📖 Venture Chronicles - February 2023

Overlooked #139

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of February.

For 2023, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for February!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

Wednesday, Feb. 1st: Carta published a chart showing that the average duration between two funding rounds is increasing at all stages and implying that startups should raise capital to have at least 24 months of runway. - Carta

Thursday, Feb. 2nd: Tom Loverro at IVP made the prediction that many early stage startups will die in the next 24 months. Most startups will have to raise in H2-23 and in 2024. Many will fail because funds will be extremely selective and many startups have unsustainable valuations. - Tom Loverro

“We're not going back to 15x+ fwd revenue multiples even for excellent companies in the public markets. (We're currently at ~4.5x for most companies and 8x-12x for the elite.) Private market multiples may not match the public markets but they will come a lot closer.”

“Raise now or sooner than you expected, before the Great Flood of 2023. If you fail, you can always try again later.”

“Trade better unit economics for growth. Growth rates are coming way down for everyone this year. It’s all relative when you’re raising money. If you can nail your unit economics, you can always ramp burn and growth later.”

Friday, Feb. 3rd: I read a post from Eli at Verticalised on the evolution of solutions serving the field services industry. - Verticalised

ServiceTitan is a diagonal SaaS. “ServiceTitan has both aspects of a horizontal SaaS tool in breadth (common workflows across multiple sub-verticals) and a narrowed focus in terms of depth (only field services).” Service Titan is focused on home services.

Service Max is focused on industrial services which is a more complicated market segment than home services because it deals with the in-house service arm of large manufacturers. It offers field service management modules but also equipment and warranty modules which are unique to this segment.

Newer players are focused on individual service verticals (e.g. Roofr for roofers, Skimmer for pools, ThrashLab for waste management). They start by handling a very specific workflow to the industry they are serving before building a more general field service platform.

Saturday, Feb. 4th: Ted Gioia wrote a thought provoking piece on techniques to evaluate a person’s character. - Ted Gioia

Look at who they marry. “A person’s choice of a spouse—or if they aren’t married, their closest lifelong partner—is much more revealing than anything they say or do in public.”

“See how they treat service workers.” “People reveal their true natures when they deal with others who have no power and can never return a favor.”

Look at how they spend their time and money.

“If they cheat at small things, they will cheat at big things.”

Sunday, Feb. 5th: Exit Fuel interviewed Josh Wolfe who is general partner at Lux Capital. - Exit Fuel

“Ask around Silicon Valley about Josh Wolfe and his firm Lux Capital, and you will likely hear a few things: (1) Josh is one of the most well-read and thoughtful allocators in the venture capital space right now, (2) Lux takes bets on frontier ideas that many firms tend to shy away from, as the opportunities are so novel and exist so close to the edge of what’s possible, and (3) Josh and his team have immense conviction - willing to be exceedingly vocal about their visions for the future, and how we, as a society, will get there.”

“Timeless advice [to raise a fund] regardless of whether it was 20 years ago or today would be this: always be prepared, ready to pitch, ready to make a lasting impression, and ready to make the ask. Be able to articulate the current situation in the markets, and why you have an indisputably different, unique angle. And lastly, arguably the most important, people can tell if you really want something, not a greedy wanting, but an ambitious wanting––an intensity even a fiery quiet one that conveys a confidence.”

“I read voraciously, and I read competitively. I have information anxiety and want to know what everyone else knows, and then know more than that or find a different angle that I think others are missing. It’s arrogance of the highest order motivated by deep-rooted insecurity and desire to earn respect, admiration and status.”

“The world has been drunk on SaaS for a decade and the hangover will suck. Attention is deservedly shifting to other areas now attracting some of the smartest engineers we’ve ever seen––from aerospace and defense to cutting-edge biotech leveraging computer science to discover and design molecules, drugs, in ways never before seen.”

Monday, Feb. 6th: Meritech published a report on public companies which are trading at an EV/ARR multiple over 10x. - Meritech

It includes 17 companies: Atlassian, Bill, Clearwater, Cloudfare, Crowdstrike, Datadog, Gitlab, MongoDB, Paycom, Paylocity, Procore, ServiceNow, Snowflake, Sprout, Veeva, Zoominfo and Zscaler.

“An ARR multiple is calculated as a company’s enterprise value divided by its current quarter implied ARR, which is total quarterly revenue multiplied by 4.”

Tuesday, Feb. 7th: Deconstructor of Fun published its predictions for 2023 in the mobile gaming market. - DoF

“In 2023, the iOS and Play stores will be officially declared dead.” “We stopped working actively to try to get featured, both due to the worry of ending up with less visibility, and due to the fact that it didnt translate to business.”

Publishers will push players to off-platform payments to avoid the 30% tax from mobile app stores.

Mobile game developers will try to secure safe harbours (e.g. Netflix, Apple, IP-related game) for their games instead of risking to publish it independently in a world in which mobile app store discovery and online marketing are no longer working.

