📖 Venture Chronicles - April 2025

Overlooked #198

Hi, it’s Alex from 20VC. I’m investing in seed & series A European vertical solutions (vSol) which are industry specific solutions aiming to become industry OS and combining dynamics from SaaS, marketplaces and fintechs. Overlooked is a weekly newsletter about venture capital and vSol. Today, I’m sharing the most insightful tech news of April.

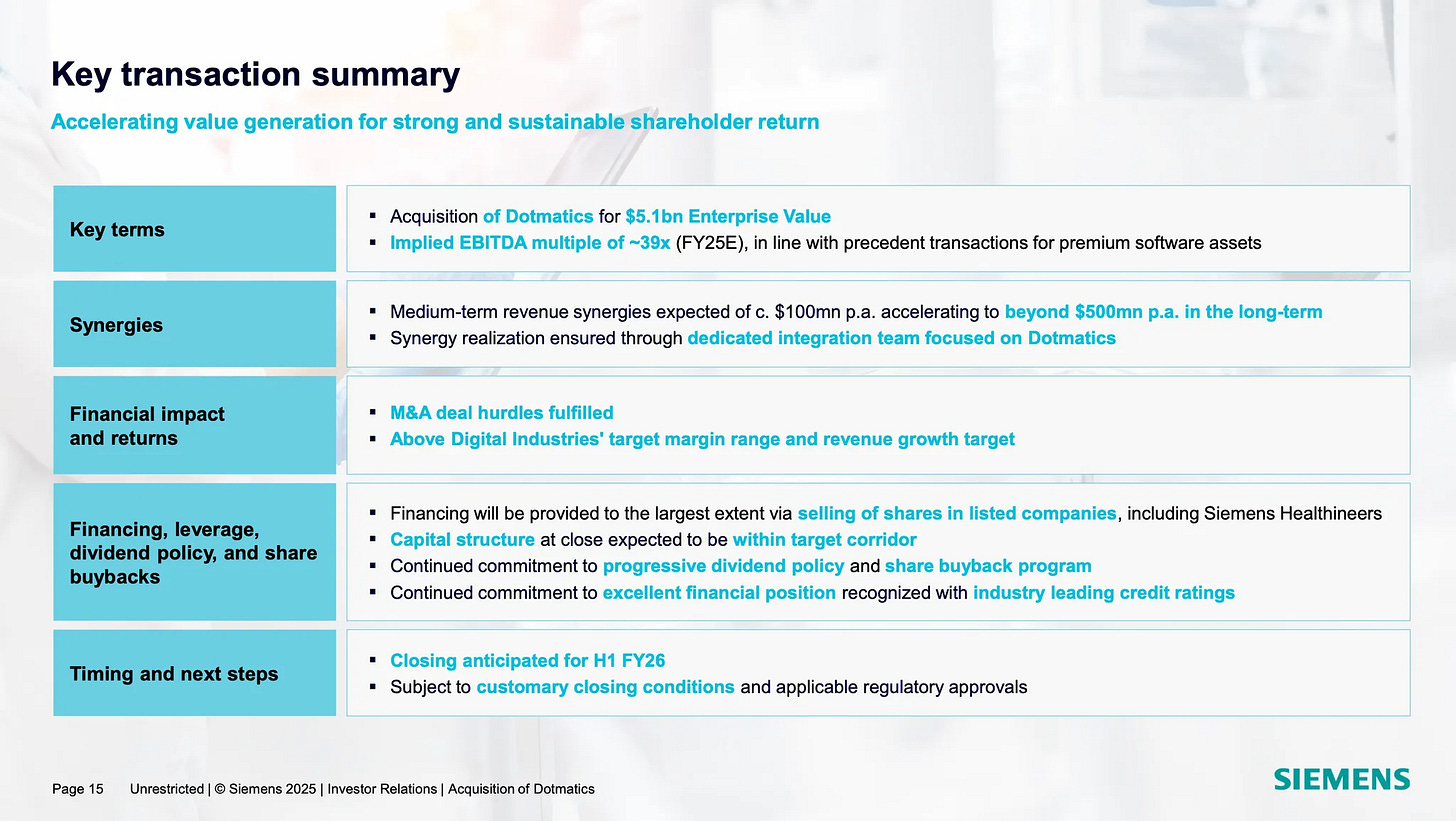

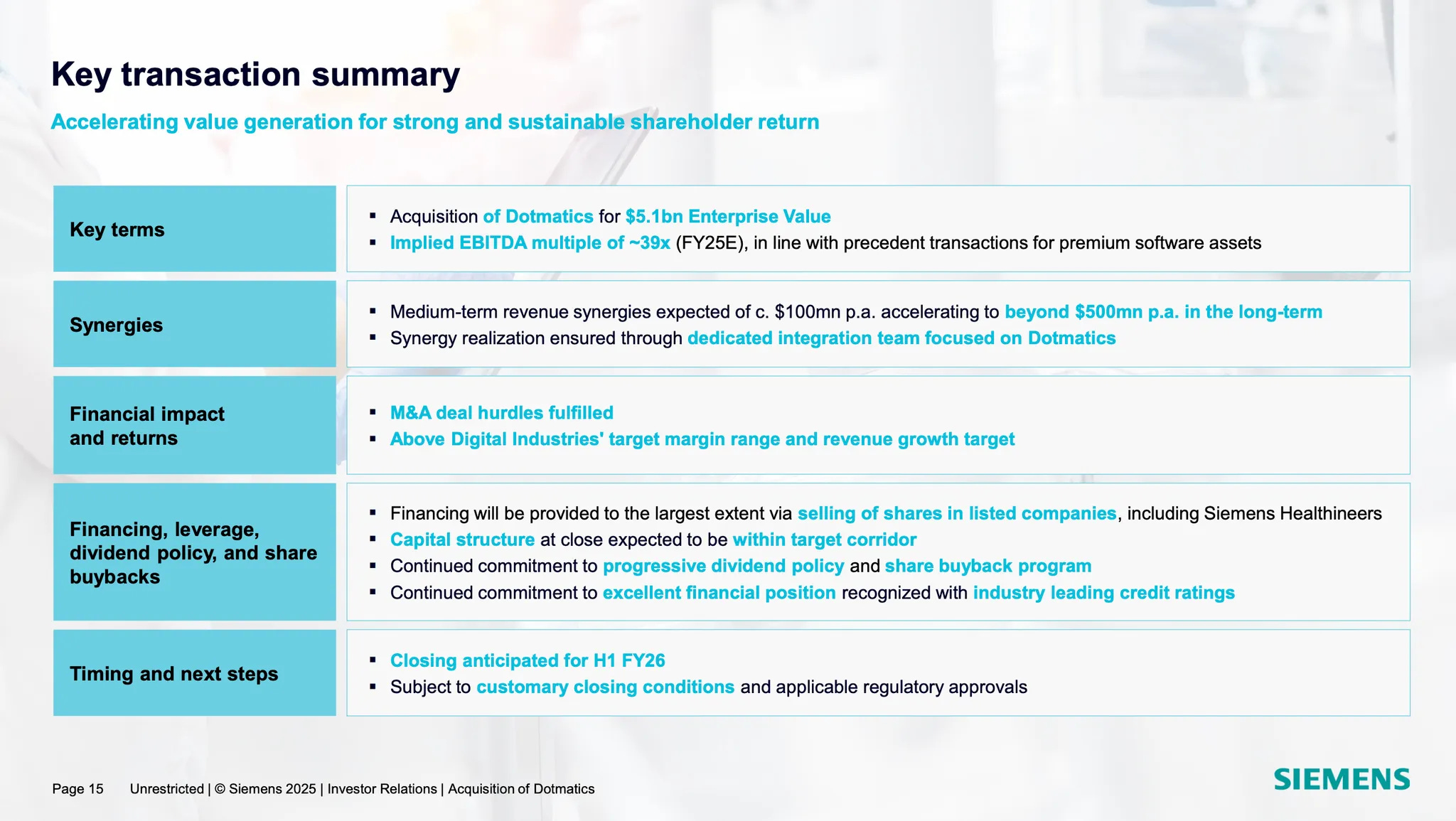

Tuesday, Apr. 1st: Siemens acquired Dotmatics for $5.1bn in another landmark vertical software deal. Dotmatics provides life-science R&D software. In 2025, the company will reach $300m in ARR with a 40% EBITDA margin implying a 17x EV/NTM ARR multiple and a 39x EV/NTM EBITDA multiple. - Bloomberg

“More than 2m scientists in 125 countries use its software, which helps to digitize lab data, enhance collaboration and analyze findings.”

“Insight first invested in Dotmatics in 2017, according to its website. A fund backed by Insight agreed in 2021 to buy the company in a deal valued at as much as £500m.”

“Combining our next-generation scientific intelligence platform and industry-leading scientific applications together with Siemens’ Digital Twin and AI capabilities, we’ll drive a new wave of innovation in life sciences R&D.”

