🗞 Venture Chronicles - January 2023

Overlooked #137

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of January.

For 2023, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for January!

Sunday, Jan. 1st: I read Fred Wilson’s 2022 retrospective and 2023’s predictions. - Fred Wilson 1, Fred Wilson 2

“The air came out of the asset price bubbles that had built up over the last decade and were accelerated/exaggerated by the pandemic. […] what happened in 2022 was entirely predictable, expected, and necessary.”

“Spending for growth has largely stopped and most tech companies and startups are growing more slowly but with better unit economics and lower cash burn.”

2023 is going to be a tough year for startups. Startups who avoided to raise in 2022 will have no choice but to raise in 2023. Out of them, many don’t have PMF, don’t have strong unit economics and/or have team-related issues. Most of them will not be able to raise capital and will fail.

“Good businesses with product market fit, positive unit economics, and strong leadership teams will raise capital although it will be at the new normal in terms of valuation. I believe that “new normal” is more or less where we were in 2015 where seed rounds were done around $10mm, A rounds were done around $15mm to $25mm, B rounds were done around $25mm to $50mm, and growth rounds had a cap at 10x revenues. This new normal will lead to many flat rounds, down rounds, inside rounds, and rounds with a lot of structure on them. None of that is good, but the worst of those options is rounds with a lot of structure. I believe founders and CEOs and Boards should take the pain of a new valuation (flat, down, whatever) over structure.”

Monday, Jan. 2nd: During the past 4 years, bookstore chain Barnes & Nobles has operated a successful business turnaround going back to profitability and opening 16 new bookstores in 2021. James Daunt who already turned around a UK bookstore chain called Waterstones joined in Aug. 2019. He succeeded mainly because he was passionate about reading and decided to put books and readers at the centre of everything. - The Honest Broker

“I could draw many other lessons from the Barnes & Noble turnaround. I praise its decentralization, and its willingness to empower booksellers at the local stores. I like the way the stores look nowadays, and the improved selection on the shelves. But the key element uniting all of this is putting books and readers first, and everything else second.”

Tuesday, Jan. 3rd: Shopify launched a HR refactoring plan to boost its productivity. It includes implementing a meeting-free day on Wednesday, removing for at least two weeks any meetings with more than 2 people, moving from an annual to quarterly planning circle. - Forbes, FT

“The most important resource we have is the time of individual contributors. Companies are built improperly around the time of the manager rather than the doer. We think it’s important to force change. You build a muscle by doing it.” said Kaz Netajian who is Shopify’s COO & VP Product

Wednesday, Jan. 4th: Since the beginning of the year, France has banned single use packaging for on-site dining in restaurants. It will prevent 150,000 tonnes of waste every year. Fast-food restaurants are the most impacted by this regulation. It’s hard for some of them to adapt to this new paradigm which implies using and washing reusable containers. For instance, 10% of McDonalds restaurants have yet to make the shift. The State is going to spend €50m per year to help the sector in this transition. - Le Monde (in 🇫🇷)

Thursday, Jan. 5th: Techcrunch wrote a paper giving more details on USV’s $200m new climate fund that I mentioned in the previous edition of Venture Chronicles. - Techcrunch

“If you look at climate, it addresses some of the core issues with the market downturn right now, including energy, food and minerals. If you invest in climate, you invest in those. We believe in every sector there’s a climate angle.”

USV invests in technologies where the science is fully de-risked (e.g. not nuclear fusion) and the capital is used to scale. It invests in companies that are not dependent from any regulation to thrive (e.g. Inflation Reduction Act). USV will fund both climate reduction and adaptation topics (e.g. FloodMapp which makes predictive flood maps).

Friday, Jan. 6th: The Economist wrote about Tesla. Its tech narrative as a tech company is being challenged by the public market which could end up valuing the company with the same multiples as traditional car manufacturers. - The Economist

In the past 12 months, Tesla once valued at $1.2tn, lost 71% of its market capitalisation. Besides the general tech public market meltdown, Tesla has been experiencing a contraction in demand, supply chain disruption and traditional car manufacturers catching up on the EV opportunity.

Saturday, Jan. 7th: I read several posts on Constellation Software which is a $30bn public conglomerate aggregating vertical SaaS. - Tom Tunguz, 25iq, Verticalized

It was started in 1995 by a former VC called Mark Leonard which raised $25m from OMERS to buy and aggregate “vertical software companies with a moat & good unit economics.”

