📖 Venture Chronicles - December 2023

Overlooked #165

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of December.

Hi everyone, Just a quick note to wish you a Happy New Year! I apologize for the long pause. It was a busy professional end of the year, and I had to work on the 2023 edition of my report on the French tech ecosystem, which I will publish early next week. I’m super excited for 2024. I have many great projects planned for this newsletter, and I think it’s going to be a great year for tech!

Friday, Dec. 1st: Lenny Rachitsky interviewed Brian Chesky who is the cofounder and CEO at Airbnb. - Lenny’s Newsletter

On product management:

“We don't have any longer the traditional product management function. We did several things.

First, we combined what one might call the inbound product development responsibilities of product manager with the outbound or marketing responsibilities of product marketing.

Second, we off boarded much of the program management functions that product managers may do to actual program managers.

Third, we made the product group smaller and more senior.”

“You can't build a product unless you know how to talk about the product. You can't be an expert in making the product unless you're also an expert in the market of it.”

On performance marketing vs. brand marketing:

“If you want to light up a room, performance marking is a laser. It can light up a corner of a room. You don't want to use a bunch of lasers to light up an entire room. You should use a chandelier and that's what brand marketing is.”

“Performance marketing though doesn't create very good accumulating advantages because it's not an investment.”

“We think of marketing as education. That we're educating people on the unique benefits of our product. We’re educating people about new things that we are making and shipping.”

On the CEO’s involvement into the details:

“A lot of people tell product led founders or engineering led founders to step away and delegate their product to other people, but suddenly they've delegated away the thing they're best at.”

“We don't have a chief product officer title, but if we had one, it would be me. I think the CEO should be basically the chief product officer of a product or tech company. If the CEO is not the chief product officer then I don't know if they're a product or tech led company.”

“If everyone says, "Oh, Airbnb is simple. I'm only doing three things." Yes, but you're one of a thousand people. So actually we're doing 3000 things. So instead of one team doing three things, three teams should do one thing. So we totally cut down the number of projects.”

“I stopped pushing decision-making down. I pulled it in. I created one shared consciousness and I said, the top 30-40 people in the company are going to have one continuous conversation.”

“We created the CEO review schedule where I said I'm getting back involved in the project and I'm going to review all the product and all the marketing. So every project I would review every week, every two weeks, every four weeks, every eight weeks or every 12 weeks. There'd be a cadence.”

“Too many founders apologize for how they want to run the company. If you're a founder, what I would tell you is the problem with finding a negotiation between how you want to run the company and how people want you to run the company, is that's a good way to make everyone miserable. Because what everyone really wants is clarity and what everyone really wants is to be able to row in the same direction really quickly.”

“I basically got involved in every single detail. And I basically told leaders that leaders are in the details. And there's this negative term called micromanagement, and I think there's a difference between micromanagement, which is telling people exactly what to do and being in the details.”

On managers being experts in their functional domain:

“We made sure that every executive was an expert in their functional domain. So you know how there's a lot of engineering managers that aren't that technical or maybe not a lot, but they exist.”

“How do you manage the people without managing their work? How do you give them development if you're not in the details with them on the work? So the same thing is true. So people had to be experts. Everyone had to be an expert.”

“There should be no people managers in the entire company. And when I say people managers, meaning your only responsibility is people, not the work or not the domain. Because you can't manage people devoid of their work.”

On pacing the organisation:

“What would it take to be 10X bigger or do something 10 times better? Because what you find is when you push people, they will sometimes think about the problem differently. And one of the best ways to get unstuck from a problem is to imagine a 10X scale or 10X better or 10X faster where you can't do the current process to do it.”

“One of the most important things for a founder or leader to do is set the pace of the team. That pace is sometimes governed not by how hard people work, but how decisive they are. If you want to improve the speed of a company, then make faster decisions. And fast decisions come from a bias of action.”

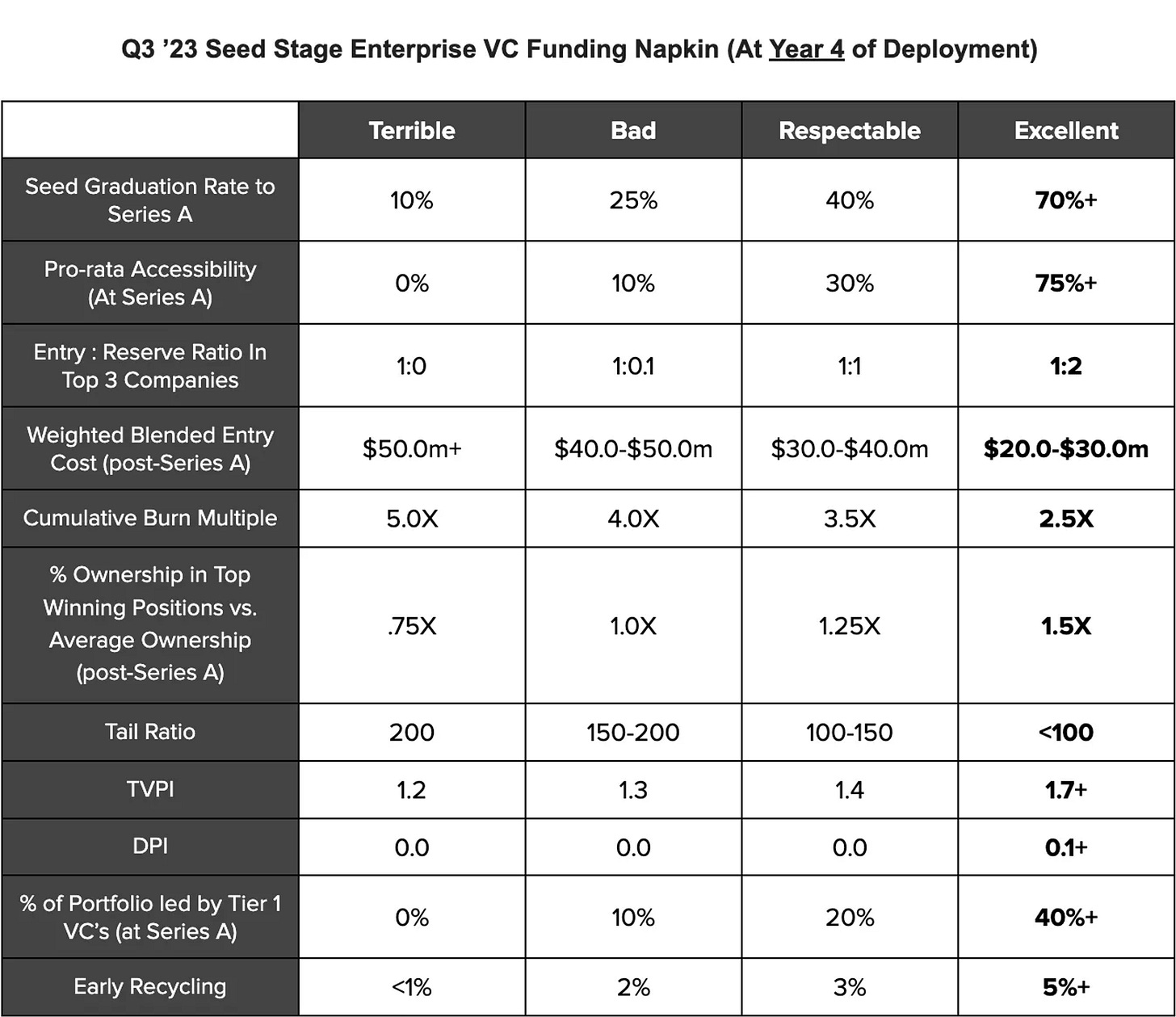

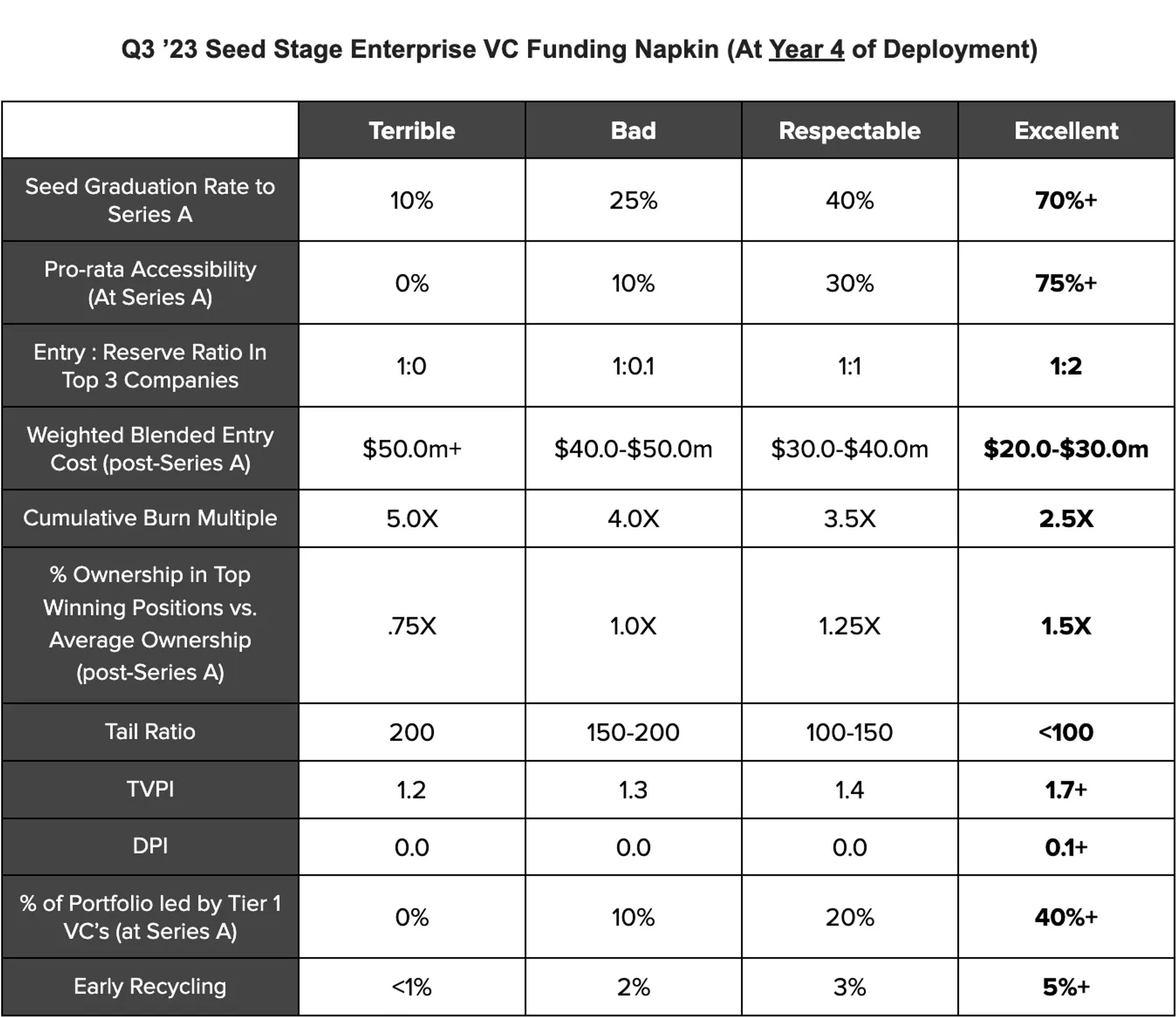

Saturday, Dec. 2nd: Farooq Abbasi at Preface Ventures shared a super interesting table to asses the performance of a seed stage fund early in its life. Thanks to Tommaso for this one! - Preface Ventures

“High-performing VC funds have high follow-on rates to Series A’s. Taking it a step further — a leading FoF referenced to me that if a seed VC fund has 50% of the portfolio graduate to Series B, the likelihood of a fund achieving above a 3.0X DPI is over 80%.”

“Reserve Ratio in Top 3 Companies: This ratio is a metric for executing that pro-rata in fund winners (top 3 positions). Investing $1.0M (entry) in a seed round and $2.0M (reserve) in the follow-on is a healthy ratio. A leading FoF highlighted an even higher ratio (1:3) in their best performing underlying businesses.”

“If Sequoia, Benchmark, Accel, or a16z lead the seed manager’s Series A company, the likelihood of a “homerun” i.e 10X return increases by 4X.”

Sunday, Dec. 3rd: The Economist wrote a great paper on the future of celebrities in a world powered by AI. - The Economist

“The famous folk complaining the loudest about the new technology are the ones who stand to benefit the most. Far from diluting star power, ai will make the biggest celebrities bigger than ever, by allowing them to be in all markets, in all formats, at all times.”

“Film and radio initially seemed like a threat to stars, who worried that their live performances would be devalued.”

“One of the paradoxes of the internet age is that, even as uploads to YouTube, TikTok and the like have created a vast “long tail” of user-made content, the biggest hits by the biggest artists have become even bigger.”

“The number of musicians earning over $1,000 a year in royalties on Spotify has more than doubled in the past six years, but the number earning over $10m a year has quintupled.”

“The number of feature films released each year has doubled in the past two decades, but the biggest blockbusters have simultaneously doubled their share of the total box office.”

“AI promises even more choice, and thus even higher search costs for audiences, who will continue to gravitate to the handful of stars at the top.”

“Digital Botox will increase actors’ shelf-life and even enable them to perform posthumously.”

“The bigger question is how the age of the omnistar will suit audiences. The risk is boredom. AI is brilliant at remixing and regurgitating old material, but less good at generating the pulse-racing, spine-tingling stuff that is, for now, a human speciality. AI output may nonetheless appeal to film studios, record labels and other creative middlemen, who prefer to minimise risk by sticking to tried-and-tested ideas.

“AI will make entertainment’s long tail even longer, with deeper niches and more personalised content. In the AI age, audiences will face heavy bombardment from a handful of omnistars, from Taylor Swift to Darth Vader. But it will be easier than ever for them to change the channel.”