Wednesday, Apr. 2nd: Eli Dukes at Verticalised wrote about AI-driven vertical rollups. - Verticalised

“A vertical venture buy out is when an early-stage company builds a game changing product for a specific industry, buys companies in that specific vertical, and implements their game changing technology that results in the end business dramatically increasing margins. From there, they run an M&A playbook at venture-scale.”

“In our view, to prove out at a Venture Buy Outs strategy requires a minimum of $20-30m dollars at the seed stage. Anything less and you are left without enough funding to prove out the scale of technology improvements on the core operations of the business. Not many founders can raise $20m for their seed-stage business.”

“You need to buy a big enough asset to prove out the full EBITDA impact of your technology in a business operating at scale. Only very limited VCs are comfortable underwriting that bet today.”

“Vertical buy outs remain a significant yet contrarian play awaiting both new financial innovations and founders with the appetite to go in and do the hard work of transforming companies into tech-enabled services. The upside is increasingly obvious with every passing model improvement and new design pattern. But so long as the bottleneck remains purely capital related and investors wait to see how AI plays out, the opportunity today remains somewhat limited.”

Thursday, Apr. 3rd: Colossus interviewed Neil Mehta who is GP at Greenoaks. - Neil Mehta

“By 27 Mehta’s seen enough, and he’s left D.E. Shaw to start a firm with his friend Benny. On a whim he calls it Greenoaks, after the street in Atherton, California where he grew up. In the first deck for Greenoaks there’s a slide called ‘Finding Value in Unusual Places’, which at the time meant the internet. The idea was that these internet companies, these unbelievably cheap businesses, were going to replace a large percentage of the S&P 500. In 2012, he bets 40% of his first fund on Coupang, an ecommerce retailer in South Korea, led by a founder, Bom Kim, whom Mehta’s fallen head-over-heels in love with. Greenoaks soon owns upwards of 15% of the company, and eventually returns about $8 billion from that one investment.”

“Today Mehta is 40, and over its first 13 years, Greenoaks has played a legendary part in the rise of Coupang, Figma, Wiz, Carvana, Stripe, Discord, Rippling, Toast, Robinhood, and other unicorns led by N of 1 founders, generating over $13 billion in gross profits, a 33% total net internal rate of return, and only about a point of principal impairment. The firm is unusually small and concentrated: five funds of 55 core companies across nearly $15 billion of assets managed by nine investment professionals—with Mehta himself as one of the largest LPs in each fund. Henry Kravis, one of the first LPs, told me that at the top of the market between 2020–2022, Greenoaks probably returned more money to investors than anyone else. “Neil’s extremely disciplined, he’s gone against the tide many times, and he’s had exceptional timing,” Kravis said. “He’s the real deal.””

“Many of Mehta’s earliest memories are of obsessively discussing business with his father, like the time they returned home from a fifth-grade classmate’s mini-golf birthday party at the Malibu Grand Prix in Redwood City. For most children, the outcome of having fun at mini-golf is that they want to play more mini-golf, perhaps even golf. But the fifth-grade Mehta had so much fun that he wanted to “get into the mini-golf business,” and so he and his dad modeled it out on Excel. “I can’t remember a day when I wasn’t talking about businesses with them,” he said.”

“He made money on the side as a top-ranked door-to-door seller of Cutco steak knives, cleaning up from stay-at-home moms with discretionary income in suburban Silicon Valley.”

“I became a big believer in capitalism, really company formation, as the primary source of human progress. I’m a fervently religious believer in capitalism … So the reason I do what I do is because I want to be a small part of being in service to the people creating those companies in the capitalist structure that allows humans to progress.”

““In the document, I tell the team: It’s easy to have opinions and spend other people’s money. But that’s not our job. We’re in the business of understanding what founders are doing, and being humble and curious and empathetic about it. Our job is to figure out how and why they’re painting their painting. That’s it.” “It’s so easy to be an art critic,” he said. “Understanding what a painter’s actually trying to do—that’s the hard part.””

““We started with a very clear mission,” Mehta said, “and it hasn’t changed. Find great founders building great businesses, become their single most important resource, work tirelessly to invest in them, and then become the most important partner they have. And do it over the course of decades, not years.””

“Greenoaks has led five of Coupang’s eight rounds, investing nearly $1 billion in Coupang across a decade.” At a certain point early on, Kim realized that Coupang wasn’t going to be Korea’s Groupon but a global ecommerce juggernaut. By the time of the company’s Series B, Mehta had essentially bet all of Greenoaks on Coupang, and was de facto involved in the fundraising.”

“A lot of them talk about how the secret to being a great investor is leaning in when others lean out, and vice versa. It’s very easy to say, but really terrifying to do in practice.” –Parker Conrad, Rippling

“All of our alpha comes from ignoring the memetic vibes of Silicon Valley and New York and focusing on the fundamentals of a business and the founder. That’s it.”

“Wiz, the Israeli agentless cloud security company, which Mehta and his partners didn’t know existed until they sussed it while diligencing the company’s competitors—at which point they called the founder, Assaf Rappaport, talked to him for 30 minutes, dropped the competitors, and a week later led a round at a $1.7bn valuation when the company was doing only $2m in revenue”

“Mehta and Peretz had known about SpaceX early on, but some of their industry mentors warned them away from Musk. “He fires people quickly, he micromanages people like crazy, he disappears for large swaths of time, comes back in and changes everything,” Mehta remembers being told. “And we were like, well, I guess we can’t back him then.” ““We didn’t do the primary work ourselves,” Mehta ruminated, venting his spleen. “We outsourced that work. I cost our investors billions of dollars because of that. We later became small investors [in SpaceX], but I’ve had to look our investors in the eye and tell them we’ve lost them tens of billions of dollars because of the mistake we made as a firm on that. And I told myself then: I’ll never not do the work myself again.””

Friday, Apr. 4th: The New Yorker wrote about the general decline in fertility rates across the world. - The New Yorker

““The Population Bomb” transformed regional unease into a global panic. India, in less than two years, subjected millions of citizens to compulsory sterilization. China rolled out a series of initiatives—culminating in the infamous one-child policy—that included punitive fines, obligatory IUD insertions, and unwanted abortions.”

“The “total fertility rate” is a coarse estimate of the number of children an average woman will bear. A population will be stable if it reproduces at the “replacement rate,” or about 2.1 babies per mother. (The .1 is the statistical laundering of great personal tragedy.) Anything above that threshold will theoretically generate exponential expansion, and anything below it will generate exponential decay. In 1960, the tiny country of Singapore had a fertility rate of almost six. By 1985, it had been brought down to 1.6—a rate that threatened to roughly halve its population in two generations.”

“Today, declining fertility is a near-universal phenomenon. Albania, El Salvador, and Nepal, none of them affluent, are now below replacement levels. Iran’s fertility rate is half of what it was thirty years ago. Headlines about “Europe’s demographic winter” are commonplace. Giorgia Meloni, the Prime Minister of Italy, has said that her country is “destined to disappear.” One Japanese economist runs a conceptual clock that counts down to his country’s final child: the current readout is January 5, 2720.”

“South Korea has a fertility rate of 0.7. This is the lowest rate of any nation in the world. It may be the lowest in recorded history. If that trajectory holds, each successive generation will be a third the size of its predecessor.”

“The end of the world is usually dramatized as convulsive and feverish, but population loss is an apocalypse on an installment plan.”

“Liberals are right to point to immigration as the obvious way to mitigate the economic effects of demographic contraction. Italy currently has a shortage of nurses, and Germany has a shortage of plumbers; a baby born today does nothing to unclog a Düsseldorf sink. Even immigration, however, is a stopgap measure: by 2100, ninety-seven per cent of the world’s countries are predicted to be below replacement. In the meantime, pro-immigration policies will continue to generate nativist backlashes. Last year, Seoul sponsored a pilot program to import a hundred nannies from the Philippines. The project, despite its lack of ambition, was wildly controversial.”

“Countries have tried everything to reverse demographic collapse. In Hungary, women with four or more children gain a lifetime exemption from income tax.”

“Some Korean companies pay their employees to have children, but the private sector now generally accepts that it must adapt to a world where children are luxuries. Analysts anticipate a hundred-and-sixty-billion-dollar “silver industry” to meet the needs of healthy pensioners. One travel agency expects that seniors, in the absence of grandchildren to spoil, will spend their disposable income on pricier trips.”

Saturday, Apr. 5th: Nikhil Namburi argues that the “sell work” thesis is a fallacy and that startups should give away work done by agents at cost and monetise on the back with adjacent offerings. - Nikhil Namburi

“Sell work not software has become a common trope among venture investors, but it seems to be aging quite poorly. The problem with this thesis is that it causes you to underwrite a TAM that’s roughly proportional to existing markets for human labor ($100Bs). But of course, customers won't pay "x% of human costs" in 7 years. They'll pay the prevailing rate of AI agents, which will be orders of magnitude cheaper than current human rates. My favorite new wave of startups is giving away agents at cost, with their actual revenue model predicated on adjacent offerings enabled by at-cost AI agents.”

