📖 Venture Chronicles - August 2022

Overlooked #121

Hi, it’s Alexandre from Eurazeo. I’m investing in seed & series A consumer and consumer enablers startups all over Europe. Overlooked is a weekly newsletter about venture capital and underrated consumer trends. Today, I’m sharing the most insightful tech news of August.

For 2022, I want to pick one piece of news per day and write a short comment about it. I want to talk about something that strikes me. Something that happened in the tech ecosystem. Here is the issue for August!

Monday, Aug. 1st: Bessemer published a new paper to share their learnings from investing into vertical SaaS. - Bessemer

“By focusing on a vertical market, these companies are able to trade market size for market share and in some cases achieve 50%+ market penetration.”

Top vertical SaaS are building “a layer cake of new products that drive continuous growth” (e.g. Veeva started with a CRM for the healthcare industry and added a product called Vault targeting research clinical opps).

If vertical SaaS interact with end consumers, it can monetize them at scale (e.g. ServiceTitan monetizing end consumers with a financing product to pay for home services provided by home services companies which are ServiceTitan’s customers).

Most vertical SaaS start by targeting SMBs and midmarket but have to move upmarket to sustain growth.

Financial services features in vertical SaaS seem to be the new eldorado to expand Total Addressable Market (TAM). Several products can be added: enhanced ACH (data-rich ACH), faster payment methods (fast ACH, virtual credit cards), cross border payments, lending/early payment discounts against receivables, credit card payments to pay vendors, spend management.

Tuesday, Aug. 2nd: Forage raised a $22m Series A from NYCA, PyPal and EO Ventures at a c.$100m valuation. In the US, 42m Americans receive food stamps that they can use offline with 250k retailers but with only 100 retailers online. Forage started as a consumer app for low-income households to get discounts on groceries. With covid, Forage discovered the pain point around food stamps as a payment method for ordering groceries online. It helps retailers accept food stamps online with a 90-day integration process. Forage charges 2.9% plus $0.30 per transaction. Forage is led by Ofek Lavian who launched and scaled food stamp as a payment method at Instacart. At Instacart, it took him 9 months, a cross-functionnal team and long discussions with public authorities to launch it. - Forbes, Turner Novak

Wednesday, Aug. 3rd: Helium is not performing as expected. It’s a flagship web3 project. It uses IoT to build a decentralized P2P wireless telecommunications network. It only makes $6.5k in monthly revenues and hotspots are not a great investment for end users. Moreover, Helium claims they are working with customers it does not have like Salesforce and Lime. - CoinTelegraph, Liron Shapira, Amir Harleem, The Verge, Stacey on IoT, Mashable

“On average, [end users] spent $400-800 to buy a hotspot. They were expecting $100/month, enough to recoup their costs and enjoy passive income. Then their earnings dropped to only $20/month.”

Helium is building a Low Power Wide Aera Networking. “The best applications don’t get built because there’s no network to use, and there’s no network because there are no applications.”

“The Helium network is designed for hundreds of millions of devices to send small bits of data really cheaply. Which means that we won’t see amazing revenue from Nova Labs until we start seeing hundreds of millions of devices on the network. […] The goal with Helium, LoRaWAN is to solve the chicken and egg problem by creating the economic system for individuals to build the network. With close to 1m nodes and 10% of the worlds population covered, this seems to have worked pretty well. So why is there only $6,500 worth of data being paid for? Unlike cellular networks there aren’t millions of existing devices that can switch to Helium. The best applications haven’t been built yet, and it takes months or years to build them.”

Thursday, Aug. 4th: I listened to a Colossus’ podcast episode on LVMH. - Colossus 1, Colossus 2

Bernard Arnault was an outsider to the luxury industry and to the French business establishment. He has a unique combination of an engineering and artistic mindset.

LVMH’s brands are timeless with certain brands being 150+ year-old (e.g. Moët & Chandon created in 1743, Hennessy in 1765, and Louis Vuitton in 1854).

Bernard Arnault is known for epic acquisitions attempts. He tried to acquire Gucci in 2001 (Pinault Printemps La Redoute made a counter offer while having the support of historical shareholders) and Hermès in 2010.

