📖 Venture Chronicles - August 2023

Overlooked #156

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of August.

Please note that the date picked for each event is not always the exact event date but the one at which I decided to write about the event.

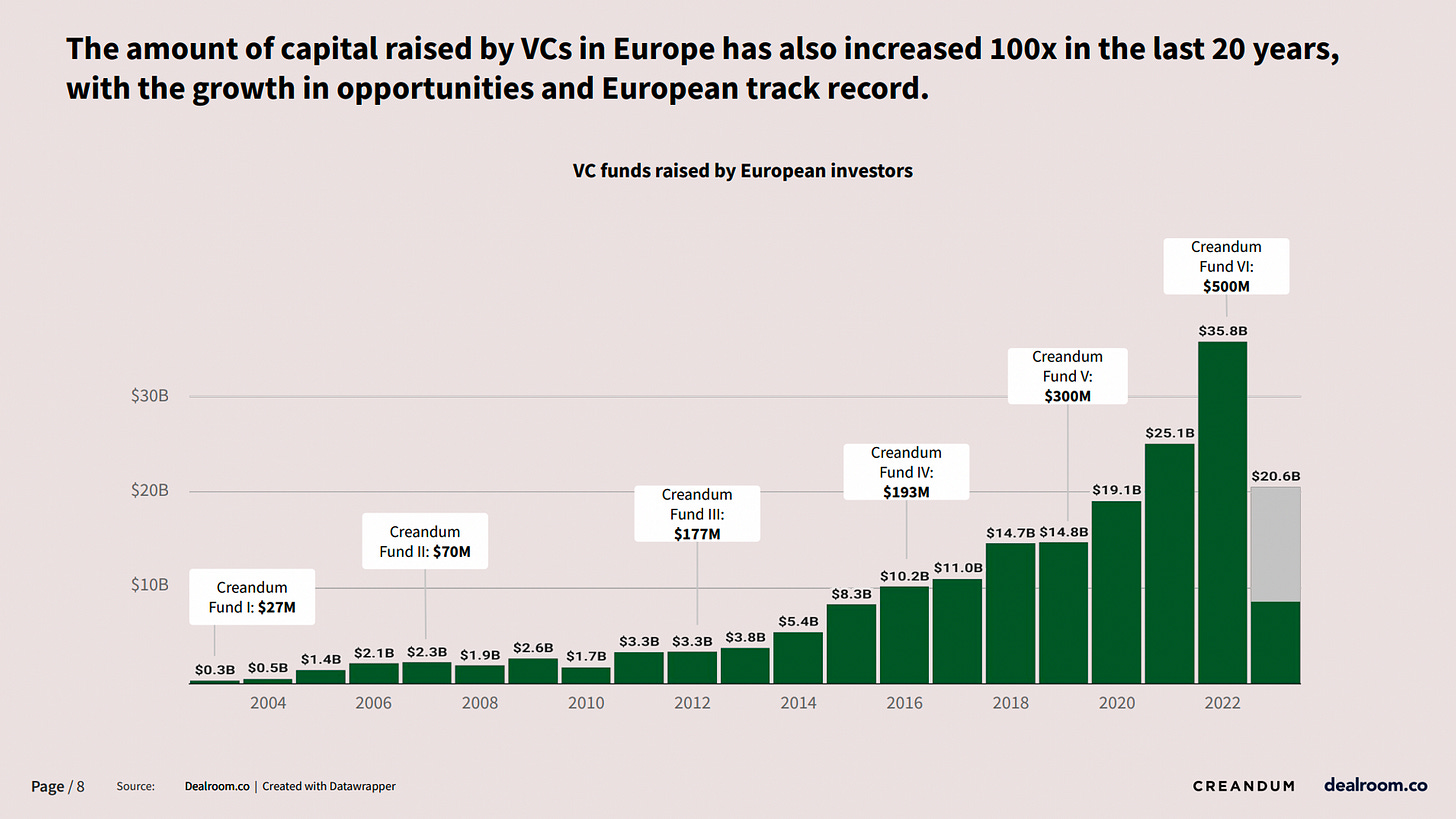

Tuesday, Aug. 1st: Creandum and Dealroom co-published a report on the rise of European tech over the past 20 years. - Dealroom

