📖 Venture Chronicles - December 2024

Overlooked #189

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of December.

Happy New Year! As we step into 2025, I want to thank you for being part of this journey. This year will be an exciting one for the newsletter, with many great projects in store - starting with my annual report on the French tech ecosystem that will drop mid-January!

Sunday, Dec. 1st: Jason Lemkin recently interviewed Dave Kellogg (Balderton) to discuss his predictions for the enterprise technology landscape in 2025. - Jason Lemkin

2025 could be the year when companies turn to IPOs as a means of generate liquidity for the venture ecosystem, even if it means going public at valuations below their previous peaks.

What metrics do private equity (PE) funds focus on?

Profitability: PE funds typically avoid turnaround acquisitions, so achieving profitability independently is essential to avoid significant valuation discounts at exit.

Growth and scale: $30m in ARR with 30% YoY.

Good retention: NRR around 100%

Reasonable previous valuation.

PE funds could pay 3-10x ARR multiples depending on the growth profile and the strategic nature of the acquired business (e.g. a PE fund could pay a premium if it is rolling up different strategic assets into a single platform).

AI is unlocking additional budgets for companies. According to Battery’s latest tech spending analysis, 59% of organizations are increasing budgets to experiment with AI. The data category is booming as companies prepare infrastructure for AI implementation. Many functions are also reallocating budgets toward AI investments rather than hiring more staff.

In customer support, there is already some push back from customers to replace humans with per outcome pricing leveraging AI.

When growth slows, the answer is not to milk the base but to find solutions to reignite new logos’ growth (at least, 20% YoY). Otherwise, you optimise to hit your numbers for the quarter but not to win in the long term. Expansion ARR should be maximum 30% of new ARR.

What do you do as a venture backed business growing less than 25% YoY? As a founder, you want to avoid becoming a zombie because it’s the worst situation - you cannot innovate, your employees are leaving, you’re worth nothing, etc. If you have a credible growth re-acceleration, execute on it. Otherwise, go to cash flow generation mode.

In terms of pricing, except you’re a price model disruptor, price like everyone in your category. In AI, the standard is not there but you should try to price the way the standard will be in two year and not try to be super innovative.

Value is the upper hand of your pricing and alternatives are the lower hand of your pricing. If you’re too far from your competitors’ prices, you will lose.

It’s not great to drive NRR with price increases. You need to add products and deliver a strong additional value in order to drive NRR.

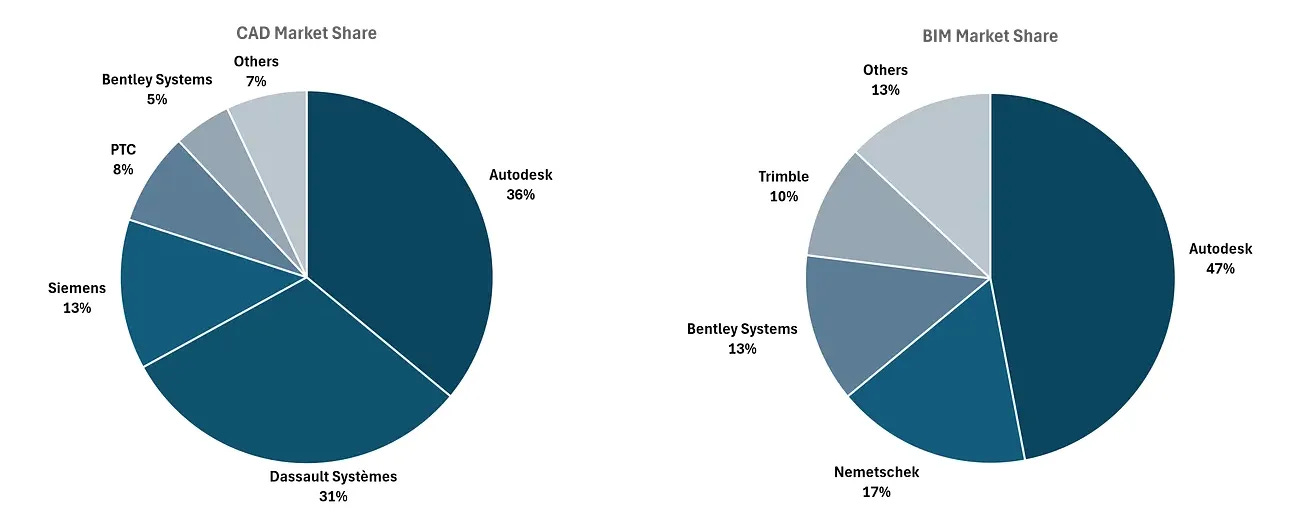

Monday, Dec. 2nd: I read a post on disrupting Autodesk’s monopoly in industrial and architectural design. - AEC Tech

“Not only were they pioneers in CAD, but they were also the first to market with BIM. In fact, the term BIM was popularized by Autodesk; they coined it and marketed it alongside their BIM solution, Revit.”

“Another reason for Autodesk's firm grip on the industry is the two-sided marketplace they've developed between engineers/architects and companies. The more architects who are proficient in Revit, the more companies adopt Revit, and vice versa. This network effect compels all parties to adopt the solution. How did they ensure architects are trained in Revit early-on? By providing free licenses to architectural schools, so that students graduate already fluent in Revit. As these new professionals enter the workforce, they naturally expect to use the software, prompting employers to embrace it—cementing Revit as the industry standard.”

“This lucrative cash cow has allowed Autodesk to dominate the acquisition space. Any potential disruptor of AutoCAD or Revit has been swiftly acquired and integrated. They purchased Softdesk in 1997, Revit in 2002 (yes, Revit was an acquisition), Spacemaker AI in 2020, and over 80 others across 30 years.”

Tuesday, Dec. 3rd: I read an old deck on Netflix’s culture. - Reed Hastings

“We believe that what makes a fantastic workplace isn’t a great office or free meals and massages — although we have some nice perks. It’s the people. Imagine working alongside stunning colleagues who are great at what they do, and even better at working together.”

“We’re a team, not a family. We’re like a pro sports team, not a kid’s recreational team.”

“To ensure they have the right player at every position, we ask them to apply what we call the “keeper test”1 — asking “if X wanted to leave, would I fight to keep them?” Or “knowing everything I know today, would I hire X again?” If the answer is no, we believe it’s fairer to everyone to part ways quickly.”

Wednesday, Dec. 4th: Britannica is reinventing its business with Gen. AI. Originally a publisher of physical encyclopedias, the company transitioned to a fully online model in 2012. Now, it is considering going public with a $1bn valuation. Britannica attracts 7bn page views annually, has doubled its revenues to $100m in just two years, and operates with a 45% operating margin. - NYT

“Britannica now uses A.I. in creating, fact-checking and translating content for its products, including the online Britannica encyclopedia.”

“It also created a Britannica chatbot that draws on its online encyclopedia’s stores of information.”

“The company has more projects powered by generative A.I. in the pipeline: an English-language tutoring software that will use the technology to power avatars and customize lessons for each student, a program to help teachers create lesson plans, and a revamped thesaurus for the Merriam-Webster website that can handle phrases, not just words.”

Thursday, Dec. 5th: Scott Belsky (Chief Strategy Officer at Adobe) wrote about the rise of luxury software. - Implications

“I’m not sure what it is about culture and human tendencies, but we tend to crave scarcity, craft, and story in whatever categories become commoditized.”

“But noticeably missing, beyond the shine of Apple’s devices, is a burgeoning industry of luxury software. While infinitely replicated bits are the ultimate commodity, software increasingly defines our identity these days. I anticipate an era of luxury software ahead of us that upgrades our work and life.”

“In a world where software seems increasingly commoditized with a plethora of options across verticals (not to mention the ability to use AI to simply replicate software instantly), I see signs of “luxury software” emerging for the more discerning customer.”