LVMH has a decentralised structure. It has 75 Maisons (brands) that are independently run in 6 different categories (fashion & leather goods, wines & spirits, perfumes & cosmetics, watches & jewelry, selective retailing, others businesses around art, entertainment or culture). “LVMH's vocation is to ensure the development of each of its Maisons while respecting their identity and autonomy, providing all the resources they need to design, produce, and market products and services defined by excellence and the highest quality.”

LVMH acquired many luxury brands with the belief that it was the best owner for these assets that were mostly family owned businesses.

Louis Vuitton is LVMH’s most important brand generating 30% of the group’s revenues and 50% of the group’s operating margin.

LVMH has managed to reach scale while being in the luxury sector because it has a diversified portfolio of brands that express themselves into multiple product categories.

The family has almost a 50% stake in LVMH and more than 60% of voting rights.

Chinese consumers are increasingly spending on luxury locally compared to abroad. LVMH built an omni-channel retail network to properly serve Chinese consumers in their country.

There is a paradox for luxury groups which want to grow while preserving scarcity as to not to impact their brand equity. After a certain scale, you will no longer be perceived as a luxury brand - at least by a portion of your historical customer base.

The whole retail experience has become increasingly important in luxury, in the past the quality of the product was the main purchasing factor. LVMH has the financial power and the in-house expertise to develop an offline retail network for the brands it acquires.

Post acquisition of Tiffany, LVMH changed the management team, modernized the brand to make it more appealing to younger audiences, made the brand more luxurious, launched design jewelry's products (vs. precious stones which was the core business of Tiffany) and doubled down on its retail network.

In the luxury sector, product performance and customer feedback don’t matter. You want your designers to have unlimited creativity and you advertise prestige - not the product.

LVMH has the following challenges for the coming years: growth paradox for luxury brands, complexity of the business, Bernard Arnault’s succession, poor ability to sell its under performing brands, demand shits in China.

LVMH’s culture has the following attributes:

Being long-term optimistic and short-term pessimistic. Being conservative in how you manage the day to day but also seizing the long term opportunities in your markets.

Make decisions to win the long term and preserve brand equity even if it’s not optimal in the short term (not over advertise, being vertically integrated, no offshoring).

Combining high decentralization with high degree of accountability and attention to details.

Luxury products vs. premium products (comparing product performances) vs. high end fashion (making as much as volumes as possible).

Friday, Aug. 5th: Shopify made a $100m strategic investment into Klaviyo. Shopify has a proprietary email marketing product but extremely limited in features compared to Klaviyo which has become a must have for most of Shopify’s merchants. Klaviyo started as an email marketing product but it has since then evolved into a full marketing automation platform adding a CRM and SMS marketing. Klaviyo and Shopify also announced that they were strengthening their partnership: (i) Shopify will start recommending Klaviyo to its Shopify Plus merchants and (ii) Klaviyo will have an early access to Shopify’s in-development features. - Klaviyo, Techcrunch

Saturday, Aug. 6th: I read a paper from The Walrus on the consequences of the rising cashless society in Canada. - The Walrus

In a 2021 survey from Payments Canada, c.40% of Canadians said that they will no longer use cash in the aftermath of Covid. By 2030, cash is forecasted to decline by 70% in Canada.

A cashless society is problematic for individuals who are underbanked (i.e. who cannot access a bank account and/or a credit line, representing 15% of Canadians) who heavily rely on cash and cheques.

Banks are also closing their retail branches. As a result, it’s starting to be extremely painful and expensive to cash a cheque (e.g. $2.99 flat fee and 3% variable fee in money marts).

The paper highlights several solutions to give access to digital financial services to underbanked: (i) rely on Canada Post to provide banking services like in France, (ii) use prepaid cards on which governments can send money to people, (iii) provide them with low cost laptops and/or phones.

Sunday, Aug. 7th: SoftBank published its Q2-22 results. - Softbank, Oscar Williams, FT, Techcrunch

Vision Fund 1 and Vision Fund 2 are both poorly performing. Vision Fund 1 is valued at a 1.24x multiple and Vision Fund 2 at a 0.80x multiple.

It’s still slowing down its investment pace. It only deployed $600m in Q2-22 compared to $2.4bn in Q1-22 and $9.6bn in Q1-21.

