📖 Venture Chronicles - April 2026

Overlooked #217

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of April.

I curated updates and insights around three themes:

Vertical Software

General Venture Capital

Entropy - other news and personal topics of interest

Vertical Software

Avoca raised $125m+ across three rounds from investors like KP, Meritech and General Catalyst and YC at a last valuation above $1bn. Avoca’s voice AI agents handle missed calls for home services (plumbers, roofers, and HVAC) contractors capturing the leads these businesses typically lose when technicians are in the field. It has an 8-figure ARR and is on track to reach $1bn in booked jobs on its platform for 2026 - Forbes, PR Newswire

“While most AI solutions today have focused on optimizing desk work and efficiency–email, docs, decks–the front office of the $1T+ services economy has lacked solutions tailored to specific industry needs. Avoca is transforming this narrative, powering 24/7 call handling, scheduling, custom marketing campaigns, and customer follow-ups, while giving service businesses the AI tools that match the quality of work they deliver.”

Cents raised a $140m series C led by Sumeru. It’s a vertical SaaS and payments platform for the laundry and garment care industry. It provides POS, payments processing, online ordering, marketing tools, and AI-powered software to laundromats and dry cleaners. It serves thousands of locations and processes approximately $1B in annual payments. Cents will use the funding for AI-powered product suite expansion, customer support scaling, new partnerships, and broader product development across the garment care vertical. - Tech Startups, Fintech Global

Crosby raised a $60m series B co-led by Lux and Index at a $400m valuation. It’s a hybrid AI-powered law firm combining AI with human lawyers to drastically speed up contract review processes. - TAMradar, Law.com

Most legal AI startups sell tools to law firms. Crosby is the law firm: vertically integrated, AI-native, eating the margin of law firms instead of enabling it.

“Crosby is a vertically integrated AI-native law firm, not merely an AI tool.”

“America’s top 100 law firms made a combined $69 billion in profit last year.”

Nick and Luke interviewed Alex Niehenke who is Partner at Scale. - Verticals Podcast

AI services has a pricing-commoditization problem. If you can interchange vendors, pricing becomes the determinant factor.

“Systems of love” beat systems of record. Founders should look for markets where incumbents are miserable and have annually raised prices (e.g. law, insurance brokers). These are ripe for AI-native disruption because customers will actively cheer for you.

Most incumbents can’t acquire their way out of the AI revolution. PE-owned incumbents are over-levered, public incumbents have crashed stocks and don’t want dilutive acquisitions. The only people who can make the bold bet are founder-CEOs who own 20–30% of the company.

“Market size almost never hits the ceiling. The great entrepreneurs are ferocious about adding more revenue streams.”

“There are only two paths: crazy growth, or be very disciplined and efficient. In my mind it’s a desert wasteland in the middle.”

General Venture

Lenny Rachitsky interviewed Keith Rabois who is managing director at Khosla. - Lenny Rachitsky

The team you build is the company you build. It’s the single most important thing when creating a startup. If you have the right people, everything else is easy.

Be ruthless at references. Tony Xu at DoorDash does 20 reference checks on every senior hire.

Barrels vs. ammunitions. Only a small number of people in any company can take an idea from inception to success. Hiring more people without more barrels just increases coordination tax.

Build on undiscovered talent. You can’t compete with infinite-money incumbents for people everyone wants. Find the people the black-box hiring process misses which are often younger, with fewer data points and therefore harder to “process” homogeneously.

Relentless application of force. The better the company is doing, the harder the CEO should push. Complacency kicks in with success, and great people get unhappy when they’re skating.

The PM role as we know it makes less sense. Year-long roadmaps are incoherent when foundation-model capabilities shift monthly. The skill required for PM is closer to being a CEO: “What are we building and why?”

Design and code are merging. At Shopify, for two years, PMs have been banned from presenting roadmaps in PowerPoint. Every product presentation must be a working demo.

Founder-driven investing. Keith’s rule: does this founder have a non-zero chance of changing an industry? If yes at seed/Series A, invest. Don’t ask other questions.

Three signs of a great early-stage company: (1) operating tempo, (2) critical density of talent that keeps improving, (3) hiring philosophy that promotes from within rather than recruiting senior external hires.

Value creation vs. value preservation. Hire senior experienced people only when you need value preservation. Value creation comes from internal promotion and undiscovered talent.

Harry interviewed Aaron Levie who is cofounder & CEO at Box. - 20VC

The new job: “agent operator.” 500k to 1m jobs will emerge for semi-technical people who sit inside marketing/legal/ops/R&D teams and know MCPs, CLIs, skills, and agents.md files. Their job is to redesign workflows for agents, not for people.

Token budgets are moving out of IT spend and into OpEx. That is the multi-trillion-dollar unlock. Software has historically been capped by corporate IT budgets; AI agents can now tap 5% of a line-of-business OpEx budget. Enterprise tech spend goes from ~10–12% of revenue toward ~20%. “The budget of tokens will have to move out of IT spend and into regular OpEx spend.”

AI diffusion will take longer than the Valley thinks. Aaron lived through the cloud cycle. It took 20 years and got way bigger than anyone modeled. The same will be true for AI. Regulated industries, compliance teams, and change management make the 18-month bubble thesis wrong.

Software is becoming headless. In the last year, tool-calling accuracy and agentic search have accelerated to the point where every software platform must be API-first. Two years ago, agents picked the wrong document inside Box. Today they don’t.

This is a sector-rotation moment, not a software bubble. Compute/infra is where returns are concentrated. Some software names are trading at aggressive lows (3× free cash flow) that don’t reflect terminal value. The pendulum will swing back.

“We’re going to do ourselves a disservice if we scare people out of engineering, out of radiology, out of healthcare because they think all these jobs will be eliminated with AI. That does a disservice to the next generation and to society. We don’t yet know any way to use AI in a capacity other than augmenting our work where we still eventually have to review the output. We haven’t removed humans from the loop — we’ve just changed where they enter it.”

“There are going to be more lawyers in the next 5 years than today. We’ve made it easy to generate legal content. But it hasn’t gotten any easier to get any of it approved by a court system or file a patent.”

“We treat software too much as one monolithic industry. Better to have a 2×2: how much business logic, how much human-agent collaboration. The moment you have human-agent collaboration, you need something the user can pop into to experience the agent’s work — that doesn’t go away.”

Harry interviewed Anjney Midha who is founder at AMP. - 20VC

AMP isn’t a traditional VC. It’s an “independent system operator for compute”. It pools GPUs across hyperscalers, neoclouds, and its own build-out, then allocates neutrally to frontier labs.