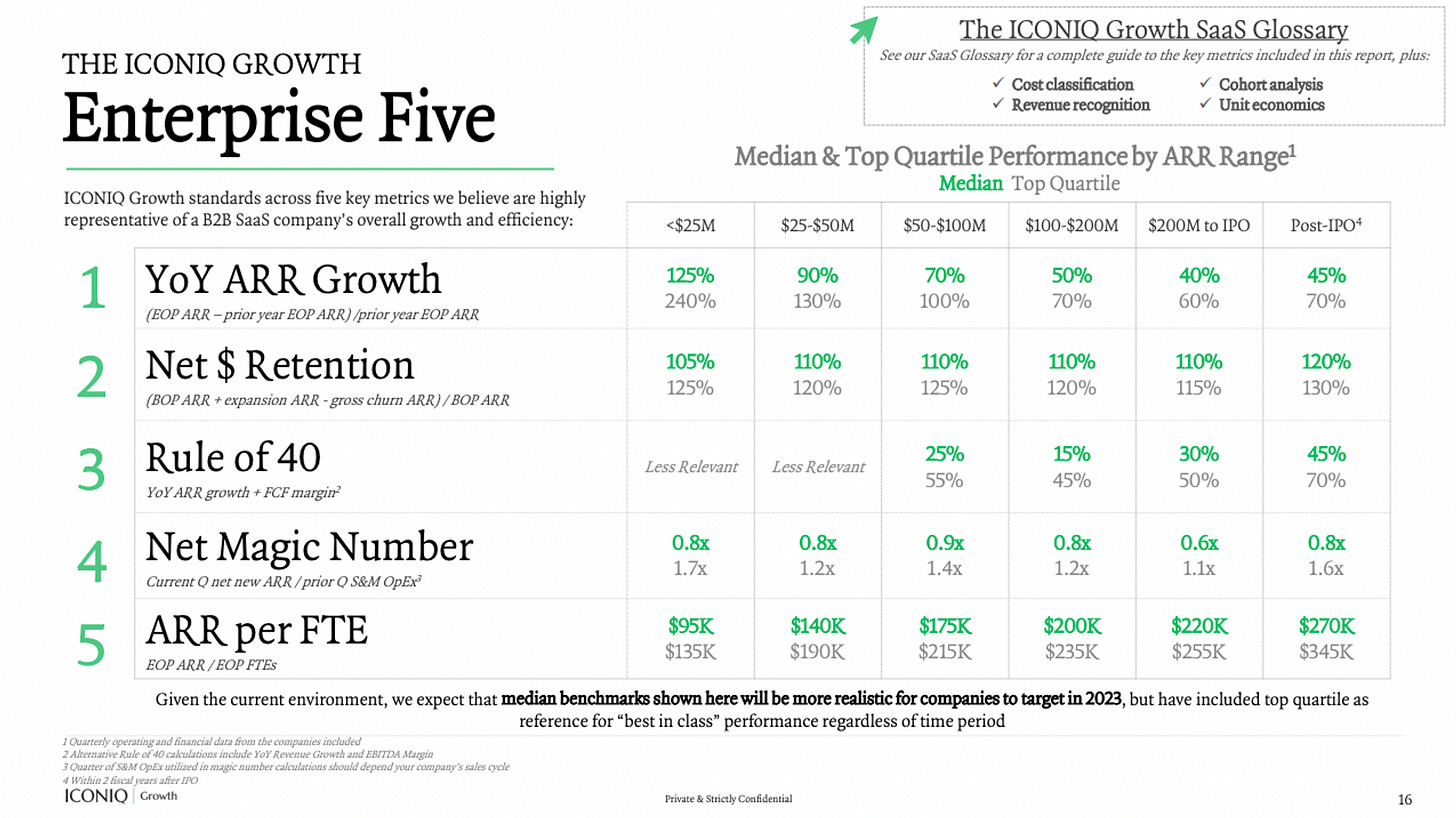

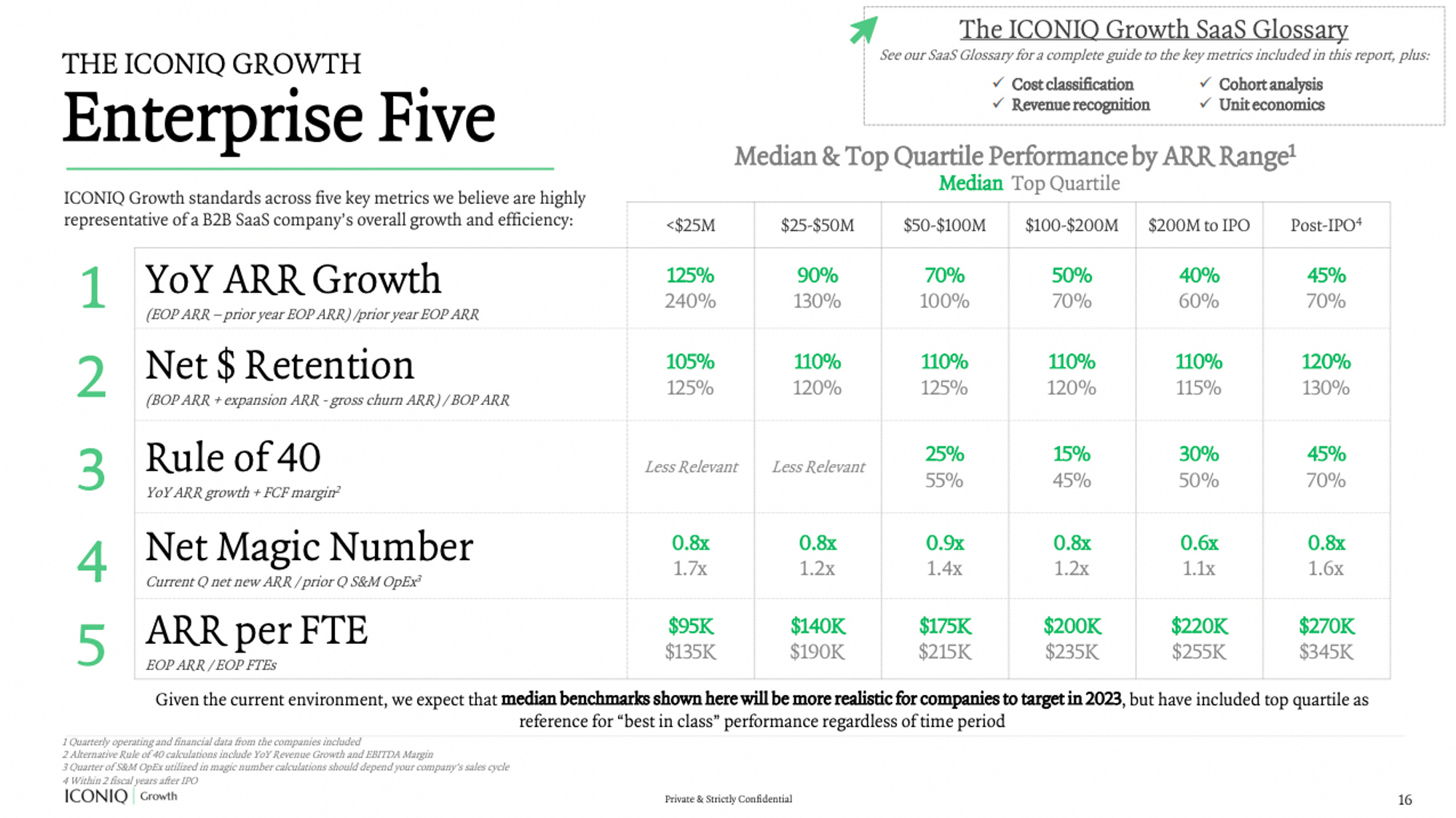

Wednesday, Aug. 2nd: Iconiq published a report on growth and unit economics benchmarking c. 100 late-stage SaaS companies. - Iconiq

Thursday, Aug. 3rd: Lula secured a $35.5m series B co-led by Khosla and NextView. It offers insurance as a service for companies allowing businesses to seamlessly integrate insurance into their offering. Lula manages all aspects including risk assessment, claims processing, and policy administration. It works with car rental, car sharing and trucking companies. It has customers like Kyte, Turo and State National. It will use the funding to expand into logistics. - Techcrunch

Friday, Aug. 4th: Ben Casnocha shared lessons from working with Reid Hoffman who is the cofounder of professional social network LinkedIn as well as VC house Greylock. - Ben Casnocha

The best way to get a busy person’s attention is to help them. Every busy person craves for unique insights which can be tied either to their professional or their personal lives.

The values that actually shape a culture have both upsides and downsides. “The values that matter offer clear pros and cons, clear upside and downside. Just as there’s no great opportunity without risk, there’s no decisive culture-shaping value that also doesn’t have drawbacks.” “I don’t believe there are “good” corporate values or “bad” corporate values–beyond the obvious. Many different types of cultures have produced successful companies. What’s important is to understand the values at work that actually shape your company’s behavior and to understand the tradeoffs involved.”

To build good partnerships, identify and emphasize any misaligned incentives. “Make misalignments explicit with yourself and the other party so that if and when they rear their head, neither side is surprised.”

Trade up on trust even if it means you have to trade down a bit on competency. “Choose to work with someone you know who’s a fast learner over someone who’s a bit more qualified who you do not know.”

Make people genuine partners will make them work harder. “When people are personally invested in the public success of a project, they’ll work harder, they’ll care more, and the final product will likely benefit.”

Saturday, Aug. 5th: Casey Winters wrote a post arguing that it’s extremely hard to build a consumer subscription business for several reasons: (i) churn is higher, (ii) ARPU (Average Revenue Per User) is lower, (iii) you cannot have a NDR (Net Dollar Retention) above 100%, (iii) payment fees are more expensive due to the Apple/Google’s mobile stores tax, (iv) customer acquisition is more complex. In order to solve some of these issues, these businesses should: (i) create & leverage network effects to improve retention & reduce acquisition costs, (ii) go multi-product early-on to improve retention and increase ARPU, (iii) work on less saturated acquisition channels (i.e. beyond Google, Apple and Meta), (iv) sell to businesses. - Casey Winters

