🗞 Venture Chronicles - December 2022

Overlooked #133

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of December.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for December!

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

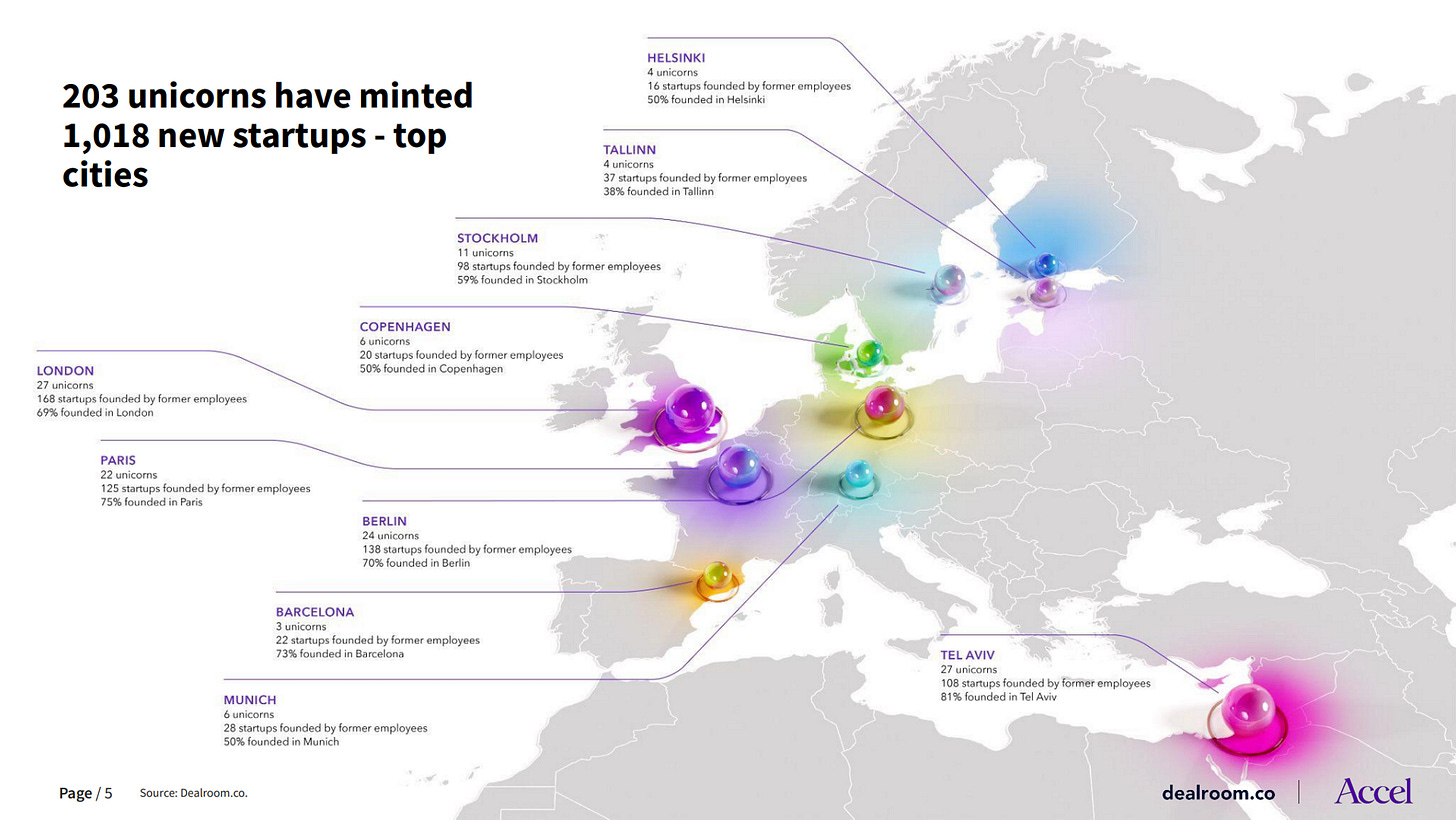

Thursday, Dec. 1st: Accel and Dealroom collaborated on a presentation on European unicorns startups mafias. - Dealroom

203 European unicorns have minted 1,018 new startups across Europe.

There are 344 VC-backed unicorns in Europe with 195 minted in 2021 and only 65 in 2022.

Criteo, Spotify and Delivery Hero created the most prolific startups mafias.

Friday, Dec. 2nd: Howard Marks published a memo on why it’s so hard to make macro forecasts. - Oaktree

“Forecasters have no choice but to base their judgments on models, be they complex or informal, mathematical or intuitive. When I think about modeling an economy, my first reaction is to think about how incredibly complicated it is.”

“How can a model of an economy be comprehensive enough to deal with things that haven’t been seen before, or haven’t been seen in modern times (meaning under comparable circumstances)?

“There’s simply no way to deal with the future that doesn’t require the making of assumptions. Small errors in assumptions regarding the economic environment and small changes in participants’ behavior can make differences that are highly problematic.”

“The bottom line is that the output from a model may point in the right direction much of the time, when the assumptions aren’t violated. But it can’t always be accurate, especially at critical moments such as inflection points . . . and that’s when accurate predictions would be most valuable.”

Saturday, Dec. 3rd: Mobile Dev Memo wrote about the future of mobile gaming in a post IDFA world. - Mobile Dev Memo

3 categories of transformations: evolutions (market level changes, revolutions (business model changes) and permutations (game design changes).

“ATT fundamentally alters the market for free-to-play mobile games: it impacts not just game design choices (permutation) or the ways in which monetization is implemented (revolution), but the fundamental character of the free-to-play gaming business model across distribution, monetization, and engagement.”

To adapt to this new paradigm, we’re going to see 3 fundamental changes: (i) the domination of centralised publishing services, (ii) the growing importance of personalisation for in game content & diversity of player journeys, (iii) increase the LTV of gamers with a systematic cross-promotion across a portfolio of games.”

Sunday, Dec. 4th: DoorDash laid off 1,250 employees, which represented 6% of its employee base. - DoorDash

"Prior to COVID-19, DoorDash was actually undersized as a company. The pandemic presented sudden and unprecedented opportunities to serve the evolving needs of merchants, consumers and Dashers. We sped up our hiring to catch up with our growth and started many new businesses in response to feedback from our audiences. Most of our investments are paying off, and while we’ve always been disciplined in how we have managed our business and operational metrics, we were not as rigorous as we should have been in managing our team growth. That’s on me. As a result, operating expenses grew quickly. Now, let’s acknowledge the macro situation. Our business has been more resilient than other ecommerce companies, but we too are not immune to the external challenges and growth has tapered vs our pandemic growth rates. While our business continues to grow fast, given how quickly we hired, our operating expenses – if left unabated – would continue to outgrow our revenue.”

“DoorDash has always been a resilient company. For the first half of our history, we were constantly cash-starved and under-resourced compared to our peers.”

“Looking ahead, we’re confident that we have reset the size and shape of our organization to match our strategic priorities. We must keep this level of discipline moving forward and act with the hunger, efficiency and creativity of the younger startup we once were while leading with the responsibility of the market leader we’ve become.”

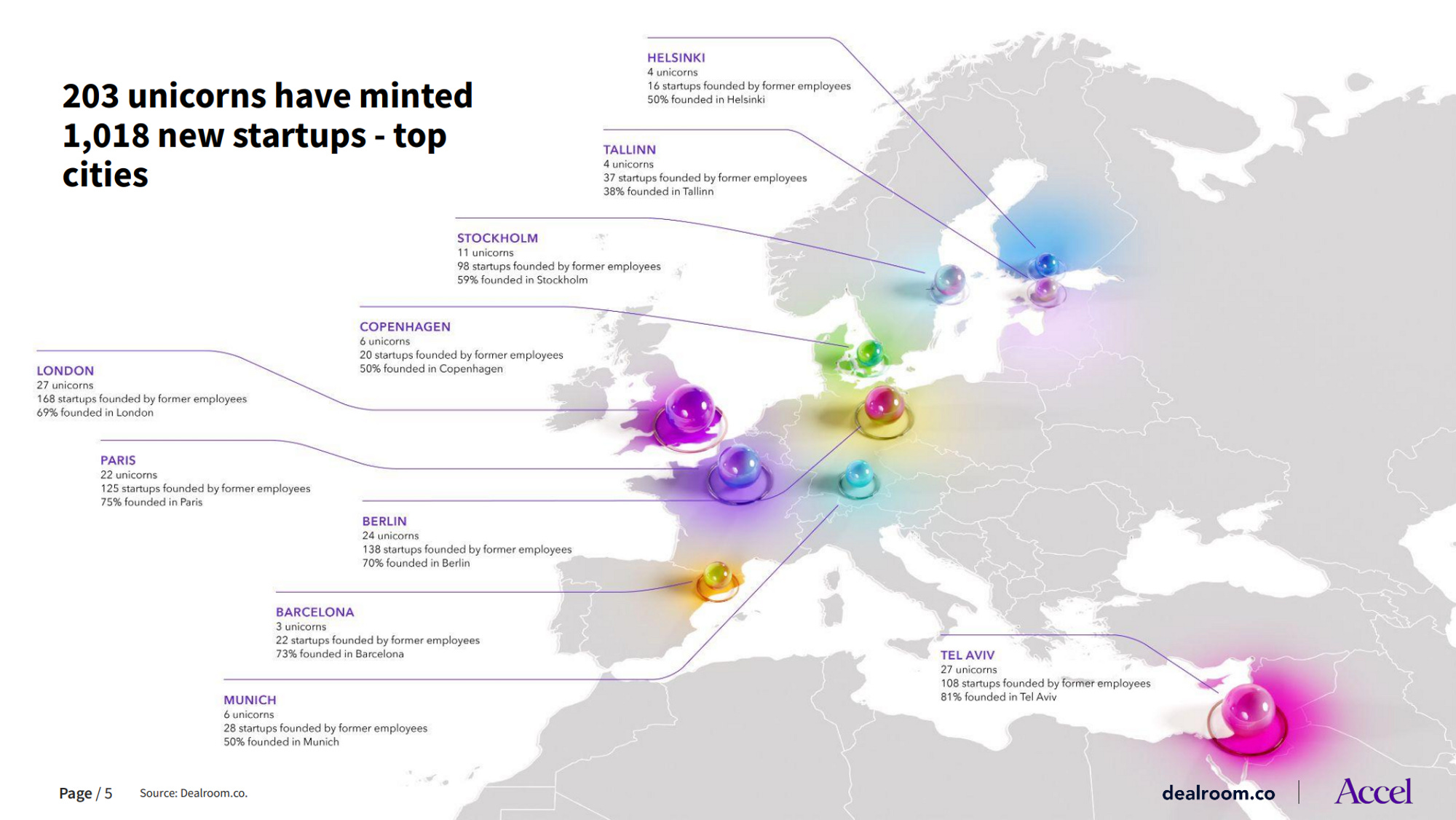

Monday, Dec. 5th: McKinsey published a global payments report. - McKinsey

“The vast majority of transactions that migrated to electronic channels in 2020 have remained electronic.” (e.g. 15% reduction in cash usage between 2019 and 2021 in Greece and 12% in Czech Republic)

Embedded finance (“the placing of a financial product in a non financial customer experience, journey, or platform”) generated $20bn in revenues in the US in 2021 and coud double in size in the next 3-5y.

