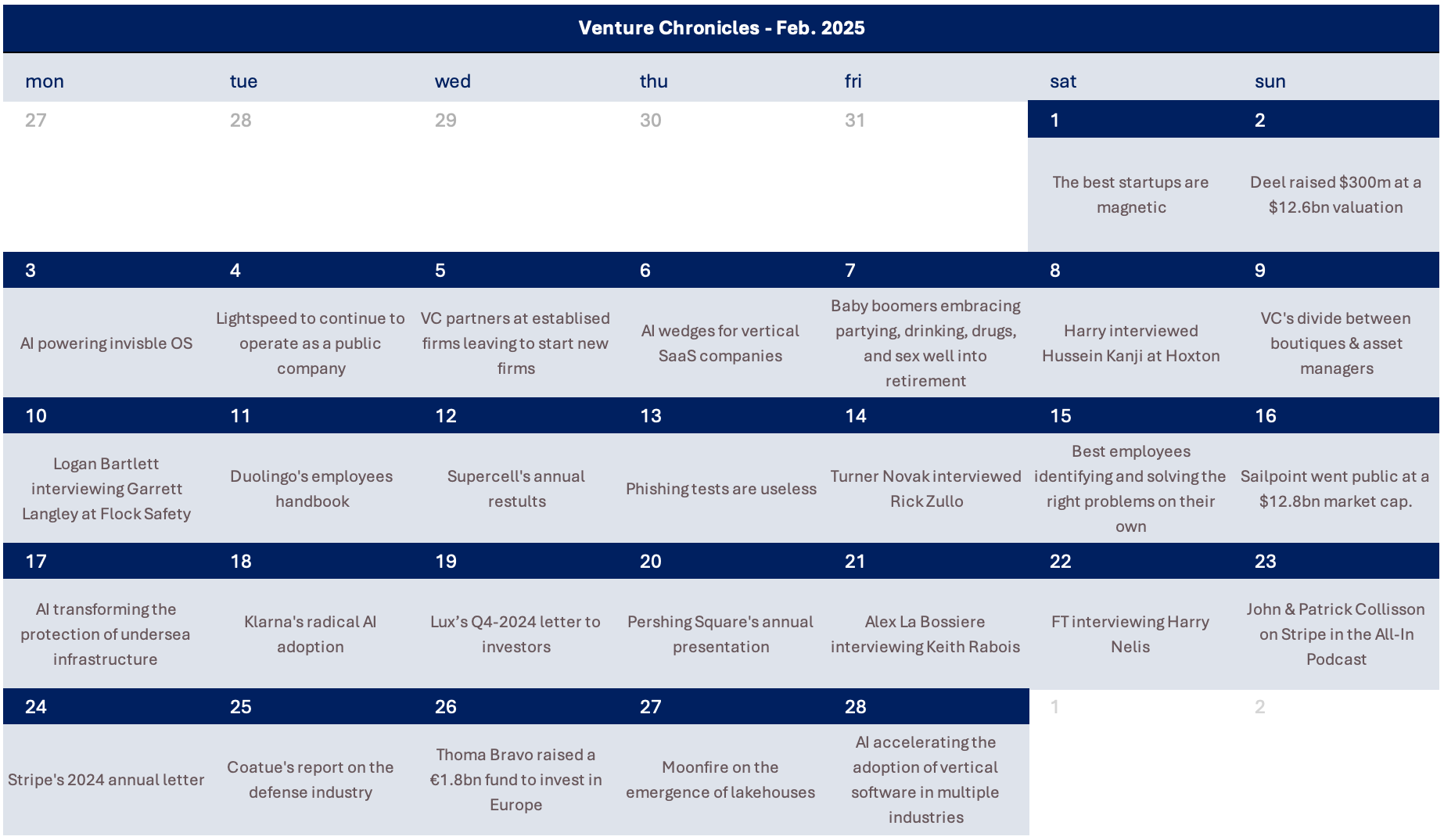

📖 Venture Chronicles - February 2025

Overlooked #193

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of February.

Saturday, Feb. 1st: The best startups are magnetic. - Ricardo Sequerra

“A significant unfair advantage I’ve observed successful startups develop early on is a somewhat elusive magnetism they cultivate around themselves. This magnetism generates a powerful field of attraction that unites teams, draws in talent, and pulls customers toward them rather than the other way around.”

“This magnetism becomes even more valuable as companies scale. It keeps your team aligned and motivated through high tides and low tides. It helps self-select candidates into a company's hiring funnel.”

“Magnetism can also attract customers without full reliance on an ever-scaling sales function. Customers want to buy your product because they identify with your story.”

Sunday, Feb. 2nd: Deel raised $300m in a secondary sale with General Catalyst and Mudabala at a $12.6bn valuation to bring liquidity to early investors. Deel is a HR and payroll platform specializing in global workforce management. It also reached $800m in ARR growing 70% YoY serving 35k customers in 150 and processing $11.2bn in payroll annually. The company has been profitable for two consecutive years. Deel is aslo laying groundwork for a potential 2026 IPO.- Techcrunch

Monday, Feb. 3rd: The future of AI is an invisible operating system that removes the need for thought by anticipating and automating tasks, seamlessly integrating into existing workflows. - Invisible OS

This AI OS will be contextually aware, predicting user needs and actions based on data analysis and real-time feedback.

The key to success lies in building within existing systems, gradually increasing automation and value, and becoming the default for productivity.

The moat for this new OS will be the ability to reimagine workflows, network effects, high switching costs, and the ability to adapt to regulatory changes.

“Every massive consumer technology business is selling the same thing: the removal of thought. In the end, convenience always wins.”

“Today's assistants are still glorified command-line interfaces waiting for the perfect prompt. Instead of eliminating cognitive friction, AI assistants today demand more from us—more effort, more interfaces, more behaviors to learn. The next wave will embody ambient intelligence: No extra commands. No expected self-education. No frothy promises about enhanced workflows.”

Tuesday, Feb. 4th: After several months of strategic review, Lightspeed’s board of directors announced that the company will continue operating as a public company and that it will buy back $400m in shares. Lightspeed is a Canada-based vertical software platform that enables small restaurants and retailers to operate their businesses. - Bloomberg

“The company said it plans to focus on building out its retail operations in North America and its hospitality business in Europe.”

“This resulted in our conclusion to double our focus on growth in retail in North America and hospitality in Europe going forward, as well as to embark on a focused transformation plan, which we've started executing.”