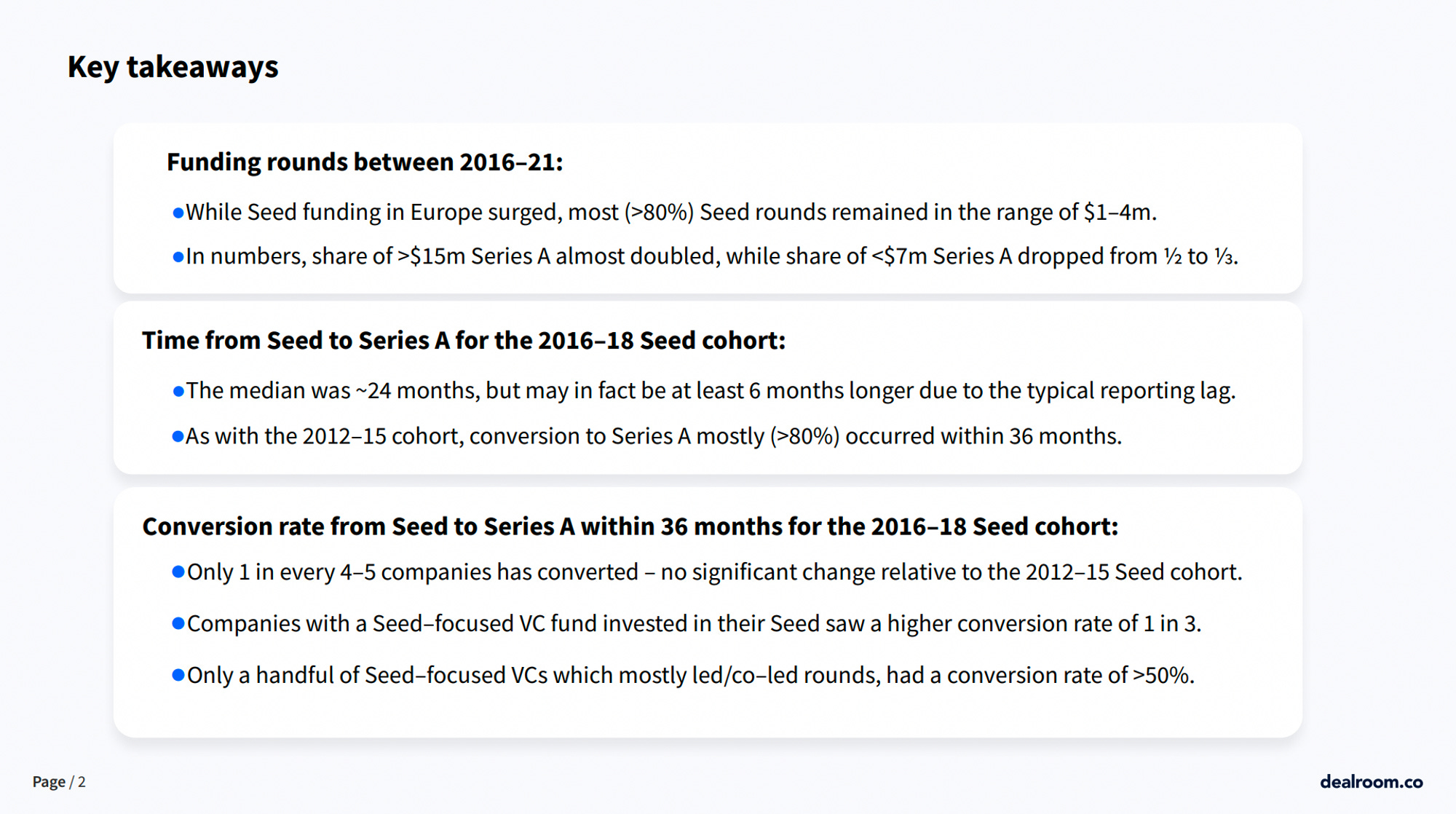

Sunday, Aug. 6th: LocalGlobe and Dealroom co-published a report on what does it takes to go from seed to series A in Europe. - Dealroom

80% of seed rounds are between $1m and $4m.

24 months is the median average to go from seed and series A.

20-25% of seed companies convert from seed to series A with some seed funds like P9, LocalGlobe and Cherry registering a conversion rate above 50%.

Monday, Aug. 7th: Alex Johnson wrote about payments in the construction industry. - Alex Johnson

“How does everyone involved in the construction of your new building get paid? […]

The laborers get paid by the subcontractors on a two-week or even one-week basis. The reason for this is simple: competition for skilled construction labor is intense, and if a subcontractor doesn’t pay their laborers on a frequent basis, they lose the laborers.

Materials need to be purchased upfront by the subcontractors (you can’t build without building materials), and the standard payment term is usually 30 days (with a 2-3% premium for those terms built into the final price).

Subcontractors are usually paid in what are called progress payments. At the end of every month, a subcontractor will submit an invoice to the general contractor. The amount of that invoice will be for whatever percentage of the project was completed during that month. So, if the total cost of the project for a subcontractor is $500,000 and they complete 10% of the project during that month, the invoice for that month will be $50,000. Additionally, the owner will often retain a portion of the total amount (usually 10%) until the project is complete, in order to ensure that the subcontractors have satisfied all of their contractual obligations.

All of these invoices from subcontractors are aggregated together by the general contractor, who then submits a master payout request to the owner. The owner will then, in turn, submit a draw request from the bank that is financing the project.

Once the bank cuts the big check, the money flows back down to the owner and then to the general contractor, and then to the subcontractors.”

“In the US, anyone who supplies labor or materials for the improvement of real estate has a legal claim against that real estate for the purpose of recouping the costs of their labor or materials. This is called a mechanic’s lien. Mechanic’s liens exist to ensure that contractors, builders, and suppliers don’t get stiffed by real estate owners.”

“In order to ensure that they are not paying for work that hasn’t been done yet or liable for subcontractors not paying their subs, laborers, or suppliers, real estate owners require a great deal of diligence to be done before they agree to make payments.”

“The U.S. construction industry is incredibly fragmented. The top 400 contractors only account for about 20% of the market, meaning that there is a massively long tail of small contractors.”

vSaaS incumbents are better positioned than newly created vertical fintechs to start offering financial services to their industry because vSaaS have distribution, data and control over workflows.

Tuesday, Aug. 8th: Hopin sold its initial product, a virtual event platform, to RingCentral for $50m ($15m upfront and $35m earn-out). Hopin managed to raise $1bn across 4 funding rounds within just 14 months. It includes a last round at a $7.75bn valuation in Aug. 2021 (after having gone from $20m in ARR in Nov. 2020 to $100m in Aug. 2021). Hopin’s CEO cashed-out c.$195m from secondaries during these funding rounds and has recently left the company. Hopin has still $400m in cash. The company acquired a live streaming business called Streamyard for $250m in 2021 which has now become the main product of the company. - Kyle Harrison, Business Insider, Techcrunch, Skift

“Investors are very much in the business of "dreaming the dream" but too often we have investors that assume the dream is supposed to be a fever dream. Instead, the reality is that human behavior changes very little, and when it does it happens very slowly.”

“One of the most un-dealt with ramifications of a 13-year bull market is the institutionalized belief in "the greater fool." People can make money, not because a business is sound, but because there is always someone else down the line who will buy you out.”

Wednesday, Aug. 9th: Apollo raised a $100m series D at a $1.6bn valuation led by Bain with the participation of Sequoia, Tribe and Nexus. It’s a sales tech platform combining sales intelligence with a database of 270m contacts as well as sales prospecting. It will use the funding to invest in product development and to double its team size by 2025. Apollo is another player (competing with Zoominfo and Gong) building a sales tech platform aiming at consolidating the sales stack in a world in which the average sales team use 10 tools on average and spend only 28% of their time actually selling. - Techcrunch

Thursday, Aug. 10th: I listened to a 20VC’s podcast episode on the current state of seed investing with Frank Rotman (QED), Jason Lemkin (SaaStr) and Sam Lessin (Slow Ventures). - 20VC

The “factory model of seed investing” in which you build and fund good companies on repeatable playbooks (e.g. DTC companies, consumer fintechs) is dead. Seed is going back to its roots as a game in which you must find overlooked outliers and in which you will have power law dynamics.

When capital was abundant, businesses were not systematically de-risked from one round to the other. It resulted in unusually low failure rates as companies progressed from one round to the next.

The best seed deals often originate outside the “factory model” and are hard to package for next investors. They’re the ones on which you have a weird thesis and on which you have a low entry price because you’re the only believer. You end-up making money on these deals because your initial unconventional belief proves to be right.

If prices don't correct at the seed stage, many companies won't be able to raise an A round because they won't have progressed far enough and fast enough to justify a 2-3x multiple on their previous valuation. “You reduce the aperture of downstream capital if you overfunded yourself at the wrong valuation early on.”

Startups need to learn to make money at a low level of scale. Either you’re in a market with an unlimited TAM where you can run unprofitably for an extended period, or you should focus on early profitability to sustain growth without relying on external capital.

Friday, Aug. 11th: The Generalist wrote about Plaid’s journey as an independent company since its failed acquisition by Visa. - The Generalist

Plaid moved from a single product providing financial data APIs to a broader platform with other products in identity verification, fraud prevention, payments as well as assets & income verification for lenders.

Compared to historical financial data connectivity providers, Plaid adopted a bottom-up approach à la Stripe building the best APIs for developers (vs. top-down sales) and a usage based business model (vs. multi-year contracts).

Plaid’s platform can help to (i) onboard users collecting data on user identity, bank balance, transaction history, income & employment status as assets & liabilities, (ii) manage risk & prevent fraud, (iii) streamline payments and (iv) improve credit decisioning.

Plaid has expanded its addressable market by selling to companies beyond consumer fintechs (50% of new deals since 2022 have been outside consumer fintechs) and by selling outside the US (esp. in Europe which is Plaid’s fastest growing market).

Plaid is facing the following risks: (i) growing into its last private valuation as it raised from Altimeter at a $13.4bn valuation in Apr. 2021 which can be compared to a $250m ARR reached in 2021 (53.6x EV/ARR multiple), (ii) commoditisation of its initial core offering around banking API connections and (iii) not sizing RTP (Real Time Payments) and FedNow as new payment networks to build on top (vs. only ACH).

Saturday, Aug. 12th: Alloy’s CEO, Sara Du, wrote about the benefit of initially targeting a single industry before adopting a broader go-to-market strategy. Alloy is a SaaS to quickly add integrations to your product. It began in the commerce vertical before expanding into a more horizontal platform (ERP, CRM, e-commerce, accounting). - Sara Du, Alloy

“Verticalization leads to focus, and a focused go-to-market has major benefits: (i) razor sharp messaging & out-bounding, (ii) discipline in the team, (iii) faster feedback loops, (iv) customer trust.”

