📖 Venture Chronicles - August 2025

Overlooked #204

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of August.

I curated updates and insights around three themes:

Vertical Software

General Venture Capital

Entropy - other news and personal topics of interest

Vertical Software

Advent acquired insurance software company Sapiens for $2.5bn in cash in another vertical software take-private. The acquisition will accelerate Sapiens’ product roadmap especially its full transition towards SaaS and the integration of AI into its platform. - Reuters, Sapiens

Sapiens serves over 600 customers in more than 30 countries. It offers an end-to-end platform (e.g. policy administration, underwriting, claims management, compliance) for insurers in several insurance segments including property & casualty, life & pension, workers' compensation and medical.

"Insurers are increasingly turning to technology to help unlock growth and profitability... We will work with Sapiens to accelerate investment into technology innovation, AI, and customer centricity.”

Topline Pro raised a $27m series B led by Northzone to bring AI automation to home‑services companies (e.g. roofers, painters, electricians, landscapers) in three core functions: marketing, sales and admin. It has 5k customers and generated $655m in cumulated revenues for its customers. - Axios, Topline Pro

“Topline Pro’s AI runs marketing, sales, and administrative tasks in the background—allowing skilled tradespeople to focus entirely on the work only they can perform.”

“We’re building AI that acts like a real teammate, one that gets the website right, keeps the reviews coming, responds to leads instantly, and helps pros stay booked without needing to learn new systems.”

Topline Pro offers 3 agents: (i) AI Marketer boosting online visibility (website optimisation, SEO, social content), (ii) AI Sales Rep handling inquiries and booking jobs and (iii) AI Operator managing scheduling, reminders, invoicing, and payments.

Toast published its Q2-2025 financial results. - Toast

It reached $1.9bn in ARR growing 31% YoY. It added 8.5k new locations reaching 148k total locations growing 24% YoY.

Toast sees accelerating growth in new segments (enterprise, international, food & beverage retail), surpassing 10k live locations in these segments, which are on track to collectively exceed $100m in ARR by year-end.

For retail, “we're building deeper inventory management tools, expanding integrations, scaling our dedicated sales team. Total ARPU for retail customers is already above $10k.”

“Toast recently took its first customer live in Australia - Graze Craze - expanding its international presence beyond the United Kingdom, Ireland, and Canada, and marking another step towards building the leading global technology platform for restaurants.”

“Non payment fintech solutions led by Toast Capital contributed $40m in gross profit and 8 basis points intake rate. We continue to expect Toast Capital contribution and net take rate to remain in the 10 basis point range.”

Plancraft raised a €38m series B led by Headline. Based in Hamburg, Plancraft is an AI centric operating system used by 20k tradespeople. It uses AI agents to generate quotes, handle customer interactions, optimise operations, etc. - Tech.eu

“Since its Series A in June 2024, Plancraft has more than doubled its team from 40 to over 100 employees. The company has already built teams in Germany, Austria, the Netherlands, and Italy.”

Euclid wrote about moats for vertical AI companies. - Euclid

“Speed is not a durable advantage. At scale, almost all companies slow down to service a large and heterogeneous customer base; competition and fast followers begin to gain absolute scale of their own; old breakthroughs become commoditized; demand for cash flow grows; and organizational torpor suffocates innovation.”

“There are two types of moats for AI-native companies - both data centric.

(i) Data Control: Proprietary control of a data asset that others can’t simply replicate—be it due to uniqueness, fragmentation, method of aggregation, specialized analysis required, etc. Synonymous with Data Gravity above.

(ii) Data Loops: Positive feedback loops that compound advantages. These moats often center around workflow, usage, and network effects.”

Tidemark wrote about Epic, arguing that it’s an excellent illustration in healthcare of how to build a successful vertical software company by first capturing the core market and then expanding into adjacent products and other stakeholders in the healthcare ecosystem. - Tidemark

“Four characteristics stand out: (i) the existence of countless specialized workflows that remain largely under-automated, (ii) the abundance of extremely sensitive, unstructured, and fragmented data, (iii) a regulatory landscape that is unique, complex, and constantly evolving and (iv) the presence of multiple stakeholders with competing priorities trying to coexist.”

“Epic now holds 48% market share among large hospitals, far ahead of Oracle Health (27%) and Meditech (15%). Even more telling, Epic is said to have near-zero customer churn, meaning that any growth comes at a competitor’s expense.”

“After locking down the large IDNs (Integrated Delivery Networks), Epic systematically expanded across entire health systems, displacing rival EHRs through the promise of a single, integrated platform.”

“Once a health system adopts the core EHR, layering on additional modules becomes the path of least resistance.”

CNBC wrote about Judy Faulkner, Epic’s founder and CEO. - CNBC

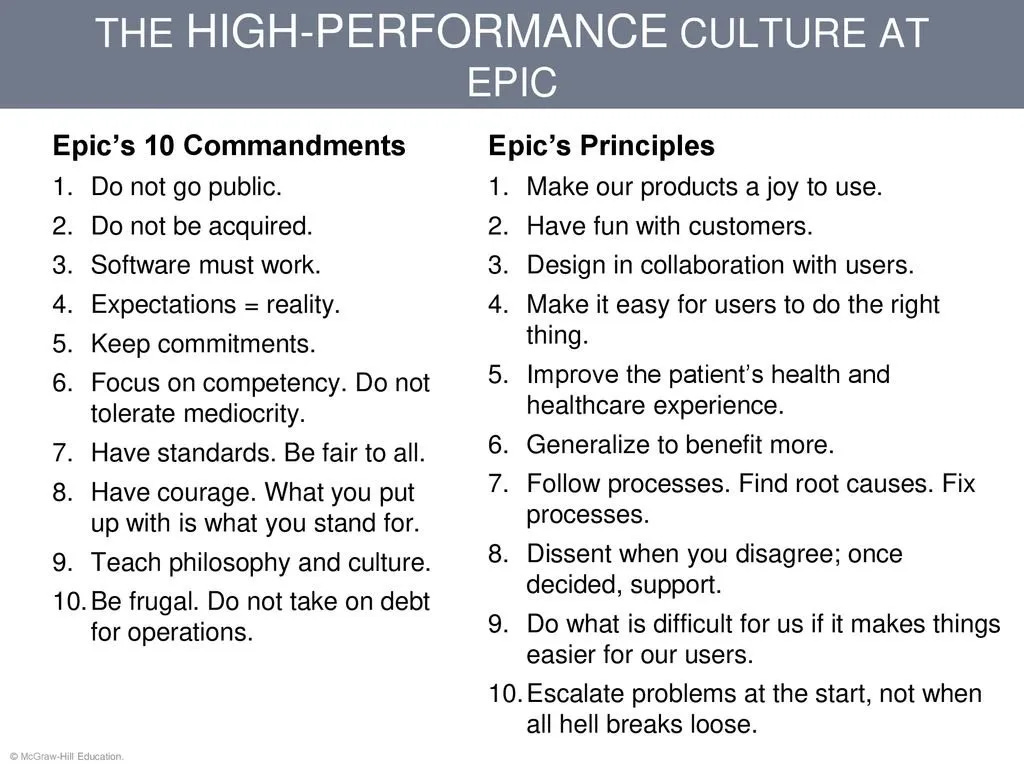

Epic has 10 commandments on how the business should operate showcased in every bathrooms and conference rooms.