Son is pessimistic of the coming months for tech startups. He claimed that many founders of private companies refuse to review their valuation expectations to adjust to what happened in public markets. Without this correction, it’s impossible to make new investments. “Unicorn companies’ leaders still believe in their valuations and they wouldn’t accept that they may have to see their valuations go lower than they think. So until the multiple of listed companies is lower than those of unlisted companies, we should wait.”

Monday, Aug. 8th: Andrew Chen (GP at a16z gaming, ex. growth at Uber) wrote on how to design a referral program. - Andrew Chen 1, Andrew Chen 2

It’s a marketing channel which gives your CAC to your users instead of Google and Facebook and which accelerates natural word of mouth and/or network effects.

Referral programs work well on product that are already spreading via word of mouth. Referrals will drive word of mouth forward by providing an economic incentive for people to talk even more about your product.

You should answer the following questions while building a referral program: (i) ask (when do you ask to refer? what is the message to refer?), (ii) target (all users or just a subset?), (iii) incentive (what are the incentives for the inviters and the receivers? do you give money away or intrinsic rewards like points or credits in your product?) , (iv) payback (”what is the success criteria for the program? how do you think about cannibalisation?”)

“Your referral program should target new users to refer their friends — this means prompting users during their initial onboarding flows, and adding emails as part of the onboarding, among other surface areas”

When measuring the payback of a referral program, (i) you should compare its efficiency with other paid marketing channels (e.g. Facebook, Google, TikTok) and (ii) using A/B testing to measure the cannibalization risk (i.e. users who would have invited their friends on the app in any case).

Tuesday, Aug. 9th: Not Boring published a deep-dive on Modern Treasury. - Not Boring

It’s an horizontal software infrastructure for any company moving money via bank transfers.

Modern Treasury partners with banks and builds an API integrated into their global banking system to make their bank transfers much more efficient both for them and their customers.

“Since more and more payments start with software, we believe software should not just initiate, but also monitor and reconcile this payment activity automatically. Modern Treasury enables its clients to marry bank statements with the company’s business logic to provide an enriched history of the company’s financial transactions.”

“It gives companies one API into banks to send wires, ACH, and real-time payments, automatically reconciles payments, and lets companies do continuous accounting instead of letting it all pile up until month end.”

Companies connect all their bank accounts via APIs in a single place. They can build payment workflows to send money directly from their bank accounts without relying on more expensive payment methods. Modern Treasury will automatically reconcile payments (matching bank transactions with specific payments) and push reconciled payments to your accounting ledger.

In the long term, “Modern Treasury could build its own “closed-loop” network through which businesses could move money to each other, from bank account to bank account, in real-time. It could reconcile the transactions instantly. It could facilitate real-time payments. It could keep the books up-to-date automatically.”

Wednesday, Aug. 10th: Finix raised $30m from investors like The General Partnership, Bain Capital, Insight, Lightspeed and Amex. It’s a payment facilitator helping SaaS, marketplaces and commerce companies to build modern payment experiences by becoming a payment facilitator themselves. As a result, Finix’s customers can build a payment experience that is much more integrated into their product while making additional revenues by processing payments. - Techcrunch

Thursday, Aug. 11th: The Financial Times wrote about the silent crash in the VC world. - FT

The venture private market is still in denial. Only a few companies who had to raise to avoid running out of cash adapted to the new reality by taking a deep cut to their valuation (e.g. Klarna). In the coming quarters, many companies will follow suit.

Many unconventional investors (hedge funds, PE firms, sovereign wealth funds, corporate VCs) poured massive capital in private startups in 2020 and 2021. These investors are gone.

“Investment discipline was loosened, with VCs spreading their bets widely across entire sectors rather than trying to single out the small number of big winners that had traditionally provided the lion’s share of the industry’s profits.”

Several sectors might be more impacted: (i) quick commerce, (ii) consumer fintechs and (iii) crypto startups.