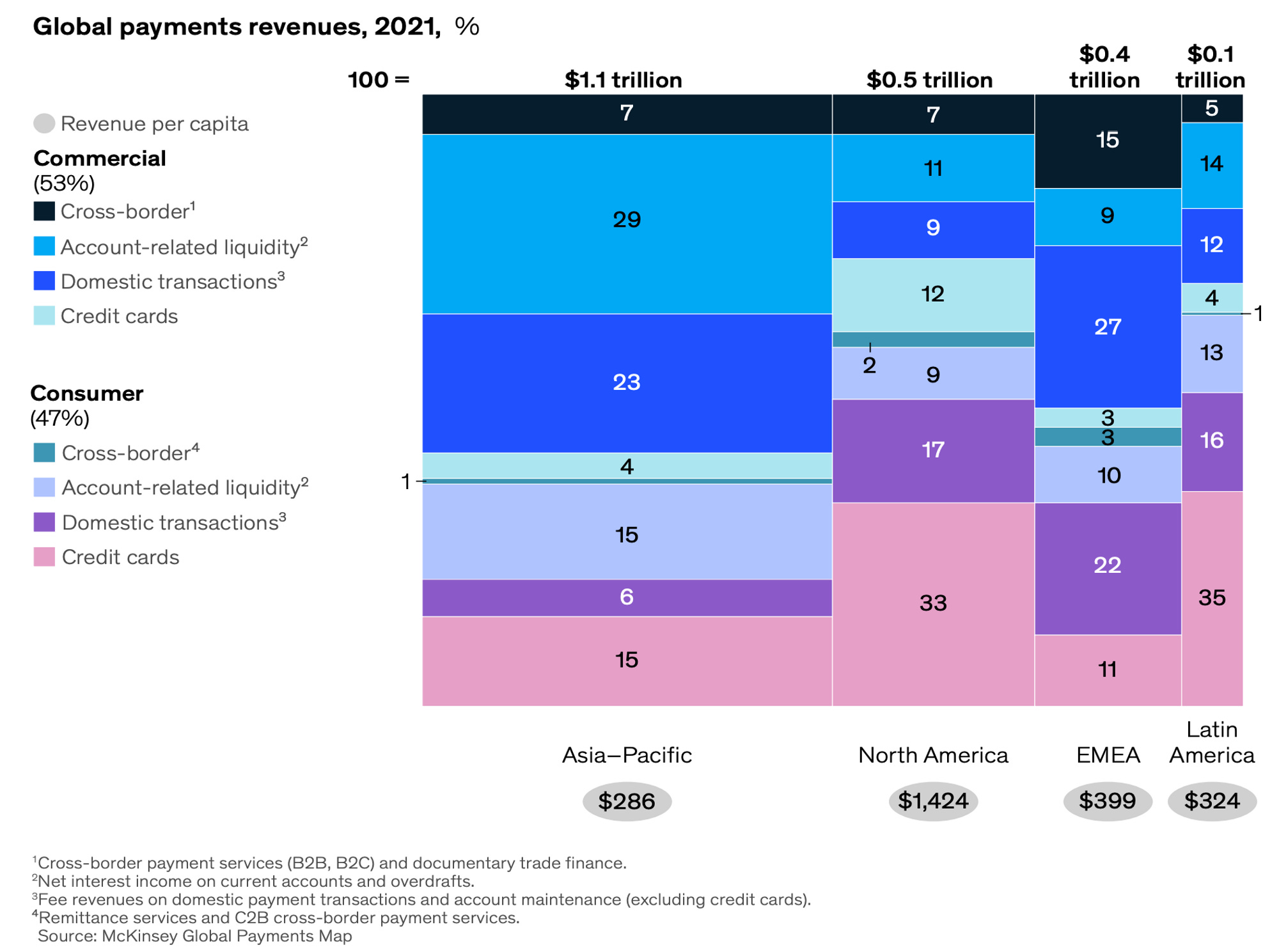

Tuesday, Dec. 6th: Dan Frommer published its 2023 consumer trends edition. - Dan Frommer

In the US, air travel and restaurant dining are almost back to pre-covid levels.

The average American spends 13 hours per day using technology and media (5h17 on video, 2h48 on audio, 1h3 in gaming). When we dig into apps, people spend more time on TikTok (98 minutes) than on any other apps (e.g. 76 min on Youtube, 53 min on Facebook and 52 min on Instagram).

More than 1/3 of Gen. Z and Millennials say they are very lonely.

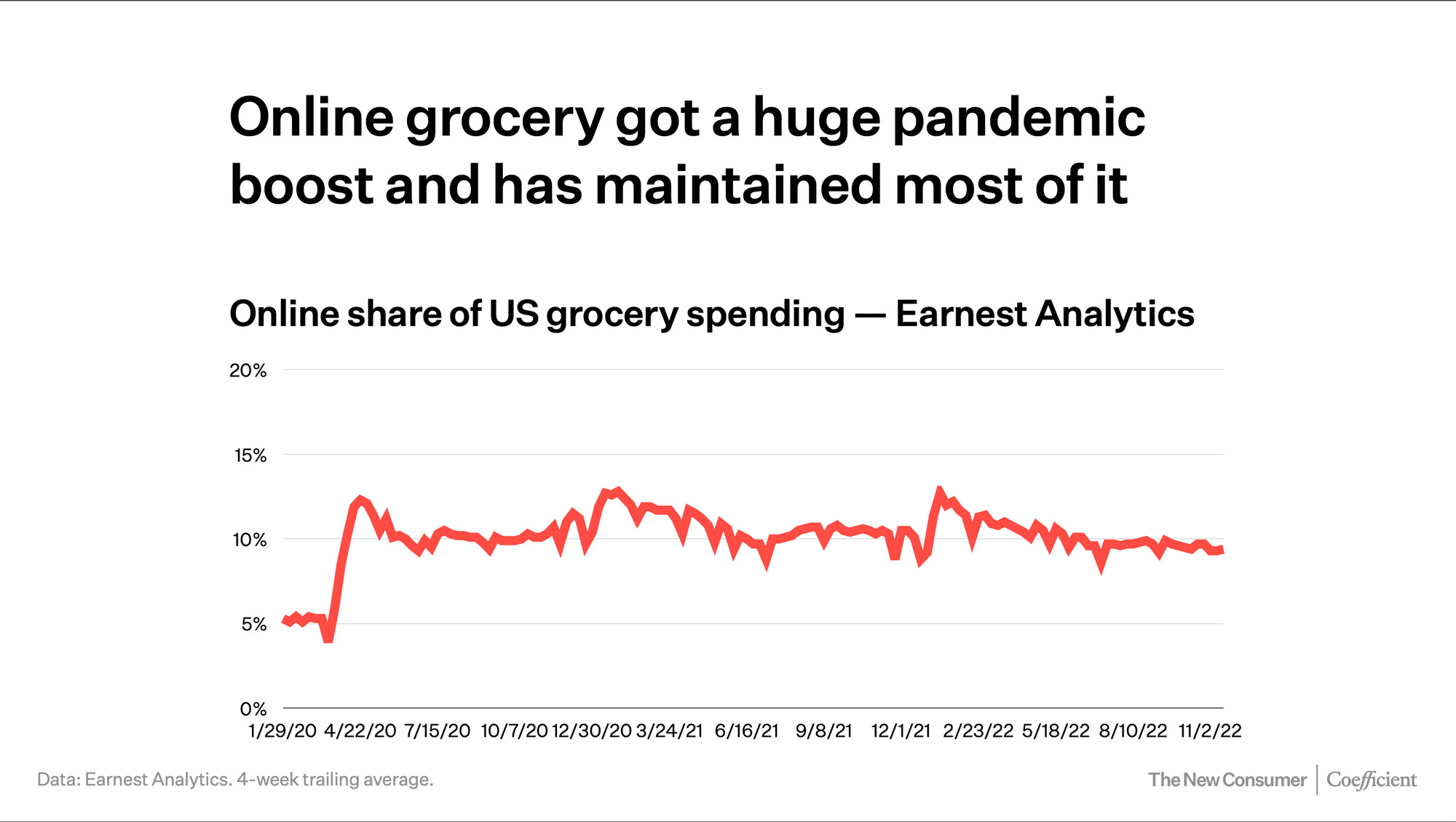

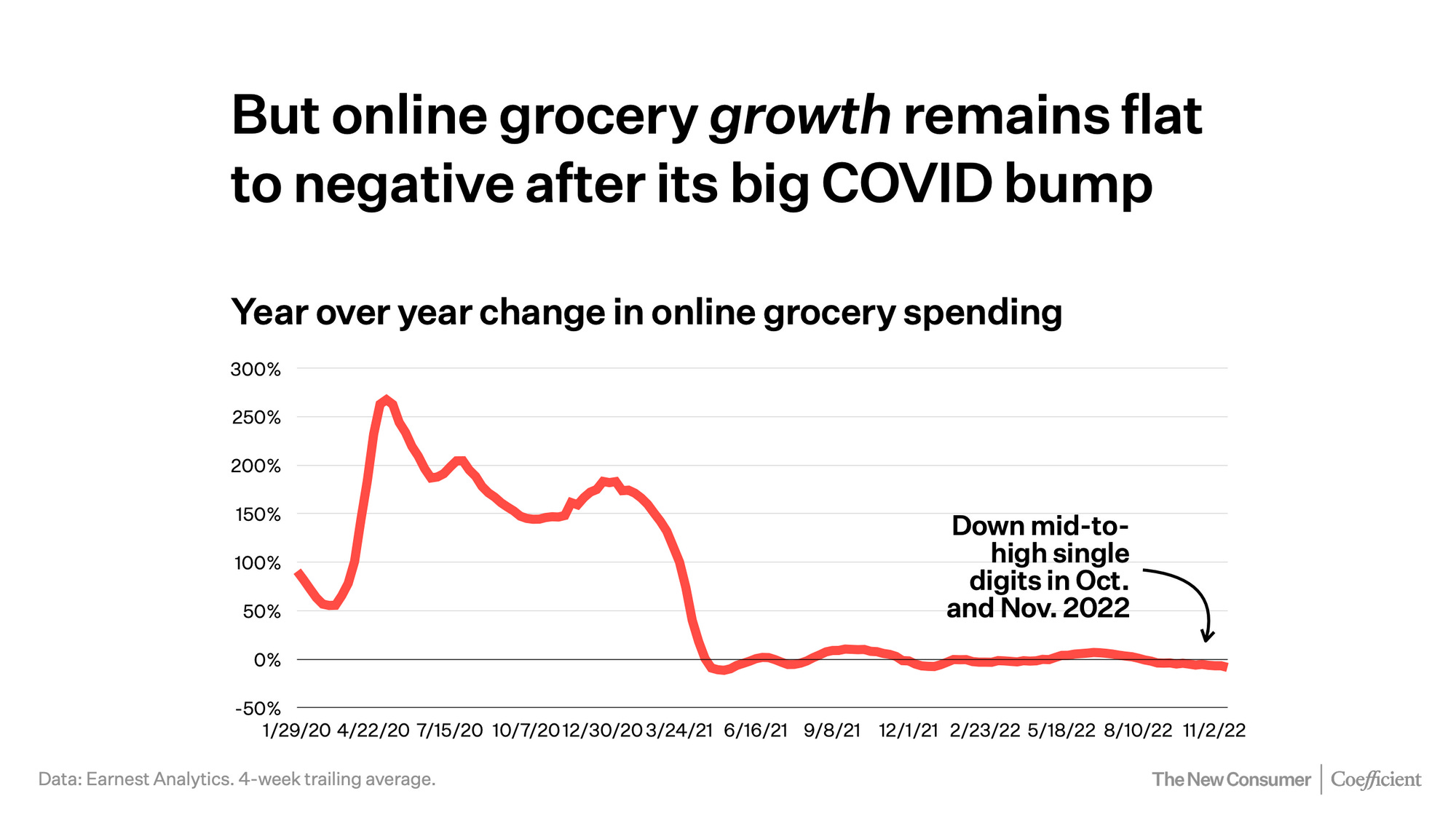

Online penetration in the grocery sector is sticking at c.10%. Year on year, growth is flat to negative. With covid, Instacart increased its market share from 50% to 75%.

Wednesday, Dec. 7th: Microsoft’s $69bn acquisition of Activision-Blizzard is being challenged by antitrust authorities in the US, the UK and in Europe. The acquisition could redistribute the cards in the console market in which Xbox is lagging behind PlayStation and the Nintendo Switch especially if Microsoft makes some Activision Blizzard’s games exclusive to Xbox (e.g. Call of Duty which is played by 45% of PlayStation owners). Moreover, it will strengthen Microsoft’s dominant position in subscription services in which it has already a 40% market share mainly driven by its GamePass offering. - The Economist