“Lightspeed founder and Chief Executive Officer Dax Dasilva, who returned for his second stint as the head of the company last February, initiated the review on whether to go private after its shares slumped deeply from their 2021 peak of nearly C$160. They slid another 16% to after the open Thursday, the steepest drop in a year.”

“Hospitality in Europe is another leading growth engine. Our market leadership is bolstered by local presence across major geographies such as Germany, U.K., France, Switzerland and Benelux. We enable our customers to comply with a broad range of fiscalization rules, a key differentiator for the Lightspeed software offering. We've recently rolled out Tableside, our handheld POS and our Kitchen Display System and are already seeing strong merchant adoption.”

“From a go-to-market perspective, we continue to roll out our new sales motion designed to drive growth by focusing on targeted outbound strategies and sales efficiency. In hospitality in Europe, we are scaling field sales teams and local marketing to support growing lead volume. Moving forward, we are prioritizing product and technology investments in our two leading growth engines.”

“In hospitality in Europe, we are optimizing front and back-of-house operations, including mobile reporting, enhanced guest experience, insights and analytics and payroll solutions.”

Wednesday, Feb. 5th: Many venture capital partners are leaving established firms to start their own or join new funds. - Forbes

“After former Facebook product leader Mike Vernal left Sequoia in 2023, he spent a lot of time considering the ideal strategy for a new venture capital firm to win deals and quickly establish itself. His solution: “Pick a trend that is going to matter a lot, that will be defining over the next decade and become the top manager in the space.””

“There is a sea change among venture capital’s partnerships bigger than any the industry’s seen in years. For months, and especially during the recent holiday season, partners from decades-old firms and new establishment heavyweights took to LinkedIn and X to announce they were moving on to a new thing. To name just a few in a long list: Alex Taussig and Nicole Quinn from Lightspeed; Matt Miller from Sequoia; Sriram Krishnan and Michelle Volz from a16z; Bilal Zuberi from Lux Capital.”

“Zuberi, who has not yet formally left Lux, said he plans to launch a firm focused on seed and Series A deals at the intersection of AI and the physical world. “I believe some senior GPs [general partners] are realizing that their passion, and expertise, lies in early stage true venture, which is a bit different than what many multi-stage firms do,“ Zuberi told Forbes.”

“Whether they jumped from an established firm or were pushed, investor departures can generally be attributed to two concurrent issues facing the industry in 2025: evaporating financial incentives and bloated partnerships.”

“People are realizing that some of these funds may not even return their capital at all. […] The golden handcuffs are breaking. Financial loyalty at VC firms has never been weaker.”

Thursday, Feb. 6th: Joe Schmidt at a16z wrote about AI wedges for startups trying to disrupt vertical software incumbents. - a16z

“A wedge is a product that helps start a relationship with a customer and (hopefully!) is able to capture valuable downstream data.”

“Wedges have historically focused on capturing data. They’ve generally enabled human-generated information to be entered into or extracted from a system. Think sales reps entering prospect information into Salesforce, ServiceTitan plumbers inputting scheduling information, or Procore construction supervisors managing project information.”

“What’s exciting about this moment in time is that LLMs can enable experiences that capture data at the point of creation in ways that were impossible for traditional software.”

“It has created what might be a golden era of vertical software — particularly in categories that have been dominated by incumbent platforms for decades, like sales (Salesforce, HubSpot), insurance (Guidewire / Duck Creek), IT service management (ServiceNow), and call centers (Genesys).”

“For industries where most sales or customer service interactions still happen over the phone or in person, vertically trained voice agents might empower a new system of record to capture data before the existing systems of record need to be populated. This eliminates the need for a human to interact with the system of record over time and captures data that, in the past, was challenging to collect.”

“Vertical software companies looking to disrupt established players must strategically position themselves to extract value. With LLMs enabling new ways of capturing and structuring data, these companies are poised to reshape industries and trigger a golden age of vertical software — provided they can integrate seamlessly and build robust moats around their data ecosystems. It’s time for startups to start drinking incumbent milkshakes”

Friday, Feb. 7th: The Economist wrote about older generations, particularly baby boomers, who are embracing partying, drinking, drugs, and sex well into retirement. - The Economist

“Whereas young people in rich countries these days are addicted to their phones, more anxious than previous generations and far less likely than them to use mind-altering substances or to party recklessly, their grandparents belong to a generation that experimented with sex, drugs and rock’n’roll. As they reach older age, they are not giving up their old habits.”

“Elderly revellers are numerous: the number of people over 65 is growing across the rich world. In Britain they are more than a fifth of the population. And they want to have fun. In a way, those over the age of 55 but under the age of 75—roughly speaking, the baby-boomers and some of what is referred to as “Generation X”—are the new problem generation.”

“Divorce rates in the rich world are generally falling. But they are rising among pensioners.”

“More subtle trends may also be in play. For a start, those retiring today are far richer than in the past. Second, they now have fewer responsibilities. From the 1970s onwards, as female participation in the labour market increased, grandparents took on more child care. But in the past decade birth rates have plunged, meaning more older people have no children or grandchildren at all.”

“A minority of the reckless old are causing more direct mischief themselves: they make up a growing proportion of people arrested and convicted of crimes. It is well known that America’s prisons are increasingly full of older inmates.”

Saturday, Feb. 8th: Harry interviewed Hussein Kanji who cofounded Hoxton Ventures. - 20VC

Hoxton differentiates itself through its focus on long-term company building, a contrarian investment approach, and a willingness to engage deeply with its portfolio companies.

Long-term vision vs. momentum investing: Hoxton aims to build durable, large companies, rather than focusing on short-term gains. Many firms, particularly in the US, have become "momentum investors" who prioritize investments based on the potential for quick markups instead of focusing on the long-term potential of a company.

Contrarian approach. Hoxton seeks out opportunities that are not immediately obvious or popular. They look for companies that are creating new categories rather than following existing trends. Hoxton is willing to make investments that may seem off-beat, waiting for the world to recognize the value of their contrarian picks.

Deep operational involvement. Hoxton takes a very hands-on approach with its portfolio companies, especially during times of trouble. They are prepared to do the "heavy lifting" to help their companies succeed.

“13 years ago when we first started, the world did not have that many VCs in Europe. Nobody was here in Europe.”

The industry has shifted towards "momentum investors," prioritizing markups over building long-term, durable companies. “I think most of us become momentum investors in this industry. We write the check largely to get the next markup, not to build the long-term durable big company of tomorrow."

Venture investors should embrace a contrarian approach, focusing on identifying and creating new categories rather than simply investing in existing trends. “I think people in Europe are largely trained in private equity. They think about how do I minimize my downside. But the venture industry is all about the power law all about the outliers."