Anj has three activities with AMP: (1) AMP Capital which is a c.$1.3bn Fund I closed Oct 2025 providing equity checks bundled with compute allocation, (2) AMP Grid which is a gigawatt-scale compute build (c.1.3 GW secured that will bring $40bn of cloud spend over 4 years with a 20/80 equity/debt split and (3) an incubation with Periodic Labs ($300m seed raised in Sept 2025).

Sovereign data has become a new moat and the thesis behind Anj’s investment in Mistral. The US Cloud Act means any workload on US-managed infrastructure is accessible to the US government. European defense, logistics, and mission-critical workloads cannot run on AWS/GCP/Azure.

Anthropic’s early days were brutal. 21 of 22 VCs passed on the seed round. Many didn’t even know what GPT-3 was. The original raise target was $500m, reanchored to $100m. Amazon ultimately “got it” because they saw the OpenAI/Azure parallel.

“Foundation model company” is a bad label. These are frontier systems companies. Anthropic was always going to build Claude Code. Mistral was always going to build Mistral Compute. The systems-code design is what matters, not one layer.

Mike Mignano interviewed Fred Wilson at USV. - USV

The biggest VC regrets are passing on price, not on the wrong company. If your gut says it’s the right team in the right market with the right product at the right time, find a way to say yes (e.g. buy secondary, take a smaller allocation), but don’t walk away over valuation.

Thesis-driven investing is iterative, not prophetic. USV’s thesis evolves: start with a rough hypothesis, make investments, learn, restate. The famous “applications differentiated by user experience and defensible by network effects” USV thesis was actually its second or third thesis, not the first.

VC firms can be largely automated with AI agents except for three things humans should still do. (1) High-level thesis development. (2) Building relationships with founders in those spaces. (3) Working with founders post-investment. Sourcing, diligence, term sheets, relationship management, event planning will all end up automated by agents.

Energy is the safest way to play AI. No matter who wins in AI, energy is a beneficiary. ~⅓ of USV’s recent activity is energy, indexed to AI without having to pick the winning model.

Founders today need to be incredible at selling and inspiring. Recruiting, fundraising, customer convincing, narrative-building.

“Startups have to play chess. They have to see three or four moves ahead.”

“Energy is a great way to play AI. Because if we know one thing, no matter who wins in AI, energy is a beneficiary.”

“Find great founders, build great relationships with them, and do everything you can to help them build great companies. That is pretty much everything you need to do to be great in this business.”

Tim Ferris interviewed solo-GP Elad Gil. - Tim Ferris

The compute bottleneck enforces parity among labs. No single lab can buy 10× more compute than the others, so OpenAI, Anthropic, Google, xAI all stay roughly close on capability for the next 24 months. When the constraint comes off, someone could break away.

The dot-com survival rate was 1 in 100. Plan accordingly. ~2,000 companies went public in the late-90s internet cycle. ~12–24 still matter today. Every cycle is like this — autos in Detroit, mobile, SaaS, crypto. AI will be no different. If you’re a founder, ask whether you’re in the surviving dozen or whether now is the value-maximizing moment to sell.

Every company has a 6–12 month value-maximizing window. Often the second derivative of growth (rate of acceleration) is your tell. If growth is plateauing, headwinds are coming, and the next 12–18 months is likely the best price you’ll ever get.

Durable AI advantage = base model leverage + product depth + workflow lock-in + data. Four lenses: (1) does your product get better when the underlying model improves? (2) how deep and broad is your product across a customer’s workflow? (3) is the AI embedded in change-managed workflows that are hard to rip out? (4) is there proprietary data being captured?

Live in the geographic cluster. 91% of all global AI private market cap sits in a 10-mile-by-10-mile area in the Bay Area. Defense tech is Southern California. Fintech is New York. The “you can do it from anywhere” advice is mostly false for breaking in. Go where the cluster is.

Power laws are unforgiving: 10 companies = 80% of two decades of returns. If you weren’t in those ten, you were a bad investor. Most regrets are not investing more aggressively, not investing wrong.

“There are moments in time where it’s very smart to be contrarian. And there are moments in time where being consensus is the smartest possible thing you can do. Right now we’re in a moment in time where being consensus is very right.”

John Collison at Stripe interviewed Mati Staniszewski who is cofounder & CEO at ElevenLabs.

ElevenLabs is at $450m ARR and added $100m ARR in Q1 and >50% enterprise revenue.

Two key innovations powered ElevenLabs’ edge: contextual prediction (understanding what comes before and after each sound) and open-ended encoding/decoding of voice characteristics (the model deduces accent, style, and emotion as emergent properties rather than using hard-coded parameters).

Counterintuitively, ElevenLabs prices newest models at cost or subsidized because they want max distribution of the frontier to build reputation and learn what’s possible.

Customers include Deutsche Telekom, T-Mobile, Revolut, Klarna, Meta, IBM. Growth pattern is classic land-and-expand: start small, usage-based commitments grow as trust builds, cross-department pollination (Deutsche Telekom went marketing → support → network-wide agent)

ElevenLabs is 470 people, structured around sub-10-person teams for every product, research, and go-to-market initiative.

Pat Grady, Sonya Huang and Konstantine Buhler shared their most recent learnings on AI. - Sequoia

AI is the first technology revolution that’s both software and services. Software TAM grew from $350bn to $650bn over 15 years of cloud. The new services TAM that AI can address is on the order of $10 trillion. Legal services in the US alone (one vertical, one geo) is a $400bn market, equal to all of cloud software.

Three discontinuous inflection points so far:

Nov 2022: ChatGPT moment. The world saw pre-training scale.

~2024 — o1: reasoning. A second scaling law emerges around inference-time compute.

2025–2026: Claude Code, Opus 4.5/4.7, long-horizon agents. Hard discontinuity. Sequoia’s view: this is functionally AGI from a commercial standpoint.

“The cars have arrived.” For years AI gave us faster horses (i.e. apps that made you 10–40% more productive). Now we’re getting cars: apps that make you 10–40× more productive and fundamentally change how work and organizations are structured.

AI applications builders should think about the MAD framework:

Moats. In a revolution of computation, capabilities change faster than customers do. Approach the value chain customer-back. Wrap yourself around the customer because what you build today might be irrelevant tomorrow.

Affordance. A design term: an object that doesn’t need to be explained. Foundation models are powerful but offer limited affordance to non-technical buyers. The opportunity is creating paths of least resistance for specific customers and specific problems.