“Epic’s CEO is 82-year-old Judy Faulkner, who started the company in a Wisconsin basement in 1979 and has helmed the enterprise ever since. En route to building a business with $5.7 billion in annual revenue, Faulkner has kept significant distance from her tech peers, both physically and otherwise.”

"Epic is best known for its dominance in electronic health record, or EHR, software. An EHR is a digital version of a patient’s medical history that’s updated by doctors and nurses. About 42% of acute care hospitals in the U.S. use Epic, putting it way ahead of Oracle Health, which is in second place at 23%.” “Epic says its technology is used in 3,300 hospitals and 71,000 clinics and by 325 million patients worldwide.”

“Faulkner has publicly described herself as “the accidental CEO.””

“Each health system that uses Epic has a point person called a “BFF,” or “best friend forever,” who is available to answer questions and help solve problems.”

"Epic doesn’t advertise or have a traditional marketing department; the company has relied heavily on word of mouth.”

“Epic faces accusations of anticompetitive practices in two lawsuits from the past year. One was filed in September by data startup Particle Health, which alleges that Epic has used its EHR market power to “snuff out” competition in other emerging health-care markets.”

“Epic’s competitors have also long accused the company of being territorial over its data and impeding efforts to share patient information between vendors.”

“Since Faulkner places such a strong emphasis on supporting her customers, she holds her staff to high standards. Most employees work in person five days a week. Hours can be long and burnout is common, former employees say. In June, The Economist analyzed 900 companies across 19 industries, and found that Epic had the worst work-life balance in the software and IT services category.”

General Venture

AI was expected to get cheaper as inference costs fell, but startups are discovering the opposite. While the price per token is dropping, advanced reasoning tasks require exponentially more tokens, driving higher bills. Complex workflows (e.g. coding or legal analysis) can consume hundreds of thousands to millions of tokens. This squeezes gross margins of historical SaaS companies integrating AI features and AI native apps. - WSJ

“Ivan Zhao, chief executive officer of productivity software company Notion, says that two years ago, his business had margins of around 90%, typical of cloud-based software companies. Now, around 10 percentage points of that profit go to the AI companies that underpin Notion’s latest offerings.”

“The fact that some AI startups are sacrificing profits in the short term to expand their customer bases isn’t evidence that they are at risk.

Pirate Wires published a strong piece on the Thiel Fellowship, which offers $100k to people under 20 who leave college to start companies. - Pirate Wires

““If Harvard were really the best education, if it makes that much of a difference, why not franchise it so more people can attend? Why not create 100 Harvard affiliates?” Peter said at the time. “It’s something about the scarcity and the status.””

“The Thiel Fellowship is gaining notoriety for producing so-called “unicorns” (billion-dollar companies) at a supposedly higher rate than top accelerators. In a contested chart that went viral earlier this month, the fellowship is even beating out Y Combinator.”

“Knowledge traveled through osmosis to younger classes, and they did a ton of business together, probably more so than your average incubator community, Danielle said. Because, in addition to a natural chemistry, the class sizes (20ish) are nice and small, especially compared to Y Combinator, which accepts roughly 500 startups each year.””

“To be a Thiel Fellow, you had to be going up against something, typically. Going up against higher ed, going up against what your family believed, going up against what your friends were doing. That takes an incredible amount of conviction.””

“Thiel Fellow-founded companies like Figma, Ethereum, Anthropic, and OYO Rooms have created more than $750 billion in value.”

“In 2015, Danielle and Michael left the Thiel Fellowship, electing to start a venture fund to fill the gap for fellows and similar upstarts.” “We think the Thiel Fellowship is the greatest investment opportunity that no one is taking advantage of.” “Their first fund, $20 million, returned more than $200 million to investors by 2020.”

“We need variance — we need people exploring different things. And those years from 18 to 23 are so prime, we’ve just seen it. It’s like people are so creative, and sadly, you don’t stay that creative through your prime. You have a peak and then you tend to tail off.”

