📖 Venture Chronicles - February 2024

Overlooked #170

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of February.

Tuesday, Feb. 1st: I watched a video Doctolib shared to celebrate its tenth anniversary, to introduce its recent product features, and to present its product roadmap for 2024. - Doctolib 1, Doctolib 2

Doctolib upgraded its booking platform to reduce the time needed to make new bookings and to more easily associate patients with bookings.

It streamlined its patient communication experience to enable doctors to send grouped and targeted communications (e.g. preventive campaigns, updates on the medical practice) to their patients (i.e. it's a Mailchimp-like product integrated into Doctolib) and to centralize patient communication that used to happen on multiple channels (phone, email, SMS, social media) into a single platform.

It will relaunch its messaging product between caregivers, leveraging Siilo’s acquisition done in 2023, with the objective of connecting 500k doctors in Europe for free.

It aims to integrate Gen. AI into its platform with (i) a medical assistant to free up time for caregivers (real-time transcription of consultations, drafts of referral letters, preparation of treatment plans) and (ii) a personal assistant to reduce the administrative burden for caregivers (automatically classifying documents received).

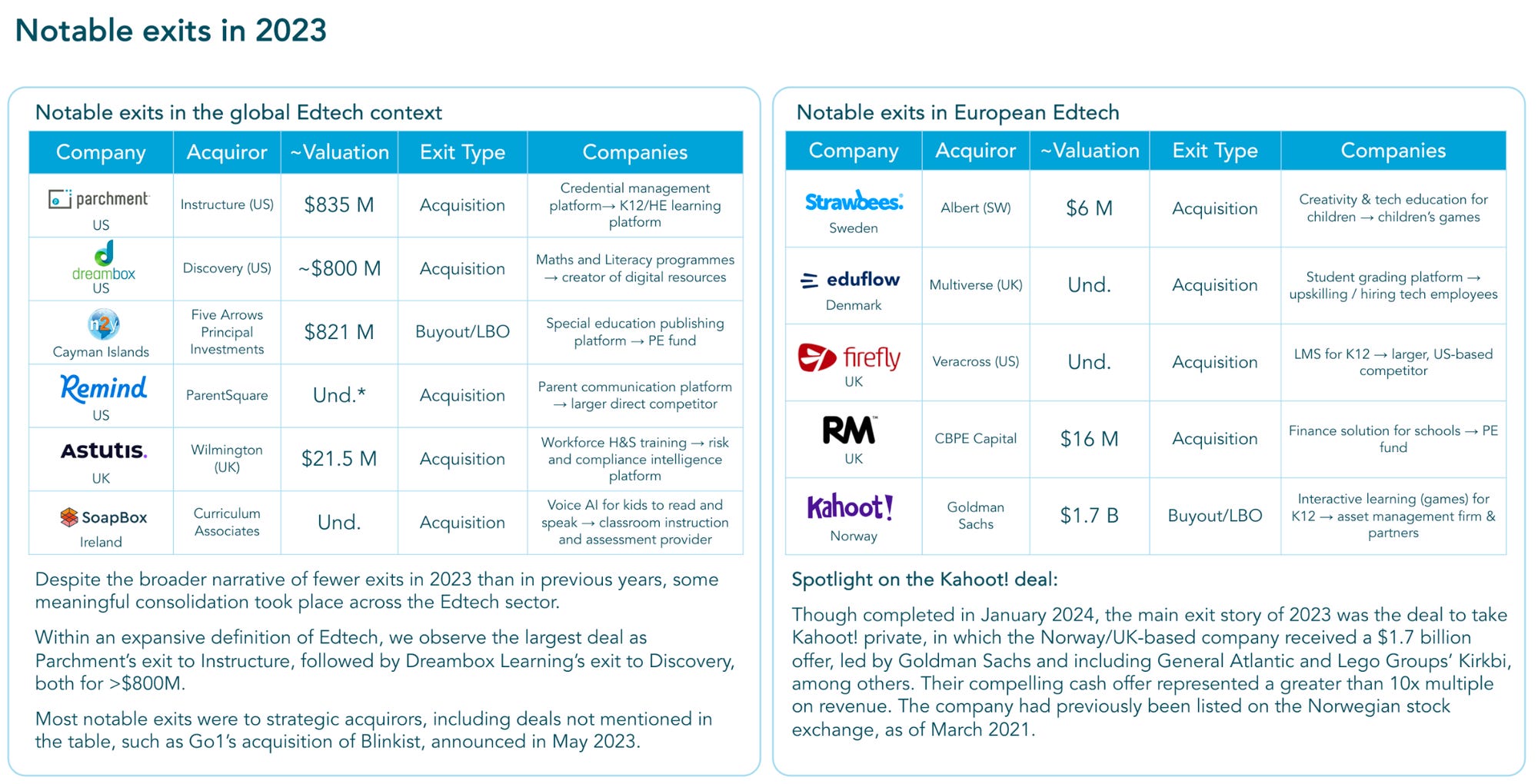

Friday, Feb. 2nd: Brighteye published its annual edtech funding report. Global edtech startups raised $5.6bn in 2023 across 915 transactions (compared to $9.6bn in 2022 with 972 deals). 32% of edtech funding came from Europe. Edtech recorded three exits above $500m in 2023, including Kahoot! ($1.7bn), Parchment ($835m), and Dreambox ($800m). For 2024, Brighteye made several predictions, including: (i) education becoming increasingly embedded into day-to-day workflows, (ii) the rise of climate and sustainability skills education, and (iii) the use of AI for knowledge management. - Brighteye