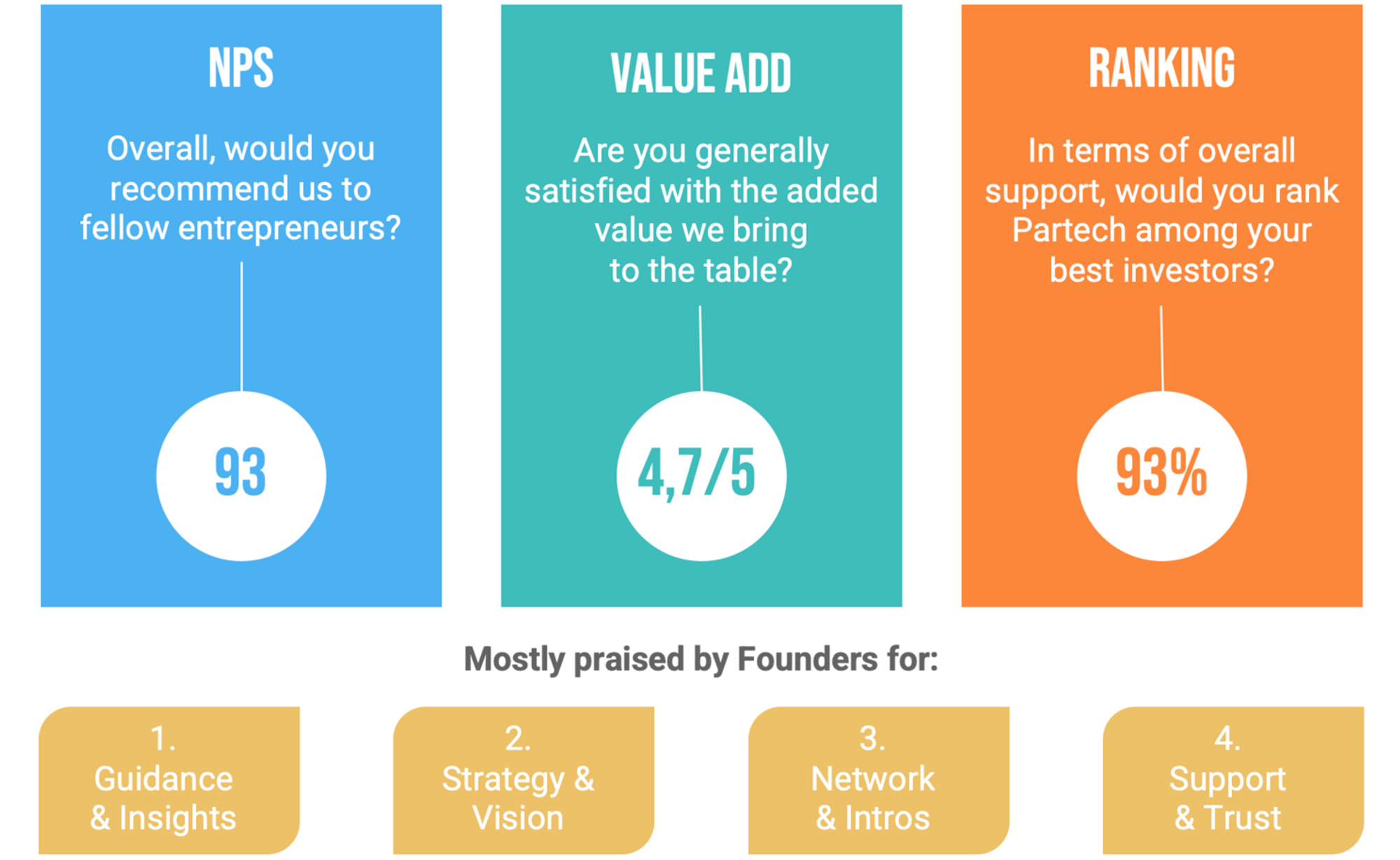

Thursday, Dec. 8th: Partech raised €120m for its 4th seed fund. It will invest in 50 companies with initial tickets between €300k and €3m combined with the potential to reinvest until series B. Partech backed companies at seed stage like Alan, Jellysmack or Sorare. 100 entrepreneurs (inc. 35 backed by Partech) are investing in the seed fund as LPs. It’s a generalist fund investing all over the world. It will actively look at investment themes including climate change, economic inclusion, health, mental well being and privacy first technologies. - Tech.eu, Boris Golden

I like Partech’s 4 main pillars as a seed fund: (i) getting in touch with founders as early as possible in their journey, (ii) forming strong and independent conviction about companies, (iii) offering financial backing to match the needs of founders at the most formative stage of their company, (iv) supporting founders on the existential challenges they will face to bring their idea to life and prepare for the journey ahead.

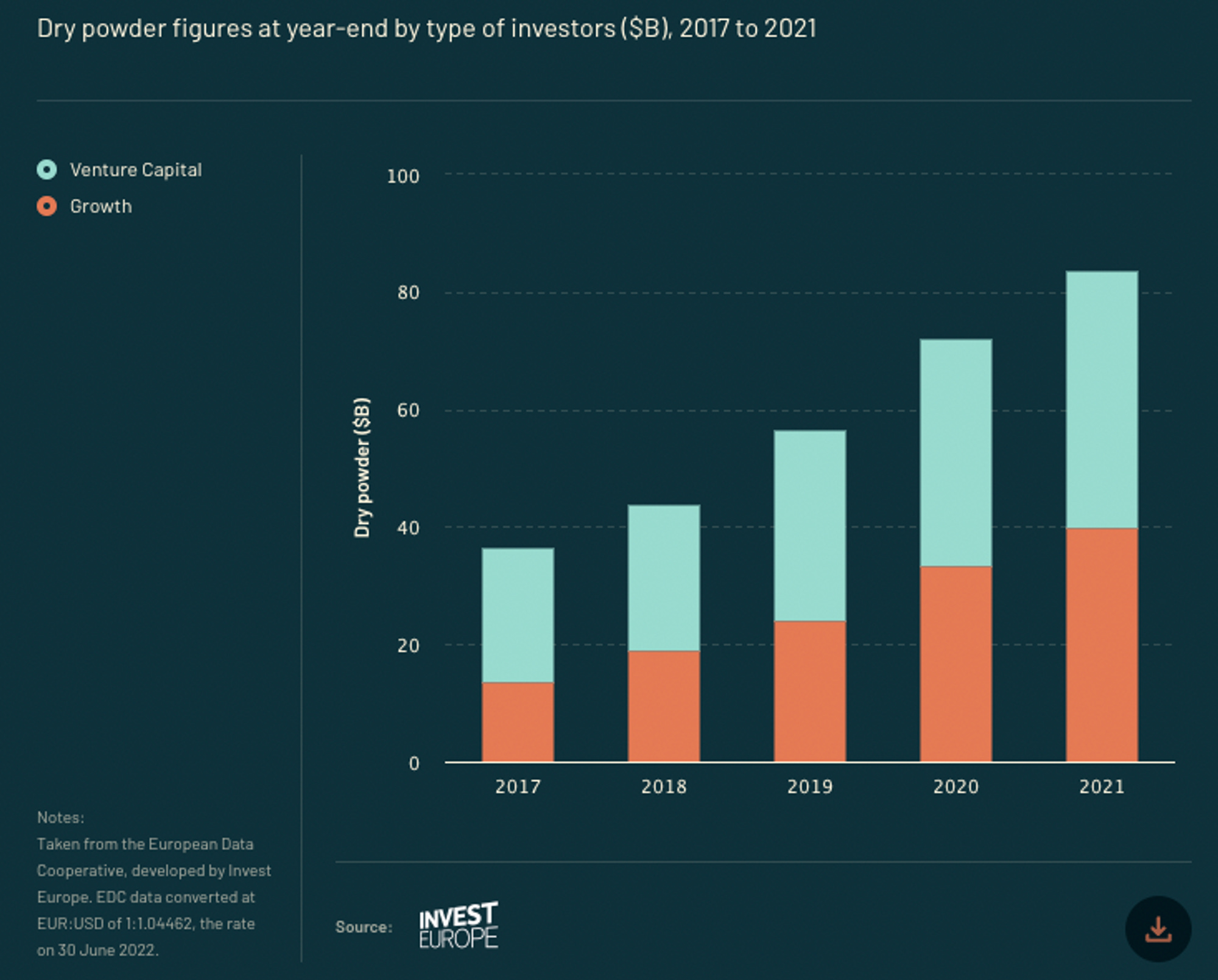

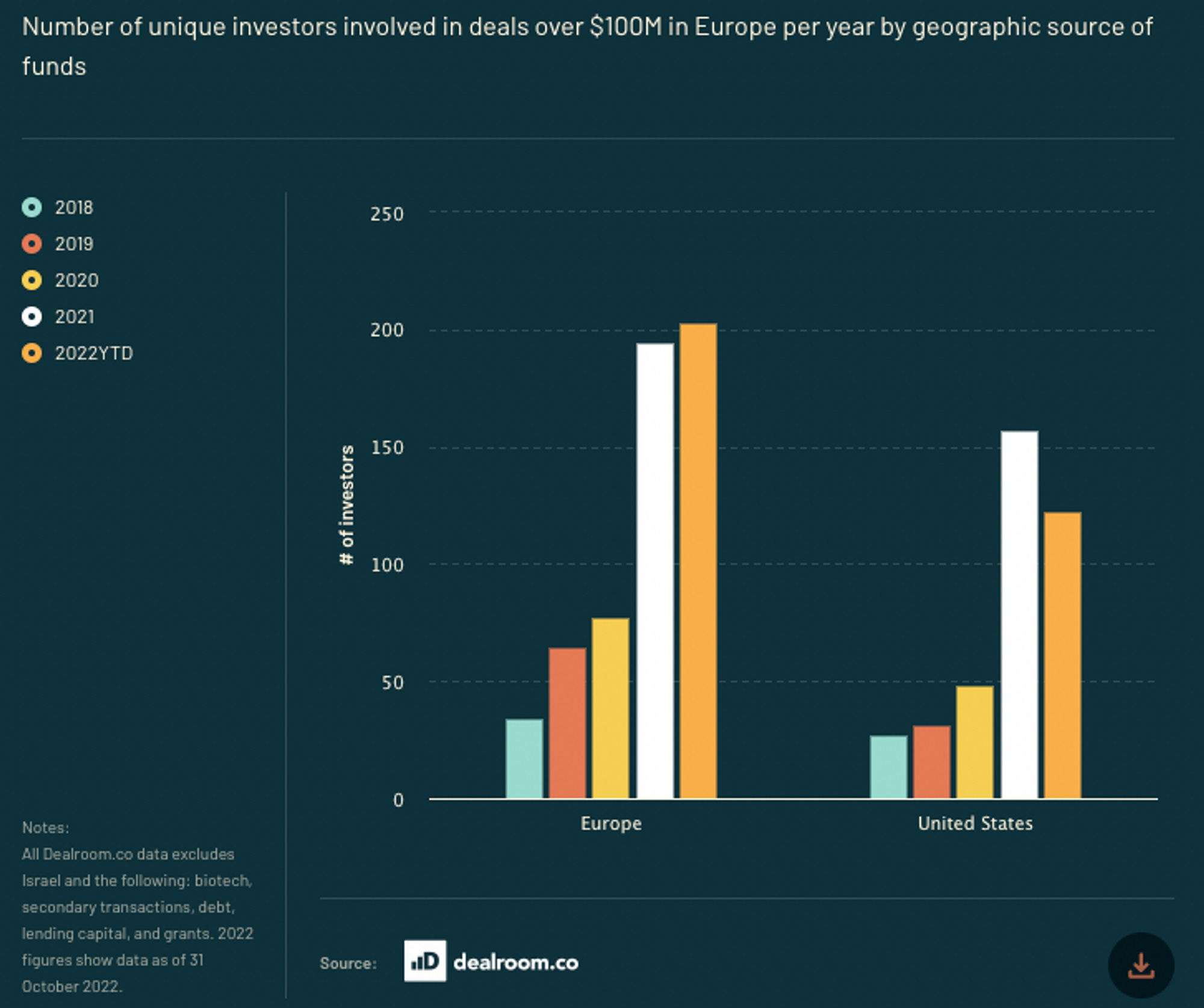

Friday, Dec. 9th: I read Atomico’s 2022 State of European Tech Report. - Atomico

At the end of 2021, European venture & growth investors sat on dry powder totalling $84bn which is the highest amount ever recorded.

In 2022, the total amount raised by European startups declined from $104bn to c.$85bn (18% decline YoY).