“All the pretenders and the speculators will get wiped out. We’ll have the believers and the builders.” - Erich Vishria (GP at Benchmark)

Friday, Aug. 12th: Boulevard raised a $70m series C led by Point72 with the participation of Index, Troba Capital and Box. It’s a vertical SaaS for beauty professionals (salons, spas, barbershops, nail salons, massage therapy). It’s an all-in-one platform including booking, POS & payments, scheduling, CRM, loyalty, reporting and marketing. It grew ARR by 188% YoY. It works with 2k salons and 25k beauty professionals. It will use the funding to grow the R&D team and explore new verticals. - Techcrunch, Dot

Saturday, Aug. 13th: AppLovin made an unsolicited offer to merge with Unity in a deal that would value Unity at $20bn. Unity would have 55% of the combined entity and Unity’CEO would become CEO of the new entity. A pre-requisite for the transaction would be that Unity terminate its acquisition tentative of AppLovin’s competitor IronSource. The mobile gaming market has been impacted by several factors in the past few months: (i) lower consumer spendings, (ii) tech public stock meltdown, (iii) advertising market by Apple’s change around IDFA, making it much harder to make performant ads. AppLovin and Unity are complementary businesses: Unity and AppLovin have large ad networks, AppLovin has an ad mediation business following the acquisition of MoPub and has a mobile game publishing arm to dog-food its advertising engine. - WSJ, Mobile Dev Memo, Stratechery

Sunday, Aug. 14th: I read a post from Jeremy Solomon on BNPL. - Fintech Fundamentals

There are 3 main categories of BNPL products: (i) Pay-in-4 ($100-400 purchases split in 4 payments over 6 weeks with the 1st payment done at purchase), (ii) 0% installment loans (for larger purchases, 3-24 months) and (iii) interest bearing installment loans (same interest as a credit card, no possibility to revolve like credit cards).

Pay-in-4:

“Pay-in-4 is designed as a payments product and not legally considered a lending product.”

“Platforms make money by negotiating a discount, similar to interchange, with the merchant. Typical pricing is a 4% discount, or ~1% more than credit card interchange fees that merchants pay with every swipe. Merchants value the offering because the additional 1% cost produces meaningful funnel conversion lift, making the additional cost inconsequential.”

“Pay-in-4 has limited to no credit underwriting component. No credit bureau pull, no cash-flow-based underwriting, etc. The platforms rely on a) success of the initial payment, indicating availability of funds; b) previous payment history; and c) threats of banning a customer from the service.”

It’s hard to make a lot of money on Pay-in-4. You charge 4% to the merchant but you have to pay 2.5% on interchange on credit cards. You have a 1.5% gross margin to cover losses, fraud, servicing and capital funding. Late fees help to improve unit economics but deteriorate the value proposition if too expensive.

0% instalment loans:

It’s a loan. It must be offered through a bank origination partnership and more traditional credit risk is performed.

It can be a lucrative business line and you can charge merchants much higher fees than 4-5%.

Interest bearing loans:

“The merchant pays a merchant discount rate similar to interchange and the borrower is charged an explicit interest rate by the lender.”

“Borrowers utilizing Interest Bearing Loans are likely using the BNPL offering as additional capacity to credit cards.”

BNPL have specific edges when they underwrite financial products compared to incumbent lenders: (i) access to differentiated data to underwrite (merchant level and SKU level underwriting), (ii) only focused on ability to repay over the term (vs. managing revolving for a credit card), (iii) frictionless experience (learning as much as possible about the borrower without being intrusive).

“Along with captive SMB financing platforms like Square Capital and Stripe Capital, BNPL stands out as a truly innovative leap forward in providing efficient credit to an underserved population.” For instance, Affirm has been impressive at reducing its credit losses cohort after cohort.

Monday, Aug. 15th: Agave Games raised a $7m round led by Balderton with the participation of Felix and 500 Global. It’s a puzzle mobile gaming studio founded in 2021 and based in Turkey. It will launch its first game in 2023 targeting top gaming markets like the US, the UK, Canada and Japan. It will monetize combining both advertising and In-App-Purchases - Sifted, Business Insider, Tech.eu

Tuesday, Aug. 16th: Gorgias raised a $30m series C at a $710m valuation (vs. $305m valuation at series B) led by Transpose Platform and Shopify. It’s a verticalised customer support platform for e-commerce merchants. It works with 10k customers selling on Shopify, Big Commerce and Adobe Commerce. It will use the funding to improve its product with two interesting features: (i) an automation add-on to answer automatically certain customers inquiries and (ii) a revenue add-on to identify customers with a high likelihood to be upsold. It’s noteworthy that in a couple of weeks, Shopify invested in both Klaviyo and Gorgias which are must-have tools in its ecosystem. - Techcrunch, Gorgias

Wednesday, Aug. 17th: I listened to a Colossus’ podcast episode with Henrique Dubugras who is Brex’s founder and CEO. - Colossus

Brex is an all-in-one finance platform for businesses integrating services usually provided by banks (credit cards, business accounts, lending) but also other financial services (expense management, bill pay, payroll).