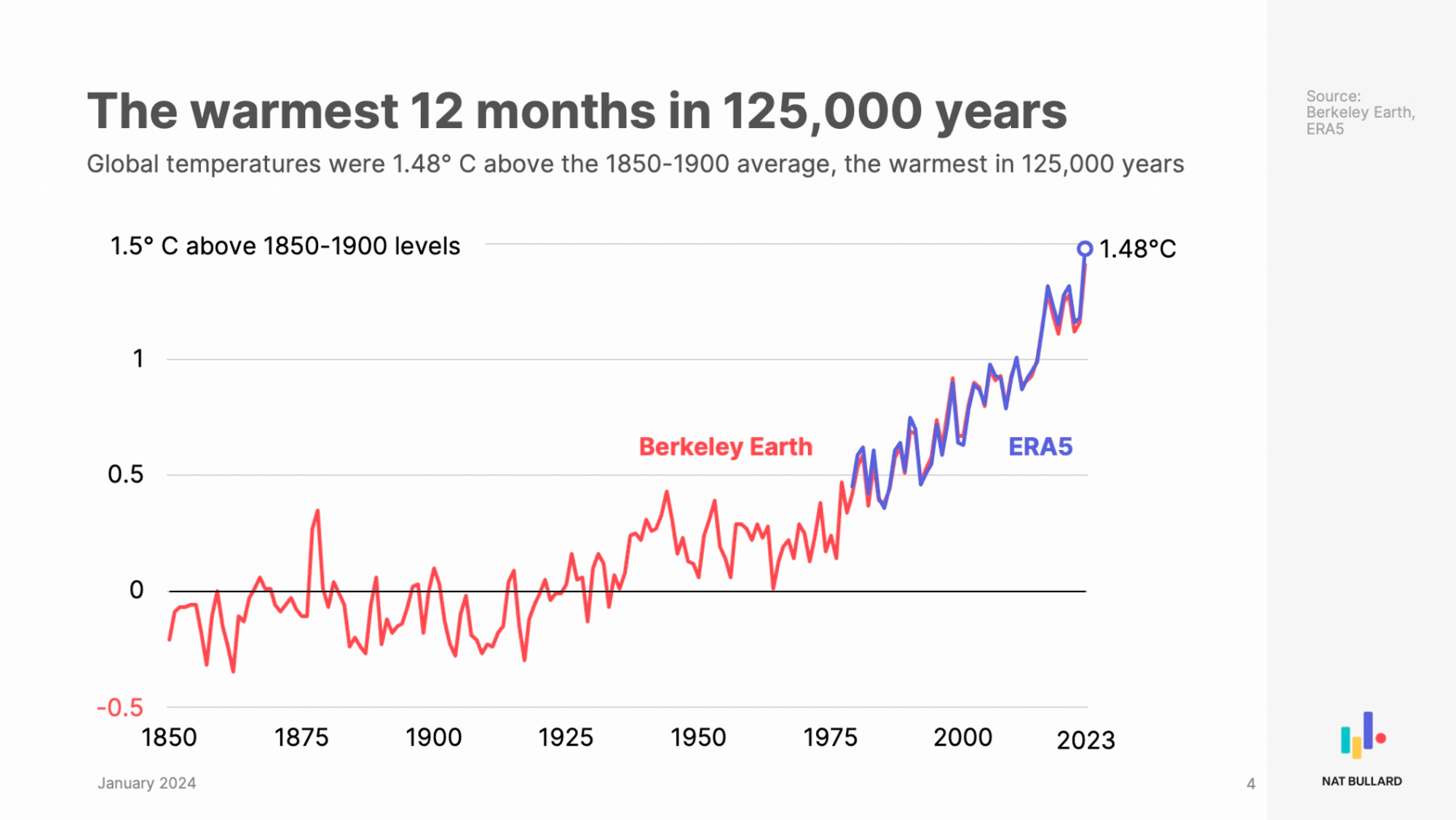

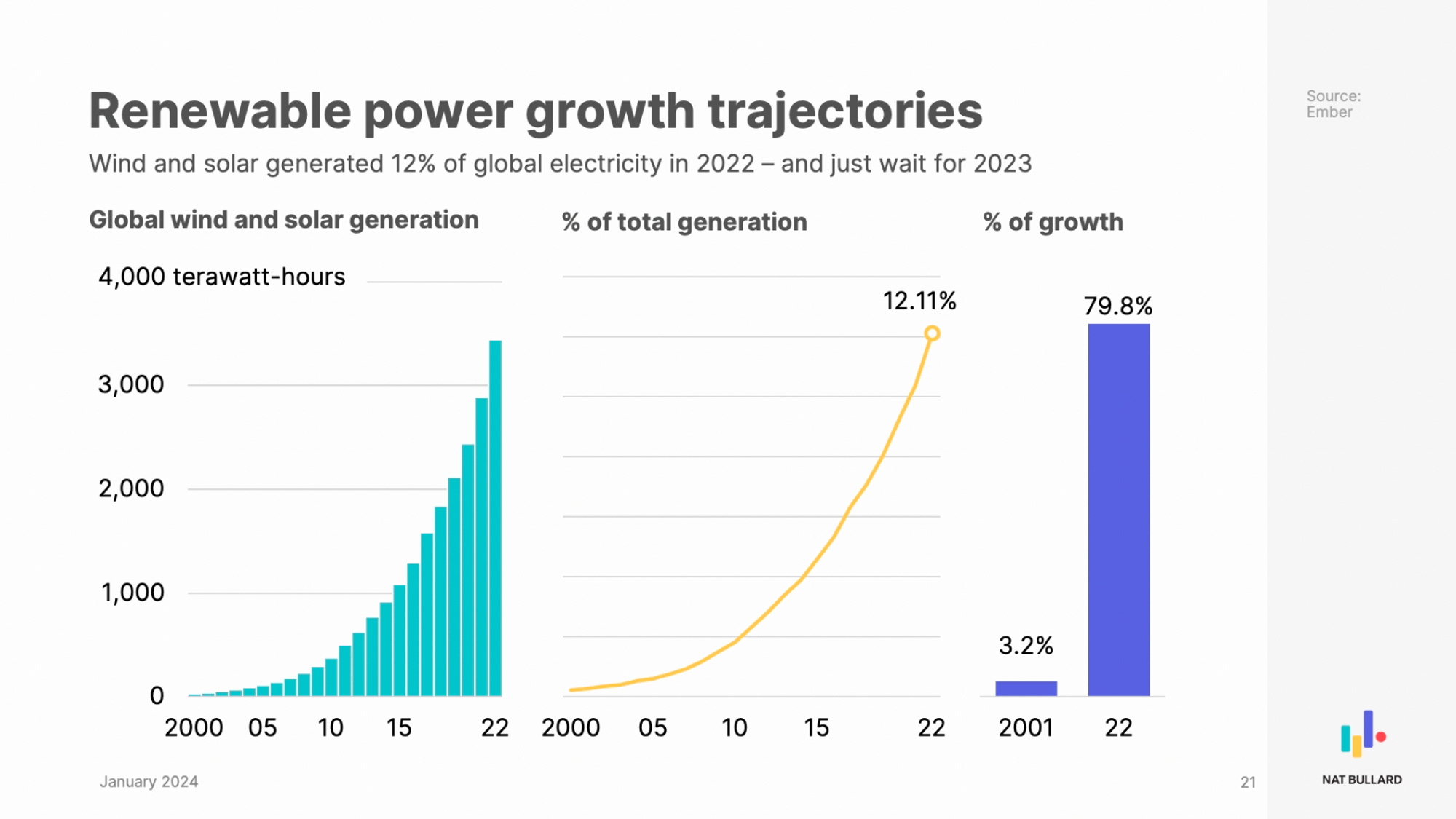

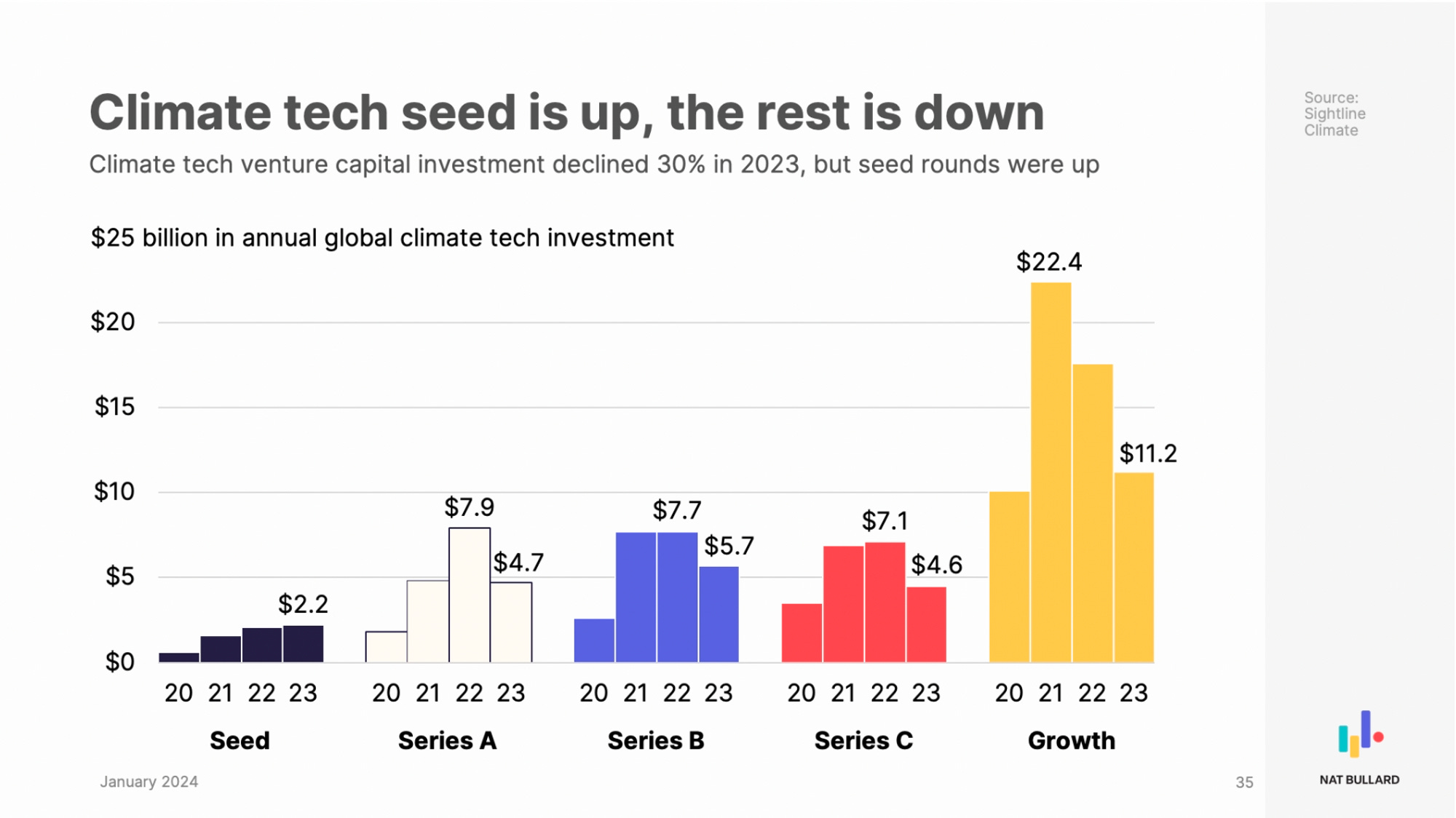

Saturday, Feb. 3rd: Nat Bullard published a report on the state of decarbonization. - Nat Bullard

Sunday, Feb. 4th: Julien Codorniou wrote about the rise of SaaS for frontline workers. - Felix Capital

“An estimated 2.7bn people work in an environment without regular access to a desk, a mobile phone, or a PC. And yet, shockingly, little technology is being designed for these frontline workers.”

“Tech is on the cusp of a SaaS revolution for the 99%. Because this market is open and ready for disruption, I see an opportunity for savvy software entrepreneurs to build the Microsoft or the Salesforce of the frontline workers’ world.”

“In 2021, the global market for frontline employee SaaS apps was valued at $21.3bn and projected to rise to $68.9bn by 2028, marking a CAGR (compound annual growth rate) of 17.6% from 2022 to 2028.”

“Once an ignored segment, frontline worker technology is now positioned at the convergence of technological advancements like AI, evolving work dynamics, and market potential driven by the need for greater efficiency, automation, compliance, and connectivity in various industries.”

“4/10 frontline workers have quit in the last year, and managers and head office staff don’t know how to fix it.“