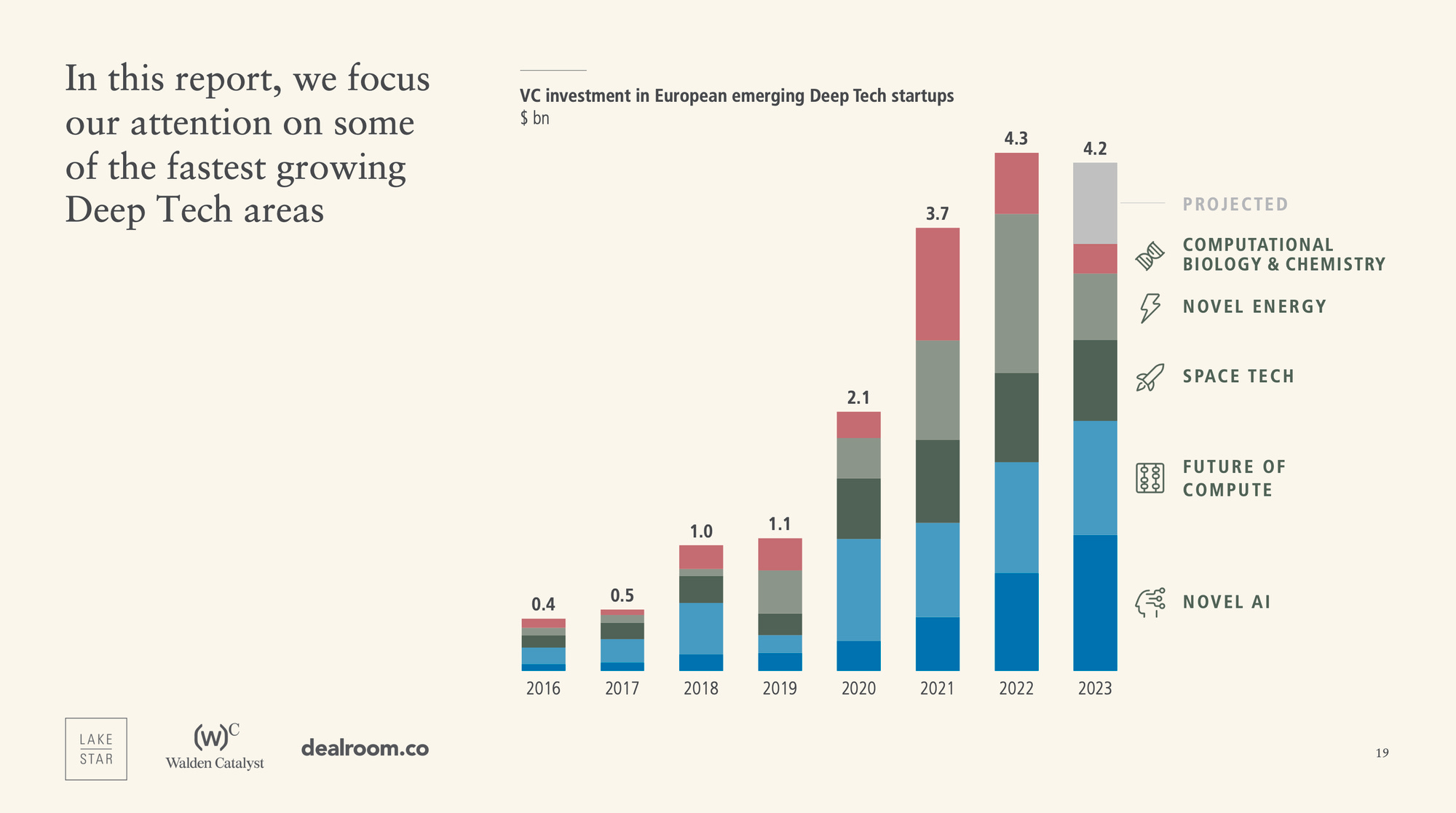

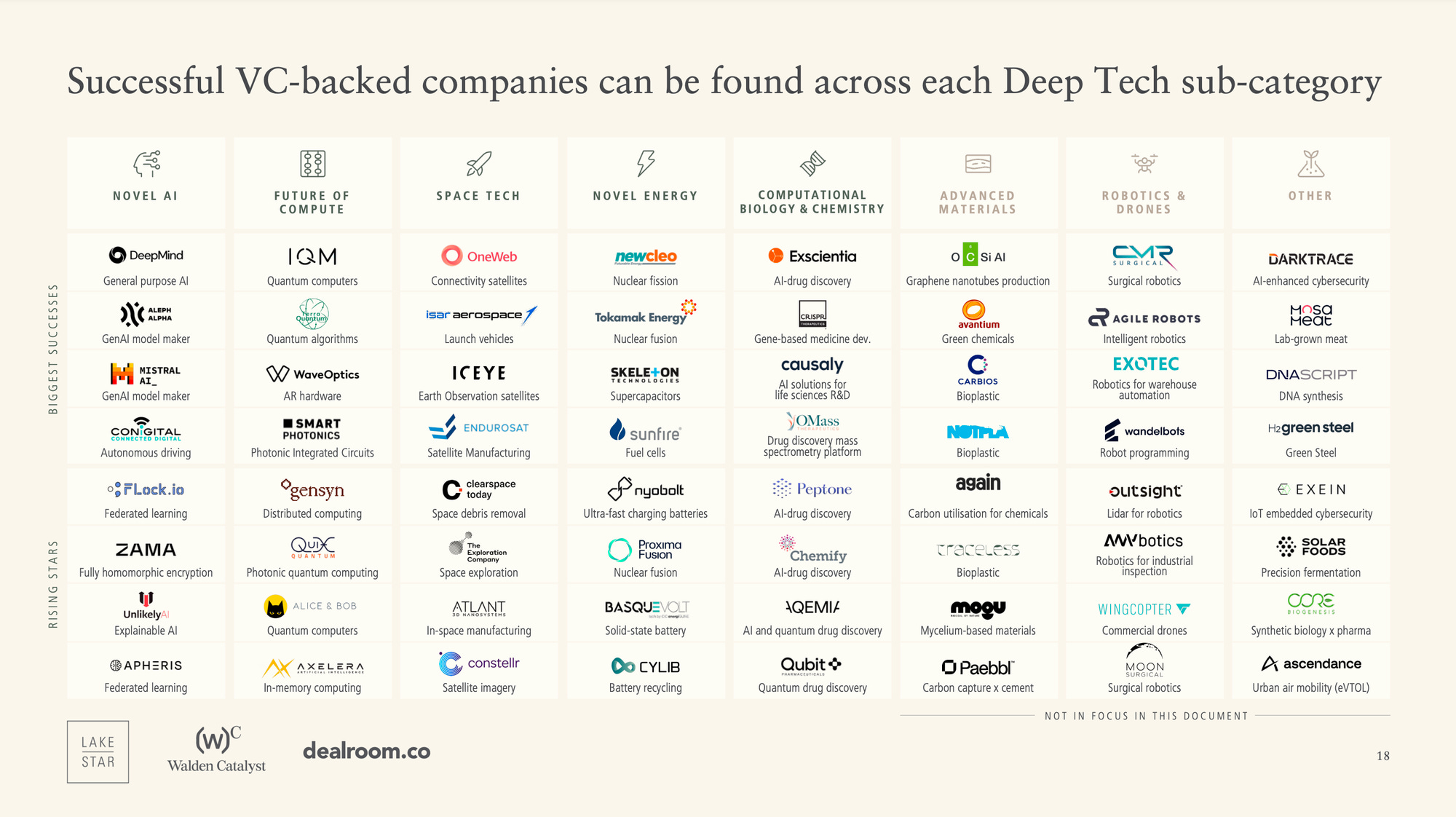

Monday, Dec. 4th: Dealroom published its 2023 European deep-tech report in partnership with Walden and Lakestar. - Dealroom

“Deep Tech is fundamentally new science and engineering making its way into products and companies for the first time. These technologies have historically unleashed mega waves of innovations such as the invention of electricity or the transistor. Deep Tech companies have a different risk profile (e.g., high tech risk, lower market risk) and require a new approach to investing.”

“Deep Tech is amongst the most resilient VC categories with ~$15bn YTD 2023 (almost on par with 2022 vs. -70% in Fintech).”

Tuesday, Dec. 5th: Motlen is acquiring Forward Partners. It’s another proof-point that the venture industry is consolidating. Molten is acquiring Forward Partners and its ownership in 43 portfolio companies (inc. Robin AI, Gravity Sketch, Sonar Analytics and Bea Fertility) for £41.4m. Molten raised £55m in the stock exchange to fund the deal (inc. £25m from Blackrock and £10m from British Patient Capital). - Molten 1, Molten 2

“The VC landscape, as we know, can be unforgiving, and despite the high quality of Forward Partners' portfolio, they, like Molten, have faced challenges in the current market conditions. We see the proposed acquisition of Forward Partners as a positive strategic move to harness Forward Partners' potential while delivering value to the shareholders of both companies.”

“It has a lot to offer when it comes to nurturing the seed-stage ecosystem, something we have made strides towards through Fund of Funds. While our FoF programme successfully bridges the gap from seed to Series A stages, there's a nuanced skill in transitioning companies from seed stage to being ready for a Series A investor like Molten. This is where Nic at Forward Partners excels. His experience and expertise, if applied not only to Molten and Forward Partners portfolios but also the 2,000 companies in the FoF portfolio, could substantially increase the returns of the entire ecosystem.”

Wednesday, Dec. 6th: NfX published a paper on evaluating AI startups. - NfX

“We’re most excited about investing in companies that simply weren’t possible before AI. We’re looking for the non-consensus markets and products with limited competition, either from incumbents or from other startups.”

“There are some industries primed for what we call AI leapfrogging. Leapfrogging happens when an industry or market (usually an outmoded industry, or an emerging market) skips a step along the technology transformation chain. These industries have historically not been digitized and don’t have a dominant cloud incumbent.”

“Much of the initial returns of the Generative AI explosion will accrue to incumbents. For now, startups need to pursue orthogonal innovation. We want to see companies with attractive initial markets, with limited incumbent activity and straightforward sales cycles. You must be able to implement fast and demonstrate value to customers quickly.”

Thursday, Dec. 7th: Casey Winters wrote about the challenge of scaling from PMF on one product and one distribution channel to multiple products and multiple distribution channels. - Casey Accidental

“After product/market fit, most companies’ obsession is not thinking about how to create their next amazing product. Their obsession is thinking about growth. […] Most companies have a primary acquisition loop that drives this scalable growth, and unfortunately, there aren’t that many acquisition loops that really scale. Even when they scale, they eventually asymptote, and companies need to find new ways to grow.”

“Most companies when they find product/market fit with their first product only have one acquisition and engagement loop that is successful, and the job of most of the team is to refine and scale those loops.”

“The company requires either new growth loops or new products to acquire, retain, or monetize better. Modeling your loops helps you start investing in building out those new growth loops or products well in advance of when you need them to sustain your growth, because of course developing them takes much more time than improving a current loop.”

“Sequencing S-Curves to drive growth of companies over the long term is not only quite difficult, but the craft of doing it is under-developed.”