To pick the initial vertical to serve, you can look at (i) where the market is pulling for your solution, (ii) which industry can make the most money most quickly.

To expand beyond your initial vertical, you should see market pull to build a broader product (e.g. Alloy had leads which wanted integrations beyond the commerce space).

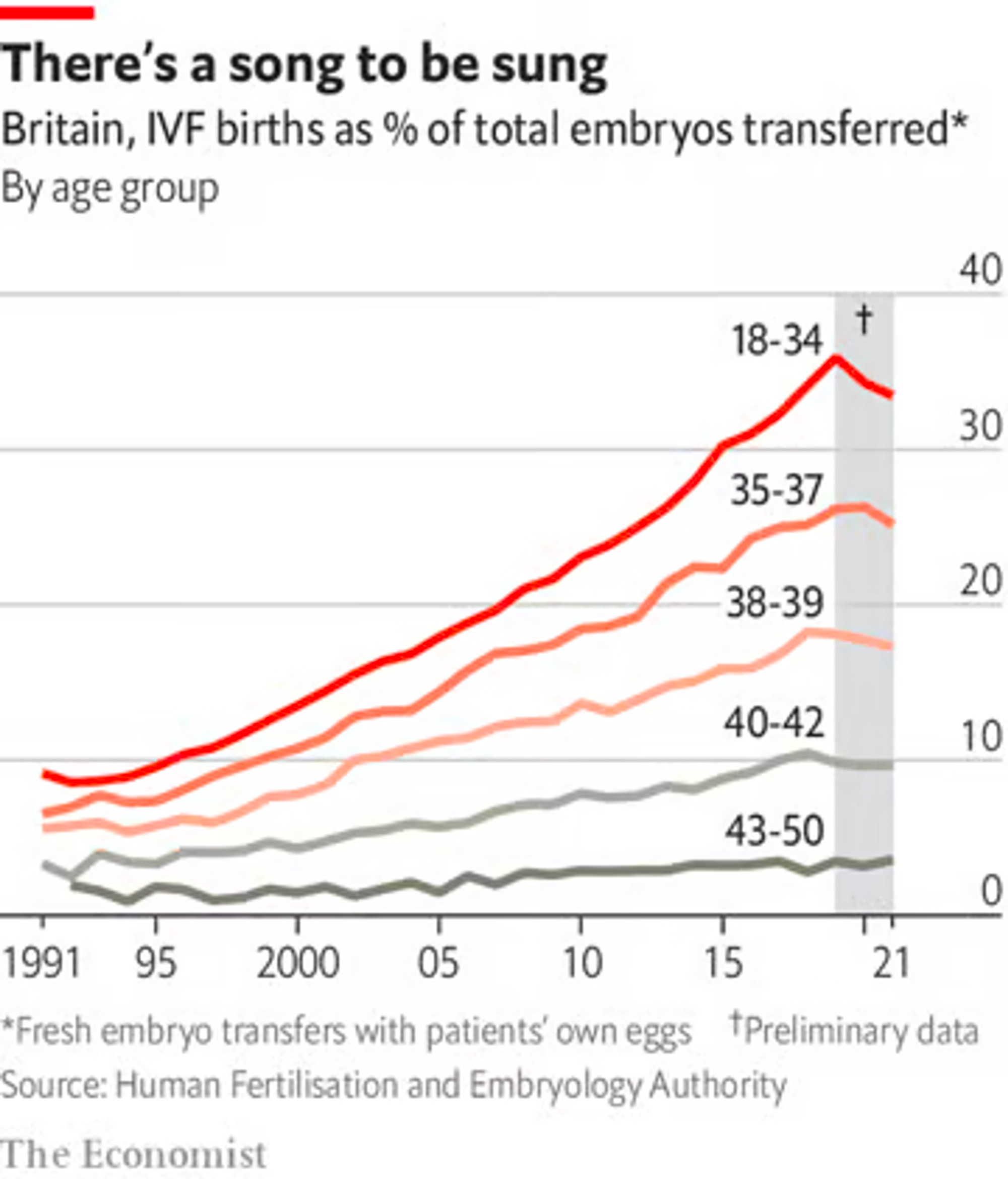

Sunday, Aug. 13th: The Economist wrote a report on the future of fertility. - The Economist

1/6 people in the world suffer from infertility. In the US, a fertility treatment cycle can cost $20k. IVF accounts for 9% of live births in Denmark.

“As IVF has become safer and more common, it has also become more effective, largely thanks to advances in the handling of embryos. In Britain, 25-30% of the embryos transferred to the wombs of women in their mid-30s now lead to live births. That is about four times better than in the early 1990s.”

“It is the age of the ovary from which the egg is taken, rather than the womb that nurtures the embryo, which matters. That is why an increasing number of women in their late 20s and early 30s are having some of their eggs frozen.”