The initial insight that led to the creation of Brex what that Brex’s founders did not have a credit score and as a result they could not get a credit card with high spending limits for their previous business. Brex started by targeting startups that were underserved by incumbents (”credit cards for startups” as clear marketing message). It adopted a different credit scoring technology based on a dynamic model re-underwriting customers everyday and not a static model based on a credit score.

Brex internalised many blocks in the infrastructure financial stack (KYC, AML, authorization system, fraud system, core ledger recording transactions, etc.) and offers its own business accounts to avoid dependencies to third parties relying on a legacy infrastructure.

In the US, credit cards offered rewards to users via points. If you’re too hard in regulating interchange, finance providers won’t have sufficient leeway to partly redistribute interchange fees to end consumers/businesses via points/cash back.

Brex moved from one product serving one segment (”credit card for startups”) to a platform with 4 products (expense management, AR/AP automated platform, banking solution and card processing platform) serving multiple segments. Having an all-in-one finance platform unlocks unique features like automating reporting or offering tailor-made & powerful lending products (e.g. instant payouts because we own the accounts).

Brex raised $57m pre-launch ($7m round led by Ribbit and $50m round led by YC Continuity). It spent one year to build the product and to have a partnership with a bank to issue cards.

Saturday, Aug. 18th: Fractal wrote about verticalised marketplaces. It argues that vertical SaaS are uniquely positioned to launch verticalised marketplaces because they have the following comparative advantages compared to horizontal solutions: (i) no cold-start problem because you can transform the customers of your SaaS product into the buyers of your marketplace, (ii) industry expertise needed to design workflows specific to the needs of the vertical (e.g. Flexport “is fundamentally a comprehensive system of record for shipping and logistics companies that has a marketplace component for booking space on carriers”). - Fractal

Sunday, Aug. 19th: Sapphire published a deep-dive on modern finance tooling. - Sapphire

Finance teams are expanding their scope of responsibilities beyond finance to give business insights to other teams (e.g. compute key business metrics like net dollar retention or helping the sales team to track its sales funnel).

Finance teams need modern tooling with the following characteristics: (i) integrated to your tool-stack, (ii) collaborative, (iii) automated and (iv) workflow-centric (e.g. forecast & budgeting, execution & control, outcomes & measurements).

Modern finance tools for mid-sized & enterprise companies will leverage the data-warehouse as single source of truth instead of leveraging multiple spreadsheets across the organisation.

Monday, Aug. 20th: Ben Evans wrote about Apple’s advertising business. - Ben Evans

Apple’s app store commissions were close to $15bn in 2020 with 90% coming from games (and esp. in app purchases within games). Many app developers are challenging Apple’s app store 30% commission starting with Epic and Spotify.

Apple is building a personalised and private ad model in which mobile app publishers and developers don’t know the targeting data.

“Apple’s business model is to sell hardware to around a billion people, bringing in about $200 per user at a 30% gross margin in 2020, then to give away, or sell, a lot of other services on top [music, apps including games, payments and perhaps advertising], both for incremental revenue (about $50 per user at 65% gross margin) and to drive retention.”

Tuesday, Aug. 21st: The Economist wrote about returns in e-commerce. In the US, 21% of online orders were returned in 2021 ($218bn in value, up to 40% in certain categories like clothing & shoes, vs. 18% in 2020). Customers are expecting free returns but free returns are extremely expensive for e-commerce merchants (retailers pay for the goods to be sent back, it’s complex to open a returned parcel and decide what to do with it, only 5% of returned goods are immediately resold). On average, retailers recoup only 1/3 of the value of returned items. To solve this issue, several solutions are appearing: (i) charging a small return fee (e.g. Zara, Uniqlo), (ii) develop a second hand business line (e.g. Amazon), (iii) work with logistic providers specialised in returns (e.g. Happy Returns) or (iv) pre-empt some returns using AR and VR. - The Economist

Wednesday, Aug. 22nd: The carbon dioxyde removal (CDR) sector needs to be regulated or at least needs to elaborate a code of conduct. - Protocol

“The really uncharted territory is what CDR means for environmental and social justice.”