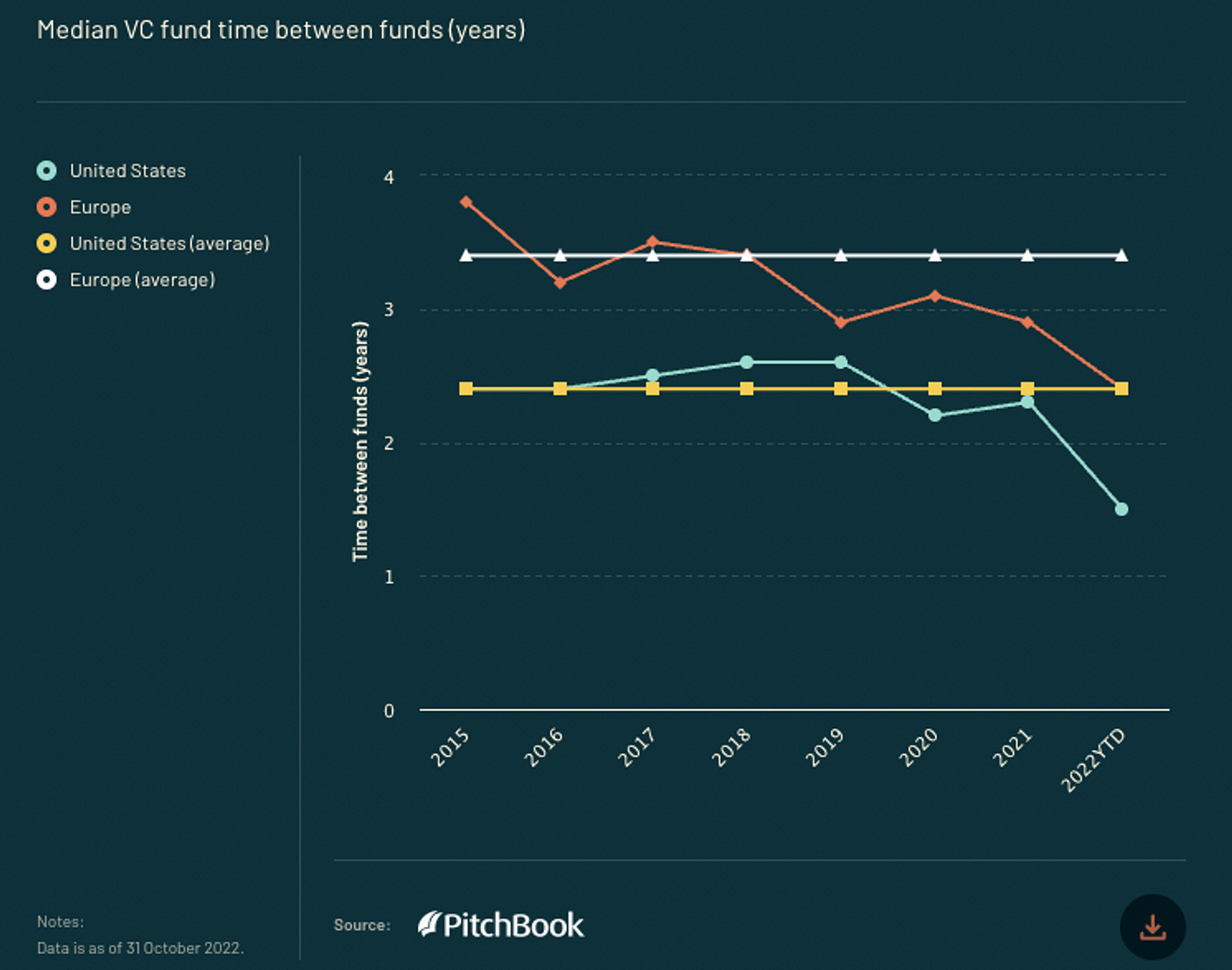

In the past couple of years, venture funds accelerated their deployment pace from 3.5 years in Europe down to 2.4 years increasing the amount of capital deployed per year by 50%. In 2023, this trend will reverse as GPs will slow down their investment pace.

82% of founders believe that it has become harder to raise venture capital in 2022 compared to previous years.

YTD, only 31 unicorns were minted in Europe compared to 105 in 2021.

Europe has a resilient investor base. In 2022, more than 3.2k different investors invested in Europe compared to 3.4k in 2021.

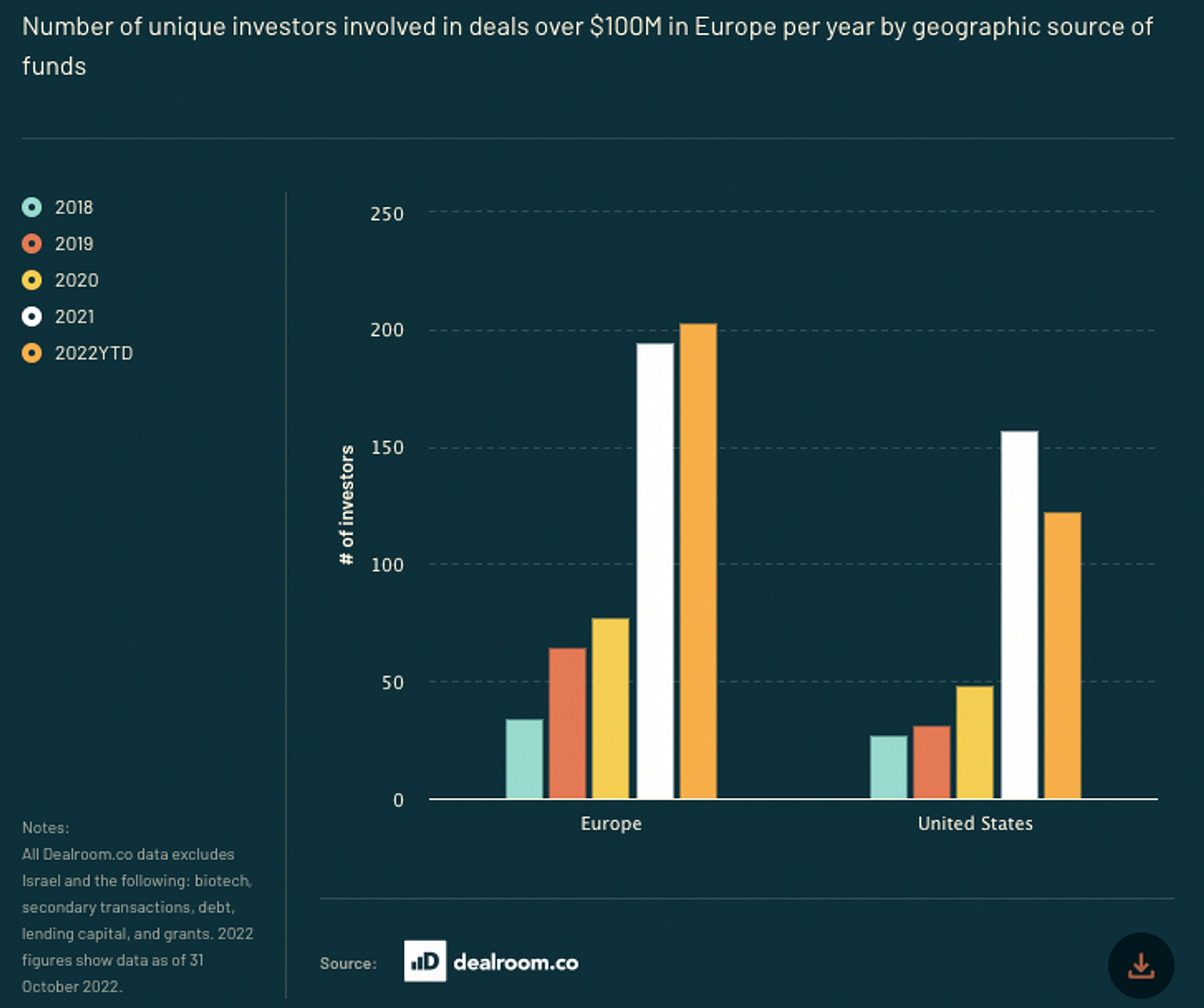

At later stages, US investors are pulling back: less US investors were involved in $100m+ rounds in 2022 compared to 2021.

The IPO window is closed with only 3 $1bn+ tech IPO both in Europe and in the US in 2022.

The digitalisation of the European economy is still in its early days: (i) 50% of the European population does not have basic digital skills, (ii) only 55% of European SMBs have reached a basic level of digitalization (using at least 4 digital technologies to run their business) and (iii) 40% of large European entreprise have low or very low digital intensity.

The tech ecosystem in Europe is maturing with 53% of founders and leaders with multi-generational experience (having worked at 2+ tech companies). 39% of founders have already built 1 company before and 17% 2 companies before.

On average, a founder has a 27% ownership at seed stage, 18% at series A, 14% at series B and 9% at series C.

Atomico updated its chart showing a misalignment between what founders want from VCs and what VCs think founders want from them.

Saturday, Dec. 10th: The Economist wrote about the current investing environment. - The Economist 1, The Economist 2

Post GFC, investors became used to a low inflation / interest rates environment pushing investors to find high-returns in risky asset classes such as stocks, buyout or venture capital.

There are 3 rules in this new environment with scarcer capital available and higher interest rates: (i) expected returns are higher, (ii) investors’ horizons have shortened, (iii) investment strategies will change (protection portfolio against inflation, reduce allocation in riskier asset classes).

Sunday, Dec. 11th: USV raised a $200m climate fund n°2 to invest in early stage startups reducing/removing emissions and providing adaptative solutions to climate change. - USV, The Information

Monday, Dec. 12th: Private-equity firm Thoma Bravo raised $32bn across 3 funds: (i) $24.3bn for Thoma Bravo Fund XV (large cap. buyout), (ii) $6.2bn for Thoma Bravo Discover Fund IV (mid-cap buyout) and (iii) $1.8bn Thoma Bravo Explore Fund II (lower mid cap buyout). Thoma Bravo is specialised in the tech sector with expertises in the following domains: healthcare, financial services, security, infra, apps. In 2022, Thoma Bravo acquired high profile tech companies such as UserZoom, Anaplan, Sail Point and UserTesting. - Techcrunch, Thoma Bravo

Tuesday, Dec. 13th: eFounders is evolving into a meta-startup studio called Hexa. Today, Hexa has 3 studios: eFounders focused on SaaS/future of work, LogicFounders focused on fintechs and 3founders focused on web3. It aims at launching studios in other areas including healthcare, climate, education, AI, property and agriculture. Each studio has an operational team with experts in product, design and marketing. - Hexa

Wednesday, Dec. 14th: Lux Capital published its Q3-2022 LP Report. - Lux, Josh Wolfe

“Our top 10 active portfolio holdings today have more than $4bn in cash on their balance sheets.”

“Over the years, Lux has started de novo, founded or co-founded nearly 20 companies in varied sectors [automation aerospace, defense, energy, biotech, physics], often singular standouts and with high ownership for small dollars - and we will be doubling down on this approach in the years ahead.”

“Amidst much chaos present and yet to come, the set of opportunities now forming may be the greatest we have seen in a decade.”

In the past quarters, Lux shared the following messages to their portfolio companies: (i) “raise as much money as you can as quickly as you can because whatever is happening now won’t last”, (ii) “hold onto that cash making it last longer and spending it more wisely”, (iv) “don’t spend on growth but instead if you do spend, spend on consolidation.”

Lux is deploying 3 investment strategies: (i) bubble (giving companies 30 months of cash to be isolated from the macro environment), (ii) anti-bubble/special situations (restructuring weak cap. tables in strong companies), (iii) consolidation (doubling down on companies in position to consolidate their markets).

Thursday, Dec. 15th: Sacra published interviews with two founders of vertical SaaS for restaurants: Chris Webb who is CEO and cofounder at ChowNow (restaurant ordering & delivery platform) and Hadi Rashid who is CEO and cofounder at Lunchbox (restaurant marketing & ordering platform). - Sacra 1 for Lunchbox, Sacra 2 for ChowNow

“COVID was a huge tailwind for DoorDash/Uber Eats, but it drove down the margins of newly delivery-reliant restaurants to 1-2%. Now, vertical SaaS for restaurants like Lunchbox and ChowNow are positioning against the aggregator model with their blended take rate of ~11% vs. 30%.”

“Restaurants have the opportunity to monetize as brands—centered around but not limited to food—to make revenue outside their 4 walls, via memberships, loyalty programs, D2C wine clubs, catering, events & classes, and ghost kitchens (1500+ in the US).”

“DoorDash has built out vertical SaaS interoperable with a restaurant’s owned SaaS stack—giving restaurants access to their massive logistics network as well as a family of products including capital (DoorDash Capital), healthcare (via Sesame), and staffing (via LANDED) they need to operate.”

Lunchbox is an online ordering platform for restaurants combined with loyalty/marketing to engage with customers. It charges a SaaS fee and a processing fee per transaction which is way cheaper than the 20-30% delivery fee that you have to pay to third party delivery platforms.

“The future for POS systems should look somewhere between where it is today (i.e. with terminal) and where Amazon Go is. It should be somewhere in the middle […] more automated [and] less dependent on a lot of manual entries.”

In 5-10 years, “We want Lunchbox to be an all in one ordering system. Whether you purchase all your integrations through Lunchbox and build your own custom solution or you buy everything out of box, we want to be that centralized source of that customer data.”

“Restaurants are increasingly thinking about how they can drive business revenue from outside their four walls.”

The Point of Sales (PoS) is the cornerstone of the restaurant tech stack. With covid, a massive migration towards cloud-based PoS has started with solutions like Toast, Square or Clover.

Restaurants don’t like third-party delivery platforms because they’re expensive and they keep customer data.