Hoxton has become very aggressive about doubling down on their best companies, aiming for 15-20% ownership and will find creative ways to inject more capital when ownership is still inexpensive.

Hoxton has a formula to exit companies going public. “The formula that we now have is at the time of the IPO as soon as you're out of lockup a third of it you sell, a third of it you sell six months later, and then a third of it you sell another six to 12 months after that."

Hoxton looks for missionary founders who are primarily driven by solving a problem, not by money or fame, and they'll often challenge the founders to really get to their core. "Most of the founders that we end up writing a check to are very missionary... what they're trying to do is solve a problem that they think is really broken."

Hoxton has the ambition to be among the 5-10 dominant "superstar venture funds" in Europe."I think there's a chance now for a few more funds to be on that list. I think you have that ambition. I have that ambition..."

Sunday, Feb. 9th: Seth Levine wrote about the growing divide in the venture industry between boutique firms and asset managers. - Seth Levine

“There is a split in how VC firms are operating: some firms are keeping to a smaller, boutique style while a handful are becoming behemoths, almost unrecognizable as venture firms. There’s very little in between.”

“At one end of the barbell would be essentially asset managers (asset aggregators) and at the other, smaller firms that were more in the mold of what we historically thought of as venture. The former would be seeking beta and predictable, if lower, returns. The latter would be seeking alpha and greater risk. The middle of the barbell would be sparsely populated and firms inhabiting that space would run the risk of being too large to execute the alpha strategy but too small to be considered true asset aggregators.”

“Fund size is fund strategy. That’s always been the case but is even more so now. Fund size has implications for both the kinds of deals your firm pursues, how concentrated your portfolio can be, as well as your approach to valuation and structure.”

“Larger firms are also generating a more significant percentage of their pay-outs to GPs from management fees than from carry.”

“These firms are chasing something more akin to beta than alpha for the most part, although occasionally they’ll be early into a new market.”

“The firms mentioned above who have all raised funds > $1B (in some cases many times that amount) are operating a different business than funds at the smaller end of the spectrum. They aggregate massive amounts of capital across a large and diverse set of funds and often build huge organizations to support their work. One of the key signs that a firm is in the asset aggregation business is not just the size and scope of the organization but specifically the size of its marketing and PR groups. These firms are often quite adept at pushing out materials and content (much of it high quality) to stay front and center in the market – not just among entrepreneurs but, importantly, among LPs. They require meaningful fundraising capacity to keep feeding the asset machine. Their funds are typically consistent performers but are unlikely to generate outsized returns.”

Monday, Feb. 10th: I listened to Logan Bartlett interviewing Garrett Langley who is the cofounder and CEO at Flock Safety. - Logan Bartlett

“In the US, you've got almost a 90% of getting away with stealing someone's car.”

“We build technology that helps law enforcement through one way or another solve crime.”

“The license place is the number one piece of evidence in solving a crime. 70%+ of crimes happen with a vehicle.”

“A camera that can read a license plate is not a new concept” but it was too expensive for small and medium cities. When Flock started, the average camera fully deployed would cost $50k mostly driven by civil engineering infrastructure work. With Flock, cities could deploy many more devices at a fraction of the cost.

“PR was our only growth strategy three years of the business because we realize that every single time a crime happens, news wants to cover.”

“Vertical SaaS can be really effective. It's hard. It's really hard. But when he gets right, like you've got incredible GRR, you've got bigger TAMs than you ever imagined because you are seeing budget shifting from headcount to software.” “It's about $150,000 a year for an entry level officer. That's the same cost of 50 cameras. Now, I can't get rid of all of my police officers, but replacing two officers to get hundred cameras will have a massive impact on the entire police department.”

“If you call 911, until you effectively finish the phone call, it's not entered into the computer aided dispatch and no one on the first responder side has any idea that somebody is calling 911. After the call, you've also got a 2 to 5 minutes lag.” Flock has a 911 call product sending in real time the 911 call to the nearest police officer.

FlockOS is a situational awareness platform. If you're a business owner or a homeowner, you can subscribe to FlockOS and the local authority will now have access to your cameras in case of an emergency.

“At Flock, we only open a role if the person is going to make an immediate measurable impact to the business within 90 days. If they're not going to do that, then it's not a job. You're just adding a body to a problem.” “We put together a very actionable 90 day plan for every new employee during the interview process.” “At he beginning of every quarter, my co founder Paige and I review every single 90 day plan to decide what roles actually get open.”

Tuesday, Feb. 11th: Duolingo published its employees handbook. - Duolingo

Duolingo has 5 core principles: (i) take the long view to prioritise long-term success over short term wins, (ii) raise the bar doing world class work, (iii) ship it pushing experiments with a sense of urgency, (iv) show don’t tell with concise communication grounded in data and (v) make it fun.

“We give candid feedback that focuses on the “what” and not the “who.”” ““The standard here is “hard on the work, easy on the people.” That means giving constructive, clear feedback that sharpens ideas without undermining relationships. (We stick to the “what,” not the “who.”).”’

“We run hundreds of experiments each week in order to constantly improve our products and our organization.”

“We ruthlessly prioritize projects with the highest impact and quickly cut what isn’t working.”

“This is how we continuously raise the bar—not by being perfect, but by being a little bit better each day.”

“We’ve seen it again and again: only things that are owned become excellent.”

Wednesday, Feb. 12th: Supercell published its annual results for 2024. It generated €2.8bn in revenues (+77% YoY) and €876m in EBITDA (31% margin). - Supercell, Bloomberg

“Our live games hit over 300m MAUs worldwide.”

“Our first new game launch in over 5 years, Squad Busters, despite generating gross revenues in excess of 100 million dollars during its first 7 months in 2024.”

“In the past 2 years, we have significantly invested into growing our live game teams. Brawl team was in fact the first one of our teams that got into a bigger scale. Although I should probably point out here that at Supercell, the word “big team” has a different meaning than in many other companies. For us, “big” means a team of roughly 60-80 people. This is in stark contrast to the live game teams that we hear can be size of 500+ people in some other companies.”

“The first thing worth talking about is to acknowledge that mobile games is one of the most competitive industries worldwide. It is very hard to break through with a new game.” “Over 60% of playtime is spent on games 6 years or older. New games account for less than 10% of playtime.”

“I can’t think of a clearer picture that shows that launching new games is harder than ever. It has become so hard that some companies (or so I have been told) have essentially given up on creating new games, and will just try to seek to buy them when they get to scale.”