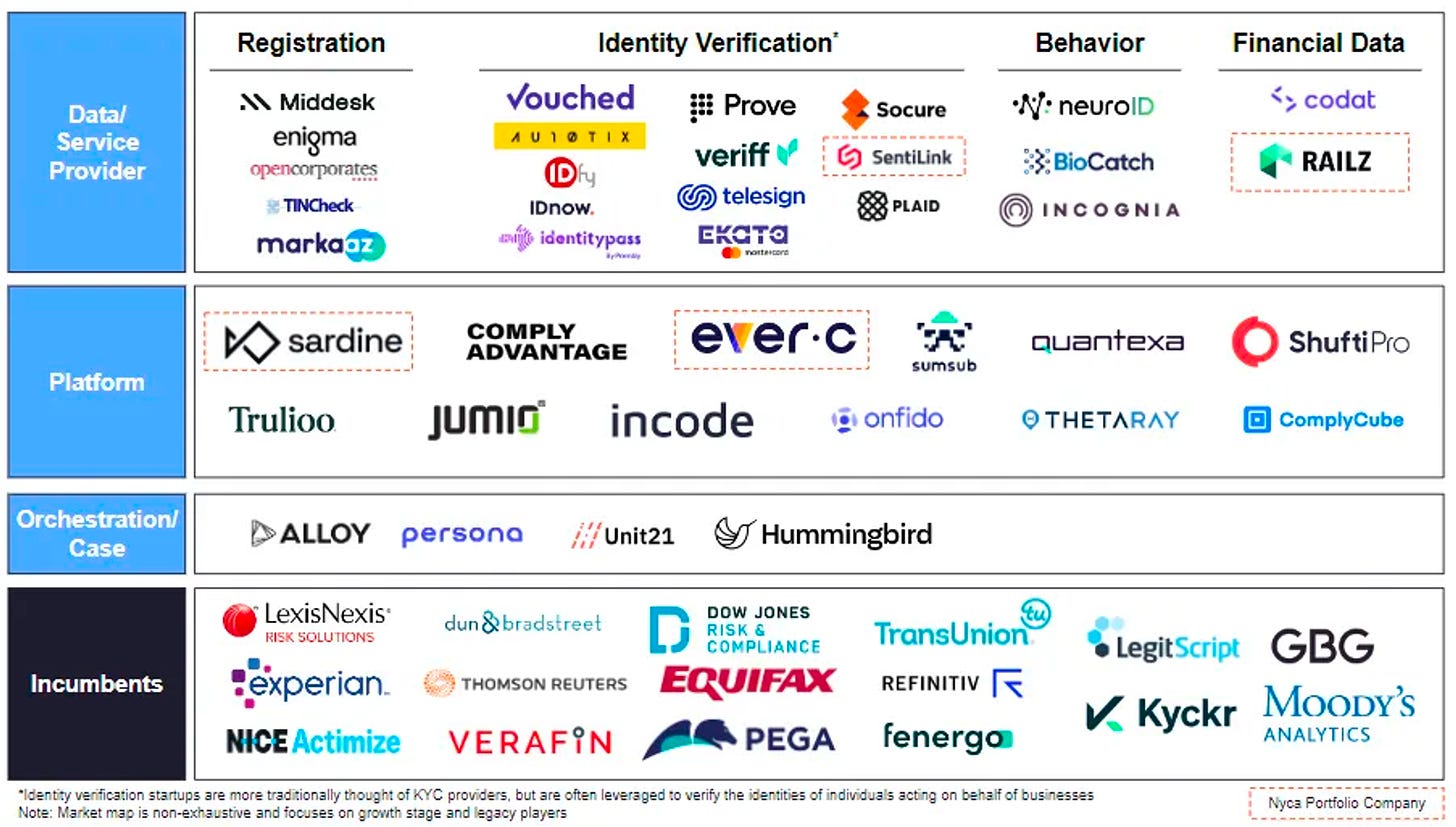

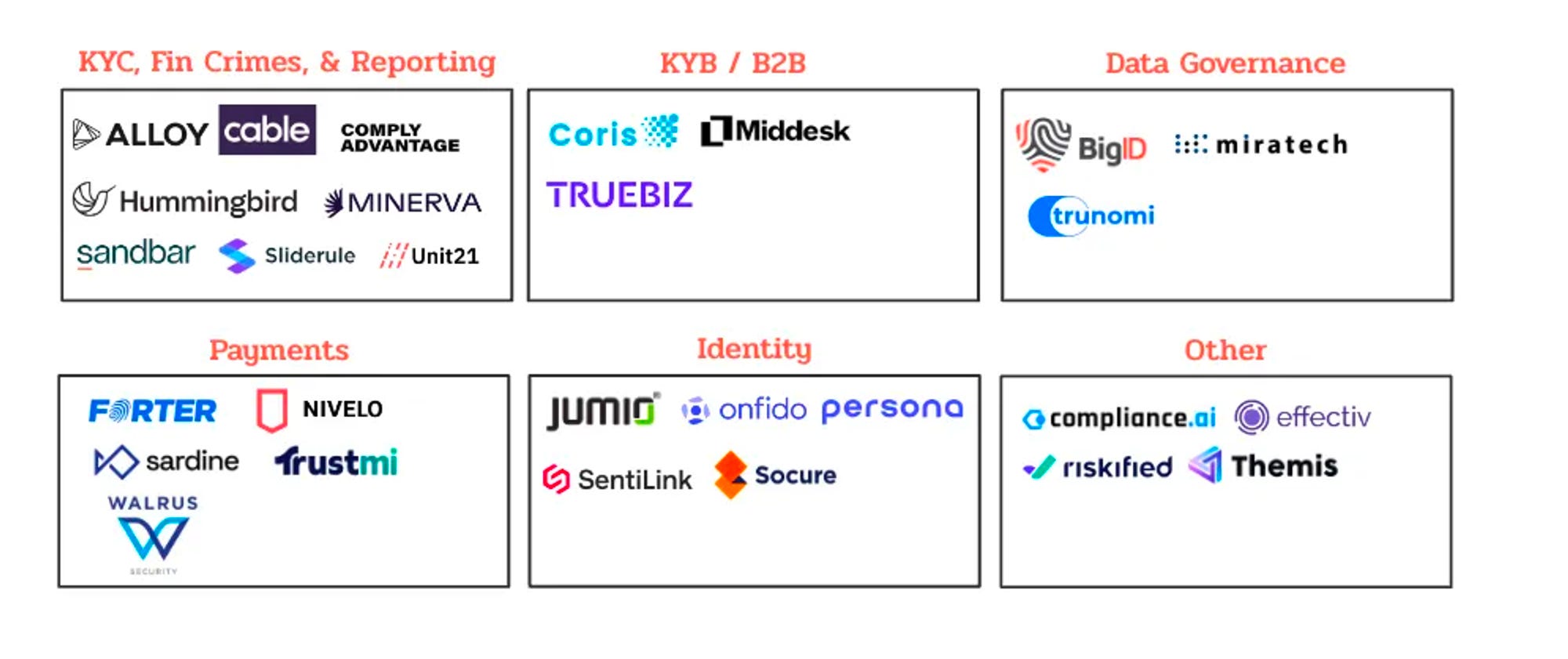

Monday, Aug. 14th: Rohan Mehta wrote about the KYB market. - Fintech Fundamentals

“Many vendors have pivoted to focus on orchestration because of the long-term stickiness and ability to own the end customer relationship (making it easier to upsell/cross-sell other solutions). A competing tension is that many large enterprises are using a platform/orchestration engine to launch something quickly, try out many vendors, and then go direct to vendors and build the orchestration themselves to save on costs and own the relationship with the data provider (i.e., to negotiate volume discounts and request customization). A key point here is that orchestration in itself is not a moat without value-add on top; many orchestrators build down over time in light of this challenge.”

To make a dent in the KYB market, there are 4 wedges: (i) alternative data, (ii) cross border data aggregation, (iii) improved AI/ML, (iv) better orchestration capabilities.

“To get to $100m+ in ARR and achieve the holy grail of a comprehensive KYB solution, a few qualities are essential:

A defensible data moat, which can come from (i) a unique data sets and lack of reliance on traditional data points, (ii) proprietary AI/ML, (iii) give-to-get models with network effects, built on modern data infrastructure that enables fast feature changes and ML enhancement.

An opinionated “open-platform strategy” allowing buyers to orchestrate end-to-end KYB workflows combining in-house assets with third party data/services.

Architecture that intentionally combines product adjacencies (credit, fraud) and enables customer segment adjacencies (non-FIs),

Relentless execution and opportunistic M&A.”

Tuesday, Aug. 15th: I listened to a 20VC’s podcast episode with Jason Lemkin who is SaaStr’s founder and who invested into unicorns like Algolia, Pipedrive, Salesloft, Talkdesk and RevenueCat. Jason talks about the current state of the venture market. - 20VC

When you start in venture, you should try to invest quickly in the great companies to which you have unfair access. Having a successful investment early in your venture career can be a massive boost, as it allows you to raise two or three funds based on that success and leverage it as a reference for a decade.

Multi-stage funds will have to return to later-stage rounds to deploy the capital they have raised. Currently, they invest in seed-stage rounds to stay active in the market, as there is limited activity at later stages.

It’s impossible for a seed fund to generate strong returns by investing into hot seed rounds.

The more crowded a category is, the later you should invest to ensure that you're backing a company that is breaking out from the competition.

There is a slowdown in series A/B because “investors want a return to rationality and founders are not there yet”. There is a misconnect between what founders and investors want. Companies with high burn will fail. Companies with runway will take the time needed to have the right traction to raise the next round at a sensible valuation.

Wednesday, Aug. 16th: Clari acquired Groove adding sales engagement to its revenue platform. Clari started with revenue forecasting in 2012. It expanded into action plans in 2021 and conversation intelligence in 2022 (acquiring Wingman). Major vendors in the B2B sales stack (e.g. Clari, ZoomInfo, Gong, Salesloft) are consolidating the market building directly competing comprehensive sales platforms via external growth and product development. - Vlad Oleksiienko, BusinessWire, Clari

Thursday, Aug. 17th: Toast published its Q2-2023 results. - Toast

Toast reached $1.1bn in ARR growing 45% YoY and reached positive adjusted EBITDA. It added 7.5k locations in the past quarter to reach 93k locations. It has 43% of its locations using 6+ products from its platform.

Toast is expanding its TAM by serving restaurants from hotels/QSRs as well as by going upmarket after large chains of restaurants. For instance, Toast is now an approved vendor to sell to Marriott’s restaurants.

Toast launched Toast Catering & Events, which is a module integrated into its POS system, to help restaurant manage catering orders and event planning (e.g. order tracking, quote and invoicing, etc.). 60% of SMBs restaurants offer catering on top of their on-premise business.

Friday, Aug. 18th: Bessemer wrote about the climate & energy software landscape. - Bessemer

“This 21st century story is not one of atoms vs. bits but rather of bits enabling atoms. While solar panels, heat pumps, and EVs will be critical to address the energy challenges ahead of us, software will play a significant role in how people build new systems and processes for the clean energy industry; much of the green transition will rely on how software optimizes the value chain and makes use of these physical energy assets.”

“Demand for technologies like EVs and heat pumps has never been higher. EV sales are projected to comprise 60% of new car sales by 2030, while global heat pump sales are expected to meet 20% of global heating needs by 2030.”

The clean energy transition has several drivers: (i) the rapid decline in the cost of solar & wind energy, (ii) the alignment of business and investment models with commercial drivers, (iii) increasing digitization enabling new energy apps, (iv) legislation in western countries.

Saturday, Aug. 19th: Sapphire wrote about the procurement tech landscape. - Sapphire

“Procurement has become more influential than ever. As macroeconomic and geopolitical shocks rocked industries and capital markets in recent years, the importance of efficient spend and maintaining supply chain resilience and visibility has risen dramatically.”