Between 2003 and 2014, Constellation Software grew its revenues by a 25% CAGR from $80m to $5bn. In 2014, it had even a 40% annual growth mainly driven by acquisitions (33%) complemented with additional customers (10%) and price increase (5%).

Constellation Software makes dozens of small acquisitions ($2-4m price tag) per year. Each business is operated by a team of 30-40 people.

“We are the anti-economies of scale company. We believe in small teams outperforming large teams, and so given the choice of taking a 200-person business and buffing it up into two smaller ones, we would much prefer to do that and believe that the benefits are there as opposed to ramming businesses together, firing a bunch of people and moving a bunch of work offshore.”

Constellation Software has a database with 30k potential targets. It adds 4k targets every year and it tries to stay in touch with each target 3-4 times a year.

“Our favorite and most frequent acquisitions are the businesses that we buy from founders. When a founder invests the better part of a lifetime building a business, a long-term orientation tends to permeate all aspects of the enterprise: employee selection and development, establishing and building symbiotic customer relationships, and evolving sophisticated product suites. Founder businesses tend to be a very good cultural fit with Constellation, and most of the ones that we buy, operate as standalone business units managed by their existing managers under the Constellation umbrella. We track many thousands of these acquisition prospects and try to regularly let their owners know that we’d love the chance to become the permanent owners of their business when the time is right for them. There is a demographic element to the supply of these acquisitions. Most of these businesses came into being with the advent of mini and micro-computers and many of their founders are baby boomers who are now thinking about retirement.”

Sunday, Jan. 8th: Usually, VCs sell their shares post lock-up when their portfolio companies are going public. In recent years, several VCs including Sequoia or a16z decided to retain their ownership into certain public companies because their value was still compounding post IPO and they were leaving returns on the table. With the current market downturn, these VCs are being punished. - WSJ

For instance, Sequoia invested $258m in total into Robinhood. This stake is now worth only $175m. Sequoia could have sell it for $498m in Dec. 2021 when its lockup expired.

“VC firms in 2022 were on pace to return the lowest percentage in more than 15 years of the assets they manage to their backers.”

“The decision on whether to hold on to a stock after its public listing or stick with the more traditional approach has at times helped define the difference between venture-capital winners and losers.” (e.g. Spark which cashed-out its stake into Affirm post lockup generating $1bn for its LPs vs. Khosla which liquidated only 1/5 of its stake for $500m and which remaining stake lost $600m in value in 2022).

Monday, Jan. 9th: Deconstructor of Fun wrote a 2022 retrospective on the gaming market. - DoF

“War, inflation, rising interest rates, recession, the struggle of performance marketing all influenced the games business that these days isn’t quite as recession-proof as it was back in 2008. This is no wonder, given that the business model has evolved from premium products to free-to-play, subscriptions, and ad monetization while competing against other forms of entertainment such as video streaming and social media.”

In 2022, the mobile gaming market decreased by 5-10% in Western countries which is noteworthy for a market used to have an annual double digit growth. Mobile gaming was impacted by Apple’s privacy policy changes, inflation, interest rate increase and the end of the lockdown.

Gaming companies all added crypto gaming into their strategy. Netflix launched its gaming platform building their own version of Apple Arcade. Embracer spent $780m to acquire the Lord of the Rings gaming IP. Call of Duty Modern Warfare 2 hit $1bn in sales in 10 days.

Tuesday, Jan. 10th: I watched Olivier Dauvers’ retrospective on the retail sector in 2022. - Olivier Dauvers

3 long-term trends are decreasing the general performance of the retail sector. First, in the past 10 years, consumption has been almost flat (0.4% annual growth) when it had previously been growing at 2-3% YoY. Second, retail is shifting from offline to online with online being less profitable for modern retailers. Third, retailers are growing their commercial capacities (more stores, more opening hours).

Retail players are drastically competing on prices (e.g. 30-50% discount on a supermarket aisle, champaign bottles below €10, €100 offered for €100 of purchase, price blocked at €0.29 for the baguette) and some players are going out of business. In 2022, stores closed (e.g. Intermarché stores in Paris) and retail chains went bankrupt (e.g. Camaieu).