Diffusion. Capability creation is far outpacing capability adoption. The gap between what foundation models can do and what enterprises actually use is your opportunity. Every day that gap widens, the opportunity grows.

Best product wins, but products change too fast. Wrap yourself around customers, because customers don’t change as fast as capabilities do. Customer obsession is more durable than product strength in this regime.

Affordance is the under-discussed lever. Claude Code is insanely powerful, but the average Fortune 500 employee can’t open a terminal. Application-layer founders win by creating products that don’t need to be explained.

The agent spectrum (using coding as the example):

2023: tab autocomplete (one AI assisting one human inline).

2024–25: agentic development (one human managing one or several agents).

2026: background / async agents, agents spawning sub-agents (current dominant paradigm by volume).

Frontier: “dark factories” in which human review removed entirely. Already in production in security.

Compressed timelines stack. Bret Taylor rebuilt Sierra over a weekend. Notion rewrote 8M lines of code in 6 weeks. “Whatever you can imagine building over the next 100 years, we think is now possible in 100 days.”

The FT interviewed Martin Casado at a16z. - FT

Where are we seeing some evidence of productivity gains? “The one that’s very obviously working is code. […] A single lawyer can now do more cases, the accuracy of healthcare will increase. We know that the call centre stuff is working. We know customer support is working. But then there’s a long tail of stuff that we’re not quite sure about.”

“There’s some disconnect between how productive [AI] makes us feel versus how productive they are.”

“The next phase is RL [reinforcement learning], where you start tackling specific problems that you have a reward signal for. We’re at that point right now.” “I think the question is less: can it do a particular vertical? I think the answer is yes in most cases. The question is: is it cost effective to do that?”

On LLMs, “you’ve got the fastest depreciating assets we’ve ever seen, and the fastest growth rate companies you’ve ever seen.”

“Nobody can predict the future, so you have to have enough exposure [to] any given path.”

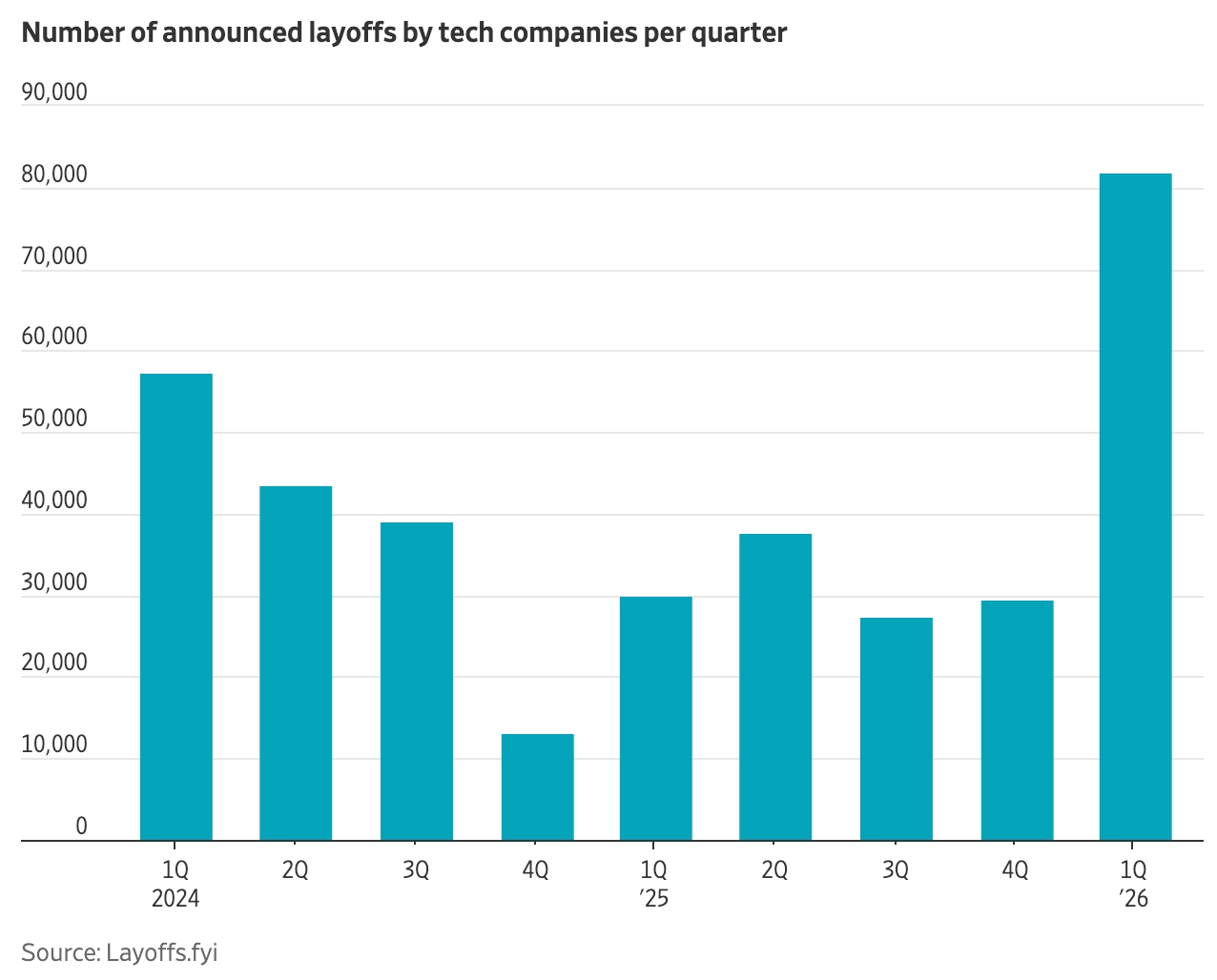

Tech giants are slashing thousands of jobs to fund AI capex. - WSJ

“Tech companies are rushing to trade their people for more chips.”

“Meta’s latest plans will cut about 8,000 people from its workforce. Microsoft, meanwhile, is trying to trim its own head count with a “voluntary retirement program,” available to about 7% of its U.S. employees.”

“Companies are straining to portray the cuts as evidence that they are confident in an AI future in which more workers will be replaced by machines.”

“Tech companies are in effect playing a game of chicken with each other on capital-spending plans. They are shelling out as much as they can—more than their rivals, they hope—on AI chips and data centers that could put them in the lead in a race they feel they can’t afford to lose.”

“The median annual revenue per employee among tech companies on the S&P 500 is about $669,000, which is 14% higher than the median for the entire index, according to data compiled by S&P Global Market Intelligence.”