“Over the past two decades, procurement tech has evolved from point solutions (i.e., FreeMarkets, Webango, diCarta in the early 1990s and 2000s) to multi-product suites (i.e., SAP Ariba, Coupa) that address the end-to-end needs of procurement teams. Today, with procurement gaining recognition as a growth engine and mission-critical function, organizations are looking for high-impact, best-of-breed procurement enablement technologies.”

Sunday, Aug. 20th: Cowboy wrote about the compliance sector. - Cowboy

In 2022, traditional financial institutions and fintechs spent $46bn on people and technology to handle compliance (vs. $41bn in 2021 and $30bn in 2019).

“Some [companies] have turned to each other, creating consortium-like structures (i.e., Unit21, Sardine, and Plaid) to build off each other’s data to minimize risk.”

“AI has created greater demand for compliance tools to combat these new and evolving risks. AI proliferation through FIs will cause these challenges to arise even faster than previously imagined.”

Monday, Aug. 21th: Will Robbins (GP at Contrary) wrote about the importance of being generalist as a venture investor. - Techcrunch

““Generalist” investing does not mean lack of technical knowledge. It does not mean a lack of preference of some verticals over others. And it certainly does not mean unsophistication in their network.”

“The eternal relevance of generalist in venture comes down to two simple and easy-to-prove facts: (1) revolutionary tech companies are thematically unpredictable, and (2) transcendent founder talent is still needed even in the most fruitful spaces.”

“The specialist investor must have the same eagle eye for outliers as the generalist investor, but with narrower aperture.”

“How can a generalist compete with a specialist when it comes to customer introductions, or tactical advice? My answer is simple: We can’t, but we don’t need to. The specific product and marketing challenges faced by entrepreneurs tend to be far too specific for an outsider to properly help.”

“Ultimately my job as a VC is selling a few simple products: cash, trusted reputation, and access to as much downstream capital as possible.”

Tuesday, Aug. 22nd: Instacart publicly released its S1 and should start trading in September. I wrote a deep-dive on Instacart’s IPO that you can find here. - Instacart

On Aug. 26th, Instacart made public its S1 filing to go public. It plans to start trading on the stock exchange in September. It was a long awaited IPO for several reasons: (i) Instacart submitted a first S1 draft to go public in May 2022, (ii) the tech IPO market has been completely dry in the last 18 months following the tech public market downturn, (iii) Instacart reshuffled its internal valuation several times going from being valued $39bn to being valued $12bn. Together with Arm and Klaviyo, Instacart is part of a first batch of private tech companies that will go public in September and that will give the tone for what will happen for other potential tech IPOs in the coming quarters (e.g. Stripe, Databricks).

Instacart was founded in 2012. It has been a major contributor to digitise the US grocery sector pioneering online delivery thanks to a mobile app empowering consumers to order online from their favourite retailers and thanks to a network of independent contractors called shoppers picking, packing and delivering grocery items to end consumers. It raised $2.9bn in capital from top-tier investors like YC, Khosla, Sequoia, a16z, Kleiner Perkins, DST, General Catalyst and Coatue. It had several near-death experiences including when the company was losing $14 in gross margin on every order in 2015 or when Amazon acquired WholeFoods in 2017 which was generating 40% of Instacart’s GMV. Instacart had also ridden an unexpected black swan with covid which brought the company to another dimension growing its GMV by 303% from $5.1bn in 2019 to $20.7bn in 2020. It brought a massive influx of consumers and retailers on its platform when everyone was stuck at home, had to order online to get their groceries delivered at home.

In July 2021, Fidji Simo became Instacart’s CEO replacing Apoorva Mehta who was Instacart’s original founder and CEO. Fidji opened a new chapter for Instacart focusing on delivering sustainable profitable growth based on three main levers: (i) building a powerful advertising platform for CPG brands, (i) selling SaaS to retailers to digitise their operations online and in-store as well as (iii) making Instacart more affordable to address price sensitive grocery consumers.

In the last 12 months, Instacart made $29.4bn in GMV (growing 6.5% YoY) and $2.9bn in revenues (growing 39.7% YoY).

Wednesday, Aug. 23rd: Lux published its Q2-2023’s LPs report. - Lux

“Human progress does not come from equanimity, but rather in the untamed and riotous competition of ideas on the very edge of human intellect.”

“At Lux, we believe that science and technology are the only practical means by which we can ever hope to take destiny into our own hands. It is no surprise that Lux strives to back the founders pushing on the frontiers of scientific knowledge and understanding and who will ultimately drive us all forward.”

“Progress-measured by time-prices-has dramatically improved over the past century, and yet, when we look at the edges of what's possible, there are still so many defining innovations ready to be discovered-and funded.”

“I have the tremendous privilege, alongside my Lux partners, to identify dreamers who are turning science fiction into science fact.”

Lux invests in 4 core areas: (i) secure our life & environment (e.g. Anduril), (ii) supercharge productivity (e.g. Applied Intuition), (iii) enable creativity & free expression (e.g. Hugging Face), (iv) reduce human suffering & advance human health (e.g. Kallyope).

“I believe that failure comes from a failure to imagine failure. To avoid failure, we need sustained commitment to long-term scientific funding, reflection on our bedrock principles of welcoming immigrants, and recommitment to fight for American values like freedom of speech and privacy worldwide.”

Thursday, Aug. 24th: The Financial Times wrote a bear case on generative AI. - FT, Gary Marcus

“Hallucinations will remain a feature, rather than a bug, of generative AI models, unfixable using their current methodology. […] For some users, this inbuilt unreliability is a deal-breaker.”

“Even more concerning is the idea that content produced by generative AI is polluting the data sets on which future systems will be trained, threatening what some have called model collapse”.

There are 3 paths for Gen. AI to make money: (i) being used as a productivity tool for use cases where 100% accuracy is not required (e.g. copywriting, call centre ops), (ii) solve real world narrow problems with higher accuracy than an horizontal model, (iii) create services & business models not possible before gen. AI.

“Few things I have ever seen have been more hyped than generative AI. […] But, to begin with, the revenue isn’t there yet, and might never come. The valuations anticipate trillion dollar markets, but the actual current revenues from generative AI are rumored to be in the hundreds of millions. Most of the revenue so far seems to derive from two sources, writing semi-automatic code (programmers love using generative tools as assistants) and writing text”

“Perhaps the only use case that really seemed compelling to either of us economically was search (e.g., using Bing powered by ChatGPT instead of Google Search) — but the technical problems there are immense; there is no reason to think that the hallucination problem will be solved soon.”

“If hallucinations aren’t fixable, generative AI probably isn’t going to make a trillion dollars a year.”