Wednesday, Feb. 8th: Tiger is still struggling to raise its next fund. It had to cut back its target from $6bn to $5bn knowing that Tiger raised $12.7bn for its previous fund. - WSJ

Investors are marking down private startups’ valuation by 30% to 80%. Almost no secondary transaction happened between March and July 2022.

Tiger is slowing down its investment pace and is pivoting to backing startups at earlier stages.

Thursday, Feb. 9th: I read a post from the Financial Times on senior workers being discriminated. - FT

“Employers in Brazil, India, Italy, Singapore, Spain, UK and the US saying they prefer staff under 45, who are a “better fit” with their company culture. These employers agreed that older workers performed just as well as younger ones; they just don’t want to hire them.”

“While companies focus on race and gender discrimination, and the needs of Gen Z, workplace age discrimination seems to be increasing. 78% of older American workers claimed to have seen or experienced it in 2020, the highest level since 2003.”

We should design career tracks to keep senior employees longer into organisations without necessarily implying that they are ones with the highest pay and responsibilities.

Friday, Feb. 10th: I listened to a Colossus podcast on Ryanair with Andrew Hollingworth who is the founder and portfolio manager at Holland Advisors. - Colossus

The airline industry has poor long term return on capital and few companies managed to build a sustainable competitive advantage.

Ryanair is the largest airline in Europe. It has a 16% market share in intra-European routes (vs. 4% in 2004 and 12% in 2016) with 170m annual travellers. It was founded in 1986. It went public in 1997. While building an airline with cheap prices for passengers and good working conditions for employees, its CEO Michael O’Leary is obsessed about killing competitors and making money for himself and shareholders. In 2018, Ryanair had a 23% EBIT margin.

As Amazon and Costco, Ryanair has a scale economy business model cutting costs as much as possible and partly redistributing the value generated to customers. It counter positioned the industry over-communicating over the fact that Ryanair was cheap, was a “brutally low-cost business”.

Ryanair has a culture of cutting costs everywhere. It made a massive order to Boeing when the manufacturer was desperate for business to have cheaper aircrafts than anybody else. It uses MAX aircrafts which is more fuel efficient than its counterparts. It flies from secondary airports which do not ask for high operations fees.

Saturday, Feb. 11th: The Economist wrote an article on YouTube claiming that the company should be spun-off from Google to be valued correctly by the market. - The Economist

“YouTube has become so integral to the entertainment landscape that to many it is DIY handbook, cookbook, childminder, jukebox, yoga instructor, news channel and time sink, all rolled into one.”

YouTube has 2.6bn MAUs and generated $29bn in ad sales in 2022 (10% of Google’s revenues). It succeeds in competing with (i) streaming services like Netflix, (ii) social media contender TikTok (YouTube Shorts receive 50bn views per days) thanks to a successful revenue sharing model with creators and (iii) music streaming services like Spotify.

An independent YouTube would reduce the criticisms on Google’s monopoly over the digital advertising market and would show the market that Google is increasing its focus on generative AI to compete with Microsoft.

Sunday, Feb. 12th: vSol for restaurants Toast acquired Delphi Display Systems. Delphi is a digital display solutions and drive-thru technology for quick-service restaurants (QSRs) used by 40k locations over the world. Toast aims to become the all-in-one solution for restaurants which use on average 7 different systems. Adding Delphi to its product suite will contribute to streamline the tech stack used by restaurants in the US. - Toast, Restaurant Business

Monday, Feb. 13th: Ricardo and Louis at P9 wrote about vertical APIs. - P9

“The advent of APIs is not only reshaping the software development industry, but it’s also reshaping older industries like banking or healthcare.”

“APIs are like LEGOs to build software. The most basic example is Stripe. Any developer that wants to process payments can use Stripe instead of building their own payment infrastructure.”

P9 highlights the following opportunities for vertical APIs: (i) leveraging industry wide protocols with modern technologies and offering new software possibilities on top, (ii) connecting fragmented software ecosystems, (iii) going after different personas initially with a narrower offering and an innovating business model, (iv) disrupt existing software incumbents, (v) Creating a new layer of abundance while leveraging scale effects.

Tuesday, Feb. 14th: Ilkka Paananen who is the founder and CEO at Supercell published an annual review of his company. - Supercell

“Supercell’s mission is to create great games that as many people as possible play for years and that are remembered forever.”

“For Supercell to thrive and fulfill our mission, we need to both invent brilliant new games (regularly!) and continuously improve those games for our players (hopefully forever!), making something that already is great even better. Doing just one of those two things is not enough. We want to do both.”

Supercell’s strategy to create new iconic mobile games includes: (i) assembling a small and independent team of experienced developers, (ii) trusting developers’ intuition and passion over data in the early days of the game development, (iii) crafting innovative games instead of copying/upgrading existing games.

“We have launched 5 hit games but we have killed 30+, by my latest count. We haven’t launched a new game globally since Brawl Stars on December 12, 2018. I’m not counting, but 4 years, 1 month, and 3 days seems like too long!”

In 2022, Supercell generated €1.77bn in revenues (6% YoY decline), €632m in EBITDA (14% YoY decline, 36% margin).