Price is the main purchasing factor in retail. The lower you price, the higher revenues per store square meter you make.

In 2022, we went from 10 quick commerce players in Paris to 2 players (Flink and Getir/Gorillas). Quick commerce is also reducing its service quality, increasing its delivery time from less than 10 minutes to around 30 minutes.

In 2022, food retail experienced a 10% annual inflation. If we dig further on top 150 products, annual inflation is even above 15%.

To fight inflation, retailers blocked the prices of certain items and put forward private label first price products against national FMCGs.

Many conflicts happened between retailers and FMCG brands (e.g. Intermarché with Nescafé, Andros, Danone Eau) because FMCG brands wanted to increase the price of their products.

Product shortages were omnipresent in 2022 (e.g. mustard, oil). In retrospect, I believe that we’re moving away from an affluent society and that entropy causing economical shortages will keep increasing in the next decades.

Retailers are trying to implement subscriptions to get additional loyalty benefits (Monoprix, Carrefour), to rent items (Kiabi, Décathlon) or to get free products everyday (Prêt à Manger, Pizza Del Arte). Subscriptions help to retain consumers in the long term.

Casino is trying to apply the commercial strategy used for non-food products (e.g. have a higher starting price than competition and offering more discounts to sell generosity over low prices all year long) to food products. They implement several levers: (i) a subscription offering a 10-20% discount for everything, (ii) buy €1, get €1 offered on your next purchase, (iii) showing that you have lower prices than anybody else, (iv) putting forward its private label called Leader Price, (v) massive discount campaigns (pay back train tickets, toll fares, energy bills with coupons).

Wednesday, Jan. 11th: I listened to a Colossus’ podcast episode on Hermès with Mark Urquhart who is a partner at Baillie Gifford. - Colossus

It’s a €9bn revenues business (50% from leather goods, 20% ready to wear, 25% silks and 5% from entry level goods like perfumes) with 70% gross margins and 40% operating margins. Hermès does not need a second act because its brand is a uniquely sustainable moat based on its heritage and its craftsmanship. It did not engage in a M&A strategy like LVMH and it remained mono-brand.

Hermès does not offshore at all. Everything is made in its French ateliers. Its main growth bottleneck is to recruit and train artisans (it takes 2 years to get someone up and running) in its ateliers. It pays top dollar for the best leather. It makes its bags from one contiguous piece of leather (vs. being stitched together from different panels).

Hermès sells almost exclusively in its stores. You need to apply to buy a handbag and you have to wait on average 18 months. Hermès generates €50k per square meter which is as high as the Apple Store on the Fifth Avenue in NY.

Hermès does not spend on advertising. People just know about the brand.

“There's been this extraordinary period of […] technology businesses, just absolutely exploding, going to huge verticals. But as I look back on that now, almost growing a little bit too fast and kind of sucking so much growth that it has made it harder now at the scale and everyone's looking for the second act in a lot of these businesses and Amazon did it with AWS. Meta hasn't really done it. But the beauty of this business is it doesn't need a second act. The first act is 185 years old. And it's still the same act that's still doing well.”

Thursday, Jan. 12th: Tracy Young shared her learnings from scaling PlanGrid to $100m in ARR. - Tracy Young

“Hire a great HR leader as a business partner to help recruit and retain the right team, and architect a good communication flow. And remember that A players can recruit other A players, but B players usually end up recruiting C players.”

“My biggest mistake was hiring a big-public-company tech executive with a fancy resume who had never worked at a startup. And although everything in my gut told me that they were the wrong fit, I felt so underwater with work that I convinced myself that my life would suck less if they were just in the building.”

“Although we skipped the corporate buyer completely in the early years of PlanGrid to much success ($50M in ARR), in order to get to $100M in ARR, we needed to go upstream toward the enterprise segment and build products for the corporate buyers who would never touch our core product. Selling to the enterprise requires a series of features and products that have nothing to do with making the end-user happy.”

“It is completely possible to have product-market fit one year and lose it the next because the world, the market and the competition shifts over time. Always go towards where it hurts the most and try to fix that problem because it’s not going away.”