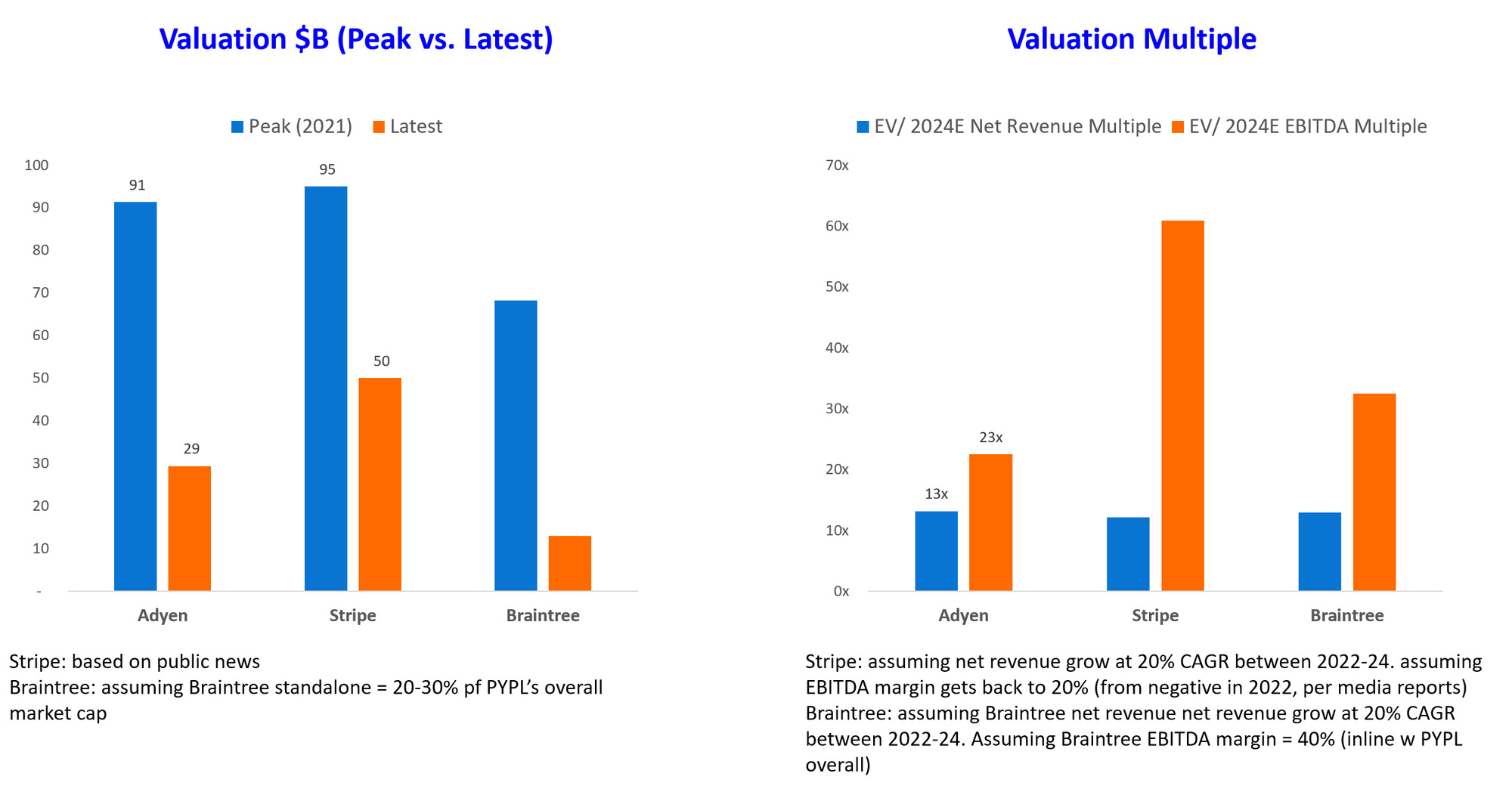

Friday, Aug. 25th: Adyen’s market capitalisation was severely impacted by the announcement of weak quarterly results missing its targets. - Reuters, Stratechery, Every, Chamath Palihapitiya, Freda Duan

Adyen is struggling to expand its business in the US (20% YoY growth in H1-23 compared to 45-80% YoY growth in the previous 4 semesters) in which competition is more intense and employees are more expensive putting strong pressures on margins.

“Adyen highlighted a few factors that affected growth in the US, including competitive pricing pressure in the digital segment, unfavourable environment with high inflation and interest rates as well as sales team capacity constraints due to lower hiring.”

“Europe is a significantly more challenging payments environment than the US: you have to deal with multiple countries, multiple currencies, and multiple payment methods within each country and for each currency. This is a problem that Adyen solved remarkably well: merchants who used Adyen could write to one API that seamlessly operated across borders, currencies, and accommodated all of the relevant payment methods that filled out the resulting matrix of markets. This was, naturally, particularly attractive to large multi-nationals who sold to each of those individual markets; unsurprisingly, then, that Adyen’s customer base has primarily been large enterprises.”

“Stripe of course grew up in the U.S. market; the complexity problem it solved was making it easy for developers of any size to collect payments. It’s an interesting contrast that speaks to how value is captured: Adyen focused on big companies, which is simpler in terms of sales and support, because it was solving the complexity of the European market; Stripe focused on the complexity of small and medium-sized businesses, because it was operating in the simpler U.S. market. Both approaches were rational, just as both approaches speak to the challenges for both companies going forward.”

“The big question is whether payments are a race to the bottom or a product wedge to other offerings. If a race, Adyen, with its superior cost structure, has a chance of winning. If a wedge, Stripe is well positioned with their more diverse product suite and larger team.”

“The most important takeaway for me from Adyen’s earnings is the following: Middlemen business models are an eventual race to the bottom. […] In short, they can grow quickly and have semi-long periods of great profitably but market efficiency will eventually catch up with all of them and they will be forced to compete their profits away to keep growing.”

Saturday, Aug. 26th: Teamshares raised $245m in equity from investors including QED, USV, Spark, Khosla, and Slow. It also secured $150m in debt financing. Founded in 2018 in the US, Teamshares specializes in acquiring small businesses from retiring owners. The company distinguishes itself by replacing all of the financial services used by these businesses with in-house products. To date, Teamshares has acquired 84 businesses, each generating annual revenues ranging from $2m to $10m. These acquisitions span 6 categories: business services, consumer services, distribution, manufacturing, restaurants, and retail. Notably, Teamshares has developed a specific equity ownership model. It acquires the entire business from owners and allocates 10% of ownership to employees, with a long-term plan to increase employee ownership to 80% within 20 years. - Techcrunch