“Scientists worry that nascent technologies like direct air capture are being deployed without sufficient oversight or forethought about potential unintended negative consequences. The issues CDR will need to confront are manifold. From noise pollution tied to direct air capture facilities to the ecological impacts of land- and ocean-based carbon removal techniques, the industry has a lot to reckon with as CDR becomes more widely tested and deployed at scale.”

“Climate researchers point to lessons learned from the carbon offset market as a warning sign of what could happen with carbon removal if proper care isn’t taken to put guardrails around a market free-for-all.”

“In any carbon removal project, it’s critical that frontline communities are consulted and included. That means both people living adjacent to project sites as well as the workers doing the removal.”

“Beyond community impact, the other risk with carbon removal is that its existence allows corporations, including fossil fuel companies that back these projects, to continue polluting the atmosphere.”

Tuesday, Aug. 23rd: Ramp launched a Flex feature to enable flexible financing for its Bill product, an Accounts Payable automation platform. Bill was launched in Oct. 21 and reached $1bn in annualised volumes in less than 6 months. With flexible financing, the vendor is paid right away and you have the flexibility to send the money in 30, 60 or 90 days in exchange of a fee. It’s a frictionless experience fully integrated into Ramp’s platform. It also preserves the flexibility for customers who can still pay their bills in multiple payment methods (cards, ACH, checks). - Techcrunch, Ramp Ramp

Wednesday, Aug. 24th: I read Lux’s Q2-2022 Quarterly Report. - Lux

“While others may say their pace is slowing, our pace pulses to a steady beat: there is always something we can be doing, an opportunity to seize, a risk to reduce, an internal process to improve.”

“If 2022 was the year of Entropic Apex, then we are dubbing next year “Twenty Twenty-RE”––as in: REdiscovering the meaning of price, REthinking inflation, REconvening at work and REwearing suits, REconstituting the finance of innovation, REinforcing our strengths, REviewing our theme of Extensionalism, REinvesting in the frontier and ‘Matter that Matters’, and finally, REcapturing human ingenuity.”

“Prices often tell more about the condition of the pricer (hope and euphoria or despair and fear) than the condition of the asset.”

“In private markets (which lag public markets), price discovery for some companies is intentionally undesired and unsought (as they suspect they won’t like what they learn and don’t wish to know yet) and for others confidently sought as they will be in high demand and successfully raise at higher valuations.”

“Remote workers and cultures that bias toward them will––especially in a downturn––be disadvantaged.”

“We see bigger than ever investment gains to be made in making gains in fields from defense, biotech and space to automation, industrial production, and novel network infrastructure to other interdisciplinary domains that advance (as we like to say) matter that matters.”

“We are only ever as good as our last investment, last decision, last interaction and impression made. We must methodically REinforce ourselves, and we see gains from deliberate institutional design over many years at Lux to compound competitive advantages.”

Thursday, Aug. 25th: Nathan Baschez wrote about the risk for BeReal to be disrupted by Meta. - Divinations

Bereal recently raised a series B led by DST at a $600m valuation and has over 8m DAUs.

Bereal has the following primitive. Every day, one notification is sent to all users at a random time. Users have 2 minutes to post a photo of what they’re doing. Bereal takes a photo using both your front and back camera. You can access and react to the photos of your friends only if you posted your own photo.

Bereal changes the nature of the pressure that you have on social media. Instead of taking the best photo as you can, you have to take the best photo as you can within two minutes. This constraint creates a new form of creativity previously unseen on social media.

Nathan says that Bereal is easy to copy for Meta because it’s only a content format innovation (like Stories) and not a novel network structure (like TikTok).

Meta is already working on testing Bereal’s content format into its app. The main goal for Meta is less to conquer Bereal’s users and is more to avoid its user-base to leave Instagram for a new social network (like what happened with Snap and TikTok).