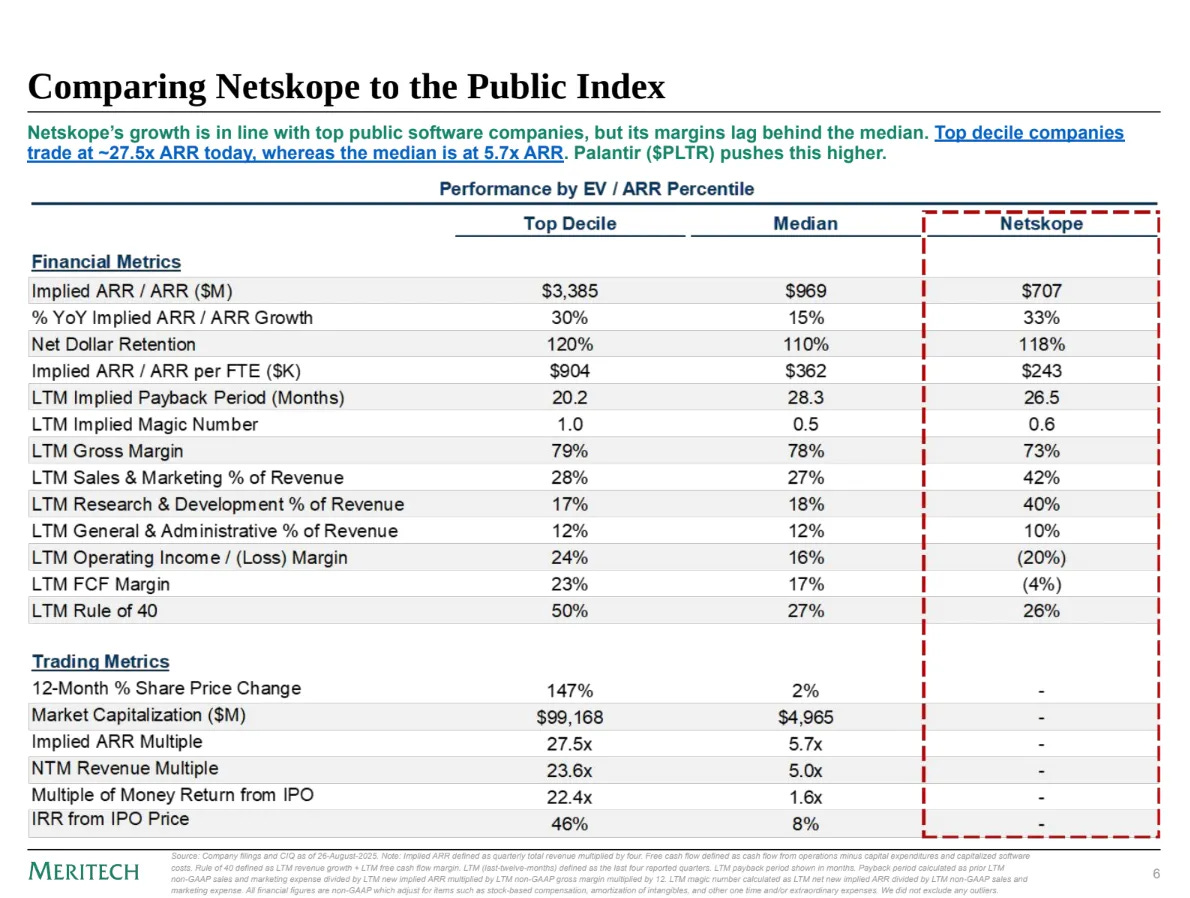

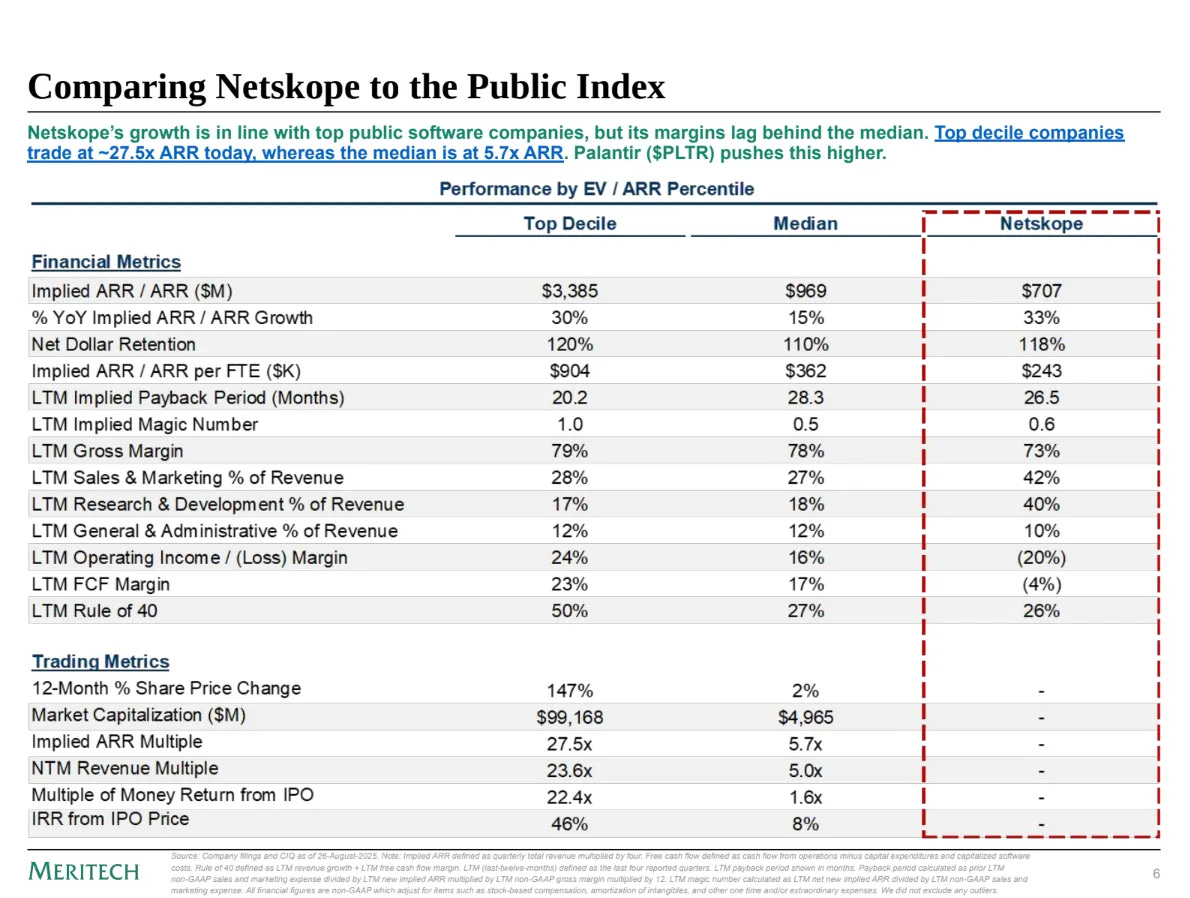

Cloud-native SASE (Secure Access Service Edge) security platform Netskope filed to go public. - Meritech, SaaStr

It generates $707m in ARR from 4.3k customers growing 33% YoY and it’s still burning money. 86% of its ARR comes from $100k+ ARR customers. 111 customers are paying $1m+ per year. Netskope has a 118% net dollar retention.

“SASE platforms deliver converged network and security-as-a-service capabilities, such as software-defined WAN and secure access to the web, cloud services, and private applications regardless of the user’s location or device.”

It previously raised $1.05bn in equity from investors including Lightspeed, Iconiq and Accel. Its last private round was at a $7.5bn valuation. Netskope aims to raise over $500m and should target a valuation below its last private valuation mark.

“Netskope One is an end-to-end SASE platform that enables companies to discover, classify, view, safeguard, and provide / remove access to data. Netskope emphasizes their core differentiation stems from building a broad array of 20+ products all running on a single policy engine, client, network, and gateway. By replacing disparate legacy point solutions with Netskope, customers are able to easily maintain consistent policy enforcement across devices and tools.”