Wednesday, Feb. 15th: The European Commission will review Figma’s acquisition by Adobe saying that “the transaction threatens to significantly affect competition in the market for interactive product design and whiteboarding software.” I previously covered the deal in my newsletter arguing that it was an anti-competitive move by Adobe because Adobe XD was loosing the product design market to Figma. The European Commission is the third public body to review the transaction after the DoJ in the US and the Competition and Markets Authority in the UK. - Techcrunch

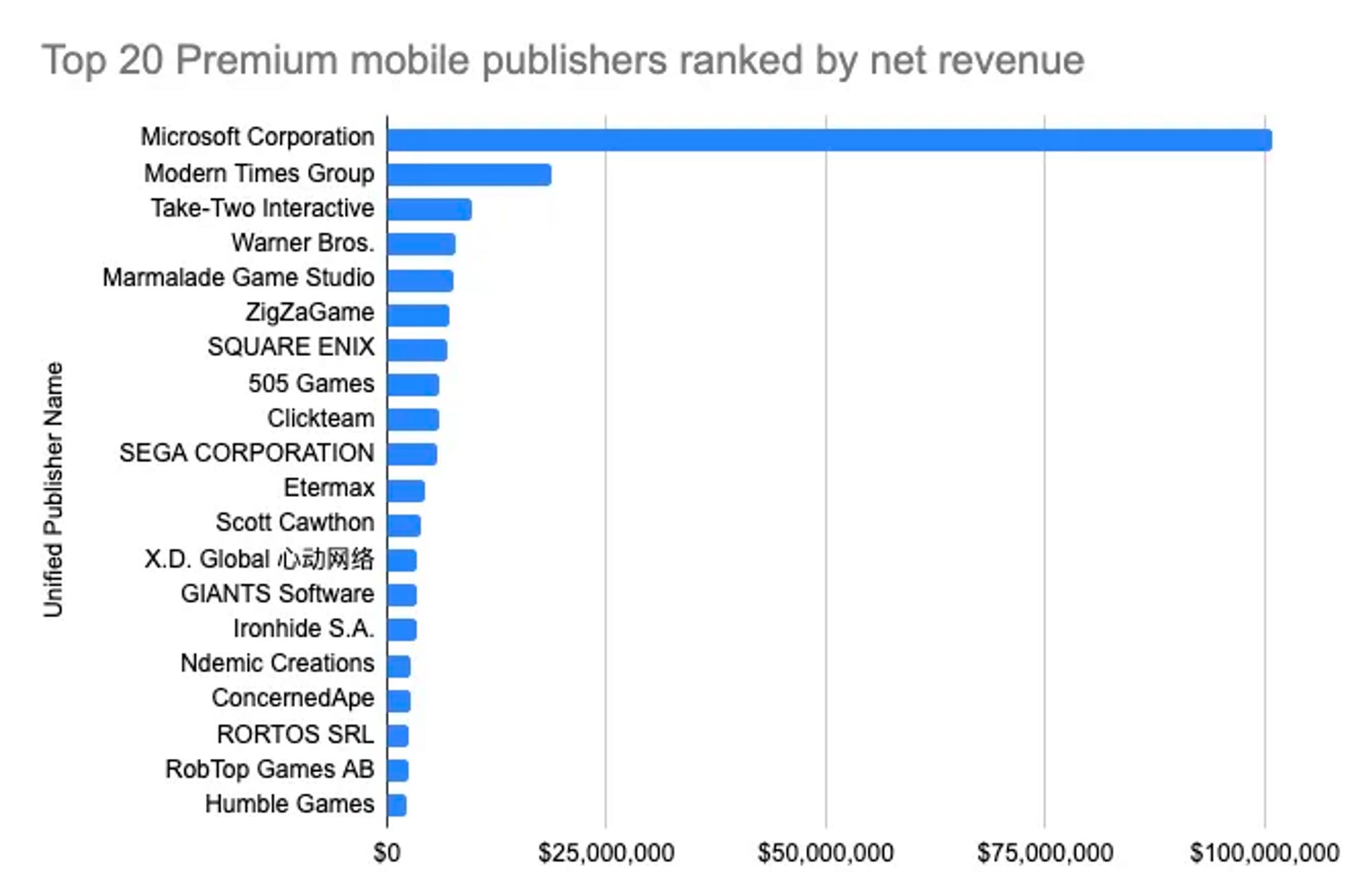

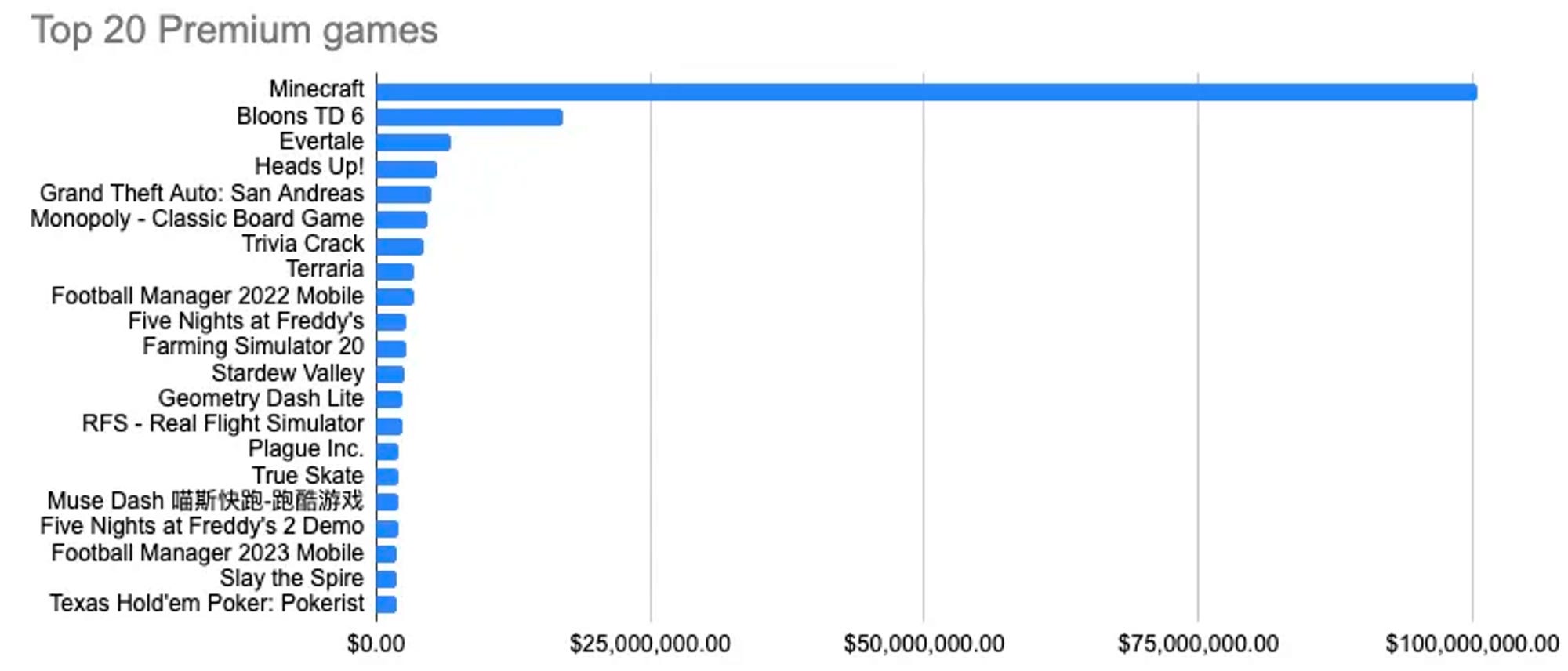

Thursday, Feb. 16th: Jules at Homa launched a newsletter on mobile gaming that you should subscribe to! The first edition is on the death of premium games on mobile which are games that require an upfront payment (e.g. Minecraft, GTA, Football Manager). Jules argues that most premium games are developed by incumbents with strong IPs and that it’s not a great category for emergent mobile gaming studios. - Game Musings

“In 2022, there were 1.2k premium games on mobile. These games represented 53m downloads and $296m revenue in 2022. The Premium segment thus represents 0.3% of mobile games revenue, a very narrow niche overall.”

“Out of the $296m premium game revenues, $100m are from Minecraft’s mobile version, making Microsoft by far the leading player in the segment. 13 Publishers netted over $1m revenue last year from Premium games, none of which are new entrants in the space.”

Friday, Feb. 17th: Speedinvest raised a €3m fund of funds to back emerging GPs. I believe that many other funds will launch a similar program in the coming years. Many partners in top venture funds already invest their personal money as LP into emerging GPs. A fund of funds is a way to scale this behaviour. It’s a great trick to build a differentiated sourcing machine on geographies, sectors and stages in which you lag behind competitors. - Sifted