“A lot of startups are claiming that they’ll be sticky due to the “moats” below, but these seem a lot weaker in an agent-centric world: (i) system of record, (ii) cognitive switching costs (in the enterprise) and (iii) "embedding deeply" in enterprise workflows.

Sunday, Apr. 6th: Wendy Xiao at Northzone wrote about AI-powered roll-up plays. - Wendy Xiao

“AI is allowing technology to adopt people versus the other way around, and that has some irreversible effects on the markets we are investing into.”

“Traditionally, much of PE’s performance has been driven by the use of leverage to drive returns on equity. At the same time, PE firms can also drive operational efficiencies and create scale by merging competitors, cutting overhead, improving processes, and more recently introducing technology. The former strategy is commoditized, but as operational talent is more scarce, the latter strategy is more differentiated and sustainable.”

“A lot of the tech adoption happening now is in sectors that were previously untouched by venture-backed tech companies because it was so hard for a company so ridden with manual and offline processes to adopt technology.”

“Some of the fastest growing venture-backed startups in AI are selling to PE rollups, and of course PE firms are incentivized to be using these technologies to cut costs within portfolio companies.”

“We are seeing VCs rolling up companies themselves to drive out costs with AI-enabled tech. We are seeing PEs hire previously venture-backed talent directly to roll this out across their portfolios.”

There are 3 potential scenarios for AI-driven vertical rollups:

“1. If the software tools completely commoditize and PEs are great at implementing the tech, the value could show up in the OPEX budget of PEs.

2. If the software tools don’t commoditize, it could go to the tech giants that will be built to serve these PE-owned offline sectors.

3. It could go directly to the venture-backed tech-enabled businesses that will completely displace the PE-owned incumbents.”

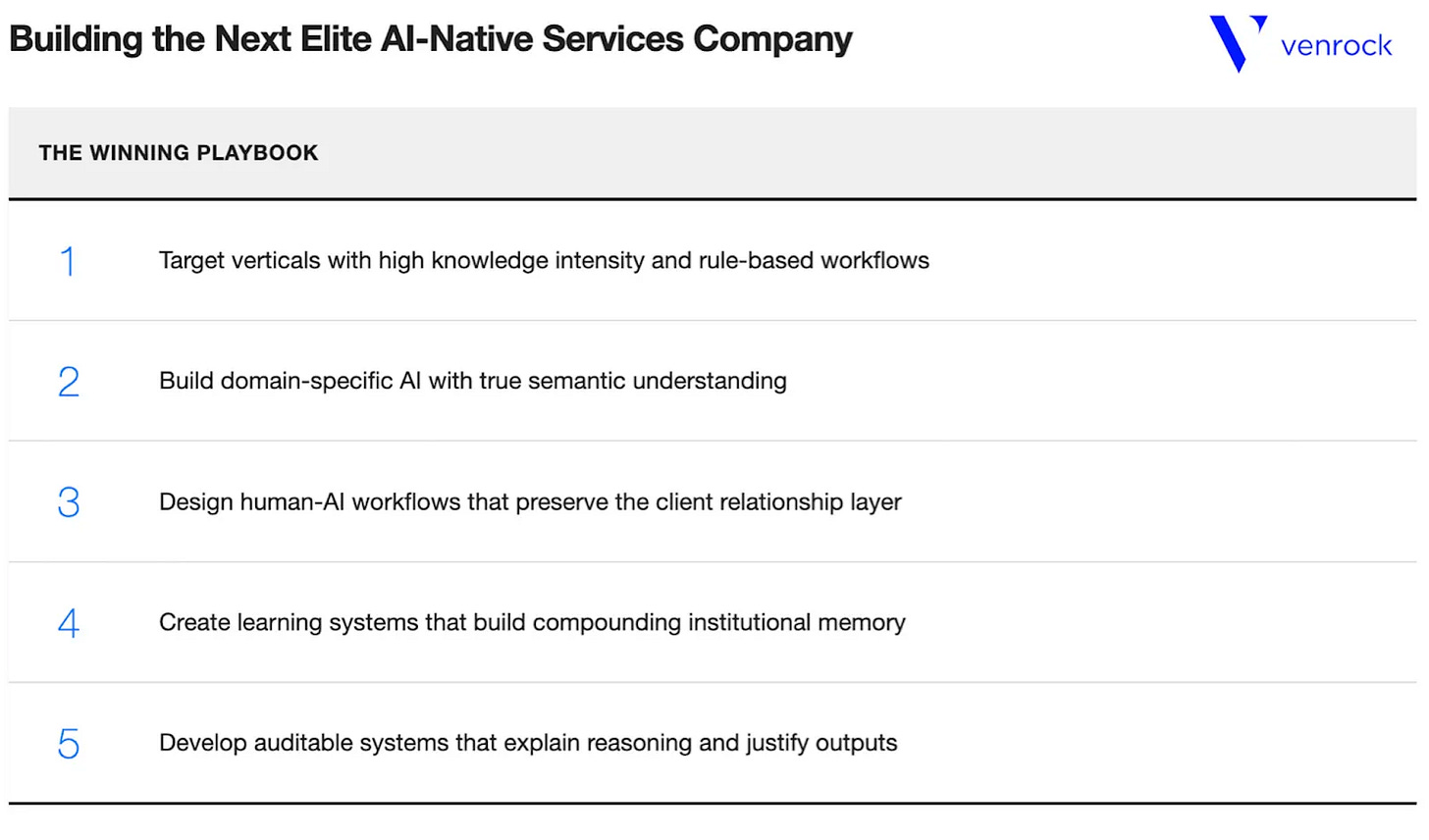

Monday, Apr. 7th: The professional services industry, worth $20 trillion globally, is poised for massive disruption as AI-native firms challenge legacy players. Traditional firms rely on human expertise, outdated processes, and prestige, while AI-driven startups offer scalable, efficient, and transparent services with superior outcomes. These new firms operate on software-like margins, democratize access to elite services, and promise 24/7 responsiveness. Key sectors like law, insurance, and consulting are ripe for transformation. - Venrock

Tuesday, Apr. 8th: Plaid raised c.$575m led by Franklin Templeton, alongside Fidelity, NEA and Ribbit at a $6.1bn valuation. It’s a massive discount compared to Plaid’s previous $13.1bn valuation reached in 2021. - Plaid, FT

“In 2025, tech multiples have massively compressed between the time that we raised last and today,” Perret said. “What I will say is that the fundamentals of the business underneath are dramatically stronger than they were in 2021. Revenue is much higher.”

“Investor sentiment around the largely lossmaking open banking sector — which is built on data-sharing technology — has not picked up.”

“The proceeds of this round will be used to address employee tax withholding obligations related to the conversion of expiring RSUs to shares, and to offer some liquidity to our current team.”

“Open banking was built on the promise that data-sharing would boost competition in the consumer finance sector by enabling innovative tools for consumers. However, companies are yet to prove they can be durably profitable while “pay-by-bank” solutions powered by the technology have not yet reached mass adoption.”

“Plaid has in recent years sought to diversify away from its core business of connecting bank accounts to websites and towards new services, including anti-fraud solutions and identity-verification tools powered by its data-sharing technology.”

Wednesday, Apr. 9th: I listened to a Business Breakdown’s podcast episode on Motorola Solutions. - Business Breakdown

Motorola divested its consumer-facing businesses (most notably mobile phones) to concentrate on the Land Mobile Radio (LMR) market for public safety and commercial clients. Over the past 15 years, Motorola Solutions has leveraged its dominant market share in LMR, optimized its cost structure, strategically allocated capital through share buybacks and acquisitions, and expanded into adjacent high-growth areas like video surveillance and command center software.

Motorola Solutions holds an estimated 80% market share in LMR networks deployed across the US, Europe, and Australia, with around 13,000 networks deployed. The business operates on a "razor-razorblade" model, selling the initial network infrastructure and then generating recurring revenue through radio sales (upgrades every 5-6 years), maintenance, and related services.

c.75% of the LMR business is tied to the government sector (public safety), with the remainder being commercial customers and heavy industries.

Compared to the cellular network, LMR networks offer superior reliability and control for critical communications, especially during emergencies. They have dedicated spectrum, backup power and multiple levels of redundancy.

Motorola entered the video market through the acquisition of Avigilon, offering an end-to-end portfolio of cameras, analytics, video management, and storage. AI is increasingly being integrated into their video surveillance offerings for proactive threat detection. This segment now accounts for about 15% of revenue and is growing at a double-digit rate.

Motorola has built a suite of software solutions for command centers, covering detection, response, and resolution phases of incident management. This includes software for receiving citizen reports, coordinating field responses, and record-keeping. This segment is synergistic with the LMR business and has seen significant penetration in 911 command centers (around 50%).

“The business operates in that classic razor razor blade business model where they sell the razor which is the network at the start and then they sell radios really perpetually for a long period of time to the customer."

Due to their market dominance, the criticality of their products for customers, and the reluctance of customers to mix and match radios across their networks due to concerns about complexity and interoperability, Motorola possesses significant pricing power.