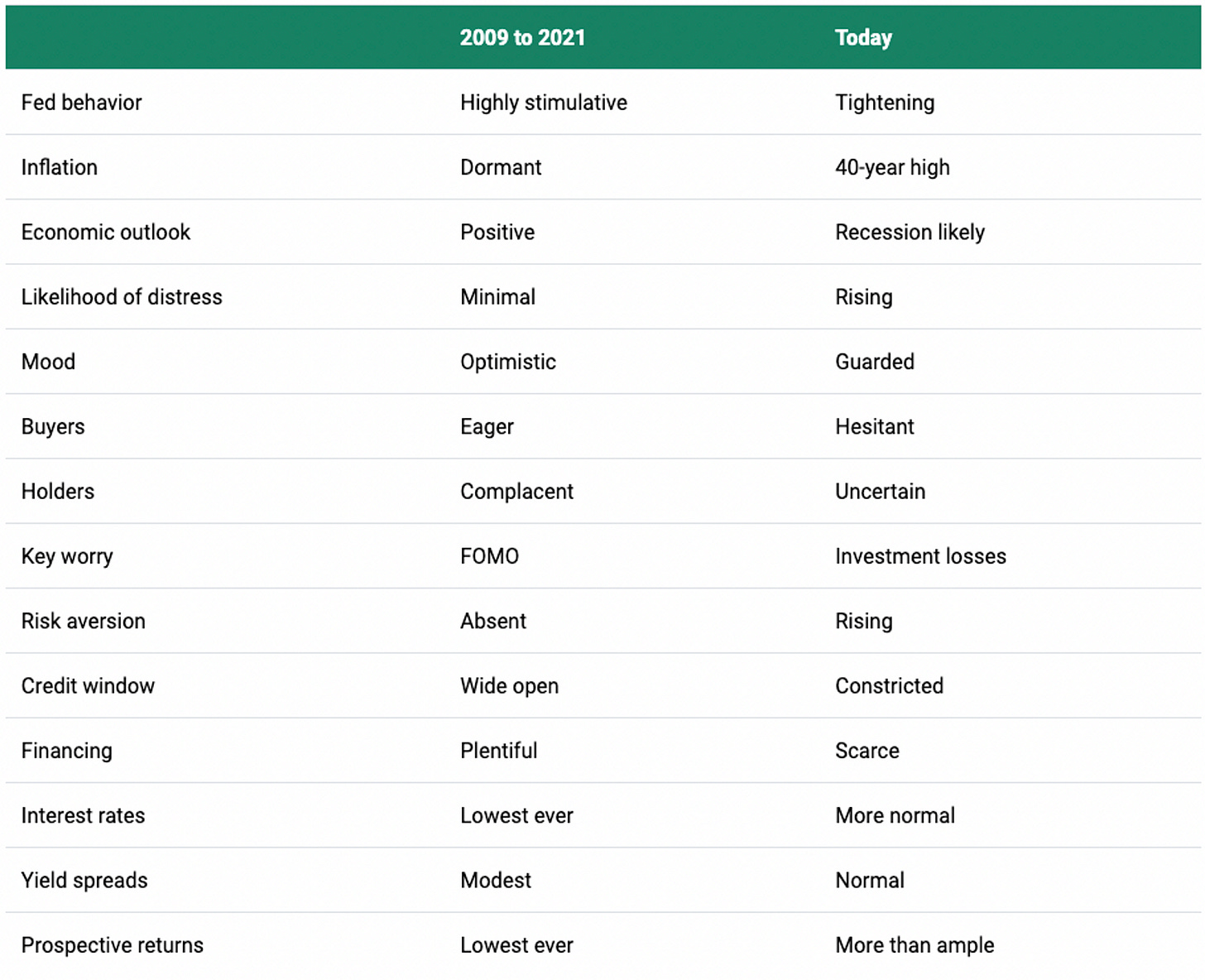

Friday, Dec. 16th: Howard Marks published a new market memo called Sea Change. - Oaktree

“It’s no exaggeration to say today’s investment world bears almost no resemblance to that of 50 years ago. Young people joining the industry today would likely be shocked to learn that, back then, investors didn’t think in risk/return terms. Now that’s all we do.”

“It seems to me that a significant portion of all the money investors made over this period resulted from the tailwind generated by the massive drop in interest rates.”

“A recession in the next 12-18 months appears to be a foregone conclusion among economists and investors. That recession is likely to coincide with deterioration of corporate earnings and investor psychology. Credit market conditions for new financings seem unlikely to soon become as accommodative as they were in recent years.”

“We’ve gone from the low-return world of 2009-21 to a full-return world, and it may become more so in the near term. Investors can now potentially get solid returns from credit instruments, meaning they no longer have to rely as heavily on riskier investments to achieve their overall return targets. Lenders and bargain hunters face much better prospects in this changed environment than they did in 2009-21. And importantly, if you grant that the environment is and may continue to be very different from what it was over the last 13 years – and most of the last 40 years – it should follow that the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead.”

Saturday, Dec. 17th: Chris Neumann (GP at Panache Ventures) wrote about VC funds pushing founders to shut-down or sell their companies after overfunding them in 2020-2021 in order to get back some cash to be reinvested in their portfolio or in new companies. - Chris Neumann

“I’ve spoken with multiple founders who took investments from large multi-stage funds in 2021 or 2022 and whose investors have approached them about selling or shutting down the company. All of these startups have years of runway and are growing and progressing at a solid pace (albeit slower than they were last year). The founders have done everything they were “supposed to”. They hit their milestones, raised over-subscribed rounds, took preemptive capital when it was “on the table” and now they’re being punished for it by the very investors who pushed them to raise more.”

“In order to convince founders to preemptively sell or shut down their companies, these investors will offer them life-changing money. All they need to do is give up their entrepreneurial aspirations, screw over their employees, customers and early investors, and potentially ruin their reputations.”

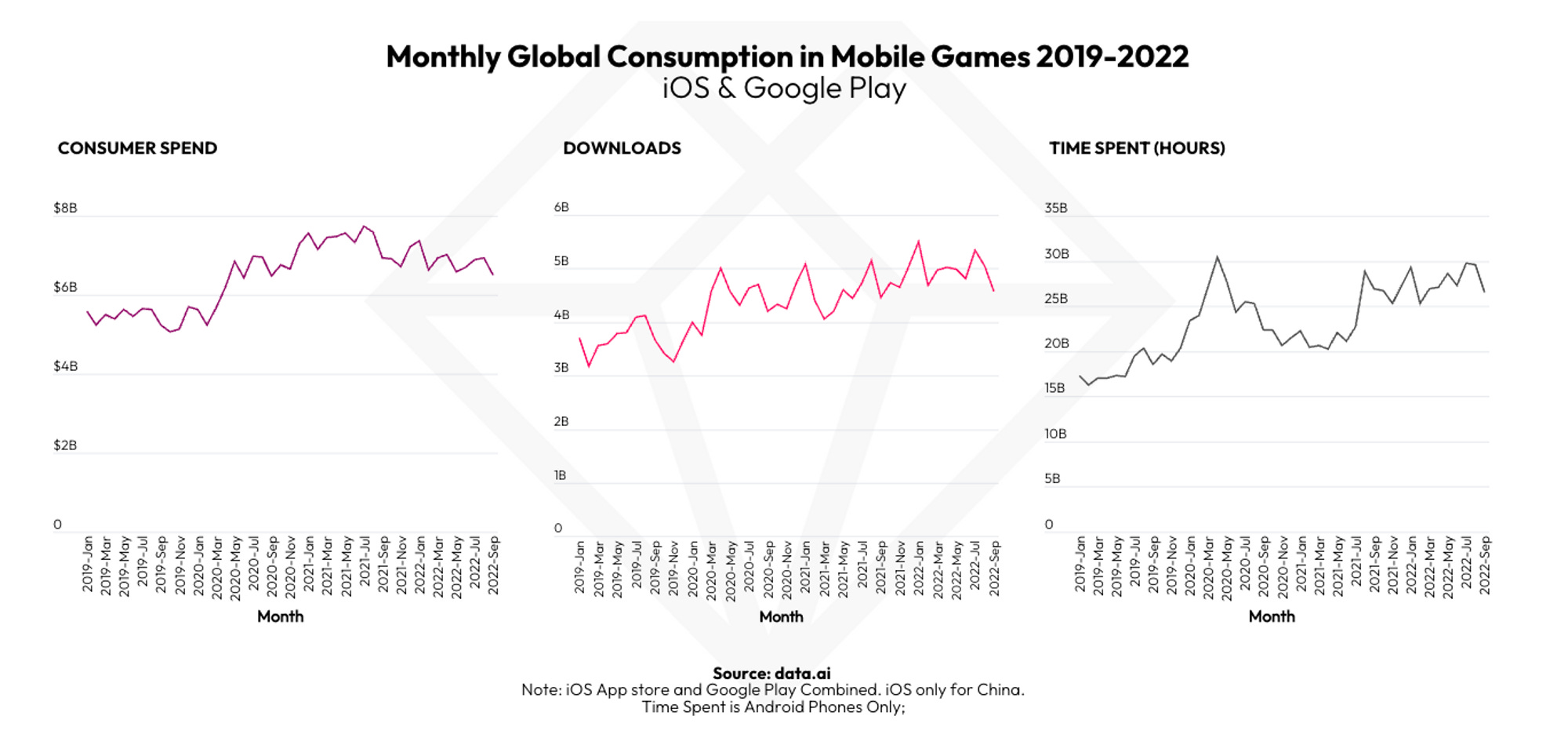

Sunday, Dec. 18th: Data.ai and Deconstructor of Fun wrote about the state of mobile gaming in 2022. - DoF, Data.ai

In H1-22, mobile gaming generated 30.0bn downloads (vs. 26.9bn in H1-21) and $41.2bn in revenues (vs. 44.5bn in H1-21).

In 2022, mobile gaming was impacted by privacy changes and a decrease in engagement in a post-covid world.

It was a consolidation year with mobile gaming publishers acquiring advertising technologies to have a better control on their data.

On hypercasual, “Google Play’s policy on banning intrusive ads will likely impact negatively the genre. Overall, the trend toward hybrid monetization is visible as the IAP revenues are up by a whopping 30% since the beginning of the year.”

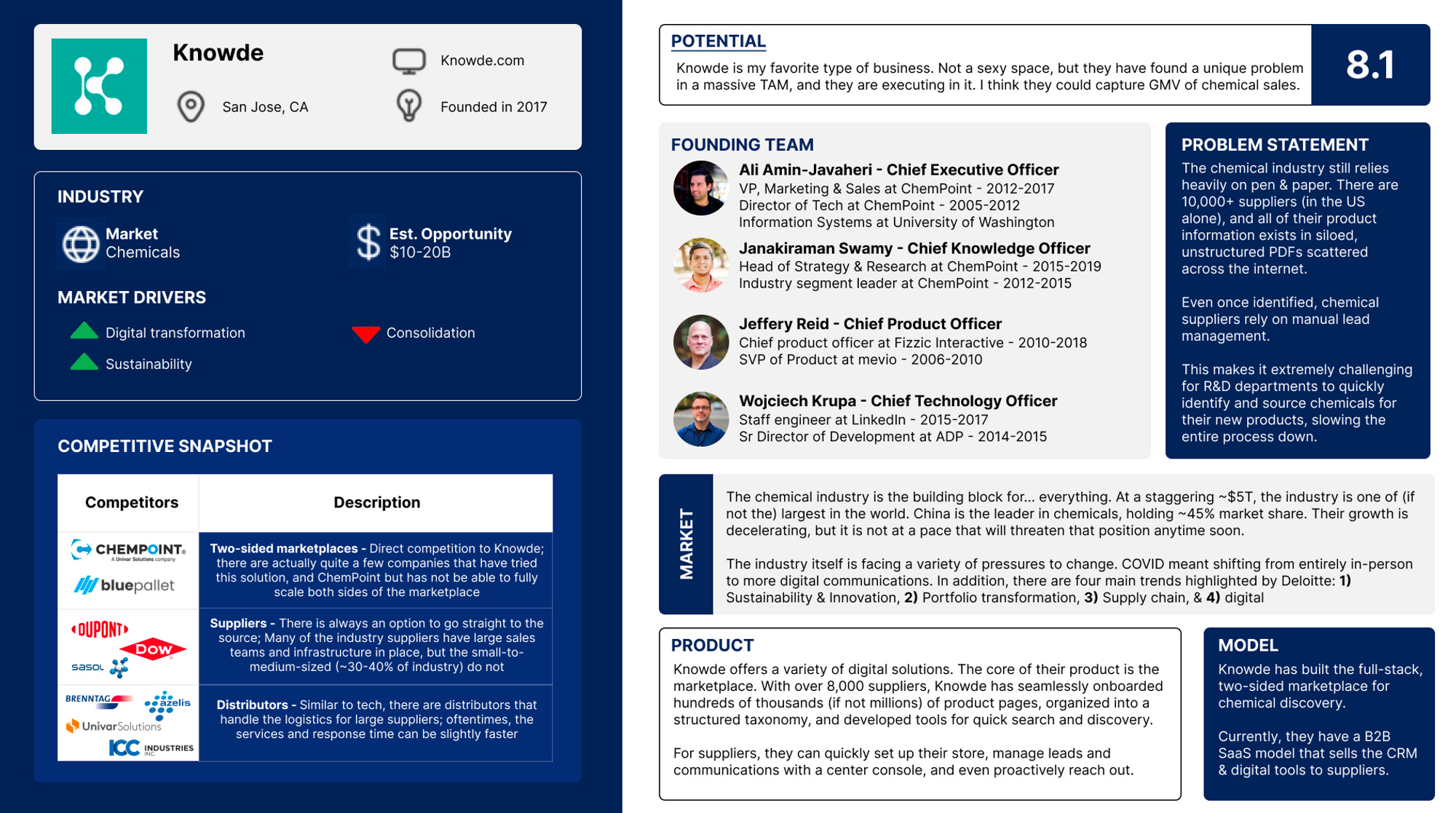

Monday: Dec. 19th: Contrary Research and Jeff Burke wrote aboute Knowde which is a SaaS-enabled B2B marketplace in the chemical industry. It started in the US in 2017. It raised $91m in total including a $72m series B in Aug. 2021 led by Coatue. - Jeff Burke, Sequoia, Contrary Research

Knowde has onboarded thousands of suppliers with their product catalogue organised in a structured taxonomy making it easy for buyers to search and peruse. Knowde sells a CRM to suppliers built on top of their store in order to generate and manage leads.