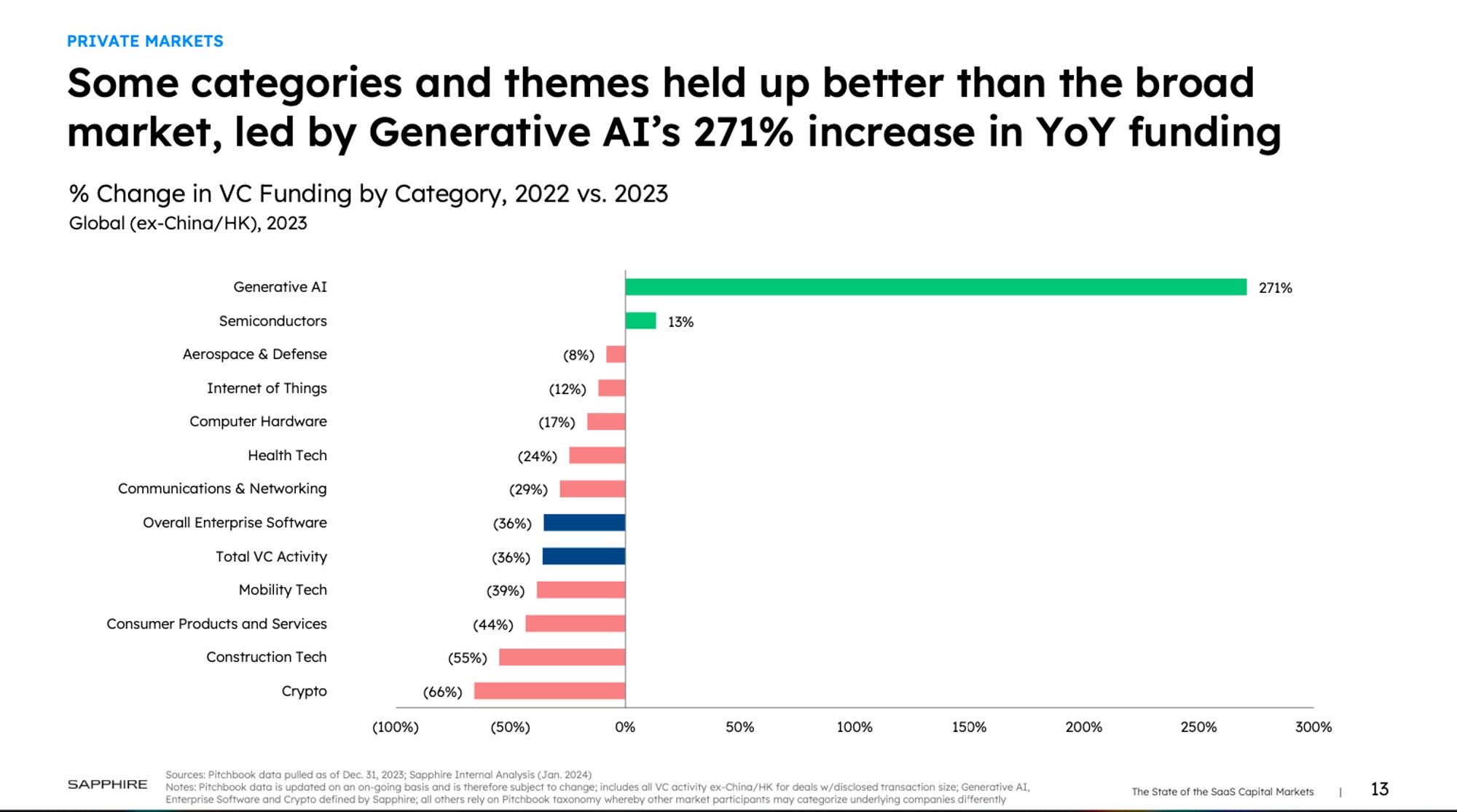

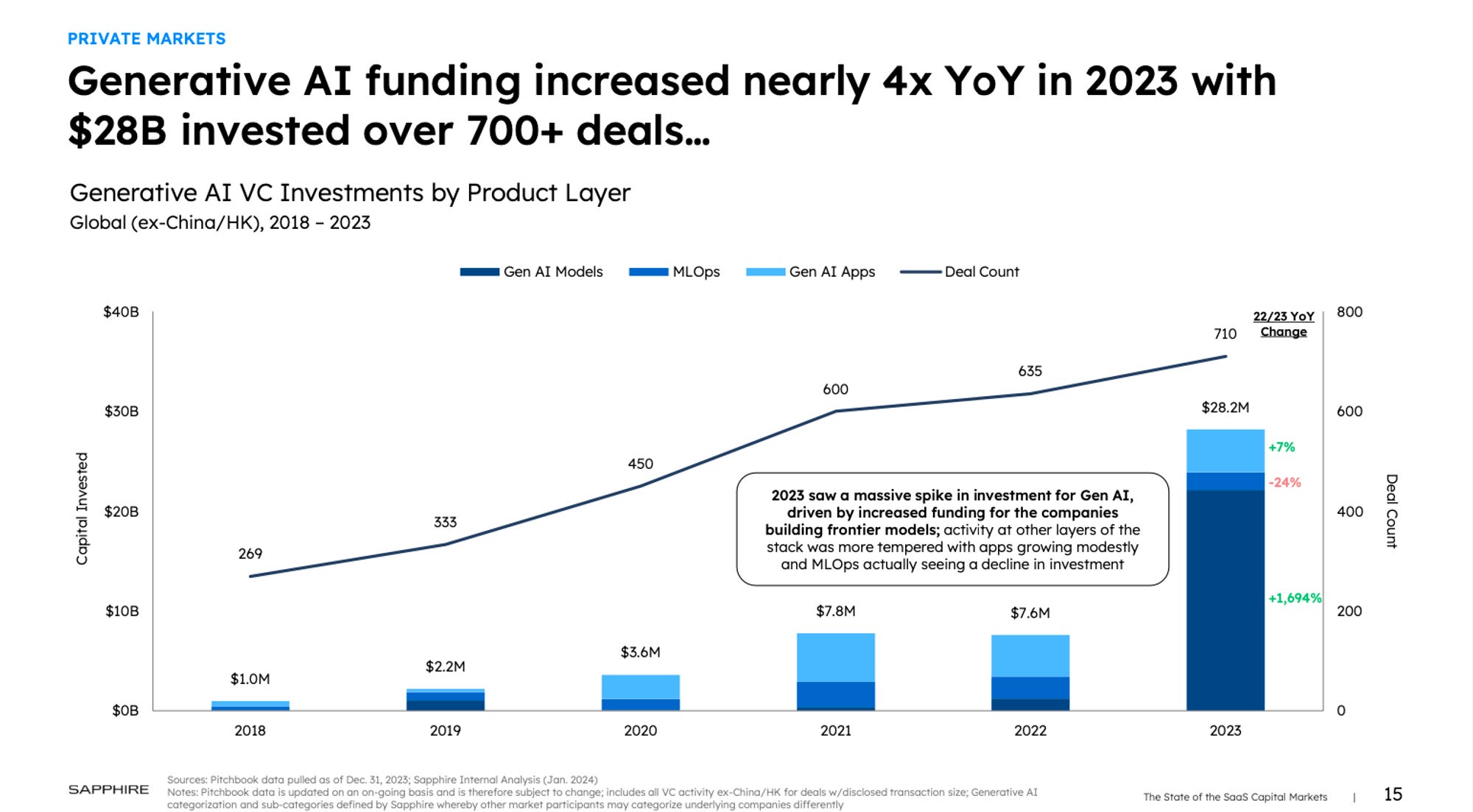

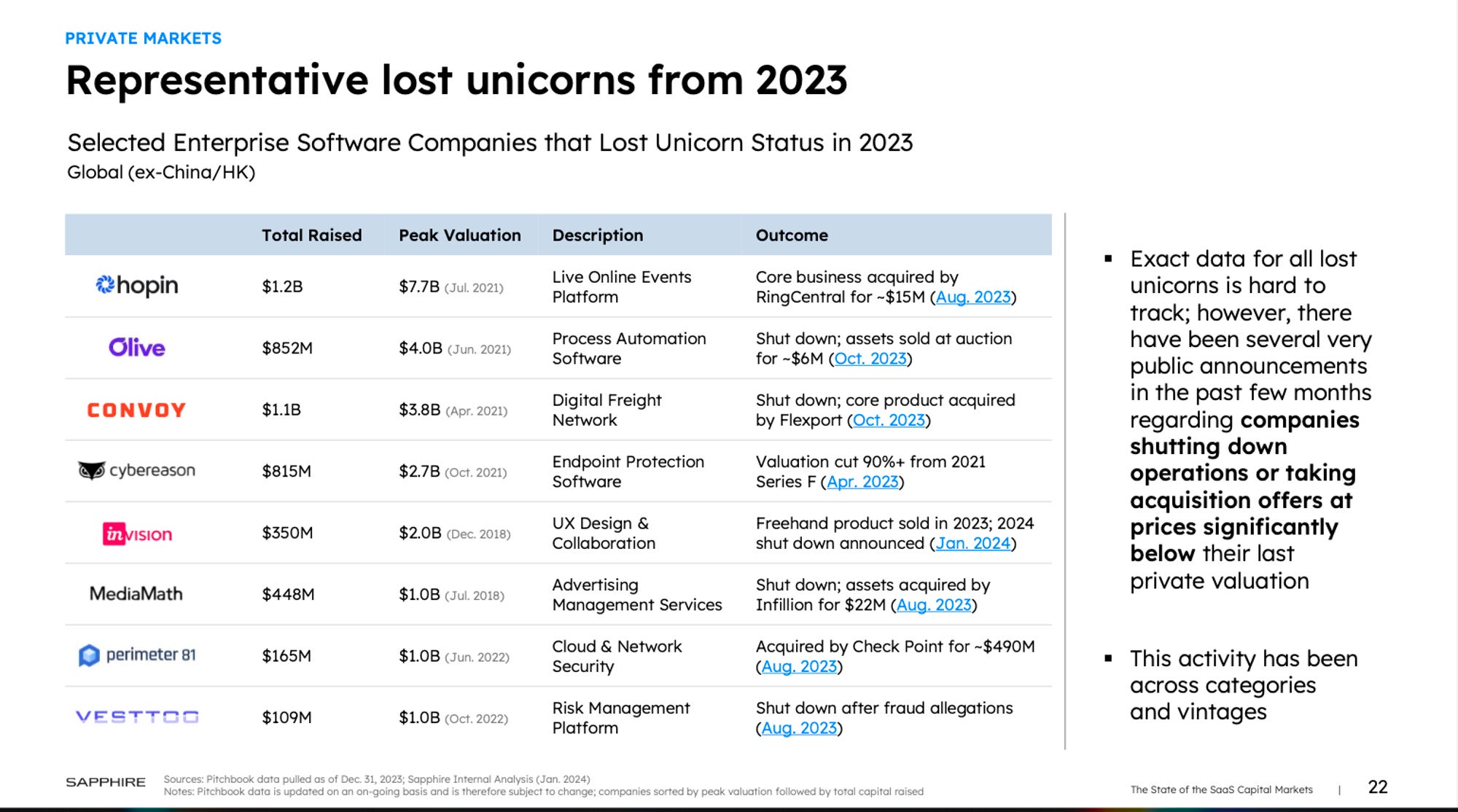

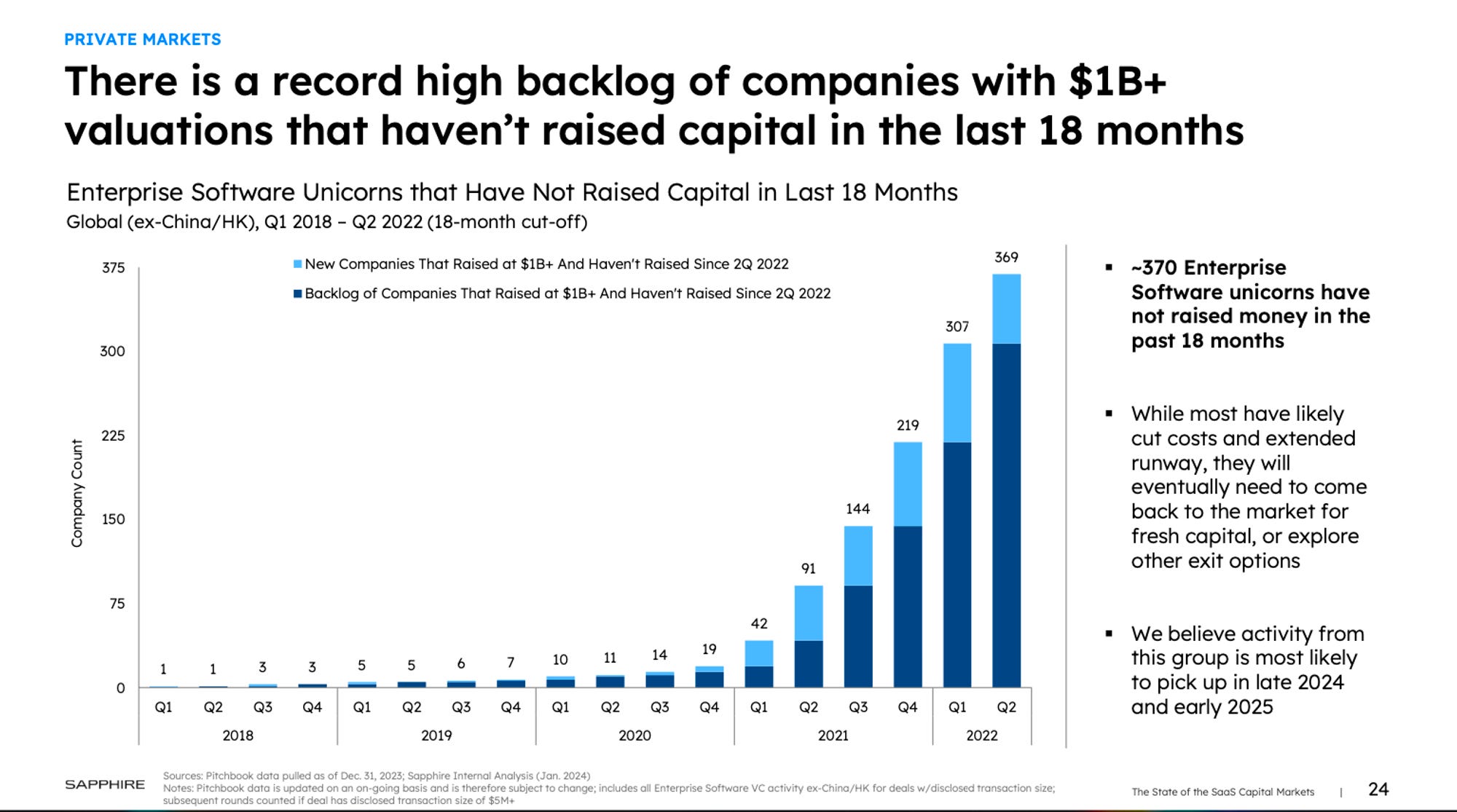

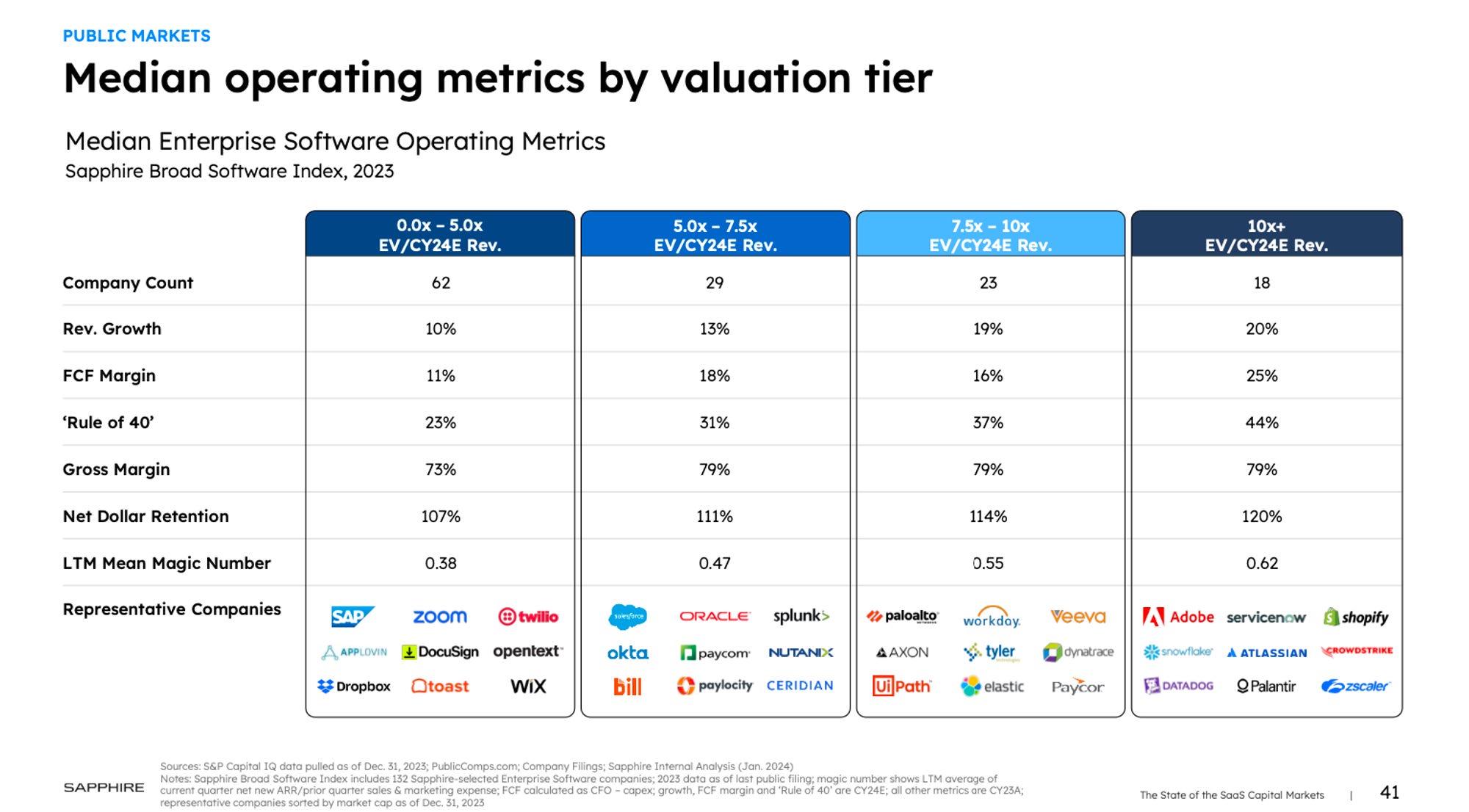

Monday, Feb. 5th: Sapphire published a study on the SaaS capital market. - Sapphire

“We will return to a "growth mindset" in software. After two years of declining growth rates across the SaaS universe, we believe growth will inflect upward in 2024 as (1) economic conditions prove resilient and (2) AI begins to reach the initial deployment stage. While the painful cuts many companies made in 2023 were potentially necessary for the long-term (and are likely still not done), company leaders and investors alike will recognize that growth can solve many of a company's remaining challenges and will embrace them playing more offense throughout the year.”

“In M&A, deal volume will pick up with small-to-medium-sized deals in the starring role. Enterprise Software M&A fell for a second consecutive year in 2023, closing the year at ~$260B in deal value across 511 completed transactions. Despite the decline, 2023 was still the fourth highest total, from a value perspective, of the past decade – far from a depressed deal-making market. In Q4, we observed what we believe will be a strong trend heading into 2024, which is a much higher velocity of small-to-midsize deal-making activity as strategics and PE firms tap their strong cash reserves and increasingly take advantage of an environment where VC is more selective. We believe regulatory scrutiny and election overhang limits potential for blockbuster deal-making in 2024 but expect a very active market in sub-$3B transactions.”

“Private-to-private M&A will increase as stronger players consolidate positions. Once considered unnecessary, given the abundance of available capital and high rates of organic growth, and/or too difficult from an execution perspective, private-to-private M&A deal activity will increase significantly in 2024 as strong private companies look to consolidate their positions, add scale (to gain efficiency and reach a higher IPO bar) and improve NDR with new land and up-sell opportunities. VCs and other stakeholders who would have resisted being acquired by another private company in the past will welcome the opportunity to roll their stakes into larger, more successful private companies that can ultimately go public or command an M&A premium at exit.”