Thursday, Apr. 10th: Roam raised a $11.5m series A led by Keith Rabois at Khosla with the participation of Founders Fund which led its seed round. It helps buyers access homes with assumable mortgages, allowing them to benefit from lower interest rates. An assumable mortgage is a home loan that allows a buyer to take over the seller’s existing mortgage, including its interest rate and terms, instead of getting a new loan. - Techcrunch

“More than 200,000 buyers have registered on its platform in the last 12 months. Roam charges each buyer 1% of the purchase price. Doing the math, 1% of $200 million translates to Roam making $2 million in revenue in 2024.”

“It has plans to be nationwide by year’s end and Singh expects that Roam will see $1bn worth of home sales facilitated by its platform in 2025.”

“Without Roam, it takes 180 days to close an assumable mortgage. With Roam, it’s 45 days.”

Friday, Apr. 11th: Alex Konrad wrote on Granola, which is a note-taking app that uses AI to create summaries from meeting notes, gaining popularity among tech users and investors. - Upstart

“Last October, Granola raised a $20m Series A funding round despite just 5,000 weekly users. That number has grown consistently by 10% each week since, Pedregal says – meaning Granola is still small, but growing fast. (Up to 50,000 users now, by Upstarts’ napkin math.)”

“The first thing you notice (or don’t) about using Granola in a meeting: it’s discreet.”

“If you’re a Granola nerd, the fun begins when the meeting’s over. Granola’s software grabs whatever notes you made and folds them into its own AI-powered summary with bullet points and quotes. Users can reformat the notes to fit specific formats like a hiring meeting or weekly standup outline with a click.”

“Meetings turned out to be catnip for an intentional early test user: VCs. Startup investors take a high volume of meetings weekly; they’re also professionally incentivized to experiment with new tools.”

“The sense that Granola has good taste – that it’s loyal to its users first, corporate buyers second – has helped it continue to ripple out among tech circles.”

“Granola’s ideal customer persona isn’t a VC anymore – it’s actually founders now, said Pedregal, as VCs increasingly might be angling to invest in Granola, or flatter its leadership. Founders use the software across a variety of job functions like sales, marketing and operations. It’s penetrated to tech executive recruiting firms, too: at Daversa Partners, president Laura Kinder said she has embraced Granola whereas other note-taking apps felt “intrusive” for confidential recruiting calls.”

“Granola plans to make it possible to group meetings together to be queried, so that a user might be able to ask about all meetings on a certain project, or interactions with a particular client. Granola also plans to add integrations and features to take actions from those surfaced insights, such as generating a customer email or drafting marketing copy.”

Saturday, Apr. 12th: Conversational interfaces, like voice assistants and chatbots, often promise a new way to interact with technology but fail to replace traditional computing methods. - Julian Lehr

“Conversational interfaces are a bit of a meme.”

“Data transfer mechanisms have two critical factors: speed and lossiness. Speed determines how quickly data is transferred from the sender to the receiver, while lossiness refers to how accurately the data is transferred. In an ideal state, you want data transfer to happen at maximum speed (instant) and with perfect fidelity (lossless), but these two attributes are often a bit of a trade-off.”

“We are significantly faster at receiving data (reading, listening) than sending it (writing, speaking). This is why we can listen to podcasts at 2x speed, but not record them at 2x speed.”

“Natural language is great for data transfer that requires high fidelity (or as a data storage mechanism for async communication), but whenever possible we switch to other modes of communication that are faster and more effortless. Speed and convenience always wins.”

“Today, we live in a productivity equilibrium that combines graphical interfaces with keyboard-based commands.”

“Modern productivity tools take these data compression shortcuts to the next level. In tools like Linear, Raycast or Superhuman every single command is just a keystroke away. Once you’ve built the muscle memory, the data input feels completely effortless. It’s almost like being handed the butter at the breakfast table without having to ask for it.”

““But what about speech-to-text,” you might say, pointing to reports about increasing usage of voice messaging. It’s true that speaking (150wpm) is indeed a faster data transfer mechanism than typing (60wpm), but that doesn’t automatically make it a better method to interact with computers.”

“The inconvenience and inferior data transfer speeds of conversational interfaces make them an unlikely replacement for existing computing paradigms – but what if they complement them?”

“Instead, AI should function as an always-on command meta-layer that spans across all tools. Users should be able to trigger actions from anywhere with simple voice prompts without having to interrupt whatever they are currently doing with mouse and keyboard.”

"This isn’t really a case against conversational interfaces, it’s a case against zero-sum thinking. We spend too much time thinking about AI as a substitute (for interfaces, workflows, and jobs) and too little time about AI as a complement. Progress rarely follows a simple path of replacement. It unlocks new, previously unimaginable things rather than merely displacing what came before.”

Sunday, Apr. 13th: Bloomberg wrote about Helsing’s evolution as a company from pure software to full stack defense platform starting with drones. - Bloomberg

“Today, as EU leaders prepare to commit record amounts to rearmament, Helsing is Europe’s most valuable defense tech startup. With deep pockets and close ties to Germany’s military, the Munich-founded company is, at least on paper, optimally positioned to benefit from the coming spending spree.”

“A strategic partnership with Germany’s biggest defense firm, Rheinmetall AG, fell apart last year. In Ukraine, where Helsing says its technology has been in use since Russia’s full-scale invasion in 2022, attack drones equipped with the company’s software have been criticized by frontline soldiers and military experts as significantly more expensive and not as effective as comparable products.”

“Facing the whiplash pace of electronic warfare and changing battlefield demands, European suppliers often seem to struggle to keep up.”

“Since its founding, Helsing said in a statement, it has “won over a dozen contracts” with “total order volumes of hundreds of millions of dollars.””

“Helsing started out with a plan to build artificial intelligence software that could process and integrate sensor data from tanks, fighter jets and other military equipment — a sort of AI brain for arsenals and battlefield decision-making.” “Soon, Helsing began cutting deals with defense contractors and bidding directly on military contracts, largely in Germany.”

“As cash began flowing into the sector, Helsing teamed up with Rheinmetall to work on the “joint development of software-based defense systems and retrofitting of existing platforms,” the companies said. In 2023, the German government selected Helsing and Saab AB to work on the Eurofighter jet program, prompting Helsing to note that it had secured a budgeted military contract faster than a US counterpart, defense tech startup Anduril.”

“In the past year, Helsing won a €40 million sealed tender from the German government to help fortify the Lithuanian border with sensor systems and drones.”

“As the war in Ukraine has dragged on, drones have become the most effective weapon in the country’s defense, and increasingly central to Helsing’s strategy. Kyiv plans to purchase some 4.5 million drones this year — some costing as little as €360 — largely from local manufacturers.”

“In November, the German news outlet Bild reported that Helsing had struck a deal with Ukrainian startup Terminal Autonomy to equip 4,000 of that company’s cheap, plywood drones with Helsing’s new custom-made software, known as Altra.”

“A former NATO official said Ukrainian forces have reported that these HF-1 drones have had more problems than comparable models. Another person who said they had seen the drone in use in Ukraine described the software as glitchy and said that soldiers found it hard to handle.”

“At the end of last year, Helsing announced plans to start making its own drones equipped with Altra software that could navigate and strike targets without the use of satellite positioning.”

“In February, it announced that it was able to manufacture 1,000 HX-2 drones a month, and that it planned to ship 6,000 to Ukraine to fulfill an order from the German government.”

Monday, Apr. 14th: TBPN interviewed Kleiner Perkins’ partner Everett Randle. - TBPN

“What made KP special back then is what makes it special now. We're a very small team. There's 10 of us total on the investment team. We all just care very deeply about the craft of venture, founders, company building. We want to keep it a craft.”

“The companies that end up going out public are the ones that have to go out and then that just becomes a vicious cycle where they maybe underperform because they're not these sort of best-in-class companies.”

Does the IPO market want you? There are 80+ SaaS companies with $500m+ ARR. A public investor will find exposure to an industry in these companies. It’s harder to list companies that will bring something different to the existing public market. You need to be cash flow positive. You need to have $500m-1bn in revenues. You need to have a special narrative around the company.

In parallel, the best private companies (SpaceX, Stripe, Databricks) are taking drastic measures not to go public doing RSU catalysed rounds to give liquidity to employees. Today, there is an unlimited supply of capital for these private companies (e.g. Databricks raised $10bn in equity in 3 months). There are multiple benefits of staying private like being more aggressive on M&A (e.g. Databricks’ acquiring pre-revenue company Tabular for $2bn). The liquidity timeline for the top 10 companies has completely evolved. The better the company, the longer the timeline to get liquidity.

With the growth fund, we only do 10-12 core investments and every single investment need to have something very unique or special about it. You can look around the table and say this has the potential to be one of the top 5 companies in the world.

You no longer have Tiger but you have 4-5 platforms (e.g. Lightspeed, GC, a16z) continuing the trend of platformising the venture capital industry. There are 4-5 different sub-asset classes in venture.