On its marketplace, Knowde has 8k suppliers, 100k products, 10k buyers conducting on average 295k searches and 1.2k quotes per months.

“In the chemical industry product discoverability was limited to physical product catalogs and PDFs. By putting all product information online along with search filters and online payments capabilities, Knowde significantly reduces the sales cycle and search costs for both sides.”

“As a chemicals marketplace, Knowde serves two primary customers: (1) ingredient, polymer, and chemistry suppliers and (2) R&D professionals and buyers of those ingredients, polymers and chemicals.”

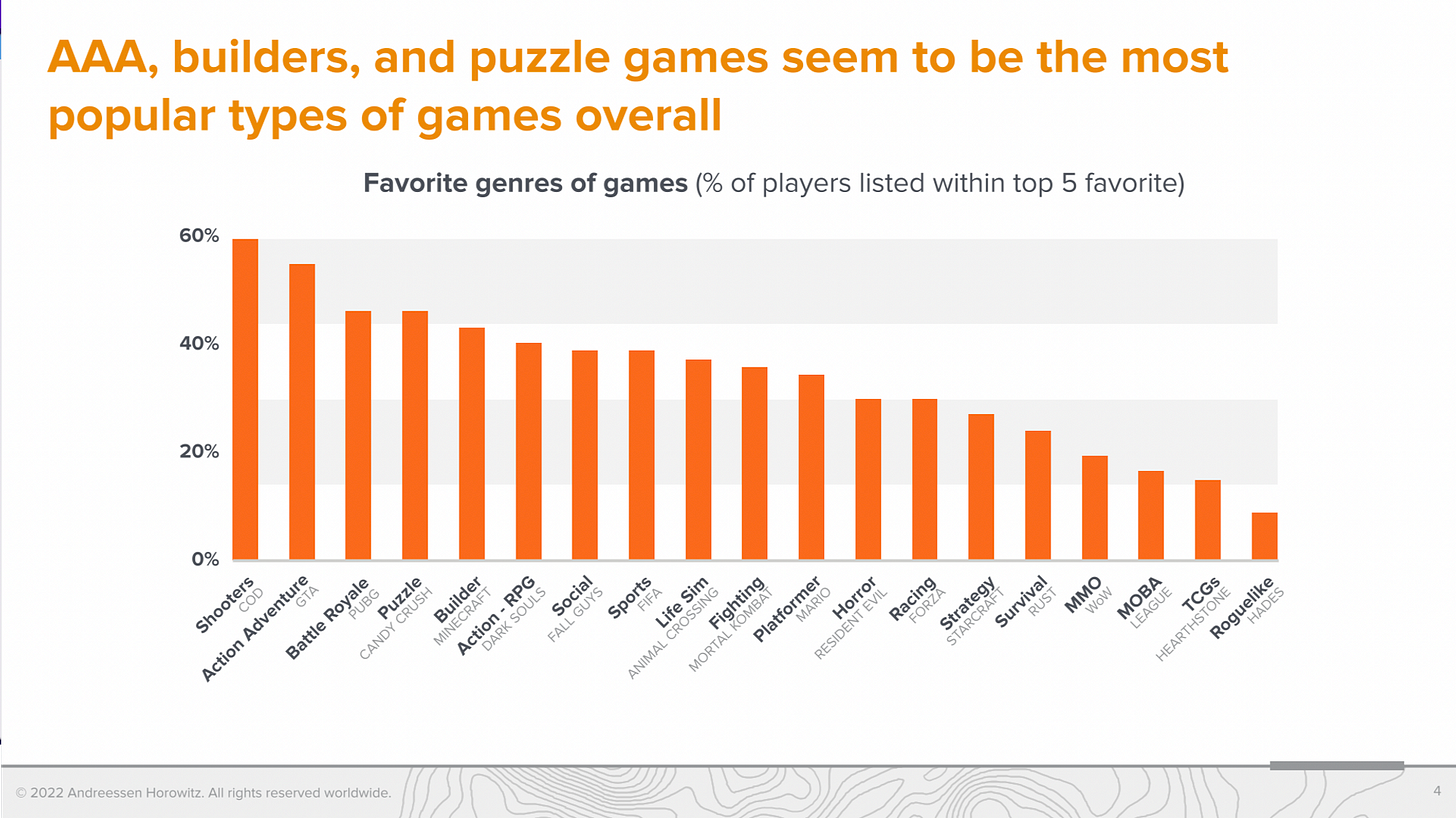

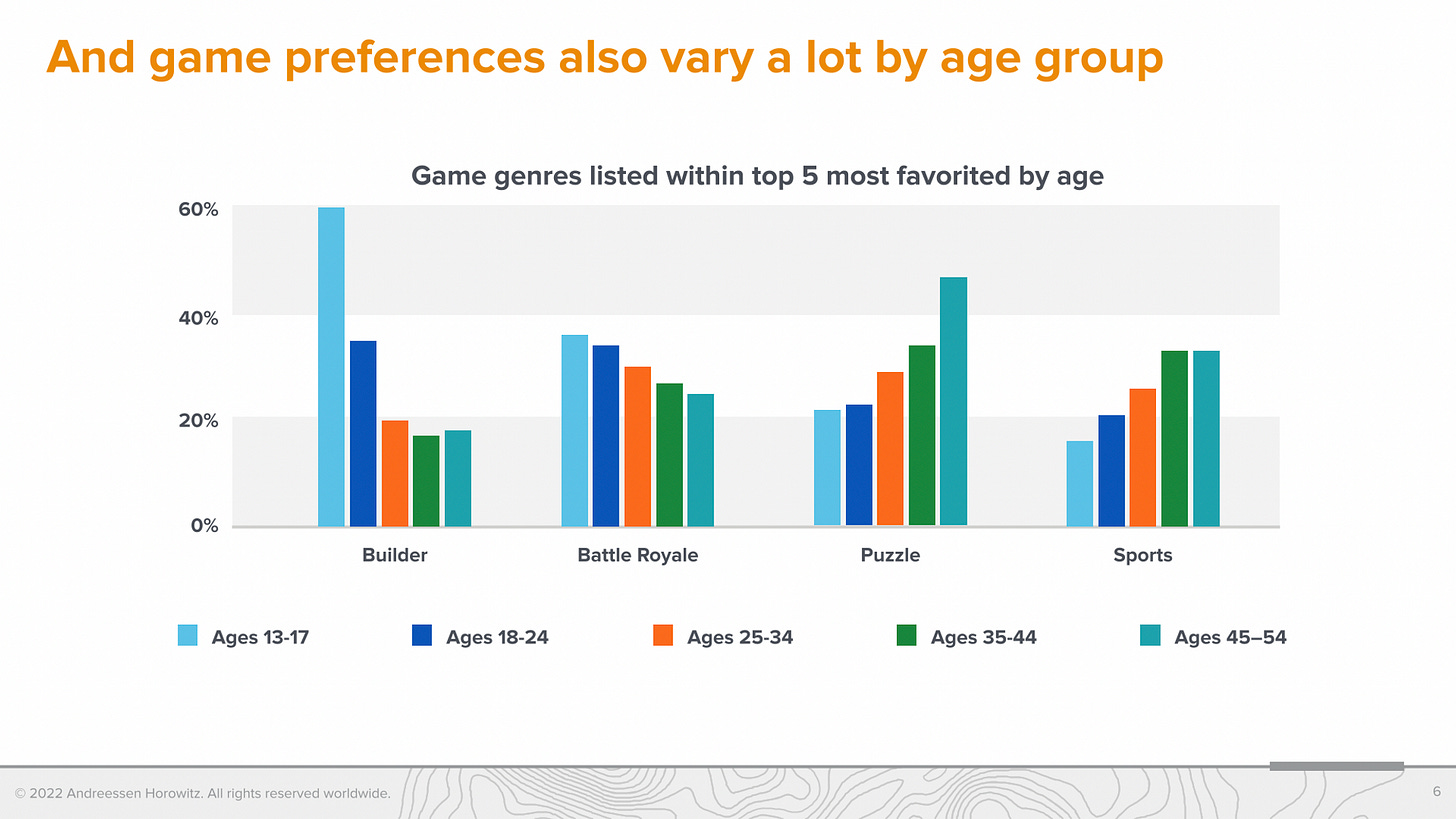

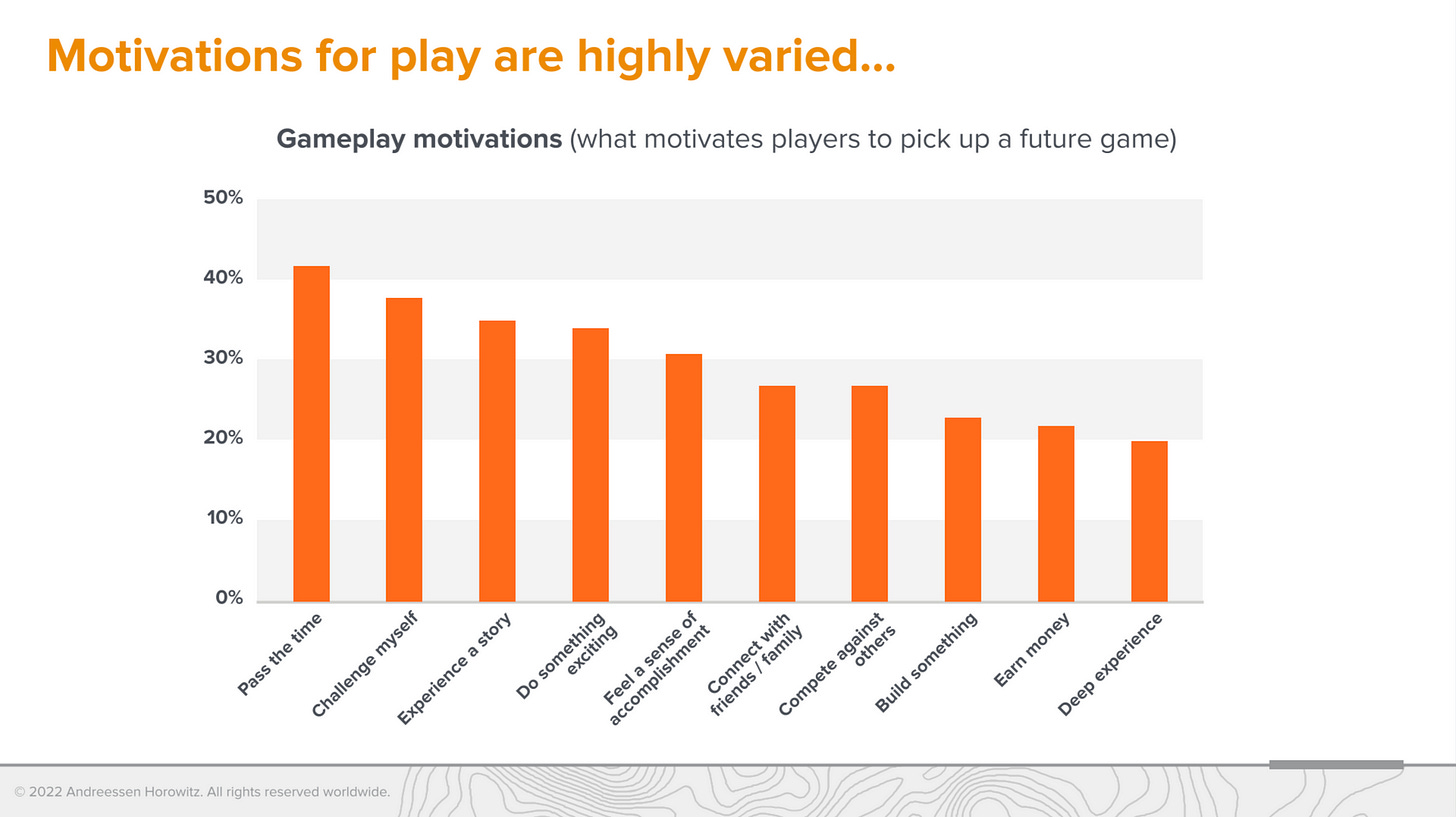

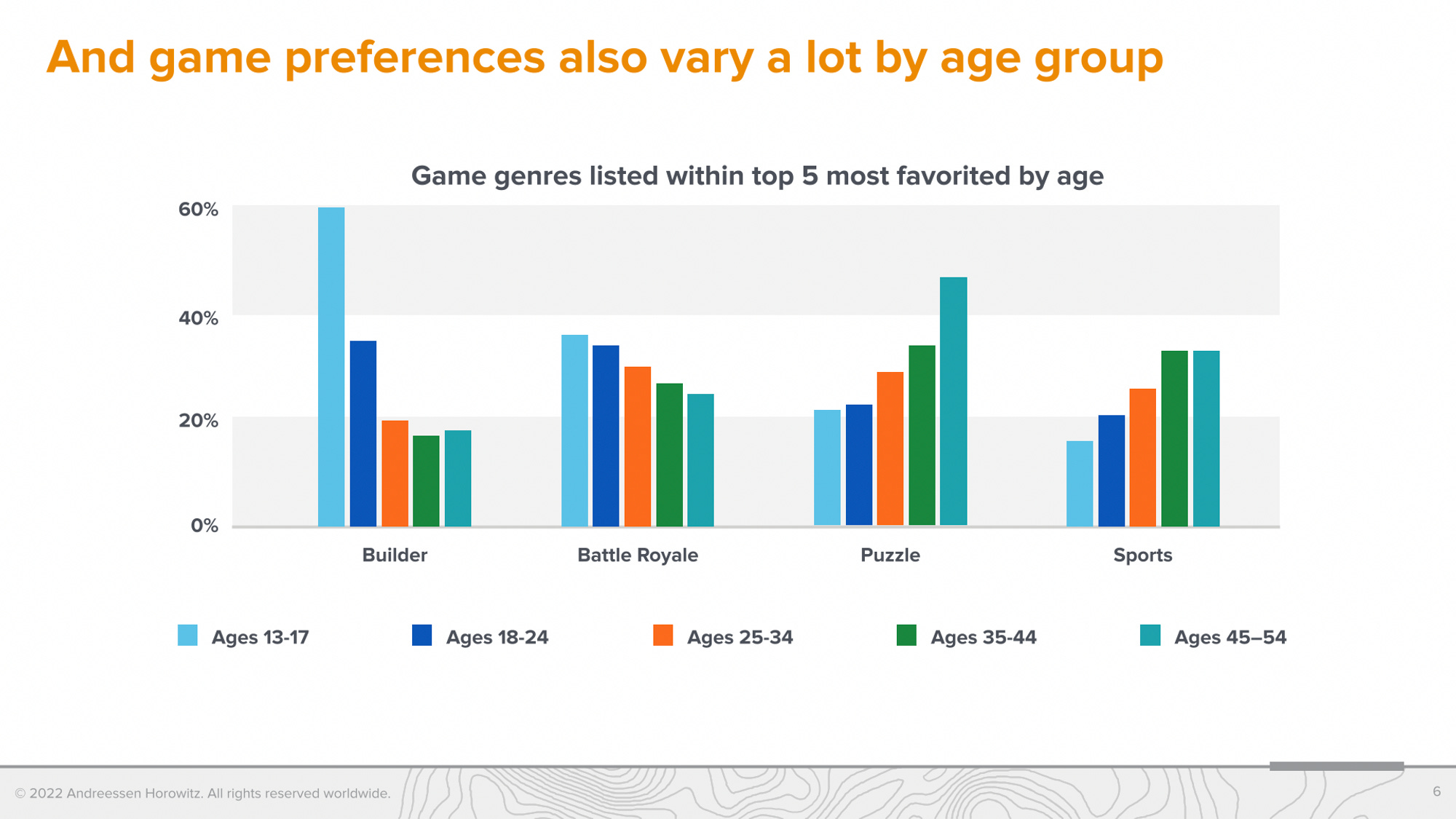

Tuesday, Dec. 20th: Robin Guo at a16z gaming ran a survey of 2k gamers. - Robin Guo

50% of gamers say that consoles are their primary device but they play much more frequently on mobile (58% of gamers play every day on mobile).

Shooters (COD), Action Adventure (GTA), Battle Royale (PUBG) and Puzzle (Candy Crush) are gamers’ favorite genres.

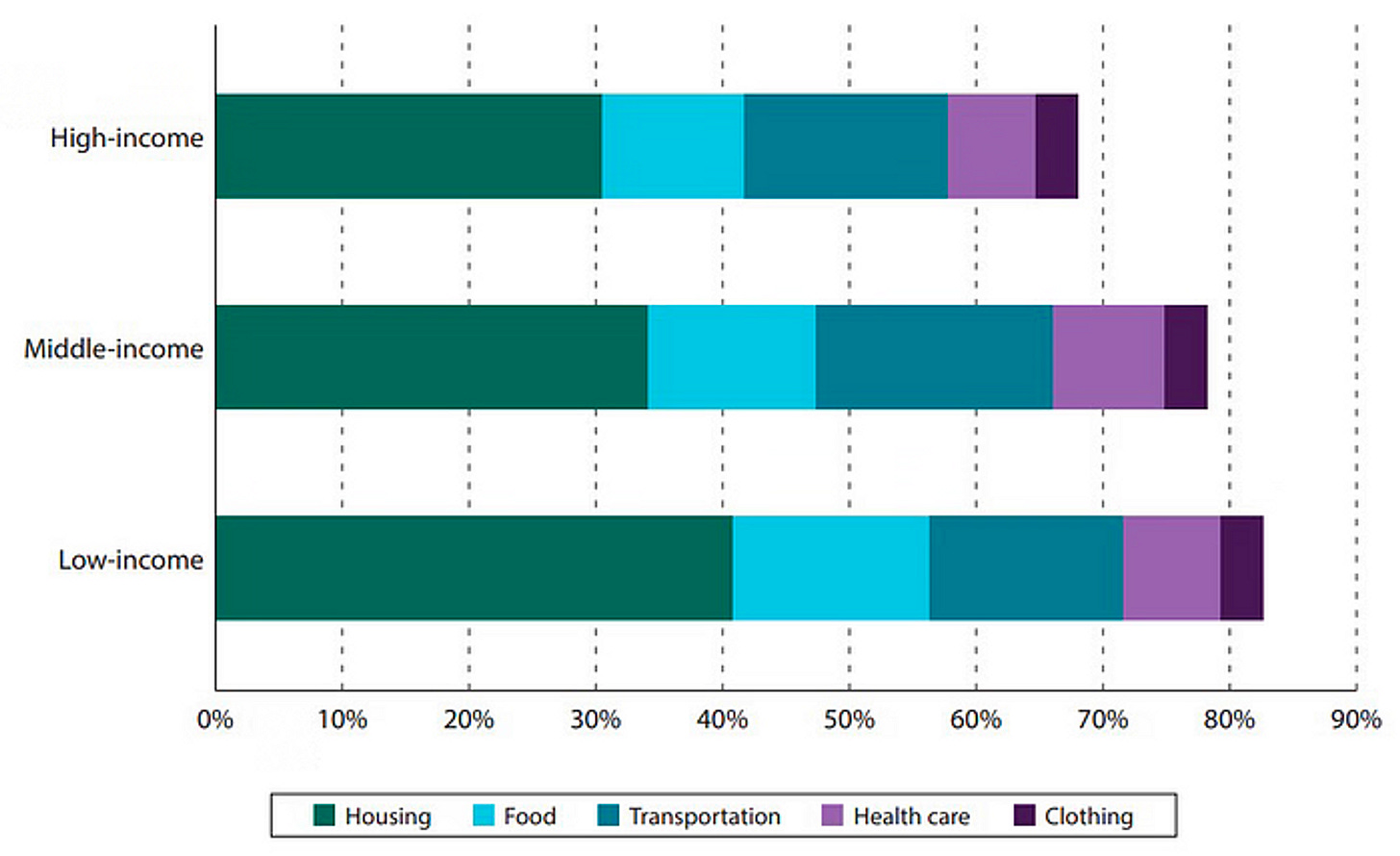

Wednesday, Dec. 21st: There is a vicious cycle from which it’s hard to escape for poor people, as certain expenses are higher when you are poor compared to when you are rich. - Finmasters

In the US, low-income households spend over 80% on necessities vs. 67% for high income households.

On housing, poor people tend to pay higher interest rates and tend to have higher maintenance costs because they have to settle for homes in poor conditions.

On food, poor people can struggle to access large stores (need to buy from convenience stores or fast food), don’t have the resources to buy in bulk and sometimes don’t have the kitchen equipment needed to properly cook at home.