““Some companies in our industry seem to have taken the approach that it’s so hard to launch new games, that let’s just give up on it,” he told the Financial Times. “They shift to a M&A strategy where every time somebody invents a new game, let’s just go and buy it. I have a big problem with that thinking.”

Thursday, Feb. 13th: Implementing phishing tests does not significantly decrease phishing success rates. - WSJ

“Phishing, where hackers send deceptive emails in an attempt to steal sensitive information, was the first step in about 14% of cyberattacks in 2024, according to an analysis of data breaches done by Verizon.”

“IT departments are crafting increasingly sensational ruses in what they say is a necessary response to increasingly sophisticated scams. Employees say they sow chaos, confusion and shame. Safety is one thing. Tricking a worker into thinking there’s a lost puppy in the parking lot is just cruel.”

“Phishing education is good,” said Linton. “Tricking people to falling for a phish so you can lecture them that they failed, that’s the part that is terrible.” “They’re more receptive to the education if they feel like you haven’t just made them a fool.”

“A 2021 study of 14,000 corporate workers by researchers at ETH Zurich university found that phishing tests, combined with voluntary training, made employees more susceptible to phishing, possibly by giving trainees a false sense of security.”

“Last year, a follow-up study by researchers at the University of California, San Diego, which looked at a wider range of training programs, found the tests led to a measly 2% reduction in phishing success rates.” “If you can't make an impact at this company within your first 90 days, there's zero reason to believe you will ever make an impact.

Friday, Feb. 14th: I listened to a podcast episode with Rick Zullo who is GP at Equal Ventures. - The Peel

“If you're not playing with $100-200m at seed, you're sub-scale because you cannot lead all the seed rounds in the market.”

“You want to make sure that you can achieve the outcomes that you want to achieve without being fully reliant on the downstream capital.”

“For our best companies, we want to make sure that they are not dependent on the big venture machine.”

In venture capital, “it is a way better business to be in the fee stream game than it is to be in the carry business.”

“The reality is the number of funds that have had more than 3x funds more than three times is extremely small.” “If you can 3x three funds in a row you are literally in legendary territory.” “There's less than 10 that have actually done.”

“It's a better business to be in the fee business and actually the public public markets treated private equity as such. If you are an asset manager, the value that you get from public market investors is based on your fee stream not your carried performance.”

“Venture is special because this is the only asset class that was about the carry. You can actually get more than 2-3 bagger fund and that there are cases where you can get 10-20 bagger funds.”

“It shouldn't take that much money to get a lot of these companies profitable if things are really working.”

Saturday, Feb. 15th: Shaan Puri wrote a blogpost on talents arguing that the best employees are the ones able to identify and solve the right problems on their own. - Shaan Puri

An A player will answer positively these two questions: (i) are you identifying the A+ problem on a daily, weekly, monthly and annual basis? and (ii) are you able to solve that problem – either alone, or by coordinating other people?

In the early days, startups should only have employees able to find the right problems and solve them.

Sunday, Feb. 16th: Security identity software Sailpoint went public at a $12.8bn market capitalisation. Thoma Bravo took SailPoint private in 2022 for $6.9bn. - SailPoint, Alex Clayton

SailPoint generates $800m in ARR (+30% YoY) from 2.9k customers and with a 114% Net Dollar Retention. It offers an identity security platform for enterprises.

“Since the last IPO, the company has transitioned to the cloud vs. on premise and calls their platform the SailPoint Identity Security Cloud.”

“Thoma Bravo owns SailPoint, and this will be the 2nd time Thoma has taken them public. Thoma acquired the company in 2014 for an undisclosed sum, took them public in 2018, and bought them back in 2022 for ~$6.3bn total purchase price and at 13.6x NTM (next-twelve-months) revenue.”

“SailPoint delivers solutions to enable comprehensive identity security for the enterprise. We do this by unifying identity data across systems and identity types, including employee identities, non-employee identities (which include contractors, consultants, and partners), machine identities (autonomous non-human users such as application level accounts, infrastructure accounts, IoT devices, application programming interface API accounts, and bots), and AI agents. Our SaaS and customer-hosted offerings leverage intelligent analytics to provide organizations with critical visibility into which identities currently have access to which resources, which identities should have access to those resources and how that access is being used.”

“According to IDSA, 90% of organizations experienced an identity-related breach in 2023, with 28% of organizations surveyed experiencing a breach involving compromised privileged identities. Identity-related breaches, such as account compromise and phishing, are typically the first step used by advanced persistent threat perpetrators.”

Monday, Feb. 17th: AI is transforming the protection of undersea infrastructure, such as pipelines and cables vital to the global economy. Following the Nord Stream sabotage, nations are enhancing surveillance using AI-powered underwater drones and mapping systems. - WSJ

German startup North.io is developing TrueOcean, a digital twin of the ocean, integrating data from sonar, satellites, and seismic recordings to detect threats in real time.

NATO has launched Baltic Sentry, deploying autonomous underwater vehicles to monitor potential attacks.

The U.S. Navy and defense firms like Boeing and Northrop Grumman are advancing autonomous underwater vehicles, though challenges remain in mapping and identifying unknown underwater threats.

Tuesday, Feb. 18th: The New York Times wrote about Klarna’s radical AI adoption in multiple functions from marketing to customer success and legal. - NY Times

“I am of the opinion that A.I. can already do all of the jobs that we, as humans, do.”

“According to Klarna, the company has saved the equivalent of $10 million annually using A.I. for its marketing needs, partly by reducing its reliance on human artists to generate images for advertising. The company said that using A.I. tools had cut back on the time that its in-house lawyers spend generating standard contracts — to about 10 minutes from an hour — and that its communications staff uses the technology to classify press coverage as positive or negative. Klarna has said that the company’s chatbot does the work of 700 customer service agents and that the bot resolves cases an average of nine minutes faster than humans (under two minutes versus 11).”

“Mr. Siemiatkowski said that A.I. had allowed his company to largely stop hiring entirely as of September 2023, which he said reduced its overall head count to under 4,000 from about 5,000. He said he expected Klarna’s work force to eventually fall to about 2,000 as a result of its A.I. adoption.”

“A former Klarna manager, who left in 2022, said the rhetorical emphasis on A.I. was no accident. According to the manager, there was a sense within the company that Klarna had lost its sheen in the media and among investors, and that Mr. Siemiatkowski was desperate to get it back.”

“The former manager said the A.I. story provided a lifeline at a time when Klarna was hoping to offer shares on the public markets.”

“The benefits of A.I. are likely to be a key selling point for any Klarna IPO.”