“Enterprise Software reached 44% of total funding on the strength of long- term (e.g., Cloud, digital transformation) and emerging (e.g., Gen AI) trends”

“Generative AI was the dominant theme (+271% in investment YoY), but was highly concentrated and still only accounted for ~10% of total VC funding”

Tuesday, Feb. 6th: Vanta reached the $100m ARR milestone. It did it in 5 years with 7k customers ($14k ACV, customer base doubled in 2022, 1/4 of customers outside the US). It helps companies to obtain security related certifications like SOC2 or ISO 27001. - Vanta, Christina Cacioppo

“Vanta was founded to turn trust into a revenue-driver for companies so that more security work is prioritized more often, and it’s working.”

In 2023, it introduced a second standalone product called Vendor Risk Management as well as many AI features (e.g. chat with a SOC 2 report). It also starts to support AI risks related frameworks like the NIST AI Risk Management Framework.

Wednesday, Feb. 7th: The Economist wrote about social networks arguing that Facebook has lost its ethos as a social network where you could chat with your close” friends. - The Economist 1, The Economist 2

“The weird magic of online social networks was to combine personal interactions with mass communication. Now this amalgam is splitting in two again.”

“Facebook itself counts more than 3bn users. Social apps take up nearly half of mobile screen time, which in turn consumes more than a quarter of waking hours. They gobble up 40% more time than they did in 2020, as the world has gone online.”

“The striking feature of the new social media is that they are no longer very social.”

“The share of Americans who say they enjoy documenting their life online has fallen from 40% to 28% since 2020. Debate is moving to closed platforms, such as WhatsApp and Telegram.”

“Since the network’s pivot to entertainment, news makes up only 3% of what people see on it. Across social media only 19% of adults share news stories weekly, down from 26% in 2018.”

“Social media have become the main way that people experience the internet—and a substantial part of how they experience life.”

“Following the arrival of competitors such as TikTok, powered by artificial intelligence, Facebook and other incumbents have been forced to reinvent themselves. Platforms that began as places for friends to interact and share their own content are turning into television-like feeds of entertainment, for passive consumption.”

Thursday, Feb. 8th: I watched a 20VC’s podcast episode with Dave Kellogg who is executive in residence at Balderton. - 20VC

Dave was CMO at BusinessObject for 9 years as the company grew from $30m to $1bn in sales and from 240 people to 4.5k people. He also ran two companies from $0m to $80m in sales and from $8m to $50m in sales.

How do you think about efficient growth? To have efficient growth, you should zoom-in and double down on what is working (in which sectors do we have the higher win-rate, the faster sales cycle, the higher ACV with the higher NDR?).

CAC ratio (sales & marketing / new ARR) answers the question of how much do you spend per dollar of ARR added. 1.5x or less is a good ratio in enterprise and 1.0x in SMBs.

In 2024, 105-108% is a good Net Dollar Retention Rate (vs. 120% in 2021-2022) mostly because there is an increased churn level but also because it’s harder to expand.

Customer success should be about renewing contracts and creating upsell. It’s not about hugging customers or doing technical support which should be included in professional services. Customer success is a selling role. The mission is not to squeeze every penny of the customer. The mission is to keep the customer happy, get them renewing and spot upsell opportunities.

“I like to hire three sales reps at a time because I want to have a good experiment.” (e.g. hiring ex-Salesforce’s reps to sell to enterprise). “Your job in the early days is to run good experiments. It means if it works we know what to replicate and if it fails we know what not to do.”

Friday, Feb. 9th: I read Dave Kellogg’s predictions for 2024. - Dave Kellogg

“Recently, I’ve heard more and more CEOs abandon this religious belief in outbound. That’s good. Standalone outbound is a low-conversion rate activity. […] Partner and inbound-generated leads often convert at double or triple the rate of outbound. I expect standalone outbound effectiveness to only get worse because of the AI-driven tools arms race.”

“As Google continues to cater to its existing customers and is increasingly run by extractors as opposed to innovators, they create the opportunity for disruption. Now, since Google is a very smart company, they’re not flat-footed in response and are very much trying to disrupt themselves. But, regardless of which vendors win, I expect generative AI’s answers to largely replace traditional search’s lists-of-links going forward.”

“In 2024, I think AI will continue to blow our socks off as we climb to peak hype. Vendors will propose a wide variety of use-cases, some of which will stick while others will not. Some features will become companies and some products will become features. What’s a technology consumer to do? Allocate time to experiment with a broad range of AI features and products. I expect many AI solutions to go from magical advantage to table stakes almost overnight.”

“If 2023 ended up the year of hunkering down, then 2024 will be the year of efficient growth. […] In 2024, expect emphasis on the usual go-to-market (GTM) efficiency metrics like CAC, CPP, and LTV/CAC, continued emphasis on both net and gross retention rates (NRR and GRR), new emphasis on overall productivity (ARR/FTE) and balanced growth measures (R40), and of course strong attention to cash burn efficiency (burn multiple).”

“I think the worst of it is over, particularly for those companies that responded quickly to the downturn by increasing focus, reducing burn, and increasing runway.”

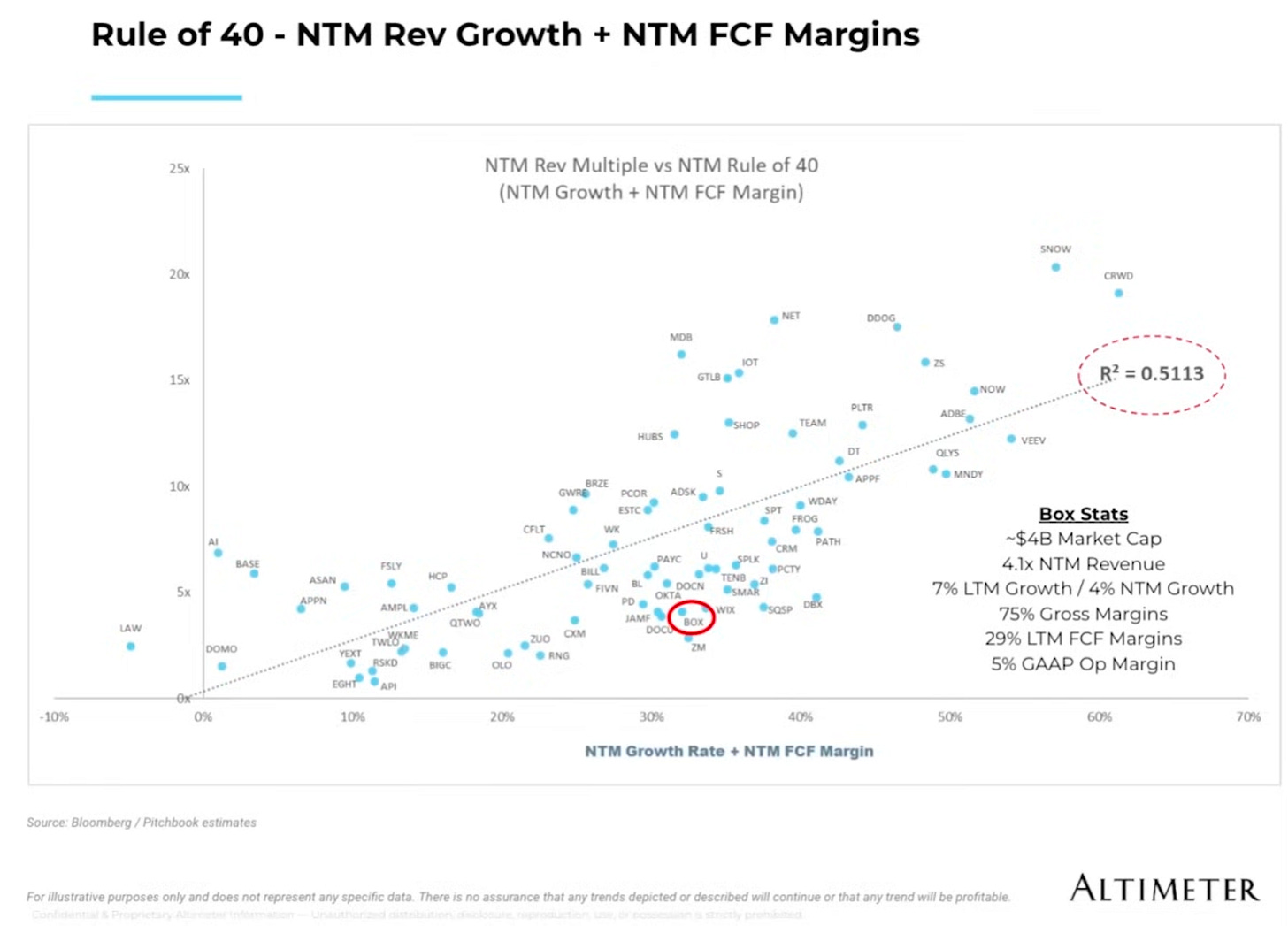

Saturday, Feb. 10th: I listened to Bill Gurley and Brad Gerstner interviewing Aaron Levie who is the cofounder and CEO at Box. - BG2

“Not all technology companies are created equal. At certain points in the history of technology, we ended up believing that all tech enabled companies should all get a 6-10x revenue multiple when the underlying economics of those business could be extremely different (5% margin vs. 95% margin). For too long, we've been treating all software and all technology companies indiscriminately.”

When capital was cheap, software companies used that capital to grow at all costs and grab as much market share as possible. “That was exactly the right decision at the time.”

What metrics matter most? “I’m a big believer in gross margin because gross margin will ultimately determining your operating margin. If you're subsidising something or you’re in a commodity business resulting in a 40-60%gross margin, there is no no way that you're going to have an operating margin that looks like a software company.”

It’s hard to avoid individual company analysis (e.g. pricing pressure dynamics, parts of a product being commoditized, longstanding moat) to understand if a software company can have a long term 30-40% profitability.

“I’ve noticed over many years of investing in startups that a lot of time, the first product will get you to $100-200m in revenues but then start to peter out. At this point, you have to figure out other growth drivers.”

In tech, you have two categories of extremely successful companies. On the one hand, the Magnificient 7 which are able to sustain 30% annual growth almost forever while being close to profitability. On the other hand, you have strong software companies (Autodesk, Adobe) which are growing 10-20% annually while having 30-40% FCF margins.

Cloud hyper-scalers (Amazon, Google and Microsoft) are still benefitting from the massive transitions to the cloud (and they’re capturing 90% of the value created from a cloud transition compared to other SaaS providers) and managed to re-accelerate their annual growth (21% YoY growth in Q4-23 vs. 19% YoY growth in Q3-23).

Sunday, Feb. 11th: Pennylane raised a €40m series C at a €1bn+ valuation from DST and Sequoia. It’s an accounting software used by 2k accountants and 120k SMBs (40x growth in 24 months). Pennylane is bundling multiple financial services to its accounting software including electronic invoicing, cash-flow management and banking. It aims to use the funding to further integrate AI into its platform and to acquire complementary products.- Techcrunch, Tech.eu

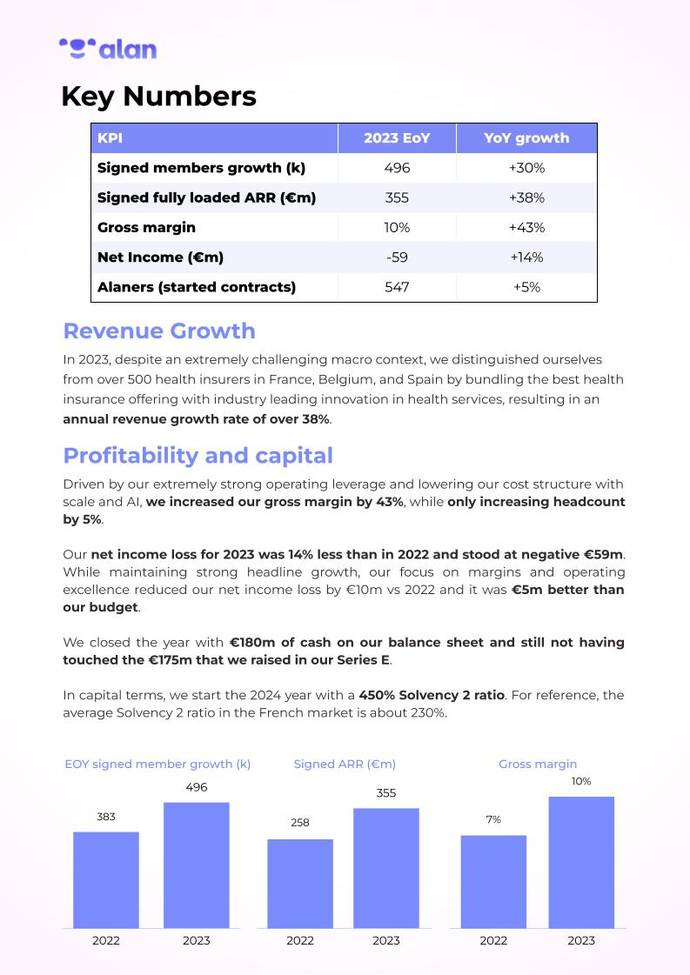

Tuesday, Feb. 13th: Alan generated €350m in revenues in 2023 (40% YoY growth) covering 500k employees in France, Belgium and Spain (vs. 375k users in 2022). It has a 10% gross margin (vs. 8% in 2022 and 13% forecasted for 2023) and burnt €59m (vs. €72.4m in 2022). It aims to become profitable by 2026 at the group level and profitable in France by 2025. It acquired 5k new customers in 2023. It has enough cash in the bank to reach profitability without raising additional capital. - Sifted, Techcrunch, Alan

Wednesday, Feb. 14th: Supercell’s CEO Ilkka Paananen published its annual letter. In 2023, Supercell generated €1.7bn in sales (4.7% YoY decline) and €580m in EBITDA (8.2% decline). - Supercell, DoF

“The presentation first highlighted the cold facts of Supercell’s performance in the last several years. We had not been able to grow our live games and had fallen behind the best companies who had done so. Furthermore, we had not released a new game since Brawl Stars in 2018. The result, I showed in detail, was Supercell falling from the #1-ranked global publisher of mobile games in 2016 to outside the Top 10 in 2023.”