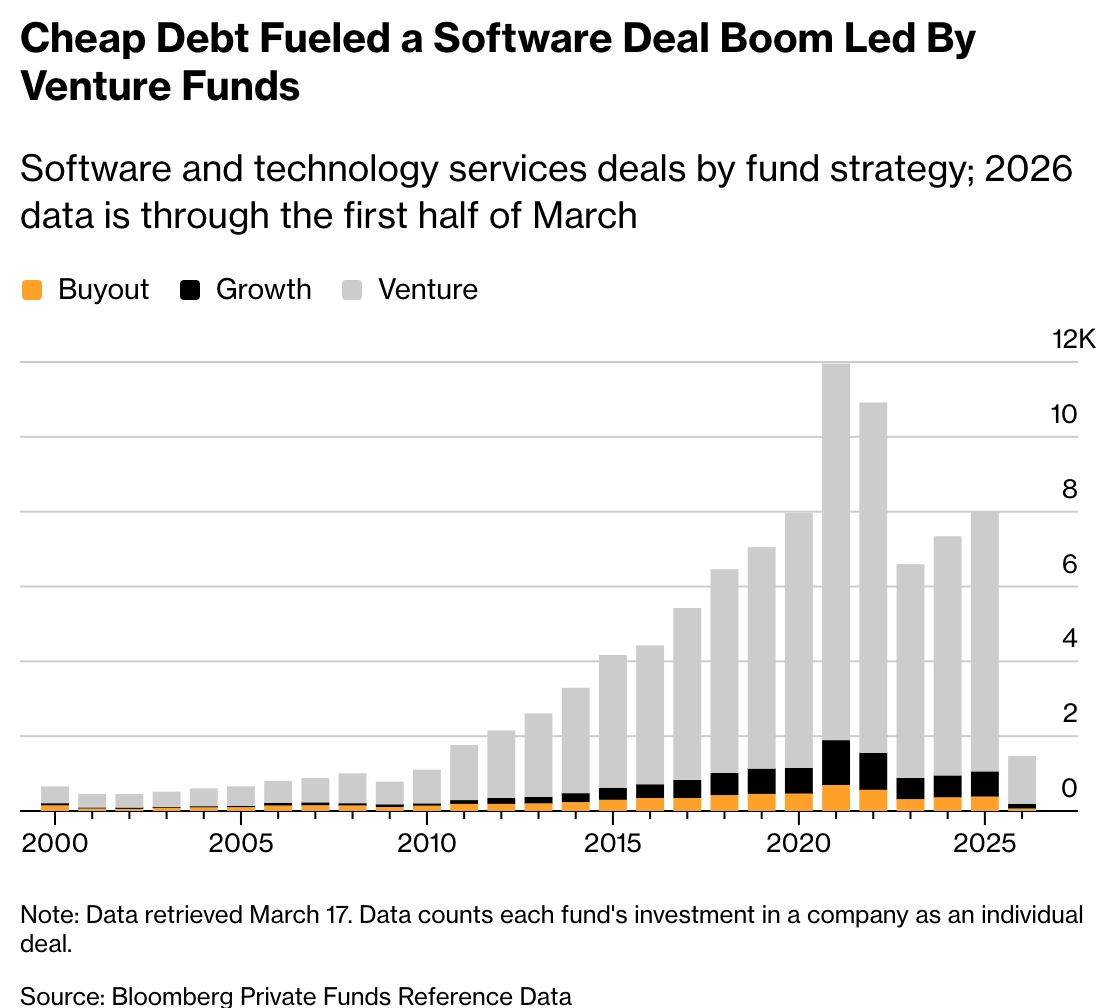

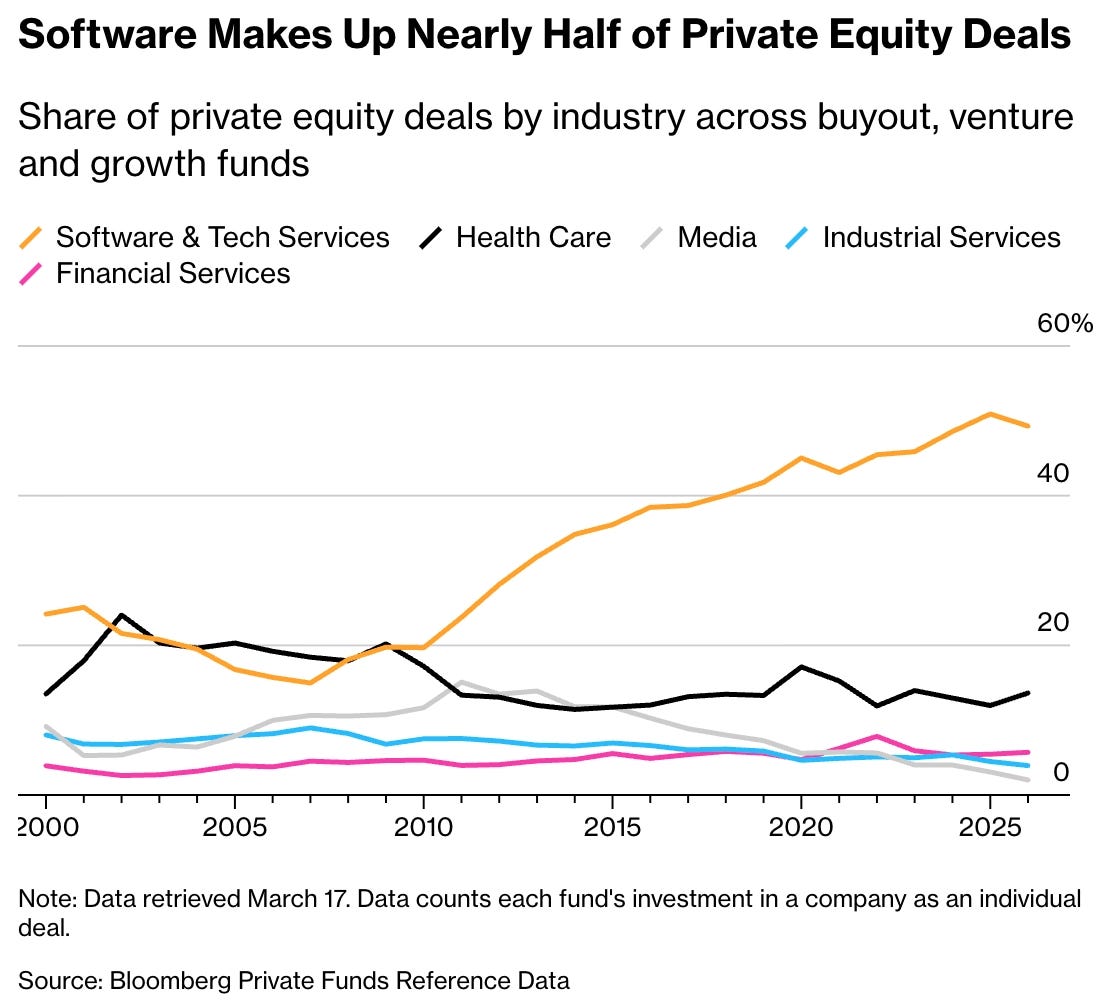

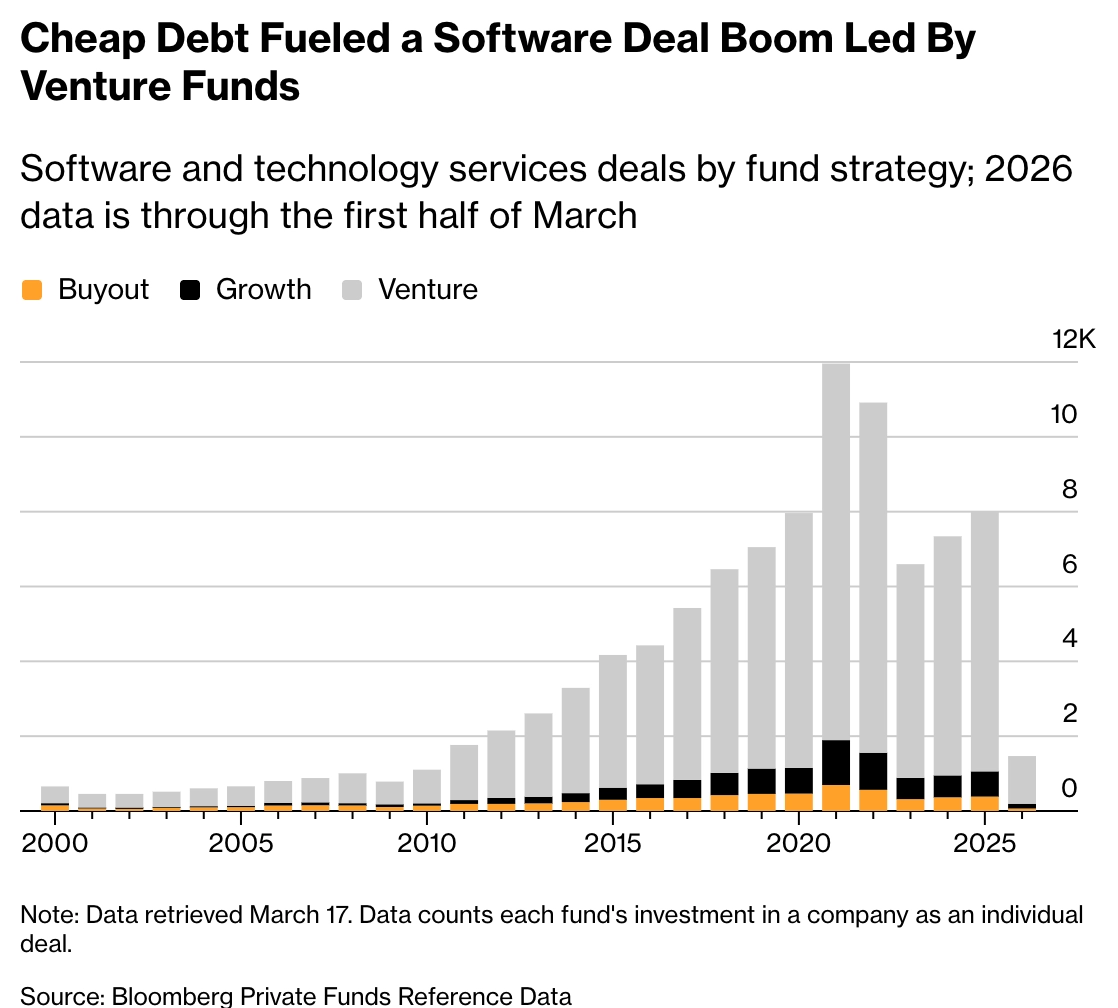

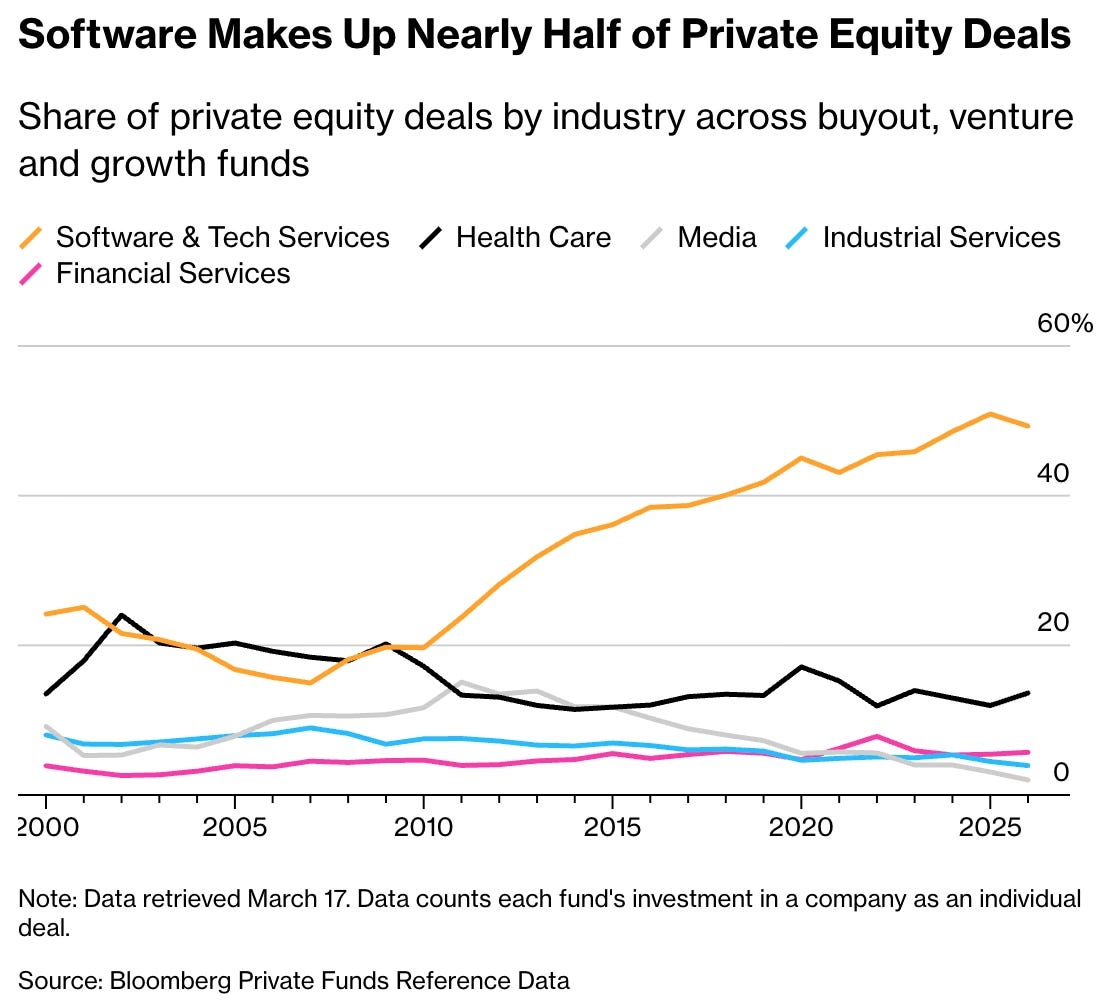

Private-equity-backed tech companies are under pressure from AI that is disrupting many existing SaaS businesses and from debt leverage with $300bn due to mature through 2028. - Bloomberg

“The software problem roiling private markets is about to face a big new test. A wall of debt maturities is looming for the industry just as artificial intelligence threatens to upend entire businesses in what’s been dubbed the SaaSpocalypse.”

“As companies look to refinance in the coming months, they face numerous headwinds, from fears about AI devaluing or replacing their products to the risk of higher borrowing costs spurred by the war in the Middle East.”

“Some private credit funds are turning away software borrowers outright as they seek to shrink their exposure to the sector, according to people with knowledge of the matter. And a number of software company sales planned by private equity have already stalled.”

“As much as 15% of software direct lending could default in the coming years.”

Thoma Bravo is shutting down its growth investing strategy to refocus on its core tech buyout business. - Bloomberg

“Almost a year ago, Thoma Bravo determined it couldn’t bring its expertise as a majority owner to its growth-equity investments because it has little say in their strategy or operations, the people said, asking not to be identified because the discussions aren’t public. The firm, which manages about $183 billion, opted to wind down the strategy after it finishes investing its remaining funds.”

Stock based compensation was always a real cost, and the AI-driven repricing of SaaS is now making that impossible to ignore. - Bill Gurley

“For the better part of a decade, the SaaS industry operated under a convenient assumption: stock-based compensation wasn’t a real cost.”