Saturday, Feb. 18th: Sarah Tavel at Benchmark wrote about how companies should seize window openings opportunities using Pinterest as an example. - Sarah Tavel

“There are moments like this in a company when a window opens -- when stars align and a sense of inevitability starts to take over your company.

“Trust me when I say this: the window will close, so do everything you can to maximize your moment.”

“Yes startups are a marathon, but this is a moment to sprint. Increase your sense of urgency. Raise your hiring bar. Consider pulling forward executive searches. If you haven't recently raised a round on funding, you might want to dust off your deck.”

“The thing about jumping through your window when it opens is that it causes it to stay opened longer. Hiring great people raises the bar internally on execution. Growth sustains if not accelerates. Things start to compound more and more. A window that might be open for a few months can stay opened for several.”

Sunday, Feb. 19th: I listened to a Colossus’ podcast episode with Chris Cerrone who is a partner at Akre Capital on Constellation Software (CSU) which is a Canadian based and publicly listed conglomerate of Vertical Market Software (VMS). - Colossus

Akre Capital invested into CSU because it fits its 3 investment criteria: (i) ability to sustainably generate above average returns on capital thanks to durable competitive advantages, (ii) skilled management team at operating the business and deploying capital, and (iii) opportunity to redeploy excess cash flows at high rates of returns.

