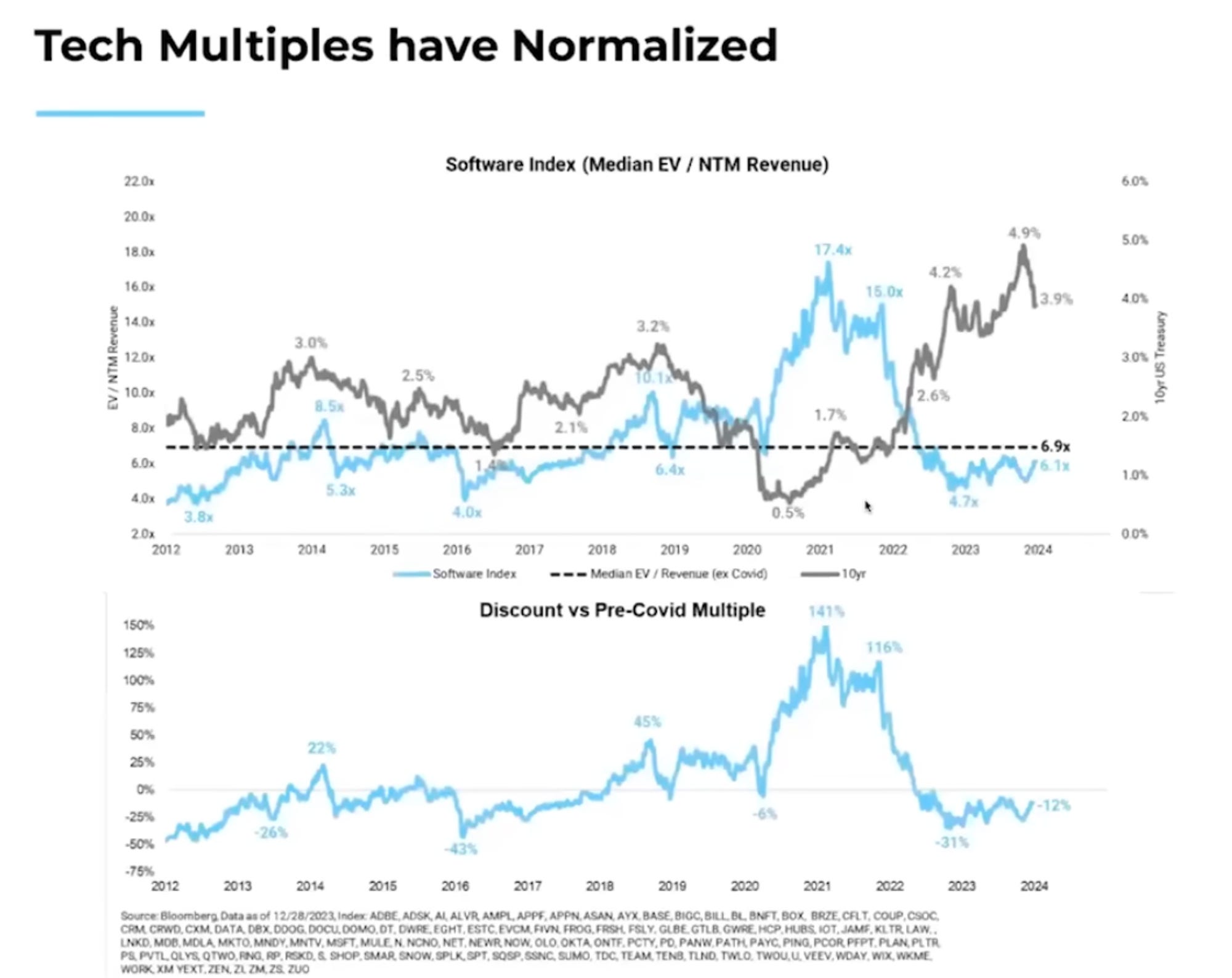

Since 2012, multiples were hugging around 6.5-7.0x EV/NTM Revenues. The ZIRP era in 2020-2021 boosted public market multiples driven by federal government’s stimulus packages and negative interest rates. Today, we’re still trading c.12% below the 10-year average multiple because interest rates are still high and growth rates are slower than they have ever been even if it has been balanced by more profitability.

“Less than 5% of the companies that were funded during 2020-2021 will ever be able to grow into the valuations from those prior periods.” Boards and founders are starting to be fine with this reality and are adapting their strategy with clearing valuation events (cf. Instacart’s IPO at $9.9bn valuation when it was valued at $40bn, Airplane’s acqui-hired by Airtable or Hopin distributing the cash on its balance sheet to its investors to rightsize the business).

“I don’t believe that you need to have $600m in revenues to go public. I think the only thing that kind of keeps people from going public is courage and determinism. There is going to be a little bit of discount but it will clean the cap. table and it will be a new baseline to grow from there. There is not magic window coming in 6-18 months from now where valuations are going to be 2-5x higher.”

In the last 10 years, a new class of investors emerged (e.g. Altimeter, Tiger, Greenoaks, Coatue) which are investing in private markets in $1bn+ companies which could go public (e.g. SpaceX, Stripe). These investors have a self interest in keeping these companies private for a long time because they can continue to put more capital at work in these companies.

“The idea that you can't innovate in the public markets is total nonsense. It’s a cheap source of capital, it keeps the valuation up to date and the company efficient. My sense is that the public market will open up in 2024-2025 with a strong backlog of IPO candidates as we had almost no IPOs in the past 2 years. IPO markets are always wide open. It's just a matter of price.”

During the ZIRP era, capital was used as weapon of economic destruction because the cost of capital was free funding the players n°2, n°3 and n°4 in a market that should have supported only a market leader. Without this, you reach scale and profitability at a faster pace.

In 2023, we were 90% down in terms of series B and series C of US based software companies. In 2021, we had this explosion of seed and series A deals and these companies are not finding a home in 2023.

It’s the best time to start a company because the environment is much more rational. You will have less competition. It will be easier to attract talent. Office real estate will be cheap. Windows of pessimism are really good times to start companies.

At this moment, you have to hold two simultaneous truths. AI is going to change everything is our world forever like the Internet did in 1999. At the same time, there are a lot of AI companies that are radically mis-priced because prices paid are assuming the bull case of the vision behind these companies when there is a lot of uncertainty. AI will play out over decades and not over a couple of months or years. As a venture investor, you’ve got to be in the game studying and understanding while being patient enough to wait for an asymmetric risk reward ratio.

Wednesday, Jan. 10th: I listened to a 20VC’s podcast episode with Jason Lemkin on 2024 predictions. - 20VC

Growth is SaaS was at all-time-low in 2023 growing only by 16% but the stock price went up because everyone became capital efficient by freezing hirings and cutting marketing costs. All the growth came from the customers base (vs. new logos) with price increases, long term contracts engagement and upsell. There is a real question-mark on how to get back to growth in 2024. It’s not going thanks to AI which will bring efficiency but which will hardly bring growth.

Many growth stage private companies have followed the same back to efficiency playbook and will need to re-accelerate growth in order to go public because they don’t want to be valued at low revenue multiples.

“I’m worried SaaS as an asset class will never experience strong revenue growth again and that public SaaS companies growing at a slow pace is the new normal. SaaS will not outgrow GDP in perpetuity and will reach maturity. At some point there is a risk that we are saturated with SaaS.”

At growth stage, you will see only decacorns hunters (vs. unicorns hunters before) and the tech ecosystem will be able to generate enough decacorns (e.g. OpenAI, Databricks, Stripe) so that few growth stage funds remain on the market with good financial returns (3x net). The venture industry has permanently changed from unicorns hunting to decacorns hunting series A and onwards.

There is a huge appetite for M&A. Companies are looking to grow again. Either you build a new product but a shortcut to do this is to buy existing products. Everyone is looking at tuck-in acquisitions of product doing $20m+ ARR that they can afford and can move the growth needle.

On Figma’s failed acquisition by Adobe, I think it does not discard mega M&A deals. At scale, companies will just buy adjacent plays rather directly competitive plays.

Thursday, Jan. 11th: l listened to a 20VC’s podcast episode with Keith Rabois about his recent career move to leave Founders Fund to move back Khosla. - 20VC

Keith previously spent 6 years at Khosla between 2013 and 2019. He was involved in the deployment of KV-IV, KV-V and KV-VI which produced significant returns. Since his departure for Founders Fund, Keith has kept co-investing massively with Khosla once per trimester (e.g. Traba, Varda).

Keith said that he was a better investor in the Khosla’s environment thanks to the contribution of the team in due diligence and decision making. Moreover, he was learning a lot from Khosla’s deep tech investments.

Within investment firms, you have social capital that you can burn to do non consensual investment decisions or pay expensive valuations and that you earn when your investments are performing.

At seed/series A, price is always a trap. When you’re not able to increase your offer at these stages, it means that you miss conviction. If everything goes right, you will make massive returns no matter the price you pay at seed/series A.

Friday, Jan. 12th: I listened to a 20VC’s podcast episode with Ed Sim at Boldstart and Jamin Ball at Altimeter. - 20VC

2024 is the year when challenges become real for startups because runway extension has its limits and profitability alone is not sufficient for a late stage startup - they also need growth.

In 2021, we crammed 5 years of growth funding into a 18 months period (2021 and first half of 2022). In 2023, growth funding down 90% compared to the peak and we’re back to the 2016-2017 trend line.

Historically, the fundraising cadence would work as following. You raise a round. You would hit 1-2 milestones and you will raise another round. In 2021, with ZIRP, everyone was risk on. Funds were no longer expecting milestones to invest capital in startups. It was the case at all stages. Today, to raise a round for these startups which raised at the peak, they need to deliver not only 1-2 milestones but 5-10 milestones and they need to grow by 5-10x to justify their valuation. At the same time, in 2022-23, macro-environment became complicated and many companies started to miss their plans. As a result, many startups are overvalued and under performing. Some of these companies are just saying that they have the cash to figure out if they have a real business. Smarter companies are already having the honest conversation about the long term viability of their business and about the right sizing of their balance sheet.

Seed is as competitive and expensive as ever. Inception rounds were off the chart last year. Seed was the only round that increased in valuation because of multi-stage founders investing at seed instead of other stages without being valuation sensitive. There is a massive bubble on inception rounds.

Having 24-36 months of cash does not mean that you have a business. At growth stage, you should have the conversation around questions like: 1/ do you have real business and do you have the energy and conviction to keep building? 2/ will you be able to grow in your valuation with your runway? and 3/ if you will not grow into your valuation what is the plan between shutting down, being acquired or raising a down round?

Many AI founders have crazy term sheets with valuations that are reminiscent to the 2021 pricing environment. The learning from the 2020-21 period should be that you don’t want to make the cap. table a risk to your business and you should raise smaller tranches of capital based on milestones achievements.

“Some founders know that if they set the bar too high from the very beginning it's going to be hard to kind of meet that expectation. Moreover, they know that every time they take a new check, they limit their exit options.”

“Everyone has had recently the realisation that they aren't that many special markets and in those special markets there's not that many special companies that exercise the right to be special right. In 2021, you were funded indiscriminately as you were going to be a public market type company meaning that you’re in a big enough market with a differentiated enough product that you can reach sustain a 30-50% YoY growth at a €100-200m ARR.”

“Everything is not always up and to the right. When you fund things that are way ahead of the market like new categories or completely different things, it always requires some extra capital to arrive to the break out moment. We funded Snyk and BigID three times before the company raised its series A.”

From a regulation standpoint, it’s really hard to see any large scale M&A. Many boards and founders will avoid taking this distracting route for customers and employees now that the likely decision will probably be a no go from the regulator.

For smaller scale M&A, the pool of large potential acquirers is limited creating a bottleneck on tech acquisitions. You will see both acquihires and you will see tuck-in acquisitions of tangential products that can be complementary to their platform. It’s a game of musical chairs because there are not many acquirer seats available per product category. Acquirers talk to 5-10 teams in the category they want to enter assessing product, team, traction and valuation and place their bets.

Many unicorns will also acquire smaller private companies to move from a single product to a platform with 2-3 products in order to become more ready to go public.

The IPO market is always open. You can always go public. It’s just a question of you accepting the market clearing price at that point in time. An IPO event is a key event for a private company because it clears the cap. table converting all the preferred shares into common and it refreshes the investor base. Moreover, it’s a source of cheap capital and it’s untrue that you cannot innovate in the public market (many companies have built Act 2, 3, 4 in the public market). Many private companies will reset the valuation of the business via an IPO and grow from there even if it means that they need to lower their valuation.

In order to go public, you need to be cash flow break-even, have 30%+ annual growth and be close to rule of 40/50 being slanted more towards growth than profitability.

The public market is a good forcing function to think about what it takes to build an enduring business over the next decades in terms of path to profitability, path from single product to multi-product platform, etc.

Saturday, Jan. 13th: InVision is shutting down. It reached a $2bn peak valuation and raised $350m from investors including GS and Spark Capital. - The Information, UXPlanet, InVision, HackerNews, Clark Valberg, UXDesign

It started as a collaborative prototyping tool for designers. It lost the category to Figma which made a single platform for designing and prototyping. InVision ended up selling its prototyping tool to its direct competitor Miro for less than $100m. Its revenues went down from $100m to $50m and it cut drastically its staff from 850 at its peak to 30 today.

“As a designer, it was amazing to how badly InVision was unable to move beyond their original simple prototyping platform. They were way ahead of the curve when they began and simply never did anything useful beyond that.”

“This is a reassuring signal that the market sometimes is entirely rational, and that product actually is more important than marketing/sales/distribution…at least in the design tools space. Invision focused on dumping millions into marketing and enterprise sales and growth hack. Yet, it had a mediocre piece of software. Meanwhile, Figma created a better product (and I’d guess spent way less on marketing for the first 5 years) and they won.”

“The reality is that Invision’s core product never made much sense as a long-term play in the first place. Any prototyping tool that exists separately from design functionality was always going to be clunky and limited. […] From day one it was only a matter of time before companies like Sketch and Figma cannibalized prototyping and handoff features for their own applications, while improving those workflows in ways that weren’t previously possible.”

“InVision did push to become a player in the UI design space. Unfortunately, the introduction of InVision Studio (the company’s answer to Sketch, Figma, and Adobe XD) was largely a flop.”

“InVision focused on marketing, sales, enterprise integrations, support staff, and basically everything under the sun except for the one thing that you’d think a design-centric company would remember: Actually having an exceptional product.”

“If nothing but to share an important takeaway for other founders, Figma is not why InVision failed. Simply, InVision failed because they stopped listening to customers. Figma built tools InVision customers had been asking for for years.”

Sunday, Jan. 14th: Pitch significantly downsized its team and changed its CEO. Pitch is building a next generation Powerpoint. It was founded in 2018 and raised over $137m including a $85m series B led by Lakestar and Tiger at a $600m valuation. Pitch used a portion of its cash to realign incentives between founders, investors and employees by reducing the ownership and the liquid preferences of investors. Pitch did not manage to reach exponential growth only growing 54% YoY in 2023 to reach €4.4m in ARR. - Christian Reber, Hana Mohan, Adam Renklint

“As many of you know, being a venture-backed company in 2023 was insanely challenging. We created sky-high expectations for our business, our employees, and ourselves as founders. Towards the end of last year, my co-founders and I noticed that those expectations were simply too high, and we decided that we wanted to take a new and completely different path for Pitch. Instead of pushing harder and harder to turn Pitch into a hyper-growth company with venture funding, we concluded it was better to build a profitable company and grow Pitch organically from here.”

“We generate >4.4m € in ARR, and we have more than 6m € in cash. We're changing course towards becoming profitable asap, with the remaining all-star team of ~40 people.”

Monday, Jan. 15th: I listened to a Colossus’ podcast episode with Jan Mohr who is the CEO at Chapters Group which is building Constellation Software for Europe. Thanks to Federico for this recommendation! - Colossus

Jan launched an investment firm at 25 years old called JMX seeded by Norman Rentrop who has a large publishing business and a large investment firm in Germany. He was doing long public investing in companies with undergoing changes and with a concentrated strategy into companies that could be held for the long term.

“One of the investor questions I'm always getting: you've arrived at that vertical market software scales the most in terms of where you can deploy capital so why didn't you only start doing vertical market software three years ago? If it was obvious, that's what we would have done. You learn by osmosis and conviction grows, and conviction doesn't jump from 0% to 100% overnight.” “Who we are today is really a result of last five years, which is a number of experiments.”

“If you build something by way of acquisition, by definition, you create a level of heterogeneity in the organization that you don't have if you build organically. It's just different. But if you build something by the way of acquisition, it's a must to have a management system.”

“Montessori has this concept around freedom within limits, so you would be very strict around setting limits for the child, but within the limits, you can be incredibly creative and free and empowered. I think that's a good mental model for what we want in terms of [operating and management systems].” “I think the guardrails are about how do we want the business to look like in five years. But within those limits, I want full empowerment of entrepreneurship and decentralization and empowerment.”

“If you look today at the type of work that is still analog, probably within Europe, in particular in Germany or France, it's mind boggling, how many processes are still pen and paper or some sort of hybrids (Excel + pen and paper + software).”

“Having a database and a unique solution to become more effective in your work is probably one of the strongest themes over the last 20 years and will be over the next 20 years.”

“Vertical markets software tend to be monopolists or duopolists, and they've gotten there in a very capital-efficient manner because normally, they have discovered and then served a customer need where you didn't really actively have to sell to customers in the classic sense, but there was just uptake for that solution.”

“Some of these verticals are tiny markets. And even if you own 60% of that market, you would be like €1-3m revenue business.”

“If you have the right management systems, you can run dozens of those software companies who, in aggregate, have the same business quality that one large homogeneous software company would have.”

There is an urgency to roll-up VMS in Europe because many owners are retiring or looking to retire in the next couple of years.

“Europe is a strange place. There are a lot of similarities between the countries. […] But when you boil down, the country-to-country differences are tremendous.” It does not work to acquire a software in a specific vertical with dominant market share in a European country and expand in other European countries for two reasons. First, you will always have local competitors in other European countries. Second, you have national specificities in each European country.”

“I think there is a unique window of opportunity to go out now. Maybe in 3-5 years, the opportunity is either gone because all the owner-operated businesses have professional ownership or there's way more competition.”