“The uncomfortable truth is that RSUs have always been a cash equivalent. Employees understand this intuitively — they sell on vest, consistently, and budget their RSU income the same way they budget their salary. When a company grants an employee $200,000 in RSUs, that employee expects $200,000 in real, spendable dollars. There is little ownership mentality or long-term alignment baked into the instrument. It is compensation that happens to route through a brokerage account.”

“Now the AI disruption of 2026 is forcing the issue. […] Companies that were valued on the assumption of durable competitive moats are now facing questions about whether those moats still hold. Stock prices reflect that uncertainty.”

“Because employees have always treated RSUs as cash, they don’t experience this as an investment that didn’t pan out. They experience it as a pay cut.”

“The companies most exposed are the ones that never reached genuine, SBC-inclusive profitability. Where equity grants were quietly subsidizing a cost structure that couldn’t stand on its own, the subsidy has now gotten dramatically more expensive — right at the moment when the business model itself is under pressure.”

Mature startups rarely pull off a successful “Act 2” product expansion due to three structural obstacles. First, economic incentives push leadership to protect existing revenue rather than invest on unproven bets. Second, the original founding team often scatters after initial success, leaving operators skilled at optimization but unsuited to zero-to-one building. Third, founders themselves get pulled in too many directions to be obsessed about a new bet. As recommendations, Vohra suggests hiring a COO to offload day-to-day duties, recruiting former founders comfortable with ambiguity, and securing investor buy-in for a multi-product vision. - Gaurav Vohra

“When growth stalls, there’s usually only one fix. Not better sales. Not more marketing. Not growth product. They’re just optimization and ornamentation. Most likely, you need a new product. A second swing. “Act 2”. But shipping a second product is hard. Most startups screw it up.”

“You need a COO or COO-like to run the business. Not parts of it; not just the boring functions you don’t like. All of it. […] You need to look at your calendar and see nothing. Your inbox should be peaceful. Your Slack should be quiet. Only if this is true have you really solved focus.”