“Already, in the consumer productivity space, we’re starting to see “luxury” email clients, calendars, browsers, and search engines emerge. While all of these capabilities are freely accessible to consumers and rather commoditized, companies like Superhuman for email, Cron (now Notion) for calendars, Arc for web browsing, and Perplexity for search have emerged as higher-end alternatives that also carry some degree of status for their users.”

Friday, Dec. 6th: European businesses face challenges such as political chaos, economic disparities, and lagging AI success. However, strengths in industries like pharmaceuticals, aviation, and industrials, plus strategic R&D and patient shareholders, highlight resilience. - The Economist

“European business can seem just as dysfunctional. In the past couple of weeks it has been a tale of bankruptcy (of Northvolt, a would-be battery champion), labour unrest (at Volkswagen, the continent’s biggest carmaker, where nearly 100,000 workers downed tools on December 3rd) and CEO defenestration (at Stellantis, a rival whose biggest shareholder).”

“The entire STOXX 600 index of large European enterprises is worth a third less than America’s “magnificent seven” technology giants. Shares of firms in the S&P 500, its transatlantic equivalent, trade at 23 times future earnings, far above the 14 or so eked out by STOXX constituents.”

“Closer inspection reveals pockets of European corporate strength, some more surprising than others.”

“Europe’s drugmakers are collectively worth more than American ones and boast twice the return on capital. Novo Nordisk of Denmark launched Ozempic before Eli Lilly began selling its weight-loss drug. Europe lacks an Nvidia, but the $3.5trn AI-chip designer would not get far without ASML, a Dutch firm whose machines etch Nvidia’s blueprints onto silicon. Ryanair and other European airlines fly rings around American carriers in terms of profitability. And nobody does posh better than the French (think LVMH) and Italians (Ferrari, also controlled by Exor).”

“European companies have two other things going for them. Many have patient shareholders, whose interests are aligned with businesses’ long-term success. […] The other advantage is low expectations.”

Saturday, Dec. 7th: Visma is considering to go public in London, Amsterdam or Oslo. Hg took private Visma in 2006 for $500m. Today, Visma is worth €19bn. Hg is still the majority shareholder defying the traditional private-equity model where most assets are sold after 3-5 years. - FT

“Hg has built up Visma over an uniquely long timeframe by facilitating private valuation stake sales roughly every three years, whereby it can transfer the company between its own funds and bring in outside investors to allow existing shareholders to sell.”

“Several Hg funds have owned stakes in Visma over the years, and today Hg and its co-investors own about 70% of the company. Other shareholders include the likes of Singapore wealth fund GIC and US private equity group TPG.”

Sunday, Dec. 8th: To be successful in venture investing, you either “believe harder” or “believe differently.” “Believe harder” entails paying premium for widely acknowledged winners, exemplified by Yuri’s Facebook investment. It excels at scale but risks overvaluation. “Believe differently” involves backing unconventional ideas undervalued by others. It’s riskier but intellectually rewarding. - Sam Lessin

“I have a strong personal bias towards the latter, but both are totally valid (and TBH the 'believe harder' approach is a better business model as a GP).”

““Believe differently” deals are intellectually and emotionally the deals I am proud of / like doing... egotistically I think it is harder, more interesting, and makes me feel like capital is more meaningful (because you are supplying dollars that might otherwise not happen).”

Monday, Dec. 9th: Charles Hudson at Precursor Capital wrote about the potential paths for the early stage venture capital landscape. - Charles Hudson

“Small and large venture funds might be in the same industry but not the same business in the future. With their larger fund sizes, multi-stage firms need massive $5-10B+ exits to generate meaningful returns. In contrast, seed-only firms can generate meaningful returns with more modest $1B+ exits.”

“What portion of the returns in seed investing will come from the proven, repeat founders who the multi-stage funds are likely to attract. If you believe 75% or more of the future returns in seed will come from this population, there is a strong argument that the multi-stage funds will dominate seed. The remaining alpha available to seed specialist firms is too small to support the number of seed-focused firms in the market today.”

Tuesday, Dec. 10th: I read a initiation coverage broker note on OneStream.

OneStream has built a next-gen SaaS leader in financial consolidation and enterprise performance management ($7bn market), leveraging its unique architecture for financial consolidation and the founders’ expertise from developing Hyperion’s dominant on-prem EPM solutions (60% market share).

OneStream has significant opportunities to capture share from on-prem incumbents transitioning to the cloud, driven by end-of-life catalysts later this decade (~$5B TAM). It can lead with its core financial close product and expand into adjacent areas like financial planning and operational planning, supported by its data platform and AI capabilities.

“The core debate around OneStream will likely focus on sustaining growth in its financial consolidation solution and maintaining strong new logo acquisition (~70% of new ARR). This includes capturing the legacy EPM base from Oracle, SAP, IBM, and others, while assessing how sticky incumbents’ revenues remain as they transition to the cloud. Additionally, the discussion will explore OneStream’s ability to expand from financial consolidation into becoming the financial data system of record, driving adjacent use cases like ESG, narrative reporting, and planning, to support NRR (118% in 1Q24).”

Wednesday, Dec. 11th: I listened to an Invest Like the Best’s podcast episode on AI with Chetan Puttagunta and Modest Proposal. - Colossus

“All the labs have hit some kind of plateauing effect on how we perceive scaling for the last two years, which was specifically in the pre-training world.” “The synthetic data as generated by the LLMs themselves are not enabling the scaling in pre-training to continue.” “We're now shifting to a new paradigm called test-time compute / reasoning.” “You actually ask the LLM to look at the problem, come up with a set of potential solutions to it, pursue multiple solutions in parallel and come back to the user with the best one.”

“Everyone knows the Mag 7 represent a larger percent of the S&P 500 today. I think thematically AI has permeated far broader into industrials, into utilities and really makes up, I would argue, somewhere between 40 and 45% of the market cap as a direct play on this.”

“In the pre-training world you were going to spend 20, 30, $40 billion on CapEx, train the model over 9 to 12 months, do post-training, then roll it out, then hope to generate revenue off of that in inference. In a test time compute scaling world you are now aligning your expenditures with the underlying usage of the model. So just from a pure efficiency and scalability on a financial side, this is much, much better for the hyperscalers.”

“The venture capital model has been could you get together a team of extraordinary people, have a technology breakthrough, be capital-light, and jump way ahead of incumbents very quickly and then somehow get a distribution foothold and go. At the model layer for the last two years that certainly didn't seem like it was possible. And literally in the last six, eight weeks that's definitively changed.”

“If you just take a step back and think about what historically cloud computing was, it was providing a set of tooling to developers and builders. AWS first articulated this vision. Amazon’s view clearly has been that LLMs are just another tool, that generative AI is another tool that they can provide their enterprise customers and their developer customers to build the next generation of products.”

“As an early stage fund with $500 million of capital, we're trying to make 30 investments every fund cycle, a billion dollar training run is essentially you're committing two funds to do one training run that may or may not work. So that's an extraordinarily capital intensive business.”

“A lot of our efforts starting in summer 2022 when OpenAI’s APIs were released was to just find entrepreneurs that were thinking about leveraging these APIs to go after the application layer and really start thinking about what are applications that simply could not exist before this current wave of AI.”

“You can just go through every single large SaaS market and go after it with an application layer investment and start to really think about what's now possible that wasn't possible two, three, four years ago.”

“I personally hope for AI to continue for a really long time. You need big disruptions as a venture investor to unlock distribution. If you just look at what happened in the Internet or in the mobile and where value accrued, value predominantly accrued at the application layer in those two waves. Now obviously our hypothesis was that this layer again was going to be very receptive to distribution unlock because of innovation at the AI application layer.”

“Application vendors that have come out with production AI applications for both consumer and for enterprise are unlocking distribution in ways that was frankly not possible in the world of SaaS or prosumer SaaS or whatever.”