“CSU acquires and plans to be the perpetual owner of hundreds of small to medium-sized vertical market software businesses.”

CSU is a decentralised organisation. “CSU extends this ethos of decentralization beyond operations into the realm of capital allocation as well.”

“When Mark [CSU’s cofounder] joined the venture world, he discovered some important shortcomings in that model of investing. It was difficult to focus narrowly enough on a specific industry in order to become a subject-matter expert. The investment returns were erratic and not especially impressive. He had this insight that high-growth businesses often fail to develop into businesses that generate high returns on capital. And the fundamental idea of venture capital is that you're building things that can be sold to other people. And I think that's a very different mindset from building something permanent where you can build a business or relationships that last for a lifetime if you want them to.”

VMS are great businesses because: (i) they are customised to the need of a specific industry making them must have and giving them high switching costs translated to a low annual churn (below 10%), (ii) they are in less competitive markets because they operate in smaller markets than horizontal markets which give them a strong pricing power (annual price increase in the mid to high single digits), (iii) they generate recurring revenues (either subscription or maintenance payments after an initial upfront licence), (iv) they can grow while being extremely capital efficient.

CSU is looking for VMS which “are essential products that fly under the radar”. They should be mission critical but they should cost less than 1% of the revenues of its customers to have both extremely high retention and room to increase prices.

CSU does not have stock based compensation. “Instead, they pay cash bonuses and they require that a significant portion of the after-tax proceeds (75% for executives) be used to purchase common shares on the open market. And then those shares are held in escrow for an average of 4 years.”

CSU’s secret sauce as an acquirer is to combine discipline, data and the preferred acquirer status. On discipline, CSU won’t deploy capital below its hurdle rate (20-30% for small acquisitions, slightly lower for larger acquisitions). On data, CSU owns 1k VMS and has a database of 50k potential targets giving data on what is a top asset and how to improve VMS performance. On the preferred acquirer status, like Berkshire Hathaway, CSU is a permanent owner of the businesses it acquires which is not the case with private equity acquirers.

Monday, Feb. 20th: The Economist wrote about how our relationship to cars has evolved in recent years. - The Economist

“After a century in which the car remade the rich world, making possible everything from suburbs and supermarkets to drive-through restaurants and rush-hour traffic jams, the momentum may be beginning to swing the other way.”

“1 in 5 Americans aged between 20 and 24 does not have a licence, up from just 1 in 12 in 1983.”

Why young adults don’t own a car? First, many use cases have been replaced by the internet (buying online vs. going to the store, streaming vs. going to the cinema). Second, young adults are not as wealthy as previous generations and can’t always afford a car (insecure/poorly paid jobs, decline in home ownership, spending longer time in education). Third, not owning a car is a way to fight against climate change.

Large cities are implementing measures to curb down on car usage. In Olso, most on-street parking spaces have been removed. In New-York, cars are banned from Central Park and certain streets in Manhattan.

“Ms Hidalgo won a second term as mayor in 2020 on a platform that included plans to turn Paris into a “15-minute city”, a fashionable idea in which each arrondissement would have its own shops, sports facilities, schools and the like within a short walk or bike ride.”

Tuesday, Feb. 21st: Techcrunch wrote about the rise of defense tech. - Techcrunch

“The Silicon Valley mentality has returned to its defense roots, embracing the role that venture-funded startups can play in maintaining America’s military dominance and technological supremacy around the world.”

“The U.S. government has never been more willing to work with startups to speed technological development and adoption, a willingness that’s been driven in part by growing tensions with Russia and China.”

The article mentions startups like Anduril (modern defense platform), Hadrian (automated factories for the space and defense industries), Shield AI (AI pilots), Vannevar Labs (platform for autonomous flying systems) and True Anomaly (space military operations).