“The KPI to track is the number of former founders on your team. They’re the pirate crew. Building anew, while optimizers pull levers and twist dials on today’s business. Run this tiny team as separately from the main business as you can. Move to a new physical location.”

**Vanta went from $100m to $300m ARR in 24 months with accelerating growth (75-80% YoY)**. It has 16k customers ($19k ACV) including 60% of the Forbes AI 50. It works with Github, Samsara, Atlassian, Cursor and Decagon. NRR over 100%. - Christina Cacioppo, Forbes

“It took us two years to grow from $10mm to $100mm in ARR and 15 months to reach $200mm. Nine months later, we crossed $300mm. Vanta’s growth rate increased each of the past four quarters – compounding really is the eighth wonder of the world!”

“AI shifted how companies approach trust: from point-in-time checks to continuous monitoring and verification.”

“What’s pulling the curve up is a problem that didn’t exist at scale 24 months ago. Vanta’s own data, drawn from its third-party risk management product and released in a recent report, found that 70% of companies now have shadow AI—tools employees adopted without security review. The company also reported that LLMs are 52% more likely to be flagged as high risk than traditional SaaS. In a single year, the average company sees employees reinstall an AI tool 1,000 times after security has revoked it. The most-reinstalled offenders, per Vanta: Claude, ChatGPT, and Cursor.”

Entropy

Matthew Gault found out that a third of new websites created since 2022 are AI generated. - 404

“The proliferation of AI-generated and AI-assisted text on the internet is feared to contribute to a degradation in semantic and stylistic diversity, factual accuracy, and other negative developments.”

“After decades of humans shaping it, a significant portion of the internet has become defined by AI in just three years. We’re witnessing, in my opinion, a major transformation of the digital landscape in a fraction of the time it took to build in the first place.”

“AI was making the internet less semantically diverse and more positive overall, but it wasn’t causing a proliferation in lies or cutting out its sources.”