“What AI applications are presenting is not a 5% improvement over an existing SaaS solution. It's about eliminating significant amounts of software spend and human capital spend. Your 10x traditional ROI definition of software is easily justified and people get it within 30 minutes”

“Now the CIO says something like, "Let's put this in as quickly as possible. We're going to run a 30-day pilot. The minute that's successful, we're signing a contract and we're deploying right away.” These are things like three, four years ago in SaaS was just completely out of the realm of possibility.”

“We've clearly bet and anticipated there's dramatic innovation and distribution unlock happening at the application layer. We've seen that happen already.”

“AI products require a total rethinking from first principles on how these things are architected. You need unified data layers, you need new infrastructure, you need new UI and all this kind of stuff. And it's clear that the startups are significantly advantaged against incumbent software vendors. And it's not that the incumbent software vendors are standing still, it's just that innovator's dilemma in enterprise software is playing out much more aggressively in front of our eyes today than it is in consumer.”

“If you're in any one of these AI application companies, it's like more of these companies are supply-constrained than demand-constrained.”

Thursday, Dec. 12th: In emerging countries, WhatsApp has become much more than a messaging app facilitating commerce, new social interactions, and promoting news. - Rest of World

"WhatsApp is among Nigeria’s most popular social media platforms — used by 51 million people in the country — and it is by far the most influential.”

“With over 2 billion users, WhatsApp is not just the most popular messaging app in the world — it’s a digital lifeline. In many parts of the world, WhatsApp is synonymous with the internet itself. For Nigerian content creators, Brazilian shopkeepers, and Indian aunties, it is often the only app they need. On WhatsApp, you can chat with friends and family, attend school, run a business, catch up on the news, shop, and even bank. Increasingly, it’s where people watch TV, book medical appointments, and arrange dates.”

“In India, WhatsApp has 400 million monthly active users; a 2022 study by the Reuters Institute at the University of Oxford showed that more than half the population trusted WhatsApp as a news source.”

“WhatsApp, originally developed as a lightweight tool for sending simple texts to friends, has by now become something infinitely bigger, more complicated, and more surprising.”

“Brazil is WhatsApp’s largest market outside of Asia, with over 56% of the country’s 212 million people using the app every month.”

“In Indonesia, the national football team uses the Channels feature, a one-way broadcast of text, links, and images, to share match updates and exclusive behind-the-scenes content. Within a short time, they amassed 2.3 million followers, with each post flooded with hundreds of emojis from enthusiastic fans.”

Friday, Dec. 13th: Hitachi wrote a blogpost on AI transforming engineering by improving design, simulation, and optimization processes. - Hitachi

"Computer-Aided Design (CAD), Engineering (CAE), and Manufacturing (CAM) enable modern engineering through digital design, virtual testing, and designs being translated into manufacturable outputs. Together, they streamline the journey from concept to production and allow the realization of engineering masterpieces such as high-speed trains, wind turbines, and innovative data centre thermal management systems. Technological advancements enable earlier design optimization and reduce reliance on costly prototypes (time and material waste).”

"We believe there to be four main areas that will emerge and/or benefit: (i) AI-powered design & optimization, (ii) physics & engineering simulation, (iii) high-performance computing (HPC), (iv) next generation Product Lifecycle Management (PLM).”

“Unlike traditional methods, which start with an engineer’s model, Generative Design uses AI to explore parameters and produce multiple compliant solutions simultaneously, leveraging vast amounts of data. Thus, AI-driven Generative Design allows engineers to iterate on numerous designs simultaneously. For instance, Airbus uses Generative Design to create aircraft partitions, evaluating thousands of design options simultaneously to achieve optimal weight reduction and structural performance.”

“The CAE market is dominated by established players like Autodesk, Dassault, Siemens, and PTC, who control much of the market through deeply embedded tools and customer relationships.”

“Additionally, startups focusing on niche applications — whether Multiphysics Simulations or fully automated design tools — stand the best chance of gaining traction by partnering with incumbents and offering next-generation capabilities. These startups can enhance existing workflows and bring new value to their clients.”

Saturday, Dec. 14th: Carta published its Q3-2024’s market update on venture. - Carta

"In the aftermath of the remarkable pandemic bull run of 2021 and early 2022, the venture market has settled into a new normal. For nine straight quarters now, private startups on Carta have raised somewhere between 1,250 and 1,650 new rounds and brought in between $15.7bn and $23.8bn in new capital. After the roller-coaster ride of the preceding two years, it’s been a notable stretch of high-level consistency.”

“More than 20% of rounds closed last quarter were down rounds. The frequency of down rounds began to climb in late 2022, and it’s remained historically high ever since.”

“M&A activity is increasing: Startups on Carta were the target of 170 M&A transactions during Q3, the highest quarterly figure in more than two years.”

Sunday, Dec. 15th: Sarah Drinkwater at Common Magic shared fundraising advice for emerging GPs. - Sarah Drinkwater

“Fundraising in 2023/2024 was so hilariously hard you have to start naive; otherwise you would not do it.”

“Knowing your strengths and weaknesses, you can build out your materials (the deck that exists to get you meetings, and the data room for interested parties) in a way that emphasizes assets and tries to anticipate known risks and open questions.”

“It’s a contrarian move to say yes to a first fund, especially in this market, and it’s an emotional decision more than it is a logical one.”

“There are no shortcuts in raising a fund — you can’t go round it so you have to go through it.”

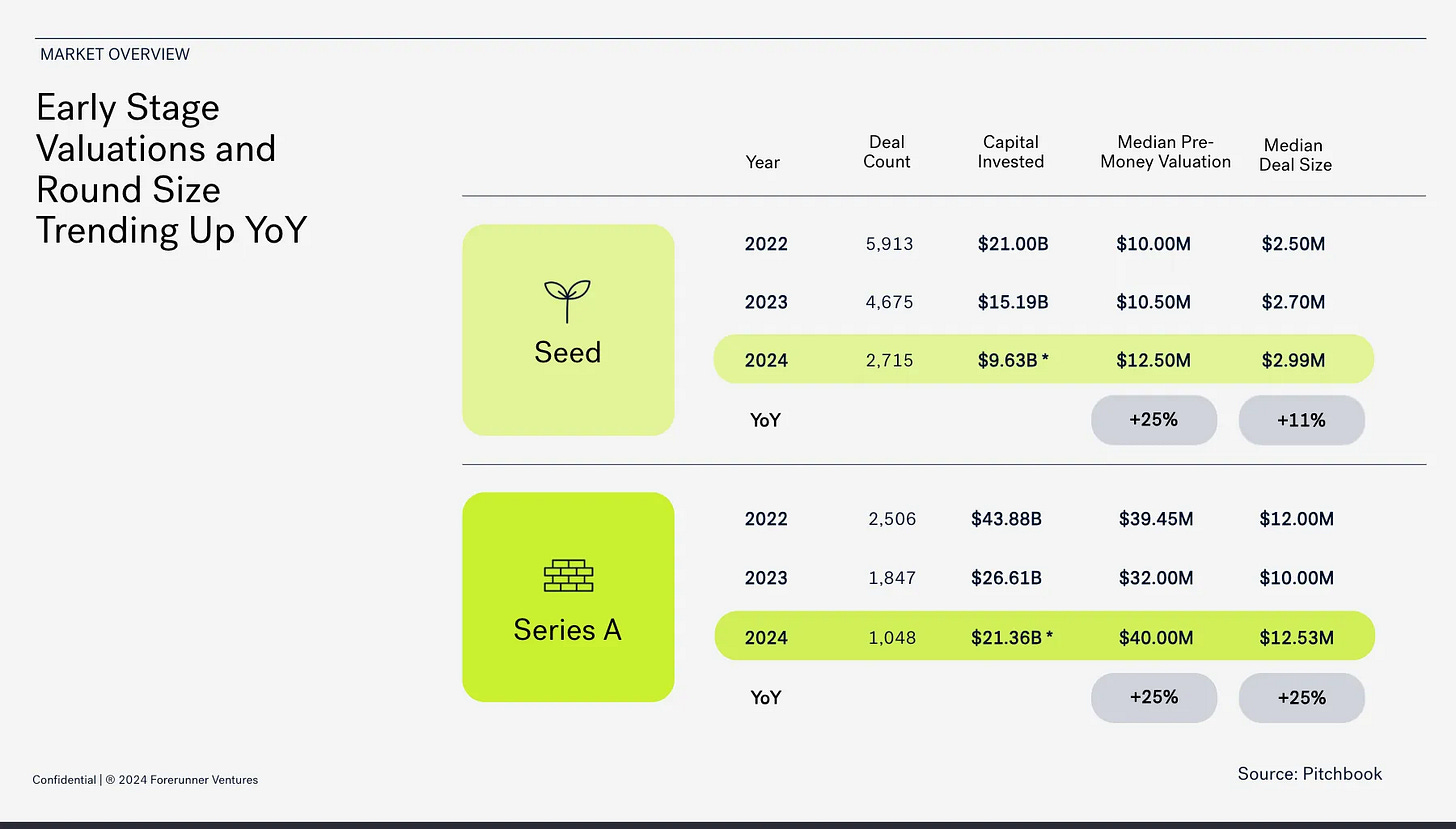

Monday, Dec. 16th: Forerunner published a presentation it shared with its LPs on the early stage venture market. - Forerunner