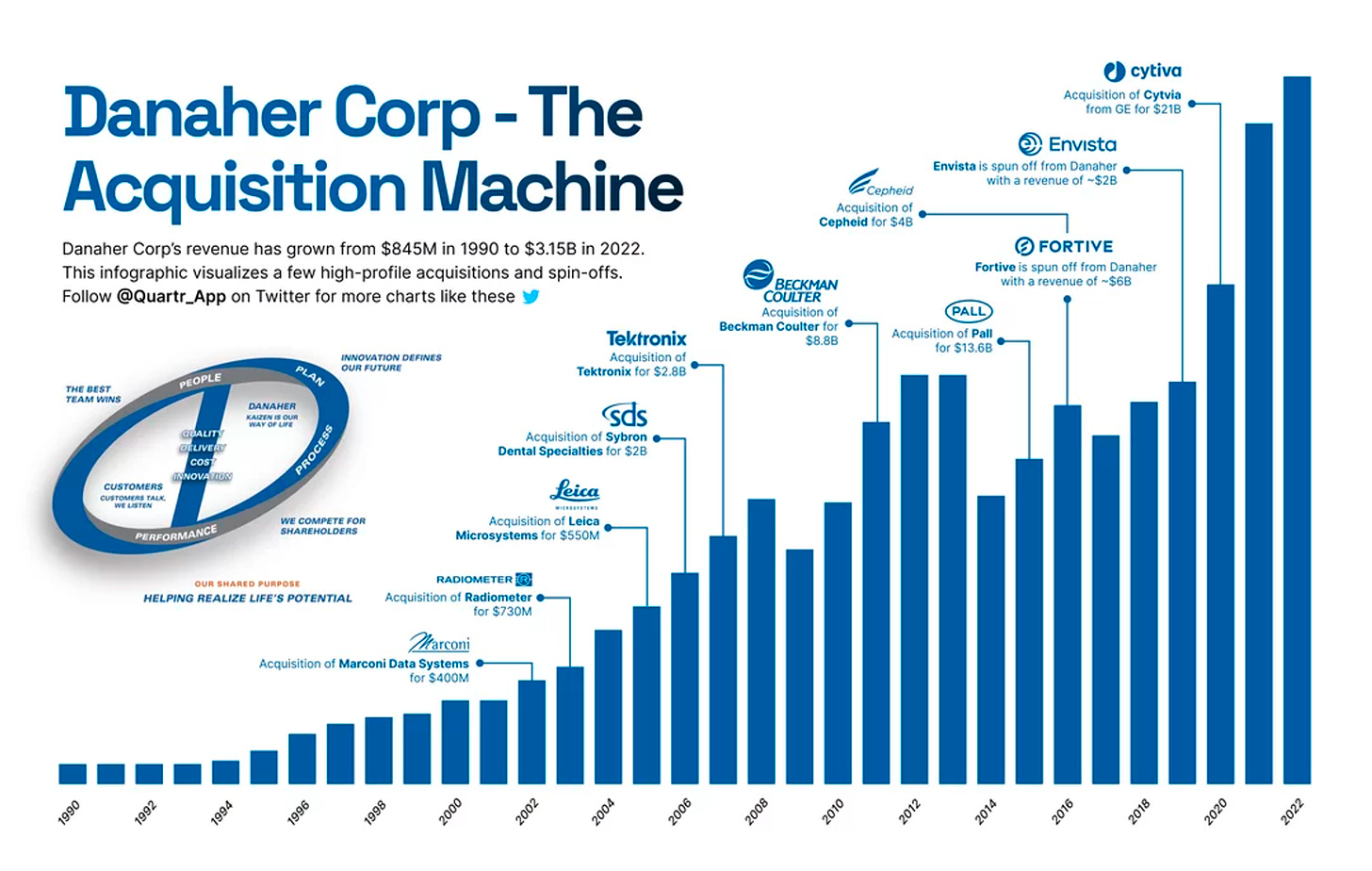

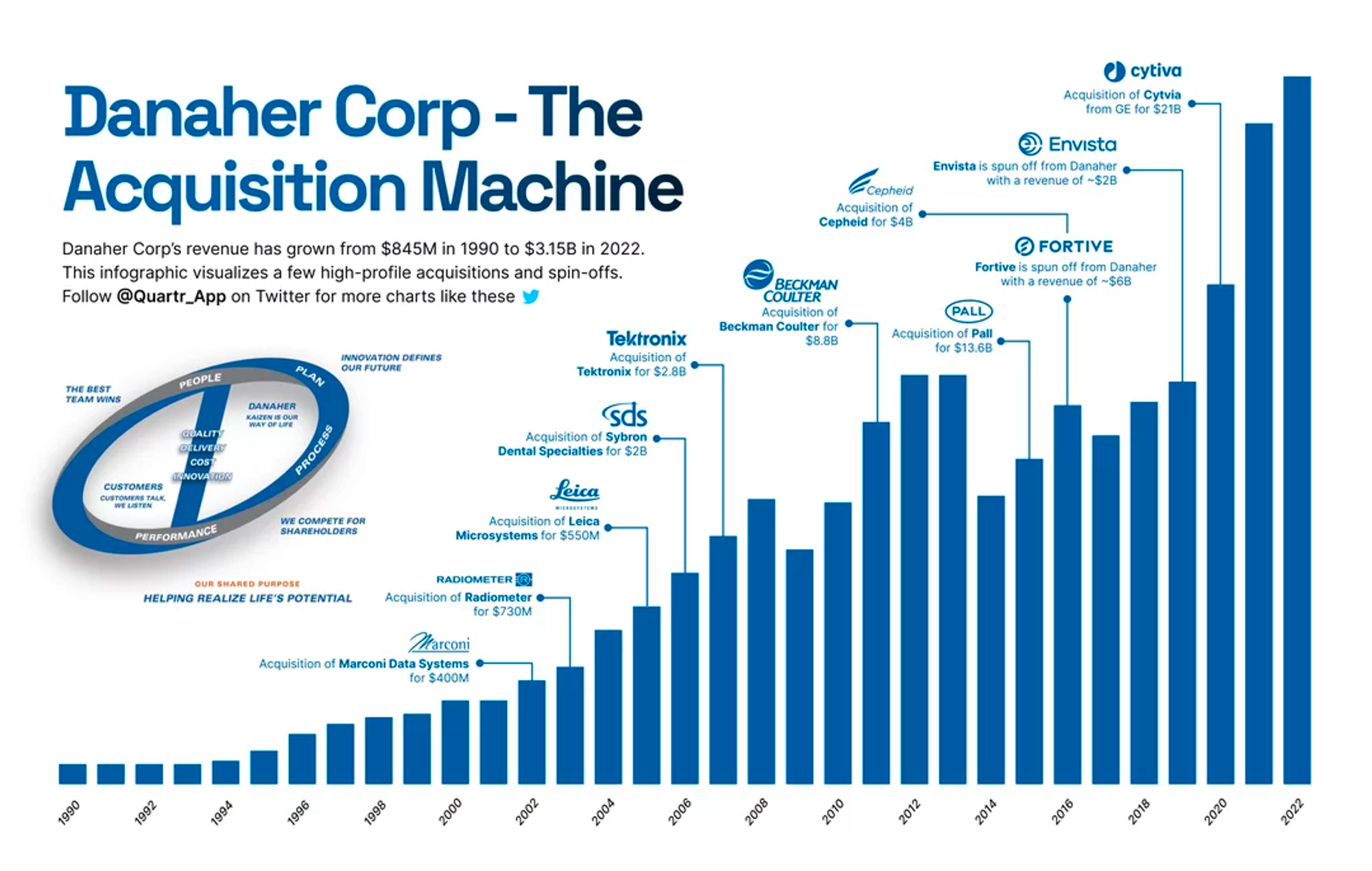

Tuesday, Jan. 16th: Quartr wrote about Danaher’s key business principles and M&A strategy. - Quartr

Danaher has a unique business system called Danaher Business System (DBS) which is based on the following core principles: (i) continuous improvement, (ii) customer first, (iii) innovation & risk taking, (iv) teamwork & collaboration, (v) accountability & results oriented, (vi) integrity & respect, (vii) leadership & development, (viii) problem solving, (ix) flexibility & adaptability, (x) global mindset.

“Danaher's journey, underpinned by the Danaher Business System (DBS) and its strategic capital allocation through acquisitions and spin-offs, is a remarkable story of value creation. The evolution of DBS from a set of operational tools to a comprehensive business philosophy, emphasizing continuous improvement, customer focus, and employee involvement, has been central to Danaher's enduring success. Coupled with a series of strategic acquisitions and thoughtful spin-offs, Danaher has not only diversified and strengthened its portfolio but also carved a niche for itself as a leader in life sciences, diagnostics, and technology sectors.”

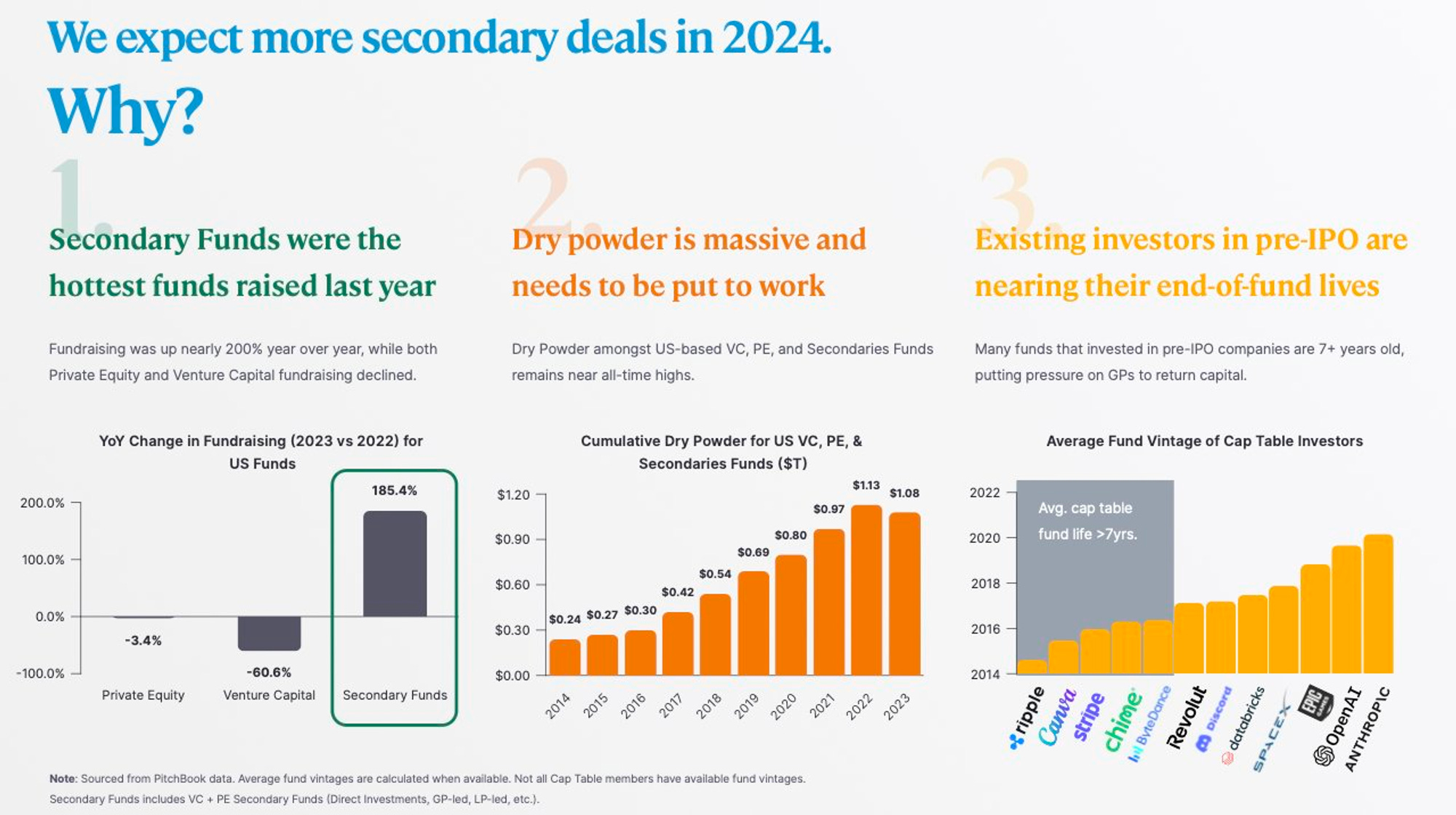

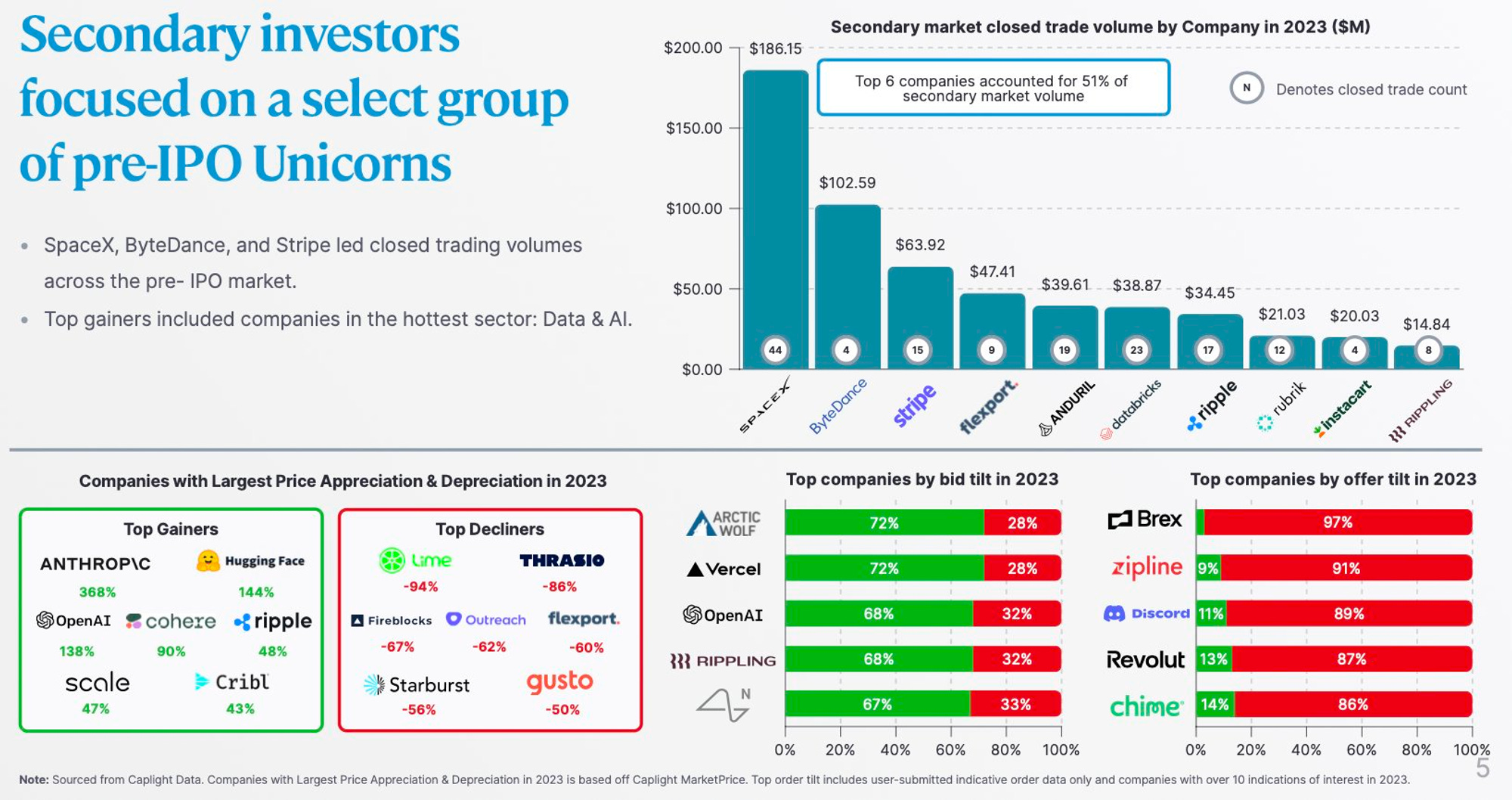

Wednesday, Jan. 17th: Contrary wrote a post predicting that we will see more secondary deals in 2024 driven by two main factors: (i) more secondary funds raised in 2022 and (ii) pressure on GPs to return capital on old funds. 6 companies (SpaceX, Bytedance, Stripe, Flexport, Anduril and Databricks) account for 51% of the total secondary volume. - Contrary

Thursday, Jan. 18th: Allocate interviewed VC managers and LPs to gather their insights for the venture market in 2024. - Allocate

“Managers who understand that their fund size dictates their investment strategy and who have a ruthlessly disciplined approach to sound portfolio construction will continue to benefit disproportionately during this market choppiness and dislocation.” - Adam Besvinick

“Angel investing activity plunged from 2021 to 2022 by more than 25%, according to one statistic. And 2023 was also a quiet year, with angels licking their wounds from markdowns and dealing with liquidity constraints. 2024 will be the year angels return to the scene with gusto and once again help shape pre-seed and seed rounds, as founders prioritize the unique wisdom of their fellow operators.” - Ben Casanocha

“Venture-backed companies are going to have a good year. Interest rates have stabilized and will start coming down. Corporate spending on software/cloud was squeezed tight in 2023 and will strengthen as companies have expenses under control and are looking to grow again. Asset gatherers gonna gather assets.” - Greg Sands

“We are returning to 2014, fewer VC firms, consolidation into the top 10, fewer dollars deployed. And as the marginal returns in SaaS evaporate, investors will be forced towards new categories like AI/Defense etc. until there's a next generational consumer computing platform.” - Delian Asparouhov

“We're not out of the woods yet. Even if we've found the soft landing, and even if the public markets continue to bounce back, the private markets will likely lag. There will continue to be a huge wave of consolidation and failures in the startup world and in the venture fund world, through much of 2024. And the IPO window likely won't truly open until 2025. So we still have some pain ahead.” - Jake Gibson

“During 2024 there will be increasing number of "the emperor has no clothes" unicorns. Some of these unicorns will go out of business, others will have to reach profitability but without any meaningful growth or exit prospects will turn into zombies. This will not end in 2024 as I believe it will continue in 2025. At the same time, there will be some unicorns who will show real resilience and will grow into the 2021 values.” - Oren Zeev

“Fundraising for everyone except the Tier 1 Funds will be tough. We will see more funds “going out of business” (many quietly) who just focus on supporting the portfolio vs raising additional capital and doing new deals. We will have both consolidation and shuffling within the micro-VC community, and those that survive will raise less capital than expected and have less management fees to run their firms. This will continue the slowdown in hiring in the industry and will also include many firms deciding to trim staff as we’ve already seen in 2023.” - Riley Rodgers

“This pattern is repeating as we speak and 2024 is going to be a year where we see many VC firms shrink staff as part of a “back to the basics” strategy while other VC firms will end up shutting their doors if they can’t raise enough LP capital to stay in business. The reduction in employment at VC firms is likely to be in the 25% range and there are many people who believe the reduction could be closer to 50% when calculated over the next few years.” - Frank Rotman

“VCs are going back to stage appropriate investing based on their fund size as they are realizing that off-stage investing has not yielded the returns they were looking for.” - TX Zhou

“VC mindset has shifted on new financings – the bar is higher but there is also 1) a realization that large outcomes (decacorns) will be rare and 2) there is much higher downstream financing risk now vs. in the past. This will put pressure on absolute value at Series B+ and make the funnel for later stage rounds narrower. More companies will need to find a path to profitability to avoid a valuation overhang. Net, mid and later stage companies will be fundamentally stronger companies. The next set of VC-backed unicorns and decacorns will actually be profitable!” - Gautam Gupta