“Competition is fierce across the large markets where Netskope competes. According to Gartner, the company competes in the SSE (Security Service Edge) and SASE platform markets. Competitors listed out are large incumbents such as Broadcom, Cisco, Fortinet, Palo Alto Networks, and Zscaler.”

Lakestar raised a $265m continuation fund to extend its ownership in top portfolio companies while generating liquidity for its historical investors. - Bloomberg, Lakestar

It raised from Lexington Partners, Industry Ventures and Performance Equity Management.

“Investors in the four existing Lakestar funds didn’t participate in the new vehicle.”

“With the lackluster IPO market delaying companies from going public, more players in the venture ecosystem have started looking at alternative ways of providing liquidity to their investors.”

“Such deals are less frequent in Europe, though German firm HV Capital in 2022 rolled out a €430 million continuation fund.”

“Continuation vehicles also enable buyout firms to keep their best-performing assets beyond the usual tenure.”

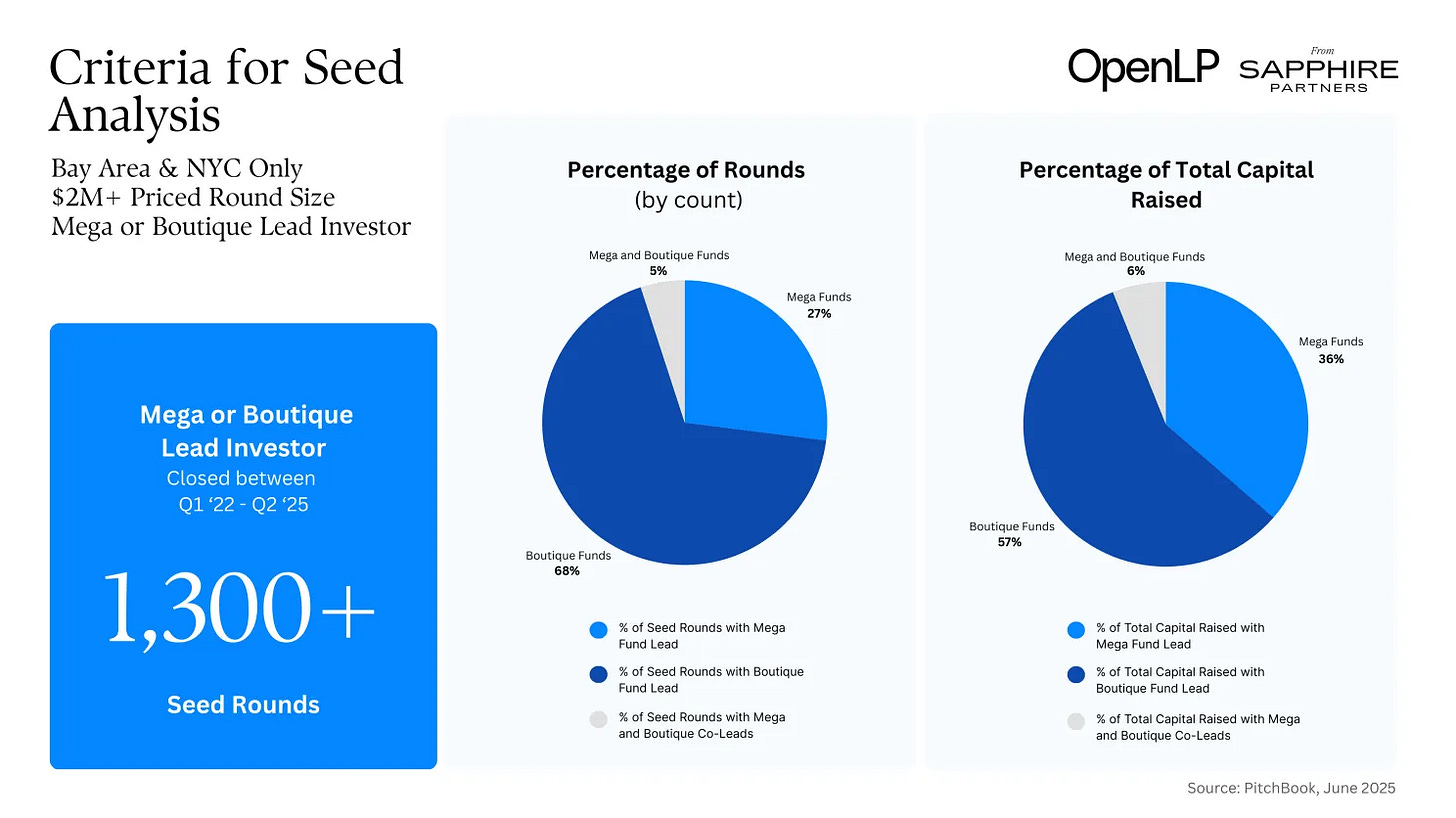

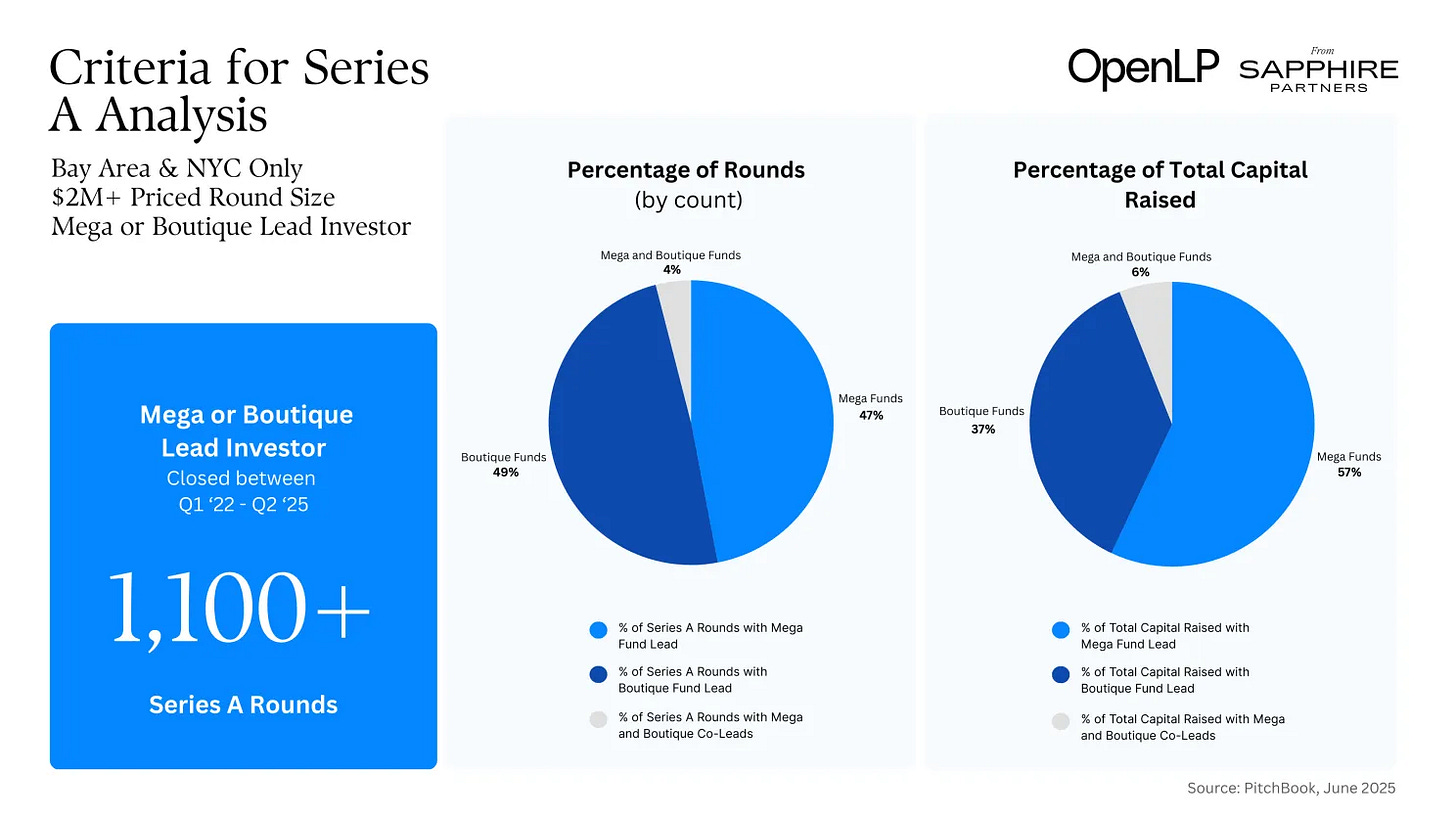

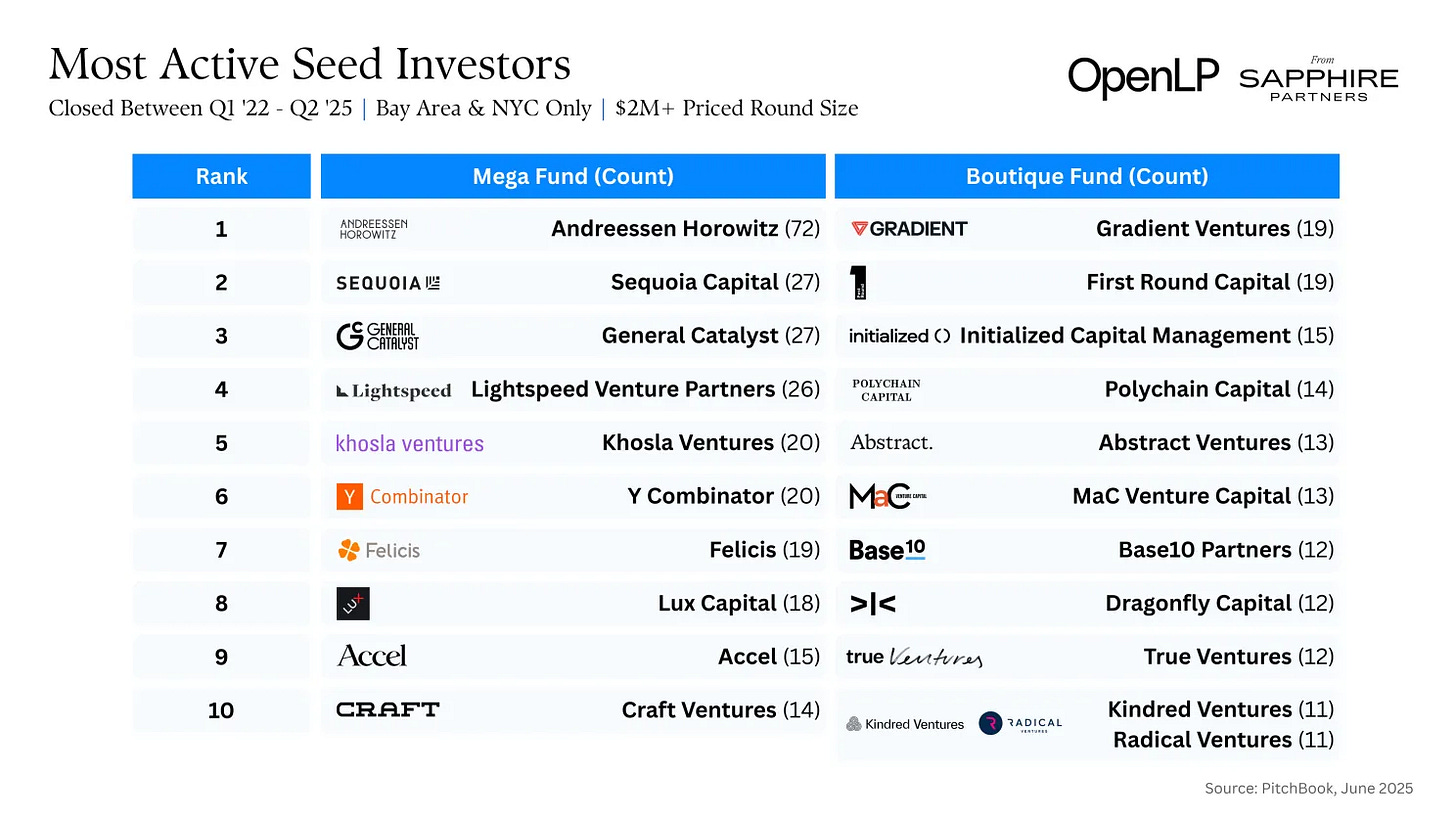

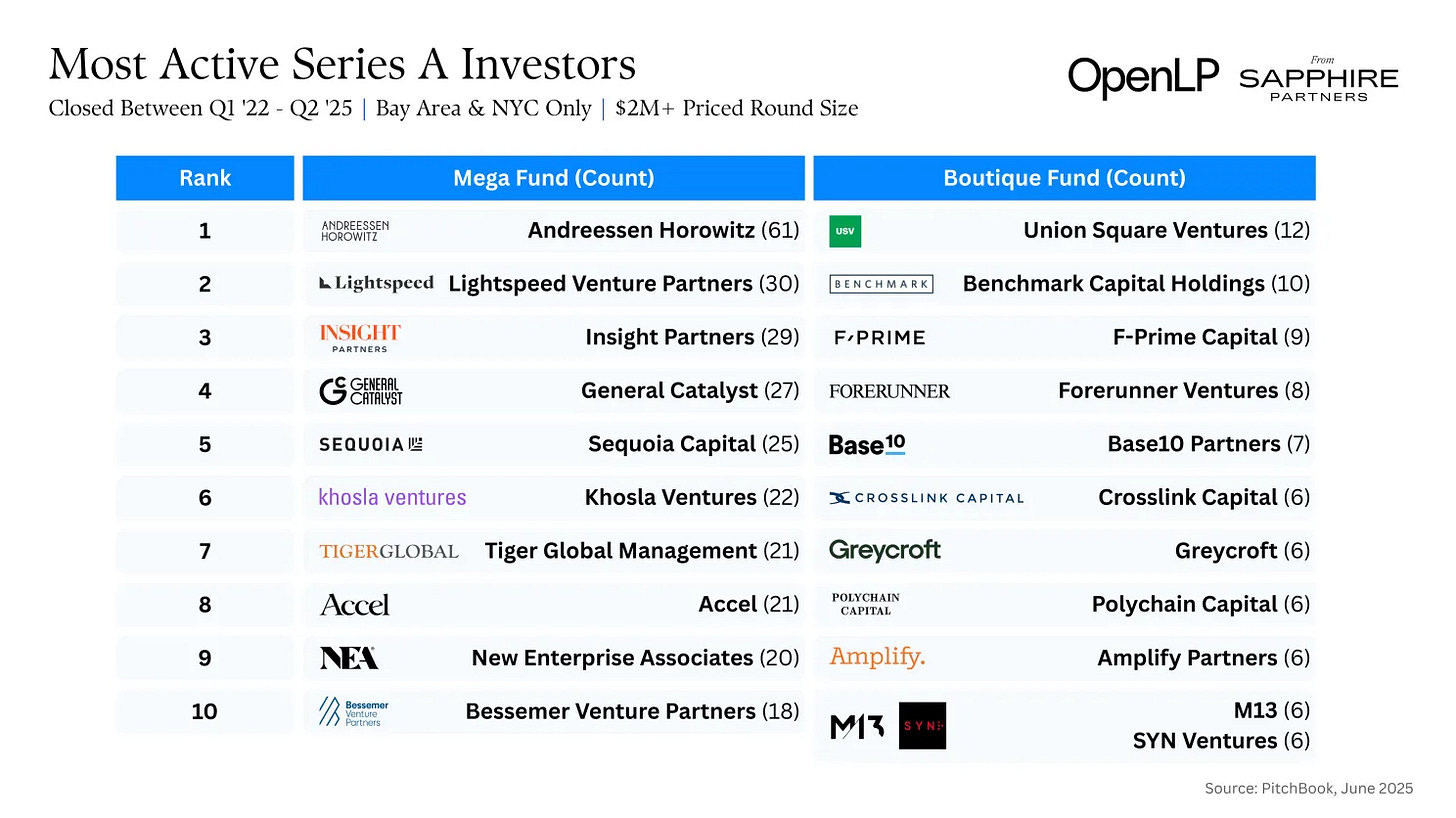

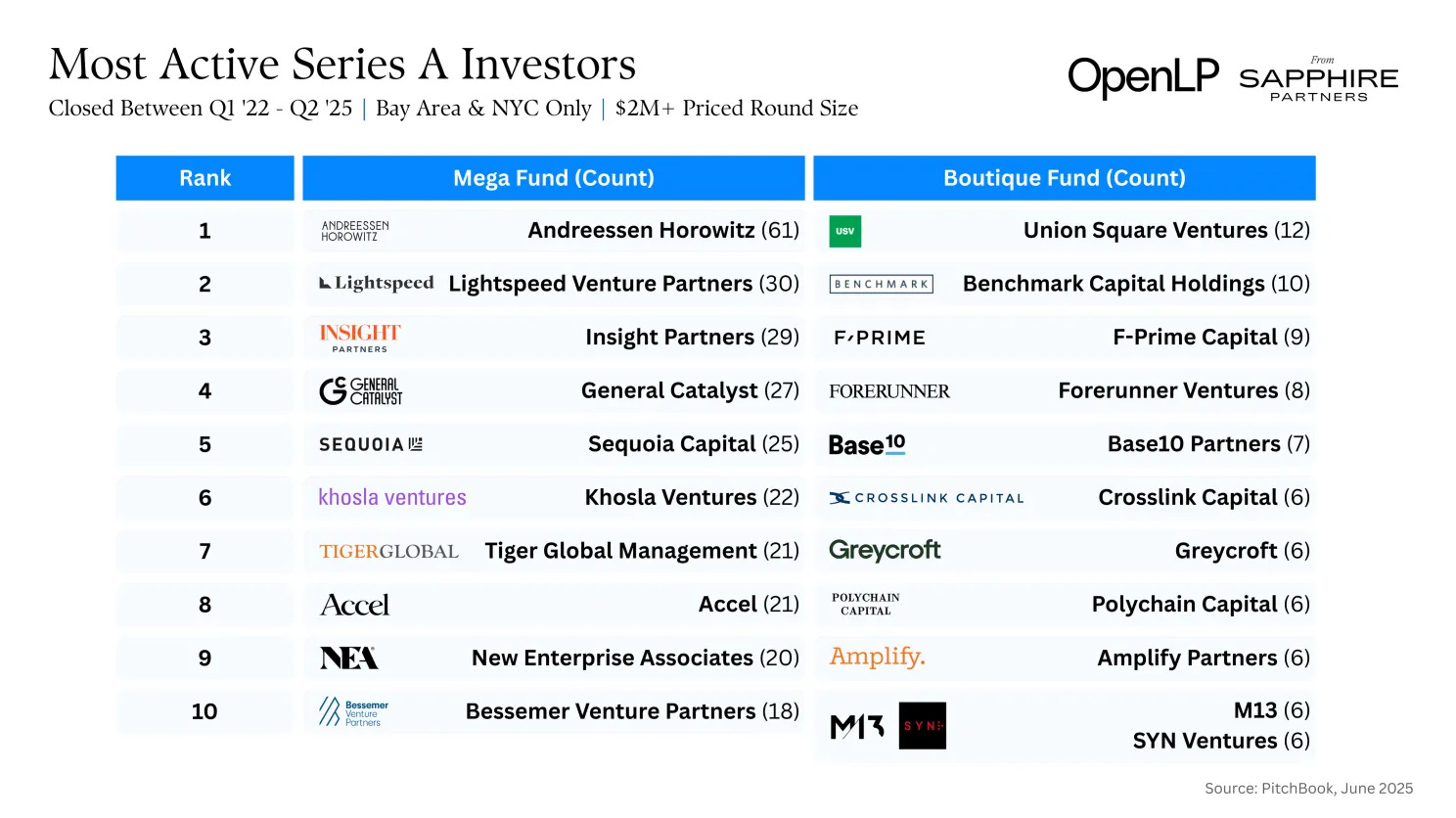

Elisabeth Clarkson from Sapphire wrote about the seed / series A venture market. - Elisabeth Clarkson

“The concern seems to be that if mega-funds are dominating at early, using investments at seed as option value on later rounds, mega-fund participation could be “breaking” venture through their overspending - shifting how value is accruing—or not—at different stages.”

“Despite the expanding influence of mega-funds, especially in their ability to write larger checks, the Seed and Series A ecosystem still has a very strong presence of boutique, stage focused early-stage funds*.”*

“For Seed, mega-funds have been leading ~25-30% of rounds from 2022-H1 2025 (by count), while boutique Seed funds consistently have led ~65-70% of rounds. And then there’s a small percentage of rounds (~5%) where a mega-fund and boutique fund share the co-lead.”