“VC funding is still off the 2021 peak, but ahead of levels 5 years ago — and 5x the market 10 years ago. In our view, this correction feels balanced.”

“This year will match or slightly beat 2023 in terms of VC dollars invested, but with lower deal count. This relates to AI companies fetching higher valuations and the companies raising successfully having stronger unit economics (“a flight to quality”).”

“This year started with high hopes for a breakout IPO year. Now, that's a 2025 topic. There have been some offerings this year that were well-received, at least initially. In terms of after-market performance, Tempus and Reddit are the standouts.”

“Most of the emerging consumer AI solutions of today have gained traction because they optimize around what models already do inherently well. This next chapter will be led by companies that apply these advantages in less/non-obvious ways to meet the consumer where they need it most.”

“Today, we see AI opportunities falling into three categories:

AI-Boosted: refers to essentially most companies. Companies working smarter, not harder, with AI and benefitting from real efficiency gains.

AI-Enabled: companies that are now uniquely possible with AI, such as Duckbill, Daydream, Juni, Alma, and Topline Pro. This really is our sweet spot.

AI-Led: where LLMs live, but it’s more than that — it’s the enabling technologies that make LLMs useable and actionable.”

Tuesday, Dec. 17th: Bowery interviewed Jared Sleeper, partner at Avenir, on vertical SaaS. - Bowery

“I think the v1.0 vertical SaaS businesses fall into two buckets and there are two ways I have seen them succeed.

One path is that they built incredibly complicated technical tools for creators or engineering specialists - many of the more under-the-radar companies like Autodesk, PTC, Dassault Systems, Bentley Systems, Aspen Technologies, etc. would fall into this bucket. Many of these are multi-billion dollar companies today.

The second path is where companies built software to solve a key problem in their industry. Examples of this approach include Veeva tackling the selling problem in pharmaceuticals, Guidewire solving for insurance workflows, Shopify solving the storefront problem, Toast solving the POS problem, and so on. These companies became the de facto drivers of innovation for their category.”

“When we think about vertical SaaS startups, it is important to remember that there's nothing inherently magical about vertical SaaS - the success has come from either building a tool that is incredibly complicated and hard to replicate and entrenched or from building a core platform that can own a control point from which you go out and add additional innovation over time.”

“In banking software, companies like Ellie Mae discovered that the control point for mortgage origination was sharing data across vendors.”

“If you are a software company and your new logos are not at least flat over time, it is very hard to maintain compounding exponential growth and the model starts to break.”

Wednesday, Dec. 18th: Fabrice Grinda shared a presentation on recent marketplaces’ trends. - Fabrice Grinda

“Cross border commerce is finally becoming a reality. Vinted is operating across Europe. What they do is they take their listings in some countries, auto translate them, sell them in other countries. When you are having a chat with a buyer seller, it’s translated automatically. They have integrated payments and shipping. It’s the first true international cross border C2C marketplace.”

“In B2B marketplaces, there is an ownership transition where younger generations would much rather order an online marketplaces than do RFQs.”

For a B2B marketplace, you want both a high average order value and high frequency of purchase.