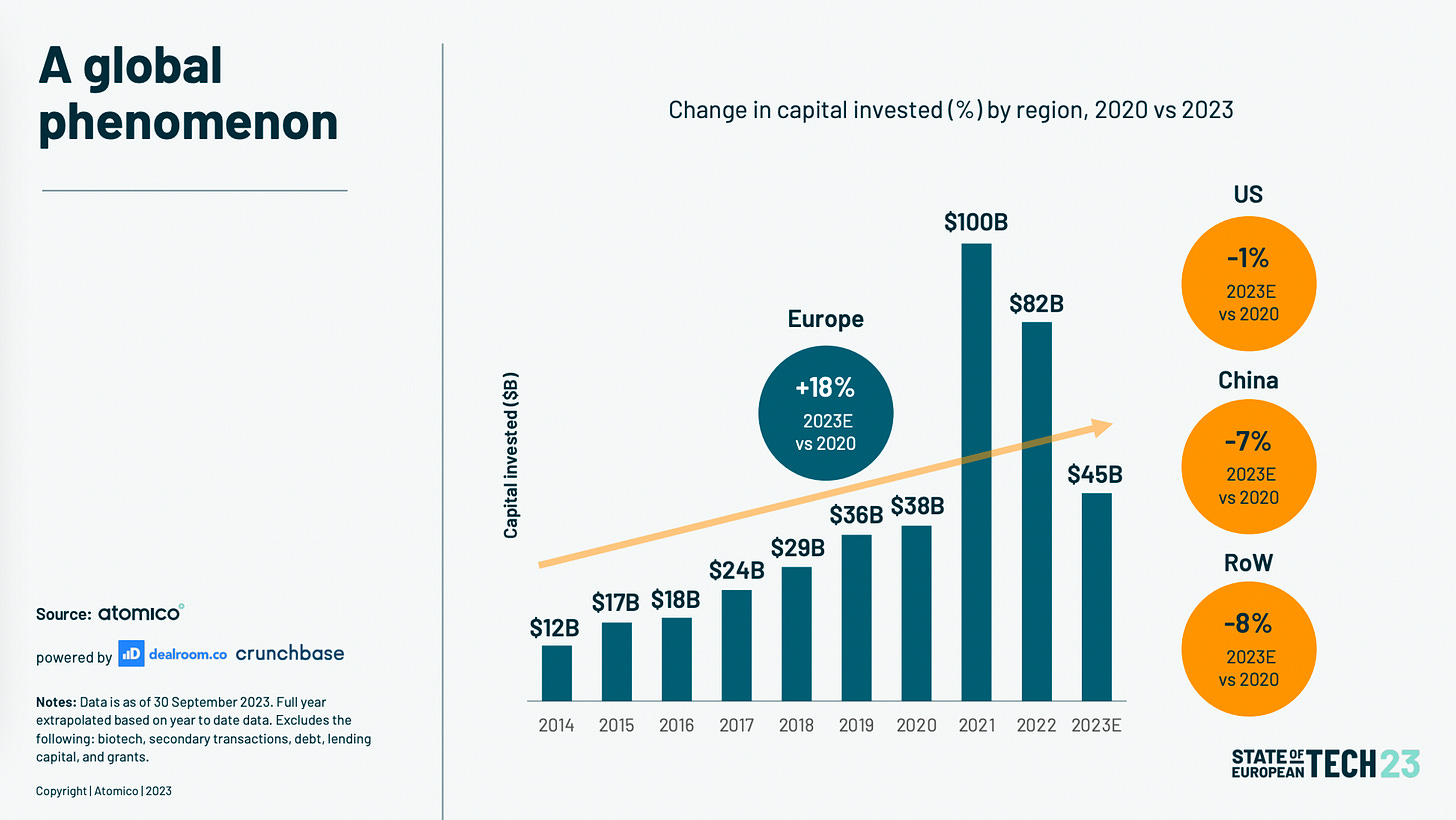

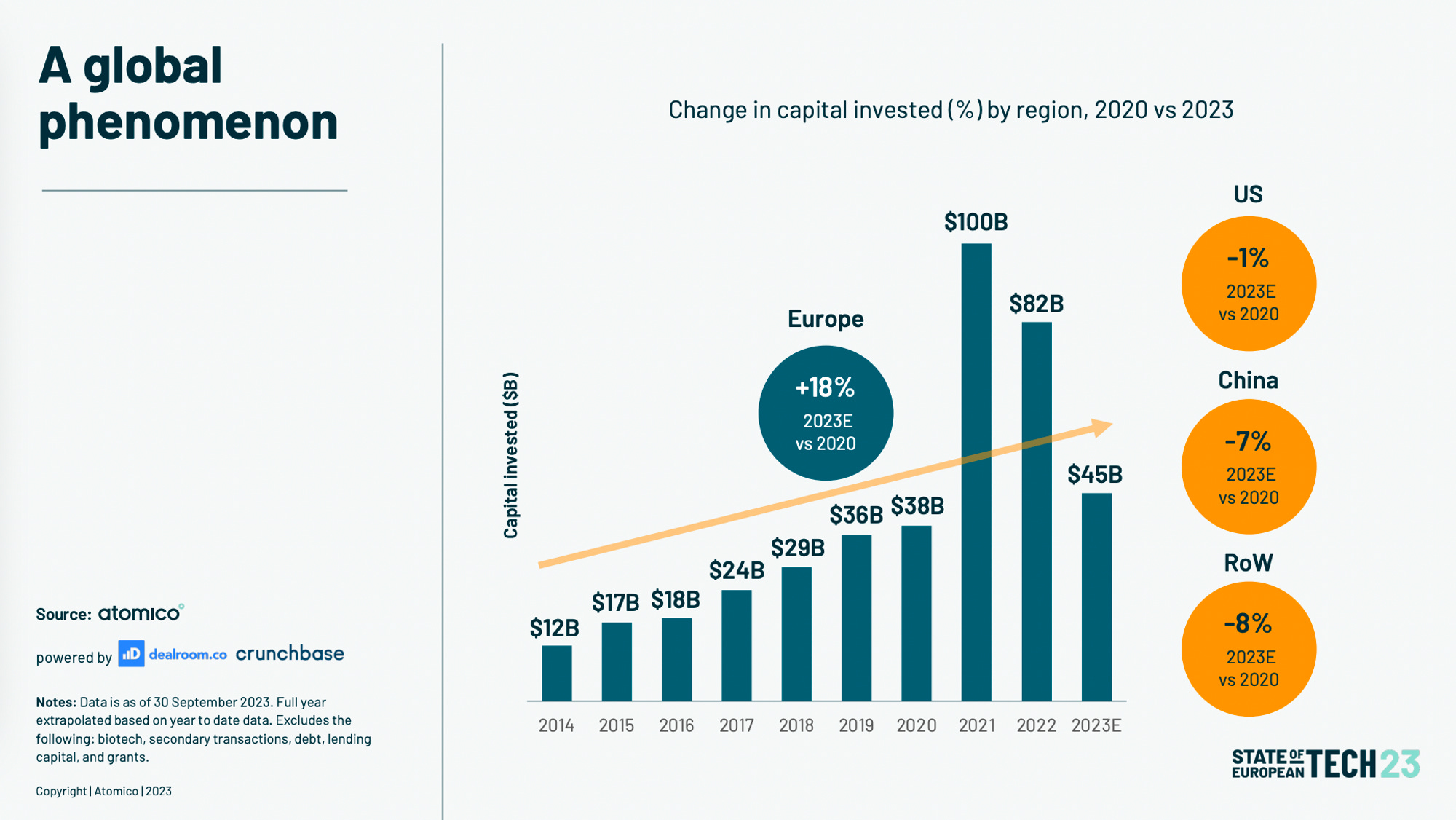

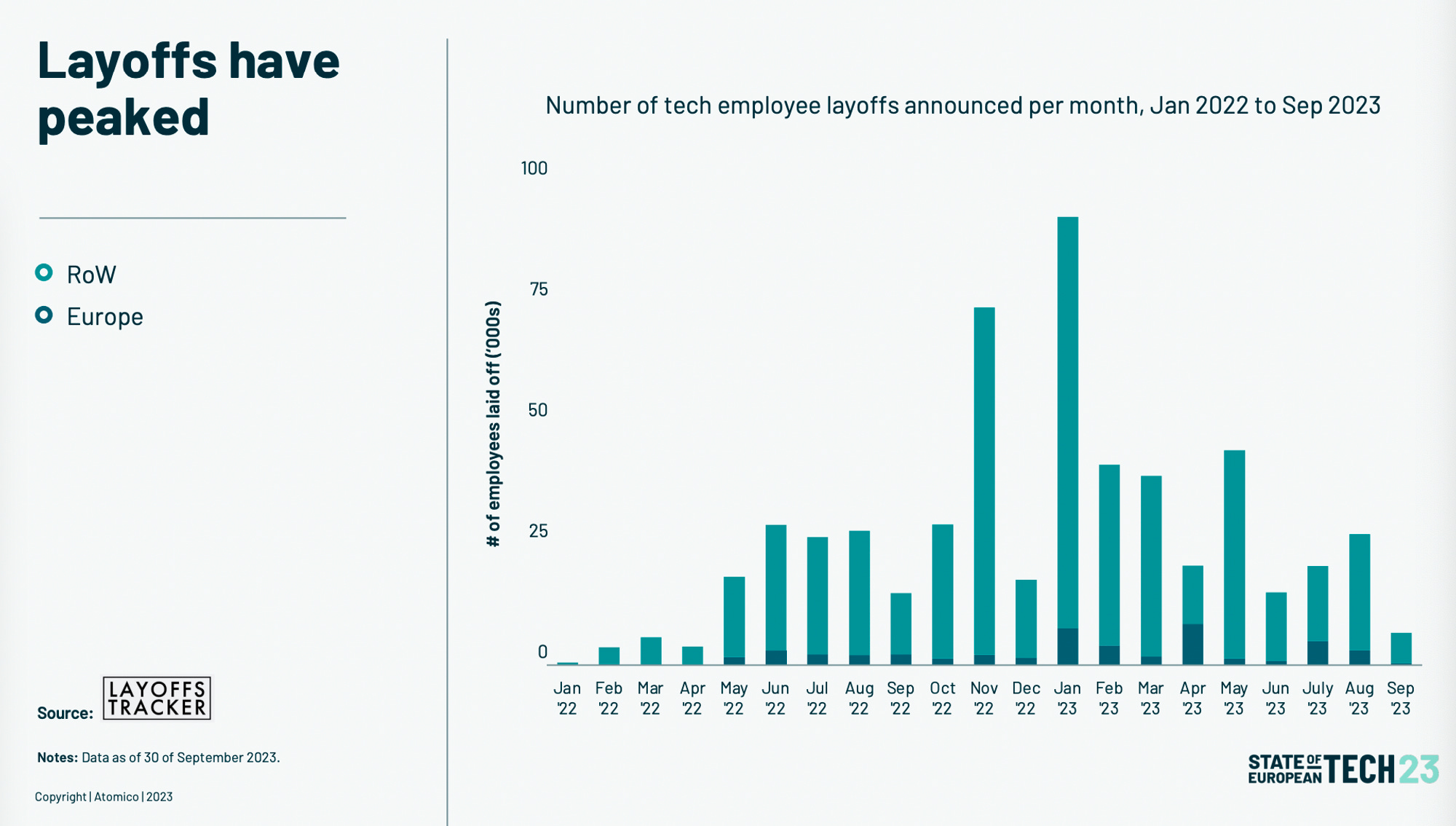

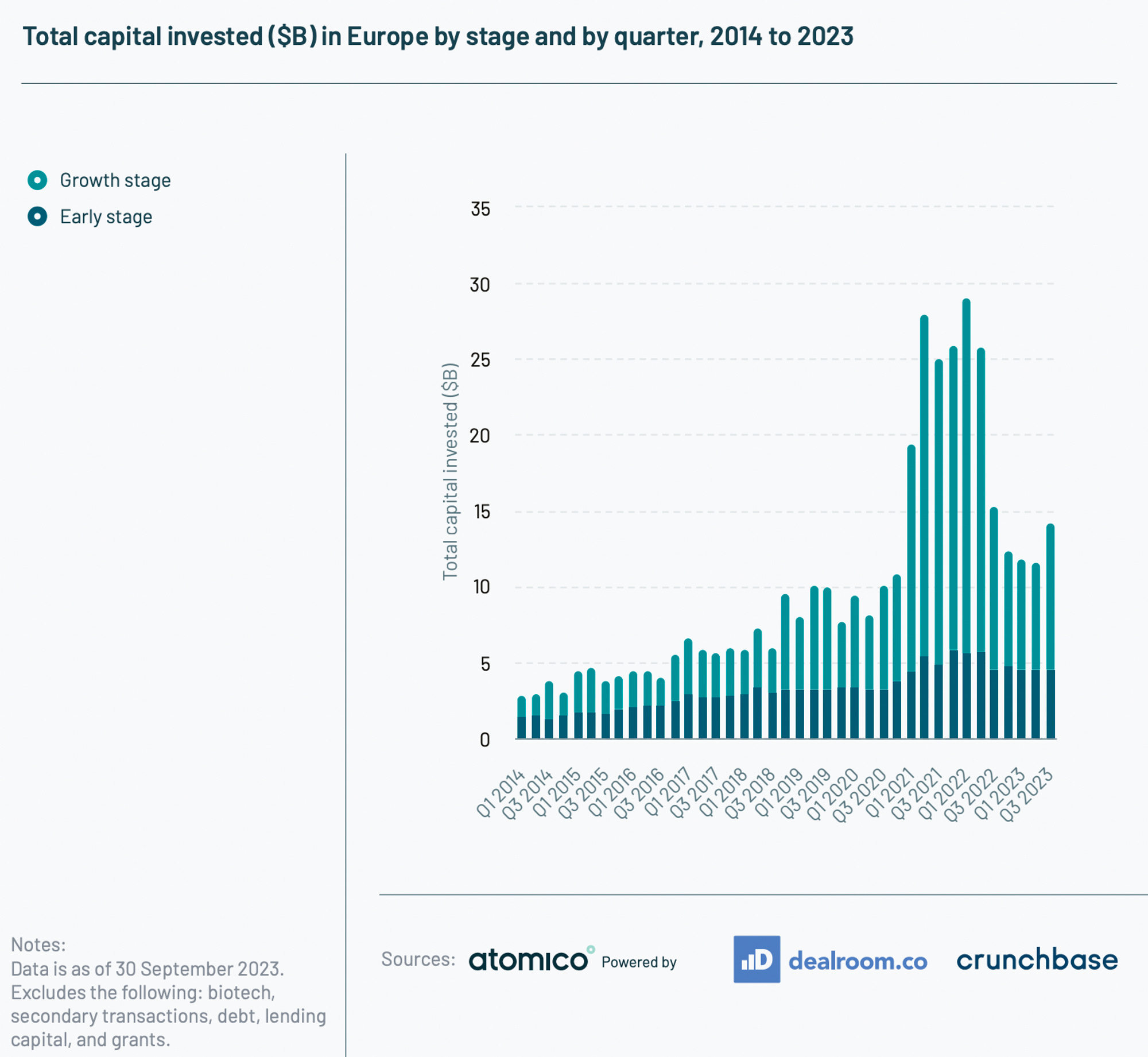

Friday, Dec. 8th: Atomico published the 2023 edition of its European State of European Tech. - Atomico

“In terms of startup formation, Europe is now creating more new startups than the US, and while startup formation has slowed this year, this is largely due to the weeding out of first-time founders, with the share of repeat founders remaining stable.”

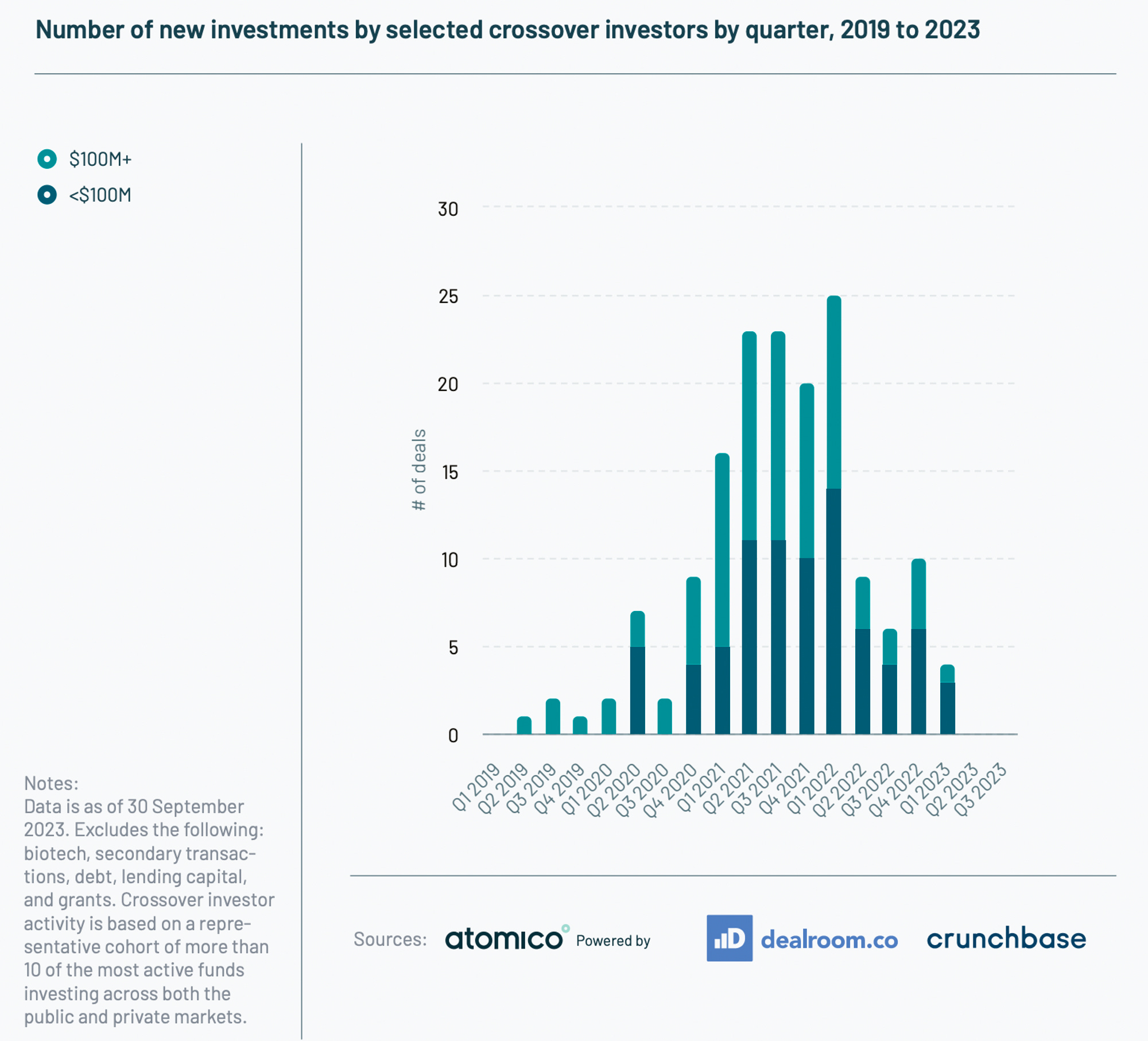

Cross-over investors have massively slowed down if not stopped to invest in private companies being a major factor in the decline of growth funding in Europe.

For the first time in 5 years, the involvement of US investors in European rounds has decreased from 21% of total deals in 2022 to 19% in 2023.

In 2023, European startups are on track to raise $45bn compared to $100bn at its peak in 2021 and $82bn in 2022. “The decrease in investment since 2021 is mainly due to a slowdown in growth stages. Early stage investment has stayed stable despite the ups and downs in investment volume since 2021.”