“Mega-funds are making their presence known, but seem to be mostly focused on the larger Seed rounds. This is what we expected to see given larger funds tend to write larger checks.”

“Similarly for the Series A rounds, we highlighted peak mega-fund lead, 63% in the $20M+ size rounds, which also happens to be the same round size that has the highest number of Series A rounds led by a mega-fund.”

“We expect early-stage investing to remain intensely competitive — especially at Seed. Nearly every VC fund will want exposure, whether because it’s their core focus or as a wedge into future rounds.”

As venture funds scale, the long-standing taboo against investing in competitors is fading. - Charles Hudson

“It’s not practical to have access to the same level of information about two competing companies while being a good fiduciary to each.”

“I think the norm of not investing in competitive companies has been a feature, not a bug.” “It sends a signal to the entrepreneur that if you take a given firm’s money, they will not turn around and back your competitor.” “It gives the investor an incentive to devote all their energy and effort to making the company successful, rather than exploring other investments in the category.”

“As venture fund sizes keep getting larger, I do think that tradition of venture firms having a norm (if not a stated policy) to not invest in competitive companies is likely to go away.”

“It has become increasingly essential for those firms to be associated with the biggest and most important companies.”

As a fund, if you want to invest in a category leader that you missed by investing in a competitor, you have two options: (i) “buy [passive] secondary positions in the companies that matter but that you missed”, (ii) “invest in competitors but have different investors take board seats and create firewalls to limit information spillover”