Friday, Jan. 13th: Digitail raised a $11m series A led by Atomico. It’s a vertical SaaS for veterinary practices. It’s both an app for owners and a Practice Information Management System (PIMS) for veterinary practices (including scheduling, record keeping and inventory management). “Digitail reduces administrative burden by 40-60%, freeing up the time to see to roughly twice as many patients per day.” In 2022, it went from $150k to $1m in ARR with 750 clinics (inc. 200 in the US) and 1.4m pet profiles created. It will use the funding to expand in North America. The US pet care market should grow from $118bn in 2019 to $277bn by 2030. - Techcrunch, Business Insider, Atomico

Saturday, Jan. 14th: Mario Gabriele from the Generalist wrote a deep-dive on Constellation Software (CSU). - Constellation

Mark Leonard created CSU out of a personal frustration as a venture capitalist. He was seeing many strong vertical market solutions (lower competition, mission critical software with high usage rate and low churn rate, strong unit economics) but could not invest in them because these businesses were too niche to generate venture returns.

CSU has a virtuous cashflow cycle because it uses the cash flow generated by its vertical market software to make new acquisitions.

CSU has a unique decentralised culture. Mario Gabriele talks about “management by abdication”. CSU does not integrate acquisitions and pushes their management team to run their business as autonomously as possible. “One of the fundamental beliefs at CSU, is that autonomy motivates people, and bureaucracy does the opposite, so we try to do as many of the important monitoring tasks with as light a touch as possible.”

Sunday, Jan. 15th: I listened to a podcast episode from Happy Millionaire with Fred Destin who founded and is a general partner at Stride. - Happy Millionaire

Startups thrive in chaos. Startups win over incumbents because they’re highly adaptable.

Stride positions itself as an anti-VC breaking as many rules as they can in the venture industry. For instance, instead of trying to have control over founders, they try to create a relationship fully built on trust.

Venture is not about downside minimisation but about upside maximisation. You don’t need to protect your downside but you need to empower founders to make the right decisions to run faster and to build bigger businesses

To pick startups, VCs want:

Entrepreneurs (i) who are attacking a problem that is fundamentally interesting enough and (ii) who have unique insights about this problem.

Companies with unlimited upside. You don’t need to have a massive initial TAM but you need to see a path to create a massive business that can move the needle in their market.

A thoughtful execution plan for the next 12-36 months.

Companies which will be able to raise follow-on rounds from the capital market and which have clearly identified risks to be tackled in the next 36 months.

Monday, Jan. 16th: Startups are failing to disrupt the insurance industry. - FT

$40bn have been invested into insurance startups in the past 5 years but consumer insurance remains undisrupted (e.g. car and home) for several reasons: (i) it’s a price driven market, (ii) it’s expensive to acquire customers via online marketing, (iii) in the early years, it’s hard to have a low cost structure (low loss ratios and low claim management costs).

Tech giants could be great contenders to disrupt the industry (e.g. Amazon planning to launch an insurance portal in the UK).

“The customers just don’t care enough about their insurance. You have a very competitive market where the majority of customers are focused on price. They care less about the features.”

Tuesday, Jan. 17th: I read Alloy’s state of fraud report. - Alloy

Fraud is a hot topic. “100% of respondents have experienced fraud. 96% have lost money to fraud over the past 12 months. 91% said that fraud increased YoY. 71% of respondents have increased their spending on fraud prevention YoY.” 47% said that they have experienced 1k+ fraud attempts in the past 12 months. 70% said that they have lost over $500k in the past 12 months.

There are several categories of costs when a fraud is committed: (i) direct financial losses, (ii) regulatory penalties, (iii) reputational damage, (iv) legal repercussions and (v) loss of customers.

Wednesday, Jan. 18th: The Economist wrote about Amazon. - The Economist

During Covid, Amazon expanded much more aggressively than other tech giants (doubled the size of its fulfilment network, increased its payroll from 800k to 1.6m between 2019 and today). Amazon’s stock price is being punished by the stock market having lost $1tn in market cap. since its peak in mid 2021.

Amazon faces 3 main challenges: (i) a retail business impacted by a lower consumer demand, (ii) cash engines facing a decelerating growth (AWS and ad business) and (iii) growing competition from retailers and from other tech giants.

Thursday, Jan. 19th: Brighteye released its European edtech funding report. - Brighteye

Global edtech startups raised $9.1bn in 2022 (vs. $20.1bn in 2021). European edtech startups raised $1.8bn in 2022 (vs. $2.5bn in 2021).