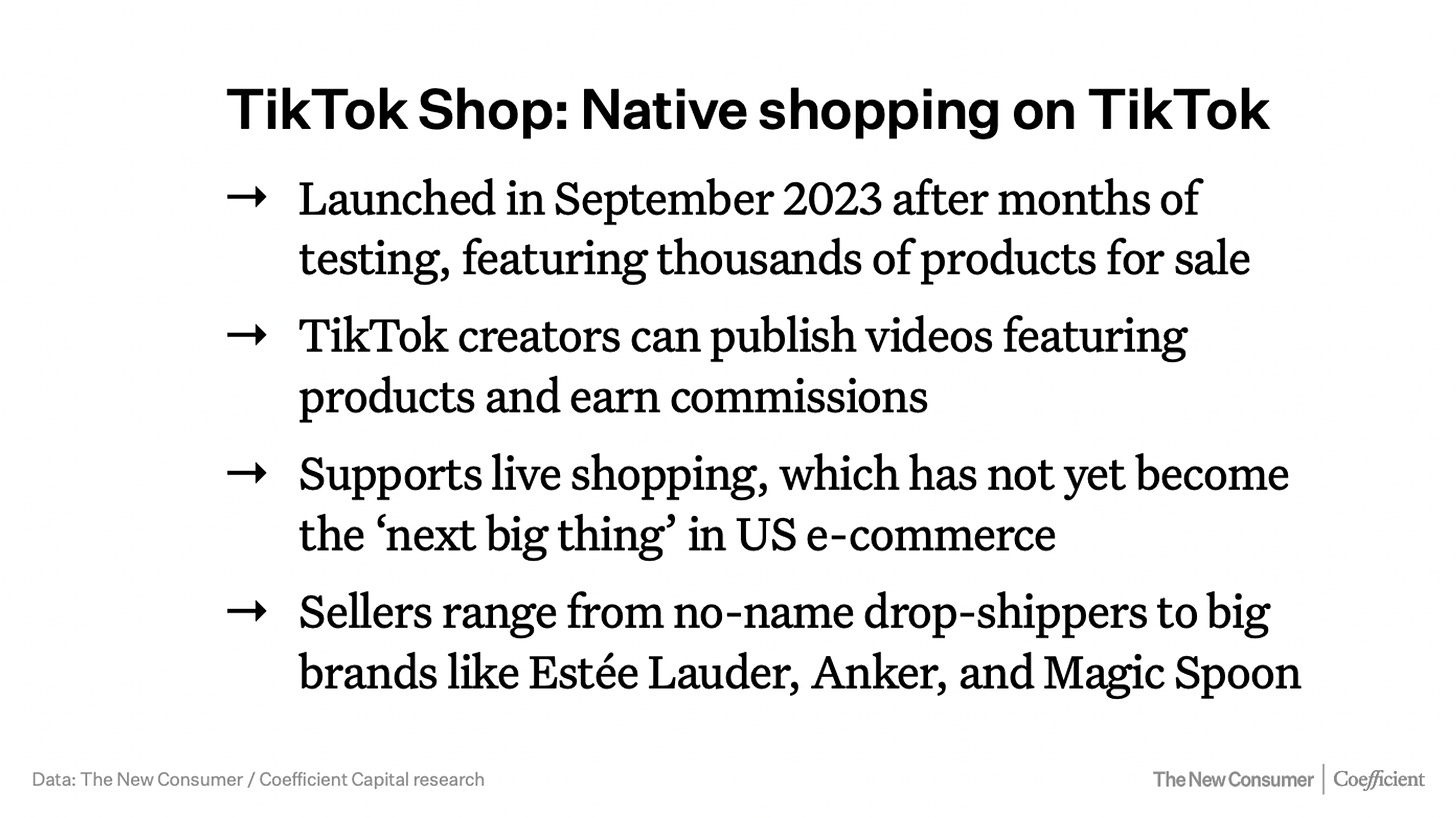

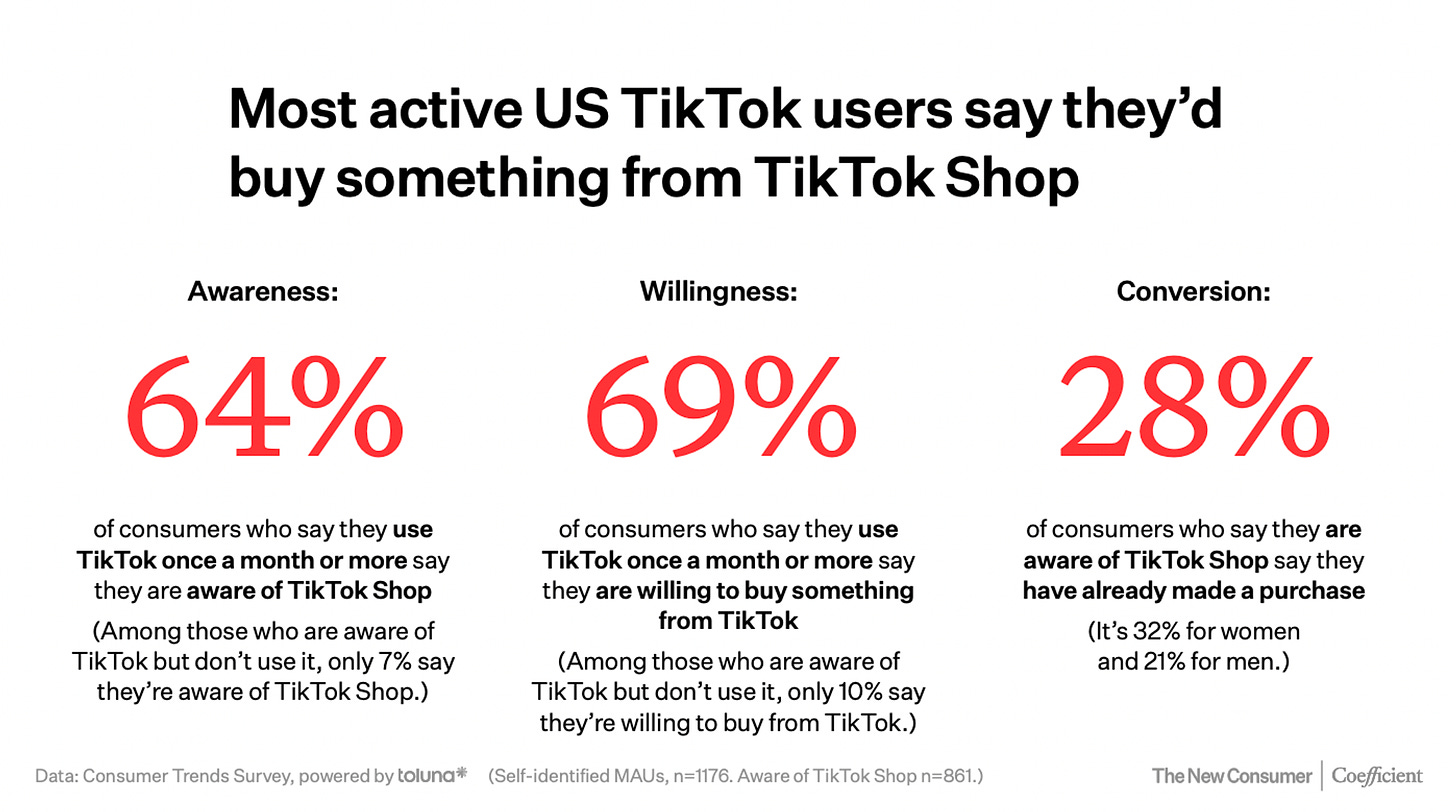

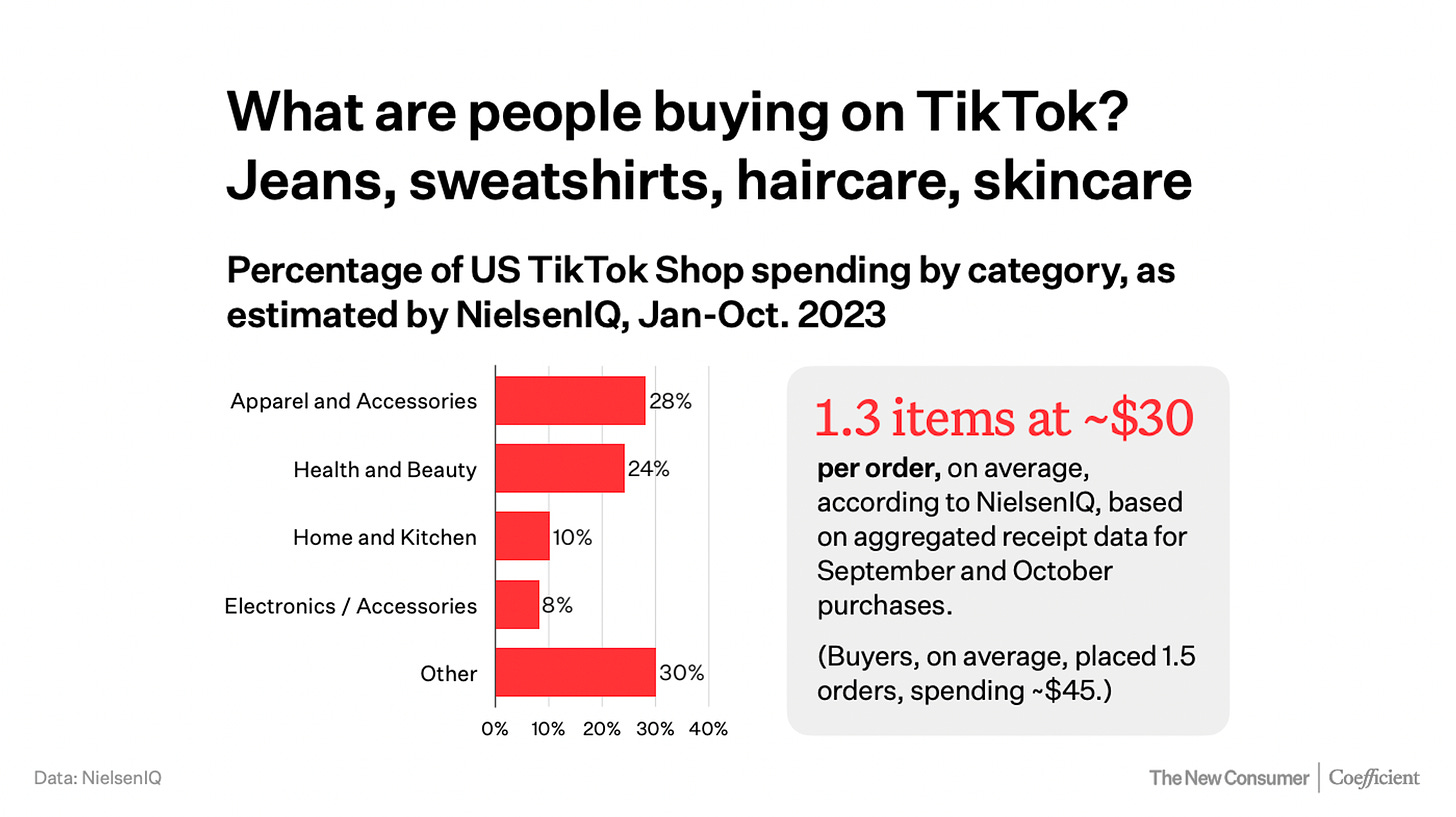

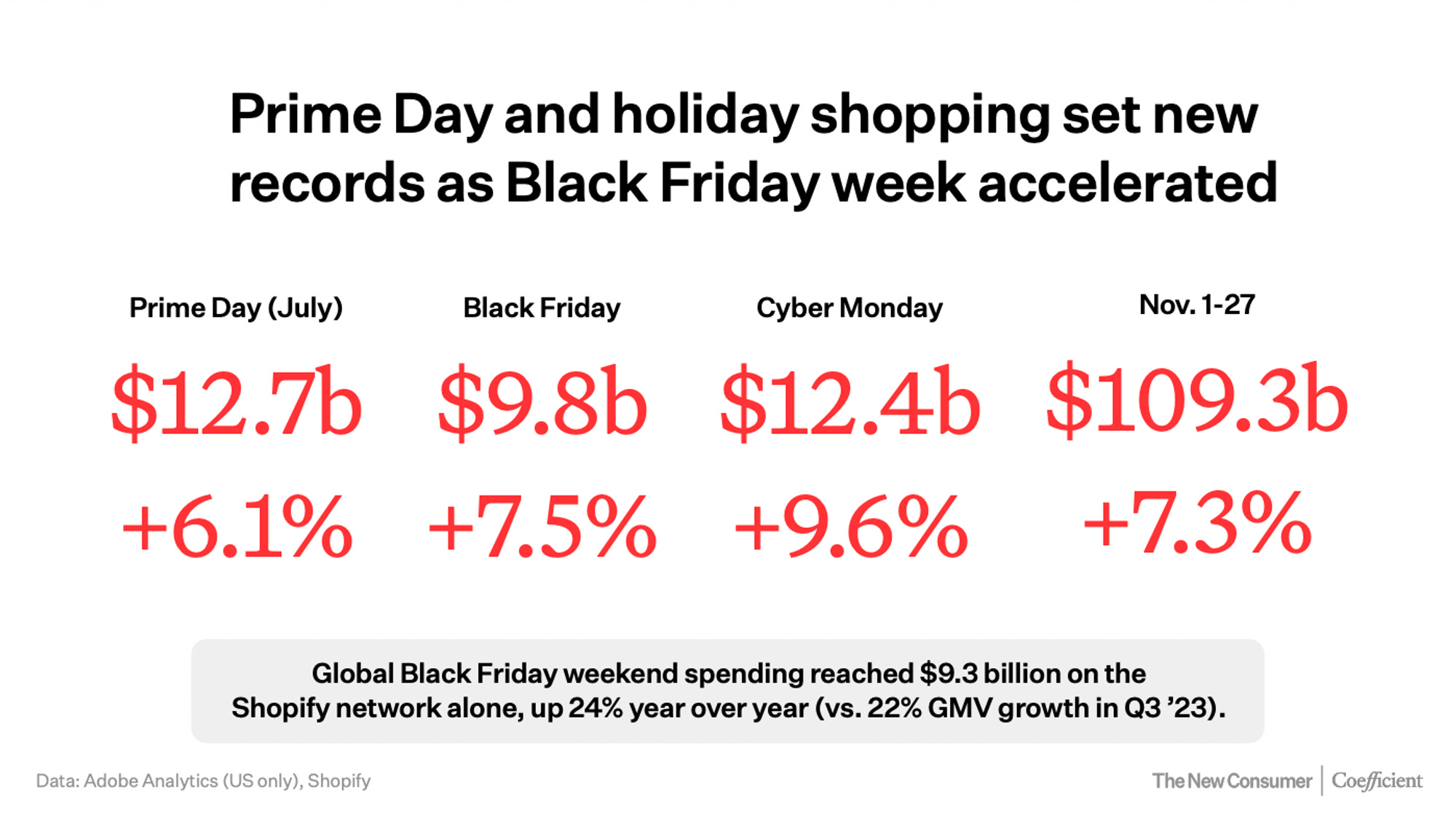

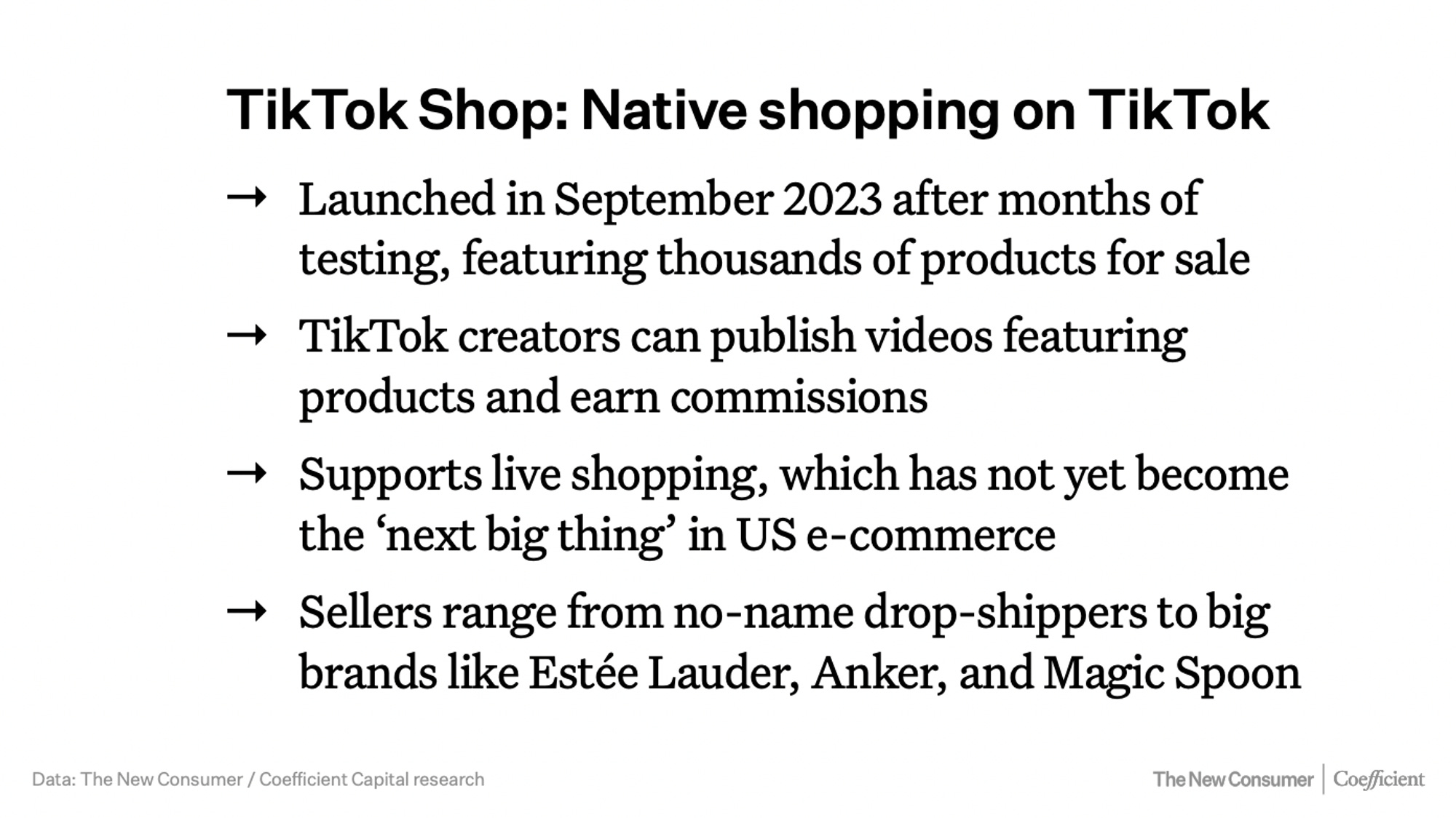

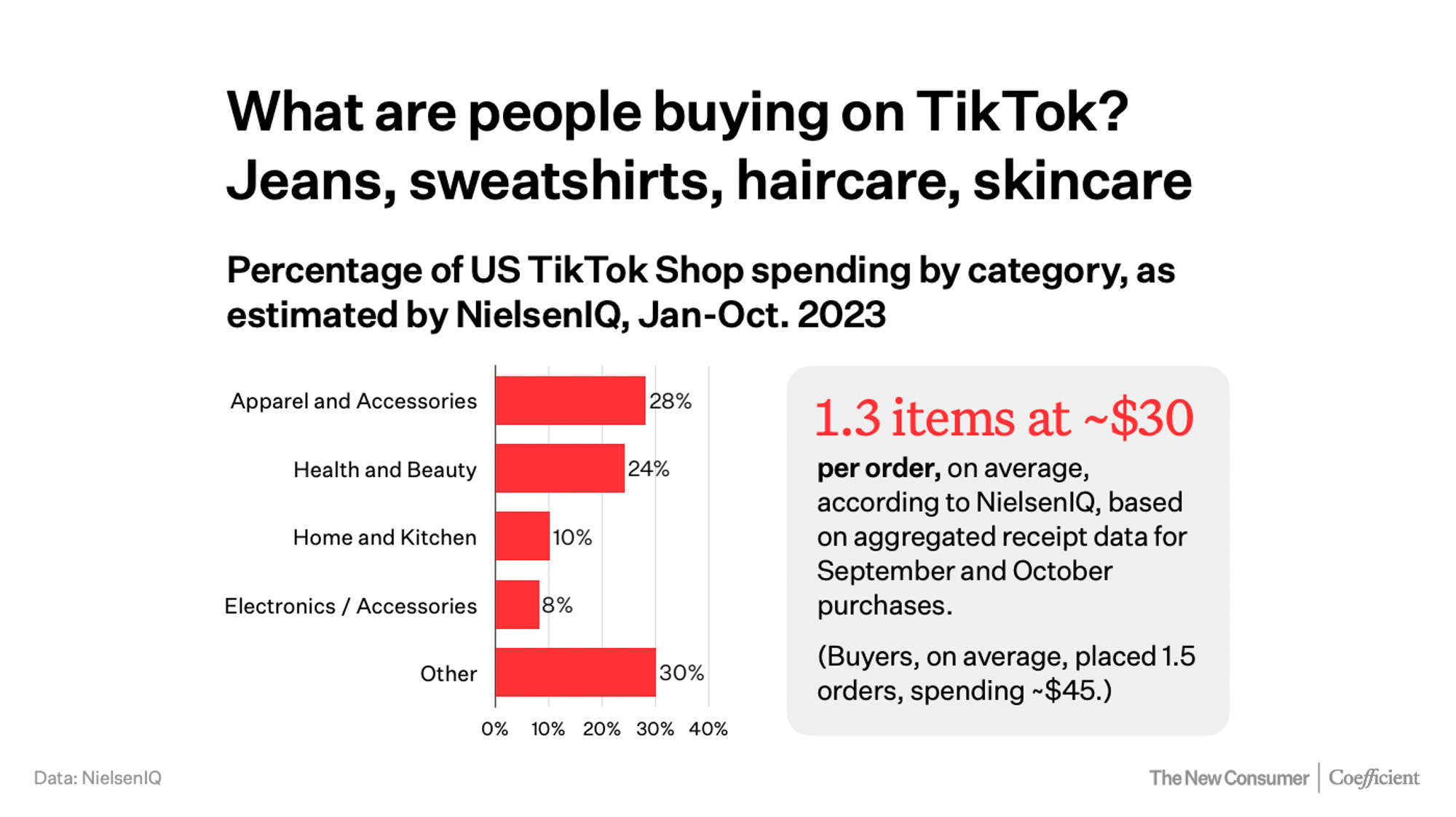

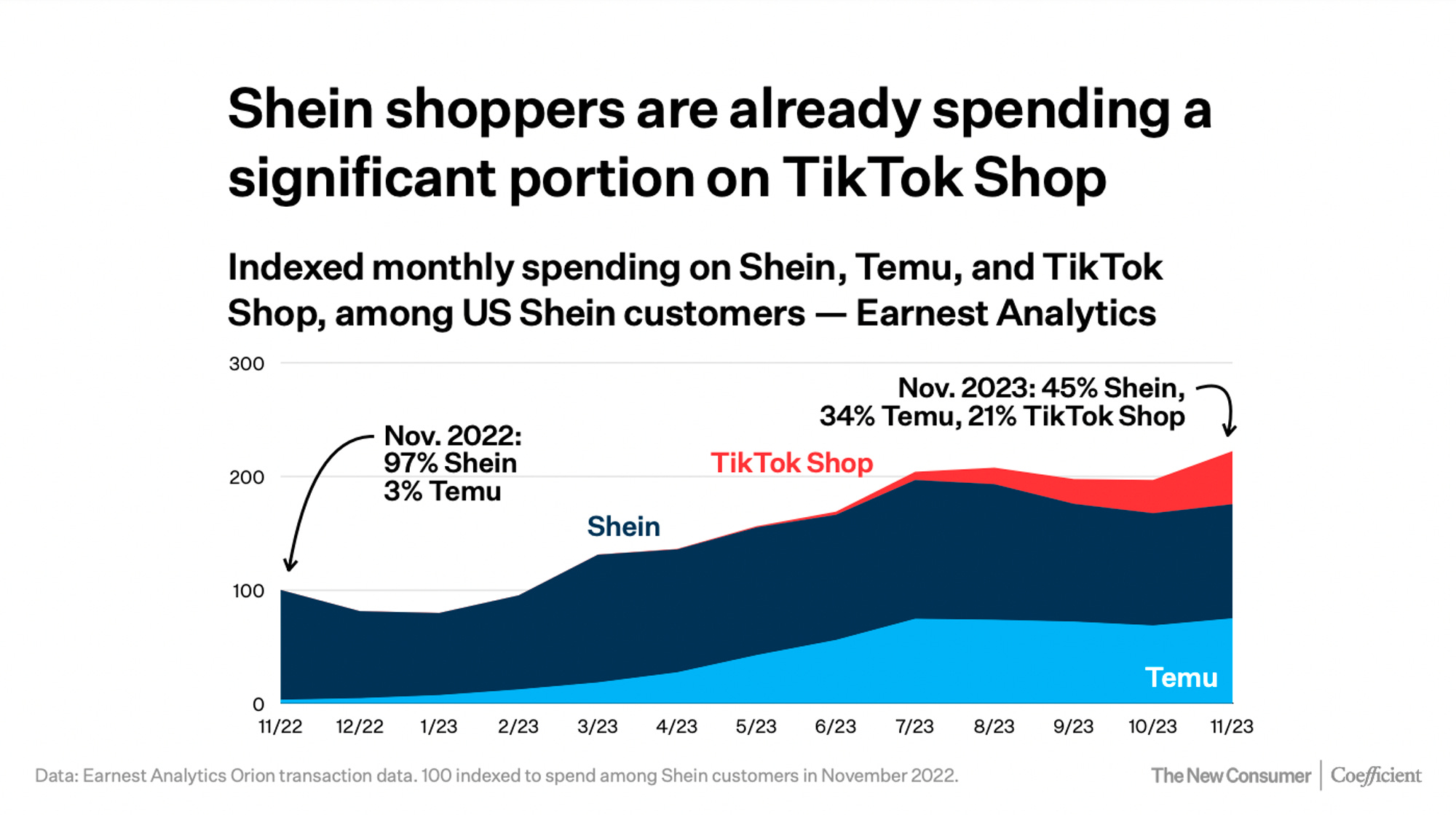

Friday, Jan. 19th: The New Consumer published the 2024’s edition of its report on consumer trends. It provides interesting US metrics on GLP-1 for weight loss and on the emergence of TikTok as e-commerce platform. - The New Consumer

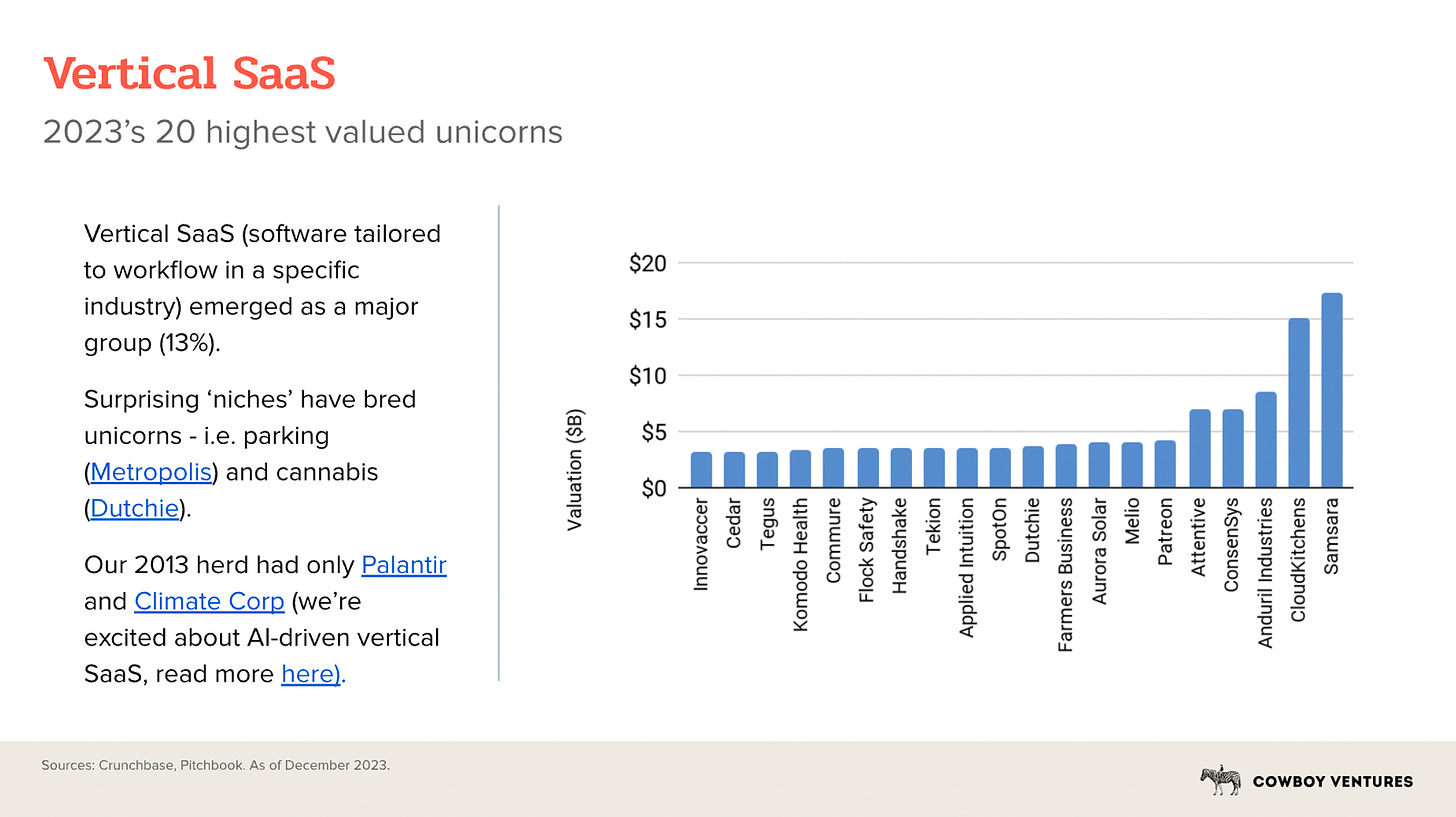

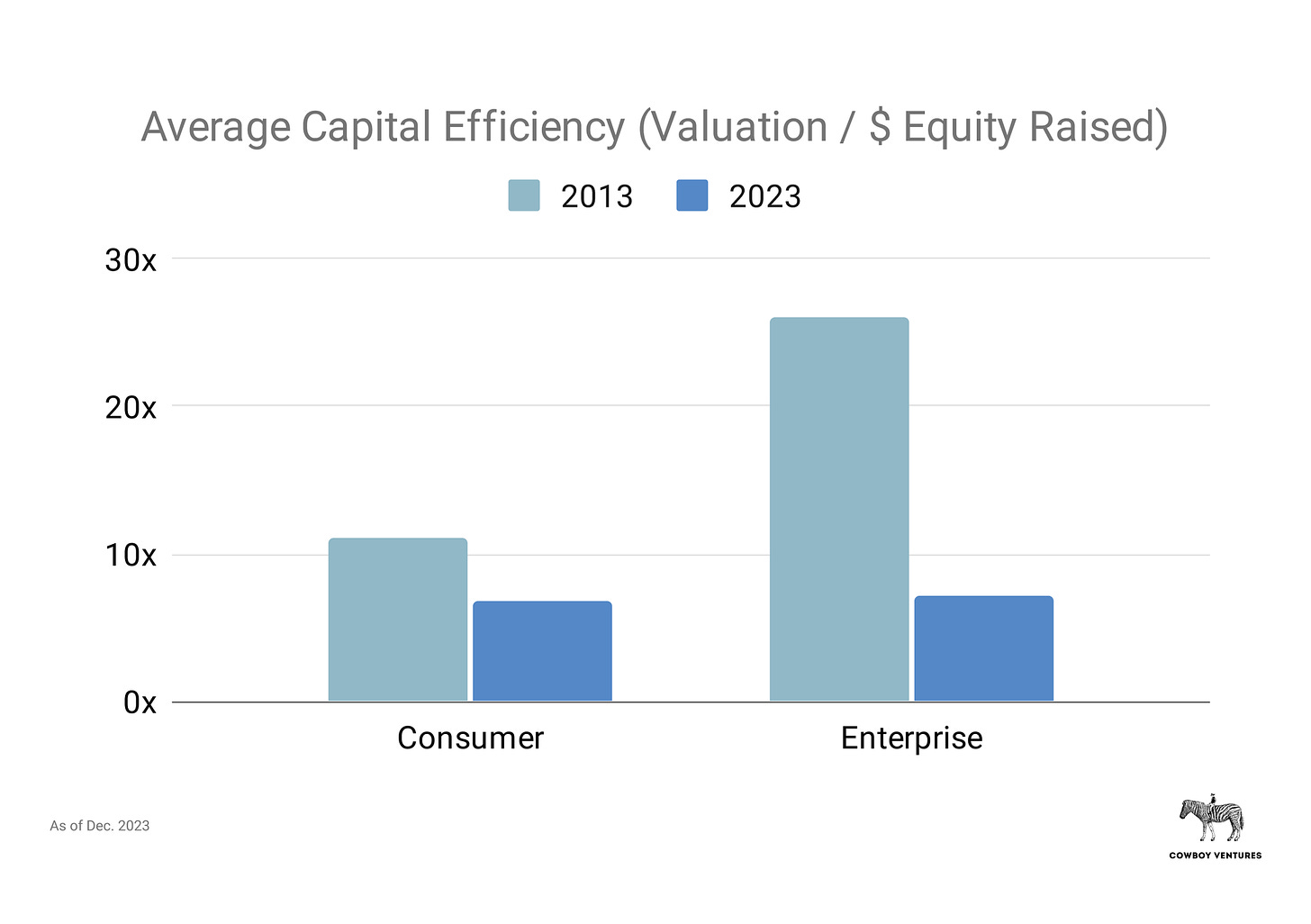

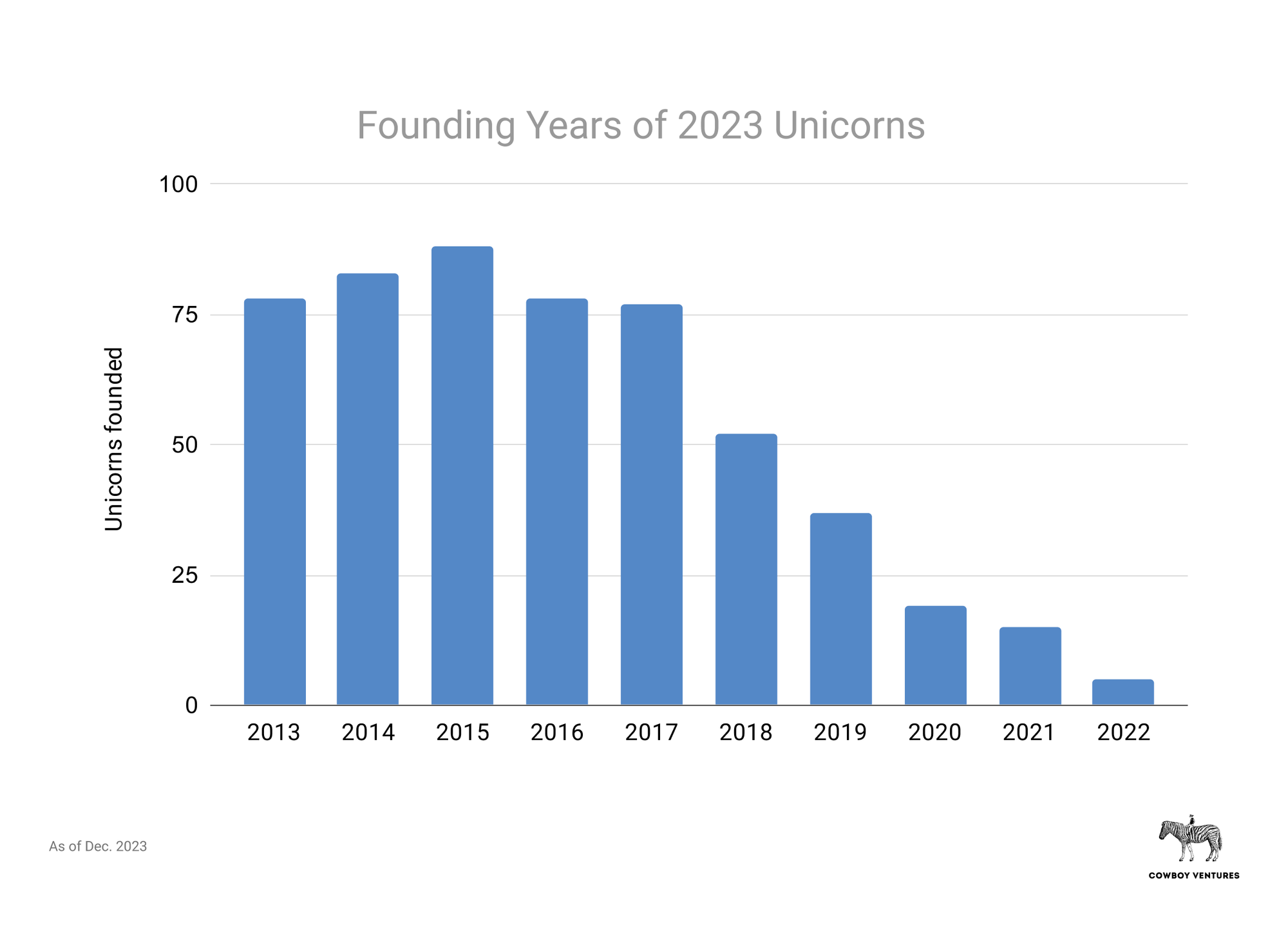

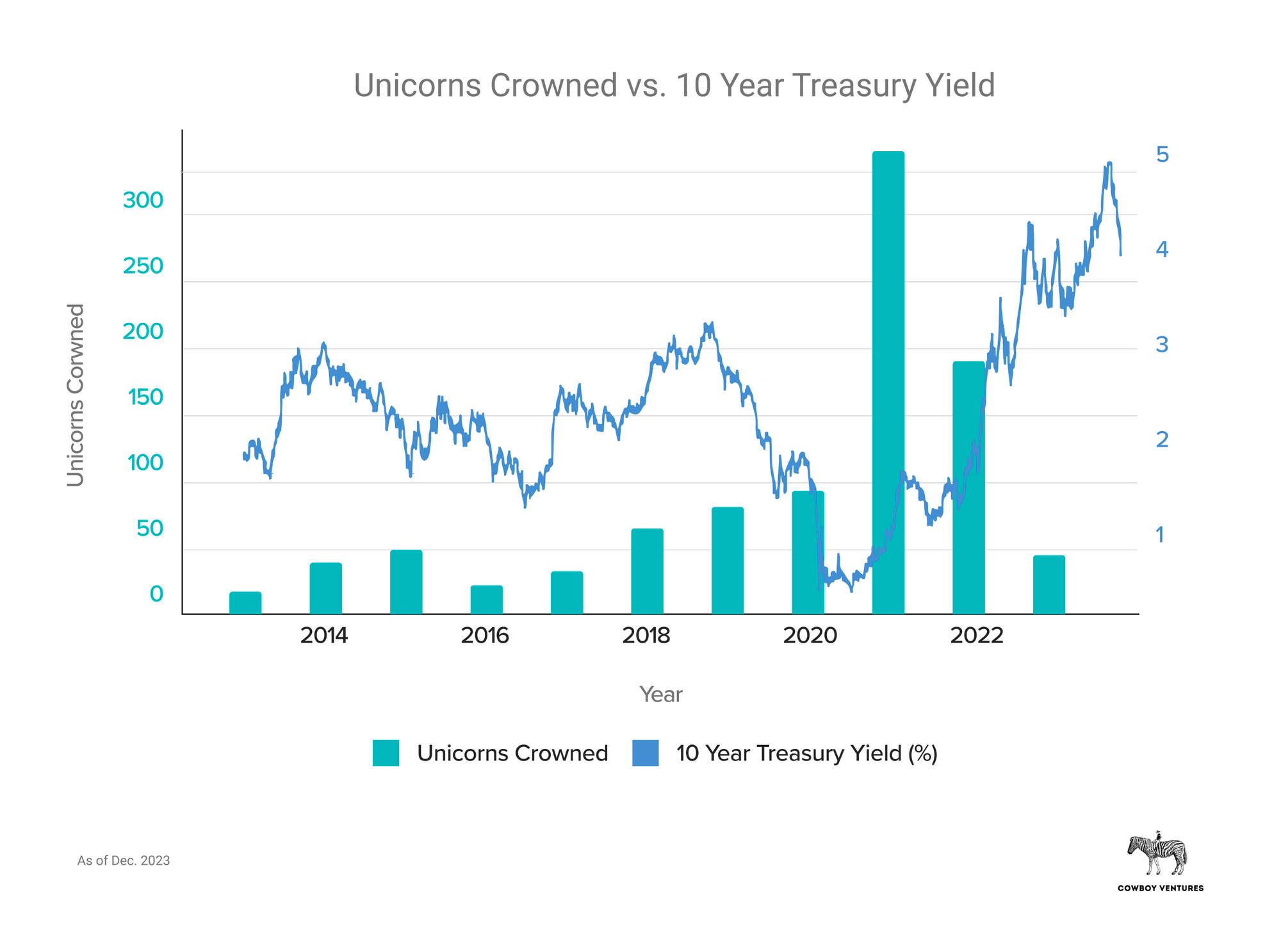

Saturday, Jan. 20th: Cowboy published a report on US unicorns. In 10 years, the number of unicorns increased by 14x from 39 to 532. 78% of unicorns are enterprise businesses (vs. 38% a decade a go). 60% unicorns are “ZIRPicorns” meaning that their valuation was acted during the previous bull market in 2020-2022 with 21% being valued just $1bn and 40% trading below $1bn on secondary markets. Only 7% of unicorns exited (vs. 66% a decade ago). - Cowboy

“60% are what we call ‘ZIRPicorns’ - they were last valued between Jan 2020 and March 2022, when interest rates were near zero and multiples at peak. When money was flowing, unprofitable private companies were often able to raise enough to fund 2-5 yrs of operations. This means operating runways are getting short for many unicorns.”