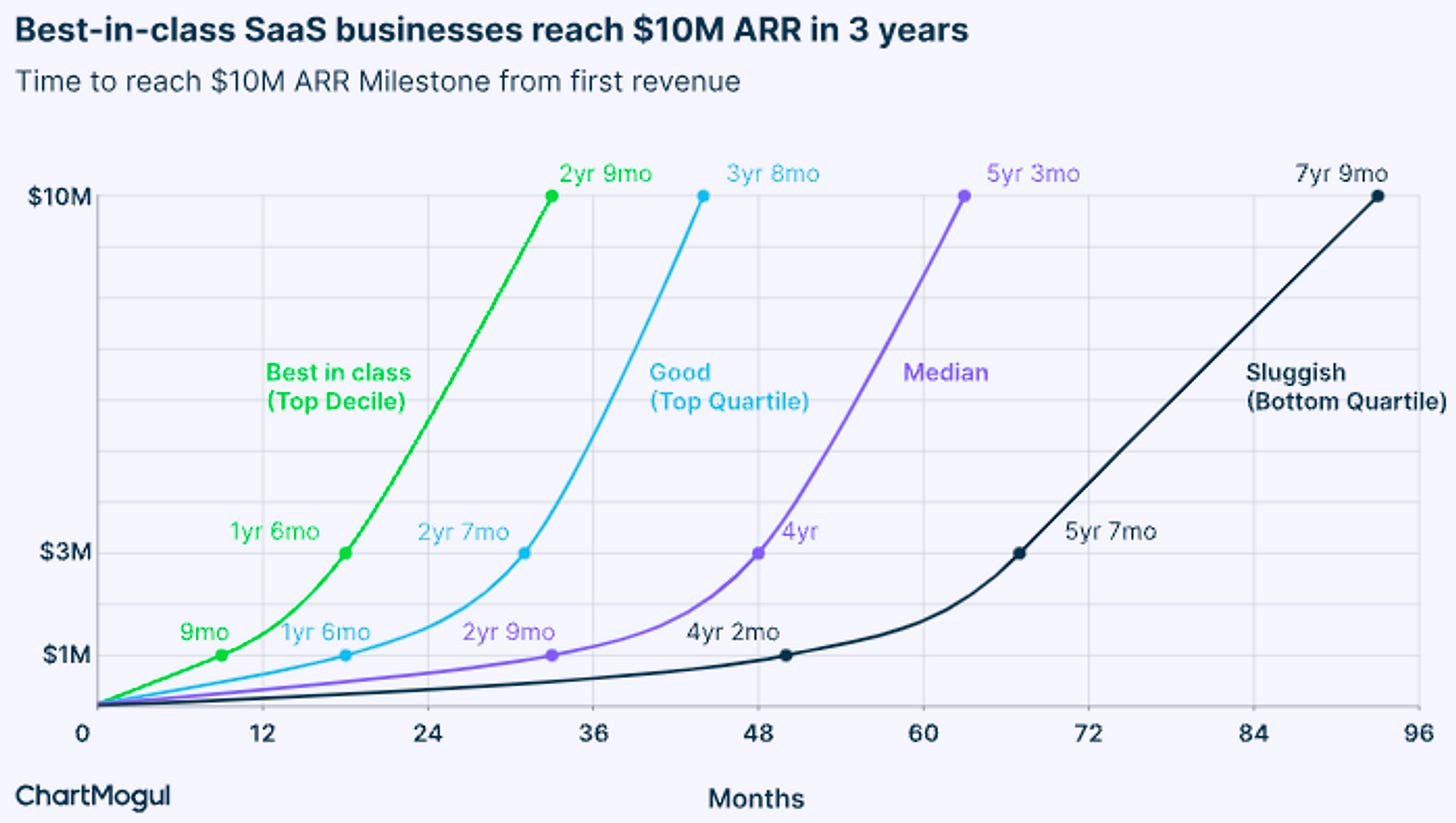

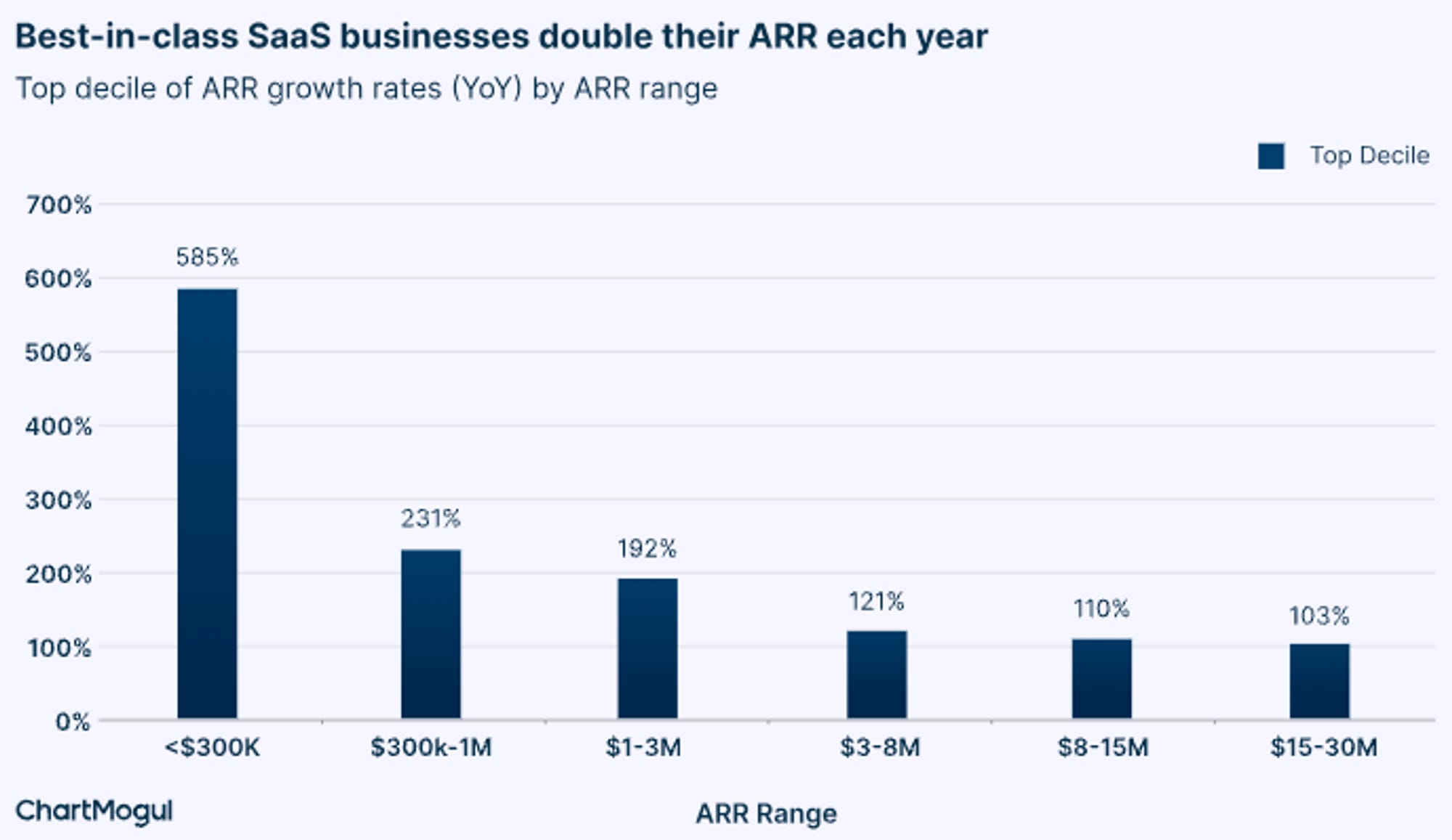

Sunday, Aug. 27th: Chartmogul published a great report with ARR growth benchmarks for SaaS companies. - Chartmogul

Top decile SaaS companies are growing by 231% YoY when they’re between $300k and $1m in ARR and by 192% YoY when they’re between $1m and $3m in ARR.

Top decile SaaS companies are going from 0 to $1m in ARR in 9 months. Top quartile SaaS companies achieve it in 18 months.

Top decile SaaS companies are going from 0 to $10m in ARR in 2 years and 9 months. Top quartile SaaS companies achieve it in 3 years and 8 months.

Only 13% of startups are able to reach $10m in ARR in less than 10 years.

36% of revenues added for SaaS businesses doing $15-30m in ARR are coming from expansion (vs. reactivation & new business).

“As companies scale, the proportion of revenue coming from annual plans increases. Companies with ARR in the range of $15-30M get 41% of their ARR from plans 12 months or longer.”

Monday, Aug. 28th: OpenAI released ChatGPT Enterprise, which is a corporate version of ChatGPT. It features data encryption for accessing its models without utilizing corporate proprietary data, offers unlimited access to GPT-4, provides sharable chat templates for team collaboration, and supports longer prompts. Notably, 80% of F500 companies have internal teams that have adopted ChatGPT. ChatGPT Enterprise is already in use by companies, including Block, Klarna, Canva, Carlyle, The Estée Lauder Companies, PwC, and Zapier.- Stratechery Bloomberg, OpenAI

Tuesday, Aug. 29th: Agave raised a $3m seed round led by Accel with YC’s participation. Agave is building Plaid for the construction industry to adress solve data silos between stakeholders and the numerous software solutions used in the industry. It has 70 customers and 4x its revenues YoY. - Agave, Techcrunch

“Our mission is to connect the fragmented systems that run construction on a single global standard.”

“Most of the software running construction was built decades ago, run on-prem, and lacked APIs. Alongside this, a growing cloud of modern tools is emerging, largely disconnected. Unlike other massive industries where startups had built sector-specific data infrastructure to solve this - like Plaid in banking - this hadn’t been done in construction.”

“Before Agave, integrations were tedious, expensive, and inefficient. Companies built connectors one by one in-house (consuming months-quarters of engineering time), engaged consultants to craft bespoke solutions (specific to just a few use-cases), or patched-together limited tools (each meeting only a subset of their needs). With Agave, construction companies and their tech providers can now connect over 30 systems with one API, even for systems with no native APIs.”

Agave’s Business Use Cases Wednesday, Aug. 30th: Acquired published a podcast episode on Costco. - Acquired

Costco makes $4bn from its membership. Members are more likely to purchase at Costco to maximize the profit from their membership. Costco’s members are also wealthier than the average American consumer because you need to be wealthy to pay for a membership and to buy in bulk.

Costco caps its markups on products at 14% to provide the best possible prices to its members.

Costco’s stores maintain a relatively small inventory with 3.8k SKUs. This approach aids vendors in negotiating the best possible prices on products with suppliers since they have a limited number of products to manage. Additionally, it accelerates inventory turnover, enabling Costco to generate revenues before having to pay its suppliers.

Thursday, Aug. 31st: Klaviyo publicly disclosed its S1 to go public. It was founded in 2012 in Boston. Klaviyo is a multi-channel (SMS, emails, push notifications) marketing automation platform for SMB businesses. It started as a marketing emailing product tailor made for e-commerce merchants using Shopify. It also leveraged the growing importance of first party data for powering efficient marketing in a world in which third party consumer data has become more difficult to access. - S1, Meritech, Clouded Judgement, Matt Turck

It’s a capital efficient business which is EBITDA profitable after having burned only $15m out of the $455m it raised in funding.

It generates $585m in revenues in the last 12 months growing at a 56.5% YoY growth. It has 130k customers ($5.1k ACV) including 1.5k customers paying over $50k per year. It has a 89% gross dollar retention and a 119% net dollar retention.

“Klaviyo has been very much focused on the Shopify ecosystem of small to medium-sized brands.” “77.5% of its total ARR in 2022 came from customers who use the Shopify platform, so it is majorly dependent on how Shopify treats it.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