Thursday, Dec. 22nd: I listened to a Colossus’ podcast episode on carbon removal with Nan Ransohoff who is head of climate at Stripe and who is leading Frontier which is a $1bn advanced market commitment to kickstart a market for carbon removal solutions. - Colossus

“The world emits out 50Gt of CO2 equivalents every year and to stay within reasonable warming targets, we need to get that down to net zero by 2050 or before. To do this, there are two main things that we can do. We can either stop emitting in the first place or we can pull CO2 that is already in the atmosphere and ocean out and store it permanently.”

With the energy transition, we need to electrify our economy increasing the demand on the grid (e.g. switching from fuel cars to electric cars) and we need to switch from a reliable source of energy (e.g. natural gas, oil, coal) to an intermittent source of energy (e.g. wind, solar).

Before Frontier, carbon removal was facing a chicken and egg problem. It was not worth starting or funding a carbon removal project because there was no demand from individuals, corporations and governments especially at initial prices to remove carbon from the atmosphere. But without demand, it’s impossible to scale the technology to a state at which it becomes an affordable solution and to an awareness at which it can switch from a voluntary market to a compliance market.

Frontier has several criteria when it evaluates carbon removal projects: (i) they should remove carbon permanently (for at least 1,000 years), (ii) they should have a path to scale to cost less than $100 per ton, (iii) they should have the potential to save at least 0.5Gt of CO2 equivalent at scale and (iv) they should not compete for arable land.

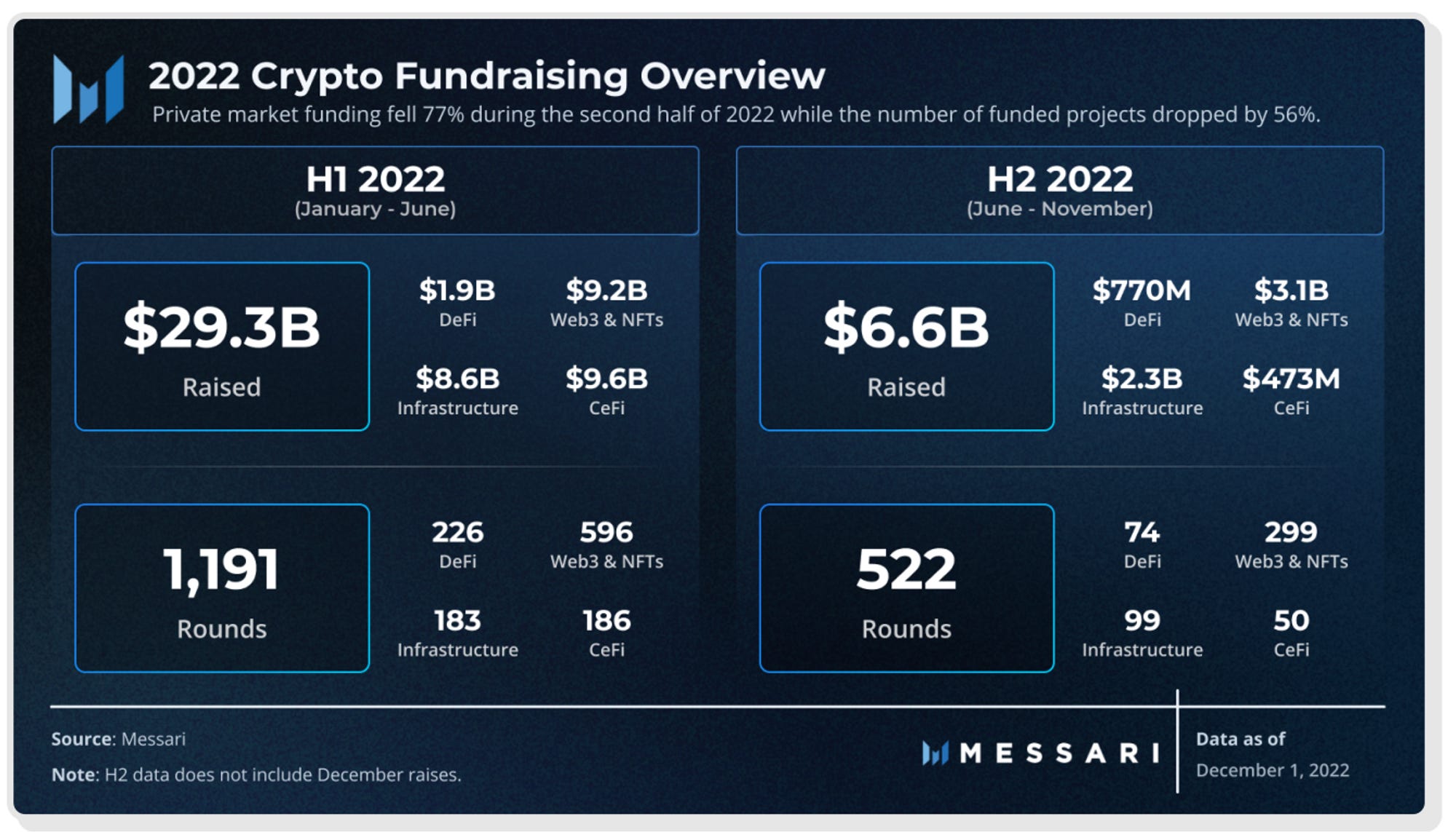

Friday, Dec. 23rd: Ryan Selkis at Messari released its 2023 crypto theses. - Messari

“I’d rather be long picks and shovels infrastructure businesses vs. specific projects in the NFT space, as almost nothing I’ve seen has established a “fundamental” driver of value beyond art.”