“I don’t think founders want the investors who back them investing in competitors. This is an issue where the business model for funds is at odds with what most founders want.”

Rob Go at Nextview wrote about how seed funds should adapt to thrive in the current venture market. - NextView

“There are two patterns to these tech supercycles that I believe will be repeated this time around. The first is the expansion of value that these technologies create. […] The second pattern is that these cycles have a predictable progression. A new technology creates a market interruption that leads to a period of frenzy that propels a rapid installation period. One or several boom and bust cycles may occur, followed by a prolonged deployment period as the technology permeates markets and society.”

"Value begins at the infrastructure layer, but eventually expands into the application layer, which is typically larger and has a broader set of winners in different domains.”

"Sustaining innovation will be about leveraging AI to transform the way VCs source, select, win, and support portfolio companies.” “Nearly every VC firm will talk about how much they incorporate AI into their work, but I’d argue that very few will successfully implement it in a practical way.”

"I personally don’t see that much disruptive innovation coming from the newer seed VCs. In fact, we’ve strangely seen the opposite: a convergence of strategies.”

“The challenge with disruptive innovation is that you have to get a lot of things right at the same time. You have to be non-consensus AND have the right timing AND have the right execution.”

“Ultimately, the challenge for seed funds is finding a way to be distinct and to execute on that distinctiveness at a very high level.”

“What we really need are investors with conviction about their weird taste, pursuing weird strategies, and supporting founders pursuing weird but potentially magical things. Couple that with great dependability, professionalism, practical support, and hustle, and you get a potentially winning combination.”