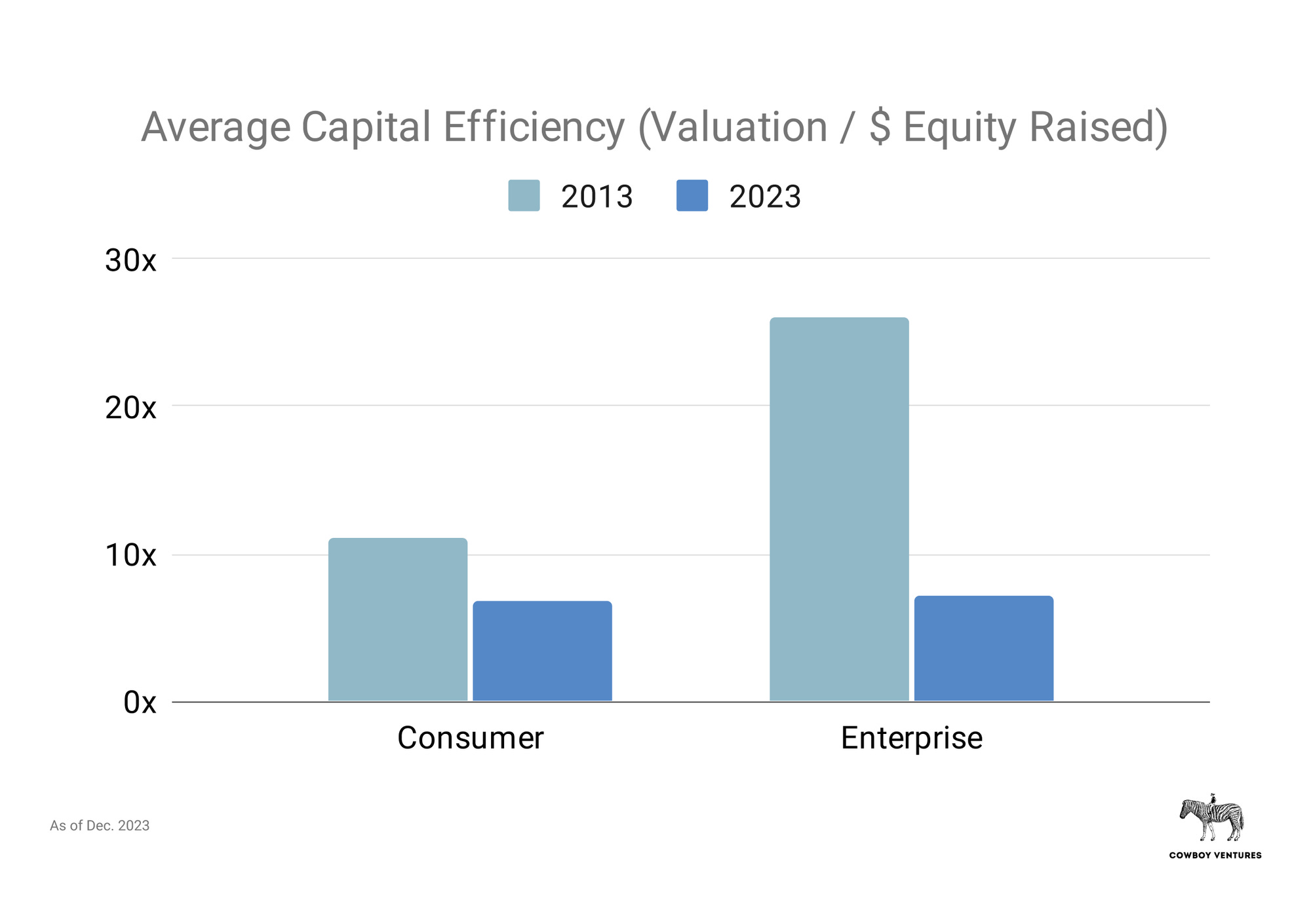

“In the past decade, tech lost its capital efficiency edge. Formerly impressive enterprise company capital efficiency of 26x plummeted to 7x, putting it in-line with consumer co efficiency (despite typically higher margins and customer retention), which also dropped from 11x to 7x. Given many unicorns are currently overvalued, even 7x is likely inflated.”

“In 2013, there were ~850 active venture funds. Today there are ~2,500. As unicorns fall out of the dataset, there will be more change at VC firms. Some VCs will retire, some will raise smaller funds (potentially right-sized for better returns) and/or downsize teams, some firms will fold. We’ve seen “VC musical chairs” in previous cycles, and it’s happening again.”