Only 7 new unicorns have been minted in Europe in 2023 compared to 107 in 2021 and 49 in 2022.

“Remarkably, nearly 9,000 companies have been initiated by alumni of European exited unicorns that were founded during the 2000s. To put this into perspective, it is nearly a staggering 50% increase compared to the unicorns founded in the 1990s.”

“In 2023 to date, 6 companies with a total value of $5B in Europe and 8 companies totalling $32B of value in the US have been taken private by PE firms. The most sizeable of these are the take-privates of Qualtrics International ($11B, led by Silver Lake) in the US and Software AG ($3B, Silver Lake) in Europe.”

Saturday, Dec. 9th: Ben Thompson from Stratechery interviewed David Baszucki who is the co-founder and CEO at Roblox. - Stratechery

Since its IPO, Roblox made strong progresses on the following dimensions: (i) international expansion (e.g. Japan), (ii) expanding in older cohorts of users (17-24 y.o.), (iii) improving Roblox’s performance (e.g. better quality, lower latency).

“Does Roblox’s long-term profitability really rely on the advertising coming to bear in a major way? Where you get so much more leverage on your revenue? […] Even without advertising, we have this incredible business that’s growing and becoming more and more leverage based on the operation side. […] Advertising is really interesting and amazing given the size of the business we’ve built so far and the amount of engagement, well north of 15 billion hours per quarter, a lot of it more and more by Gen X and Gen Z type people. So what’s actually pretty amazing is we haven’t fully tapped into that, we see a huge future for ads that complements our current transactional business.”

On advertising, Roblox is launching both traditional units (e.g. watch a video ad on a billboard in a Roblox’s game) and full experiential units (e.g. Nike Land, Vans World, Gucci Garden where it’s an experience similar to go to a boutique in a shopping mall in which you can look and interact with the merchandise).

“I think the size of the potential immersive advertising experience is uncharted right now. It’s immersive, there’s so much time spent there, the memories are really profound when I go with a friend to do that. So I do think it’s uncharted and very big.”

Three AI waves are currently impacting Roblox’s model: (i) boring being the scenes AI infrastructure (e.g. translation, trust-and-safety, moderation, image detection), (ii) allow more people to become creators on Roblox (e.g. text or voice prompt to design your avatar or to create a gaming experience), (iii) leveraging data to create personalised experience on the fly based on how users behave.

“The AI wave, particularly the generative AI wave, and the Metaverse are inseparable, because you have this asset generation challenge where I would argue gaming has hit a wall, and Roblox has gone around this by starting relatively low fidelity, letting anyone create, and having this user-generated content, but to have a truly immersive extendable experience, you need a leverageable way to generate that content, which is AI.”

Sunday, Dec. 10th: The Generalist wrote a great blog-post on Hummingbird which is a super successful and under the radar European seed fund. - The Generalist

“Hummingbird believes that every “legendary” company goes through two to three near-death moments. That has come from its experience backing startups like Peak Games and Gram Games. This belief has led Hummingbird to double down on startups when other investors have packed up their pencils. According to leadership, this has been a key driver of returns.”

“Hummingbird has delivered three vintages with over 10x net returns. It’s done so without hitting the buzziest startups of the past cycle, instead capitalizing on a roster of relatively under-the-radar giants, including Peak Games, Gram Games, Kraken, BillionToOne, and FPL Technologies.”

“If you want to deliver consistently superior returns, Hummingbird believes you need to find the most exceptional entrepreneurs on earth – not merely the top 1%, but the top 0.1%.”

“Hummingbird is pursuing a very specific kind of entrepreneur – someone with unreasonable ambitions, astonishing clock speed, and a frightening hunger that portends a deep, personal unease.”

“A decade after Peak was founded, it was sold. In 2020, Zyga acquired Sidar Sahin’s company for $1.8 billion. For Hummingbird, it marked a stunning validation of their approach. They had found an outlier founder in an unusual geography and backed him to the hilt. From an investment of just $5 million, they had scored a return of $276 million – a gross multiple of 54.4x. Peak alone returned Hummingbird’s first fund 9.1x.”

“Over the past three years, Hummingbird has assembled a team of 10 investors. That came from an applicant pool of 8,700. Hummingbird looks for a very particular kind of investor, just as it does on the founder side of things. The firm operates “nomadically,” with “hubs” in North America, Europe, and Asia, but the freedom to chase one’s curiosity. If an associate wants to follow in the footsteps of someone like Gelenbe and map out the Thai ecosystem or obsess over the machinations of the NFT market, they can do so.”

““Our team has a target of speaking with 20 to 30 companies a week [per person],” Ileri said. “If you have ten people, that makes more or less 10,000 companies per year.””

“Nomads hunts for opinionated, non-consensus investors aiming for extremely asymmetric outcomes. “It is trying to find funds that can do 10x,” Gort said. “Which then excludes a few models. It will exclude models that have more than $250 million under management. It’s just hard to return that. There are some exceptions, but in general, it’s hard to do. It will exclude people that have a very diversified portfolio. It will also exclude complex decision-making models or playing in a pool where there’s not a lot of alpha, where there’s not a lot of arbitrage involved.”

Monday, Dec. 11th: The New York Times wrote about startups struggling. - NY Times

“WeWork raised more than $11 billion in funding as a private company. Olive AI, a health care start-up, gathered $852 million. Convoy, a freight start-up, raised $900 million. And Veev, a home construction start-up, amassed $647 million. In the last six weeks, they all filed for bankruptcy or shut down. They are the most recent failures in a tech start-up collapse that investors say is only beginning.”

“After staving off mass failure by cutting costs over the past two years, many once-promising tech companies are now on the verge of running out of time and money. They face a harsh reality: Investors are no longer interested in promise.”

“Approximately 3,200 private venture-backed U.S. companies have gone out of business this year, according to data compiled for The New York Times by PitchBook, which tracks start-ups. Those companies had raised $27.2 billion in venture funding.”

“One area that is thriving? Companies in the business of failure. SimpleClosure, a start-up that helps other start-ups wind down their operations, has barely been able to keep up with demand since it opened in September, said Dori Yona, the founder. Its offerings include helping prepare legal paperwork and settling obligations to investors, vendors, customers and employees.”