“Mr. Siemiatkowski has brought clarity to this discussion. In his eagerness to court investors, and in his tendency to overstate the case and say the quiet part out loud, he has laid bare Silicon Valley’s ambition. In his own slightly muddled way, for his own slightly idiosyncratic reasons, he is helping to surface a conversation that has largely been whispered in the executive suites.”

Wednesday, Feb. 19th: Josh Wolfe published Lux’s Q4-2024 letter to investors. - Lux

“As we enter 2025, the rapid rush of superlatives of recent quarters is moderating as markets are balanced between consensus and contradiction, stability and risk, promise and peril. Apple nearly reached a $4 trillion market cap in December as Bitcoin hit its highest price ever, yet the highest inflation in a generation abated. The S&P 500 rose the fastest for a new administration since Reagan in 1985, even as credit delinquencies reached their highest since the aftermath of the Great Recession.”

“The fissures of reality are widening—credit spreads remain tight, dry powder is anything but and the real economy is already showing signs of structural strain. Rising operating costs and consumer belt-tightening have led to a subtle but noticeable uptick in restaurant and store closings.”

“We continue to hold the view that the natural cost of capital is higher and rising, dry powder in private equity and venture capital is “wet” (due to under-reserves and overallocation) and 30-50% of venture firms will exit the market from failed succession planning, partner in-fighting and other Shakespearean dramas. New entrants are also struggling: 2024 was the worst fundraising year for debut funds in a decade.”

“Meanwhile, the “Magnificent Seven” tech giants, which drove over 50% of the S&P 500’s returns in 2024, embody both the opportunity and the concentration risk embedded in today’s markets.”

“The true differentiator for future AI advantage? Proprietary data. If open models match closed-source performance, then those with deep reservoirs of unique data—Meta (via WhatsApp, Instagram) and Bloomberg—will emerge as kingmakers.”

Thursday, Feb. 20th: Pershing Square published its annual presentation. - Pershing Square

Friday, Feb. 21st: I listened to Alex La Bossiere interviewing Keith Rabois. - Alex La Bossiere

“There's too much capital chasing too few founders. The scarce resource is world class founders.” “The idea that you can take a company from scratch overcome all the inertia inertia and reinvent an entire industry is borderline ridiculous. There's a scarcity of people who are kind of crazy enough to actually embrace that challenge and then also have the ven diagram overlap with the skill set to pull that off.”

“You either have a superpower or you don't you. If you don't have a a superpower your chance of creating an iconic company is literally zero. You need to be in the top one1 to 15 basis points on some dimension.”

“Vertical integration is the key to build a trillion dollar business because it’s very difficult to build vertical integration but if you do it successfully it creates a multi-decade competing advantage. You create accumulative advantages.”

“I don't believe startups are discovered. I believe they're invented. You forge them through willpower.”

“The mispriced talent is almost surely the most most appropriate advantage you can sort of create and forge. You're looking for talent that large tech companies don't know how to process.

If someone's very young and early in their career they may not have enough data points to read.

Most large companies become homogeneous in their hiring process and so people who have disruptive characteristics break the mold those people can be very high leverage and won’t be recruited by large companies.

Geographic arbitrage is another compounding advantage.”

Saturday, Feb. 22nd: The FT interviewed Harry Nelis who is a partner in Accel’s London office. - FT

“We raised our first [Accel Europe] fund in 2000. And the first billion-dollar outcome took five years to materialise [Skype]. And the next two took another five years. So, initially, it wasn’t that clear that Europe was going to develop into a vibrant ecosystem, the kind of ecosystem that it is today.”

“In the beginning, there really weren’t any repeat entrepreneurs yet. So everybody who started a company did it for the first time.”

“Over time, when you go through enough cycles, there’s a successful entrepreneur, they exit a company, their team wants to do it again, then a flywheel starts to happen. That flywheel today is happening on a really big scale. […] That’s the key thing that has changed.”

“For a long time it felt less like a flywheel and more like a conveyor belt: if people got successful in Europe, they just moved to the US.”

“Many entrepreneurs have realised that Europe is a great place to start a business, especially when it comes to engineering. We’ve got great universities. Our employee base for engineers actually is more stable here than it is in the US.”

“What has changed is that becoming an entrepreneur is an acceptable career path.”

“What does that competition and extra capital mean on the ground? We need to be running even harder than we did in the past. That we need to spend even more time on aeroplanes flying across Europe to speak to an entrepreneur. It means that deals happen faster. It means that sometimes in the case of a great company, the valuation becomes very high because there are multiple people going after it — in the same way as it happens in the US. It’s a faster market.”

“38% of founders of [European] AI companies came from positions in universities, as professors or as researchers, which was an astoundingly big number in my mind. 25% of co-founders come from DeepMind, Amazon, Google, etc.”

“Currently companies are experimenting with AI. Everybody is experimenting with AI. But there are very, very few real applications in operation today. So it’s all experimental budgets and no real applications yet.”

“What are the biggest lessons you’ve learnt over Accel’s 25 years in Europe? One thing is venture is a people business. In the end, whether it’s the entrepreneurs, whether it’s the investors on our team, venture is a people business. Number two is it’s all about the outliers, in terms of a successful venture fund. And then the third one is, great companies can come from anywhere.”

Sunday, Feb. 23rd: John and Patrick Collison appeared on the All-In Podcast. - All-In Podcast

“When we started, we thought it would only be for startups. We thought those were the people who needed a problem solved and as time went on we just found out it was kind of broken for everyone.”

“The structural secular insight that's happening is that every kind of money movement is going from being manually orchestrated to being orchestrated by software. We’re helping with everything beyond payments like card issuance, cross border transactions, stablecoins, etc.”

“Stablecoins are most interesting and seeing most adoption where there is some cross-border component: managing corporate treasury around the world (e.g. Tesla), send remittances to people in other countries, paying contractors all over the world (e.g. ScaleAI), people in other countries wanting to store dollars.”

“Companies are losing 1-3% of revenues to AP and AR. Some of that might be because of the transaction rails themselves. A lot of it is just because of broken inefficient processes where you have humans sending invoices, humans reconciling them, humans trying to line up transfers in your bank account statement and figure out what corresponds to what and so on.”

“A big part of what Stripe ends up doing is act as a reputation network to keep fraud out of the system.”

“Most businesses lose more money to fraud than they do to the kind of pure transaction cost themselves. There's even indirect costs where you make the consumer experience more hostile because you have to protect against possible fraud.”

“Leaders are starting to step up and speak their mind and speak more directly. They lead from the front rather than lead from the back.”