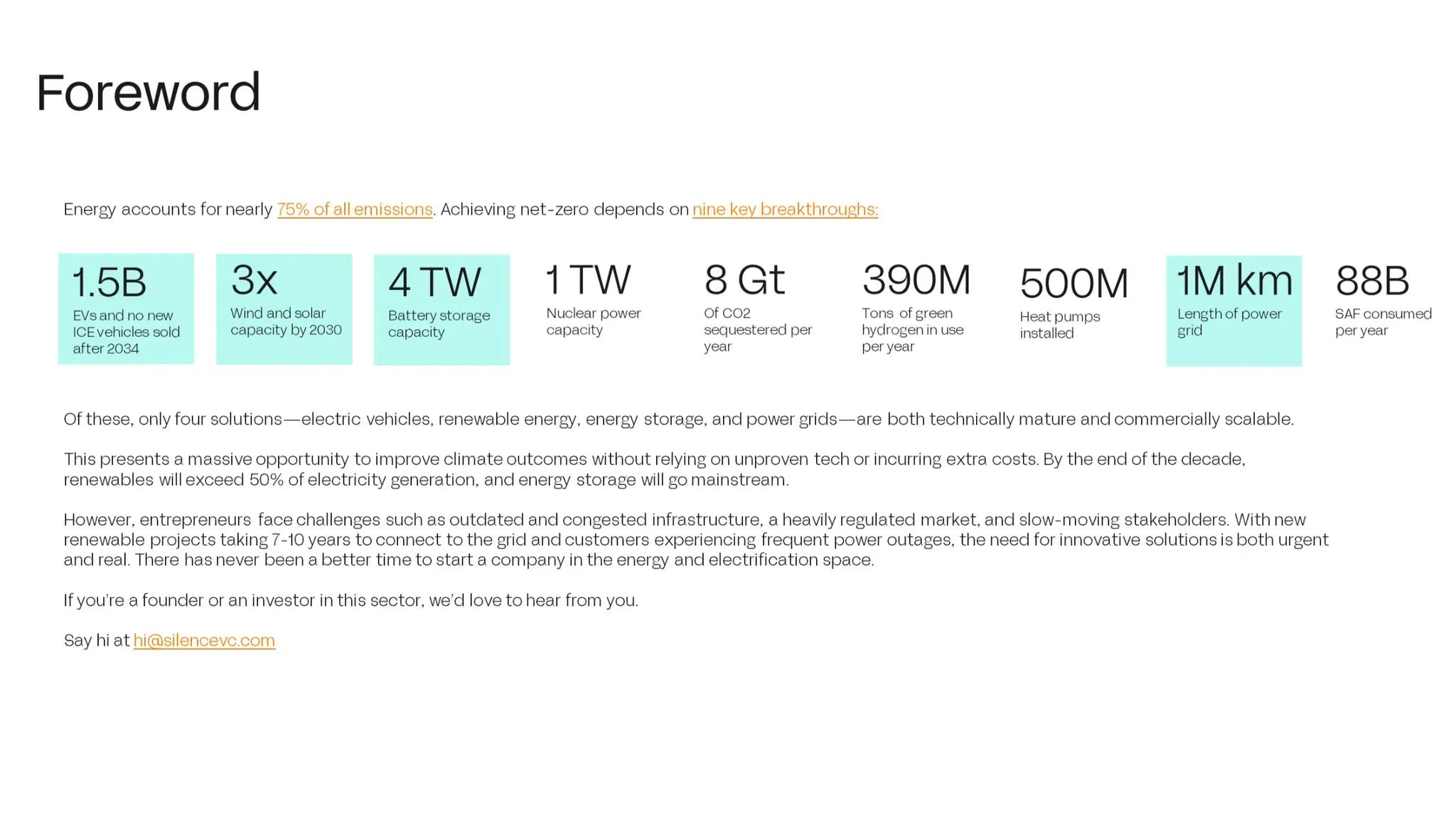

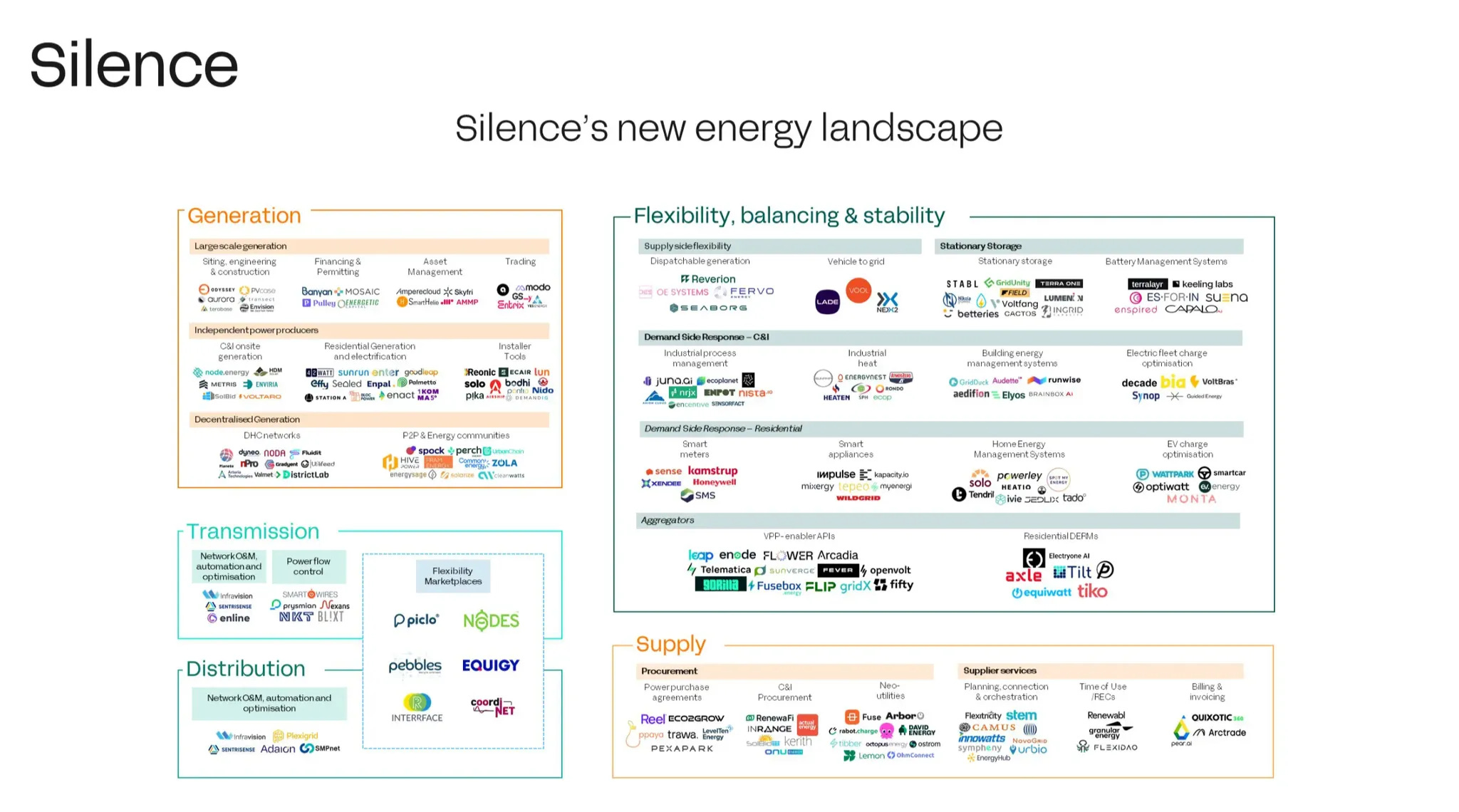

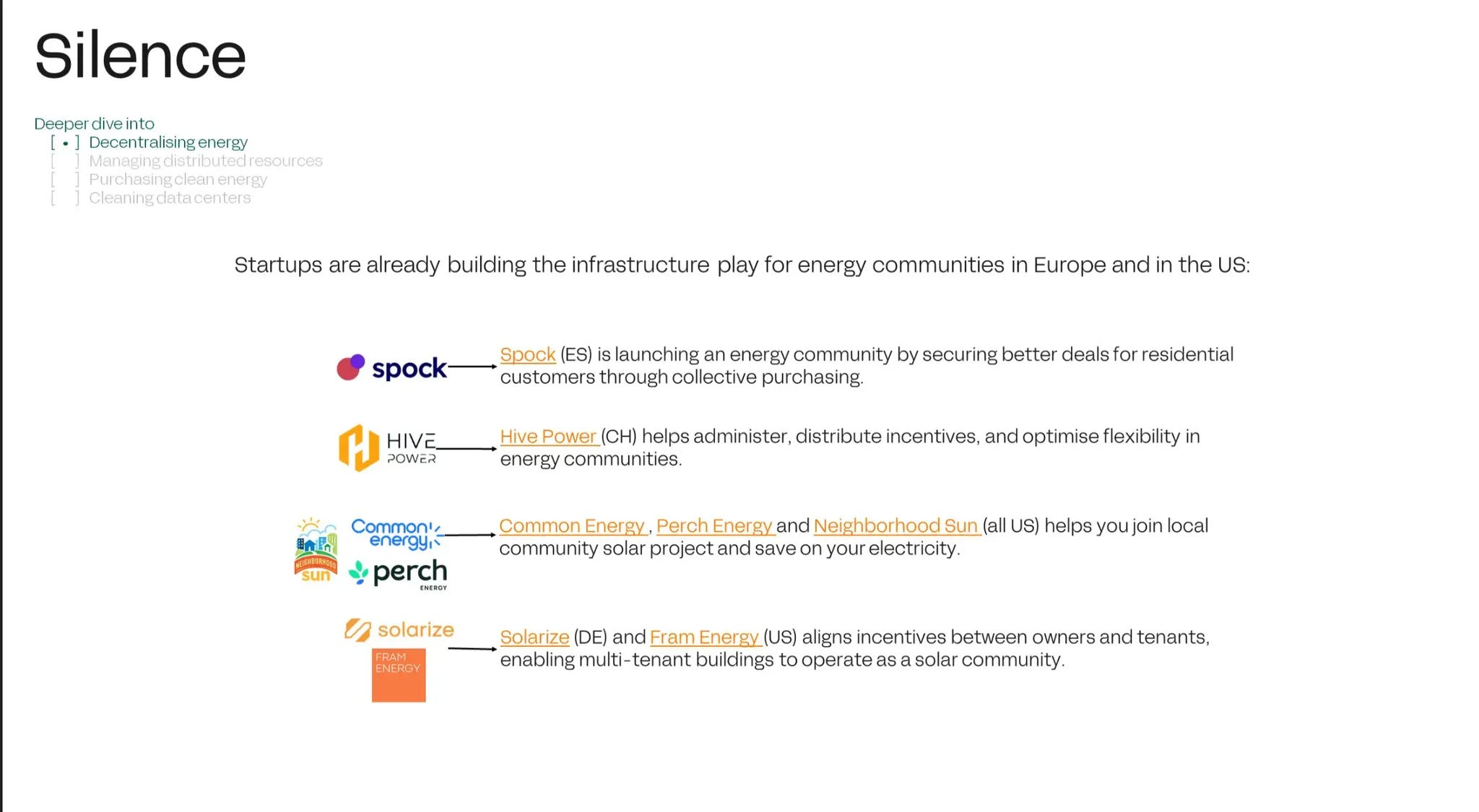

Thursday, Dec. 19th: Silence published its investment thesis in the energy sector. - Silence

Friday, Dec. 20th: General Catalyst invested $200m into Verkada at a $4.5bn valuation. Founded in 2016, Verkada provides internet-connected security products (e.g. cameras with facial recognition, alarm systems & intercoms) mostly to police departments. It raised $650m to date and the previous round was done at a $3.5bn valuation. - Bloomberg

Saturday, Dec. 21st: Databricks raised $10bn at a $62bn valuation led with Thrive, a16z, Insight and Iconiq. It will cross $3bn in ARR in Jan. 2025 growing at 60% YoY (accelerating as Databricks was growing 50% YoY when it was generating $1.5bn in ARR) with 80% gross margins and positive free cash flow. It has also 500+ customers which are generating $1m+ in ARR. Databricks will use the funding to provide liquidity to its employees, to launch new AI products, to acquire companies and to expand its go-to-market internationally. - CNBC, FT

“The “vast majority” of the $10bn will go towards helping employees at the start-up cash out lucrative stock options and to pay the taxes they incur when those options vest.”