“As a standalone business I have an incredibly hard time seeing BeReal turn into something real. Not only do they have to continue attracting new users exponentially, then they have to build an ad business, is much harder than it seems.”

Friday, Aug. 26th: Brian Potter wrote about the lack of economies of scale in the construction industry. - Construction Physics

You have economies of scale when the unit cost of each unit produced falls as the volume of output units increases. It’s the case in many sectors like manufacturing, transportation or agriculture.

In construction, economies of scale don’t exist. (i) At the level of individual buildings, “a large building is only marginally less expensive on a per-square foot basis than a small building is.” (ii) The cost per square foot is not significantly lower when you compare an apartment building and a single family house. (iii) Construction is a sector that is extremely fragmented. “By market cap, the largest US construction company is smaller than the 15th largest mining company, and the 20th largest car company, despite the fact that the construction industry is larger than the car industry and the mining industry combined.”

Saturday, Aug. 27th: Bloomberg wrote about Softbank’s broken business model. - Bloomberg

Softbank’s initial strategy was to write large checks to enable his portfolio companies to operate at a loss for several years to have the time to establish market dominance and in a second stage to generate long term profits. It wanted to dominate nascent industries by investing massive capital into potential winners (e.g. $5.5bn in Didi, $4.4bn in WeWork, $7.7bn in Uber, $1.5bn in Olo).

Softbank is well known for offering 2-3x the amount required by founders and for threatening them to invest into a competitor if they did not take their money.

Softbank brought the blitzscaling philosophy (i.e. win a market whatever the cost because most internet markets end up being monopolised by a single player) to another level. According to Bloomberg, it’s a strategy with 2 shortcomings: (i) it can harm consumers and (ii) it works with tech companies with sound unit economics.

Softbank contributed to distort the venture capital market. It forced venture funds to respond by investing larger checks at inflated valuations.