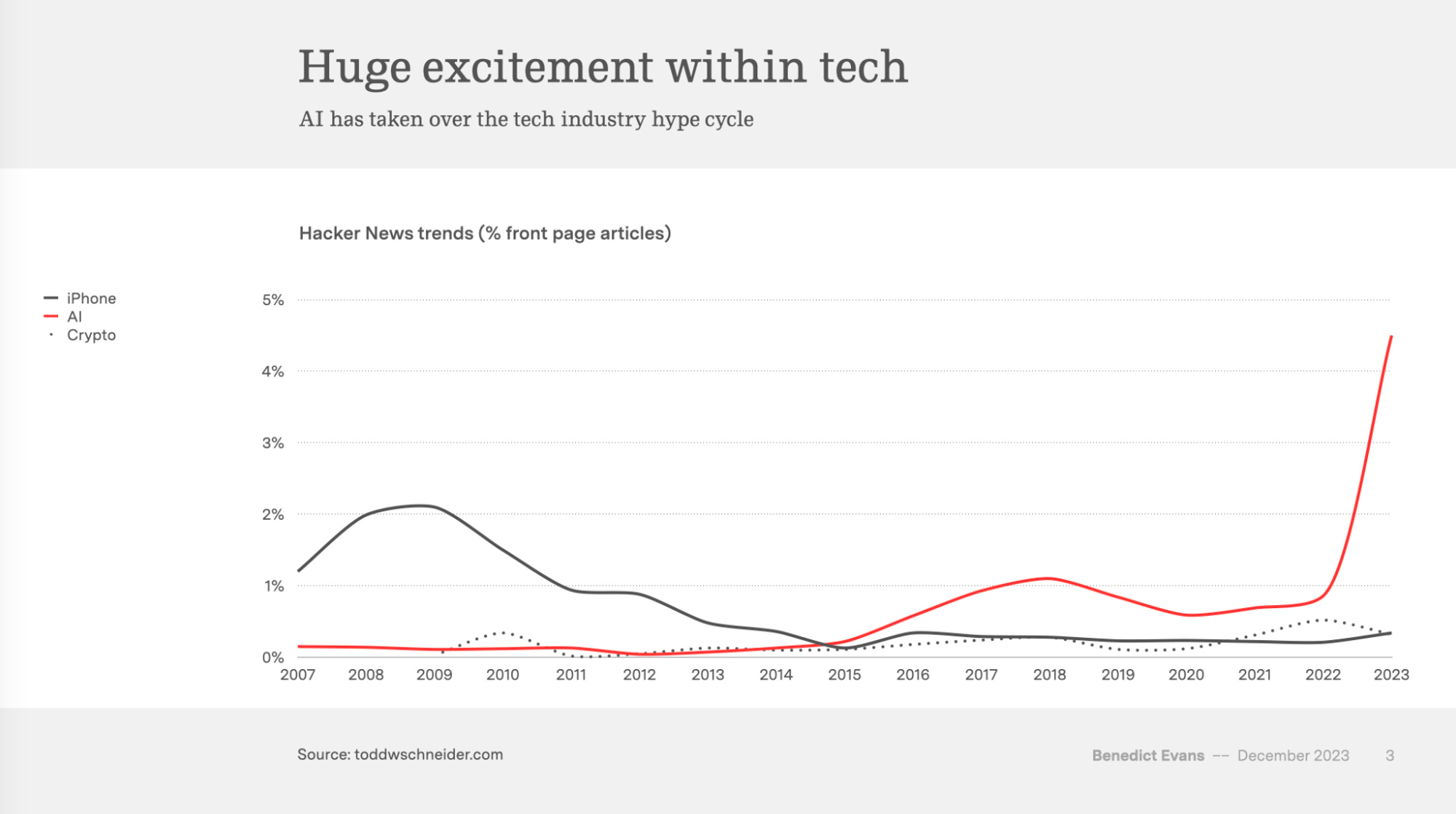

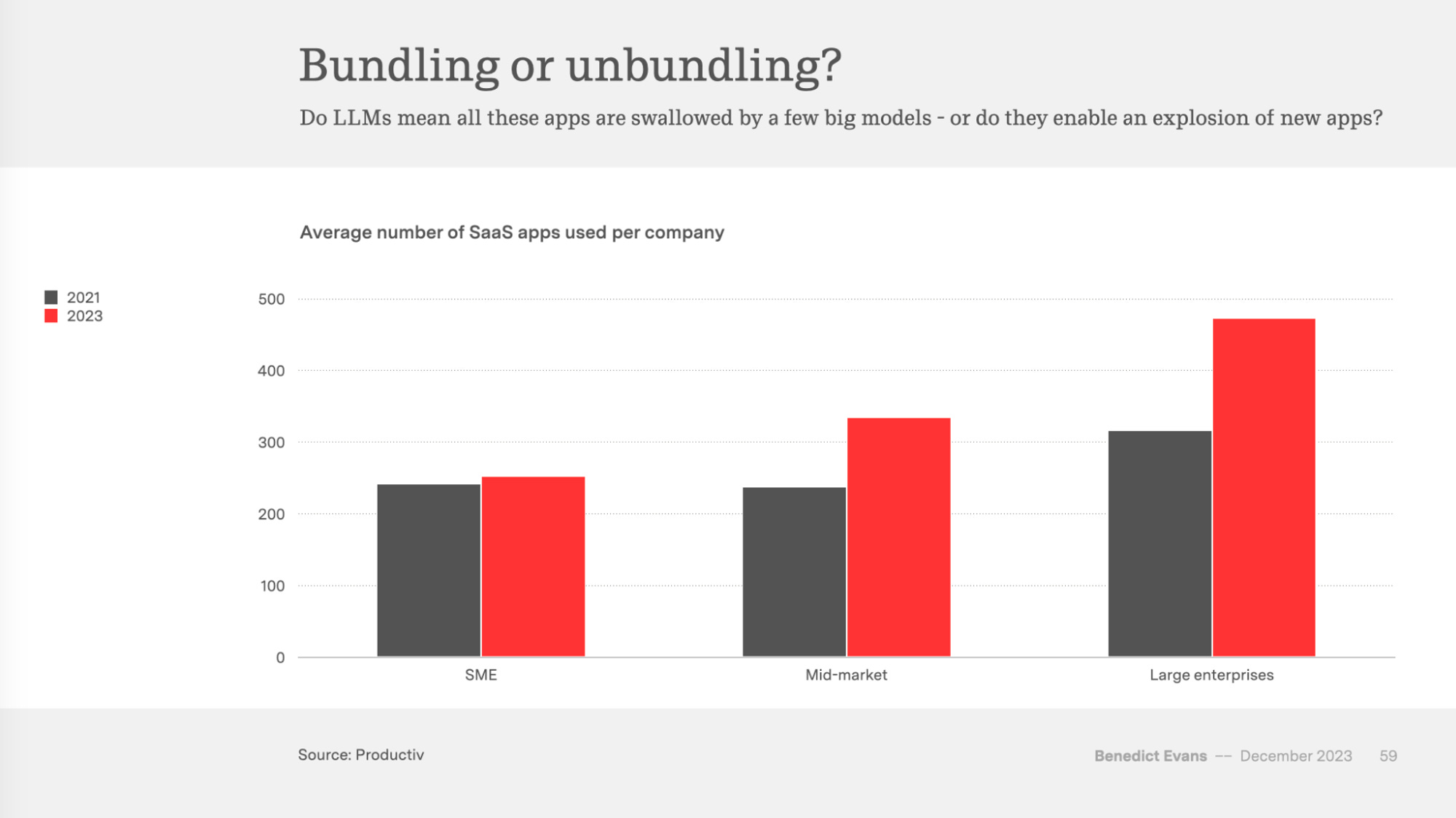

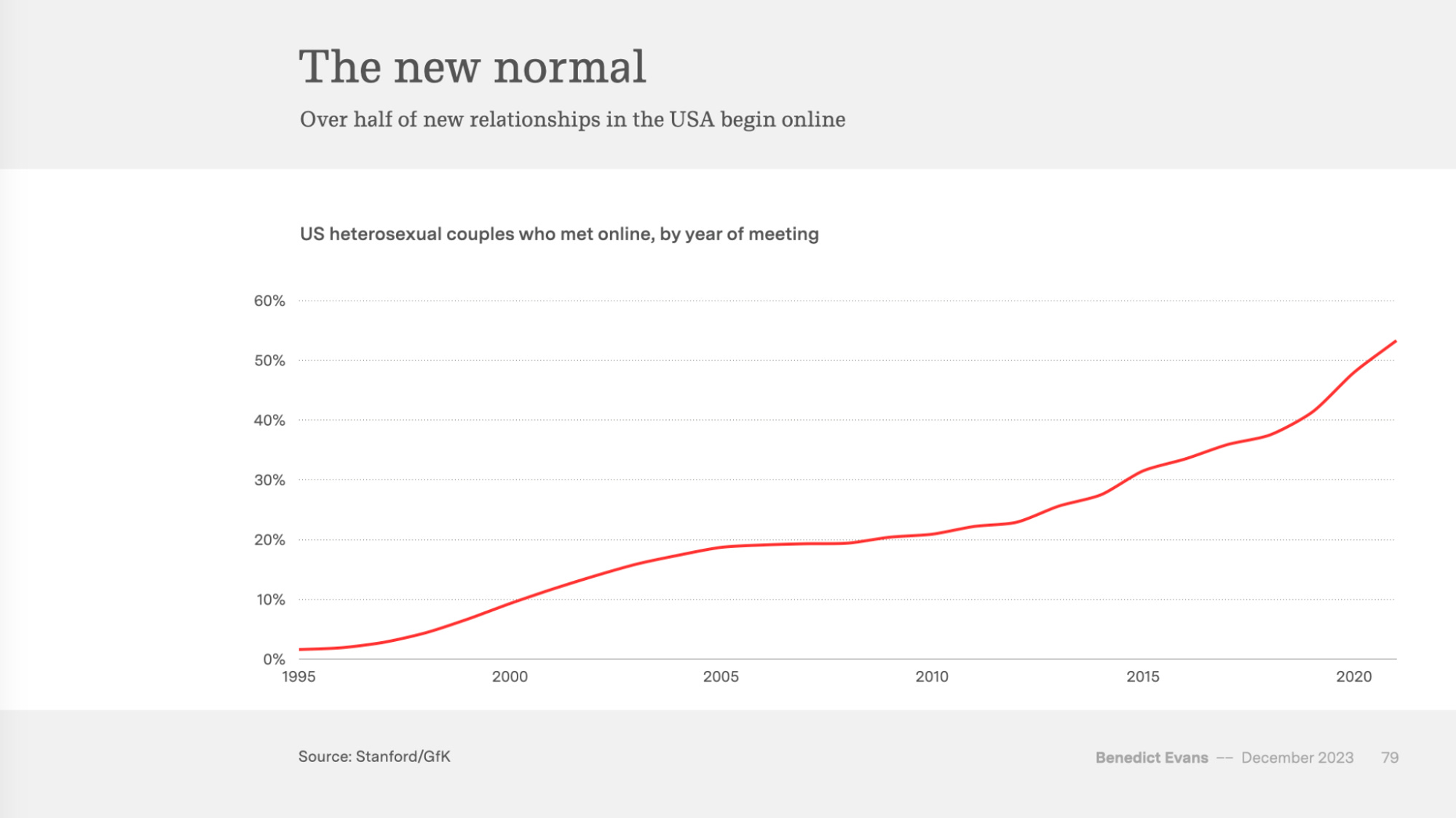

Tuesday, Dec. 12th: Ben Evans published its annual presentation on tech. - Ben Evans

Wednesday, Dec. 13th: Luke Skertich wrote about SaaS enabled marketplaces. - Part I, Part II

A SaaS enabled marketplace is a solution combining a SaaS offering and facilitating a transaction. Examples include Slice (pizzerias), Fresha (beauty salons), Odeko (coffee shops), ResQ (restaurants), Alma (mental health care practices).

To build a successful SaaS enabled marketplace, founders should consider the following characteristics: (i) define who is the customer that you should sell SaaS to between the demand and the supply, (ii) add value added services to the transaction to streamline it for both side of the marketplace (e.g. logistics, fintech, ads), (iii) start with a small subset of SKUs, (iv) start with a restricted initial geography, (v) create a repeatable playbook for finding new users.

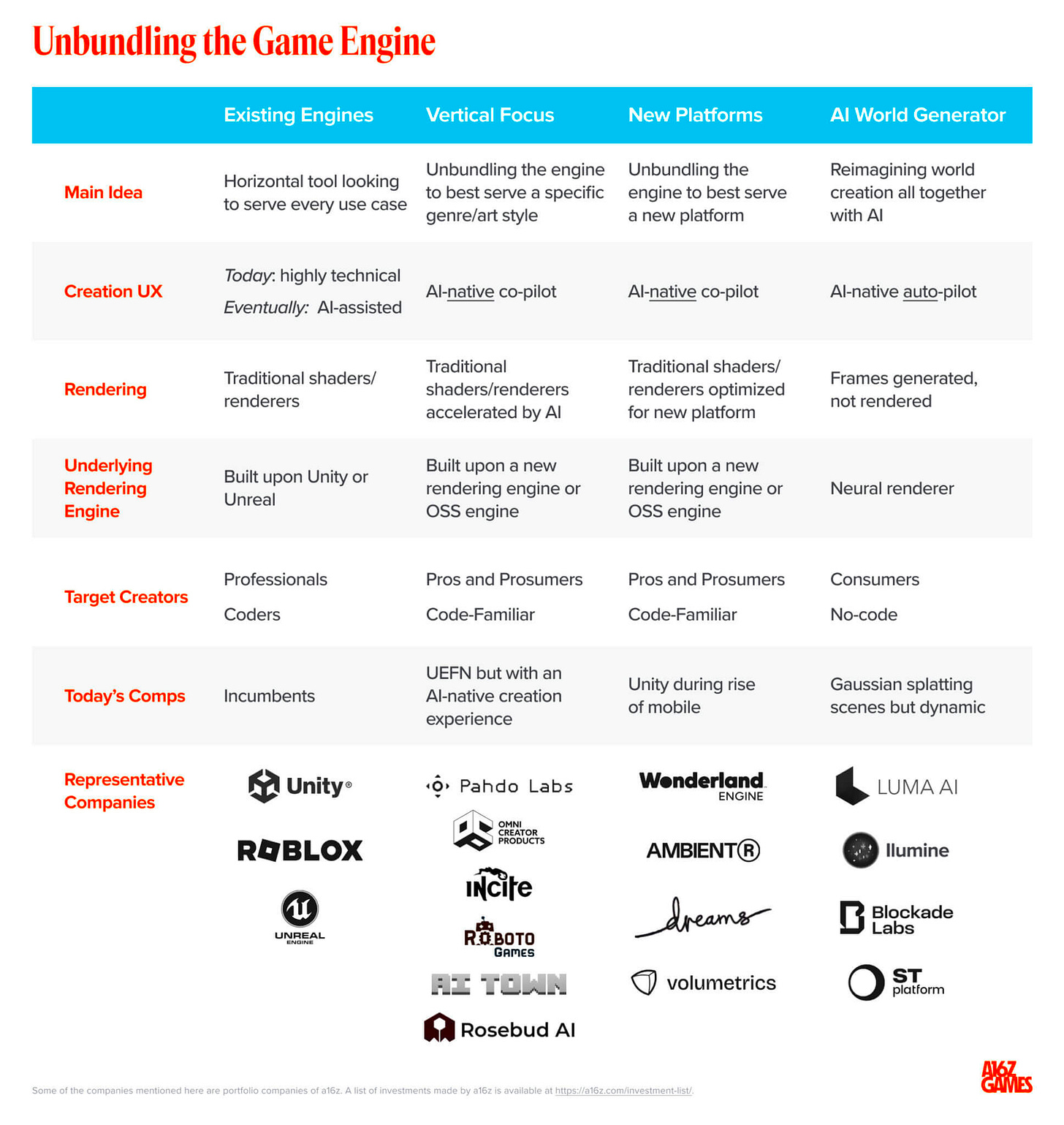

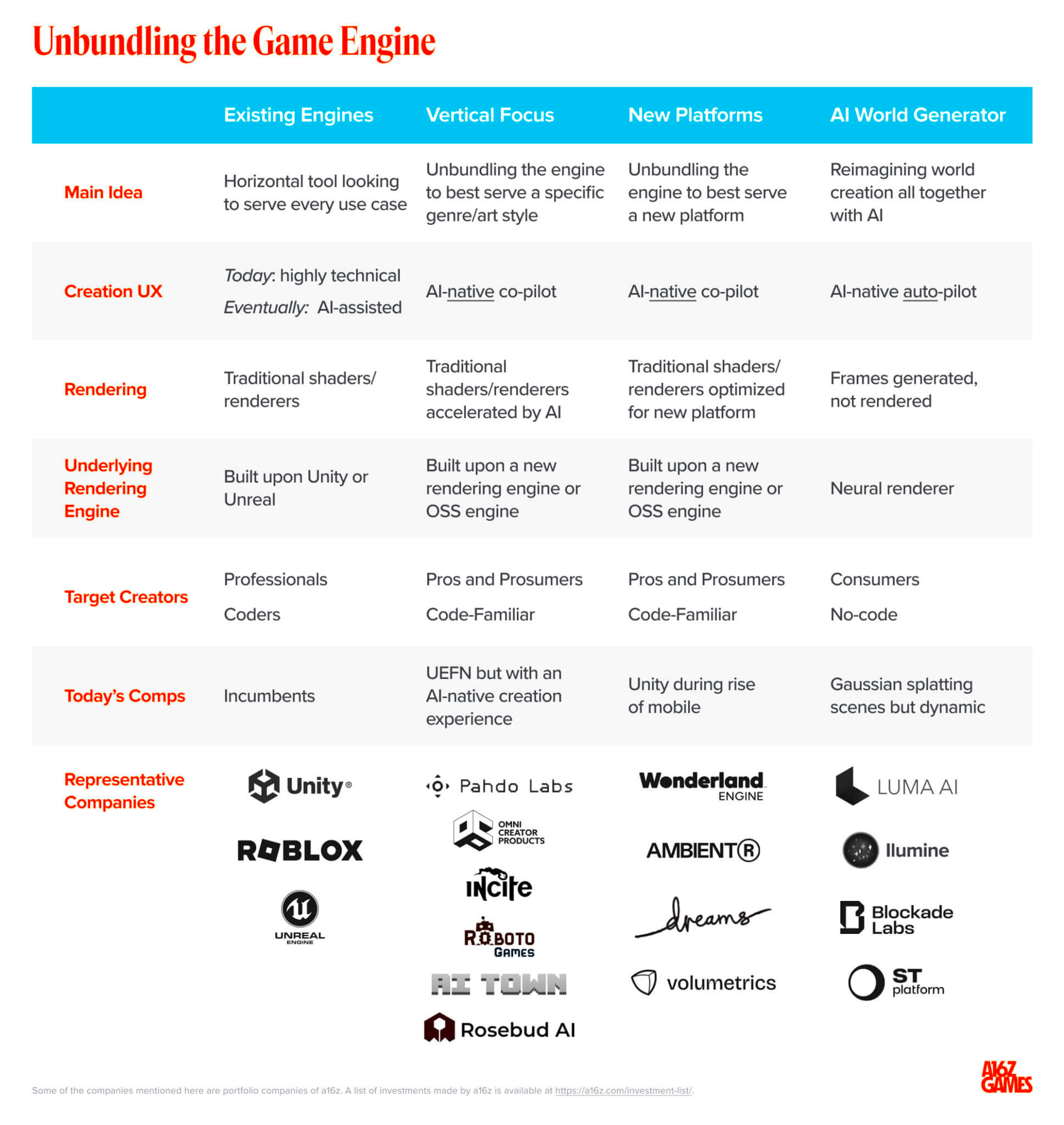

Thursday, Dec. 14th: a16z wrote about game engines arguing that there is a unique opportunity to create a new gen. AI native game engine to disrupt Unity, Unreal and Roblox. - a16z

“Unity, Unreal, Roblox and Godot – the predominant 3D engines – are all 15+ year old technologies architected for a different era of computing. The emergence of generative AI, cloud computing, and new spatial platforms is poised to disrupt 3D creation end-to-end.”

“Before the 2010s, most studios developed their own internal engines to build their games. Now, almost all games are built using the third party engines shown below, excluding some of the largest AAA budget games that still develop on their own (e.g. EA’s Frostbite, Infinity Ward Engine, etc).”

“We are moving towards a state where creation may start with a simple text box to generate a first draft of your project. And with that, the barriers to entry for new creators dramatically decrease.”

“With the help of AI, the creation experience moves towards auto-pilot but the creator should always be able to intervene and express directorial control over any decision. No longer will content creation be the project bottleneck but team collaboration and review. Creator roles within a studio will move from extreme specialization (e.g. riggers, environment artists, texture painters) towards creative generalists.”

“Rather than competing with the incumbent engines head on trying to serve every use case, a Next Gen Engine will likely arise through a few routes where a traditional game engine is unbundled: (i) vertical focus (best-in-class at serving a specific game genre or art style), (ii) new platforms (optimizing for a specific platform, (iii) AI world generator (building a consumer facing AI world building platform).”

“As a GTM strategy and as a way to prove out the engine, we are likely to see the developer build the first game (or series of games) on top of the platform. Enabled by AI, doing so should be possible at a fraction of the time and cost to develop a game over the last decade.”

“3D Creation Engines should charge a revenue share vs SaaS pricing. We believe Unreal and (now) Unity have paved the way for a future engine to charge a revenue royalty share rather than a fixed SaaS price fee. Between 2-5% of revenue will likely remain the norm to use a commercial engine and all the services that come with it.”

Friday, Dec. 15th: Singular raised €400m for its second early-stage fund from LPs including OTPP, Mudabala, BPI or Vintage Investment Partners. It had raised a first €225m fund in 2020. It started fundraising at the end of 2022 with a €350m target. Singular retained all its LPs from the 1st fund into the second fund with sometimes larger tickets. It will back seed to series B European startups with €1-25m tickets. - Sifted, Les Echos (🇫🇷)

“When you’re a good team working together for 10 years with a good track record, and you say you’re going to start your own thing, LPs see the potential. It’s a bit like being a seed-stage startup. If you’re repeat founders who have done good things, everyone wants to shoot a term sheet.” - Jérémy Uzan

“LPs are aware that when the second fund comes along, they won’t yet know how well the first fund has performed. In a way, they already knew that they would back fund one and fund two. It’ll be with fund three that the cleaver will come down.” - Jérémy Uzan

Saturday Dec, 16th: I listened to a 20VC’s podcast episode with Peter Lacaillade who is managing director at SCS Financial Services. - 20VC

The best fund managers are forces of nature combining work ethic, ambition and passion for what they do.

Peter looks at several criteria to assess investment opportunities in funds: (i) quality and alignment in the team, (ii) investment strategy, (iii) competitive advantages to execute this strategy, (iv) fund sizing to execute the strategy, (v) track record.

When Peter started as an LP in 2011, he could not access top tier venture funds and decided to back what was the next generation of promising GPs including Thrive, a16z and Founders Fund.

SCS invests in 10 funds per vintage out of 2k opportunities. It invests only when it has an extremely high level of excitement. 3-5 funds will exceed expectations. 3-5 will meet expectations. 1-3 will underperform. It takes 4 years to know which fund will over-perform or under-perform.