“The most surprising result was that our Truth Decay hypothesis wasn’t confirmed. It’s worth noting that we were specifically looking for an increase in verifiably untrue statements, which we didn’t find.”

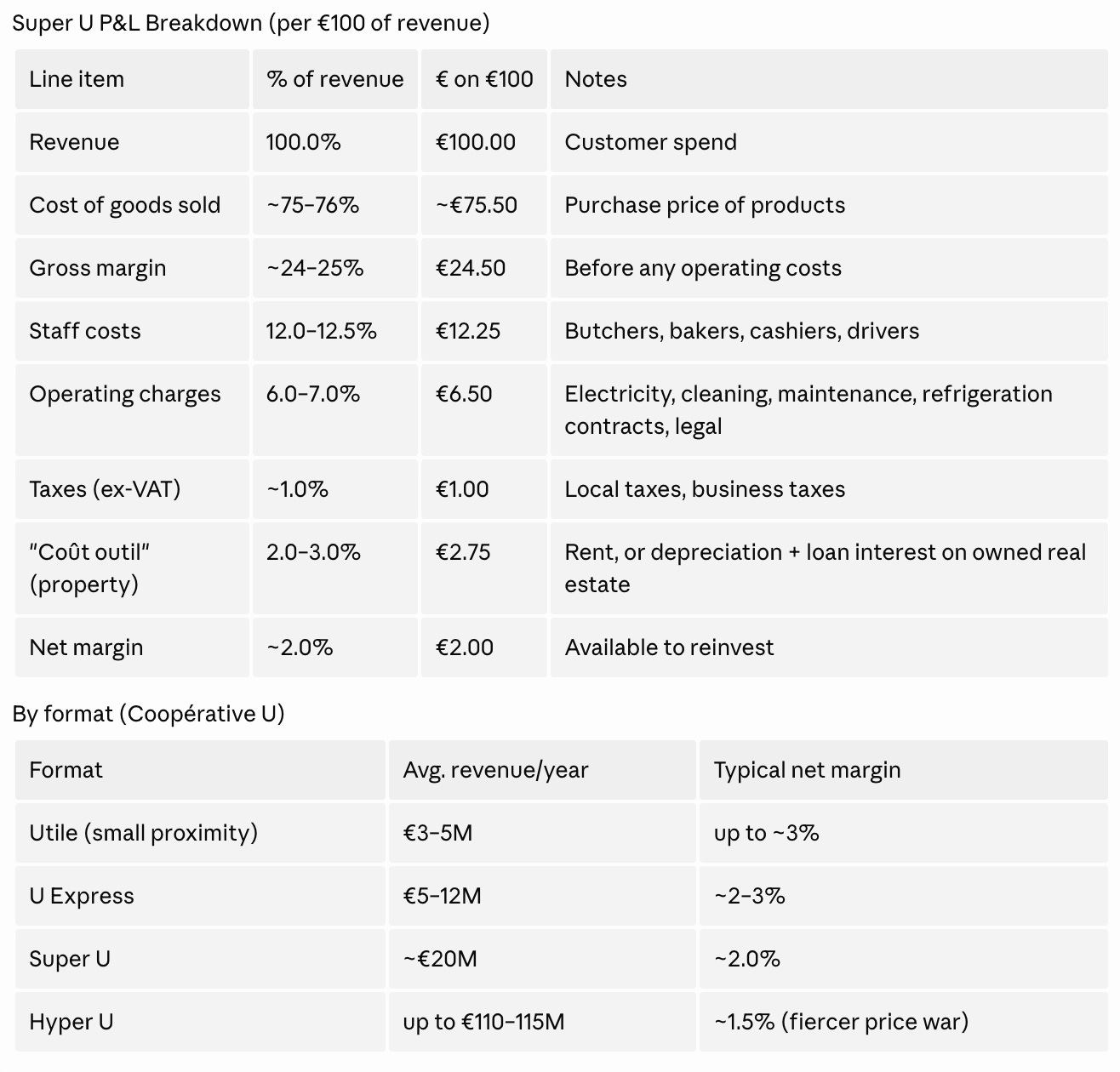

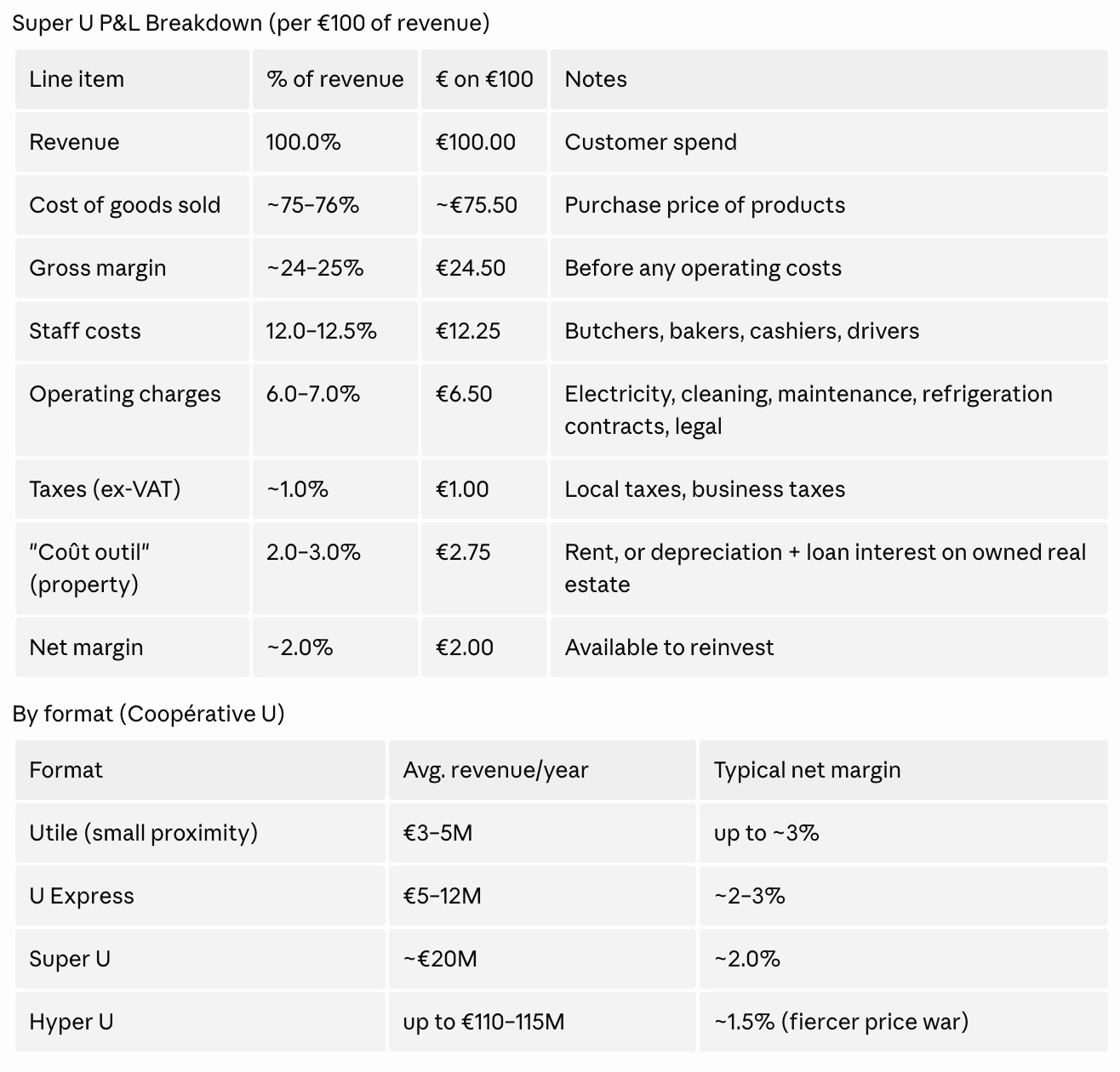

Matthieu Stefani interviewed Dominique Schelcher who is CEO at Système U which is French fourth largest grocery retailer. - GDIY

Two retail models in France: independents (Leclerc, Intermarché, U) where bosses own their stores, vs. integrated groups (Carrefour, Auchan) centralized from Paris. The independent cooperative model creates stronger alignment and local accountability.

It’s a centime business: Out of €100 spent, €2 stays with the retailer. Gross margin ~25%, but staff (~12%), operating charges (~6–7%), taxes (~1%), and property(~3%) eat almost everything.

Human-scale beats gigantism: Hyper U averages 6,000 m² (vs. Auchan’s old 20,000+). Formats that work today are ones where customers see staff they know.

Cooperation with competitors is survival: U pools purchasing with Carrefour and REWE in Europe because French market is tiny vs. global multinationals who “don’t care about distributors.”

France has entered decommercialization: Square meters are closing both in retail and in city centers. But craftsmanship is returning to downtowns as fast fashion and fast retail pull back.

Biggest growth opportunity = better food: Rising awareness links bad food to €19B in health costs annually. 35% of French people have abandoned a purchase on responsibility/quality grounds.

The social escalator still works in retail: A summer-job hire became a store director in 11 years, then bought the store from his boss. Salaries paid on 13 months; profit-sharing adds 0.5–2 months in good stores.

Fuel is a call product, not profit: 1–2 centimes/liter. Real business is in-store food sales.

“The secret of a good retailer is to never stray from their customers. Always listen to them, be close to their needs, constantly question yourself.”

China is starting to outcompete the US and Europe in high-end manufacturing. - FT

“Twenty years ago the global economy was shaken by a first “China shock” as a wave of low-cost goods destroyed the business models of manufacturers in advanced economies.”

“Now a second shock is under way — one that is even more threatening to China’s trading partners: an assault on high-end manufacturing.”

“Vicious domestic competition, coupled with vast industrial scale, ample pools of engineering talent and some of the highest subsidies in the world, has generated world-beating Chinese champions in EVs, solar panels, batteries, wind turbines and a lengthening list of advanced manufacturing sectors.”

“Companies that can survive in China are unbeatable anywhere else in the world.”

“It is a similar story across Chinese industry, from chemicals to solar to the manufacturers providing components for the car and wind giants: volumes keep rising but profits are shrinking or negative.”