Tuesday, Apr. 15th: The Economist wrote about LinkedIn which has now 1.1bn users and booming revenue under Microsoft’s ownership from $3bn in 2016 to $17bn in 2024. Once a networking site, it’s now a key content and recruitment platform, evolving into Microsoft’s test-bed for AI tools. - The Economist

“LinkedIn is taking on a new strategic function for Microsoft. As the tech giant bets big on AI, LinkedIn is providing its owner with a billion willing guinea pigs, perhaps giving it an edge in the AI race.”

“Every other social network lives on advertising. LinkedIn sells ads too—$7bn-worth last year, analysts estimate—but makes the largest share of its revenue from its recruitment business. LinkedIn claims that it is the world’s biggest, filling a job vacancy every couple of seconds. The company also made $2bn last year from paid subscriptions, a business no other social network has cracked.”

“Although LinkedIn is still independently run, it has become integrated with the Microsoft machine: Outlook, Microsoft’s email and calendar app, can retrieve contact information from LinkedIn; Dynamics, its customer-relationships software, uses data from LinkedIn to help salespeople reach the right people in companies they are hoping to do business with.”

“More AI tools are on the way, including an agent that tracks down job candidates. Siemens, a German technology company which got early access, reports that it radically reduced time spent searching for staff.”

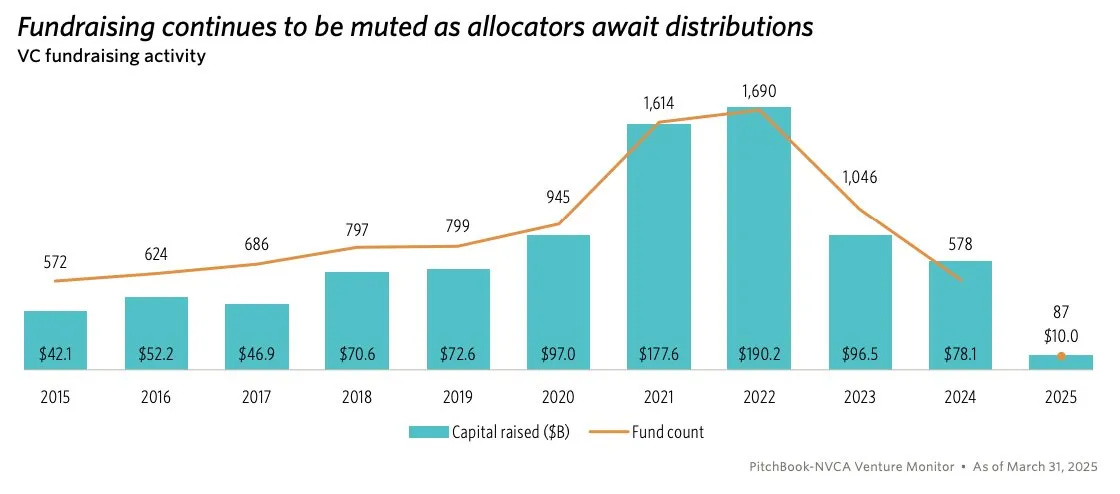

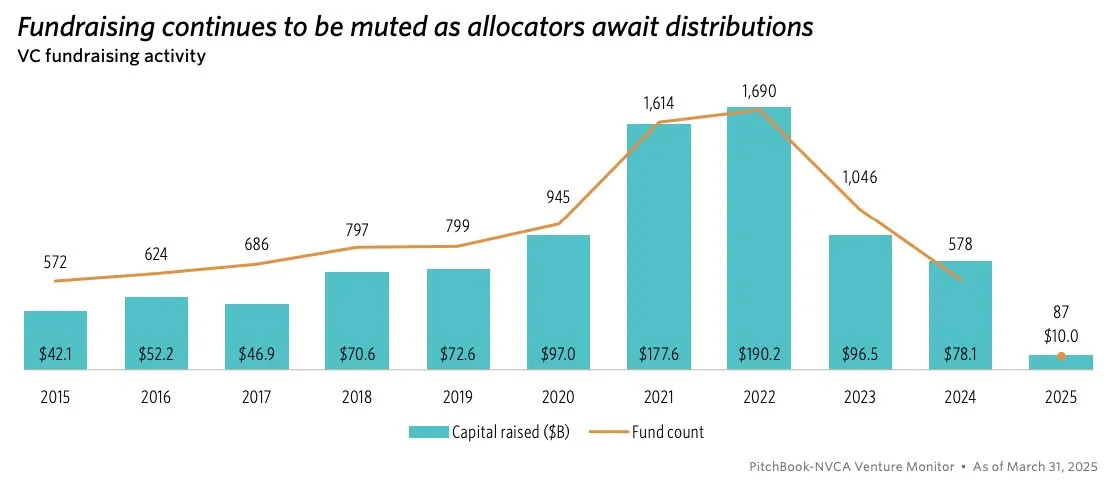

Wednesday, Apr. 16th: In Q1-2025, VC funds’ fundraising did not recover mainly due to a lack of liquidity in the asset class and macro uncertainties. - Beezer Clarkson

“LPs continued to concentrate into their highest-conviction managers – both established & emerging.”

“In Q1-25, only $10bn was raised across 87 VC funds, setting a pace for the lowest year of fundraising in a decade. 2024 saw a concentration of capital raised by a few managers, with the top decile of funds by size contributing over 71% of the capital raised.”

“77% of managers that raised in 2021 or 2022 have yet to close a fund since, and that percentage increases to 85% when looking at emerging firms.”

Thursday, Apr. 17th: I listened to an Invest Like the Best’s podcast episode with Neil Mehta who cofounded Greenoaks in 2012. - Invest Like the Best

“Neil was so convinced of Coupang's potential that he invested 40% of their initial $50 million fund into the company—a bet that eventually returned about $8 billion. Over its first 13 years, Greenoaks has backed legendary companies like Figma, Wiz, Carvana, Stripe, Discord, Rippling, and Toast—generating over $13 billion in gross profits with a 33% net IRR.”

“Greenoaks operates with remarkable concentration: just 55 core companies across nearly $15 billion in assets, managed by only nine investment professionals. Their approach reflects their singular pursuit: finding companies that will become a meaningful part of the S&P 500.”

“JDCE stands for Jaw-Dropping Customer Experience. A very small number of the world's founders are going to produce a significant proportion of the value that humans enjoy. It's really hard in the world of capitalism to build something that delights humans at a differential rate to what anybody else on earth can do. Think about when you pick up your iPhone or the first time you might have used an Uber, if you're a developer, the first time you use Stripe for payments, or if you're a trader, maybe you opened Robinhood. It usually starts with breaking trade-offs. It usually starts with doing something very difficult, either technically or operationally, that would usually give competitors nightmares. You have to do something that was borderline impossible or perceived to be impossible before. You have to do it from a customer-centric perspective. You have to really figure out what the customer pain points are.”

“Focus means saying no to everything else, everything else, at the cost of doing what the single most important thing is. There's two parts to that.

It's the ability to prioritize what is most important. You have to practice it to be able to intuitively grok what is most valuable and most important.

And then the ability to maniacally do that at the cost of everything else is an intestinal fortitude that just not a lot of people have.”

“I don't think there are many truly amazing founders that are building bad businesses. I maybe ran into one or two, but they figured it out pretty quickly. I think that truly remarkable founders think in terms of jaw-dropping customer experiences, they think in terms of competitive moats, they think in terms of scale, getting to large TAMs. So every once in a while I run into a founder that hasn't figured that all out yet. But usually they're very young and the learning curve is very steep. It always starts with founders for us.”

“Without exception, all the businesses we've been invested in for more than five years have gone through a rough patch or two. Where the fundamental premise of the business and the quality of the business is being questioned.”

“We just said we'd like to invest in great businesses that are going to be a meaningful part of the S&P 500. To this day, I still have a list of the S&P 500 companies on my desk. I stare at that list all the time, and I just try to figure out what companies are not on that list today, that will be on that list tomorrow. And then how do I work tirelessly to become the single most important partner they have.”

Friday, Apr. 18th: Doss, which is building a next generation ERP, raised a $18m series A led by Theory Ventures and reached $1m ARR only two years after inception. - Upstarts, Tom Tunguz

“Doss is taking on one of the least cool – and biggest – categories in software: enterprise resource planning, or ERP. If customer relationship management, or CRM, is the brain of a business’ software back-end for selling pretty much any kind of goods, the ERP is its heart – where accounting and procurement live, inventory and financial planning.”

“Doss currently works with more than 30 customers and has reached $1 million in annual recurring revenue.”

“Doss is an example of a thesis Tunguz, a longtime popular blogger in business software circles, calls “composable software” – software that can be developed faster, and adapted dynamically, using AI’s coding and technical abilities.”

“Companies can put together Lego blocks of components to match what they need,” Tunguz says. “AI enables Doss to sell its product in a way that doesn’t look like any other ERP.”

“With contracts ranging from $10,000 annually into the hundreds of thousands, Doss plays in the mid-market of companies between $5 million and $200 million in sales.”

“Incumbents can’t emulate Doss’s approach without undermining their own channel partners and integrators.”