Edtech trends to follow in 2023: (i) climate education, (ii) European multinational K-12 infrastructure software companies, (iii) generative AI education applications, (iv) apprenticeship model in higher education to gain momentum, (v) M&A in the edtech sector.

Friday, 20th: Sequoia raised a $195m dedicated fifth seed fund. It will invest in Europe and in the US. It will also be used to fund Sequoia Arc program which invests $500k-$1m into rising founders. It’s a generalist fund but its partners are interested in thematics like AI, consumer social, AR/VR, hardware or genetic sequencing. Sequoia invested at seed in companies like Airbnb, Dropbox, Nubank, Stripe, Whatsapp, Palo Alto Networks and Youtube. - Techcrunch, Sequoia,

“It’s never too early to partner with Sequoia. We want to meet founders right at the beginning of their thought process and play an active role early on: fleshing out ideas, posing questions as food for thought, introducing them to potential customers, and dreaming together about their vision.”

“Over 50 years, we have experienced every cycle of economic euphoria and economic gloom. While markets gyrate, outlier founders building outlier companies persist. They embrace constraints, unlock creative advantages, make technological leaps and are determined to endure. Airbnb, Block, Stripe and WhatsApp all emerged during the Great Recession. We are confident that the next legends are being formed in this moment and we strive to be their first true believers.”

Saturday, 21th: Nik Milanovic wrote about fintechs in the agriculture sector. - Forbes

Agriculture is a large sector (accounting for 5% of US GDP) underserved in terms of modern financial services. Startups are pursuing several opportunities: (i) agriculture lending, (ii) farm payments, (iii) pricing data & commodities trading, (iv) insurance, (v) marketplaces for farmers, (vi) verticalised neobanks.

“Over the next decade, we will see a parallel market of products across all fintech categories – banking, lending, savings, payments, investment, HR, payroll, and trading – develop focused specifically on agriculture.”

Sunday, 22th: I found a chart on food chains showing the number of units in the US compared with the average revenue per unit. Subway has 21k locations in the US and each location generate on average $440k in annual sales. Other top chains including Five Guys, McDonald’s, Krispy Kreme, Raising Cane’s or Check-fil-A are generating more than $3m in annual sales. - Chartr

Monday, Jan. 23rd: The Economist wrote about Goldman Sachs (GS) struggling to reinvent itself. - The Economist

GS is accumulating several failures: (i) it’s too dependent on its investment banking division which is operating in a depressed industry, (ii) it’s struggling to compete in the consumer market dominated by winner-takes-all dynamics, (iii) an increasing competition in European and Asia from local players.

“There is something uniquely hard about reforming elite firms whose unwritten code is that they are smarter than everyone else. […] Goldman’s culture of self-regard remains at odds with the facts. Instead it now needs to be self-critical. For yesterday’s masters of the universe, that may be the hardest leap of all.”

Tuesday, Jan. 24th: Dealroom partnered with Lakestar and Walden to publish a report on European deep-tech. - Dealroom

Deep-tech trends: generative AI, AI-first biology, privacy-preserving AI, quantum computing, AR/VR, advanced AI chips, nuclear fusion, next gen. batteries, green hydrogen, reusable space rockets, satellites, in-space transportation, in-space manufacturing, spacedebris removal.

In 2022, European deep-tech startups raised $18bn (vs. $23bn in 2021 and $11bn in 2020). Deep-tech is more resilient than other sectors, declining only by 9% in H2-2022 compared to H2-2021 when the whole European ecosystem was declining by 46%.

A funding gap exists between deep-tech focused investors which don’t have the firepower to fund companies at growth stage and generalist venture funds.

Wednesday, Jan. 25th: Last year, French healthcare unicorn Alan grew by 62% YoY to reach €250m in ARR (mostly Gross Written Premium coming from its healthcare insurance product) and added 125k new members. In 2023, Alan targets €380m in ARR (52% growth YoY) with a 13% gross margin. In 2025, Alan wants to become profitable. It has €230m in the bank to reach this objective. In May 2022, Alan raised a €183m series E at a €2.7bn valuation. - Alan, Sifted

Thursday, Jan. 26th: Arda Capital wrote about declining returns in software investing. - Arda Capital

“Historically, building a software business capable of becoming a unicorn or going public required some insight or innovation (technical, GTM, data). But because of the availability of capital over the last decade, many founders and management teams have underinvested and/or ignored this requirement as they grew their businesses. In an era of cheap capital, it became too easy to hire a few additional reps, spend a little more on SEO and marketing to maintain healthy growth rates, and fend off investor concerns. As a result, many recent software unicorns have built businesses with thin or non-existent durability of growth or moats. Many software businesses today have unit economics and capital efficiency that are meaningfully worse than what investors have come to expect from the business model.”