Monday, Feb. 24th: Stripe published its 2024 annual letter. - Stripe

“Businesses on Stripe generated $1.4 trillion in total payment volume in 2024, up 38% from the prior year, and reaching a scale equivalent to around 1.3% of global GDP.”

“Stripe was profitable in 2024, and we expect to be so in 2025 and beyond. Durable profitability allows us to plow back much of our operating earnings into research and development.”

“Stripe’s Revenue and Finance Automation Suite, with Billing at its core, has now passed a $500 million revenue run rate. Billing is being used by more than 300,000 companies, manages nearly 200 million active subscriptions, and is emerging as the revenue engine of the AI era.”

“The businesses on Stripe span every chromosome of the economic genome, from top corporate leaders (half of the Fortune 100 uses Stripe) to hyper-growth companies (we count 80% of the Forbes Cloud 100 and 78% of the Forbes AI 50 as customers) to newly formed upstarts (one in six new Delaware corporations incorporates with Stripe Atlas)”

“Today, 60% of all small businesses in America use vertical SaaS platforms to help run their business.” “Vertical SaaS started and is most mature in the US, but is now becoming a global phenomenon. Over a quarter of Australian small businesses are using vertical SaaS, as are nearly a fifth of small businesses in the UK. Other markets like Singapore (14%), France (8%), and Germany (5%) are more nascent, but adoption is growing quickly.”

“The 43% of US GDP that is driven by small businesses contains untapped potential energy. of these businesses say growth capital is hard to come by. Vertical SaaS, with Stripe Capital, can help.”

“The most effective lever we have to keep businesses safe is Stripe’s reputation network. Data from $1.4 trillion in annual payments volume means that each payment makes the next payment safer, a flywheel spinning with now-considerable momentum. When a credit card is used for a payment, there is a greater than 92% chance that Stripe has encountered the same card before. We can then compare this transaction to prior behavior.”

“Some say that the European economy has lost its way and that the decline can’t be arrested. We can’t allow that to happen. We are proud Europeans, Stripe maintains a headquarters in Ireland (in addition to South San Francisco), and Stripe serves a very large number of businesses across the European continent.”