“European economies including the UK, Germany and France are among those in the path of the wave of merchandise exports, since the continent’s high energy prices and labour costs leave it particularly vulnerable to cheaper products from elsewhere.”

“Companies which should exit the market keep operating, sustained by government capital, especially China’s politically favoured industries, such as solar, wind, batteries and EVs.”

“Chinese businesses are subsidised at between three and nine times the rate of their rich-world counterparts.”

“Selling more abroad, where profit margins are healthier and competition less brutal, is top of many Chinese companies’ priorities.”

Acquired broke down Ferrari. - Acquired

Ferrari is both inclusive and exclusive: the exclusivity of a luxury brand is married to the inclusivity of a sports team. It has apex clients spending tens of millions on garage collections, and 400 million fans who will never afford one but wear the merchandise and watch every race.

Ferrari makes 4 types of cars:

The Range (~85% of units, ~$280–500K) are sports cars and GTs.

The Special Series (~10%, $500K–$1M) are higher-performance limited versions. The Icona series (~$2.3M) pays homage to classic models and smooths revenue between supercar decades.

The Supercar (1–5% of units, $3.5–5M) is the profit engine: the F80’s 799 units at ~$4M each contributing an estimated ~15% of annual revenue and potentially ~30% of annual profits given 80–90% gross margins.

~80% of new Ferraris go to existing owners; ~48% to multi-Ferrari collectors. Ferrari is sold out through 2027.

Ferrari does not build cars and find buyers. Every car is manufactured only after a customer orders and customizes it. Every Ferrari that rolls off the line is unique.

Humans do manual work at every station except windshield installation (safety reasons). Any car can be made on any line which is unheard of in the auto industry. This “inefficiency” is the point: it enables launching 4 new models per year, rapid iteration, short design-to-delivery cycles, and direct tech transfer from the F1 team across the street.

Ferrari delivered 13,6k cars in 2025 on $8.2bn revenue with 38.8% EBITDA margins. Gross margins average 50% (vs. Ford 7%, BMW 14%, Porsche 15–25%, Toyota 18–21%). Profit per car exceeds $170,000. Porsche needs to sell 6 cars to match the profit of one Ferrari.

Ferrari is a luxury company, not a car company. The company trades at ~35x P/E, on par with Hermès (35–60x) and far above automakers (8–10x).

F1 went from cost center to profit center. Thanks to Liberty Media’s stewardship, Ferrari’s racing team is now worth ~$6.5B, generates meaningful sponsorship revenue (HP title deal ~$100M/year), and remains the single best marketing spend possible.

“Ferrari will always deliver one car less than the market demand.” - Enzo Ferrari

“There is not a direct correlation between Ferrari victories on the track and the number of cars that you can sell. But if for many years you do not win, it means that you do not add wood to the fire of the myth. The myth of Ferrari is based on competition. You can win or you can lose, but you cannot only lose.” - Luca di Montezemolo

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