“The average lifetime burn multiple for SaaS businesses at IPO has steadily increased over the past few years.”

“Most software businesses fall into a bucket of vanilla SaaS. These software segments are filled early on with multiple competitors with similar feature sets, rough product parity, and relatively low customer switching costs.”

SaaS’ sources of defensibility: mission-critical system of record (e.g. payroll), great product with organic demand & efficient GTM (e.g. Altassian), becoming industry standard for a function (e.g. Salesforce), ecosystem dynamics (e.g. Bill), discover an underserved segment/market (e.g. Veeva).

Friday, Jan. 27th: Deel disclosed impressive metrics: $296m in ARR (5.2x YoY growth), a $12bn valuation (40.5x EV/ARR multiple), 15k customers, 85% gross margin and EBITDA positivity. It started in 2019 as a platform to hire remote employees and contractors without needing to have a local subsidiary. Deel also released a HR suite specifically built for global/remote-first companies as it supports all categories of employees (local employees, international employees, contractors, etc.). It decided to offer its HR suite for free for all companies with less than 200 employees which is going to be an aggressive acquisition strategy to bring companies into its ecosystem before monetizing them when they start hiring/contracting people abroad. - Techcrunch, The Split, Deel

Saturday, Jan. 28th: FJ Labs raised $260m in dry-powder for a pre-seed/seed fund and a series B+ opportunity fund. It invests in marketplaces and other businesses powered by network effects. It has invested into 900+ companies including Alibaba, Coupang, Flexport, and Delivery Hero. - Techcrunch

FJ Labs does “angel investing at venture scale. We don’t lead. We don’t price. We don’t take board seats. We decide after two one-hour meetings over the course of a week whether we’ll invest or not because we have extraordinary pattern recognition that allows us to decide extremely quickly.”