Venture funds are drastically changing the modalities to generate liquidity for their LPs. - Tom Tunguz

“The buy-and-hold strategy that built venture capital for five decades has reached its breaking point.”

“The investment landscape has fundamentally shifted beneath our feet. Time to IPO has tripled from four years two decades ago to 12-13 years today. M&A exits, once a reliable four-year path to liquidity, now stretch seven to eight years on average. The math has become untenable for traditional fund models.”

“Limited partners now demand distributed-to-paid-in capital (DPI) ratios by fund three or four to justify continued investment. This pressure creates a liquidity paradox: funds must show returns precisely when their portfolio companies need the most support to reach meaningful exits.”

“Private equity firms solved this equation decades ago with concentrated portfolios and active value creation. They typically hold 10-15 core positions, enabling intensive operational support and strategic guidance.”

“GP-led secondaries have emerged as the industry’s most significant innovation in response to this challenge. These transactions allow funds to extend hold periods for their best assets while providing partial liquidity to existing investors. The market for GP-led deals has exploded from negligible volumes five years ago to over $100 billion annually today.”

Databricks raised a $1bn series K at a $100bn valuation co-led by Thrive and Insight to accelerate its AI strategy including a database for AI agents competing with Supabase and an AI agents platform. It previously raised in January a $10bn round at a $62bn valuation. - Databricks, Techcrunch

“At the June Data + AI Summit, Databricks introduced a new product, Agent Bricks, which builds high-quality, production AI agents optimized on your enterprise data, and Lakebase, a new type of operational database (OLTP), built on open source Postgres, and optimized for AI Agents.”