Saturday, Apr. 19th: Lighthouse acquired The Hotels Network. Lighthouse (ex. OTA Insight) is a Belgian based vertical software platform in the hospitality sector providing AI-driven tools for pricing optimization, market analysis, and revenue management. It has 70k hotels and short term rental providers as customers and was recently valued over $1bn in a $370m series C led by KKR in Nov. 2024. The Hotel Network is a marketing personalisation software serving 20k hotels in 100 countries. The company was founded in 2015 and raised $15m. Its product will be integrated into Lighthouse’s platform. - Lighthouse, Skift, EU Startups

“The tech by London-based Lighthouse is meant to help hoteliers make decisions about pricing, promotion, and distribution. […] The tech by The Hotels Network aims to deliver personalized offers and marketing messages to consumers as they’re shopping for hotels, with the goal of increasing direct bookings. That means the content shown on a hotel’s website could be different depending on the consumer and what their goals are.”

“Combining the two technologies means that hotels should be able to personalize pricing and then make offers in a more targeted way, all from one platform. Now, the companies will spend the next months working to fully integrate the tech.”

Sunday, Apr. 20th: Forbes wrote on US drone companies’ heavy reliance on Chinese components despite U.S. efforts to support local manufacturing. - Forbes

“The conflict in Ukraine, rising tensions over Taiwan and the dominance of Chinese drone companies like market leader DJI have underscored the need for the U.S. military to source cheap and mass-produced drones from American and allied companies. But Thornton’s exchange highlighted an open secret in Silicon Valley: most drone companies answering the Trump administration’s America First mandate have a “Made in China” parts problem.”

“China currently controls close to 90% of the global commercial drone market, and manufactures most of the key hardware used to build them – airframes, batteries, radios, cameras and screens, according to market research firm Drone Industry Insights UG.”

“Several American drone companies with Pentagon contracts — including Skydio, one of the largest — are scrambling to rebuild their supply chains after Chinese sanctions cut off access to suppliers.”

“China could shut [the drone industry] down globally for a year.” “It's a national security issue, not just for the United States, but for the global West.”

“For example, military purchases from Orqa, a drone company that pitched itself as “DJI of the West,” were halted after allegedly banned Chinese components were found in its products. “Most of the western drone companies still rely on Chinese components,” Orqa’s CEO Srdjan Kovacevic told Forbes. (He said Orqa has moved its manufacturing inhouse.)”

“Responding to a proposed Commerce Department measure that is considering banning or restricting Chinese-made drones and components, venture capital firm Andreessen Horowitz — which has backed drone unicorns Anduril, Skydio and Shield AI — called for a more considered response with gradual restrictions on drone parts sales from China, while simultaneously allowing for U.S. companies to continue sourcing components from the country.”

Monday, Apr. 21st: Sam Gerstenzang at Bulton & Watt wrote about the evolution of internet marketplaces and vertical SaaS, highlighting the rise of "business-in-a-box" models that take on operational risks for higher profits. - Sam Gerstenzang

“The third wave of vertical SaaS has been the “business-in-the-box” where you take on real operational risk, and make most of your money from a take rate rather than a a fixed SaaS fee. They include entrants in to mental health (Grow Therapy, Headway, Alma, and so on), nutrition (Nourish, Berry Street, Fay), travel agents (Fora), and medspas (Moxie - that’s us!).”

“Just like there was an “Uber for x” for everything post Uber’s success, I fear that many of the new businesses in a box are going to end up as zeros.”

There are 3 criteria for a successful business: (i) a supply of new entrants to the market, (ii) a major shared COGS upon which you can drive meaningful cost reduction and (iii) the possibility to shape customer demand.

Tuesday, Apr. 22nd: Alex Niehenke at Scale wrote about the impact of Generative AI on the construction industry. - Scale

“The architecture, engineering, and construction (AEC) industry is plagued by two major problems: project delays and cost overruns. Of major projects, only 8.5% finish on time and on budget.”

“There are two lanes of innovation we’ll see as AI comes for AEC. The first is that LLMs will allow a new wave of vendors to run at the collaboration and interoperability problems costing time and money.” “The second is discipline-specific and purely additive: using generative AI to replace human labor supporting design, engineering, etc. The problems and tasks in AEC are a nice balance of constrictive and creative, with a ton of legacy data from previous projects, making the subdisciplines a good candidate for AI support.”

“Generative AI can provide an intuitive interface in contrast to traditional AEC systems like AutoCAD that are incredibly complex, requiring years of training to the point where they are taught in school. Therefore, experts are required in each organization to create and interpret data in these systems.”

“Motif and Arcol are bringing the ease of concepting software with the depth of production software, all powered on the back of LLMs.”

“Augmenta takes simple inputs and creates a full 3D electrical schematic in hours that would have previously taken days if not weeks or months to produce.”

“We know that LLMs are particularly good at interpreting large volumes of unstructured data, and reverting that into digestible, mostly accurate, but not perfectly precise data. This sounds a lot like estimating, which is plagued with data overload and human limitations on what can be processed and updated in a timely fashion.”

“AI will make the tasks of some of these players redundant and furthermore will allow you to move around the value chain in unpredictable ways.”