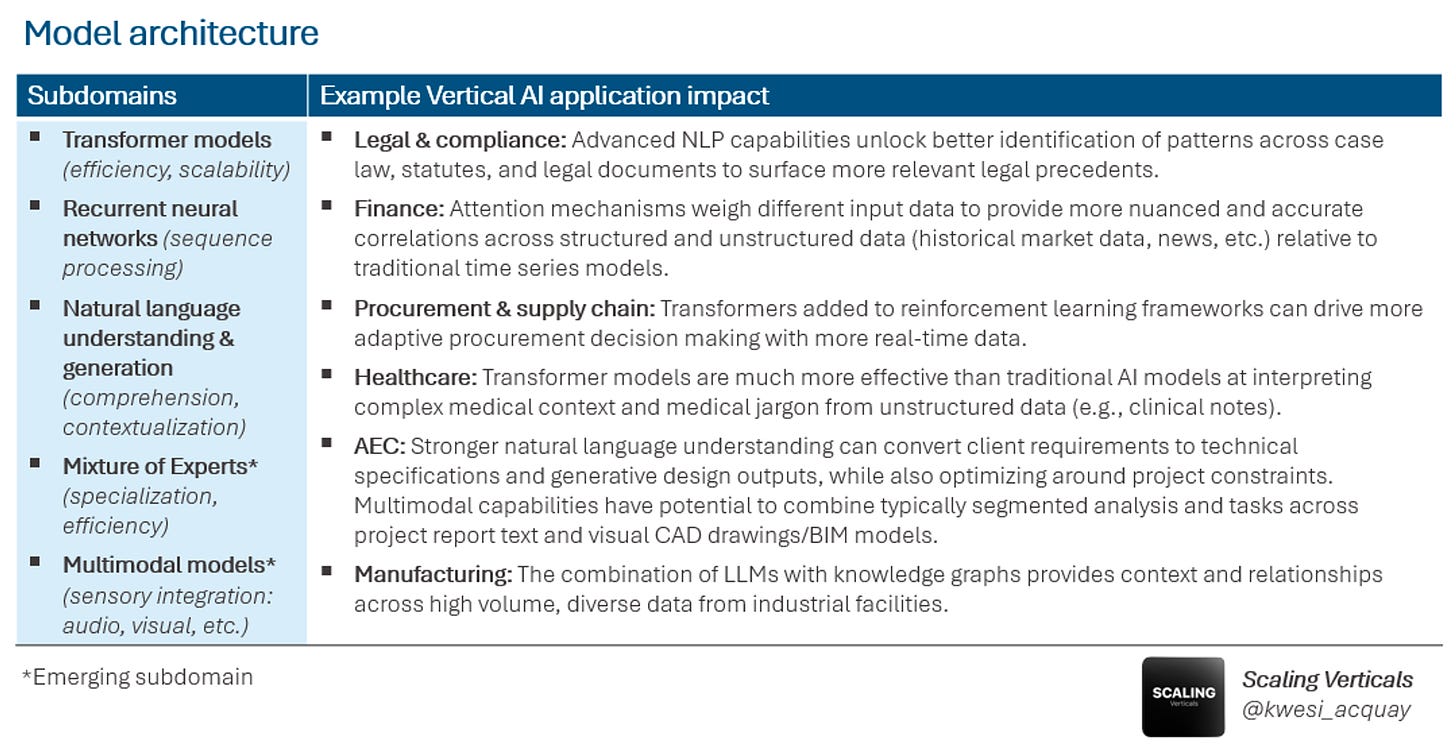

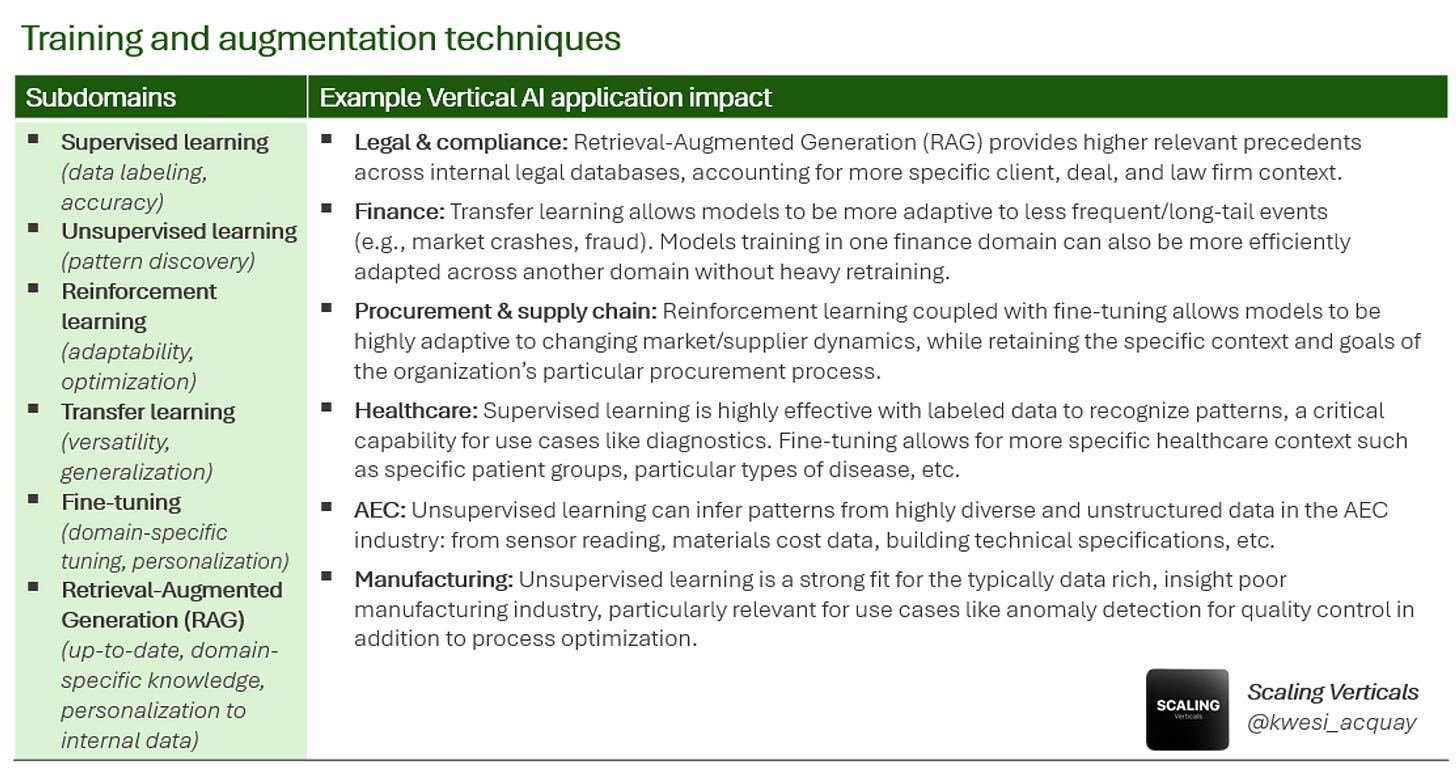

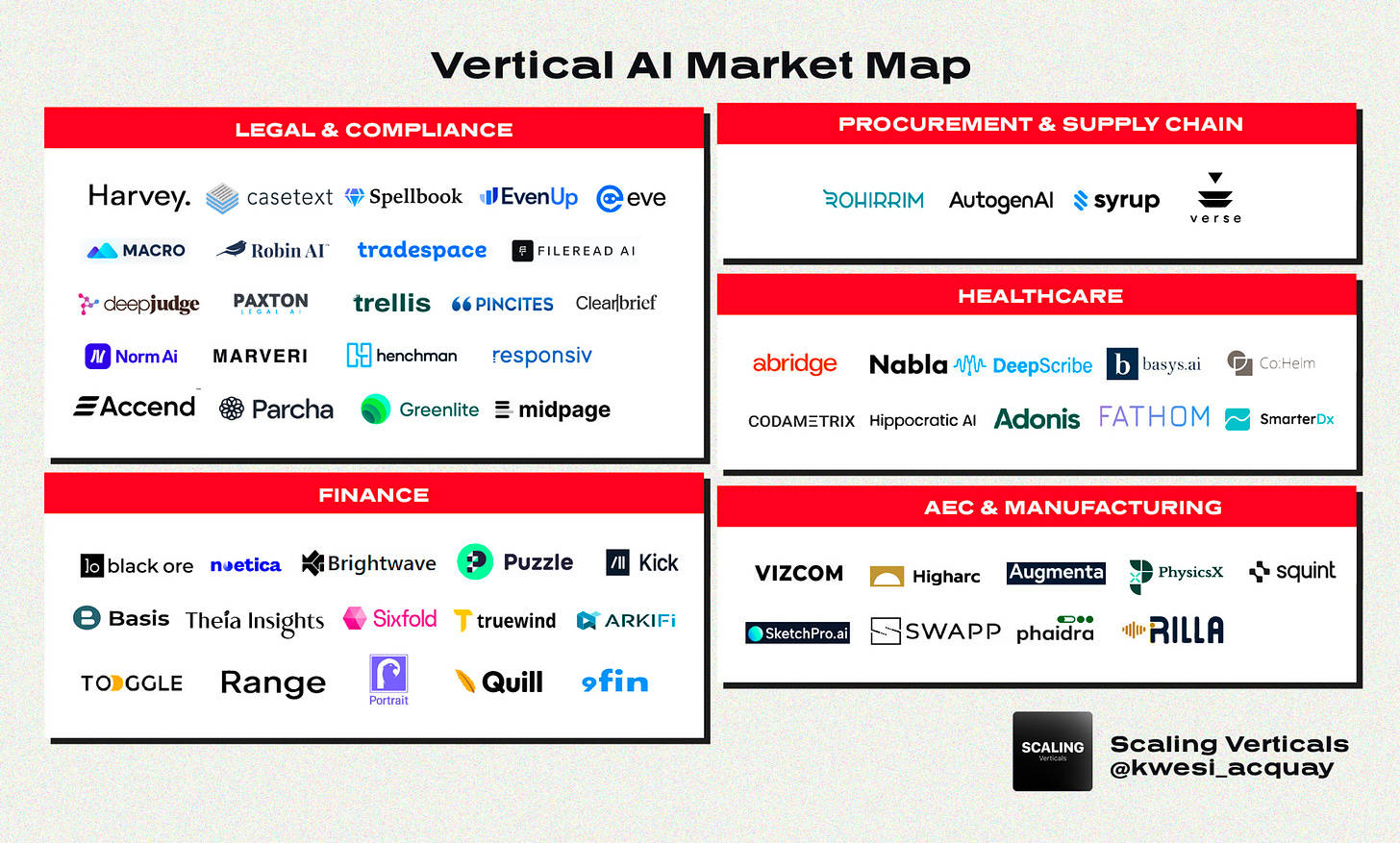

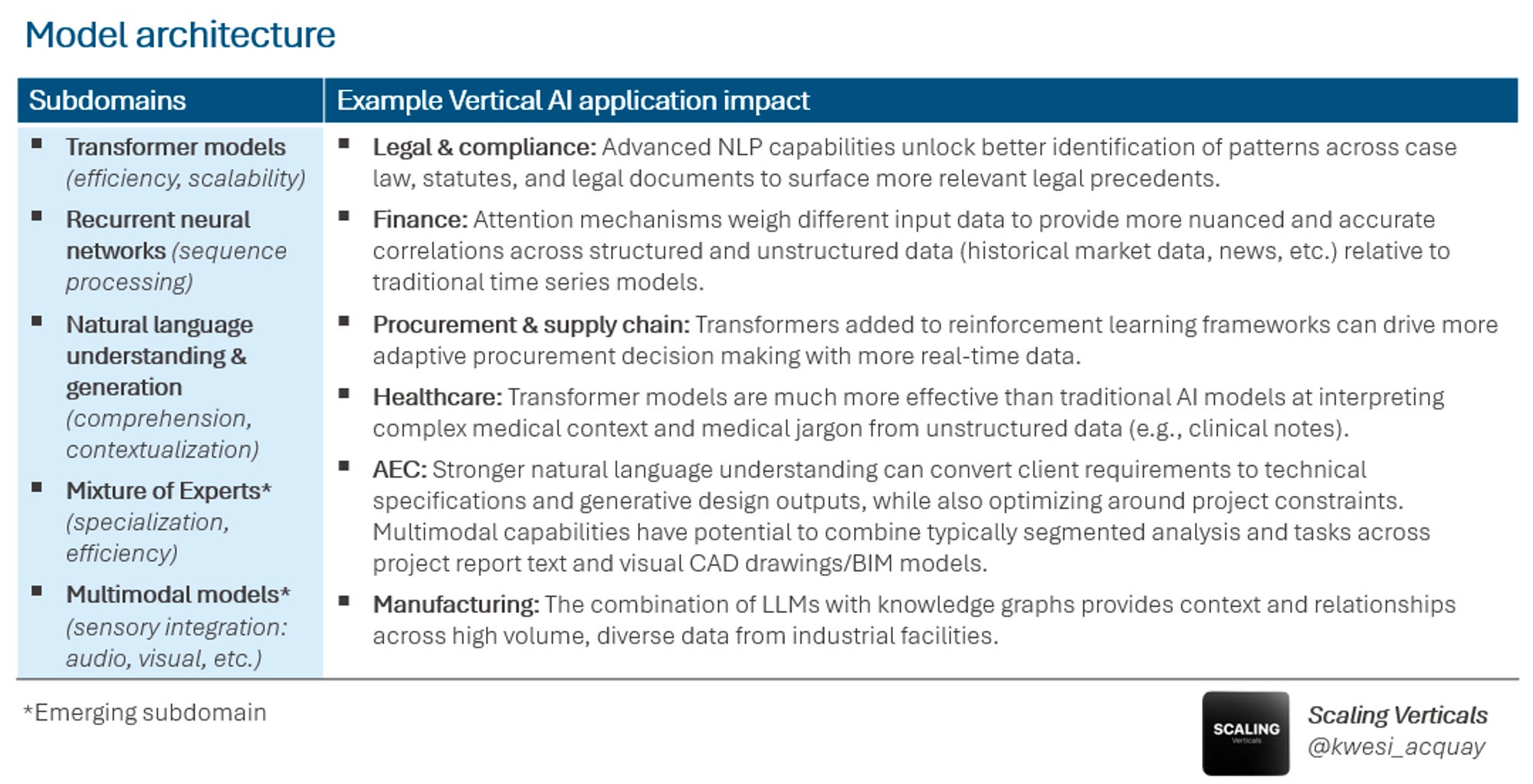

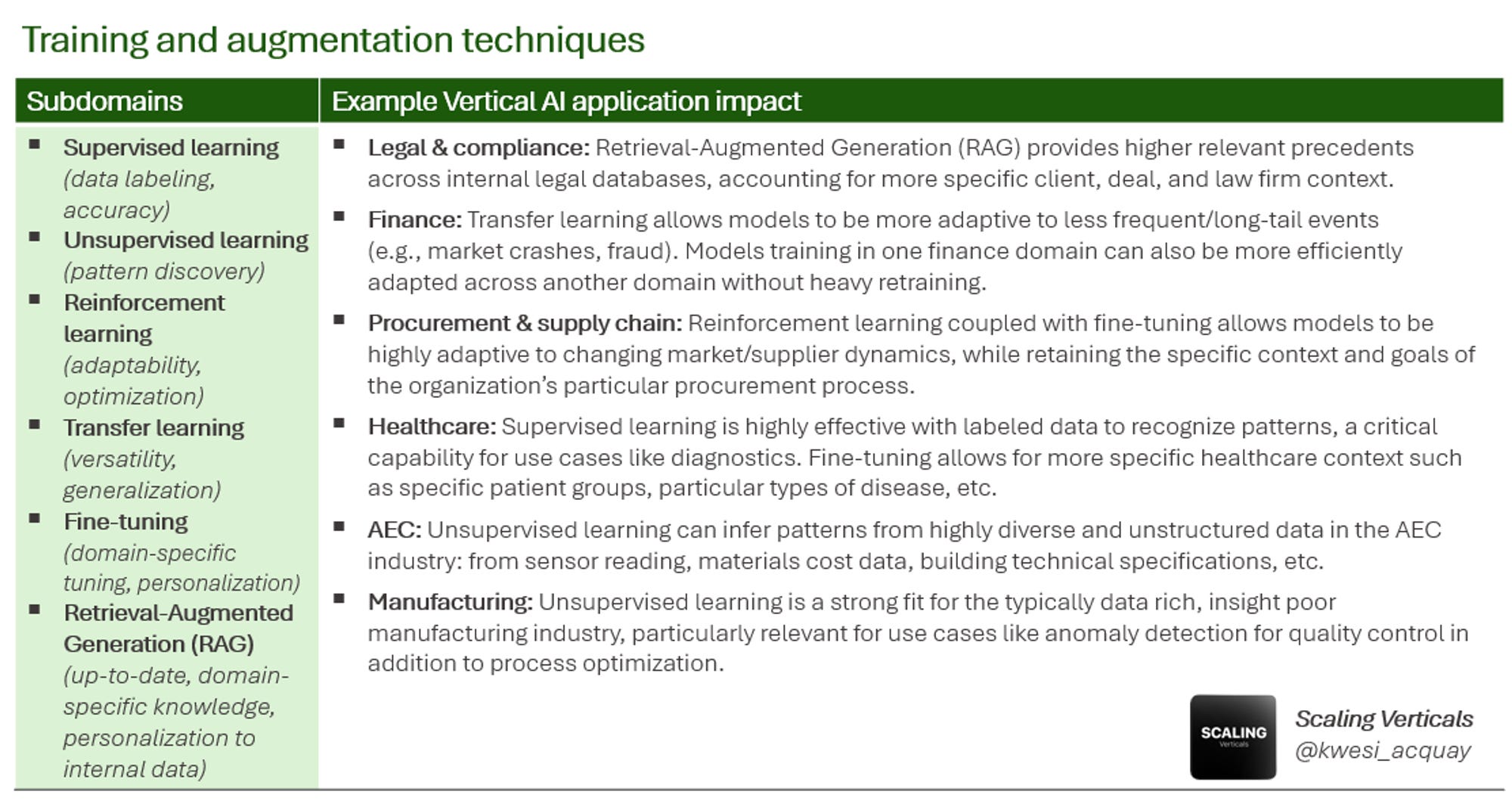

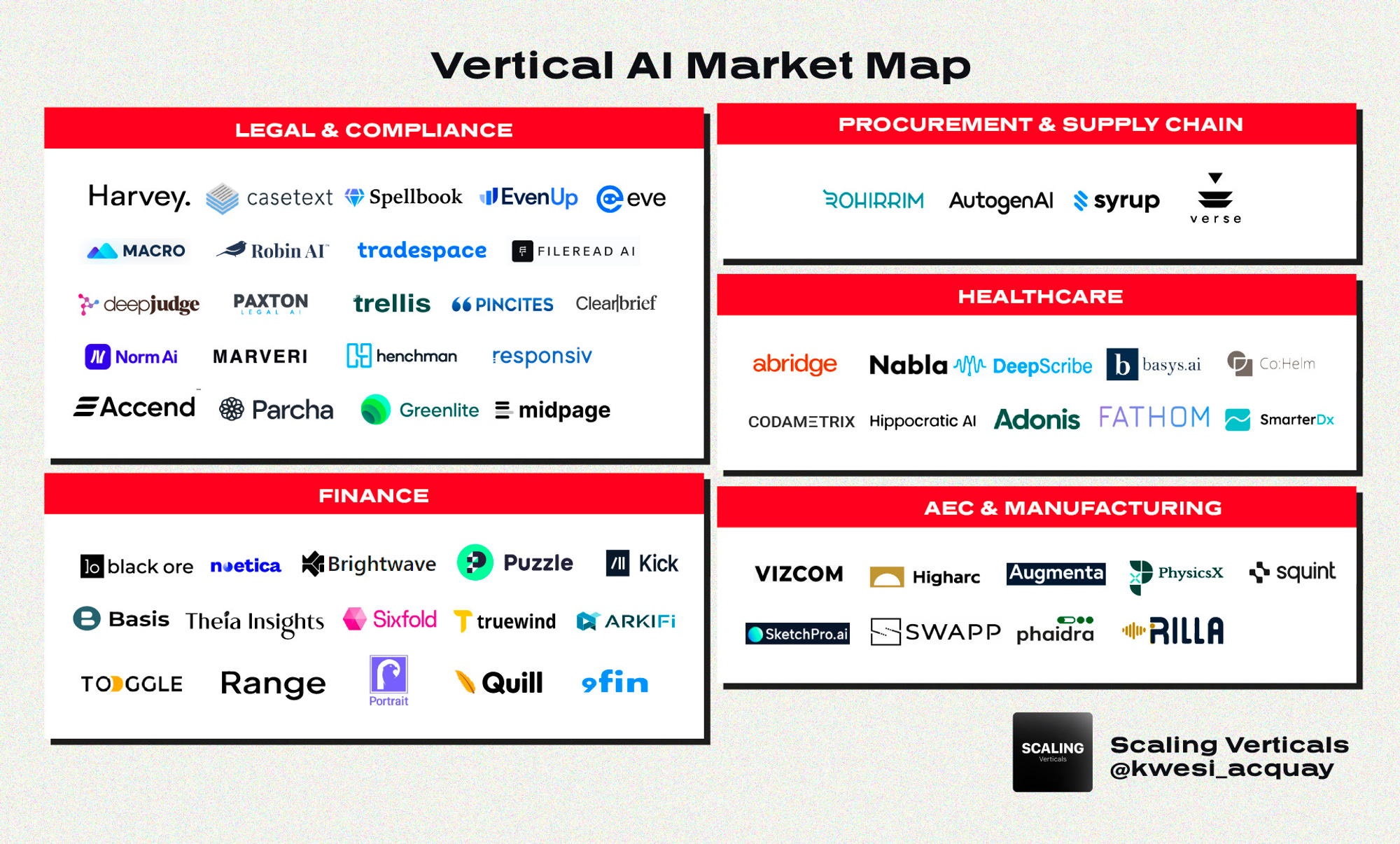

Sunday, Jan. 21st: Kwesi Acquay at Redpoint wrote about AI-driven vertical SaaS. - Kwesi Acquay

“The advent of LLMs not only solved the critical data infrastructure and resource challenges of traditional AI but also introduced new transformer model properties and training techniques, unlocking new potential for AI at the application layer.”

Monday, Jan. 22nd: Thema was recently announced publicly. It is a new fund of funds targeting first-time VCs, offering to write cheques of up to £5m into 3-4 first-time funds annually. Thema is open to being the first LP in these funds and will also take a 15-20% stake in the newly formed GPs. - Sifted

“Thema will support emerging fund managers by removing administrative and legal headaches, helping them focus on their zone of genius and leveraging their unique insights.”

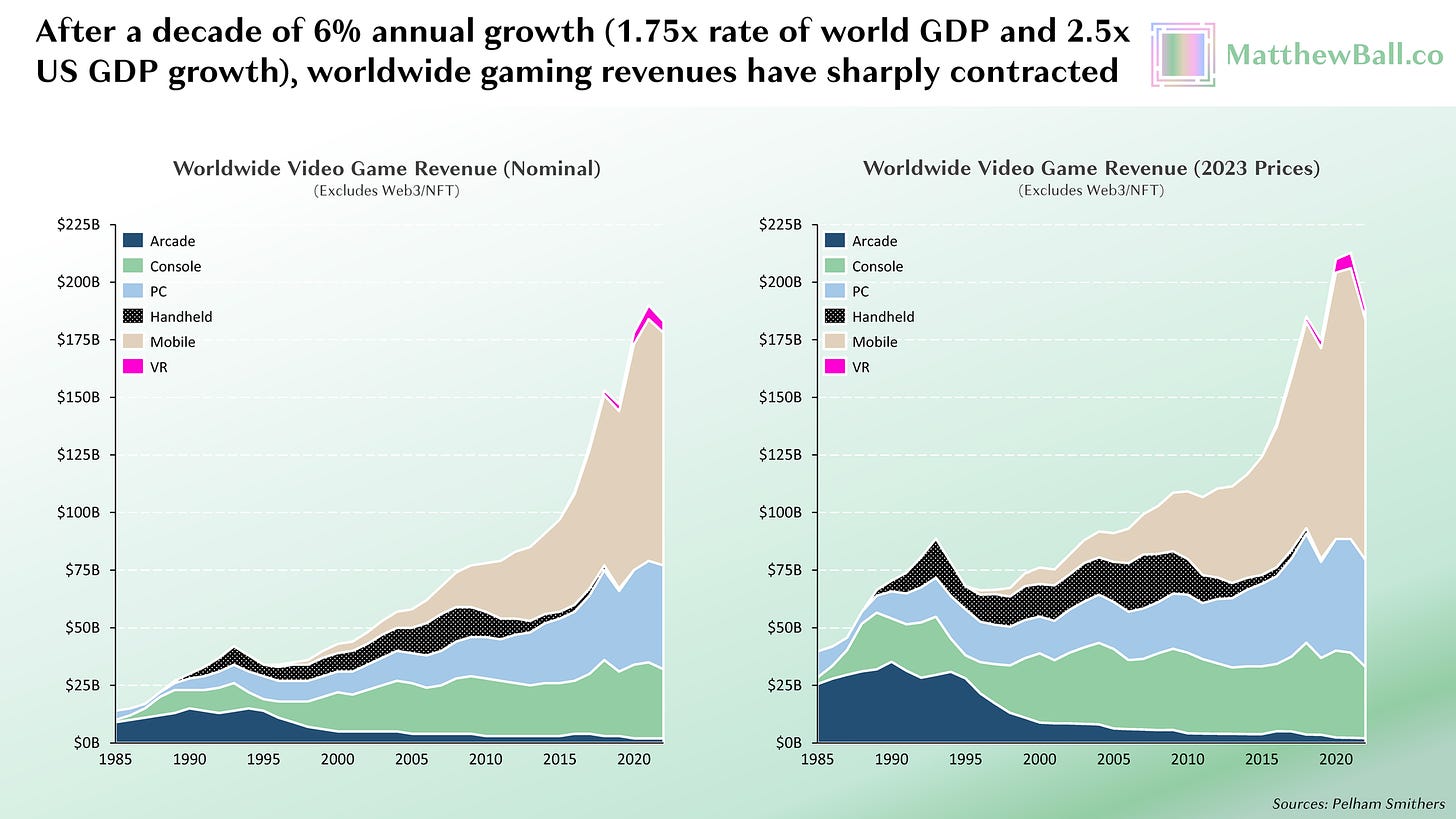

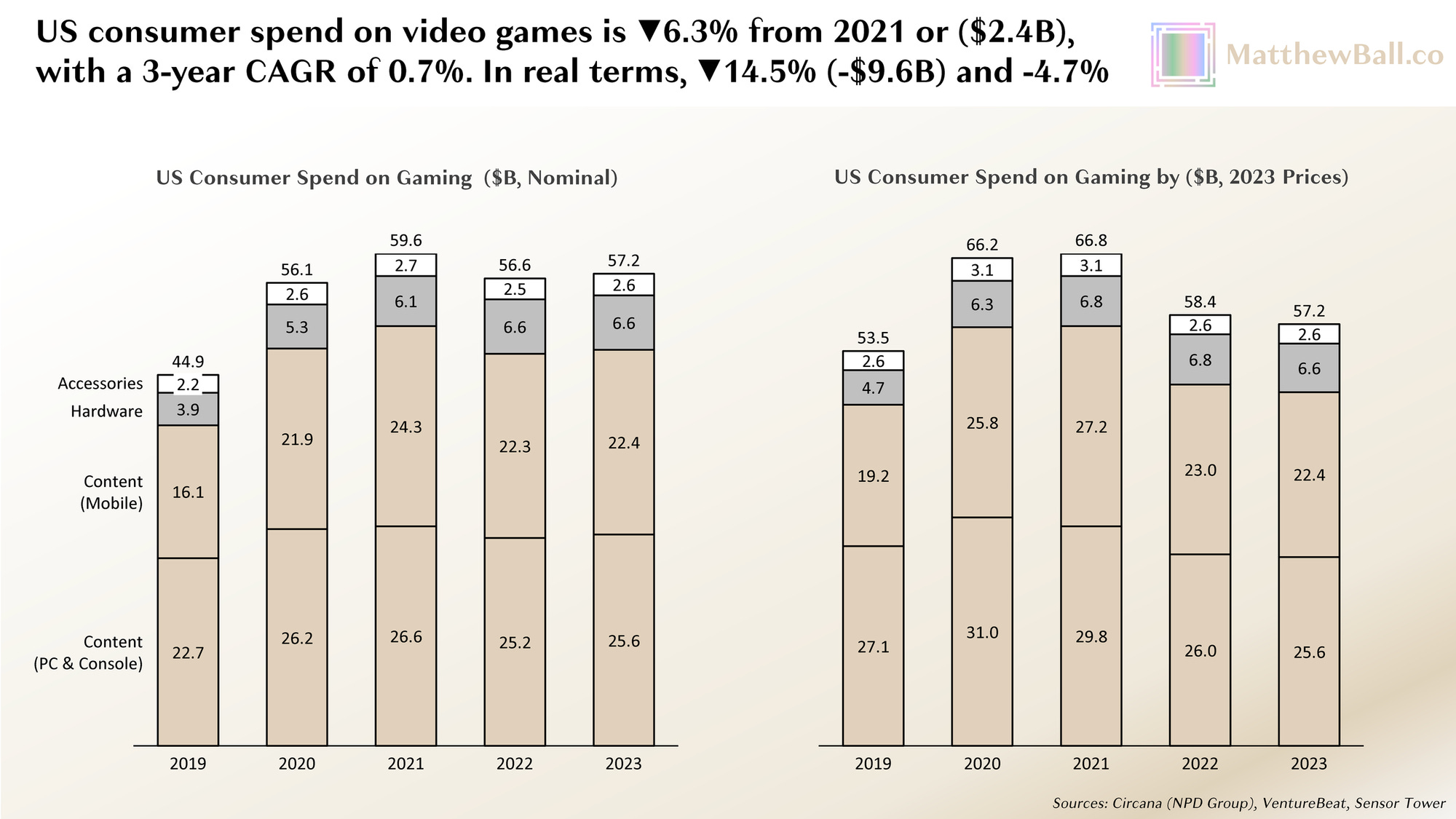

Tuesday, Jan. 23rd: Matthew Ball wrote about the gaming industry. - Matthew Ball

“Roblox, the most popular gaming ecosystem globally, grew its daily active users from 59 million in Q3 2022 to about 70 million in Q3 2023, with monthly active users growing from 275 million to 350 million and monthly hours from roughly 4.6 billion to 5.6 billion.”

“The Super Mario Bros. Movie grossed $1.4 billion worldwide, ranking second for all theatrical releases in 2023 and third among all animated films in history.”

“For those who worked in gaming, last year was brutal. A record 10,500 game developers, artists, testers, and other gaming employees were laid off in 2023, topping the prior record holder, 2022, which saw 8,500 in job losses. Unfortunately, 2024 has seen 5,850 in cuts after only 25 days.”

“There are several reasons behind the many layoffs detailed above, but the first may be the most important. It’s also the most overlooked and most counter-narrative: video game revenues are falling.”

“Weak revenue growth is not sufficient to explain the rash of layoffs—companies can, by definition, survive on the same revenue as before and probably on a bit less, too. Yet costs for game makers have grown considerably during this period, too.”

“Some have posited that the rise of game subscription bundles such as Xbox Game Pass, Ubisoft+, and EA Play have harmed spending on packaged games. The idea is that these offerings cannibalize $20–$70 purchases and reconstitute them into monthly (i.e., pause-able) subscriptions that cost $5–$17 per month and in some cases span hundreds of titles.”

“With 25–30m subscribers worldwide, Game Pass reaches no more than 20% of U.S. console and PC gamers.”

“Seventeen years after the first iPhone, there are not many new players for mobile devices to onboard to gaming, least of all high-ARPU players. TikTok, Reels, YouTube Shorts, and all the rest, meanwhile, are devouring much of the idle time once spent playing mobile games.”