“Providing early employees a way to sell their stock has been a motivating factor behind many of the largest deals for venture-backed companies over the past year, including at AI company OpenAI and Elon Musk’s SpaceX.”

Sunday, Dec. 22nd: Gil Dibner wrote about the growth trajectory of AI native companies. - Angular

“As Ed Sim pointed out recently, the “triple-triple-double-double” (TTDD) revenue trajectory that defined successful enterprise startup revenue trajectories for the past decade is being re-evaluated in the face of AI application companies that seem to be growing much faster. The new upper bound seems to be two years of 10x revenue growth (10x10x), but even somewhat more modest pathways such as Ed’s proposed “quintuple-quadruple-triple-double” (QQTD) are more frequently observed than previously. TTDD get you from $1M to $36M in four years. QQTD gets you from $1M to $120M in four years. 10x10x gets you to $100M in just two years. The list of companies that are apparently achieving results on the upper end of this scale is longer than ever before: Bolt, Cursor, Together.ai, 11x, Eleven Labs, Character.ai, Sublime, Wiz, and several more.”

“The idea that $1M ARR guarantees a Series A round is pretty much dead right now. VCs need to see a path to $10m ARR in 12-18 months and a growth rate of 4-5X for a Series A round fundraising to be anything other than very hard.”

“AI excitement is supercharging adoption. Enterprise buyers began 2024 with a tremendous appetite for adopting AI-first products across their organizations.”

“Sales durability is a massive question mark. Undoubtedly, many of these hyper-growers will evolve into successful and sustainable businesses with durable revenues and customer stickiness. But undoubtedly, many will not.”

“The double-edge sword of LLMs and GenAI is that they make it very easy to build a product that is 80% of the way to great, but getting to truly great remains very difficult - maybe more difficult than previously. In a world where nearly anyone can deliver an 80% good solution to customers, I believe the best strategy for a seed fund is to identify situations where founders are obsessed with delivering a product that can get to 100% - even if it takes longer and even if the initial growth looks a bit shakier.”

“Good conditions for the top 20 Series A firms. The Series A firms have the luxury of waiting to see the revenue trajectory around the $1-2M mark, and can snap up the 10x10x/QQTD hyper-growers. For them, there is little incentive to fund before that trajectory is clear - and zero incentive to invest in 2-3x growers at the $1M level if they believe they will find others that will grow faster. These conditions are actually optimal for the top 20 Series A VCs in the world who can reliably access and win these opportunities. For any Series A firm not in the top 20, the situation is darker.”

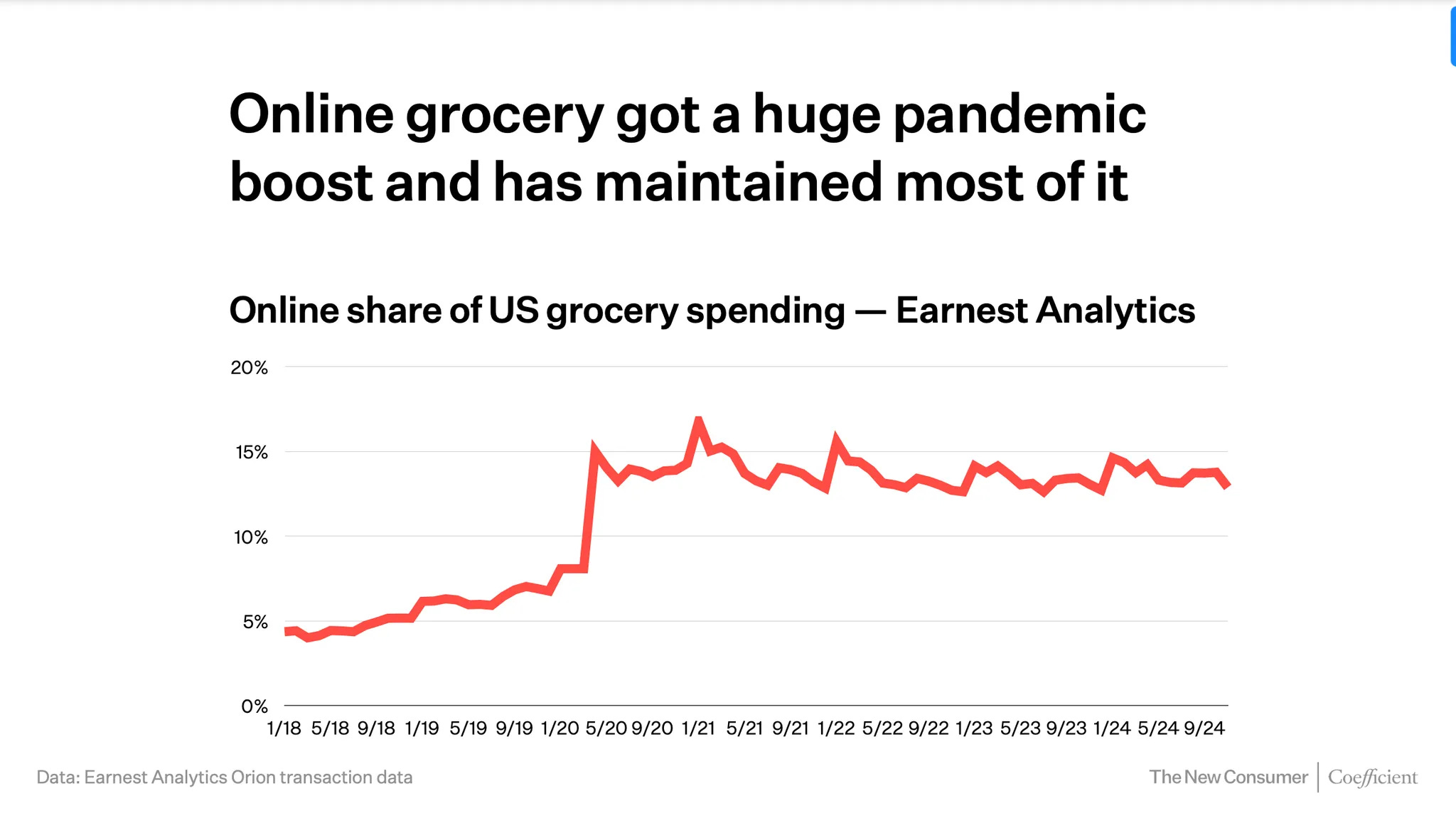

Monday, Dec. 23rd: Dan Frommer shared its 2025 consumer report. - The New Consumer

TikTok Shop is a rising e-commerce force, outpacing competitors like Shein in growth. Gen Z leads daily TikTok use (~60%) and significantly drives TikTok Shop’s success.

60% of Americans mistakenly believe the US is in a recession. Rising prices/inflation remain the top concern, despite decelerating inflation rates.

Tuesday, Dec. 24th: I listened to a Turpentine VC podcast episode with Tom Tunguz who is the founder and general partner at Theory Venture. - Turpentine

Theory Ventures focuses on building a concentrated portfolio of early-stage investments in emerging technologies like AI, the modern data stack, and blockchain applications.