“The best-in-class companies grew their live games, we had not (GGWP: Dream Games, Riot Games, King, Playrix, and others). Several great new games came out and performed extremely well since we launched Brawl Stars, we had not launched any (h/t: Royal Match, Genshin Impact, Monopoly Go, CoD Mobile, and others).”

A new game within Supercell should be operated as a startup with the following characteristics: (i) a team of entrepreneurs (ambitious, resourceful, fast execution, risk takers), (ii) operating under a defined set of constraints (with a pre-defined budget to hit a milestone), (iii) external validation putting the game in from of players as early as possible, (iv) operating in a distraction free environment.

“Once startups have found the so-called “product market fit” (which in my mind means that they’ve been able to develop something that their customers love), they move on to the next phase which is all about making sure as many customers as possible get to use their product/service, while simultaneously making the product/service better. If startups get to this phase, they become “scaleups”. This scaling phase is very different and requires a different type of thinking. I believe the same applies to games and we would benefit from taking in some lessons from the scaleups.”

“Our games declined during the first half of 2023 as the mobile games market overall has continued to decline. […] For our live games, every quarter last year was better than the one before it, and right now we are on a strong growth trajectory.”

Ikka did not discuss M&A and Supercell’s proprietary game engine which were topics that were usually covered in his annual letters.

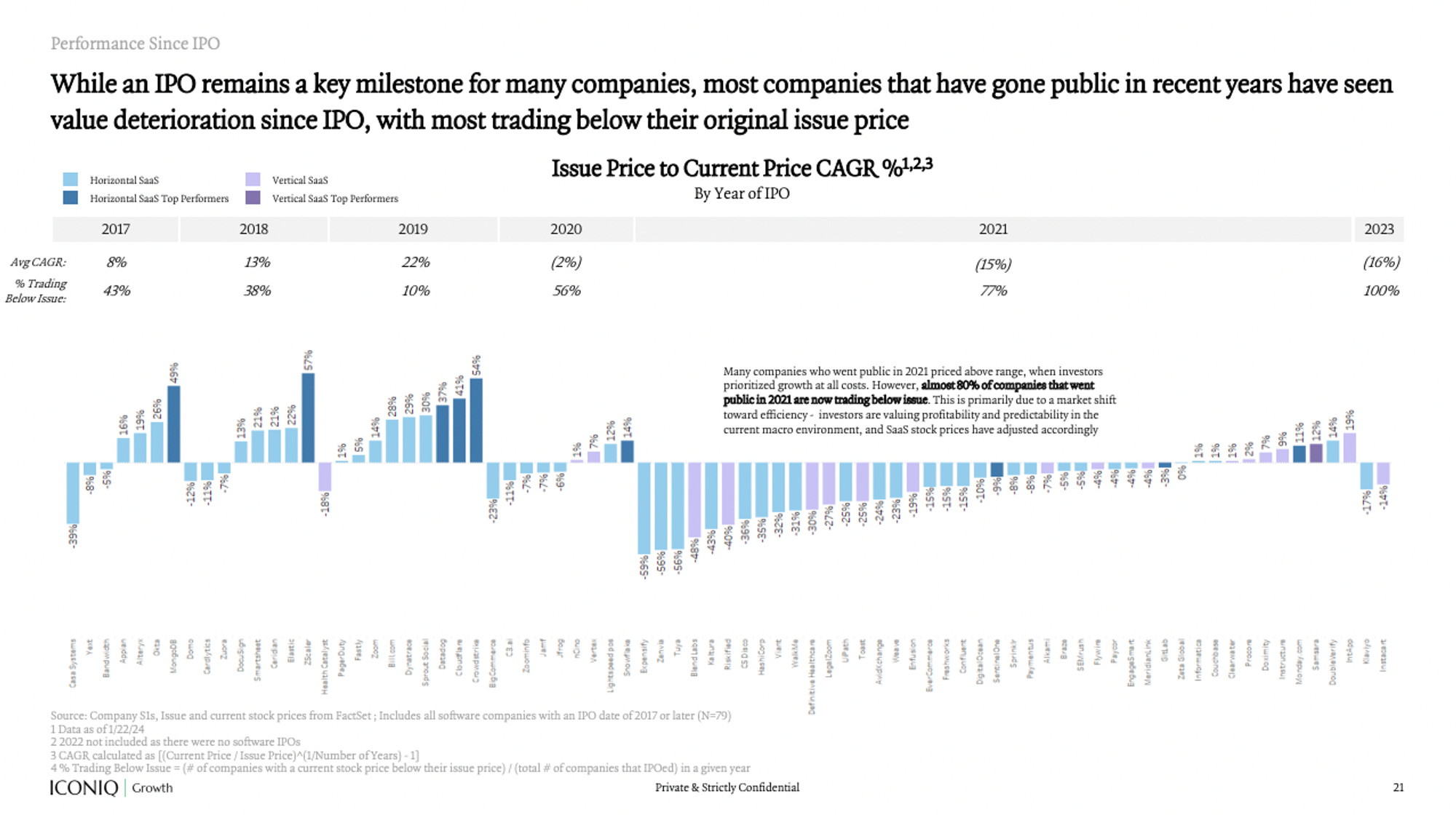

Supercell’s Sales (black) and EBITDA (red) in €m Thursday, Feb. 15th: Iconiq published a report on the SaaS IPO landscape. - Iconiq

“Equity multiples and performance are directly correlated with interest rates and the public markets have seen a significant compression in value amidst rising interest rates and macroeconomic volatility. In particular, high-growth companies (i.e. growing 30%+ YoY) have seen the largest deterioration in value over the last 2 years.”