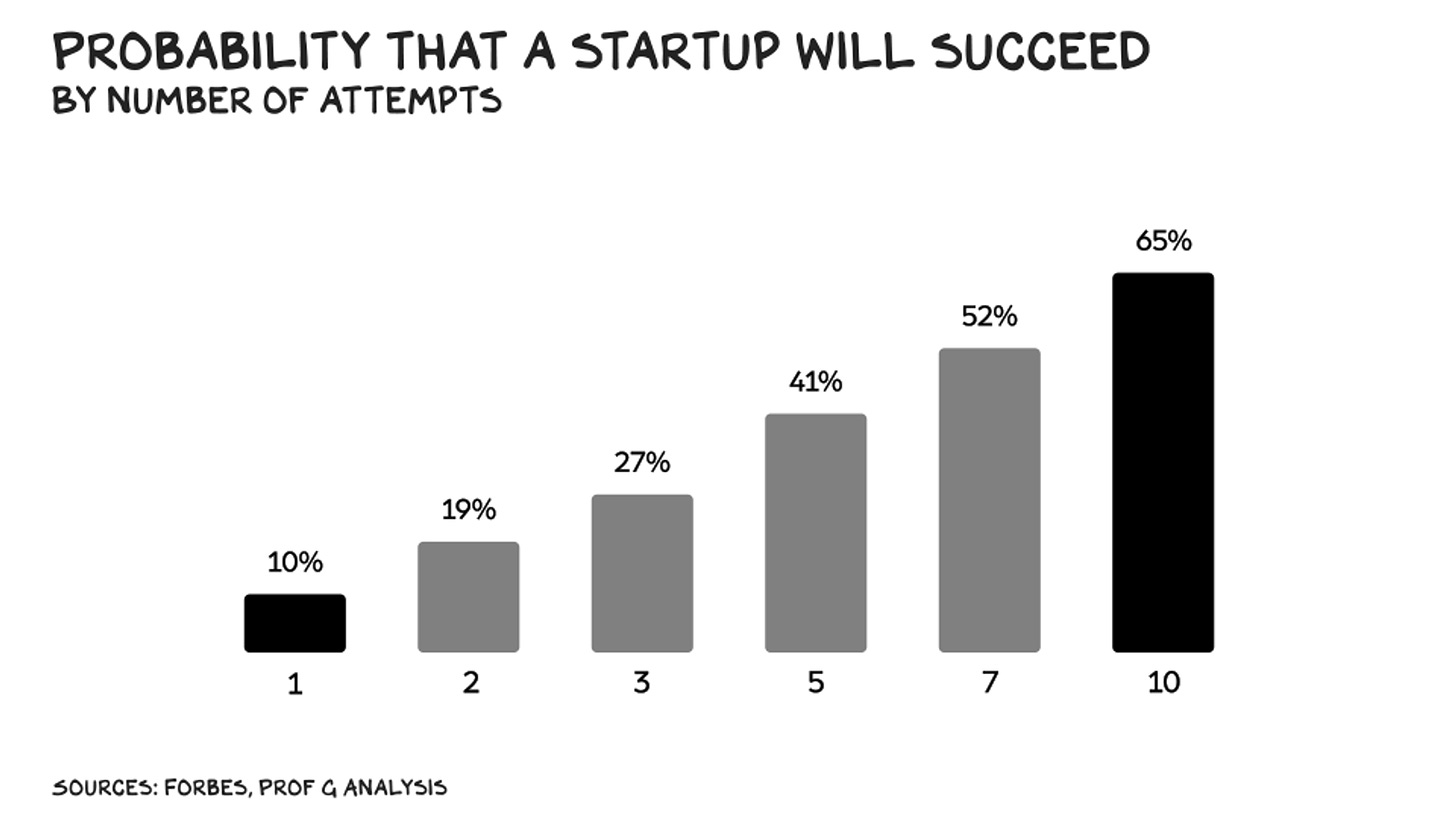

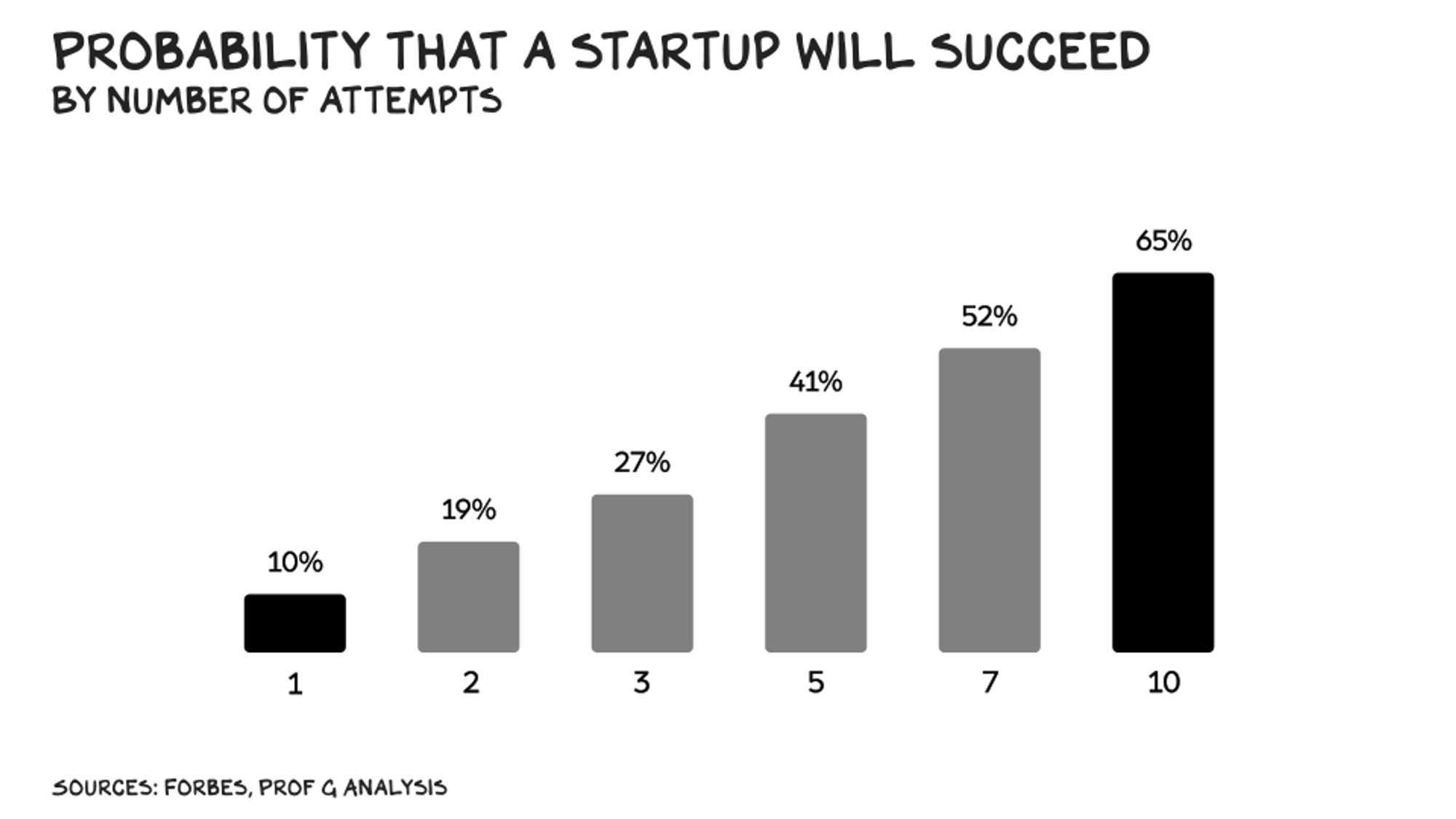

Wednesday, Jan. 24th: Scott Galloway wrote about the importance of knowing how to quit. - No Mercy / No Malice

“Grit is great. Perseverance is a virtue. But, narratively, it’s overrated. Greatness is a function not just of grit, but of talent, luck, where and when you are born … and knowing when to quit.”

“Most CEOs have one thing in common: They are quitters. Specifically, your career trajectory will be steeper if every several years you switch jobs.”

“If you want to be successful, you will likely need to quit the majority of your jobs, homes, friends, and investments.”

“A big data study of 46 years of VC investments found prior failure to be “the essential prerequisite for success.” The key is learning from each mistake.”

“Nobody is paying as much attention to your failures as you are, so fear them but don’t let them paralyze you. When you do fail, don’t feel you need to excuse them or blame others. Being gracious in victory is admirable. What’s harder, but can pay greater dividends, is being gracious in failure. Express gratitude to everyone who believed in you, and demonstrate grace to those who didn’t.”

Thursday, Jan. 25th: Louis Coppey published a great paper on Vertical Software 2.0 which resonates with what I call vSol in this newsletter. - P9

B2B marketplaces are vertical software businesses because most of them end up adding a SaaS business model (automating workflows and process for buyers and/or sellers) on top of the marketplace business model (take rate when you create new matches between buyers & sellers).

“Vertical software solutions that reach a certain scale can start building distribution/procurement value propositions for their client base. For Amenitiz, our portfolio company that’s building an all-in-one software for small independent hotels, this could mean plugging their client base of small hotels as inventory to distribution partners like GDS to increase their clients’ bookings.”

To increase their TAM, vSaaS have traditional levers including:

“Expanding the product scope to increase the ARPA,

Broadening the target market by going after different companies, and/or,

Going after different personas in the same organization”

“The emergence of additional business models in software (inc. financial services, distribution/procurement, advertising, automating work to capture HR budget & not only software budgets) provides as many additional answers to the “size of the opportunity/TAM” question.”

Friday, Jan. 26th: I listened to a 20VC’s podcast episode with Tooey Courtemanche who is CEO and cofounder at Procore. - Procore

In 2012, Procore was making $4.8m in revenues a decade after inception. In 2015, it was making $9.6m in revenues. “In 2002, if you walked to any construction site in the in the world, there was no internet at the job site. I had built a vertical SaaS to serve an industry that could not actually use my technology.” “We just were super early but I knew it was going to happen. It was the last industry I was aware of that had not digitized. I had seen all these other industries digitize and I was convinced that it was just a matter of time before it would happen. We just had to be patient.”

If you were to invest in Procore in 2002, the risk ratio was extremely high because you had to believe that: (i) the construction industry was going to digitise, (ii) workers at the job-site were going to be proficient enough to use technology, (iii) the internet would be available at the job site, (iv) mobile apps would help workers to do their job on the field and (v) construction companies would look at Procore as a productivity tool and not only a documentation tool.

In 2015, the construction market tipped to us and construction companies started to digitise their operations on Procore.

“The only thing that matters in you know in business is that you survive to fight another day.”

In its investment memorandum, Bessemer wrote that the best outcome for Procore would be to be sold for $300m.

“Up until 2017, we only had one product which is Procore’s flagship product and which is a project management tool. What we had heard is that our customers were sick of having point solutions and they really wanted to have our platform as the platform of choice for all their core business needs (e.g. financial management, quality and safety). We prioritized new products based on the biggest needs of our customers.”

A key lesson on product expansion for Procore was that it needed to ship enterprise grade new products and not beta products. For instance, Procore had to fully re-architecture its financial management product to make sure that it was enterprise grade and able to scale with our customers.

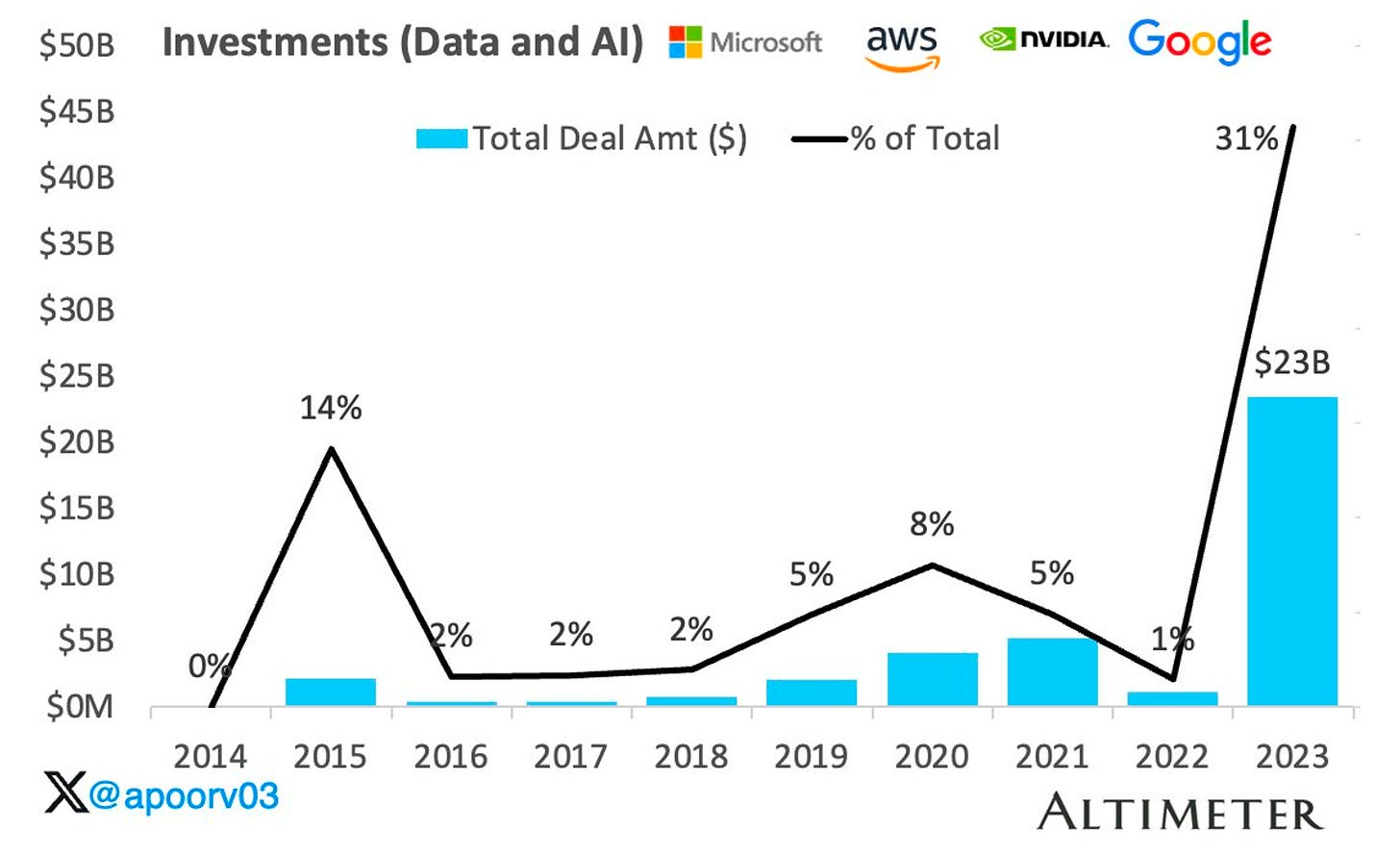

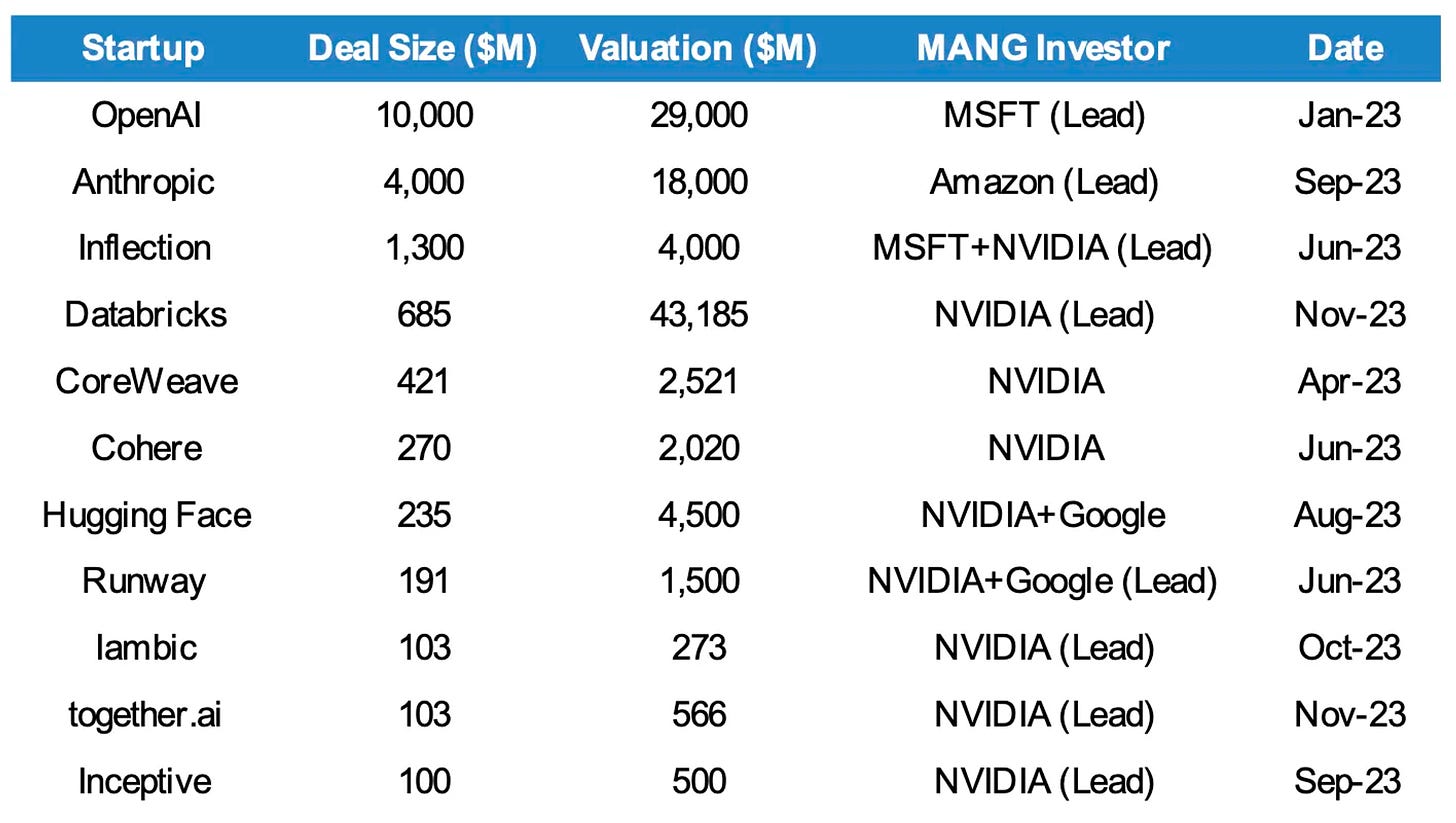

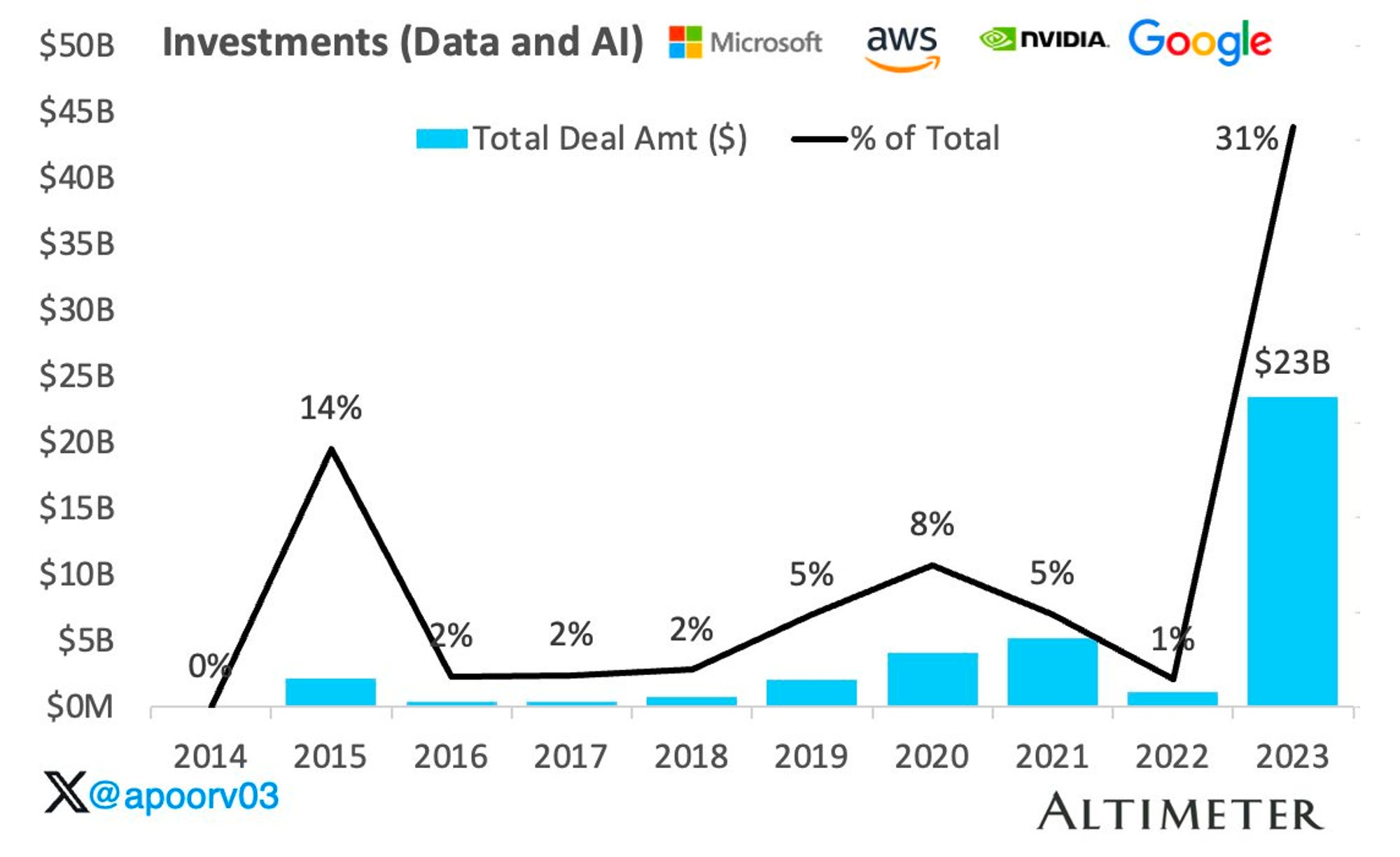

Saturday, Jan. 27th: I listened to a podcast on venture with Bill Gurley and Brad Gerstner. - BG2, Apoorv Agrawal

In 2023, 9% of the funding raised by startups in North America involved Microsoft, Amazon, Alphabet, and Nvidia. This percentage rose to 31% for startups in the data and AI sectors.