Theory dedicates significant time to researching specific sectors, aiming to gain a comprehensive understanding of the market landscape. They then invest at the early stage, seeking opportunities to secure significant ownership and continue supporting companies as they grow. "Our goal is to be able to focus on categories that we really care about, go really deep, invest in companies in these categories and help them grow as quickly as we can.”

Theory Ventures' approach stands in contrast to the two prevailing models in venture capital:

The "index fund" model, characterized by broad diversification and later-stage concentration through growth funds (e.g. YC).

The "classical venture" model, involving early bets with significant ownership but without the same level of deep research and ongoing support.

The venture capital asset class experienced massive growth in the past decade, surging from $8bn to $300bn in the past 12 years. However, this growth is expected to correct, settling around $150 to $180bn. This correction is due to hedge funds finding public markets more attractive and the increasing difficulty for large growth funds to raise capital.

Similar to the evolution of private equity, venture capital is witnessing the emergence of large, multi-stage firms offering a suite of products. These firms leverage their brand and network to attract both LPs and startups, aiming to deliver consistent top-quartile returns across various strategies. This trend could lead to some of these firms going public, similar to trends in the asset management industry.

Tom highlights 3 key areas of interest for AI investments:

Enterprise Readiness around LLMs: develop tools and infrastructure that address the challenges enterprises face in adopting LLMs

Risk management: Solving issues related to data security, privacy, and compliance when moving data in and out of LLMs.

Legal and contractual frameworks: Addressing questions around terms and conditions, indemnification, and liability associated with using LLM-powered tools.

Redefining categories with LLMs: The ability of LLMs to understand and process natural language opens up possibilities for creating entirely new software categories. Instead of simply enhancing existing tools like CRMs or customer support platforms, the focus is on combining functionalities and reimagining workflows.

AI enabled data tooling: Applying AI to improve the efficiency and accessibility of data tools:

Solving LLM limitations in data Analysis: Addressing the non-deterministic nature and hallucination tendencies of LLMs to ensure accurate and consistent data analysis.

Text-to-SQL and democratization of data: Enabling users without SQL expertise to interact with data and perform sophisticated analysis using natural language interfaces.

Small data movement and enhanced developer experience: Leveraging the increasing power of personal computers to develop and process large datasets locally, reducing costs and improving developer workflows.

Wednesday, Dec. 25th: The Economist shared 2025 predictions on multiple sectors in the economy. - The Economist

IT spending rises by 8% to $3.6trn as companies tap into artificial intelligence.

About 30% of large American firms invest $10m or more in AI, up from 16% in 2024.

Gartner predicts 30% of Gen AI projects will not pass the POC stage amid daunting costs and uncertain benefits.

Shippers must also navigate green trends: 40% of their emissions are brought under the EU’s emissions-trading system.

Lower inflation encourages central banks, including America’s Federal Reserve, to cut interest rates further—and prompts consumers to go shopping.

Increased defence budgets. America, the biggest defence spender, will raise its military budget by 4%, to $884bn, but China, the second-biggest, will increase its spending faster. NATO will debate a national defence-spending target of 2.5% of GDP, although one in three members have missed the current goal of 2%.

Health-care systems will ache in 2025 as populations age and staff struggle. Nearly 12% of the world’s population will be aged 65 or over. Yet only 10% of global GDP will be spent on health, down from 11% during the covid-19 pandemic. Worldwide spending will reach $11trn, nearly half of it in America.

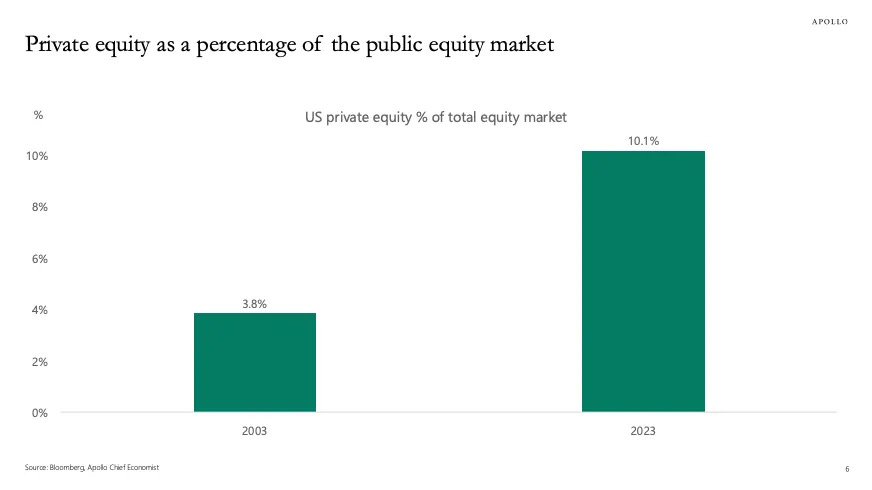

Thursday, Dec. 26th: Apollo published a presentation with key insights into the private equity market. - Apollo

PE’s share of the total U.S. equity market has grown from 3.8% in 2003 to 10.1% in 2023, indicating a significant expansion of the PE sector over the past two decades.

Lower interest rates could spark a new wave of deals as, on one hand, sponsors seek to deploy capital raised in the past three years and, on the other, managers may be willing to part with existing investments as cheaper borrowing costs may bolster valuations.

The exits-to-investments-ratio his at a 10-year low of 0.35x compared to 0.50x between 2012 and 2015.

It takes longer to raise a fund with 75%+ of funds spending more than 1 year raising capital and 50% spending more than 2 years raising.

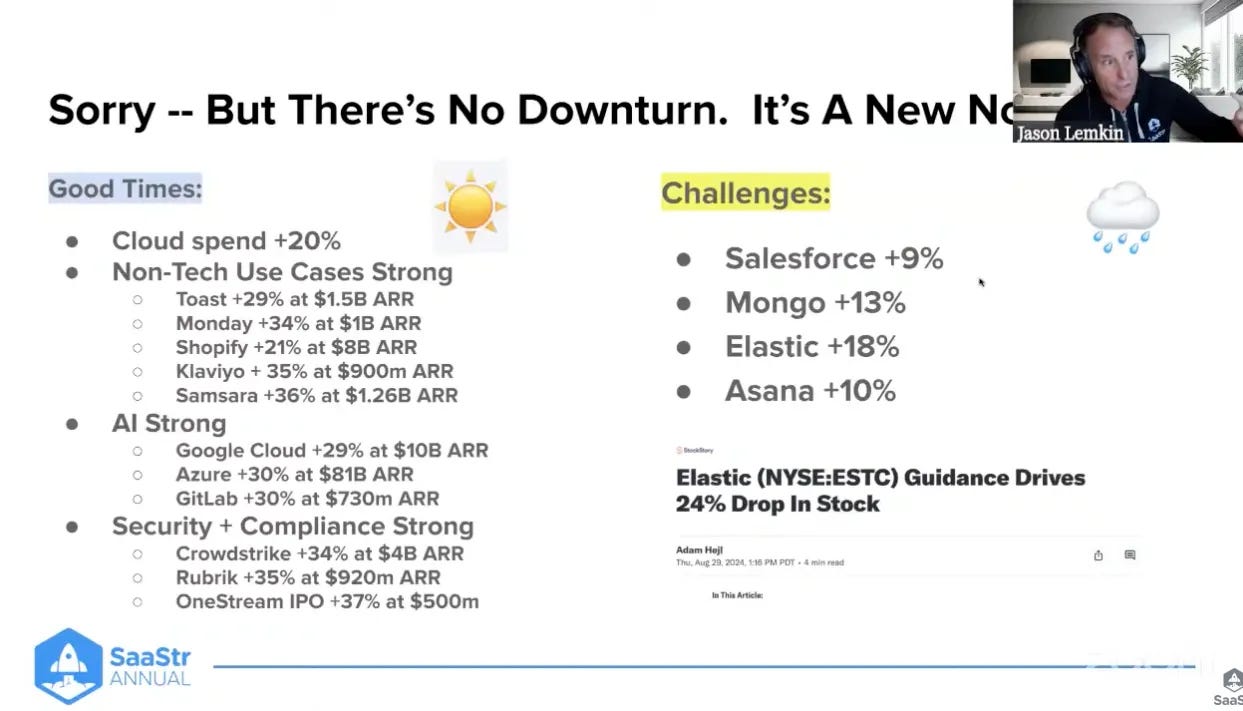

Friday, Dec. 27th: I watched Jason Lemkin discuss the evolution of SaaS over the past 12 months. - SaaStr

Despite narratives claiming a downturn in the cloud market, overall spending is accelerating, up 20% this year.