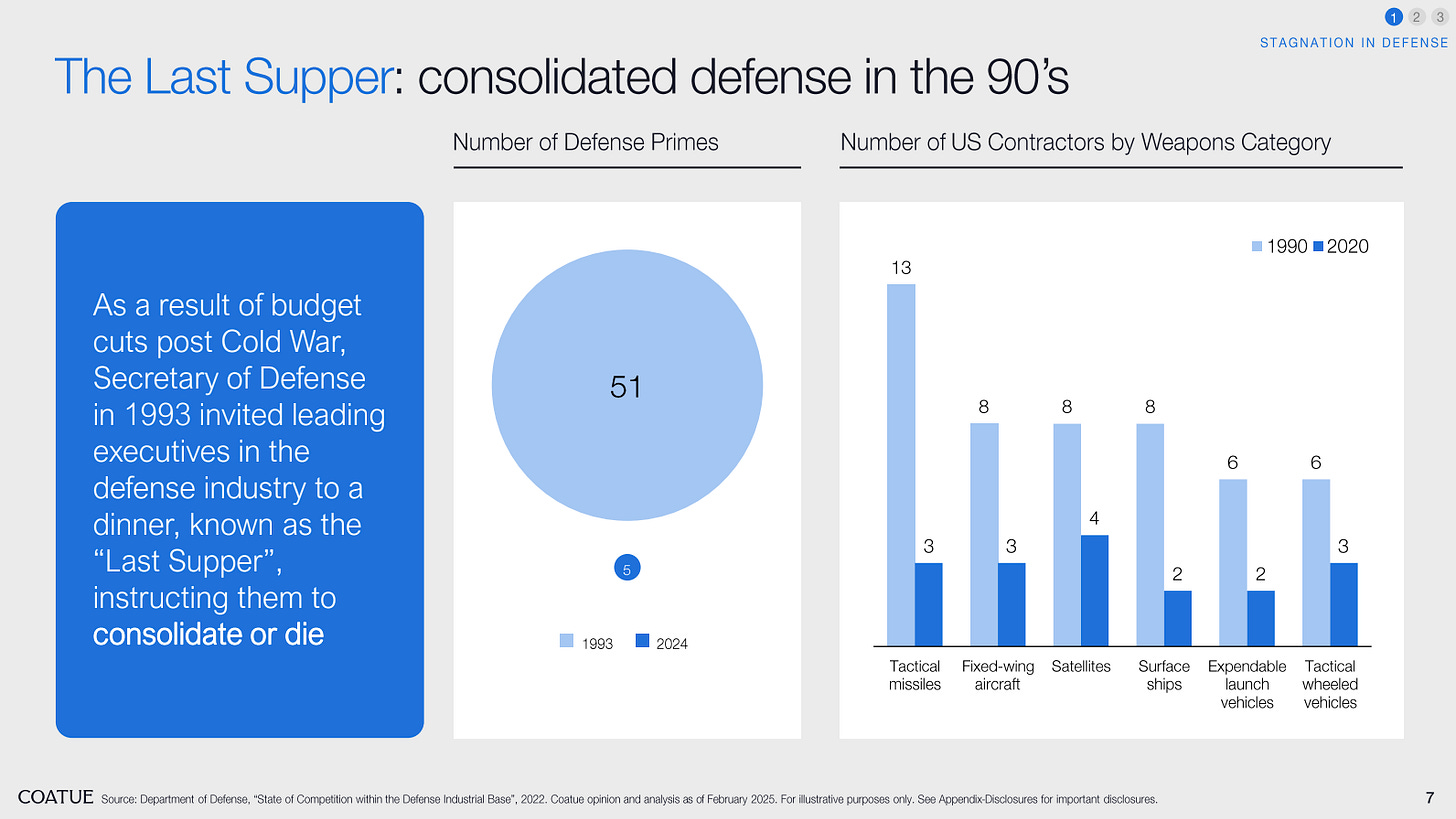

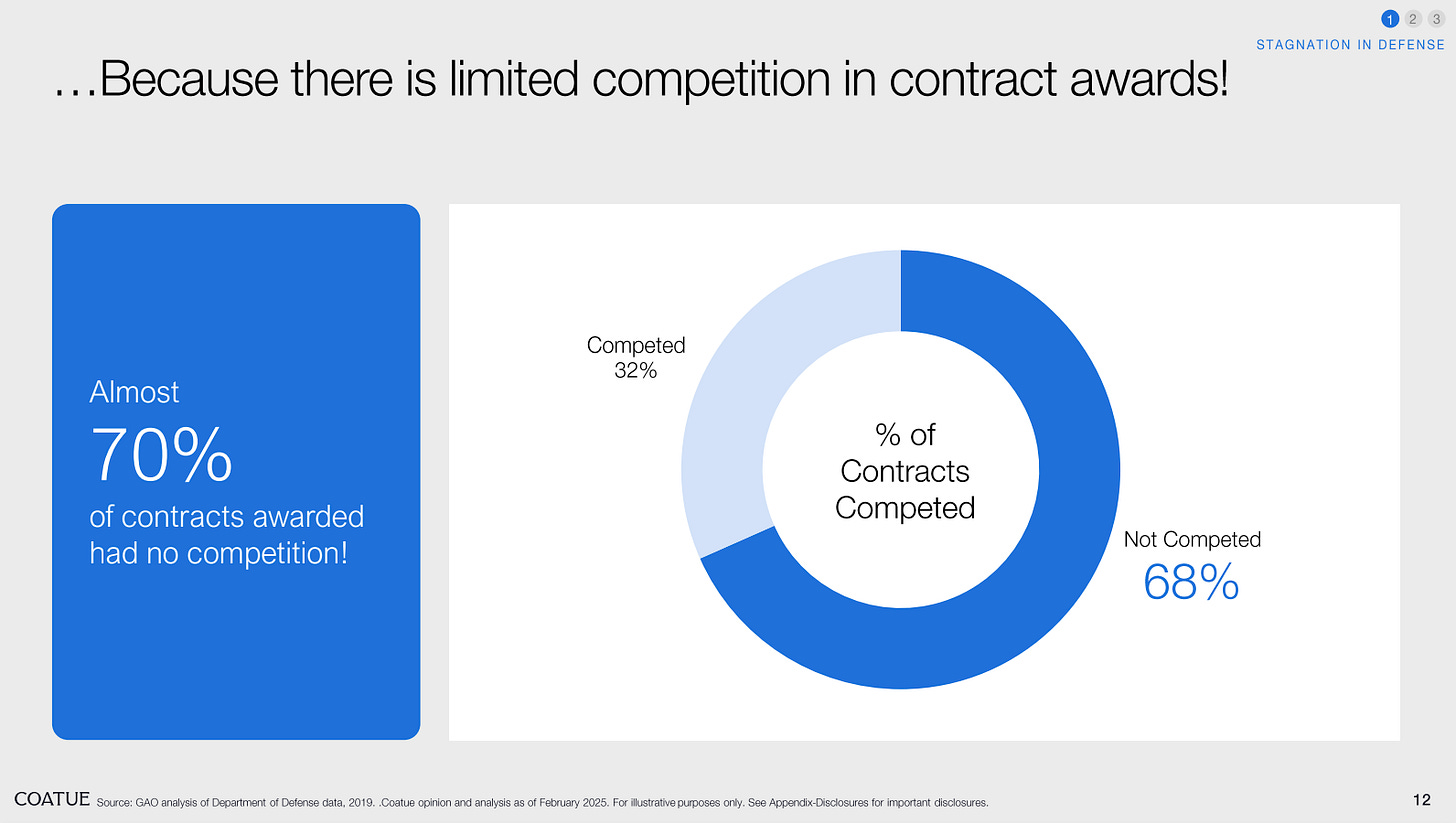

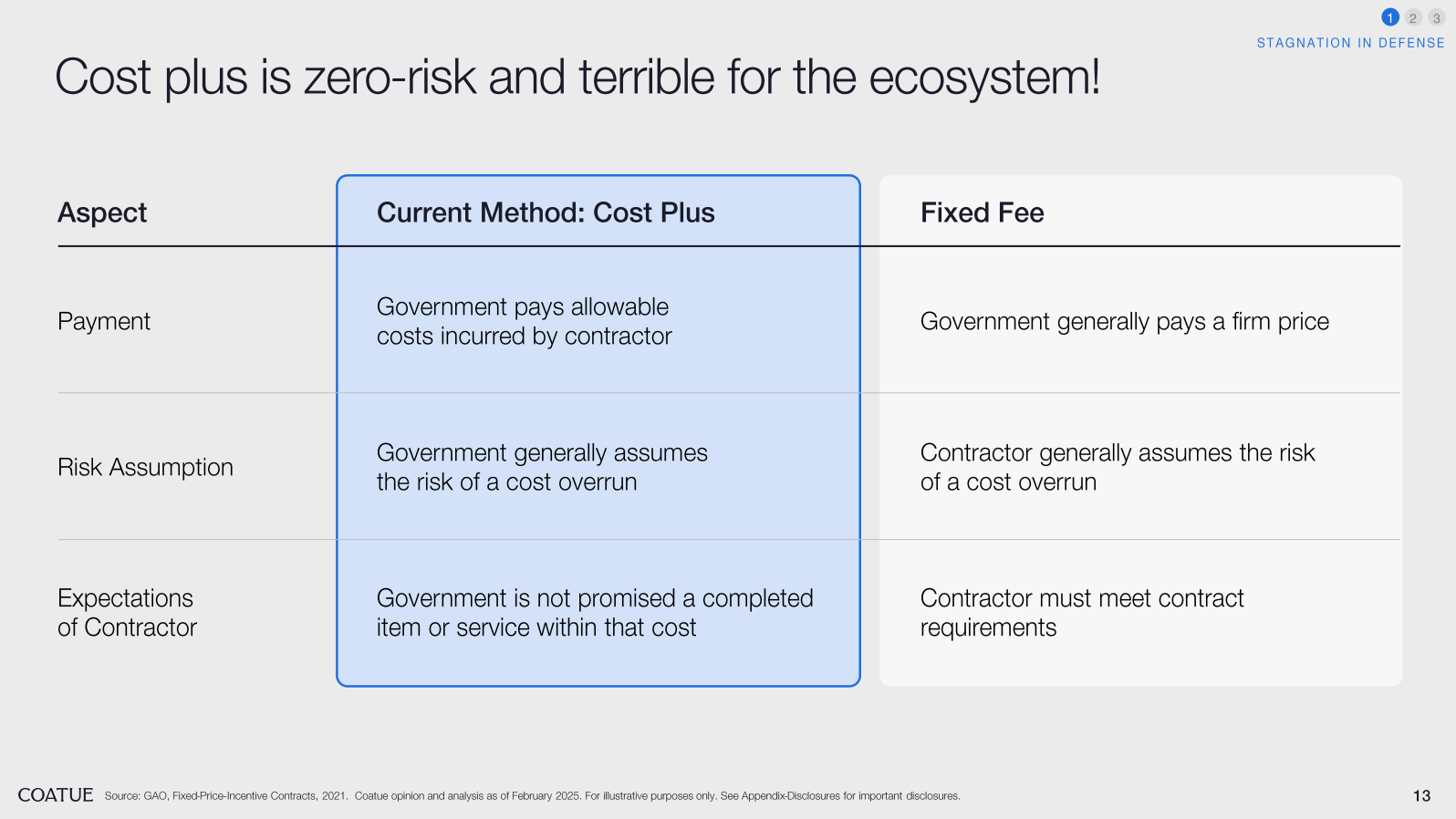

Tuesday, Feb. 25th: Coatue published a report on the defense industry. - Coatue

“The U.S. defense budget accounts for 3–5% of GDP, yet it is defined by inefficiency and stagnation. Since the 1990s, consolidation has reduced competition, with the “Big 5” primes winning nearly half of all major defense contracts—70% of which face no competition at all.”