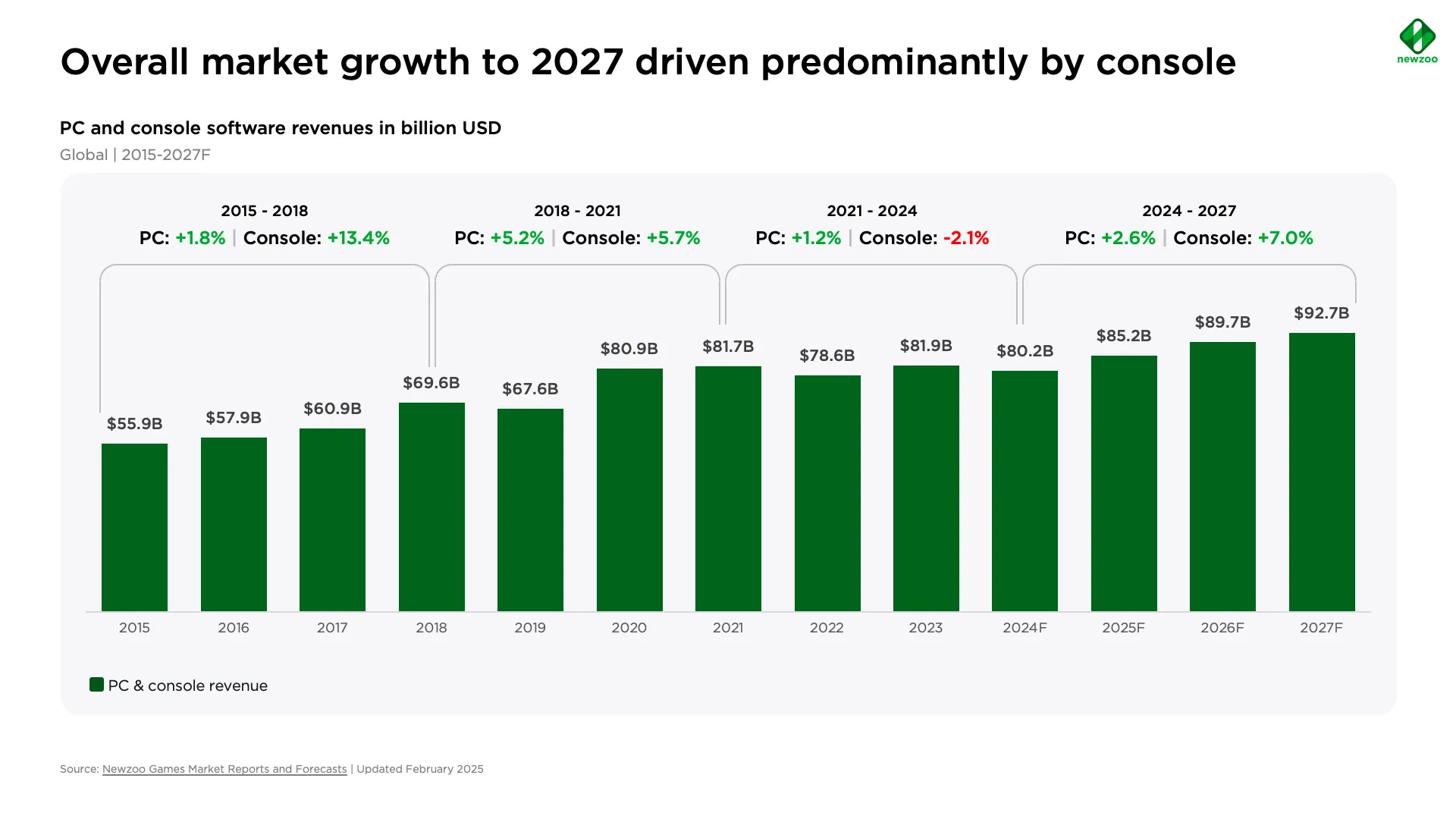

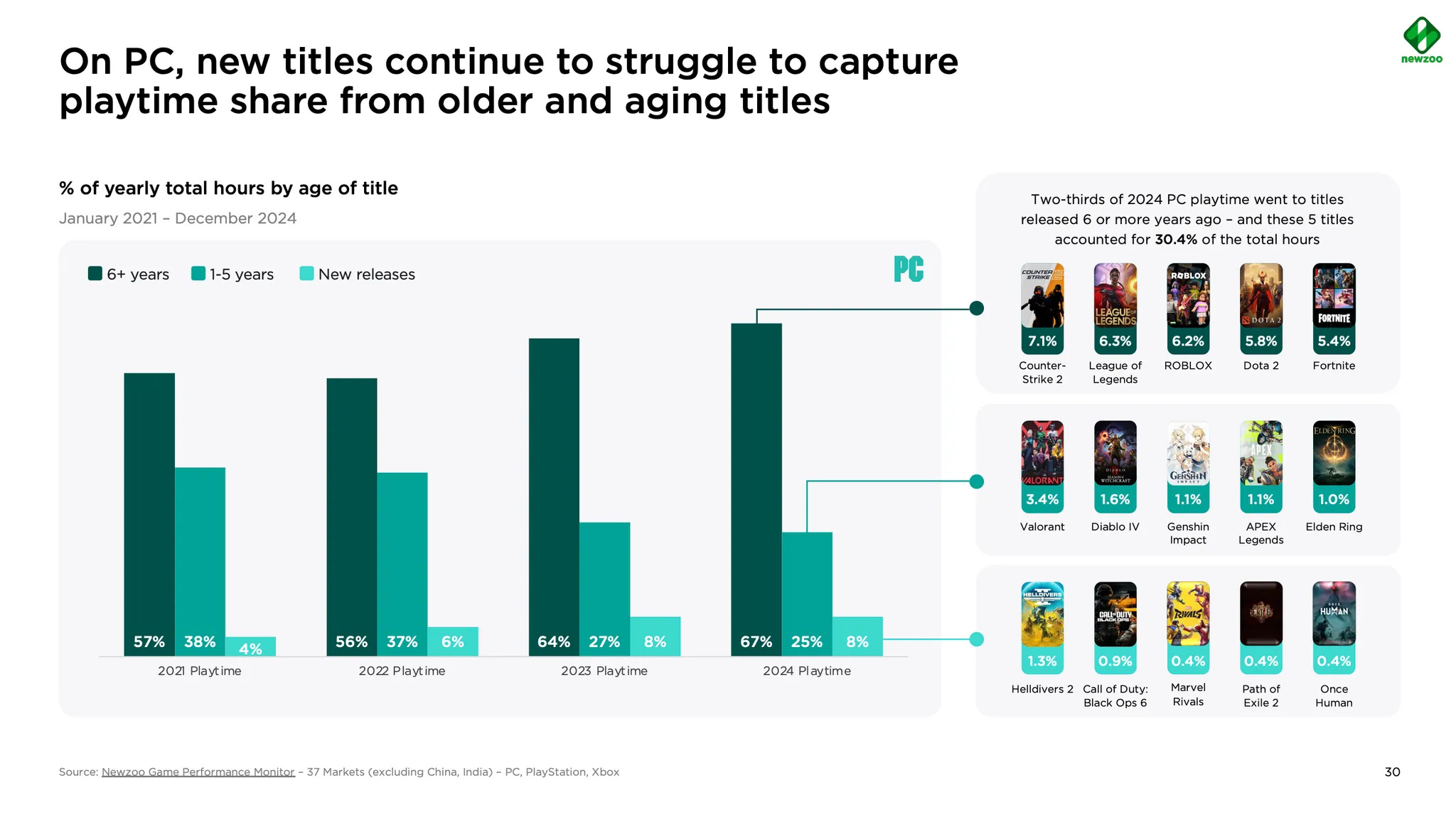

Wednesday, Apr. 23rd: Newzoo published the 2025 edition of its PC & Console Gaming report. - Newzoo 1, Newzoo 2

“Player growth has plateaued, turning the live-service market into a zero-sum battle for attention. Players are overwhelmed by an ever-increasing amount of content yet spending more time on fewer titles.”

“The number of games people play is declining on Steam and Xbox as players become increasingly fragmented and harder to reach. On Steam, the share of players engaging with three or fewer games annually rose from 22% in 2021 to 34% in 2024.”

“Despite an ever-expanding game library, Xbox players are engaging with fewer titles over time—highlighting that access alone doesn’t ensure sustained play.”

“Success on Steam now starts outside Steam. 46% of traffic to Steam games now comes from outside the platform via social media, creators, and community buzz.”

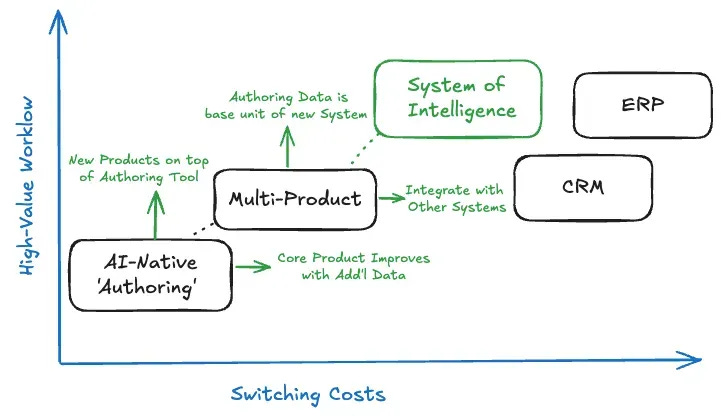

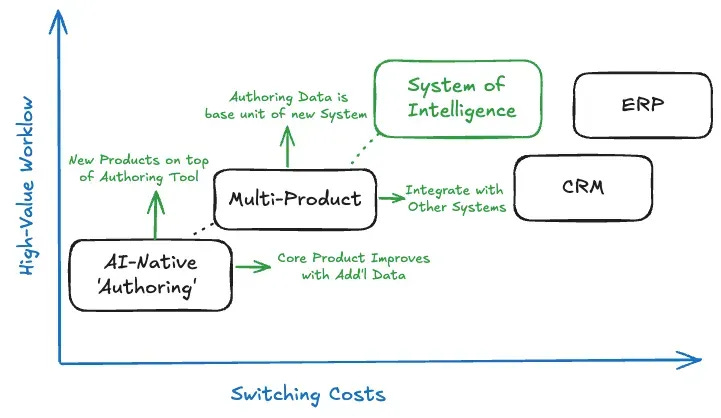

Thursday, Apr. 24th: Emerging vertical AI products focus on solving specific customer pain points by leveraging AI to enhance workflows and drive revenue. Successful startups should create easily adoptable "wedge" products that serve as entry points for broader systems of intelligence. - Euclid

“AI-first vertical software will be the near-term winners of LLMs' increasing performance and decreasing costs. Since then, we’ve seen incredibly rapid revenue growth from early breakouts like Abridge, EvenUp, Fieldguide, and others.”

“Both SaaS-first and AI-first vertical products target high-value workflows. SaaS, however, inherently requires the adoption of a new UI, including training and perhaps even market education. Vertical AI wedge products, however, can leverage natural-language interfaces to reduce or even eliminate the adoption curve.”

“We continue to believe—in AI as in SaaS—that workflows generating more revenue or eradicating constraints to growth are king. Especially when time-to-proof can be near-immediate.”

“We look for three critical ingredients in a successful AI-native vertical wedge product: (i) serving as the authoring layer (i.e., launch point) for a valuable internal workflow, (ii) powering an essential workflow that unlocks revenue, perhaps agnostic to peripheral systems to start, but absorbing downstream progressively and (iii) becoming the highest engagement application, leveraging usage to build moat.”

Friday, Apr. 25th: Harry recorded a 20VC’s podcast episode on the evolution of venture capital with Rory O’Driscoll (GP at Scale) and Jason Lemkin (SaaStr’s founder). - 20VC

PE firms are increasingly hesitant to acquire sub-scale SaaS companies without strong pricing power, as their focus lies on boring, dominant players in niche verticals where costs can be cut and prices raised.

“PE guys ironically love the things that we don't love let. They love a boring software company in a tiny vertical with 40% market share where they can screw the customers for the next five years by raising prices because there's nowhere else to go. Venture investors love horizontal markets where you can get a billion dollar outcome. When you discover that the path to this outcome does not work, you end up with an asset in a competitive category with no pricing power.”

"The Thrive strategy is brilliant. They buy the best property on every block. It's like Monopoly: Stripe of the fintech block, Open AI for the AI block, Databricks for the data infrastructure block. Then you just go home when you're done and you wait for the checks to roll in. It’s genius"

In SaaS, two things have massively changed.

Existing markets are saturated - everyone has a video-conferencing or a e-signature provider.

AI is reshaping markets at an insane velocity. “I've had companies acquire and lose product market fit two or three times in a two-year period. It's terrifying.”

Product market fit is no longer a stable long-term asset on which you can build a sustainable company. The rapid advancements in AI and the exploratory nature of the current market mean that companies can fall out of favor much faster than before. Historically, if you hit product market fit and you had a decent team, you had five years to scale the business before thinking about Act 2 or reinventing yourself.