Tech companies targeting non-tech sectors are massively performing (Toast, Monday, Shopify, Klaviyo, Samsara).

AI is strong with cloud providers having their growth re-accelerating.

Security and compliance sectors are also performing well.

We are entering in the “hyper-functional SaaS era” where customers are demanding much more from SaaS products.

AI is table stakes. It’s no longer a differentiator but a basic expectation.

Automation should be everywhere in the product leveraging AI.

Public companies should be extremely efficient - improving their product while re-accelerating growth.

Multi-product has become the new normal.

There is massive “point-solutions” fatigue. Buyers want platforms and want them to handle more of their software needs.

Developing a second product is critical to avoid TAM exhaustion and maintain growth.

Relying solely on a single product will eventually limit growth potential.

The second product should ideally be larger than the first to significantly contribute to revenue.

Sequencing is key: introduce the second product before growth from the initial product decays, but not so early that it strains resources.

Saturday, Dec. 28th: Bessemer published its series A investment memorandum in ServiceTitan. ServiceTitan had amazing metrics when Bessemer invested with $3.5m ARR (6x YoY) and $9.4m CARR (10x YoY) while being cash flow positive. It had 236 paying SMB customers paying on average $15k ACV. - Bessemer

“ServiceTitan is a vertical SaaS company for home services businesses. ServiceTitan sits at the core of a home services business’ daily operations and provides everything from inbound call management to mobile dispatching/invoicing to back office management.”

“We first met the ServiceTitan team at the Muckerslab Demo Day in LA 1 year ago when they were ~$1M in ARR. We’ve tracked them closely over the course of the year and since then they grew their SMB business to >$3M ARR ($5M CARR) and landed a massive $4M ACV deal with a large plumbing franchise.”

“ServiceTitan’s key differentiation is that in addition to offering back office service management like all their competitors, ServiceTitan also offers sales & marketing performance tracking, enabling businesses to capture more potential revenue.”

“We recommend that BVP invest $17M in the $18M series A financing of ServiceTitan at a $75M pre money valuation. This represents a ~15x ARR multiple of March ending run rate, but 8x CARR multiple which feels reasonable given their growth and opportunity.”

“There are 600k home services businesses in the United States. ServiceTitan is initially targeting three of the largest and most sophisticated verticals within home services: electrical, plumbing, and HVAC, which together account for roughly half of the broader home services market.”

“ServiceTitan has had the most initial traction with Nexstar Network, a well-known association comprised of 550 businesses. ServiceTitan took a bottom up approach and grew organically in the Nexstar member base, acquiring 20 customers before forming a formal strategic partnership with Nexstars one year ago.”

“Gross dollar churn averages under 1% each month. Net churn is slightly negative as customers are upsold on additional mobile licenses.”

Sunday, Dec. 29th: Beezer Clarkson at Sapphire shared its 2024’s annual review for LPs. - Beezer Clarkson

“The liquidity drought is entering its fourth year, and LPs have less and less capital to recycle into new commitments. 2024 saw $69bn in exit value through the first three quarters, an increase from 2023, but a far cry from the $780bn in exit value we saw in 2021.”

“Deal activity slowed as well (reducing capital calls for LPs), but not nearly as much as exit activity. Simply put, there is still way more capital going out of LP accounts than coming in.”

“Compared to previous cycles, we’re seeing more firms keep fund sizes flat or downsize to fit the opportunity set, and far fewer opportunity and follow-on funds.”

“At the fund level, LPs have had to make difficult decisions in their portfolios over the past year, often prioritizing existing managers vs adding new relationships, with most concentrating capital in high-conviction names. This can be seen in the numbers: 2023 saw $86B raised across 836 venture capital funds, while 2024 is on pace for $87B across only 507 funds (the lowest level in nearly a decade).”

“The top 30 VC funds took home 75% of all US VC this year, with a16z and GC accounting for 25%+ of that total.”

“We think the maturing of the venture secondaries market is a welcomed trend for the industry. Alternative options for liquidity provide LPs and GPs alike with additional tools for managing their portfolios and exposures, which should help relieve the extended liquidity challenges in the market and hopefully reallocate fresh capital into the new wave of opportunities.”

Monday, Dec. 30th: CCC acquired EvolutionIQ for $730m (15-16x NTM revenues). - Tanjay Jaipuria, CCC

CCC is a publicly listed vertical SaaS in the Property & Casualty (P&C) insurance sector.

EvolutionIQ is an AI-powered platform for disability and injury claims resolution started in 2019. It plans to generate c.$45-50m in revenue next year at 75%+ gross margins 95% GDR and 150% NDR. It’s used by 7 out of the top 15 disability carriers.

“The deal expands on CCCS’ footprint in the P&C market with total TAM expanding to $15bn+ (vs. prior $10bn) with CCCS expecting to now address a $7bn (prior $6bn) opportunity.”

Tuesday, Dec. 31st: Nikhil Basu Trivedi compiled 2025 predictions from top venture capital leaders. It’s always a good list. Below are my favourite ones. - NBT

Battle between traditional SaaS incumbents & AI-agents native startups. “The next big thing in 2025 will be the beginning of a battle between AI agent startups and established SaaS players. Agent startups, after proving initial value with narrow use cases, will be forced to expand into traditional SaaS territory - building workflow tools and moving deeper into systems of record to capture more customer value and prevent churn. Meanwhile, SaaS platforms will aggressively integrate their own agent capabilities, leveraging their existing customer relationships and data. The key tension: agents need to get sticky, while SaaS needs to stay competitive. Expect M&A activity as both sides race to build complete solutions.” - Jake Saper (Emergence)

Explosion of voice AI applications. “The next big thing in 2025 will be a Cambrian explosion of voice AI applications. Latency on inference, latency on networking, and more advanced turn detection / background noise detection / etc will lead to truly human-like experiences with software. As we “pass the Turing test” on voice AI applications we’ll see an explosion of building in this category.” - Jamin Ball (Altimeter)

AI-native social network. “The next big thing in 2025 will be AI-driven tooling cracking social networking and online fun in a new way, with winners scaling faster than the fastest mobile breakouts, and with novel interfaces that aren’t chatbots.” - Rebecca Kaden (USV)

AI democratising software development. “The next big thing in 2025 will be lots of new products coming from the falling barriers to software engineering. So far, most AI products were imagined by AI engineers and researchers - we’ve yet to fully see the creative output of non-AI builders using this general purpose technology. I think a blockbuster app will top iOS or similar charts that’s built by someone who can’t actually code.” - Nathan Benaich (Air Street)

Liquidity for the startups ecosystem. “The next big thing in 2025 will be both the tech M&A and IPO markets booming, as companies take advantage of a more receptive stock market and a more permissive FTC to deliver liquidity and exits to shareholders.” - Gokul Rajaram (Marathon)

Growth stage becoming more institutionalised than ever. “The next big thing in 2025 will be the continued maturation of financial products for late stage, seemingly pre-IPO companies. “Will they go public or not?” will continue to be a debate, but firms will offer secondaries, private debt, partial buyouts and more. And with an ironic twist, you’ll start to see names of those firms like General Catalyst or A16Z floated more frequently to IPO themselves.” - Aashay Sanghvi, Partner at Haystack

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