“The conflict in Ukraine has redefined warfare economics. Affordable systems like drones and missiles have proven devastatingly effective, disrupting traditional notions of high-cost, high-impact military assets. The lesson is clear: wars are no longer won solely through superior spending but through speed, innovation, and adaptability.”

Wednesday, Feb. 26th: Thoma Bravo raised a €1.8bn fund to invest in European mid-market tech companies after having invested €14bn in the region. - Thoma Bravo

“Thoma Bravo has been investing in Europe for fourteen years, having deployed over €14 billion of equity across 16 transactions in the region. Since the opening of its first international office in London in 2023, Thoma Bravo’s European team has made four investments across the Netherlands, Germany and Sweden, including the €400m take-private of EQS Group and growth investments in USU, Hypergene and LOGEX.”

Thursday, Feb. 27th: Mike Airpaia at Moonfire wrote about the rise of lakehouses in the data infrastructure combining the strengths of datwarehouses and datalakes. - Moonfire

“In the last two decades, data infrastructure has undergone dramatic shifts. We’ve moved from tightly-coupled data systems like Hadoop to cloud data warehouses that separate storage and compute, and now toward the lakehouse – an architecture blending the strengths of data lakes and data warehouses”

“However, Hadoop’s tightly-integrated storage-and-compute model also revealed limitations as technology and needs evolved. One issue was inflexible scaling: storage and compute were bundled on the same machines, so scaling one meant scaling both. If you needed more storage for growing data, you had to add more compute nodes (even if CPU was under-utilized), and vice versa. Over time, many enterprises found that data growth far outpaced their growth in compute needs. This often led to excess capacity and wasted cost.”

“Entering the 2010s, two trends prompted a fundamental change in data architecture: cloud infrastructure and cheap, scalable storage. Cloud providers offered virtually unlimited storage (e.g. S3, Google Cloud Storage, Azure Blob Storage) at low cost, independent of compute. This made it feasible – and attractive – to decouple storage from compute in analytics platforms. Rather than storing data on the same nodes that do the computing (as Hadoop did), cloud data warehouses began storing data in a central service (a cloud storage layer) and spinning up compute resources on-demand to query that data.”

“The separation of storage and compute unlocked flexibility – theoretically, multiple compute engines could access the same data in the central storage. In practice, however, many organizations found themselves dealing with data fragmentation in this new landscape. The issue was that while storage became a common layer, the analytical engines on top were diverse (each with its own formats, optimizations, and ecosystems). Without careful design, teams ended up creating multiple copies of data for different purposes, undermining the single-source-of-truth ideal.”

“To break down data silos and enable a true single source of truth on cloud storage, the industry turned to open table formats. Projects like Apache Iceberg and Apache Hudi (and Databricks’ Delta Lake, which later became open source) were developed to bring database-like capabilities to data lakes. In simple terms, an open table format defines how to organize data files and metadata in a data lake so that multiple compute engines can treat the data as a coherent, transactional table.”

“A data lakehouse is an architecture that combines the best elements of a data lake and a data warehouse into a unified platform. It decouples storage from compute (like the cloud warehouses do) in an open way (using formats like Iceberg/Hudi/Delta on object storage), and thus allows a wide range of compute engines to interact with the data. In effect, a lakehouse looks like a warehouse to end-users (you can run SQL and get ACID guarantees) but behaves like a lake behind the scenes (flexible storage, support for unstructured data, multiple tools, low cost).”

“The lakehouse paradigm is creating new frontiers for innovation. In an environment where inexpensive, centralized storage meets a diverse array of pluggable compute engines, several critical areas for innovation have emerged. These include performance acceleration, real-time analytics, multi-format data streaming, and verticalized, industry-specific solutions—all complemented by continued improvements in user interfaces, governance, operations, and integration.”

“One of the most compelling aspects of the lakehouse model is that all data resides in one central repository, making it easier to enforce consistent controls and governance. This opens a powerful opportunity for verticalized lakehouse solutions that are tailor-made for highly regulated sectors such as finance, healthcare, and government. In these industries, compliance, auditability, and robust security controls are not optional—they are mission-critical. Startups can develop industry-specific lakehouse platforms that “bake in” regulatory and compliance features from the ground up. For example, a healthcare lakehouse might include pre-integrated data models (like FHIR), HIPAA-compliant access controls, and detailed data lineage tracking, while a financial services lakehouse could offer built-in support for SEC/FINRA compliance, risk models, and fraud detection analytics. By addressing these vertical-specific requirements, such solutions can accelerate adoption in markets where generic platforms fall short, and command premium pricing for their specialized functionality.”

Friday, Feb. 28th: AI is accelerating the adoption of vertical software in multiple industries. - Euclid

“Vertical AI is breaking down traditional barriers to industry adoption that have held back entire generations of SaaS startups.”

“AI, however, is transforming the traditional vertical go-to-market. LLM-based wedge products have proven the ability to drastically reduce market education, avoid rip-and-replace legacy systems of record, and change buying calculus altogether, with innovative new value propositions and pricing schema.”

“LLMs give vertical software solutions the opportunity to greatly reduce the upfront investment cost of adoption.”

“Once the benefits are widely proven—especially at an industry-leading organization—the enablers of fast scaling above kick in and growth can be breathtaking. Abridge grew from single-digit ARR to nearly $100M ARR in little more than a year.”

“Early data from BVP’s portfolio companies saw average Vertical AI revenue growth of ~400% year-over-year—extremely impressive for businesses with a likely mean stage of Series A+.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋

Another great edition, Alex!

I will be deploying significant capital within the UK ecosystem. Let me know if it makes sense to connect :)