“More than 15,000 organizations worldwide — including Block, Comcast, Condé Nast, Rivian, Shell and over 60% of the Fortune 500 — rely on the Databricks Data Intelligence Platform to take control of their data and put it to work with AI.”

“"A year ago, we saw in the data that 30% of the databases were not created by humans. For the first time, they were created by AI agents. And this year, the statistic is 80%,” he said, adding that he predicts this stat to increase to 99% of new databases within a year.””

David Beisel at NextView wrote on handling entry valuations in venture. - Nextview

“You always wish that you owned more of your winners, regardless of the initial price that you paid. But in those cases, the initial deal impression is overshadowed by its success. Whereas with your losers, that first negative impression is only amplified.”

“In VC, there’s no reward for “value investing”: success hinges on identifying and backing upside outliers, not securing deals at relatively attractive prices. Playing a game of ‘subprime’ venture capital leads to partnering with ‘subprime’ entrepreneurs.”

“A critical tension exists: valuation matters less at the individual company level than at the portfolio level.”

“The strategy for VC success is not to systematically overpay. It’s to truly differentiate oneself on dimensions other than price. It’s best for founders to chose you, and not merely the highest bidder who happens to be you.”

I listened to Jack Altman interviewing Gregory Rosen, a partner at BoxGroup. - Jack Altman

BoxGroup has a "collaborative venture" model. They never lead rounds which enable them to successfully collaborate with all lead investors. To scale, it increased the number of deals it does per year instead of scaling ticket sizes which would have eventually led them to lead rounds.

The goal is to make it as easy as possible for a founder to say yes to them. They can be the "first yes" for a founder without a lead, helping them find an amazing lead, or quickly "round out a syndicate" if a founder already has a lead.

"We trade ultimate ownership percentage points for a more collaborative flexible model that lets us just see better companies and hopefully get into more better companies.”

Box sees about 5,000 to 6,000 qualified or referred opportunities a year, resulting in approximately 70 to 80 investments annually.

To get truly early, BoxGroup partners spend significant time meeting individuals who haven't yet left their jobs or may never start a company. “There is no substitute for time.”

Investment decisions are often made by one individual or a small "pod" (2-3 people). This "single trigger" approach is "incredibly" structurally important, as "consensus driven decision-making at seed doesn't work.”

The most crucial advice in venture is to "just focusing on the thing that you are outlier in.” You have 3 core archetypes of investors: (i) the hyper-networker trying to see everything and engaging in intense networking, (ii) the philosopher/media/thought leader with thought leadership to attract inbound dealflow, (iii) the specialist with a deep focused on a specific area.

It’s not obvious that Cursor has real product market fit as the company is massively subsidising the usage of its product operating at negative gross margin. - Chris Paik

“Product-market fit is the story founders love to tell. Business-model–product fit is the part they often skip. (i) Product-Market Fit: Users repeatedly choose your product. (ii) Business-Model–Product Fit: The extraction of value is sustainably in excess (and proportional) to the cost of delivering value.

“Cursor has relied on a subscription model that historically allowed for “unlimited” use. That’s a fixed revenue, variable cost setup. When variable costs scale with intensity of usage but revenue doesn’t, you’re not selling software, you’re underwriting risk.”

“Any time “unlimited” shows up in a variable-cost business, PMF becomes a permanently open question. Until Cursor prices consumption in proportion to cost, it cannot know.”

“Subsidies are not a business model. They’re, at best, a bridge to an operational or structural moat that later confers pricing power.”

“If Cursor steps down to cheaper, weaker models, the users who care about performance will notice and churn; those who can tolerate weaker models can get them cheaper elsewhere.

I read a post on Palantir’s startup mafia. - WSJ

“The founders lean on other ex-Palantir executives and engineers for support and financing, tapping the network for hiring and funding. Venture-capital firms have sprung up whose mission is to invest in companies founded by people with Palantir experience.”

“Alumni have either started or are leading more than 350 tech companies, and at least a dozen have been valued at over $1 billion, says Luba Lesiva, who was head of investor relations at Palantir from 2014 to 2016. Lesiva runs a venture firm called Palumni VC, a play on the words Palantir alumni, which invests in startups founded or led by ex-Palantir employees.”

"A big appeal of the Palantir alumni is their common strategy, developed at Palantir, called “forward-deployed engineering,” which is basically a glorified term for consulting. Palantir software engineers often travel to their clients and embed themselves. Engineers can find themselves in conflict zones or locales as varied as Omaha or Oman. Once there, they use technological acumen to help solve their clients’ thorniest and most vexing problems.”

“One of the highest-profile companies tapping into the Palantir alumni network is Anduril. […] It includes three former Palantir employees on its founding team: Trae Stephens, Matt Grimm and Brian Schimpf. The company, which makes software and hardware products and systems for national-security operations, was last valued in June at $30.5 billion.”

Entropy

Jumia is fighting with Temu and Shein to win the African e-commerce market. - Rest of the World

“Jumia is now using the same playbook its Chinese rivals have thrived on: adding Chinese merchants to the seller pool to stay competitive. It is also leveraging the U.S.-China trade war as Chinese merchants look to diversify into African markets.”

“Jumia has been cutting its losses since 2022. The company has exited underperforming businesses such as food delivery across several African markets, and sharpened its focus on physical goods in core markets like Nigeria.”

“Over the past three years, we’ve restructured Jumia to serve the African middle class with maximum affordability. Our typical customer earns $200–$500 a month, with about $20–$30 in discretionary income. That means offering $5–$10 shoes, $80 TVs instead of $200 or $1,000 items.”

“Temu focuses on low-cost items like fashion and beauty, but we serve a wider range: fridges, phones, TVs. Our brand remains strong. In Nigeria, Jumia’s GMV is up 36% year over year, despite Temu’s entry.”

“We do believe that the U.S. tariffs will be an opportunity for Jumia. Chinese vendors have been very focused on the U.S. as a market over the past couple of years. But the traffic and volumes of Temu have really collapsed over the last couple of months after the increase in tariffs. So, we believe that the Chinese manufacturing will have to rebalance its exports, and that they will have to pay more attention to places like Africa.”

“At this stage, we’re leveraging AI in some obvious fields like call center automation, so we have smaller call centers processing more orders because we’ve been able to automate lots of requests that are now managed by AI-enabled bots. These bots manage simple requests such as order status, and we keep improving them to give them conversational ability. It’s helping us to be a lot more efficient and save money.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