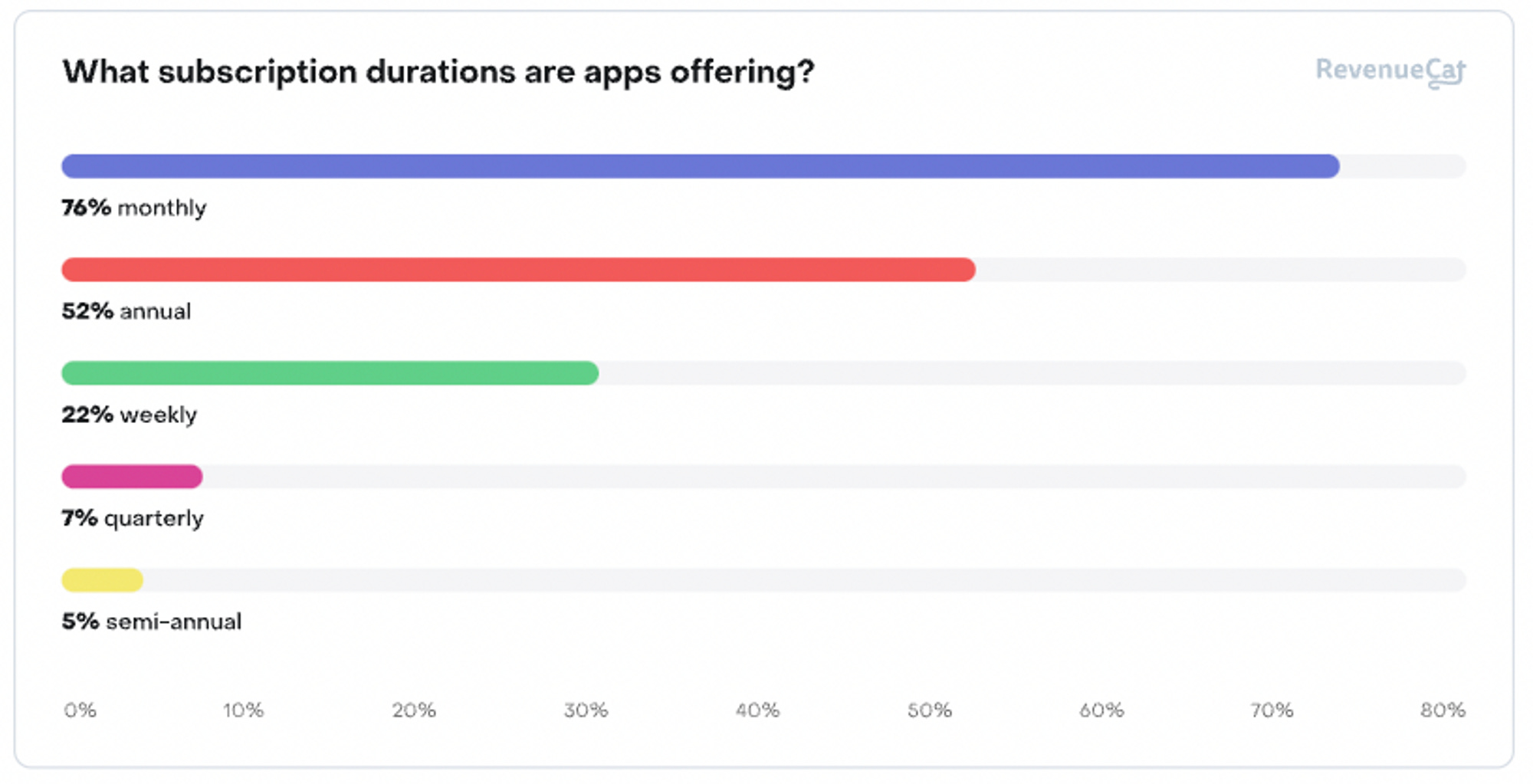

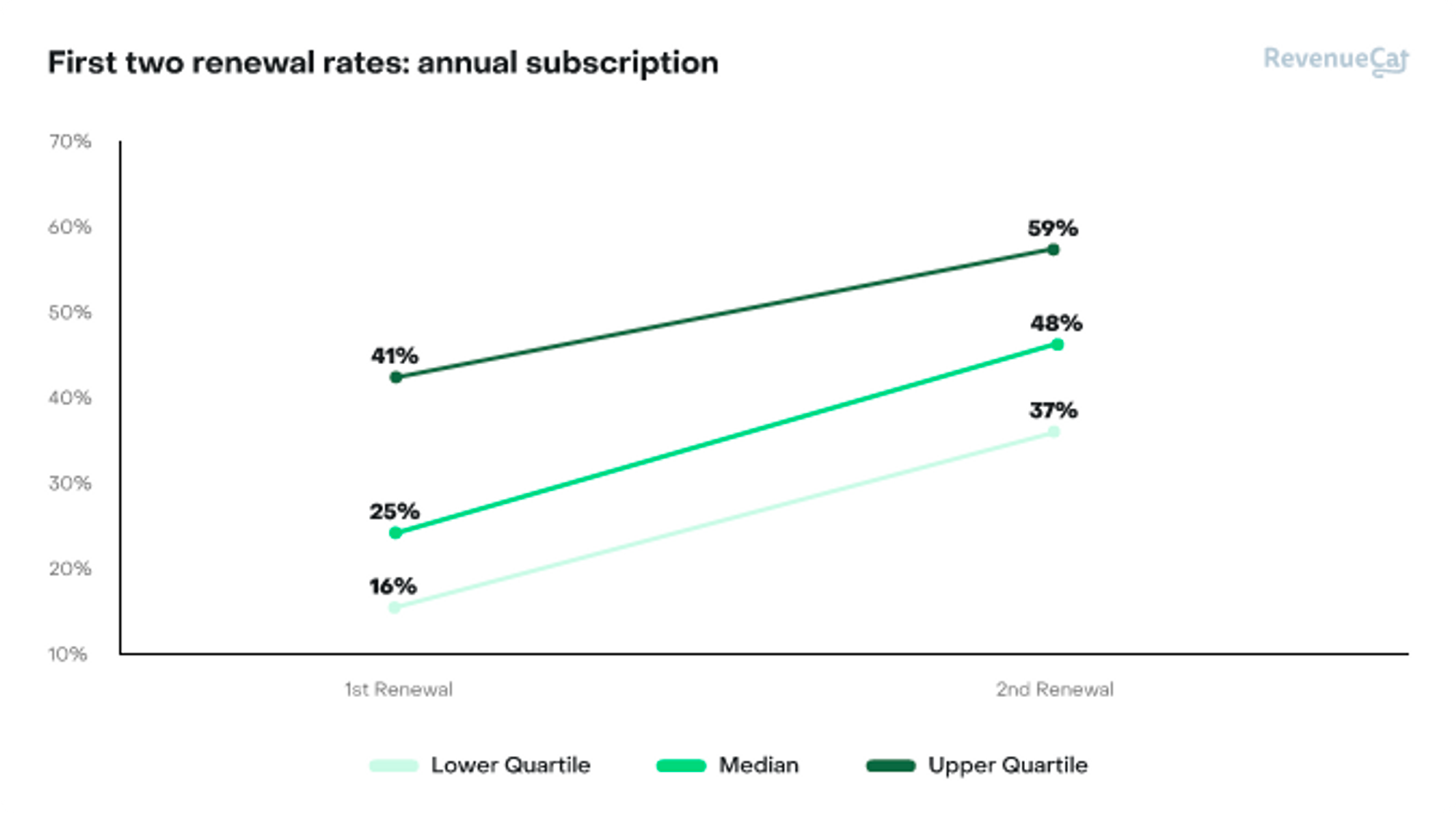

Sunday, Jan. 29th: Revenue Cat published a report on subscription apps aggregating data from 22k apps. - Revenue Cat

Less than 2% of downloads convert to paid users (4% for top apps). For apps with a free trials, 3.7% of downloads start a trial and out of them 38% convert to paid subscribers (60% for top apps). Top quartile apps have an annual renewal rate above 41%.

Monday, Jan. 30th: I listened to Tim Ferris interview Benchmark investor Bill Gurley. - Tim Ferris

“One of the most common mistakes entrepreneurs make is they come up with some kind of technological breakthrough in their own mind, but they don’t spend any time analyzing the industry structure or whether the go-to market is going to be possible or not.”

In venture, you need to “have strong opinons, loosely held”. “All investors have to work within that framework because things change. There’s many, many variables. None of them are constant, they’re all dynamic. And the minute you set a very hard rule, then you might be setting yourself up for a mistake.”

Benchmark has an equal partnership structure. As a result, everyone in the team wants his other partners to be as successful as possible. Everyone’s voice is heard and there is no hierarchy.

The VC industry is set up to go through booms and busts. It’s like a rollercoaster. Risk appetite increases very slowly but when it crashes it happens all at once.

Books recommendations: The Rational Optimist by Matt Ridley, Competitive Strategy by Michael Porter, Innovator’s Dilemma by Michael Porter, Crossing the Chasm, Startup by Kaplan, Build by Tony Fadell, Shoe Dog by Phil Knight, Complexity by Mitchell Waldrop, Range by David Epstein.

Tuesday, Jan. 31st: I listened to a 20VC’s podcast episode with Albert Wenger from USV. - 20VC

“To be a good operator, you have to stay focused on one thing for a long period of time and you have to be great at dealing with people.”

“The limiting factor in our society is no longer capital but attention. What do we attention to as individual, as a society and as humanity?”

USV nails the boutique strategy being hyper-focused on an investment thesis. USV thinks about large transformative forces in our world creating opportunities for new startups. Investing in climate is an extension of our thesis-driven approach. Having 3 vehicles with a specific thesis (early stage, opportunity, climate) forces us to be extremely disciplined on how we allocate capital.

Jeff Bezos “is probably the best entrepreneur that I’ve ever been around or got to know. It’s remarkable and it’s multifaceted. [..] He has built a organizational framework to take what [he] believes and run the whole company that way.” “He’s institutionalized […] experimentation and risk seeking.

“AWS is maybe one of the top five business move in the history of the world.[…] They launched that out of a consumer internet company and became one of the most important enterprise companies. It’s fairly unprecedented, it’s just amazing.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

The veterinary field is fascinating, and the market is exceptionally vast in the USA. I'd love to chat about the French market with you and hear your insights. I'm actively involved in developing projects in this industry !