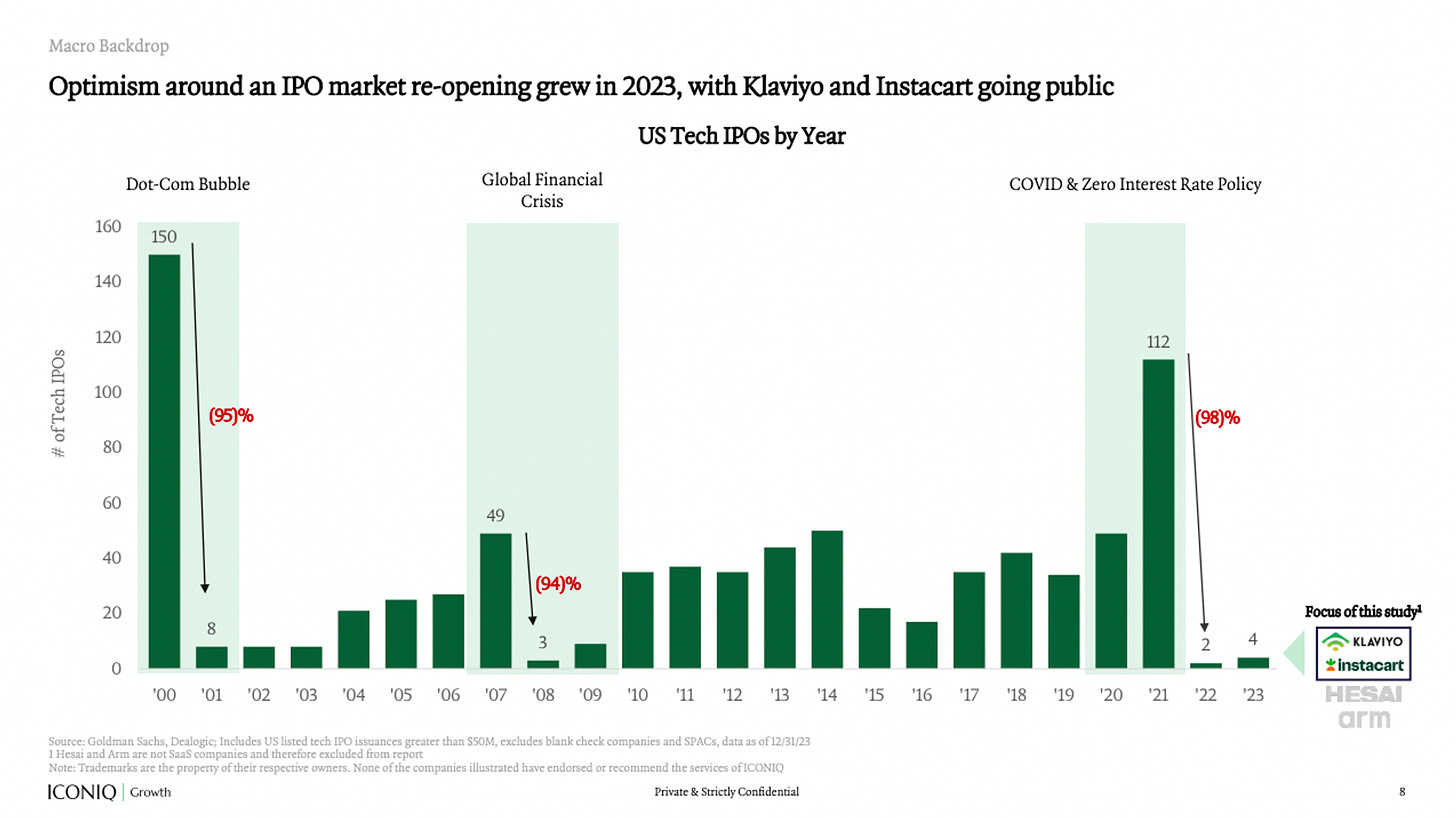

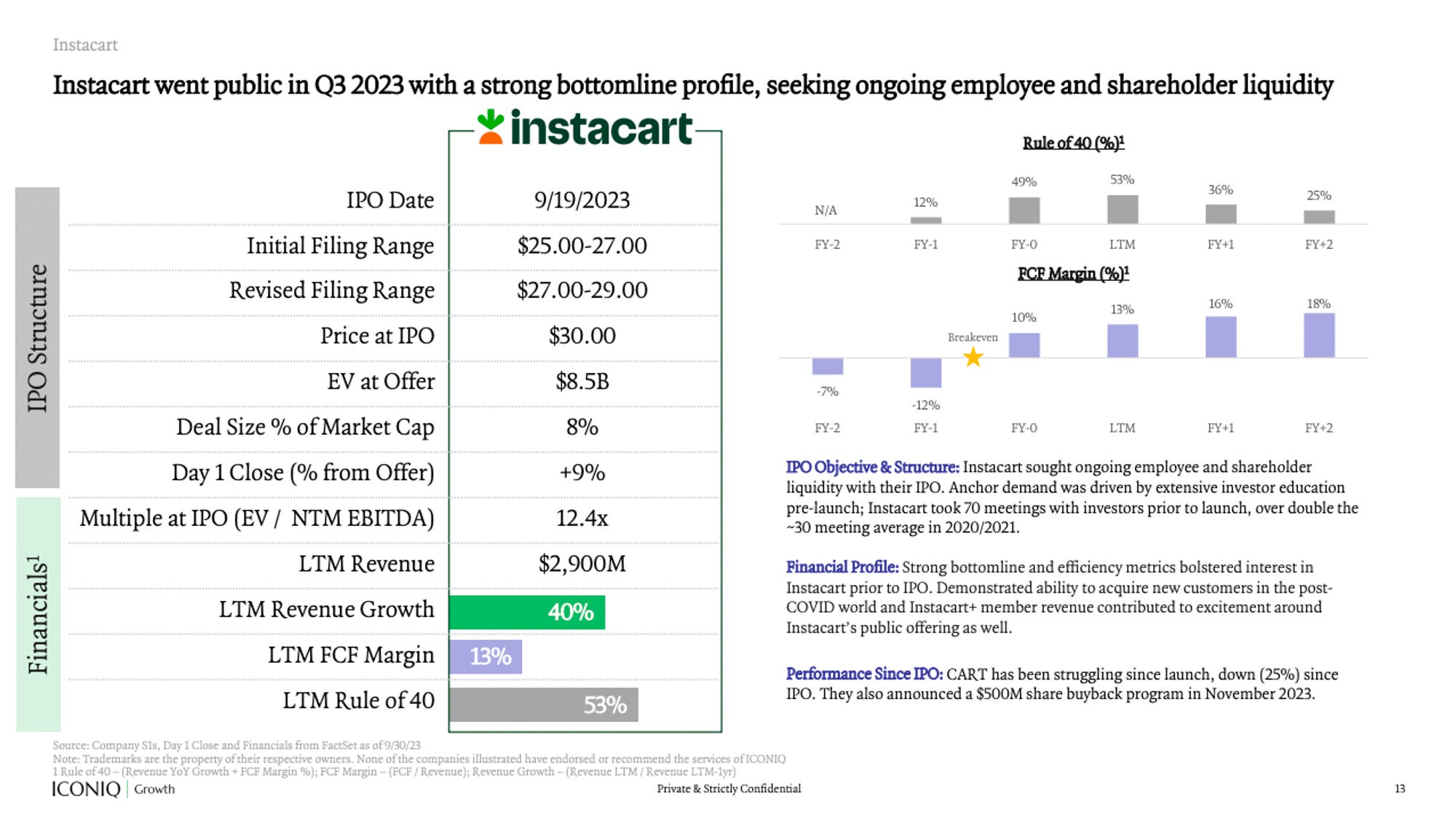

“Optimism around an IPO market re-opening grew in 2023, with Klaviyo and Instacart going public; both companies commanded exceptionally strong financial profiles across both growth and efficiency. With the tailwinds from COVID and the resulting zero interest rate policy and low cost of capital environment, we saw companies with less efficient profiles go public from 2020-2021. The 2023 class of IPOs has reversed this trend, with median YoY revenue growth and Rule of 40 above 2018 levels. However, despite their premium financial profiles both companies commanded forward revenue multiples below the 2021 average.”

“In the current environment, YoY growth, gross margin, FCF margin, Rule of 40 and NDR are the five metrics most highly correlated with EV/NTM revenue. From December 2020 to December 2023, the relative importance of profitability and gross margin increased significantly. While the market has placed a decreasing emphasis on growth over the past few years, as of December 2023 revenue growth still had a larger impact on public revenue multiples than FCF margin. Rule of 40 is the primary driver of valuation in the public markets in the current environment, with revenue growth and NDR tied for a close second, indicating sustainable and efficient growth is top of mind for investors”

Friday, Feb. 16th: YC published a list of themes that it would like to fund in the coming years. - YC

Applying ML to robotics. “Robotics hasn't yet had its GPT moment, but we think it’s close. […] With the rapid improvements in foundation models, it's finally possible to make robots that have human-level perception and judgment.”

New ERP software. “ERPs are usually known to be expensive, painful to implement, and disliked by users, yet are absolutely necessary and the very definition of business critical to its customers. We would like to see new startups that build software that helps businesses run. Ideally that software would be loved by its customers for its flexibility and ease of use.”

Small fine tuned models as an alternative to giant generic ones. “Giant generic models with a lot of parameters are very impressive. But they are also very costly and often come with latency and privacy challenges. Fortunately, smaller open-source models like Llama2 and Mistral have already demonstrated that, when finely tuned with appropriate data, they can yield comparable results at a fraction of the cost.”

AI to build enterprise software. “What if AI could change how enterprise software gets built and sold? The core of what every customer wants is the same — they just want it customized around the edges. AI is good at writing code — especially when you give it an existing codebase to learn from. So what if instead of long enterprise sales cycles you just give customers a simple starter product and have them tell your AI how they want it customized? In the future, every enterprise could have their own custom ERP, CRM or HRIS that is continually updating itself as the company itself is changing.”

Saturday, Feb. 17th: Toast published its 2023 full-year results. Toast had an impressive year reaching EBITDA profitability while growing its ARR by 35%. - Toast 1, Toast 2

In FY-2023, Toast reached $1.2bn in ARR (35% YoY growth) with a 111% Net Dollar Retention and 106k locations (34% YoY growth). It had a 14 month payback period.

“The company should continue to see healthy market share gains in the coming years and the company has adopted a much more aggressive approach to cost management.”

Toast laid-off 10% of its workforce. “As you know, Toast grew rapidly over the past 3 years to support our growing customer community. As we've taken a look across the organization, it has become clear that we grew our team too quickly in some areas, and we need to restructure the organization to best align with our most important priorities. The changes we announce today primarily focus on non customer-facing roles.”

“We're focused on four strategic priorities: first, scaling restaurant locations within our core business; second, driving ARR and ARPU by building products and experiences our customers love; third, expanding our addressable market by launching and scaling new growth vectors; and fourth, setting up the company to scale and deliver ongoing operating leverage.”

“For new customers, earlier this month, we rolled out simpler product packaging that will enable our new business reps to maximize initial product attach and ARPU while balancing strong location growth.”

“To complement our success across SMB restaurants, our product team is hard at work to make Toast an even better fit across enterprise, hotel restaurants and international markets.”

Sunday, Feb. 18th: Sam Lessin published an article highlighting the differences between funds optimising for assets under management and funds optimising for financial performance. - Sam Lessin

“On one hand- you have the 'fee optimizers'. These funds generate 'returns' for their investors only to the extent that it helps them gather more AUM to charge fees on ... and the public markets (for those that are public) only value those entities as fee-generating machines who just have to make enough profits for folks to keep growing and gathering more fees but over a basic hurdle they don't really care how they perform for LPs or for entrepreneurs because they have no incentive to be.”

“On the other hand- you have the 'return optimizers'. These folks stay small because - let's be clear - it is way easier to generate multiples on small dollars than it is on billions or tens of billions of dollars.... They don't have much in the way of fee-income to write home about... and because they don't produce large consistent cashflows the public markets care zero for these folks - but they make their money on epic returns / specific fund investments which are more idiosyncratic and look much more like / are much more aligned with how the entrepreneur themselves get paid. They eat only when their investments / founders eat.”

Monday, Feb. 19th: Mirakl reached $160m in ARR (20% YoY growth) while processing $8.6bn in GMV (50% YoY) from 450+ customers in 2023. It reached profitability in Q4-23 on its flagship product (Mirakl Platform). - Mirakl

“More than 30 Mirakl-powered platforms surpassed the $100M GMV threshold in 2023.”

“With the launch of Mirakl Ads and our newly signed global partnership with Havas, Mirakl is positioned to be a leading player in the exponentially growing retail media ecosystem in 2024.”

Mirakl launched Artificial Mirakl Intelligence (AMI) which is a suite of AI features integrated into the broader Mirkal’s platform (e.g. boost SEO, improve data quality & completeness of product catalogs, optimise conversion by changing product titles).

Tuesday, Feb. 20th: Morgan Beller who is general partner at NFX wrote a post comparing AI applications to the bottled water industry. - NFX

“This is just the reality: there will be 100 teams trying to make the same generative AI application as you are right now. Plus there will be incumbents gunning for your market.”

“What we’re seeing with AI is that tech provides you basically no protection from the start. Tech differentiation in AI is a shrinking moat.”

“[As an AI founder in the application space], you can either guarantee a loss and not play the brand and marketing game. Or, you can give yourself a small chance of success by playing the game, and seeking other avenues to build your advantage.”

“At a certain point every technology will reach an inflection point where the tech itself is no longer the secret sauce. […] When we reach this point, usually one of two things happens: (i) an entirely new industry forms on top of this technology (tech-bio on top of genome sequencing or electric vehicles on top of electric batteries), (ii) companies double down on new ways to differentiate themselves (i.e. brand in AI).”

“Once you realize that the underlying tech is no longer your differentiator, you start asking yourself different questions, seeking new niches, and focusing on new points of differentiation.”

Wednesday, Feb. 21st: The Economist wrote on Costco. It’s the world third largest retailer behind Walmart and Amazon. Costco has a 8% annual staff turnover compared with 60% on average in the retail industry. - The Economist

“The company is guided by a simple idea—hook shoppers by offering high-quality products at the lowest prices. It does this by keeping markups low while charging a fixed membership fee and stocking fewer distinct products, all while treating its employees generously.”

“Most retailers boost profits by marking up prices. Not Costco. Its gross margins hover around 12%, compared with Walmart’s 24%. The company makes up the shortfall through its membership fees: customers pay $60 or more a year to shop at its stores. In 2023 fees from its 129m members netted $4.6bn, more than half of Costco’s operating profits.”

“The more members the company has, the greater its buying power, leading to better deals with suppliers, most of which are then passed on to its members. The fee also encourages customers to focus their spending at Costco, rather than shopping around. That seems to work; membership-renewal rates are upwards of 90%.”

“It has also expanded its own brand, Kirkland Signature, which now accounts for over a quarter of its sales, well above average for a retailer. Its margins on its own-brand products are about six percentage points higher than for brands such as Hershey or Kellogg’s.”

Thursday, Feb. 22: Planity raised a $50m series C led by Infravia with the participation of existing investors Crédit Mutuel, Revaia and BPI. It’s a SaaS enabled marketplace for the beauty industry. It reached $40m in ARR (growing at 60% YoY) from 40k customers (25% market share in France). It operates in 3 European markets (France, Germany and Belgium). 10m appointments are booked every month on Planity. It will use the capital to (i) continue its expansion in other European geographies, (ii) to expand into fitness centers, (iii) to integrate AI features into its platform and (iv) to recruit 300 people.. - Tech.eu, Techcrunch, Planity

Friday, Feb. 23rd: I listened to a Colossus’ podcast episode with Parker Conrad who is the CEO and cofounder at Rippling who is an all-in-one platform for HR, IT and finance. - Colossus

Today, if you want to launch a really narrow point SaaS solution, there is an extremely high likelihood that there are already multiple other companies doing the same thing.

A compound startup is a startup which is taking on a constellation of interrelated products or features and build them in this way where they're seamlessly interoperable to create a unique value proposition for customers. Compound companies are not new. Saleforce, Microsoft, Oracle and SAP are already compound companies.

“Now that there's a little more stability in the underlying vectors for how we deliver software [following the transition from on-premise to cloud], I think the overwhelming product and commercial advantages of deeply integrated software and bundled contracting and pricing are going to start to re-dominate and a new generation of massive business software vendors are going to emerge.”

“All of the markets that we end up going into are areas where we think we have unique and distinct product advantages that come from the fact that this new product is deeply integrated with the employee data with the rest of Rippling and in particular, with a set of underlying platform capabilities that we call middleware. The idea behind middleware is that there are a set of product components that end up being repeated a lot across a lot of different software verticals. And one of the advantages of building a set of interrelated products is that you can abstract out these capabilities and be much better at those capabilities than any of your point solutions and competitors are. These capabilities include workflow automation, role-based permissions, custom policies, approvals and routing, reporting and analytics.”

Salesforce is a system for managing business process and workflow that relates to customers and customer data. Rippling is doing the same for employees and employee data.

Rippling have 4 key advantages over hyper-focused companies building in the HR, IT or finance sectors:

Products are more deeply integrated with employee data and with Rippling overall,

Middleware capabilities are much more powerful than standalone competitors,

The learning curve is lower to use a new product when you stay on the Rippling’s platform

You have pricing and contracting advantages because you can amortise S&M and R&D costs across a whole bunch of different SKUs.

“We love going into competitive and commoditized markets because we think that those are the cases where we win. […] In these markets, Rippling is the only product that is not a commodity because it has these unique and differentiated advantages in the form of our platform capabilities and the integration with Rippling & employee data.”

“We have an app shop today and we have partners in that app shop that compete with our specific products.” It does not matter because we want to give high flexibility to our customers and if they want to have a strong point solution on a given SKU, they should be able to use it seamlessly within the Rippling’s ecosystem.