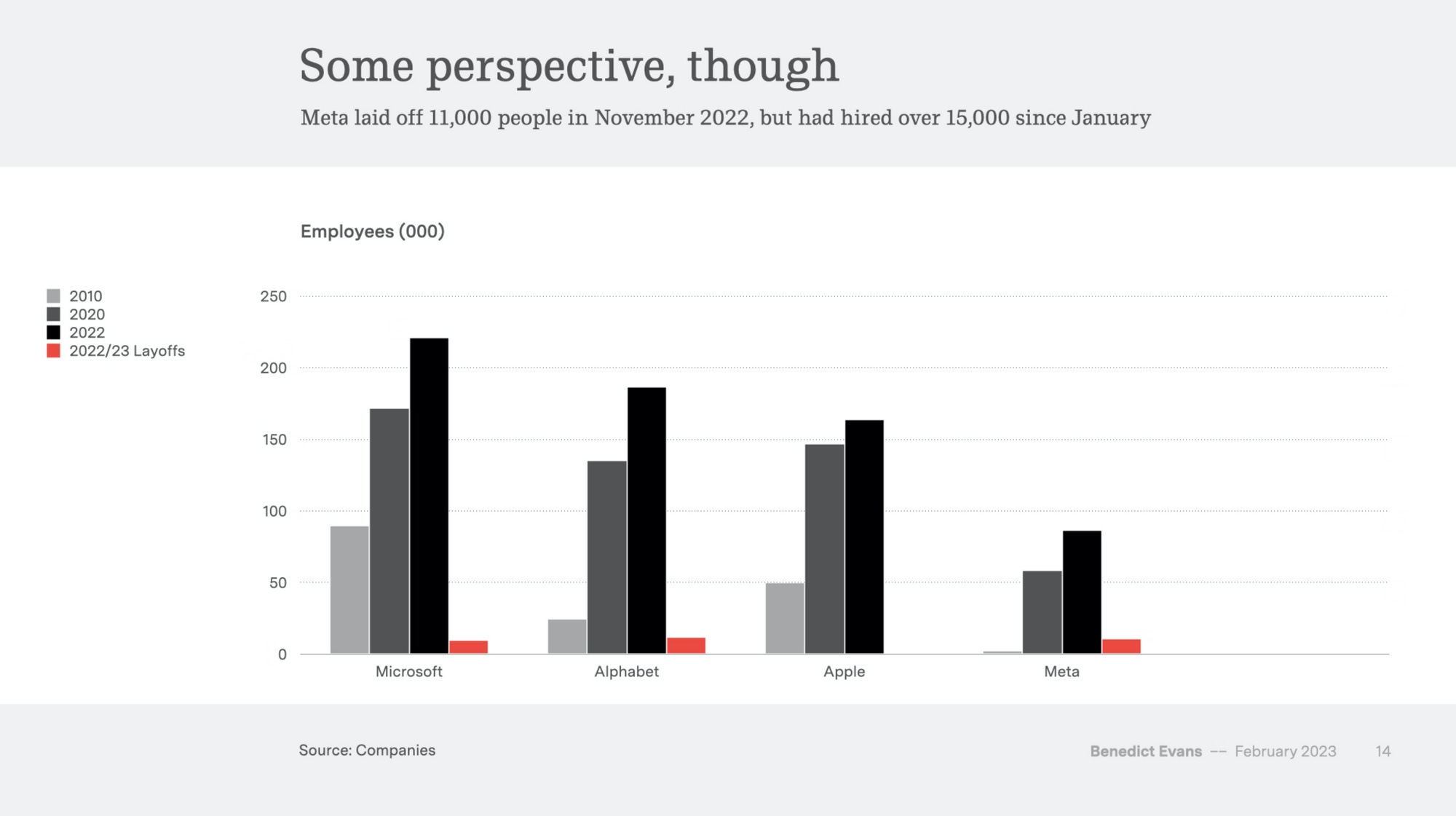

Wednesday, Feb. 22nd: Ben Evans published its annual presentation on tech around 3 key themes which are (i) the end of free money, (ii) the new gatekeepers (GAFAM) and (iii) the hype cycle shift towards generative ML. - Ben Evans

Thursday, Feb. 23rd: My friend Florian published a great introduction to crypto. - Florian Unger

"One of the reasons why Crypto/Web3 is difficult to understand is because the average user cannot really see its impact. While Web2 was primarily a front-end revolution, making it easier for users to interact with each others (read and write on the Web, i.e.: read the news, write your blog), Web3 is mostly defined as a back-end revolution (read news, write your blog, own your data/tokens/digital property rights).”

Crypto give citizens in non/partly free countries access to institutions we have in the Western world like (i) strong property rights, (ii) free speech, (iii) separation between the money and the State.

In recent years, crypto saw several technological breakthroughs: (i) eigenlayer which “allows Ethereum stakers to secure additional middleware in the ecosystem with their economic power”, (ii) the merge helping Ethereum to move from a proof of work to a proof of stake consensus mechanism, (iii) account abstraction, (iv) modular blockchains outsourcing core functions of the blockchain (consensus/settlement, execution, data availability) to other blockchains, (v) scaling solutions.

“It is clear for us that Crypto is the next logical step of the evolution to “open-source” the end-to-end tech stack. We believe that due to its tech stack, Crypto will not only “open-source” data but will revolutionize the internet as we know it. This will lead to permissionless innovation, better products and economic freedom.”

Friday, Feb. 24th: Nathan Baschez shared his learnings on writing on the Internet. - Every

“Most people read deep non-fiction writing in order to cultivate an obsession.” “A better (and more fun) strategy is to work unusually hard to cultivate your own obsessions. Run experiments! Do research! Try things! And, of course, write about it. When you’re pursuing your own curiosity, it matters less if others immediately care.”

“To sharpen your angles, ask yourself early in the writing process what the central question is. Once you can frame this, the rest of the piece becomes much easier to write.”

Ask for feedback from professional editors and readers in your target audience.

Saturday, Feb. 25th: The Atlantic wrote about the decreasing trust within our societies. - The Atlantic

“Trust is to capitalism what alcohol is to wedding receptions: a social lubricant. In low-trust societies (Russia, southern Italy), economic growth is constrained.” Trust into institutions (states, churches) is decreasing but also trust between individuals at work and in their private life.