Sunday, Dec. 17th: I listened to a Colossus’ podcast episode with Erik Serrano who is the CEO at Stable Asset Management which is a $3bn firm backing the next generation of GPs. - Colossus

“I think people underestimate how the life cycle of a firm follows the life cycle of a human in investing. You invest in the intellectual capital of the humans that are part of that team.”

Top GPs are resilient (i.e. they never give up, they love so much their job that they will overcome any discouraging news and obstacles, most of the times it comes from adversity at a young age) and have varying perception (i.e. seeing things that other people don’t believe, being contrarian in investing by having a point of view coming from a life experience or analysis that is different from the crowd).

When it seeds a fund, Stable has several revenue streams: (i) return on invested capital, (ii) excess of management fees, (iii) carried interest, (iv) appreciation of the EV from the stake it takes in the GPs (with a mechanism in which founders can buy back the stake we have in their GPs).

Monday, Dec. 18th: Adobe will no longer acquire Figma for $20bn following anti-competitive concerns raised by the European Union and the UK. Adobe will pay Figma a $1bn break-up fee. In 2023, Figma grew its ARR by 40% to $600m and expanded its team from 800 to 1.3k people while remaining cash flow positive. I wrote about this acquisition, arguing that it was anti-competitive for Adobe to acquire Figma, whose UX/UI design platform was disrupting Adobe’s design monopoly. I believe that Figma will thrive as an independent company and can reach a similar valuation as a public company if it chooses to go public in the next 12-24 months. - Reuters, Figma, Techcrunch, Sam Lessin, Semil Shah, Stratechery

“We want to make it easy for anyone to design and build digital products on a single multiplayer canvas—from start to finish, idea to production.”

“The majority of startups who consider an acquisition to be their best exit option shouldn’t worry much about the fallout of this deal getting blocked. […] In fact, the vast majority of startup deals look nothing like the Figma or Plaid deals. The median exit value of U.S.-based startups this year was $64.5 million, according to PitchBook. That is less than 1% of the value of the $20 billion Adobe was ready to pay for Figma. What’s more, the majority of startup acquisitions don’t involve nearly as much market share and influence as this deal.”

“You have to build a real / full businesses these days - building a great product with strategic value to an acquiring platform isn’t a viable strategy anymore.”

“My hypothesis moving forward is that when these large pools of capital (which are incredibly powerful and influential) make the next set of long-term commitments to early-stage capital (which directly affects innovation and the jet fuel for entrepreneurs), they will likely use an adjusted calculus that they need to refocus on two elements: 1/ moving their capital entry point to earlier-stage and lower valuations to control entry price, which allows for a smaller acquisition and liquidity for investors and shareholders; and 2/ making sure the bigger winners are on a path to a public offering, which will likely be valued at lower multiples then the previous eras.”

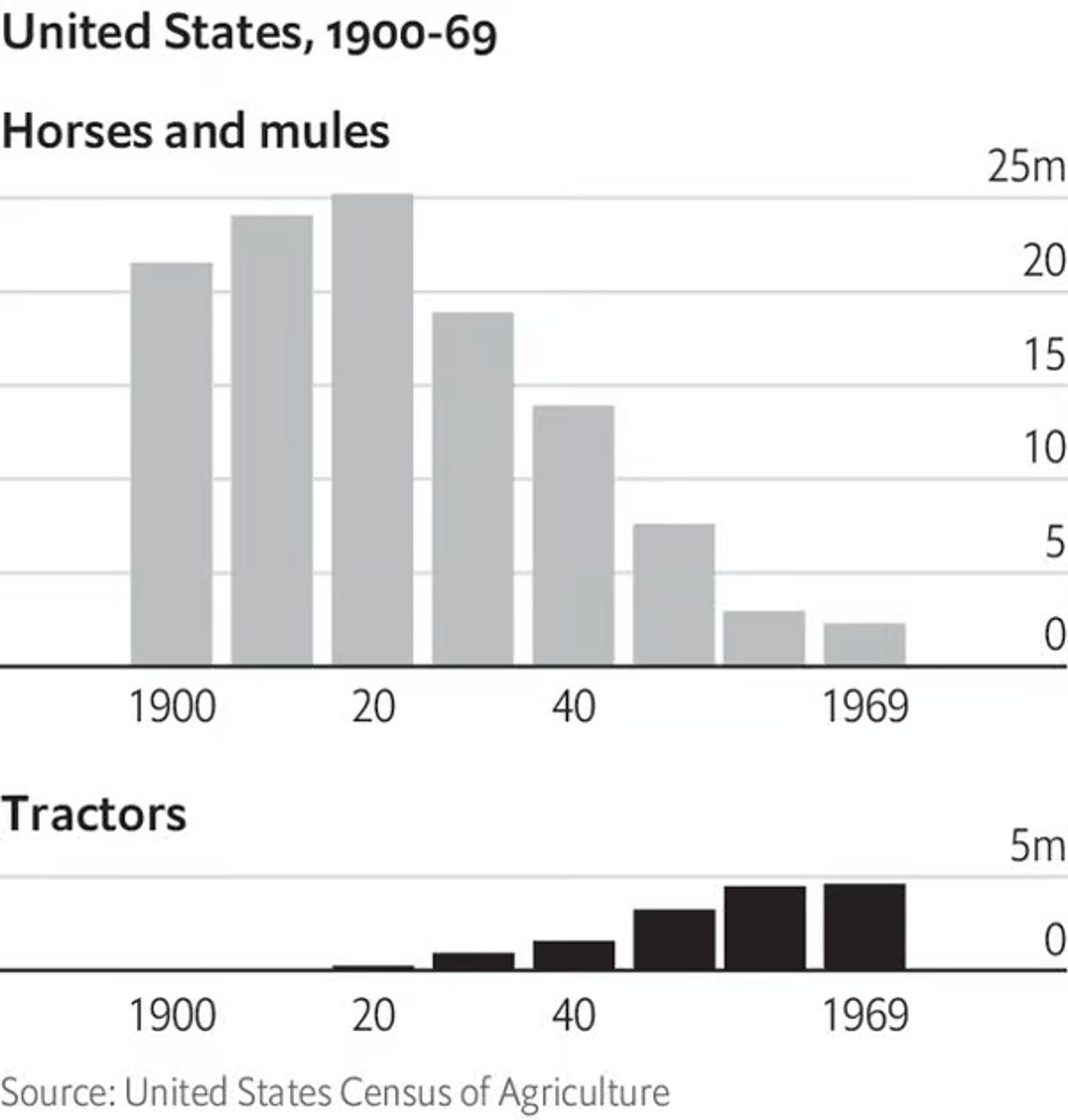

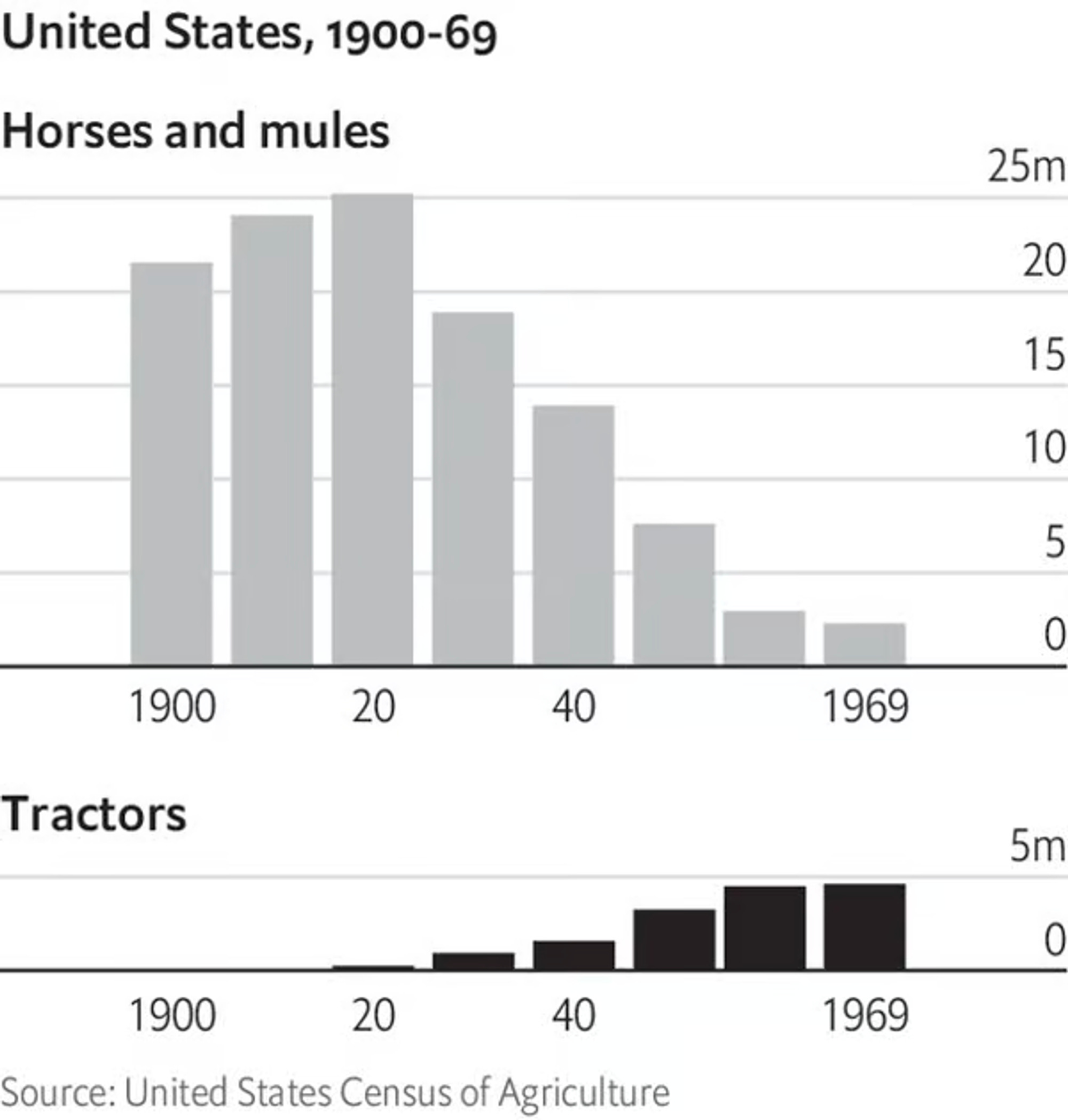

Tuesday, Dec. 19th: The Economist wrote an amazing paper drawing an analogy between the adoption of General AI in the 21st century and the adoption of tractors in agriculture in the 20th century. It takes time for a society to adopt new technology, as was the case with tractors. There is a high likelihood that the same will be true for Generative AI.- The Economist

“Over the sweep of history the tractor has indeed had an immense impact on people’s lives. But it conquered the world with a whimper, not a bang.”

“The slow diffusion of the tractor produced slow productivity gains. The data are spotty, but in the first half of the 20th century annual productivity growth in agriculture probably never exceeded 3%. That 8% GDP effect is real, but it made itself felt only over decades.”

“Three reasons explain why the triumph of the tractor took so long. First, early versions of the technology were less useful than people had originally believed, and needed to be improved. Second, adoption required changes in labour markets, which took time. And third, farms needed to transform themselves.”

“The history of the tractor hints at how quickly generative ai may take over. At present most ai models still have metal wheels, not rubber tyres: they are insufficiently fast, powerful or reliable to be used in commercial settings. Over the past two years real wages have hardly grown as inflation has jumped, limiting companies’ incentives to find alternatives to labour. And companies have not yet embraced the full-scale reorganisation of their businesses, and in-house data, necessary to make the most of ai models. No matter how good a new technology may be, society needs a long, long time to adjust.”

Wednesday, Dec. 20th: I read an article from Jorge Mazal who was CPO at Duolingo on its strategy to re-accelerate growth at scale to 4.5x the number of DAUs over 4y. - Lenny’s Newsletter

In both failed experiments (more gamification inspired by a puzzle game and a strong referral program inspired by Uber), “we had borrowed successful features from other products, but the wrong way. We had failed to account for how a change in context can impact the success of a feature. I came away from these attempts realizing that I needed a better understanding of how to borrow ideas from other products intelligently. Now when looking to adopt a feature, I ask myself: (i) why is this feature working in that product?, (ii) why might this feature succeed or fail in our context, i.e. will it translate well? (iii) what adaptations are necessary to make this feature succeed in our context?”

“We immediately saw that CURR had a gigantic impact on DAU—5 times the impact of the second-best metric. In hindsight, the CURR finding made sense, because the Current User bucket has an interesting characteristic: current users who stay active return to the same bucket.”

"Duolingo already had a leaderboard for users to compete with their friends and family, but it wasn’t particularly effective. [….] The leaderboards feature had a huge and almost immediate impact on our metrics. Overall learning time increased by 17%, and the number of highly engaged learners (users who spend at least 1 hour a day for 5 days a week) tripled.”

“If a user reached a 10-day streak, their chances of dropping off were reduced substantially.” […] “To date, the streak feature is one of Duolingo’s most powerful engagement mechanics. When people talk about their Duolingo experience, they often bring up their streak.”

“Through our efforts over four years, we were able to increase CURR by 21%, which represents a reduction in the daily churn of our best users by over 40% and, together with our other successful bets, led to an increase in our DAU of 4.5x. […] The quality of the user base also improved; the share of our DAU with a streak of 7 days or longer increased almost 3 times to more than half of our DAU. This means that not only does Duolingo have a much higher number of active users now, but also that those users are much more likely to keep coming back, refer their friends, and subscribe to Super Duolingo.”