“We're in this exploratory phase. Things are changing - both the underlying AI technology and how customers want to use it.” “It’s especially challenging here because, unlike automating back-office tasks, you’re trying to augment the thought processes of sales reps or SDRs—which is complex, constantly evolving, and hard to figure out.”

“If you're not understanding that you're underwriting more risk, you're missing the movie.” “You know less than what you would have known 10 years ago at a similar stage SaaS company. A lot more things can go wrong. On the other hand, the upside is here and is bigger than ever.

“The real problem with SaaS is there is a ton of SaaS companies that have slowed down from you exceptional growth rates. If you triple, triple, double, double, it’s still a great trajectory. What you don’t want to have is growth slowing down massively before the $100-300m ARR mark.”

$3tn is the fair market value of privately held venture assets. $1tn is in high growth and new companies. $2tn is in slower growth and mature companies. They no longer have the trajectory to IPO but they have meaningful value. There is ground work to be done to bring these companies to liquidity looking at multiple options like private to private to consolidate a market, private equity exits or grinding to profitability.

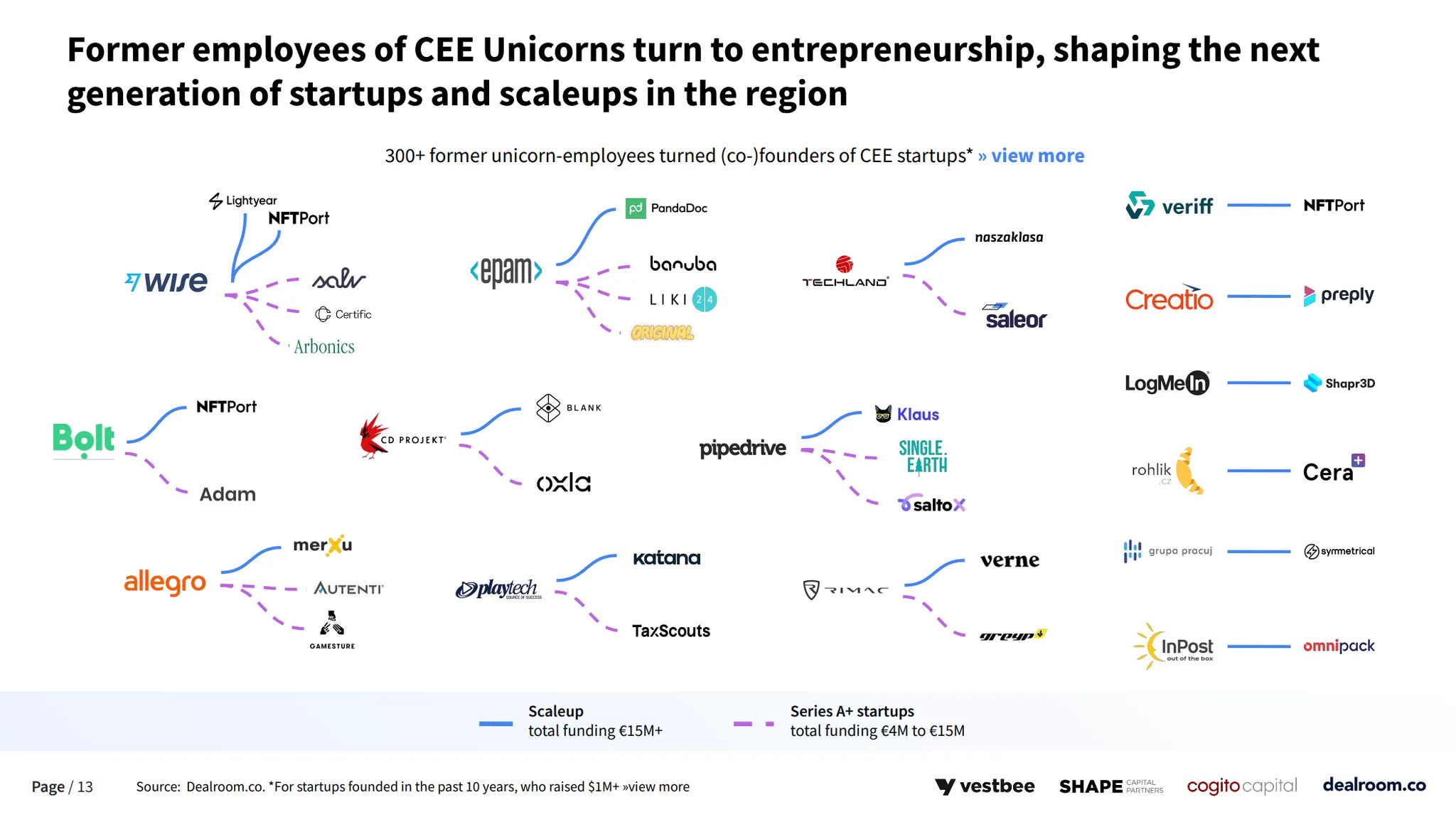

Saturday, Apr. 26th: Dealroom published a report on the Central & Eastern European venture market. - Dealroom

Sunday, Apr. 27th: Thoma Bravo acquired Boeing’s digital aviation software business for $10.55bn. It includes Jeppesen which provides navigation products and ForeFlight, an aviation navigation app. - FT, Boeing

“The planned disposal is part of an effort by Kelly Ortberg, who took over as Boeing’s chief executive in August, to streamline the heavily indebted aerospace and defence group, which has struggled to recover after safety scandals in recent years.”

“The private equity group would finance its deal with more than $6bn of equity and about $4bn in a private loan led by Apollo Global Management, said people briefed on the matter.”

“Boeing said it would keep its core digital capabilities that supply the aircraft and fleet-specific data the group uses to provide maintenance, diagnostics and repair services to its defence and commercial aircraft customers.”

"This transaction is an important component of our strategy to focus on core businesses, supplement the balance sheet and prioritize the investment grade credit rating.”

Monday, Apr. 28th: Ziv Reichert wrote a blogpost making the case of transcription as a great wedge to build a B2B product. - Ziv Reichert

“We’re quickly transitioning to a world where every professional conversation is transcribed.” “Simply put, we’re beginning to outsource our long-term memory to machines.”

“We can thank the proliferation of transcription tools for this shift. From general-purpose products like Granola to vertically focused ones like Heidi Health and Abridge in healthcare, RemyAI and EliseAI in real estate, Attio and Claap in sales, Metaview in recruiting, Superthread in product management and Model ML in financial services - these products help professionals seamlessly capture the full context of their day-to-day meetings.”

“The immediate value is clear: capture everything without losing focus on the person in front of you. But the real promise lies in what can - and inevitably will - be built on top of all this captured context: deep workflow automation, with transcription as the wedge.”

“So much of professional life follows the same pattern: we talk to others, capture what was said, and then act on it.”

“At its simplest, knowledge work comes down to two things: 1) transmitting and extracting information to and from others, and 2) taking action based on it.”

“I believe any conversation worth remembering, personal or professional, will soon be fully indexed and searchable.”

“Transcription models paired with LLMs represent what those second brains should have been, had the technology existed.”

Tuesday, Apr. 29th: The rise of AI is sparking debate about the future of SaaS, with some believing AI will replace traditional models. SaaS will continue to thrive by offering curated user experiences, domain expertise, and ongoing support. - Brandon Gleklen

3 key reasons to be long on SaaS in an AI-centric world: (i) UI design, data models, and proprietary data still matter, (ii) not all workflows are best solved conversationally, (iii) customer service & domain expertise, (iv) maintenance, update & ongoing costs, (v) industry standardization.

“Modern AI is undeniably transformational, but rather than signaling SaaS's demise, it represents an opportunity for tremendous growth.”

“The pricing pressure posed by AI is real and will likely reshape SaaS monetization strategies. Pressured by AI, traditional per-seat pricing models may evolve toward consumption- or outcomes-based pricing, aligning provider incentives closely with customer outcomes.”

Wednesday, Apr. 30th: In 2024, Revolut generated £3.1bn in sales (72% YoY growth) and £1.1bn in net profit (26% margin) from 52.5m customers (38% YoY growth). - FT, Revolut

“Revolut’s record profits were underpinned by growth in customer numbers, which boosted its two largest sources of revenue: the fees it makes from card payments and the interest it earns on deposit.”

“A surge in crypto trading also helped the fintech last year. Revolut’s wealth business, which comprises stock and digital asset trading, brought in £506mn in revenues — a nearly fourfold increase on 2023.”

“Revolut secured a UK banking licence with restrictions in July last year. The licence, obtained after a protracted three-year process with UK regulators, represented a milestone that will enable Revolut to roll out lending products in its home market.”

“It has also targeted corporate customers, with its business offering now accounting for about 15 per cent of revenues.”

“Our position as a primary financial services provider continued to improve, with a 59% year-on-year increase in customers using us as their main bank.”

Thanks to Julia for the feedback! 🦒 Thanks for reading! See you next week for another issue! 👋