“The economists Paul Zak and Stephen Knack found, in a study published in 1998, that a 15% bump in a nation’s belief that most people can be trusted adds a full percentage point to economic growth each year.”

“Trust is about two things: competence (is this person going to deliver quality work?) and character (is this a person of integrity?).”

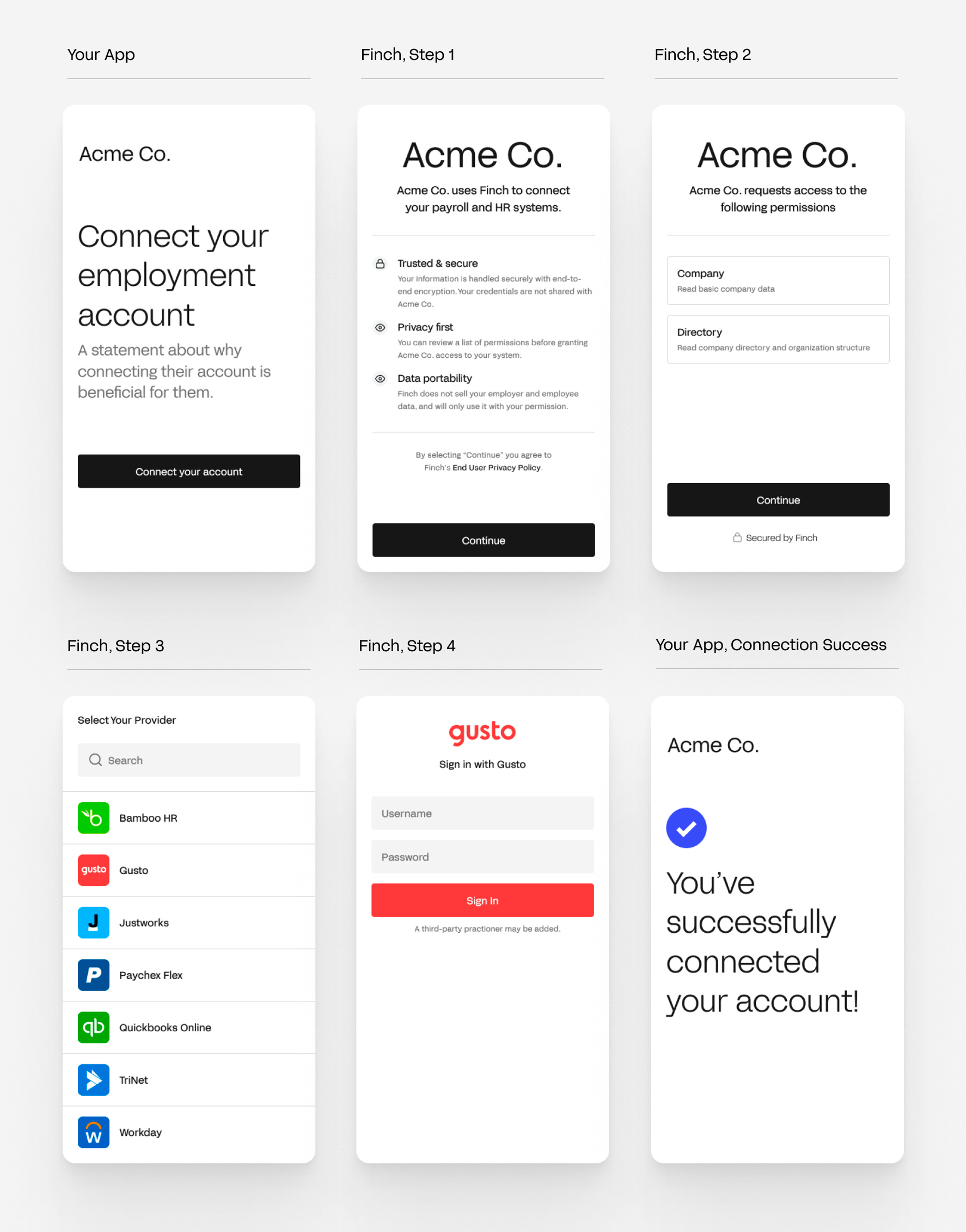

Sunday, Feb. 26th: US-based payroll API provider Finch raised a $40m series B with General Catalyst and Menlo. It offers a unified API to access in a read or write mode to 200 payroll systems and HR management systems. Finch has grown revenues 12x since its last round in Jun. 2022 and 2m employees leveraged its platform. It will use the funding to connect to more systems, to expand to other verticals beyond payroll, to grow its product team and to expand internationally (Canada, UK, Europe). - VentureBeat, Finch, Techcrunch

“Over 580M U.S. employment records and $15T of funds are processed across 20,000 employment data systems, including payroll, HRIS, benefits administration, and others. Moreover, the ecosystem lacks necessary connectivity, with records mainly passed via manual data entry, SFTP, and emails filled with sensitive information.”