Microsoft made a massive investment in OpenAI. “A big part of that investment was not cash dollars but credits for the cloud services.” Other cloud services providers became fearful of loss of relevance or market share and started to make copycat transactions (e.g. Amazon into Anthropic). These investments are creating a market disruption in the AI market.

LLMs are using this cloud credits to train their models or to resell their software packaged with the compute. On the training side, it makes impossible for newcomers to compete without the backing of large cloud providers. “It’s a sport of kings to build a LLM.” On the resell side, LLMs could resell their software at negative gross margins because they don’t perceive cloud credits as a COGS.

“Once you have these credits inside your company, somebody going to be ignorant to the cost because it's now not a real cash cost or is going to fool himself that it can sell his software below the replaceable cost of the credit” (i.e. at negative gross margin). In a price war between LLMs, it’s easy to imagine that they will price below the cloud credit cost.

“It may also be that the lack of M&A leads to people to be more experimental with how you know they want to deploy Capex.”

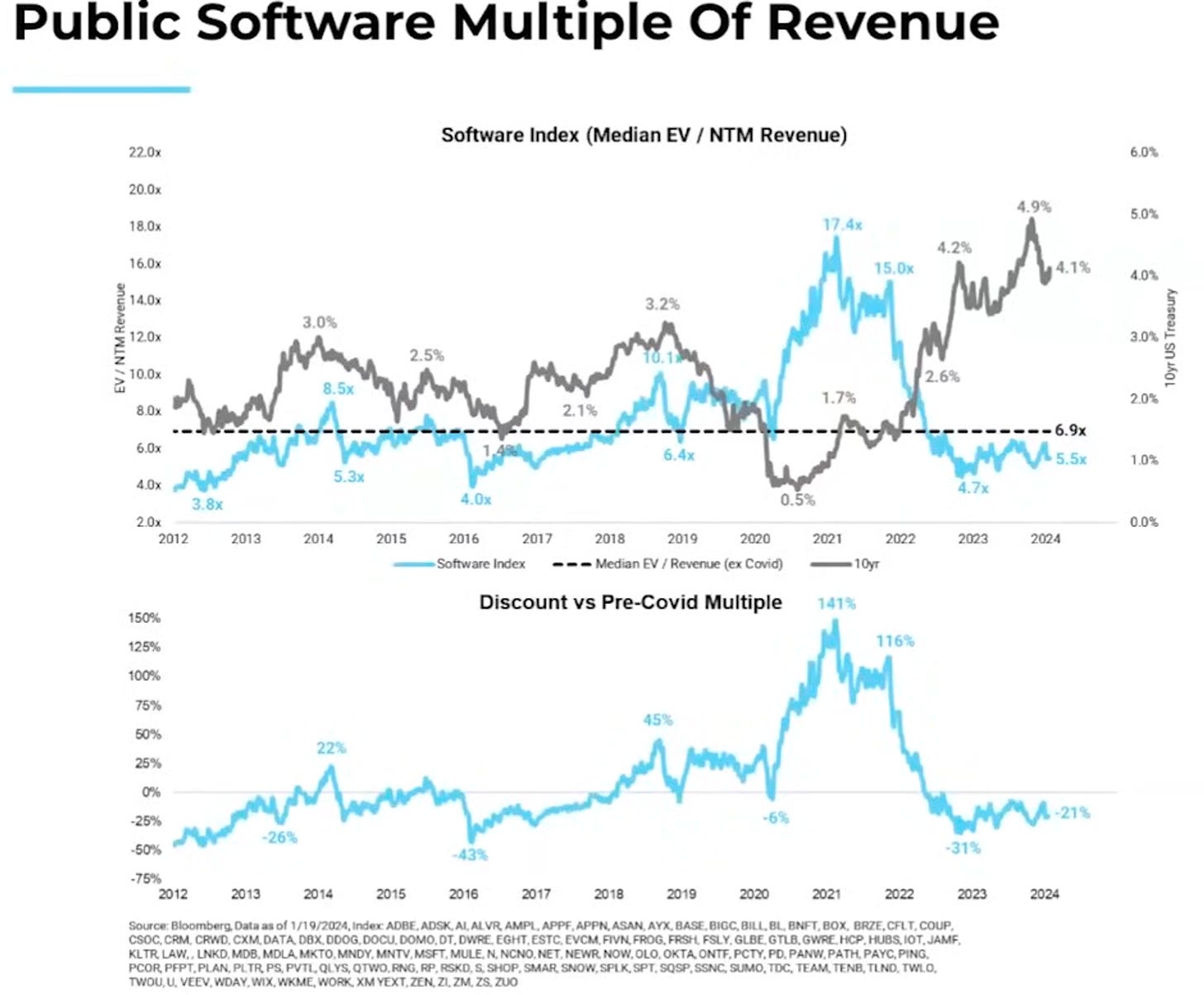

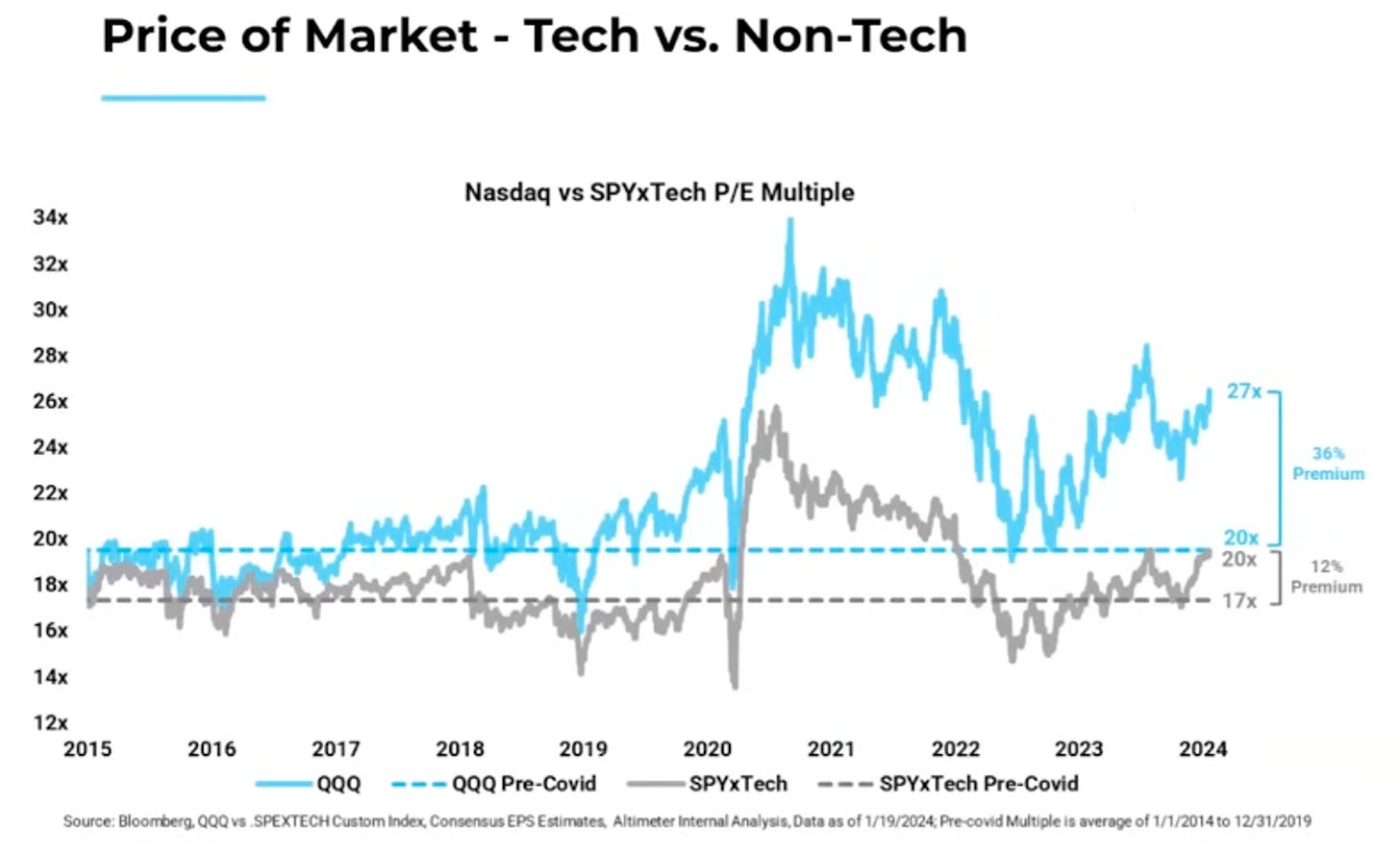

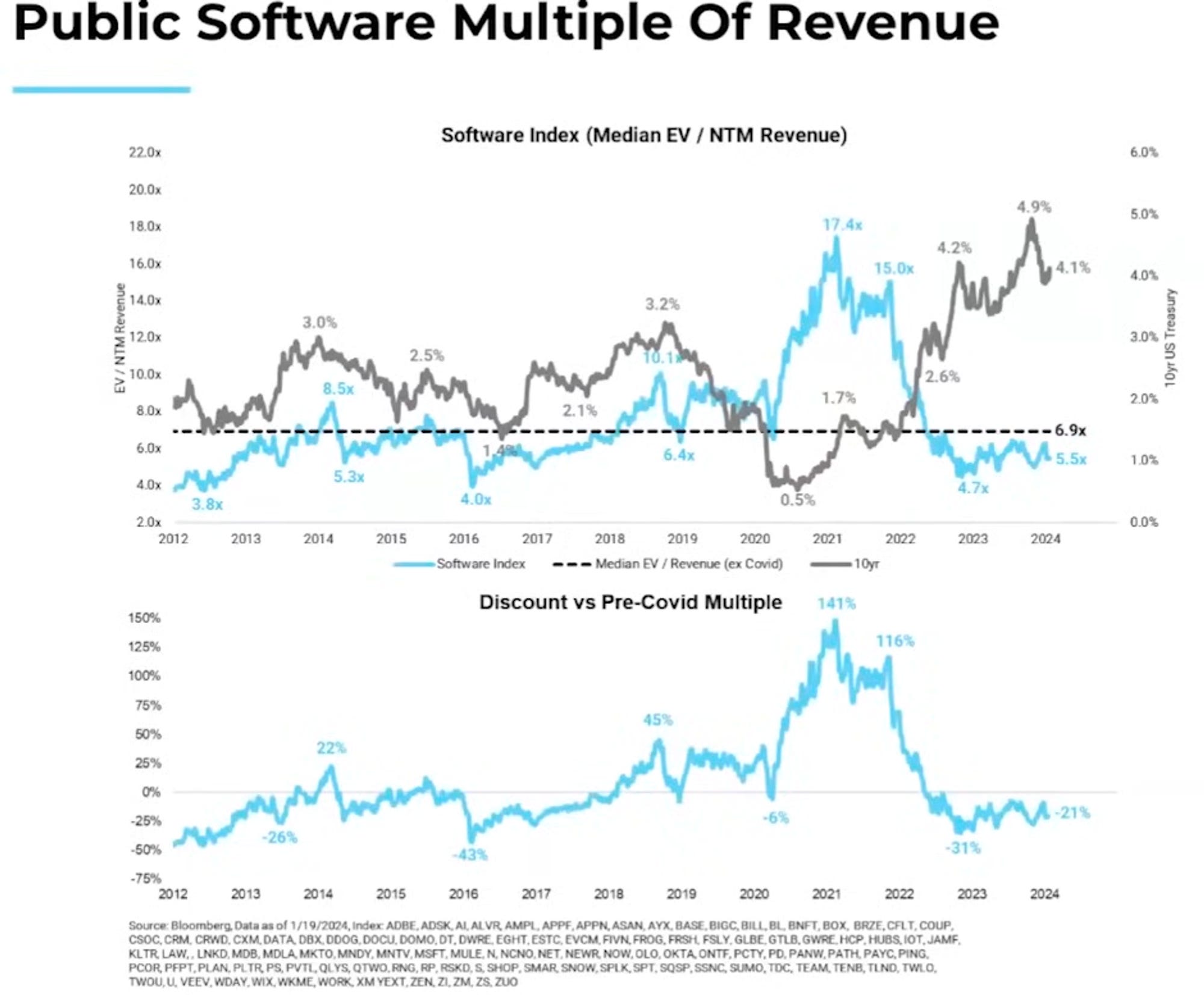

In 2023, we saw a multiple expansion in the public market which is more a reversion to the mean after the big pullback in 2022. In 2020-2022, multiples skyrocketed driven by ZIRP and the belief that covid would bring digitisation to an unseen level. Today, both tech and non-tech are trading at a premium of 10y historical average (software is still trading at a discount).

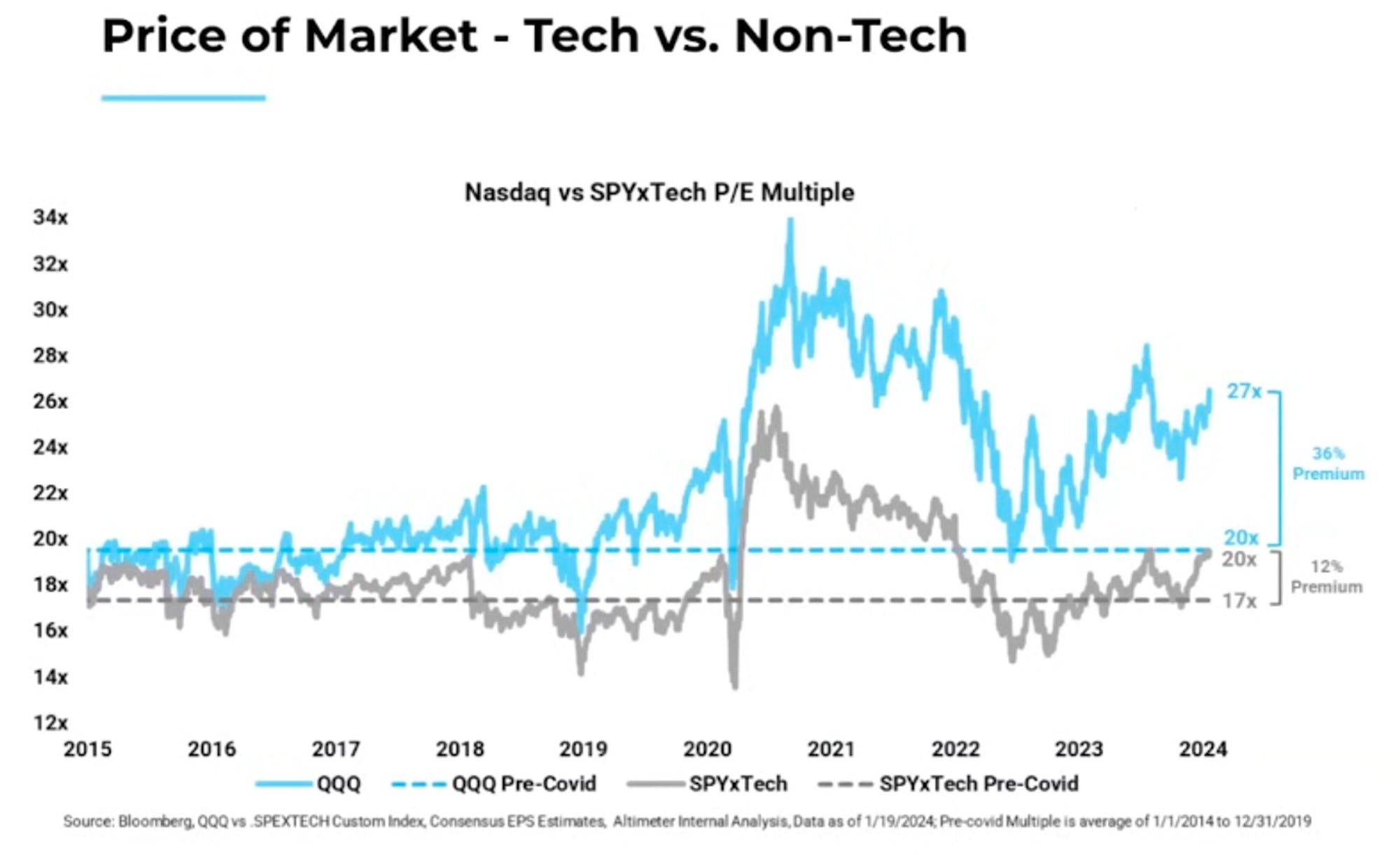

Today, the largest tech companies have some of the highest growth rates. We were told that companies had diminishing returns as they scale because they can no longer innovate and have a good return on capital. With technology, it seems that companies have an increasing advantage of scale in which you need to have a large amount of cash to pursue the key opportunities in technologies (e.g. AI and VR). It’s the first time in history that large companies don’t become laughing stocks even in technology where some stocks in the 1st generation became irrelevant (e.g. HP, Dell).

In private markets, the main differences compared to previous market correction is that many private companies had raised massive amount of cash before the correction and aggressively reduced their cost structure when the correction happened. It massively elongated the runway of private companies delaying the day of reckoning. In 2023, we’re already seeing many shutdowns in tech (c.800 companies in the US according to Carta).

Founders should get in touch with their real valuation as quickly as possible and design a plan to have the best possible outcome given the new market reality. “It's not good for the employees, it's not good for the company and it's not good for the investors if you're living in delusion when it comes to your to you know to your cap table and to your valuation.”

Sunday, Jan. 28th: Clément Vouillon share some recent learnings on vertical SaaS. - Clément Vouillon

“There are probably fewer verticals than I thought that are large enough to support “VC backed” types of companies. A corollary is that plenty of vSaaS are probably better suited for “PE style” trajectories than for “VC backed” trajectories. From a VC perspective, it can make sense to invest mainly in vertical SaaS companies at Series A once they have ticked all the boxes. And if you do invest in a VSaaS at pre-seed / seed, then you need to be ready to be on board for a long time and to financially support the company from seed to series A (included).”

“Most vSaaS customers want Swiss Army knives. Most vertical markets require a Swiss Army knife type of product –a.k.a a product with a ton of features. This is because users in many verticals prefer an all-around tool over using multiple separate applications.”

“vSaaS founders need early stage investors that can support them financially for a longer time. For vSaaS founders who raise pre-seed or seed rounds, it seems to me that it’s crucial to raise with VCs capable of doing bridge rounds and even doing the Series A.”

“Not taking VC money early can be a good option. In the past couple of months I saw an increasing number of VSaaS that raise money after spending +6 years self funding their company.”

Monday, Jan. 29th: Lightspeed is employing a private-equity technique known as a continuation fund to offer liquidity to its LPs. It plans to transfer a portfolio of 10 holdings, valued at approximately $1bn, into a new fund which it will continue to manage. Insight has already utilized continuation funds, and NEA is currently discussing with LPs the possibility of raising a similar fund. - FT

“Selling the stakes to a continuation fund would give existing investors the chance to cash out, bring in new backers and allow Lightspeed to hold on to the investments for longer.”

“Continuation funds can also be controversial with LPs, because they have to decide whether to lock up capital with a VC for another lengthy period or cash out potentially at a discount.”

Tuesday, Jan. 30th: Palword is making a splash in the gaming industry. Described as “Pokemon with guns”, it was released on Jan. 19th. It has already sold 8m copies on Steam alone and has surpassed 2m concurrent players on the platform (2nd record after PUBG). The game is successful for two main reasons. First, it combines elements from various popular genres, including open-world survival games, creature collection, and crafting. Second, it leverages a growing frustration around the Pokémon franchise which has not innovated for years. Palworld is accused of copying Pokémon characters design and is being pursued by The Pokémon Company. In parallel, it seems that Palword has used Gen. AI to design gaming assets. - Eurogamer, Gamerant

Wednesday, Jan. 31st: USV updated its investment thesis. It’s now framed as “investing at the edge of large markets under transformative pressure.” - USV

“The “edge” of large markets is often the best place to introduce new ideas and approaches. Startups at the edge often start out looking weird, yet have the potential to take on incumbents in surprising new ways.”

“Technological and societal pressures can upset existing market structures, creating openings for new companies and networks to meet the market in new ways.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