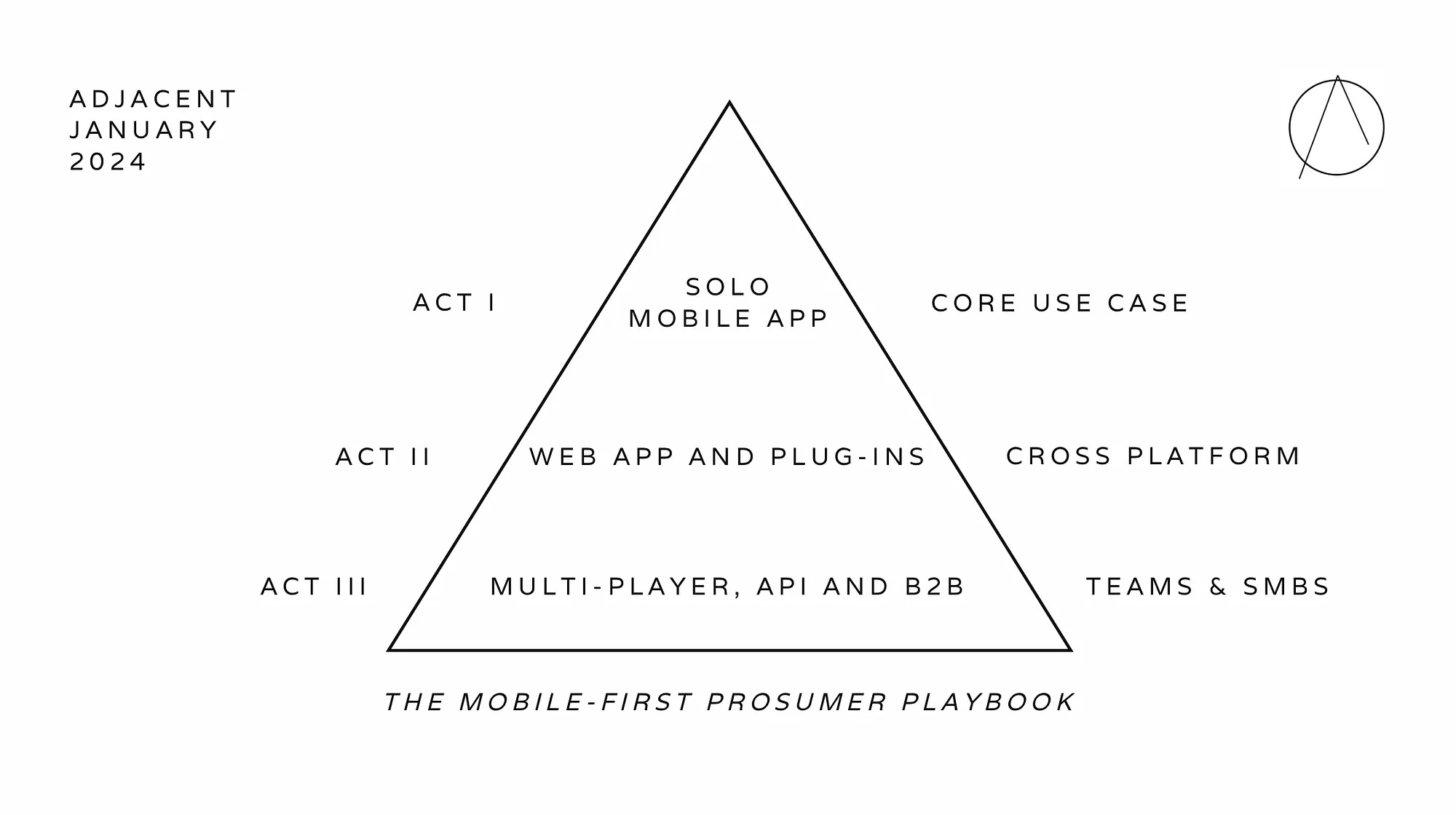

Thursday, Dec. 21st: Nico Wittenborn shared a playbook on how prosumer mobile app can expand their addressable market by becoming cross platform (mobile app, web, plugins) and by addressing teams (multi-player, APIs, B2B). - Nico Wittenborn

“The advantages of starting out with a focused mobile team are clear: They only require a small team, limitations force simplicity, it is frictionless to launch to 175+ countries via the app stores and annual subs have a strong cash flow advantage (ideally paying back CAC on day 1). This often means reaching positive cash flow much earlier than other venture funded companies, giving founders the opportunity to choose when to raise.”

“Cross platform usage always increases engagement and retention for those users that adapt both and it also facilitates better targeting and helps to drive up margins (via Stripe vs AppStore payments). This step can also significantly enhance the core product experience.”

Friday, Dec. 22nd: Fred Wilson wrote a retrospective of what happened in 2023 and shared some predictions for 2024. - Fred Wilson 1, Fred Wilson 2

“2023 will most certainly be remembered as the year that AI went mainstream with consumers, thanks to Chat GPT and other consumer interfaces to large AI models.”

“The end of the 2022/2023 tech/startup downturn happened when two things came together. The first is the end of a period of rising interest rates that had sent the stock market and broader capital markets reeling. The second is the emergence of a new tech megatrend, AI, which has been developing in front of our very eyes for as long as I have been in tech, so that is over forty years now”

“Before something can become mainstream, it takes a consumer interface that allows everyone to see the power of the technology firsthand.”

“As we enter 2024, the capital markets have found their footing and are moving higher. The Fed has taken interest rates as far as they want at this time and inflation has come down. It seems that a “soft landing” is likely.”

“I have never seen an environment with more innovation in the forty years I have been in the tech sector. It is breathtaking to see.”

“With the AI stack well developed and supported, we are moving into the application era of AI, much like the browser brought us the application era of the web and the iPhone brought us the application era of the mobile device. This is a big deal. While in 2023, everyone was rightly focused on the large language models like OpenAI, Anthropic, Gemini, Llama, etc, we will see new AI-first applications emerge in 2024 that will start to move the focus and the conversation up the stack. And we will see legacy applications embrace AI to make their products better and to remain competitive with the AI-first disrupters.”

“In addition, we are seeing many large firms scale back or even shut down. And new firms are struggling to raise funds. This is a rationalization of a sector that got very big very fast in the last decade and will need time to find a new normal. Because venture funds have a ten-year life but often take much longer to fully liquidate, the venture capital business changes more slowly than the businesses it funds. I think we are a couple years into a transition that will take at least the first half of this decade to play out.”

“While the capital markets will likely be robust in 2024, I do not expect that venture capital investing and venture capital fund formation to grow that much year over year in 2024.”

Saturday, Dec 23rd: I read Goldman Sachs’ initiation coverage on Instacart.

Instacart is leveraging two secular trends: “1) the potential for delivery platforms to enable the digital transition of the grocery industry as consumers increase their adoption of online channels and 2) the rise of retail media networks as an area of growth within the broader digital advertising industry that can continue to attract greater ad/promotion budgets over time.”

“Key risks include: uncertainty around near-term order growth given the normalization of customer behavior post-pandemic, slowing grocery inflation and lower government benefits; questions around normalized GTV growth medium-term; concerns about market share/competitive intensity; customer concentration risk; the impact of a slower rate of advertising revenue growth on revenue/profits; potential overhang from the expiration of employee lock-ups; volatility caused by the global macroeconomic environment & investor risk appetite for growth stocks.”

“In 2022, the North America grocery market was sized at $1.6tn of which ~$170bn was spent online (11% of total). We expect that North America online grocery sales will grow at a +16% CAGR between 2023 and 2028 as consumers increasingly lean on online channels for more meal occasions and as the industry continues to invest against this evolution in consumer preferences. Our forecasts have online grocery penetration reaching 21% in 2028.”

Sunday, Dec. 24th: Countdown is shutting down. It’s an early stage fund focused on hard tech industrial startup which backed companies like K2 Space, Hadrian and Galvanick. Countdown had raised a first $3m fund and a second $15m fund. - Techcrunch

“Funding industrial startups is not inefficient enough to justify our existence and that larger, multi-stage venture firms are best positioned to generate strong returns on the most valuable industrial startups.”

“A 50-100% price difference at the pre-seed and seed stage is immaterial to a multi-stage firm managing billions of dollars, but can and should be the difference between a yes and no for a firm of our size.”

Monday, Dec. 25th: Ed Suh wrote about current trends in the venture industry. - Ed Suh

“VC is a mainstream industry now. No longer a cottage business of a handful of small collections of partners in Menlo Park, it is transforming in a parallel path that its cousins in private equity, hedge funds, investing banking, all went through. With that come growing pains: compression of low hanging alpha, increased scrutiny from the broader public, including regulators, and increased responsibilities as its influence has grown.”

“Doug Leone recently described how the venture industry has morphed from a high margin artisan business to a low margin mainstream business. […] Traits that used to differentiate firms and provide alpha on their own - specialization, hustle, founder friendliness, marketing, portfolio services - are all arguably table stakes today. Every venture firm in existence does all the above at least reasonably well. […] Some combination of extreme contrarianism, extreme specialization, and highly differentiated strategy/network, are necessary for new firms to even try to compete today.”

Tuesday, Dec. 26th: I listened to a Turpentine VC’s podcast episode with Sam Lessin who is GP at Slow about what will happen in 2024. - Turpentine VC

“The factory model of VC is over. It’s the idea that startups could raise subsequent rounds of funding and go public at high multiples while providing liquidity along the way.”

VC should be about high risk innovation capital. Over the last decade, something changed dramatically in the venture model. We started to believe that the venture industry would be able to produce an unbelievable number of public decacorns outcompeting legacy companies and that we just had to work backward from inception to IPOs on a funding model to produce these outcomes. Today, it turns out that the public market no longer want these companies (burnt by the SPAC bubble, best tech companies can remain private eternally, big tech platforms capturing most of the upside).

“Venture capital on easy mode is over. It was never there in the first place. We believed that VC would become an asset management business which let it scale a ton more that it otherwise would have and let a thousands of people work in venture that otherwise would have never worked in VC.”

“Venture is not the best way way to make a dollar in the world in finance. It’s just the most interesting.”

“When interest rates are low, there's a lot of money looking for returns right. What happens is that the money goes further and further out the risk curve and looks for weirder and weirder in places to put money.”

It’s wrong to think that there is an infinite good number of companies and that every industry will be disrupted. At any moment in time, there is going to be a tiny number of important companies with the potential to become the next tech platforms.