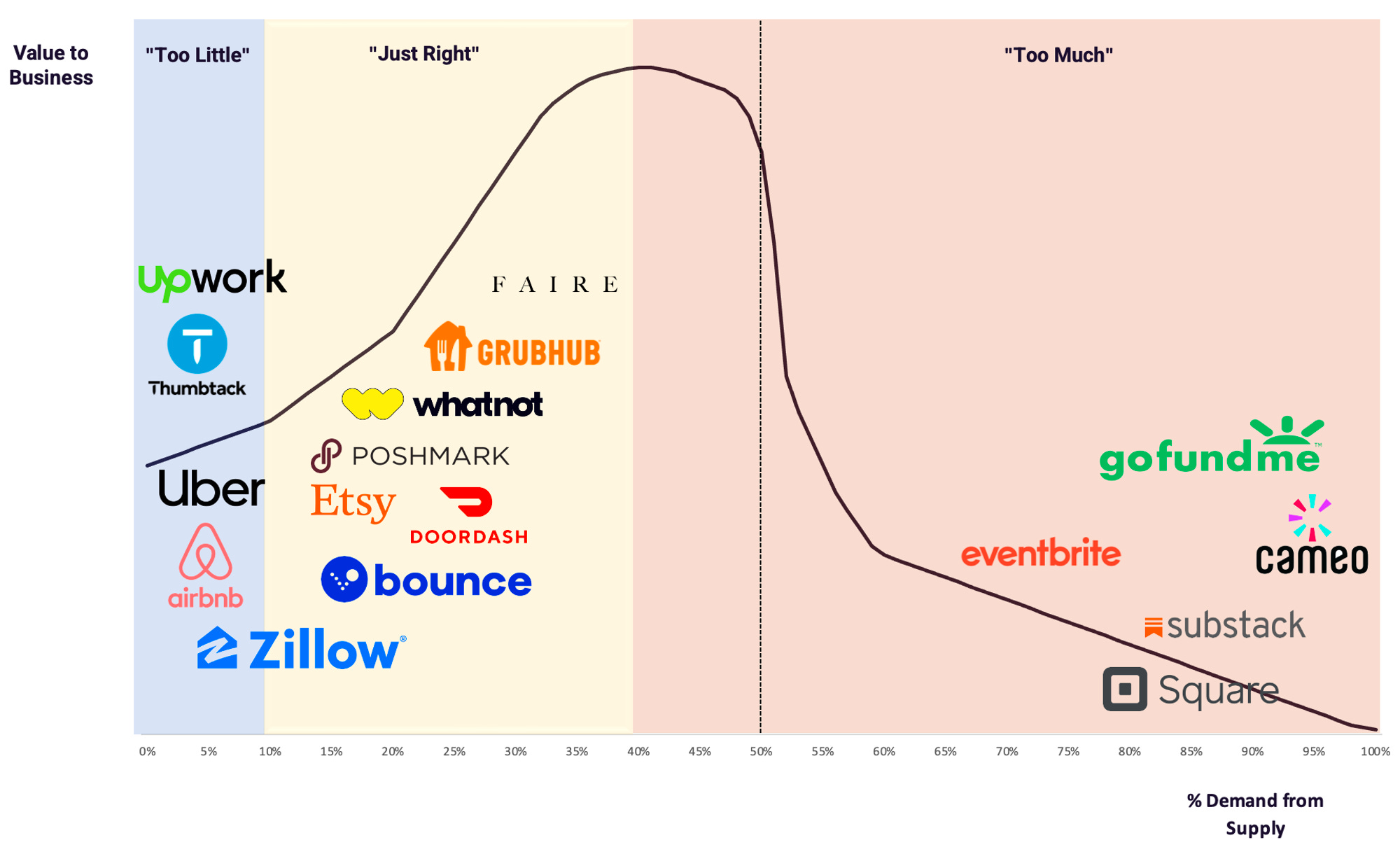

Saturday, Feb. 24th: Casey Winters wrote about marketplaces leveraging their supply to bring demand into the marketplace. - Casey Accidental

In order to scale a marketplace, founders can leverage supply to bring demand. The best marketplace are driving 10-40% of their demand from their supply. If you’re besides this range, you may have an underperforming marketplace model.

“Our rule of thumb is that a marketplace needs to generate at least 50% of the transactions for cross-side network effects to exist. If a supplier would get 50% more transactions through a platform vs. on their own, most rational suppliers would prefer that vs. the 15-25% higher margins they could get going directly to their customers and avoiding a marketplace fee.”

In order to leverage your supply to bring more demand, the marketplace should have the following characteristics: (i) the supply should have enough demand and enough leverage on that demand to bring them on the marketplace, (ii) the supply should be sufficiently incentivised by value added services to transact directly on the marketplace and (iii) the demand should be promiscuous enough so that their diversify their base of suppliers.

To activate this channel, the marketplace can create marketing tools to help suppliers attractive more transactions (e.g. website builders, embedded checkouts into suppliers’ own websites, email & SMS marketing, etc.).

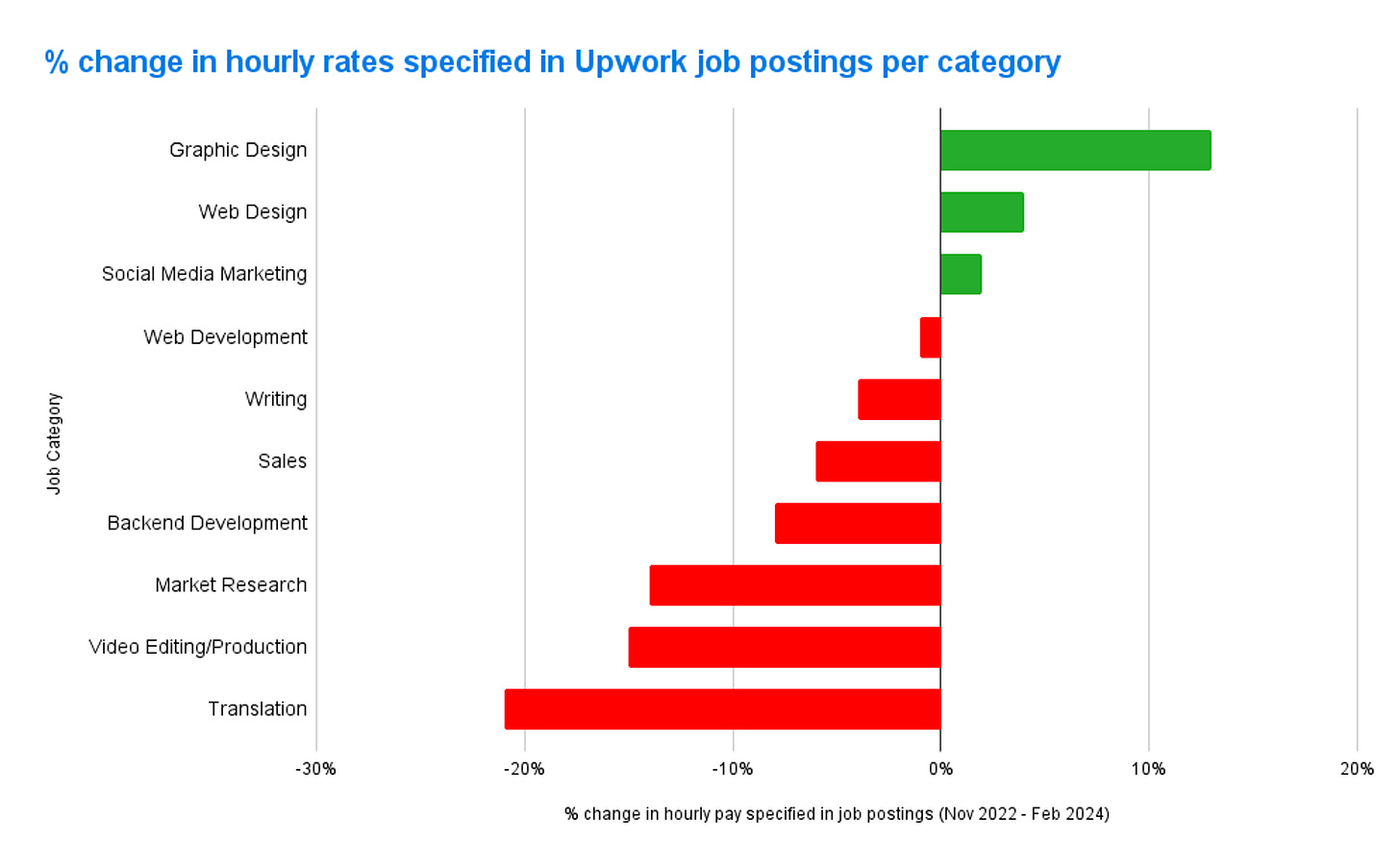

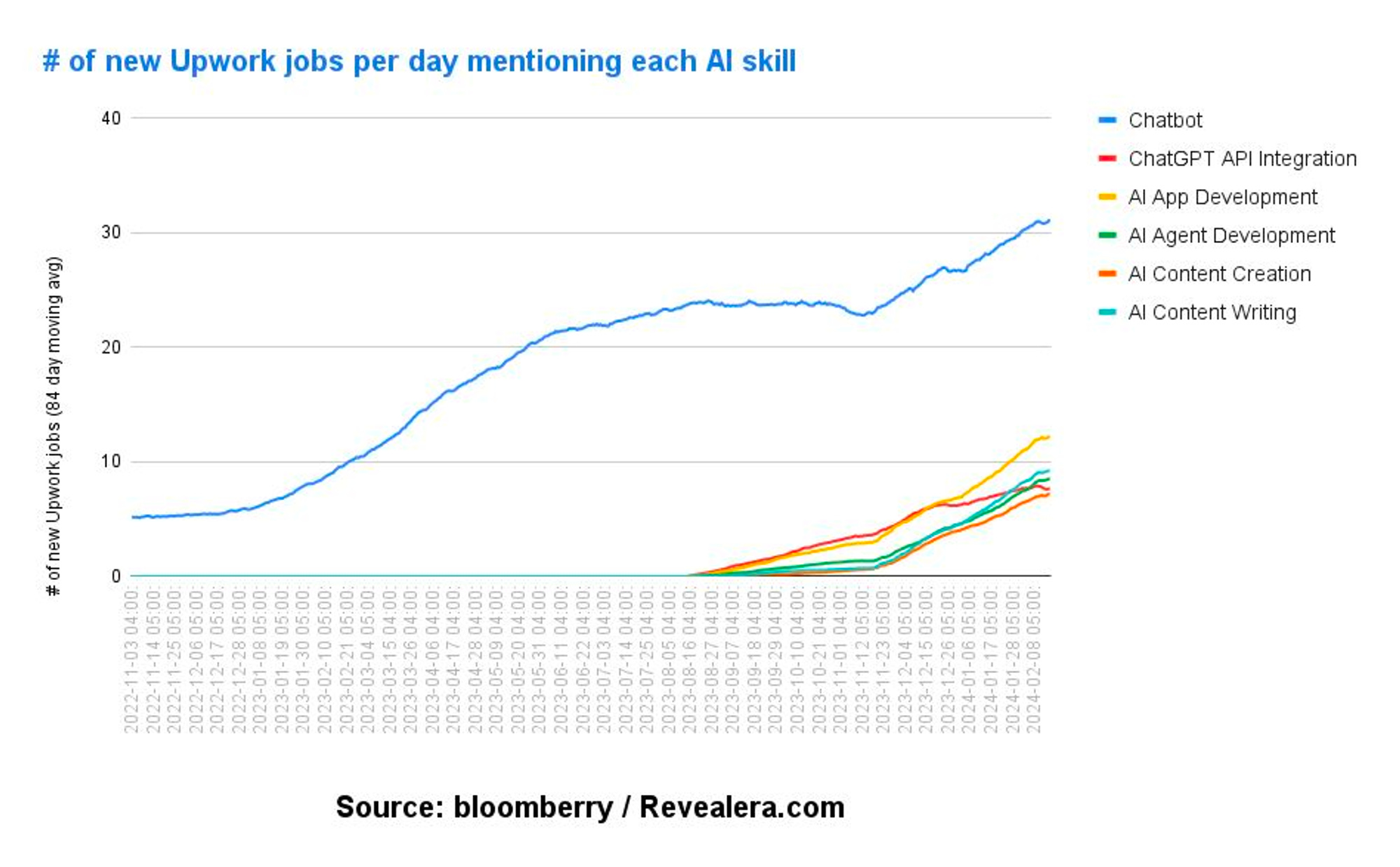

Sunday, Feb. 25th: Bloomberry analysed freelancing jobs on Upwork to understand which jobs are most likely to be replaced by AI. Writing, customer service and translation are the most impacted jobs. - Upwork

"I was surprised to see graphics design, video editing/production, and even software development jobs go up, given all the anecdotal stories we’ve been hearing about people using ChatGPT to generate code, illustrations and even full featured videos.” The articles talks about two reasons: (i) Gen. AI tools are “not polished enough for other jobs like video and image generation” and (ii) “it will take time for users to learn how to use these tools effectively, and understanding what they can/can not do”.

“The most popular use case, by far for AI right now is in developing chatbots.”

Monday, Feb. 26th: The Time wrote on MrBeast. - Time

“Donaldson is probably the most watched person on earth.” “A recent video in which he and his posse of besties go on a vacation and spend $1 to $250,000 per day garnered 52m views in 24 hours. That’s 20 times the number of people who watched the Succession finale and more than twice as many people as saw Barbie or Oppenheimer during opening weekend. His most popular video, a version of the Korean TV show Squid Game, has been seen half a billion times.”

“In 2023 alone these videos gained him 99m new YouTube subscribers, almost double the growth of any other channel.”