Monday, Feb. 27th: Gokul Rajaram wrote about monitoring the second important metric beyond your north star metric to ensure that you’re building a long term sustainable business. - Gokul Rajaram

“The second most important metric for every company is a check metric on the North Star Metric (NSM). It’s a metric that constrains the NSM and ensures that the NSM grows in a way that is sustainable and creates long-term value.”

“Every good company has a NSM. But if you want to build a company where people’s behaviors and actions are aligned with long-term value, don’t stop with the NSM. Put some more thought and add a check metric to your company’s top level goals. You won’t regret it, and your company’s stakeholders will thank you for it.

Pairing a north star metric with a check metric: (i) orders and gross profit for marketplaces, (ii) DAUs and time spent for social medias.

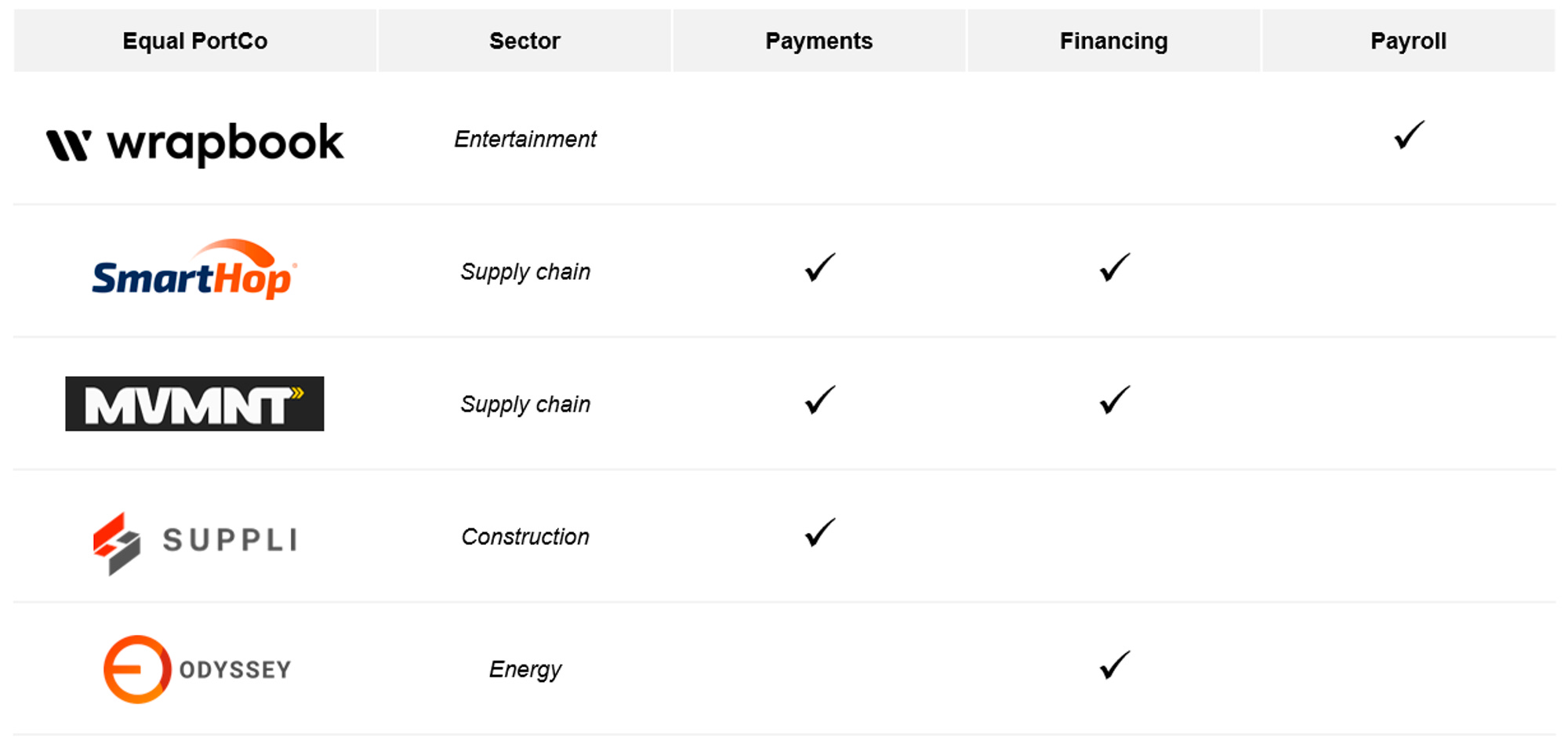

Tuesday, Feb. 28th: Richard Kerby who is general partner at Equal Ventures wrote about vertical fintechs. - Equal Ventures

“Marrying vertical software and financial services can be extremely powerful because of the significant increase in market size that occurs from combining these two product offerings and business models. Workflow software can be quite sticky, but there is always only so much that a business will be willing to pay for software. Conversely, financial services (payments, take rates, insurance, lending, etc.) can be lucrative ways to monetise but tends to have challenges regarding retention.”

“Providing a customer with workflow improvement while also bundling one or more financial services products enables you to supplement SaaS revenue with fintech or even partially or entirely subsidise SaaS revenue with financial services revenue.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