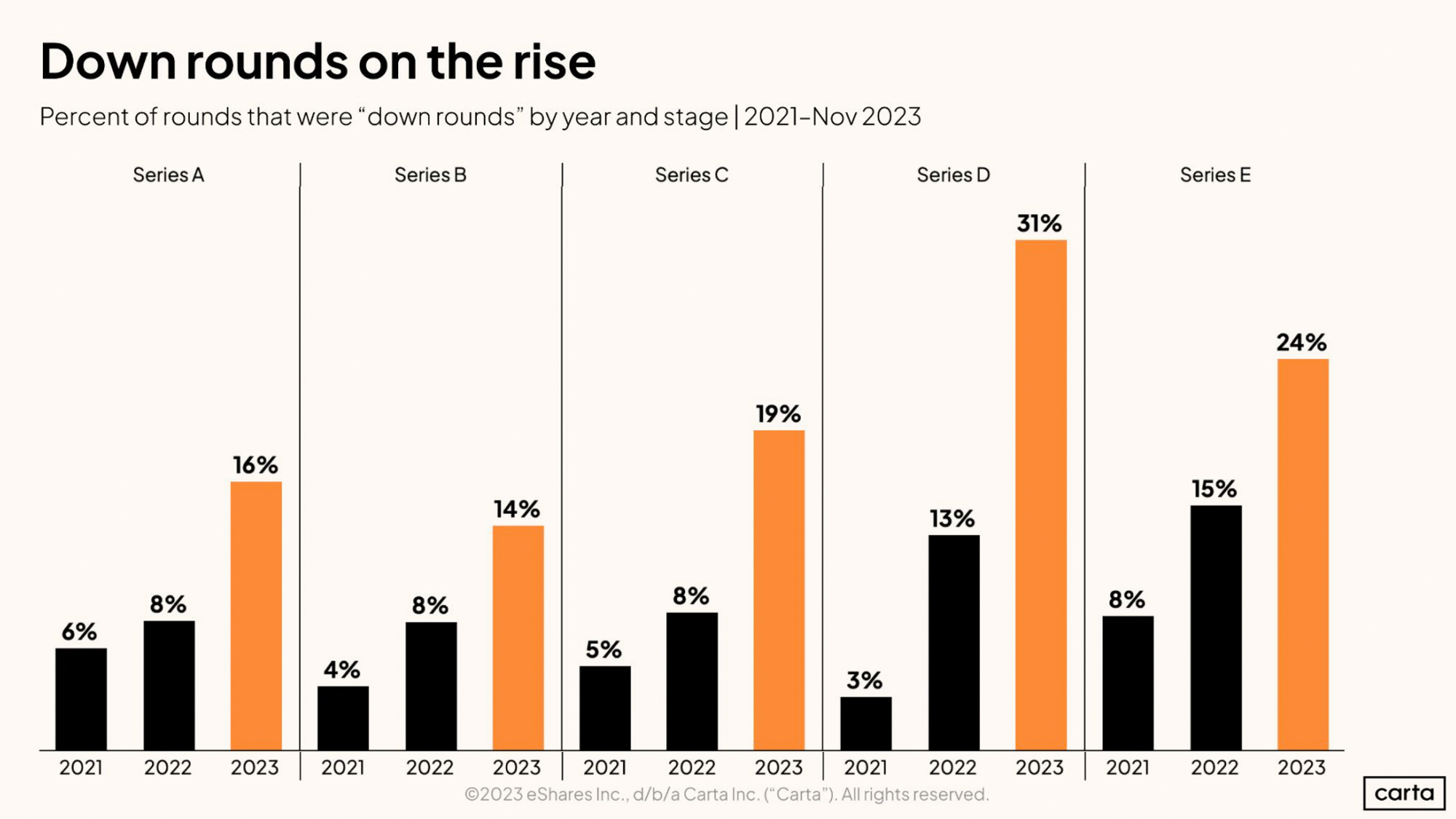

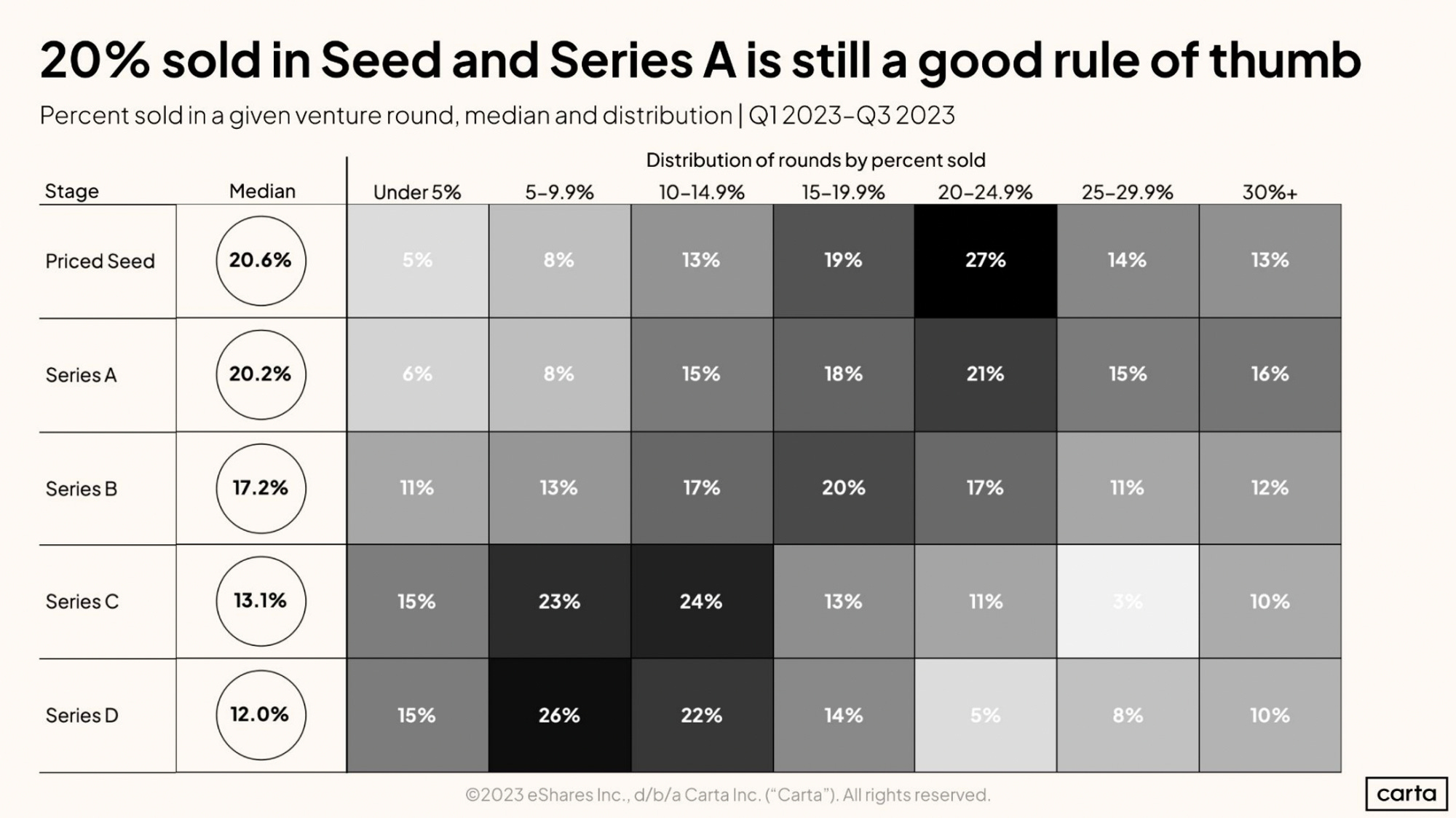

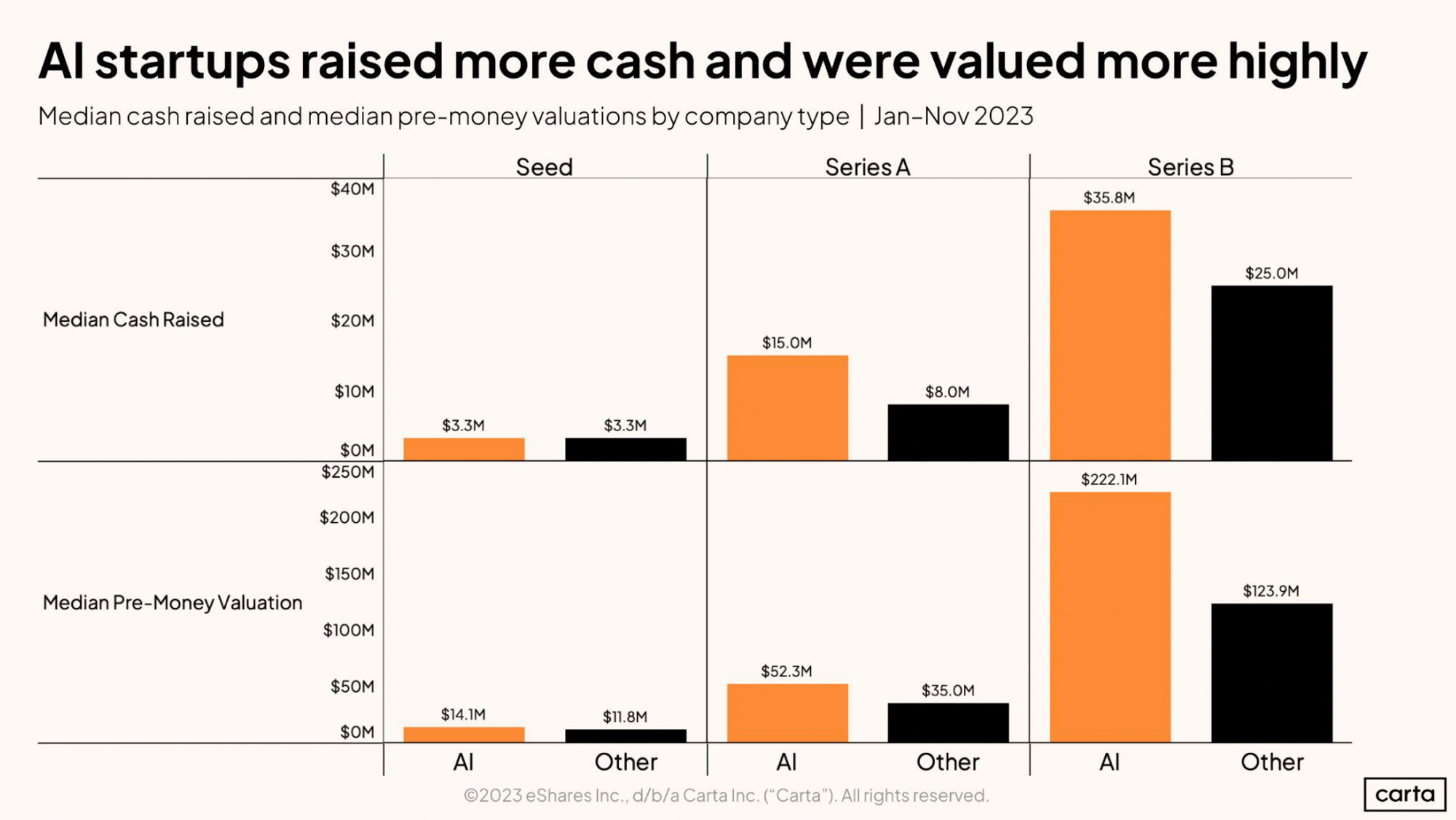

Wednesday, Dec. 27th: Peter Walker published a 45-slide deck leveraging Carta’s data on what happened to US startups in 2023. - Peter Walker

“Valuations remained robust for seed and Series A companies while falling drastically for late-stage.”

Bridge rounds are exploding with 40% of series A (vs. 29% average in the past 5y) and 36% of series B (vs. 25% average) being bridge rounds. It’s the same story with downrounds. For instance, at series A, 16% of rounds were downrounds in 2023 (vs. 6% in 2022) and at series D, 31% of rounds were downrounds in 2023 (vs. 13% in 2022).

At seed, the median dilution is 20.6%. At series A, it’s 20.2%. At series B, it’s 17.2%.

There is a large premium in amount raise and pre-money valuation when you’re raising as an AI startup. For instance, at series A, you can raise 87.5% more at a 49% higher valuation.

Thursday, Dec. 28th: Nikhil Basu Trivedi asked many leaders in tech about their predictions for what will happen in 2024. - NBT

"The next big thing in 2024 will be businesses seeing material improvements in productivity from AI, with ARR per employee increasing 10-15%.” - Tom Tunguz (Theory Ventures)

“The next big thing in 2024 will be "Prototype to Production." In 2023 everyone was experimenting with AI. But there were lots of questions that limited the roll out of these experiments. What would they cost? Are they secure? What are the compliance risks? In 2024 a lot of these questions will be answered, and we'll see AI applications moving from experiments / prototypes / internal apps to large scale customer facing deployments.” - Jamin Ball (Altimeter)

“The next big thing in 2024 will be services becoming productized thanks to GenAI. Businesses like McKinsey and Accenture will face pressure to productize as tech-first startups like Mechanical Orchard offer their customers better, faster, cheaper outcomes enabled via GenAI.” - Jake Saper (Emergence)

“The next big thing in 2024 will be AI colliding with The Real Economy. I believe that more $10B outcomes in artificial intelligence will be with companies serving the Real Economy—we've already seen this with restaurants (Toast, Popmenu), Logistics (Flexport, Motive), Food (Instacart), and Finance (Nubank)—and leveraging AI at the application layer, rather than startups building in the infrastructure layer.” - Adeyemi Ajao (Base10)

“The next big thing in 2024 will be bridge rounds. While larger firms are chasing momentum rounds with valuations detached from fundamentals in AI, there will be a LOT of great companies with PMF, proven unit economics and strong growth, just not strong enough to get most of the multi-billion AUM funds excited. With reserves depleted for most insiders, outsiders will need to come in and find some great companies at reasonable multiples that will likely drive some amazing long-term returns. Great companies don't need to belong to hype cycles, they just need to be great companies.” - Rick Zullo (Equal Ventures)

“The next big thing in 2024 will be continued flight to quality by LPs. LPs are projecting capital calls to once again outpace distributions for 2024 as the exit market remains shut. This means I expect LP to continue to carefully assess their portfolios, digging in to understand the underlying health of their indirect companies and then selectively re’up’ing with managers they have conviction can generate outperformance. I also see a high potential in 2024 for the continued contraction in the number of venture funds raised and their size. Along with this, I anticipate seeing the retirement of some established investors countered by seeing a number of newer investors spin out to start the next generation of venture funds.” - Beezer Clarkson (Sapphire)

“The next big thing in 2024 will be the proliferation of retail media networks, expanding beyond the large players (Walmart, Amazon, Instacart, etc) into a longer-tail of retailers/marketplaces. We're seeing a perfect storm of factors: ATT/privacy-related challenges forcing demand-side channel diversification & supply-side use of 1P data, increased pressure to monetize, and more accessible rails to spin up in-house ad networks. One result of this: a broader set of marketplaces will have viable business models, as the critical scale for ads to work has lowered.” - Mike Duboe (Greylock)

Friday, Dec. 29th: Lazard and Elaia are partnering to launch a growth fund, and Lazard will progressively become Elaia’s majority shareholder. It’s another proof point of the great reshuffling currently happening in venture capital, with funds closing, merging, and reducing the size of their new vehicles. Elaia and Lazard will raise a growth fund of several hundred million, leveraging Lazard’s private wealth and institutional network. - Les Echos (🇫🇷)

Saturday, Dec. 30th: Michael Dempsey wrote about category creation in tech. - Michael Dempsey

“At this stage of technology development and penetration, whether you’re a technologist or capital allocator, if you’re not too early, you’re too late.”

“If the prior decade of technology as an asset class was about incumbent industries being swallowed up by tech, leading to an expansion of the market cap of “tech” as a category, than the next may be about disruption and market cap destruction within tech itself.”

“Categories are built around narratives that people hope will come true across a variety of fundamental property types (e.g. tech moats, margin profile, TAM expansion, industry turnover, new markets). Across all of these narratives the idea is that you can create new forms of distilled legibility around previously broadly illegible companies and then create multiple expansion either from increased capital flows and/or a belief in company superiority.”

“Like the early understanding of revenue quality and TAM in SaaS was a meaningful alpha generating opportunity for a period of time, there will likely be other categories that make many investors a lot of money. That said, due to the scale of venture capital and technology in 2024, the windows will be far smaller and the penetration of investors flocking to it will be stronger, creating faster feedback loops and tighter bubble windows”

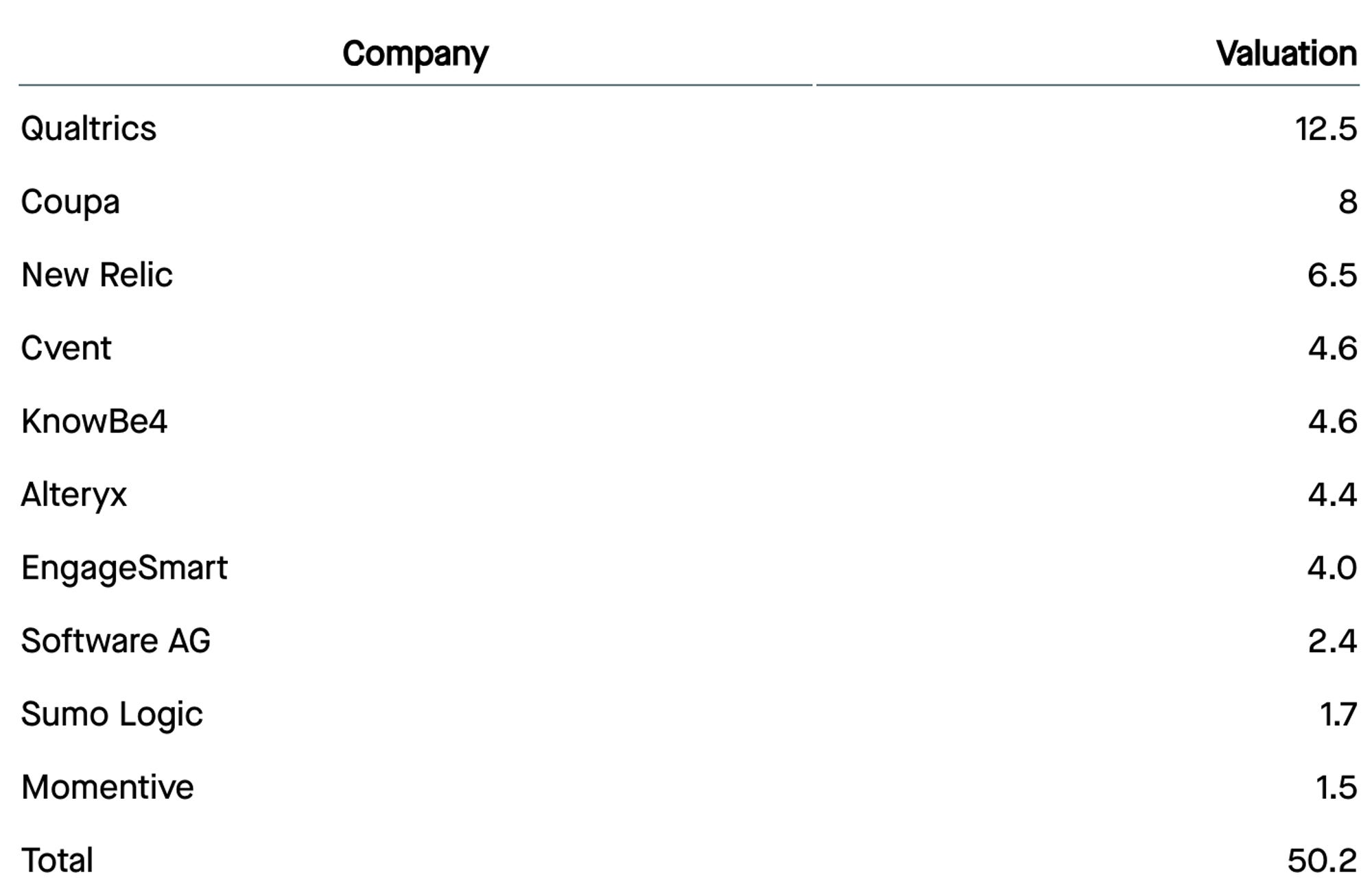

Sunday, Dec. 31st: Tomasz Tunguz argued that the tech M&A market will be active in 2024 driven by take-private transactions which had a strong momentum in 2023 and the rebound of strategic M&A transactions thanks to more sales predictability and lower stock volatility. - Tomasz Tunguz

“Venture-backed software M&A in the US, Canada, & Europe during 2023 totaled about $10b, about 20% of take-privates.”

In 2023, private equity funds acquired 10 publicly traded software companies for a total value of $50.2bn.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