“Donaldson’s swift rise has been spurred by massive changes in the media landscape where individuals have replaced institutions as the gatekeepers of entertainment and information.”

“His sway has grown such that in 2022 he launched a line of snacks, Feastables, that by 2023 was in multiple countries and will have, according to him, $500 million in annual revenue this year.”

“In December 2020, he started a food-delivery service, MrBeast Burger. It grew to a reported 1,700 virtual locations and $100 million in total revenue by August 2022, before becoming ensnared in a legal battle. He also has a toy deal and is reportedly on the verge of signing a nine-figure deal with Amazon.”

“Donaldson is not your usual entrepreneur. For one, he’s happy to talk about how much revenue he brings in: about $600 million to $700 million a year. For two, he claims to not be rich. “I mean, not right now,” he clarifies. “I’m not naive; maybe one day. But right now, whatever we make, we reinvest.”

“Like Feastables, his production company was not profitable in 2023, nor is it expected to be in 2024.”

“Brands pay $2.5 million to $3 million to have Donaldson give them a shout-out. To run an ad before one of his videos is about as expensive.”

“Donaldson won’t need advertisers anyway. “I know a video is gonna get 200m views,” he says. “And I sell that video to a different company, which is just sad. In a perfect world, I would own a couple of different companies—chocolate, and maybe a global games company—and then that’s what I would promote in the videos.” Feastables, in its second year, brought in about 70% of MrBeast’s revenue. Plans are under way for digital products, including games and apps, and he has several tools for aspiring YouTubers including ViewStats for audience analysis and CreatorGlobal for an audio translation.”

Tuesday, Feb. 27th: Reddit published its S1 to go public. - Reddit, Bloomberg

Reddit has 100k active communities (500 communities with 1m+ subscribers), 76m average DAUs in Dec. 23, 267m average WAUs and 500m MAUs in Dec. 23. In 2023, it generated $804m in sales (vs. $667m in 2022, 21% YoY growth) and burnt $69.3m in EBITDA (vs. -$108.4m in 2022).

Reddit has 1bn posts and 16bn comments. It was also in the top 10 of most visited websites in the US in Dec. 2023.

“Our mission is to bring community, belonging, and empowerment to everyone in the world.”

“Reddit is a global, digital city where anyone in the world can join a community to learn from one another, engage in authentic conversations, explore passions, research new hobbies, exchange goods and services, create new communities and experiences, share a few laughs, and find belonging. People are diverse and have multiple interests. Just like in a city, where citizens are part of multiple subcommunities, on Reddit, users often belong to multiple communities.”

“Communities on Reddit are organized based on specific interests and are called subreddits. Within subreddits, Redditors engage in active and in-depth conversations by sharing experiences, submitting links, uploading images and videos, and replying to one another in comment threads on any topic.”

“Commerce is another area of growth that has emerged organically on Reddit. In fact, new community-based marketplaces have already sprung up specifically for commercial purposes, such as r/ PhotoShopRequest, where users can request photoshop services for payment, or r/ RandomActsofCards, where users request and send cards to each other and spread a little bit of joy around the world.”

“We generally find that the longer Redditors have been on Reddit, the more engaged they become. As of December 2023, when someone first makes an account, the average active minutes for logged-in users on Reddit starts at approximately 20 minutes per day, but increases to over 35 minutes a day for those who have been on Reddit for over five years and even over 45 minutes a day for those who have been on Reddit for over seven years.”

“75% of people on Reddit said they believe Reddit is a trustworthy place to inform their decision to buy a new product across specified consumer product categories.”

35m daily search queries were done on Reddit in Dec. 23.

50% of users are not in the US. 90% of posts on Reddit are in English.

Reddit signed $203m in aggregate contract value to let third parties train their AI algorithms on Reddit’s data with at least $66m to be recognised in 2024.

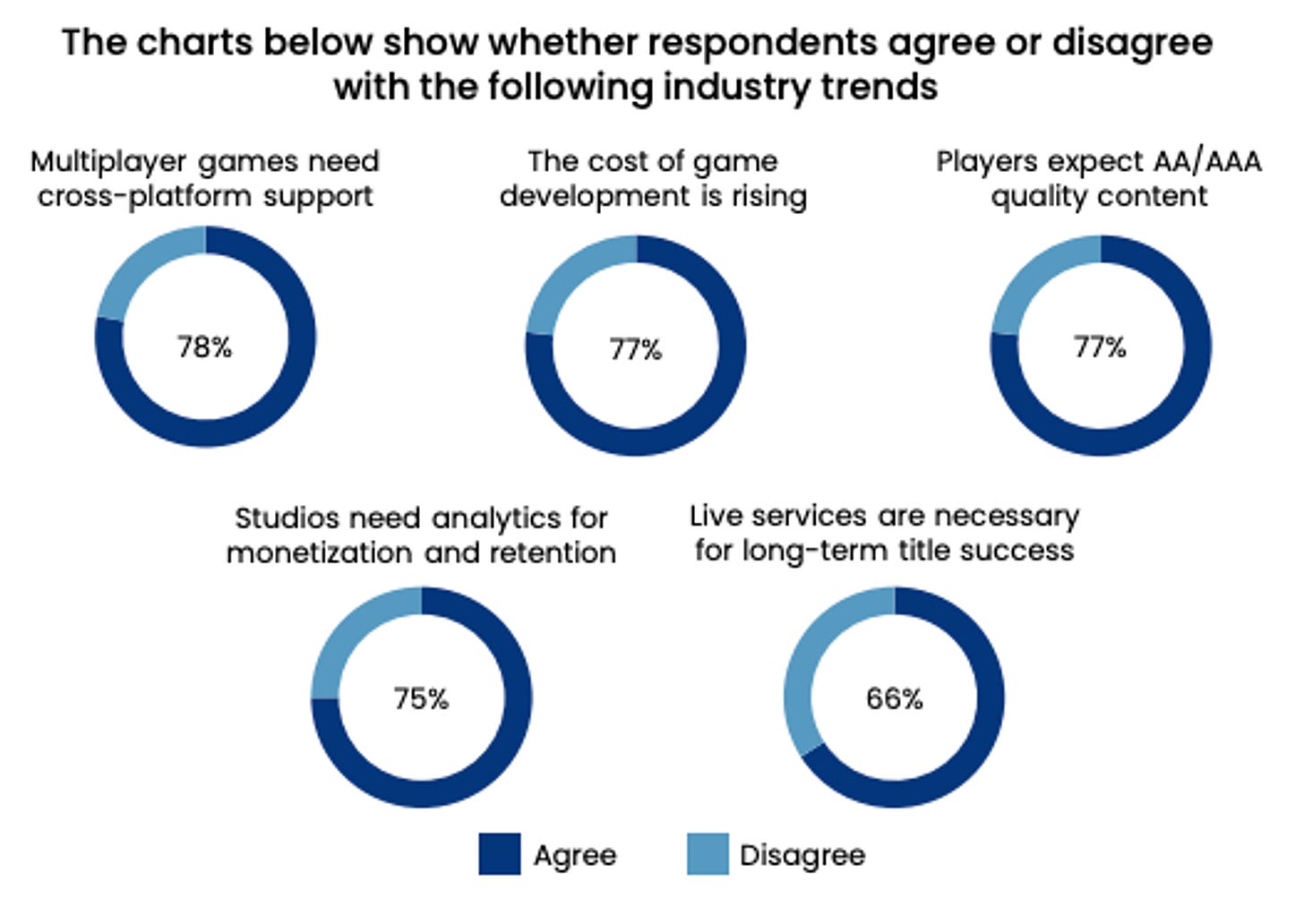

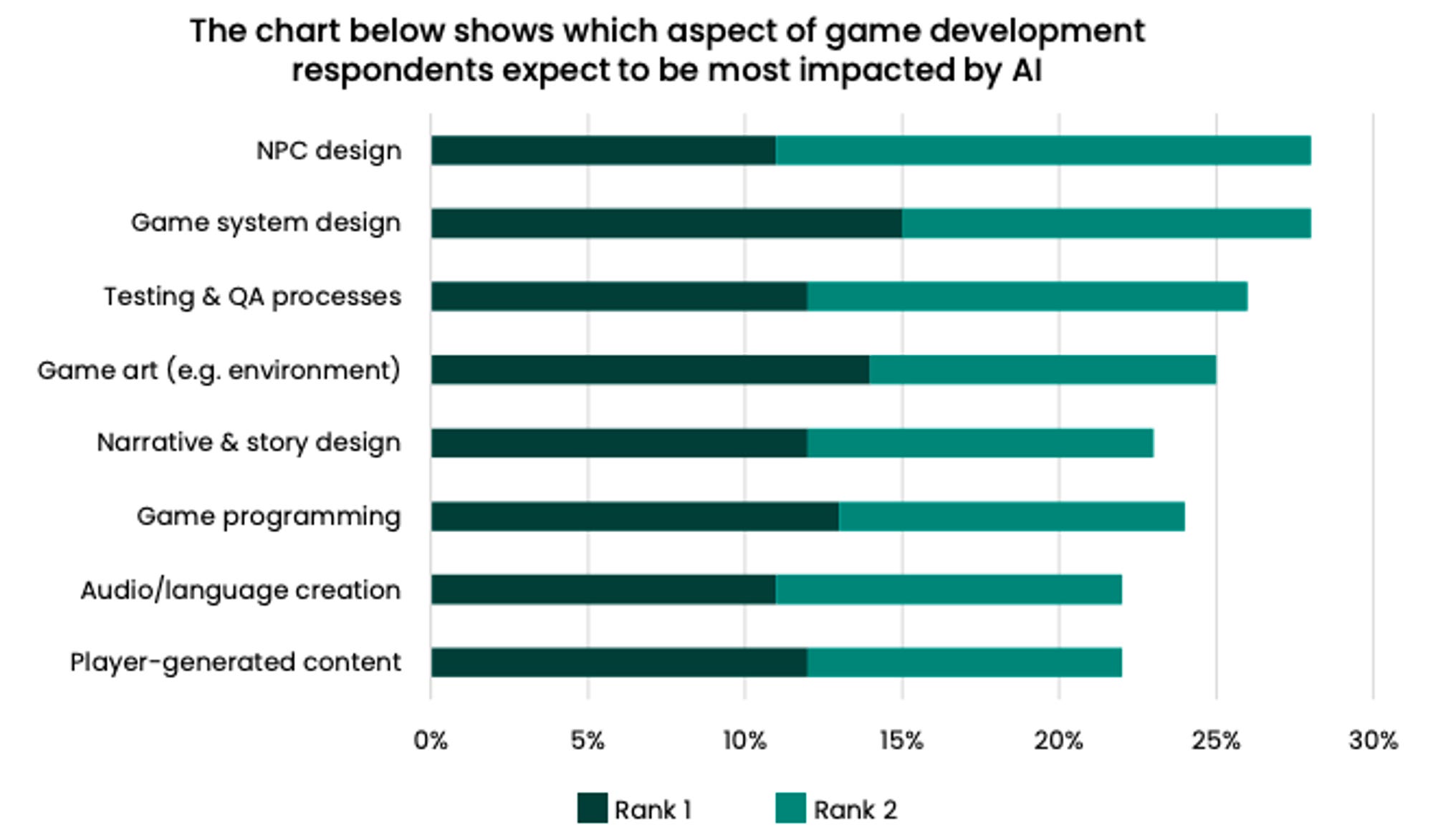

Wednesday, Feb. 28th: Griffin published a report on game development. - Griffin

“77% of studios reported that the cost of game development is continuing to rise.” “65% of studios are currently working on a title with a regular update cadence for their game.” “88% of respondents are actively evaluating new tools to bring into their workflows.” “65% of studios are planning to increase their use of off the shelf tools.” ”52% of artists see AI creating as much value as a human artist within 2 years”

Thursday, Feb. 29th: I listened to a podcast with Bill Gurley and Brad Gerstner on the impact of AI on big tech companies. - BG2

The stock market for US tech companies has been relatively flat since the beginning of the year. The market is discriminating between AI winners and losers. Moreover, the general macro-economy is still unclear with inflation & interest rates staying a bit higher than expected.

To understand the impact of AI on big tech companies you need to look at 1/ if their existing business is attacked or enhanced by AI and 2/ at if AI is opening new business opportunities.

Microsoft was quickly put into the AI winner category by the public market because investors understood that AI will have a massive impact on personal productivity for both white collar workers on the Office Suite and developers using Github and Microsoft’s IDEs. Moreover, Microsoft’s close relationship with OpenAI suggests that they can move at a faster pace than other established tech giants.

Mike Mauboussin developed a concept called Competitive Advantage Period (CAP) to estimate the number of years into the future that the company is going to sustain a competitive advantage translated into sustaining returns on incremental capital are superior to its cost of capital. Different businesses have different amount of durability. When a company is facing an innovator dilemma, its CAP can close super fast having a dramatic impact on its market capitalisation (e.g. Yahoo or Blackberry).

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