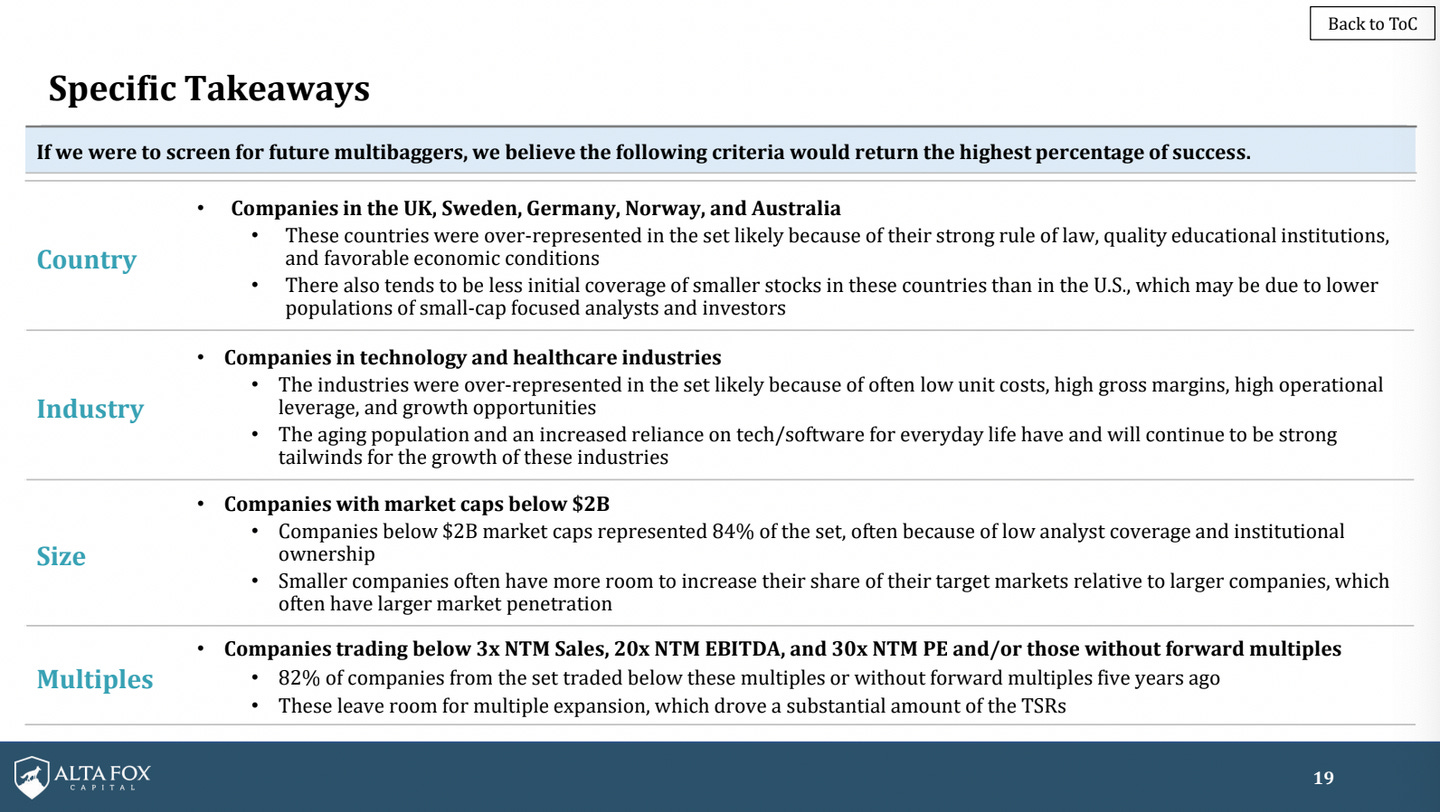

Sunday, Aug. 28th: I skimmed over a 400+ slide presentation from Alta Fox trying to understand the factors behind the best performing stocks in the past 5 years. - Alta Fox

These stocks have the following characteristics: (i) they have one or several moats, (ii) they are financially healthy, (iii) they’re good at acquiring & integrating companies, (iv) they tend to have an initial market cap. below $2bn, (v) they tend to be either in tech or in healthcare.

Monday, Aug. 29th: The Wall Street Journal wrote about the “product drop” phenomenon in retail and e-commerce. A product drop will have the following characteristics: (i) time-limited events, (ii) quantity limited products, (iii) exclusive products, (iv) a specific process to get the product (e.g. waiting in line at a physical store, registering for a lottery online). With its mechanics, drops make shopping appealing again in a world in which we can get whatever we want with a single click on Amazon. Brands are also using drops to strengthen their brand image (e.g. Chipotle dropping a candle or Nike dropping exclusive sneakers are both doing drops to reinforce their core business which is more mass market). - WSJ

Tuesday, Aug. 30th: I listened to a Colossus’ podcast episode on Block which is the parent company behind Square, Cash App and Afterpay. - Colossus

Block started in 2009 with Square as a card reader to help micro and small businesses accept card payments. It’s now a platform combining software, hardware and financial services with 40+ products severing all customer sizes.

It has 2 main ecosystems: (i) Square which is merchant facing (payment processing, integrated payment software, loans, Square card, instant transfer) and (ii) Cash App which is consumer facing (peer to peer transfer, BNPL, BTC and stock trading).

The initial insight that led to the creation of Square in 2009 was that many micro and small businesses were excluded from the financial system because they could not accept cards payments. At the time, you needed to rely on traditional financial services with a long process (3-4 weeks, paper based) and a low approval rate (only 40%).

Square has specific capabilities like (i) integrating hardware and software seamlessly, (ii) leveraging data to underwrite merchants (with a different paradigm in which you trust first and verify second instead of verifying fist and trusting second), (iii) bundling financial services with hardware/software to solve business workflows, (iv) having a deep customer empathy to open new product opportunities.

The initial insight that led to the creation of CashApp in 2013 was that there was an opportunity to serve the 60m people underbanked in the US with a value proposition similar to Venmo which was getting traction with its peer-to-peer payment method.

Wednesday, Aug. 31th: Francis at Investi shared its framework to invest in public software companies. - Investi

They look at both execution (high growth, high gross margin & positive operating margin, sales efficiency, great retention) and moats (high switching costs, must-have, lasting differentiation, platform ecosystem or network effects).

“In an industry that sees an extraordinary number of start-ups, very few go on to become giants. Of the nearly 3,000 companies that we studied, only 28% reached $100m in annual revenues; 3% went on to log $1bn in annual sales, and just 0.6% —17 companies in total—grew beyond $4bn.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