Areas in which to build in crypto in 2023: (i) solving security issues at scale, (ii) under-collateralized lending with new identity & reputation primitives, (iii) scalable decentralised cloud networks.

Post bull market, there are now only 13 decentralised applications with $10m in run rate revenues.

Like in all tech sectors, a massive slowdown in crypto fundraising happened in H2-22 ($6.6bn raised) compared to H1-21 ($29.3bn raised) and 2021 ($28.5bn raised). Companies should be ready to survive another crypto winter (1-2y duration) and it will be extremely hard to raise without a compelling investment case.

Saturday, Dec. 24th: In the same edition, The Economist covered two French industrial historical success stories which are currently showing some limitations: nuclear and high-speed trains. - The Economist 1 on Nuclear, The Economist 2 on Nuclear, The Economist 3 on high-speed trains

Nuclear is increasingly appearing as the best solution in Europe to fight climate change while giving back energy sovereignty to European countries against Russia and Middle East countries. In Europe, nuclear accounts for 25% of energy generation (vs. 10% in the world and 70% in France).

In France, the nuclear sector is not in good-shape. “France built too many reactors too quickly and then not enough.” As a result, (i) all reactors are requiring maintenance at the same time, (ii) it has lost its expertise overtime and ends up overspending on new reactors and (iii) France has become too dependent on nuclear energy under-investing in renewables (9% of its power supply vs. 25% in the UK).

France has a dual-speed train system. On the one hand, it has high speed lines that are extremely efficient (100m people are travelling via TGV every year, 2 hours between Paris and Bordeaux or Paris and Lyon). On the other hand, it has secondary lines that are getting worse over time (e.g. today, it takes an additional 30 minutes to travel from Paris to Limoges compared to 30 years ago). France launched a plan to invest in its non-TGV train network. It will invest €3bn to renovate the lines between Paris and Clermont and between Paris and Toulouse. It will also invest in slow night trains for long routes.

Sunday, Dec. 25th: Mews raised a $185m series C at a $865m post money valuation co-led by Goldman Sachs and Kinnevik at a 21% dilution which is relatively high for a series C. New investors like Revaia, Derive Ventures and Orbit Capital and existing investors like Battery, Notion and Salesforce also participated in the round. - Techcrunch, Mews 1, Mews 2

Mews is a vertical SaaS for hotels that sells a modern Property Management System (cloud-based, open to third party apps with a marketplace of 600 apps, easy to use and collaborative) which is the cornerstone software to manage an hotel. It works for all hoteliers from independent hotels to small & mid chains like Nordic Choice to large hotel chains like Accor.

Mews has 3.2k hotels and increased its revenues by 174% YoY and its payments volumes by 227% to reach a $2.3bn run-rate which is an impressive growth at this scale. Mews’ business model combines a SaaS fee and payment fees when it processes bookings for hotels.

It will use the funding for product development, commercial expansion, geographical expansion and M&A (in 2022, Mews acquired a POS called Bizzon).

In the Netherlands, Mews already has a market share over 20% which shows the potential for vertical SaaS to achieve higher market share penetration compared to horizontal SaaS by becoming the de facto standard in their vertical.

In 2022, Mews and Salesforce announced a partnership to connect Mews’ PMS to Salesforce’s CRM, enabling hoteliers to create personalised experiences for customers before, during and after their stay.

Monday, Dec. 26th: Dataiku raised a $200m series F led by Wellington at a $3.7bn valuation which is a 20% discount compared to its previous round ($400m series E led by Tiger in Aug. 2021). It helps data experts and business users in corporations integrate AI into their operations with an end-to-end (design, deploy and manage AI applications) and collaborative platform. Dataiku disclosed that it has over 500 customers (inc. 150 enterprise customers like GE, Ubisoft, OVH, Unilever, Merck) generating over $150m in ARR (implying a valuation at a 25x ARR multiple). - Tech.eu, Dawn, GlobeNewswire

Tuesday, Dec. 27th: Weekend Fund published a deep-dive on verticalised labor marketplaces. - Weekend Fund

With covid and market changing conditions, 44% of workers are looking for a new job. It has led to the rise of verticalised labor marketplaces offering services for both workers and employers.

Successful verticalized labor marketplaces are doing more than matchmaking workers and companies. They offer services like SaaS tools worker management, compliance), social networks for workers or financial services (insurance, payroll, payments).

“Labor marketplaces looking to distinguish their talent pool from others are wise to begin embedding training and credentialing into their platform. […] Embedding training within labor marketplaces is notoriously difficult to build as a team needs to (1) Acquire a talent pool, (2) Build out a training program to upskill workers, and (3) Establish a marketplace to match workers with jobs. This three-legged approach can be massively successful but if one of the legs fails, the whole platform will become shaky”.

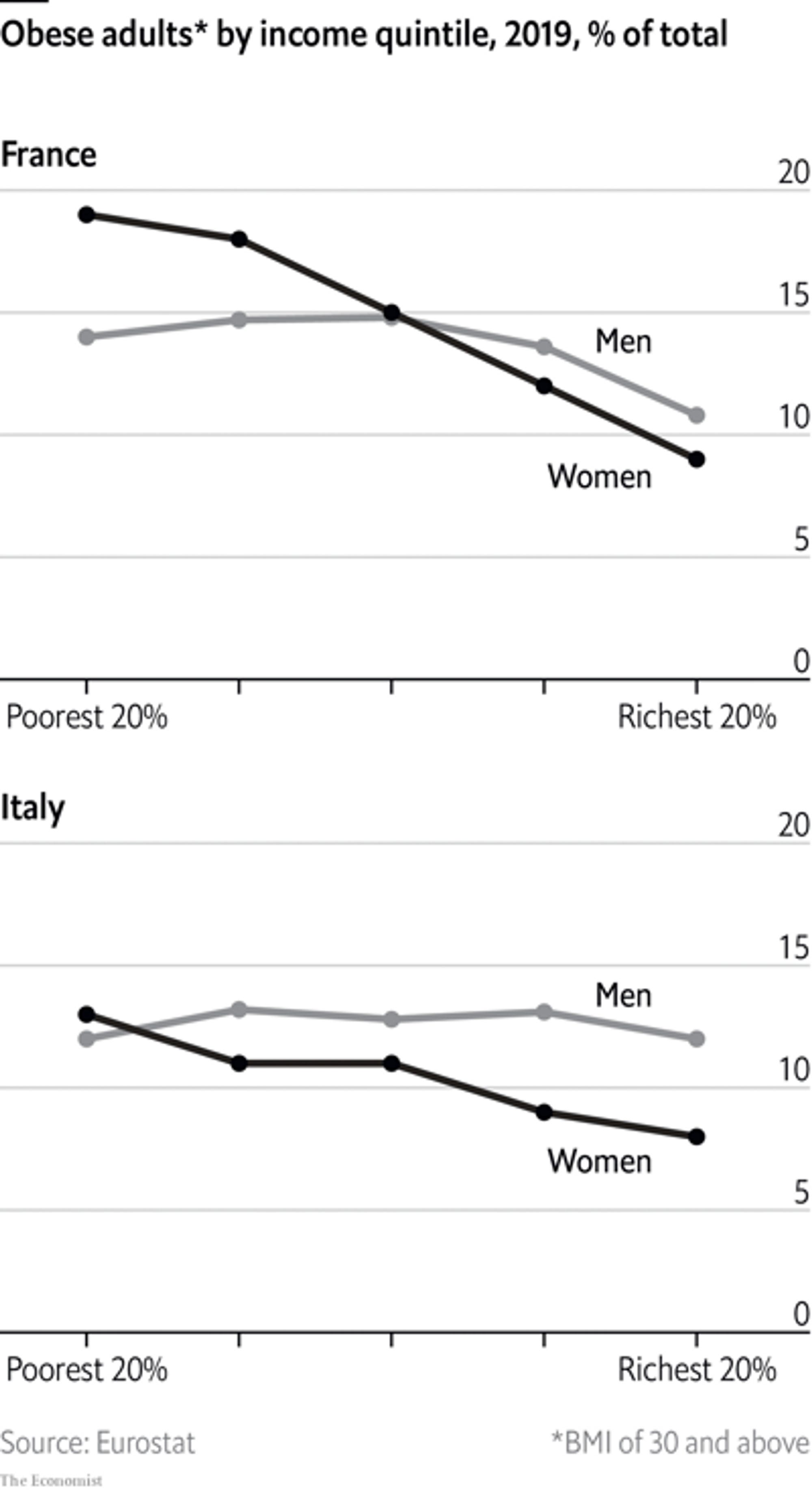

Wednesday, Dec. 28th: The Economist wrote about the idea that “it is economically rational for ambitious women to try as hard as possible to be thin.” - The Economist

“Wealthy people are thinner than poor ones in countries such as America, Britain, Germany and rich Asian countries, such as South Korea.”

“The correlation between income and weight at the population level in advanced countries is driven almost entirely by women.” “In other words, rich women are much thinner than poor women but rich men are about as fat as poor men.”

“Myriad studies which find that overweight or obese women are paid less than their thinner peers while there is little difference in wages between obese men and men in the medically defined “normal” range.” “The penalty for an obese woman is significant, costing her about 10% of her income.”

“It is economically rational for everyone to devote time to education because it has clear returns in the labour market and for future wages. In the same way it appears to be economically rational for women to pursue being thin.”

Thursday, Dec. 29th: Kyle Harrison wrote about the upcoming wave of M&A in the tech industry. - Kyle Harrison

In a world with low interest rates and unlimited capital available for tech startups, we end up with over-funded tech categories with dozens of players well capitalised (e.g. banking as a service, cloud security or spend management).

“There are a number of companies that are bolstering their product platforms, and expanding their addressable market that would love to snap up some innovative additions.” (e.g. Adobe acquiring Figma).

Kyle expects consolidation to happen in the following sectors: cloud security, customer support, marketing, no-code builders, spend management, banking as a service, cloud, data, data pipelines, API tolling, data & ML, DevSecOps.

Friday, Dec. 30th: Getir acquired Gorillas for $1.2bn (vs. $3bn valuation at Gorillas’ last funding round in Sep. 2021 and $1.3bn raised in total by Gorillas) and the combined entity is worth $10bn (vs. $11.8bn valuation when Getir raised its last round in Mar. 2022). Getir is mainly paying in stocks (only $40m in cash). Gorillas’ CEO and cofounder Kagan Sümer is expected to leave the company. In Europe, there are now only 3 quick commerce contenders left: GoPuff, Getir and Flink. Getir’s rationale to acquire Gorillas is to lower competition intensity by removing a direct competitor and to reach a critical size to have a better bargaining power with suppliers. - FT

Saturday, Dec. 31st: YC published a request for startups in the climate sector highlighting 5 different categories: energy related, science required, climate adaptation, green fintech and carbon accounting & offsets. - YC

Energy related: electrify buildings, energy management, EV value chain, electrify other vehicles, batteries, long term energy storage, energy production, critical minerals.

Science required: carbon removal & carbon capture, renewable fuels, vehicle breakthroughs, advanced energy generation, agriculture, construction, industrial heat & processes.

Climate adaptation: climate intelligence, fire, water/drought.

Green fintech (e.g. automating and streamlining non-venture financing of climate tech, leverage public funds to unlock private sector funds, etc.)

Carbon accounting & offsets: carbon accounting software, carbon offset & removal marketplaces.

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